61

Errors

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | elwin-perry |

| View: | 295 times |

| Download: | 11 times |

Errors

Errors

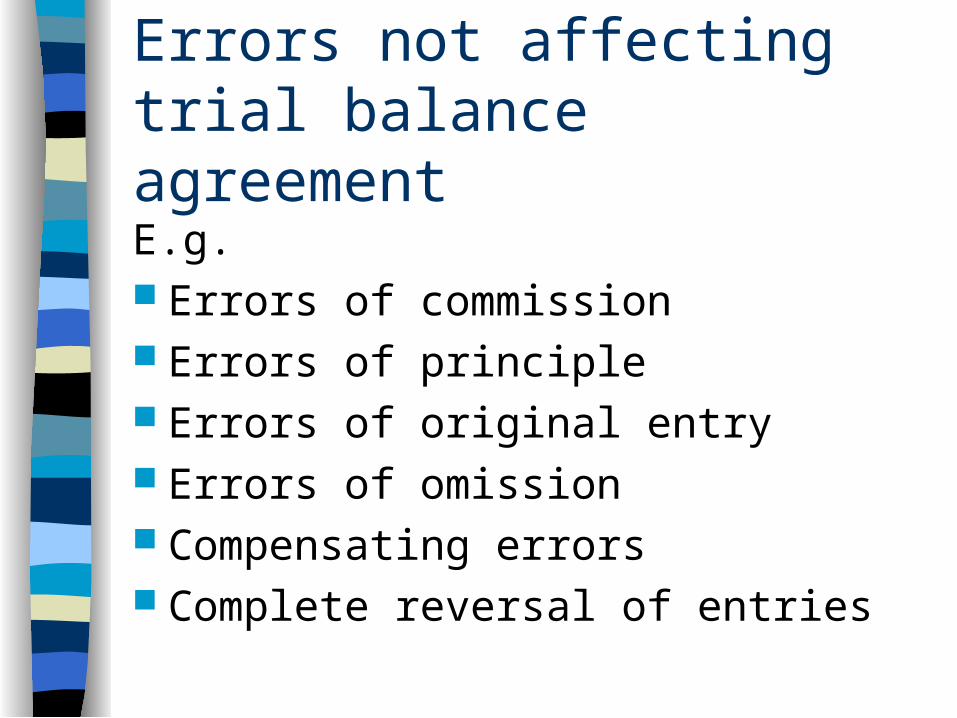

Errors not affecting trial balance agreement

Errors affecting trial balance agreement

Errors not affecting trial balance agreement

E.g. Errors of commission Errors of principle Errors of original entry Errors of omission Compensating errors Complete reversal of entries

Errors affecting trial balance agreement Suspense account

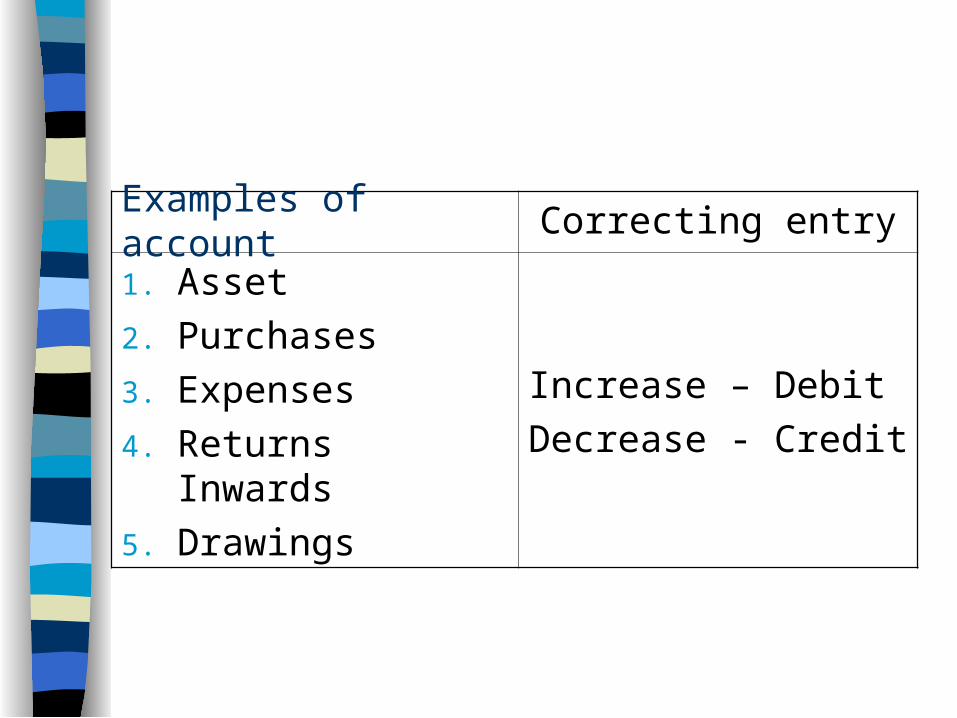

Correcting entry

1. Asset

2. Purchases

3. Expenses

4. Returns Inwards

5. Drawings

Increase – Debit

Decrease - Credit

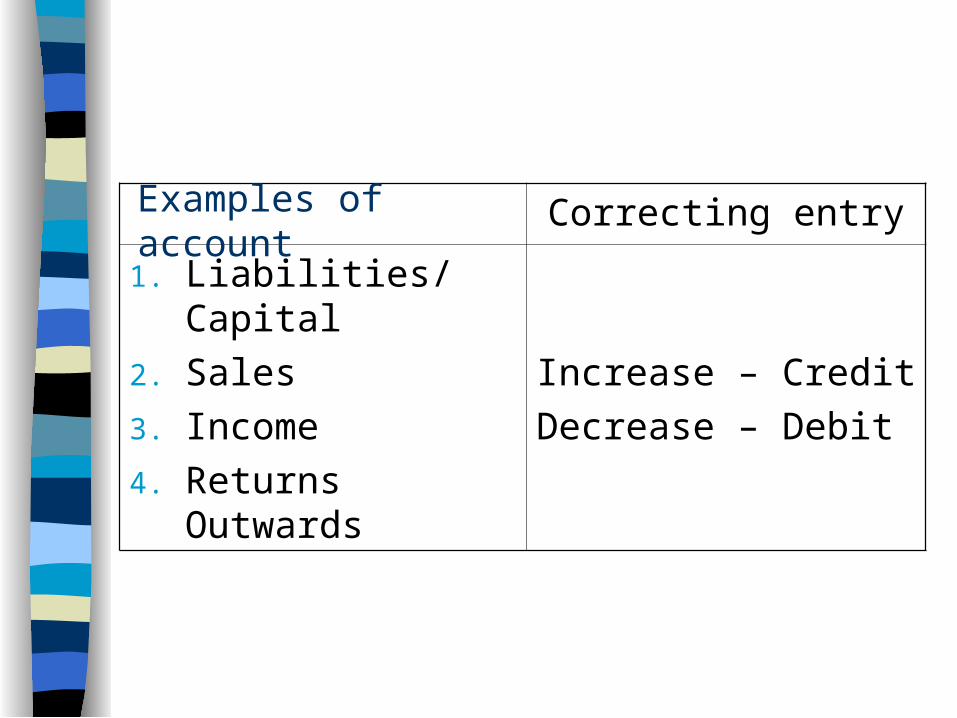

Examples of account

Correcting entry

1. Liabilities/Capital

2. Sales

3. Income

4. Returns Outwards

Increase – Credit

Decrease – Debit

Examples of account

Errors Not Affecting Trial Balance Agreement

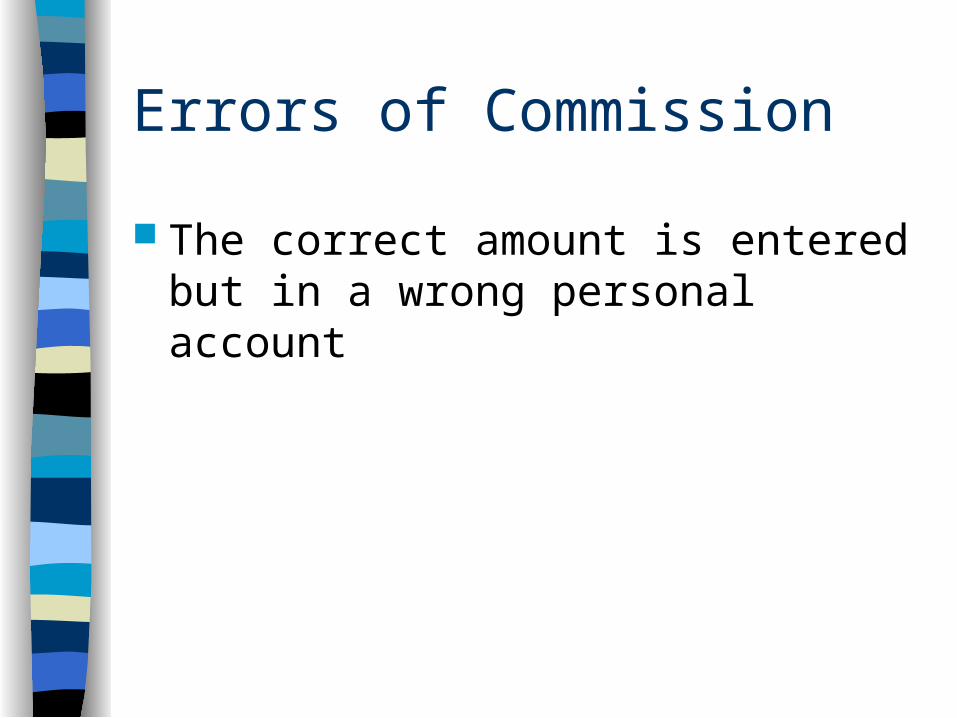

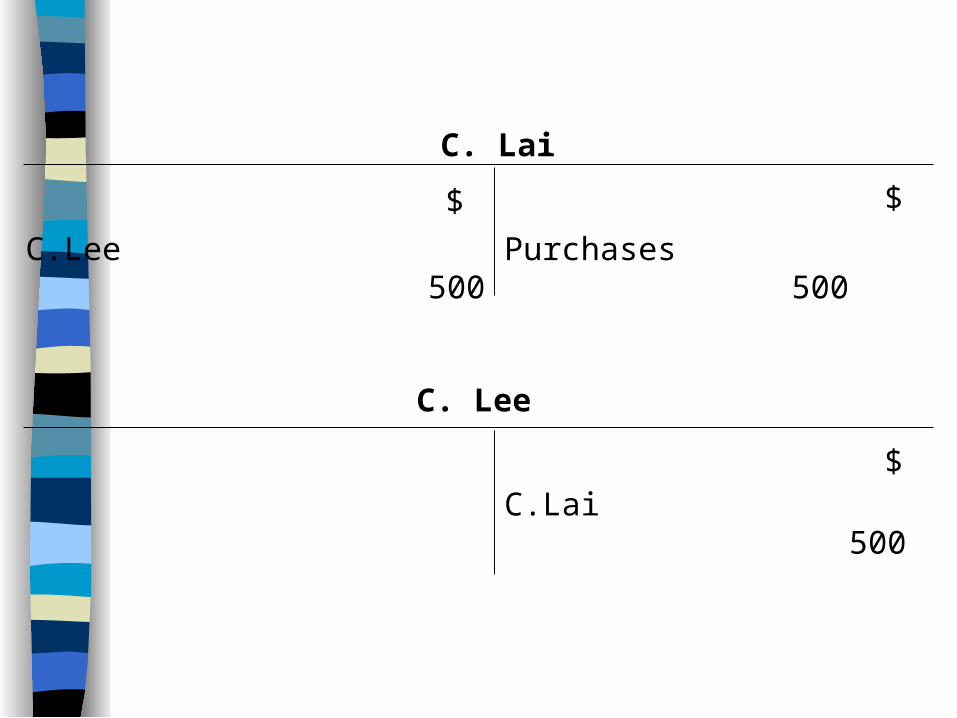

Errors of Commission

The correct amount is entered but in a wrong personal account

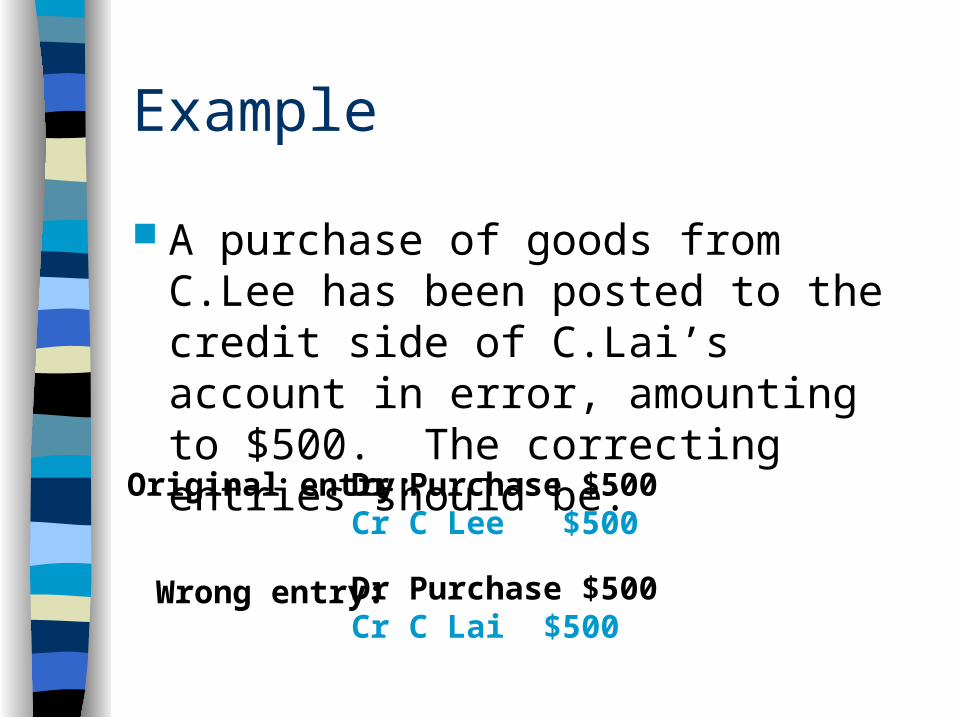

Example

A purchase of goods from C.Lee has been posted to the credit side of C.Lai’s account in error, amounting to $500. The correcting entries should be:

Original entry:

Wrong entry:

Dr Purchase $500Cr C Lee $500

Dr Purchase $500Cr C Lai $500

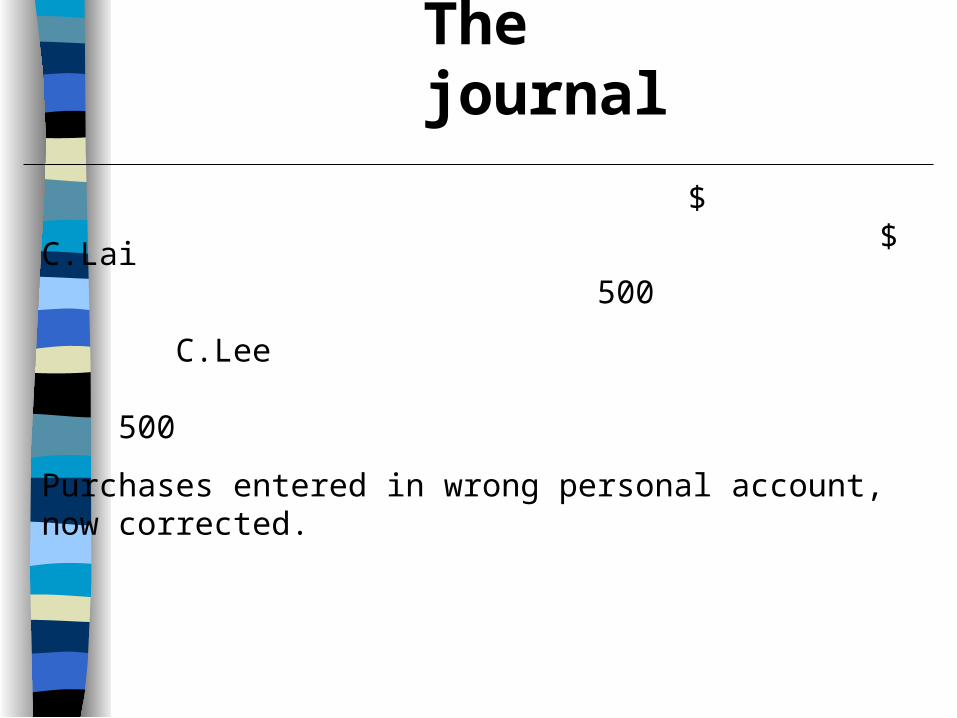

$ $

C.Lai 500

C.Lee 500

Purchases entered in wrong personal account, now corrected.

The journal

$$

C.Lee 500

C. Lai

Purchases 500

$

C. Lee

C.Lai 500

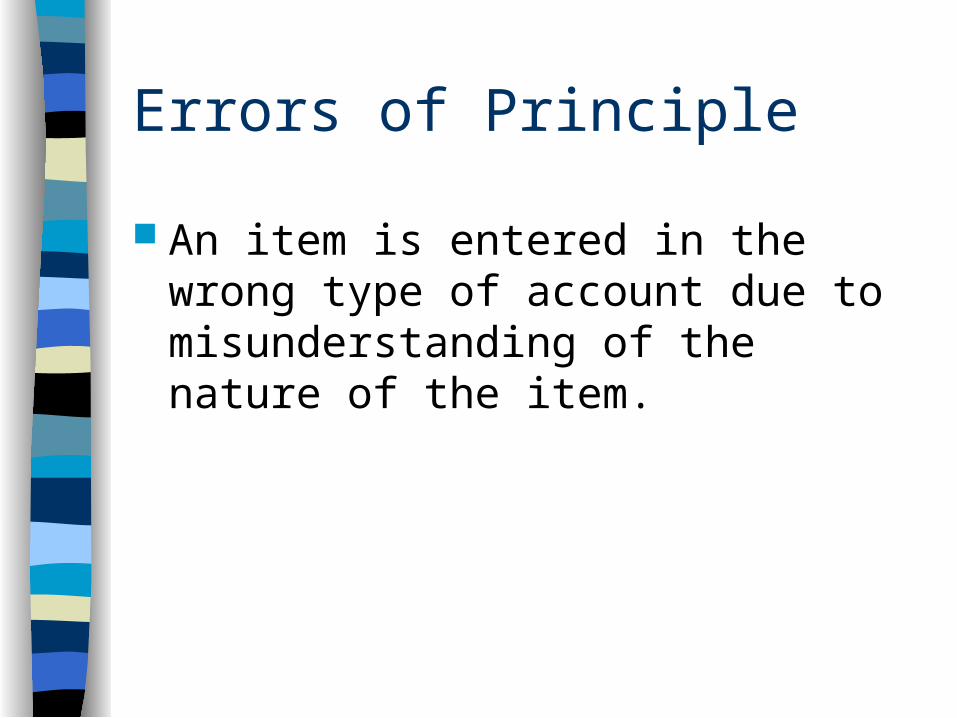

Errors of Principle

An item is entered in the wrong type of account due to misunderstanding of the nature of the item.

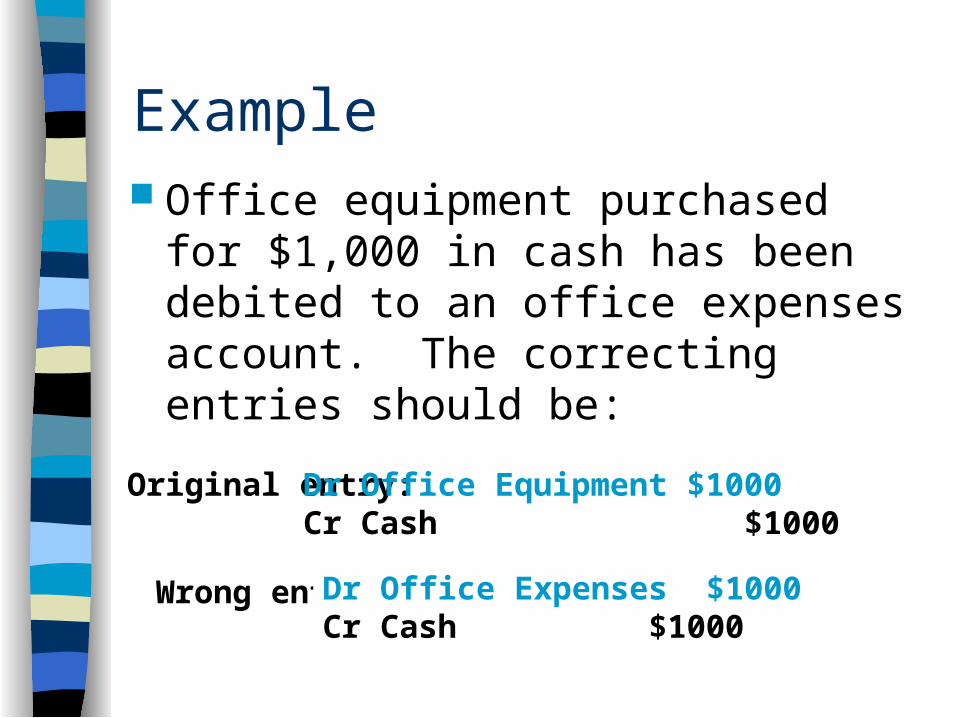

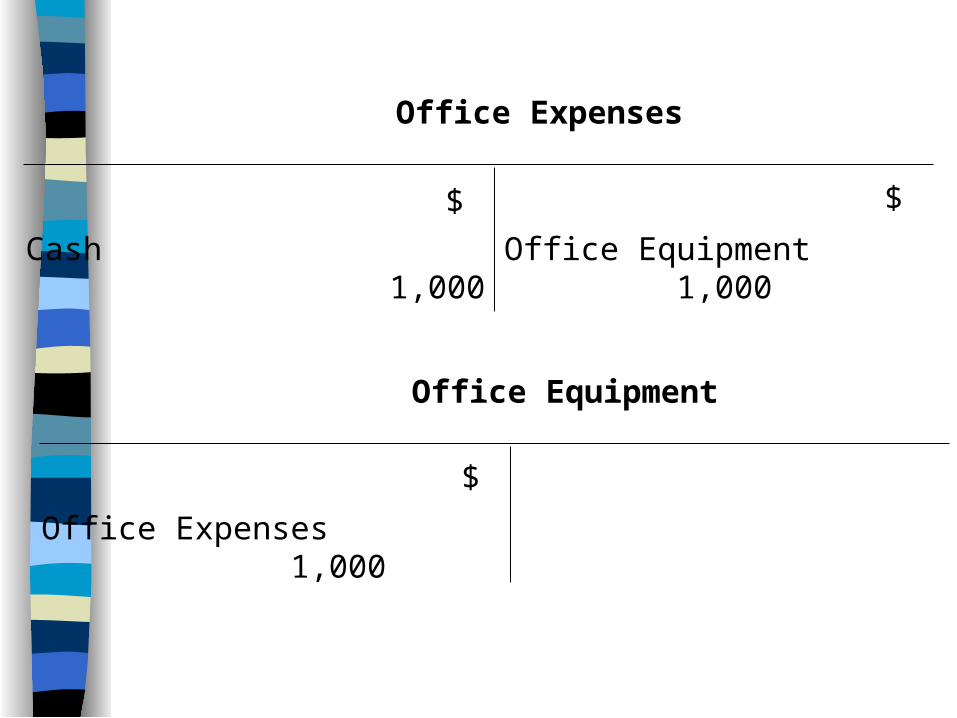

Example Office equipment purchased for $1,000

in cash has been debited to an office expenses account. The correcting entries should be:

Original entry:

Wrong entry:

Dr Office Equipment $1000Cr Cash $1000

Dr Office Expenses $1000Cr Cash $1000

$ $

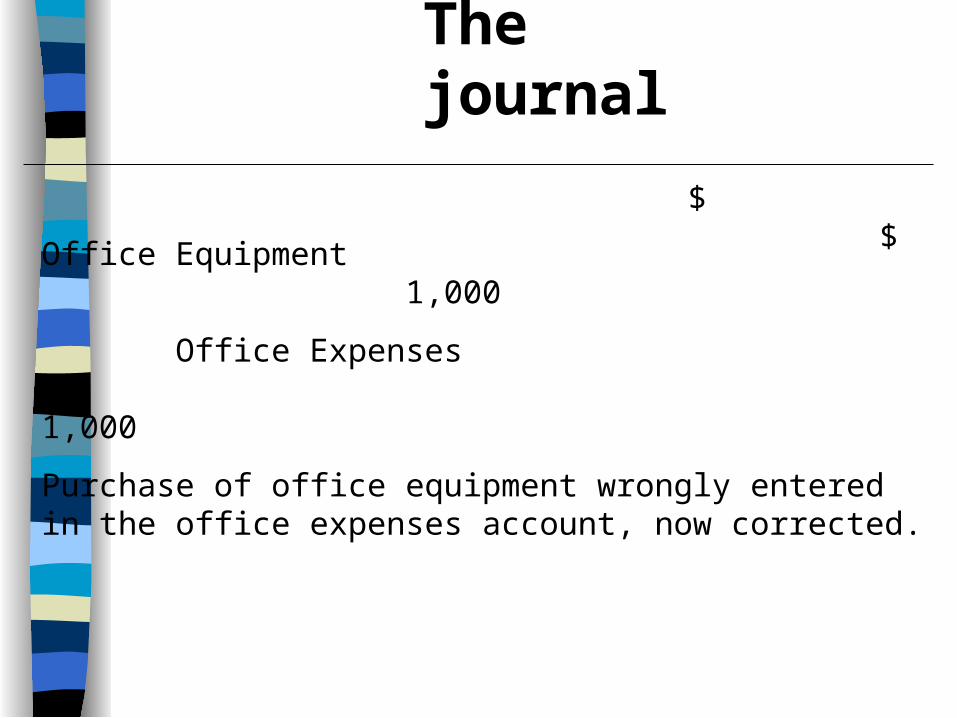

Office Equipment 1,000

Office Expenses 1,000

Purchase of office equipment wrongly entered in the office expenses account, now corrected.

The journal

$$

Cash 1,000

Office Expenses

Office Equipment 1,000

$

Office Equipment

Office Expenses 1,000

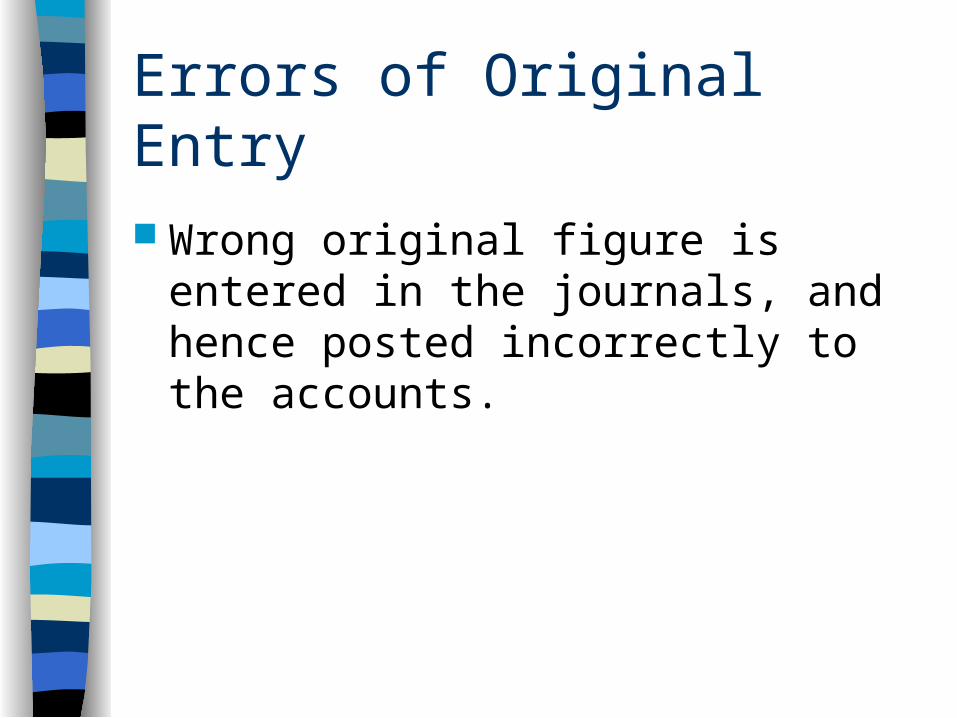

Errors of Original Entry

Wrong original figure is entered in the journals, and hence posted incorrectly to the accounts.

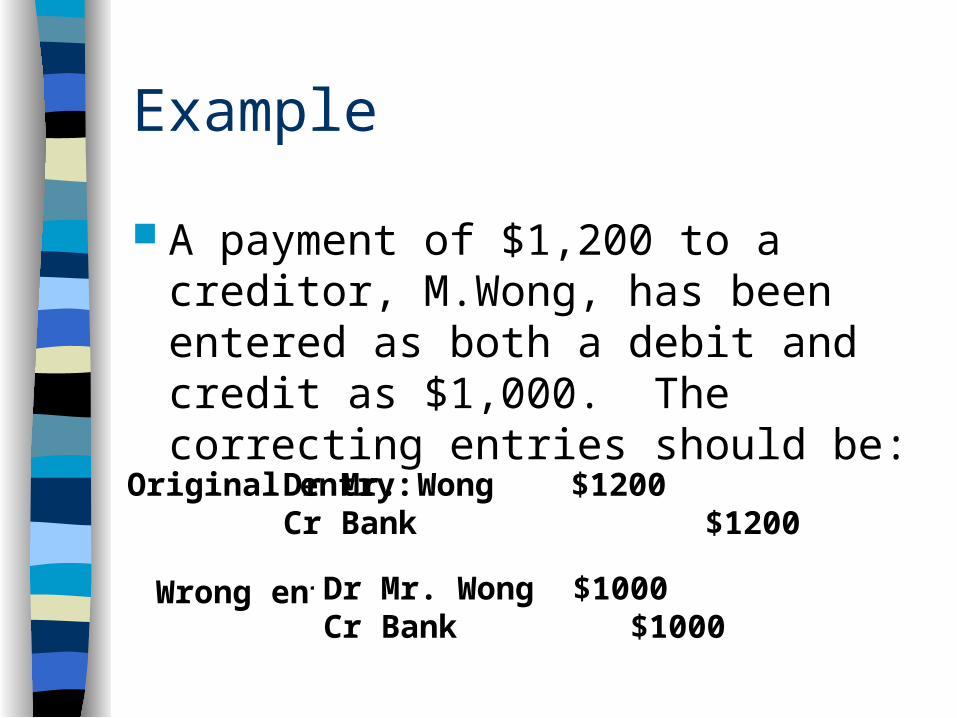

Example

A payment of $1,200 to a creditor, M.Wong, has been entered as both a debit and credit as $1,000. The correcting entries should be:

Original entry:

Wrong entry:

Dr Mr. Wong $1200Cr Bank $1200

Dr Mr. Wong $1000Cr Bank $1000

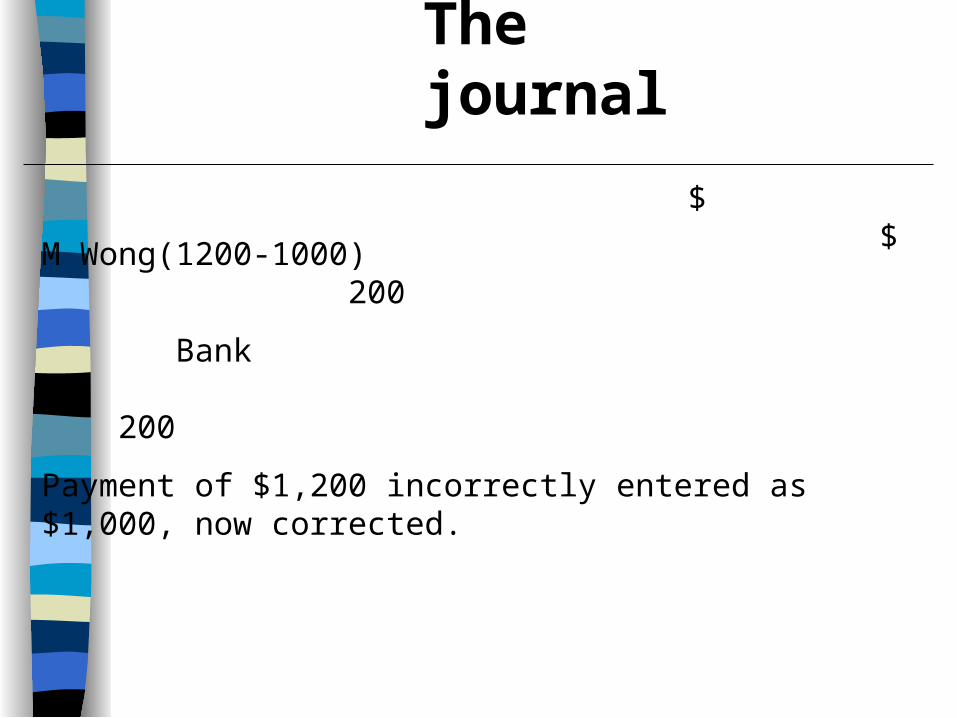

$ $

M Wong(1200-1000) 200

Bank 200

Payment of $1,200 incorrectly entered as $1,000, now corrected.

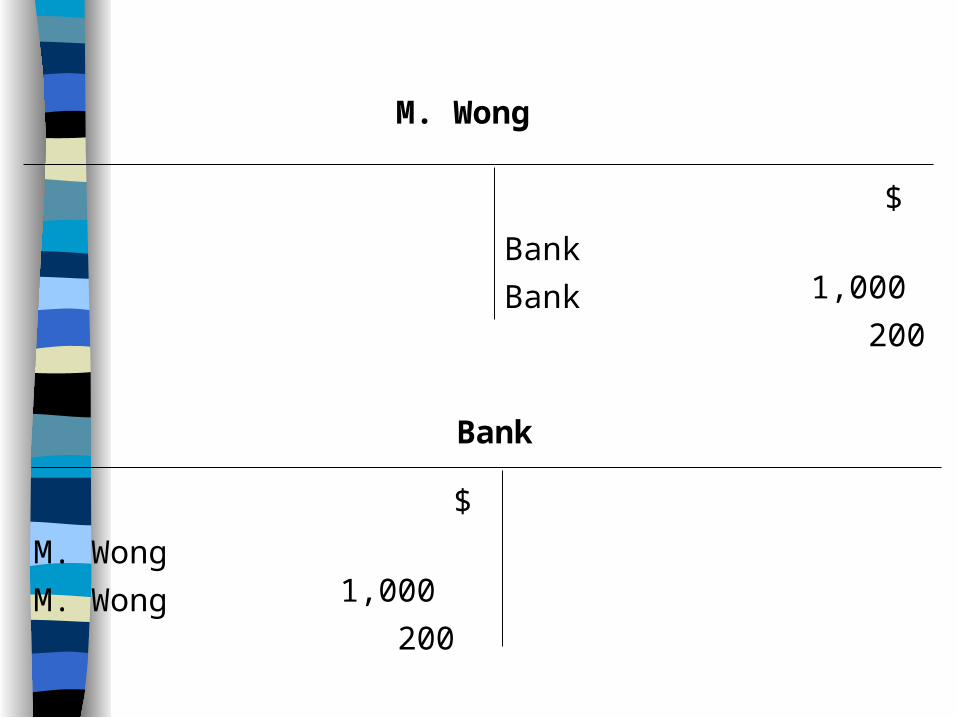

The journal

$

M. Wong

Bank 1,000

Bank 200

$

Bank

M. Wong 1,000

M. Wong 200

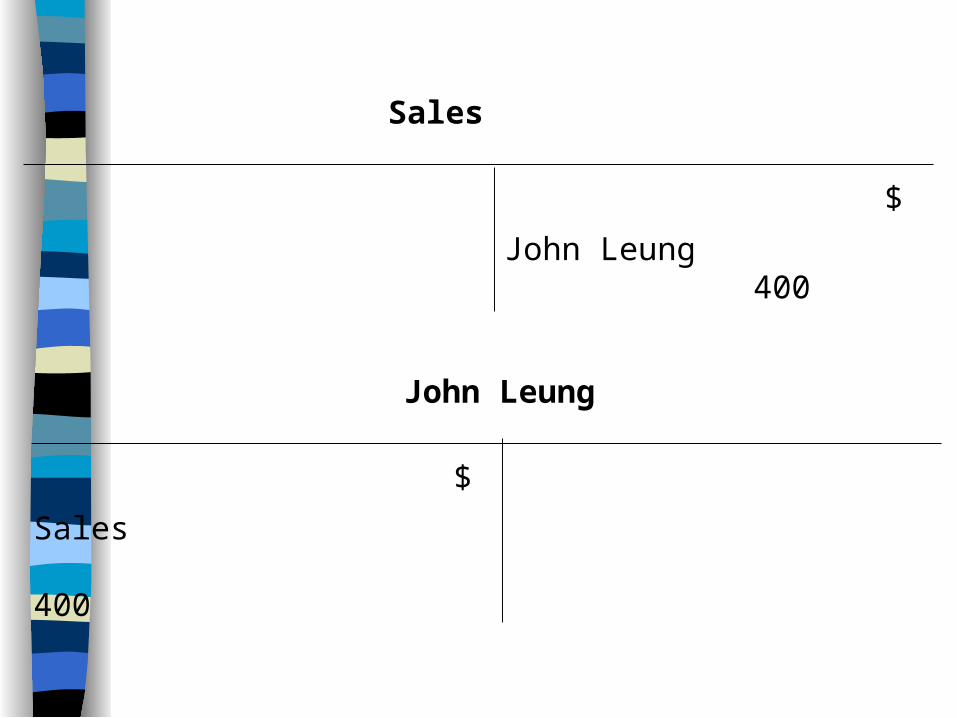

Errors of Omission

A transaction has been completely omitted from the accounts.

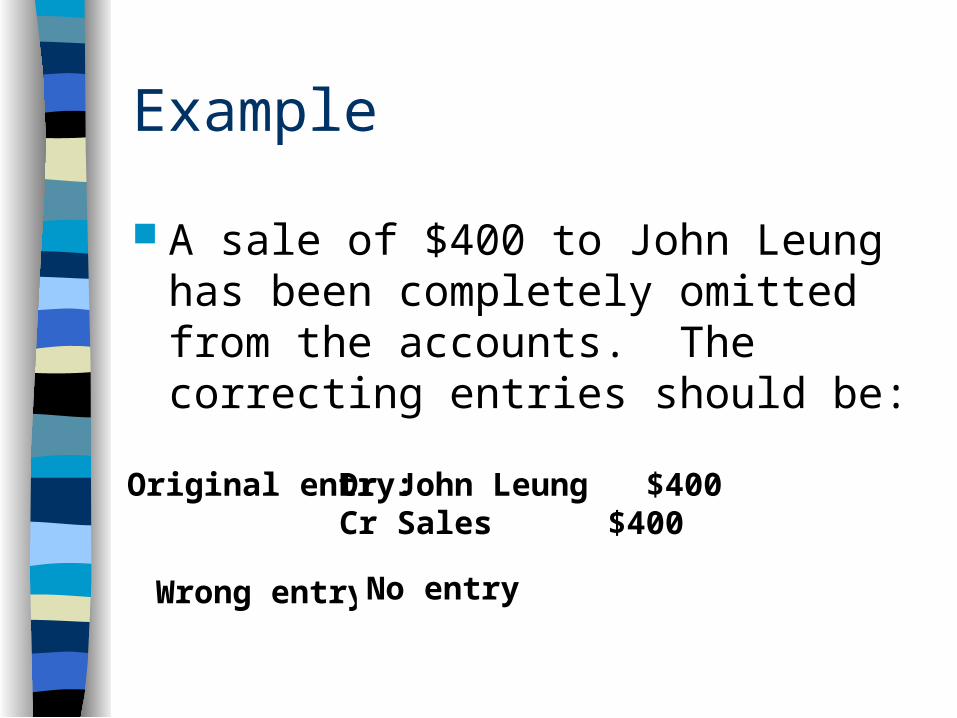

Example

A sale of $400 to John Leung has been completely omitted from the accounts. The correcting entries should be:

Original entry:

Wrong entry:

Dr John Leung $400Cr Sales $400

No entry

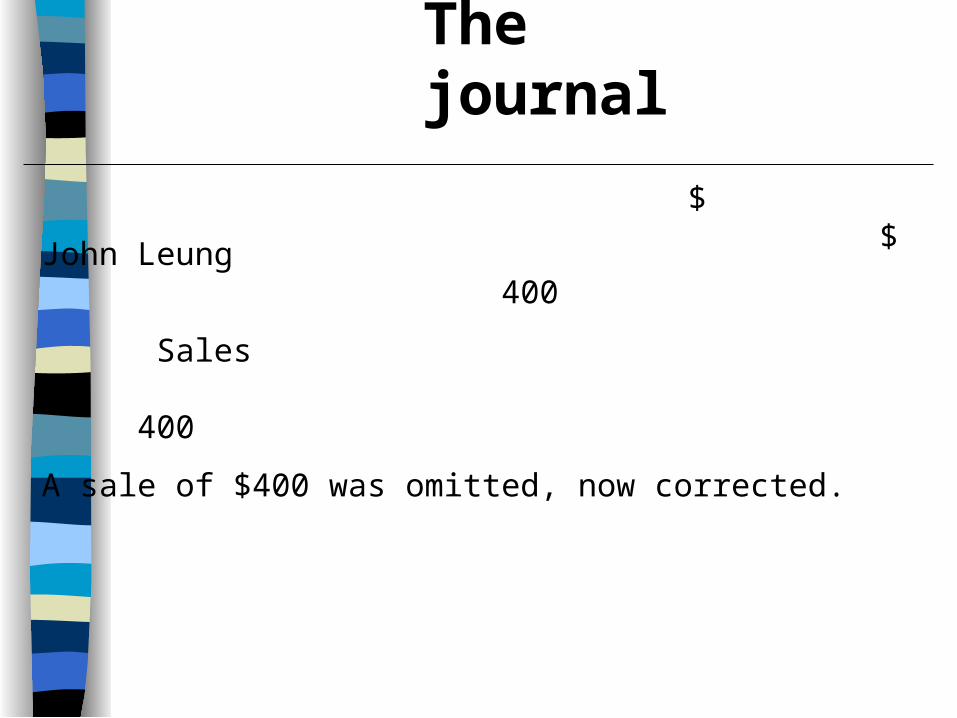

$ $

John Leung 400

Sales 400

A sale of $400 was omitted, now corrected.

The journal

$

Sales

John Leung 400

$

John Leung

Sales 400

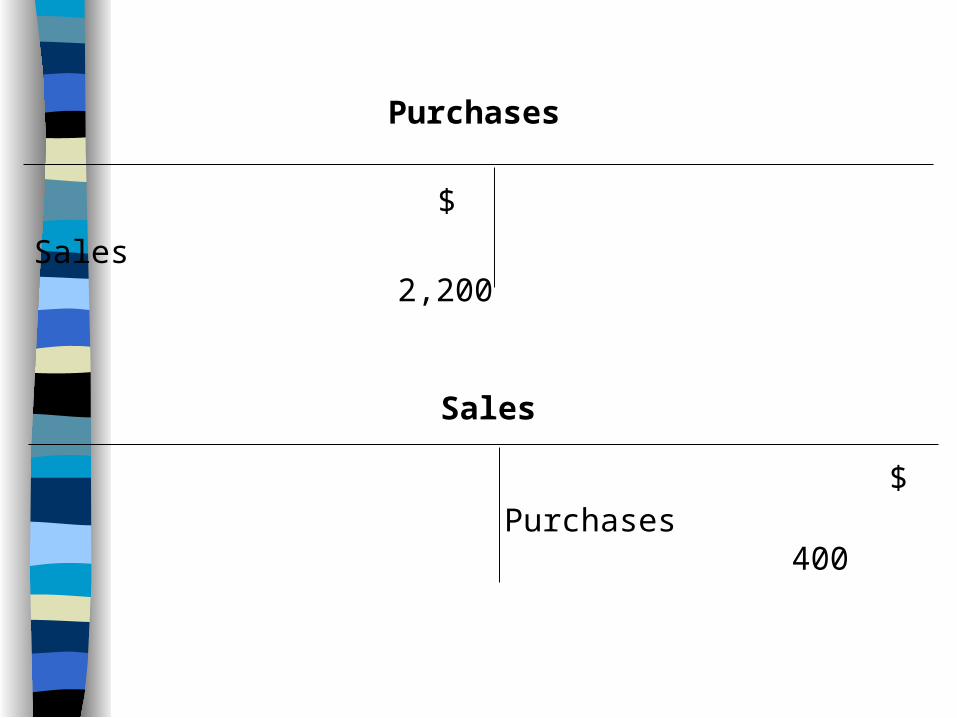

Compensating Errors

Debit side errors are equal to credit side errors.

Example

The purchases account was undercast by $2,200, and the sales account was also undercast by $2,200. The correcting entries should be:

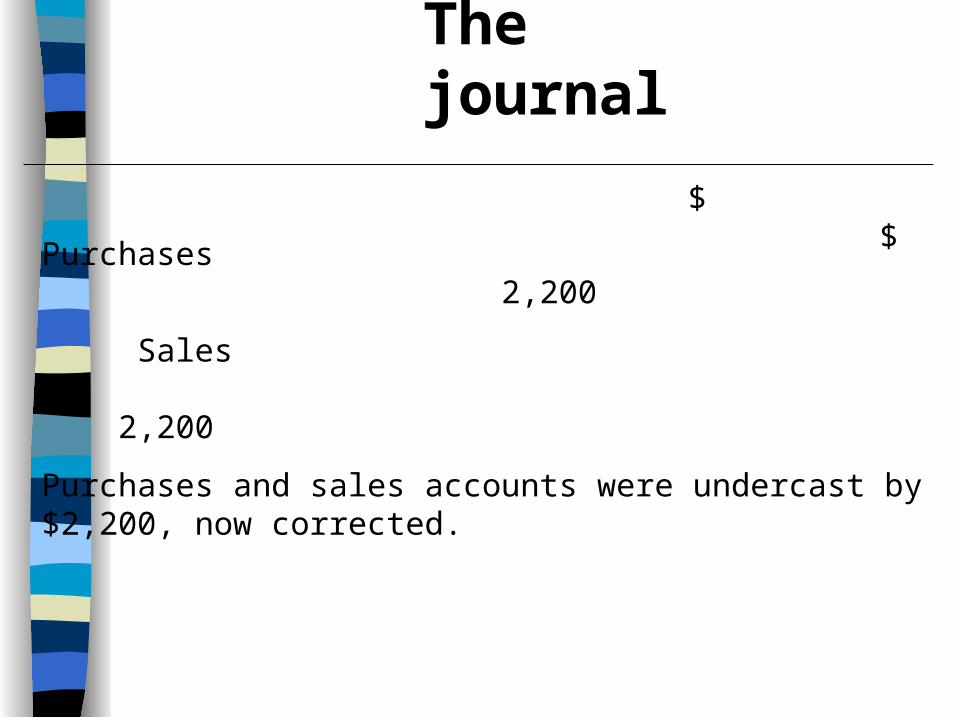

$ $

Purchases 2,200

Sales 2,200

Purchases and sales accounts were undercast by $2,200, now corrected.

The journal

$

Purchases

Sales 2,200

$

Sales

Purchases 400

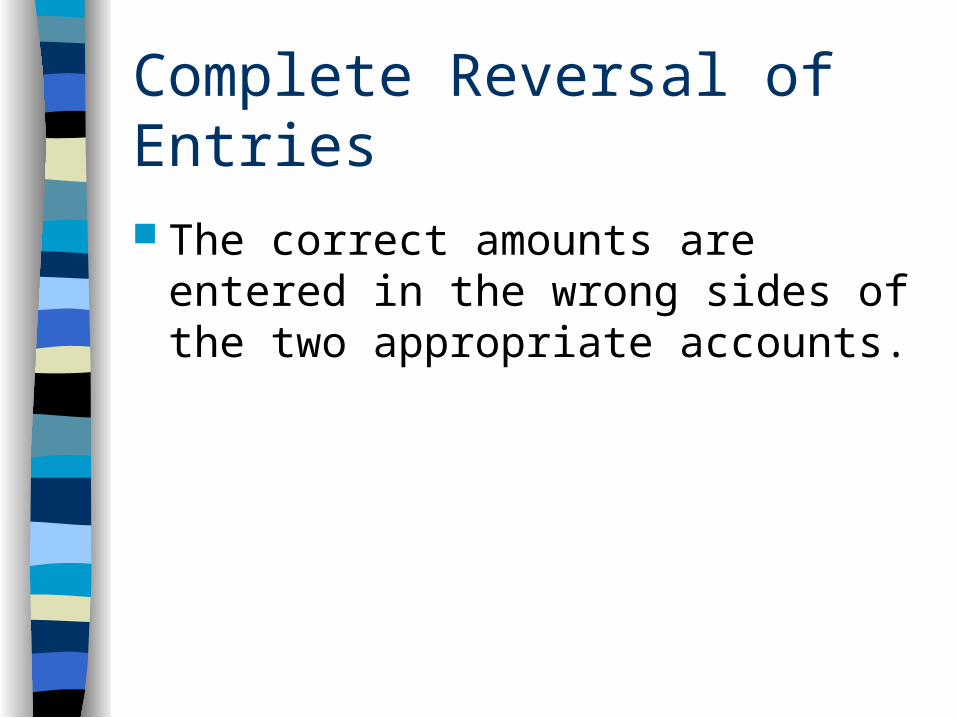

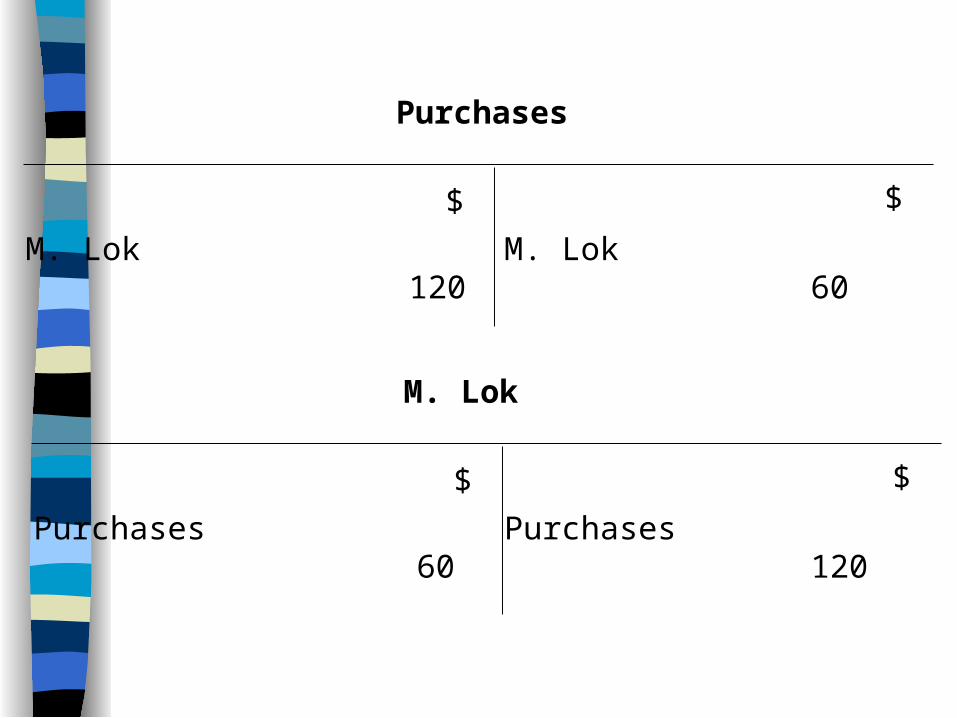

Complete Reversal of Entries

The correct amounts are entered in the wrong sides of the two appropriate accounts.

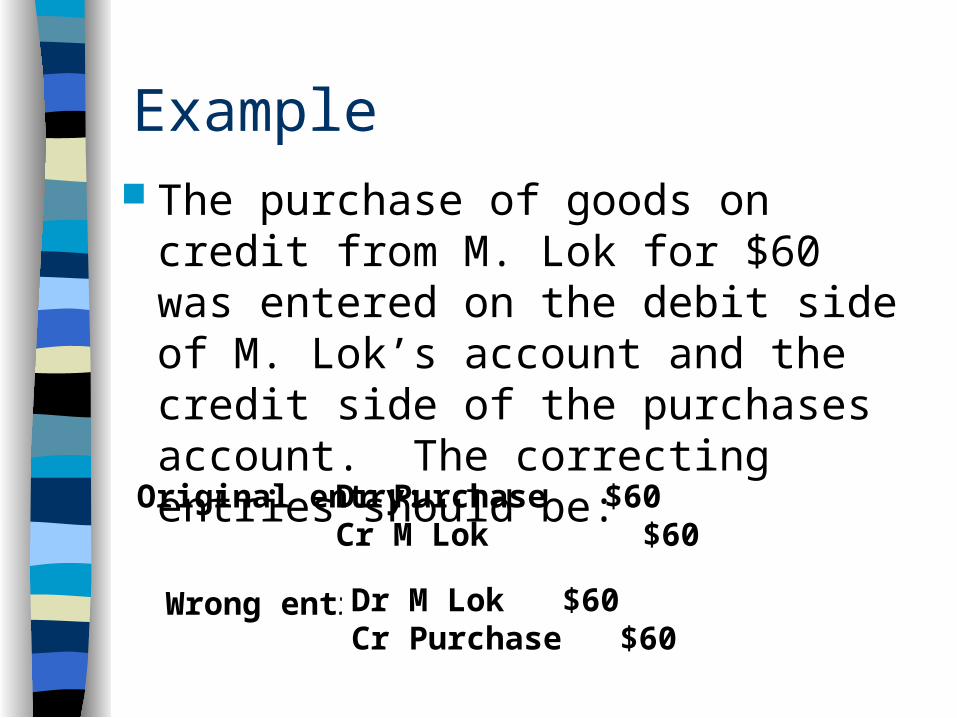

Example The purchase of goods on credit from

M. Lok for $60 was entered on the debit side of M. Lok’s account and the credit side of the purchases account. The correcting entries should be:

Original entry:

Wrong entry:

Dr Purchase $60Cr M Lok $60

Dr M Lok $60Cr Purchase $60

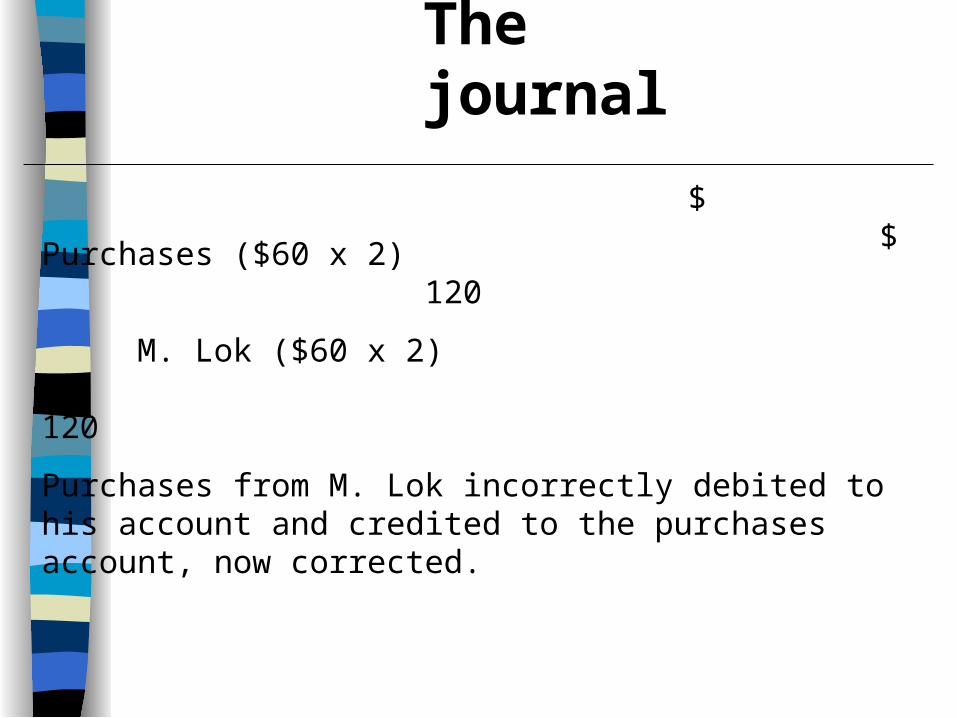

$ $

Purchases ($60 x 2) 120

M. Lok ($60 x 2) 120

Purchases from M. Lok incorrectly debited to his account and credited to the purchases account, now corrected.

The journal

$$

M. Lok 120

Purchases

M. Lok 60

$$

Purchases 60

M. Lok

Purchases 120

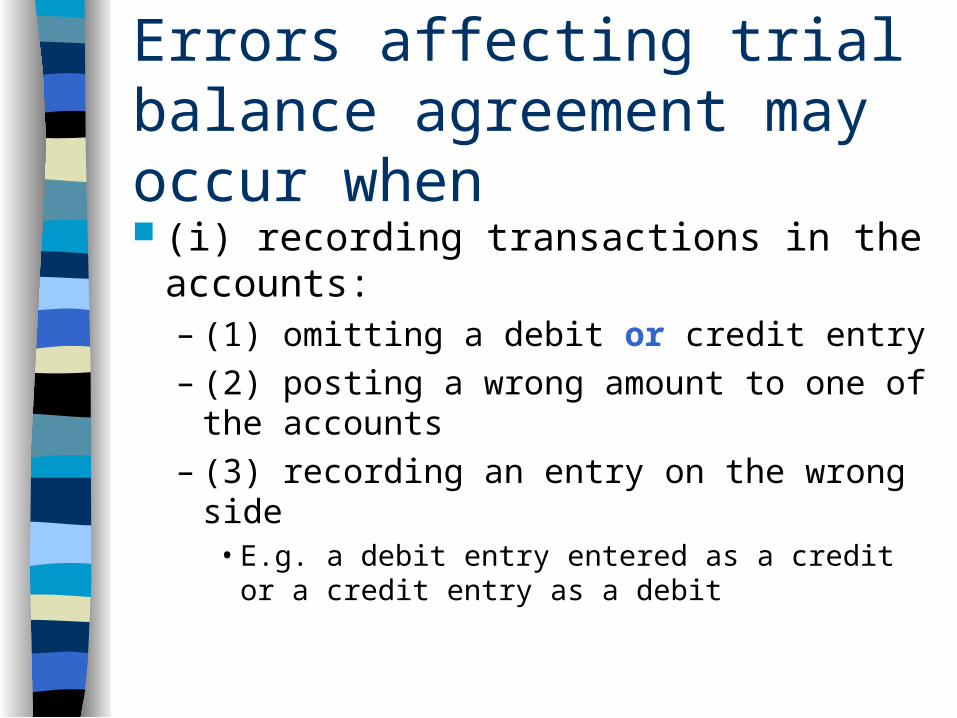

Errors Affecting Trial Balance Agreement

Errors affecting trial balance agreement may occur when (i) recording transactions in the

accounts:– (1) omitting a debit or credit entry– (2) posting a wrong amount to one of the

accounts– (3) recording an entry on the wrong side

• E.g. a debit entry entered as a credit or a credit entry as a debit

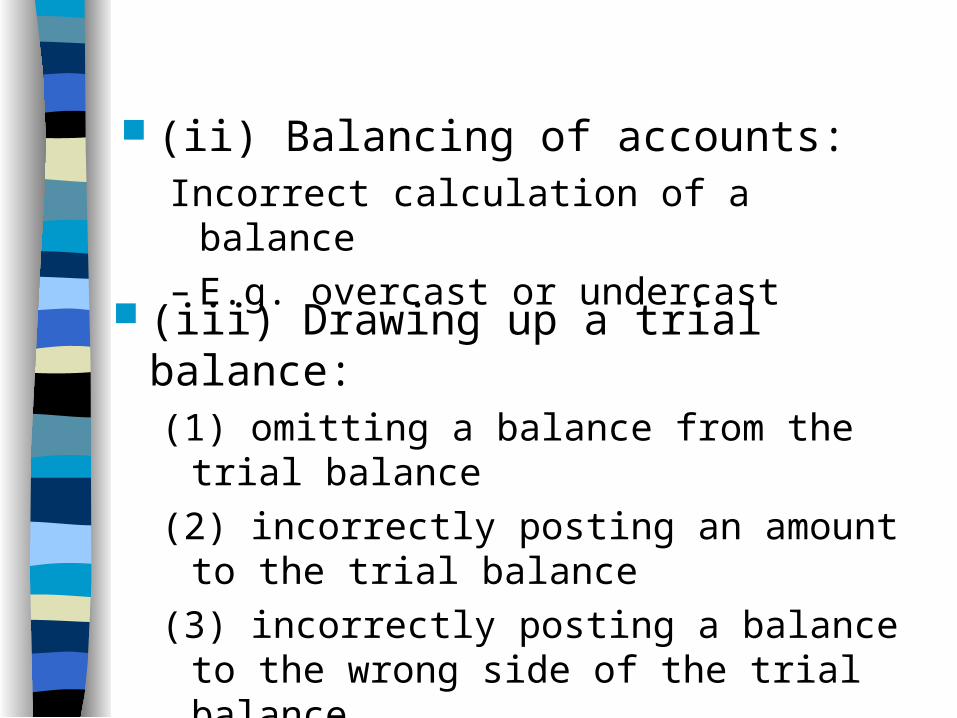

(ii) Balancing of accounts:Incorrect calculation of a balance– E.g. overcast or undercast

(iii) Drawing up a trial balance:(1) omitting a balance from the trial balance

(2) incorrectly posting an amount to the trial balance

(3) incorrectly posting a balance to the wrong side of the trial balance

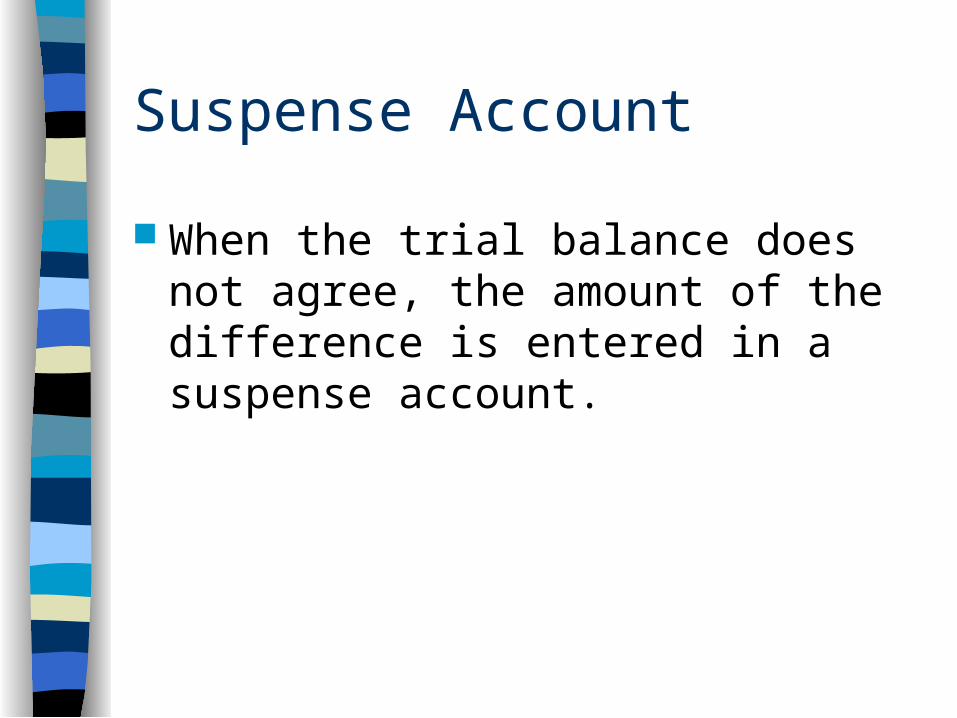

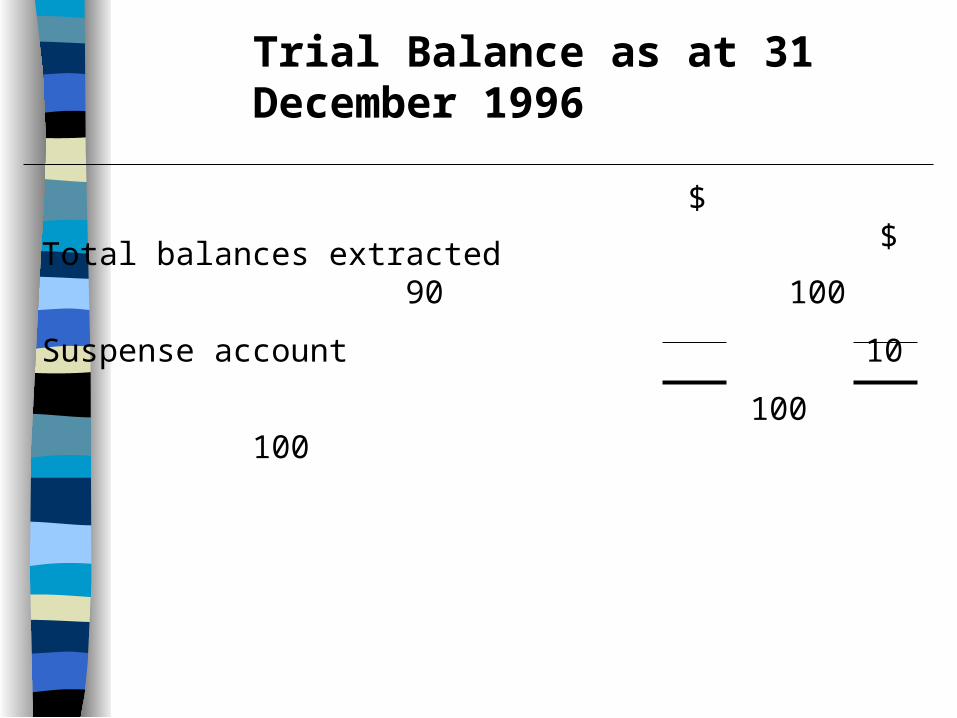

Suspense Account

When the trial balance does not agree, the amount of the difference is entered in a suspense account.

$ $

Total balances extracted 90 100

Suspense account 10

100 100

Trial Balance as at 31 December 1996

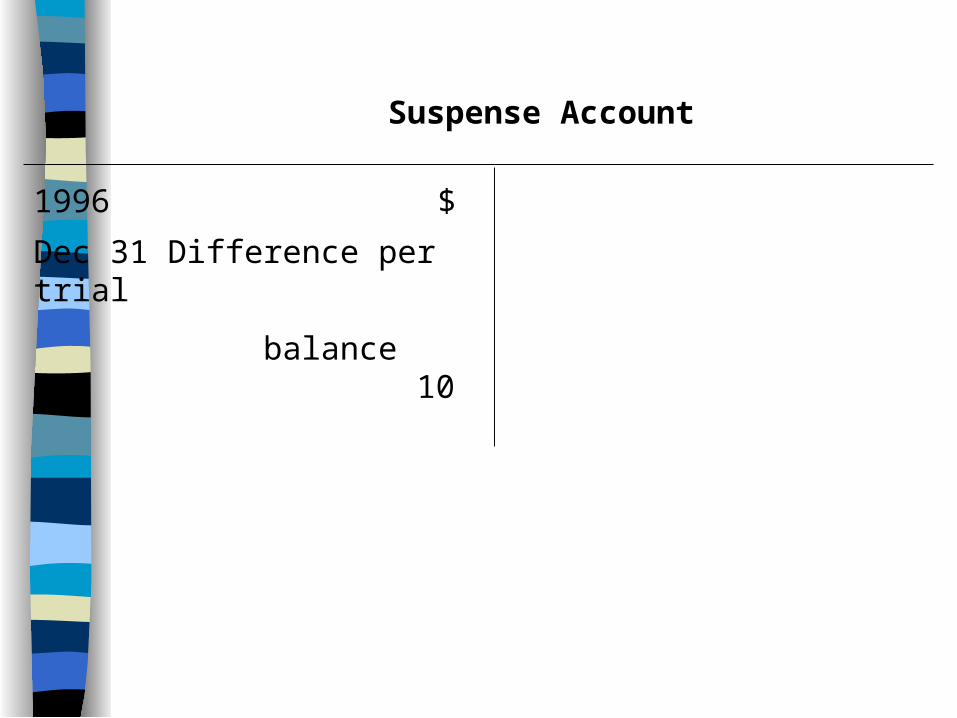

$

Suspense Account

Dec 31 Difference per trial

balance 10

1996

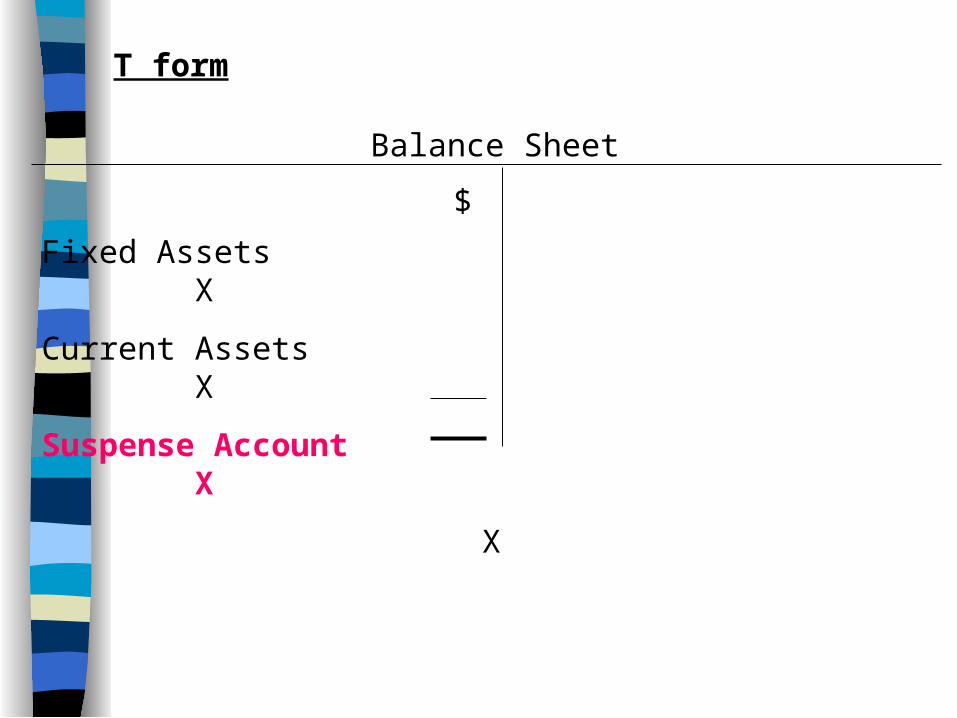

How To Show a Suspense Account on the Balance Sheet

Debit Balance of the Suspense Account

$

T form

Fixed Assets X

Current Assets X

Suspense Account X

X

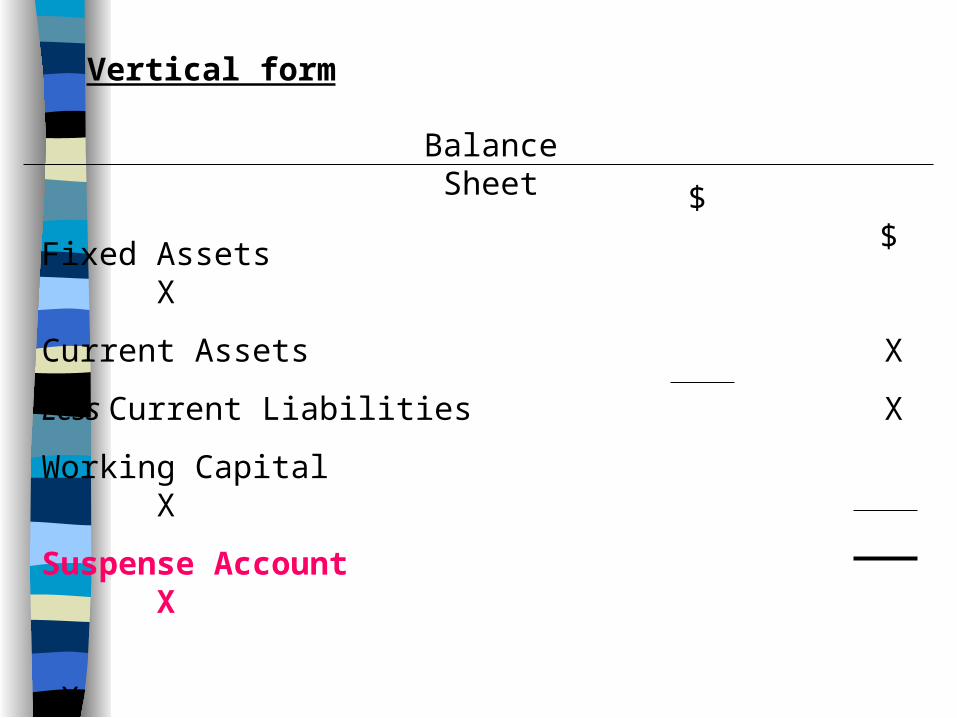

Balance Sheet

$ $

Fixed Assets X

Current Assets X

Less Current Liabilities X

Working Capital X

Suspense Account X

X

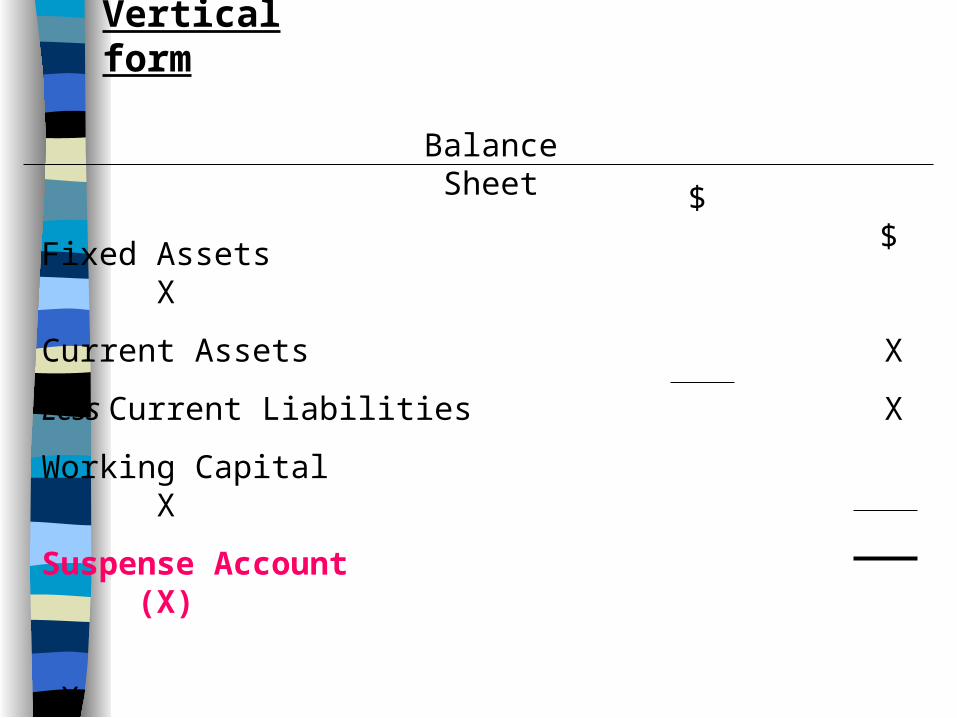

Vertical form

Balance Sheet

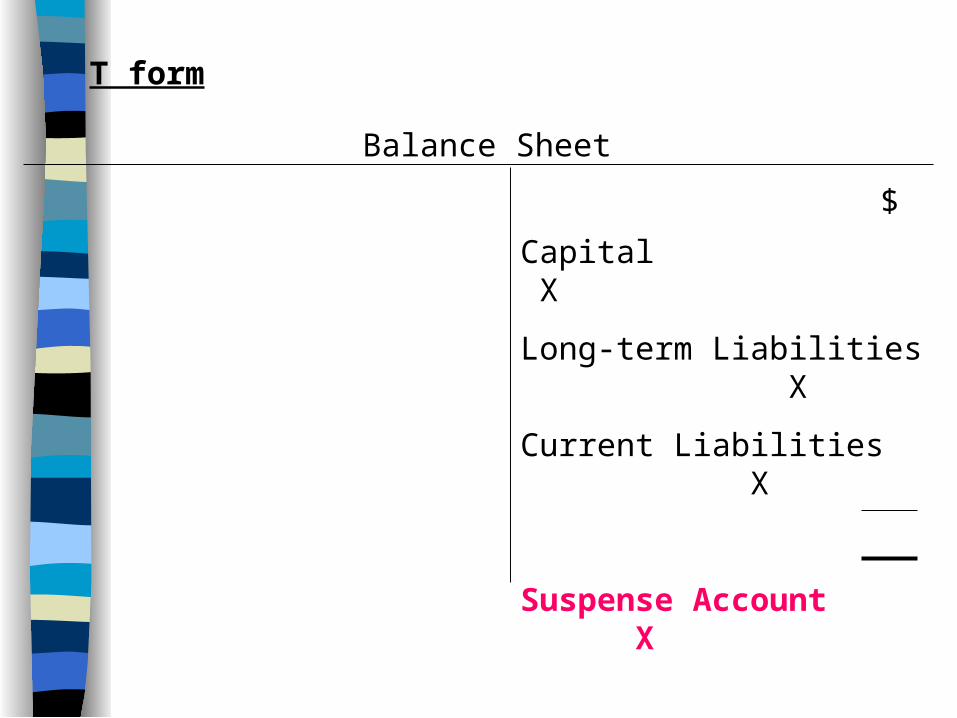

Credit Balance of the Suspense Account

$

T form

Capital X

Long-term Liabilities X

Current Liabilities X

Suspense Account X

X

Balance Sheet

$ $

Fixed Assets X

Current Assets X

Less Current Liabilities X

Working Capital X

Suspense Account (X)

X

Vertical form

Balance Sheet

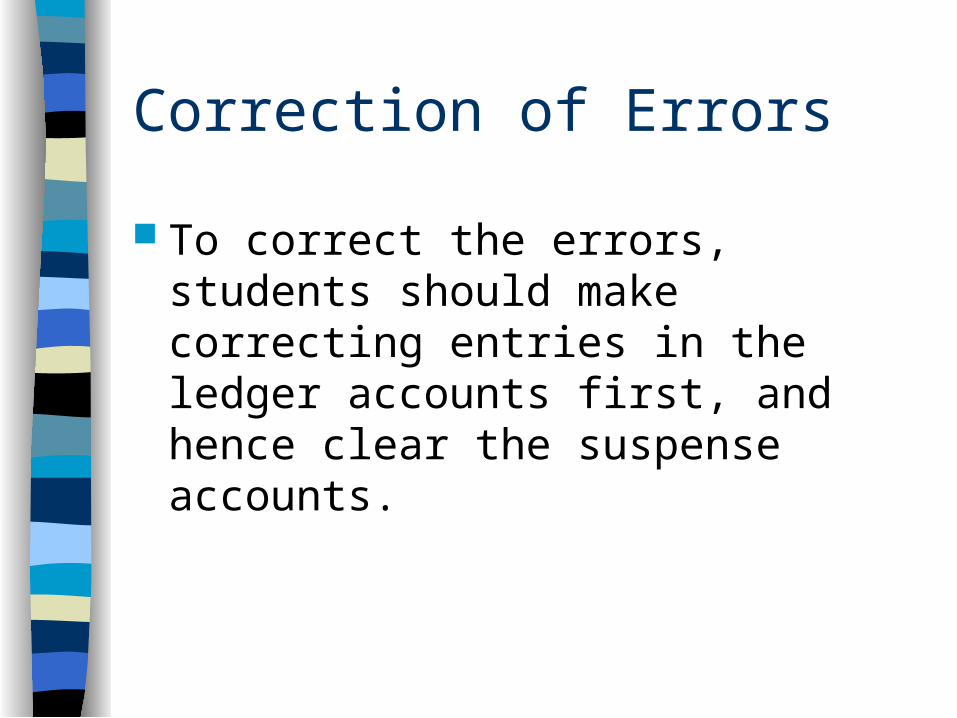

Correction of Errors

To correct the errors, students should make correcting entries in the ledger accounts first, and hence clear the suspense accounts.

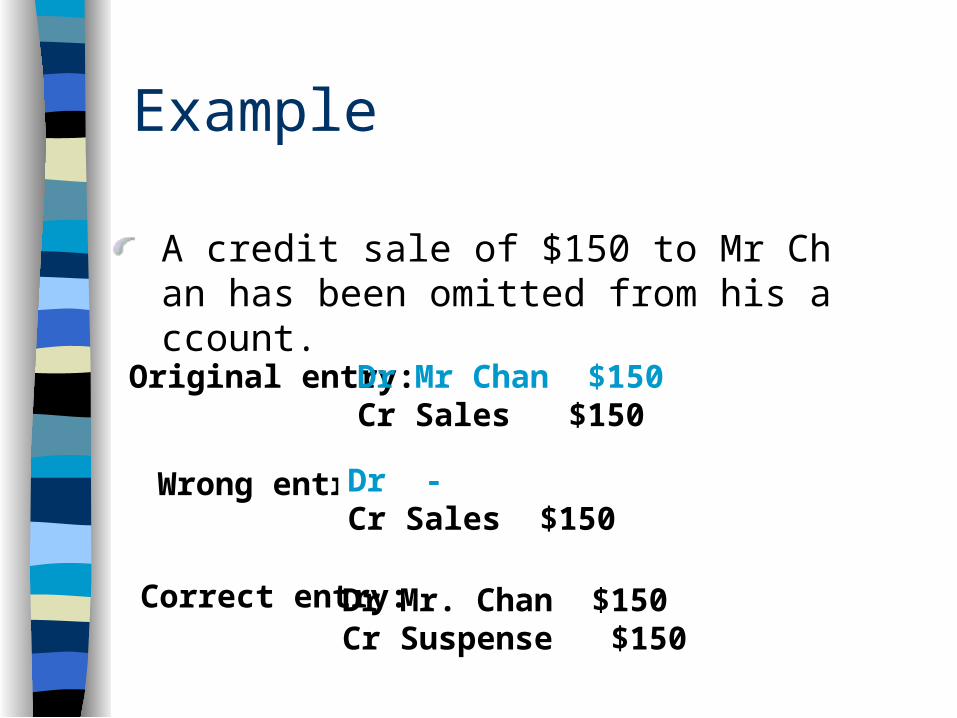

Example

Original entry:

Wrong entry:

Dr Mr Chan $150Cr Sales $150

Dr -Cr Sales $150

A credit sale of $150 to Mr Chan has been omitted from his account.

Correct entry: Dr Mr. Chan $150Cr Suspense $150

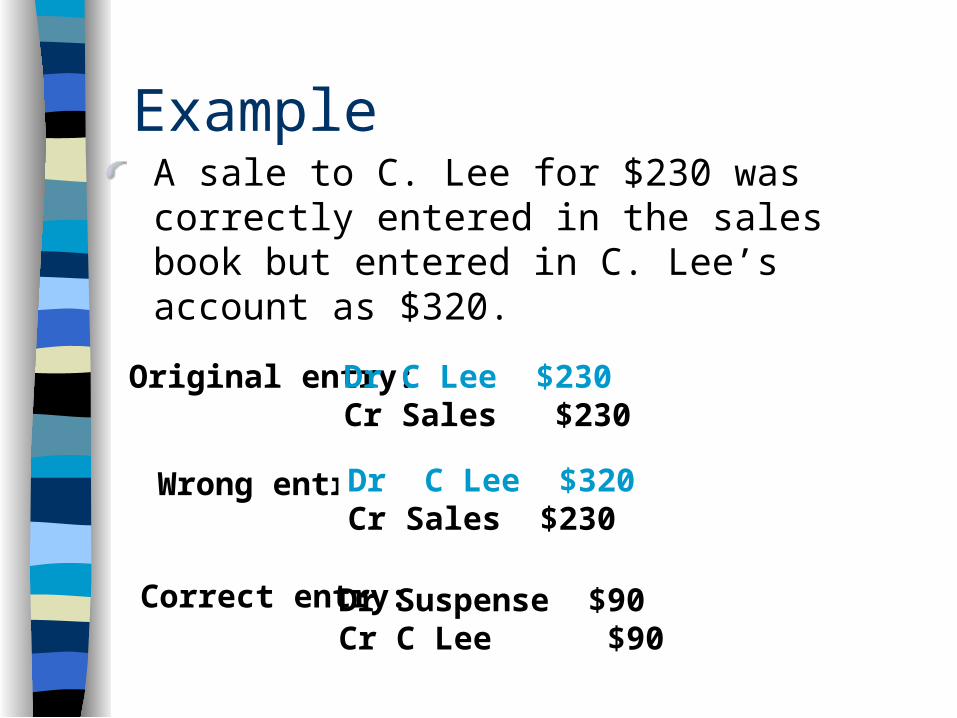

Example

Original entry:

Wrong entry:

Dr C Lee $230Cr Sales $230

Dr C Lee $320Cr Sales $230

Correct entry: Dr Suspense $90Cr C Lee $90

A sale to C. Lee for $230 was correctly entered in the sales book but entered in C. Lee’s account as $320.

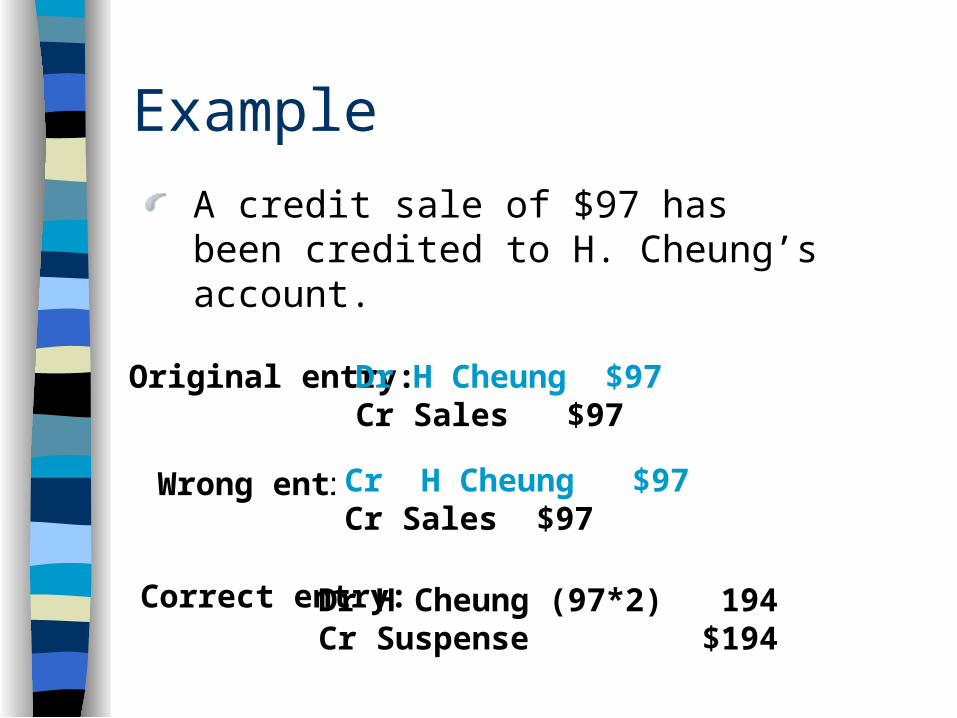

Original entry:

Wrong entry:

Dr H Cheung $97Cr Sales $97

Cr H Cheung $97Cr Sales $97

Correct entry: Dr H Cheung (97*2) 194 Cr Suspense $194

Example

A credit sale of $97 has been credited to H. Cheung’s account.

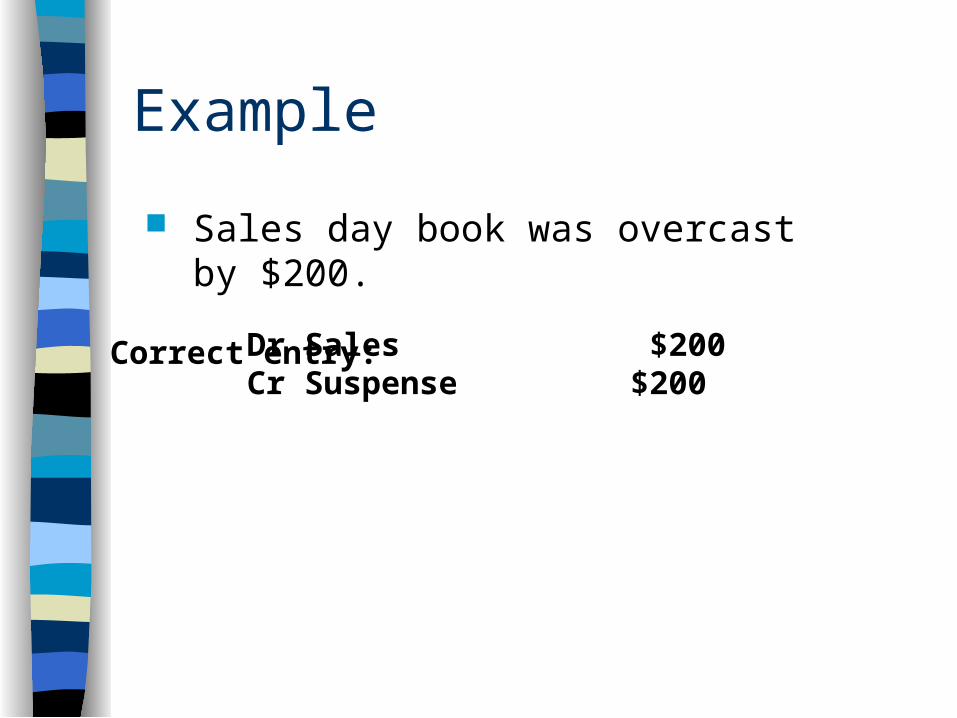

Correct entry: Dr Sales $200 Cr Suspense $200

Sales day book was overcast by $200.

Example

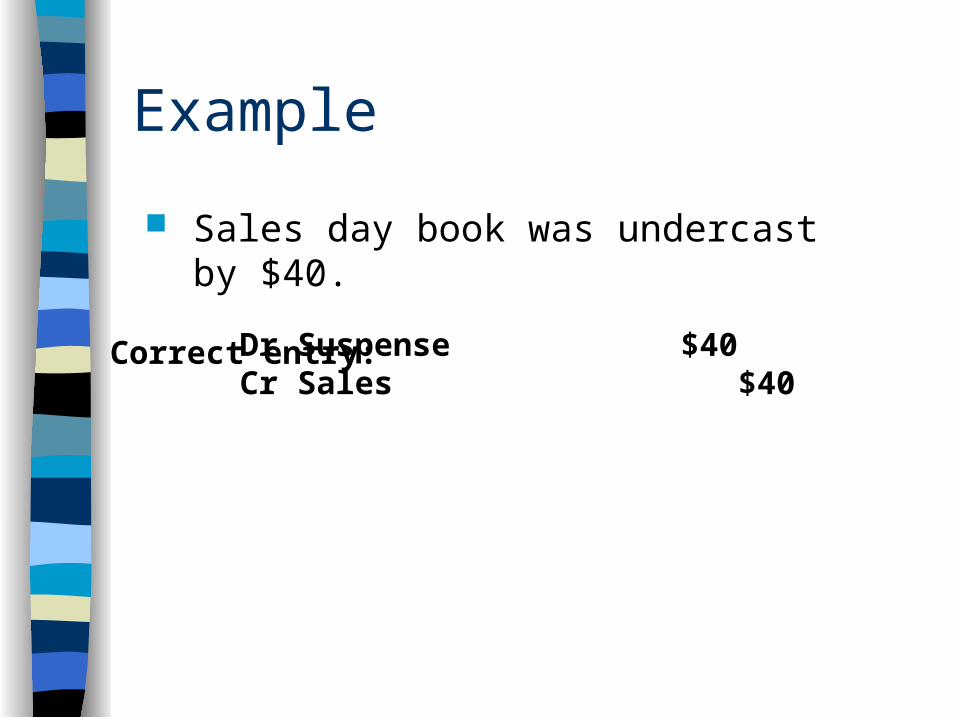

Correct entry: Dr Suspense $40 Cr Sales $40

Sales day book was undercast by $40.

Example

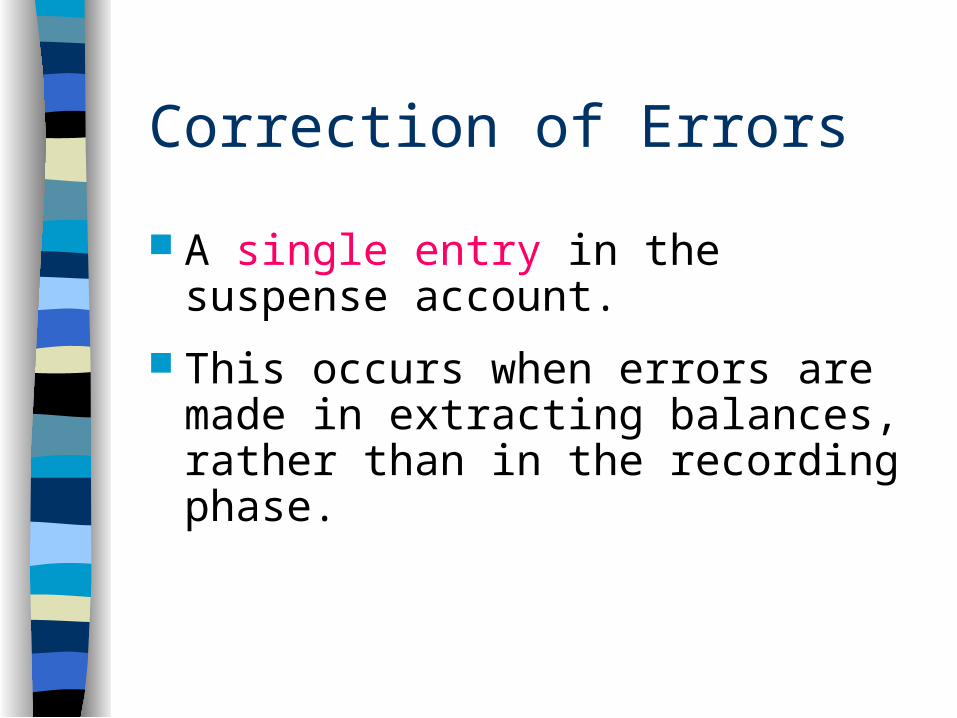

Correction of Errors

A single entry in the suspense account.

This occurs when errors are made in extracting balances, rather than in the recording phase.

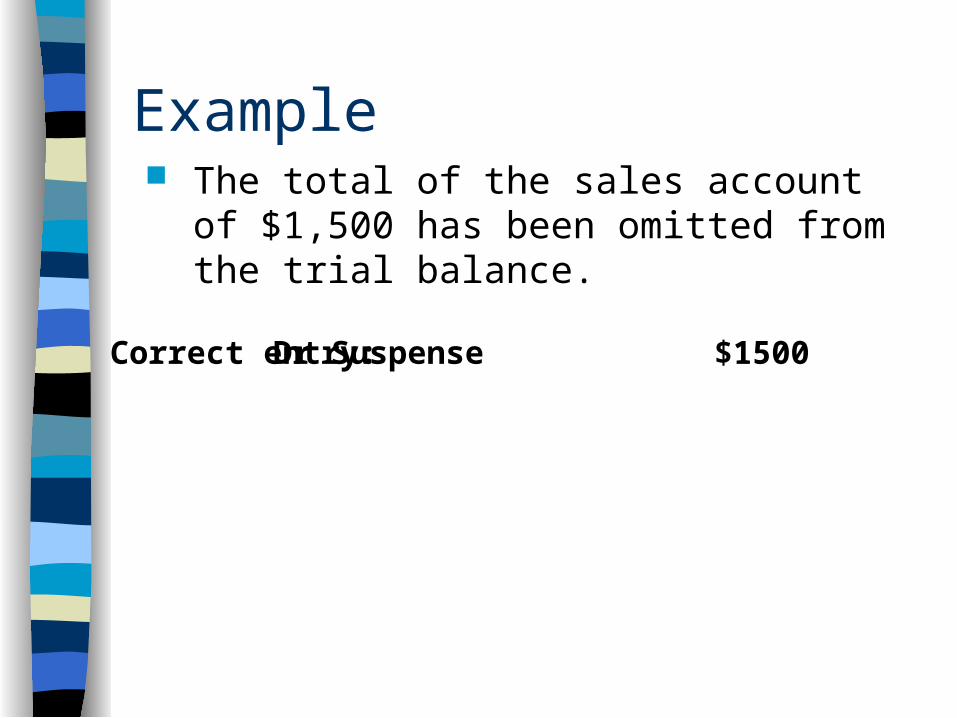

Correct entry: Dr Suspense $1500

Example The total of the sales account of $1,500

has been omitted from the trial balance.

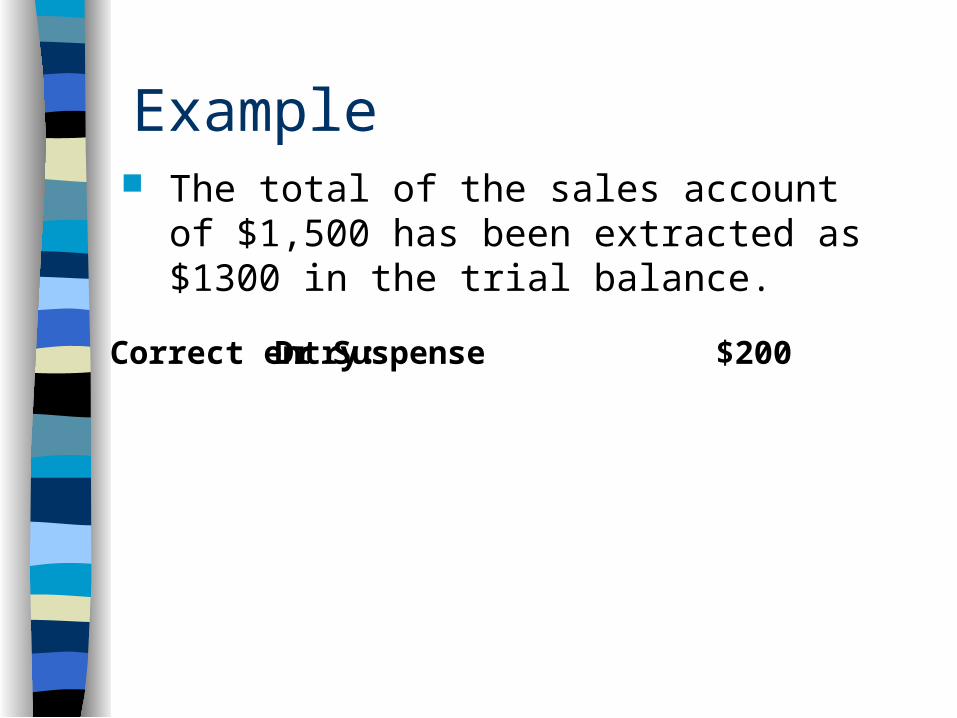

Correct entry: Dr Suspense $200

Example The total of the sales account of $1,500

has been extracted as $1300 in the trial balance.

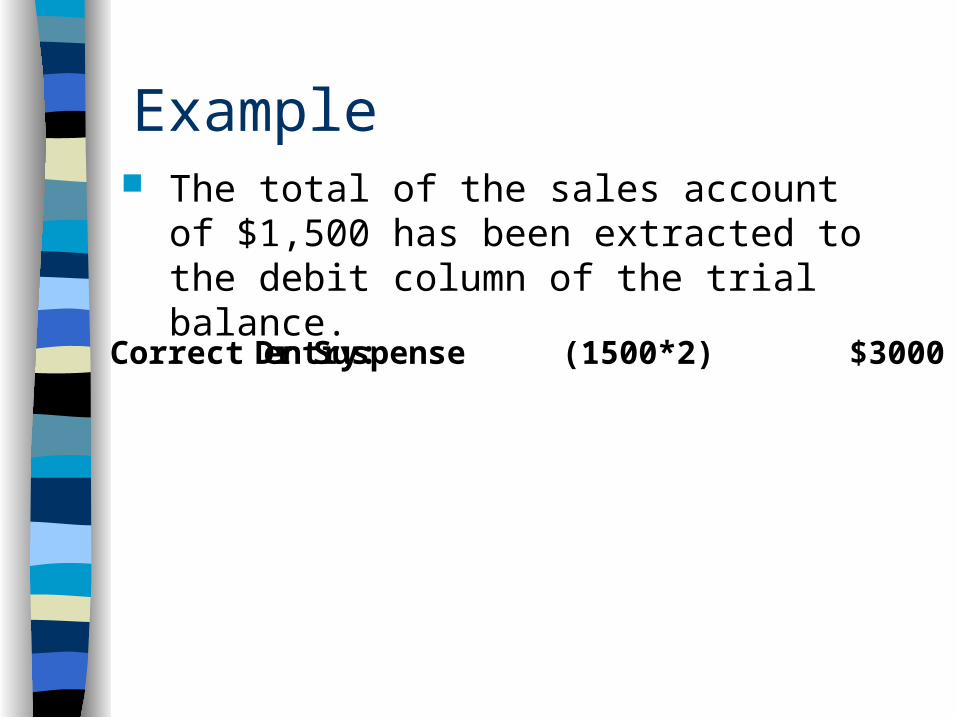

Correct entry: Dr Suspense (1500*2) $3000

Example The total of the sales account of $1,500

has been extracted to the debit column of the trial balance.

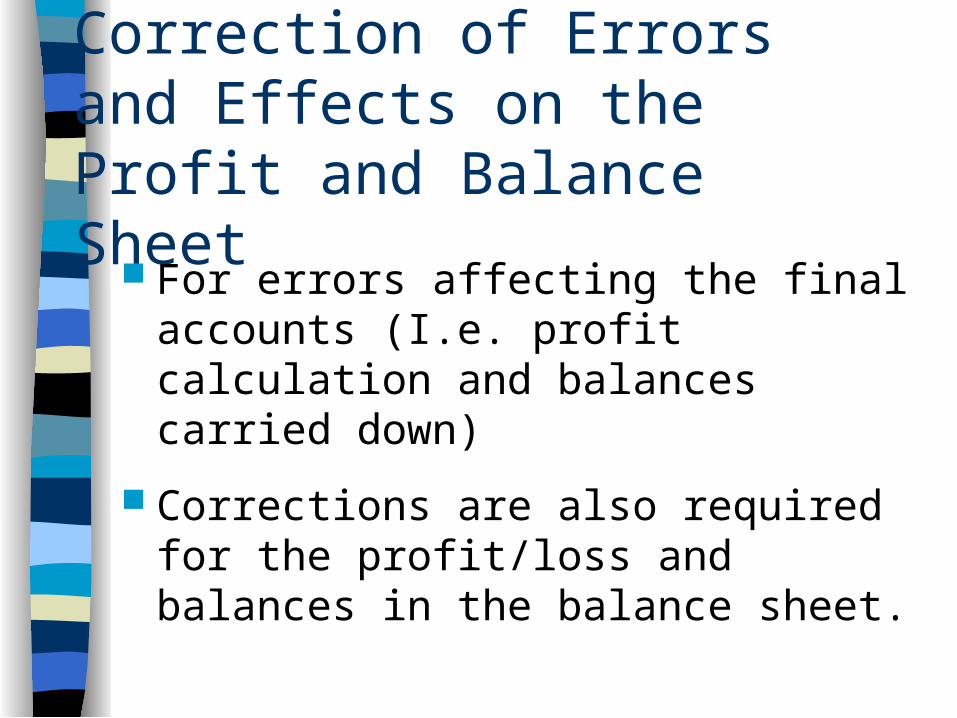

Correction of Errors and Effects on the Profit and Balance Sheet

For errors affecting the final accounts (I.e. profit calculation and balances carried down)

Corrections are also required for the profit/loss and balances in the balance sheet.

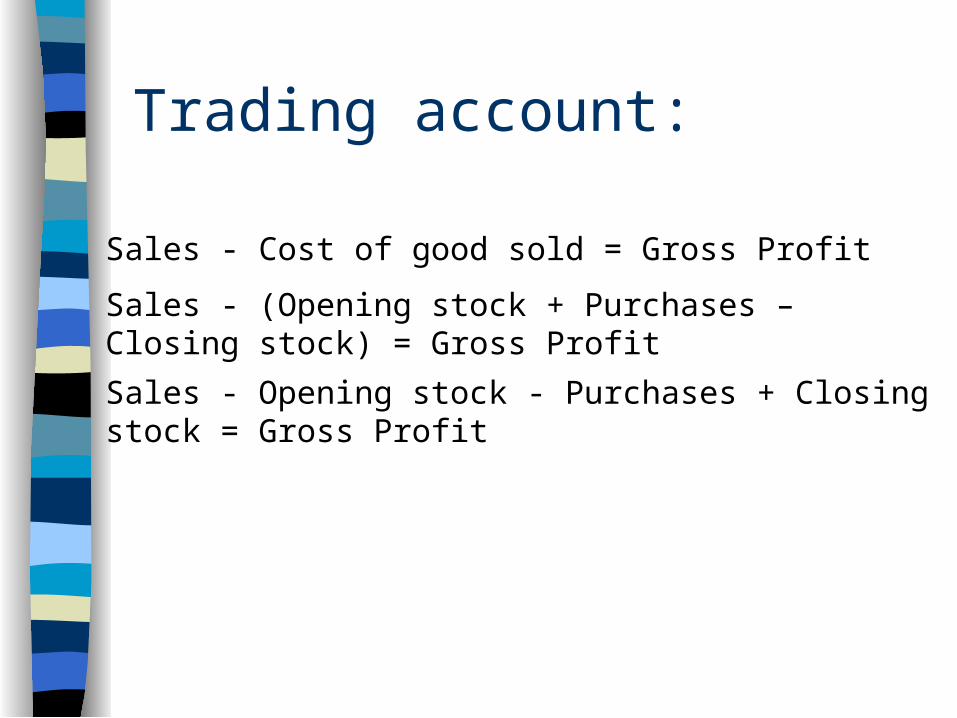

Trading account:

Sales - Cost of good sold = Gross Profit

Sales - (Opening stock + Purchases – Closing stock) = Gross Profit

Sales - Opening stock - Purchases + Closing stock = Gross Profit

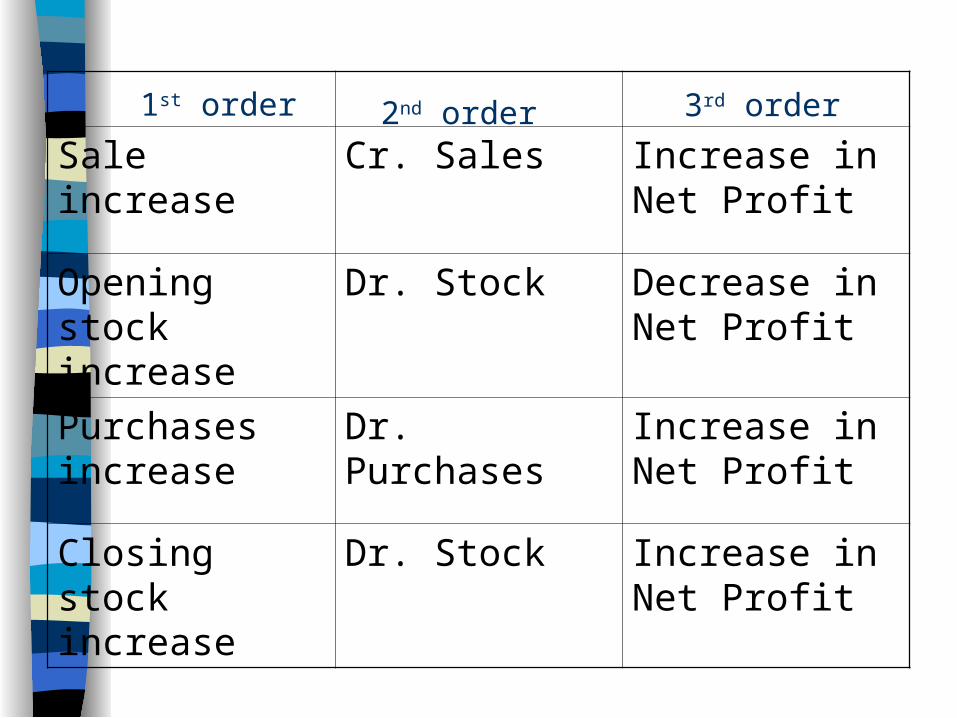

1st order

Sale increase Cr. Sales Increase in Net Profit

Opening stock increase

Dr. Stock Decrease in Net Profit

Purchases increase

Dr. Purchases Increase in Net Profit

Closing stock increase

Dr. Stock Increase in Net Profit

2nd order 3rd order

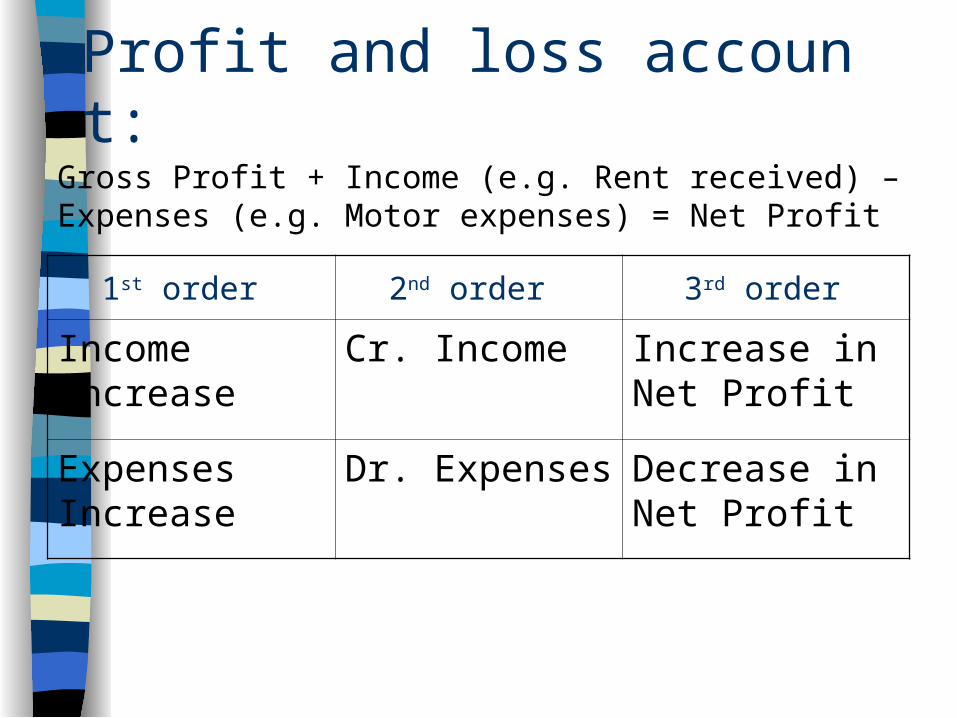

Profit and loss account:

Gross Profit + Income (e.g. Rent received) – Expenses (e.g. Motor expenses) = Net Profit

1st order

Income increase

Cr. Income Increase in Net Profit

Expenses Increase

Dr. Expenses Decrease in Net Profit

2nd order 3rd order

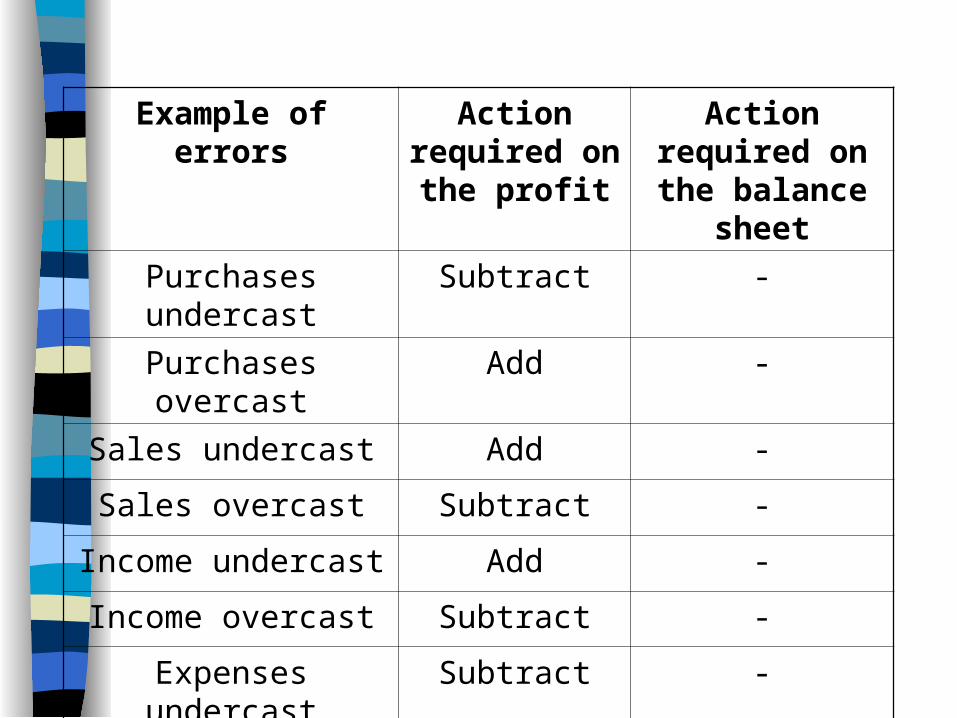

Example of errors Action required on

the profit

Action required on the balance

sheet

Purchases undercast Subtract -

Purchases overcast Add -

Sales undercast Add -

Sales overcast Subtract -

Income undercast Add -

Income overcast Subtract -

Expenses undercast Subtract -

Expenses overcast Add -

Example of errors Action required on

the profit

Action required on the balance

sheet

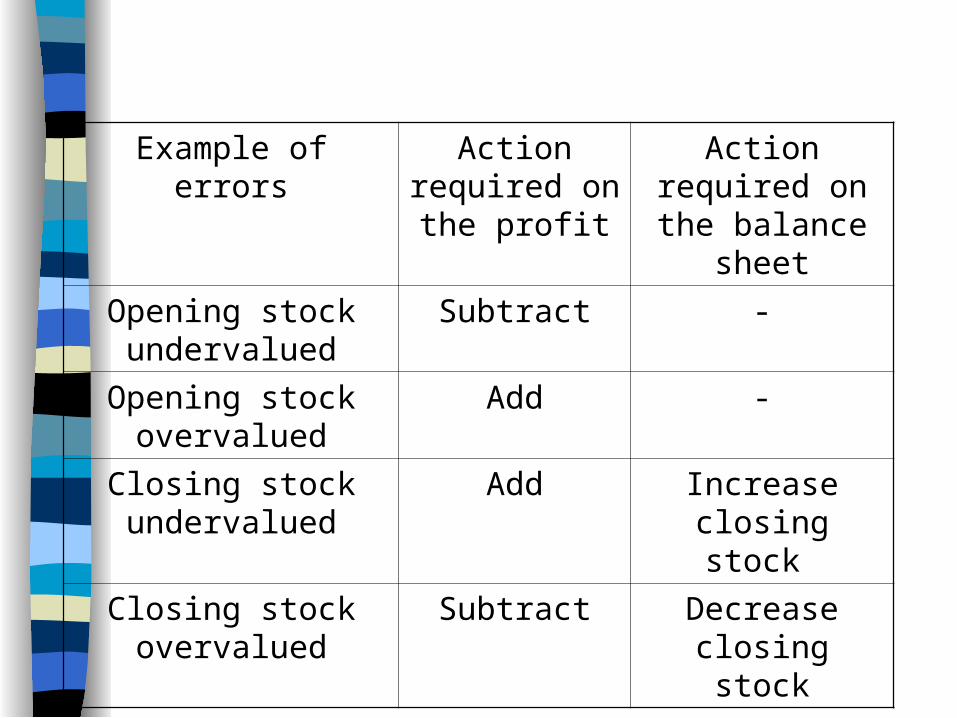

Opening stock undervalued

Subtract -

Opening stock overvalued

Add -

Closing stock undervalued

Add Increase closing stock

Closing stock overvalued

Subtract Decrease closing stock

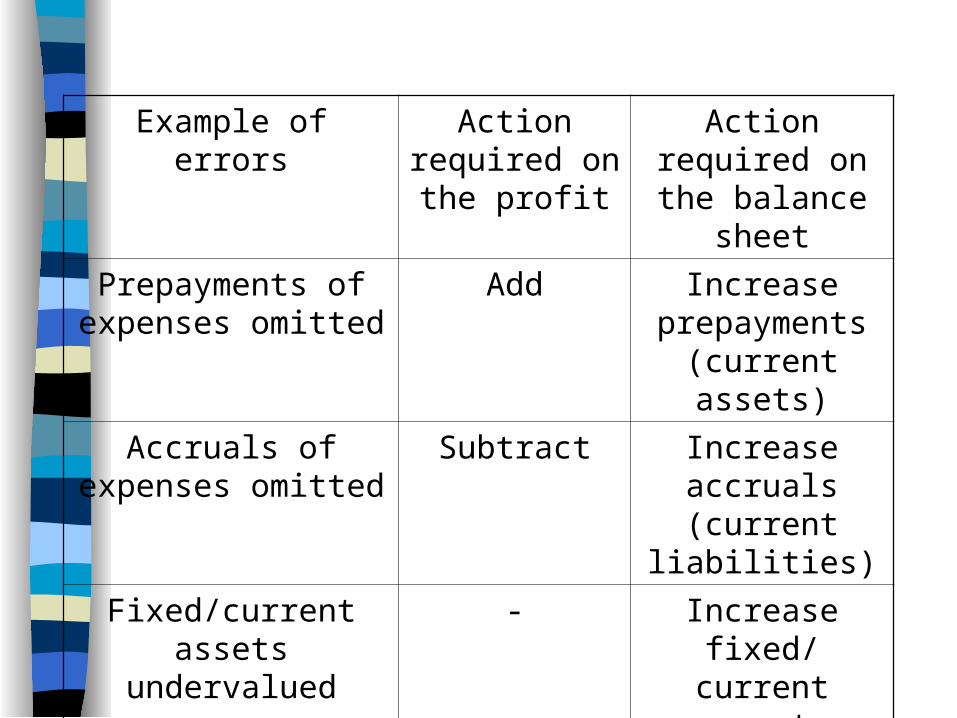

Example of errors Action required on

the profit

Action required on the balance

sheet

Prepayments of expenses omitted

Add Increase prepayments

(current assets)

Accruals of expenses omitted

Subtract Increase accruals (current

liabilities)

Fixed/current assets undervalued

- Increase fixed/ current asset

Liabilities understated - Increase liabilities

![HIGHER SECONDARY – FIRST YEAR · 10. Trial Balance and Rectification of Errors [ 21 Periods ] Definition – Objectives – Advantages – Methods – Format – Sundry debtors](https://static.documents.pub/doc/80x56/60175f2a2ae75d29de6722f2/higher-secondary-a-first-year-10-trial-balance-and-rectification-of-errors-.jpg)