Essays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricingEssays on asset pricing

136

ESSAYS ON ASSET PRICING APPROVED BY SUPERVISING COMMITTEE: ________________________________________ Karan Bhanot, Ph.D., Chair ________________________________________ Donald Lien, Ph.D., Co-Chair ________________________________________ John Wald, Ph.D. ________________________________________ Lalatendu Misra, Ph.D. ________________________________________ Hamid Beladi, Ph.D. Accepted: _________________________________________ Dean, Graduate School

This dissertation is dedicated to my dear husband Emmanuel. Thank you for providing me with constant inspiration and love.

ESSAYS ON ASSET PRICING

by

MARGOT CLAUDETTE QUIJANO, B.A.

DISSERTATION Presented to the Graduate Faculty of

The University of Texas at San Antonio In Partial Fulfillment Of the Requirements

For the Degree of

DOCTOR OF PHILOSOPHY IN BUSINESS ADMINISTRATION

THE UNIVERSITY OF TEXAS AT SAN ANTONIO College of Business

Department of Finance August 2008

iii

ACKNOWLEDGEMENTS

This dissertation could not have been written without Dr. Karan Bhanot, who not only

served as my supervisor, but also encouraged and challenged me throughout my academic

program. He and the other faculty members: Dr. Hamid Beladi, Dr. John Wald, Dr. Donald Lien,

and Dr. Lalatendu Misra, patiently guided me through the dissertation process. I thank them all.

August 2008

iv

ESSAYS ON ASSET PRICING

Margot Claudette Quijano, B.A., Ph.D.

University of Texas at San Antonio, 2008

Supervising Professor: Karan Bhanot, Ph.D.

In this dissertation, I analyze how either political or macroeconomic factors impact asset

prices or returns. In chapter 1, I include three components in the definition of wealth: the market

value of debt, equity and labor income. I show the ratio of consumption-to-wealth, which

includes the value of debt, enhances the predictability of stock returns at different forecast

horizons and provides a plausible measure of time-varying component of risk aversion of the

representative investor.

In the second chapter, I develop a measure of the consumption-to-wealth ratio that

accounts for equity, debt flows, housing wealth and labor income and then relate this measure to

equity returns. I estimated a measure for the change in expectation of the consumption-to-wealth

ratio (u-ccw). This measure proves to contain much more useful information than other

alternative predictors, when it came to forecast stock returns. In addition, I find statistically

significant evidence in favor of including the discounted future consumption growth.

Finally, in the third chapter, I analyze the impact of this uncertainty on the value of F&F

debt and equity as well as the cost of the implicit subsidy by the Federal Government. I show

that, counter to intuition, an increase in the likelihood that the government will not subsidize

these entities may increase the expected cost of the subsidy to the government, by reducing the

market value of these companies. A cap on the value of their investment portfolio is a more

effective mechanism to reduce the risk exposure of the federal government.

v

TABLE OF CONTENTS

Acknowledgements………………………………………………………………………………iii Abstract………………………………………………………………………………………...…iv List of Tables……………………………………………………………………………………viii List of Figures……………………………………………………………………….....................ix Introduction…………………………………………………………………………......................x Chapter 1: Impact of Debt Values on Consumption and Equity Returns………............................1

1.2.1 Including debt in the consumption-to-wealth ratio and its relation to stock returns…..…………………..……………………………4 1.2.2 Consumption-to-wealth ratio and risk aversion…………………………...8

1.3 Data and methodology ………………………………………………………………..9

1.3.2.1 Estimating the relationship between consumption to wealth and equity returns.………….......................................12 1.3.2.2 Estimating conditional risk aversion…………………….……..13 1.3.2.3 Choice of instrumental variables……………………………....16

1.4.1 Consumption-to-Wealth ratio and expected future stock returns……..…17

1.4.1.1 Estimates of consumption to wealth ratio and its relationship with stock returns……………………….......17 1.4.1.2 In-sample performance of cedyt………………………………….18 1.4.1.3 Out-of-sample forecasts………………………………….…..20

vi

1.4.2 Risk aversion coefficients………………………………………………..23 1.4.3 Robustness Check and Monte Carlo estimations………………………...26

Chapter 2: Unexpected Consumption to Wealth ratio and Equity Returns……….……………..41

2.1 Introduction…………………………………………………………………………..41

2.1.1 Literature review…………………………………………………………43 2.2 Theoretical approach…………………………………………………………………44

2.2.1 Housing, debt, equity and human capital wealth and their relation to stock returns…………………..……………………………....45

2.2.1.1 Consumption to wealth ratio…………………………………45 2.2.2 Modifications to the Campbell and Mankiw (1989) consumption to wealth model.………….………………………………………………46

2.2.2.1 Disaggregate total wealth and disaggregate returns to total wealth……………………………………...…47

2.3.1 The relationship between consumption to wealth ratio and equity returns…………………………………...……………………48 2.3.2 Vector Error Correction Model, Vector Autoregressive Model, and the Changes in Expectations of Consumption to Wealth…………....49

2.4.1 DLS estimates for the Consumption-to-Wealth ratio……………………54 2.4.2 VECM, VAR and Changes in Expectations of Consumption to Wealth Ratio..……………...………………………………….………55

2.4.3 In-sample and Out-of-sample performance……………………………...56

2.5 Conclusions………………………………………………………………..................62 Chapter 3: Will Pulling Out the Rug Help? Uncertainty about Fannie and Freddie’s Federal Guarantee and the Cost of the Subsidy…………………….............................71

3.1 Introduction…………………………………………………………………………..71 3.2 The model……………………………………………………………………………79

3.2.1 Value of the business when there is no debt……………………………..80 3.2.2 Uncertainty in the guarantee and the role of debt………………………..83

3.2.2.1 Value of F&F when the costs and benefits of debt are included…..…………….………………………..84 3.2.2.2 The Value of Debt and Equity of F&F…………....................86

3.3 Impact of uncertainty about the federal guarantee…………………………………...88

3.3.1 Firm value with an uncertain guarantee………………………………….88 3.3.2 Debt values and uncertainty in the guarantee……………........................90

3.4 Uncertainty and cost of the subsidy…...……………………………………………..92 3.5 Conclusions………………………………………………………………..................95

Figure 1.5 CEDY and Business Cycles................................................................................40

Figure 2.1 Quarterly Real Consumption Growth Rate.........................................................69

Figure 2.2 Welch and Goyal Performance Tests..................................................................70

Figure 3.1 Sample Paths for Possible Asset Values.............................................................99

Figure 3.2 Firm Value with Uncertainty about the Subsidy...............................................100

Figure 3.3 Debt Firm Value with Uncertainty about the Subsidy......................................101

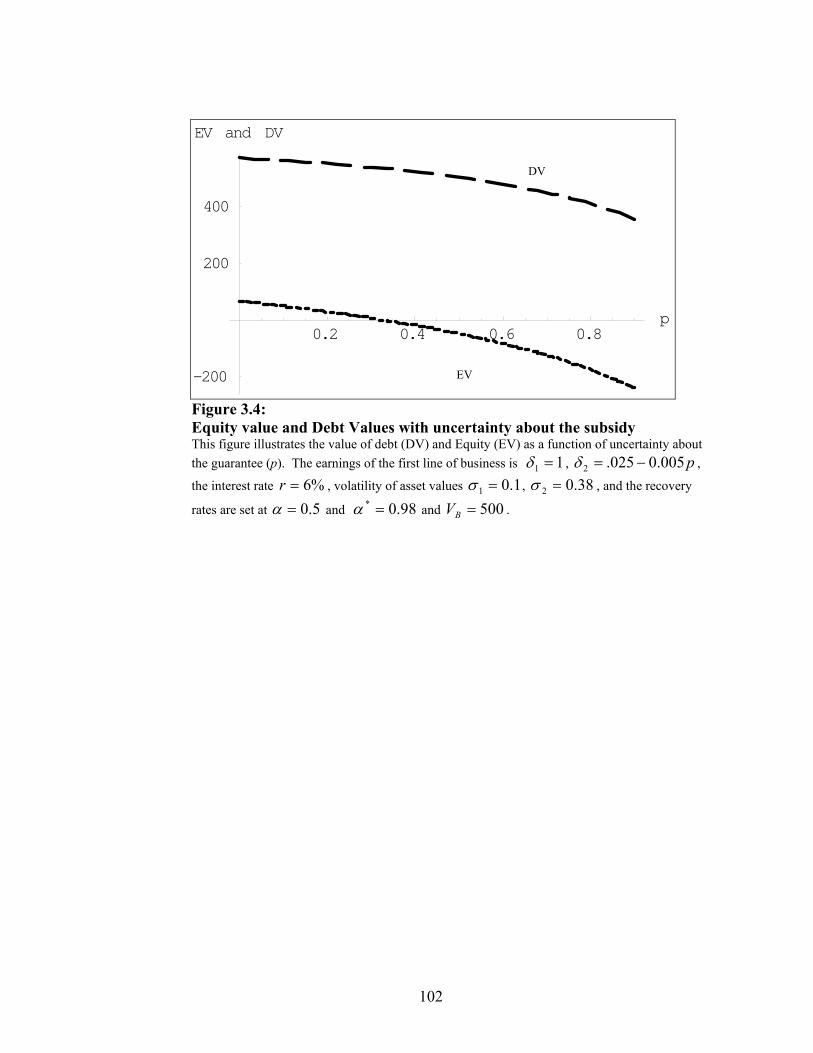

Figure 3.4 Equity Value and Debt Value with Uncertainty about the Subsidy..................102

x

INTRODUCTION

My dissertation consists of three chapters: 1) “Impact of Debt Flows on Consumption and

Equity Returns”, 2) “Unexpected Consumption to Wealth ratio and Equity Returns” and 3) “Will

Pulling Out the Rug Help? Uncertainty about Fannie and Freddie’s Federal Guarantee and the

Cost of the Subsidy”.

The main idea of this dissertation is to analyze how either political or macroeconomic

factors impact asset prices and returns. The first chapter explores the importance of debt flows in

explaining equity returns. In the second chapter I investigate how the composition of wealth and

the changes in expectations of consumption to wealth ratio affect equity returns. The third

chapter focuses on how frictions created by government charters impact asset prices of

Government Sponsored Enterprises (GSEs).

In first chapter, I study the importance of debt in an agent’s consumption and wealth, and

then evaluate its relationship with equity returns. I include three components in individual

wealth: the market value of debt, equity and labor income. Using financial and real data for the

period 1959 to 2006 obtained from the Federal Reserve, coupled with aggregate interest rate

payments from the Flow of Funds data, I show that the inclusion of debt in the ratio of

consumption-to-wealth enhances the predictability of stock returns at different forecast horizons

and provides a plausible measure of time-varying component of risk aversion of the

representative investor. Overall, the evidence points to the importance of considering the impact

of debt when evaluating the relationship between consumption and equity returns.

Chapter 2 provides evidence on the importance of considering four components of wealth

when explaining the relationship between consumption, wealth and equity returns. I develop a

measure of the consumption-to-wealth ratio that accounts for equity, debt flows, housing wealth

xi

and labor income and then relate this measure to equity returns. I estimated a measure for the

change in expectation of the consumption-to-wealth ratio (u-ccw). This measure proves to

contain much more useful information than other alternative predictors, when it came to forecast

stock returns. Using Campbell and Yogo (2006) tests and Goyal and Welch (2003, 2006) plots,

the predictive power of u-ccwt is shown to be superior to alternative models. In addition, I find

statistically significant evidence in favor of including the discounted future consumption growth.

Lastly, in the third chapter, I empirically find that a higher probability that the

government will not subsidize these GSEs may increase the expected cost of the implicit subsidy

to the government. Comments by the Federal Reserve Chairman have created concerns about

whether the government would protect bondholders in the event of default by Fannie Mae or

Freddie Mac (F&F). I analyze the impact of this uncertainty on the value of F&F debt and equity

as well as the cost of the implicit subsidy by the Federal Government. Uncertainty about the

Federal Guarantee increases expected losses to debt holders in bankruptcy, thereby increasing

the cost of new funds for Fannie and Freddie when debt is used to finance a part of the firm.

Also, uncertainty about the guarantee reduces the profitability of their asset holdings (mortgage

portfolios) by increasing the costs of managing and hedging these portfolios. I show that, counter

to intuition, an increase in the likelihood that the government will not subsidize these entities

may increase the expected cost of the subsidy to the government. Thus, public demonstrations

from the government about their little financial support for GSEs may in fact be self-defeating. A

cap on the value of their investment portfolio is a more effective mechanism to reduce the risk

exposure of the federal government.

xii

Overall, this evidence points to the importance of considering the four main components

of wealth, consumption growth, and change in expectations of consumption-to-wealth ratio when

analyzing expected equity returns.

1

CHAPTER 1: IMPACT OF DEBT VALUE ON CONSUMPTION,

WEALTH AND EQUITY RETURNS

1.1 Introduction

The finance literature has attempted to take theoretical models of consumption based

asset pricing to equity market data without much success. Most of the empirical evidence on

explaining this relationship between consumption and equity returns is built on the assumption

that equity returns correspond to the entire claim on the existing stock of capital (Rouwenhorst

(1995)). To my knowledge there is no research paper that empirically accounts for the market

value of debt implicit in consumption to wealth ratios and its influence on equity returns. I

segregate agent wealth into market value of debt, equity and labor income and test the impact of

including debt in the relation between consumption to wealth ratio and equity returns.

In related work, theory has tried to resolve the inconsistency between the implications of

extant models for the relationship between consumption and asset prices by modifying

assumptions about agent utility functions (Epstein and Zin (1989, 1991)), via behavioral

assumptions (Constantinides (1990), Campbell and Cochrane (1999)) and by including

transaction costs (Constantinides et. al. (2002)). Other studies focus on the impact of taxes and

regulatory systems which may affect equity returns (McGrattan and Prescott (2000, 2001)). I

contribute to this area of research from an empirical standpoint by modifying the measure of

wealth via including debt values in this setting.

Other empirical work has examined the relationship between aggregate equity returns and

debt using asset pricing models. Empirical evidence supports the idea that business cycles may

affect equity returns as well as changes in default spreads (e.g., Chen, Roll, and Ross (1986),

2

Keim and Stambaugh (1986), Campbell and Shiller (1988), Fama and French (1989), Chen

(1991) and Ferson and Harvey (1991)). Jagannathan and Wang (1996) also showed how spreads

between junk bonds and risk free securities explain movements of stock returns. Vassalou and

Xing (2004) assess the effect of default risk on equity returns using the Merton (1974) model for

measuring default risk. Vassalou, Chen and Zhou (2005) show that the inclusion of default and

liquidity variables in Merton’s asset pricing model improves its performance, but the

improvement is largely due to the inclusion of the default variable. In addition to these studies

Zhang (1997) and Alvarez and Jermann (2000) have studied the impact of default risk on asset

pricing using models of endogenous solvency constraints. Chang and Sundaresan (2005) show

that equity premium depends on two things: the covariance of consumption with wealth and the

covariance of consumption with the amount of leverage. These articles look at the relationship

between debt and equity returns from different perspectives. However, the economic

relationship between the ratio of consumption–to–wealth, which includes debt values, and equity

returns has not been examined.

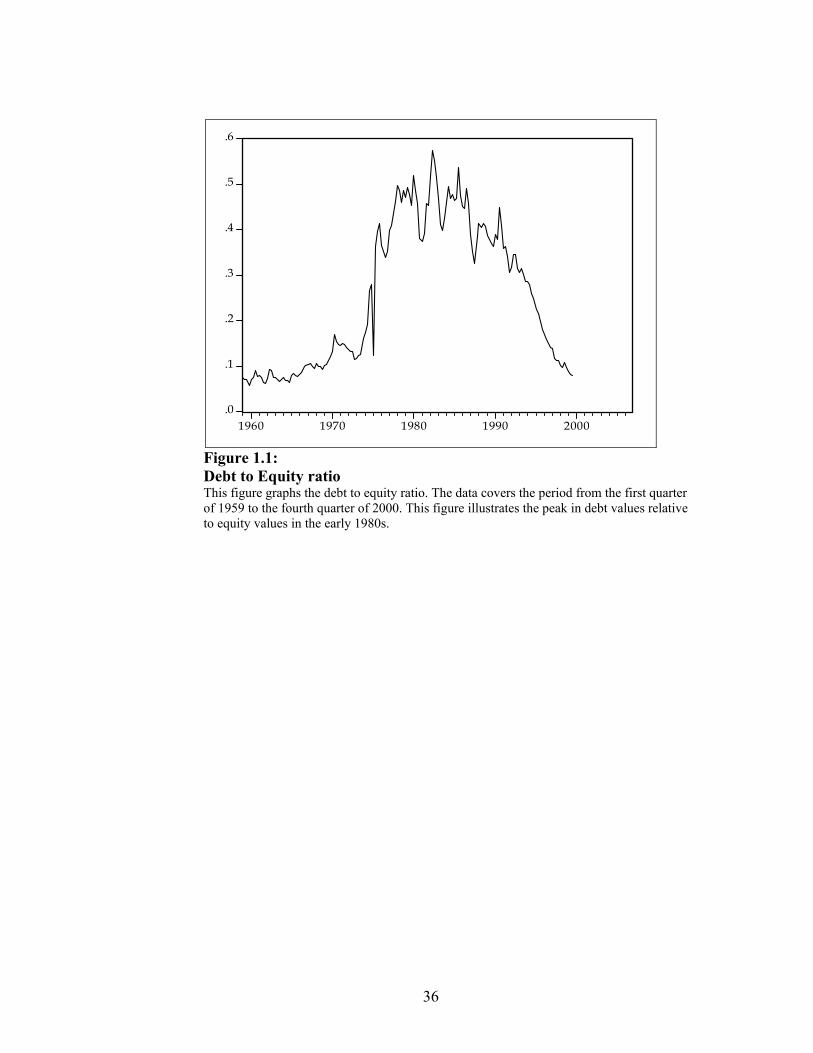

Figure 1.1 shows that market values of corporate debt compared to equity value were low

and stable before the year 1975. It is not surprising that the pioneering works on asset pricing

(Lucas (1978), Breeden (1979)) did not give a relevant role to payouts from debt as these were

not very volatile and were relatively less important before the 1980s. It was not until late 1970s

that debt values started to increase relative to equity values and peaked in the early 1980s1. Debt

values and its payouts have been more volatile and have become a significant part of the

economy.

I assess the relevance of debt in explaining asset returns in this article via its role in

wealth. To achieve my objective, I provide a simple framework that links consumption with the 1 Hall (2001) documents this incident extensively.

3

market values of debt, equity and human capital. The framework relies on earlier work by

Campbell and Mankiw (1989), Lettau and Ludvigson (2001a) and Duffee (2005). I assume, in

addition, that agent wealth is derived from debt payments plus the traditional sources of income

– labor and equity. I relate this newly computed consumption-to-wealth ratio with future asset

returns. I first compute the long term trend in the ratio of consumption–to–wealth, and then

evaluate deviations from this long term trend. I argue that deviations from the long term ratio

explain future equity returns better when debt values are included in the calculations of wealth.

For the empirical tests, I use quarterly observations on financial time-series for the United

States over the period of 1959 to 2006. This data is compiled by CRSP, the Federal Reserve, the

Census Bureau, and the Bureau of Economic Analysis. The value of outstanding equity is equal

to the total market value of NYSE-AMEX-NASDAQ stocks obtained from CRSP database.

Using the Flow of Funds Data, I infer the market value of leverage (explained in section 1.3).

My results show that the broader measure of consumption-to-wealth ratio provides

statistically significant results for future equity returns for different forecast horizons that are

more significant when compared to existing approaches. I also find significant evidence in favor

of a time-varying component in the risk aversion of investors. When relating equity returns to

consumption, the coefficient for the ratio of consumption–to–wealth has the appropriate sign and

supports the notion that this measure is counter to the business cycle, similar to expected equity

returns (Cochrane (2005)). For high values of consumption-to-wealth ratio and expected equity

returns, the price of consumption risk must also be high. Overall, this evidence points to the

importance of considering a broader definition of wealth when evaluating its relationship with

equity returns.

4

As a robustness check for my results in time-variation in risk aversion, I perform two

Monte Carlo experiments; in the first case I check for the correct inference from the GMM risk

aversion estimates in a finite sample, while in the second case I check for the consumption-to-

wealth ratio’s ability to capture a time-varying component in risk aversion that is independent of

the consumption-to-wealth ratio.

The article is organized as follows. Section 1.2 gives the theoretical background.

Section 1.3 describes the data and methodology and Section 1.4 contains empirical findings and

robustness tests. Section 1.5 concludes.

1.2. Theoretical approach

My objective is to include debt flows and the market value of debt into the representative

agent’s intertemporal decision equation, when the agent decides between current and future

consumption. I adapt the framework of Campbell and Mankiw (1989) and add debt to the mix.

This setting allows me to determine the role that debt plays in consumption, and its relationship

with equity returns. In section 1.2.2, I show how a time-varying risk aversion coefficient is

estimated using the consumption-to-wealth ratio with debt values.

1.2.1 Including debt in the consumption-to-wealth ratio and its relation to stock

returns

My hypothesis is that the correlation between the ratio of consumption-to-wealth and

future equity returns is higher when the market value of debt is included in the computation of

wealth. Consider the constraint faced by an agent who decides between allocating his current

wealth, tW , to current consumption, tC , while investing the balance. Assume that 1, +twR is the

5

return on wealth that is invested. The equation for a period by period budget constraint can

therefore be written as:

))(1( 1,1 tttwt CWRW −+= ++ (1)

My primary contribution is that I explicitly account for market value of debt in the

definition of wealth. In particular, rttt DEHW ++= , where the first element corresponds to

labor income and the next two elements represent the market value of equity and debt,

respectively. Lettau and Ludvigson (2001a) follow a similar approach but exclude debt values in

their measures. In the spirit of their framework, I proxy for human capital by computing labor

income as wages and salaries plus transfer payments minus personal contributions for social

insurance minus taxes.

To relate the ratio of consumption-to-wealth with equity returns, I divide equation (1) by

tW . Using logs and then manipulating the result, I arrive at the following equation, where lower

cased letters represent log of the variables:

))exp(1log(1,1 tttwt wcrw −−+=Δ ++ (2)

Using a first order Taylor expansion of ))exp(1log( tt wc −− around a long run average ratio of

consumption to wealth “ )( wc − ” gives (shown in Campbell and Mankiw (1989)):

))(/11())exp(1log( tttt wckwc −−+≈−− ρ (3)

Substituting equation (3) into (2) gives:

))(/11(1,1 tttwt wcrkw −−++≈Δ ++ ρ (4)

where )exp(1 wc −−=ρ and can be interpreted as the average ratio of invested wealth to total

wealth,W

CW − , and ( ) ( )ρρρ −−−= 1log/11)log(k is a constant with no relevance in this

6

article. Equation (4) states that the growth in wealth, 1+Δ tw , is in function of a constant k, log of

wealth returns, and the log of consumption-to-wealth ratio. Campbell and Mankiw (1989) show

that after rearranging terms in equation (4) and by solving forward gives the consumption-to-

wealth ratio, tt wc − , at time t:

∑∞

= ++ −+Δ−=−1 , )1/()(

i ititwi

tt kcrwc ρρρ (5)

Equation (5) is the log linear version of an infinite horizon budget constraint. It holds either ex-

ante or ex-post. This implies, for example, that a high consumption wealth ratio (left hand side

of equation (5)) would require either a low consumption growth rate, itc +Δ , or high returns on

wealth, itwr +, .

Equation (5) is the starting point of my analysis. I segregate net wealth on the left hand

side into its components equity ( te ), debt ( td ) and labor income ( ty ). These wealth components

are weighted by their respective percentage shares in total wealth, θ (following Lettau and

Ludvigson (2001a). The resulting left-hand side for the log of consumption-to-wealth ratio is:

tttt ydec 321 θθθ −−− . The right-hand side needs to be decomposed in three different returns

and a consumption growth term. Since wealth is segregated into equity, debt and labor income,

then returns on wealth should be a linear combination of returns on equity, debt and labor

income. Thus, I have that log of returns on aggregate wealth is an approximation of the sum of

log returns on wealth components times their respective wealth shares2,

tytdtetw rrrr ,3,2,1, θθθ ++≈ (6)

Taking expectations gives the following equation that relates consumption and wealth

components to the returns on wealth factors,

2 Using first order Taylor expansions for log(

tyttdttet rrr ,,3,,2,,1 θθθ ++ ) .

7

∑∞

= ++++ +Δ−++=−−−1 ,3,2,1321 )(

i itityitditei

ttttt crrrpEydec ψθθθθθθ (7)

The left-hand side of equation (7) is simply the log of consumption minus the log of equity, debt

and labor income, respectively. The right-hand side variables are, sequentially, returns to equity,

debt and labor income, along with consumption growth and a constant,ψ . The constant

represents the value of the consumption-to-wealth ratio in a steady state, when returns and

consumption growth are small. Deviations on expectations about future returns and consumption

growth are estimated from known consumption and wealth patterns.

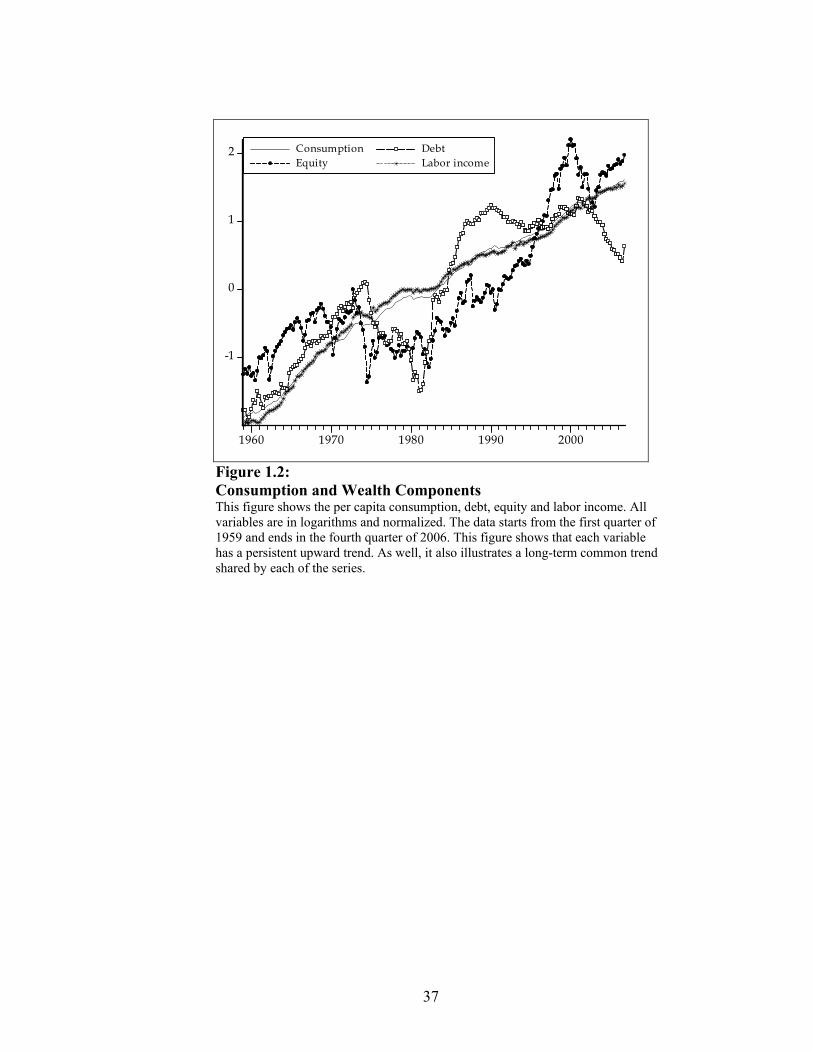

Figure 1.2 shows how the different wealth components and consumption vary through

time. However, I assume that a linear combination of these variables is stable; hence I argue that

these variables are cointegrated and I need to estimate this long-term common trend and use

deviations from this trend to analyze revisions on future equity returns. The common trend

deviation of ct, et, dt, and yt is denoted cedy. I obtain, cedy, by equating it to the residuals from

the cointegrating equation that estimates the long term relation between consumption and wealth

components. In other words, cedy represents the revisions to the long term consumption-to-

wealth ratio. If revisions to expected discounted future consumption growth and returns to labor

income and to debt are small, then cedy will mostly reflect changes to expected equity returns.

Hypothesis 1: cedy reflects revisions to expected future equity returns.

A natural examination for hypothesis 1 is to test the importance of cedy on the expected

equity returns (this test is carried out in section 1.4.1). Lettau and Ludvigson (2001a) obtain a

similar expression to equation (7), however they do not account separately for the components of

asset holdings (they denoted their long term trend deviation of consumption, assets and human

8

capital as cay – where ct, at and yt represent consumption, asset holdings and labor income,

respectively). The authors proxy for asset holdings by using the net household worth series

provided by the Federal Reserve Board. This measure is noisy since the Federal Reserve

estimates this household worth series as a residual; that is, for any particular asset, the Federal

Reserve estimates first the participation of other economic agents and then attributes the rest to

households3. I empirically show that accounting separately and explicitly for debt and equity

flows in asset wealth improves the correlation between stock return patterns and the

consumption-to-wealth ratio. This implies that cedy may be a better proxy for market

expectations of future stock returns than other measures such as cay.

1.2.2 Consumption-to-wealth ratio and risk aversion

As noted in the previous section, the consumption to wealth ratio may provide important

information about future asset returns. Then, it would be reasonable to assume that this

consumption to wealth ratio may also help capture the disposition of any particular investor to

bear risk.

Hypothesis 2: The conditional risk aversion coefficient is time varying and cedy can capture this variation.

The theoretical background for my hypothesis is gleaned from Lucas (1978),

Constantinides (1990) and Duffee (2005). The representative household consumes from different

sources of wealth and orders its preferences over alternate expected consumption paths. If

3 The Federal Reserve also bundles households and nonprofit organizations together, so the net worth series is actually a measure of household and nonprofit organizations total wealth.

9

returns follow a lognormal distribution and a risk-less asset is present, Campbell, Lo and

MacKinlay (1997) show that,

),(cov)(var21

11111 +++++ Δ=+ tttttttt cerererE α (8)

where ert+1 is the excess rate of return of the risky asset over a riskless asset (excess returns

onwards), ),(cov 11 ++ Δ ttt cer is the conditional covariance –conditional on a set of information at

time t –between the one-period-ahead excess return on the risky asset and the one period change

in consumption in time t+1; and, 1+tα is the state-dependent sensitivity of expected excess

returns to the conditional covariance. In sum, equation (8) states that excess returns are

determined by a coefficient of risk aversion, also called price per unit of consumption risk, times

the expected covariance between excess returns and consumption growth. Because excess

returns are related to the measure of consumption to wealth ratio, I hypothesize that the latter

captures the time variation in risk aversion.

1.3. Data and methodology

1.3.1 Data

I need four primary ingredients to conduct my empirical tests- aggregate consumption,

the stock of debt, labor income and the stock of equity as well as returns to each component. I

use quarterly observations on the financial time-series for the United States over the period of

1959 to 2006. This information is compiled by CRSP, the Federal Reserve, the Census Bureau

and the Bureau of Economic Analysis databases.

I also computed the excess returns and returns to equity using the value-weighted CRSP

Index (CRSP-VW), which includes the NYSE, AMEX and NASDAQ stocks, and the S&P 500

10

index. The excess returns were calculated as the difference between the equity returns and

returns to a risk-less asset. The risk-less asset used in this article corresponds to the three month

Treasury bill.

For comparison purposes with cedy, I used Lettau and Ludvigson’s (2001a) consumption

to wealth measure (cay), dividend to price ratio , dividend to earning ratio, term structure of

interest rates, and short term interest rates as alternative predictive measures of equity returns.

The term structure of interest rates was calculated as the spread between the 10 year Treasury

bond yield and the three month Treasury bill yield. The dividend ratios were obtained from

Professor Shiller’s website (http://www.econ.yale.edu/~shiller/data/ie_data.xls). The Lettau and

Ludvigson’s consumption to wealth measure, cay, was calculated following the procedure stated

in the authors’ (2001a) paper. The short term interest measure is simply the three month

Treasury bill minus its previous year average; Campbell (1987) called this measure a

stochastically detrended interest rate.

The 10 year Treasury bond yields and three-month Treasury bill yields were obtained

from the Federal Reserve database. All data is in real terms and was deflated by the PCE chain-

type price deflator, 1992 = 100. Data on consumption, equity, debt and income are in per capita

terms, the estimates for population were obtained from the Census Bureau. Table 1.1 reports

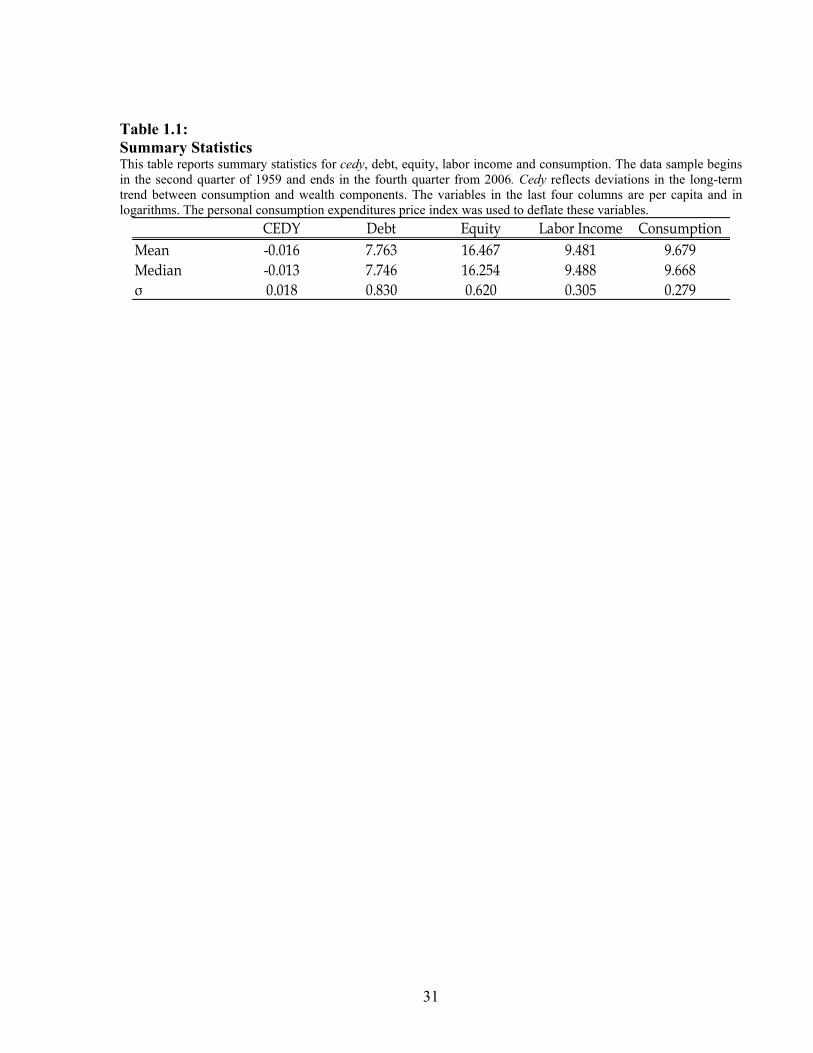

summary statistics for cedy, consumption, debt, equity and labor income per capita. Debt has the

highest volatility followed by equity compared to the rest of the variables. This suggests that

volatility in cedy may be a result of movements in debt or equity. I now describe in more detail

the manner in which I construct these variables.

As in Lettau and Ludvigson (2001a), labor income is calculated as “wages and salaries

plus transfer payments plus other labor income minus personal contributions for social insurance

11

minus taxes. Taxes are defined as (wages and salaries/ (wages and salaries + proprietors income

with IVA and Ccadj + rental income + personal dividends + personal interest income)) times

(personal tax and non-tax payments), where IVA is inventory evaluation and Ccadj is capital

consumption adjustments” (p.845). As an alternative, I also use Jagannathan and Wang (1996)

definition of labor income, which equals the growth in total personal, per capita income less

dividend payments from the National Income and Product Accounts4. All labor income

components are published by the Bureau of Economic Analysis.

Equity value, debt value and other information needed to test my hypotheses are

calculated as follows. The stock of outstanding equity is equal to the total market value of

NYSE-AMEX-NASDAQ stocks obtained from CRSP database. Following Hall (2001), market

value of debt is computed as the sum of financial liabilities (excluding equity) and total market

value minus total book value of bonds and financial assets. Book value of bonds (corporate and

tax exempt), financial assets and financial liabilities series were obtained from the Federal

Reserve Flow of Funds accounts. Total book and market values of bonds are adjusted for the

value of tax exempt securities. The market value of bonds is computed as the present value of

future coupons and principal payments on the outstanding assigned bond issues. To estimate the

present value of coupons and repayments, I need a corporate interest rate coupled with the

assumption that newly issued bonds have coupons as if they were non-callable ten-year bonds.

The net increase in the book value of bonds is added to the principal repayments from bonds

issued previously in order to compute the value of newly issued bonds. Then, to work out the

present value of bonds after they were issued, an interest rate for ten-year corporate bonds was

calculated as follows. First, I obtained the spread between Moody’s long-term corporate bonds

4 Results are qualitatively similar when compared to Lettau and Ludvigson’s measure of labor income.

12

with a BAA grade and the long-term Treasury Constant Maturity Composite for the quarterly

period from 1959 until 2000. I use the spread between BAA Moody’s long term corporate bonds

and twenty-year Treasury bonds after the year 2000, because the long-term Treasury Constant

Maturity was discontinued. After deriving the BAA spreads, I added these to the 10 year

Treasury bond yields to obtain the interest rate for 10 year corporate bonds.

Consumption data is collected from the Bureau of Economic Analysis. Total

consumption used for this paper is simply the sum of non-durable goods and services minus

clothing and shoes from personal consumption expenditures. Figure 1.3 illustrates the

consumption growth - it highly fluctuates in a small range of values resulting in a low standard

deviation.

1.3.2. Empirical Methodology

1.3.2.1 Estimating the relationship between consumption to wealth and equity

returns.

To test the degree of predictability of future stock returns using the consumption-to-

wealth ratio, I first estimate cedy. The theoretical framework suggest that consumption, equity,

debt and labor income share a long run common trend and deviations from this trend are possibly

short lived. There are several techniques that can be used to estimate the long term trend. I use

dynamic least squares (DLS) because it is able to handle concerns about endogeneity that are

important for the task at hand. The dynamic equation to be estimated has the form:

The residuals from equation (9) represent the deviations of the long-term trend estimated

by the cointegrating equation above. These deviations equal to my consumption measure, cedy.

After obtaining cedy, I calculate out-of-sample and in-sample estimates of future stock returns.

For the in-sample regression, the whole sample period is used and the parameters estimated will

determine the fitted values for stock returns, which are compared to the realized returns.

Many researchers argue that in-sample estimates possess a look-ahead bias. Thus, I

perform out-of-sample predictions to overcome this problem. The out-of-sample regressions start

with an initial sample of 65 observations; I then calculate cedy and relate it to the h-period-ahead

stock return. I continue this process, by expanding the sample used in regressions by one

observation at a time until the end of the sample period. Diebold and Mariano (1995) tests are

conducted to assess the statistical significance of these out-of-sample predictions.

1.3.2.2 Estimating conditional risk aversion

Equation (8) has been the subject of numerous tests in financial literature where tα is

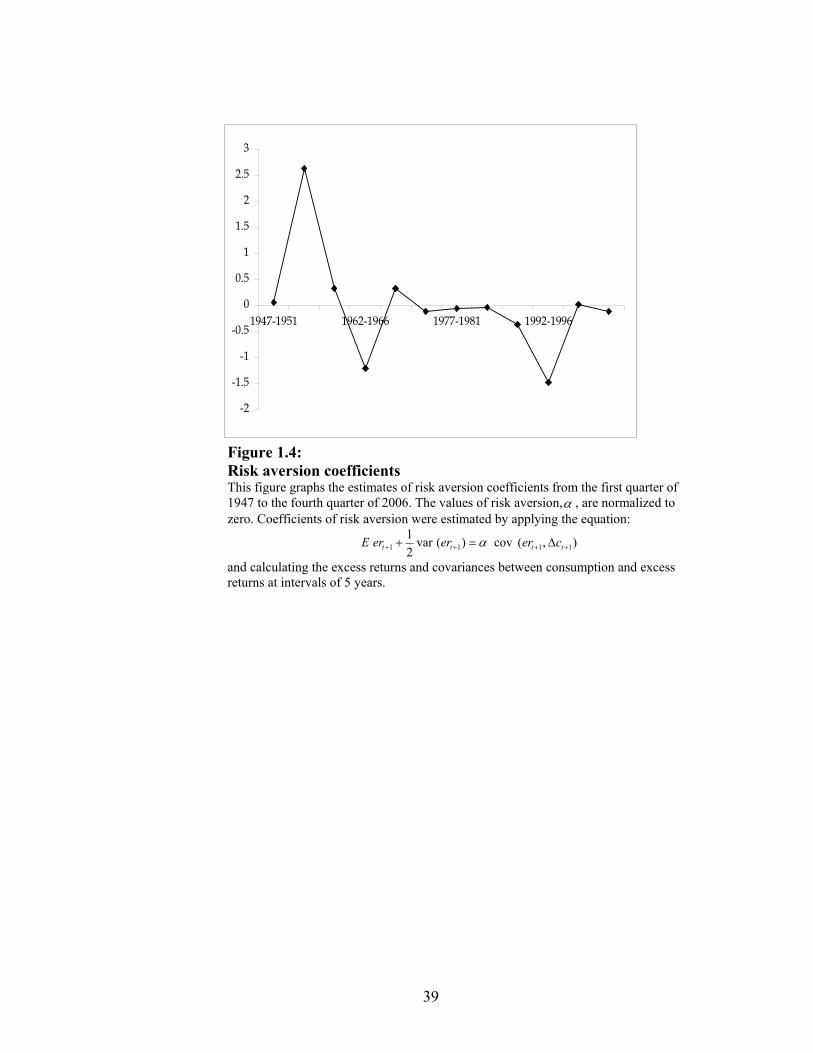

replaced by its time invariant counterpart α (Campbell et al (1997)). However, as Figure 1.4

suggests, the price of consumption risk is possibly not stable over time. Thus, a proper estimation

of equation (8) must allow for time varying behavior in tα . To test this equation using time

series, I form conditional second moments and then estimate the following equation:

1111011 ),(voc)(rav21

++++++ +Δ+=+ tttttttt ecererer αα (10)

where 1+tα is a parameterized known alternative for the representative agent’s state dependent

risk aversion coefficient. Following Duffee (2005), to estimate the conditional covariance, I

14

compute period-t+1 excess stock returns and consumption growth as sums of one-step-ahead

expectations and innovations,

1,11 +++ += terttt erEer ε

and (11)

1,11 +++ +Δ=Δ tcttt cEc ε

The product of innovations obtained from equations (11) equals the conditional covariance. It is

impossible to know the true innovations or the information sets that investors rely on. Therefore,

I have to construct fitted residuals based on known information as substitutes for true

innovations. These fitted residuals depend on a set of ex-post variables that serve as my

information set at time t and are my independent variables for the equations below. This set of

variables is carefully described in section 1.3.2.3. The regressions for returns and consumption

growth can be expressed as,

1,1 ' ++ += terrtrt Zer εβ (12)

1,1 ' ++ +=Δ tcctct Zc εβ (13)

where rβ and cβ are parameter vectors and the vectors Zr,t and Zc,t are realized in period t or

before. As in Duffee (2005), I call the set of equations (12) and (13) the zero-stage regressions.

The product of the residuals from the equations above is equal to the ex-post conditional

covariance between consumption growth and stock returns. It is important to note, that I am

interested in the expected conditional covariance as applicable in equation (10). I assume that

this conditional covariance can be represented in parametric form on a set of ex-post

instrumental variables, Xt, in the following regression,

111 '),(cov +++ +=Δ ttttt Xcer υω (14)

15

The ex-post instrumental variables, Xt, are also described in section 1.3.2.3. Once I estimate

equation (14) I arrive to an expected conditional covariance given by,

tttt Xcer 'ˆ),(voc 11 ω=Δ ++ (15)

Equation (15) embodies the first-stage regression; while the following equation

represents the second-stage regression,

11121011 ),(voc)()r(av21

+++++ +Δ++=+ ttttttt cerserer μααα (16)

The second component on the left side is an ex-post estimate of the variance of stock

returns that equals the square fitted residuals from equation (12), 21,1 )ˆ()r(av ++ = terter ε . Equations

(14) and (16) are estimated in a single step using the generalized method of moments (GMM) of

Hansen (1982). GMM is useful since it does not force us to make any assumption about

distributions of returns and errors. As well, it is flexible in the use of several instruments and

restrains residuals to be orthogonal with instruments chosen.

Our main interest lies on the right hand side of equation (16). Specifically, the estimated

parameters that proxy the conditional price of consumption risk (the risk aversion coefficient):

tt s211 ααα +=+ (17)

The term st reflects time variation in the investor’s volition to bear consumption risk. Due

to the number of instruments – there are more moment restrictions than coefficients to estimate –

moments may overidentify the coefficients and some moment restrictions may be inappropriate.

Hansen (1982) “J” tests are required to test if the GMM regression is correctly specified. In

addition, a likelihood ratio test variation for GMM developed by Newey and West (1987b),

called the D-test, is needed in order to test the statistical significance of a time-varying

component in the risk aversion coefficient.

16

1.3.2.3 Choice of instrumental variables The vectors Zr,t and Zc,t are instrument vectors that are used in equations (12) and (13).

The instrument vector Zc,t is used to construct fitted consumption growth residuals, and Zr,t, is

used to construct fitted stock return residuals. I follow Duffee’s choice of instruments for these

equations and include in Zc,t a constant term and a one-period lagged quarterly consumption

growth term. This minimizes the autocorrelation problems found in consumption growth. The

vector Zr,t includes a constant and my consumption–to-wealth ratio, cedy.

The choice of instruments, Xt, for equations (15) and (16) is partly motivated by the

composition effect of wealth noted by Santos and Veronesi (2003). The first instrument I include

is the ratio of stock market wealth to consumption, this variable has the intuitive appeal that as it

increases, consumption is more tightly tied to the performance of the equity markets and thus I

can expect the conditional covariance to behave accordingly. In addition, to account for the so-

called leverage effects present in stock return volatility –which in turn can affect the conditional

covariance between returns and consumption growth – I include lagged excess returns in Xt.

The composition effect also applies to the several other components of total wealth which

differ from stock wealth. This implication suggests that consumption does not only move with

stock market wealth as most literature has implied, but it also moves due to payments from debt,

real estate or labor5. Thus, I also include a measure of volatility of market value of debt in the

instruments set. Again, this choice of instrument is motivated by an intuitive notion, as debt

values become more unstable, we may observe higher volatility in expected future consumption

and very possibly create a contagion effect in equity prices6.

5 In the present study I am only concerned with the impact that debt has on stock returns, therefore real estate is not considered. 6 The events related to credit problems on summer 2007 seem to validate this story as great uncertainty in debt values was reflected as major swings in equity prices.

17

1.4. Empirical Results

This section contains the empirical results. I first provide results on the relationship

between consumption-to-wealth ratio and stock returns. I show that the consumption to wealth

ratio improves the predictability of multi-period-ahead stock returns because of a more thorough

segregation of the net wealth (discussed in Section 1.4.1). Section 1.4.2 contains the results on

the risk aversion coefficient. Cedy confirms the existence of a time-varying component in risk

aversion.

1.4.1 Consumption-to-Wealth ratio and expected future stock returns

I first outline the behavior of the consumption-to-wealth ratio and its relationship with

equity returns. I then test the in-sample and out-of-sample performance of cedy on future equity

returns.

1.4.1.1 Estimates of consumption to wealth ratio and its relationship with stock

returns

Values of cedy represent deviations of the consumption to wealth ratio from its long run

trend. Thus, cedy may contain relevant information regarding revisions about expectations of

future equity returns. From section 1.3.2.1, the parameters for the dynamic equation (9) are

estimated using quarterly data from the first quarter of 1959 to the fourth quarter of 2006 and

yield the following7,

7 For equation (18) l=4. I specified different values for the parameter l, which controls the leads and lags of regression (17), results were mainly unaffected by the choice of lag length.

18

tttt ydec)53.44()82.4()58.8()18.13(

76.003.005.048.1 +++= (18)

The estimated residuals from equation (18) are equivalent to the values for cedy. Newey-West

adjusted t-statistics are displayed in parenthesis below each coefficient of equation (18). Figure

1.5 gives an idea about the performance of cedy over time and illustrates that the relation

between consumption and wealth is stable over the years. As robustness check, I perform

several unit root tests to confirm that cedyt is I(0). The Augmented Dickey Fuller test statistic is -

3.75 and significant at the 1% level, while the Kwiatkowski-Phillips-Schmidt-Shin test statistic is

0.19 and cannot reject stationarity even at the 10% level. This also implies that the linear relation

between consumption and wealth is mirrored by the stable pattern of returns to components of

wealth and consumption growth shown in equation (7).

Remark 1: Cedy values are stationary and represent deviations from the long-term common trend among consumption, equity, debt and labor income. This is analogous to the idea that Cedy values correspond to short-run deviations on returns to wealth.

Next, I use the estimated values of cedy and perform in-sample and out-of-sample tests

and comparisons. This examination sheds light on the importance of separating more thoroughly

the net wealth into its different components.

1.4.1.2 In-sample performance of cedy

To evaluate the in-sample performance of cedy, I run OLS regressions where one-period

ahead returns on the S&P 500 index are regressed against different explanatory variables. As

means of comparison with cedy, I also use Lettau and Ludvigson (2001a) measure cay, the

dividend to price ratio and the dividend to earnings ratio. The last two measures are included

19

because the extant evidence suggests that they possess forecasting power on stock returns, albeit

at very long horizons (Campbell and Shiller (1988) and Fama and French (1988)). Table 1.2

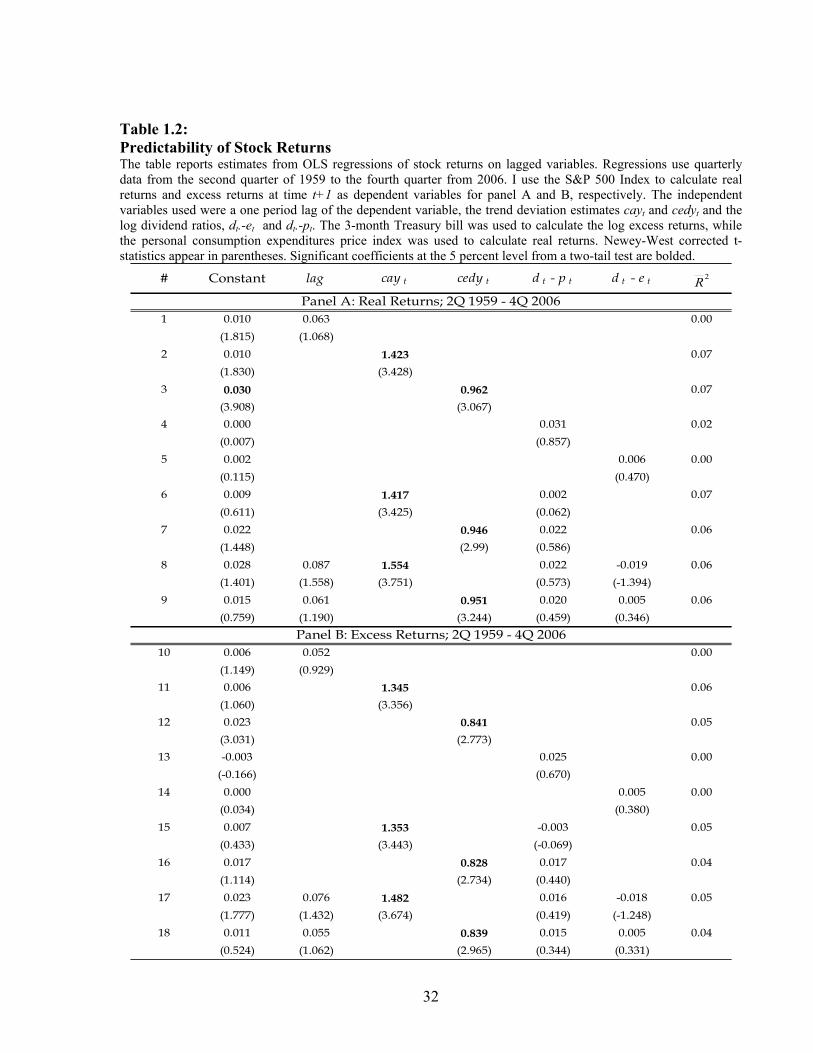

shows a set of estimates resulting from the use of my lagged trend deviation, cedy, and other

lagged variables of interest as independent variables. The table reports in-sample OLS estimates

of the S&P 500 Index real returns and excess returns. For each regression, I correct for serial

correlation and heteroskedasticity in standard errors using the Newey-West (1987) method.

Panel A and panel B show two sets of regressions that differ only in their choice of

dependent variables. On the one hand, panel A reports results using real stock returns as the left-

hand side variable; while on the other hand and for robustness check, panel B reports the

outcome of regressions using real excess returns as the dependent variable. The parameters of

each regression are estimated using the whole sample data.

The first row in panel A reports a regression using a one-period lagged real returns of the

S&P 500 index as independent variables. Results in row 1 show minimum or no explanatory

power over the dependent variable, having an adjusted R2 of zero. In contrast, row 2 and 3 in

panel A, suggest that the use of cay or cedy as independent variables generate superior outcomes,

both with an adjusted R2 of 7%. An interesting conclusion from Table 1.2, is that the dividend

ratios have a seemingly poor effect on real returns over a one-quarter-period; their respective

adjusted R2 is almost or equal to zero. Past literature has accounted for a statistically significant

predictive power that dividend to earnings or prices have on future stock returns (Fama and

French (1988)). My results show that, at least for the case of in-sample short horizons, the

dividend ratios do not contribute much to the explanation of variation in future stock returns. In

addition, I show that these measures do not have the power to subsume the effect that cay or cedy

have on one-period-ahead equity returns; this is revealed in rows 6 and 7 in panel A.

20

Finally, in row 8 and 9 I regress the one-period-ahead returns on all non-consumption

variables (dividend ratios and the lag of the dependent variable) simultaneously with either cay

(row 8) or cedy (row 9). The inclusion of these non-consumption variables actually worsens the

adjusted R2, against using cay or cedy alone, due to the penalty of adding insignificant variables

to the regression. Panel B shows qualitatively similar results relative to panel A.

Remark 2: Cedy provides statistically significant results while explaining in-sample one- period-ahead real and excess returns.

1.4.1.3 Out-of-sample forecasts

This sub-section describes the results for out-of-sample forecasting regressions and tests

using cedy and the other variables introduced in the previous sub-section. The motivation for

this out-of-sample exercise is to avoid the look-ahead bias pertaining to the in-sample

regressions, where some variables may find significant in-sample power explaining future

returns but this power disappears completely when using out-of-sample measures.

Table 1.3 reports a set of results for multi-period-ahead forecast comparisons using the

lagged trend deviation, cedy, as my benchmark. The table reports increasing-window OLS

regression estimates on the predictability of the S&P 500 Index returns. For every single

regression, I corrected for serial correlation and heteroskedasticity in standard errors with the

Newey-West (1987) method.

Each column in Table 1.3 depicts a comparison of predictive models between cedy and

the alternative measures. The different and alternative models, in sequence, utilize either cay,

dividend ratios, term structure of interest rates, short term interest rates or a constant return as

predictive measures, all at time t. There is substantial evidence that expected returns are not

21

constant (Campbell et al (1997)), however, as a basis for comparison it may be useful to contrast

the results derived from using cedy as a forecasting measure against the simplest possible model

such as the constant return model. Since Campbell (1987) found evidence that term structure of

interest rates has predictive power on stock returns, I also included the term structure of interest

rates, trm, and short term interest rates, short, as alternative predictive factors. The term structure

is the difference between the 10 year Treasury bond yield and the three month Treasury bill

yield. The short term interest measure is simply the three month Treasury bill minus its previous

year average; Campbell (1987) called this measure a stochastically detrended interest rate.

The first column in Table 1.3 represents the forecasting horizon in quarters. For example,

h=8 means that the forecast is being estimated two years (8 quarters) forward. To test the

accuracy of the forecasting models, I use the mean square forecasting error (MSFE) as the loss

function and the Diebold-Mariano (1995) test to determine which model performs the best. To

easily compare among models I divide the MSFE estimated when using cedy by the MSFE

estimated from the alternative models; this equals to MSFEcedy/MSFEalternative (MSFE ratio

onwards). Thus, a MSFE ratio that is less than unity means that the mean square forecast error

from the model using cedy is lower than that of the alternative model, confirming the superiority

of the cedy model. The Diebold-Mariano (1995) procedure tests the null hypothesis that two

models have equal predictive power –more properly, it tests that the forecast errors from two

competing models are about the same; in my case, a rejection of this hypothesis represents

statistical evidence in favor of the higher forecasting ability of cedy 8.

Few simple steps are required to estimate the out-of-sample regressions. First, I estimate

equation (9) applying a DLS technique within the estimation period. The initial quarterly

8 I follow Harvey, Leybourne and Newbold (1998) and correct for serial correlation in the Diebold-Mariano statistic; for this I use the Newey-West procedure.

22

estimation period starts from the second quarter of 1959 to the fourth quarter of 1974. The

residuals of this regression equal my consumption-to-wealth measure, cedy. Second, I exclude

the last observation from the cedy series (e.g. fourth quarter of 1974) and perform an OLS

regression of h-period stock returns against the remaining values of cêdy (e.g. from second

quarter of 1959 to the third quarter of 1974). I then record the parameters from this model. Third,

I use the coefficient of cêdy from step two and multiply it by the previously excluded observation

of cêdyt (in this case the 4th quarter of 1974). This product equals the forecast of equity returns h

periods into the future. I record this prediction and estimate the square forecast error. The

process is updated one observation at a time until the fourth quarter of 2006. Finally, the mean

square forecast error is calculated.

In almost every case shown in Table 1.3, the forecasting power of cedy is superior to the

one of alternative measures. In most instances, the MSFE ratio is below unity and the Diebold-

Mariano test rejects at a very high significance level the null hypothesis that the alternative

measures have as much predictive power as cedy. There are a couple of cases where the average

forecasting error from the cedy model is marginally worse compared to other alternative models

(e.g. constant and cay, in horizon 1 and 16 respectively). However, this relation disappears as

horizons change. It is interesting to note that the constant return model seems to be the second

best alternative to the cedy model at shorter horizons, underscoring the difficulty of generating

short to medium horizon out-of-sample forecasts that can improve upon a simple mean.

Another important result is that in almost all cases, as the forecasting horizon increases,

the forecasting power of cedy outperforms that of the alternative measures. These results

implicate cedy as an important predictor of expected future stock returns; the Diebold-Mariano

test gives strong statistical evidence of the superiority of cedy compared to usual benchmarks.

23

Remark 3: Results suggest that cedyt can provide statistically significant and superior predictions on future stock returns for different horizons ahead compared to usual benchmarks.

1.4.2 Risk aversion coefficients

Results from the previous section suggest that cedyt provides significant information

regarding future stock returns. In particular investors revise their willingness to hold risky assets

using cedy or an equivalent measure in their information set. If this is true, we should observe a

time-varying component in risk aversion which may be captured by cedy. Hall (2001) argues

that the increased use of debt as a source of funding over the past few decades makes it difficult

to imagine that equity holdings and human capital represent the entire flow of returns on total

wealth. Thus, total wealth should reflect time varying changes in leverage too.

To estimate the price of consumption risk and test its time dependence I use equation

(16), reproduced below for convenience,

11121011 ),v(oc)()r(av21

+++++ +Δ++=+ tttttt cerserer μααα

where ts2α represents the time dependent component in risk aversion and 1α represents its fixed

component.

There are several theoretical models that employ equation (15) or an equivalent one

(Campbell and Cochrane (1999) and Constantinides (1990)), however extant tests of equation

(16) are few, most notably Duffee (2005), and most find none or weak evidence in favor of time

variability of the price of consumption risk. I estimate equation (16) using the GMM method of

Hansen (1982). I utilize cedy at time t as a proxy for the time-varying component, st, in (16). As

a robustness check I also estimate (16) using the dividend to price ratio (dt – pt) and Wachter’s

(2002) measure of surplus consumption. As substitutes for st, I consider the dividend to price

24

ratio since empirical evidence suggests this measure possesses forecasting power on returns over

long horizons, and I also include Wachter’s surplus consumption measure since it arises naturally

in habit formation models.

As mentioned in section 1.3, the instrument’s set used for the GMM estimation include

the market equity to consumption ratio, a one period lagged excess return, the square of the

return on debt as a measure of volatility in debt returns, and the proxy for time variation in risk

aversion, st, for each case. Due to the number of moment restrictions that overidentify the

coefficients, GMM estimation is carried out in the usual two step procedure, where the first step

uses an identity matrix as the weighting matrix and the second step uses the Newey-West

(1987b) weighting matrix.

Table 1.4 reports the coefficients of the components that form the price of consumption

risk for the different proxies used. In addition, the t-statistics, derived using the delta method,

are presented in parenthesis. Unlike previous empirical research on time variation of risk

aversion, I find significant evidence of a time dependent component in the price of risk. Table

1.4 implies that cedy is the only variable capable of capturing statistically significant time

variation in risk aversion. The coefficient for cedy has the appropriate sign; as shown in figure

1.5, cedy is countercyclical to the business cycle, similar to expected equity returns (Cochrane

(2005)). Therefore for high values of cedy the price of consumption risk must also be high.

The full estimation results for equation (16) using cedy are presented in Table 1.5. Panel

A shows the parameter estimates. The first row in panel A presents a regression with the

restriction 02 =α , that is imposing time invariance in the risk aversion coefficient, while row 2

presents an unrestricted estimation; again, t-statistics are derived using the delta method and are

25

presented in parenthesis. Overall, results in panel A validate the choice of using cedy as a

measure of time variation in risk aversion.

Panels B and C in Table 1.5 present two different tests for equation (16). Due to the

number of instruments, there are more moment restrictions than coefficients to estimate, thus

moments overidentify the coefficients and some moment restrictions may be inappropriate.

Hansen (1982) developed a specification test for overidentifying restrictions, the “J” statistic of

this test is presented in Panel B along with its p-value derived from a 2χ distribution with

degrees of freedom equal to the number of excess restrictions. Evidence in this table is in favor

of not rejecting the null hypothesis that the unrestricted regression is correctly specified.

Panel C presents the likelihood ratio test variation for GMM developed by Newey and

West (1987b), called the D-test. For this test, I first estimate the unrestricted equation –presented

in row 2 in panel A- using its Newey-West weighting matrix and then I estimate the restricted

equation (row 1), where 02 =α , using the exact same values inside the Newey-West weighting

matrix obtained from the unrestricted version of the model (row 2). Once estimating both

equations with the same Newey-West weighting matrix, I obtain the respective “J” statistics and

calculate the difference between them: the D-test statistic. If the restriction, 02 =α , is

appropriate, the D-test statistic should follow a 2χ distribution with one degree of freedom. The

test rejects such restriction at the 5% significance level. This confirms the evidence in favor of

cedy. Hence, my measure of deviations of consumption-to-wealth ratio captures the time-

variation in the risk aversion coefficient.

26

1.4.3 Robustness Check and Monte Carlo estimations

It is possible that the favorable results obtained for cedy are just the product of incorrect

inference or sheer good luck. After all, cedy may be capturing other elements incorporated in

stock returns that may be unrelated to the risk aversion that investors experience. As a robustness

check for my results, I perform two Monte Carlo experiments; in the first case I check for the

correct inference from the GMM estimators in a finite sample, while in the second case I check

for cedy’s ability to capture a time-varying component in risk aversion that is independent of

cedy. Results of the Monte Carlo robustness tests are presented in panel D, Table 1.5.

Case 1

Since the results from GMM estimation are distributed normal only asymptotically, for

correct inference it’s important to study the small sample properties of the coefficients estimated.

To test if cedy captures the time-varying risk aversion component in equity returns in a sample of

finite size, I construct stock returns that exclude any time-variation in risk aversion (stock-FRA

returns onwards) and then use GMM to estimate equation (16) on this artificial data to check the

empirical distribution of the coefficients.

I first generate 190 one-step-ahead innovations of stock returns and consumption growth

from a multivariate normal distribution with zero mean and covariance matrix that matches the

one of residuals obtained from equations (12) and (13) during the zero stage regressions. I chose

to generate only 190 observations in order to match the number of actual observations that I use

in this paper, from the first quarter of 1959 to the fourth quarter of 2006.

I construct the stock-FRA returns series restricted so excess returns do not possess a time-

varying component,

27

*11,1,

*1

*01,1, ˆ),v(ocˆˆ)r(av

21

+++++ +Δ++−= ttFRAtFRAtFRAtFRA cererer μαα (19)

For this returns series, I utilize the artificial residuals to construct the variance and covariance

variables; the parameters *0

α and *1

α are those of the first row of Table 1.5 which were estimated

from equation (16) on the actual data restricted to 2α =0. In order to incorporate an element of

random shocks in excess returns I sample a noise component, *1ˆ +tμ , from a normal distribution

with mean zero and variance equal to the one recorded from the residuals of the restricted

regression mentioned above.

Once I computed the stock-FRA returns using equation (19), I used these observations to

test the relevancy of cedy. These newly generated stock-FRA returns exclude a time-varying risk

aversion component by construction. I now estimate equation (16) utilizing the new stock-FRA

returns, the artificial innovations and actual cedy series; since the stock-FRA returns do not

possess a risk aversion time-varying component, this experiment gives us the small sample

distribution of cedy under the (correct) null hypothesis that its coefficient is zero.

I perform this procedure 5,000 times obtaining as many coefficients for cedy. The 5,000

coefficient estimates of cedy should be zero, because stock-FRA returns were created purposely

without cedy’s influence but may randomly take numbers that differ from zero. With these

estimates I am able to derive the significance value for the hypothesis that the coefficient of cedy

presented in Table 1.5 is statistically different from zero. My results show that only 4.8% of the

5,000 estimates are equal or greater than 1.068, therefore it is logical to think that cedy’s

coefficient from Table 1.5 does not represent a coincidence or randomness and in fact is different

from zero, capturing the time-varying component of risk aversion nested in equity returns.

28

Case 2

Constantinides (1990) and Campbell and Cochrane (1999) stated that the time varying

component in risk aversion is related to investor’s habit consumption. They also imply that this

habit follows a pattern that has similarities to an AR(1) process. Therefore, I generate stock

returns (stock-AR returns onwards) that incorporate an AR(1) component as the source for time

variation in risk aversion and check if the success of cedy is due to some independent source of

risk, namely the AR(1) process, that is captured by cedy by just unexpected luck.

I utilize the parameters from row 1 in Table 1.5, artificial innovations of stock returns and

consumption growth and the generated noise component as in the first case to calculate these

stock-AR returns. I include the AR(1) process in equation (16) by replacing ts2α with yt where

tνκ += 1-tt yy and κ is restricted to be randomly and uniformly distributed between 0.05 and

0.95 in order to keep AR(1) process stationary. Notice that yt can reflect persistence in risk

aversion as κ approximates to 0.95 and it is nearly a memoryless process when κ is near to its

lower bound. The following is the stock-AR returns’ equation:

*

11,1,

1,1,*1

*01,1,

ˆ)),v(oc

),v(ocˆˆ)r(av21

+++

++++

+Δ+

+Δ++−=

ttARtAR

tARtARtARtAR

cer

cererer

μ

αα

(y t

(20)

Stock-AR returns do not have a trace of cedy and include an AR(1) component. The

stock-AR returns, the artificial innovations and cedy are used to regress equation (16). I perform

this procedure 15,000 times and generate 15,000 different coefficients for cedy. Replications for

this procedure triple those in case 1 since the AR(1) component adds additional randomness to

the process and to this case. Since stock-AR returns intentionally do not include cedy as a

defining factor, then any of the 15,000 coefficients generated should not be relevant even if by

chance they are different from zero.

29

This experiment gives the small sample distribution for the (correct) null hypothesis that

the coefficient of cedy from equation (16) is insignificant when the time-varying risk aversion is

caused by a process independent of cedy. The significance value for the coefficient of cedy

estimated from equation (16) on actual data, presented in Table 1.5, is 8.23%. This p-value

seems reasonable considering all the amount of uncertainty and randomness in the Monte Carlo

experiment, thus I can be fairly confident that cedy’s coefficient is significant, and its value has

not been determined by randomness but due its ability to capture time-varying risk aversion in

equity returns.

1.5. Conclusions

This article provides evidence on the importance of considering market value of debt in

explaining the relationship between consumption, wealth and equity returns. I develop a

measure of the consumption-to-wealth ratio that accounts for debt values and then relate this

measure to equity returns. The components of wealth include market value of debt, equity and

human capital. I estimate the extent to which inclusion of debt improves the correlation

between this consumption-to-wealth ratio and expected future stock returns. I show that

deviations to this broader measure of consumption-to-wealth ratio, denoted cedy in this article,

can provide statistically significant predictions on future stock returns for different horizons that

surpass other benchmarks. In almost every case tested, the predictive power of cedy is superior

to the one corresponding to alternative factors.

I find statistically significant evidence in favor of a time-varying component in the risk

aversion of investors. The coefficient for cedy has the appropriate sign and supports the notion

that cedy is countercyclical to the business cycle, similar to expected equity returns (Cochrane

30

(2005)); for high values of cedy the price of consumption risk must also be high. Overall, this

evidence points to the importance of considering a more comprehensive definition of wealth

when considering its relationship with equity returns.

31

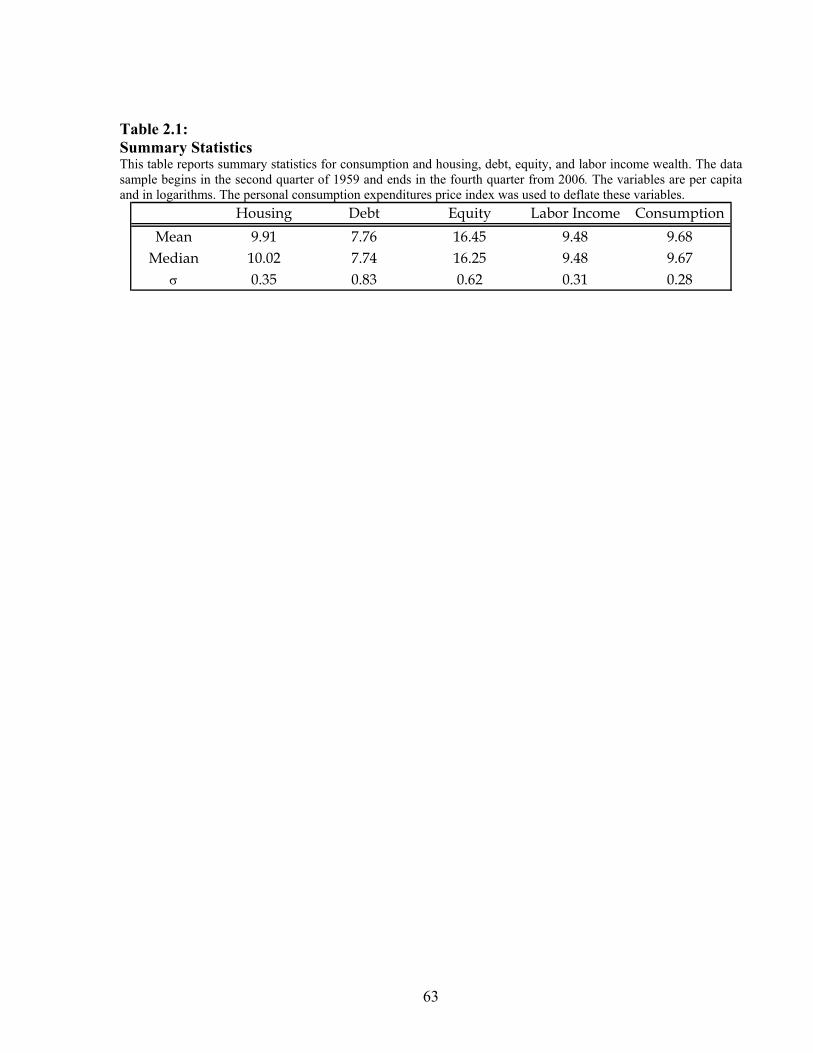

Table 1.1: Summary Statistics This table reports summary statistics for cedy, debt, equity, labor income and consumption. The data sample begins in the second quarter of 1959 and ends in the fourth quarter from 2006. Cedy reflects deviations in the long-term trend between consumption and wealth components. The variables in the last four columns are per capita and in logarithms. The personal consumption expenditures price index was used to deflate these variables.

Table 1.2: Predictability of Stock Returns The table reports estimates from OLS regressions of stock returns on lagged variables. Regressions use quarterly data from the second quarter of 1959 to the fourth quarter from 2006. I use the S&P 500 Index to calculate real returns and excess returns at time t+1 as dependent variables for panel A and B, respectively. The independent variables used were a one period lag of the dependent variable, the trend deviation estimates cayt and cedyt and the log dividend ratios, dt.-et and dt.-pt. The 3-month Treasury bill was used to calculate the log excess returns, while the personal consumption expenditures price index was used to calculate real returns. Newey-West corrected t-statistics appear in parentheses. Significant coefficients at the 5 percent level from a two-tail test are bolded.

Table 1.3: Out-of-Sample Forecasts of Stock Returns This table reports the results for a multi-period ahead forecast comparisons. The dependent variable is the excess return on the S&P 500 Index at time t+1. Each case represents a comparison between two models, where the cedy model is always being tested. The ratios of the root-mean square forecasting error (MSFE) of the cedy model to the alternative model are reported in columns two to seven. Cedyt is at time t. The models denoted as constant, cayt, dt.-pt, dt.-et, trmt, and shortt, are simply the forecasting models of the stock returns using a constant, and the time t variables of cay, dividend yield, dividend payout, term structure of interest rates, and short term interest rates, respectively. The initial quarterly estimation period starts from the second quarter of 1959 to the fourth quarter of 1974. Then, the model is increasingly re-estimated until the fourth quarter of 2006. The first column corresponds to the forecast horizon, which represents the lags (also corresponding subscript t of the independent variables) of the independent variables and increases in quarters. Diebold-Mariano (1995) test according to the Harvey, Leybourne and Newbold (1998) adjustment were estimated. The null hypothesis of equality of forecasts is rejected at 10%, 5% or 1% significance level if the estimate below comes with: *,**,or ***, respectively.

cedy t vs. cay t cedy t vs. d t - p t cedy t vs. d t - e t cedy t vs. trm t cedy t vs. short t cedy t vs. constant

Table 1.4: Price of Risk This table reports GMM estimates for the price of consumption risk using three proxies for its time-varying component. Among these proxies I consider cedyt, dividend to price (dt-pt) and Wachter (2002) surplus consumption measure. GMM regressions use quarterly data from the second quarter of 1959 to the fourth quarter from 2006. I use the S&P 500 Index and the 3-month Treasury bill to calculate the log excess returns at time t+1. The personal consumption expenditures price index was used to deflate excess returns. The coefficient α1 corresponds to the static component of the price of risk, while α2 represents the coefficient of the time-varying component. The instruments used in the regression are described in section 1.4.2. Delta method t-statistics appear in parentheses. Significant coefficients at the 5 percent level from a two-tail test are bolded.

Price of Risk α1 α2

cêdy t -99.68 1.068

(-0.909) (2.076)

d t -p t -162.88 0.940

(-1.139) (1.236)

Surplus Consumption -52.414 -0.616

(-0.583) (1.741)

35

Table 1.5: GMM Estimation results Panel A in this table reports complete GMM estimates for the price of consumption risk using cedyt, as the proxy for the time-varying component. GMM regressions use quarterly data from the second quarter of 1959 to the fourth quarter from 2006. I use the S&P 500 Index and the 3-month Treasury bill to calculate the log excess returns at time t+1. The personal consumption expenditures price index was used to deflate excess returns. The coefficient α1 corresponds to the static component of the price of risk, while α2 represents the coefficient of the time-varying component. The instruments used in the regression are described in section 1.4.2. Delta method t-statistics appear in parentheses. Significant coefficients at the 5 percent level from a two-tail test are bolded. Panel B presents Hansen (1982) specification tests for overidentifying restrictions. Panel C presents the Newey-West (1987b) Likelihood ratio GMM test statistics for the null hypothesis that restricts α2 to equal to zero.

# Constant α1 α2

1 0.023 -44.73

(2.372) (-0.387)

2 0.029 -99.68 1.068

(3.072) (-0.909) (2.076)

J statistic: 1.319

P-value: 0.517

Restricted J statistic: 5.702

Unrestricted J statistic: 1.319

P-value: 0.036

Case 1 - Small Sample DistributionHo: α2 = 0

P-value: 0.048

Case 2 - AR(1) processHo: α2 = 0

P-value: 0.082

Panel A: GMM Estimates

Panel B: Specification Test

Panel C: Test of Restriction α2 = 0

Panel D: Monte Carlo Simulations

11121011 ),v(oc)()r(av21

+++++ +Δ++=+ tttttt cercedyerer μααα

36

.0

.1

.2

.3

.4

.5

.6

1960 1970 1980 1990 2000

Figure 1.1: Debt to Equity ratio This figure graphs the debt to equity ratio. The data covers the period from the first quarter of 1959 to the fourth quarter of 2000. This figure illustrates the peak in debt values relative to equity values in the early 1980s.

37

-1

0

1

2

1960 1970 1980 1990 2000

ConsumptionEquity

DebtLabor income

Figure 1.2: Consumption and Wealth Components This figure shows the per capita consumption, debt, equity and labor income. All variables are in logarithms and normalized. The data starts from the first quarter of 1959 and ends in the fourth quarter of 2006. This figure shows that each variable has a persistent upward trend. As well, it also illustrates a long-term common trend shared by each of the series.

38

-.015

-.010

-.005

.000

.005

.010

.015

.020

.025

1960 1970 1980 1990 2000

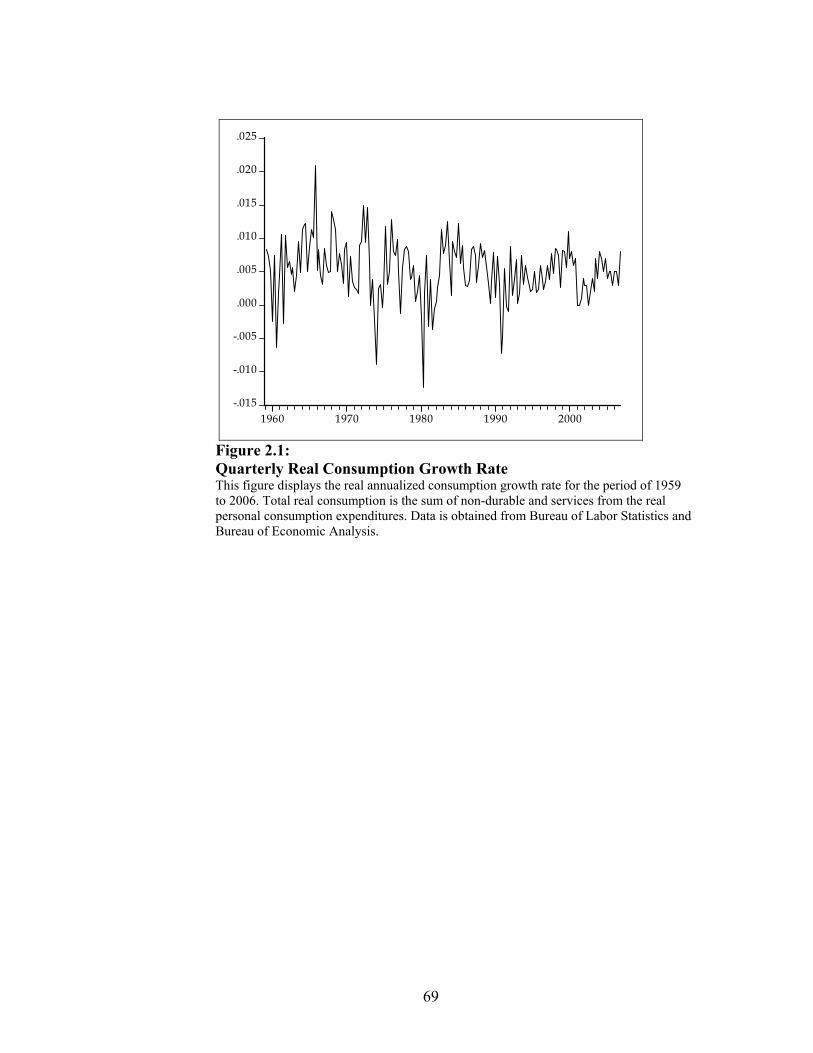

Figure 1.3: Quarterly Real Consumption Growth Rate This figure displays the real annualized consumption growth rate for the period of 1959 to 2006. Total real consumption is the sum of non-durable and services from the real personal consumption expenditures. Data is obtained from Bureau of Labor Statistics and Bureau of Economic Analysis.

39

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

1947-1951 1962-1966 1977-1981 1992-1996

Figure 1.4: Risk aversion coefficients This figure graphs the estimates of risk aversion coefficients from the first quarter of 1947 to the fourth quarter of 2006. The values of risk aversion,α , are normalized to zero. Coefficients of risk aversion were estimated by applying the equation: ),(cov)(var

21

1111 ++++ Δ=+ tttt cerererE α

and calculating the excess returns and covariances between consumption and excess returns at intervals of 5 years.

40

-2

-1

0

1

1960 1970 1980 1990 2000

Figure 1.5: CEDY and Business Cycles This figure graphs the estimates of cedy from the first quarter of 1959 to the fourth quarter of 2006. Shaded regions indicate recessions as defined by the NBER.

41

CHAPTER 2: EXPECTATIONS, CONSUMPTION TO WEALTH RATIO

AND EQUITY RETURNS

2.1. Introduction

Finance literature has historically attempted to take theoretical models of consumption

based asset pricing to equity market data. Early ground-breaking works on asset pricing include

Lucas (1978) and Breeden (1979) among others; however, most of these early works only give a

relevant role to payouts from equity. In light of this, recent studies, such as Jagannathan and

Wang (1996), Lettau and Ludvigson (2001a, 2001b), Julliard (2004), Duffee (2005), Piazzesi,

Shneider and Tuzel (2007), have focused on models that include other wealth sources which are

proven to have a substantial effect on asset prices.

The framework presented in this article, shows how consumption and several wealth

components are directly related to discounted future returns to wealth. I segregate wealth into

four components: payments to debt (by lending money and obtaining an interest on the loan),

equity, real estate (housing), and labor income. I use these four variables because, through

history and based on literature findings, they have been considered as the main sources of

wealth. To my knowledge, there is no previous work that has utilized these four wealth sources

together to explain changes in equity returns.

My first contribution in this article is to shed light in the arena of asset pricing by finding

relevancy on using a more thorough wealth segregation to explain movements of equity returns. I

provide a parsimonious framework that connects consumption with the market values of debt,

housing, equity and human capital. My theoretical motivation relies on the work made by

Campbell and Mankiw (1989), Campbell (1996), and Lettau and Ludvigson (2001a).

42

Starting with Lettau and Ludvigson (2001a), previous work argue that deviations from

the long run stable state between consumption and wealth predict future stock returns; I make the

case instead that it is the changes in expectations of the consumption to wealth ratio from one