16

European Economic Forecast Winter 2015 Pierre Moscovici Commissioner for Economic and Financial Affairs, Taxation and Customs 5 February 2015

| Date post: | 15-Jul-2015 |

| Category: |

Government & Nonprofit |

| Upload: | euintheus |

| View: | 437 times |

| Download: | 2 times |

European Economic Forecast Winter 2015

Pierre Moscovici Commissioner for Economic and Financial Affairs,

Taxation and Customs

5 February 2015

EU growth is gradually improving

2

GDP growth in the EU

85

90

95

100

105

-3

-2

-1

0

1

2

3

4

07 08 09 10 11 12 13 14 15 16

GDP growth rate (left scale)GDP (quarterly), index (right scale)GDP (annual), index (right scale)

forecast

quarter on quarter % change index, 2007=100

3.1 0.5

-4.4

1.7 -0.4

Figures above horizontal bars are annual growth rates.

2.00.0 1.3

1.72.1

Steep fall in oil pricesBrent oil spot prices (USD/€)

3

30

50

70

90

110

130

12 13 14 15

USD/bbl

EUR/bbl

price per bbl

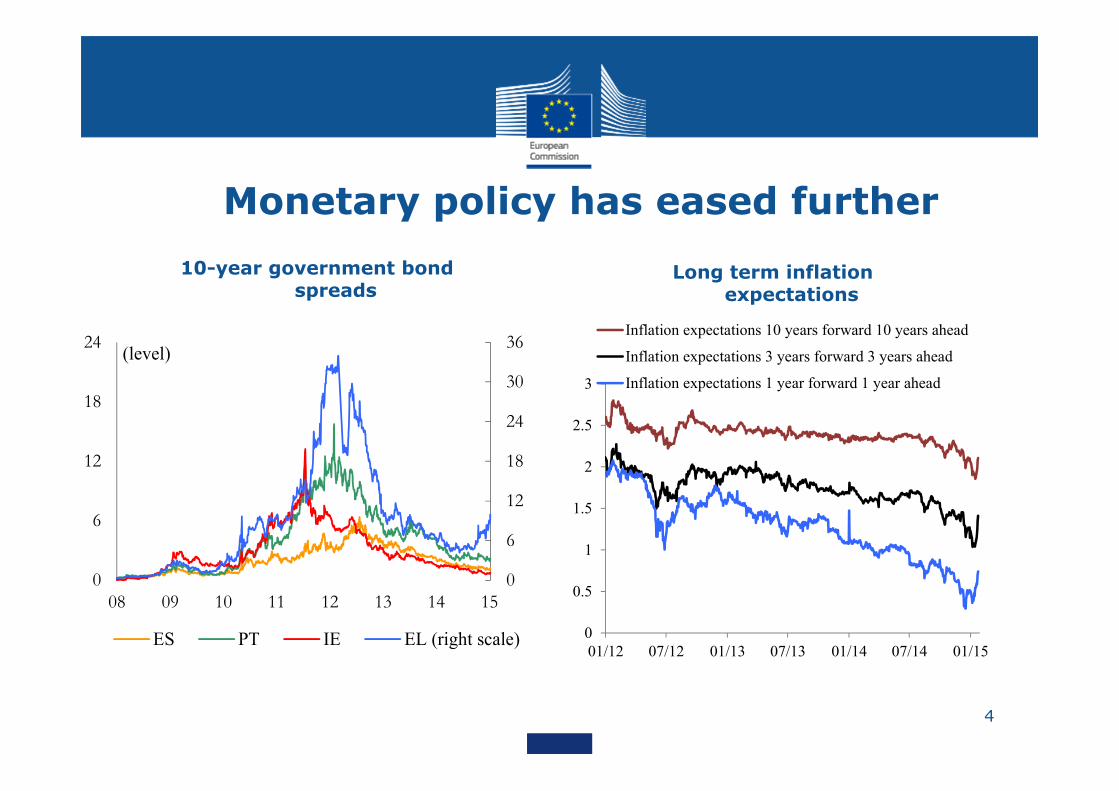

Monetary policy has eased further

4

10-year government bond spreads

Long term inflation expectations

0

6

12

18

24

30

36

0

6

12

18

24

08 09 10 11 12 13 14 15

ES PT IE EL (right scale)

(level)

0

0.5

1

1.5

2

2.5

3

01/12 07/12 01/13 07/13 01/14 07/14 01/15

Inflation expectations 10 years forward 10 years ahead

Inflation expectations 3 years forward 3 years ahead

Inflation expectations 1 year forward 1 year ahead

Euro has depreciated against major peers

5

Euro exchange rates, USD and JPY

Real and nominal effective exchange rate

90

100

110

120

130

140

150

160

170

180

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

06 07 08 09 10 11 12 13 14 15

USD/EUR (left scale)JPY/EUR (right scale)(level) (level)

-6

-4

-2

0

2

4

6

8

LV LT EE FI SI LU AT

SK DE

BE

NL PT MT IT FR ES

EL CY IE

EA19

NEER

REER

%monthly averages (% change March - December 2014)

The fiscal stance in the EU is now neutral

6

Budgetary developments, EU

-7

-6

-5

-4

-3

-2

-1

0

1

2

-7

-6

-5

-4

-3

-2

-1

0

1

2

09 10 11 12 13 14 15 16

General goverment balance (left scale)Structural balance (right scale)

forecast

% of GDP % points

Upbeat signals on bank lending

Bank lending to households and non-financial corporations, euro area

Net changes in credit standards and credit demand, euro-area

7

-50-30-101030507090110

-100-80-60-40-20

0204060

06 07 08 09 10 11 12 13 14 15

Credit standards - past 3 months (left scale)Credit standards - next 3 months (left scale)Credit demand - past 3 months (right scale)Credit demand - next 3 months (right scale)

balance

tightening ↑

↓ easingbalance

decrease ↓ increase ↑

-10

-5

0

5

10

15

05 06 07 08 09 10 11 12 13 14

bank lending to NFCs

total NFC debt funding

GDP (nominal growthrate)

%

8

Growth in global GDP

Global growth is firming, but is uneven across regions

30

35

40

45

50

55

60

65

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

07 08 09 10 11 12 13 14

Emerging economies

Advanced economies

Global manufacturing andservices PMI (right scale)

% points index

Source: Global Insight, Markit Group Limited

EU growth is gradually improving

9

GDP growth in the EU

85

90

95

100

105

-3

-2

-1

0

1

2

3

4

07 08 09 10 11 12 13 14 15 16

GDP growth rate (left scale)GDP (quarterly), index (right scale)GDP (annual), index (right scale)

forecast

quarter on quarter % change index, 2007=100

3.1 0.5

-4.4

1.7 -0.4

Figures above horizontal bars are annual growth rates.

2.00.0 1.3

1.72.1

All EU economies set to grow in 2015

10

Investment growth is set to pick up

11

90

95

100

105

110

115

08 09 10 11 12 13 14 15 16

EA

EU

index, avg('00-'07) = 100

forecast

Total investment, EU and euro area

Unemployment is slowly declining

12

Employment growth and unemployment rate, EU

6

7

8

9

10

11

-0.8-0.6-0.4-0.20.00.20.40.60.81.0

07 08 09 10 11 12 13 14 15 16

Employment (quarter on quarter % change, leftscale), forecast (year on year % change, left scale)Unemployment rate (right scale)

% % of the labour

forecast

Forecast figures are annual data.

Significant differences in fiscal performance between countries

13

-15

-13

-11

-9

-7

-5

-3

-1

1

3

SI EL ES IE CY PT FR BE IT MT

SK LT FI NL

AT

LV EE

DE

LU

2013 2015

% of GDP -7

-6

-5

-4

-3

-2

-1

0UK HR PL HU RO SE CZ BG DK

2013 2015

% of GDPEA Non-EAGeneral government balance, EU

Risks to the growth outlook

14

Risks on the downside:• Geopolitical risks• Renewed financial market volatility• Delayed implementation of structural reforms• Long period of low inflation

Risks on the upside:• Faster than expected impact of policy measures• Further depreciation of the euro• Larger impact of low oil prices

EU growth map 2015

15

European Economic Forecast Winter 2015

Pierre Moscovici Commissioner for Economic and Financial Affairs,

Taxation and Customs

5 February 2015