12

April 2019 Valuation Insights Equity Risk Premium in India

April 2019

Valuation InsightsEquity Risk Premium in India

Section Page

1. Foreword 03

2. Executivesummary 04

3. Backgroundandcontext 05

4. Approachandmethodology 06

Contents

About Valuation Insights

ValuationInsightsisaperiodicpublicationofGrantThorntonIndiaLLP,amemberfirmwithinGrantThorntonInternationalLtd.Itisourefforttodiscussandaddressvariousvaluationissuesusingthebestpracticesandinternationalguidelines.Ourteamofprofessionalssharestheirthoughtsonthenuancesofvaluationsandtheirstrategicandpracticalimplications.

02ValuationInsights

Disclaimer

ERPestimationinvolvestheuseofsubjectiveestimatesandmultipleapproaches.HencedifferentresearchersmaycomeoutwithdifferentERPs.Further,theERPconcludedinthisreportrepresentstheERPprevailingafterthepublicationdateandhenceshouldnotbeconsideredrepresentativeoftheERPprevailingatanyotherhistoricaldate.TheERPremainsstableforafairlylongperiodunlessthereisadrasticchangeintheeconomicandmarketconditions.Hence,theconcludedERPcouldbeconsideredeffectivetillsuchtimethecurrentanalysisisupdatedinthefutureorthereisasignificantchangeintheeconomicandmarketconditions.

Thedocumentisforinformationpurposeonly.Theanalysisisbasedongenerallyacceptedmethodologies,informationavailableinthepublicdomainaswellasinformationsourcedfrominternationaldatabases.Theinformationcontainedinthisdocumentispublishedfortheassistanceoftherecipientbutisnottoberelieduponasauthoritativeortakeninsubstitutionfortheexerciseofjudgementbyanyrecipient.

Thisdocumentisnotintendedtobeasubstituteforprofessional,technicalorlegaladvice.Wehavenoobligationtoupdatethisreport.Allopinionsexpressedinthisdocumentaresubjecttochangewithoutnotice.Whileduecarehasbeentakeninthepreparationofthisdocumentandinformationcontainedherein,GrantThorntondoesnotacceptanyliabilitywhatsoeverforanydirectorconsequentiallosshowsoeverarisingfromanyuseofthisdocumentoritscontentsorotherwisearisinginconnectionherewith.

ValuationInsights03

Foreword

Akeychallengeoftenfacedbyinvestors,advisersandcorporatefinanceprofessionalsistoquantifytheadditionalpremiumoropportunitycostthatshouldbedemandedforholdingtheequityassetclass.Giventhesubjectivityinvolvedinestimatingsuchapremium,thequestionspillsovertotheunderlyingassumptionsoftheapproachtobeused,timeperiodconsidered,marketdefinition,etc.Thisriskpremiumneedstobereassessedperiodicallyinlinewithfluctuationsinthestockmarketperformanceandforecastofeconomictrendsofthecountry.

Wearepleasedtosharewithyouourresearchontheequityriskpremium(ERP)inIndia.Inthesecondeditionofourpublicationonthistopic,wehaveanalysedtheERPforIndiafromtwoperspectives:HistoricalandForward-Looking(asofacut-offdateof31December2018).

HistoricalanalysisindicatesthattheIndianstockmarketgaveanaverageannualisedreturnof16.70%during2001-18fordifferentinvestmenthorizons,implyinganexcessreturnof8.86%overtherisk-freerate.Wefurtheradjustedthisexcessreturnforthereturngeneratedduetoexpansioninthevaluationmultiples(consideringthatthevaluationmultiplescannotkeeponexpandinginperpetuityforadeveloped/efficientequitymarket).

Onaforward-lookingbasis,weestimatedthereturnexpectationpricedinthecurrentmarketindex.Thiswasestimatedastheratewhichwhenusedtodiscountthefuture

expectedcashflows(basedonconsensusforecasts)fromconstituentcompaniesoftheNiftyindex,resultsinapresentvalueofthesecashflowswhichisequaltothemarketcapoftheNiftyindex.ThisanalysisindicatesthatdespitetheNiftyindextradingatanearall-timehighPEmultiple,theexpectedhealthygrowthinfutureearnings/cashflowsstillimpliesanexpectedreturnof15.17%witharisk-freerateof7.50%.

WhilethetwoanalysesprovidetwodifferentestimatesofERP,eachapproachhascertaininherentprosandcons.Hence,anaverageofthetwoestimates(rounded),ie6.75%,hasbeenconsideredasrepresentativeofthecurrentERPforIndia.

WehopetheERPestimatewillbeausefulinputforvaluationprofessionals,corporatesandinvestorsintheirvaluationanalysis.

Manish SaxenaPartnerGrant Thornton India LLP

Darshana KadakiaPartnerGrant Thornton India LLP

Wearepleasedtosharewithyouourresearchontheequityriskpremium(ERP)inIndia.Inthesecondeditionofourpublicationonthistopic,wehaveanalysedtheERPforIndiafromtwoperspectives:HistoricalandForward-Looking(asofacut-offdateof31December2018).

04ValuationInsights

Executive summary

Equityriskpremium(ERP)istheexcessreturnoverandabovethereturnonarisk-freeassetwhichaninvestordemandsforinvestingintheequityassetclass.ThesignificanceofERPintheworldofinvestingandpolicydecisionmakingcannotbeemphasisedenough.

WhilevarioustechniqueshaveevolvedovertimetoestimatetheERPinagivenmarket,wehaveusedtwoofthemostcommonlyandinternationallyacceptedapproaches,ieHistoricalEstimateApproachandImpliedEstimate(Forward-LookingEstimate)ApproachtoestimatetheERPfortheequitymarketsintheIndianeconomy.Ourfindingsareasfollows:

HistoricalApproach 5.68%

Forward-LookingApproach 7.67%

Equityriskpremium(rounded) 6.75%

ValuationInsights05

Equityriskpremium(ERP)isakeycomponentoftheoverallrequiredrateofreturnforequityinvestments.Equitiesareoneofthemostwidelyusedassetclassesforinvestmentpurposesforbothshortandlong-termperiods.Giventheriskinherentinequitiesstemmingfromthenatureoftheassetclassanduncertaintyoffutureexpectedcashflowsvis-à-visarisk-freeasset,investorsdemandanadditionalreturnforholdingequities.Simplyput:

ERP is the additional return that investors desire for holding investments in equities instead of a risk-free asset.

Sincetherequired/expectedrateofreturnthatarationalinvestorshoulddemandastheopportunitycostofinvestinginequitiesisseldomvisibleoridentifiablethroughproxyinstrumentstradedinthemarket,ERPbecomesanimportantelementindeterminingthisrequiredrateofreturn,whichplaysacrucialroleforaninvestortodeterminetherisk-returntrade-offforanyinvestment.

ThefollowingisabriefsummaryofthekeyareasofinvestmentandpolicydecisionmakingthatstrengthenthesignificanceofERP:

Significance of ERPAsdiscussedabove,opportunitycostiskeytoinvestmentdecision-makingforanyinvestor.TheCapitalAssetPricingModel(CAPM)isoneofthemostwidelyusedtoolsfordeterminingthisrequiredrateofreturnthattheinvestorshouldearnonequityinvestmentsandthatshouldholdinequilibriumintheequitymarket.Themodelprovidesarelativelyobjectiveapproachtowardsdeterminingtherequiredrateofreturn,andisgroundedinthesimplisticchiefassumptionthattheriskofanassetisdeterminedbasedontheasset’scontributiontosystematicriskoverandabovetherisk-freerate.

Background and context

Required rate of return = Risk free rate + ß (Equity risk premium)

Therefore,giventhewidespreadacceptanceanduseoftheCAPMworldwide,estimatingtheERPbecomescrucialtothedecision-makingprocess.

ERPplaysasignificantroleinthefollowingkeyareasofinvestmentandpolicydecisions:• Intheworldofcorporatefinance,ERPisimportantwhile

determiningthecostofequityandcostofcapitalforfirmsfortheirinternaldecision-makingprocesstooptimisethedebt-to-equityratiosanddecidinguponinvestments,buy-backandpolicies,etc.

• Inareasofvaluationsandcapitalbudgeting,itisusedtoarriveatthefairvalueofequityinvestmentsornetpresentvaluesforprojectsservingasaproxyforthediscountratetodeterminethepresentvalueofexpectedfuturecashflows.

• ERPisalsousedasagaugeofmarketsentimentfortheequitymarketsasitprovidesdirectiontowardsinvestorconfidenceasaproxyfortheopportunitycostofinvesting.

• Itisoftenusedasacheckintheindividualsavingversusinvestmentdecision-makingprocesswhileputtingasideanamountforfutureconsumptionpurposessuchasretirementorhealthcareneeds,aswellasallocationofwealthtodifferentassetclasses.

06ValuationInsights

Asdiscussedintheprevioussections,owingtotheimportanceandwidespreaduseofERP,theapproachandmethodologyfollowedtoestimateERPiscritical.Evenforlong-establishedanddevelopedequitymarkets,estimatingthemagnitudeofERPischallengingandcouldbeareasonforalteringinvestmentdecisions.

Broadly,threeapproachesexistforestimatingERP:• HistoricalEstimate• Forward-LookingEstimate• Survey-BasedEstimate

Forthepurposesofouranalysis,wehaveconsideredtheHistoricalEstimateandForward-Lookingapproaches.Underboththeapproaches,wehaveconsideredacut-offfortheestimatedateof31December2018forallmarketinputs.

Historical EstimateERPunderthisapproachisestimatedasanaverageofexcessreturnscalculatedasthedifferencebetweenthetotalreturnforanequitymarketandthereturnontherisk-freeassetsofvariousinvestmenthorizons.Thisapproachisoftenconsideredasareliablechoiceofestimation,asitisbasedontheassumptionsofhomogeneousmarketsandmarketefficiencyoveralongperiod.Averagereturnsintheequitymarketprovideasaproxyforunbiasedestimateofinvestors’expectations.

Input estimatesWhileestimatingtheERPusingthisapproach,selectionofthefollowinginputsisimportant:

• Market portfolioThemarketportfoliousedtoestimatethereturninequitymarketsisoftenbasedonabroad-basedequitymarketindexwhichservesasaproxyofthecountry’sequitymarketandisreflectiveoftheeconomicconditionsofthecountry.

WehaveusedtheTotalReturnNifty50indexastherepresentativeoftheequitymarketinIndia,basedonthefollowingfactors:

– Theindexrepresentsandisreflectiveoftheeconomicconditionsofthecountry.

– Thetotalvolumestradedontheindexreflectasignificantportionoftheliquidityintheequitymarketofthecountry.

Approach and methodology

– TheindexwaslaunchedinApril1996andhasasufficienttradinghistorytocarryouttheestimationofERPwithoutcompromisingonthetimeperiodrequiredfortheestimate.

– Thecomponentsoftheindexconstituteabroadmixofindustriesandsectorsinthecountry.

ThefollowingtableisabriefsnapshotofthecharacteristicsofNifty50:

Table 1: Sector representation of Nifty 50

Sector Weight (%)

Financialservices 37.18%

Energy 15.44%

Informationtechnology 14.82%

Consumergoods 10.80%

Automobile 6.59%

Metals 3.81%

Construction 3.69%

Pharmaceuticals 2.53%

Cementandcementproducts 1.63%

Telecommunications 1.55%

Fertilisersandpesticides 0.75%

Mediaandentertainment 0.60%

Services 0.59%

Source:NationalStockExchangeofIndia

ValuationInsights07

Closing prices of Total Return Nifty 50 Index (June 2001 to December 2018)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jun-

01Ju

n-02

Jun-

03Ju

n-04

Jun-

05Ju

n-06

Jun-

07Ju

n-08

Jun-

09Ju

n-10

Jun-

11Ju

n-12

Jun-

13Ju

n-14

Jun-

15Ju

n-16

Jun-

17Ju

n-18

Risk-free rate of returnThechoicetobemadefortherisk-freerateisoftenthetenureoftheratetobeconsidered.Inthespecificcaseofanupward-slopingyieldcurve,wheretheyieldsonlongertermbondsarelargerthantheyieldsonshortertermbonds,whichisalsowitnessedinIndia,therisk-freeratebasedonlongertenuresispreferredovershortertermsforthefollowingreasons:

• Long-termyieldsarelesssusceptible/sensitivetounexpectedinflationshocks.

• BasedontheusesofERPasmentionedpreviously,themostcommonofthembeingforthedeterminationofthecostofequityunderCAPM,long-termrisk-freerateisalsosynonymouswithinvestorexpectationsoflong-termreturns.

Wehaveusedthe10-yearrisk-freerateaspublishedbyClearingCorporationofIndiaLimited(CCIL).Therisk-freeratepublishedbyCCILisbasedontheNelson-Siegel-Svenssonmodel.

Time periodForthechoiceoftimeperiodforthesampleconsideredtoestimatetheERP,wehaveconsideredthelongesttenureavailablebasedontheavailabilityofdatatoincreasetheprecisionofourestimation.Sincetherisk-freeratepublishedbyCCILwasavailablefromJune2001,wehaveconsideredtheperiodfromJune2001toDecember2018.

Duringthistimeperiod,wehaveconsideredvariousinvestmenthorizons,withtheshortestinvestmenthorizonofoneyear,andthenestimatedtheERPfortheseinvestmenthorizons.

10-year zero coupon yield (June 2001 to December 2018)

Jun-

01Ju

n-02

Jun-

03Ju

n-04

Jun-

05Ju

n-06

Jun-

07Ju

n-08

Jun-

09Ju

n-10

Jun-

11Ju

n-12

Jun-

13Ju

n-14

Jun-

15Ju

n-16

Jun-

17Ju

n-18

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Types of meanThechoiceofmeanusedtoestimatetheriskpremiumhasanimportantimpactontheestimate,andthechoiceremainsbetweenarithmeticandgeometricmean.WehaveusedthearithmeticmeantoestimatetheERPoveralltheinvestmenthorizonsasitbestrepresentssingle-periodholdingreturns,whicharesynchronoustothechoiceofmodel,theERPisusedwith,iemostofthemajorfinancemodelsincludingCAPMandothermulti-factormodelsaresingle-periodreturnmodels.

MethodologyToestimatetheERPundertheHistoricalEstimateapproach,wefollowedthefollowingmethodology:

WeestimatedthecompoundedannualisedgrowthintheTotalReturnNifty50Indexpricesandbondpricesbasedonthe10-yearzerocouponyieldsforvariousinvestmenthorizonsas:

Return=Index closing at n2

Index closing at n1( (365

(n2 - n1)

Wethenestimatedtheexcessreturnas:

Excess return = Return on TR Nifty 50 - Return on bond prices

Thereafter,weincorporatedaforward-lookingassumptionintheanalysisbyeliminatingthesupply-sidecomponent.Thesupply-sideadjustmenttakesintoaccounttheearningsthatcompaniesgenerate(supply).Itisestimatedbyremovingthe

08ValuationInsights

growthintheprice-to-earningsratiofromtheexcessreturnasestimatedabove.

Theunderlyingargumentformakingtheaboveadjustmentisthatforamaturedeconomy,long-termgrowthintheprice-to-earningsratioisnotexpectedtoimproveinperpetuity;

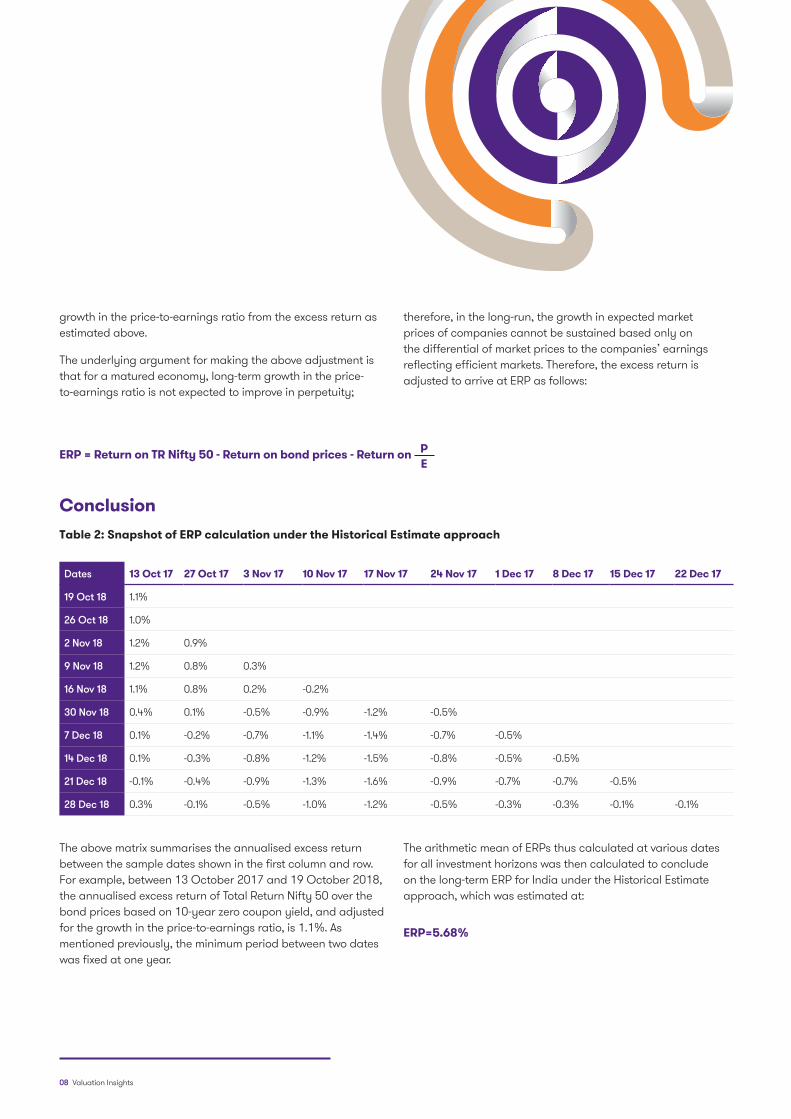

Theabovematrixsummarisestheannualisedexcessreturnbetweenthesampledatesshowninthefirstcolumnandrow.Forexample,between13October2017and19October2018,theannualisedexcessreturnofTotalReturnNifty50overthebondpricesbasedon10-yearzerocouponyield,andadjustedforthegrowthintheprice-to-earningsratio,is1.1%.Asmentionedpreviously,theminimumperiodbetweentwodateswasfixedatoneyear.

ConclusionTable 2: Snapshot of ERP calculation under the Historical Estimate approach

Dates 13 Oct 17 27 Oct 17 3 Nov 17 10 Nov 17 17 Nov 17 24 Nov 17 1 Dec 17 8 Dec 17 15 Dec 17 22 Dec 17

19 Oct 18 1.1%

26 Oct 18 1.0%

2 Nov 18 1.2% 0.9%

9 Nov 18 1.2% 0.8% 0.3%

16 Nov 18 1.1% 0.8% 0.2% -0.2%

30 Nov 18 0.4% 0.1% -0.5% -0.9% -1.2% -0.5%

7 Dec 18 0.1% -0.2% -0.7% -1.1% -1.4% -0.7% -0.5%

14 Dec 18 0.1% -0.3% -0.8% -1.2% -1.5% -0.8% -0.5% -0.5%

21 Dec 18 -0.1% -0.4% -0.9% -1.3% -1.6% -0.9% -0.7% -0.7% -0.5%

28 Dec 18 0.3% -0.1% -0.5% -1.0% -1.2% -0.5% -0.3% -0.3% -0.1% -0.1%

ThearithmeticmeanofERPsthuscalculatedatvariousdatesforallinvestmenthorizonswasthencalculatedtoconcludeonthelong-termERPforIndiaundertheHistoricalEstimateapproach,whichwasestimatedat:

therefore,inthelong-run,thegrowthinexpectedmarketpricesofcompaniescannotbesustainedbasedonlyonthedifferentialofmarketpricestothecompanies’earningsreflectingefficientmarkets.Therefore,theexcessreturnisadjustedtoarriveatERPasfollows:

ERP = Return on TR Nifty 50 - Return on bond prices - Return on PE

ERP=5.68%

ValuationInsights09

Forward-Looking EstimateForward-lookingestimatestocalculatetheimpliedERPprevalentintheeconomy,indirectlycapturedinthecurrentmarketvalueoftheequitymarket,isanotherimportantapproachtoestimatetheERP.TheimportanceofthisapproachstemsfromthefactthatERPtoalargeextentisbasedoninvestorexpectationsofeconomicandfinancialmetricsgoingforward.Theseestimatesarelesssubjectivetoissuesofnon-stationarityanddatabiasesascomparedtohistoricalestimates,andthereforehistoricalestimatesandforward-lookingestimatesareoftenusedinconjunction.

Theapproachofforward-lookingestimatestoarriveattheERPisgroundedintherealitythatthetotalvalueoftheequitymarketasrepresentedbyabroadequityindex,reflectedinitsmarketcapitalisation,isthepresentvalueofallthefuturecashflowsexpectedtobeearnedintheequitymarketwhichareinturnrepresentedbytheexpectedfuturecashflowsoftheconstituentsoftheequityindex.

Thediscountratewhichequatesthepresentvalueofexpectedfuturecashflowstothetotalmarketcapitalisationofalltheconstituentsoftheindexrepresentsthetotalmarketreturnexpectationbyinvestorsintheequitymarket.Thereafter,ERPisestimatedasthedifferencebetweenthetotalmarketreturnandtherisk-freerate.

ERP = Market return - Risk free rate

MethodologyUnderthisapproach,weconsideredthefollowingmethodologytoestimatetheERP:

• WeusedtheFreeCashFlowstoEquity(FCFE)approachtoestimatetheexpectedfuturecashflowsforeachoftheconstituentsoftheNifty50Index.

FCFE = Cash flows from operations-Interest expense-Capital expenditure + Increase (Decrease) in net borrowings

• Weconsideredamulti-stagegrowthmodeltoestimatetheexpectedfuturecashflowsforeachoftheconstituentsofNifty50fromFY2019throughFY2028,andthereafterconsideredaterminalperiodwhichrepresentstheexpectedfreecashflowsinperpetuity.

– ToestimatetheFCFEfortheperiodFY2019throughFY2021,wereliedonconsensusanalystestimatesforeachcomponentofFCFE.

– Thereafter,futurefreecashflowsfromtheperiodFY2022toFY2028wereextrapolatedtoreachanormalisedgrowthrateof7.50%intheterminalperiod,whichisbasedon10-yearzerocouponyieldasof31December2018aspublishedbyCCIL.

• TheFCFEfortheindexwasthencalculatedbyweighingtheFCFEsofeachoftheindexconstituentsbytheweightsofeachconstituentintheindexasof31December2018.

• TheFCFEfortheterminalperiodwasthencapitalisedusingtheGordonGrowthModeltoarriveattheterminalvalueasof31March2028.Thepresentvalueunderthismodelisestimatedas:

Terminal value=(Market return-g)

(FCFE(n-1) )*(1+g)

where

(n-1) is the period ending 31 March 2028

g is the long-term sustainable growth rate of 7.5%

(based on 10-year zero coupon yield as of 31 December 2018 as published by CCIL)

• Basedontheabove-estimatedcashflows,weestimatedtheimpliedmarketreturn,whichequatesthepresentvaluesofsuchcashflowstotheadjustedmarketcapitalisationoftheindex,asfollows:

Market capitalisation of Nifty 50

Present value of terminal value

= +(1+Market return)n

∑FCFEn

where

Market capitalisation of Nifty 50 as of 31 December 2018 was adjusted for non-operating assets such as cash and cash equivalents, long-term investments, etc.

10ValuationInsights

ConclusionBasedontheaboveestimates,wearrivedatamarketreturnof15.17%,whichwasthenusedtoarriveattheimpliedERPunderCAPMasfollows:

ERP=Beta

Market return - Risk free rate

Therisk-freerateconsideredasof31December2018was7.50%,whichisbasedonthe10-yearzerocouponyieldaspublishedbyCCIL.Abetaof1.0xforthemarketportfoliowasthenconsideredtoconcludeonthelong-termERPforIndiaundertheForward-Lookingapproach,whichwasestimatedas:

ERP=7.67%

PleasenotethattheERPasestimatedundertheForwardEstimateApproachisbasedontherisk-freerateprevailingasoftheestimateddateof31December2018.Whileaminorchangeintherisk-freerateshouldnotimpactthefundamentalexpectationasarrivedatunderthisapproach,anysignificantchangeintherisk-freeratemayleadtoamaterialchangeintheERPexpectation,andtherebyrequirere-estimation.

Conclusion – ERPBasedonthearithmeticmeanofERPsestimatedunderboththeapproachesasdescribedabove,webelievethatanERP (rounded) of 6.75%canbeconsideredasareasonablepremiumforinvestingintheequitymarketsintheIndianeconomy.

ValuationInsights11

• ClearingCorporationofIndiaLimited

• ThomsonReutersDatabase

• CapitalIQDatabase

• NationalStockExchangeofIndia

Acknowledgements

Sources

Editorial review Design

TanmayMathur GurpreetSingh

Authors

ManishSaxena

AmitBora

PriyankaJain

PranjalKapoor

VibhorSinghal

For media queries, please contact:

Spriha Jayati E:[email protected]:+919323744249

12ValuationInsights

Contact us

For more information or for any queries, write to us at [email protected]

To know more, please visit www.grantthornton.in or contact any of our offices as mentioned below:

Follow us @GrantThorntonIN

©2019GrantThorntonIndiaLLP.Allrightsreserved.

“GrantThorntoninIndia”meansGrantThorntonIndiaLLP,amemberfirmwithinGrantThorntonInternationalLtd,andthoselegalentitieswhichareitsrelatedpartiesasdefinedbytheCompaniesAct,2013.

GrantThorntonIndiaLLPisregisteredwithlimitedliabilitywithidentitynumberAAA-7677andhasitsregisteredofficeatL-41ConnaughtCircus,NewDelhi,110001.

ReferencestoGrantThorntonaretoGrantThorntonInternationalLtd(GrantThorntonInternational)oritsmemberfirms.GrantThorntonInternationalandthememberfirmsarenotaworldwidepartnership.Servicesaredeliveredindependentlybythememberfirms.

NEW DELHINationalOfficeOuterCircleL41ConnaughtCircusNewDelhi110001T+911142787070

NEW DELHI6thfloorWorldmark2AerocityNewDelhi110037T+911149527400

AHMEDABAD7thFloor,HeritageChambers,Nr.AzadSociety,NehruNagar,Ahmedabad-380015

BENGALURU5thFloor,65/2,BlockA,BagmaneTridib,BagmaneTechPark,CVRamanNagar,Bengaluru-560093T+918042430700

CHANDIGARHB-406A,4thFloorL&TElanteOfficeBuildingIndustrialAreaPhaseIChandigarh160002T+911724338000

CHENNAI7thFloor,PrestigePolygon471,AnnaSalai,TeynampetChennai-600018T+914442940000

DEHRADUNSuiteno.2211,2ndfloorBuilding2000,MichiganAvenue,DoonExpressBusinessParkSubhashNagar,Dehradun-248002T+911352646500

GURGAON21stFloor,DLFSquareJacarandaMargDLFPhaseIIGurgaon122002T+911244628000

HYDERABAD7thFloor,BlockIIIWhiteHouseKundanBagh,BegumpetHyderabad500016T+914066308200

KOCHI6thFloor,ModayilCentrepointWarriamroadjunctionM.G.RoadKochi682016T+914844064541

KOLKATA10CHungerfordStreet5thFloorKolkata700017T+913340508000

MUMBAI16thFloor,TowerIIIndiabullsFinanceCentreSBMarg,Elphinstone(W)Mumbai400013T+912266262600

MUMBAI9thFloor,ClassicPentagonNrBislerifactory,WesternExpressHighway,Andheri(E)Mumbai400099T+912261767800

NOIDAPlotNo.19A,7thFloorSector–16ANoida201301T+911204855900

PUNE3rdFloor,UnitNo309to312WestWing,NyatiUnitreeNagarRoad,YerwadaPune-411006T+912067448800