81

European Car and Light Commercial Vehicle Production Outlook November 2013 SMMT, the 'S' symbol and the ‘Driving the motor industry’ brandline are trademarks of SMMT Ltd

European Car and Light Commercial Vehicle Production Outlook November 2013

SMMT, the 'S' symbol and the ‘Driving the motor industry’ brandline are trademarks of SMMT Ltd

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 2

Contents

Introduction and analysis overviews:

About this report 3

Executive Summary 4 Demand Side Perspective 11

Production Outlook Overview 13

Country Rankings 28 Alternative Scenarios 31

Disclaimer 36

Individual vehicle manufacturer reviews:

BMW 38

Daimler 41 Fiat (incl. Chrysler) 44

Ford 49

GM 51 Honda 54

Hyundai-Kia 55

PSA 56 Renault-Nissan-Dacia 61

Suzuki 66

Tata – Jaguar Land Rover 67 Toyota 70

Volkswagen (incl. Porsche) 71 Volvo 78

Aston Martin 80

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 3

About this report

This is the fifth short version of the 2013 Production Outlook report from AutoAnalysis. In January we produced our full “Foundation” report and readers are referred to this report for full details on the recent history and developments at each VM in particular.

The aim of the shorter reports is to focus on the Production Outlook volumes and developments at the VMs since the previous report. This means this report and the remaining reports in 2013 will be much shorter than the Foundation report.

The views and projections contained in this report are those of the author, Ian Henry of AutoAnalysis. They do not represent an official SMMT view. The projections regarding new model timings, changes in production locations and the associated production volumes shown here have been compiled on the basis of information from a variety of sources. In most cases, the vehicle companies do not provide official information on which models will be made at which plants, nor do they provide detailed information on future volumes and timings. They have been prepared on the basis of judgments made by AutoAnalysis, taking into account the information, opinion and inside from a range of industry, press and analyst sources available at the time of compiling this report.

Ian Henry of AutoAnalysis will gladly address SMMT members’ specific questions on this report.

Readers’ comments and questions on this report will be greatly appreciated. Please e-mail: [email protected].

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 4

Executive Summary Recent sales fall reversed? Although 2012 and the first 8 months of 2013 had seen steady falls in

registrations across the EU, there are signs that the bottom has been reached and the long awaited upturn has begun, 2012 had seen a fall of 8.2% in EU27 car registrations, something which was directly reflected in the fall in production which Europe witnessed last year. The first eight months of 2013 saw this decline continue, although July 2013 actually saw a year-on-year increase of 5%. However, this was a short-lived phenomenon, and the figures for August showed a 5% fall for the month and a year-to-date fall of 5.2%. Throughout this period, the UK remained the only major market showing signs of growth, with a rise of 10.4% year-on-year in the first eight months of the year; even in Germany, so long the engine of growth in Europe, registrations have fallen by 6.6% in the year to date.

In September and October, however, the market began to turn around – the UK continued to grow and Spain was boosted (possibly only temporarily) but government-supported incentives which resulted in a year-on-year growth of more than one-third. Total EU sales in rose 5.4% in September and 4.7% in October.

Once again in October, the UK continued to grow, this time by 10.2%; in France and Germany, the other major markets, there was also a modest rise in October, both growing by just over 2% although they still show year-to-date declines, by 7.4% in France and 5.2% in Germany.

Production recovering … Our total for 2012 European production including Russia is c18.12mn, a fall of

around 1mn from 2011. We now see that most of this fall will be recouped by the end of 2013, with production including Russia rising to nearly 18.98mnn. This rise is driven by a combination of factors, partly Russia, but more crucially a recovery in production in Spain and continued rises in the UK and Turkey.

Taking Russia out of the equation, we have 2012 European production down at just over 16.6mn units, a fall of c1.75mn units from 2011. We now see European production without Russia rising to 17.82mn in 2013 – as noted above, we see Spain, Turkey and the UK contributing much of this recovery.

European production, excluding Russia, has clearly started to recover, despite the continued sales falls across EU markets for much of the year. This rise in production reflects continued strong exports of premium brands (especially JLR and the German brands), the supply of models from Spain to emerging markets by PSA, the strength of LCV demand (underpinning production in Spain and Turkey especially) and general pipeline filling by the VMs with a series of new models.

In addition, new models from Dacia (including at its plant in Morocco which we treat as part of Europe from a production point of view) and strong demand for Skoda and Hyundai-Kia models also highlight the increasing role of new “value” brands, at the expense in many cases of traditional volume brands.

Just as recent production volumes have been underpinned by premium brands and some newer entrants, we also expect the main winners in the near term will be the same companies. Thus we expect most of the growth will come from the premium brands from Germany, JLR/Mini/Nissan in the UK, the value brands (ie Dacia, Skoda and Hyundai-Kia) and also LCVs, especially the expanding range from Ford. Ford will also be boosted by rising production in Russia.

However, we expect to see a mix of (at best) stable and in some cases continued decline in production at the volume VMs. Opel/Vauxhall is expected to see total production dip below 900,000 pa through to 2015 (with its recovery dependent on the new Astra and Corsa models after this date). Citroen is likely to fall similarly, while its sister brand Peugeot will also fall in the long run, despite its recent production boost from the 208 and 2008. Fiat will have a tough period until its expanded 500 range comes on stream – and it is possible that funding restrictions could mean this will be delayed and its volumes could be lower than projected in this report.

There will also be a number of exceptions to this negative picture at the volume VMs. This will mainly in the crossover segments, eg the B-segment

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 5

models from PSA (2008) and Renault (Captur) and, as noted above, emerging markets models (301 and C4 Elysee) made in Spain by PSA.

Modest restructuring finally under way The decisions in 2012, by GM, PSA and Ford to restructure and start cutting

excess European manufacturing capacity over the next few years suggest that the volume VMs have finally faced up to the reality of declining demand (in the face of both premium brands and new value brands starting to encroach onto their traditional territory), increased competition and the cumulative impact of substantial financial losses sustained over several years.

While these three VMs are beginning their structural problems through capacity cutbacks, (Ford has closed Southampton in the UK and will soon close Genk in Belgium, Opel is closing Bochum in Germany and PSA is closing Aulnay in Paris), other volume VMs are following a different route.

Fiat and Renault have embarked on restructuring plans which for now exclude plant closures. Renault announced further investment in Spain at the end of last year and this year it has confirmed additional investment in its Douai plant in France as well as plans to bring production of the Nissan Micra to France, to the Flins plant near Paris.

Renault commitment to its Spanish car and powertrain operations includes the production of new engines and two new models at the Palencia factory, alongside the new B-segment crossover, the Captur, which is now in production at the Valladolid factory The Captur is likely to be boosted later this year with the addition of a Samsung badged model, increasing plant utilisation and filling in a gap in the Korean brand’s range.

Like Renault, rather than close any plants, Fiat is investing in its Italian operations, to re-organise the production allocation between its four main Italian plants and re-focus its product line-up around its premium Alfa and Maserati brands and a much slimmed down Fiat range; whether this brave strategy will be successful in the long run remains to be seen, but Fiat has clearly recognised the need to change tack.

Fiat’s reorganisation plans are, however, taking time to be fully implemented, partly because of financial restraints on the company ahead of the full takeover of Chrysler (Fiat needs access to Chrysler’s cash resources to implement its new strategy. Problems with the design and specification of several of the new Alfa models which are integral to the Alfa brand’s revival have delayed the new models’ launches and this will have a direct impact on Alfa volumes which we now see as not growing until 2015 at the earliest.

Rather than close factories, Fiat is reorganising its Italian operations, changing the production allocation between its four main Italian plants. This reflects a new strategy which focuses on the premium Alfa and Maserati brands and a much slimmed down Fiat range, based on the 500 and Panda models; whether this strategy succeeds remains to be seen, especially given the continued delays to the new Alfa product programme.

Fiat plans to use its Italian, Serbian, Polish and Turkish plants as global supply points, a strategy which is new to the company. This will involve selling vehicles under the Jeep – and Ram – names from plants in Italy and Turkey, and possibly the other plants too. If this succeeds, it may well be able to hold onto its existing manufacturing footprint, but if it does not then closures and production cutbacks which appear to be off Fiat’s agenda at this point may well be required. The Fiat Ducato van has been launched in North America under the Ram name in Q4/2013.

This strategy – of investment for growth rather than cutting capacity – is consistent with the announcement in early 2013 from Renault, committing it to growing production in France to 710,000 by 2016 in exchange for its unions agreeing to a range of cost cuts and 7,500 jobs. Even though Renault is adding the Nissan Micra to its Flins factory, our view is that the Renault target will not be met by 2016 if Clio production moves to Turkey in the volumes expected or unless LCV production turns out to be higher than currently projected. We are more confident of Renault reaching its 710,000 target by 2018 however.

We remain somewhat sceptical of Fiat and Renault’s plans to grow their way out of their current predicaments, ie avoiding plant closures as part of their restructuring plans. However, for the short term at least, both car companies

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 6

have managed to find ways to keep existing plants in operation and convince their backers that continued investment is the way forward.

Meanwhile, in the UK, Honda has cut several hundred jobs and retrenched somewhat, while Vauxhall moved production at its Ellesmere Port plant from a 5-day to a 4-day week (although working four longer days and nominally maintaining production levels). These moves have been described as necessary to “right-size” these plants’ capacities on an interim basis while demand recovers ahead of new model launched planned for these factories; the companies remain committed to these UK factories in the long run.

Elsewhere, the common approach to falling demand – putting factories on temporary shutdown – is being followed; Ford has announced a series of down days recently for its Craiova plant which makes the B-Max, sales of which are slowing.

By contrast with the problems and pressure to change faced by the volume VMs, at several other VMs, especially the Koreans, the VW group, the German premium brands, JLR and indeed some of the Japanese, the current economic uncertainty has been less of a problem.

Inevitably, there will always be winners and losers as markets evolve; our view is that the losers are likely to be the traditional volume brands whose recent and likely future restructuring may actually only serve to delay the eventual demise of one of the traditional volume players. The path being followed by the Koreans and the premium brands is not easy, but their relative stability and in most cases modest growth, amidst the prevailing economic uncertainty, only reinforces the pressure on the volume brands.

JLR’s announcement at the Frankfurt motor show in September that it would launch a new range of aluminium-bodied Jaguars from 2015 with a major expansion at Solihull is indicative of the positive outlook for the premium brands in general. Since this announcement was made, news has emerged of the range of models which will appear on the new JLR aluminium platform, including Jaguar and Land Rover SUVs and a range of conventional Jaguar bodystyles, sedan, coupe and estate.

The full report contains further insight into the new JLR range and the potential production volumes which will flow from this range expansion. Our view is that

by the end of the period under consideration here, JLR could well be producing around double the volumes it made in 2012; the precise point in time when this is reached will depend on the exact launch timetable for the recently announced models and variants thereof and the degree to which production in China and even India takes some production away from the UK; however, based on our current understanding of JLR’s plans, we do not expect the expansion of JLR’s production footprint to have a significant impact until later in decade by when the recently announced new models will be in full production.

In general, the premium brands have had fewer problems in terms of excess capacity than the volume companies. Although Mercedes had to implement production slowdowns for some of its large car lines during 2012, this was largely a function of model cycle effects. In fact, as we have noted before, Mercedes has had a structural shortage of capacity for its new A-/B-class range; and in order to overcome this problem it has had to bring on stream additional capacity at a contract manufacturer, Valmet in Finland in order to cope with stronger than expected demand for the A-class. It has also accelerated plans to increase production in Hungary as the range of derivatives of the A-/B-class widens; the recently launched CLA sedan for example has exceeded all initial sales expectations and it would not be surprising if production capacity for this model were to be raised in the future.

Theoretically, capacity could have been found in Rastatt or Hungary, were production limited to the basic A- and B-class models – however, both factories are going to be making much more than just the basic models, and this production complexity lies behind the decision to move some production to Valmet. Even so, Daimler is bringing forward the planned expansion of its new Hungarian factory.

In parallel, to meet long-run expected demand for Minis, BMW has reached agreement with the new owners of the Nedcar plant in the Netherlands, to produce up to 100,000 Minis there per year from 2014 – capacity at the Mini plant in Oxford is at its limit. BMW models could be added to the production line-up in the Netherlands in the years ahead, although for now we believe this plant will be allocated to Minis only.

The change in the market towards premium brands is evident in the continued expansion of the product ranges offered by the German brands Audi, BMW

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 7

and Mercedes – but it is also evident in the recent announcements of further expansion at JLR in the UK – and the intention of Nissan to add production of its first Infiniti model in Europe in the period covered by this review.

The premium brands, notably JLR, Mini and the Germans, continue to see strong export market demand, especially from North America, China and much of Asia. Demand appears to be holding up well here. The global appeal of premium brands is moreover evident in Nissan’s decision to export its UK-made Infiniti model on a global basis.

While export markets outside Europe may have their own problems and be subject to their own fluctuations, such export markets are generally not open to the European volume VMs; Ford, Opel, PSA, Renault and Fiat tend have their own production facilities in these markets already, making exports of the same or similar (but normally more expensive) European-made models impractical. Fiat and Ford (in LCVs) are trying to circumvent this traditional block on their sales but how successful this strategy will be – especially at Fiat – remains open to debate just now.

In our view, what the current situation suggests is that, in the main, the losers are likely to be the traditional volume brands whose recent and likely future restructuring may only serve to delay their eventual demise. It remains to be seen what format this “demise” might take, as outright closure of a major European volume brand might seem difficult to imagine – some form of corporate realignment, ie merger, is likely however. It is a question of timing.

Production in Russia will be increasingly important Russian production will also help drive future production growth in Europe as a

whole, with c2.6mn units – and quite possibly more – currently scheduled to be made by European, Japanese and Korean VMs in Russia there in 2017-18.

Predicting the volumes to be made in Russia by the international brands remains a challenge for a number of reasons. There is currently an extensive range of CKD/SKD activity in the country, with models from BMW, GM, Hyundai and others assembled by local assemblers – these do not count as full manufacturing for the purposes of this report but over time we expect some or all of these to switch to full manufacturing operations. Secondly, our

analysis covers the Renault/Dacia-based models which will gradually the old Lada models which are not covered. Thirdly, new VM activity is being added to Russia on a regular basis, for example Mazda in Primorsky in the Far East of the country, details of which remain sketchy at best.

As a result of these factors, it is likely that Russian production by the international brands will effectively be at least 0.5mn units higher in the long term, and possibly even higher than this.

As a result, the significance of Russia in determining the future direction for many VMs and suppliers should not be underestimated. In 2013, production in Russia will account for 60% of the net growth in European production.

Although there will be some production growth in 2013 in the UK, Slovakia, Hungary, Turkey and the Czech Republic, some of this will be “cancelled” out by declines at the volume VMs in France and Germany, plus barely unchanged numbers in Spain and Italy.

Changes in the geography of vehicle production Although there will be broadly stable production in Germany and some

production growth in the UK, Czech Republic, Slovakia, Hungary and Romania, to some extent this is “cancelled” out by declines at the volume VMs in France and Italy, as well as recent slowdowns in production in smaller markets, i.e. Belgium (as Ford’s production cutbacks there begin), Poland (which is hit by declines at Fiat and Opel) and Slovenia (Renault).

Through to 2018 France will see some recovery – from an expected 1.84mn in 2013 – to 2.1mn in 2018; however, this will be much lower than the peaks in 2007-8 and indeed below the level of French production in 2010-11; similarly, Italy – even with the new models from Fiat – will see long run production below 900.000, well below the 1.2mn produced in 2007.

Interestingly, Spain is likely to see its 2018 production volume – at 2.6mn – back to close to its 2007 level of 2.76mn. This reflects investment plans and production allocation by several VMs; the breadth of VMs and their production range in the country is actually a potential strength of Spain.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 8

Production will also rise in Turkey will rise, reflecting the strength of LCV production there by Ford and the transfer of production to Turkey by Renault; meanwhile Spanish production growth reflects the commitment of VW and PSA in particular to the country – and in the case of PSA, the decision to produce a vehicle for emerging markets in Spain; in addition, Ford is shifting large car production to Spain from Belgium which will help underpin production volumes there.

Clear opportunities for UK suppliers …

As a result of continued production growth in the UK, especially at JLR, Nissan and BMW Mini, there will be a corresponding increase in business to be placed with suppliers. The opportunity for UK suppliers will be significant. The announcement of the new Jaguars which was made at the Frankfurt motor show in September will result in significant new business potential for JLR’s supply base.

UK production is expected to rise in 2013 to 1.6mn units; this will continue in the years ahead. We expect the 2mn units’ barrier to be breached in 2017. This rise in production will mean significant opportunities for suppliers in the UK; JLR has already awarded substantial new contracts for the Evoque, F-TYPE and the new engine plant. In the full report we detail the volumes we expect from the most recently announced models by JLR and explain how these could yet be added to in the years to come.

The value of supply contracts for the Evoque, F-TYPE and the new engine plant will be repeated – and probably exceeded – once the new models referred to above have been fully sourced, although details of the work awarded to suppliers will not be made public for a couple of years yet.

In parallel with the new business from JLR, GM has boosted the UK supply bases through re-sourcing more than £300mn worth of business to the UK. Interestingly, some of this is for export, for supply to GM plants in Germany and Spain. GM has also committed to doubling the UK content of the next Astra and Vivaro from 2015 and is now in the midst of searching out new UK-based suppliers.

Other boosts to the UK supply base come from the centralisation of Auris production in the UK, the continued expansion and widening of the model range made at Nissan, the addition of Mini production at Nedcar and other lower volume models such as the Bentley SUV, production of which has now been confirmed for the UK. All of these developments mean additional business opportunities for the UK supply base.

The rise in UK production from these new models will result in further supply opportunities for UK suppliers, or suppliers willing to locate in the UK. Nissan is still in the process of sourcing suppliers for the new models which will be produced in the next few years; although many sourcing decisions have been made, there should still be opportunities for suppliers for models from 2016 onwards. In addition, the centralisation of Auris production in the UK and the widening of the Mini range, allied to the addition of Mini production at the Netherlands, should represent further opportunities for UK suppliers.

Furthermore, as we have previously stated, it is also worth noting that Ford’s Bridgend engine plant has won the contract to supply the EcoBoost engines for the next Mondeo (and related models), further cementing the role of that factory – and its suppliers – within the Ford manufacturing network in Europe. Ford’s UK engine plants have a worldwide supply role, with engines from Bridgend for example being fitted to Focus cars made in Thailand.

As noted above, JLR is also opening its own engine plant in the UK which will offer significant opportunities for the UK supply base. UK engine production already exceeds 2mn units; it is not inconceivable that 3mn engines could be produced in the UK in the long run.

The UK government and the Automotive Council believe that there are supply opportunities worth at least UK£3bn at UK based VMs; in our view, this greatly understates the potential business open to suppliers to the UK VMs. In fact, we would expect the value of new business which will be placed by UK VMs over the next few years, both on new models and on re-sourcing to UK suppliers if they come to the UK, will be more like double this sum.

Potential investors in the UK will moreover be encouraged to set up operations in the UK to supply the UK VMs by the new Automotive Investment Organisation, a dedicated arm of UKTI, focused on attracting more investment to the UK by automotive suppliers.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 9

Production Outlook summary and alternative scenarios We continue to reduce the rate and overall volumes for the recovery; last time we projected that Europe, without Russia, would reach 19.7mn units in 2016 in our Base Outlook. We now see this at 19.95mn in 2016, 20.87mn in 2017 and 21.14mn in 20-18. We agree with the general consensus that there will be a long term recovery in terms of European, although we remain cautious.

This caution derives from the fact that a large part of the recovery plans for Ford, Fiat and indeed PSA include export beyond Europe. While exports beyond Europe are well-established at the premium brands, and can be reasonably expected to continue, the volume brands have much less established records in this area. In the case of Fiat and Jeep exports from Italy in particular this strategy is untested and unproven.

Furthermore, the recovery in European production will be somewhat stymied by the increase in production capacity which is being installed outside Europe by the French and German VMs especially – moves such as the production of the Volkswagen Passat in the US will inevitably reduce the export market opportunities for European car plants, reducing their long run output in some cases. New plants built by VW-Audi in North and South America and China and PSA in China are leading the way in this area. These moves and similar moves by BMW and Mercedes in China and Brazil reflect these companies’ increasingly global positioning but also limit the potential for exporting to these markets from European factories.

In addition to our Base Outlook, we provide a number of alternative scenarios which address the implications of greater falls in various markets than in the Base Outlook. Specifically, we look at the implications of deeper falls for a longer time period across the whole of Europe and also a slower recovery. It is, of course, impossible to predict which scenario is most likely, but rather the aim of these scenarios is to highlight the scale of the problem which could face Europe if the current recession is deeper and the ultimate recovery slower and later than we currently expect.

In our Base Outlook, we now European production recovering in the next couple of years, rather than falling steeply now as it did in the 2008-9 downturn. However, in our Worst Case scenarios, we describe the conditions, in terms of markets falling,

which would be a collapse to the levels seen in 2009. In 2009, excluding Russia, European production fell to just under 16mn units.

In the event that 2014 sees a reversal of the recent slowdown in decline and partial recovery, ie we see continued decline and the hoped-for recovery in the major markets fails to materialise and if exports beyond Europe also decline, then a sustained fall in production over the next 2-3 years to below 16mn is not just conceivable, but in fact highly probable. In the worst case scenario, European production could still be as low as c15.7mn in 2016, c16.17mn in 2017 and c16.66mn in 2018: if European production volumes remain at this level for a period of three or more years, it seems inconceivable to us that all the existing VMs could survive in their current forms. Who might actually disappear – or be absorbed within another company in some of industrial restructuring remains a matter for conjecture right now, but something which will need to be considered seriously in the months and years ahead.

The worst of the scenarios we have prepared has the 2018 volume (excluding Russia) – 16.66mn – at nearly 4.5mnmn units down on our Base Outlook. The implications of such a sustained decline would almost certainly be additional plant closures and significant further industry restructuring, possibly including the loss of a major name from the industry, either entirely or through merger with another stronger player.

In our Base Outlook, we do not see European production immediately falling as steeply now as it did in the 2008-9 downturn. In fact we still think the most likely outcome is a slow, steady recovery. However, in our Worst Case scenarios, we describe the background conditions, in terms of markets falling, which would be a collapse to the levels seen in 2009. In 2009, excluding Russia, European production fell to just under 16mn units. We have 2012 production excluding Russia at just over 16.6mn, rising to just over 17.8mn units this year. The start of the recovery reflects the new model programmes which are coming on stream and in particular, will actually start this year, partly due to improved production volumes at Mercedes and BMW, the increase in production at JLR, the strong performance of Hyundai-Kia and the boost given to the market by new crossover B segment models from PSA and Renault.

However, as our alternative scenarios section makes clear, 2013-14 could actually be much worse than 2012. In the event that Q4/2013 and indeed

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 10

2014 see a reversal of the recent upturn and then further decline, (most likely because the much-vaunted recovery in the major markets especially fails to materialise and exports beyond Europe also decline), then a sustained fall over the next 2-3 years to below 17mn is conceivable. The view of most VMs at the Frankfurt motor show and in response to the recent ACEA figures which showed continued decline in European sales is that we have no reached the bottom of the downturn, that the rate of sales decline has now slowed and that further declines are not expected. Time will tell if this optimism is justified or not. There remains distinct possibility that production volumes could indeed remain at the reduced levels as set out in the Alternative Scenarios. In summary, our view is that, whatever the actual decline or slower recovery, the recovery will be slower than was seen in 2010. At this time, there was an immediate bounce-back in 2010-11, largely due scrappage incentives across Europe. Although such schemes could theoretically be reinstated, given European governments’ financial difficulties, we can no longer envisage a repeat of such schemes being especially likely. Spain has however introduced some sales incentives but we think this will be both short-lived and something of an exception. In addition, we have to factor in the impact of unemployment and the associated decline in consumer confidence in some countries, especially Spain and Italy where unemployment continues to rise and disposable incomes are under increasing pressure.

It is worth repeating the point made above, namely that in the worst case, European production will be remain below 16mn until 2016, below 16.2mn in 2017 and not climb above 16.6mn until 2018. Put another way, this would mean European production may not get back to last year’s levels for another 5 years and even by 2018 would still be below the 2008 pre-recession volumes: if European production volumes remain at this level for a period of three or more years, it seems inconceivable to us that all the existing VMs could survive in their current forms. Who might actually disappear is a matter for conjecture right now, but something which will need to be considered seriously in the months and years ahead.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 11

Demand Side Perspective European sales in decline …

European passenger car registrations fell by 8.2% in 2012 as a whole, continuing the decline in European demand of recent years; this depressing picture has, by and large, continued in the first five months of 2013. For January–May, the regional decline was 6.8% and 5.9% for May alone. The picture for June, for which the figures were released just as this report was being finalised were similar – Europe had seen a decline of 6.6% in H1 and 5.6% in June alone.

Although July produced slightly better results across Europe, with a 5% rise being recorded, by the time the August figures were released, the picture of reversal and decline has returned to the fore. August alone saw a 5% decline across Europe, with the year-to-date decline at 5.2%.

However, September and October saw better figures, with total EU registrations up 5.2% in September and 4.7% in October.

More specifically, in October:

The UK continued its strong performance, up 10.2% for the month and 4% for the year.

France and Germany were up 2.6% and 2.3% respectively in October by were still down 7.4% and 5.2% for the year-to-date

Spain was up 1.1% for the year-to-date and 34.4% for the month of the October – due to sales incentives underpinned by the government. In total the monthly figures were still down, by 8% and the year-to-date numbers were also down 5.6%.

In terms of other markets, there was a mixed picture. Positive results for the year to October included:

Austria (+1.6%), Bulgaria (+11.6%), Denmark (+10.9%), Estonia (+21.5%), Finland (+11.0%), Hungary (+26.7%), Netherlands (+37.4%), Poland (+19.3%), Portugal (22.8%), Slovakia (+37.6%), Slovenia (23.1%) and Sweden (+5.4%).

The other negative markets in October were Belgium, the Czech Republic, Greece and Romania

In terms of the year to date figures, the picture was still largely negative - because of the poor performance of these markets in the early months of the year. Indeed, apart from the UK and Spain, the only markets with positive year to date results were:

Denmark (5.8%), Estonia (+14.7%), Hungary (+6.5%), Poland (+4.8%), Portugal (+8.1%), Slovenia (+4.5%).

The figures so far for 2013 are somewhat more positive than for the full year data for 2012 as a whole which can be summarised as follows:

EU27 registrations were just over 12.5mn, down from almost 13.6mn in 2011.

The UK was the only major market which saw an increase in registrations in 2012, by 5.3% to just under 2.05mn units.

Bulgaria, Estonia, Hungary and Luxembourg also experienced gains in 2012, but all other markets shrank.

Even Germany, so long the engine of growth in Europe, saw a contraction of nearly 3%, while France fell by c14%, Italy by c20% and Spain by over 13%.

In terms of the VMs, the picture for 2012 was also broadly negative, ie:

VW group was down 1.6%, but Audi was up 3.1%.

PSA was down almost 13%, with both Peugeot and Citroën declining by the same percentage.

Renault was down by 22%, while Opel/Vauxhall fell by nearly 16%.

Ford fell by 13% and Fiat by 15%.

At the premium brands, BMW fell by just 0.5%, and Mercedes by 1.8% (note how Audi continued to grow by contrast); Volvo fell by almost 10%.

However, Jaguar-Land Rover did much better, up nearly 26% with most of this growth due to Land Rover which was up 33% year-on-year.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 12

The picture at the major Japanese VMs was also negative, with Toyota down 3.1%, Nissan and Honda each down by 6.3%.

Hyundai-Kia continued to grow, with Hyundai up 9.4% and Kia up 14.1%.

In terms of January-October figures for the VMs, there were positive results in European registrations for the following:

BMW +0.9%

Dacia +20.2%

Mercedes +6.8%

Kia +0.8%

Jaguar +9.2%

Land Rover +16.6%

SEAT +10.7%

And Skoda +1.2%

Other VMs and brands were negative, such as Volkswagen (-6%), Audi (-2.4%), Ford (-4.8%), Fiat group (-8%), Renault (-3.6%) and PSA (-10.3%).

Light commercial vehicles The picture with LCVs has not been much better – these were down by 13.3% in 2012 across Europe, with all the major markets declining, ie: Germany -6%, UK -8%, France -11%, Spain -26% and Italy -32%.

The negative picture from 2012 has continued in January-March 2013 with total European LCV registrations down by around 10%; the UK actually increased by c11%, but it remains to be seen if this is a real change in fortunes for the sector or just a one-off. France (-9.2%), Germany (-9.6), Spain (-9%) and Italy (-22.5%) all fell between January and May, albeit by lower percentages than in the four months to April, suggesting that the decline in the LCV market is finally slowing.

By the time that figures for the period to June were released, there was still no sign of improvement in the LCV market. June figures were down 4.2% for the month although both the UK (+3.4%) and Spain (+21.9%) saw monthly rises in LCV sales.

Germany was down 6.7%, France down 8.6% and Italy fell by 10.9%. Looking at the first half of the year as a whole, the UK is the only market to show an overall rise, up 11.2%; by contrast, Spain was down 3.8% despite the rise in June; Germany fell 9%, France by 9.1% and Italy by 20.1%. The overall decline in LCV registrations in Europe was 5.9% for H1.

And there was not much improvement in Q3; in terms of year-pt-date figures for the 9M to September:

The market is down 6.1% - although the UK was up by the same percentage

Germany was down 8.9%, France was down 8.4%. Italy was down 14.1% and Spain was down 12.1%.

In fact the only LCV markets, apart from the UK, showing positive results were: the Czech Republic (+7.9%), Estonia (+34.8%), Greece (+26.1%), Ireland (+21%), Lithuania (+1.3% and Poland (+1.9%). The LCV market clearly has a long way to go before it returns to health.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 13

Production Outlook Overview

Introduction In the previous edition, we extended the Production Outlook to 2018.

As before, although we include the full manufacturing volumes for the European/Japanese/Korean/American VMs in Russia, we do not include the CKD volumes for these VMs in Russia; the CKD numbers are part of the reported figures for individual countries herein. Furthermore, we do not include the indigenous Russian brands (mostly the original Ladas), which are all slowly being replaced by international models (essentially Renaults, Dacias and Nissans).

As a result we understate the number of vehicles assembled in Russia (the CKD volumes in Russia are countered within the production volumes for the countries where the kits originate, ie elsewhere in Europe, Korea, North America, Japan or China. There remains a lack of information to allow fuller coverage of the Chinese VMs; Great Wall has now opened its plant in Bulgaria, while the Chery plant in Turkey, which is a JV with Turkish company, Mermerler, will not actually start production until 2015; when fuller information is available on these VMs we will report on them in detail.

Production fell in 2012 … Owing to disputes over data provision, France still has not released official data at model level for 2012 production, so our figures still have some element of being provisional about them. Official German data is also less detailed than in the past and as a result some of the German numbers may be subject to minor change in due course when more detailed data is accessible. Our total for 2012 European production, including Russia, is just under 18.2 units. Without Russia, we record Europe in 2012 at just over 16.6mn units, down almost 1.75mn down on the c18.38mn units total for last year. For 2013, we now expect a modest recovery to c18.97mn units, including Russia, compared to 18.66mn units which we projected last time. This increased total is indicative of the stronger signs of recovery which are now evident compared to our last report. Moreover, we have Europe without Russia growing to just over 17.8mn units which

an improvement on last time (17.4mn – again reflecting better than expected performances of some new models). In fact we now think that 2013 will see Europe, excluding Russia, recovering almost 2/3 of the losses it experienced in 2012. More specifically, we see the 2013 revival occurring as follows: Spain (+230k), mainly due to better than expected performances from Ford

and Citroen Germany (+130k), with slow and steady improvement mainly at the premium

brands Romania (+100k), due to the new Dacia Logan/Sandero range coming on

stream, plus the Ford B-Max, albeit at lower volumes than originally expected Serbia (+100k), where the new Fiat 500L and variants based on this new

model are now in production Morocco (+90k), with the new Dacia Dokker and Lodgy models in their first full

year of production Turkey (+70k), with Hyundai i10/i20 and various models from Renault and

Toyota contributing strongly. UK (+60k), with the growth coming from JLR and the new Toyota Auris; a

boost in Q4 may be expected with the new Mini. By contrast, 2013 will see declining production in France, Belgium, Italy, Poland, Portugal and Slovenia. In summary, bulk of the growth in Western/Central European production will come from the premium brands in particular. PSA’s emerging markets models made in Spain and the continued growth of Dacia, partly because of the addition of production in Morocco (which counts within “greater” Europe for the purposes of this report) show that there is a strong market, in Europe and beyond, for value brands/products. The continued weak economic outlook, lack of consumer confidence (the UK’s current boom in car sales notwithstanding) and the progressive shift of production from Europe to China and the US at several VMs, means that we still have to sound a note of caution. Although the economic figures in the UK are better than expected of late, the recovery is not secure across Europe and we continue to produce our scenarios looking at what might happen if the recovery stalls and export markets go into reverse.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 14

Certainly Fiat, Ford, Opel, PSA and Renault have given us much cause for concern in 2012 – and this has not been entirely dissipated of late.

2012 versus 2011 Looking at 2012 versus 2011 in particular we can note specifically:

Fiat, which lost c158,000 units in 2011 over 2010, saw a further fall of around 187,000 to just over 1.03mn units in 2012, despite the new Panda, continued strong production of LCVs and the arrival of the new 500L series. Delays in the launch of various models, including variants of the new 500L range and the decision to drop the Bravo replacement did not help. The situation was worsened at the group level by delays to various new Alfa models and associated delays to the equivalent Chrysler or Jeep versions. (The situation at Alfa in terms of new model launch times has still not been resolved and in the detailed numbers in the Outlook we have put Alfa’s growth to at least 2015: it could well be later than this.)

As a result of the economic situation and these programme delays, we do not expect Fiat’s recovery in production to reach a significant level until 2015 for the group and 2016 for the Fiat brand in particular. Moreover, as we have noted before, this recovery will be at least partly contingent upon US consumers accepting European-made models (especially those made for sale under the Jeep brand), production growth at Fiat’s Turkish affiliate Tofas, and production in Russia, at an all-new plant, being a success. Fiat is also in the midst of reorganising the allocation of production between its Italian factories, although the full implications of this change will not be felt for some time. Fiat has suggested that it wants to make around 150,000 small (B-segment) SUVs for Jeep in its Italian factories for global sale, but especially in North America. This total, alongside the proposed 130,000 small SUVs for the Fiat brand, seems optimistic to us and we have projected somewhat lower numbers for both brands in the Outlook.

Ford, which we estimate to have been down by c209,000 units in 2012 over 2011. This decline was largely due to the slowdown in production of its large models made in Belgium, the Fiesta (ahead of this an imminent facelift and then an all-new model in the next couple of years) and delays to new models expected to be made in Romania.

Ford also intends to make a major push with its LCV range, widening its range to include small vans which will be sold under the Transit brand; Transit is intended to be transformed into a global brand in its own right, with a range of models bearing the Transit name. The bulk of the growth in Ford production projected at the end of the period covered in this Outlook comes from increased LCV production in particular, as well as a general rise in production in Russia, as opposed to a significant rise in passenger car production at its traditional European operations.

GM Opel/Vauxhall, which lost just over 40,000 units in 2011 compared to 2010, saw a further fall of around 260,000 units in 2012, with this loss spread across most of its model range. The expectation is that Opel/Vauxhall volumes will continue to fall for the next two years ahead of the new Astra and Corsa which are due from 2015 onwards. The replacement Zafira and all-new Insignia follow soon afterwards (a heavily revised and updated Insignia was shown at the Frankfurt show but this was not a completely new model). The recently launched Adam and Cascada will help ameliorate the general decline, as will the Insignia facelift, but these are not high volume models and Opel/Vauxhall needs its new volume models sooner rather than later to help it recover its production volumes to any appreciable extent.

We have noted in previous reports, the model cycle timings of the Opel/Vauxhall range could not have been timed worse as they have coincided with the deepest trough in the current economic downturn. GM has cut into its cost base by confirming it will close Bochum – and has in fact brought this closure forward to 2014. The financial benefits of this move and the alliance with PSA will, however, take some time to be fully evident.

The company is embarking on a new strategy, Drive! 2022, which will see the model range extensively overhauled in the next few years. GM management in the US is backing its beleaguered European operations, so perhaps Opel/Vauxhall will be able to turn around its fortunes later in the decade. Press reports that PSA would be sold to GM – or at least GM would take an increased stake in PSA and direct its strategy – have been strenuously denied by both sides and we certainly do not expect any closer association between PSA and GM in the near future. GM executives have made it clear that the task facing both companies in the near future is to make sure the currently planned joint programmes come to fruition.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 15

PSA, which was stable in 2011 over 2010, is estimated to have lost around 360,000 units in 2012. Earlier in the year, we had expected that it would see a further c50,000 unit decline in 2013; however, the greater than expected success of the 301 and C4 Elysee (models made in Spain emerging markets) and similar success of the 208/ 2008 mean that we now expect PSA to experience a small rise in production this year from 2.018mn to 2.049mn units; however, PSA’s position remains challenging as much of its model range is heading into the downward phase of model cycles and facing tremendous competition in very difficult economic times. Like Opel/Vauxhall, we do not expect to see any significant benefit from the GM-PSA alliances until much later in the decade, most probably after 2017 by when the first jointly developed models should have appeared.

Although PSA has stopped the decline in its volumes, its “recovery” will be modest at bestir and we still do not see it getting back to 2007-8 production volumes – the pressure to close more than one factory in Europe (ie in addition to Aulnay) may well become stronger. We think that there are likely to be further changes to PSA’s production arrangements once the GM alliance moves into all-new model programmes, but on balance, these are unlikely before 2016/7. As noted above, in the GM section, we expect the companies to focus on making their current plans work before embarking on a further round of alliances

Renault: although group production, including Nissan and Dacia, is largely on an upward curve, at Renault itself the reverse is true in the last couple of years; we estimate Renault to have lost around 204,000 units in 2012. We expect Renault to lose another 80,000+ units in 2013. By contrast, Dacia continues to go from strength to strength, adding c60,000 units in 2012. Nissan meanwhile saw another record production year in the UK.

In comparison to the volume brands, most other brands were either stable in 2012 or saw modest increases in production. The Volkswagen brand saw a small rise in production volumes, of around 62,000, largely on the back of the new Golf, while SEAT also saw a rise in production of c26,000, but this was actually due to the Audi Q3 which is made at SEAT in Barcelona. BMW/Mini also saw a modest rise in 2012 production, due to rising Mini output. Audi actually fell somewhat in 2012, 2011 having be an unusually high year.

We now turn to a brief commentary on how we see 2013 turning out for the major

VMs:

Summary of 2013 projections: BMW will be up around 125,000 with improved performance at both BMW and

Mini

Daimler will be up around 140,000 due mostly to strong performances from the variants on the A-class, eg the CLA

Fiat is up very slightly but by only c33,000, one-third of which comes from Maserati’s expanding model range; we don’t see Fiat really improving until 2015 when the 500X comes on stream

Ford will be up c50,000, partly due to models made in Spain doing better than expected

Opel/Vauxhall continues its decline by just over 60,000, reflecting the age of its models; as noted before, until the next Corsa and Astra come on stream we do not see much material improvement for the Opel/Vauxhall brands in Europe.

Hyundai-Kia is up slightly, mostly due to the i10/i20 in Turley.

PSA improves somewhat this year following new models like the 2008 and the emerging markets models made in Spain – however, this is likely to be a short-lived phenomenon with the Peugeot brand especially expected to decline somewhat in the years ahead. Citroen will do better with the expanded DS range.

Renault will decline slightly as its main volume and large cars continue to age; the success of the Captur B segment crossover provides some modest relief ahead new models coming on stream from 2015. Nissan grows slightly while Dacia grows strongly due largely to the new plant in Morocco coming on stream and some growth in Russia.

Tata-JLR will have an especially strong 2013, with both Jaguar and Land Rover experiencing strong growth. We don’t see much growth in the next couple of years at JLR – but once the new range of Jaguars and Land Rovers, as presaged at the Frankfurt motor show this year, come on stream, from 2015 onwards, JLR will see very strong and rapid growth as its range expands.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 16

Toyota is on an upward curve now, partly because of an expanded range in Russia and also the new Auris/Corolla/Verso range produced in the UK and Turkey.

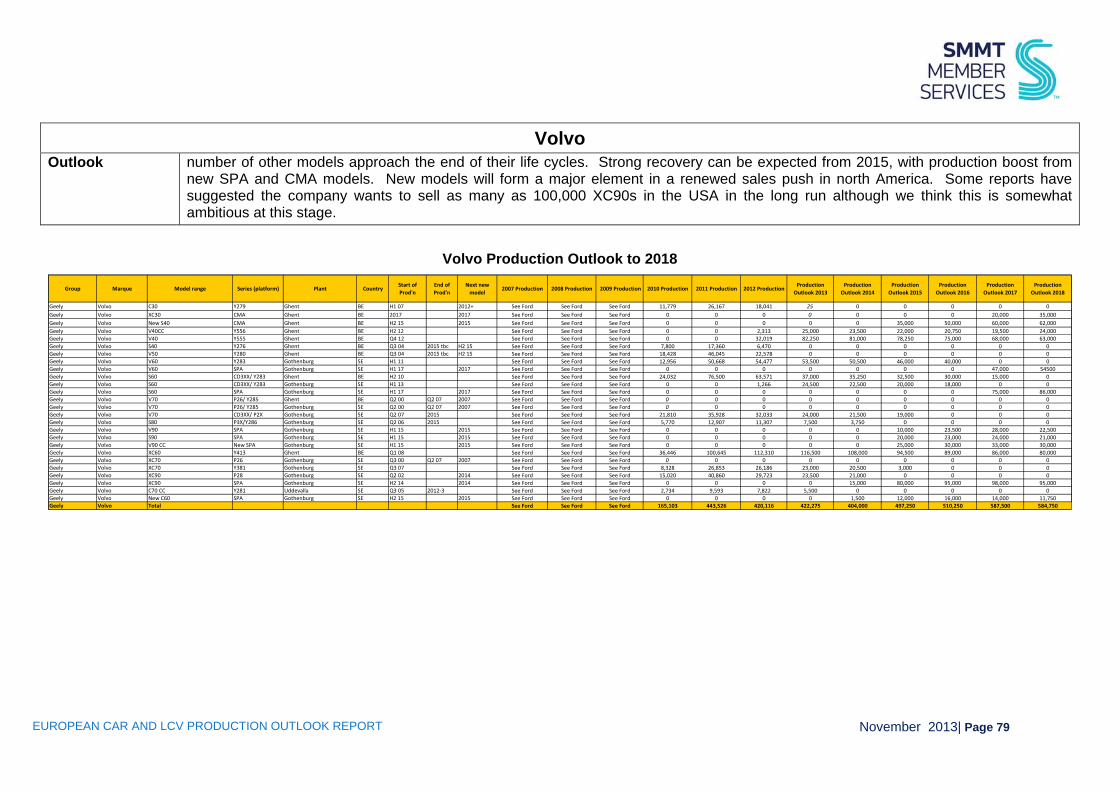

Volvo is expected to be broadly stable this year and will actually fall slightly next year as model changeovers take place – from 2015 however several models on the new SPA platform come on stream and will give the brand a strong boost in production.

The VW group has had a generally better year than 2012 but the most successful brand in production terms is likely to be Skoda, mainly because of the Rapid/Seat Toledo.

Turning now to the country picture, we look at the main vehicle production countries in alphabetical order:

o Belgium: Having seen over 851,000 vehicles made there in 2007, production has fallen steadily since then to just o490,000, owing to declining production of the large Fords and the older Volvo models made there.

o The one bright spot in Belgium is the Audi plant which will produce over 200,000 upa by the end of our Outlook period. However, this will not stop the long-run decline in Belgian production which will now take place following the decision by Ford to close its Genk factory.

o Production in Belgium will now settle back in the range 450,000 upa and will rely on Audi and Volvo for any future growth. The recovery at the end of the period covered here reflects the expanded range which we expect to be produced by Volvo on its CMA platform from 2016 onwards.

Czech Rep.: production climbed to over 1mn units for the first time in 2010, a level which was sustained in 2011 and 2012. The country has benefited greatly from the success of Hyundai and Skoda which have more than compensated for falling production at the PSA-Toyota JV. We expect Skoda and Hyundai to continue to grow, while the PSA-Toyota JV will produce a new model in the near future – on the back of this, we have a broadly positive outlook for Czech production, expecting it to exceed 1.3mn upa by the end of the period covered by this report. If Hyundai invests further at Nosovice, as we expect it will, then the 1.4-1.5mn upa level could be reached and indeed surpassed by the end of the decade or in the 2020s for sure.

France: production reached c2.25mn units in 2011, following two years of growth; despite the rise in production in 2010-11 (after the collapse in 2009), the 2011 total was still some way off the 2.5mn units in 2008 and the 2.9mn units of 2007. However, 2012 saw a steady fall in French production to just under 2mn units, a low point for many years, a fall of 268,000; this fall is in spite of the benefit of the new Peugeot 208, the new Yaris, revised Smart and the EVs from Renault. Moreover: o We expect France to remain below the 1/9m level from this year until

2016, after which point we expect a climb up above 2mn pa once again. o There will be a revival in French production from 2016, but with Renault

increasingly orientating itself towards Russia and other emerging markets, following PSA’s lead, we do not expect French production to climb back once again to past levels.

o Renault has announced a renewed commitment to production in France, but to a large extent this will only partially make up some of the recent losses in production and will not fully compensate the country for the loss of PSA production and earlier overall decline. There is, moreover, no cast-iron guarantee that Renault’s targets for increasing production in France will be successful; we think these are optimistic ambitions in any case and will depend on the success of other brands, not just Renault. Renault is going to make Micras for Nissan and will continue to make small vans for Mercedes, but we remain to be convinced that these contracts will be sufficient to make up for the loss of production of other models, especially the Clio which is moving increasingly to Turkey.

o As a result, we now expect France will actually fall behind Spain and will also face a challenge from the UK in the battle for 2nd, 3rd and 4th spots in the EU country rankings behind Germany. In fact we expect the UK will over take France from 2016 onwards.

o By the end of the Outlook period, we expect production in France, still at just over 2.1mn, will be around 807,000 units down on the 2007 level, reflecting already planned production shifts by PSA and Renault to Slovenia, Slovakia and Turkey, political pressures from the French government and Renault’s recent renewed commitment to French production notwithstanding.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 17

Germany: although 2011 saw German production climb to almost 6.13mn units, it fell to just over 5.61mn in 2012; following the new Golf and other models at the premium brands having a strong performance in 2013, we now expect a rise to 5.75mn in 2013, a slightly lower 5.7mn in 2014 and then 5.8mn in 2015 as new model programmes settle down. We now expect Germany to reach 6mn units again in 2018.

The fall in 2012 in German production was attributable to a number of reasons, including: o A large part of 2011 production was actually for “brought forward demand”

attributable to temporary scrappage schemes and to meet the initial burst of recovery demand from North America in particular.

o Failing short-term production of several models which are due to be replaced in the next 2-3 years, eg Mercedes C-class, Ford Fiesta, Opel Astra, and the Volkswagen Passat/CC.

o A shift of some production away from Germany, with the Passat already being made in the USA as well as Germany, and the Mercedes A- and B-class seeing some production moving to Hungary. Audi will move production of the Q5 to Mexico and BMW will make all its X series models from the X3 upwards in North America rather than Europe.

o A general decline in production in Germany by Opel and Ford. However, 2013 and 2014 will see the loss of 2012 fully recouped; moreover,

o By the end of the period covered by our report however, we expect production to have climbed back towards 6mn upa, reaching 5.9mn in 2017 and 6m in 2018, with a series of new models boosting production.

o The continued importance of Germany to European vehicle production will remain. All the principal German brands will remain focused on producing vehicles in Germany, although the capacity installed by the premium German brands outside Germany is also increasing.

o Daimler has started full-scale production at the new Mercedes plant in Hungary; and BMW has said it will establish full manufacturing in Russia, although this will almost certainly be after the time period with which this report is concerned; Daimler has established a van production JV in Russia, but has said it will not build a car plant there for the time being. BMW has committed to a new plant in Brazil and Mercedes is expected to

increase capacity there in the near future as well. o Audi has expanded production capacity in Neckarsulm in Germany and at

Gyor in Hungary and it is now building a factory in Mexico with production of the Q5 starting there in 2015. It worth repeating the comment made in previous reports that one of the reasons for the expansion of BMW and Mercedes production outside Germany has largely been undertaken in order to free up capacity in Germany and to allow the German factories to produce a wider range of models.

o VW, BMW and Mercedes are all expanding the production ranges in the US and China – and this trend will undoubtedly continue in the years ahead.

Hungary: for some years, vehicle production in Hungary had been limited to Suzuki and a small volume at Audi. However, we will now see a steady rise in production in Hungary in the years ahead. Audi is adding capacity to allow production in Hungary of more than 100,000 upa (for the A3 sedan primarily) and Mercedes is producing some of the new A- and B-class programmes in an all-new plant in the country. We expect the 208,000 units made in 2011 to double by 2016 (slightly later than expected before) and then climb to nearly 460,000 upa by 2016-17, with the bulk of this growth coming from Audi and Mercedes. Suzuki’s renewed commitment to its Hungarian operations, announced in late 2012, should see even more production growth later in the decade, but we need further details on the company’s plans before commenting in greater detail here. If Mercedes can bring its expanded capacity on stream sooner than expected and accelerate the new model programme associated with the factory, then the 0.5mn units barrier will be breached sooner rather than later

Italy: just as France saw a fall from its 2007 peak, so has Italy experienced a similar fall in production. Vehicle production in Italy was over 1.2mn units in 2007, but it fell steadily every year until 2011 when production was just over 751,000 units. This decline continued in 2012, with full year Italian production at c632,000 confirming the scale of the fall. We expect production to fall again to 626,000 in 2013: o Reduced production volumes have coincided with a series of major

reorganisations at Fiat, the closure of one plant (in Sicily) and extensive negotiations with the unions about improving the efficiency and cost base

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 18

of its Italian operations. The reduced production volumes at Fiat in Italy have been such that total vehicle production in Italy is now running at a total below that achieved by Nissan UK on its own.

o The details of the latest reorganisation were provided in the Foundation report from January, but the key aspects are that: Pomigliano remains production site for the Panda and is likely to be

the production site for the Pandona, the anticipated Panda-based replacement for the Punto.

Melfi will make small SUVs for both Fiat and Jeep. Cassino will make mid-size/compact Alfa Romeos and possibly some

Chrysler versions. And Mirafiori will make a range of other Alfa Romeos and a new set

of Maserati models, although the timescale for the Alfa models in particular remains uncertain

o The full effect of these new manufacturing arrangements has yet to be seen, - and indeed their implementation may be delayed owing to financial restrictions at Fiat ahead of the full takeover of Chrysler being completed. However, our initial assessment is that they will not arrest the long run decline in Fiat production in Italy; accordingly, we do not see Fiat volumes in Italy climbing above 1mn again during the period covered by this report. We now project these as peaking at around 880,000 units by 2018. However even reaching this number assumes success for the B-SUVs, Pandona and Alfa models – and is somewhat lower than projections provided earlier in the year

o In fact such has been the slowdown at Fiat and so significant have the various delays to new models been that we now expect a decline in production in Italy in both 2013 and 2014, to 626,000 and 590,000 units respectively. We do not expect a recovery in production in Italy until 2015 at the earliest.

Poland: here production reached its peak in 2008 when nearly 930,000 vehicles were made; since then production has fallen, and we expect this fall to continue in 2013-14, especially in the absence of further commitment to its plants there from Fiat, VW and GM. Production in 2014 will be in the region of 555,000. The real cause of falling production in Poland is Fiat which has transferred production of the Panda to Italy and which we expect will lose the

Ford Ka volumes in the next few years as well: Fiat will bring some production (of the 500) back from Mexico when the new 500 model goes into production, alongside a smaller City car version; even so, this expanded 500 range is unlikely to compensate fully for the loss of Panda production, and indeed the loss of Opel Zafira production. Poland too has seen total production volumes fall to below that achieved by Nissan UK alone, although with the next Astra and other new models coming on stream the country is well positioned to experience a revival in production in the later years of the decade. However, production in Poland will, like that in Italy fall for the next couple of years before recovering from 2015 onwards. Additional Opel production later in the period covered should mean Polish production will once again climb above 800,000 upa.

Portugal: here production fell from just under 168,000 in 2007 to just under 149,000 in 2010, but rose again in 2011, to c183,000 units – although we now expect it to fall steadily over the next few years and we n140-150,000 upa. The increase in Portuguese production in 2018 will be due to a replacement for the Sharan/Alhambra MPV expected at this time.

That said, in the long term, it would not be surprising to see PSA close its Mangualde plant and it is not inconceivable that Volkswagen could consider re-allocating its own production in Portugal to other group plants at some point in the future. Certainly, we do not expect the VW to produce as many sports cars in Portugal as in recent years and while we expect the VW Sharan to have a good couple of years with the all-new model, we see volumes here falling; the best days of the large MPV segment are arguably behind it.

Romania: like Hungary, this country should see a rise in production volumes in the coming years. The Dacia factory has reached close its capacity, while the country has finally seen Ford producing its first all-new model – the B-Max – here. The B-Max was due to be produced at a rate of c100,000 upa from 2013, but production volumes will be below this target; moreover, we no longer think that Ford will add a second model here within the period cover by the Outlook. Sales of the B-Max in 2013 have been disappointing and a number of down days have been scheduled for the factory in the last four months of the year. Ford had said it would add a second model to the Romanian plant, but it would appear that this programme has been delayed, indefinitely for now. The continued popularity of Dacia range and Ford’s reduced volumes suggest that

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 19

annual Romanian production will be in the region of 420-450,000 upa, depending on the stage in various model cycles. The Dacia plant is understood to be close its full capacity – this has led Renault to build a second Dacia factory in Morocco to supply Europe and the near East.

Serbia: ahead of the recent European economic “crisis”, Fiat agreed to take on the former Zastava plant in Serbia and received significant EU, Serbian government and EIB support. Its initial plans are to make a series of small 5- and 7-seater MPVs based on the Fiat 500 platform. We had also expected this plant would also make a version of the Uno (project 326) which is being made in Brazil, but we now think this has been delayed.

This plant was due to make as many as 180,000 500L and variants this year, but production targets have been lowered, to a maximum of 140,000 units this year. Once all the variants have been launched, and assuming there is no global collapse, it is possible that future production could well exceed 200,000 in the second half of the decade depending on which models (eg the 326) are allocated to this plant. However, for now we have the maximum volumes coming out of Serbia at 150,000 upa. Whether Fiat would have taken on this plant had it been able to foresee the state of the global car market by 2012 is an interesting question – almost certainly the 500L could have been made in Poland or at one of the under-utilised plants in Italy.

Slovakia: production here continues t rise, or remains on the up – due to the Volkswagen Up! and its sister models from SEAT and Skoda. In 2007, production in Slovakia was just over 538,000 and after falling in 2008-9, was back to the 2007 level in 2010. In 2011, with growth at Kia (due to the Sportage and continued success of the cee’d), and the new Touareg at Volkswagen, output climbed to nearly 578,000 units:

On the back of this, and full year production for the Volkswagen Up!, 2012 production is estimated to have risen to over 846,000, up c268,000 units, the bulk which was due to the Volkswagen Up! and its SEAT/Skoda versions. The expansion in this range, the expected continued success of Kia and the widening of the Audi SUV range will all help to push Slovakian production towards 950,000 upa by 2018, similar to the level projected previously. By the end of the decade, production could conceivably climb above 1mn upa, or sooner – depending on the success of variants of the Up! which are due to be introduced, such as the proposed Audi Q1.

Slovenia: here there is just one factory, owned by Renault. Production fell in 2012 and will remain at a similar level this year owing to poor sales for the Twingo and the cutting of one shift; it will take the new Twingo and Smart derivatives from 2014 for production to recover to around the 190,000 upa level. Without the JV with Daimler/Smart underpinning production here, we suspect this plant could well have been deemed superfluous to Renault’s needs. However, having invested heavily to produce the new Twingo and Smart four-seater, there would be little to be gained from closing this plant and moving production elsewhere.

Spain: production in Spain was just over 2.75mn units in 2007, after which point it fell in 2008 and 2009; there was a recovery in 2010 on the back of increased production to meet small cars for the various European scrappage schemes. However 2011 saw a slight fall and 2012 saw a further fall to c1,939,000, a fall of c415,000 units. 2012 saw falling production at most VMs in Spain. Despite the generally negative picture for the Spanish economy as a whole, the outlook for vehicle production in Spain is actually very positive and we expect Spain to see production rise to around 2.3mn units through the latter years of the decade.

More specifically:

o 2013 should now see a recovery to 2.17mn units, with output from Ford and PSA boosting the hitherto negative picture and production volumes much more than had been expected

o Similarly, VW’s Pamplona plant is expected to produce a wider range of models based on the Polo, including a small MPV (the SUV we had expected is now expected to come VW Brazil), VW has also committed to investing c€800mn in Pamplona for the new Polo and various derivatives to be made there over the next five years.

o Meanwhile Ford has allocated a number of new models to Valencia, ie the Mondeo/S-Max/Galaxy which will move from Genk from 2014 onwards; the C-Max will in turn move from Spain to Germany. We had expected production of the Kuga also to move entirely away from Spain, to Russia and the USA, but we now expect some Kuga production to remain in Spain.

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 20

o We expect Fiesta production to be concentrated in Germany; on the one hand this will lead to a direct reduction of production in Spain, but Ford Spain will become the centre of large car production for Ford in Europe.

o Opel has made Zaragosa as the lead Corsa plant and sole source for the Meriva; it will also continue producing the Meriva, despite the imminent arrival of the Mokka. The next Meriva will share the same platform as replacement B-MPV models from PSA. Production of the Meriva and its Citroen counterpart has been confirmed for Zaragosa – one of the few definite successes of the PSA-GM alliance in action.

o PSA is expecting to see a rise in production at Vigo, possibly to 440,000 units this year, following the success of the 301 and C4 Elysee – we think this may be a somewhat overoptimistic target, but certainly some production growth at PSA Spain is expected – we have the Vigo production volume for 2013 at under 420,000 units.

o In addition, Renault has pulled back from the possible closure of the Valladolid plant which will be the sole plant for the new Captur. We understand that there will also be Samsung version of the Captur for export to Korea. At the end of last year, Renault Spain also confirmed the long term future of the Palencia plant, as well as investment in its engine and transmission parts factories in the country. Renault will not, it appears, close a plant in Spain.

o Production in Spain will be sustained by the Volkswagen Polo, strong LCV/SUVs and Pick-up production by Nissan and the decision by PSA to allocate their emerging markets C-segment vehicle to Spanish production, at its Vigo plant. The decision by Renault to invest in Palencia will also help underpin production in Spain.

o With new models coming to Spain and the renewed commitment to country by al the VMs there, we now expect production in Spain in 2018 to climb back to ward 2.6mn, ie around 150,000 units lower than it was in 2007; this is better than we had expected earlier in the year and for now we believe no plants will close in Spain, assuming the models planned for the country come to fruition and are successful..

Sweden: here vehicle production will be much lower than in the past in the short term, by the end of the period covered here we expect it will climb to

c330,000 upa, ie close to the 2007 level when Sweden produced just over 340,000 vehicles. However, this fell to just under than 189,000 in 2011; we have 2012 showing a further fall to 163,000 and with the success of the S60./V60 and continued popularity of the old XC90, we expect to see a broadly stable production volume in 2013 of c161,000. This will be followed by a strong model-led and export-led recovery from 2015 – when the new SPA platform models will begin to be in full production. One variable will be the split of production between Sweden and Belgium for the S60: Volvo has configured its factories so that both can make the model according to the demands for other models at each factory.

Turkey: here, apart from a dip in 2009 and 2012 when production fell, respectively, to just under 850,000 and just over 985,000 units, production has been around 1-1.1mn upa in recent times. Model life cycle effects and the general economic uncertainty meant a slight fall in production in 2012 (which is likely to be recovered in 2013), but the new Chery factory and the new Renault Clio should give production a boost to 1.4mn by 2016 and nearly 1.5mn by 2018. This total will be underpinned by the new Ford Transit and the new Ford small van from 2014. All being well, we expect production in Turkey to settle down at around 1.4-1.5mn upa for the remainder of the decade.

UK: production here fell significantly from 1.72mn units in 2007 and 1.62mn units in 2008 to only 1.075mn units in 2009; 2010 and 2011 were excellent recovery years for UK vehicle manufacture. Production was around 1.44mn units in 2011, and 2012 saw output rise again to 1.56mn units. The positive picture at JLR, Nissan, Mini and Toyota means we now expect 2013 production be over 1.6mn, 1.65mn in 2014; we think the next boost to UK volumes will come in 2015, with the new JLR models coming on stream, along with the next Astra – we project 2015 will be around 1.77mn, rising thereafter to 1.98mn in 2016, before breaching the 2mn upa barrier in 2017/18; the timing of this barrier being breached will depend on model timings for Jaguar Land Rover in particular; the announcements at the Frankfurt motor show concerning the new Jaguar models mean we are even more confident than before that the 2mn upa barrier will indeed be breached in the near future.

Finally, we have to consider Russia:

Here we only cover the international brands which have full manufacturing operations in Russia. Back in 2007, just 170,000 vehicles were made on this

EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2013| Page 21

basis, mostly the Ford Focus and the Renault Clio which was made at Avtoframos. Since then, VW has opened a plant at Kaluga, Ford has added the Mondeo and is expanding its manufacturing line-up in Russia, especially through its JV with Sollers; GM has opened its all new plant at St Petersburg and several other VMs have also started full production in Russia. GM and VW have also established JVs with GAZ, while Fiat is opening its own plant, backed by the Russian bank Sberbank, although its production volumes will be somewhat lower than originally suggested.

Toyota and Nissan have relatively small operations and they have been joined by PSA and Mitsubishi with their JV which started as a CKD operation but which is being transformed into a full production unit and Nissan has committed to expanding production in Russia, with the new Almera to be joined by the Qashqai in the next few years. Nissan will also produce models from its “rising markets” brand Datsun in Russia from 2014 and Toyota has confirmed it will add the RAV4 SUV to its production line-up in the near future too. Suzuki will soon open a plant, and Honda will do the same in the near future; even Mazda should have an operation of some form in Russia in the coming years. Both Nissan and Toyota have invested in new press and large injection moulding facilities in Russia to bring these plants into line with capabilities at its other plants around the world.

Hyundai has opened a brand new plant capable of making 300,000 vehicles and is well on the way to utilising this capacity. However, the biggest change in Russia involves Renault/Dacia models being made at AvtoVAZ, the manufacturer of Ladas. In 2012, Renault-Nissan took effective management control of AvtoVAZ.

Together, these developments mean that in 2012 around 1.1mn foreign brand cars were made in Russia by these international brands – and by 2018 the total will exceed 2.6mn units and could quite possibly be higher than this. Much will depend on whether some of the current CKD operations in Russia become full manufacturing operations sooner than planned and also on the actual rate at which the old Ladas are replaced by new models based on the Dacia Logan platform.

Increasing Russian production will clearly underpin European production growth; moreover, for suppliers this means that the need to follow the VMs to Russia is even more pressing than it has ever been. The importance of

Russia to European production became especially evident in 2011 when production of international brands there climbed over 800,000; in 2012, the 1mn units barrier was breached this total is rising steadily; we expect the 2mn barrier for international brands’ production to be reached in 2015.