Journal of Agricultural and Applied Economics, 31,3(December 1999):437–448 O 1999 Southern Agricultural Economics Association Evaluating the Performance of Agricultural Bank Management: The Impact of State Regulatory Policies Bernard K.N. Armah, Jr., Timothy A. Park, and C.A. Knox Lovell ABSTRACT We evaluate agricultural bank management performance, focusing on the impacts of in- terstatebanking laws on productivity change. The generalized Malmquist productivity in- dex decomposes productivity change into technological change, technical efficiency change, and change in scale economies. While managerial productivity rose from 1982 to 1991, statesthat adopted the most liberal interstatebanking laws experienced the greatest improvement in productivity. Large agricultural banks were more efficient in states that had more liberalized interstatebanking laws while small agriculturalbanks fared better in states with more restrictive laws. Key Words: generalized Malmquist index, interstate banking, productivity change. Before 1978, no state permitted out-of-state acquisitions of its banks. Within 25 years the interstate banking regulations that had been in place for over a century disappeared as states adopted liberalized interstate banking laws. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 allows banks to branch across state borders after June 1997 if states concur. Deregulation which had proceeded as a state and regional initiative ef- fectively shifted to a uniform federal policy. Policy analysts and state legislators continue to examine whether these provisions benefit or hurt banks in their states. The main objective of this study is to eval- uate changes in the productivity of agricultural BernardK.N.Armah,Jr.isagraduatestudentandTim- othyA. Parkis associateprofessor,Departmentof Ag- ricultural and Applied Economics, and C.A. Knox Lovell is professorin the Departmentof Economics, all at the Universityof Georgia, Athens,Georgia. bank management linked to the banking de- regulation using the generalized Malmquist in- dex. This index enables us to investigate the contribution of scale economies to productiv- ity change. For agricultural banks in states that had some form of interstate banking law prior to the Riegle-Neal Act, we estimate productiv- ity change focusing on the impacts of inter- state banking laws on the economies of scale and managerial productivity change. We ex- amine the impacts of relaxing government re- strictions on structural changes in agricultural banking by applying the generalized Malm- quist index which explicitly incorporates the influence of scale economies on productivity change. The survival of small local banks has been vital to the economic and social development of rural areas. Opponents of interstate banking assert that this policy could lead to the erec- tion of new entry barriers. When large bank-

Transcript

Journal of Agricultural and Applied Economics, 31,3(December 1999):437–448O 1999 Southern Agricultural Economics Association

Evaluating the Performance of AgriculturalBank Management: The Impact of StateRegulatory Policies

Bernard K.N. Armah, Jr., Timothy A. Park, and

C.A. Knox Lovell

ABSTRACT

We evaluate agriculturalbank management performance, focusing on the impacts of in-terstatebanking laws on productivity change. The generalized Malmquist productivity in-dex decomposes productivity change into technological change, technical efficiencychange, and change in scale economies. While managerialproductivity rose from 1982 to1991, statesthat adopted the most liberal interstatebanking laws experienced the greatestimprovement in productivity. Large agriculturalbanks were more efficient in states thathad more liberalized interstatebanking laws while small agriculturalbanks fared better instateswith more restrictive laws.

Before 1978, no state permitted out-of-stateacquisitions of its banks. Within 25 years theinterstate banking regulations that had been inplace for over a century disappeared as statesadopted liberalized interstate banking laws.The Riegle-Neal Interstate Banking andBranching Efficiency Act of 1994 allowsbanks to branch across state borders after June1997 if states concur. Deregulation which hadproceeded as a state and regional initiative ef-fectively shifted to a uniform federal policy.Policy analysts and state legislators continueto examine whether these provisions benefit orhurt banks in their states.

The main objective of this study is to eval-uate changes in the productivity of agricultural

BernardK.N. Armah,Jr.is a graduatestudentandTim-othy A. Parkis associateprofessor,Departmentof Ag-ricultural and Applied Economics, and C.A. KnoxLovell is professor in the Departmentof Economics,all at the Universityof Georgia,Athens,Georgia.

bank management linked to the banking de-regulation using the generalized Malmquist in-dex. This index enables us to investigate thecontribution of scale economies to productiv-ity change. For agricultural banks in states thathad some form of interstate banking law priorto the Riegle-Neal Act, we estimate productiv-ity change focusing on the impacts of inter-state banking laws on the economies of scaleand managerial productivity change. We ex-

amine the impacts of relaxing government re-strictions on structural changes in agriculturalbanking by applying the generalized Malm-quist index which explicitly incorporates theinfluence of scale economies on productivitychange.

The survival of small local banks has beenvital to the economic and social developmentof rural areas. Opponents of interstate bankingassert that this policy could lead to the erec-tion of new entry barriers. When large bank-

438 Journal of Agricultural and Applied Economics, December 1999

ing organizations acquire local banks andgrow in market share, these institutions mayapply newly acquired market power to carryout predator y pricing. This drives smallercompetitors from the market and prevents theentry of new firms. With the concentration oflocal markets, banks with large market sharescan increase fees on services, increase loanrates, and reduce rates of deposits, denying thepublic the benefits of more intense competi-tion among suppliers of financial services.Thus, removing restrictions on interstate bank-ing and branching might cause small banks togradually disappear.

Supporters of interstate banking contendthat removing interstate banking restrictionswould result in the entry of more efficientbanks into local markets where previouslysheltered banks earn excess profits. Propo-nents argue that an intensified level of com-petition will eliminate inefficient banks andimprove the quality and availability of finan-cial services for consumers and small busi-

nesses.The importance of the new regulatory re-

gime is illustrated by examining the dramaticreductions in the number of agricultural banks.From 1980 to 1991, agricultural banks de-clined from 5,316 to 3,952 as 350 agriculturalbanks failed and 950 either consolidated ormerged. Sixty-four banks were taken over bythe Federal Deposit Insurance Corporationwhich allowed solvent banks to take over con-trol of the assets of the failed banks evenacross state lines.

Bank mergers have been justified by theexistence of scale and scope economies. Bycontrast most studies of bank costs find in-creasing returns to scale only for small bankswith less than $100 million in total assets anddecreasing returns to scale for larger banks.Measuring the impacts of these changes on theperformance of banks is critical given recentstructural and legislative developments. Pro-

ductivity measures that explicitly account forthe impacts of scale economies will enablelegislators and banking analysts to identifywhether productivity changes are mainly driv-en by technical efficiency changes, changes in

technology or movement toward operation atan optimal scale.

Regulatory Environment and LiteratureReview

In this section we briefly describe the originsand development of banking regulation alongwith the types of interstate banking laws thathave been adopted by states. We summarizekey studies examining the impacts of interstatebanking on the structure and the profitabilityof the commercial banking industry and theeffects of interstate banking on managerialskill. The analysis identifies key variables usedin previous studies and the role of data aggre-gation in measuring the interstate banking im-pacts.

The first federal legislation focusing on thegeographic scope of bank operations was theMcFadden Act, passed in 1927 and amendedin 1933, which permitted national banks thesame branching opportunities that states al-lowed their state-chartered banks. Bank hold-ing companies (BHCS) are banks that own oneor more other banks and offer bankers an or-ganizational form to circumvent intrastatebranching restrictions. The Douglas Amend-ment of the Bank Holding Company Act of1956 prohibited BHCS from acquiring banksin other states unless those states specificallyallowed such acquisitions. The McFadden Actand the Douglas Amendment implied the rightof each state to determine a legally enforce-able position on interstate banking expansion.

By 1991, different forms of interstate bank-ing laws had been adopted in the UnitedStates. The approaches to interstate legislationgenerally fit one of three basic categories: na-tionwide open-entry, national reciprocity, orregional reciprocity. Nationwide open-entrypermitted acquisitions and other activities bybank holding companies found anywhere inthe nation. This was the most liberal form ofinterstate banking law and the majority of thestates in this group were found in the West.Reciprocity meant that out-of-state BHCScould make acquisitions in a given state onlyif those out-of-state BHCS were in states thatgranted similar privileges to BHCS in the other

Armah, Park, and L.ovell: Performance of Agricultural Bank Management 439

state. States that adopted the national reci-procity law were not aligned in any distinctgeographic pattern across the United States.

Regional reciprocity meant that interstatebanking was limited only to states specified inthe state legislation and reciprocity was re-quired. These compacts were usually limitedto adjacent states or those next to the adjacentstates. Most Southern states, including Ala-bama, Arkansas, and Georgia adopted thislaw. States that had not adopted any form ofinterstate banking law consisted mostly ofMidwestern states with a large scale of agri-cultural activity.

Lence (1997) summarizes key trends influ-encing the structure of the banking industrysince 1980, highlighting the role of economicforces driven by bank efficiency, market pow-er, and portfolio diversification along withgovernment forces such as the relaxation ofbranching and interstate banking restrictions.Most of the studies listed were based on in-dividual bank data.

Our analysis is based on state-level data tomeasure the impact of state characteristics askey determinants of bank efficiency. Paneldata allow us to evaluate the impact of policyinitiatives and shifting state regulatory strate-gies across cross-sectional units over time.States did not uniformly and consistentlyadopt similar banking regulations. By April 1,1989 seven states, including California, Col-orado, and Pennsylvania had some form of re-gional interstate banking law. In March 1990,Pennsylvania adopted national reciprocitywhile California and Colorado adopted thesame law in January, 1991. By observingthese units over different points in time, paneldata allow us to separate the effects of scaleeconomies and technological change on pro-ductivity. The availability of extended panelsof state-level data permits us to focus on thesources of productivity changes identified inthe generalized Malmquist index.

Other researchers have conducted studiesconcerning the impacts of the new intrastatebranching and interstate banking laws on com-mercial banks. Berger, Kashyap, and Scaliseundertake simulations using commercial bankdata aggregated nationally from 1979 to 1994

which suggest that nationwide banking will re-sult in substantial consolidation of the bankingindustry. The study concludes that littlechange will occur in the distribution of indus-try assets across organization size. Chong in-vestigates the impacts of interstate banking oncommercial banks’ risk and profitability usingcapital market data and the event study meth-odology. The evidence shows that interstatebanking improves the profitability of commer-cial banks and is associated with significantincreases in the banks’ exposure to marketrisk.

Hubbard and Palia examine whether amore competitive environment requires great-er management skills in chief executive offi-cers using interstate bank regulation as a mea-sure of competitive conditions. Interstateregulations with fewer entry barriers lead to ahigher level of potential competition and de-mand managers with greater skills, resultingin higher compensation levels for these man-agers. This evidence indicates that a more

competitive environment creates the need formanagers with greater managerial talent whocan enhance the bank’s competitive position.

Swamy et al. investigate the determinantsof U.S. commercial bank performance from1980 to 1993 using state-level commercialbank data on rates of return on assets (ROA)and equities (ROE). Explanatory variablesinclude bank-specific variables, location re-striction variables and a variable to measuregeneral economic conditions. Locational re-strictions such as barriers to entry significantlyimprove commercial bank profits. Berger alsoused ROA and ROE in evaluating the bankingindustry,

Studies determining the impacts of thebanking and branching restrictions have typi-cally employed data aggregated at various lev-els such as industry, state, and national levels.Wallace uses state-level data to analyze struc-tural and efficiency changes in financial per-formance across agricultural and nonagricul-

tural banks from 1980 to 1991. Althoughsignificant consolidation has occurred, smallagricultural banks have stayed competitive andoutperformed nonagricultural banks on several

440 Journal of Agricultural and Applied Economics, December 1999

measures of profitability, liquidity, efficiency,and solvency.

McLaughlin uses aggregated bank holdingcompany (BHC) data to examine the impactsof interstate banking and branching reform onthe BHCS. Observed changes in bank behaviorfollowing liberalization of state branching andinterstate banking from 1988 to 1993 showthat BHCS responded quickly to state branch-ing liberalization by consolidating their bankswithin states. However, the BHCS were slowerto respond to interstate banking reforms to ex-pand into additional states.

Mengle’s analysis is based on individualand aggregated bank data to show that inter-state branching is a logical and feasible stepin the evolution of the geographical structureof American banking. The study outlines somearguments for interstate branching and thendiscusses ways of application, the likelihoodof adoption, and possible effects on the bankstructure in the United States. Mengle con-cludes that both banks and consumers wouldbenefit from such a law and suggests that thenumber of large banks would decrease whilesmall bank numbers would likely remain un-changed.

Model Development

Economies, Hubbard, and Palia develop amodel of monopolistic competition betweenlarge and small banks that highlights the linkbetween performance measurement and inter-state banking restrictions. We outline the mainfeatures of the model here, focusing on its test-able implications for assessing managerial per-formance in agricultural banks. Assume thereare M banking markets with m participatingbanks in each market. Competition betweenbanks takes place in a three-stage sequentialmodel of a differentiated products markets:banks enter, choose locations, and choose pric-es.

Small banks participate in only one marketwhile large banks participate in g markets asthe degree of competition in each market isdefined by the number of participants. Themodel determines the equilibrium price andnumber of banks and a profit function for each

type of bank. The profits of bank i in market

j are H,J (Pj; gi, m), where Pj = (Pi,j, . . . . P~,J)is the vector of prices charged by all banks inthis market, and g, is the number of marketsin which the bank participates. The profits ofbank i in market j are decreasing in the num-ber of competitors in that market. Profits ofsmall banks depend on one market only. Prof-its per branch of large banks participating ing~ markets are

‘II H,,,(p,; at m)(1) n’ (F’gh,m) = ,? gh

where P is a vector of all prices for all marketsin which the large bank participates whichrange from 1 to g~.

Depositors are informed about bank prof-itability by identifying banks that operate inmultiple markets. Large banks have lower lev-els of profit variability than smaller banks dueto their ability to diversify their portfoliosacross multiple markets. This risk-pooling ar-gument applies even if all markets representidentical distributions. Drawing from econom-ic activity across geographic markets that arenegatively correlated is an additional factorthat lowers the variability of profits for largebanks relative to small banks.

To attract additional deposits, banks thatoperate in only one market respond by holdingmore capital per dollar of assets than banksoperating in many markets. Small banks holdmore equity capital per branch than largebanks because they are not as diversified.Large banks with branches in multiple marketshave higher expected profits than small banksin any market in which both types of banksparticipate.

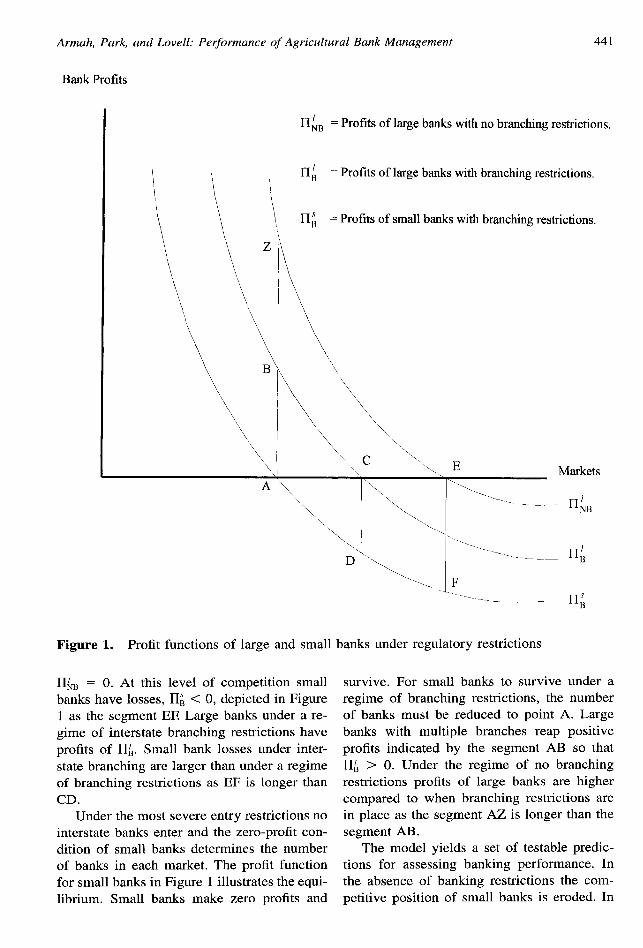

Figure 1 presents a graphical depiction ofthe profit functions of large and small banksfor the regimes when interstate branching isprohibited and when nationwide open entry isallowed. With no restrictions on interstatebanking, the free-entry equilibrium is deter-mined by the zero-profit condition for largebanks. Profits of large banks facing no inter-state banking restrictions are I& and the free-entry equilibrium number of banks is given by

Armah, Park, and Lovell: Pe#ormance of Agricultural Bank Management 441

Bank Profits

l-i’NB = Profits of largebankswith no branchingrestrictions.

\\

11: = Profits of largebankswith branchingrestrictions.

\ \\~~= Profits of smallbankswith branchingrestrictions.

A

/“\

\ ‘\‘\

\ “’’.\\c “\, E

l\ 1A.

\

‘\‘\

Figure 1. Profit functions of large and small

~~B = O. At this level of competition smallbanks have losses, II; <0, depicted in Figure1 as the segment E17 Large banks under a re-gime of interstate branching restrictions haveprofits of I&. Small bank losses under inter-state branching are larger than under a regimeof branching restrictions as EF is longer thanCD.

Under the most severe entry restrictions nointerstate banks enter and the zero-profit con-dition of small banks determines the numberof banks in each market. The profit functionfor small banks in Figure 1 illustrates the equi-librium. Small banks make zero profits and

I ‘\ I “=.

4 \ =%—‘-i..,

‘---\,_

-=______D’

\ -.. . . F=.. _

banks under regulatory restrictions

survive. For small banks to survive under aregime of branching restrictions, the numberof banks must be reduced to point A. Largebanks with multiple branches reap positiveprofits indicated by the segment AB so that11~ > 0. Under the regime of no branchingrestrictions profits of large banks are highercompared to when branching restrictions arein place as the segment AZ is longer than thesegment AB.

The model yields a set of testable predic-tions for assessing banking performance. Inthe absence of banking restrictions the com-petitive position of small banks is eroded. In

442 Journal of Agricultural and Applied Economics, December 1999

markets where small banks are dominant,Economies, Hubbard, and Palia suggest thatinterstate banking regulation allows smallbanks to deter entry by large banks. These re-sults imply that assessments of bank perfor-mance and productivity should be based onprofitability measures plus characteristics spe-cific to the environment in which banks op-erate.

Measuring Productivi~ Change Using the

Generalized Malmquist Productivity Index

The technical efficiency of a production unitis a comparison between observed and optimalvalues of its output and input. This compari-son can take the form of the ratio of observedto maximum potential output obtainable fromthe given input. Alternatively, we may definethe comparison as the ratio of minimum po-tential to observed input required to producethe given output, or some combination of thetwo.

In this section, we discuss the generalizedMalmquist productivity index which we use tomeasure and decompose bank managementproductivity change into technical efficiencychange, technological change, and change inscale economies. The generalized Malmquistindex proposed and implemented by Grifell-Tatj6 and Lovell explicitly incorporates the in-fluence of scale economies on productivitychange and accounts for three key componentsof efficiency changes over time.

First, banking firms undergo changes intechnical efficiency over time as they respondto competitive pressures and adjust marketingstrategies. Index E accounts for this compo-nent which is due to managerial efficiency andreflects productivity change arising fromchanges in the manager’s technical efficiencybetween tand t + 1. This index E measures afirm catching up to the best-practice frontierand represents technical efficiency change.

Second, firms adopt innovative technolog-ical and marketing techniques and induce thefrontier technology to shift outward over time.The index T captures the activities and per-formance of the best-practice firms in adoptingand managing new technology between the

two periods resulting in shifts in the produc-tion frontier (innovation). The index T mea-sures the contribution to productivity changedue to any technical change in the industry.

Third, large banks may achieve economiesof scale over time as they spread productiveresources over multiple products more effi-ciently. Managers may exploit these efficien-cies to combine a bank and an insurance agen-cy and sell loans, acquire deposits, and marketinsurance policies in one organization. Thescale index S measures this third componentand attains a value greater than unity if achange in the producer’s scale of productioncontributes positively to productivity change.A change in the scale of production positivelyaffects productivity change if it is a movementtoward the technically optimal scale. The in-dex of change in scale economies ensures thatthe generalized Malmquist index does notoverstate productivity change when inputgrowth occurs in the presence of decreasingreturns to scale.

Let X’t = (x’/, . . . . x~) a O denote an (N X

1) vector of inputs and y“ = (y\’, . . . . y~) =O represent an (M X 1) vector of outputs forproducer i=l, . . .. Iinperiodt =1, . . ..T.An output-oriented generalized Malmquist in-dex of productivity for producer i between pe-riod t and t + 1, using period t technology asa reference can be expressed as

(2) G,(x,t, y“, X“+l,Ytl+l)= E.T. $

where, the right-hand side elements in equa-tion (2) are

The calculation and decomposition of thegeneralized Malmquist index requires the cal-culation of six output distance functions foreach cross-sectional unit. The within-period

Armah, Park, and Lovell: Performance of Agricultural Bank Managetnent 443

output distance function D~(x’t, y’t) for produc-er i in period t is obtained from the followinglinear programming model:

(4) [D’(x”, y“)]-’ = max 0

subject to

(5) ey: s ~ z“y~,

~ zJtx{ 5::,

z]t ~ o ~z,t= 1,

J

m=l, . . ..M

n=l, . . ..N

‘j=l, . . .. I

where the zJtisan activity variable. The struc-ture of the best practice technology availablein period t is characterized by the constraintsof the problem. The technology described bythe program satisfies convexity, strong dispos-ability of output and inputs, and variable re-turns to scale.

The objective of the problem is to achievethe maximum feasible radial expansion in theoutputs of producer i without violating bestpractice. Producer i is pronounced technicallyefficient if the maximum is unity; for anymaximum greater than unity, the producer isviewed as technically inefficient, The problemis solved I times, once for each producer inthe sample period t, resulting in technical ef-ficiency scores for each producer and yieldingthe values of the I output distance functionsDt(xlt, ylt) in period t.

The remaining five output distance func-tions which make up the generalized Malm-quist productivity index are calculated in asimilar way by modifying the constraints ofthe problem. identified in (4) and (5). For ex-ample, the convexity constraint identified asthe fourth constraint in equation set (5) is de-leted to calculate the constant returns to scaledistance functions D~(x”, Y“) and D~(x”+’, y“).

The mixed distance function D’(x”+ 1, y’t+1)is estimated by comparing observations in pe-riod t + 1 with the best-practice frontier ofperiod t.D’+’ (x”, y“) uses data from both pe-riods to evaluate (xt, yt) relative to technologyconstructed from t + 1 data. In estimating thedistance functions for the index of scale econ-

omy change, D:(x’t+ i, ylt) evaluates data com-prising period t+ 1 inputs and period toutputsusing period t technology. The subscript cshows that the distance function is defined rel-ative to some constant returns to scale tech-nology. Dt(xt+’, yl) performs the same evalu-ation as D~(x”-”, y“) to a variable returns toscale technology.

After solving these six linear programmingproblems for each set of observations, we in-sert the values into equation (2) to obtain thegeneralized Malmquist index and its compo-nents. An index below unity shows a declinein productivity while a value exceeding 1 sug-gests growth.

Data and Variables

This section discusses the data and measuresof inputs and outputs used in the analysis. Theestimates of the productivity indexes werebased on annual statewide aggregate data foragricultural banks for 1982 and 1991 using in-formation on the agricultural and nonagricul-tural banking performance from Wallace. Wefocus on data that were available for 36 statesfor both sample periods, building on the in-sights presented by Swamy et al. and Berger,Hanweck, and Humphrey who also used state-level data in their analyses of U.S. commercialbanks.

Banks consolidate or merge to ensure anincrease in present or future profits. They op-erate in markets and engage in activities thatboost their current or future profits. We mea-sure managerial performance using profitabil-ity measures consistent with Swamy et al. andBoyd and Gertler. Managers of financial insti-tutions and other industry professionals eval-uate bank performance based on financial ra-tios derived from balance sheets and incomestatements. Profitability ratios measure theability of the firm to produce net returns suf-ficient to sustain survival and growth andserve as an indicator of bank management’sresponse to changing market conditions.

The output variables chosen for this studyare two ratios drawn from the profitabilitymeasures—the rate of return on assets (ROA)and the rate of return on equity (ROE). The

444 Journal of Agricultural and Applied Economics, December 1999

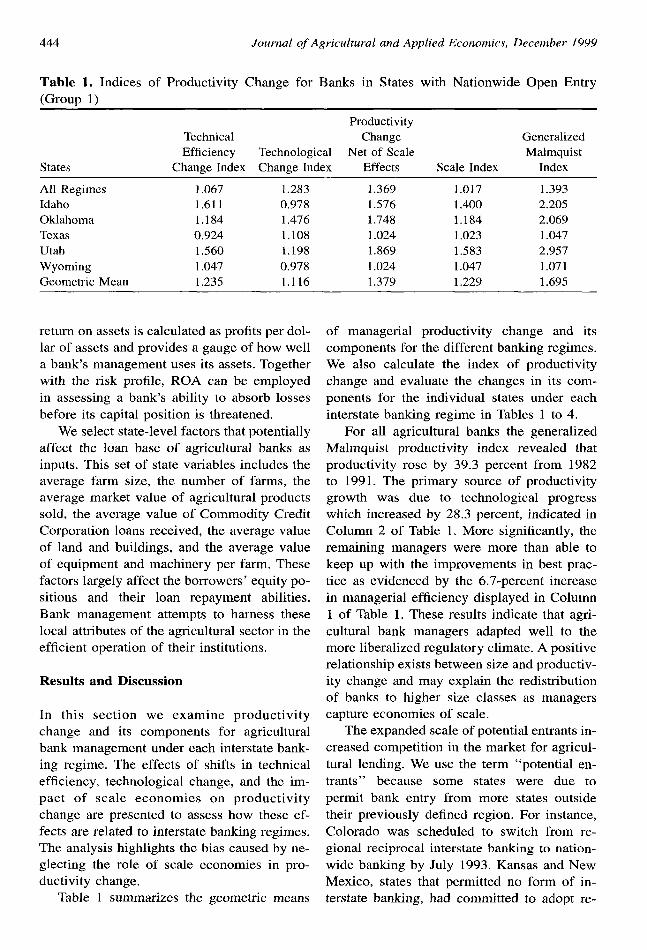

Table 1. Indices of Productivity Change for Banks in States with Nationwide Open Entry(Group 1)

ProductivityTechnical Change GeneralizedEfficiency Technological Net of Scale Malmquist

States Change Index Change Index Effects Scale Index Index

return on assets is calculated as profits per dol-lar of assets and provides a gauge of how wella bank’s management uses its assets. Togetherwith the risk profile, ROA can be employedin assessing a bank’s ability to absorb lossesbefore its capital position is threatened.

We select state-level factors that potentiallyaffect the loan base of agricultural banks asinputs. This set of state variables includes theaverage farm size, the number of farms, theaverage market value of agricultural productssold, the average value of Commodity CreditCorporation loans received, the average valueof land and buildings, and the average valueof equipment and machinery per farm. Thesefactors largely affect the borrowers’ equity po-sitions and their loan repayment abilities.Bank management attempts to harness theselocal attributes of the agricultural sector in theefficient operation of their institutions.

Results and Discussion

In this section we examine productivitychange and its components for agriculturalbank management under each interstate bank-ing regime. The effects of shifts in technicalefficiency, technological change, and the im-pact of scale economies on productivitychange are presented to assess how these ef-fects are related to interstate banking regimes.The analysis highlights the bias caused by ne-glecting the role of scale economies in pro-ductivity change.

Table 1 summarizes the geometric means

of managerial productivity change and itscomponents for the different banking regimes.We also calculate the index of productivitychange and evaluate the changes in its com-ponents for the individual states under eachinterstate banking regime in Tables 1 to 4.

For all agricultural banks the generalizedMalmquist productivity index revealed thatproductivity rose by 39.3 percent from 1982to 1991. The primary source of productivityygrowth was due to technological progresswhich increased by 28.3 percent, indicated inColumn 2 of Table 1. More significantly, theremaining managers were more than able tokeep up with the improvements in best prac-tice as evidenced by the 6.7-percent increasein managerial efficiency displayed in Column1 of Table 1. These results indicate that agri-cultural bank managers adapted well to themore liberalized regulatory climate. A positiverelationship exists between size and productiv-ity change and may explain the redistributionof banks to higher size classes as managerscapture economies of scale.

The expanded scale of potential entrants in-creased competition in the market for agricul-tural lending. We use the term “potential en-trants” because some states were due topermit bank entry from more states outsidetheir previously defined region. For instance,Colorado was scheduled to switch from re-gional reciprocal interstate banking to nation-wide banking by July 1993. Kansas and NewMexico, states that permitted no form of in-terstate banking, had committed to adopt re-

Armah, Park, ana! Lovell: Pe#ormance of Agricultural Bank Management 445

Table 2. Indices of Productivity Change for Banks in States with National Reciprocal Entry(Group 2)

ProductivityTechnical Change GeneralizedEfficiency Technological Net of Scale Malmquist

States Change Index Change Index Effects Scale Index Index

All RegimesIllinoisKentuckyLouisianaMichiganNebraskaNew YorkNorth DakotaOhioPennsylvaniaSouth DakotaVermontWashingtonWest VirginiaGeometric Mean

gional reciprocal and nationwide interstate recorded a scale index of 1 as found in Col-banking laws respectively by July, 1992. Man- umn 4 of Table 2, efficiency was mainly dueagers of larger banks more efficiently em- to diversification of outputs and inputs underployed local resources in the operation of their constant returns to scale. Here, small and largeinstitutions. For banks in states such as Ken- agricultural banks could easily coexist sincetucky, Pennsylvania, and West Virginia that the size of the bank yielded no advantages.

Table 3. Indices of Productivity Change for Banks in States with Regional Reciprocal Entry(Groun 3)

ProductivityTechnical Change GeneralizedEfficiency Technological Net of Scale Malmquist

States Change Index Change Index Effects Scale Index Index

For banks in states with nationwide openentry, the fifth column of Table 1 shows thatproductivity rose by 69.5 percent with an av-erage scale index of 1.229 (Column 4, Table1). This suggests a positive relationship be-tween size and productivity change as largebanks were more efficient under these com-petitive conditions than small banks. Thisfinding is consistent with the results of Bil-lingsley and Lamy that larger BHCS were ex-pected to reap greater benefits from nation-wide interstate banking. Technologicalimprovements for banks under this regimewere slower than in any other group at 11.6percent. The measure of technical efficiencychange indicates that bank managers kept upwith improving technology at a faster rate(23.5%) than those in more restrictive bankingregimes.

Productivity changes for states with nation-al and regional reciprocity laws were lower.For agricultural banks in states with nationalreciprocity (Table 2), the improvement was36.1 percent while that for agricultural banksin regional reciprocity (Table 3) states was33.5 percent. Restrictions on entry by banksfrom other states may have limited potentialor actual competition. As a result local banksmay have gained an increase in market powerand did not have to operate at the most effi-cient level to increase their levels of profit. Weobserve that the average scale indices were0.974 in states with national reciprocity and0.968 in states with regional reciprocity indi-cating that more restrictive conditions seemedto favor small agricultural banks.

Featherstone and Moss (1994) estimateeconomies of scale and scope in agricultural

banking by disaggregating outputs used in ag-ricultural lending. Based on 1990 Call Reportsfrom 7,108 rural or agricultural banks, they

report an overall economies-of-scale measureof 0.986, indicating nearly constant returns to

scale. Economies of scale are exhausted atbank sizes exceeding $60 million. This resultis consistent with the measures obtained herefor banks operating under the more restrictivebanking regimes where scale economy mea-sures of 0.974 and 0.968 were obtained. Bothfindings suggest that restrictive interstatebanking and branching laws favor small agri-cultural banks.

These results reinforce implications fromthe Economies, Hubbard, and Palia model

which suggest that interstate banking restric-tions enhance the competitive position ofsmall banks. The empirical findings align withthose presented in Swamy et al. who foundthat profits for commercial banks were higherin states with substantial barriers to entry. Un-der reciprocity regimes, the main driving forceof productivity change was technological

change. Berger, Kashyap, and Scalise notedthat technological and financial innovations,including improvements in information pro-

cessing and telecommunications technologies,plus the dramatic increases in automated tellermachines over this period played an importantrole in transforming the banking industry.These developments confirm the significantrole of technological change in productivitygrowth. The changes in productivity and theimpact of the productivity components weresimilar for both types of interstate banking

reciprocity laws. This suggests that there is lit-

Armah, Park, and Lovell: Performance of Agricultural Bank Management 44’7

tle advantage in restricting interstate bankingto a smaller region rather than nationwide.

With no interstate banking entry (Table 4),managerial productivity rose by 36.5 percent.Technology improved at a high rate of 14.8percent while the rate of technical efficiencyincrease was lower at a rate of 3.2 percent.These figures may reflect bank responses topotential competition. For example in 1992,Kansas and New Mexico were due to adoptthe regional and national reciprocity laws re-spectively.

The third columns in each table shows theindices of productivity change net of scaleeconomies and demonstrates the importance ofusing the generalized Malmquist index forevaluating productivity change in agriculturalbanks. A value for the scale index greater thanunity indicates that a change in the producer’sscale of production contributes positively toproductivity change. A positive contribution toproductivity results from expansion under in-creasing returns or contraction of productionin the region of decreasing returns to scale.

These calculations demonstrate that ne-glecting scale economies in measuring pro-ductivity change in agricultural bank manage-ment causes the actual productivity growth tobe understated for states with nationwideopen-entry where output growth occurred inthe presence of increasing returns to scale. Forstates with some form of reciprocity law, pro-ductivity growth net of scale economies over-states actual growth in productivity since out-puts expanded in the region of decreasingreturns to scale. A change in the scale of pro-duction contributes to a decline in productivitychange if it is away from the direction of thetechnically optimal scale.

Summary and Conclusions

The purpose of this study was to evaluate theperformance of agricultural bank managementfrom 1982 to 1991 facing different types ofinterstate banking laws. A generalized Malm-quist productivity index highlights the contri-bution of scale economies to productivitychange. We evaluated the effects of shifts intechnical efficiency, technological change, and

the impact of scale economies on productivitychange in agricultural banks. The magnitudesof these impacts are related to different typesof interstate banking regimes.

Results showed that managerial productiv-ity change, measured by the generalizedMalmquist index, did increase over the periodby 39.3 percent. States that had adopted orwere about to adopt the most liberal interstatebanking laws experienced the most improve-ment in productivity.

We observed an overall positive relation-ship between agricultural bank size and pro-ductivity. Large agricultural banks were moreefficient in states that had a more liberalizedinterstate banking law while small agriculturalbanks fared better in states with more restric-tive laws. Neglecting the impacts of scaleeconomies on productivity change causes usto understate actual productivity growth andthe efficacy of the generalized Malmquist in-dex in eliminating this bias is confirmed inevaluating productivity growth in states withnationwide open-entry.

Interstate banking reforms enhance mana-gerial productivity of agricultural banks andallow managers to take advantage of econo-mies of scale. Managers must also adopt moreefficient practices in the operation of smallbanks. High costs of adjustment limit the abil-ity of small banks to expand. For small agri-cultural banks to survive in the more liberal-ized markets, managers must operate moreefficiently by making use of specializedknowledge about locaI clients.

References

Berger, A.N. “The Relationship Between Capitaland Earnings in Banking.” Journal of Money,

Credit and Banking 27(1995):432–456.Berger, A,N., G.A. Hanweck, and D. Humphrey.

“Competitive Viability in Banking.” Journal ofMonetary Economics 20(1987):501–520.

Berger, A, N,, A.K. Kashyap, and J.M. Scalise.“The Transformation of the U.S. Banking In-dustry: What a Long Strange Trip It’s Been.”Brookings Papers on Economic Activity

2(1995):55–201.

Billingsley, R.S. and R.E. Lamy. “Regional Recip-rocal Interstate Banking: The Supreme Court

448 Journal of Agricultural and Applied Economics, December 1999

and the Resolution of Uncertainty.” Journal of

Banking and Finance 16(1992):665–686.

Boyd, J,H, and M. Gertler, “U.S. CommercialBanking: Trends, Cycles and Policy. ” WorkingPaper No. 4404, National Bureau of EconomicResearch, 1993.

Chong, B.S. “The Effects of Interstate Banking onCommercial Banks’ Risk and Profitability. ” TheReview of Economics and Statistics 73(1991):

78–84.

Economies, N., R.G. Hubbard, and D. Palia. “ThePolitical Economy of Branching Restrictionsand Deposit Insurance: A Model of Monopolis-tic Competition Among Small and LargeBanks.” Journal of Law and Economics39(1996):667-704.

Featherstone, A.M. and C.B. Moss. “MeasuringEconomies of Scale and Scope in AgriculturalBanking. ” American Journal of Agricultural

Economics. 76(August 1994):655–661.Grifell-Tatj6, E. and C.A.K. Lovell. “The Sources

of Productivity Change in Spanish Banking. ”European Journal of Operational Research

98(1997):364-380.

Hubbard, R.G. and D. Palia, “Executive Pay and

Performance: Evidence from the U.S. BankingIndustry. ” Journal of Financial Economics

39(1995):105-130.Lence, S.H. “Recent Structural Changes in the

Banking Industry, Their Causes and Effects: ALiterature Survey. ” Review of Agricultural Eco-nomics. 19(Fa11/Winter 1997):37 1–402.

McAllister, PA. and D. McManus. “Resolving theScale Efficiency Puzzle in Banking. ” Journal ofBanking and Finance 17( 1993):389–405.

McLaughlin, S. “The Impact of Interstate Bankingand Branching Reform: Evidence from theStates.” Federal Reserve Bank of New York,Current Issues in Economics and Finance1(1995):1–6.

Mengle, D.L. “The Case for Interstate BranchBanking. ” Federal Reserve Bank of Richmond,Economic Review 76( 1990):3–16.

Swamy, l?A. V.B., J.R. Barth, R. Y.Chou, and J.S.Jahera, Jr. “Determinants of U.S. CommercialBank Performance: Regulatory and Economet-ric Issues. ” Research in Finance 14(1996): 117–156.

Wallace, G.B. “Agricultural and NonagriculturalBanking Statistics. ” Washington, D. C.: USDAERS, Statistical Bulletin No. 883, 1994.

![Cooperative and Agricultural Credit Bank[2]](https://static.documents.pub/doc/80x56/577d354c1a28ab3a6b900e64/cooperative-and-agricultural-credit-bank2.jpg)