Estate Planning Estate Planning Parman R. Green Parman R. Green University of Missouri Extension University of Missouri Extension Ag Business Mgmt. Specialist Ag Business Mgmt. Specialist [email protected]660 542-1792 660 542-1792

Transcript

Estate PlanningEstate PlanningParman R. GreenParman R. Green

University of Missouri ExtensionUniversity of Missouri Extension

Ag Business Mgmt. SpecialistAg Business Mgmt. Specialist

Transfer & Preservation of Family BusinessTransfer & Preservation of Family Business

Meet Requirement for “Special” ProvisionsMeet Requirement for “Special” Provisions

Special BequestsSpecial Bequests

Deal with Living Will, Durable Power of Deal with Living Will, Durable Power of Attorney, and Long-term Care IssuesAttorney, and Long-term Care Issues 33

Federal Estate and Gift Federal Estate and Gift Exclusion AmountsExclusion Amounts

YearYear MaximumMaximum

RateRate

EstateEstate

ExclusionExclusion

GiftGift

ExclusionExclusion

20032003 49%49% $1.0 million$1.0 million $1.0 million$1.0 million

20042004 48%48% $1.5 million$1.5 million $1.0 million$1.0 million

20052005 47%47% $1.5 million$1.5 million $1.0 million$1.0 million

20062006 46%46% $2.0 million$2.0 million $1.0 million$1.0 million

20072007 45%45% $2.0 million$2.0 million $1.0 million$1.0 million

20082008 45%45% $2.0 million$2.0 million $1.0 million$1.0 million

20092009 45%45% $3.5 million$3.5 million $1.0 million$1.0 million

20102010 35% gifts35% gifts RepealedRepealed $1.0 million$1.0 million

20112011 55% + 5%55% + 5% $1.0 million$1.0 million $1.0 million$1.0 million 44

55

ESTATE & GIFT TAXESTATE & GIFT TAXUNIFIED RATE SCHEDULEUNIFIED RATE SCHEDULE

(selected brackets)(selected brackets)

not over 10,000not over 10,000 18% of such 18% of such 10,000 to 20,00010,000 to 20,0001,800 + 20% > 10,0001,800 + 20% > 10,000 … ….. … ….. … …..

500,000 to 750,000500,000 to 750,000 155,800 + 37% > 500,000 155,800 + 37% > 500,000 750,000 to 1,000,000 248,300 + 39% > 750,000750,000 to 1,000,000 248,300 + 39% > 750,000 1,000,000 to 1,250,000 345,800 + 41% > 1,000,0001,000,000 to 1,250,000 345,800 + 41% > 1,000,000 1,250,000 to 1,500,000 1,250,000 to 1,500,000 448,300 + 43% > 1,250,000 448,300 + 43% > 1,250,000 1,500,000 +1,500,000 + 555,800 + 45% > 1,500,000 555,800 + 45% > 1,500,000

Tools & ProvisionsTools & Provisions

Marital DeductionMarital Deduction

Annual Gift ExclusionAnnual Gift Exclusion

Gift SplittingGift Splitting

Ed. & Medical GiftsEd. & Medical Gifts

Charitable GiftsCharitable Gifts

Title OwnershipTitle Ownership

Non-probate TransfersNon-probate Transfers

Generation SkippingGeneration Skipping

Business OrganizationBusiness Organization

Special Use ValuationSpecial Use Valuation

14 yr. Tax Installment14 yr. Tax Installment

Life InsuranceLife Insurance

WillsWills

TrustsTrusts

AnnuitiesAnnuities

Medicare, Medicaid, Long-Medicare, Medicaid, Long-term Care Ins.term Care Ins.

Living WillsLiving Wills

Durable Power AttorneyDurable Power Attorney

66

Tools & ProvisionsTools & Provisions

Marital DeductionMarital Deduction

Annual Gift ExclusionAnnual Gift Exclusion

Gift SplittingGift Splitting

Educational & Medical GiftsEducational & Medical Gifts

Charitable GiftsCharitable Gifts77

BEQUEST vs GIFTBEQUEST vs GIFT

160 A. purchased 1950 in for $16,000.160 A. purchased 1950 in for $16,000.Current FMV is $320,000.Current FMV is $320,000.

Built-in taxable gainBuilt-in taxable gain -0- -0- 304,000 304,000

88

Tools & ProvisionsTools & Provisions

Title OwnershipTitle Ownership– Sole OwnershipSole Ownership– Tenants in CommonTenants in Common– Joint Tenancy (JTWROS)Joint Tenancy (JTWROS)

Tenancy by Entirety (restricted to husband & wife)Tenancy by Entirety (restricted to husband & wife)

99

Avoiding ProbateAvoiding Probate

Joint Tenancy & Tenancy by the EntiretyJoint Tenancy & Tenancy by the Entirety

Non-probate Transfers Non-probate Transfers – Pay on Death (Pay on Death (PODPOD) ) [ex: checking accounts, CDs][ex: checking accounts, CDs]

– Transfer on Death (Transfer on Death (TODTOD) ) [ex: stocks, bonds, vehicles][ex: stocks, bonds, vehicles]

– Beneficiary Deed Beneficiary Deed [example: real estate][example: real estate]

Revocable TrustRevocable Trust

1010

Tools & ProvisionsTools & Provisions

Generation Skipping Generation Skipping – Children for life, grandchildren with remainder interestChildren for life, grandchildren with remainder interest

Business OrganizationBusiness Organization– Sole proprietorshipSole proprietorship– PartnershipPartnership– Limited Liability CompanyLimited Liability Company

– Corporation “C” or “S”Corporation “C” or “S”

1111

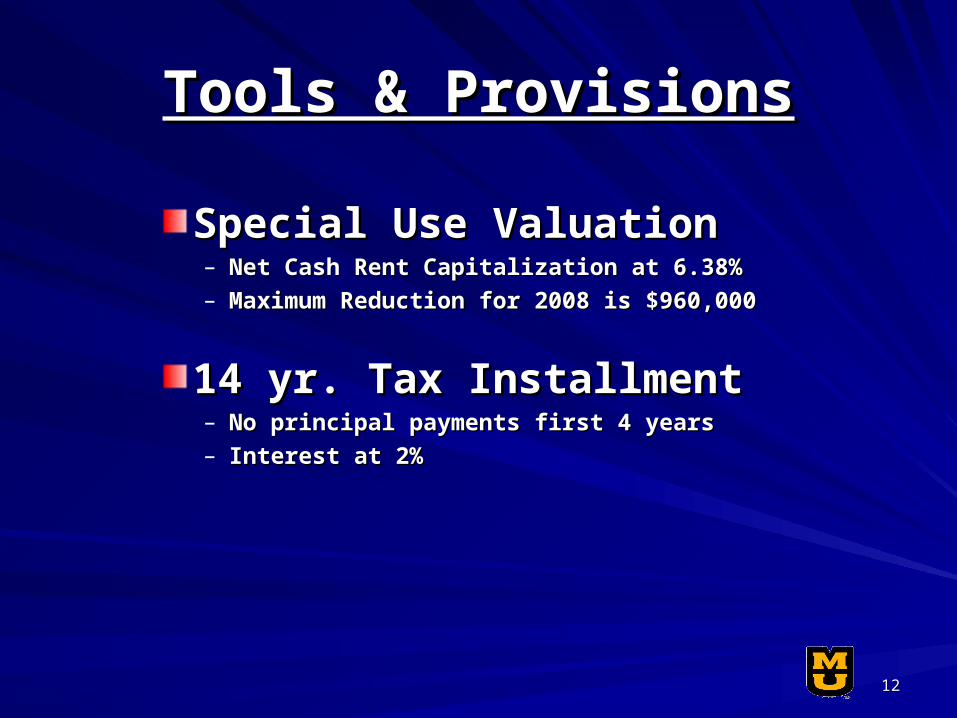

Tools & ProvisionsTools & Provisions

Special Use ValuationSpecial Use Valuation– Net Cash Rent Capitalization at 6.38%Net Cash Rent Capitalization at 6.38%– Maximum Reduction for 2008 is $960,000 Maximum Reduction for 2008 is $960,000

14 yr. Tax Installment14 yr. Tax Installment– No principal payments first 4 yearsNo principal payments first 4 years– Interest at 2%Interest at 2%

1212

Tools & ProvisionsTools & Provisions

Life InsuranceLife Insurance

WillsWills

TrustsTrusts

AnnuitiesAnnuities

1313

Life InsuranceLife Insurance

Incidents of Ownership Incidents of Ownership right to:right to:– Change beneficiariesChange beneficiaries– Borrow against policyBorrow against policy– Cancel the policyCancel the policy

Consider a “Irrevocable Life Insurance Trust” Consider a “Irrevocable Life Insurance Trust” if you have a taxable estate.if you have a taxable estate.

Living TrustLiving Trust (Revocable Trust) (Revocable Trust)Testamentary TrustTestamentary TrustIrrevocable TrustIrrevocable TrustLife Insurance TrustLife Insurance TrustMarital Deduction & Bypass TrustsMarital Deduction & Bypass TrustsQualified Terminal Interest Trust “QTIP”Qualified Terminal Interest Trust “QTIP”Grantor Retained Annuity TrustGrantor Retained Annuity TrustQualified Personal Residence TrustQualified Personal Residence TrustCharitable Remainder TrustCharitable Remainder TrustCharitable Lead TrustCharitable Lead Trust……. many more!. many more!

1616

Priority of EstatePriority of EstateAsset Transfer MethodsAsset Transfer Methods

Right of Survivorship (title)Right of Survivorship (title)

TrustTrust

Non-probate TransferNon-probate Transfer

WillWill

IntestateIntestate

1717

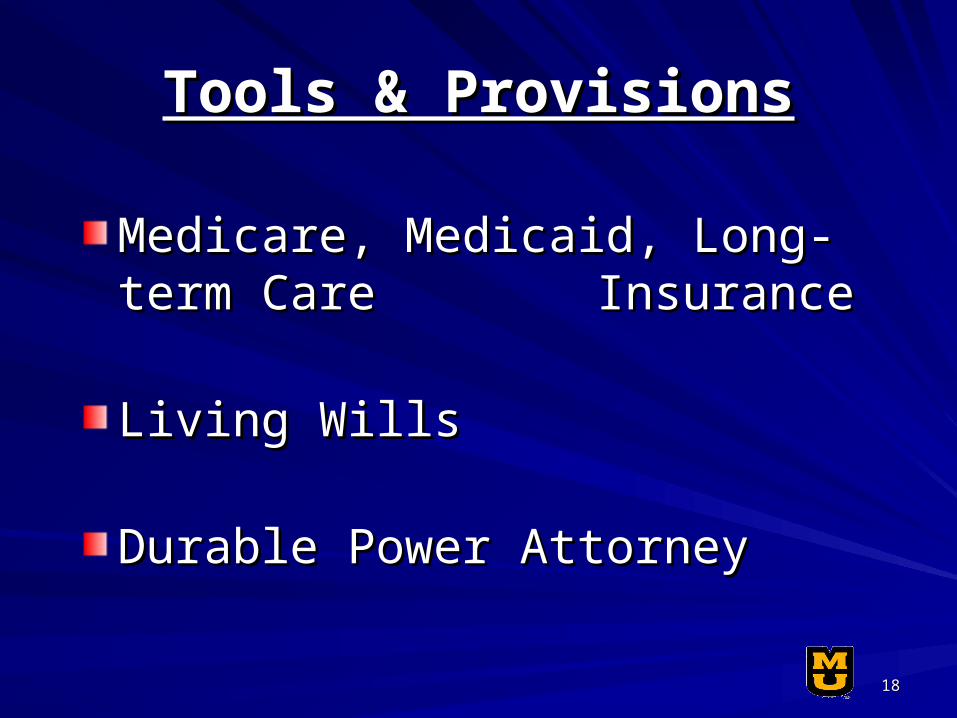

Tools & ProvisionsTools & Provisions

Medicare, Medicaid, Long-term Care Medicare, Medicaid, Long-term Care InsuranceInsurance

Living WillsLiving Wills

Durable Power AttorneyDurable Power Attorney

1818

What’s Their Estate?What’s Their Estate?

Jack and Jill are 67 years young and have 2 adult Jack and Jill are 67 years young and have 2 adult children and 6 grandchildren. They own as children and 6 grandchildren. They own as JTWROSJTWROS 1,280 acres worth $3,000,000. Jack and Jill have 1,280 acres worth $3,000,000. Jack and Jill have $200,000 and $100,000 in IRAs, respectively. They $200,000 and $100,000 in IRAs, respectively. They have $150,000 in their checking account, held as have $150,000 in their checking account, held as JTWROS. The farm machinery is valued at JTWROS. The farm machinery is valued at $350,000 and the grain in storage is worth $350,000 and the grain in storage is worth $200,000. Jack owns a life insurance policy on his $200,000. Jack owns a life insurance policy on his life and Jill is the named beneficiary – its face value life and Jill is the named beneficiary – its face value is $500,000 (for this exercise list this asset at it’s is $500,000 (for this exercise list this asset at it’s face value).face value).

They owe the bank $100,000 on a land mortgage.They owe the bank $100,000 on a land mortgage.

What’s Their Estate?What’s Their Estate? Jack Jack Jill Jill CashCash 75,000 75,000 75,000 75,000InventoryInventory 100,000 100,000 100,000100,000MachineryMachinery 175,000 175,000 175,000175,000Real EstateReal Estate 1,500,000 1,500,000 1,500,000 1,500,000Retirement Accts. 200,000 Retirement Accts. 200,000 100,000100,000Life InsuranceLife Insurance 500,000 500,000

AssetsAssets 2,550,000 1,950,000 2,550,000 1,950,000Short Term Liab.Short Term Liab. 0 0 0 0Long Term Liab.Long Term Liab. 50,000 50,000 50,000 50,000

Net EstateNet Estate 2,775,000 2,775,000 1,625,000 1,625,000

Strategies for Jack & JillStrategies for Jack & Jill

Transfer life insurance to an Transfer life insurance to an irrevocable life insurance trust.irrevocable life insurance trust.

Income to wife for life – Income to wife for life –

remainder interest to children.remainder interest to children.

2222

Strategies for Jack & JillStrategies for Jack & Jill

Establish by-pass trusts so Establish by-pass trusts so surviving spouse has right to surviving spouse has right to income, but keeps those assets income, but keeps those assets from being included in the from being included in the survivors estate when they die.survivors estate when they die.

2323

Strategies for Jack & JillStrategies for Jack & Jill

Provide for continuation of business?Provide for continuation of business?

Provide for charitable bequests?Provide for charitable bequests?

Provide for distribution of certain assets to Provide for distribution of certain assets to certain heirs?certain heirs?

Provide for distribution in trust for the Provide for distribution in trust for the grandchildren?grandchildren?

2424

Strategies for Jack & JillStrategies for Jack & Jill

What happens to the farm business if Jack What happens to the farm business if Jack is in an accident and is in a prolonged is in an accident and is in a prolonged comma?comma?

To compound the problem, what happens To compound the problem, what happens if Jill was killed in this accident – who will if Jill was killed in this accident – who will manage the financial affairs and make manage the financial affairs and make health care decisions for Jack?health care decisions for Jack?