26

ERES Conference 2010 External shocks on property markets & implications for asset allocation Anthony De Francesco, IPD AUS/NZ Saturday 26 June 2010

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | rhoda-davis |

| View: | 214 times |

| Download: | 1 times |

ERES Conference 2010 External shocks on property markets & implications for asset allocationAnthony De Francesco, IPD AUS/NZSaturday 26 June 2010

© IPD 20102www.ipd.com/australia

Introduction

External shocks and property markets

Modelling approach and preliminary results

Implications for asset allocation

Summary remarks

Outline

© IPD 20103www.ipd.com/australia

Introduction

External shocks and property markets

Modelling approach and preliminary results

Implications for asset allocations

Summary remarks

Outline

© IPD 20104www.ipd.com/australia

Some dimensions to the GFC- a brief review of events

External shocks Need to identify and distinguish between structural and temporary shocks Transmission of shocks across markets and countries Non-linearity of shocks – how it impacts behaviour of markets from “normal” state

Capital markets and macroeconomy Access to capital restricted – the role of financial (banking) sector Pricing: an upward re-rating of risk across the complete asset space as well as across

property sectors

Property markets Performance impacted by fall-out in capital markets Performance impacted by spill-over into space markets

Asset allocation Standard SAA process frustrated with significant departure of asset performance from

historical averages Conventional models not robust to shocks

© IPD 20105www.ipd.com/australia

Objective of study

Gauge and assess the nature and influence of shocks on property markets Examine the nature of the shocks Explore the influence of shocks on the asset markets

Use econometric modelling to explore the interplay between shocks and asset markets Indentify key drivers on return performance Quantify relationships

Implications for asset allocation Consider other dimensions which makes the framework more robust

© IPD 20106www.ipd.com/australia

Introduction

External shocks and property markets

Modelling approach and preliminary results

Implications for asset allocations

Summary remarks

Outline

© IPD 20107www.ipd.com/australia

The influence of global shocks - understanding the transmission mechanism across markets

DIRECT PROPERTY

CAPITAL MARKETSFINANCIAL (BANKING)

SECTOR

MACROECONOMY

LABOUR MARKETS

EQUITY MARKETS

LISTED PROPERTY

DEBT MARKETS

Valuation multiplier

B/S impacts

Liquidity run

Leverage

Non-linear effects arise due to shocks between Balance Sheet (B/S) and real economy.

© IPD 20108www.ipd.com/australia

-10.0%

-7.5%

-5.0%

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

Mar-00 Sep-01 Mar-03 Sep-04 Mar-06 Sep-07 Mar-09

Economic activity for selected economiesannualised real GDP growth ending March 2010

Euro AUS UK JPN

US CHN NZ

Source: RBA and IPD Research.

The influence of global shocks - the interplay between various markets: display high correlations

25

50

75

100

125

150

175

200

225

250

Jan-05 Oct-05 Jul-06 Apr-07 Jan-08 Oct-08 Jul-09 Apr-10

Performance in selected listed share marketsprice indices (100=January 2005) ending May 2010

AUS S&P200NZ NZSE50US DJIAUK FTSE100SGP StraitsTimesJapan TOPIXHK Hang Seng

Source: RBA and IPD Research.

GFC (Global financial crisis)

SDC (Sovereign debt crisis)

-30%-25%-20%-15%-10%

-5%0%5%

10%15%20%25%30%35%40%

Dec 85 Dec 88 Dec 91 Dec 94 Dec 97 Dec 00 Dec 03 Dec 06 Dec 09

Property returns for selected global markets annual nominal total return on quarterly periods

JPN UK US AUS NZ

Source: IPD Research.

Binding leverage constraints impacts the financial transmission channels which results in high correlation among macroeconomic aggregates.

© IPD 20109www.ipd.com/australia

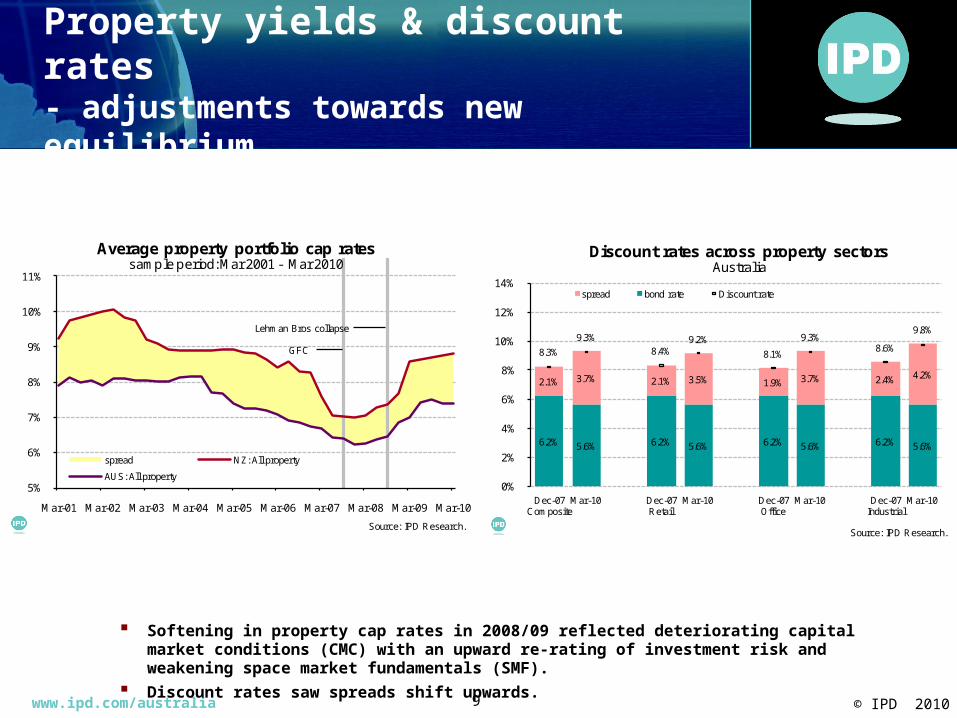

Softening in property cap rates in 2008/09 reflected deteriorating capital market conditions (CMC) with an upward re-rating of investment risk and weakening space market fundamentals (SMF).

Discount rates saw spreads shift upwards.

Property yields & discount rates- adjustments towards new equilibrium

5%

6%

7%

8%

9%

10%

11%

Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

Average property portfolio cap ratessample period: Mar 2001 - Mar 2010

spread NZ: All property

AUS: All property

Source: IPD Research.

GFC

Lehman Bros collapse

6.2% 5.6% 6.2% 5.6% 6.2% 5.6% 6.2% 5.6%

2.1% 3.7% 2.1% 3.5% 1.9% 3.7% 2.4% 4.2%

8.3%

9.3%

8.4%9.2%

8.1%

9.3%8.6%

9.8%

0%

2%

4%

6%

8%

10%

12%

14%

Dec-07Composite

Mar-10 Dec-07Retail

Mar-10 Dec-07Office

Mar-10 Dec-07Industrial

Mar-10

Discount rates across property sectorsAustralia

spread bond rate Discount rate

Source: IPD Research.

© IPD 201010www.ipd.com/australia

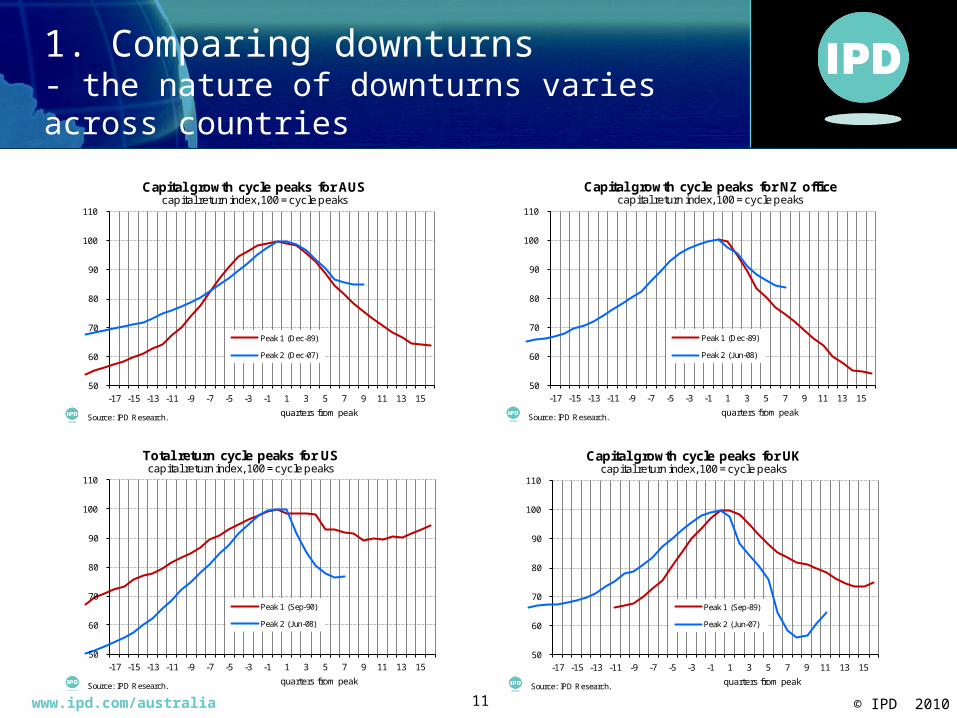

1. Comparing downturns - synchronised downturn with variation

A synchronised downturn was experienced in many property markets around the world due to common factor risks.

However, the nature of the downturns vary across country, reflecting country-specific risk.

-30%-25%-20%-15%-10%

-5%0%5%

10%15%20%25%30%35%40%

Dec 85 Dec 88 Dec 91 Dec 94 Dec 97 Dec 00 Dec 03 Dec 06 Dec 09

Property returns for selected global markets annual nominal total return on quarterly periods

JPN UK US AUS NZ

Source: IPD Research.

© IPD 201011www.ipd.com/australia

1. Comparing downturns- the nature of downturns varies across countries

50

60

70

80

90

100

110

-17 -15 -13 -11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15

quarters from peak

Capital growth cycle peaks for AUScapital return index, 100 = cycle peaks

Peak 1 (Dec-89)

Peak 2 (Dec-07)

Source: IPD Research.

50

60

70

80

90

100

110

-17 -15 -13 -11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15

quarters from peak

Capital growth cycle peaks for NZ officecapital return index, 100 = cycle peaks

Peak 1 (Dec-89)

Peak 2 (Jun-08)

Source: IPD Research.

50

60

70

80

90

100

110

-17 -15 -13 -11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15

quarters from peak

Total return cycle peaks for UScapital return index, 100 = cycle peaks

Peak 1 (Sep-90)

Peak 2 (Jun-08)

Source: IPD Research.

50

60

70

80

90

100

110

-17 -15 -13 -11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15

quarters from peak

Capital growth cycle peaks for UKcapital return index, 100 = cycle peaks

Peak 1 (Sep-89)

Peak 2 (Jun-07)

Source: IPD Research.

© IPD 201012www.ipd.com/australia

2. Synchronicity of property cycles- asymmetry between downturns and recovery

A synchronised downturn was experienced in many property markets around the world due to common factor risks.

However, the nature of the downturns vary across country, reflecting country-specific risk. Consider that Australia experienced a relatively sharp rise in capital return and now experiencing a relatively shallow downturn.

55

65

75

85

95

105

-15-14-13-12-11-10 -9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11

quarters from peak

Capital growth profiles for selected markets capital return index, 100=current cycle peak

CAN JPN UK

US AUS NZ

Source: IPD Research.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Dec 03 Dec 04 Dec 05 Dec 06 Dec 07 Dec 08 Dec 09

Capital growth cycles for selected markets annual nominal capital return on quarterly periods

CAN

JPN

UK

US

AUS

NZ

Source: IPD Research.Note: direct property returns based on global IPD indices.

© IPD 201013www.ipd.com/australia

3. Various “states” of return profile- stable versus unstable periods

Downturns linked to changing macroeconomic conditions.

Occur with significant departure of markets from fundamentals (associated with shocks).

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Mar-86 Nov-89 Jul-93 Mar-97 Nov-00 Jul-04 Mar-08

Direct property total returns annualised returns on quarterly rests using PCA/IPD Index

TotalRetailIndustrialOffice

Source: IPD Research.

recession: 1990/91 high interest rates deregulation of capital markets

GFC: 2007/08 low interest rates

excess capital

Pronounced cycles Period of stability Pronouncedcycles

© IPD 201014www.ipd.com/australia

Overview

External shocks and property markets

Modelling approach and preliminary results

Implications for asset allocations

Summary remarks

Outline

© IPD 201015www.ipd.com/australia

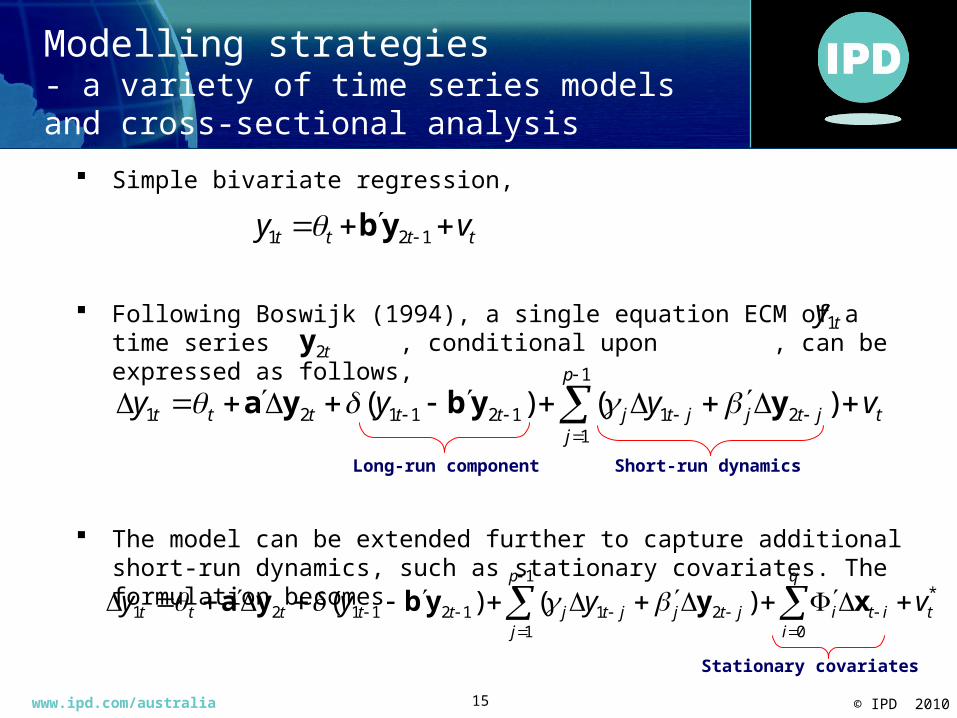

Simple bivariate regression,

Following Boswijk (1994), a single equation ECM of a time series , conditional upon , can be expressed as follows,

The model can be extended further to capture additional short-run dynamics, such as stationary covariates. The formulation becomes

t

p

jjtjjtjttttt vyyy

1

121121121 )()( yybya

*

0

1

121121121 )()( tit

q

ii

p

jjtjjtjttttt vyyy

xyybya

t2yty1

Long-run component Short-run dynamics

Stationary covariates

tttt vy 121 yb

Modelling strategies- a variety of time series models and cross-sectional analysis

© IPD 201016www.ipd.com/australia

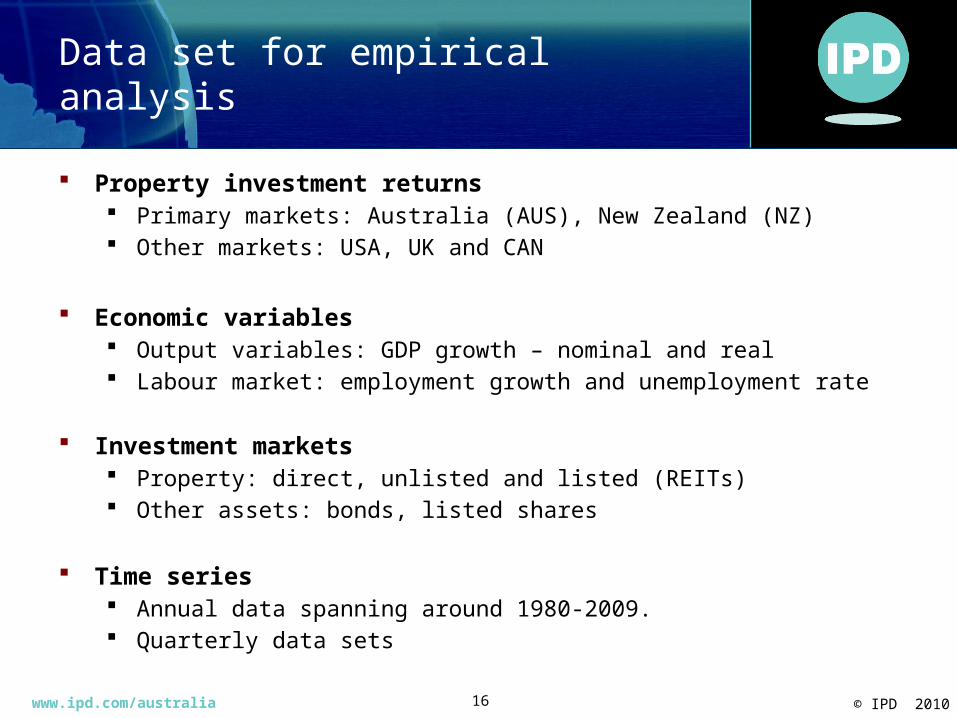

Data set for empirical analysis

Property investment returns Primary markets: Australia (AUS), New Zealand (NZ) Other markets: USA, UK and CAN

Economic variables Output variables: GDP growth – nominal and real Labour market: employment growth and unemployment rate

Investment markets

Property: direct, unlisted and listed (REITs) Other assets: bonds, listed shares

Time series Annual data spanning around 1980-2009. Quarterly data sets

© IPD 201017www.ipd.com/australia

Macro-property investment - the interplay between labour markets and real economy driving return

There is a strong link between the real economy, labour markets and property markets.

Correlation between nominal GDP growth and property returns: 0.81.

Correlation between employment growth and real property return: 0.74.

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Dec-85 Jan-89 Feb-92 Mar-95 Apr-98 May-01 Jun-04 Jul-07

AUS direct property and employment annualised returns versus employment growth, quarterly rests

Total property (lhs)

Employment (rhs)

Source: IPD Research.Note: return and growth rates expresed in real terms.

0%

2%

4%

6%

8%

10%

12%

14%

16%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Dec-85 Jan-89 Feb-92 Mar-95 Apr-98 May-01 Jun-04 Jul-07

AUS direct property and the macroeconomy annualised returns versus economic growth, quarterly rests

Total property (lhs)

GDP (rhs)

Source: IPD Research.Note: return and growth rates expresed in nominal terms.

© IPD 201018www.ipd.com/australia

The influence of macroeconomy - the impact of real economy varies across country property markets

R² = 0.65

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0.0% 2.5% 5.0% 7.5% 10.0% 12.5% 15.0%

Pro

pert

y re

turn

GDP growth

AUS: direct property and the macroeconomy annual observations: 1985-2009

Source: IPD Research.

Correlation: 0.81

Source: IPD Research.

R² = 0.38

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

-5.0% -2.5% 0.0% 2.5% 5.0% 7.5% 10.0%12.5%15.0%

prop

erty

retu

rn

GDP growth

UK: direct property and the macroeconomy annual observations: 1987-2009

Source: IPD Research.

Correlation: 0.61

R² = 0.28

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

-2.5% 0.0% 2.5% 5.0% 7.5% 10.0%

prop

erty

retu

rn

GDP growth

NZ: direct property and the macroeconomy annual observations: 1990-2009

Source: IPD Research.

Correlation: 0.53

R² = 0.40

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0.0% 2.5% 5.0% 7.5% 10.0% 12.5%

prop

erty

retu

rn

GDP growth

US: direct property and the macroeconomy annual observations: 1980-2009

Source: IPD Research.

Correlation: 0.63

The variable impact on property markets is reflected with varying degree of positive correlation values.

This provides some support for a diversification strategy.

© IPD 201019www.ipd.com/australia

The influence of macroeconomy - cycles have significant influence on relationship

Moderate correlation values between GDP growth and property returns.

Single equation results for various countries Single equation results for various countriesnominal total returns versus nominal GDP nominal total returns versus nominal GDP

annual observations ending 2009 annual observations (sample excludes tw o cycles)

Country

AUS NZ USA CAN UK

intercept -0.064 -0.032 -0.040 0.026 -0.046

slope 2.340 2.071 2.119 1.229 2.451

sample 25 20 30 25 23

R2 0.65 0.35 0.40 0.26 0.38

correlation 0.81 0.59 0.63 0.51 0.61

Diagnostics

Single equation results for various countriesnominal total returns versus nominal GDP

annual observations (sample excludes tw o cycles)

Country

AUS NZ USA CAN UK

intercept -0.011 0.099 0.008 0.069 0.026

slope 1.977 0.150 1.943 0.683 1.639

sample 14 15 15 15 15

R2 0.46 0.00 0.21 0.07 0.06

correlation 0.68 0.04 0.46 0.26 0.24

Diagnostics

Correlations fall away with the purging form the sample period.

© IPD 201020www.ipd.com/australia

Property cycles and real economy- the relationship between capital growth and labour markets

Countries with steep declines in capital growth have experienced a rapid deterioration in labour markets.

R² = 0.31

-25%

-20%

-15%

-10%

-5%

0%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Cap

ital r

etur

n (r

eal)

Change in unemployment rate (ppts)

Direct property versus labour markets annualised values for 2008-2009 across selected countries

Source: IPD Research.

Correlation: -0.56

AUS

US

UK

CAN

NZJPN

R² = 0.013

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

-4.0% -2.0% 0.0% 2.0% 4.0% 6.0%

Cap

ital r

etur

n (n

omin

al)

GDP growth (nominal)

Direct property versus GDP growth annualised values for 2008-2009 across selected countries

Source: IPD Research.

Correlation: 0.11

AUS

US

UK

CAN

NZJPN

© IPD 201021www.ipd.com/australia

Overview

External shocks and property markets

Modelling approach and preliminary results

Implications for asset allocations

Summary remarks

Outline

© IPD 201022www.ipd.com/australia

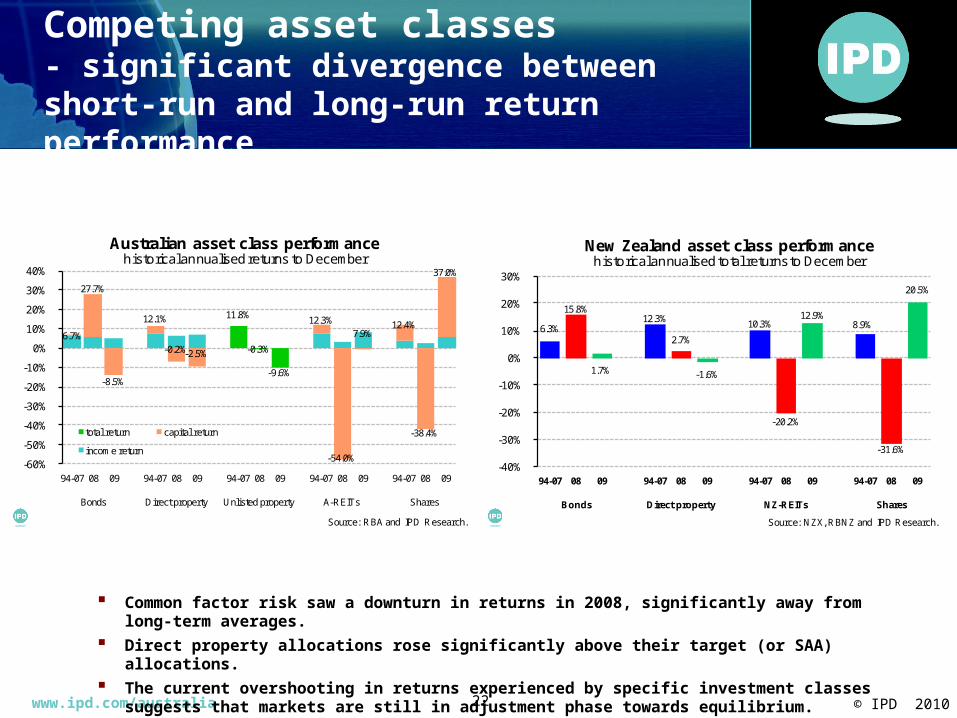

Competing asset classes- significant divergence between short-run and long-run return performance

Common factor risk saw a downturn in returns in 2008, significantly away from long-term averages.

Direct property allocations rose significantly above their target (or SAA) allocations.

The current overshooting in returns experienced by specific investment classes suggests that markets are still in adjustment phase towards equilibrium.

11.8%

-0.3%

-9.6%

6.7%

27.7%

-8.5%

12.1%

-0.2%-2.5%

12.3%

-54.0%

7.9%12.4%

-38.4%

37.0%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

94-07 08 09 94-07 08 09 94-07 08 09 94-07 08 09 94-07 08 09

Bonds Direct property Unlisted property A-REITs Shares

Australian asset class performancehistorical annualised returns to December

total return capital return

income return

Source: RBA and IPD Research.

6.3%

15.8%

1.7%

12.3%

2.7%

-1.6%

10.3%

-20.2%

12.9%8.9%

-31.6%

20.5%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

94-07 08 09 94-07 08 09 94-07 08 09 94-07 08 09

Bonds Direct property NZ-REITs Shares

New Zealand asset class performancehistorical annualised total returns to December

Source: NZX, RBNZ and IPD Research.

© IPD 201023www.ipd.com/australia

State-space and risk-reward- current market dynamics highlight that markets are in transition phase

Different “state” environments reflect significant movements in volatility.

The distinctly different states of the world require different strategies for asset allocation.

-35%

-25%

-15%

-5%

5%

15%

25%

35%

0% 5% 10% 15% 20% 25% 30% 35%

actu

al re

turn

annual volatility

Risk-reward trade-off for various investments annualised observations

Shares

A-REITs

Unlisted property

Direct property

Bonds

DUMMY

Shares

A-REITs

Unlisted property

Bonds

Direct property

lower risk

Source: IPD Research.

Stable "state" (1994-2007)

Unstable "state" (2007-10:Q1)

-10%

-5%

0%

5%

10%

15%

0% 5% 10% 15% 20%

actu

al re

turn

annual volatility

Risk-reward trade-off for NZ investments annualised observations

Shares

NZ-REITs

Direct property

Bonds

DUMMY

Shares

NZ-REITs

Unlisted property

Bonds

Direct property

lower risk

Source: IPD Research.

Stable "state" (1994-2007)

Unstable "state" (2007-10:Q1)

© IPD 201024www.ipd.com/australia

Introduction

External shocks and property markets

Modelling approach and preliminary results

Implications for asset allocations

Summary remarks

Outline

© IPD 201025www.ipd.com/australia

Summary results

Direct property returns Influenced by a variety of macroeconomic aggregates, but highly contingent

on cycle profile Importance of labour markets Property cycle patterns vary across country due to varying influence of

financial sector

Asset allocation Distinction between permanent and transitory shocks Need to consider different “states” when formulating target asset allocations

Research

Expand research to include more countries Explore the impact of shocks across both direct and listed property markets

© IPD 201026www.ipd.com/australia

Intellectual Property Rights and use of IPD statistics as benchmarksWhether in the public domain or otherwise, IPD's statistics are the intellectual property of Investment Property Databank Limited.It is not permissible to use data drawn from this presentation as benchmarks.

© Investment Property Databank Limited (IPD) 2010. Database Right, Investment Property Databank Limited (IPD) 2010. All rights conferred by law of copyright and by virtue of international conventions are reserved by IPD

Contact

Anthony De FrancescoManaging DirectorTelephone: +61 2 9248 1901

Mobile: +61 (0) 405 506 284

Email: [email protected]

IPD – AUS/NZAddress: Suite 3, Level 3, 275 George Street, Sydney NSW 2000, AustraliaWeb: www.ipd.com/newzealand

IPD - UK1 St. John’s LaneLondon, EC1M 4BLUnited KingdomTel: +44 (0)20 7336 9200Email: [email protected]: www.ipd.com

![IPD/Bim Thesis Proposal - engr.psu.edu · [IPD/BIM THESIS PROPOSAL] Jason Brognano, Michael Gilroy, Stephen Kijak, David Maser December 6, 2010 KGB Maser KGB Maser| BIM/IPD Thesis](https://static.documents.pub/doc/80x56/605d339025f9181d960e06e8/ipdbim-thesis-proposal-engrpsuedu-ipdbim-thesis-proposal-jason-brognano.jpg)

![IPD/Bim Thesis Proposal - Penn State College of Engineering€¦ · [IPD/BIM THESIS PROPOSAL] Jason Brognano, Michael Gilroy, Stephen Kijak, David Maser December 6, 2010 KGB Maser](https://static.documents.pub/doc/80x56/605d339025f9181d960e06e9/ipdbim-thesis-proposal-penn-state-college-of-engineering-ipdbim-thesis-proposal.jpg)