RIZVI INSTITE OF MANAGEMENT STUDIES & RESEARCH COMPANY: AMARA RAJA BATTERIES SUBMITED TO: Prof. SANJEEV PATKAR SUBMITED BY NAME: ABBAS BADAMI ROLL NO.: 7 CLASS: MMS-A (FINANCE) SEMESTER: IV BATCH: 2011-2013

Transcript

RIZVI INSTITE OF MANAGEMENT STUDIES & RESEARCH

COMPANY: AMARA RAJA BATTERIES

SUBMITED TO: Prof. SANJEEV PATKAR

SUBMITED BY

NAME: ABBAS BADAMI

ROLL NO.: 7

CLASS: MMS-A (FINANCE)

SEMESTER: IV

BATCH: 2011-2013

Table of Contents

Q1. 5 years Balance Sheet & Profit & Loss Account with 2years Forecasted ................... 1

Q2. Business Model & Cost Sheet as defined by Goldratt ................................................... 6

Substituting the values as below in the above equation,

Capital at Start 929.51

ROC 35.23%

Growth* 22.00%

Cost of Capital 10.00%

Value of the firm = Rs. 1,954.30 Cr .We find that an investor can pay a maximum of 6.8 times the EPV value. Hence we would be willing to pay a maximum of Rs. 321.53 Cr x 6 =

Rs. 1,954.30 Cr. At current stock price of Rs. 298, the company is trading at Rs. 929.51 Cr. Hence there is sufficient Margin of safety available to the investor at present level.

Intrinsic Value as per Dividend Discount Formula

The Company has on an average paid Rs. 216.03 Cr as dividend per year for the past 5 years.

As can be seen under a range of figures, the higher end of valuation is reached at Rs 929.51

Cr. Hence the fair price per share is Rs. 298/-

Value ofbusiness (Rs Cr)

Shareprice (Rs)

Current 929.51 298

Fair Valuation 1954.3 302

*assumed

18 | P a g e

FCFF

FCFF is a metric used to determine a firm's financial health and profitability by

measuring how much cash is available for all claim holders in the firm (debt holders and

share holders) after all taxes and needs for reinvestment have been met.

The formula of FCFF is given by:

FCFF = EBIT (1 - tax rate) - Capex + Depreciation - Change in non-cash working capital

Or FCFF= NOPAT - Net Investments

NOPAT = EBIT (1-t)

Net Investments = (fixed asset +current asset of current year) – (fixed asset + current asset of

previous year)

This model assumes that there is no interest expense or tax benefit from that interest expense.

Positive FCFF implies that there is sufficient cash to either service debt (through interest

payments or principal repayments) and / or service the equity holders (through dividends or

share repurchases). On the other hand, negative FCFF means that the firm has not generated

sufficient revenue to cover its costs and will have to raise more cash, either through issuing

more debt or selling more equity.

FCFE

FCFE is a measure used to determine how much cash is available to pay to a company's

equity shareholders after accounting for all expenses, reinvestment, and debt repayment.

FCFE is commonly used to gauge the health of companies. Positive FCFE indicates what can

be paid out to equity holders (as a dividend or repurchased stock) without harming the firm's

operations or growth opportunities while negative FCFE, it implies that the firm must issue

new equity to raise cash. The formula is given by:

FCFE = Net Income - Net - Change in Net Working Capital + New Debt - Debt Repayment.

Or FCFE = FCF – Non operating income.

19 | P a g e

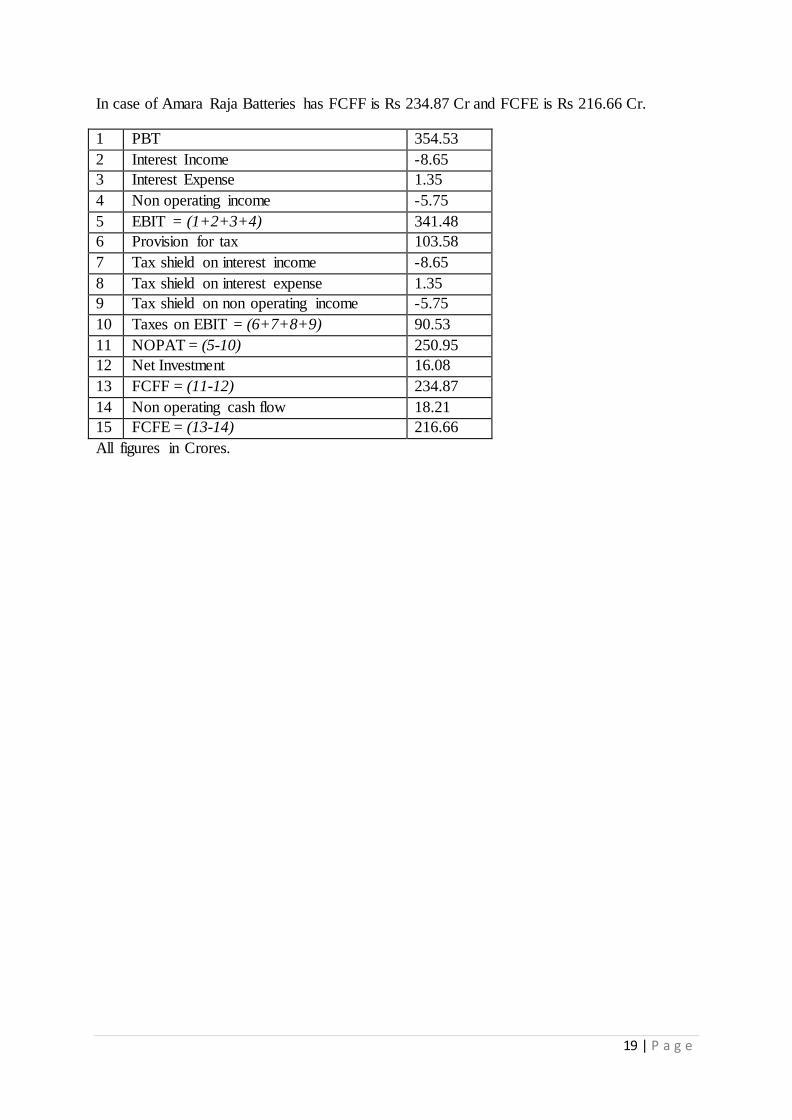

In case of Amara Raja Batteries has FCFF is Rs 234.87 Cr and FCFE is Rs 216.66 Cr.

1 PBT 354.53

2 Interest Income -8.65

3 Interest Expense 1.35

4 Non operating income -5.75

5 EBIT = (1+2+3+4) 341.48

6 Provision for tax 103.58

7 Tax shield on interest income -8.65

8 Tax shield on interest expense 1.35

9 Tax shield on non operating income -5.75

10 Taxes on EBIT = (6+7+8+9) 90.53

11 NOPAT = (5-10) 250.95

12 Net Investment 16.08

13 FCFF = (11-12) 234.87

14 Non operating cash flow 18.21

15 FCFE = (13-14) 216.66

All figures in Crores.

20 | P a g e

9) Morning Star Model – Business Moat

Moats are important to investors because any time a company develops a useful

product or service. It isn't long before other firms try to capitalize on that opportunity by

producing a similar--if not better--product. Basic economic theory says that in a perfectly

competitive market, rivals will eventually eat up any excess profits earned by a successful

business. In other words, competition makes it difficult for most firms to generate strong

growth and margins over an extended period of time. Amara Raja Batteries falls into the

network effect.

The Network Effect: The network effect occurs when the value of a particular good or

service increases for both new and existing users as more people use that good or service. It

can also occur when other firms design products that compliment an existing product, thereby

enhancing that product's value. For example, the fact that there are literally millions of people

using eBay (EBAY) is the thing that both makes eBay's service incredibly valuable and

makes it all but impossible for another company to duplicate its service. The moat is a wide

moat according to me

The “distributor” status doesn’t restrict Amara Raja Batteies by being a mere member

of the channel, value addition is provided at every step of the process elevating Amara Raja

Batteires from being a distributor to a marketing partner. Amara Raja batteries does not

distribute it contributes. Amara raja batteries has dedicated business and sales teams for

developing the business for every brand it distributes and these professionals act as an

extension of business development team of the vendors.

Amara Raja Batteies have end to end supply chain capabilities starting from import,

warehousing, and stock movement across geographies to packing / repacking, order

processing and delivery to the parts of the world where we operate, together with Amara Raja

Batteies door delivery infrastructure. Amara Raja Batteies also provide our customers with

project based delivery services which require a highly coordinated activity of delivery of

multiple products to multiple locations and in some cases installing them as well. The wide

spectrum of products offered from multiple vendors helps Amara Raja Batteies to provide the

customers a single sourcing point.

Amara Raja Batteies provides differentiated value offerings up and down the supply

chain, in some or the other touching everyone in the chain from the vendor to the end

customer. Customer does not mean only to whom Amara Raja Batteies sells its products but

also at time vendors who sells their products to Amara Raja Batteies also become customer of

it as they do purchase from Amara Raja Batteies.

Hence, it would be difficult for the competitor’s to imitate the wide and diversified

although related service, which benefits the users.

21 | P a g e

10) CANSLIM Investment strategy

The stock market can make or break dreams in a single afternoon. As with any

investment, the stock market carries with it a certain degree of risk, regardless of which stock

strategy investors choose. Equally true is the fact that some stock strategies are superior and

safer than others. Originally developed by William O'Neil, the CANSLIM stock strategy

employs a prudent analysis of earnings and other financial information while also assessing

the relative strength of the company and its potential for future growth in earnings. In other

words, the CANSLIM strategy looks at both tangible and intangible items when screening

potential stock purchases.

C=Current Earnings

Earnings may not be the only important indicator of the current strength of a company

but they certainly provide useful information to help in the decision-making process. The

CANSLIM stock strategy requires a careful analysis of the most recent earnings per share

(EPS) reported by the company. Earning should rise at least 20% over previous financial

year. In case of Amara raja batteries India EPS in Mar '12 is 25.18 and Mar '11 was 17.34.

However, it has increased but not by 20%.

A=Annual Earnings

Although current earnings will tell investors where the company currently stands, annual

earnings tend to paint a more complete financial picture. CANSLIM stock strategists will

look back 4-5 years to see if annual earnings have been increasing at a healthy rate. Most

investors using CANSLIM tend to prefer companies with annual earnings increases in the 25-

50% range. If the earnings increases are strong and better than the rest of the competition,

then the company is in a good position to have a strong period of growth, and therefore, be a

sound investment. Amara Raja Batteies, we can see earnings are rising and so stock price, as

compared to peers too Amara Raja Batteies is better off.

Mar 2012 Mar 2011 Mar 2010 Mar 2009 Mar 2008

Net Profit 94.36 110.16 95.66 149.01 216.03

N=New

Companies, much like people, can get stuck in a rut. Without innovation, a company will

eventually die. But before it does, it will see its stock prices plummet, and take any investor

still clinging to it down. “NEW” in this case refers to new products or strategy to tap the un

tap market, hence Amara Raja Batteries scores well as they tap the un tap market like

AFRICA and keeps on adding new product to distribute to its customers.

S=Supply/Demand

Actually, it might make more sense for the "S" to stand for size as the CANSLIM stock

strategy assumes that it is easier for smaller companies to have significant growth spurts than

22 | P a g e

larger ones. Amara Raja Batteries has grown huge in last 2 decades and hence it is difficult to

have the same percentage of growth as compared to its peers in small cap as they have a

small base to compare with, hence, growth of Amara Raja Batteries is good.

L=Leader or Loser

Investors in the stock market must be able to discern the market leaders from those pulling up

the rear. Companies that manage to continually lead their industry typically have great

returns, and are fundamentally sound. Investors can identify leaders from losers by looking at

the Relative Price Strength (RPS). The relative price strength looks at companies over a given

period of time and then ranks them from 1-99. A business with an RPS of 75 indicates that

the stock of this company has outperformed 75% of the stocks in the market group. However,

CANSLIM stock strategy does not recommend companies with an RPS of less than 70.

Amara Raja Batteries has the considerable market share; hence it cannot be said as a market

leader based on marcap.

I=Institutional Sponsor

Every growing business needs the sponsorship of institutional investors in order to be taken

seriously as a sound investment opportunity. However, too many institutional investors can

be a problem as well. When this happens, the stock can potentially become more volatile in

the event of a natural disaster or crisis, because institutional investors are apt to sell off. Since

such investors tend to buy large chunks of stock at a time, too many sell-offs could send stock

prices crashing. Therefore, CANSLIM stock strategy includes staying away from any

company with more than 10 institutional investors. Amara Raja Batteries has more than 10

institutional investors hence fails in this criteria in form of MF’s, financial institution and

FII’s

M=Market Direction

For instance, investors who buy in just before a bear market emerges can literally be wiped

out if they are not careful. While the long-term prospects may be bright, short-term losses

will likely add up quickly. It may be years, if ever, before the stock prices recover to where

they were when the investment was initially made. At this point of time Indian stock markets

are really bullish on their view as it is growing and hence great chance to buy the stock as

number of FII entering markets are high as well as volumes are also on rise.

Hence, Amara Raja Batteries performs pretty well on most of the parameters of the

CANSLIM strategy of investing, Hence it would be a better deal to invest in stocks.

Truthfully, no stock investment strategy will guarantee a profit. Although the CANSLIM

stock strategy does require some personal judgment on the part of investors, it remains a

highly structured, well-researched, and proven system. And, while there may be no

guarantees, the CANSLIM stock strategy does remove the guesswork from choosing stock

investments to a certain extent, and provides investors with a solid foundation from which to