44

European Gold Forum Matt Manson, President and CEO, April 17, 2018

European Gold ForumMatt Manson, President and CEO, April 17, 2018

Forward Looking Information

2

This presentation contains "forward-looking information" within the meaning of Canadian securities legislation. This information and these statements, referred to herein as “forward-looking statements”, are made as ofthe date of this presentation and the Corporation does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by law. Capitalized terms in these FLS nototherwise defined in this presentation have the meaning attributed thereto in the most recently filed AIF of the Corporation.

These forward-looking statements include, among others, statements with respect to Stornoway’s objectives for the ensuing year, our medium and long-term goals, and strategies to achieve those objectives and goals,as well as statements with respect to our beliefs, plans, objectives, expectations, anticipations, estimates and intentions. Although management considers these assumptions to be reasonable based on informationcurrently available to it, they may prove to be incorrect.

Forward-looking statements relate to future events or future performance and reflect current expectations or beliefs regarding future events and include, but are not limited to, statements with respect to: (i) the amountof Mineral Reserves, Mineral Resources and exploration targets; (ii) the amount of future production over any period; (iii) net present value and internal rates of return of the mining operation; (iv) assumptions relating torecovered grade, size distribution and quality of diamonds, average ore recovery, internal dilution, mining dilution and other mining parameters set out in the 2016 Technical Report as well as levels of diamond breakage;(v) assumptions relating to gross revenues, cost of sales, cash cost of production, gross margins estimates, planned and projected capital expenditure, liquidity and working capital requirements; (vi) mine expansionpotential and expected mine life; (vii) the expected time frames for the ramp-up and achievement of plant nameplate capacity of the Renard Diamond Mine (viii) the expected financial obligations or costs incurred byStornoway in connection with the ongoing development of the Renard Diamond Mine; (ix) future market prices for rough diamonds; (x) sources of and anticipated financing requirements; (xi) the effectiveness, funding oravailability, as the case may require, of the Senior Secured Loan and the remaining Equipment Facility and the use of proceeds therefrom; (xii) the Corporation’s ability to meet its Subject Diamonds Interest deliveryobligations under the Purchase and Sale Agreement; and (xiii) the foreign exchange rate between the US dollar and the Canadian dollar. Any statements that express or involve discussions with respect to predictions,expectations, beliefs, plans, projections, objectives, assumptions or future events or performance are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are made based upon certain assumptions by Stornoway or its consultants and other important factors that, if untrue, could cause the actual results, performances or achievements ofStornoway to be materially different from future results, performances or achievements expressed or implied by such statements. Such statements and information are based on numerous assumptions regarding presentand future business prospects and strategies and the environment in which Stornoway will operate in the future, including the recovered grade, size distribution and quality of diamonds, average ore recovery, internaldilution, and levels of diamond breakage, the price of diamonds, anticipated costs and Stornoway’s ability to achieve its goals, anticipated financial performance. Although management considers its assumptions on suchmatters to be reasonable based on information currently available to it, they may prove to be incorrect. Certain important assumptions by Stornoway or its consultants in making forward-looking statements include, butare not limited to: (i) required capital investment (ii) estimates of net present value and internal rates of return; (iii) recovered grade, size distribution and quality of diamonds, average ore recovery, internal dilution,mining dilution and other mining parameters set out in the 2016 Technical Report as well as levels of diamond breakage, (iv) anticipated timelines for ramp-up and achievement of nameplate capacity at the RenardDiamond Mine, (v) anticipated timelines for the development of an open pit and underground mine at the Renard Diamond Mine; (vi) anticipated geological formations; (vii) market prices for rough diamonds and theirpotential impact on the Renard Diamond Mine; and (viii) the satisfaction or waiver of all conditions under the Senior Secured Loan and the remaining Equipment Facility to allow the Corporation to draw on the fundingavailable under those financing elements.

Forward Looking Information (continued)

3

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that estimates, forecasts, projections and other forward-looking statements will not beachieved or that assumptions do not reflect future experience. We caution readers not to place undue reliance on these forward- looking statements as a number of important risk factors could cause the actual outcomesto differ materially from the beliefs, plans, objectives, expectations, anticipations, estimates, assumptions and intentions expressed in such forward-looking statements. These risk factors may be generally stated as therisk that the assumptions and estimates expressed above do not occur, including the assumption in many forward-looking statements that other forward-looking statements will be correct, but specifically include,without limitation: (i) risks relating to variations in the grade, size distribution and quality of diamonds, kimberlite lithologies and country rock content within the material identified as Mineral Resources from thatpredicted; (ii) variations in rates of recovery and diamond breakage; (iii) slower increases in diamond valuations than assumed; (iv) risks relating to fluctuations in the Canadian dollar and other currencies relative to theUS dollar; (v) increases in the costs of proposed capital, operating and sustainable capital expenditures; (vi) operational and infrastructure risks; (vii) execution risk relating to the development of an operating mine at theRenard Diamond Mine; (viii) failure to satisfy the conditions to the funding or availability, as the case may require, of the Senior Secured Loan and the Equipment Facility; ( ix) developments in world diamond markets; and(x) all other risks described in Stornoway’s most recently filed AIF and its other disclosure documents available under the Corporation’s profile at www.sedar.com. Stornoway cautions that the foregoing list of factors thatmay affect future results is not exhaustive and new, unforeseeable factors and risks may arise from time to time.

Qualified Persons

The Qualified Persons that prepared the technical reports and press releases that form the basis for the presentation are listed in the Company’s AIF dated February 23, 2017. Disclosure of a scientific or technical naturein this presentation was prepared under the supervision of M. Patrick Godin, P.Eng. (Québec), Chief Operating Officer. Stornoway’s exploration programs are supervised by Robin Hopkins, P.Geol. (NT/NU), Vice President,Exploration. Each of M. Godin and Mr. Hopkins are “qualified persons” under NI 43-101.

Non-IFRS Financial Measures

This presentation refers to certain financial measures, such Adjusted EBITDA, Adjusted EBITDA margin, Average diamond price achieved, Cash Operating Cost per Tonne of Ore Processed, Cash Operating Cost per CaratRecovered, Capital Expenditures and Available Liquidity, which are not measures recognized under IFRS and do not have a standardized meaning prescribed by IFRS.

“Adjusted EBITDA” and “Adjusted EBITDA Margin” are used by management and investors to assess and measure the underlying pre-tax operating performance of the Corporation and are generally regarded by management as better measures to evaluate performance trends. “Adjusted EBITDA” is defined as net income (loss) before depreciation, interest and other financial (income) expenses, and income tax, adjusted for impairment charges, unrealized gains and losses related to the changes in fair value of U.S. Denominated debt and other non-recurring or unusual items that are not reflective of the Corporation’s underlying operating performance and/or unlikely to occur on a regular basis. “Adjusted EBITDA Margin” is the calculation of Adjusted EBITDA divided by total revenues. “Average diamond price achieved” is a measure used by the Corporation to measure the value of diamonds sold into the market in the period, prior to adjustments to reflect the impact of the stream. This measure is used by management and investors as it reflects the average diamond price achieved during the period and is more comparable to the average diamond price achieved by to other diamond producers. Average diamond price achieved is calculated based on reported revenues adjusted for the amortization of deferred stream revenue, and remittances made to/from stream participants and gains or losses from revenue hedging activities divided by the number of carats sold in the period. “Cash Operating Cost per Tonne Processed” and “Cash Operating Cost per Carat Recovered” are used by management and investors to measure the mine’s cash operating cost based on per tonne of ore processed or per carat recovered. Cash Operating Cost Per Tonne Processed is calculated based on reported operating expenses adjusted for the impact of inventory variation, excluding depreciation, divided by tonnes of ore processed for the period. Cash Operating Cost per Carat Recovered is the total cash operating cost divided by carats recovered. “Capital Expenditure” is the term used by the Corporation and investors to describe capital expenditures incurred during the period. This measure is used by management and investors to measure the amount of capital spent by the corporation on sustaining, margin improvement, and/or growth capital projects in the period. “Available Liquidity” comprises cash and cash equivalents, short-term investments and available credit facilities (less related upfront fees) and is used by the management and investors to measure the amount of cash resources available to the Corporation, over and above the cash generated from operations, to support the operating and capital requirements of the business.

100% Owned Renard Diamond Mine – Québec, CanadaThe Canadian Diamond Mine Connected by Permanent Road Access

4

EKATISNAP LAKE

DIAVIKGAHCHO KUE

VICTOR

MONTREAL (800km)

TEMISCAMIE (240 km)MISTISSINI (360 km)

CHIBOUGAMAU (420 km)

Route 167 ExtensionRenard Mine Road

RENARD

Quebec’s first Diamond Mine; Canada’s sixthFinanced 2014; First processing July 2016; commercial production Jan 1, 2017; construction completed 5 months ahead of schedule & C$37M below budget1

Production Ramp Up and First Operating Year CompletedFY2017 Production targets in line with guidance; lower pricing at sale than expected and processing upgrade underway

Low Cost, Long Mine Life Asset with UpsideLowest cost diamond producer in Canada; Life of Mine Plan to FY2030; Upside on mine life, processing capacity and pricing

Strong Social License and Institutional SupportPartnered with the Crees of Eeyou Istchee; Investissement Québec, CDPQ (la Caisse), Orion and Osisko as investors, lenders and/or streamers

Strong Balance SheetAs of December 31, 2017, cash, cash equivalents and short term investments of $81.0 million. Debt of $308.1 million. Available liquidity2 of $101.8 million.

1. C$771.2 million to December 31, 2016 and $2.8 million of costs deferred to 2017 compared to a starting budget of C$811M (July 2014)2. See Note on “Non-IFRS Financial Measures”; includes cash, cash equivalents and available credit facilities

Renard Mine Site

5

Crusher

R2 & R3 Pit

Ore Stockpiles

R65 Pit Power Plant

Process Plant

Maintenance Shop

Admin/DryAccommodation

December 2017

UG Mine Development, October 2017

R2-R3 Pit, June 2017

UG Mine Portal

PKC Facility

Ore-Waste Sorting

Mine PlanBusiness Case, Including 13Mcarat Inferred Mineral Resources, March 30, 2016

Combined open pit and underground mining

2015-2018 Open pit R2, R3

2014-2029 Open pit R65

2018-2035 Underground R2, blasthole shrink stoppage with panel retreat

2029-2035 Underground R3, R4 (longhole stopingand blasthole stoppage respectively)

All pipes open at depth.

6

7

9

10

11

R3 OPEN PITR2 OPEN PITR65 OPEN PIT

RETURN AIR RAISE FRESH AIR

RAISE

PORTAL

BACKFILL RAISES IN CROWN PILLAR

410L

270L

710L

590L

470L

290L

400L

250L

860L

VENTILATION RAISE

MAIN RAMP

5

1

4

2

3

86

Reserve and Resource categories are compliant withthe "CIM Definition Standards on Mineral Resourcesand Reserves". Mineral resources that are not mineralreserves do not have demonstrated economicviability. The potential quantity and grade of anyExploration Target (previously referred to as a“Potential Mineral Deposit”) is conceptual in nature,and it is uncertain if further exploration will result inthe target being delineated as a mineral resource.

RENARD 65

RENARD 4

RENARD 9

RENARD 2

RENARD 3

2017 Operating and Financial ResultsAs of December 31, 2017

7

FY2017 Mining, Processing and Sales ResultsAt December 31, 2017. All quoted figures in CAD$ unless noted

8

419512 506 519

385 417 442398

9282 87

77

0

200

400

600

800

1,000

Q1 Q2 Q3 Q4

Tho

usa

nd

s To

nn

es/

cara

ts

Tonnes

Carats

Grade (cpht)

Mining

Processing

626500 523

442

1,2451,329

1,074

827

0

200

400

600

800

1,000

1,200

1,400

Q1 Q2 Q3 Q4

Tho

usa

nd

s To

nn

es

OP Ore

OP Total (Ore& Waste)

459

350406

487

0

100

200

300

400

500

600

Q1 Q2 Q3 Q4

Tho

usa

nd

s C

arat

s

Carats

$44.5 $40.9$48.1 $52.6

$73

$87$94

$86

$97

$117 $118$108

$0

$20

$40

$60

$80

$100

$120

$0

$20

$40

$60

$80

$100

$120

$140

Q1 Q2 Q3 Q4

Mill

ion

s d

olla

rs

Pri

ce p

er

Car

at

GrossProceeds

US$/ct

$/ct

Carat Sales1

Gross Proceeds2,3 and Pricing

1. Q1 carat sales include 52,681 carats of smaller and lower quality goods carried over from Stornoway’s first sale in November 2016. Q4 carat sales include 32,989 carats that were sold in the third quarter for which revenue was realized in the fourth quarter.

2. See note on “Non-IFRS Financial Measures”3. Before Stream and royalty

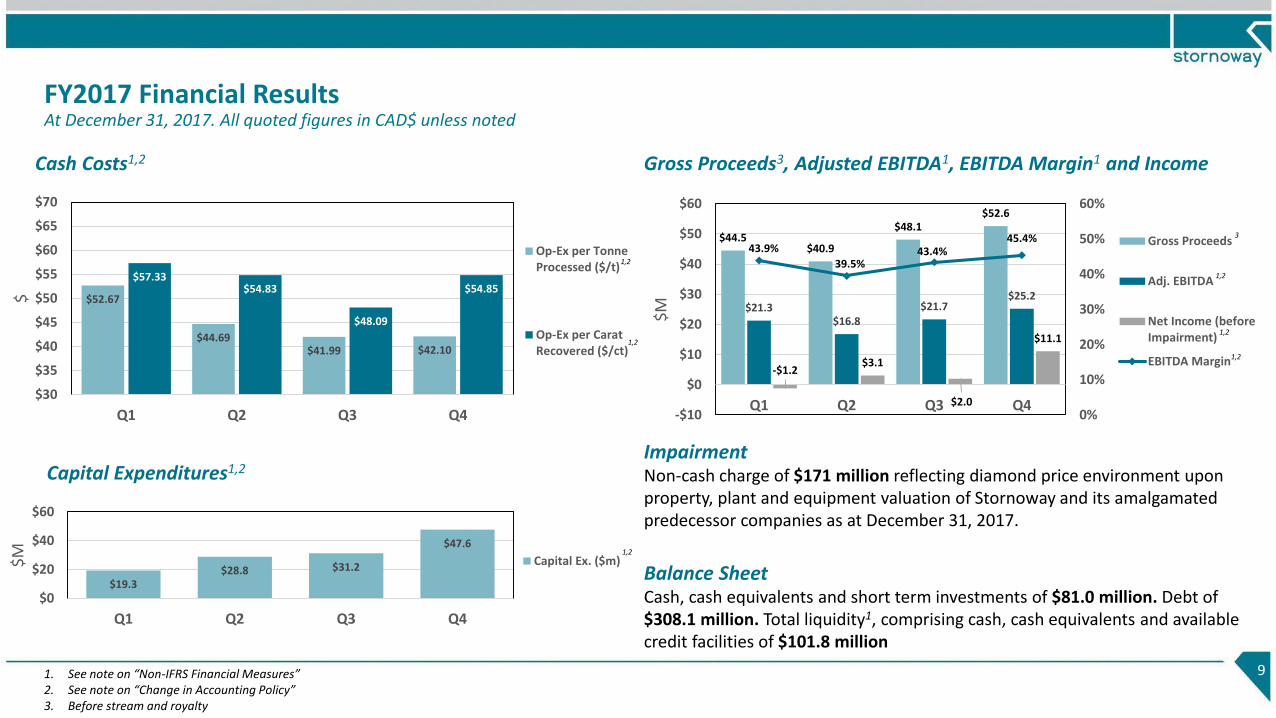

FY2017 Financial ResultsAt December 31, 2017. All quoted figures in CAD$ unless noted

Gross Proceeds3, Adjusted EBITDA1, EBITDA Margin1 and Income

9

$44.5$40.9

$48.1$52.6

$21.3$16.8

$21.7$25.2

-$1.2$3.1

$2.0

$11.1

43.9%

39.5%43.4%

45.4%

0%

10%

20%

30%

40%

50%

60%

-$10

$0

$10

$20

$30

$40

$50

$60

Q1 Q2 Q3 Q4

$M

Gross Proceeds

Adj. EBITDA

Net Income (beforeImpairment)

EBITDA Margin

Cash Costs1,2

$52.67

$44.69$41.99 $42.10

$57.33$54.83

$48.09

$54.85

$30

$35

$40

$45

$50

$55

$60

$65

$70

Q1 Q2 Q3 Q4

$

Op-Ex per TonneProcessed ($/t)

Op-Ex per CaratRecovered ($/ct)

$19.3$28.8 $31.2

$47.6

$0

$20

$40

$60

Q1 Q2 Q3 Q4

$M

Capital Ex. ($m)

Capital Expenditures1,2ImpairmentNon-cash charge of $171 million reflecting diamond price environment upon property, plant and equipment valuation of Stornoway and its amalgamated predecessor companies as at December 31, 2017.

Balance SheetCash, cash equivalents and short term investments of $81.0 million. Debt of$308.1 million. Total liquidity1, comprising cash, cash equivalents and available credit facilities of $101.8 million

1. See note on “Non-IFRS Financial Measures”2. See note on “Change in Accounting Policy”3. Before stream and royalty

1,2

1,2

1,2

1,2

1,2

1,2

3

2017 Full Year Results Compared to FY2017 GuidanceAt December 31, 2017. All quoted figures in CAD$ unless noted

10

FY2017 Guidance

FY2017 Result

Open Pit Tonnes Mined 4.4m 4.48m

Underground Tonnes Mined 0.5m 0.45m

Tonnes Processed 2.0m 1.96m

Carats Recovered 1.7m 1.64m

Grade (cpht) 85 84

Carats Sold 1.8m 1.70m

Price (US$/ct) $100 to $132 $85

Gross Proceeds1,2 (US$) $180 to $230 $145m

Cash Operating Cost per Tonne Processed1,3 ($/t) $60 $45.02

Cash Operating Cost per Carat Processed1,3 ($/ct) $70 $53.60

Capital Expenditures1,3,4 $78.7m $126.9m

1. See note on “Non-IFRS Financial Measures”2. Before stream and royalty

3. See note on “Change in Accounting Policy”. Under the changed accounting policy, cash operating costs are lower and capital expenditures are higher than was contemplated in the 2017 guidance.

4. Excluding $22m of extraordinary capital approved by the Board of Directors in August 2017 for ore waste sorting.

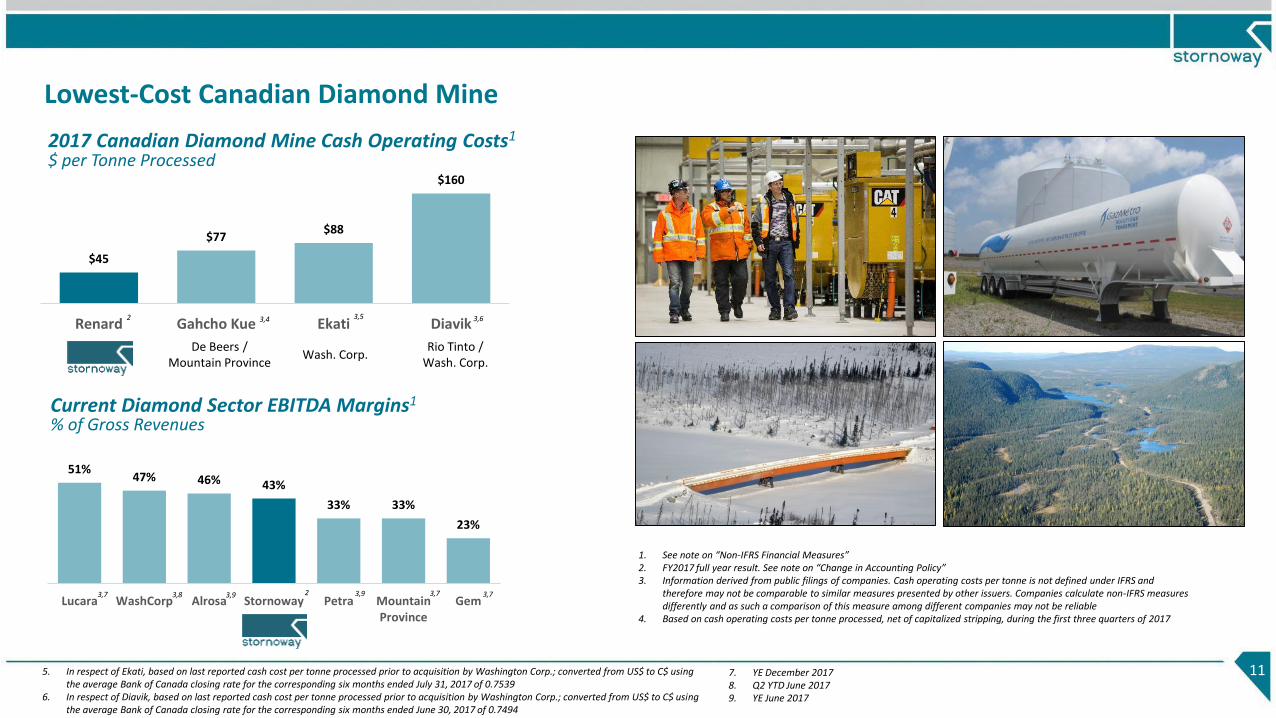

51%47% 46% 43%

33% 33%

23%

Lucara WashCorp Alrosa Stornoway Petra MountainProvince

Gem

Lowest-Cost Canadian Diamond Mine

11

1. See note on “Non-IFRS Financial Measures”2. FY2017 full year result. See note on “Change in Accounting Policy”3. Information derived from public filings of companies. Cash operating costs per tonne is not defined under IFRS and

therefore may not be comparable to similar measures presented by other issuers. Companies calculate non-IFRS measures differently and as such a comparison of this measure among different companies may not be reliable

4. Based on cash operating costs per tonne processed, net of capitalized stripping, during the first three quarters of 2017

7. YE December 20178. Q2 YTD June 20179. YE June 2017

Current Diamond Sector EBITDA Margins1

% of Gross Revenues

$45

$77$88

$160

Renard Gahcho Kue Ekati Diavik

De Beers / Mountain Province

Wash. Corp.Rio Tinto /

Wash. Corp.

2017 Canadian Diamond Mine Cash Operating Costs1

$ per Tonne Processed

3,42 3,5 3,6

3,73,7 3,9 2 3,9 3,7

5. In respect of Ekati, based on last reported cash cost per tonne processed prior to acquisition by Washington Corp.; converted from US$ to C$ using the average Bank of Canada closing rate for the corresponding six months ended July 31, 2017 of 0.7539

6. In respect of Diavik, based on last reported cash cost per tonne processed prior to acquisition by Washington Corp.; converted from US$ to C$ using the average Bank of Canada closing rate for the corresponding six months ended June 30, 2017 of 0.7494

3,8

Renard Project Resource Reconciliation

12

Actual Plan % Variance

Ore Tonnes Processed 2.35m 2.22m +6%

Carats Recovered 2.09m 1.91m +9%

Grade (cpht) 89 86 +3%

Monthly Carats Recovered

--

50

100

150

200

250

Tho

usa

nd

Car

ats

R65 Ore

R3 Carats

R2 Carats

Commercial Production Declared

Monthly Ore Milled

--

50

100

150

200

250

Tho

usa

nd

To

nn

es

R65 Ore

R3 Ore

R2 Ore

NameplateThroughput(tpd)

Commercial Production Declared

Renard Project Operating KPIsProject to Date as at December 31, 2017

Q1 2018 Operating ResultsAs of March 31, 2018

13

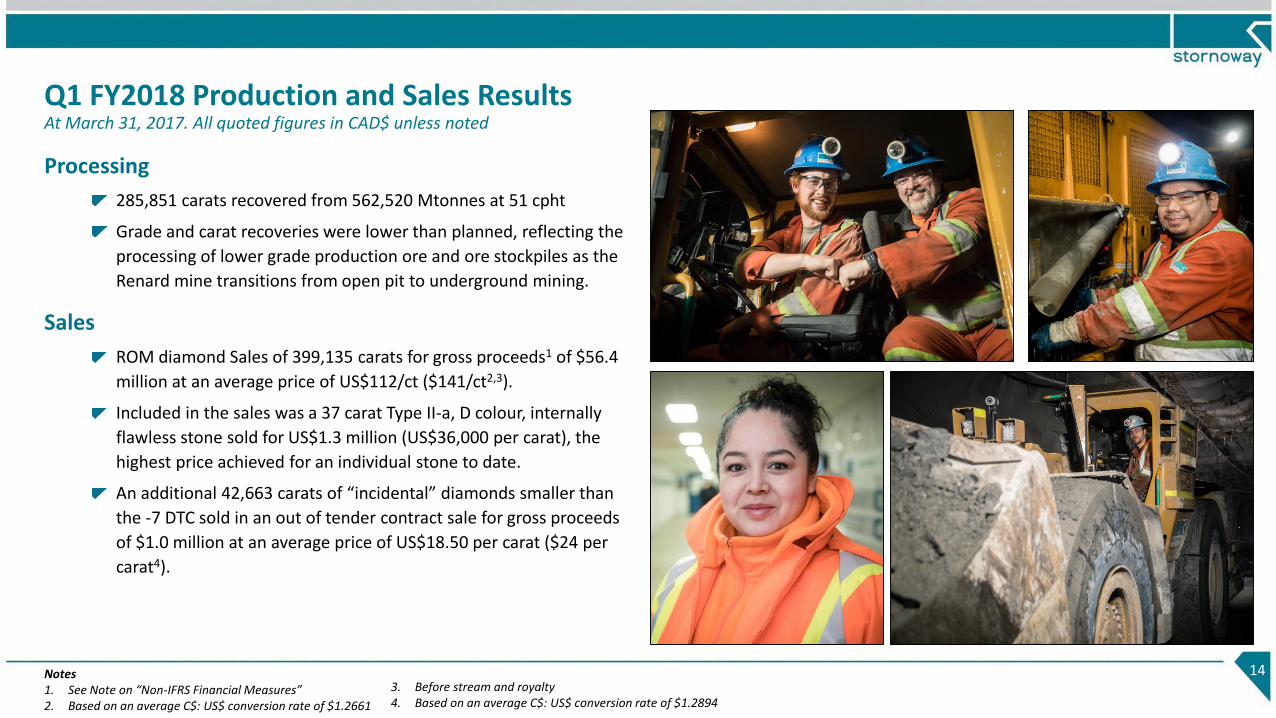

Q1 FY2018 Production and Sales ResultsAt March 31, 2017. All quoted figures in CAD$ unless noted

Processing

285,851 carats recovered from 562,520 Mtonnes at 51 cpht

Grade and carat recoveries were lower than planned, reflecting the

processing of lower grade production ore and ore stockpiles as the

Renard mine transitions from open pit to underground mining.

Sales

ROM diamond Sales of 399,135 carats for gross proceeds1 of $56.4

million at an average price of US$112/ct ($141/ct2,3).

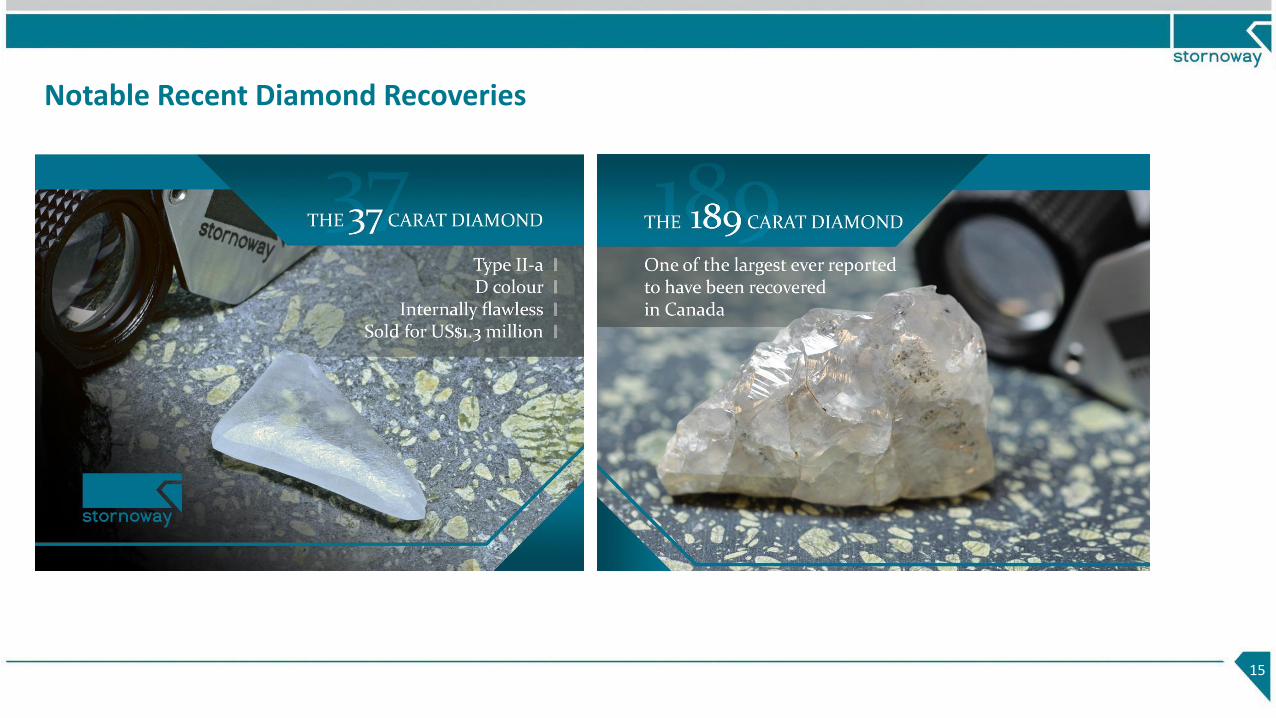

Included in the sales was a 37 carat Type II-a, D colour, internally

flawless stone sold for US$1.3 million (US$36,000 per carat), the

highest price achieved for an individual stone to date.

An additional 42,663 carats of “incidental” diamonds smaller than

the -7 DTC sold in an out of tender contract sale for gross proceeds

of $1.0 million at an average price of US$18.50 per carat ($24 per

carat4).

14Notes1. See Note on “Non-IFRS Financial Measures”2. Based on an average C$: US$ conversion rate of $1.2661

3. Before stream and royalty4. Based on an average C$: US$ conversion rate of $1.2894

Notable Recent Diamond Recoveries

15

Note on Diamond Sales

16

Renard Diamond Price Movements, Real Terms1

1. Sale by sale basis, normalized for variations in quality and size distribution2. Before stream and royalty

November 2016, Base = 100

March 2018 = 120

Pricing achieved at sale is highly dependent on product mix and the prevailing rough diamond market

First sale in November 2016 resulted in positive customer experience and word of mouth. Attendance at tenders has steadily increased through 2017 and into 2018.

In real terms, pricing for Renard diamonds has increased +20% between the first sale in November 2016 and March 20181

Bidding Statistics

14.2 13.5 12.1

13.6 14.5 12.8 11.7 11.5 12.7 13.3

18.5 15.3 16.1

153

124 119 133 127

151 142

150 151 163

190 173

196

90 83 81 96 103 107

97 105 110 109

132 119

137

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

-

50

100

150

200

250

Bids per Parcel Attendees Bidders

FY2017 Q1 2018 Sales

Number of Sales 9 3

Carats Sold 1,701,561 399,135

Gross Proceeds (C$M)2 186.2 56.4

Average Price per Carat (US$/ct) 85 112

Average Price per Carat (C$/ct) 109 141

Average Exchange Rate (C$:US$) 1.2916 1.27

100

112110

114115

119 119

110 111114

120 119 120

90

100

110

120

130

Ind

ex

(No

v 2

01

6=1

00

)

OutlookAs of December 31, 2017

17

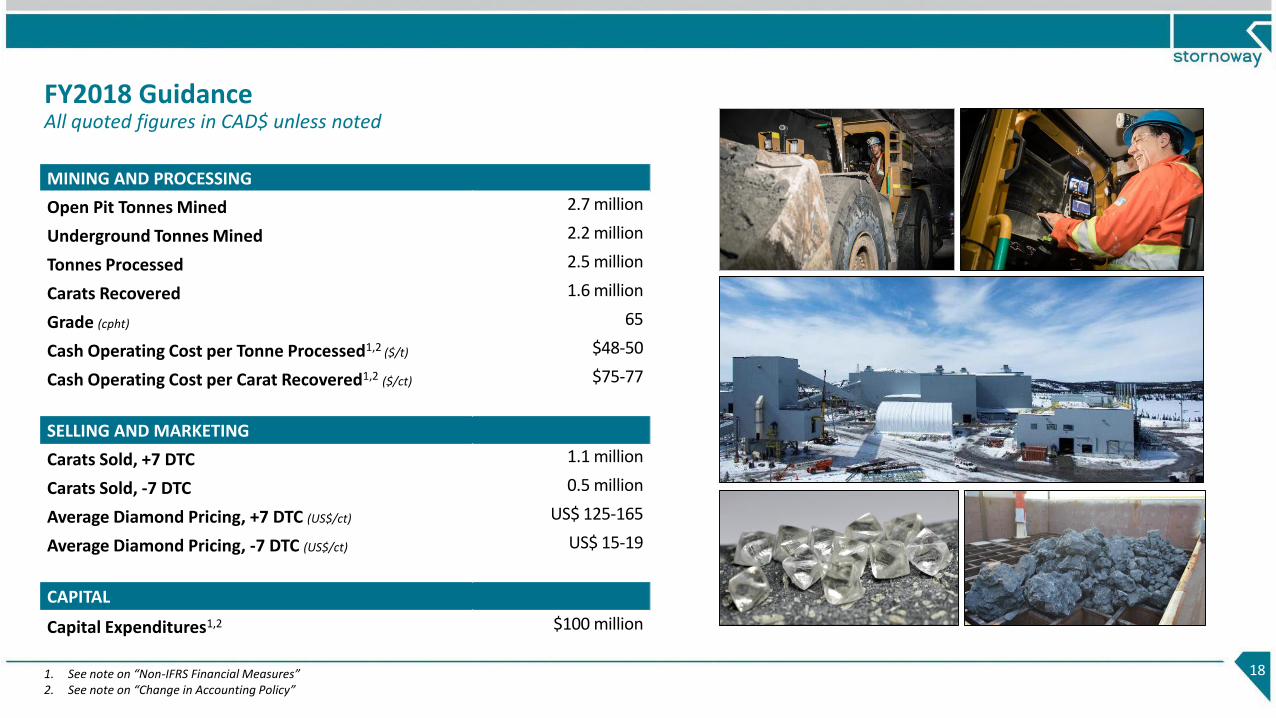

FY2018 GuidanceAll quoted figures in CAD$ unless noted

18

MINING AND PROCESSING

Open Pit Tonnes Mined 2.7 million

Underground Tonnes Mined 2.2 million

Tonnes Processed 2.5 million

Carats Recovered 1.6 million

Grade (cpht) 65

Cash Operating Cost per Tonne Processed1,2 ($/t) $48-50

Cash Operating Cost per Carat Recovered1,2 ($/ct) $75-77

SELLING AND MARKETING

Carats Sold, +7 DTC 1.1 million

Carats Sold, -7 DTC 0.5 million

Average Diamond Pricing, +7 DTC (US$/ct) US$ 125-165

Average Diamond Pricing, -7 DTC (US$/ct) US$ 15-19

CAPITAL

Capital Expenditures1,2 $100 million

1. See note on “Non-IFRS Financial Measures”2. See note on “Change in Accounting Policy”

Mining: Transitioning to Underground

19

In the first half of 2018 principal production will transition from the Renard 2-Renard 3 open pit to the underground mine.

Development of the underground mine is progressing on schedule with first ore production in Renard 2 at the 290m level.

At year end, 4,869m of lateral development had been completed compared to a plan of 4,460m, the fresh air raise had been completed, 26 out of 32 FY2018 production draw points had been excavated, and a production drilling inventory of 436,424 tonnes of drilled ore had been established.

The first production blast occurred successfully on December 20th, 2017.

Processing of underground production ore commenced in the first quarter of 2018, with full production scheduled for the second quarter.

In 2018, 5,000 meters of underground delineation drilling is planned to test the depth potential of the high grade Renard 3 kimberlite with a view to the acceleration of its inclusion in the Renard underground mine plan.

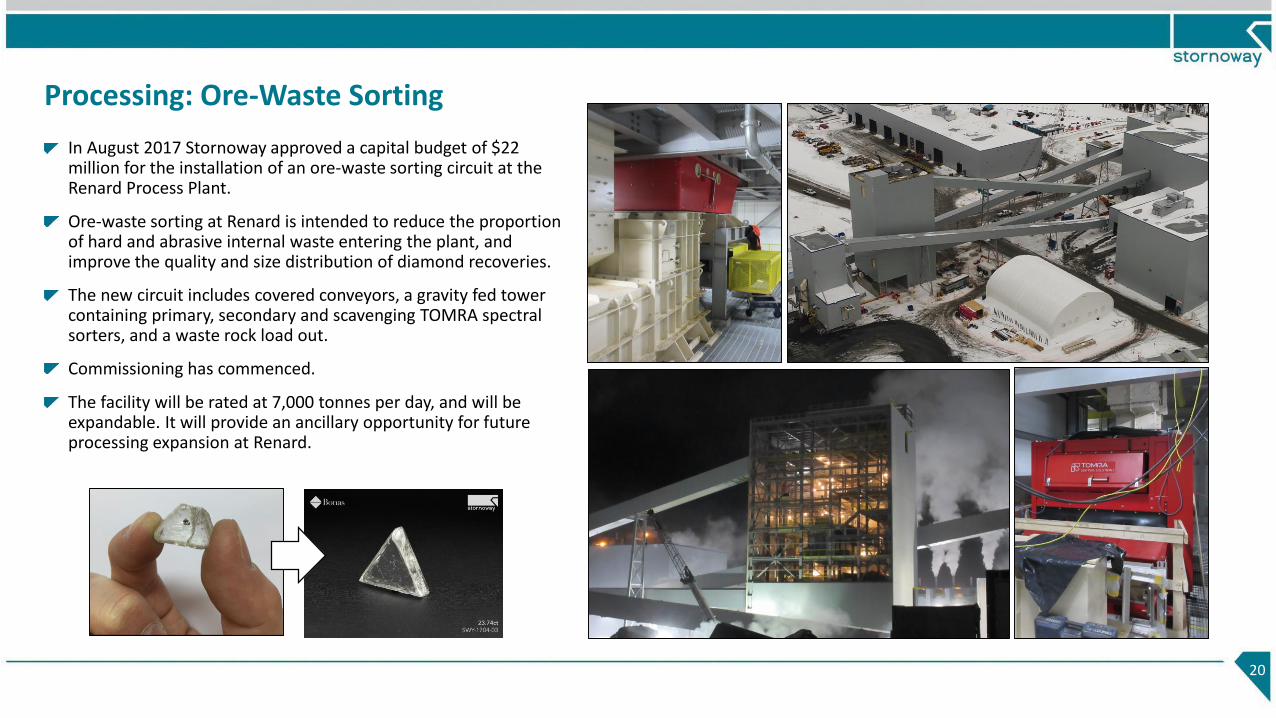

Processing: Ore-Waste Sorting

20

In August 2017 Stornoway approved a capital budget of $22 million for the installation of an ore-waste sorting circuit at the Renard Process Plant.

Ore-waste sorting at Renard is intended to reduce the proportion of hard and abrasive internal waste entering the plant, and improve the quality and size distribution of diamond recoveries.

The new circuit includes covered conveyors, a gravity fed tower containing primary, secondary and scavenging TOMRA spectral sorters, and a waste rock load out.

Commissioning has commenced.

The facility will be rated at 7,000 tonnes per day, and will be expandable. It will provide an ancillary opportunity for future processing expansion at Renard.

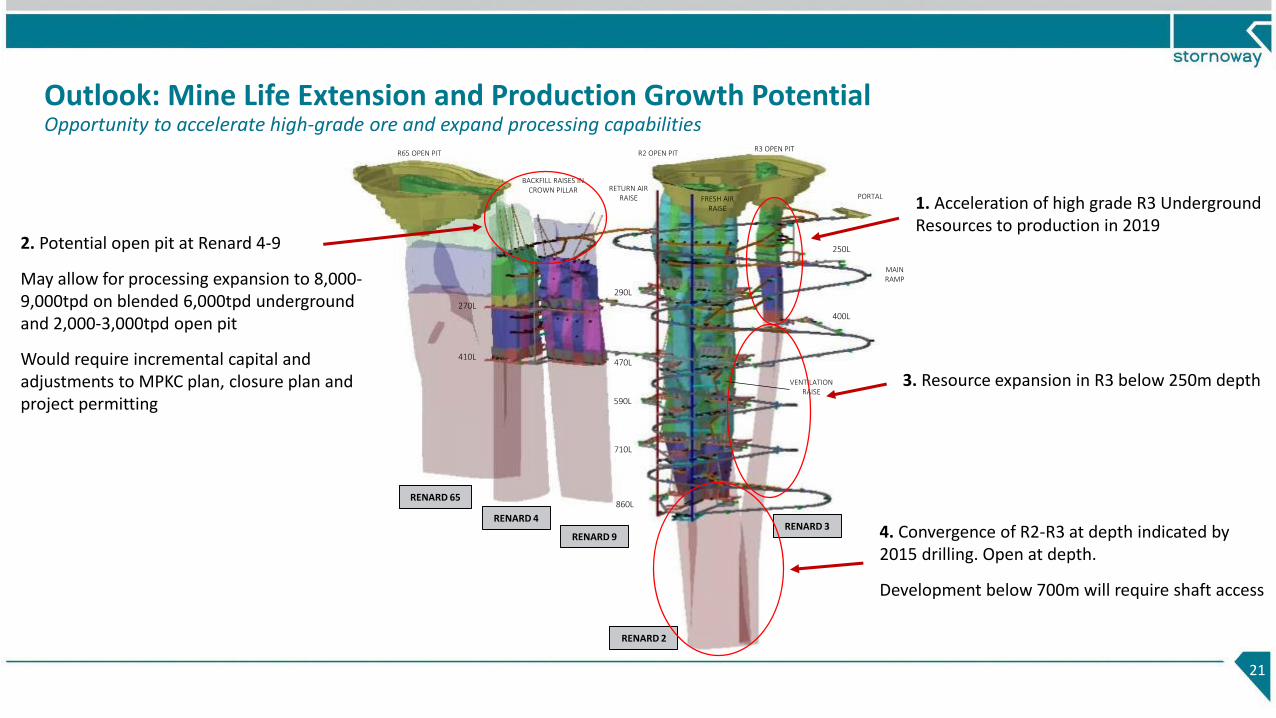

Outlook: Mine Life Extension and Production Growth Potential Opportunity to accelerate high-grade ore and expand processing capabilities

21

R3 OPEN PITR2 OPEN PITR65 OPEN PIT

RETURN AIR RAISE FRESH AIR

RAISE

PORTAL

BACKFILL RAISES IN CROWN PILLAR

410L

270L

710L

590L

470L

290L

400L

250L

860L

VENTILATION RAISE

MAIN RAMP

RENARD 65

RENARD 4

RENARD 9

RENARD 2

RENARD 3

1. Acceleration of high grade R3 Underground Resources to production in 2019

3. Resource expansion in R3 below 250m depth

2. Potential open pit at Renard 4-9

May allow for processing expansion to 8,000-9,000tpd on blended 6,000tpd underground and 2,000-3,000tpd open pit

Would require incremental capital and adjustments to MPKC plan, closure plan and project permitting

4. Convergence of R2-R3 at depth indicated by 2015 drilling. Open at depth.

Development below 700m will require shaft access

2018 Exploration: Renard “100 Target” Brownfield Exploration Program$3m Budget Approved for 2018

100 Target 2018 drill program using light RC rigs

Based on geophysical and geochemical compilation and untested anomalies

Approach last used successfully at Adamantin Project, 100km south of Renard

Only c.40 targets at Renardtested before exploration ended in 2007/08

Delineation drilling and microdiamond assessment will follow upon any discovery made.

Additional Canadian greenfieldsdiamond exploration, including drilling, is planned for 2018

22

Renard pipesHibou dyke

Priority 1 (red) and 2 (orange) Targets anomalies

Route 167

property outline

Undrilled EM anomalies (examples)

Renard pipes

The Future: Diamond Mine Depletion, 2018-2025

The largest individual diamond mine (Argyle) and the two largest Canadian mines are expected to be depleted starting in 2020

23

Forecasted Rough-Diamond Production of Depleting Mines, Mcts, Optimistic Scenario

Argyle Mine, Australia

Source: Bain & Company “The Global Diamond Industry 2017: The Enduring Story in a Changing World”; Company Reports

Victor De Beers

Komsomolskaya ALROSA

Argyle Rio Tinto

Voorspoed De Beers

Koffiefontein Petra

Diavik Rio Tinto / Washington Corp

Sable, Pigeon, Lynx,Misery Main, Koala (Ekati)

Washington Corp

30

25

20

15

0

35

2016 2017F 2018F 2019F 2020F 2021F

10

5

2022F 2023F 2024F 2025F

Diavik Mine, Canada

Capital Structure & Balance Sheet

24

Balance Sheetnote 2

Cash and Equivalents C$81 million

Total Debt C$308.1 million

Available Liquiditynote 3 C$101.8 million

Project Finance SponsorsInvestissement Québec, Orion Mine Finance, CDPQ,

Blackstone Tactical Opportunities

1. As of April 12, 2018.2. As of December 31, 2017, audited.3. Cash, cash equivalents, and available credit facilities. See “Non-IFRS Financial Measures”.

Capital Structure

Recent Share Price (TSX)note 1 C$0.57

52 week range C$0.50 – $0.86

Market Capitalizationnote 1 C$484 million

Shares Outstanding 835.3 million

Warrants 14.0 million

Employee Options 39.7 million

49.5%39.6%

10.9%

Project FinanceSponsors

Institutional Retail and Insiders

Share Ownershipnote 4

Institutional Shareholders

4. Fully Diluted

25

Head Office:

1111 Rue St. Charles Ouest,

Longueuil, Québec J4K 4G4

Tel: +1 (450) 616-5555

IR Contact:

Orin Baranowsky, Chief Financial Officer

Tel: +1 (416) 304-1026 x2103

www.stornowaydiamonds.com

Stornoway Diamond Corporation TSX:SWY, TSX:SWY.DB.U

Appendix

26

Mine PlanBusiness Case, Including 13Mcarat Inferred Mineral Resources, March 30, 2016

Extension of UG at Renard 2 to 860L (stope 5)

Deferral of UG at Renard 3 (stope 6) and its extension to 400L (stope 7)

Deferral of UG at Renard 4 (stope 8) and its extension to 410L (stope 9)

New UG at Renard 9 to 410L (stopes 10 and 11)

Does not include non-resource exploration upside. All pipes open at depth.

Does not include mining of Inferred Mineral Resources at Renard 65 below open pit pending confirmation of Renard 65 ROM $/carat.

27

7

9

10

11

R3 OPEN PITR2 OPEN PITR65 OPEN PIT

RETURN AIR RAISE FRESH AIR

RAISE

PORTAL

BACKFILL RAISES IN CROWN PILLAR

410L

270L

710L

590L

470L

290L

400L

250L

860L

VENTILATION RAISE

MAIN RAMP

5

1

4

2

3

86

Reserve and Resource categories are compliant withthe "CIM Definition Standards on Mineral Resourcesand Reserves". Mineral resources that are not mineralreserves do not have demonstrated economicviability. The potential quantity and grade of anyExploration Target (previously referred to as a“Potential Mineral Deposit”) is conceptual in nature,and it is uncertain if further exploration will result inthe target being delineated as a mineral resource.

RENARD 65

RENARD 4

RENARD 9

RENARD 2

RENARD 3

RENARD 65

RENARD 4

RENARD 9

RENARD 2

RENARD 3

RETURN AIR RAISE FRESH AIR

RAISE

PORTAL

BACKFILL RAISES IN CROWN PILLAR

410L

270L

710L

590L

470L

290L

400L

250L

860L

VENTILATION RAISE

MAIN RAMP

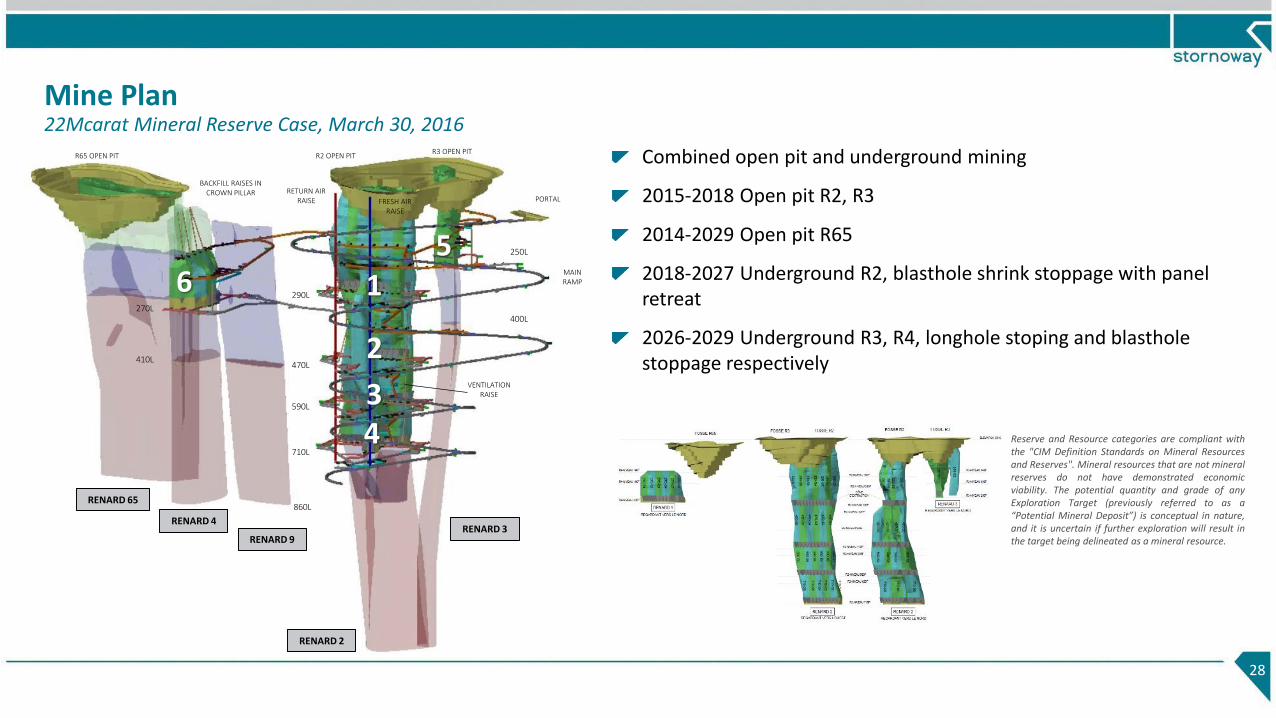

Mine Plan22Mcarat Mineral Reserve Case, March 30, 2016

Combined open pit and underground mining

2015-2018 Open pit R2, R3

2014-2029 Open pit R65

2018-2027 Underground R2, blasthole shrink stoppage with panel retreat

2026-2029 Underground R3, R4, longhole stoping and blastholestoppage respectively

28

1

4

2

3

65

R3 OPEN PITR2 OPEN PITR65 OPEN PIT

Reserve and Resource categories are compliant withthe "CIM Definition Standards on Mineral Resourcesand Reserves". Mineral resources that are not mineralreserves do not have demonstrated economicviability. The potential quantity and grade of anyExploration Target (previously referred to as a“Potential Mineral Deposit”) is conceptual in nature,and it is uncertain if further exploration will result inthe target being delineated as a mineral resource.

Mineral ReservesEffective December 31, 2017

29

Notes1 Reserve categories follow the CIM Standardsfor Mineral Resources and Mineral Reserves.2 Totals may not add due to rounding.3 Represents mine and stockpiled ore as ofDecember 31, 20164 Carats per hundred tonnes. Estimated at a +1DTC sieve size cut-off.5 Changes from December 31, 2016 MineralReserve estimate shown in italics

PROVEN MINERAL RESERVES(1,2) Stockpile(3) Carats (millions) Tonnes (millions) Grade (cpht)(4)

Renard 2, All Units 0.45 1.74 26Renard 3 0.08 0.11 72Renard 65 0.07 0.21 35

Total Stockpile Proven Mineral Reserves 0.60 2.07 29

PROBABLE MINERAL RESERVES(1,2) Open Pit Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 0.08 0.12 67Renard 3 0.24 0.22 109Renard 65 1.35 4.50 30

Total OP Probable Mineral Reserves 1.67 4.85 34

PROBABLE MINERAL RESERVES(1,2) Underground Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 15.29 18.66 82Renard 3 0.78 1.15 68Renard 4 1.67 3.46 48

Total UG Probable Mineral Reserves 17.74 23.26 76

Total Proven and Probable Mineral Reserves(5) 20.01 (-1.94) 30.17 (-2.83) 66 (-1)

Mineral ResourcesEffective December 31, 2017, Exclusive of the Mineral Reserves

30

INDICATED MINERAL RESOURCES(1,2) Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2 -- -- --Renard 3 -- -- --Renard 4 1.99 2.93 68Renard 65 0.83 3.16 26

Total Indicated Mineral Resources 2.81 6.09 46

INFERRED MINERAL RESOURCES(1,2) Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 3.67 5.55 66Renard 2, w/o CRB 3.36 4.08 82CRB 0.31 1.47 21

Renard 3 0.61 0.54 112Renard 4 2.46 4.75 52Renard 65 1.18 4.93 24Renard 9 3.04 5.70 53Lynx 1.92 1.80 107Hibou 0.26 0.18 144

Total Inferred Mineral Resources 13.13 23.45 56

Notes1 Resource categories were completed in accordance with the "CIMDefinition Standards on Mineral Resources and Reserves". Mineralresources that are not mineral reserves do not have demonstratedeconomic viability.2 Totals may not add due to rounding.3 Carats per hundred tonnes. Estimated at a +1 DTC sieve size cut-off.

Inferred Mineral Resources

Indicated Mineral Resources and/or Reserves

High Range TFFE

Renard 65775m depth

Renard 4775m depth Renard 9

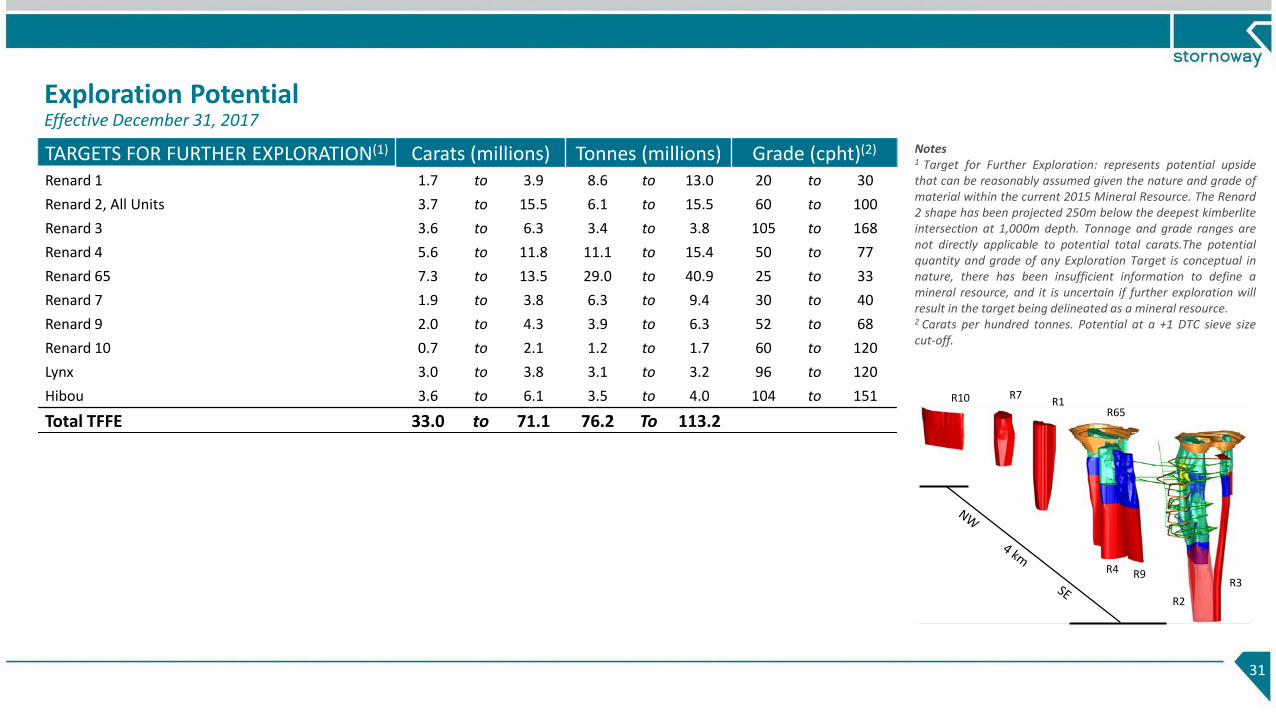

775m depth

Renard 21,250m depth

Renard 31,250m depth

North East View

Notes1 Target for Further Exploration: represents potential upsidethat can be reasonably assumed given the nature and grade ofmaterial within the current 2015 Mineral Resource. The Renard2 shape has been projected 250m below the deepest kimberliteintersection at 1,000m depth. Tonnage and grade ranges arenot directly applicable to potential total carats.The potentialquantity and grade of any Exploration Target is conceptual innature, there has been insufficient information to define amineral resource, and it is uncertain if further exploration willresult in the target being delineated as a mineral resource.2 Carats per hundred tonnes. Potential at a +1 DTC sieve sizecut-off.

Exploration PotentialEffective December 31, 2017

31

TARGETS FOR FURTHER EXPLORATION(1) Carats (millions) Tonnes (millions) Grade (cpht)(2)

Renard 1 1.7 to 3.9 8.6 to 13.0 20 to 30

Renard 2, All Units 3.7 to 15.5 6.1 to 15.5 60 to 100

Renard 3 3.6 to 6.3 3.4 to 3.8 105 to 168

Renard 4 5.6 to 11.8 11.1 to 15.4 50 to 77

Renard 65 7.3 to 13.5 29.0 to 40.9 25 to 33

Renard 7 1.9 to 3.8 6.3 to 9.4 30 to 40

Renard 9 2.0 to 4.3 3.9 to 6.3 52 to 68

Renard 10 0.7 to 2.1 1.2 to 1.7 60 to 120

Lynx 3.0 to 3.8 3.1 to 3.2 96 to 120

Hibou 3.6 to 6.1 3.5 to 4.0 104 to 151

Total TFFE 33.0 to 71.1 76.2 To 113.2

R10 R7R1

R65

R4 R9

R2

R3

Resource ReconciliationFour Measurements in a Diamond Project

1. Reconcile actual pipe geology with geological model (example from Renard 2 & 3 on 480m level shown opposite)

2. Reconcile size distribution; understand plant recovery characteristics

3. Reconcile grade

4. Reconcile quality assortment and value

Note on Reporting: Stornoway will report production and sales data on a quarterly basis. Resource reconciliation will be measured on a 12-month rolling average.

32

Renard 2

Renard 3

Since ore processing at Renard began, diamond production has been influenced by:

Experience in First Year of Diamond Production

33

ItemImplications for:

Grade Price Revenue

1. Better than expected feed grades because of better geology

Higher n/a Higher

2. Higher levels of diamondbreakage than initially expected

Lower Lower Lower

3. Higher than expected production of small (-3mm) diamonds

Higher Lower Higher

4. Positive reaction to Renard diamonds in the rough market

n/a Higher Higher

5. Market conditions for certain diamond categories

n/aNet

LowerNet

Lower

Net Result Experienced to DateHigher than expected grades

and lower than expected pricing at sale

29.28ctSold for US$530,000 April 2017

(US$18,100/carat)

Renard 2 Kimb2b ore, 30-40% dilution, 290m level

34

Renard Diamond Price ReconciliationBased on Mixed Renard 2-Renard 3 Production Sold to Date

Diamond Price Timeline – Renard 2&3 (US$/ct)

November 2011 – Feasibility Study: WWW1 base case model valuation for combined R2-R3 diamond sample based on an average of 5 independent valuators.

March 2016 – Mine Plan: Mine Plan

price revised based on published

rough price indices

December 2017: Sales to end-FY2017

$139

$87

($15)

($28)

($9)

$60

$70

$80

$90

$100

$110

$120

$130

$140

($15) ($28) ($9)Mar-16 Dec-17 Project to Date

$/ct

Price Reconciliation 2016 - 2017 Breakdown (US$/ct)

Price factors: (Diamond Market and

recovered diamond quality)

Size Distribution factors: (higher

smalls production and lower large

recovery)

Short Term FY2017 Market factors:

(eg Indian demonetization)

US$/ct

$182

$139

$87

1. WWW International Diamond Consultants

Physical diamond attributes (Size and Quality) influenced by Plant

Market

35

2016-2017 Mining and Processing

Ore Processed, Carats Recovered, head grade

Monthly Material Mined (Ore and Waste)

Monthly Processed Ore Grade

Monthly Ore Milled

Monthly Carats Recovered

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Car

ats

per

To

nn

e

R2 Grade

R3 Grade

R65 Grade

Commercial Production Declared

--

50

100

150

200

250

Tho

usa

nd

Car

ats

R65 Ore

R3 Carats

R2 Carats

Commercial Production Declared

--

50

100

150

200

250

Tho

usa

nd

To

nn

es

R65 Ore

R3 Ore

R2 Ore

NameplateThroughput(tpd)

Commercial Production Declared

--

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Mill

ion

To

nn

es

Total WasteMined

Total OreMined

Commercial Production Declared

Process Plant

36

Successful ramp up to nameplate capacity of 6,000 tpd (2.16 Mt/a)

Based on 78% plant utilization

Average processing rate in the Fourth Quarter was 6,014 tpd

Expansion to 7,000 tpd (2.52 Mt/a) is scheduled for 2018 based on 83.5% utilization and +2% throughput.

Flow sheet:

Primary jaw crushing to < 230mm

Twin DMS circuits at +1mm -19mm

LDR circuit at +19mm -45mm, scalable to -60mm

Oversize +45mm to secondary cone crusher

LDR and DMS tails +6mm -19mm to tertiary High Pressure Grinding Rolls

Large Diamond Recovery (“LDR”) through TOMRA XRT

Ore-waste sorting module approved August 2017.

Commissioning scheduled for end Q1 FY2018

Diamond Sales

Stornoway sells 100% of the Renard diamond production by arms length tender in Antwerp with Bonas-Couzyn as sales commissionaire.

Sales are on an undivided basis:

Stornoway acts as sales agent through its commissionaire on behalf of both itself and the streamers.

Stornoway has exclusive authority over marketing strategy.

Other than under exceptional circumstances, Stornoway is a price taker and does not hold inventory outside of normal goods-in-progress.

Stornoway will support the Québec or Canadian brand identification initiatives of its clients through chain of custody certification.

The Bonas contract has a 3 year term, renewable. Bonas is responsible for GDV valuation support, sorting, tender sales, contract sale negotiation, back office support, security. Outside of the contract, SWY pays courier and transport insurance costs and out of pocket management expenses.

Total marketing costs are forecast at less than 3% of revenue, of which the streamers pay their proportional share.

37

38

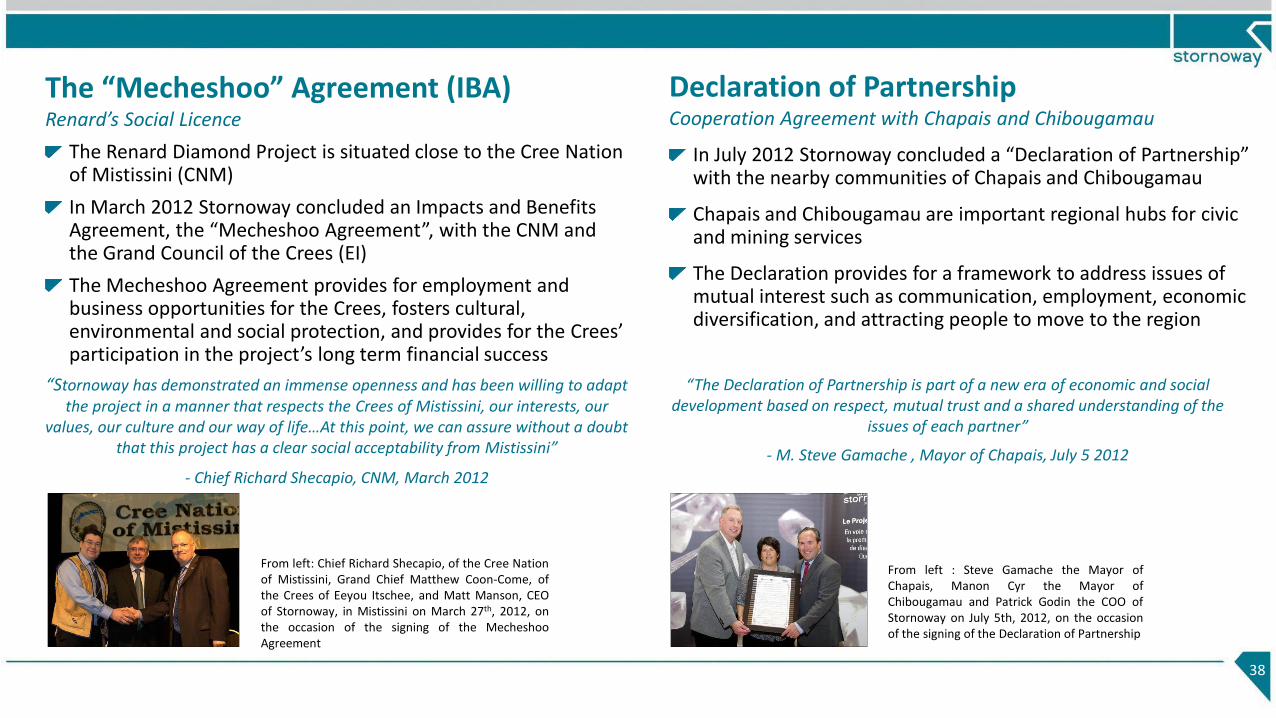

The “Mecheshoo” Agreement (IBA)Renard’s Social Licence

The Renard Diamond Project is situated close to the Cree Nation of Mistissini (CNM)

In March 2012 Stornoway concluded an Impacts and Benefits Agreement, the “Mecheshoo Agreement”, with the CNM and the Grand Council of the Crees (EI)

The Mecheshoo Agreement provides for employment and business opportunities for the Crees, fosters cultural, environmental and social protection, and provides for the Crees’ participation in the project’s long term financial success

“Stornoway has demonstrated an immense openness and has been willing to adapt the project in a manner that respects the Crees of Mistissini, our interests, our

values, our culture and our way of life…At this point, we can assure without a doubt that this project has a clear social acceptability from Mistissini”

- Chief Richard Shecapio, CNM, March 2012

Declaration of PartnershipCooperation Agreement with Chapais and Chibougamau

In July 2012 Stornoway concluded a “Declaration of Partnership” with the nearby communities of Chapais and Chibougamau

Chapais and Chibougamau are important regional hubs for civic and mining services

The Declaration provides for a framework to address issues of mutual interest such as communication, employment, economic diversification, and attracting people to move to the region

“The Declaration of Partnership is part of a new era of economic and social development based on respect, mutual trust and a shared understanding of the

issues of each partner”

- M. Steve Gamache , Mayor of Chapais, July 5 2012

From left: Chief Richard Shecapio, of the Cree Nationof Mistissini, Grand Chief Matthew Coon-Come, ofthe Crees of Eeyou Itschee, and Matt Manson, CEOof Stornoway, in Mistissini on March 27th, 2012, onthe occasion of the signing of the MecheshooAgreement

From left : Steve Gamache the Mayor ofChapais, Manon Cyr the Mayor ofChibougamau and Patrick Godin the COO ofStornoway on July 5th, 2012, on the occasionof the signing of the Declaration of Partnership

39

Origin of Renard’s WorkforceTargeting Local Hiring: Stornoway Employees at Mine Site

43% Northern Québec

52% Other

Québec

5% Other

Canada

58

78

22

13

49

57

48

37

17

23

0 10 20 30 40 50 60 70 80 90

Mistissini & Eeyou Istchee

Chiobougamau

Chapais

Other Communities (NQ)

Abitibi-Temiscamingue

Saguenay Lac St-Jean

Montreal

Quebec

Other Communities (QC)

Other Communities (CA)

402 Employees at Mine Site at April 30, 2017

FY2017 Sustainable Development HighlightsAs at December 31, 2017

40

Health, Safety & Environment

12 months with zero LTIs1 for SWY employees

One incident of administrative environmental non‐conformity due to reporting a glycol spill outside of the 24-hour prescribed delay

Rescue training center constructed at Renard

Increased mining wastewater usage rate from 46% to 78%

2017 Economic Benefits & Employment

$194m in goods & services contracting in Quebec

$58m in contracting to 70 suppliers in Mistissini, Chapais &Chibougamau

$13m in wages for 169 employees from host communities

In December, 437 mine located employees, 12% Cree, 26% from Chibougamau/Chapais, and 62% from outside region

68 internal employee promotions at Renard

2017 “Job Creator of the Year” Award for Northern Quebec

Social & Community

In 2017, Stornoway supported the following initiatives: Centraide/United Way Foundation, Breast Cancer Foundation, Einstein Youth Forum, Cree Mineral Exploration Board (CMEB)

1. Incidents requiring medical aid, temporary re-assignment, or lost time

Local Contracting and Purchasing

Stornoway Prioritizes:

Local hiring and procurement

Contracts from the Cree community of Mistissini, (Eskan and Sakhiikan) and with the families of Sydney Swallow (Kiskinshiish Camp Services) and Emerson Swallow (Swallow-Fournier)

Purchasing from Mistissini, Chibougamau and Chapais

$93 million in goods and services in 2016

estimated $12 million in payroll was added to the local economy

41

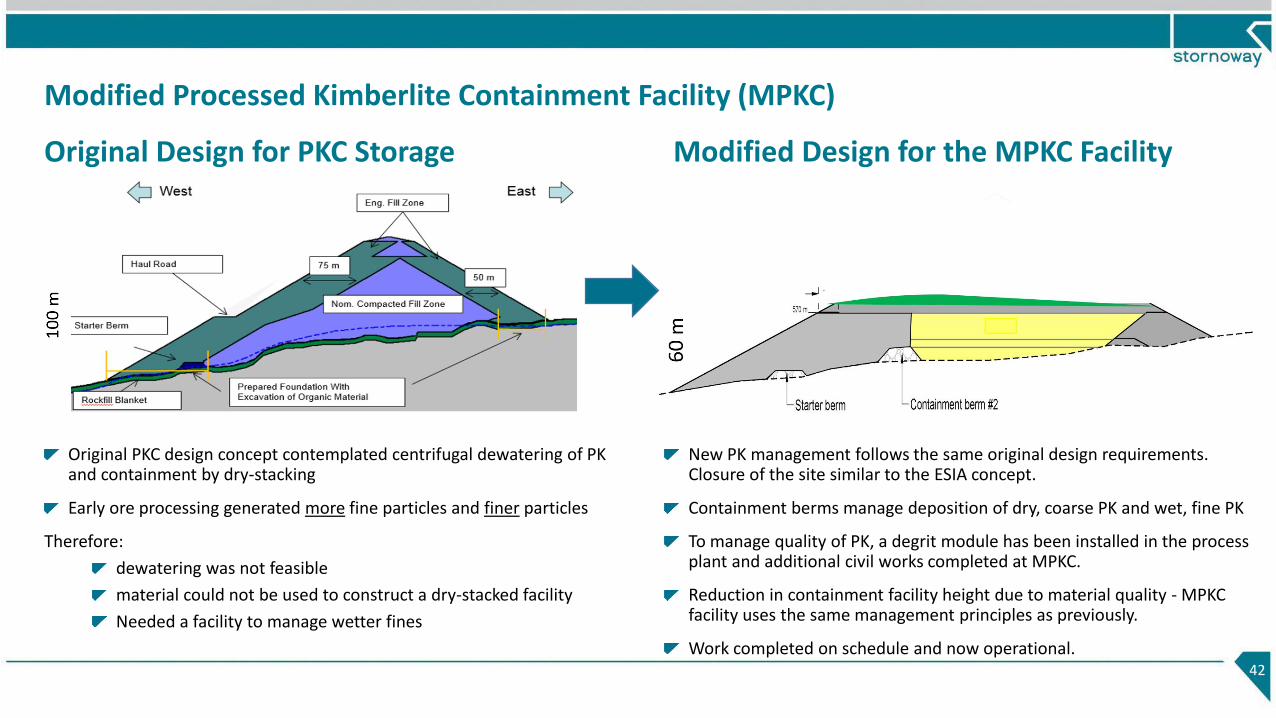

Modified Processed Kimberlite Containment Facility (MPKC)

42

Original Design for PKC Storage Modified Design for the MPKC Facility

Original PKC design concept contemplated centrifugal dewatering of PK and containment by dry-stacking

Early ore processing generated more fine particles and finer particles

Therefore:

dewatering was not feasible

material could not be used to construct a dry-stacked facility

Needed a facility to manage wetter fines

New PK management follows the same original design requirements. Closure of the site similar to the ESIA concept.

Containment berms manage deposition of dry, coarse PK and wet, fine PK

To manage quality of PK, a degrit module has been installed in the process plant and additional civil works completed at MPKC.

Reduction in containment facility height due to material quality - MPKC facility uses the same management principles as previously.

Work completed on schedule and now operational.

Victor De Beers

Komsomolskaya ALROSA

Argyle Rio Tinto

Voorspoed De Beers

Koffiefontein Petra

Diavik Rio Tinto / Washington Corp

Sable, Pigeon, Lynx,Misery Main, Koala (Ekati)

Washington Corp

30

25

20

15

0

35

2016 2017F 2018F 2019F 2020F 2021F

10

5

2022F 2023F 2024F 2025F

Several mines that currently supply 29 million carats a year are expected to be fully depleted by 2030

High depletion rates from existing mines such as Rio Tinto’s Argyle mine which is expected to close within the next few years

Even under the most optimistic supply scenario, multiple new mines are required to replace existing supply

Limited number of economically viable projects due to expensive diamond exploration

Forecasted Rough-Diamond Production of Depleting Mines, Mcts, Optimistic Scenario

The Future: Diamond Supply Outlook

Forecasted Rough-Diamond Production of New Mines, Mcts, Optimistic Scenario

Source: Bain & Company “The Global Diamond Industry 2017: The Enduring Story in a Changing World” 43

Washington Corp

Endiama/ALROSA

Shore Gold

Stornoway

De Beers /Mountain Province

ALROSA

Namakwa Diamonds

Gem Diamonds

DiamondCorp

Koidu Holdings

Lucara

Firestone Diamonds

Otkritie

Jay (Ekati)

Luaxe

Star-Orion South

Renard

Gahcho Kué

Karpinsky-1

Kao

Ghaghoo

Lace

Koidu

Karowe,ex “AK6”

Liqhobong

Grib

30

25

20

15

0

35

2013 2015 2017F 2019F 2021F 2023F

10

5

2025F 2027F 2029F 2030F

Forecasted growth in supply fromrecently developed mines and new mines (+26 Mcts)

Recently developedmines (+7 Mcts)

Pat GodinCOO & Director

Management and Board

44

Non-Executive DirectorsKey Executive Officers

Matt Manson President, CEO& Director

• 20 years in the diamond industry• President and CEO since 2009

• COO since 2010• Professional mining engineer with

20+ years of experience

Annie Torkia-LagaceVP Legal

• Over 14 years of legal experience practicing law and extensive transaction experience

Ebe ScherkusIndependent/Board Chairman

• Chairman since September 2012• President & COO/Director at

Agnico Eagle from 2005 to 2012

Hume KyleIndependent

• EVP & CFO at Dundee Precious Metals• 25+ years of private sector and public

accounting experience

John LeBoutillierIndependent/ IQ Designate

• Recently retired Chairman of Industrial Alliance Insurance and Financial Services Inc.

Gaston MorinIndependent/ IQ Designate

• Professional engineer previously employed by ArcelorMittal Mines as VP, Technology

Marie-Anne TawilIndependent/ IQ Designate

• Member of the board of directors of Hydro-Québec since 2005

Peter NixonIndependent

• 30 years of experience in research and institutional equity sales, largely focused on mining

Douglas SilverOrion Designate

• Portfolio manager at Orion Mine Finance

• 30 years of experience in the international mining industry

Orin BaranowskyCFO

• Over 15 years of finance experience• Over $1 billion of capital raisings for

mining companies

Martin BoucherVP Sustainable Development

• Over 25 years experience in HSEC roles in Quebec Mining including Falconbridge, Canadian Royalties

Ian HollVP Processing

• Over 20 years of experience with De Beers in construction, commissioning and operation of diamond process plants in Canada, Botswana and Namibia