15

European Distribution System Operators for Smart Grids Adapting distribution network tariffs to a decentralised energy future September 2015

European Distribution System Operators

for Smart Grids

Adapting distribution network tariffs to a decentralised energy future September 2015

1

Key messages The European Union’s 2009 energy policy objectives have triggered the rapid growth of distributed

renewable energy sources (DRES) across Europe. By the end of 2013, installed capacity of photovoltaic

systems and wind turbines in Europe reached 81 GW1 and 117 GW2 respectively.

In most European countries today, the costs incurred by DSOs are generated by the grid they build to

be ready for any supply and demand situation and its maintenance, whereas revenues are most

commonly based on the energy flowing through the grid and delivered to final consumers. The

variability of electricity generation resulting from the larger integration of DRES and prosumers,

together with increasingly variable electricity consumption, are significantly impacting the ability of

distribution system operators (DSOs) to perform their duties in a business as usual scenario.

Uncertainty regarding DSO costs and revenues is rising, and debate in ongoing at European and

member state level on how to guarantee that grids are prepared for any situations while encouraging

the integration of DRES in a way that is socially and economically fair.

Reviewing and updating current distribution network tariffs will ease the transition towards a more

decentralised energy system. Tariff structures vary across Europe reflecting local grid conditions and

consumer needs, nonetheless European Distribution System Operators for Smart Grids (EDSO)

encourages national regulatory authorities (NRAs) and policy makers to consider the following high-

level recommendations when designing distribution network tariffs.

Grid users should be able to:

Self-generate and self-consume energy as long as the costs induced by their use of grid

services, including insurance against periods when it is not possible to consume one’s

own generated electricity, is reflected in their bill.

Receive compensation from DSOs when adapting their energy consumption/generation

in response to signals (eg. at peak times).

Sign up for “smart contracts” with DSOs, granting them a quicker and cheaper

connection, in exchange for occasional and limited curtailment/grid

disconnection/activation of storage at peak times.

Receive clear and appropriate information before and after new distribution network

tariffs are implemented.

Operators of (non-residential) DRES should:

Be offered reduced locational connection charges in order to incentivise them to connect

in areas requiring less grid reinforcement, and thus costing less to society.

NRAs are invited to:

Make distribution network tariffs more capacity based, and less volumetric based, in order to limit revenue uncertainty for DSOs.

Set up short price periods, ideally one year. The regulatory period, however, should not

be shortened.

1 EPIA, Global Market Outlook for Photovoltaics 2014-2018, June 2014 2 EWEA, Wind in Power 2013 European Statistics , February 2014

2

Table of Content

Key messages .......................................................................................................................................... 1

Introduction ............................................................................................................................................. 3

1. Understanding distribution network tariffs .................................................................................... 4

a. What are network tariffs? ........................................................................................................... 4

b. Understanding capacity versus volumetric tariffs ....................................................................... 5

c. Why should distribution network tariffs be rethought? ............................................................. 6

2. Designing network tariffs for a smooth energy transition .............................................................. 9

a. Reconciling the interests of utilities, prosumers and DSOs ........................................................ 9

b. Optimising renewables integration ........................................................................................... 10

c. Building consumer support for changes in network tariffs – Netherlands case study ............. 11

Annex – Effect of the switch to capacity tariffs in the Netherlands in 2009 ......................................... 13

3

Introduction

The European Union’s 2009 energy policy objectives have triggered the rapid growth of distributed

renewable energy sources (DRES) across Europe. By the end of 2013, installed capacity of photovoltaic

systems and wind turbines in Europe reached 81 GW and 117 GW respectively.

The use of PV is likely to continue to grow worldwide and users to become more active, increasingly

reflecting on the way they consume and produce energy. In a business as usual scenario, this translates

into huge investments by electricity distribution system operators (DSOs) to increase hosting capacity

in the low and medium voltage networks. In a more cost-efficient “smart” scenario it means DSOs will

be actively involved in the management of power flows instead of merely carrying out traditional

reinforcements such as installing more cables or larger transformers.

Meanwhile, electric vehicles and the development heat pumps could also challenge distribution

networks, while on the other hand could offer grid support if smartly reactive.

In order to cope with the growing variability of electricity consumption and generation, an adapted

regulatory framework is needed. This framework should square the circle by ensuring:

- Stable and predictable revenues necessary for DSOs to ensure a secure and stable supply of

electricity in all supply and demand situations, while…

- Not hampering the development of distributed generation and the achievement of the EU’s

energy policy objectives, and…

- Keeping the door open for the development of grid-optimised flexibility services that will help

to reduce grid costs for all network users.

A first step in that direction should be the reviewing and updating of current distribution network tariff

schemes.

In this paper, EDSO presents high-level principles to be drawn upon by national regulatory authorities

(NRAs) and legislators when redesigning distribution network tariffs and which align the interests of

DSOs, owners of distributed generation and society as a whole.

4

1. Understanding distribution network tariffs

a. What are network tariffs? DSOs are entrusted with a naturally monopolistic activity meaning that their revenues and activities

are overseen by NRAs. Network costs paid by consumers are commonly set to allow the recovery of a

pre-determined revenue by adding a charge to customer bills (network tariff) and fixing a price for

connection to the grid (connection charge). As the electricity network is currently built to be available

to all customers at all times, irrespective of their actual consumption and generation patterns,

questions are arising in the context of the energy transition around how to share the costs among grid

users and of how to determine charges for services.

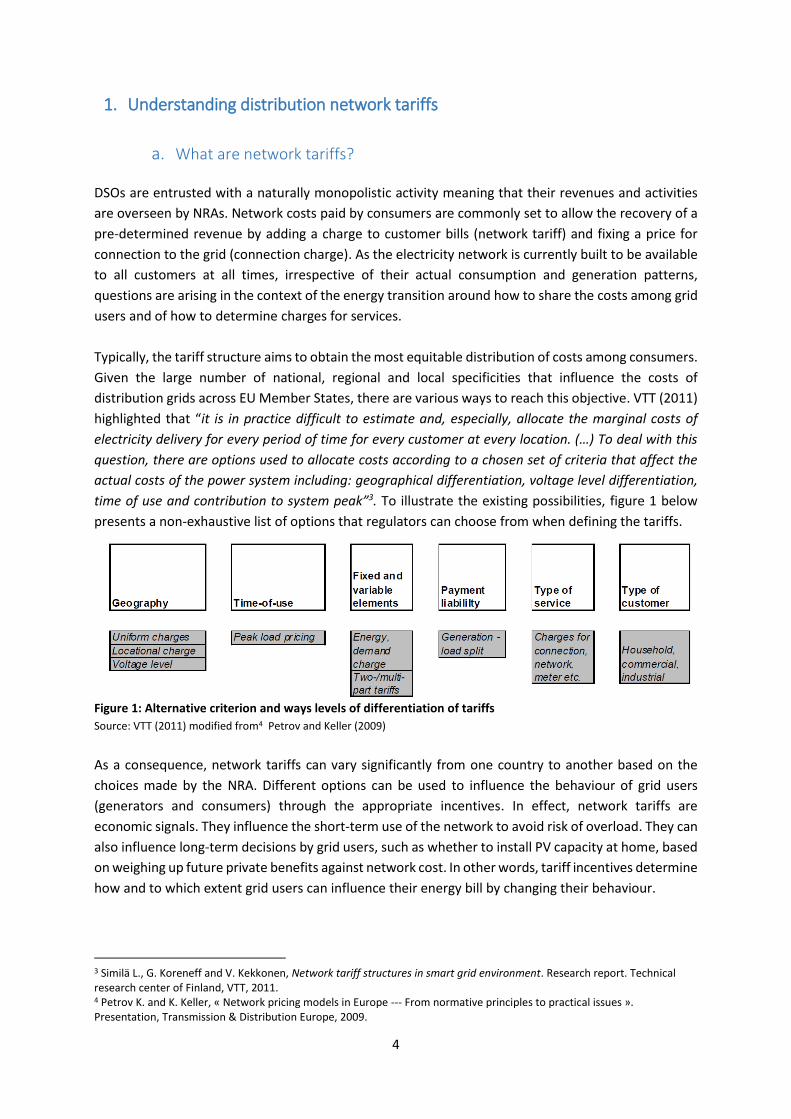

Typically, the tariff structure aims to obtain the most equitable distribution of costs among consumers.

Given the large number of national, regional and local specificities that influence the costs of

distribution grids across EU Member States, there are various ways to reach this objective. VTT (2011)

highlighted that “it is in practice difficult to estimate and, especially, allocate the marginal costs of

electricity delivery for every period of time for every customer at every location. (…) To deal with this

question, there are options used to allocate costs according to a chosen set of criteria that affect the

actual costs of the power system including: geographical differentiation, voltage level differentiation,

time of use and contribution to system peak”3. To illustrate the existing possibilities, figure 1 below

presents a non-exhaustive list of options that regulators can choose from when defining the tariffs.

Figure 1: Alternative criterion and ways levels of differentiation of tariffs

Source: VTT (2011) modified from4 Petrov and Keller (2009)

As a consequence, network tariffs can vary significantly from one country to another based on the

choices made by the NRA. Different options can be used to influence the behaviour of grid users

(generators and consumers) through the appropriate incentives. In effect, network tariffs are

economic signals. They influence the short-term use of the network to avoid risk of overload. They can

also influence long-term decisions by grid users, such as whether to install PV capacity at home, based

on weighing up future private benefits against network cost. In other words, tariff incentives determine

how and to which extent grid users can influence their energy bill by changing their behaviour.

3 Similä L., G. Koreneff and V. Kekkonen, Network tariff structures in smart grid environment. Research report. Technical research center of Finland, VTT, 2011. 4 Petrov K. and K. Keller, « Network pricing models in Europe --- From normative principles to practical issues ». Presentation, Transmission & Distribution Europe, 2009.

5

b. Understanding capacity versus volumetric tariffs

Volume and capacity are two key factors in most network costs making up a consumer’s bill. These are

sometimes referred to as energy and non-energy, or even energy and power. Most total network costs

are composed of a combination of both:

Volumetric tariffs charge consumers on the basis of the total volume of energy a consumer

withdraws from, or feeds into, the grid. The measuring unit is watt per hour (Wh, KWh, MWh)

Capacity tariffs are based on the maximum amount of energy withdrawal (and in some cases

feed-in) potential at a connection point at any one time. The measuring unit is the watt (W).

Capacity can be:

- Standard capacity and charges fixed equally across types of grid users (eg. domestic,

medium-significant grid users) and levied per metering point

- Contractually agreed maximum capacity for each consumer and corresponding price

- Variable, i.e. time-Of-Use (ToU) tariffs, where tariffs vary at different times of the day

to incentivise the easing of load peaks and congestion. ToU can be fixed ahead of time

(for a month, or year) on the basis of historical data on grid use in a particular network,

or can be dynamic, responding to real-time signals from the DSO. Smart meters are

required for ToU schemes.

According to the latter two types of capacity tariffs, two consumers with the same volume of

consumption or generation pay differently to use different levels of grid capacities, as shown in the

figures below. This allows to account for the different levels of strain on the grid, irrespective of total

volume passing through the network.

6

Figure 2 – Cases exemplifying inefficiency of volumetric system to address capacity

Depending on the EU Member State, the network tariff paid by the customer in low voltage (LV)

distribution networks can be predominantly based on capacity, for example in Finland, the

Netherlands, and Spain, but is more commonly heavily based on total volume.

c. Why should distribution network tariffs be rethought?

The ‘standard’ household consuming approximately 3,500 kWh per year is progressively disappearing.

Electricity consumption and local peak loads are being significantly impacted by increasing

electrification and decentralisation of electricity generation. Further technological progress, for

example, energy storage appliances, is expected to reinforce this trend. As such, the fact that LV

network tariffs in most Member States are volumetric is becoming problematic.

Volume-heavy tariff structures - Energy consumption impacts DSO income and

investment/planning ability

Where the make-up of tariff structures is volume-heavy, i.e. in most of Europe, matching costs and

revenues is not an issue for DSOs when electricity consumption remains stable or steadily increases by

a few percent every year. However, consumption patterns are changing, with various factors

contributing to diminishing overall volumes of energy used.

On the one hand, energy efficiency targets have driven measures, new technologies and behavioral

change that all contribute to reducing energy use while performing the same tasks. Households are

increasingly generating a greater share of their own consumption as a result of widespread uptake

DRES such as solar panels, meaning a reduction in the amount of energy taken from the grid.

In some countries, an additional challenge is stemming from net metering which applies to consumers

with their own renewable production unit and which in effect deducts the volume of self-generated

energy fed into the grid from the total volume consumed by that prosumer from the grid. The off-set

is either full or part depending on the policies in the Member State. Under net metering, a PV system

owner receives credits for at least a portion of the electricity he generates, then how long one can save

credits, and how much they are worth vary from country to country.

7

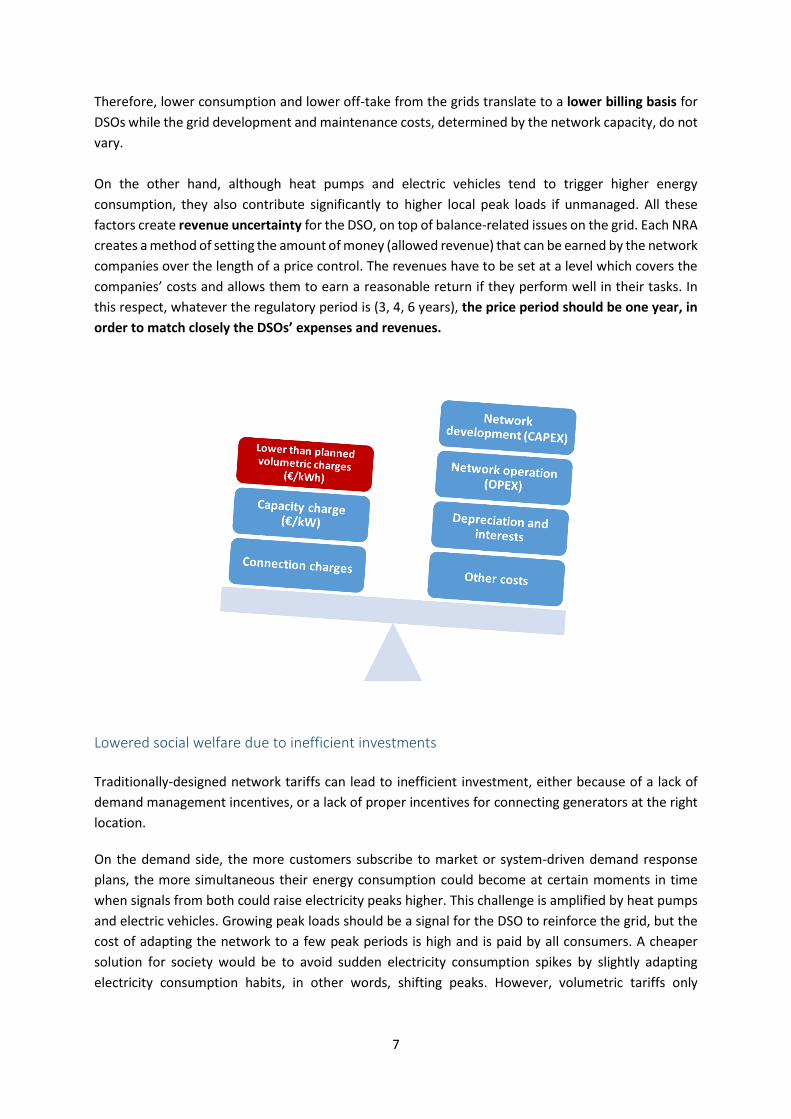

Therefore, lower consumption and lower off-take from the grids translate to a lower billing basis for

DSOs while the grid development and maintenance costs, determined by the network capacity, do not

vary.

On the other hand, although heat pumps and electric vehicles tend to trigger higher energy

consumption, they also contribute significantly to higher local peak loads if unmanaged. All these

factors create revenue uncertainty for the DSO, on top of balance-related issues on the grid. Each NRA

creates a method of setting the amount of money (allowed revenue) that can be earned by the network

companies over the length of a price control. The revenues have to be set at a level which covers the

companies’ costs and allows them to earn a reasonable return if they perform well in their tasks. In

this respect, whatever the regulatory period is (3, 4, 6 years), the price period should be one year, in

order to match closely the DSOs’ expenses and revenues.

Lowered social welfare due to inefficient investments

Traditionally-designed network tariffs can lead to inefficient investment, either because of a lack of

demand management incentives, or a lack of proper incentives for connecting generators at the right

location.

On the demand side, the more customers subscribe to market or system-driven demand response

plans, the more simultaneous their energy consumption could become at certain moments in time

when signals from both could raise electricity peaks higher. This challenge is amplified by heat pumps

and electric vehicles. Growing peak loads should be a signal for the DSO to reinforce the grid, but the

cost of adapting the network to a few peak periods is high and is paid by all consumers. A cheaper

solution for society would be to avoid sudden electricity consumption spikes by slightly adapting

electricity consumption habits, in other words, shifting peaks. However, volumetric tariffs only

8

encourage grid users to reduce their overall energy consumption, but do not incentivise them to limit

their immediate consumption to a specific level. Specific incentives are needed for that purpose.

On the generation side, producers are usually not charged for using the network. They might only be

subject to a connection charge, which can be shallow (only the direct cost of the connection is

charged), shallow-ish (direct connection cost and a share of grid reinforcement costs) or deep (full

connection and network reinforcement costs). Unless where deep connection charges are applied,

there are no incentives for distributed generation project promoters to install their generation units in

places where only limited network reinforcement will be necessary. For prosumers, traditional

network tariffs at low voltage do not incentivise them to reduce their injection at peak production

times by aligning their own consumption to their own production.

Questionable distribution of costs among citizens

While costs incurred by the DSO are not lowered, the costs of distributed energy sources connected

to the grid translate into higher tariffs paid by non-generators. Costs of maintaining the grid secure

act as a kind of insurance against the maximum potential grid use at any moment, which remains

unchanged unless these generators are completely independent from the grid. Prosumers may offset

the effect of an increasing bill due to more self-consumption or net-metering while their share of the

network costs will be transferred to other, and sometimes more vulnerable, consumers who cannot

afford to invest in their own production units. On the other hand, if prosumers were able to contribute

to grid stability through “smart contracts” with the DSO or in response to capacity based tariff

incentives, they could help to keep network costs under control for themselves and their neighbours

by reducing the peak loads that drive the network costs.

Key messages

• Grid Users should be able to self-generate and self-consume energy as long as the costs

induced by their use of grid services, including insurance against periods when it is not

possible to consume one’s own generated electricity, is reflected in their bill.

• NRAs are invited to set up short price periods for DSOs, in order to match closely the DSOs’

expenses and revenues.

9

2. Designing network tariffs for a smooth energy transition Based on the shortcomings of current network tariffs, EDSO invites policy makers and regulators to

take into account the proposals below when designing future tariff structures.

a. Reconciling the interests of utilities, prosumers and DSOs

Driving fairer, more predictable and cost-reflective network tariffs Today, in countries where smart meters have not been deployed, a tariff based predominantly on a

fixed or contracted capacity can help to better reflect real DSO costs and avoid discrimination between

users owning distributed generation and those who do not. This type of tariff also benefits customers

who can anticipate more easily the network-related part of their bill: a cold winter or a hot summer

will have a lesser impact, as the variable part of their network costs is reduced on their bill.

Furthermore, capacity tariffs allows consumers to reduce their bill in the longer-term if they limit the

maximum individual peak use they contract. To help consumers adapt, retailers, consumer

associations, public authorities, and DSOs can provide guidance 5 which can, for example, advise on

how to better stagger consumption over time or promote the uptake of smart appliances and home

energy management systems.

With smart meters, another option could be envisaged: a distribution tariff component based on the

actual capacity used by each grid user. This system would be more conducive to flexibility than tariffs

based on contracted capacity.

Rewarding consumer responsiveness - carrots without sticks ToU capacity-based schemes require that the times at which different tariffs apply are communicated

to consumers in advance, for example, for the following month or year. These predictable variations

in tariffs would help consumers to identify times at which running their appliances will cost less money.

ToU schemes have been used by suppliers in a number of Member States and have shown to be

manageable and economically rewarding for consumers. ToU for the network tariffs could also benefit

consumers.

In contrast, dynamic tariffs try to solve congestions that are imminent. In this case, tariffs vary on short

notice until a sufficient number of grid users change their usage to solve a peak-load or congestion

issue. Dynamic tariffs implemented as the main network cost recovery component run the risk of

penalising consumers who are unable to react to the signals. Also for reasons of complexity, much like

for some approaches to demand response tested across Europe so far, interest in such systems can be

lacking among regular households. Part automated options can be deemed preferable.

A relatively flat tariff system (based on contracted capacity) is simpler to administer and to understand,

as well as ensuring the DSO can develop and maintain the grid to the required standard, but is not the

most conducive to consumer flexibility. However, a flat capacity-based tariff system with an element

5 See for instance http://www.bajatelapotencia.org/como-bajar-la-potencia/ for Spain

10

of ToU, or specific rebates, can prove a win-win solution that offers tangible rewards to the

consumer. This is the case in France for LV and MV users6 where the distribution tariff structure

present both a capacity component and ToU rates for energy consumption. Also being simple to

explain and master, uptake of the solution is increased.

Other solutions exist in order to incentivise consumers to become more flexible, and be rewarded for

it. In most Member States, if grid capacity is requested by consumers or potential consumers, it must

be provided. So far, the benefits and limitations of different tariff structures have been laid out. While

still relevant, capacity-based tariffs could be used alongside smart contracts with large businesses,

industrial facilities, SMEs or DRES (i.e. significant grid users) to reduce (or defer) the need to reinforce

the grid, thus reducing the network costs. For example, such a contract could stipulate that the DSO is

able to limit the consumption or production of a grid user a certain number of times a year, for a limited

duration, at critical moments under agreed conditions. In exchange, existing grid users could get a

single payment or rebate, while new grid user could benefit from a cheaper and quicker connection

(due to the lack of or limited grid reinforcement).

NRAs should adapt the necessary legislation and codes to incorporate these new flexibility service and

connection options7, while still allowing DSOs to limit grid access as a last resort for maintaining the

operational security of the grid and its users. However, the choice of whether to offer such contracts

in certain situations and areas should always be left to the DSO, backed up by a well-designed incentive

scheme. Furthermore, NRAs should ensure that DSOs are allowed to recover these types of payments.

b. Optimising renewables integration Incentivising DRES to connect where less costly

In most EU countries today, when project promoters decide to build a wind farm or to install a large

quantity of solar panels, they first select a location, and then ask the network operator for further

6 http://www.erdf.fr/sites/default/files/documentation/TURPE_4_Plaquette.pdf (in French) 7 See chapter 5.8 (Demand-side management) as an example of these arrangements approved by GEMA http://www.scottishpower.com/userfiles/document_library/SPD_LC14_Statement_14-15_(FINALS).pdf

Key messages

• Grid users should receive compensation from DSOs when adapting their energy

consumption/generation in response to signals (eg. at peak times)…

• … and be able to sign up for “smart contracts” with DSOs, granting them a quicker and

cheaper connection, in exchange for occasional and limited curtailment/grid

disconnection/activation of storage at peak times.

• NRAs are invited to make distribution network tariffs more capacity based, and less

volumetric based, in order to limit revenue uncertainty for DSOs.

11

information on the connection charges. A system providing locational signals reflecting network

development costs is needed to coordinate the long-term developments of the network and of

distributed generation. Differentiated connection charges, based on the location of the connection

point could be a way to take advantage of specific characteristics of grid users while avoiding market

distortions that might be the result of differentiated tariffs for generators in different locations. In

particular, these one-time payments would have an influence on the choice of the location of

generation without altering the marginal cost of the generation unit.

Application of differentiated connection charges to many users with distributed generation (e.g.

photovoltaics), electric vehicles and other appliances that use intelligent solutions (based on their

utilisation patterns and controllability) although more complex, could become a solution in the

medium to long term.

c. Building consumer support for changes in network tariffs – Netherlands case study

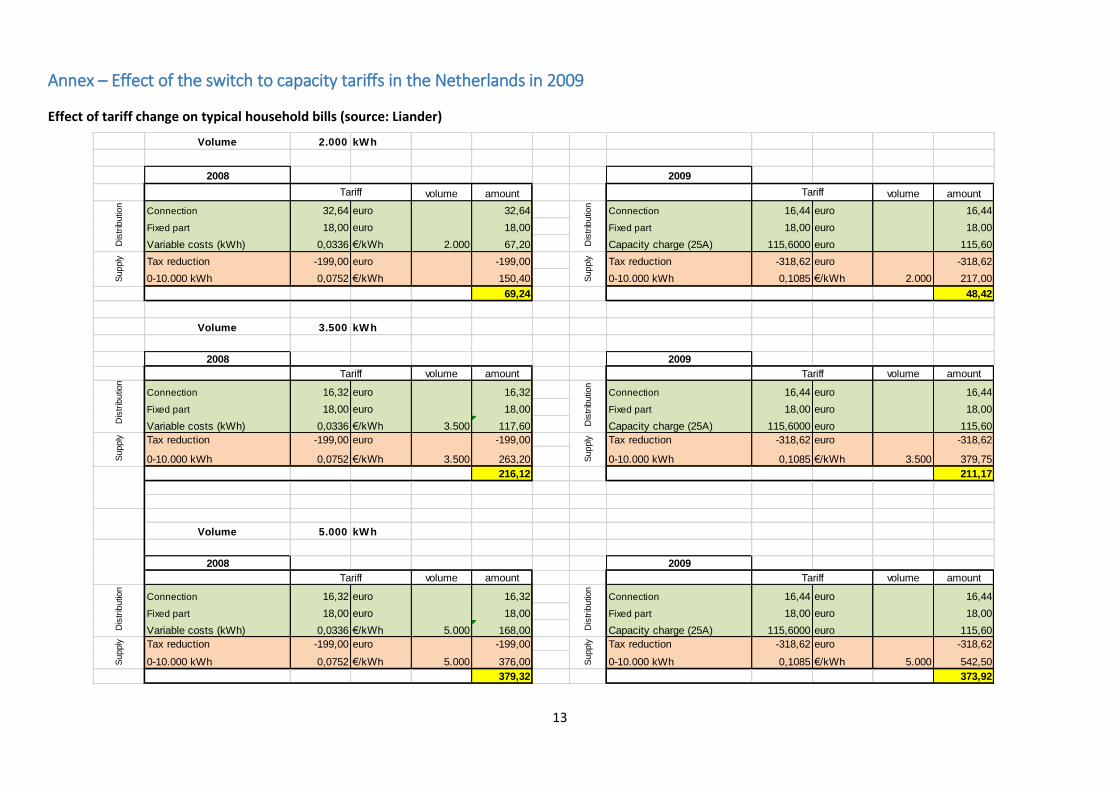

Capacity-based tariffs are already used today in some countries. In 2008, the Dutch government

decided to switch from a mixed tariff (combination of volumetric and capacity) to a system inherently

based on flat capacity for household consumers. Three arguments justified the change:

Network costs are mainly capacity driven and determined by peak demand

New tariffs were considered necessary to introduce a retailer-centric model (only one bill sent

by the retailer, compared to separate bills sent by DSOs and retailers)

Capacity tariffs simplified (aggregated) billing between DSOs and retailers.

A large media campaign was organised in order to prepare citizens for the change. Among other

initiatives, an awareness website was created by the DSOs and the government, informational sheets

were published in national newspapers, and customers with a large connection and little consumption

received a letter inviting them to check their real capacity needs.

In 2009, the capacity tariff was introduced for all connections in the retail market, both for electricity

(≤ 80A) and gas (≤ 40m3/h). In order to limit the number of disgruntled customers and avoid a public

backlash, the effects of the introduction of the capacity tariff were compensated through a revision of

the “energy tax”.

The energy tax had been introduced in 1996 to stimulate energy efficiency, and consisted in a variable

volumetric component. This change was accompanied by a fixed tax reduction on the energy bill. The

more energy a household would consume, the more energy tax it would pay.

Key message

• Grid users should be offered reduced locational connection charges in order to incentivise

them to connect in areas requiring less grid reinforcement, and thus costing less to society.

12

In 2009, the variable component of the energy tax was increased. A fixed tax rebate ensured that

households with a standard connection would continue to pay approximately the same bill. The

transition towards a new distribution tariff happened in several steps:

1. A compensation arrangement for customers with a connection above 25A was introduced.

These customers were able to reduce their connection capacity for a fixed charge of €50 in 2009

or 2010.

2. If not possible to reduce the real connection capacity, a transitional measure enabled

consumers to get a single sum compensation for 2009 and 2010. The compensation was mainly

for larger connections with a low consumption e.g. buildings with elevators, churches, etc.

3. In 2013, distribution companies agreed to compensate customers who had not understood that

they were paying for an oversized connection, and reduced their contracted capacity for free.

This was mainly applicable to gas connections.

Overall, the impact of this new policy has been positive. It was transparent for consumers, reduced revenue uncertainty for DSOs and had no measurable negative-impact on energy efficiency (which has been feared as a side-effect), because there is still an incentive by the energy tax and supplier charge per kWh. The change to a new tariff scheme also led to a substantial reduction in administrative costs in the

energy sector, as it is easier for DSOs to bill suppliers: there are few categories of consumers and the

charges paid by all consumers fitting in one category is the same.

Key message

Grid users should receive clear and appropriate information before and after new

distribution network tariffs are implemented.

13

Volume 2.000 kWh

2008 2009

volume amount volume amount

Connection 32,64 euro 32,64 Connection 16,44 euro 16,44

Fixed part 18,00 euro 18,00 Fixed part 18,00 euro 18,00

Variable costs (kWh) 0,0336 €/kWh 2.000 67,20 Capacity charge (25A) 115,6000 euro 115,60

Tax reduction -199,00 euro -199,00 Tax reduction -318,62 euro -318,62

0-10.000 kWh 0,0752 €/kWh 150,40 0-10.000 kWh 0,1085 €/kWh 2.000 217,00

69,24 48,42

Volume 3.500 kWh

2008 2009

volume amount volume amount

Connection 16,32 euro 16,32 Connection 16,44 euro 16,44

Fixed part 18,00 euro 18,00 Fixed part 18,00 euro 18,00

Variable costs (kWh) 0,0336 €/kWh 3.500 117,60 Capacity charge (25A) 115,6000 euro 115,60

Tax reduction -199,00 euro -199,00 Tax reduction -318,62 euro -318,62

0-10.000 kWh 0,0752 €/kWh 3.500 263,20 0-10.000 kWh 0,1085 €/kWh 3.500 379,75

216,12 211,17

Volume 5.000 kWh

2008 2009

volume amount volume amount

Connection 16,32 euro 16,32 Connection 16,44 euro 16,44

Fixed part 18,00 euro 18,00 Fixed part 18,00 euro 18,00

Variable costs (kWh) 0,0336 €/kWh 5.000 168,00 Capacity charge (25A) 115,6000 euro 115,60

Tax reduction -199,00 euro -199,00 Tax reduction -318,62 euro -318,62

0-10.000 kWh 0,0752 €/kWh 5.000 376,00 0-10.000 kWh 0,1085 €/kWh 5.000 542,50

379,32 373,92

Dis

trib

utio

nS

upply

Dis

trib

utio

nS

upply

Dis

trib

utio

nS

upply

Dis

trib

utio

nS

upply

Dis

trib

utio

nS

upply

Dis

trib

utio

nS

upply

Tariff Tariff

Tariff Tariff

Tariff Tariff

Annex – Effect of the switch to capacity tariffs in the Netherlands in 2009

Effect of tariff change on typical household bills (source: Liander)

14

EDSO for Smart Grids is a European association gathering leading electricity distribution system operators (DSOs), cooperating to bring smart grids from vision to reality. www.edsoforsmartgrids.eu