426

Euromoney Encyclopedia of Islamic Finance

Edited by Aly Khorshid

12222234567891011123111456789201111234567893011112343567894011112344222

EUROMONEY

BOOKS

Published by

Euromoney Institutional Investor PLC

Nestor House, Playhouse Yard

London EC4V 5EX

Tel: +44 (0)20 7779 8999 or USA 11 800 437 9997

Fax: +44 (0)20 7779 8300

www.euromoneybooks.com

E-mail: [email protected]

Copyright © 2009 Euromoney Institutional Investor PLC and the individual contributors

ISBN: 978 1 84374 544 0

This publication is not included in the CLA Licence and must not be copied without the permission

of the publisher.

All rights reserved. No part of this publication may be reproduced or used in any form (graphic, elec-

tronic or mechanical, including photocopying, recording, taping or information storage and retrieval

systems) without permission of the publisher. This publication is designed to provide accurate and

authoritative information with regard to the subject matter covered. In the preparation of this book,

every effort has been made to off the most current, correct and clearly expressed information as

possible. The materials presented in this publication and for informational purposes only. They reflect

the subjective views of authors and contributors and do not necessarily represent current or past

employers, the editor or the publisher engaged in rendering accounting, business, financial, invest-

ment, legal, tax or other professional advice or services whatsoever and is not liable for any losses,

financial or otherwise, associated with adopting any ideas, approaches or frameworks contained in

this book. If investment advice or other expert assistance is required, the individual services of a

competent professional should be sought.

Typeset by Phoenix Photosetting, Chatham, Kent

Printed by TJ International, Padstow, Cornwall

The views expressed in this book are the views of the authors and contributors alone and do not reflect the

views of Euromoney Institutional Investor PLC. The authors and contributors alone are responsible for the

accuracy of content.

Contents

Foreword viiiPreface xAbout the editor xiiAbout the contributors xiiiIntroduction xxi

Part I – Overview of Islamic finance

1 Basic elements of Islamic finance 3Aly Khorshid

2 Fundamentals of Islamic finance 23Aly Khorshid

3 Shari’a standard asset wealth management and will-writing(wasiyah) mechanisms 38Mohammed Ma’sum Billah

4 The role of Shari’a advisors in the development and enhancement of Islamic securities 49Aznan Hasan

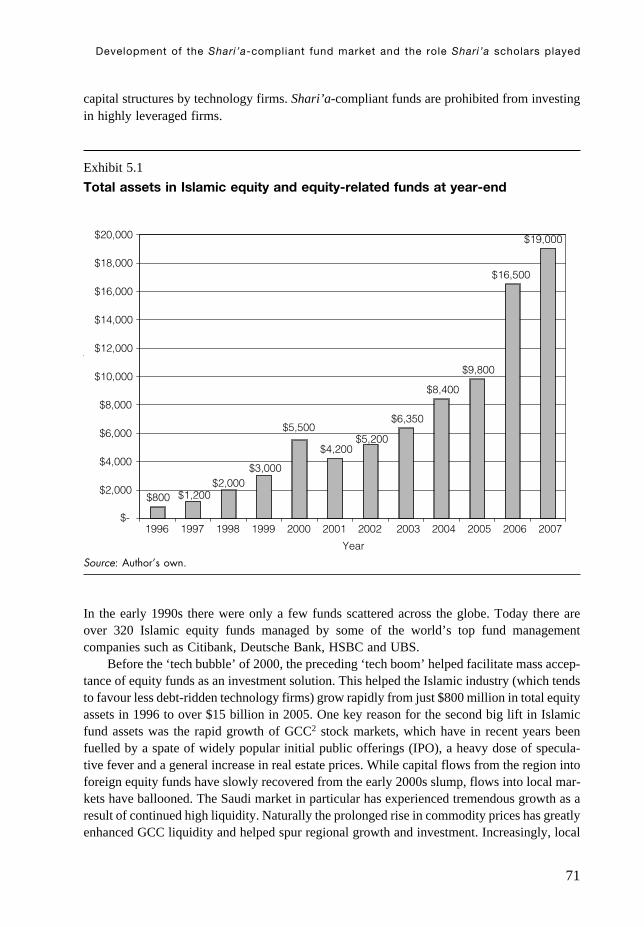

5 Development of the Shari’a-compliant fund market and the role Shari’a scholars played 70Tariq Al-Rifai

6 Corporate governance in Islamic finance 79Nasser Saidi

7 Islamic finance: can it contribute something worthwhile to global finance? 99M. Umer Chapra

12222234567891011123111456789201111234567893011112343567894011112344222

v

Part II – Application

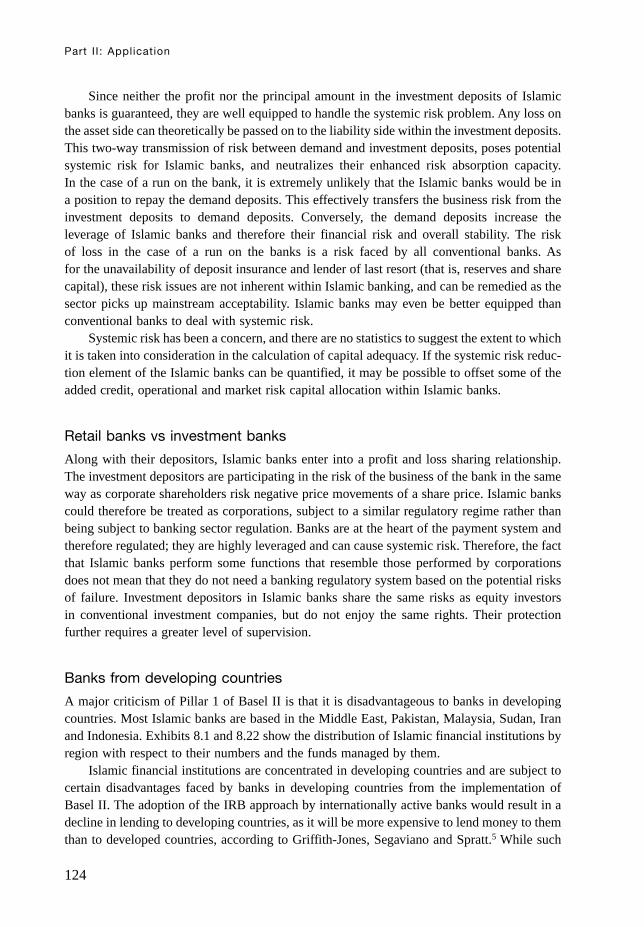

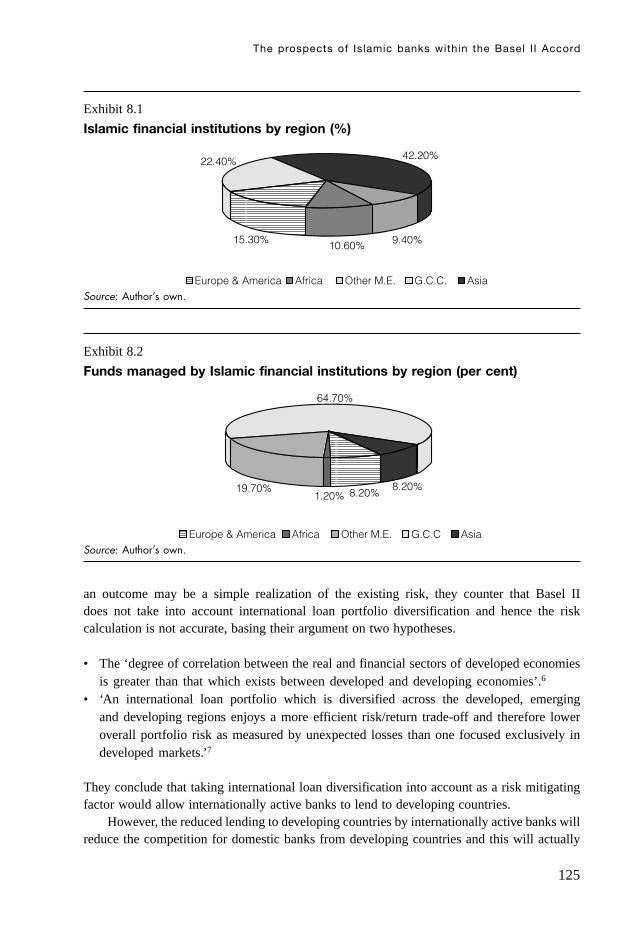

8 The prospects of Islamic banks within the Basel II Accord 115Aly Khorshid

9 Al-suyulah: the Islamic concept of liquidity 131Mohd Daud Bakar

10 Islamic finance across the GCC and cross-border considerations 147Hari Bhambra

11 Money laundering and Islamic banking 160Aly Khorshid

12 Globalization of the Islamic banking and finance industry 171Dourria Souheil Mehyo

13 Standard & Poor’s views on the growth and diversification of Islamic finance 183Mohamed Damak

14 Role and responsibilities of Shari’a scholars in Shari’a advisory services 195Mohammed Akram Laldin

15 Islamic banking tolerates challenges to risk management 208Aly Khorshid

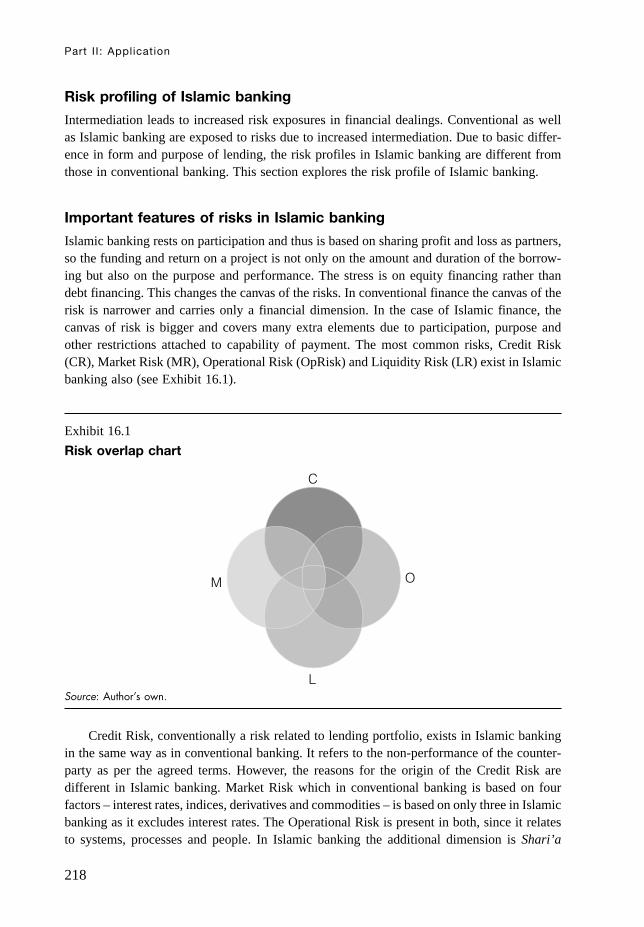

16 Risk structures of Islamic finance contracts 215Sunil Kumar

Part III – Products

17 The potential of Islamic finance in the global market 227Aly Khorshid

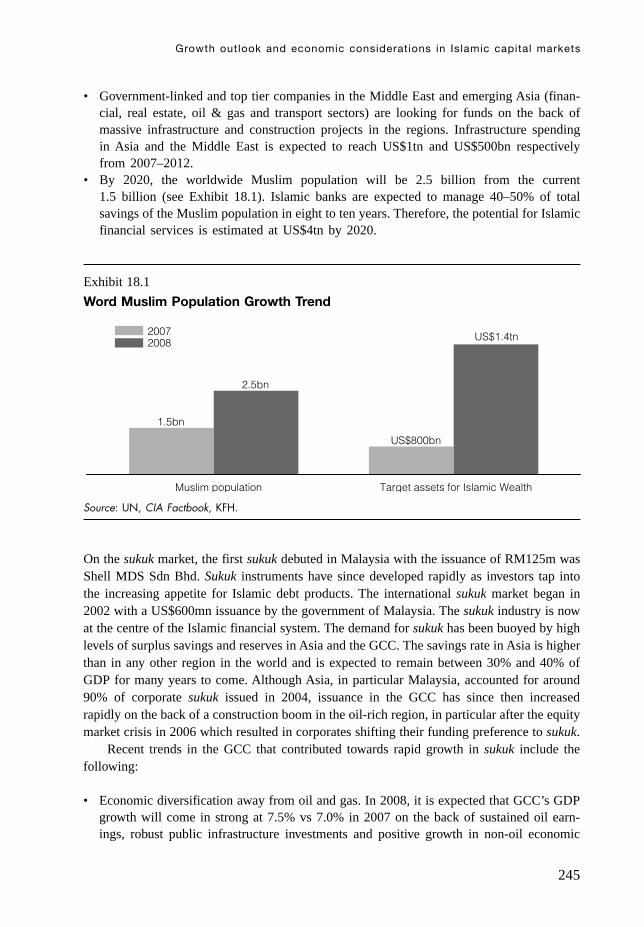

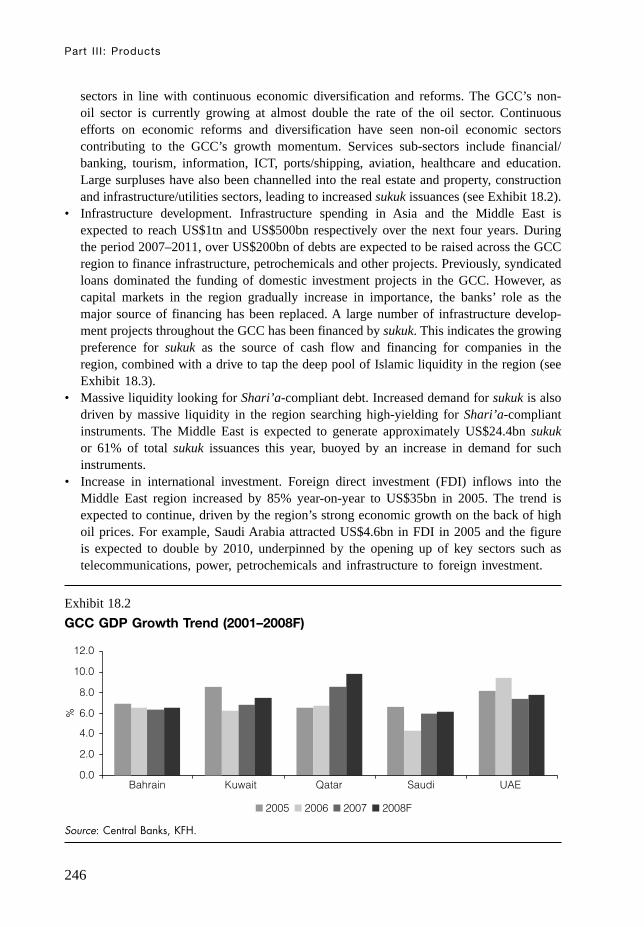

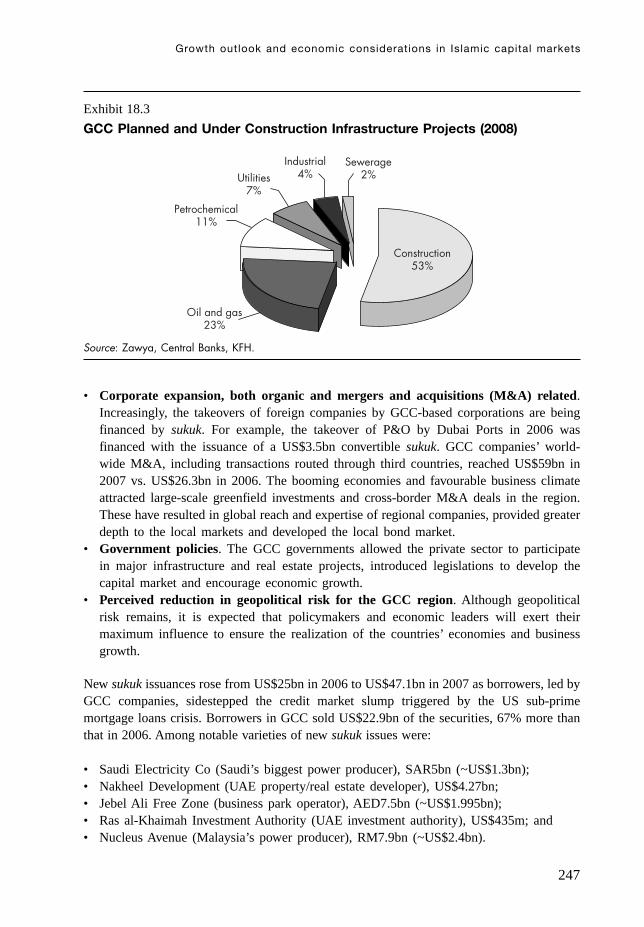

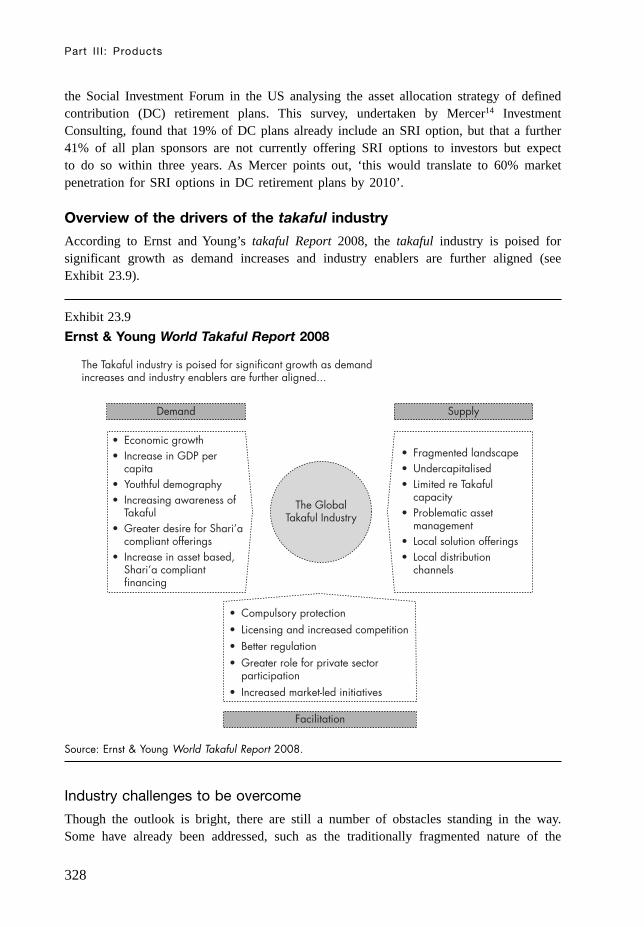

18 Growth outlook and economic considerations in Islamic capital markets 244Baljeet Kaur Grewal

19 Understanding derivatives within Islamic finance 254Aly Khorshid

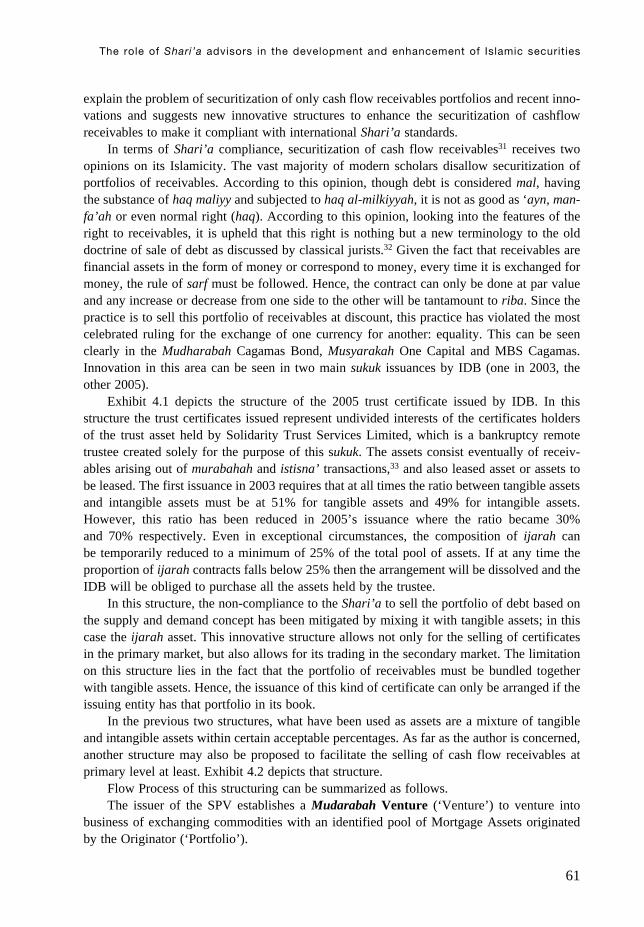

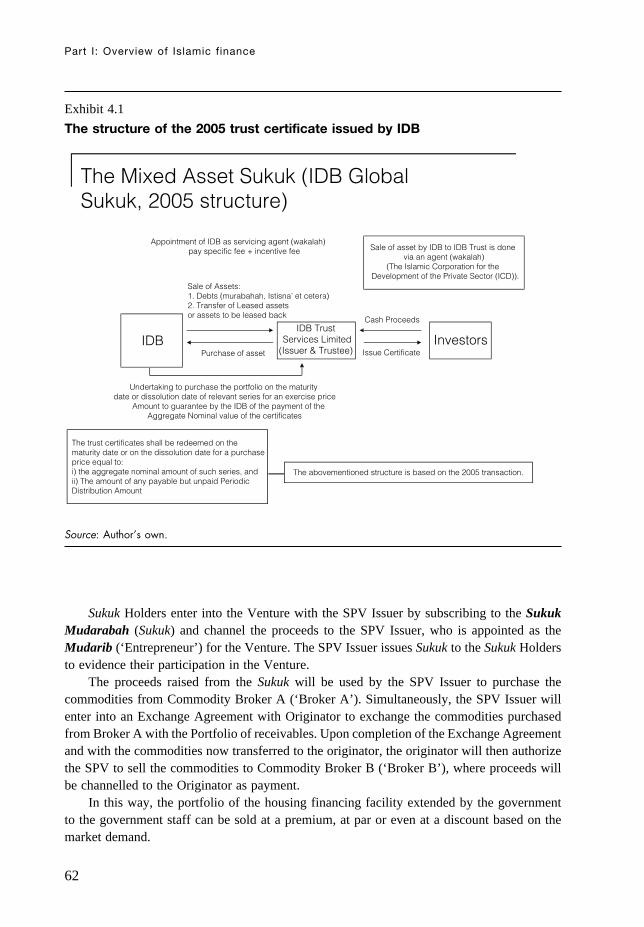

20 Capital market transparency and fragmentation: lessons for Islamic markets 270John Board

Contents

vi

21 Sukuk and securitization 279Aly Khorshid

22 Development of a secondary sukuk market 301Aly Khorshid

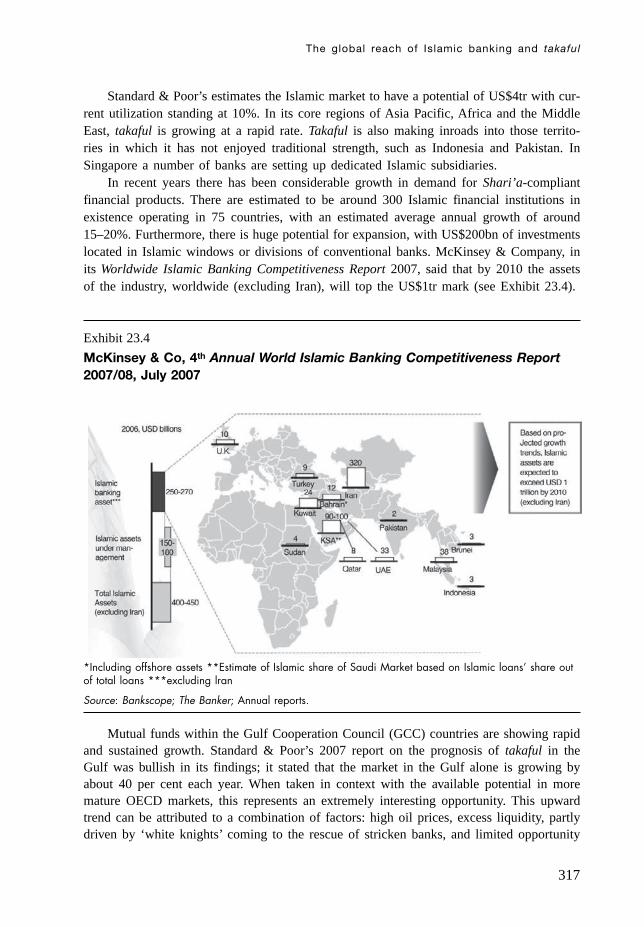

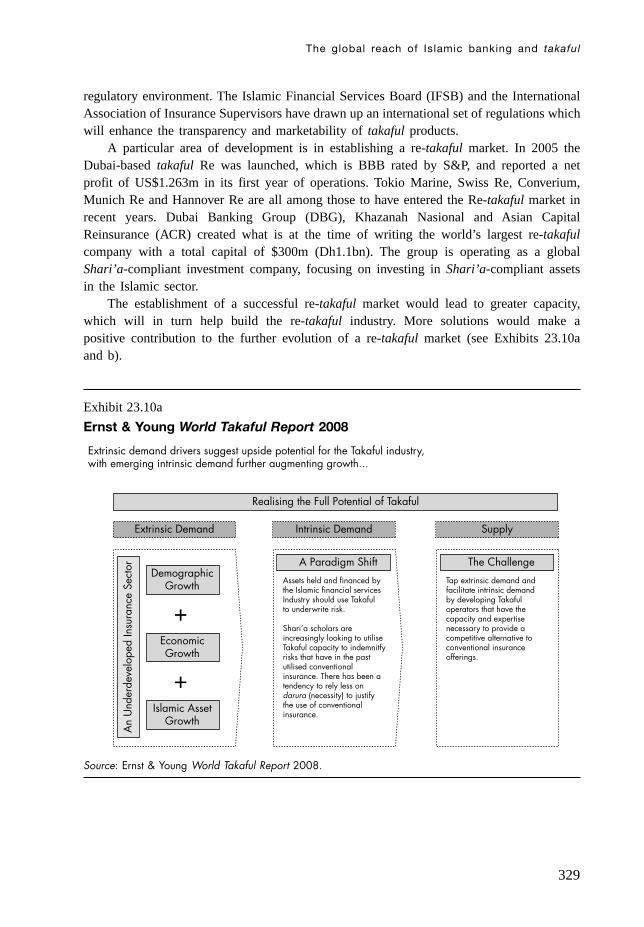

23 The global reach of Islamic banking and takaful 312Sohail Jaffer

Part IV – Special issues and special considerations

24 The role of women in Islamic finance 335Aly Khorshid

25 Offshore structuring 346Tahir Jawed

26 Ethical investment versus Islamic investment 352Aly Khorshid

Part V – Tax and regulatory issues

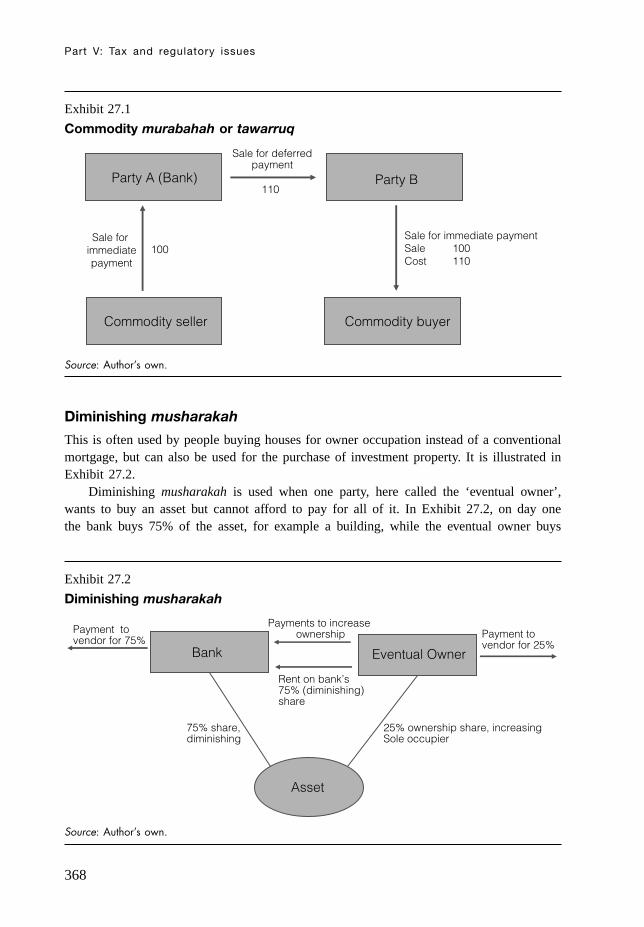

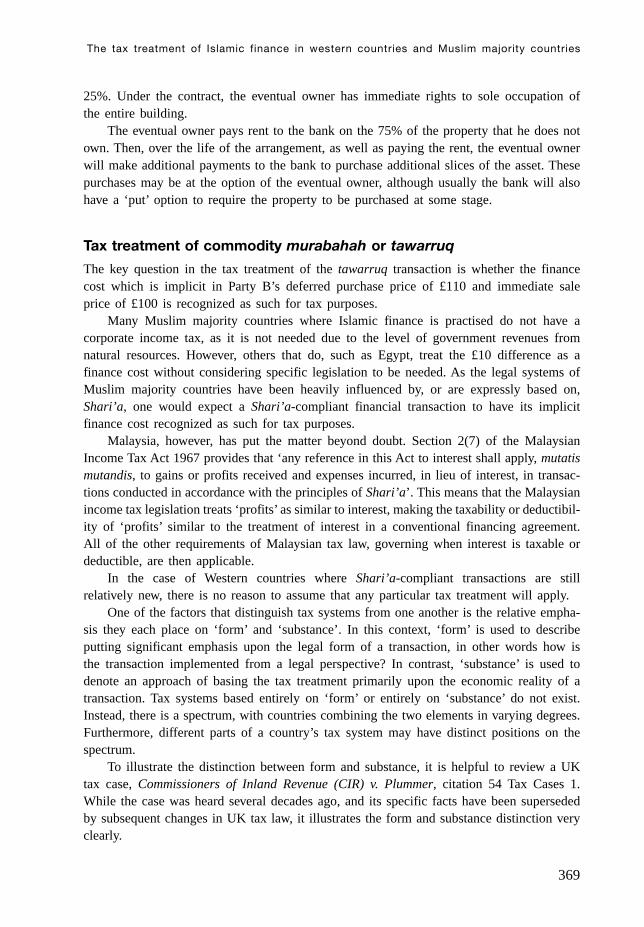

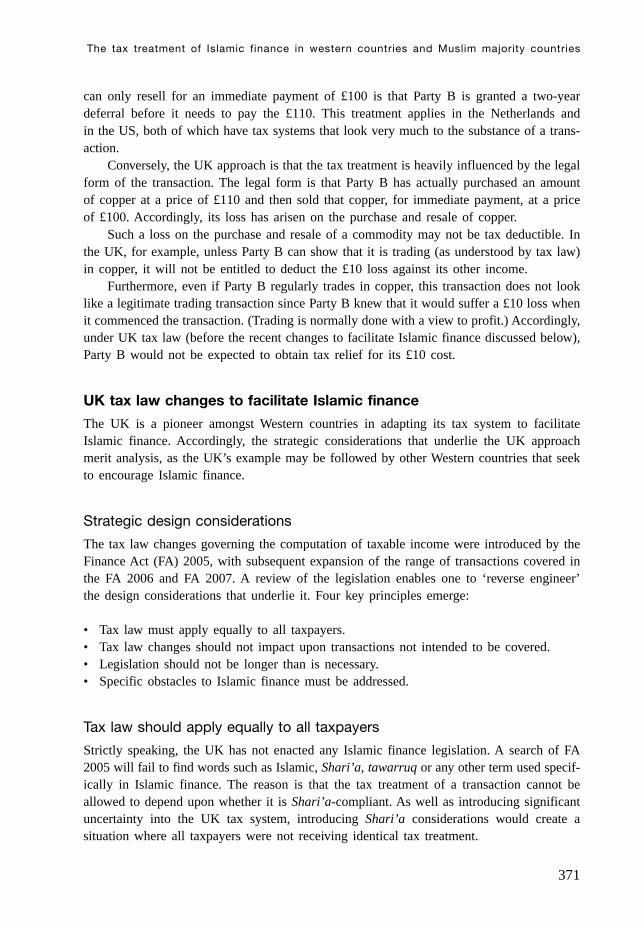

27 The tax treatment of Islamic finance in western countries and Muslim majority countries 367Mohammed Amin

28 The regulation of Shari’a-compliant financial services and products: approaches and challenges 377Andrew Henderson

Glossary of Islamic finance 386

12222234567891011123111456789201111234567893011112343567894011112344222

Contents

vii

Foreword

In the last five years the world has witnessed a rising interest in Islamic finance. The Islamicfund industry, specifically in Asia, is undergoing significant growth. Most of it has beendemonstrated strongly in Muslim countries such as Malaysia and in the Gulf region, butthe principles are spreading into non-Muslim countries too.

Historically speaking, there have always been similar funds and investments that havekept within the rules of other religions such as Judaism and Christianity. Investments drivenby religious values are considered ‘ethical investments’, and it can be argued that Islamicinvestment fits this category and has many aspects in common with secular ethical finance.Islamic investment as we know it today was driven in the 1960s and 1970s by consumerdemand; nowadays it has expanded to organizations and institutions.

Surplus wealth derived from oil sales, especially in the Gulf region, meant there hadto be ways to reinvest, which in turn led to this growing need in Islamic countries to focuson Islamic finance. Saudi Arabia and the United Arab Emirates have provided good exam-ples of how to establish such markets. Once the infrastructure and regulations were set inplace, the ambition to attract money from other international markets grew; and now thegoal is to maintain and sustain interest in investment from within the originating countries.

The Malaysian government, under the Islamic Financial Centre, has led the way bypresenting certain incentives to make Kuala Lumpur into a centre for Islamic finance.Malaysia currently represents the main source of Islamic bonds, sukuk, insurance and takaful,and is considered the second largest market after Saudi Arabia. Markets such as the UnitedArab Emirates and Bahrain are rapidly rising in stature. We have even witnessed interestin this particular sector in non-Muslim countries, such as Hong Kong, Singapore and Japan.

In recent years, technology, resources, infrastructure and indices have become vitaltransformation tools, driving further growth. While there is still the belief that rudimentaryrules and restrictions may interfere with this market’s growth, a large number of listedstocks are Shari’a-compliant and an integral part of Islamic finance.

Nonetheless, no one in the industry would deny that important challenges remain.Introducing instruments and tools was not straightforward, and methods of regulation needto be consistent with conventional financial instruments. This looks like increasing thedemand for transparency, governance and regulation, which are critical in Islamic finance,and the industry should not be outside the boundaries of normal regulation.

Another reason to establish such markets was to avoid market volatility, especially inthe Western market. The September 11 attacks in 2001 also put pressure on Muslim invest-ments abroad, especially in the US, which drove investment back home to Muslim countries.Once these markets proved their successful performance and confidence, more interest fromthe West returned to these markets. As these markets grow, more interdependence develops,

viii

leading to greater complexity. Market authorities need to pay attention to the impact ofmarket volatilities to which Islamic markets are not immune, just like conventional markets.

Other current challenges for market growth stem from access to specialists: trainingand education are essential, and addressing this issue is one of the most pressing problemsat present. The Encyclopedia of Islamic Finance is a collection of scholarly work and knowl-edge from this vibrant sector. Its purpose is to bring understanding and awareness of theimportance of this fast-growing industry. The book demonstrates in easy and simple languagethe essentials of Islamic finance from the theoretical and ethical viewpoint of Islam to up-to-date capital market products, derivatives, securitization, sukuk and the development ofsecondary sukuk markets. All fundamentals of Islamic finance; Shari’a scholars’ responsi-bilities and roles; tax issues; offshore companies; legal issues; indices; corporate governance;takaful and re-takaful; and womens’ role in Islamic finance are dealt with in these pages.

The material included in this book was built upon depth of research and is intendedto provide a valuable reference work for scholars, academics and specialists working in thefield.

Lubna bint Khalid Al QasimiMinister of Foreign Trade to the United Arab Emirates

Former Chairperson of UAE Securities and Commodities AuthorityOctober 2008

Foreword

ix

x

Preface

This Euromoney Encyclopedia of Islamic Finance is a collection of chapters from a numberof diverse sources within the finance industry, governmental financial departments andacademia. It aims to bring up-to-date, the debates surrounding Islamic finance, by tappinginto the breadth of knowledge and expertise that is creating a hugely successful industry.Some of the chapters have already been published in other publications or online; somestarted their lives as academic papers, and a number were commissioned especially for thisbook. The authors themselves are of many nationalities, but the majority are from, orcurrently reside in, the Middle East, Malaysia, Pakistan, Europe or the USA. Each has beenchosen for his or her expertise in a particular aspect of Islamic finance with the ultimateaim of producing a rounded, comprehensive encyclopedia on this vibrant and growing sectorof the finance industry.

Readership

Islamic finance is continuing to draw attention and respect from at least two important groups.First are the world’s Muslims themselves. Saving and investing in Western-style banks

has been out of the question for pious Muslims, although many were forced to use secularinstitutions as there was no alternative. For example, high street bank accounts would havebeen opened when an employer only paid wages electronically. Loans caused further prob-lems because of interest, and links with pork, alcohol, pornography, weapons and otherforbidden industries, placed immovable obstacles in the path of would-be investors whoheld their Islamic faith dear. The Islamic banking and finance industry, whose every instru-ment has been scrutinized, analyzed and often reconstructed by respected scholars, juristsand government-appointed bodies, gives investors the reassurance that every possible stephas been taken to ensure Shari’a compliancy. Does every Muslim agree with the reliabilityof every instrument? Of course not. Controversy surrounds many of them, but rather thancausing a defeatist attitude, it has forced the creators and proponents to argue their casemore deeply. The industry as we know it today is in its infancy compared with secularbanking; hopefully the arguments will soon be won and lost and anyone belonging to aparticular branch of Islam will be able to invest in instruments with a completely clearconscience. This collection of works will hopefully play its part.

The second interested group has encompassed those within the conventional financeindustry. To those versed in the orthodoxy of the free market, a system of finance thatplaces limitations on business can at first glance inspire bewilderment. But there is some-thing in Islamic finance that inherently creates stability and long-termism, and thereforeopportunity. At the time of compiling this encyclopedia in 2008, the world’s financial

institutions have been in turmoil, with several notable banks requiring help from centralreserves, either being bought out or simply collapsing. Analysis of the causes is still ongoing,but most observers point the finger at rampant and often reckless speculative dealings andthe provision of easy credit, particularly to individuals unable to service their debts. Withthe house of cards collapsing around us, governments and a somewhat reluctant financeindustry are looking for solutions. They could do a lot worse than looking in the directionof Islamic finance; and indeed many of them already are. It has been convincingly arguedthat the so-called ‘credit crunch’ simply could not have happened if an Islamic attitude toresponsible lending were followed. Without the inability to deal with pork, alcohol, et cetera,the two models would be cousins working in parallel; but the basis of Islamic finance andthe natural aversion to excess might turn out to be a lifeline for western banking.

It is for these two groups detailed above, and indeed anyone interested in Islam, thatthis encyclopedia might be of interest.

A note on standardization and transliteration

When collecting together chapters from a number of diverse sources, one of the editor’sfirst decisions is how to standardise spelling, annotation and transliterations.

As far as spelling English words is concerned, it was decided early on to minimise theediting by limiting it to standardizing spellings using the ‘Mid-Atlantic’ orthography, a mixtureof British English (for example, colour, centre not color, center) and using -ize spellingsinstead of –ise, as is usual in academic works. Footnotes were changed to notes at eachchapter’s end. Figures and tables referred to as ‘above’ or ‘below’ were changed to numberedexhibits to allow for typographical differences between manuscript and printed page. Otherthan these minor changes and general editing, the chapters are exactly as their originals.

This also means that transliterations of Arabic words remain faithful to their authors’tastes and traditions. This does actually lead to a good deal of diversity, but the editor feltthat demonstrating this diversity of spellings is beneficial to those studying the subject; inaddition it was never the editors’ intention to impose one system of presenting Arabic ontothis English work’s readers.

Some authors take a very European approach to transliterating Arabic, ignoring alldiacritical marks; others do the same but insist on italicizing the words. Another group triesto faithfully reproduce the exact vocalization using the Roman alphabet, and within thisgroup there is a degree of variation between spellings. Readers soon become accustomedto these various spellings, and it does reflect the usage in the outside world. In this work,hamzas are represented as apostrophes unless text in Arabic is presented.

Taking one example – Shari’a – it can be seen that spellings vary, but it is alwaysobvious what the word is; this is typical of Arabic transliteration. A selection is: Sharia,Shariah, Shari’a, Shari’ah, Syariah, Syaria, Syari’ah, and this list is by no means exhaustive. Some writers do not capitalize the S, although as a proper noun it should startwith a capital in written English. Retaining phonetic integrity between different languagesand alphabets is probably impossible without writing entire books in the InternationalPhonetic Alphabet (IPA), but no doubt there would still be conflicts caused by regionalpronunciations.

Preface

xi

About the editor

Aly KhorshidAly Khorshid has been involved with financial institutions for over two decades, andpossesses comprehensive skills and knowledge on Islamic finance. He is a recognized experton Shari’a-compliant finance within Islamic law, Islamic moamlat and Islamic contracts.He is partner and CEO of Islamic Finance with Elite Horizon economic consultancy, andhas responsibilities for structuring, endorsing and advising on Shari’a-complaint products.He has particular experience in capital and stock market products. He served as consultantto the Central Bank on establishing an Islamic banking system within the Central Bank’sregulatory policies and corporate governance. He is actively involved in structuring theIslamic home purchase scheme and Islamic capital market products. He is experienced inconducting comprehensive due-diligences on financial institutions to identify potential invest-ment opportunities. He started his career with international marketing and trade: his firstShari’a board membership was with Bank Al-Baraka (the first Islamic bank in the UK).His roles include dealing with the UK Treasury and Bank of England departments in rela-tion to the regulation of Islamic banking issues. He is now serving as a Shari’a boardmember in several Islamic institutions. He holds a PhD in Islamic studies and economicsfrom the University of Leeds (UK), and studied Fiqh and Shari’a at Al-Azhar University(Egypt). He also holds a Masters degree in management (UK). His publications includeIslamic Insurance: A Modern Approach to Islamic Banking, and the Encyclopedia of IslamicFinance. He has also had many articles published on Islamic finance. He is a trustee memberof Academy UK; a member of the Institute of Management Consultancy (UK); and a visitinglecturer at El-Azhar University (Egypt), the School of Oriental and African Studies (SOAS),and the University of London in Islamic finance. He is a regular speaker on Islamic financeissues at conferences and on television.

xii

About the contributors

Mohamad AkramDr Mohamad Akram is currently the Executive Director of the International Shari’ahResearch Academy for Islamic Finance (ISRA). Prior to joining ISRA, he was an AssistantProfessor at the Kulliyah of Islamic Revealed Knowledge and Human Sciences, InternationalIslamic University, Malaysia (IIUM). In the period 2002–2004, he was a Visiting AssistantProfessor at the University of Sharjah, Sharjah, United Arab Emirates. At present, he is aMember of HSBC Amanah Global Shari’a Advisory Board, a Member of Yassar LimitedShari’a Advisory Board, Chairman of HSBC Amanah Malaysia Berhad’s Shari’a Committee,Chairman of HSBC Takaful Malaysia Berhad Shari’a Committee, a Member of the IslamicAdvisory Board of HSBC Insurance Singapore, Shari’a Advisor to Equity Trust MalaysiaBerhad and Shari’a advisor to ZI Syariah Advisory Malaysia. In addition, he is also anAssociate Consultant of the International Institute of Islamic Banking and Finance (IIIF),Kuala Lumpur. Dr Akram holds a BA Honours degree in Islamic Jurisprudence andLegislation from the University of Jordan, Amman, Jordan and a PhD in the Principles ofIslamic Jurisprudence (Usul al-Fiqh) from the University of Edinburgh, Scotland, UK. Hehas presented many papers related to Islamic Banking and Finance and other Fiqh topicsat National and International level and has conducted many training sessions particularlyon Islamic Banking and Finance for different sectors since 1999. He is a registered ShariahAdvisor for the Islamic Unit Trust with the Securities Commission of Malaysia and hasacted as Shari’a advisor in the issuance of several sukuk. In addition, he is also a prolificauthor of academic works specifically in the areas of Islamic Banking and Finance.

Tariq S Al-RifaiTariq Al-Rifai is Founder and Chairman of Failaka Advisors. He is often quoted in themedia and viewed as a leading authority on Islamic equity and private equity funds. Tariqhas been involved in Islamic funds and investment products for over a decade. He has beencalled on for his insight into the Islamic Fund industry. He has also advised institutionalclients on Islamic funds and fund structures. He is an active speaker at Islamic Financeevents around the world and has previously presented at events in Bahrain, Cambridge (US),Dubai, Kuala Lumpur, London and New York.

Failaka was established in 1996 and published its first report in 1997. Shortly after,the firm debuted its annual Failaka Islamic Fund Awards. While continuing to build Failaka,Al-Rifai became a partner in the London office of The International Investor, a Kuwait-based investment bank, where he was responsible for building distribution relationships withfinancial institutions in Europe and the Middle East. Al-Rifai went on to become VicePresident of Islamic Banking at HSBC Bank in New York, where he was responsible for

xiii

launching HSBC’s Islamic finance programme in the USA. Al-Rifai is currently VicePresident at UIB Capital in Chicago, the US private equity arm of the Bahrain-based UnicornInvestment Bank.

Al-Rifai earned his BS in International Finance at St Cloud State University inMinnesota, and earned his MBA in International Management at DePaul University inChicago.

Mohammed AminMohammed Amin is a partner in PricewaterhouseCoopers LLP and leads PwC’s IslamicFinance practice in the UK. His personal specialization is taxation, both of Islamic Financeand general financial institutions. Amin is a member of the HM Treasury Islamic FinanceExperts Group, established by the Economic Secretary to the Treasury to advise theGovernment on Islamic Finance strategy.

Within PwC, Amin is also an elected member of PwC’s Supervisory Board and serveson the firm’s audit committee. Externally, Amin is a Council Member of the CharteredInstitute of Taxation (CIOT); he serves on the Policy & Technical Committee of theAssociation of Corporate Treasurers (ACT); chairs the Business and Economics Committeeof the Muslim Council of Britain. He is a member of the Editorial Advisory Board of NewHorizon, the magazine of the Institute of Islamic Banking and Insurance, and is Vice-Chairman of the Conservative Muslim Forum.

Amin graduated in mathematics from Clare College, Cambridge, UK. He is a Fellowof the Institute of Chartered Accountants in England & Wales, an Associate Member of theACT, and a Fellow of the CIOT.

Amin was recently included in the judging panel for the Muslim Power 100, a list ofthe hundred most influential Muslims in the UK, as well as being included in the list itself.Many of his articles and presentations can be found on his blog http://pwc.blogs.com/mohammed_amin/islamicfinance.

Mohammed Daud BakerDr Mohammed Daud Bakar received his first degree in Shari’a from the University ofKuwait in 1988 and obtained his PhD from the University of St Andrews, UK in 1993. In2002, he completed his external Bachelor of Jurisprudence at the University of Malaya. DrDaud is member of the Central Shari’a Advisory Council of the Central Bank of Malaysiaand Securities Commission of Malaysia. He also serves as a member of the Shari’a boardof Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), theInternational Islamic Financial Market (Bahrain), the Dow Jones Islamic Market Index,Unicorn Investment Bank (Bahrain), and BNP Paribas.

Hari BhambraHari has a remarkable reputation in Financial Services, both from a regulatory and industryperspective. She has been part of the development team of two regulatory agencies to inte-grate and develop a new regulatory regime. Her career began at the Financial ServicesAuthority in London where she drafted aspects of the FSA regulations. She was also partof the development team which created the Dubai Financial Services Authority in DIFC,

About the contributors

xiv

Dubai where she created the ‘Shari’a Systems’ regulatory model for the regulation of IslamicFirms.

Hari’s commercial training began at Goldman Sachs in London where she was respon-sible for implementing and monitoring FSA systems and controls on behalf of the bank.After Goldman Sachs, Hari joined a boutique compliance consultancy in London as a SeniorConsultant before moving to Dubai.

Hari has also been instrumental in seeking to remove barriers to cross-border marketingof Islamic products under the Mutual Recognition Arrangement signed by the SC and DFSA.

She was also appointed as the sole advisor by Financial Services Volunteer Corps US(FSVC) to advise the Central banking agency of a secular Islamic jurisdiction on the intro-duction of Islamic Financial products. In 2007, Hari left the DFSA and together with twostrategic partners, established Praesidium LLP, a regulatory and client advisory firm.

Md. Ma’sum BillahProfessor Billah was born in 1968 and holds a DBA (e-Commerce), PhD (Takaful), MBA (i-REITs), MCL (Comparative Law), MMB (Hadith-Corporate Mu’amalat) and LLB (Hons).He is the former Director of the Islamic Chamber of Commerce and Industries (ICCI) incharge of Global Trade & Investment Cooperation (OIC Countries). Billah has also beenglobally noted as an Islamic corporate & financial advisor, trainer, presenter, writer, commen-tator, reviewer and publisher in different parts of the world on: Shari’a compliance; appliedIslamic banking; finance; Islamic project & infrastructure finance; restructuring of Islamicfinancial instruments; Islamic financial product innovations; takaful; re-takaful; Islamic business; Islamic wealth, asset & property management; Islamic capital markets; bonds &sukuk markets; Islamic money markets; Islamic investment; corporate mu’amalat’ i-REITs;and Islamic e-commerce. He also holds the position of President, Chairman, Director,Advisor, Adjunct-Professor and Member of several institutions, NGOs and professionalbodies at international, regional and local levels. Currently, he is the Group ExecutiveChairman of the Middle Eastern Business World (MBW) Group of companies. Billah isalso the Founder of a leading Islamic finance site: http://www.applied-islamicfinance.com.For further enquiries contact [email protected].

John BoardJohn Board is Professor of Finance and Director of the ICMA Centre, Henley BusinessSchool, UK. He has lectured on many aspects of finance at a number of universities andbusiness schools around the world. His overall research agenda is characterized by the application of finance theory to real world problems and issues. In pursuit of this, he hasbeen widely published in books, academic and professional journals, as well as radio andtelevision. His recent research has been in the area of market regulation in which he hasacted as consultant to, among others, the House of Commons, the Financial ServicesAuthority, the City of London Corporation, and a number of London’s financial markets.

Among his recent publications are: Transparency and Fragmentation: Financial MarketRegulation in a Dynamic Environment (Palgrave, 2002), and The Competitive Position ofthe Gulf as a Global Financial Centre (City of London Corporation, 2008).

About the contributors

xv

M Umer ChapraM Umer Chapra, born in February 1933, is presently serving as Research Advisor at theIslamic Research and Training Institute (IRTI) of the Islamic Development Bank (IDB).Prior to joining IRTI in November 1999, he worked at the Saudi Arabian Monetary Agency(SAMA), from where he retired as Senior Economic Advisor after a long service of 35years. This post had actively involved him in different phases of Saudi Arabia’s hectic paceof economic development. As a token of appreciation for his services, he was awarded theSaudi nationality by King Khalid in 1983 on the recommendation of Shaikh MuhammadAba al-Khail, the then Minister of Finance and National Economy. He has also taught inthe USA at the universities of Wisconsin and Kentucky and worked in Pakistan at theInstitute of Development Economics, and the Islamic Research Institute. He has madeseminal contributions to Islamic Economics and Finance over more than three decades inthe form of 15 books and monographs and more than 100 papers and book reviews. Hismost outstanding contributions have been his four books: Towards a Just Monetary System(1985); Islam and the Economic Challenge (1992); The Future of Economics: an IslamicPerspective (2000); and Muslim Civilization: The Causes of Decline and the Need for Reform(2008). All four of these books have been widely acclaimed. Consequently, he has receiveda number of awards, including the Islamic Development Bank Award for Islamic Economics,and the prestigious King Faysal International Award for Islamic Studies, both in 1990. Someof his books and papers have been translated into a number of languages, including Arabic,Bangla, French, German, Indonesian, Japanese, Malay, Persian, Polish, Spanish, Turkishand Urdu. E-mail: [email protected]. Website: www.muchapra.com.

Dr Mohamed DamakDr Mohamed Damak is an Associate for Standard & Poor’s, based in Paris (France). He isthe co-Chairman of the Islamic finance workgroup within Standard & Poor’s and is respon-sible for banks in the Middle East & North Africa. Mohamed joined Standard & Poor’s inearly 2006 and prior to this, Mohamed had internships at Citibank (credit analyst) andBanque Internationale Arabe de Tunisie. Mohamed has a PhD in Finance and an MBA inMoney, Banking and Finance from the University of Paris II Panthéon Assas. Mohamedalso holds an MSc in Financial Institutions Management from ESC Tunis.

Baljeet Kaur GrewalBaljeet Kaur Grewal is Managing Director & Vice Chairman at Kuwait Finance HouseResearch Ltd. In her capacity as Chief Economist, Baljeet heads the Global Economics &Research entity and is responsible for investment advisory. Kuwait Finance House is also theonly Islamic Bank worldwide with a notable Investment Banking Research presence, instru-mental in promoting Islamic banking and facilitating portfolio fund movement globally.

Prior to this, Baljeet was attached to the Maybank Group Malaysia, ABN AMRO BankSingapore, ABN AMRO Amsterdam and Deutsche Bank, London, with experiences rangingfrom Credit Structuring, Origination & Syndication and Capital Market Research. She has broad experience in investment banking, having participated in notable fund raisingtransactions in Asia & the Middle East.

To date, she has undertaken research in Islamic finance with a principle focus on debtcapital markets and sukuks. She has written and published numerous articles on Developing

About the contributors

xvi

Economies & Debt Markets, World Economic Growth and GCC & SEA Economies; aswell as addressed numerous international conferences & forums.

Baljeet holds a First Class Honours degree in International Economics from theUniversity of Hertfordshire, UK and has undertaken extensive research with internationalbodies. She is also the award recipient of the prestigious Sheikh Rashid al-Makhtoum awardfor Regional Contribution to Islamic Finance in Asia 2006.

In 2007, Kuwait Finance House was awarded ‘Best Research in Islamic Finance’ bythe Dow Jones Islamic and Terrapin Group.

Aznan HasanDr Aznan Hasan is an Assistant Professor in Islamic Law and the former head of the IslamicLaw Department, Ahmad Ibrahim Kulliyyah of Laws, at the International Islamic UniversityMalaysia. He taught Islamic legal theory, Islamic commercial law and Islamic banking andfinance at both undergraduate and postgraduate levels. He has served as a Shari’a advisorto various financial institutions, legal firms and corporate bodies, at both local and inter-national arenas. He was a member of the Shari’a Advisory Council of Bank Negara Malaysia.He resigned in August 2008 to become the Chairman of the Shari’a Committee for ACRRetakaful Bahrain and ACR Retakaful Malaysia. He is also a licensed Shari’a Advisor forthe issuance of Islamic securities and Islamic Unit Trust Schemes, for the SecuritiesCommission of Malaysia. He is a Shari’a Advisor for Bursa Malaysia, the sole MalaysianExchange and Dat al-Istithmar, London. He is also a Shari’a Consultant for AsembankersMalaysia Berhad and an external Shari’a Fellow at the Islamic Banking and Finance Instituteof Malaysia (IBFIM). He is also an Advisory Committee Member for Bursa Malaysia’sFBM Index.

Dr Aznan Hasan received his first degree in Shari’a from the University of al-Azhar.He then successfully completed his Masters degree in Sharia from Cairo University withdistinction (mumtaz). He then obtained his PhD from the University of Wales, Lampeter,UK.

Andrew HendersonDr Andrew Henderson is counsel in the corporate department of the Dubai office of CliffordChance LLP. He leads the financial services regulation group and advises on the UnitedArab Emirates, Dubai International Financial Centre and UK financial services and marketslaw and regulation; aspects of Bahrain, the Qatar Financial Centre and Saudi Arabia finan-cial services and markets regulation as well as on local and international law aspects ofderivatives and other financial products. Andrew has a particular interest in Islamic financeregulation, having advised firms who wish to carry out Islamic finance business. He alsoadvises regulatory bodies on rules and policy for the regulation of Shari’a-compliant secu-rities and investments. He holds a PhD in law from Cambridge University.

Sohail E Jaffer Mr Jaffer is a Partner and the Head of International Business Development for ‘white label’bancassurance and investment services within the FWU group, an international financialservices group headquartered in Munich. The group’s core activities include bancassurance,asset management and individual pension plans. The group is also recognised for its global

About the contributors

xvii

leadership and expertise in Sharia-compliant investments and insurance (takaful). He success-fully originated, negotiated and won several major bank distribution deals in the GCC region,Pakistan and Malaysia. The group’s international network includes Luxembourg, Italy, UAEand Malaysia.

From June 1998 until June 1999 he was Senior Vice President within the InternationalMutual Funds Group of Scudder, Stevens and Clark Ltd, based in London and responsiblefor their international product development in Europe and Japan.

From January 1989 until May 1998, Mr Jaffer was Vice President with Citibank London.He was with the Financial Institutions Group until 1996 and later joined Citibank’s AlternativeInvestment Strategies (AIS) Group. He was a Director and his responsibilities included inter-national business development and asset-gathering from institutional investors in Europeand the Middle East region. He was also a member of Citi’s Hedge Funds Policy andStrategy Committee.

Mr Jaffer was an audit partner with the Price Waterhouse practice in Africa from July1984 until September 1988. Mr Jaffer is a UK qualified certified accountant (FCCA). Heis currently a Regional Advisory Council Member (EMEA) of the Alternative InvestmentManagement Association (AIMA), was a Council member of AIMA for the period 2001 toSeptember 2008 and past Chairman for the period 1997 to 2000. He has written extensivelyon alternative investments and has edited several Euromoney publications on hedge funds,multi-manager strategies, four Islamic books on retail banking, asset management, insur-ance (takaful), wealth management and a recent CPI publication on investing in the GCCmarkets. He is also a member of ALFI’s Asset Management Advisory Committee, MiddleEast working group and their Hedge Fund Committee. ALFI is the Association of theLuxembourg Funds Industry. He is also a member of MIFC’s Strategic Focus Group (SFG).MIFC is the ‘Malaysia International Islamic Finance Center’.

Tahir JawedTahir Jawed qualified as a solicitor in the UK with Clifford Chance and spent six yearsworking in their London, New York and Dubai offices. Tahir joined Maples and Calder inthe Cayman Islands in 2000 and opened their Dubai office in 2005, becoming the firstoffshore lawyer in the Middle East. Tahir is considered the market leader in the offshorestructuring of Islamic finance transactions having worked on many landmark sukuk issuancesand Shari’a-compliant funds and has been recognized for his work with industry awardsfrom International Financial Law Review and Islamic Finance News. Tahir has also beennamed by The Brief as one of the twenty most prominent lawyers in the Middle East.

Sunil Kumar KhandelwalDr Sunil Kumar is the Head of Risk Management Middle East for IRIS Integrated RiskManagement AG, Switzerland which is a part of FRS Global. He is responsible for theorganization’s growth and operations for Middle East. Prior to joining IRIS, Dr Sunil washeading the International Certifications at the Emirates Institute for Banking and FinancialStudies in the UAE. He holds a PhD in applied IT to Banking from the India Institute ofTechnology Bombay and the MBA in Finance from the University of Southern Queensland,Australia. His interests include an Islamic Banking, Risk Management, Basel, and IT Security

About the contributors

xviii

in Financial Institutions. He has travelled extensively and has a strong understanding of thefinancial sector in the Middle East. He has headed several consultancy projects over thelast few years for various types of financial institutions. He is an acclaimed trainer andspeaker. Dr Sunil is the author of pioneering work in the field of risk management in Islamicbanking and his co-authored book entitled Financial Risk Management for Islamic Bankingand Finance by Palgrave McMillan, UK has been well accepted by the risk community allover the world. It is also featured as recommended reading for FRM by GARP. He is onadvisory committees for select projects in different parts of the world. He also contributesregularly to the financial press all over the world. He is a member of GARP, PRMIA,ISACA and EFA. He can be contacted at [email protected].

Dourria MehyoDourria is the AVP-Product Strategy at Path Solutions, heading the Business Analysis andProposals Management Functions. She is responsible for the enhancement and setting ofthe roadmap for Path Solutions iMAL to be in line with the Islamic Banking industry trendsand best practices. Dourria has eight years of experience in the Islamic banking industry.She started her career in software implementations at many of the leading Islamic Investmentand Commercial banks in the GCC countries. She has five years’ experience auditing andconsulting at PricewaterhouseCoopers in their Beirut office. In addition, Dourria has hadseveral articles published in leading Islamic Finance magazines in relation to Islamic finance,Islamic banking rules and regulations and related IT requirements. Dourria is a CPA andMBA degree holder.

Nasser H SaidiDr Nasser H Saidi is the Chief Economist of the Dubai International Financial CentreAuthority (DIFCA) and Director of the Hawkamah-Institute for Corporate Governance atthe DIFC. He served as the Data Protection Commissioner of the DIFC from January toAugust 2007.

He is a former Minister of Economy and Trade and Minister of Industry of Lebanon(1998-2000). He was the First Vice-Governor of the Central Bank of Lebanon for twosuccessive mandates, 1993-1998 and 1998-2003. He is co-chair with the OECD of theMENA Corporate Governance Working Group and established the Lebanon CorporateGovernance Task Force. He was a Member of the UN Committee for Development Policy(UNCDP) for two mandates over the period 2000-2006, appointed as a member in hispersonal capacity by former UN Secretary General Kofi Annan.

He has a recent book, Corporate Governance in the MENA countries: ImprovingTransparency & Disclosure, and a number of books and publications addressing macroeco-nomic, capital market development and international economic issues in Lebanon and theregion. His research interests include macroeconomics, financial market development,payment systems and international economic policy, and ICT.

Saidi has served as an economic adviser and director to a number of central banks andfinancial institutions in the Arab countries, Europe and Central and Latin America. Prior tohis public career, Dr Saidi pursued a career as an academic, as a Professor of Economicsat the Department of Economics of the University of Chicago, the Institut Universitaire de

About the contributors

xix

Hautes Etudes Internationales (Geneva, CH), and the Université de Genève, and was alecturer at the American University of Beirut and the Université St Joseph in Beirut.

He holds a PhD and an MA in Economics from the University of Rochester in the US;an MSc from University College, London; and a BA from the American University ofBeirut.

Rodney WilsonProfessor Rodney Wilson is Director of Postgraduate Studies at Durham University’s Schoolof Government and International Affairs. He currently chairs the academic committee ofthe Institute of Islamic Banking and Insurance in London and is acting as consultant to theIslamic Financial Services Board with respect to its Shari’a Governance Guidelines. Hisprevious consultancy experience included work for the Islamic Development Bank in Jeddahand the Ministry of Economy and Planning in Riyadh. He has written numerous books andarticles on Islamic finance for leading international publishers as well as professional guides.

Professor Wilson teaches masters level courses on Islamic economics and finance andsupervises PhD students working on Islamic finance. He has acted as Course Director forEuromoney Legal Training in London, Bahrain, Kuwait, Bangkok and Singapore, and hastaken courses for the Kuwait Investment Authority, the Commercial Bank of Kuwait, theArab Banking Corporation, Citibank, HSBC, the Monetary Authority of Singapore and SJBerwin, the international law firm and private equity specialist. For further information,visit http://www.dur.ac.uk/sgia/profiles/?mode=staff&id=498.

About the contributors

xx

xxi

Introduction

Rodney Wilson Durham University

Producing a subject encyclopedia is always an ambitious task. A decade ago there was,arguably, insufficient breadth to Islamic finance to justify a specialist encyclopedia; as sucha work might have been a rather slim volume. This work is therefore timely as there havebeen so many developments in Islamic finance that virtually all areas of banking, insur-ance, asset management and capital markets fall within the remit of the subject.

Work in this area is interdisciplinary, as it requires finance specialists, economists,commercial lawyers and Islamic scholars. Islamic finance brings together those with theo-logical and historical interests and others focused on more worldly and immediate concernsinvolving money, profits and enterprise. The results have been remarkable, as it has notonly resulted in the provision of Shari’a-compliant and Shari’a-based solutions for thosewanting to manage their finance in accordance with their religious beliefs, but it has alsocontributed to the wider debate on the morality of much current financial practice.

Shari’a-compliant or Shari’a-based?

In an encyclopedia, it is usual to define basic concepts first; in this case the differencebetween financial transactions which are Shari’a-compliant and those which are shari’a-based. Shari’a itself refers to Islamic law which is derived from the teaching in the HolyQur’an and the Hadith; the words and deeds of the Prophet, as recorded in the Sunnah.This has been constantly re-interpreted over the ages with respect to each field of humanactivity, including banking and finance. This process of re-interpretation or application isknown as ijtihad; the effort of an Islamic scholar qualified in fiqh, Islamic jurisprudence,to give an opinion on what is permissible, halal, and what is not, haram, in the light ofreligious teaching. To provide such an opinion or fatwa on the legitimacy of financial trans-actions, requires some understanding of contemporary financial practices as well asknowledge of fiqh.

Shari’a is universal and applies at all times in all states, both to those that are pre -dominately Muslim and to those where Muslims are in a minority. States are also governedby national laws which are jurisdiction-specific. Islamic financial contracts must complywith Sharia’h, but must also be enforceable under national laws. Therefore, Islamic financecontracts are usually drafted by the commercial law firms which serve the financial insti-tutions, the role of the Shari’a scholars being to read the draft contracts and to suggestwhat revisions are needed to ensure the contracts comply with Shari’a.

Financial contracts are usually drafted under common law rather than civil law, as underthe former, the signatories to the contract are bound by the terms and conditions specified.Under civil law, the validity of a contract can be more easily challenged by one of thesignatories in a secular court, but this implies the judgement of the Shari’a scholars is beingquestioned. This is less likely under common law, where secular courts can withhold Shari’aprinciples, as long as these are reflected in the contract. Malaysia and the Indian subcon-tinent are governed under English common law, but in most Arab states and Indonesia civillaw applies, apart from those designated financial centres such as the Dubai InternationalFinancial Centre or the Qatar Financial Centre, who have their own governing laws andregulations and are exempt from the national civil laws of the countries in which they arelocated. Both use common law and have become significant centres for Islamic financialactivity.

If a contract is Shari’a-compliant or Shari’a-based, this implies different starting pointsfrom a legal perspective. Shari’a compliance is the most straightforward from a contem -porary common law perspective, as it involves taking a conventional financial contract suchas a mortgage, and changing the terms and conditions so that there is no reference to ribaor interest and that there is no element of ambiguity or contractual uncertainty (gharar)that one of the parties could potentially exploit. Often the changes are relatively minor andthe contract continues to serve the same function as it did before the revisions and amend-ments were undertaken. In support of this approach, it is argued that the financial needs ofMuslims are no different from those of non-Muslims, the challenge for the scholars beingto provide input into the contract specification that ensures they are halal. The legitimacyand validity of such contracts ultimately depends on the reputation and credibility of the scholars themselves, which is why they should be named in brochures and web-basedmaterial issued by the financial institutions, with details given of their qualifications andexperience.

The alternative Shari’a-based approach implies starting from contracts developed byfiqh scholars over many centuries such as mudarabah or musharakah partnership contractsinvolving profit and loss sharing. There is no conventional financial equivalent of thesecontracts, although they may be drafted to comply with common law and be enforceableby national courts. All scholars agree that it is preferable to have Shari’a-compliant contractsto those that are non-compliant, but most would prefer to see Shari’a-based contracts, notleast as they accord most closely to Islamic financial principles, which stress justice incommercial transactions and the rightful earning of rewards. Wages and salaries, for example,are seen as a legitimate return for work but rewards for inactivity are unjustified, apart fromfor those that cannot work and are in need.

Economic justice in Islamic finance

Islamic finance should not simply be viewed as being concerned with prohibitions but ratheras a positive approach to ensure the parties to financial transactions are involved in a morallyworthwhile endeavour. Financial systems should be designed to serve a wider social good,and not simply individual greed, all too often pursued at the expense of others. All rewardshave to be justified in Islamic finance, with wages and salaries related to work and effort,

Introduction

xxii

as already indicated, and rental income to landlords justified through their responsibilitiesfor the properties leased. Financing leases are prohibited in Shari’a as the owner tries topass on all responsibilities to the tenant, whereas to justify a rental income from a building,the owner must assume responsibilities for the external maintenance of the building as withan ijara operating lease.

Profit is also seen as a justifiable reward in Islamic finance, which rather than beingrelated to work or ownership, is compensation for risk sharing. In business and financethere are always risks including credit, market and operational risk, but if risks are sharedbetween the parties, this is more just than simply assigning all the risk to a single party.With conventional lending the borrower assumes all the risk, and is penalized further forpayment delays or defaults. In contrast, in Islamic finance, the risks are shared between thebank and the client. Of course Islamic banks have to manage credit risk, and unscrupulousdefaulters should not be treated leniently, otherwise moral hazard problems might arise.

Misselling of financing products is clearly immoral, as with the sub-prime mortgagesin America and to a lesser extent in Britain, where borrowers were encouraged to take ondebts they could not afford by mortgage brokers and bank sales teams, who earned up-frontfees for each mortgage sold. When the inevitable defaults occurred this was of no concernto the mortgage brokers and sales teams who had moved on to other activities. Islamicbanks have to adopt fair and transparent charging structures which do not exploit the ignorance of the client. Their staff must ensure, as far as possible, that clients can meettheir financial obligations. So far, the record of Islamic home financing has been favourable,with none of the defaults that have characterized the sub-prime crisis.

Islamic finance is inherently participatory, with the financier getting involved with theclient and taking an interest in how the funding is utilized. This is not only to ensure thefinancing is serving a moral purpose, although that is important, but also to help the clientmanage the funds received effectively. The financier can act as an agent for the client, aswith murabahah where the financier purchases a good on behalf of the client and re-sellsit to the client for a mark-up which makes the transaction profitable. What justifies themark-up is the ownership responsibilities exercised by the bank, which serves as a traderrather than simply a financier. If the good is defective, the bank has a responsibility toremedy this, which is why it needs to check on the validity and transferability of warranties,thus taking a burden from the client.

Islamic and conventional banking: similar services but differentfinancing methods

Critics of Islamic banks suggest that their remit should be different to conventional banks,with a focus on serving the poor and needy, rather than promoting the development of capitalism. The early experiments with Islamic finance in the 1960s in Pakistan and Egyptinvolved the establishment of credit unions in poor rural areas, enabling members to obtaininterest free finance from the contributors’ funds. The clients were similar to those of theGrameen Bank in Bangladesh, a microfinance institution which serves a poor ruralconstituency, but is not Shari’a-compliant as its lending involves interest.

Introduction

xxiii

The take-off for Islamic banking coincided with the oil boom of the 1970s in the Gulf,with institutions such as the Dubai Islamic Bank being established in 1975 and the KuwaitFinance House opening for business in 1977. These were oil-rich states, not poor devel-oping countries, the initial clients of the new Islamic banks being wealthy merchant familieswanting to finance their growing import and distribution businesses. Murabahah was theideal tool for this, as not only was it Shari’a-compliant but also, as the bank acted as initialpurchaser, no letter of credit was required to guarantee payment by the client. This resultedin signi ficant cost savings for the client. Furthermore as the bank could bulk purchase onbehalf of several clients it could often obtain discounts which could be shared with theclient.

By the late 1980s, Islamic banks were seeking to diversify their asset portfolios andidentify more profitable financing methods, as there was increasing competition inmurabahah and mark-ups were being squeezed. Ijara leasing contracts were promoted, asthese lengthened the period to asset maturity, reducing asset turnover and the resultantarrangement costs. Whereas murabahah financing was typically for periods of three toeighteen months, ijara contracts were for three to five years. Of course with ijara financing,liquidity was reduced and risks increased with the longer period to maturity, but this couldbe built into the rental, to provide an attractive risk and return profile for this category ofasset.

Financial engineering involving Shari’a-based products

The 1990s witnessed further product development involving both short-term receivablesfinancing using salaam and longer-term project finance with istisna. Salaam involves makinga pre-payment for a good to be delivered in the future, usually after ninety days. As an up-front payment is made, the price paid will usually be at a discount to the anticipated spotprice on delivery. The effect is similar to a forward transaction where the price is guaran-teed. Salaam contracts cannot be traded, as such activity would be speculative; rather it canbe regarded as a hedging instrument. To increase liquidity, however, a bank can enter aparallel or reverse salaam contract, under which the commodity or good will be deliveredto a third party after, for example, sixty days. As the period is shorter to delivery, the thirdparty will pay a higher price for the contract, the difference between this and the initialpurchase price representing the bank’s margin or profit.

Istisna finance can be for periods of five years or more with this traditional method offinancing manufacturing being adapted to cover projects. Often an investment bank isinvolved as it covers payments by the project management company for supplies and wagecosts. Once the project is completed, it is handed over to the operating company whichpays the project management company. This revenue can then be used to repay the invest-ment bank. Rather than having an illiquid asset for a five-year period or longer, the investmentbank may enter a parallel istisna agreement to sell the right to the repayment to one ormore Islamic banks or investment companies. This creates smaller tranches suitable forinvestors who want to place millions of dollars rather than billions. Rather than having asingle large investment in a potentially high risk project, where there could be cost over-

Introduction

xxiv

runs or delays in construction, the Islamic banks and investment companies may prefer tohave a diversified portfolio of istisna assets to spread risk.

The preponderance of Islamic retail banking

Most Islamic banking is retail rather than involving investment banking, with employeeshaving their salaries paid into current accounts where the funds are restricted to financingShari’a-compliant activities conducted without riba. Those with savings are encouraged by Islamic banks to open unrestricted investment mudarabah accounts which enables themto share in the bank’s profits or restricted mudarabah accounts where the deposits are usedfor a specific project and the depositor shares in the profits from the project. The latterusually produces a higher return, but the risks from concentration are greater. Many Islamicbanks have been promoting these accounts, which have proved popular with clients worldwide.

Retail banking products include car and housing finance, with the former usuallyinvolving murabahah or ijara and the latter ijara wa iqtina, a hire purchase contract, ordiminishing musharakah. With diminishing musharakah, the client and an Islamic bankform a partnership, with the client providing ten per cent or more of the capital and theIslamic bank ninety per cent or less. This initial funding is used to purchase a property.Each year the client buys out part of the bank’s share in the partnership, creating a repay-ments stream, with the client’s share in the partnership gradually increasing. The client alsopays rent for the share the bank owns. If each repayment instalment was equal, this wouldfront-load the payments obligations of the client, as they have to make larger rental paymentsat the start to reflect the bank’s higher ownership share. In order to avoid this scenario, therepayments are usually structured exponentially with lower repayments initially but higherrepayments later. This may suit younger home buyers whose income will increase withcareer progression. It is worth noting that the property is not re-valued during the life ofthe financing. The client enjoys all the capital gain on the property if the market is rising.The bank only has its initial funding repaid, its gain accruing from the rent. Arrangementand management costs are covered by set up charges and the administrative fees. In otherforms of musharakah, all parties share in any capital gains or losses, but this is not accept-able to most property buyers who anticipate long-term asset appreciation.

Shari’a-compliant capital market products

The major development in Islamic finance in the last decade has involved the issuance ofsukuk Islamic securities and a methodology for ensuring that equity investment can beShari’a-compliant.

Sukuk are based on Islamic financing structures such as salaam, murabahah, ijara,mudarabah and musharakah which are securitized so that apart from salaam sukuk, theycan be traded in a market. All sukuk must be asset backed to be Shari’a-compliant andhence buyers and sellers are not merely trading financial instruments, but a title to a realasset such as piece of real estate, buildings or equipment. Salaam sukuk are similar totreasury bills but provide a mark-up for the investor rather than interest. Unlike treasury

Introduction

xxv

bills, they cannot be traded as indicated above, as the asset is only delivered in ninety dayswhen the sukuk matures and is not in possession of the investors. Murabahah sukuk havea fixed return and correspond to bonds, while with ijara sukuk returns vary which meansthey have the financial characteristics of floating rate notes. These have proved the mostpopular type of sukuk, not least because returns usually vary in line with changing marketfunding costs.

The main concerns of Shari’a scholars with sukuk is that the investors have a cleartitle to the underlying asset, and that in the case of mudarabah and musharakah, the assetsthemselves are re-valued so that the investors do not merely get the nominal value of theirinvestment refunded as with a debt instrument. This creates a dilemma for the investors, asthose wanting Shari’a-compliant debt instruments, do not wish to invest in assets subjectto market risk, their preferred exposure being to default risk only. Takaful Islamic insur-ance operators, for example, cannot take too much exposure to market risk, as although aproportion of their holdings are in equities, most are in sukuk for the same reasons as insur-ance companies hold bonds and floating rate notes. If there were excessive holdings ofequity instruments and the market value of these investments fell, takaful operators wouldno longer be able to fulfil their obligations to those policyholders making claims. Thiswould mean a breach of contract and would be unfair to those in need of accident or othercompensation. Those who argue for all sukuk being equity-based need to be aware of thewider social and legal consequences. Land or buildings may be used as the underlyingassets for sukuk, but investors wanting exposure to real estate may prefer to invest directlyin this rather than in sukuk. From a portfolio perspective, sukuk have to be viewed as onecomponent of a multi-asset allocation strategy.

Implications of financial market volatility for Islamic investment

Sukuk issuance has increased enormously since 2000, with over 200 issues in 2007 aloneworth $45 billion. Much of the activity was in the first seven months of the year however,as sukuk issuance after August was adversely affected by the crisis in securitized debt obli-gations resulting from the sub-prime defaults. The pricing of sukuk has been linked to thatof conventional debt securities, as sukuk represents only a small proportion of the overallmarket, and therefore sukuk issuers and investors are price takers rather than price makers.The higher price which needs to be offered for sukuk financing has deterred many issuers,with funding plans either abandoned as projects are rethought, or postponed until marketconditions become more certain.

The slow-down applied more especially to US dollar-denominated sukuk, the currencyfor most sub-prime debt, but issuance in other currencies has been less affected. Malaysiansukuk are mostly local currency denominated, and appear to be unaffected and in the Gulf, there has also been a trend in favour of local currencies. Only the Kuwaiti dinar hasbeen allowed to appreciate against the US dollar so far, but investors in riyal- or dirham-denominated sukuk are expecting that these currencies are likely to be decoupled from theUS dollar, possibly in 2010, when a new joint float might occur as part of a move towardsmonetary union in the Gulf Co-operation Council states. It is likely that there will beincreasing currency diversification in sukuk issuance. The British government is planning a

Introduction

xxvi

series of sterling denominated sovereign sukuk issues, the pricing for which will provide abenchmark for subsequent sterling corporate sukuk issuance from London. There have alreadybeen several euro-denominated sukuk, including on behalf of the German state government,and many more are likely in the years ahead.

The volatility in equity markets worldwide does not seem to have constrained investorinterest in Shari’a-compliant managed funds. By 2008, there were over 400 of these funds,most of which were equity based, although there were also 50 specialized real estate funds.Investment in equity is permissible, as long as the companies are involved in acceptablebusiness activities and have limited debt-based leverage. A methodology has been devel-oped to ascertain what is permissible by institutions such as the Dow Jones Islamic Indexes.Ideally, any company involved in interest-based transactions, especially conventional banks,should be excluded but the guidelines recognize that most companies may have some interest-based income and obligations. Borrowing up to one third of capital is permissible in linewith the discretionary limits in Islamic inheritance law, but beyond that the financing isregarded as highly speculative and therefore not allowed.

The future for Islamic finance

A browse through this encyclopedia demonstrates how wide ranging the areas covered byIslamic finance have become. The scope extends to banking regulation and risk manage-ment as well as corporate and Shari’a governance. The coverage also includes takaful andwealth management, as well as retail open and closed funds. Product innovation is alsodiscussed, as are tax issues and the role of Islamic finance in offshore centres. Aly Khorshidhas succeeded in attracting an excellent group of contributors who are the leading academicsand professionals in the field of Islamic finance and the reader can benefit from their knowledge.

The future will of course be determined partly by the choices made today, and in this,Islamic finance is no exception. Being Shari’a-compliant is not simply a substitute for beingShari’a-based; rather they represent different directions for Islamic product development.The industry is also changing as the economies of the Muslim world evolve. Some remainpoor and underdeveloped, but many are highly developed and play an increasing role inthe global economy, enhancing the prospects for Islamic finance. Some observers see a typeof Islamic capitalism developing based on riba-free finance which challenges the assump-tions underlying Western capitalism. There is an ideology implicit in Islamic finance thatmay ultimately shape the development of global finance, not least because there is increasingworldwide concern with moral and ethical issues and not simply with making money andmaterial advance.

Introduction

xxvii

Part I

Overview of Islamic finance

12222234567891011123111456789201111234567893011112343567894011112344222

12222234567891011123111456789201111234567893011112343567894011112344222

3

Chapter 1

Basic elements of Islamic finance

Aly KhorshidElite Horizon

Introduction

There are differences between a capitalist economic system and an Islamic economic system,one of the most obvious being that capitalist economies are not governed by divine ruling.This has allowed practices such as excessive interest-accumulation and gambling, and thesepractices in turn concentrate wealth in the hands of the few. Monopolies are created, andthese paralyse market forces. In Islam, divine restrictions are put onto economic activities,and these have the effect of maintaining balance, justice and equality.

The conventional concept of financing is that the banks and institutions deal in moneyonly. Islam does not recognize money as a subject-matter of trade, except in some cases.Financing in Islam is always based on liquid assets, which creates real assets and invento-ries. Financing based on musharakah, mudarabah, salaam and istisna’ creates real assets.These means of financing are criticized as having the same result as interest-based borrowing.However, they are backed by assets, and they can be distinguished from interest-basedborrowing on the following grounds:

• In conventional financing, the financier has no concern about how the money is used bythe client in an interest-bearing loan. In murabahah, the financier purchases the commodityrequired by the client, thus assets back the financing.

• In murabahah the purpose of the loan must be under Shari’a, but in conventional financingthere is no such ruling.

• In murabahah the financier who purchases the commodity holds the risk, and the profitis reward for this risk. This risk is not assumed in an interest-based loan.

• In an interest-bearing loan, the amount to be repaid increases with time, but in murabahahthe price is fixed once agreed.

• As the risk of a lease is placed on the financier, it is the financier who will suffer theloss if it is damaged.

Assets always underpin Islamic financial transactions; there is no gap between the supplyof money and the production of real assets, which is the case in conventional economiesthat suffer inflation.

Islamic banks have been growing, and have had to contend with constraints in theirrespective countries, such as lack of support from the government and legal systems. Thus,they have not been able to abide by all the requirements of Shari’a. This is permitted throughthe rule in Shari’a, where some relaxations are given in exceptional circumstances. However,to keep within the realms of Shari’a rule, the aim should be to establish total Islamic order.

Musharakah

Musharakah literally means ‘sharing’. In musharakah, the return is based on the actualprofit earned by the joint venture. Interest is prohibited in Islam, as the rate of interest isthe main cause for imbalances in the system of distribution. Musharakah favours the commonpeople, as the financier must declare if the loan is to assist the debtor or to share the profits.Nothing can be claimed if the financier is assisting, and if the profits are shared, the losses(if any) are also shared. If the profits shared are large, they cannot all be secured by thefinancier, but will be shared among the depositors of the bank (the common people).Musharakah, however, is considered somewhat outdated, and there is no prescribed proce-dure, only a broad set of principles. New procedures can be accepted as long as they donot violate any basic principles.

Shirkah also means sharing, and is more commonly used in Islamic jurisprudence thanmusharakah because of its wider meaning. In the terminology of the Islamic Fiqh, shirkahhas been divided into two kinds – Shirkat-ul-milk and Shirkat-ul-‘aqd.

Shirkat-ul-milk

This is joint ownership of two or more persons in a property. This is used in two ways:firstly, optional – by the decision of the parties to purchase something jointly; and secondly,compulsory, such as after a death – in which property inherited will be jointly owned.

Shirkat-ul-‘aqd

This is a partnership affected by a mutual contract, or joint enterprise. This is divided intothree types:

• Shirkat-ul-amwal: Partners invest capital into a commercial enterprise.• Shirkat-ul-A’mal: Partners provide a service and according to an agreed ratio; fees are

distributed among them.• Shirkat-ul-wujooh: Partnership in goodwill; partners purchase commodities and sell them

on the spot, and distribute the profit to an agreed ratio.

Musharakah has been introduced recently by those who have written on the subject ofIslamic modes of financing, and is restricted to this type of Shirkah: Shirkat-ul-amwal.However, in some cases it includes Shirkat-ul-a’mal.

Part I: Overview of Islamic finance

4

Rules of musharakah

• The contract must be drawn up with free consent of all parties without fraud or mis -representation.

• Distribution of profit must be agreed at the time of the contract.• The distribution of profit is determined by the profit accrued, not the capital invested,

that is an agreed percentage of the actual profit.• The ratio of profit and loss has been debated among Muslim jurists. According to Imam

Malik and Imam Shafi’i, each should get the profit in proportion to his investment; butaccording to Imam Ahmad, the ratio of profit may differ from the investment ratio if itis agreed between them. Imam Abu Hanifah argues that the ratio of profit may differfrom the investment in normal conditions, but if the partner expresses in the agreementthat he is a sleeping partner, then his share cannot be more than his investment. For theratio of loss, there is a consensus that each partner shall suffer the loss according to theratio of investment. The view of Imam Ahmad and Imam Abu Hanifah is a principlementioned in the maxim: ‘Profit is based on the agreement of the parties, but loss isalways subject to the ratio of investment.’

If a partner wants to participate in a musharakah by contributing some commodities to it,he can do so (according to Imam Malik) without any restriction, and his share in themusharakah shall be determined on the basis of the current market value of the commodi-ties at the time of contract. According to Imam al-Shafi’i, however, this can only be doneif the commodity is from the category of dhawat-ul-amthal (a commodity which can becompensated with similar commodities such as wheat or rice). According to Imam AbuHanifah, if the commodities are dhawat-ul-amthal, mixing the commodities of each partnertogether can do this. If the commodities are dhawat-ul-qeemah (commodities not able to becompensated with similar commodities such as cattle), they cannot form part of the sharecapital. The view of this Imam meets the needs of the modern business and is more reason-able.

Each person has a right to manage the principle of musharakah, and an agreement canbe made for one person to carry out the management.

Termination of musharakah

The musharakah is deemed terminated under the following conditions:

• Each partner has a right to terminate the musharakah at any time after giving his partnernotice. The assets, if in cash form, will be distributed between them. If they are notliquid, they may agree either to liquidate them or to distribute them as they are. If theassets are machinery, it will be sold and the profits shared.

• If one partner dies, then his part is terminated. His heirs will have the option to withdraw the share or continue.

• If a partner becomes insane or incapable of effecting commercial transactions, themusharakah will be terminated.

12222234567891011123111456789201111234567893011112343567894011112344222

Basic elements of Islamic finance

5

By mutual agreement, one of the partners can terminate the musharakah while the otherscontinue. The others may purchase the share of the terminating partner. The price of theshare is also determined by mutual consent.

Mudarabah

Mudarabah is a partnership where the investment comes from the first partner, ‘rabb-ul-mal’, and the management and work is the responsibility of the second, ‘mudarib’. Asummary of the differences between musharakah and mudarabah is as follows:

• In musharakah, investment comes from all partners, but in mudarabah, investment is theresponsibility of the rabb-ul-mal.

• In musharakah, all partners participate in the management, but in mudarabah, the mudaribalone conducts the management.

• All partners in musharakah share the loss to the extent of their ratio of investment, butin mudarabah the loss is suffered by the rabb-ul-mal only as he is the sole investor.However, if the mudarib has been negligent, he will suffer the loss.

• The partners’ liability in musharakah is unlimited. In mudarabah the liability of the rabb-ul-mal is limited to his investment, unless he has permitted the mudarib to incur debtson his behalf.

• In musharakah, the assets, once mixed in a joint pool, become jointly owned by themaccording to the proportion of investment. In mudarabah all goods purchased by the mudarib are solely owned by the rabb-ul-mal. The mudarib can earn his share inthe profit should he sell the goods profitably. He is not entitled to claim his share of theassets.

Restricted mudarabah (al-mudarabah al-muqayyadah) is when the rabb-ul-mal specifies a particular business for the mudarib to invest the money in. Unrestricted mudarabah(‘al-mudarabah al-mutlaqah) is when it is open for the mudarib to undertake whicheverbusiness he wishes.

In cases where the rabb-ul-mal contracts mudarabah with more than one person througha single transaction, the mudarib shall run the business as if they were partners.

The distribution of profit must be agreed upon at the beginning of the contract. Themudarib cannot claim any periodical salary, fee or remuneration for the work done by himfor the mudarabah. This is agreed by most schools of Islamic Fiqh. However, Imam Ahmadhas allowed for the mudarib to withdraw his daily expenses of food from the mudarabahaccount. The Hanafi jurists restrict this right of the mudarib only to a situation when he ison a business trip outside his city. Any profit will first be used to offset any loss, and therest will be distributed according to the ratio.

Musharakah and mudarabah in combination

The two systems may be combined in order for the mudarib to contribute some money intothe business. In this, the mudarib may allocate for himself a certain percentage of profit on

Part I: Overview of Islamic finance

6

account of his investment as a sharik, and allocate another percentage for his managementand work as a mudarib. The normal basis for allocation of the profit in the above examplewould be that the second party shall secure one third of the actual profit on account of hisinvestment, and the remaining two thirds of the profit shall be distributed among themequally. However, the parties may agree on any other proportion. The one condition is that the sleeping partner should not receive a larger percentage than the proportion of his investment.

In the Islamic Fiqh partners cannot leave and join the enterprise without causing anaffect to the continuity of business in some way. However, these were written before themodern age of large-scale commercial enterprises. This does not mean, however, thatmusharakah and mudarabah cannot be used for a running business. If the basic principlesare followed, their application may be varied.

1 Financing through musharakah and mudarabah participation in the business, and inmusharakah sharing the assets of the business to the extent of the ratio of financing.

2 An investor must share the loss incurred by the business to the extent of his financing.3 The partners determine the ratio of profit.4 The loss suffered by each partner must be exactly in proportion to his investment.

Musharakah securitization

In the case of large projects where huge amounts are required, every subscriber is given amusharakah certificate, which represents his proportionate ownership of the assets. Afterthe project has begun, these certificates can be bought and sold in the secondary market,but not when all the assets are liquid. When there is a combination of liquid and non-liquidassets, it cannot be sold unless the non-liquid part of the business is separated and is soldindependently.1 However, the Hanafi school asserts that whenever there is a combinationof liquid and non-liquid assets, it can be sold and purchased for an amount greater than theamount of liquid assets. For example, a Musharakah project contains 40% non-liquid assets,such as machinery, fixtures et cetera. and 60% liquid assets, such as cash and receivables.Each musharakah certificate having the face value of Rs. 100 represents Rs. 60 worth ofliquid assets and Rs. 40 worth of non-liquid assets. This certificate may be sold at any pricemore than Rs. 60. If it is sold at Rs. 110 it will mean that Rs. 60 of the price is againstRs. 60 contained in the certificate and Rs. 50 is against the proportionate share in the non-liquid assets. But it will never be allowed to sell the certificate for a price of Rs. 60 orless, because in the case of Rs. 50 it will not set off the amount of Rs. 60.

Single transaction financing

Musharakah and mudarabah can be employed for financing imports and exports. Forexporting, musharakah will be easier to use. As the price of the goods to be exported isknown beforehand, the financier can calculate his profit. There may be a condition to securethe financier from any exporter negligence. The condition would be that it is the responsi-bility of the exporter to export the goods in conformity with the conditions of the letter ofcredit, and the exporter would be liable for any discrepancies. On the basis of musharakah

12222234567891011123111456789201111234567893011112343567894011112344222

Basic elements of Islamic finance

7