EQUITIES RESEARCH ASIA OIL & GAS/CHEMICALS 2017 Outlook: Less is more A range of production curbs, from OPEC cuts to China’s supply side reform, is reflating prices in the oil markets from upstream to downstream. We forecast a 2017 Brent price of USD58/bbl (+USD14/bbl y-y) and strong chemical margins. Heightened price volatility is a natural consequence of greater policy interference and thus uncertainty. We expect the refining and chemical upcycle to continue into its third year, with rebounding diesel demand and stricter gasoline standards boosting refining margins. Our refining BUYs are SKI, S-Oil and TOP. Despite peaking ethylene margins, overall chemical margins are supported by strong demand and supply-side measures in China. Our chemical BUYs are LC, NYP and PTTGC. Recovering oil prices and diesel demand are positive for CNOOC and Sinopec (both BUY), but current high implied LT oil prices and diminishing oil reserves remain concerns. In India, our top BUYs are HPCL, PLNG and GAIL as beneficiaries of continued strong domestic oil & gas demand growth. Yong Liang Por [email protected]+852 2825 1877 Amit Shah [email protected]+91 22 6196 4394 Our research is available on Thomson One, Bloomberg, TheMarkets.com, Factset and on http://eqresearch.bnpparibas.com/index. Please contact your salesperson for authorisation. Please see the important notice on the inside back cover. 2 DECEMBER 2016 PREPARED AND PUBLISHED BY NON-US BROKER-DEALER(S): BNP PARIBAS SECURITIES (ASIA) LTD, BNP PARIBAS SECURITIES INDIA PVT. LTD. (SEBI REGISTERED RESEARCH ANALYST). THIS MATERIAL HAS BEEN APPROVED FOR U.S DISTRIBUTION. ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES CAN BE FOUND AT APPENDIX ON PAGE 124

Transcript

EQUITIES RESEARCH

ASIA OIL & GAS/CHEMICALS 2017 Outlook: Less is more

A range of production curbs, from OPEC cuts to China’s supply side reform, is reflating prices in the oilmarkets from upstream to downstream. We forecast a 2017 Brent price of USD58/bbl (+USD14/bbl y-y)and strong chemical margins. Heightened price volatility is a natural consequence of greater policyinterference and thus uncertainty.

We expect the refining and chemical upcycle to continue into its third year, with rebounding dieseldemand and stricter gasoline standards boosting refining margins. Our refining BUYs are SKI, S-Oiland TOP. Despite peaking ethylene margins, overall chemical margins are supported by strongdemand and supply-side measures in China. Our chemical BUYs are LC, NYP and PTTGC.

Recovering oil prices and diesel demand are positive for CNOOC and Sinopec (both BUY), but currenthigh implied LT oil prices and diminishing oil reserves remain concerns. In India, our top BUYs areHPCL, PLNG and GAIL as beneficiaries of continued strong domestic oil & gas demand growth.

Our research is available on Thomson One, Bloomberg, TheMarkets.com, Factset and on http://eqresearch.bnpparibas.com/index. Please contact your salesperson for authorisation. Please see the important notice on the inside back cover.

2 DECEMBER 2016 PREPARED AND PUBLISHED BY NON-US BROKER-DEALER(S): BNP PARIBAS SECURITIES (ASIA) LTD, BNP PARIBAS SECURITIES INDIA PVT. LTD. (SEBI REGISTERED RESEARCH ANALYST). THIS MATERIAL HAS BEEN APPROVED FOR U.S DISTRIBUTION. ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES CAN BE FOUND AT APPENDIX ON PAGE 124

ASIA OIL & GAS/CHEMICALS Yong Liang Por

To find out more about BNP Paribas Equities Research:

Visit : http://eqresearch.bnpparibas.com/ For ipad users : http://appstore.apple.com/BNPP-equities/

ASIA OIL & GAS/CHEM ICALS BNP PARIBAS Yong Li ang Por

THIS REPORT IS SOLELY FOR RECIPIENTS WHO ARE NON-CHINESE INVESTORS LOCATED OUTSIDE THE PEOPLE'S REPUBLIC OF CHINA ("PRC"). WITHOUT THE PRIOR WRITTEN CONSENT OF BNP PARIBAS, THE RECIPIENTS OF THIS REPORT SHALL NOT FURTHER DISTRIBUTE SUCH REPORT OR DISCLOSE ANY INFORMATION THEREIN TO ANY OTHER PERSON INCLUDING BUT NOT LIMITED TO ANY OTHER NON-CHINESE INVESTORS OR ANY PERSON IN PRC. 2 DECEMBER 2016 SECTOR REPORT

ASIA OIL & GAS/CHEMICALS

2017 Outlook: Less is more

Increased intervention The oil markets, from upstream to downstream, are being reflated by a broad range of supply-

side measures. OPEC’s decision on 30 November to cut production heralds the return of the Saudi put, tightening the oil market for at least the duration of the initial six-month agreement. We assume a Brent price of USD58/bbl for 2017 (vs USD44/bbl in 2016). Similarly, chemicals have benefited from China’s cut in coal production and rising freight costs. We think the price of increased intervention, and thus policy uncertainty, is heightened volatility.

Refining and Chemical upcycles continue

We expect Asian refining margins to improve modestly in 2017, on the back of rebounding diesel demand, gasoline specification changes and stable China exports. Our Refining BUYs are SKI, S-Oil and Thai Oil, which we favour for their attractive valuations and high dividend yields. Despite peaking ethylene margins, we expect overall chemical margins to remain strong, boosted by rebounding China demand, weakening competitiveness of coal-chemicals, and slowing capacity additions. Our Chemical BUYs are Lotte Chemical, NYP and PTTGC.

China recovers; India boom continues

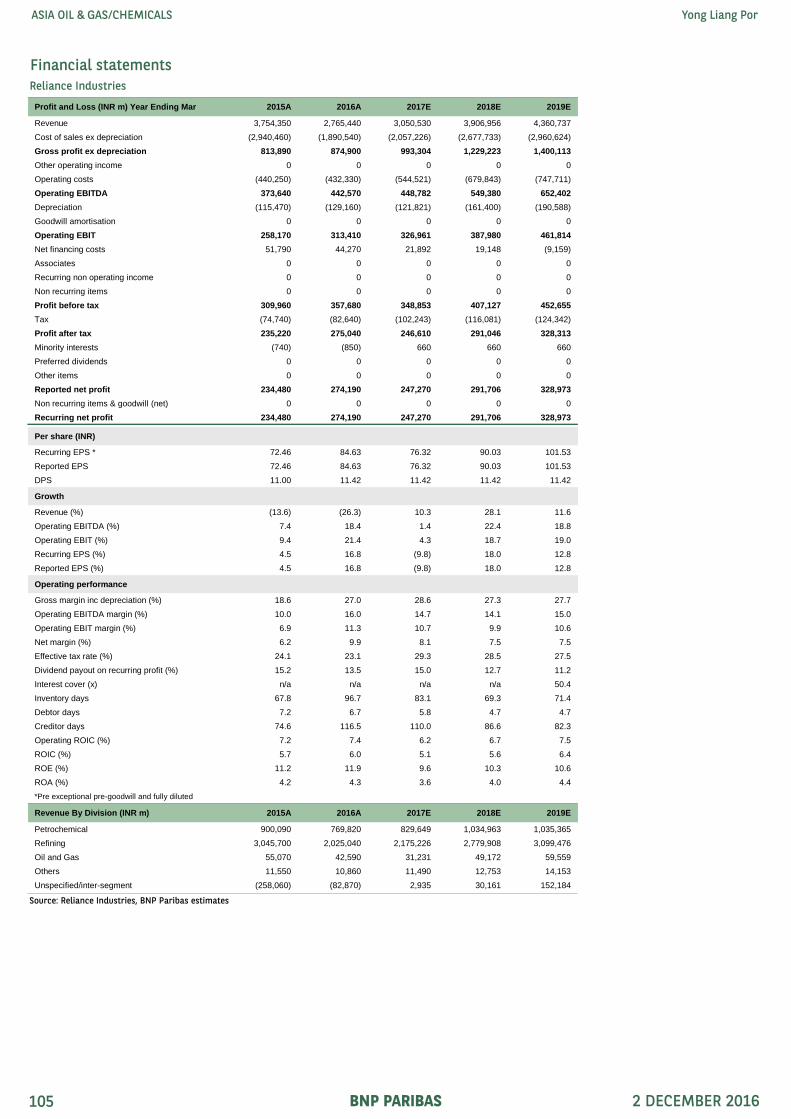

China NOCs stand to benefit from rising oil prices and recovering diesel demand, but share price performance may be curbed by high implied LT oil prices and diminishing oil reserves. Our China BUYs are CNOOC and Sinopec, which offer higher dividends and cheaper valuations than PetroChina (HOLD). In India, our top BUYs are HPCL, PLNG and GAIL, as beneficiaries of continued strong oil and gas demand growth and more favourable gas pricing. We also rate RIL BUY as plant expansions are now closer to starting up and the telecom launch has been successful.

We have a positive top-down view on the Asian Oil & Gas and chemical sector, where we see reflation taking hold in 2017 as overproduction is reined in on all fronts.

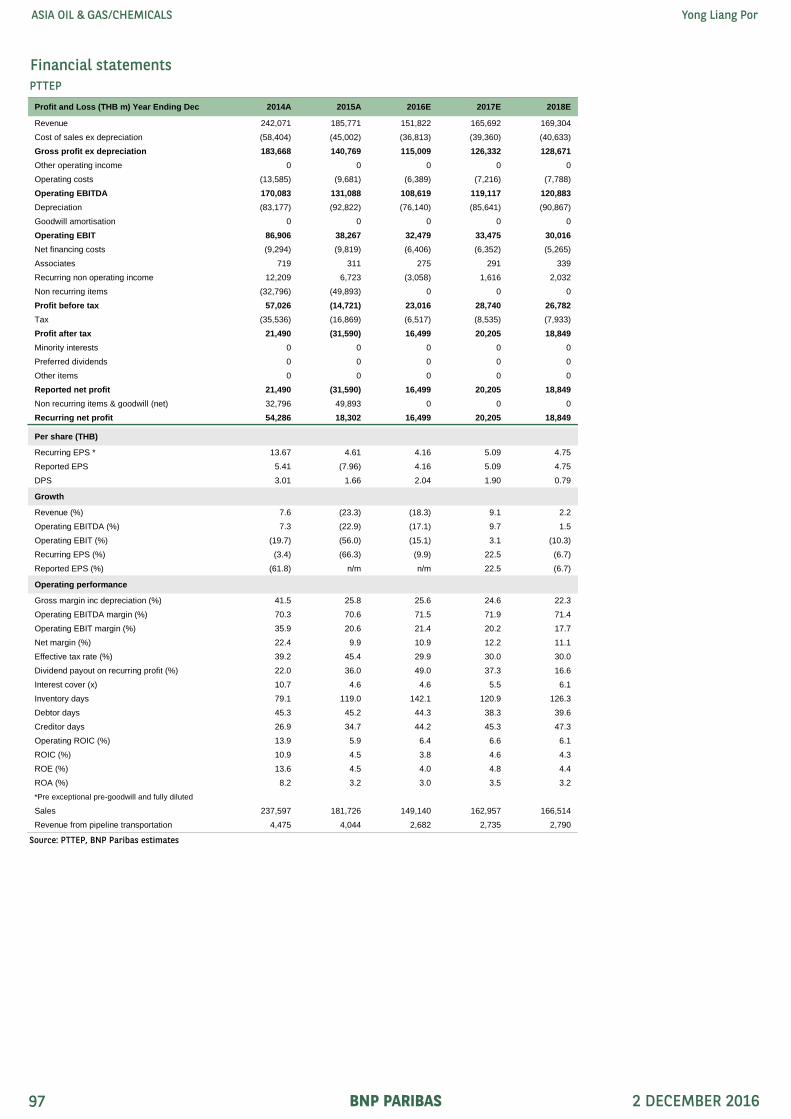

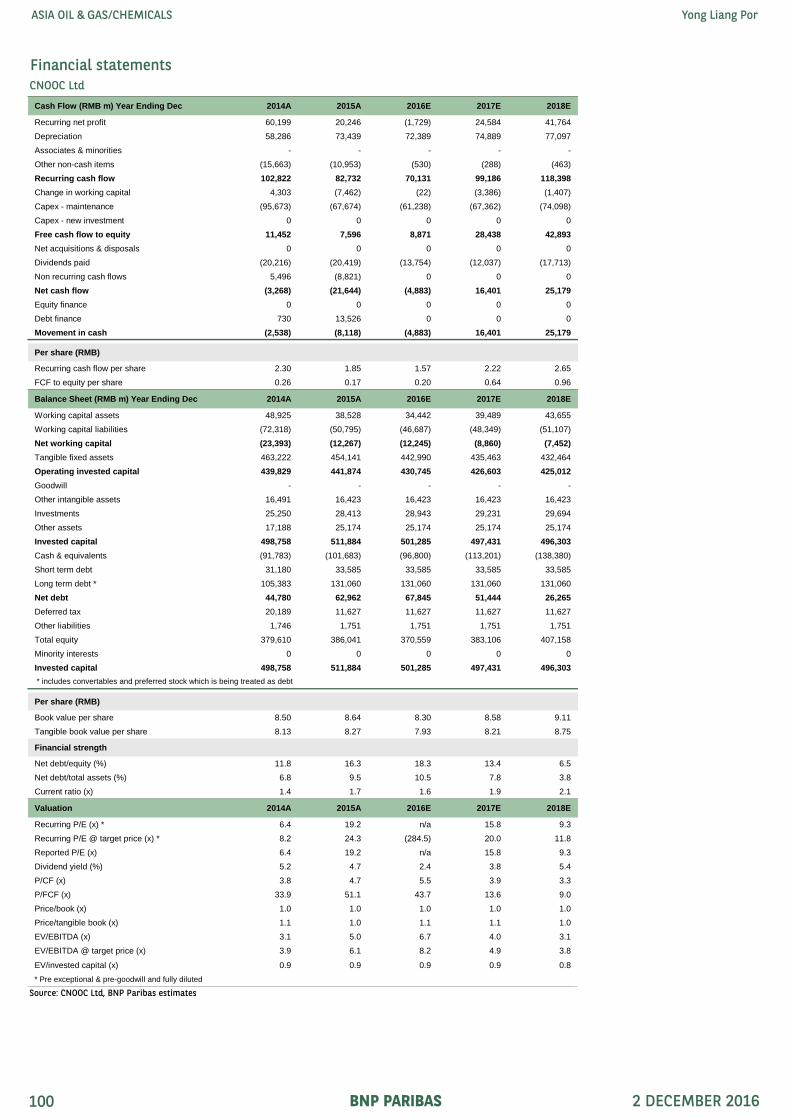

We believe OPEC’s decision on 30 Nov to reduce oil production, leading to a rebalanced market, signals the bottom for oil prices. We forecast a Brent price of USD58/bbl in 2017 and have BUYs on CNOOC, PTTEP and Sinopec.

We expect the period of high margins and steady earnings for the refining sector to continue, with supply-demand balanced between rebounding diesel demand, changing gasoline standards, and rising China exports. Our BUYs are SKI, S-Oil and Thai Oil.

Despite falling ethylene margins, we expect overall chemical margins to remain strong, as rebounding demand, weakening competitiveness of coal-chemicals and slowing capacity growth boost margins of aromatics, chlor-alkali and polyester chains. Our BUYs are Lotte Chem, NYP and PTTGC.

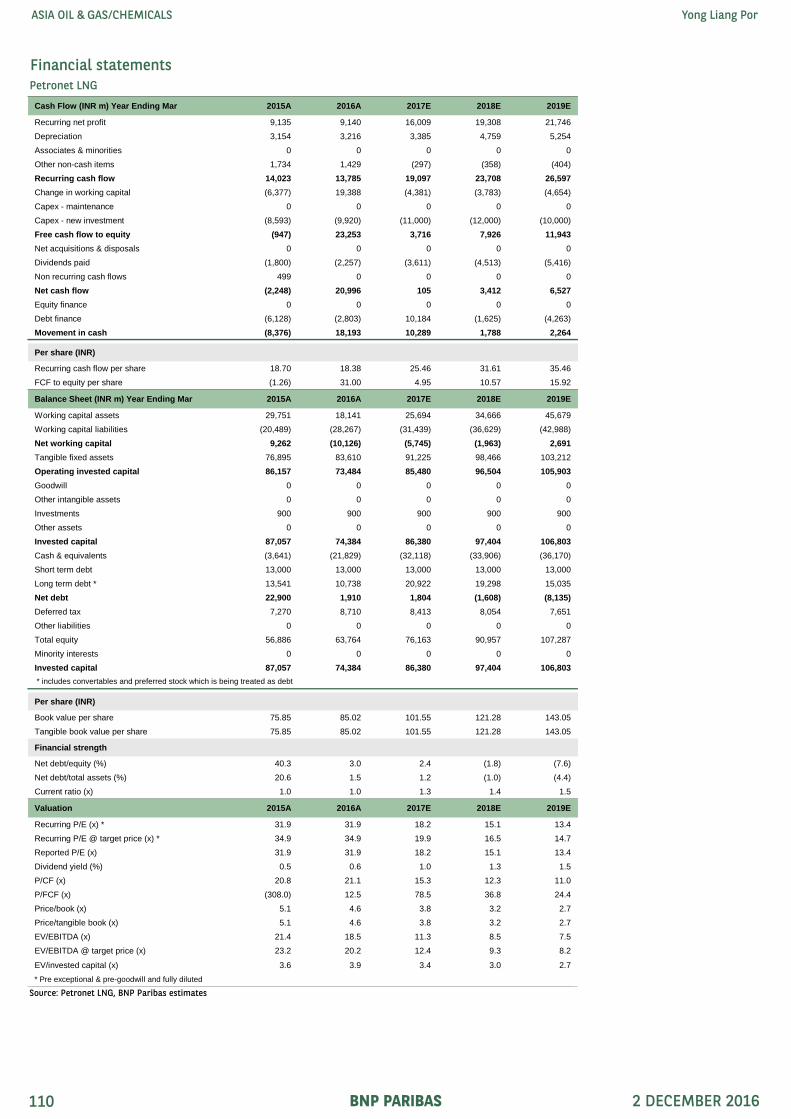

In India, our top BUYs are HPCL, PLNG and GAIL, as beneficiaries of continued strong oil and gas demand growth and more favourable gas pricing. We also rate RIL BUY as plant expansions are now closer to starting up and the telecom launch has been successful.

Catalysts

In 2017, we see reflationary dynamics in the energy markets being driven by 1) rising oil prices following OPEC’s decision to cut production; 2) rebounding diesel demand with recovering commodity production; and 3) China’s supply side reforms, which have reduced chemical oversupply.

Risks to our call

Oil prices may not recover if OPEC members do not adhere to the production cut targets, or if US production rebounds more quickly than we expect.

Refining margins may fall if refiners excessively increase runs or if our anticipated rebound in diesel demand does not materialise.

Chemical margins may falter if the current strength in Chinese demand is due to commodity speculation instead of end-product demand.

In 2016 to date, Brent prices fell to a bottom of USD28/bbl in January and rallied strongly to USD49/bbl by June, as discussions over a production freeze in April improved sentiment while significant production disruptions in Nigeria and Canada brought the market to a balance in mid-16. Subsequently, production growth resumed, resulting in falling prices, leading OPEC to propose a production cut in September.

On 30 November, OPEC followed through with its September proposal, agreeing on a 1.2mb/d production cut effective from 1 January 2017, for a duration of six months and extendable by another six months. Other non-OPEC countries, including Russia, indicated they would contribute production cuts of 600kb/d.

With this production cut, we expect the oil market to tighten in 2017 by up to 0.9mb/d. We now have more conviction in a tightening market as we believe there is upside to major agencies’ oil demand forecasts; we expect diesel demand to rebound in 2017 after a record 400kb/d fall in 2016.

From this point, we believe the trajectory of oil prices will depend on compliance with OPEC cuts and the pace of US production increases. Near term, oil prices remain restrained by record inventories and the rising USD; the latter point leads us to slightly lower 2017/18 Brent assumptions by USD2/bbl each to USD58/68 per barrel.

In these circumstances, our BUYs are CNOOC, PTTEP and Sinopec, as beneficiaries of modestly rising oil prices and reasonable valuations. We are cautious on PetroChina as we believe there is less upside potential to gas prices, while valuations and dividend yields are relatively less attractive.

Exhibit 1: Global oil supply less demand Exhibit 2: Global oil demand growth comparison

As of 30 Nov 2016 Sources: Bloomberg; BNP Paribas estimates

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

10 11 12 13 14 15 16 17E

Without OPEC cut With OPEC cut(mb/d)

Surplus

Deficit

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

16E 17E

(mb/d)IEA BNPP IHS

BNP PARIBAS 2 DECEMBER 2016 5

ASIA OIL & GAS/CHEMICALS Yong Liang Por

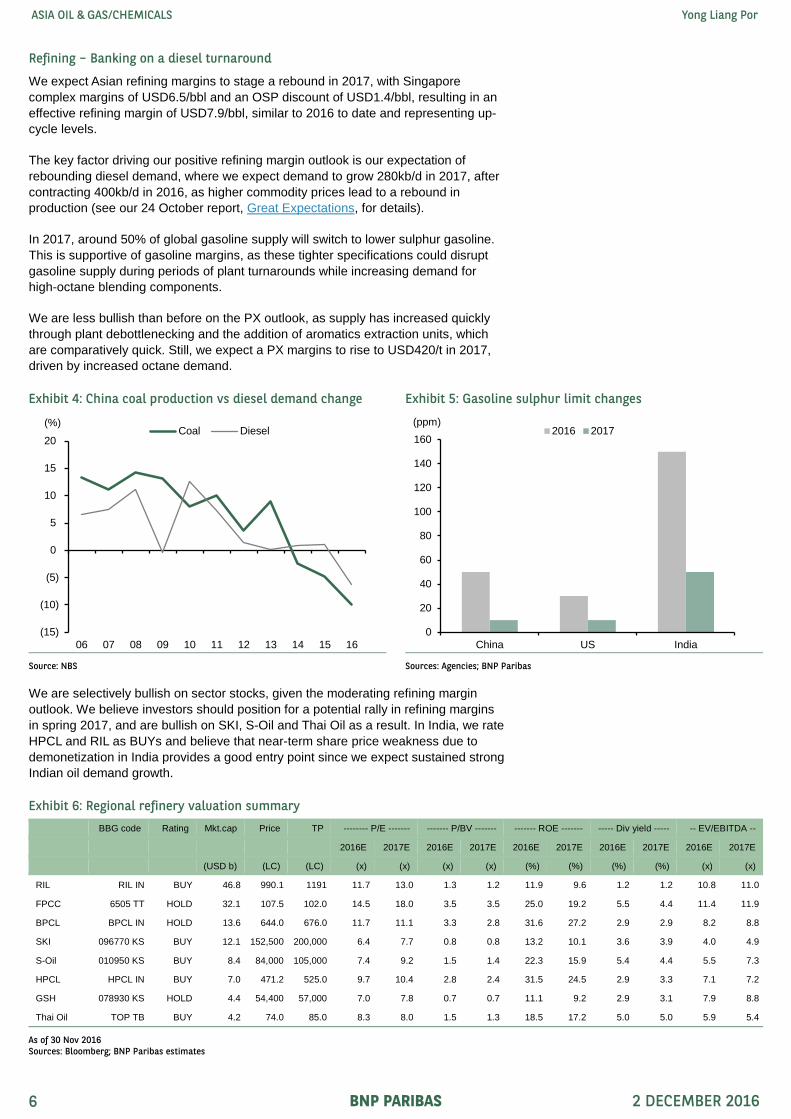

Refining – Banking on a diesel turnaround

We expect Asian refining margins to stage a rebound in 2017, with Singapore complex margins of USD6.5/bbl and an OSP discount of USD1.4/bbl, resulting in an effective refining margin of USD7.9/bbl, similar to 2016 to date and representing up-cycle levels.

The key factor driving our positive refining margin outlook is our expectation of rebounding diesel demand, where we expect demand to grow 280kb/d in 2017, after contracting 400kb/d in 2016, as higher commodity prices lead to a rebound in production (see our 24 October report, Great Expectations, for details).

In 2017, around 50% of global gasoline supply will switch to lower sulphur gasoline. This is supportive of gasoline margins, as these tighter specifications could disrupt gasoline supply during periods of plant turnarounds while increasing demand for high-octane blending components.

We are less bullish than before on the PX outlook, as supply has increased quickly through plant debottlenecking and the addition of aromatics extraction units, which are comparatively quick. Still, we expect a PX margins to rise to USD420/t in 2017, driven by increased octane demand.

We are selectively bullish on sector stocks, given the moderating refining margin outlook. We believe investors should position for a potential rally in refining margins in spring 2017, and are bullish on SKI, S-Oil and Thai Oil as a result. In India, we rate HPCL and RIL as BUYs and believe that near-term share price weakness due to demonetization in India provides a good entry point since we expect sustained strong Indian oil demand growth.

Exhibit 4: China coal production vs diesel demand change Exhibit 5: Gasoline sulphur limit changes

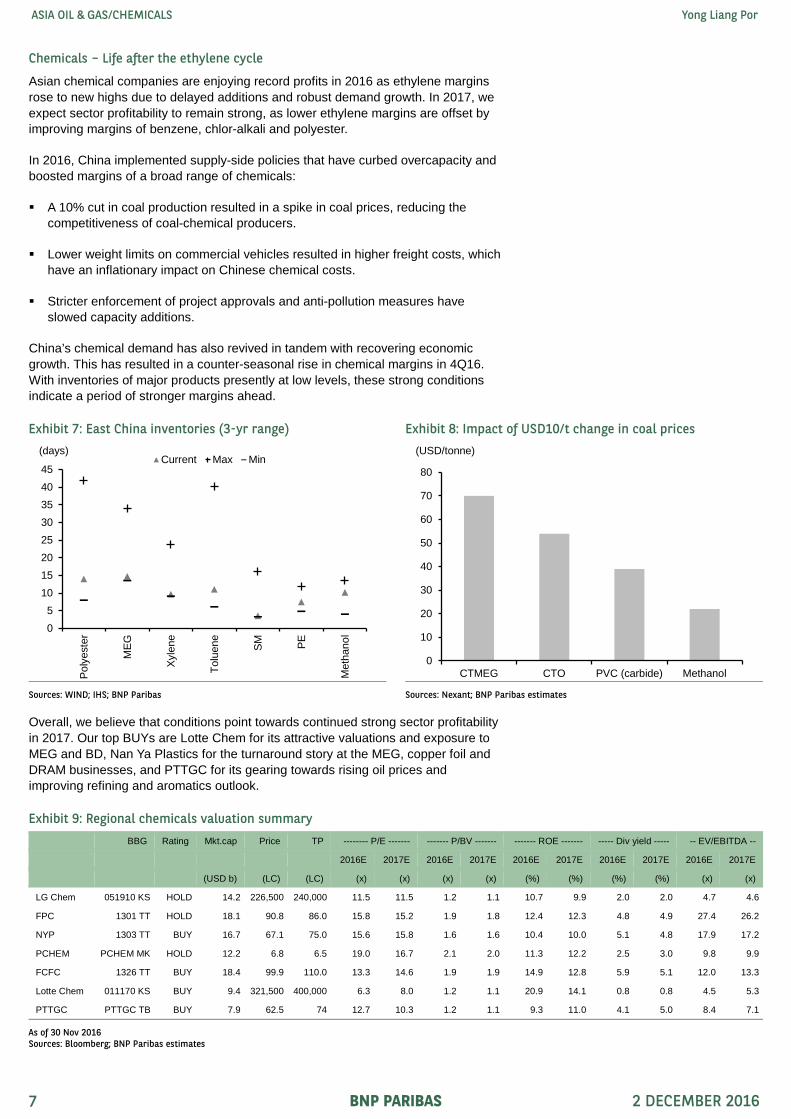

Asian chemical companies are enjoying record profits in 2016 as ethylene margins rose to new highs due to delayed additions and robust demand growth. In 2017, we expect sector profitability to remain strong, as lower ethylene margins are offset by improving margins of benzene, chlor-alkali and polyester.

In 2016, China implemented supply-side policies that have curbed overcapacity and boosted margins of a broad range of chemicals:

A 10% cut in coal production resulted in a spike in coal prices, reducing the competitiveness of coal-chemical producers.

Lower weight limits on commercial vehicles resulted in higher freight costs, which have an inflationary impact on Chinese chemical costs.

Stricter enforcement of project approvals and anti-pollution measures have slowed capacity additions.

China’s chemical demand has also revived in tandem with recovering economic growth. This has resulted in a counter-seasonal rise in chemical margins in 4Q16. With inventories of major products presently at low levels, these strong conditions indicate a period of stronger margins ahead.

Overall, we believe that conditions point towards continued strong sector profitability in 2017. Our top BUYs are Lotte Chem for its attractive valuations and exposure to MEG and BD, Nan Ya Plastics for the turnaround story at the MEG, copper foil and DRAM businesses, and PTTGC for its gearing towards rising oil prices and improving refining and aromatics outlook.

Exhibit 7: East China inventories (3-yr range) Exhibit 8: Impact of USD10/t change in coal prices

As of 30 Nov 2016 Sources: Bloomberg; BNP Paribas estimates

As of 30 Nov 2016 Sources: Bloomberg; BNP Paribas estimates

Exhibit 13: Regional Chemicals – P/BV comparisons

As of 30 Nov 2016 Sources: Bloomberg; BNP Paribas estimates

(30)

(20)

(10)

0

10

20

30TO

P

Sino

pec

FPC

C

FPC

BPC

L

OIN

L

FCFC

Petro

Chi

na

NY

P

PCH

EM PTT

PTTG

C

GAI

L

SKI

CN

OO

C

LGC

GS

PLN

G

RIL

PTTE

P

S-O

il

LC

ON

GC

(%)

Under

Over

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

SNP PTR CNOOC PTT PTTEP

(x)8yr avg. 16E PB 11 P/BV 08 P/BV

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

TOP SKI SOIL GSH

(x)8yr avg. 16E P/BV 11 P/BV 08 P/BV

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FPC NYP FCFC LGC LC

(x)8yr avg. 16E P/BV 11 P/BV 08 P/BV

BNP PARIBAS 2 DECEMBER 2016 8

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Oil market outlook – The intervention game

2016 – Light at the end of the tunnel

Brent prices fell to a 12-year low of USD28/bbl in January 2016, on concerns over the lifting of Iran sanctions and storage tanks running out of capacity. In response, key producers agreed to discuss a production freeze in Doha in April, which triggered oil prices to rally to USD40/bbl by March.

The Doha discussions subsequently failed, on Iran’s insistence to raise production, but oil prices continued to rise as Canadian wildfires and violence in Nigeria caused global oil production to contract by an average of 0.4mb/d y-y from May to August 2016, bringing the oil market closer to balance.

The balanced oil market in mid-16 resulted in the Brent price rising to USD49/bbl in June, but persistently high stocks blunted the price increase, while the steady increase in oil production from July onwards, particularly from OPEC, reawakened oversupply concerns.

Again, in response to oversupply concerns, OPEC announced in late September a plan to cut production to 32.5-33mb/d, sending oil prices back to USD50/bbl in October. On 30 November, OPEC agreed to cut production by 1.2mb/d to 32.5mb/d from 1 January 2017 for a period of six months, extendable by another six months.

Exhibit 16: OECD industry stocks Exhibit 17: Global oil production

Source: IEA Source: IEA

2030405060708090

100110120

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep-

14N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5Se

p-15

Nov

-15

Jan-

16M

ar-1

6M

ay-1

6Ju

l-16

Sep-

16N

ov-1

6

(USD/b)

OPEC chooses not to cut production

US rig count collapses

Iran sanctions

lifted

OPEC proposes

cuts

Iran deal, China equity

decline

(80)

(60)

(40)

(20)

0

20

40

60

Peak 2 4 6 8 10 12 14

1986 1996 2008 2014

(% change from peak year)

(Year of low prices per downturn)

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(mm bbl)5-yr avg 2016

28

29

30

31

32

33

34

35

60

61

62

63

64

65

66

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep-

14N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5Se

p-15

Nov

-15

Jan-

16M

ar-1

6M

ay-1

6Ju

l-16

Sep-

16

(mb/d)(mb/d) Non-OPEC (LHS) OPEC (RHS)

BNP PARIBAS 2 DECEMBER 2016 9

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Non-OPEC supply on the mend

In 2016 to date, global oil supply has grown 0.3mb/d, the slowest growth since 2009, as non-OPEC production growth contracted by 1mb/d, offset by OPEC production growth of 1.3mb/d.

Non-OPEC production declined the most in the US (-0.6mb/d) and China (-0.3mb/d). US production fell 0.4mb/d in conjunction with a 40% decline in US E&P capex, while China production fell as production at high cost fields was cut. Russian production was the biggest positive surprise this year, rising 0.2mb/d to date, as rouble depreciation significantly lowered costs.

In 2017, the IEA forecasts non-OPEC production to grow by 0.5mb/d, with increases in Russia, Kazakhstan and Brazil offsetting declines in China. In our view, the risks regarding non-OPEC production growth are skewed to the upside:

US oil production remains resilient, as declining production at Bakken and Eagle Ford basins is being offset by higher production at the Permian Basin. In fact, overall US oil production may already be recovering, rising to 8.68mb/d in November 2016 from 8.49mb/d in October 2016, while the US oil rig count has recovered to 471 at present from 316 in May.

Since 2015, oil producers have successfully cut costs, with global breakeven costs falling USD5/bbl to USD46/bbl at present. Russian and UK costs have fallen the most, which we attribute to local currency depreciation.

Source: IEA data and forecasts Source: IEA data and forecasts

Exhibit 20: US oil production by basin Exhibit 21: Global break-even price comparison

Source: EIA Source: IHS

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

11 12 13 14 15 16E 17E

OPEC Non-OPEC(mb/d)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

11 12 13 14 15 16E 17E

(mb/d)Russia US China Brazil

500

700

900

1,100

1,300

1,500

1,700

1,900

2,100

13 14 15 16

(kb/d)Bakken Eagle Ford Permian

0

10

20

30

40

50

60

70

80

Kaza

khst

an

US

- G

OM UK

Can

ada

Chi

na

Rus

sia

Iran

Saud

i

Glo

bal

(USD/b)2015 2017

BNP PARIBAS 2 DECEMBER 2016 10

ASIA OIL & GAS/CHEMICALS Yong Liang Por

OPEC accelerating before braking

In 2016 to date, OPEC production has risen by 1.3mb/d y-y to a new record of 33.8mb/d, an increase of 4.8mb/d from 2010 levels. The major contributors of the increase were Iran, Iraq and Saudi Arabia, whom we assume were motivated to raise production ahead of production cut discussions.

On 30 November, OPEC agreed to a 1.2mb/d cut in production. We believe that a high degree of compliance is likely, for these reasons:

OPEC members have seen a significant deterioration in their fiscal positions since 2014, with key members remaining in deficit even with oil prices of USD60/bbl. Iraq is the most indebted major OPEC producer, while Saudi Arabia has implemented significant cost-cutting measures, such as reducing fuel subsidies and cutting civil servant salaries.

There is very little spare capacity left in OPEC following the rapid production increase in 2016. The IEA estimates OPEC’s spare capacity in October 2016 at just 2.1mb/d, its lowest level since 2008.

The largest share of the production cut is being borne by Saudi Arabia, restoring Saudi spare capacity to above 2mb/d, in line with its historical range, and also lowering Saudi’s market share of OPEC production closer to 2009 levels, which was the last time that OPEC made a collective cut.

Exhibit 22: OPEC fiscal breakeven sensitivity analysis (2016) Exhibit 23: Government debt as % of GDP

Source: Wood Mackenzie Source: IMF data and forecasts

A major concern to oil markets this year has been the deceleration of demand growth. Based on the aggregated data of 16 major countries representing over 80% of global demand, we estimate that oil product demand grew 740kb/d in 9M16, compared with 1.2mb/d in 2015, which is disappointing considering that oil prices had averaged USD10/bbl lower in 2016 vs 2015.

The main culprit of weakening global oil demand in 2016 to date has been the 407kb/d decline in diesel demand, a similar decline to that during the financial crisis. If diesel demand had been flat, global oil demand growth would have been flat y-y. In 2016, gasoline demand growth has slowed, but is still growing well above the historical trend, while jet demand growth has remained stable at above 200kb/d.

We attribute this sharp fall in diesel demand to declining commodity production globally, with record declines of oil and coal production in the US and China. US coal production fell as utility providers switched to cheaper natural gas, while China coal production fell after the government cut the number of working days for coal miners from 330 to 276 from April 2016.

In response to these production cuts, and factoring in recovering commodity demand in China, prices of main commodities, particularly coal, have risen sharply from October. The Chinese government has since temporarily rescinded the coal miners’ working day restriction for November and December, to boost coal production, while the EIA forecasts US coal production to rise 3% in 2017.

Exhibit 26: Global oil product demand growth Exhibit 27: Global oil demand growth breakdown

Source: IEA Source: IEA

Exhibit 28: US & China commodity production Exhibit 29: Coal, iron ore & Henry Hub prices

Sources: EIA; CEIC Source: Datastream

0

200

400

600

800

1,000

1,200

1,400

2011 2012 2013 2014 2015 9M16

(kb/d)

(1,000)

(500)

0

500

1,000

1,500

2,000

2011 2012 2013 2014 2015 9M16

(kb/d) LPG Naphtha Gasoline Diesel Jet Fuel oil

(20)

(15)

(10)

(5)

0

5

10

15

20

2011 2012 2013 2014 2015 9M16

(%)China coal China oil US coal US oil

0

20

40

60

80

100

120

140

160

180

10 11 12 13 14 15 16

(index) Coal (Newcastle port) Iron ore (Qingdao port)

Henry Hub

BNP PARIBAS 2 DECEMBER 2016 12

ASIA OIL & GAS/CHEMICALS Yong Liang Por

As a result of recovering commodity production, we believe global diesel demand can grow at 280kb/d in 2017, a modest level relative to the historical 10-year average growth rate of 340kb/d pa.

In summary, we expect global diesel growth to rebound from negative 400kb/d in 2016 to positive 280kb/d in 2017, a swing of 680kb/d, which underpins our view that global oil demand growth could surprise on the upside in 2017 by 100-300kb/d compared with agency forecasts.

The unexpected increase in fuel oil demand in 2016 to date further convinces us that global oil demand could surprise positively. In 2016, fuel oil demand has risen 130kb/d, the first year since 2005 that fuel oil demand growth has been positive.

We attribute the increase primarily to higher marine fuel sales, as seen in their rising sales in Singapore and the US, on China’s renewed appetite for commodity imports, with copper, iron ore and coal imports rising by 34%, 9% and 9% y-y for 9M16.

Next year, these strong positive factors may not be repeated, but we believe that as long as oil prices do not rise above USD60/bbl, the pace of fuel oil demand destruction may remain slower than the historical trend.

Exhibit 30: Global diesel demand growth Exhibit 31: Global oil demand growth comparison

Exhibit 32: Global fuel oil supply and demand Exhibit 33: Singapore marine bunker sales

Source: IEA Source: Port of Singapore

(0.6)

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

04 05 06 07 08 09 10 11 12 13 14 15 16E17E18E

(mb/d)

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

16E 17E

(mb/d)IEA BNPP IHS

(400)

(300)

(200)

(100)

0

100

200

2011 2012 2013 2014 2015 8M16

(kb/d)Demand Supply

(2)

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 2013 2014 2015 10M16

(y-y %)

BNP PARIBAS 2 DECEMBER 2016 13

ASIA OIL & GAS/CHEMICALS Yong Liang Por

We estimate 2017 Brent price of USD58/bbl

With OPEC’s production cut, we expect the oil market to tighten in 2017 by up to 0.9mb/d. We have added conviction in a tightening market, as we believe there is upside potential to major agencies’ oil demand forecasts; we expect diesel demand to rebound in 2017 after a record 400kb/d fall in 2016.

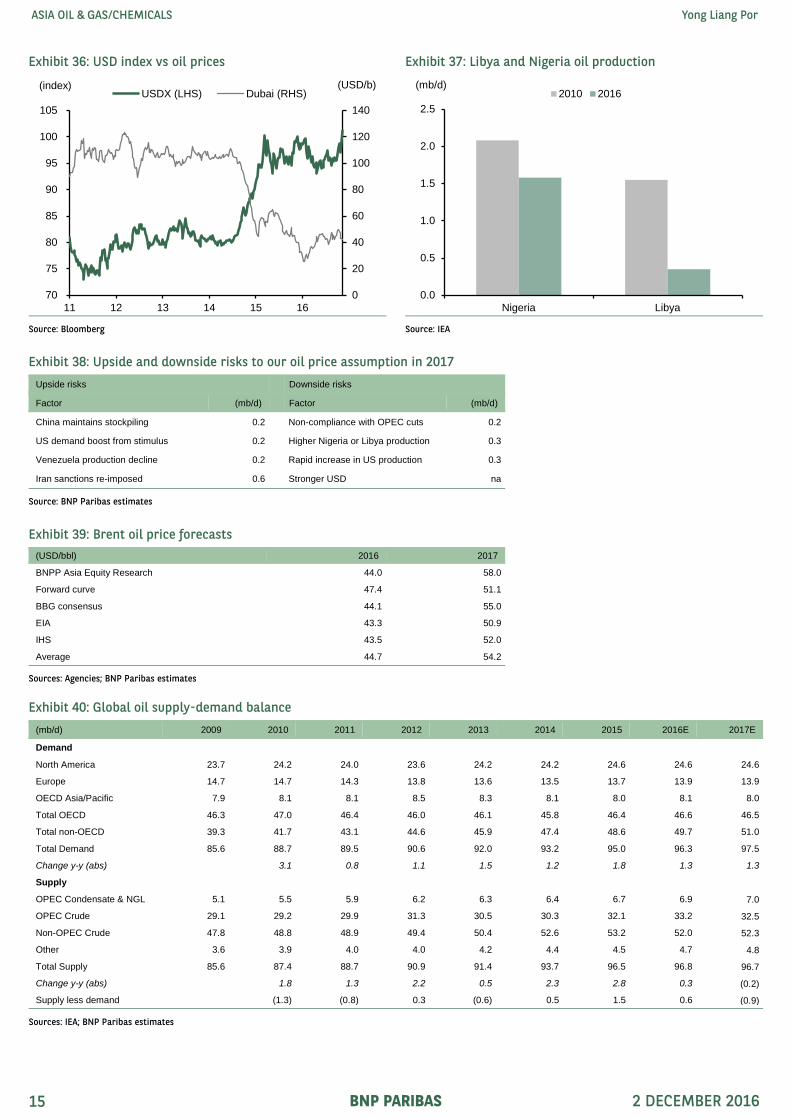

From this point, we believe the trajectory of oil prices will depend on compliance with OPEC cuts and the pace of US production increases. Near term, oil prices remain restrained by record inventories and the rising USD; on which latter point we slightly lower our 2017/18 Brent assumptions by USD2/bbl each, to USD58/68 per barrel.

We believe the larger significance of the November 30 meeting is the re-emergence of OPEC as the swing producer in the global oil market, forced upon it by its weakening fiscal position and the recognition of US tight oil producers as a long-term presence in the oil markets.

The key risks to our view of oil prices are:

Upside could emerge if non-OPEC countries, such as Russia, were to implement the 600kb/d cut in 2017 production that was proposed during the 30 November OPEC meeting. However, we are sceptical this can be implemented as there does not seem to be any incentive to do so and have not factored this in.

Historically, the USD has had a negative correlation with oil prices. BNPP forecasts stronger US economic growth under the Trump administration leading the Fed to raise rates six times to 2.25% by 4Q18, causing USD appreciation and weighing down oil prices.

Supply from Libya and Nigeria is dependent on political outcomes that could rapidly move production higher or lower. If the Nigerian government were to reach an agreement with militants, output could rise by a few hundred thousand barrels a day. Libya also has upside potential, with output rising to 500kb/d in early October from less than 300kb/d in August.

At present, both the IEA and EIA forecast flat US oil production of 8.7mb/d in 2017, but this could be revised upwards since the average breakeven cost of new US tight oil production is now at USD50/bbl. Still, we believe this is likely to take up to a year to significantly ramp up production, given the lead times for obtaining drill permits and site preparation, drilling, pressure pumping, and factoring in delays to first production.

Exhibit 34: Global oil supply less demand (annual) Exhibit 35: Global oil supply less demand (quarterly)

2016 – High expectations and weak diesel sink margins

In 2016 to date, Asian refining margins have weakened to USD6.1/bbl from USD7.7/bbl in 2015. Margins began the year strongly, but quickly declined with sharply rising oil product inventories, bottoming out at USD3.9/bbl in August. Margins rebounded strongly from September onwards as refineries severely lowered runs in September-October.

By product, gasoline, diesel, jet and LPG saw weakening margins, partially mitigated by rising margins of fuel oil and naphtha. Diesel margins declined to USD10.7/bbl, the lowest level since 2009 and representing the 5th consecutive year of decline. Fuel oil margins were the biggest positive surprise, leading simple margins to USD4.1/bbl in November, the highest level in the past two years.

During 2016, refineries anticipated strong gasoline and weak diesel demand, and adjusted their product yields accordingly. As gasoline demand growth slowed significantly and diesel demand fell sharply, this resulted in surpluses of these two major products, whose high inventories have only begun receding since September.

In our view, the most important reason for the y-y decline in complex margins this year was the record 400kb/d decline in diesel demand, on a par with the decline of the financial crisis in 2009. We attribute this decline to the effects of declining commodity production, slowing industrial production and a mild winter.

Exhibit 43: Global supply vs demand growth (2016, y-y chg) Exhibit 44: Global diesel demand by country (2016, y-y chg)

Source: IEA Source: IEA

2

3

4

5

6

7

8

9

10

11

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(USD/b) 2016 2015 5-year av

(20)

(15)

(10)

(5)

0

5

10

15

20

Gasoline Diesel HSFO Naphtha

(USD/b)2013 2014 2015 2016

(600)

(400)

(200)

0

200

400

600

800

Gasoline Diesel Jet Fuel oil

(kb/d)Supply Demand

(250)

(200)

(150)

(100)

(50)

0

50

100

Chi

na US

Braz

il

Saud

i

Can

ada

Iran

Rus

sia

Indo

nesi

a

Aust

ralia

Japa

n

Taiw

an

Mex

ico

Thai

land

Kore

a

EU

Indi

a

(kb/d)

BNP PARIBAS 2 DECEMBER 2016 16

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Recovery on multiple fronts

We expect to see a broad-based refining margin recovery in 2017, driven by recovering gasoline and diesel margins as well as strong fuel oil margins.

We believe diesel demand should recover strongly, as

commodity production, particularly coal, should increase in the coming months in response to higher prices. For example, the Chinese government has allowed coal mines to increase production since October, and the EIA forecasts US coal production to rise 3% in 2017 after falling 18% in 2016, and

China demand should recover as major economic indicators have turned positive this year. The recent ban on truck overloading and reduced maximum truck tonnage may also boost diesel demand due to a higher frequency of trips.

In 2016, global gasoline demand has grown by 324kb/d, half the growth of 2015, but we think that underlying trends are still healthy as:

China gasoline demand growth is likely understated by up to 250kb/d, as we believe the spike in China’s mixed xylene imports this year was because it was used as gasoline blendstock, but not accounted for as gasoline for tax reasons.

Gasoline imports by developing countries are likely to rise next year, due to a combination of weak production in Latin America (Petrobras and Pemex facing financial issues) and recovering commodity production (Africa and Latin America).

Exhibit 47: Mexico and Brazil refinery runs Exhibit 48: Mexico and Brazil gasoline imports

Source: IEA Source: IEA

0

20

40

60

80

100

120

140

160

180

200

11 12 13 14 15 16

(USD/tonne) Newcastle coal Iron ore (Qingdao)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015 2016

(%) Electricity FAIRetail Construction

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2010 2011 2012 2013 2014 2015 2016

(mb/d)Mexico Brazil

0

100

200

300

400

500

600

700

2010 2011 2012 2013 2014 2015 2016

(kb/d)Mexico Brazil

BNP PARIBAS 2 DECEMBER 2016 17

ASIA OIL & GAS/CHEMICALS Yong Liang Por

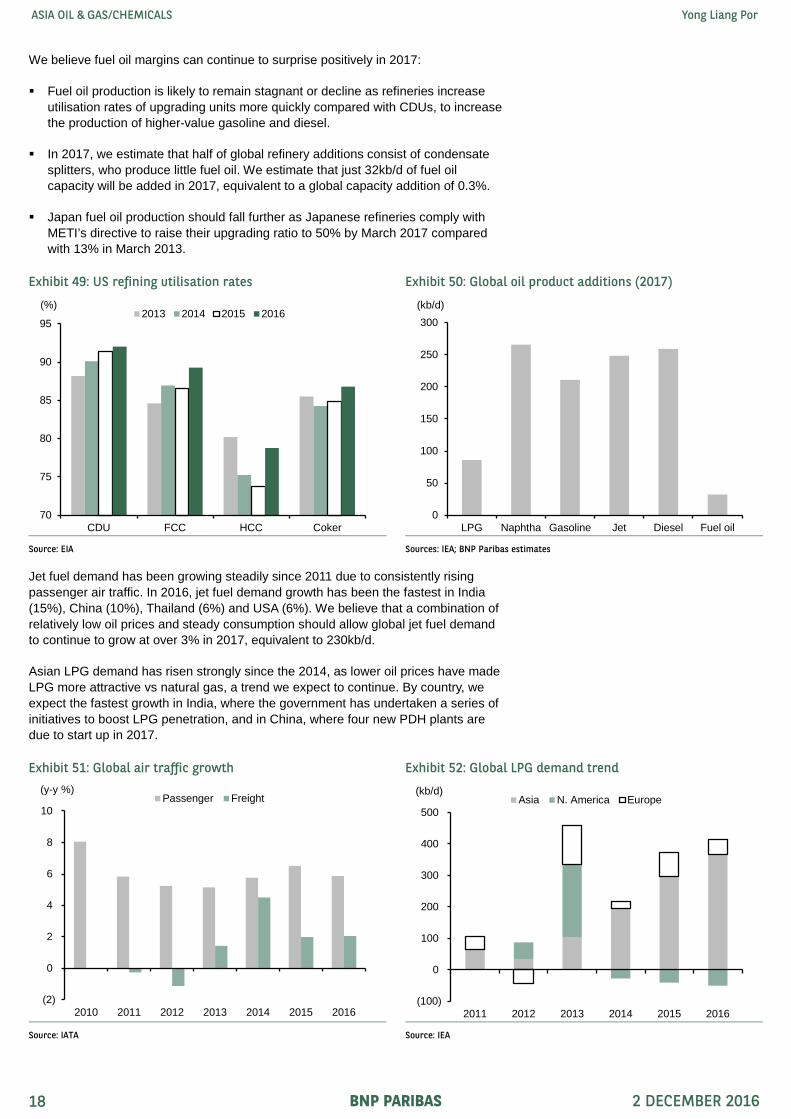

We believe fuel oil margins can continue to surprise positively in 2017:

Fuel oil production is likely to remain stagnant or decline as refineries increase utilisation rates of upgrading units more quickly compared with CDUs, to increase the production of higher-value gasoline and diesel.

In 2017, we estimate that half of global refinery additions consist of condensate splitters, who produce little fuel oil. We estimate that just 32kb/d of fuel oil capacity will be added in 2017, equivalent to a global capacity addition of 0.3%.

Japan fuel oil production should fall further as Japanese refineries comply with METI’s directive to raise their upgrading ratio to 50% by March 2017 compared with 13% in March 2013.

Jet fuel demand has been growing steadily since 2011 due to consistently rising passenger air traffic. In 2016, jet fuel demand growth has been the fastest in India (15%), China (10%), Thailand (6%) and USA (6%). We believe that a combination of relatively low oil prices and steady consumption should allow global jet fuel demand to continue to grow at over 3% in 2017, equivalent to 230kb/d.

Asian LPG demand has risen strongly since the 2014, as lower oil prices have made LPG more attractive vs natural gas, a trend we expect to continue. By country, we expect the fastest growth in India, where the government has undertaken a series of initiatives to boost LPG penetration, and in China, where four new PDH plants are due to start up in 2017.

Exhibit 49: US refining utilisation rates Exhibit 50: Global oil product additions (2017)

Source: EIA Sources: IEA; BNP Paribas estimates

Exhibit 51: Global air traffic growth Exhibit 52: Global LPG demand trend

Source: IATA Source: IEA

70

75

80

85

90

95

CDU FCC HCC Coker

(%)2013 2014 2015 2016

0

50

100

150

200

250

300

LPG Naphtha Gasoline Jet Diesel Fuel oil

(kb/d)

(2)

0

2

4

6

8

10

2010 2011 2012 2013 2014 2015 2016

(y-y %)Passenger Freight

(100)

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016

(kb/d)Asia N. America Europe

BNP PARIBAS 2 DECEMBER 2016 18

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Changing fuel standards provide support for gasoline and PX

In 2017, these countries are switching to lower sulphur gasoline:

China is switching to Standard V fuels for inland markets, which lowers sulphur content in gasoline and diesel to 10ppm from 50ppm.

US is switching to Tier-3 gasoline, which lowers sulphur content to 10ppm from 30ppm.

India is switching to nation-wide Bharat-IV fuels in April 2017, which lowers sulphur content in gasoline to 50ppm from 150ppm.

Pakistan is switching to 92 RON gasoline from 87 RON.

Altogether, these changes could cause disruptions to gasoline supply in 2017, since:

Refiners may face increased difficulties in maintaining gasoline supply during turnarounds of sulphur-reducing units, according to industry consultants Turner, Mason & Co.

Sulphur-reducing units will need to be run at a higher severity than before, which could lead to more frequent or more lengthy maintenance.

Not all refineries may have the financial resources to upgrade their equipment to meet these new standards. In the US, Philadelphia Energy Solutions (Not listed), which operates a 330kb/d refinery on the US east coast, disclosed that it would have to undertake capex to meet the Tier-3 standard, but financial difficulties have caused it to defer capital spending in 2016.

Another effect of the tightening gasoline standards is the loss of octane, since more severe sulphur-reduction causes octane loss, which we calculate could reduce global PX supply by 7% in 2017 (see Turbocharging PX, 6 June 2016, for full details).

The tightness in octane is most obvious in the US, where premium gasoline, which has a higher octane, has continued to raise its market share, to 11.9% in August 2016, a 13-year high that we believe is being driven by the rising adoption of turbo-charged engines. As a consequence, the price of premium gasoline in the US has averaged USD0.44/gallon higher than conventional gasoline in 2016, a historical high.

Downside risk from China exports and PX capacity creep

In 2016, Chinese oil product exports have risen more quickly than we anticipated, to 366kb/d in 2016, triple the figure of one year ago and equivalent to the output of a new world-scale refinery. On 4 November 2016, China increased the VAT rebate for oil product exports to 17%, stoking concerns that exports would further increase.

Exhibit 53: US premium gasoline market share Exhibit 54: US premium less regular gasoline price

We expect China oil product exports to remain high in 2017, but for the pace of increase to slow down, since we expect diesel demand to recover, a sharp slowdown in new crude import quotas, and stricter enforcement to reduce tax evasion among independent refineries, leading them to lower runs.

In 2016, PX margins have risen USD50/t to USD395/t, which we attribute to a shortage of octane triggered by a switch to Standard V fuels in East China from 1 January 2016, which resulted in a spike of mixed aromatic imports for gasoline blending that in turn reduced PX supply.

This tightness has been alleviated in 4Q16, as refineries have been able to increase MX and PX capacity by more than we anticipated. A total of six new MX plants started up in North Asia in 2H16, while major PX producers have debottlenecked capacity by 5-10% this year in response to the strong margins.

These capacity additions have blunted the strength in PX, and we now expect PX margins to be subdued for the next few months until Reliance begins full commercial production of the second phase of its 1.4m t PX plant in early 2017.

Exhibit 55: China oil product trade Exhibit 56: China new crude import quotas

Source: CEIC Source: NDRC

Exhibit 57: MX & PX additions in Asia Exhibit 58: China imports of gasoline blendstocks

Sources: ICIS; BNP Paribas estimates Source: CEIC

(400)

(300)

(200)

(100)

0

100

200

300

400

2010 2011 2012 2013 2014 2015 2016

(kb/d)

Net exports

Net imports0

200

400

600

800

1,000

1,200

1,400

3Q15 4Q15 1Q16 2Q16 3Q16 Total

(kb/d)

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q16 2Q16 3Q16 4Q16

('000 tpa)MX PX

0

500

1,000

1,500

2,000

2,500

3,000

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

('000 tonnes)Naphtha Mixed aromatics

BNP PARIBAS 2 DECEMBER 2016 20

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Investment strategy – primed for a spring surge

To reflect the developments discussed above, we make the following changes:

We raise our 2016-18 Singapore complex refining margin forecasts by USD0.1-0.3/bbl, to reflect the stronger outlook for gasoline and diesel.

We lower 2017-18 PX margin forecasts by USD20/t for each year, to reflect the larger-than-expected MX additions and PX capacity creep.

To reflect these changes in margin assumptions, we make the following changes to our earnings estimates and target prices.

We expect GRMs to descend from the current high levels in December 2016 and January 2017 as refineries return from maintenance. However, we expect a strong rebound in spring 2017 as when the IEA projects a significant level of refinery maintenance in March and April 2017, while US refinery maintenance could be complicated by the shift to Tier-3 gasoline standards, as detailed above.

SKI, which we believe offers a favourable risk/reward balance due to its attractive valuations (2017E P/B of 0.8x vs ROE of 10%) and attractive 2017E dividend yield of 3.9%. We believe the key positive catalysts for SKI are: 1) the final decision on 2016 DPS in February 2017; and 2) securing suitable M&A targets at fair prices.

S-Oil, whose recent confirmation of a 40% dividend payout ratio on 2016 earnings demonstrates that the interests of the major shareholder, Saudi Aramco (Not listed), are aligned with minority shareholders. We believe S-Oil’s plant optimisation and upgrade projects should create long-term value.

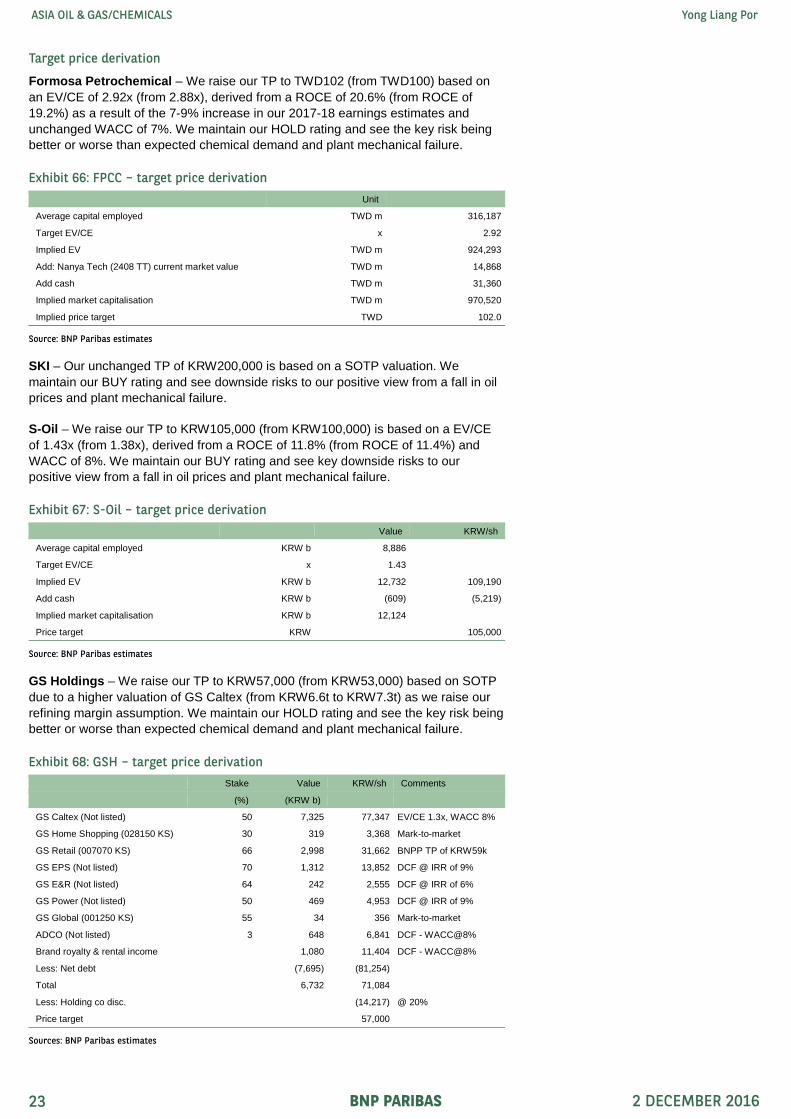

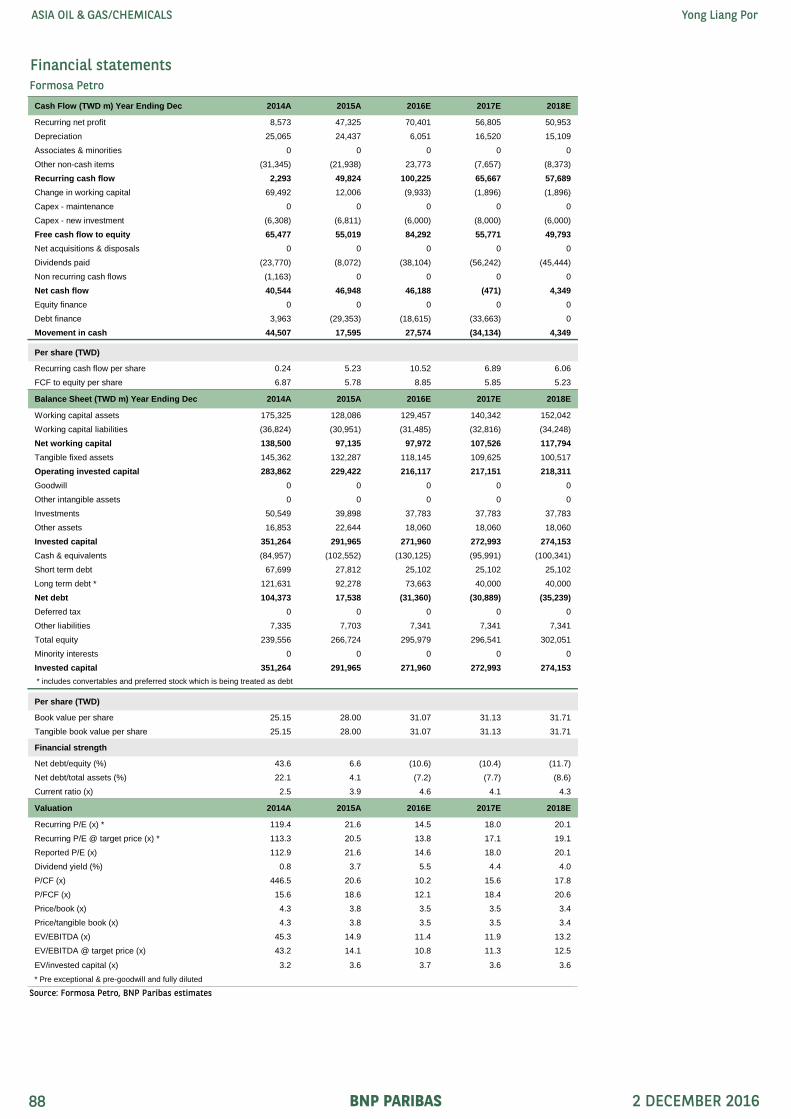

Formosa Petrochemical – We raise our TP to TWD102 (from TWD100) based on an EV/CE of 2.92x (from 2.88x), derived from a ROCE of 20.6% (from ROCE of 19.2%) as a result of the 7-9% increase in our 2017-18 earnings estimates and unchanged WACC of 7%. We maintain our HOLD rating and see the key risk being better or worse than expected chemical demand and plant mechanical failure.

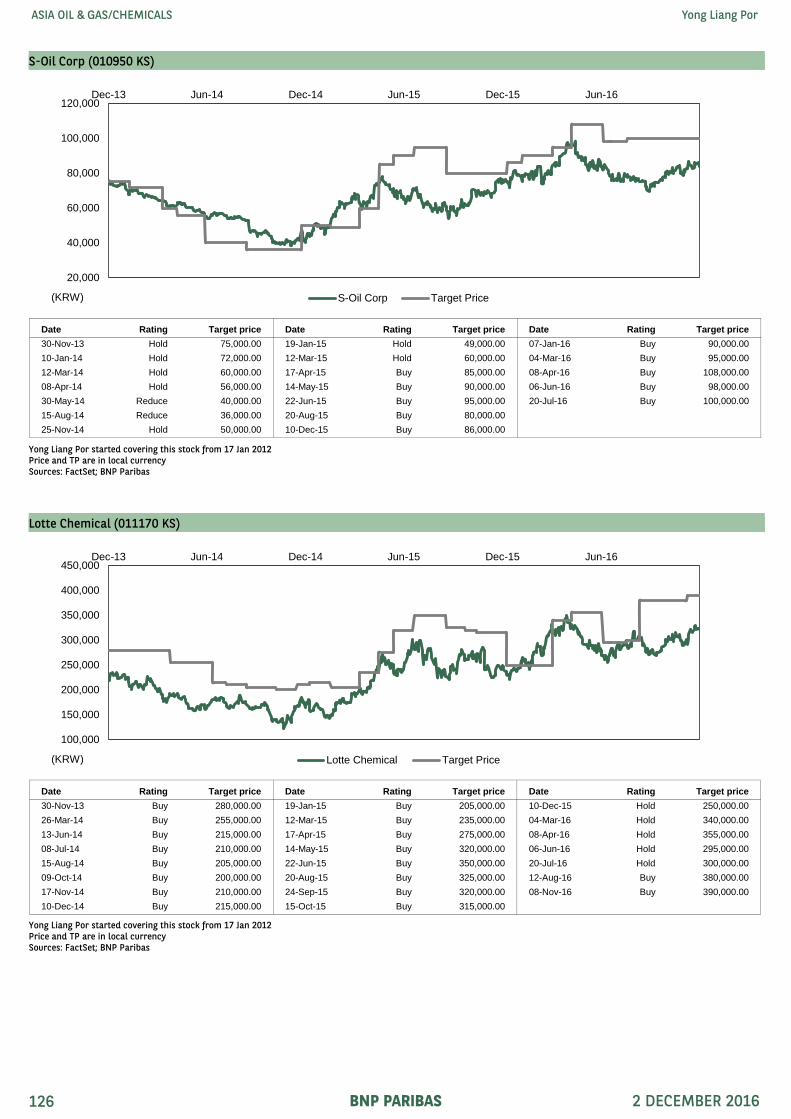

SKI – Our unchanged TP of KRW200,000 is based on a SOTP valuation. We maintain our BUY rating and see downside risks to our positive view from a fall in oil prices and plant mechanical failure.

S-Oil – We raise our TP to KRW105,000 (from KRW100,000) is based on a EV/CE of 1.43x (from 1.38x), derived from a ROCE of 11.8% (from ROCE of 11.4%) and WACC of 8%. We maintain our BUY rating and see key downside risks to our positive view from a fall in oil prices and plant mechanical failure.

GS Holdings – We raise our TP to KRW57,000 (from KRW53,000) based on SOTP due to a higher valuation of GS Caltex (from KRW6.6t to KRW7.3t) as we raise our refining margin assumption. We maintain our HOLD rating and see the key risk being better or worse than expected chemical demand and plant mechanical failure.

Exhibit 66: FPCC – target price derivation Unit

Average capital employed TWD m 316,187

Target EV/CE x 2.92

Implied EV TWD m 924,293

Add: Nanya Tech (2408 TT) current market value TWD m 14,868

Add cash TWD m 31,360

Implied market capitalisation TWD m 970,520

Implied price target TWD 102.0

Source: BNP Paribas estimates

Exhibit 67: S-Oil – target price derivation Value KRW/sh

GS Power (Not listed) 50 469 4,953 DCF @ IRR of 9%

GS Global (001250 KS) 55 34 356 Mark-to-market

ADCO (Not listed) 3 648 6,841 DCF - WACC@8%

Brand royalty & rental income 1,080 11,404 DCF - WACC@8%

Less: Net debt (7,695) (81,254) Total 6,732 71,084 Less: Holding co disc. (14,217) @ 20%

Price target 57,000

Sources: BNP Paribas estimates

BNP PARIBAS 2 DECEMBER 2016 23

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Chemical outlook – Life after the ethylene cycle

In 2016, chemical margins have staged a strong post-CNY rally, as rising oil prices, seasonal maintenance, low inventories, prolonged shutdown of Shell’s (RDSA LN, NR) Singapore cracker and closure of Asahi Kasei’s (3407 JP, NR) cracker in January triggered restocking, which caused a rapid increase in product margins from March to May. In 2Q, ethylene margins averaged USD731/t, the second strongest quarter on record.

Unlike 2015, chemical margins remained steady throughout 3Q16 as heavy plant maintenance continued throughout the quarter, which was partly caused by enforced plant closures in China for the G-20 summit. Most surprisingly, margins of PVC, caustic soda, methanol and urea have rallied strongly in 4Q as the coal price spiked.

On a y-y basis, products whose margins rose were butadiene, ethylene, benzene, PX, styrene and PVC. Products with stable margins were PE, PP and ABS. Products with deteriorating margins were MEG, butyl acrylate, epoxy resins and 2-EH.

In 2016, ethylene margins have averaged USD670/t, a record high, which lifted margins of PE to record highs. Benzene and PX margins improved but are still near the bottom of their recent historical ranges. Products at the bottom of their historical ranges are MEG, AN, ABS, 2-EH, methanol and urea.

Exhibit 69: Margin performance of key products (2016 to date)

Source: Datastream

Exhibit 70: Margin performance of key products – 2016 vs 2015 vs historical six-year average

Source: Datastream

(200)

0

200

400

600

800

1,000

1,200

1,400

Ethy

lene

Prop

ylen

e

BD

Benz

ene

PX

HD

PE

LDP

E

PP

MEG PT

A

PVC

SM AN ABS

Phen

ol

2-E

H

Met

hano

l

Ure

a

(USD/tonne)Current Average Max Min

(200)

0

200

400

600

800

1,000

1,200

1,400

Ethy

lene

Prop

ylen

e

BD

Benz

ene

PX

HD

PE

LDP

E

PP

MEG PT

A

PVC

SM AN ABS

Phen

ol

2-E

H

Met

hano

l

Ure

a

(USD/tonne)2016 2015 Max Min

BNP PARIBAS 2 DECEMBER 2016 24

ASIA OIL & GAS/CHEMICALS Yong Liang Por

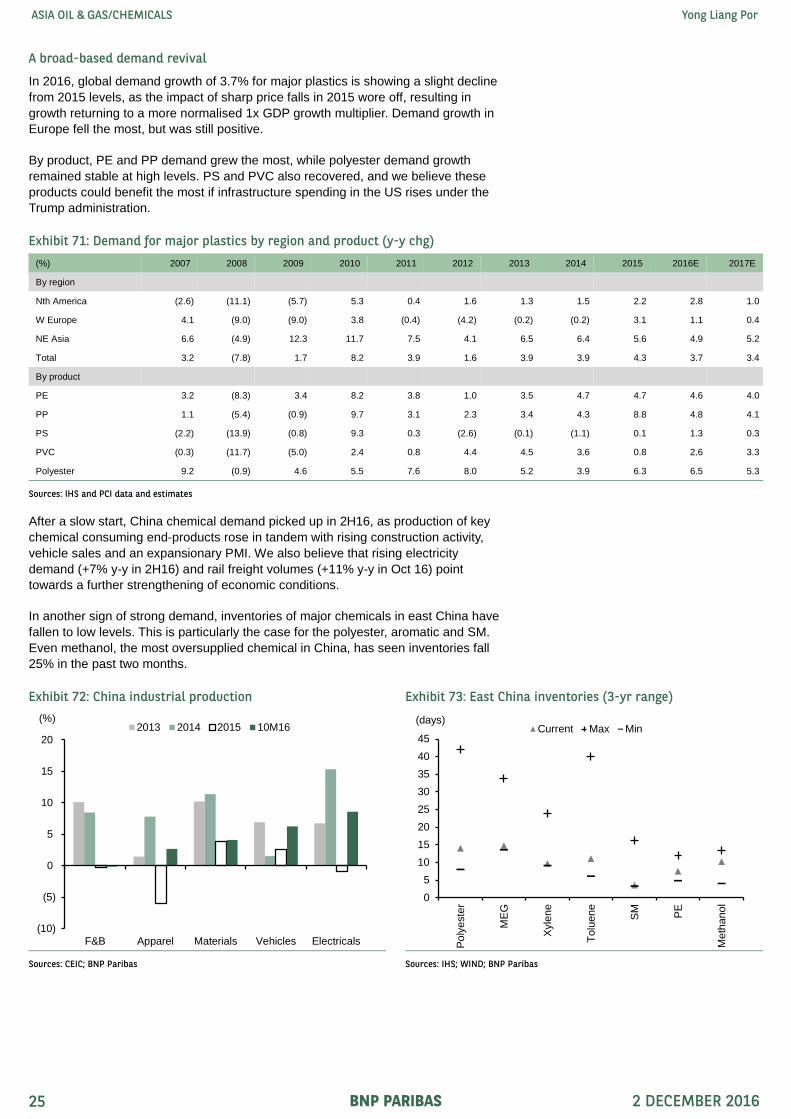

A broad-based demand revival

In 2016, global demand growth of 3.7% for major plastics is showing a slight decline from 2015 levels, as the impact of sharp price falls in 2015 wore off, resulting in growth returning to a more normalised 1x GDP growth multiplier. Demand growth in Europe fell the most, but was still positive.

By product, PE and PP demand grew the most, while polyester demand growth remained stable at high levels. PS and PVC also recovered, and we believe these products could benefit the most if infrastructure spending in the US rises under the Trump administration.

After a slow start, China chemical demand picked up in 2H16, as production of key chemical consuming end-products rose in tandem with rising construction activity, vehicle sales and an expansionary PMI. We also believe that rising electricity demand (+7% y-y in 2H16) and rail freight volumes (+11% y-y in Oct 16) point towards a further strengthening of economic conditions.

In another sign of strong demand, inventories of major chemicals in east China have fallen to low levels. This is particularly the case for the polyester, aromatic and SM. Even methanol, the most oversupplied chemical in China, has seen inventories fall 25% in the past two months.

Exhibit 71: Demand for major plastics by region and product (y-y chg)

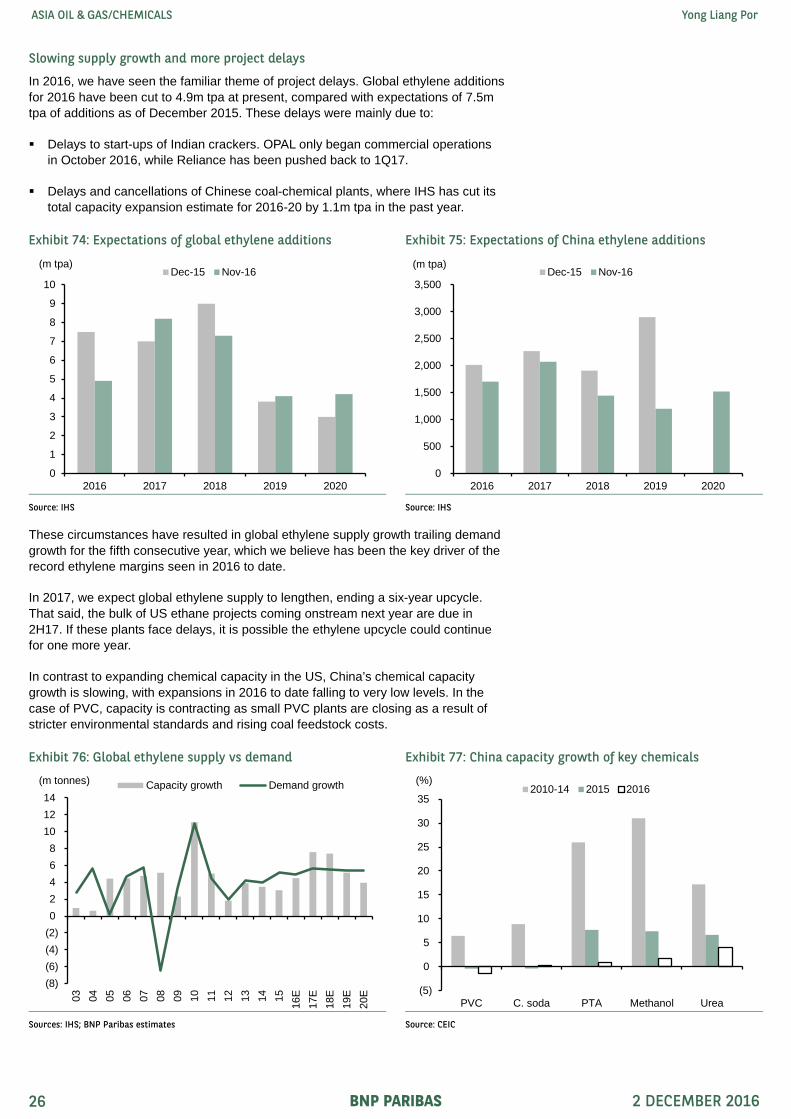

In 2016, we have seen the familiar theme of project delays. Global ethylene additions for 2016 have been cut to 4.9m tpa at present, compared with expectations of 7.5m tpa of additions as of December 2015. These delays were mainly due to:

Delays to start-ups of Indian crackers. OPAL only began commercial operations in October 2016, while Reliance has been pushed back to 1Q17.

Delays and cancellations of Chinese coal-chemical plants, where IHS has cut its total capacity expansion estimate for 2016-20 by 1.1m tpa in the past year.

These circumstances have resulted in global ethylene supply growth trailing demand growth for the fifth consecutive year, which we believe has been the key driver of the record ethylene margins seen in 2016 to date.

In 2017, we expect global ethylene supply to lengthen, ending a six-year upcycle. That said, the bulk of US ethane projects coming onstream next year are due in 2H17. If these plants face delays, it is possible the ethylene upcycle could continue for one more year.

In contrast to expanding chemical capacity in the US, China’s chemical capacity growth is slowing, with expansions in 2016 to date falling to very low levels. In the case of PVC, capacity is contracting as small PVC plants are closing as a result of stricter environmental standards and rising coal feedstock costs.

Exhibit 74: Expectations of global ethylene additions Exhibit 75: Expectations of China ethylene additions

Source: IHS Source: IHS

Exhibit 76: Global ethylene supply vs demand Exhibit 77: China capacity growth of key chemicals

Sources: IHS; BNP Paribas estimates Source: CEIC

0

1

2

3

4

5

6

7

8

9

10

2016 2017 2018 2019 2020

(m tpa)Dec-15 Nov-16

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2016 2017 2018 2019 2020

Dec-15 Nov-16(m tpa)

(8)(6)(4)(2)02468

101214

03 04 05 06 07 08 09 10 11 12 13 14 15 16E

17E

18E

19E

20E

(m tonnes) Capacity growth Demand growth

(5)

0

5

10

15

20

25

30

35

PVC C. soda PTA Methanol Urea

(%)2010-14 2015 2016

BNP PARIBAS 2 DECEMBER 2016 26

ASIA OIL & GAS/CHEMICALS Yong Liang Por

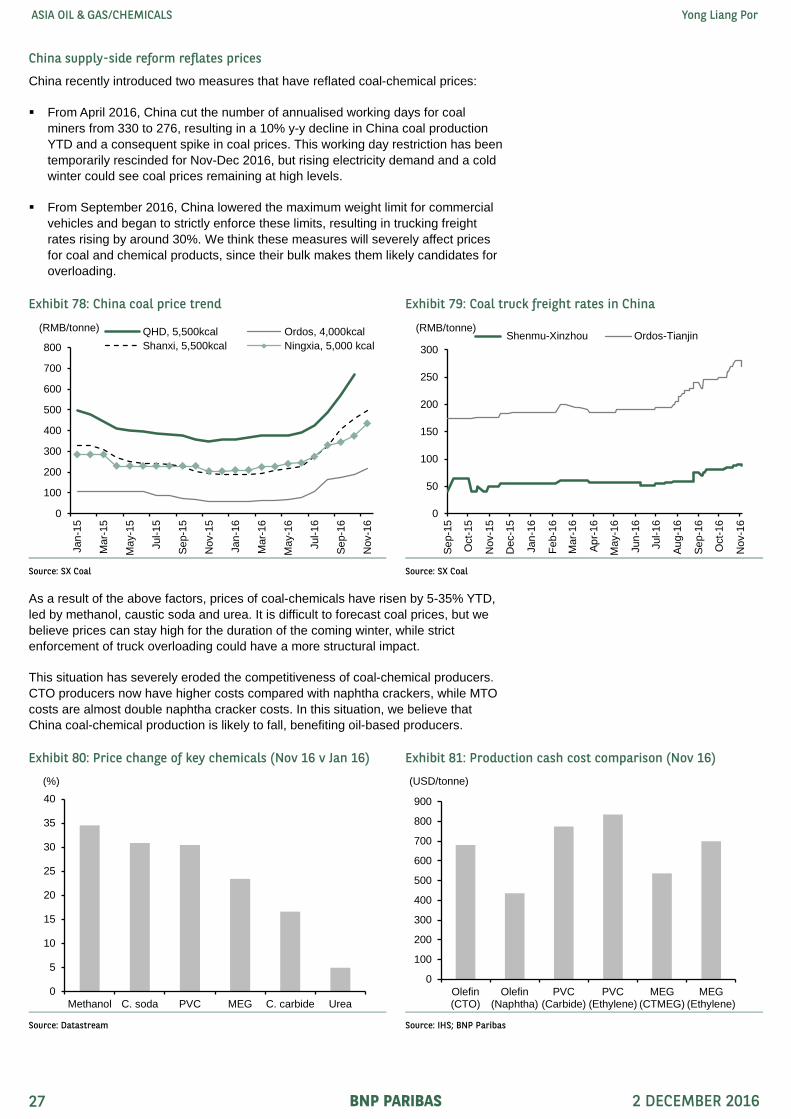

China supply-side reform reflates prices

China recently introduced two measures that have reflated coal-chemical prices:

From April 2016, China cut the number of annualised working days for coal miners from 330 to 276, resulting in a 10% y-y decline in China coal production YTD and a consequent spike in coal prices. This working day restriction has been temporarily rescinded for Nov-Dec 2016, but rising electricity demand and a cold winter could see coal prices remaining at high levels.

From September 2016, China lowered the maximum weight limit for commercial vehicles and began to strictly enforce these limits, resulting in trucking freight rates rising by around 30%. We think these measures will severely affect prices for coal and chemical products, since their bulk makes them likely candidates for overloading.

As a result of the above factors, prices of coal-chemicals have risen by 5-35% YTD, led by methanol, caustic soda and urea. It is difficult to forecast coal prices, but we believe prices can stay high for the duration of the coming winter, while strict enforcement of truck overloading could have a more structural impact.

This situation has severely eroded the competitiveness of coal-chemical producers. CTO producers now have higher costs compared with naphtha crackers, while MTO costs are almost double naphtha cracker costs. In this situation, we believe that China coal-chemical production is likely to fall, benefiting oil-based producers.

Exhibit 78: China coal price trend Exhibit 79: Coal truck freight rates in China

Source: SX Coal Source: SX Coal

Exhibit 80: Price change of key chemicals (Nov 16 v Jan 16) Exhibit 81: Production cash cost comparison (Nov 16)

In 2016 to date, the average price of cotton has risen 4% while that of natural rubber fell 7%. Cotton prices rose with the declining trend in global inventories, while natural rubber prices fell as global inventories remained stubbornly high. Natural rubber prices have risen 17% in the past two months, which we attribute to disrupted production from heavy rains caused by La Nina weather conditions.

We believe cotton prices have the potential to appreciate, as the USDA expects global production to remain low in 2017 as farmers decrease plantings in response to the low price of cotton and more attractive price of soybean (+11% YTD).

In contrast, the supply-demand balance for natural rubber could remain in surplus, as rubber plantings continue to rise and demand remains subdued. Industry consultant The Rubber Economist, estimates that global natural rubber acreage increased at a 5% CAGR from 2010-15, mainly from smaller rubber producers such as Laos, Cambodia, Myanmar and Ghana.

While supply continues to rise, global rubber demand has grown at just 1% in both 2015 and 2016 to date, due to subdued rubber tyre demand. In 2017, the Rubber Economist forecasts demand to grow at 2.8%, but this is still below production growth of 4%. Hence, we do not believe the recent increase in natural rubber prices is sustainable.

Exhibit 82: Global cotton inventory and price Exhibit 83: Global cotton production

Sources: USDA; Datastream Source: USDA

Exhibit 84: Global natural rubber inventory and prices Exhibit 85: Global natural rubber production

(m tonnes)(m hectares)Acreage (LHS) Production (RHS)

BNP PARIBAS 2 DECEMBER 2016 28

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Long term trends: Synthetic materials propel polyester growth

In 2016, PCI forecasts global polyester demand growth of 6.5%, which is higher than the growth rate of other major chemicals such as PE and PP, whose growth is usually in line with GDP growth. We believe the following two structural trends support polyester’s continued strong growth:

The growing preference for man-made fibres over natural fibres. Synthetic fabrics have increased their acceptance in mainstream apparel, particularly in active-wear. In 2014, the US imported more textiles and apparel made of synthetic fibres than natural fibres for the first time. In turn, this has led textile producers to configure machines to use synthetic fibres, creating a self-reinforcing trend.

Cotton prices are 71% more expensive than polyester, which is partly due to the oil price decline since November 2014. We believe this premium is likely to persist in the coming years, based on our assumption of Brent oil prices of USD58/bbl in 2017 and USD68/bbl in 2018.

Consequently, we expect man-made fibres to further increase their textile volume market share to 73% and reach total sales volume of 83m tonnes by 2020. As we assume the majority of man-made fibre growth will come from polyester, this is sufficient to generate global polyester demand growth of between 4m and 5m tonnes per annum for 2015-2020E.

Exhibit 86: US imports of textiles and apparel Exhibit 87: Cotton and polyester price trend

Source: US Dept of Commerce Source: US Dept of Commerce

Exhibit 88: Global demand of textile fibres Exhibit 89: Global polyester demand growth

Long-term trends: Unlocking developing Asian demand

From 2005-2015, we estimate that China chemical demand saw a CAGR of 10%, accounting for 45% of global chemical demand growth in that period. As China’s economic growth is slowing down and the country is transitioning to a more service-led economy, this source of demand growth is likely to ebb, in our view.

We believe the rapid development of other developing Asian economies can partially offset slowing China demand growth. These countries include Vietnam, India, Indonesia and the Philippines (VIIP), who have a combined population of 1.7b, GDP of USD3.7t and a GDP per capita of USD2,340. GDP growth of VIIP averaged 6.3% pa from 2010-15, and the IMF forecasts growth of 6.4% pa for 2016-20.

In comparison with China, the VIIP economy is presently only the same size as the Chinese economy in 2007, and the growth rate is slower compared with China at the equivalent GDP level. However, there is significant room for growth, as VIIP chemical consumption per capita was very low at just 7.7kg in 2015.

In this regard, we believe India has the greatest potential for growth, as the government has introduced measures to boost infrastructure spending and domestic consumption. For example, the Clean India programme entails construction of a new sewerage system, which requires significant volumes of PVC and PP for pipes. We estimate that annual VIIP demand for chemicals will expand by 14m tonnes from 2015 to 2020, equivalent to six new world-scale crackers.

Exhibit 90: GDP growth of key developing countries Exhibit 91: Aggregate GDP per capita of VIIP

Source: IMF Source: IMF

Exhibit 92: GDP comparison vs China Exhibit 93: Polyolefin demand vs GDP per capita (2015)

Source: IMF Sources: IHS; IMF; BNP Paribas estimates

In 2017, we expect a majority of chemicals to face a tightening supply-demand balance, as capacity expansions slow following years of rapid expansion. Products that face lengthening supply include AN, PE, PX, urea and ethylene. Our key conclusions for 2017 product margins are:

Ethylene and PE to fall from 2016 levels, but remain at still-high levels.

PX margins should improve after 1Q17 once Reliance starts up its new plant.

BD, benzene and SM margins should further improve.

SBR overcapacity continues to weigh on non-integrated margins.

Strong margins of coal-chemicals such as PVC, caustic soda, MEG and PP, although this is dependent on continued high coal prices. For these products, our nameplate utilisation rate model is less useful as China’s supply-side measures play a more important role in price formation.

For 2018, we expect only three of 22 chemicals to see excess supply, as capacity expansions slow down further. We expect the biggest beneficiaries to be MEG, benzene, PX, BPA, phenol and SBR, as they face the largest tightening scenarios, which should bring about significant improvements in their utilisation rates.

Exhibit 94: Global supply less demand change (2017) Exhibit 95: Global utilisation rate (2017)

Investment strategy – Bullish on value and laggard plays

We make no significant changes to our chemical margin estimates in this report, as we had already made upward revisions to prices and margins of coal-chemicals in our previous report, Black Beauty, 8 November 2016. To take into account company-specific factors, we make the following earnings revisions:

Formosa Plastics, Formosa Chemicals and Nan Ya Plastics – we raise 2017-18 earnings estimates by 2-4% to reflect the stronger contributions from FPCC, where we had raised earnings by 7-9% over the corresponding period.

LG Chem – we lower 2017-18 earnings estimates by 5-7% to reflect lower EV battery sales in China following the recent proposal by the Ministry of Industry and Information Technology (MIIT) to raise the bar for annual output of certified lithium-ion battery makers to 8GWh.

Our top sector BUYs are:

Lotte Chem offers a favourable risk/reward balance due to its attractive valuations (2017E P/B of 1.1x vs ROE of 14%) and exposure to MEG and SM, whose margins could positively surprise. We believe LC’s focus on chemical capacity expansions should enable it to create long-term value.

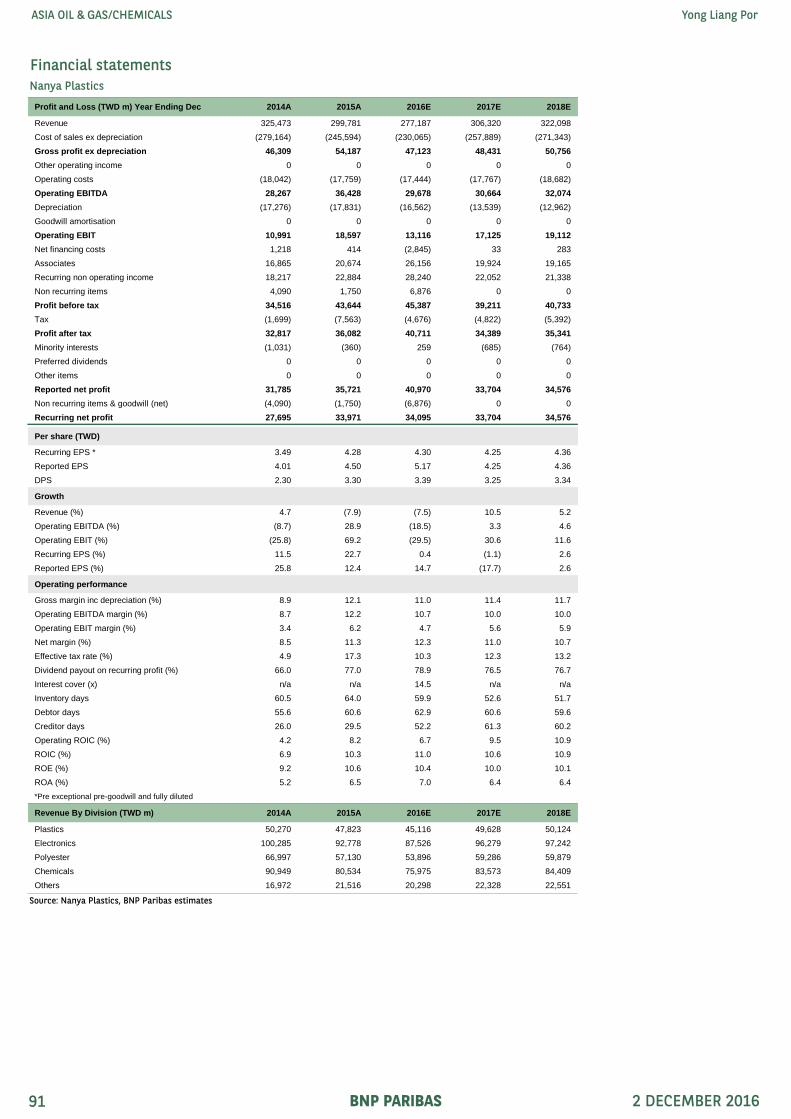

Nan Ya Plastic is a potential turnaround story, in our view, due to rebounding MEG margins, rising copper foil margins and reduced DRAM exposure. YTD, NYP’s share price performance has significantly lagged its sister Formosa group companies, and we expect improving product margins to enable its share price to catch up.

PTTGC is well placed to benefit from potentially rising oil prices in 2017E, while y-y comparisons should benefit from the low base effect in 2016, when earnings have been negatively affected by a series of unplanned plant shutdowns.

In 2017, we believe these factors could further boost the chemical outlook: 1) USD strength benefits local currency operating profits; and 2) increased US infrastructure spending should boost chemical demand. The key downside risks to our positive view are: 1) a sharp fall in coal prices; and 2) China commodity speculation, which has played a part in driving chemical prices higher, may be curbed.

Exhibit 98: Changes to earnings estimates and target prices

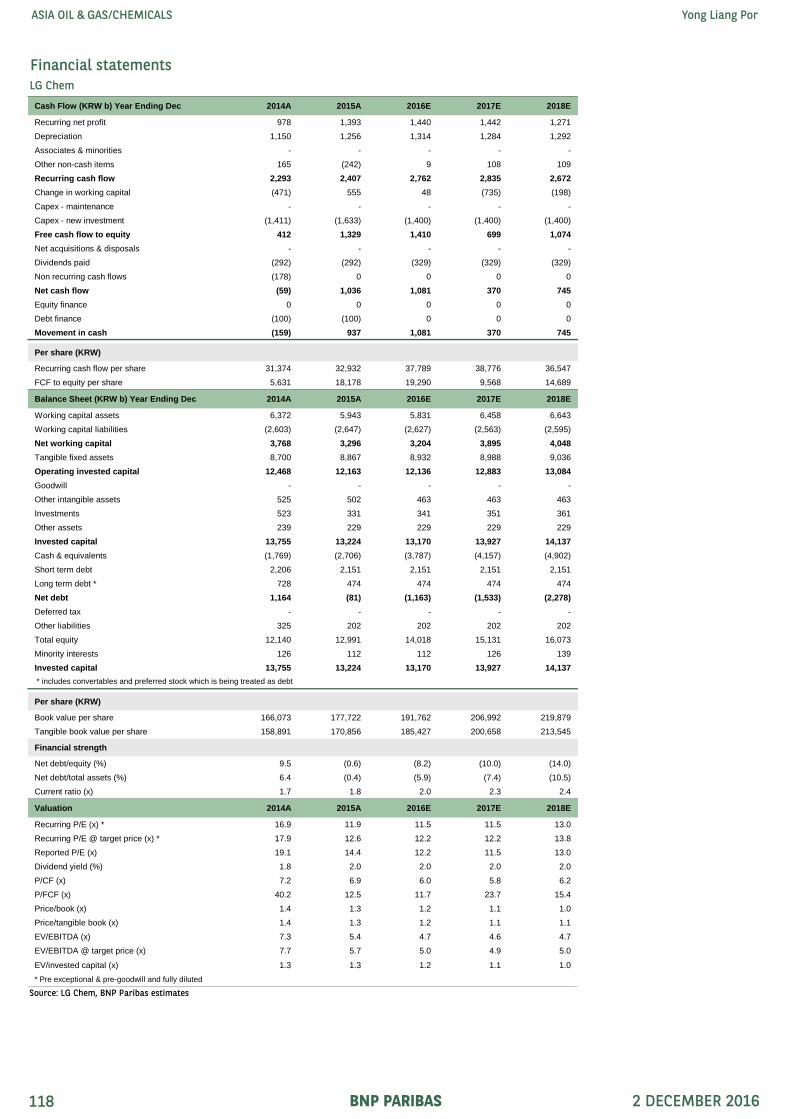

LG Chem – We cut our TP to KRW240,000 (from KRW265,000) based on a EV/CE of 1.25x (from 1.38x), derived from a lower ROCE of 10.5% (from 11.6%) as a result of the 5-7% cut to 2017-18E earnings estimates and WACC of 8%. We maintain our HOLD rating and see the key upside/downside risks being stronger/weaker-than-expected chemical and EV battery demand.

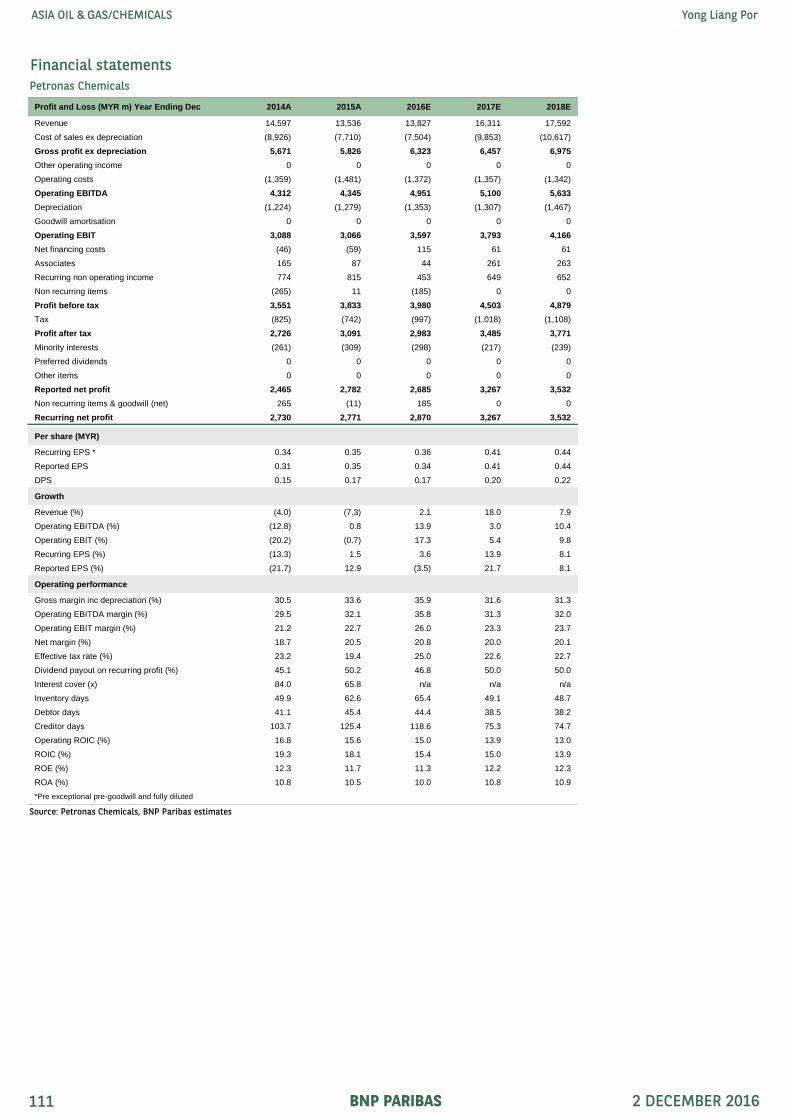

Petronas Chem – Our unchanged TP of MYR6.5 is based on a target EV/CE of 1.64x, derived from a ROCE of 13.4% and WACC of 8% (unchanged). We maintain our HOLD rating and see the key upside/downside risk to our TP coming from volatile oil prices.

Formosa Plastic – We raise our TP to TWD86 (from TWD85) based on SoTP, due to our higher valuation of FPCC (from TWD281b to TWD286b). We maintain our HOLD rating and see the key risk being better or worse than expected chemical demand and plant mechanical failure.

Lotte Chemical – We raise our TP to KRW400,000 (from KRW390,000) which is based on a EV/CE of 1.4x (from 1.7x), derived from an ROCE of 12.5% (from 14.7%) and as we roll over capital employed to 2017E (from 2016E) and WACC of 9% (unchanged). We maintain our BUY rating and see the key downside risk coming from weaker-than-expected chemical demand and plant mechanical failure.

Exhibit 102: LGC – TP derivation Value Won/sh

Average capital employed KRW b 13,168

Target EV/CE x 1.25

Implied EV KRW b 16,516 225,939

add cash KRW b 1,163 15,905

Implied market capitalisation KRW b 17,679

Price target KRW 240,000

Source: BNP Paribas estimates

Exhibit 103: FPC – TP derivation Value TWD/ Comments

(TWD m) share

Average invested capital TWD m 120,161 At 1.2x EV/IC

Target EV/IC x 1.2

Implied EV TWD m 140,670 22.1

Less debt TWD m (57,763) (9.1) 2016E net debt

Add investments:

Formosa Petrochem. (30%) TWD m 286,637 45.0 TP @TWD102

Nan Ya Plastic (10%) TWD m 58,124 9.1 TP @TWD75

Formosa Chemical (3%) TWD m 18,436 2.9 TP @TWD110

Formosa Sumco (3532 TT) TWD m 7,810 1.2 Market price @TWD41.7as at 30/11

Nanya Tech (2408 TT) TWD m 15,985 2.5 Market price @TWD40as at 30/11

Other investments TWD m 74,579 11.7 At 1x book value

Implied market capitalisation TWD m 544,493

Price target TWD 86.0

Source: BNP Paribas estimates

Exhibit 104: LC – TP derivation Value KRW/sh

Average capital employed KRW b 11,523

Target EV/CE x 1.4

Implied EV KRW b 15,671 457,223

Add cash KRW b (1,998) (58,289)

Price target KRW 400,000

Sources: BNP Paribas estimates

BNP PARIBAS 2 DECEMBER 2016 34

ASIA OIL & GAS/CHEMICALS Yong Liang Por

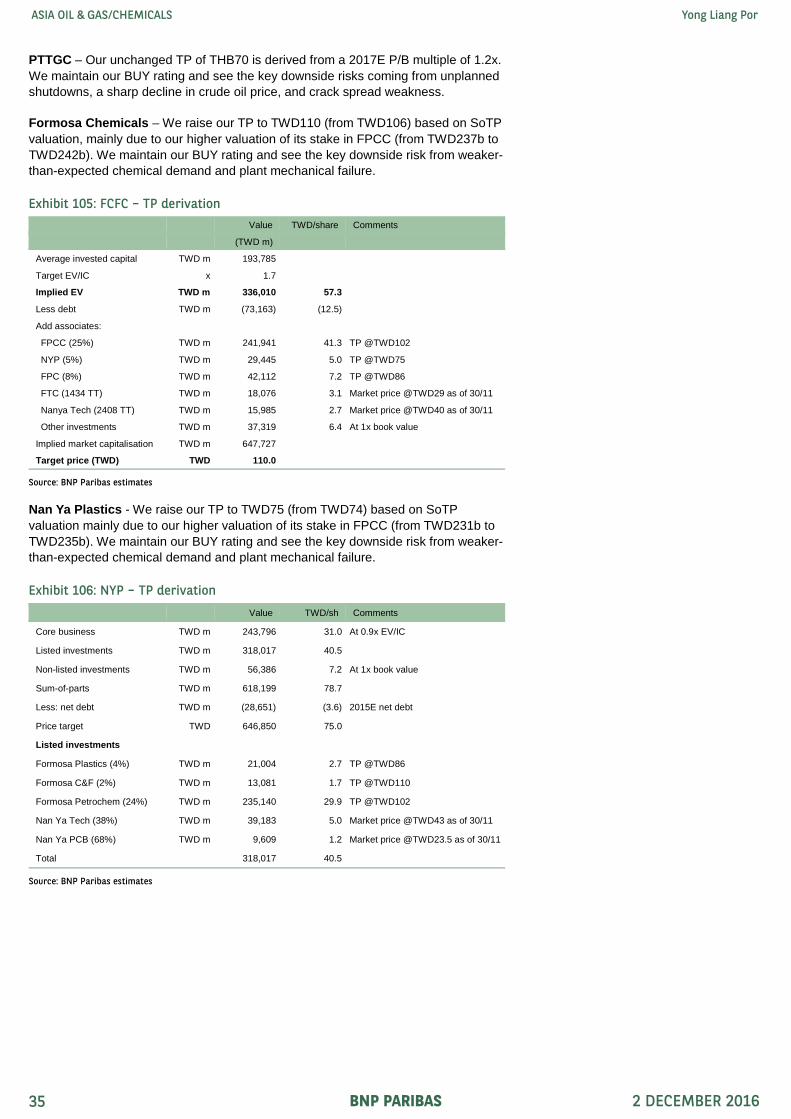

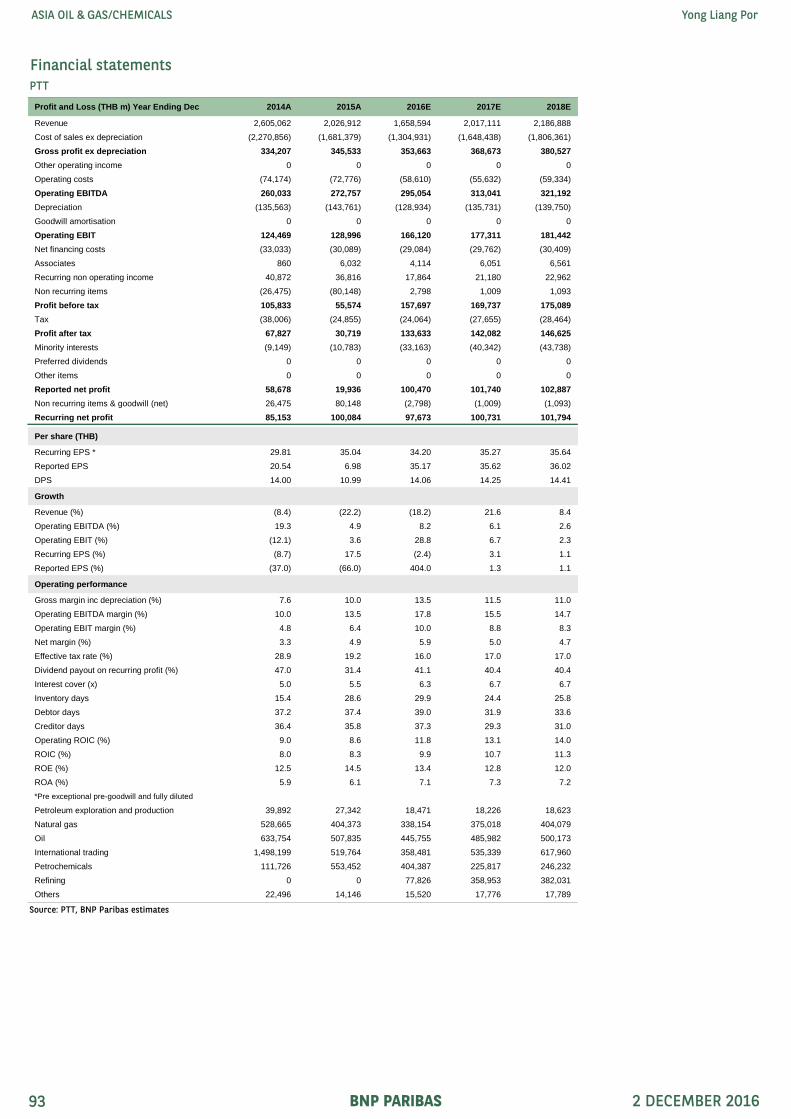

PTTGC – Our unchanged TP of THB70 is derived from a 2017E P/B multiple of 1.2x. We maintain our BUY rating and see the key downside risks coming from unplanned shutdowns, a sharp decline in crude oil price, and crack spread weakness.

Formosa Chemicals – We raise our TP to TWD110 (from TWD106) based on SoTP valuation, mainly due to our higher valuation of its stake in FPCC (from TWD237b to TWD242b). We maintain our BUY rating and see the key downside risk from weaker-than-expected chemical demand and plant mechanical failure.

Nan Ya Plastics - We raise our TP to TWD75 (from TWD74) based on SoTP valuation mainly due to our higher valuation of its stake in FPCC (from TWD231b to TWD235b). We maintain our BUY rating and see the key downside risk from weaker-than-expected chemical demand and plant mechanical failure.

Exhibit 105: FCFC – TP derivation

Value TWD/share Comments

(TWD m)

Average invested capital TWD m 193,785

Target EV/IC x 1.7

Implied EV TWD m 336,010 57.3

Less debt TWD m (73,163) (12.5)

Add associates:

FPCC (25%) TWD m 241,941 41.3 TP @TWD102

NYP (5%) TWD m 29,445 5.0 TP @TWD75

FPC (8%) TWD m 42,112 7.2 TP @TWD86

FTC (1434 TT) TWD m 18,076 3.1 Market price @TWD29 as of 30/11

Nanya Tech (2408 TT) TWD m 15,985 2.7 Market price @TWD40 as of 30/11

Other investments TWD m 37,319 6.4 At 1x book value

Implied market capitalisation TWD m 647,727

Target price (TWD) TWD 110.0

Source: BNP Paribas estimates

Exhibit 106: NYP – TP derivation

Value TWD/sh Comments

Core business TWD m 243,796 31.0 At 0.9x EV/IC

Listed investments TWD m 318,017 40.5

Non-listed investments TWD m 56,386 7.2 At 1x book value

Sum-of-parts TWD m 618,199 78.7

Less: net debt TWD m (28,651) (3.6) 2015E net debt

Price target TWD 646,850 75.0

Listed investments

Formosa Plastics (4%) TWD m 21,004 2.7 TP @TWD86

Formosa C&F (2%) TWD m 13,081 1.7 TP @TWD110

Formosa Petrochem (24%) TWD m 235,140 29.9 TP @TWD102

Nan Ya Tech (38%) TWD m 39,183 5.0 Market price @TWD43 as of 30/11

Nan Ya PCB (68%) TWD m 9,609 1.2 Market price @TWD23.5 as of 30/11

Total 318,017 40.5

Source: BNP Paribas estimates

BNP PARIBAS 2 DECEMBER 2016 35

ASIA OIL & GAS/CHEMICALS Yong Liang Por

China outlook – Step by step

2016 – Government lends a helping hand

In 2016 to date, the China oil & gas sector has had a less eventful year than usual, with no major policy or price changes. Government measures were mainly supportive of NOCs, in recognition of the difficult operating conditions. The major reform announced this year concerned the gas transmission tariff, which would not have any significant impact on companies’ earnings.

China’s supply-side reform has extended to the oil & gas sector, with China oil production declining by 6% in 2016 to date, the largest fall on record as NOCs cut production at high-cost fields. To make up for the lower production, China’s oil imports have risen by 0.9 mb/d in 2016 to 7.7mb/d, a record high. This trend was also evident in the gas sector, as production growth slowed and imports jumped.

In 1Q16, as NOCs suffered large upstream losses, the government froze oil product prices at mid-December 2015 levels, effectively setting a price floor for oil at USD40/bbl. This allowed Chinese refineries to generate a record operating profit in that quarter, which the government has so far allowed them to keep despite an earlier directive to direct these windfall profits to an unspecified environmental fund.

To alleviate refining sector overcapacity, the government has encouraged capacity rationalisation among independent refiners and increased oil product export quotas, causing oil product exports, notably diesel, to sharply rise in 2016.

Exhibit 107: China oil production & imports Exhibit 108: China gas production and imports

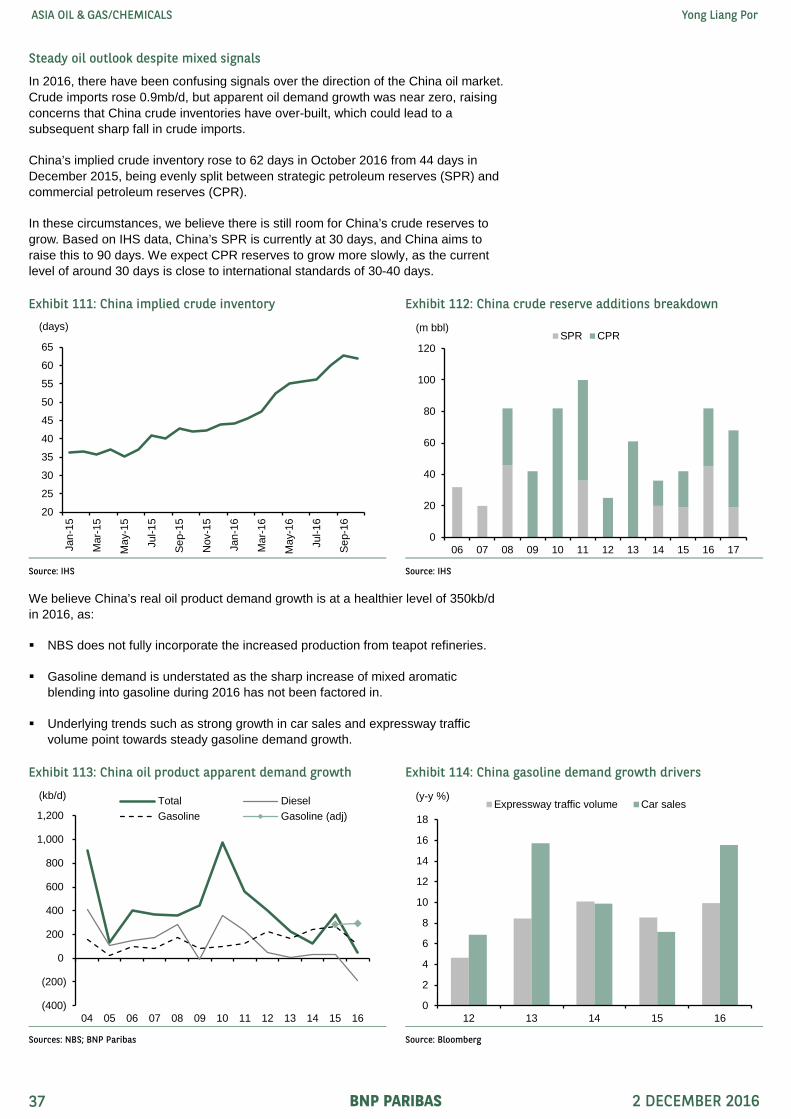

In 2016, there have been confusing signals over the direction of the China oil market. Crude imports rose 0.9mb/d, but apparent oil demand growth was near zero, raising concerns that China crude inventories have over-built, which could lead to a subsequent sharp fall in crude imports.

China’s implied crude inventory rose to 62 days in October 2016 from 44 days in December 2015, being evenly split between strategic petroleum reserves (SPR) and commercial petroleum reserves (CPR).

In these circumstances, we believe there is still room for China’s crude reserves to grow. Based on IHS data, China’s SPR is currently at 30 days, and China aims to raise this to 90 days. We expect CPR reserves to grow more slowly, as the current level of around 30 days is close to international standards of 30-40 days.

We believe China’s real oil product demand growth is at a healthier level of 350kb/d in 2016, as:

NBS does not fully incorporate the increased production from teapot refineries.

Gasoline demand is understated as the sharp increase of mixed aromatic blending into gasoline during 2016 has not been factored in.

Underlying trends such as strong growth in car sales and expressway traffic volume point towards steady gasoline demand growth.

Exhibit 111: China implied crude inventory Exhibit 112: China crude reserve additions breakdown

Source: IHS Source: IHS

Exhibit 113: China oil product apparent demand growth Exhibit 114: China gasoline demand growth drivers

Sources: NBS; BNP Paribas Source: Bloomberg

20

25

30

35

40

45

50

55

60

65

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16(days)

0

20

40

60

80

100

120

06 07 08 09 10 11 12 13 14 15 16 17

(m bbl)SPR CPR

(400)

(200)

0

200

400

600

800

1,000

1,200

04 05 06 07 08 09 10 11 12 13 14 15 16

(kb/d) Total DieselGasoline Gasoline (adj)

0

2

4

6

8

10

12

14

16

18

12 13 14 15 16

(y-y %)Expressway traffic volume Car sales

BNP PARIBAS 2 DECEMBER 2016 37

ASIA OIL & GAS/CHEMICALS Yong Liang Por

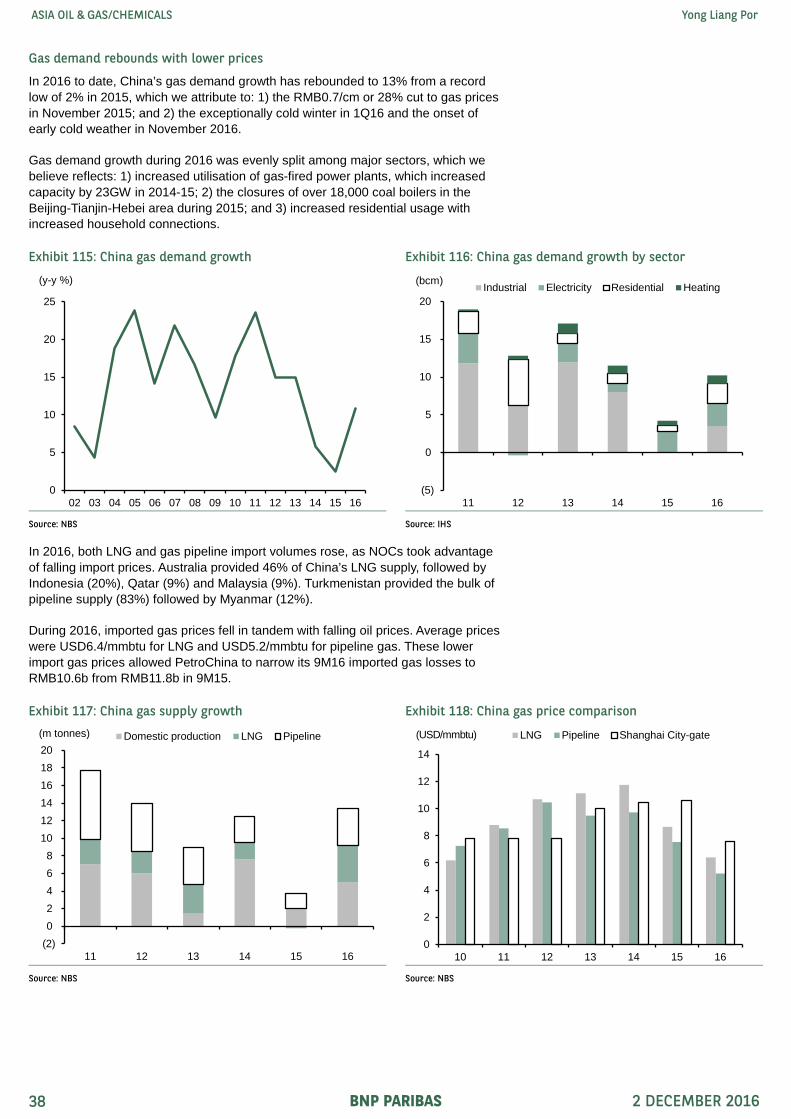

Gas demand rebounds with lower prices

In 2016 to date, China’s gas demand growth has rebounded to 13% from a record low of 2% in 2015, which we attribute to: 1) the RMB0.7/cm or 28% cut to gas prices in November 2015; and 2) the exceptionally cold winter in 1Q16 and the onset of early cold weather in November 2016.

Gas demand growth during 2016 was evenly split among major sectors, which we believe reflects: 1) increased utilisation of gas-fired power plants, which increased capacity by 23GW in 2014-15; 2) the closures of over 18,000 coal boilers in the Beijing-Tianjin-Hebei area during 2015; and 3) increased residential usage with increased household connections.

In 2016, both LNG and gas pipeline import volumes rose, as NOCs took advantage of falling import prices. Australia provided 46% of China’s LNG supply, followed by Indonesia (20%), Qatar (9%) and Malaysia (9%). Turkmenistan provided the bulk of pipeline supply (83%) followed by Myanmar (12%).

During 2016, imported gas prices fell in tandem with falling oil prices. Average prices were USD6.4/mmbtu for LNG and USD5.2/mmbtu for pipeline gas. These lower import gas prices allowed PetroChina to narrow its 9M16 imported gas losses to RMB10.6b from RMB11.8b in 9M15.

Exhibit 115: China gas demand growth Exhibit 116: China gas demand growth by sector

Source: NBS Source: IHS

Exhibit 117: China gas supply growth Exhibit 118: China gas price comparison

Source: NBS Source: NBS

0

5

10

15

20

25

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

(y-y %)

(5)

0

5

10

15

20

11 12 13 14 15 16

(bcm) Industrial Electricity Residential Heating

(2)02468

101214161820

11 12 13 14 15 16

(m tonnes) Domestic production LNG Pipeline

0

2

4

6

8

10

12

14

10 11 12 13 14 15 16

(USD/mmbtu) LNG Pipeline Shanghai City-gate

BNP PARIBAS 2 DECEMBER 2016 38

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Depleting oil production and reserves point to M&A

In 2016 to date, China’s domestic oil production has fallen 5%, the second-largest decline after the US, representing a reversal from the historical 10-year CAGR of 1.9%. Wood Mackenzie projects China oil production falling to 3.5mb/d by 2020 due to:

The impact of heavy capex cuts since 2015, which have cut production most heavily at mature oil fields such as Daqing (PetroChina) and Shengli (Sinopec), and high-cost heavy oil fields like Liaohe (PetroChina).

High likelihood of more field shut-ins at high-cost China oil wells, where one-third of production currently generates a negative net present value at Brent prices of USD40/bbl.

The high cost of pre-development projects in China, of whom 35% are loss-making at USD40/bbl and are at risk of deferral or cancellation.

This weak production outlook points towards continued weakness in the oil services sector. IHS estimates that onshore wells drilled in China are likely to remain range-bound at 17,000 wells pa from 2016-20, half the levels of 2013, as China NOCs prioritise higher efficiency and cost-effectiveness.

In this scenario, IHS expects China’s fracturing utilisation rates to only gradually recover to 40% in 1H18 from 32% in 1H16.In this segment, PetroChina enjoys a higher utilisation rate of around 50%, compared with Sinopec at 30%.

Exhibit 119: China domestic oil production Exhibit 120: China oil supply breakeven cost (NPV 10)

Source: Wood Mackenzie Source: Wood Mackenzie

Exhibit 121: China onshore wells drilled Exhibit 122: China fracturing utilisation rates

Source: IHS Source: IHS

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

10 11 12 13 14 15 16 17E 18E 19E 20E

(mb/d)PetroChina Sinopec CNOOC Others

0

20

40

60

100 600 1,100 1,600 2,100 2,600 3,100 3,600

(USD/boe)

Liquid production in 2016 (kb/d)

MainlyCNOOC

MainlyPetroChina

MainlySinopec

4

6

8

10

12

14

16

18

20

1H13

2H13

1H14

2H14

1H15

2H15

1H16

2H16

1H17

2H17

1H18

2H18

1H19

2H19

1H20

2H20

('000 wells)

20

25

30

35

40

45

50

55

60

65

1H13

2H13

1H14

2H14

1H15

2H15

1H16

2H16

1H17

2H17

1H18

2H18

1H19

2H19

1H20

2H20

(%)

BNP PARIBAS 2 DECEMBER 2016 39

ASIA OIL & GAS/CHEMICALS Yong Liang Por

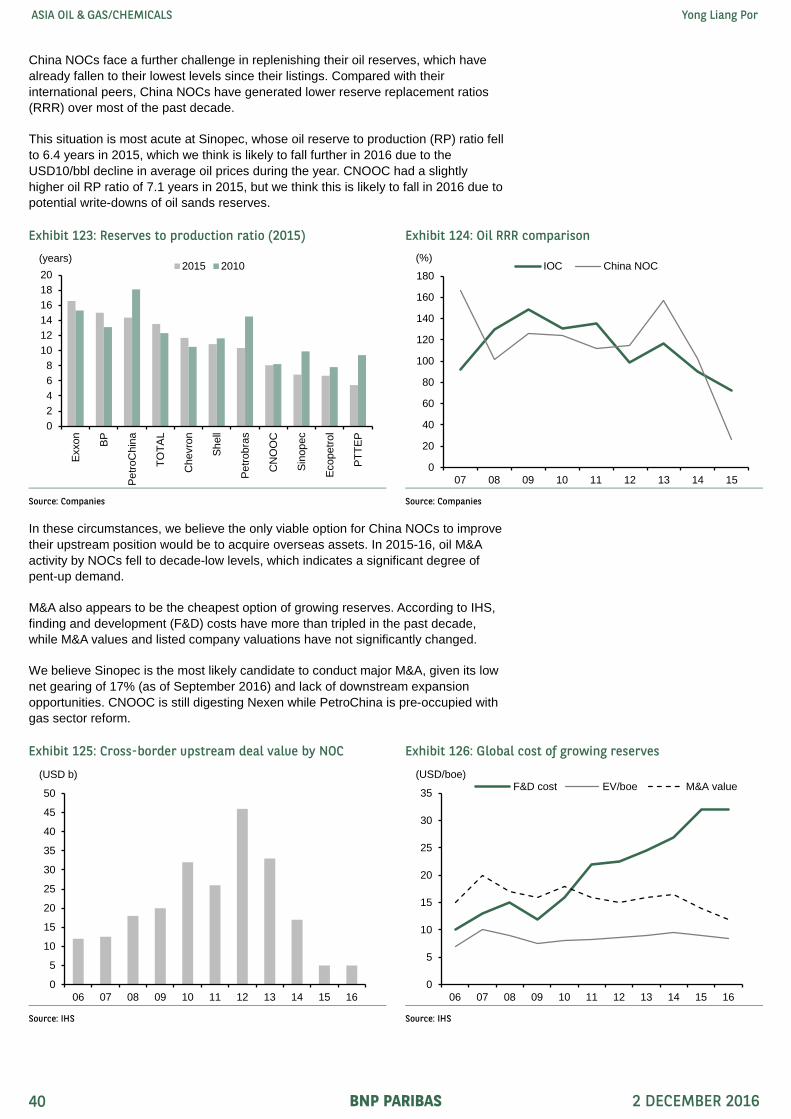

China NOCs face a further challenge in replenishing their oil reserves, which have already fallen to their lowest levels since their listings. Compared with their international peers, China NOCs have generated lower reserve replacement ratios (RRR) over most of the past decade.

This situation is most acute at Sinopec, whose oil reserve to production (RP) ratio fell to 6.4 years in 2015, which we think is likely to fall further in 2016 due to the USD10/bbl decline in average oil prices during the year. CNOOC had a slightly higher oil RP ratio of 7.1 years in 2015, but we think this is likely to fall in 2016 due to potential write-downs of oil sands reserves.

In these circumstances, we believe the only viable option for China NOCs to improve their upstream position would be to acquire overseas assets. In 2015-16, oil M&A activity by NOCs fell to decade-low levels, which indicates a significant degree of pent-up demand.

M&A also appears to be the cheapest option of growing reserves. According to IHS, finding and development (F&D) costs have more than tripled in the past decade, while M&A values and listed company valuations have not significantly changed.

We believe Sinopec is the most likely candidate to conduct major M&A, given its low net gearing of 17% (as of September 2016) and lack of downstream expansion opportunities. CNOOC is still digesting Nexen while PetroChina is pre-occupied with gas sector reform.

Exhibit 123: Reserves to production ratio (2015) Exhibit 124: Oil RRR comparison

Source: Companies Source: Companies

Exhibit 125: Cross-border upstream deal value by NOC Exhibit 126: Global cost of growing reserves

Source: IHS Source: IHS

02468

101214161820

Exxo

n

BP

Petro

Chi

na

TOTA

L

Che

vron

Shel

l

Petro

bras

CN

OO

C

Sino

pec

Ecop

etro

l

PTTE

P

(years)2015 2010

0

20

40

60

80

100

120

140

160

180

07 08 09 10 11 12 13 14 15

(%)IOC China NOC

0

5

10

15

20

25

30

35

40

45

50

06 07 08 09 10 11 12 13 14 15 16

(USD b)

0

5

10

15

20

25

30

35

06 07 08 09 10 11 12 13 14 15 16

(USD/boe)F&D cost EV/boe M&A value

BNP PARIBAS 2 DECEMBER 2016 40

ASIA OIL & GAS/CHEMICALS Yong Liang Por

Healthy gas volume growth but limited price upside potential

In contrast to oil, China’s gas sector continues to enjoy strong demand growth and stable prices. In 2016, the shape of gas sector reform has become clearer, with the government stepping back from a big-bang approach (such as creating an independent pipeline company) and towards these incremental measures:

On 12 October, NDRC announced a tariff-setting mechanism for pipeline tariffs and pipeline operating rate of return, based on an after-tax return on full investment of 8%. This system improves pricing transparency and paves the way for eventual liberalisation of well-head and city-gate prices.

On 16 November, NDRC announced that the city-gate gas price in Fujian (3% of China demand) would be liberalised and based on negotiations between suppliers and customers. We assume this liberalisation will be extended to other major cities in due course.

On 20 November, NDRC removed the price cap of natural gas for fertiliser producers, which would allow gas suppliers to significantly raise gas prices equivalent to 7% of China’s demand.

On 22 November, local news reported that PetroChina would lift non-residential city-gas prices by 10-15% from 20 November 2016 to15 March 2017, the first time that PetroChina has applied for a price increase since NDRC granted gas suppliers flexibility to negotiate prices within a +/- 20% range.

Broadly, these measures have moved the gas market closer to full deregulation with greater price flexibility, improved third-party access and lowered transmission costs. These measures are broadly positive for demand growth, by better matching supply with demand, and should allow gas demand to return to mid-teens growth.

While we are positive on gas volume growth in China, we see less upside potential for gas prices due to considerable oversupply: