Ethics and the characteristics of unethical behavior Friday, December 1, 2017 Ryan Gamble – Partner, Kansas City Tax Practice Leader Grant Thornton's Year End taxGuide Event Amanda Richardson – Senior Manager

Transcript

Ethics and the characteristics of unethical behavior

Friday, December 1, 2017

Ryan Gamble – Partner, Kansas City Tax Practice Leader Grant Thornton's Year End taxGuide Event

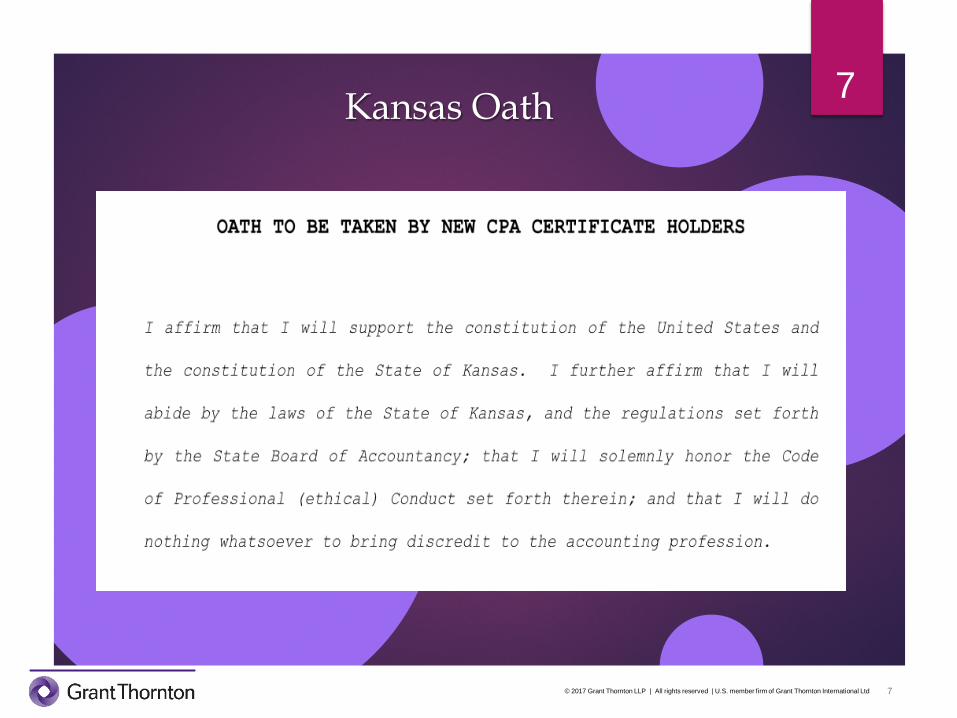

.300 Principles of Professional Conduct 0.300.010 Preamble .01 Membership in the American Institute of Certified Public

Accountants is voluntary. By accepting membership, a memberassumes an obligation of self-discipline above and beyond the requirements of laws and regulations.

.02 These Principles of the Code of Professional Conduct of the American Institute of Certified Public Accountants express the profession’s recognition of its responsibilities to the public, to clients, and to colleagues. They guide members in the performance of their professional responsibilities and express the basic tenets of ethical and professional conduct. The Principles call for an unswerving commitment to honorable behavior, even at the sacrifice of personal advantage. [Prior reference: ET section 51]

0.300.030 The Public Interest .01 The public interest principle. Members should accept the obligation to

act in a way that will serve the public interest, honor the public trust, and demonstrate a commitment to professionalism.

.02 A distinguishing mark of a profession is acceptance of its responsibility to the public. The accounting profession’s public consists of clients, credit grantors, governments, employers, investors, the business and financial community, and others who rely on the objectivity and integrity of members to maintain the orderly functioning of commerce.

.04 Those who rely on members expect them to discharge their responsibilities with integrity, objectivity, due professional care, and a genuine interest in serving the public. They are expected to provide quality services, enter into fee arrangements, and offer a range of services—all in a manner that demonstrates a level of professionalism consistent with these Principles of the Code of Professional Conduct.

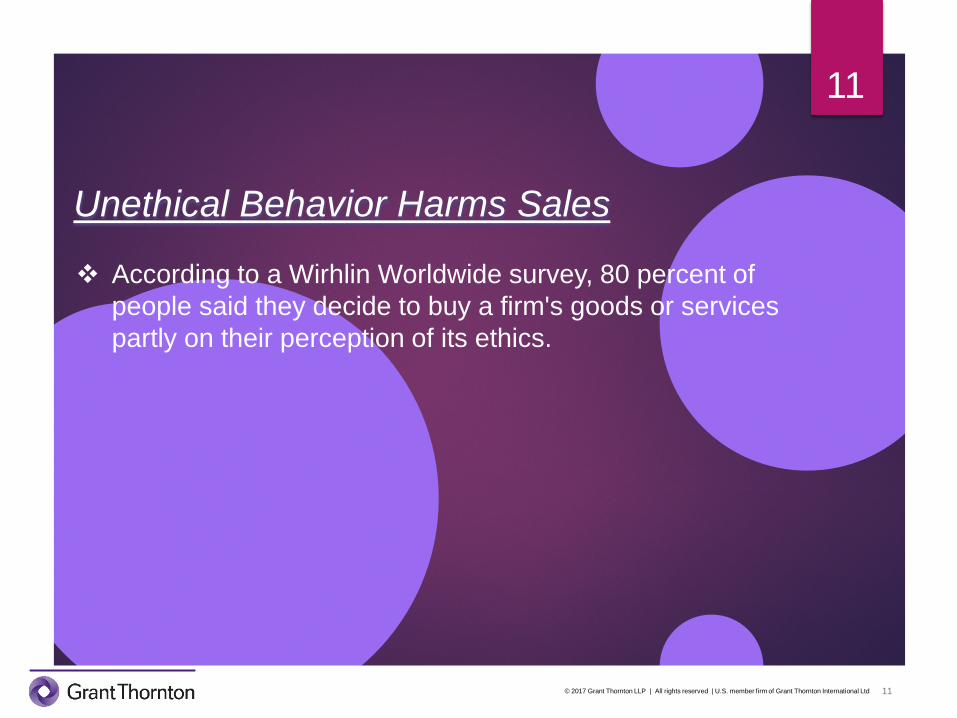

According to a Wirhlin Worldwide survey, 80 percent of people said they decide to buy a firm's goods or services partly on their perception of its ethics.

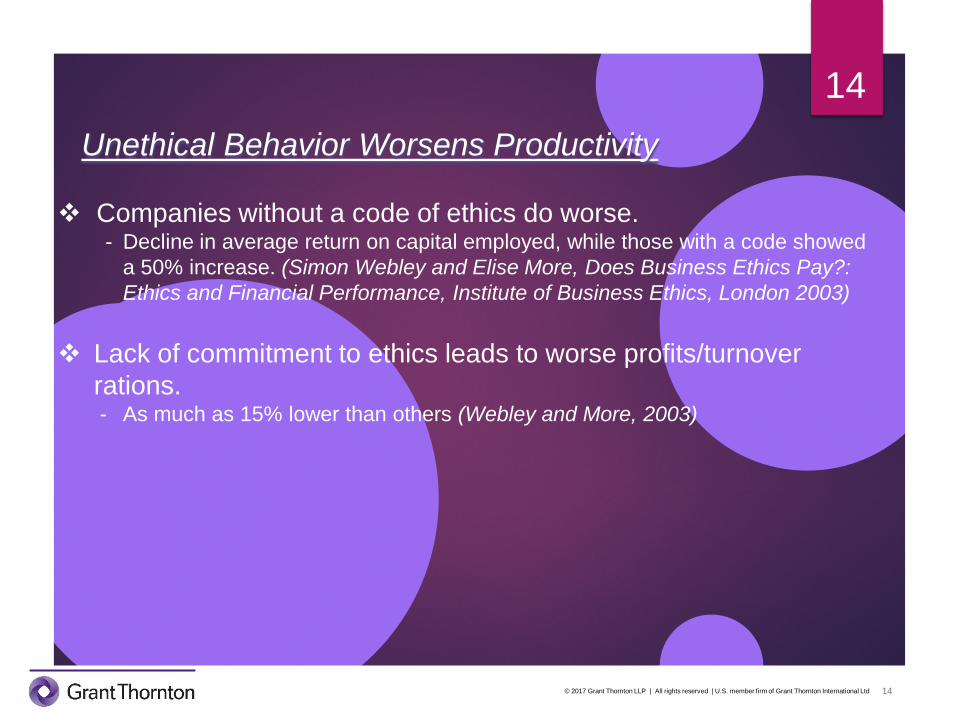

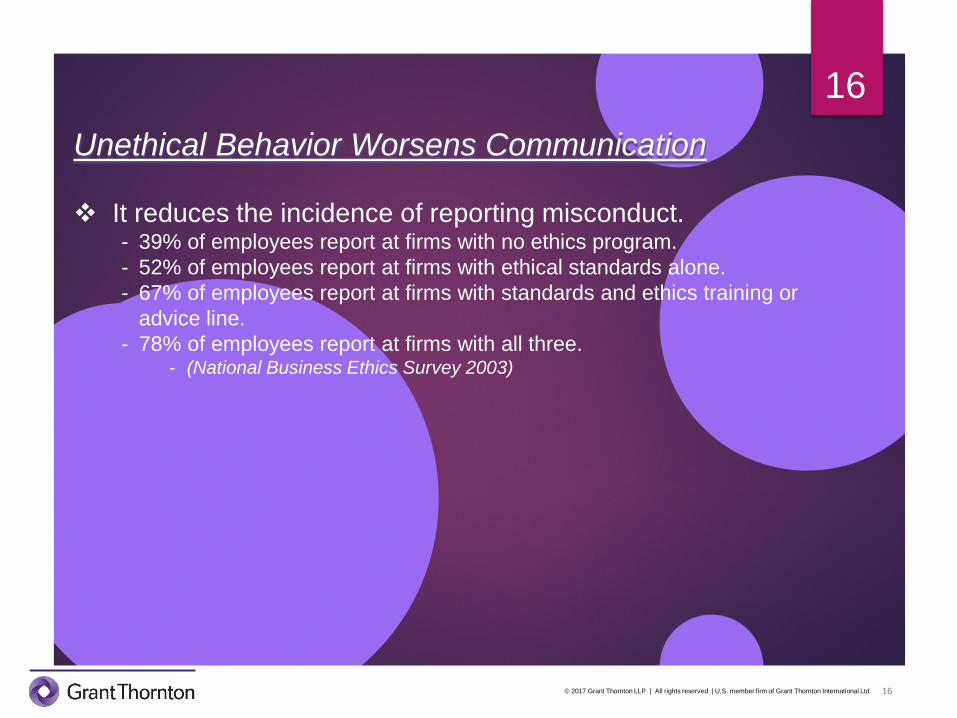

It reduces the incidence of reporting misconduct. - 39% of employees report at firms with no ethics program. - 52% of employees report at firms with ethical standards alone.- 67% of employees report at firms with standards and ethics training or

advice line.- 78% of employees report at firms with all three.

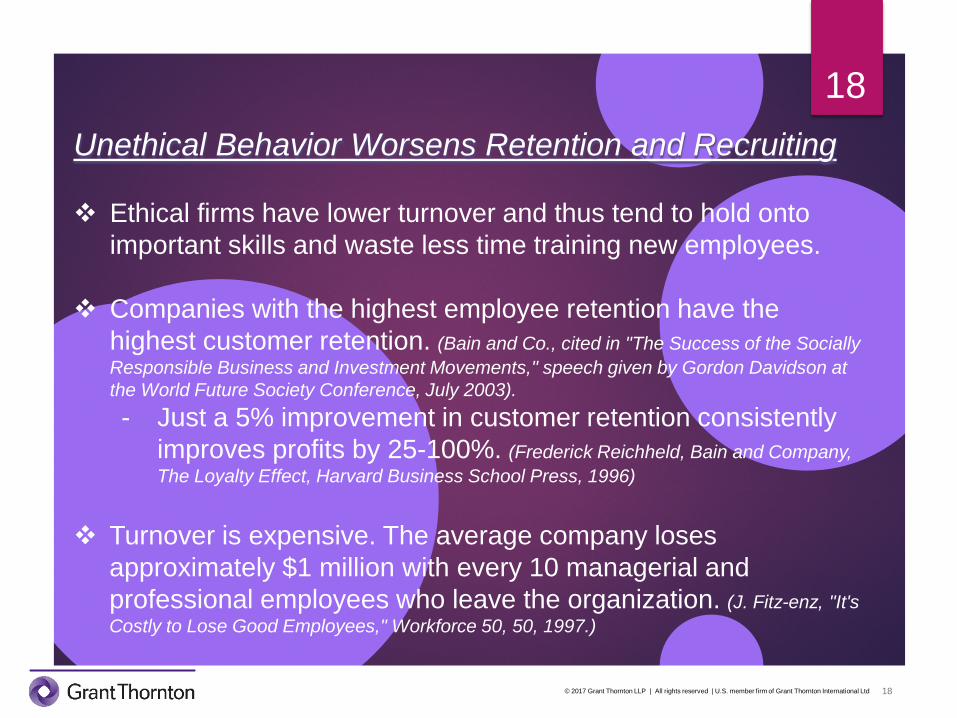

Unethical Behavior Worsens Retention and Recruiting

Ethical firms have lower turnover and thus tend to hold onto important skills and waste less time training new employees.

Companies with the highest employee retention have the highest customer retention. (Bain and Co., cited in "The Success of the Socially Responsible Business and Investment Movements," speech given by Gordon Davidson at the World Future Society Conference, July 2003).- Just a 5% improvement in customer retention consistently

improves profits by 25-100%. (Frederick Reichheld, Bain and Company, The Loyalty Effect, Harvard Business School Press, 1996)

Turnover is expensive. The average company loses approximately $1 million with every 10 managerial and professional employees who leave the organization. (J. Fitz-enz, "It's Costly to Lose Good Employees," Workforce 50, 50, 1997.)

Company: Telecommunications company; now MCI, Inc.

What happened: Inflated assets by as much as $11 billion, leading to 30,000 lost jobs and $180 billion in losses for investors.

Main player: CEO Bernie Ebbers

How he did it: Underreported line costs by capitalizing rather than expensing and inflated revenues with fake accounting entries.

How he got caught: WorldCom's internal auditing department uncovered $3.8 billion of fraud.

Penalties: CFO was fired, controller resigned, and the company filed for bankruptcy. Ebbers sentenced to 25 years for fraud, conspiracy and filing false documents with regulators.

Company: Tesco What happened: Inflated profits by $331M Main players: John Scouler, Carl Rogberg Christopher Bush How they did it: Coercion and false accounting. How they got caught: Finance personnel reported concerns to

HR both resigning shortly thereafter. Penalties: $160M fine and $109M investor compensation

scheme. Currently at trial with the three former executives charged with fraud by false accounting and fraud by abuse of power.

(Business Insider, "'The current environment has broken me': Tesco accounting scandal 'compromised' staff and sparked resignations", Thomas Colson, Oct. 3, 2017)

Misrepresenting hours worked Employees lying to supervisors Management lying to employees, customers,

vendors or the public Misuse of organizational assets Lying on reports/falsifying records Sexual harassment Stealing/theft Accepting or giving bribes or kickbacks Withholding needed information from employees,

customers, vendors or public

45

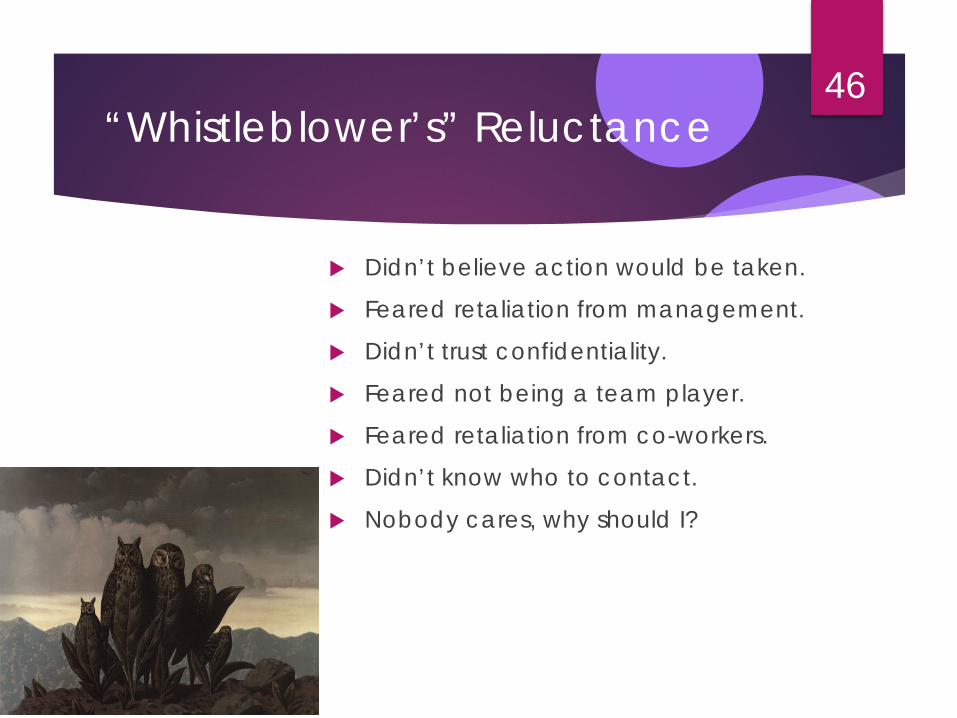

“Whistleblower’s” Reluctance

Didn’t believe action would be taken.

Feared retaliation from management.

Didn’t trust confidentiality.

Feared not being a team player.

Feared retaliation from co-workers.

Didn’t know who to contact.

Nobody cares, why should I?

46

Ethical Tips for Organizations

Develop a code of ethics. Communicate code and bake it into culture top-

down. Treat ethics as a process. Create open lines of communication. Set good examples. Educate employees – frame issues through

storytelling. Value forgiveness.

47

Benefits of Managing Ethics in the Workplace

Improves society.

Maintains a moral course in turbulent times.

Cultivates employee teamwork, productivity, morale and development.

Acts as an insurance policy.

48

Benefits of Managing Ethics in the Workplace (cont’d)

Establishes values for quality management, strategic planning and diversity management.

For a manager to share your resignation letter with your coworkers. For a coworker to refuse to speak to you. For a manager to tell your coworker that she plans to write you up. To fill a job without advertising it and giving other people a chance to

apply for it. For an employer to reveal your salary to your coworkers. To hold employees to different standards than others – favoritism. For your boss to ask you to pick up his lunch. For a manager to yell. To make you stay at the office and work if you decline to go on the

company cruise/outing. To share your performance stats with your coworkers. To have a random coworker deliver the message that you're fired. For your boss to require you to read a self-help book and test you on

To ban sugary foods from the office. For your employer to give your cell phone number to other employees. To fire you for companioning about something that is not illegal. To not hire someone because you dislike their relatives. To hire a family member over a more qualified unrelated candidate. For HR to forward your confidential emails to other people. To fire someone via email. To be a jerk. For your boss to require you to put little bags of wedding favors

together.

- Ethics Alarms.com, November 5, 2013

51

Ethical Dilemmas CaseBy Carnegie Mellon Tepper School of BusinessAugust 1, 2002

The company for which Chris is controller is facing financial difficulties and needs a bank loan to continue in existence.

Chris and Robin, the CEO, know a material receivable is probably uncollectable, but no adjustment to the allowance account has yet been made.

Robin, the CEO, fears that booking the allowance adjustment will cause the auditor to report the construction company’s shaky financial position in the audit report.

Without a clean audit opinion, the bank will likely refuse the loan, and the construction company may fail.

Diana is new on the job. Diana suspects William of siphoning off the extra sales revenue. She has no proof to back up her suspicions. William has been consuming conspicuously. John may not suspect William of wrongdoing. Poor internal control and a lack of segregation of duties exist. Evidently, franchise owners are not aware of the problem or trust John, who