54

Evaluating Your Annual Fund Consultants of Philanthropy ● Fund Raising ● Training Robert Croft, CFRE October 20, 2011 www.slideshare.net/ rncroft

| Date post: | 20-Aug-2015 |

| Category: |

News & Politics |

| Upload: | robert-croft |

| View: | 4,393 times |

| Download: | 1 times |

Evaluating Your Annual Fund

Consultants of Philanthropy ● Fund Raising ● Training

Robert Croft, CFREOctober 20, 2011

www.slideshare.net/rncroft

Crandall, Croft & Associates,Evaluating Your Annual Fund

What a Profession!

“The 30 Best Careers for 2009”(November 2008)

“Top 15 Jobs with Stress that Pay Badly”(November 2009)

Crandall, Croft & Associates,Evaluating Your Annual Fund

Today’s Objectives

The Benefits of a Development AuditHow to conduct a self evaluationLearn how to Analyze your programHow to take this information and start

creating an annual fundraising plan

Crandall, Croft & Associates,Evaluating Your Annual Fund

How are You Doing?

How are You Doing?

Crandall, Croft & Associates,Evaluating Your Annual Fund

The New Normal?

Nonprofit Research Collaborative Study (FEP Study)

In the first half of 2011:– 44% saw an increase– 25% raised the same– 20% raised less

In the first half of 2010:– 43% saw an increase– 24% raised the same– 33% raised less

Crandall, Croft & Associates,Evaluating Your Annual Fund

Crandall, Croft & Associates,Evaluating Your Annual Fund

Crandall, Croft & Associates,Evaluating Your Annual Fund

What is a Development Audit?

An internal assessment of your overall fundraising program

Examines governance, human capital, development systems, procedures, donor relations and fundraising approaches

It is an essential tool to measure the gap between an organization’s current fund raising efforts and established best practices in the industry

Crandall, Croft & Associates,Evaluating Your Annual Fund

Reasons to Consider an Audit

Planning a new fundraising initiativeNot satisfied with current resultsHave a need to diversify revenue streamsWant to increase board participationCurrently engaged in strategic planningWould like an objective, expert evaluationWould like to raise the program to a higher

level by incorporating industry best practices Source: What is a Development Audit and When Does Your

Organization Need an Audit – Linda LysakowskiAFP Information Exchange

Crandall, Croft & Associates,Evaluating Your Annual Fund

Why Conduct an Audit?

“If you don't know where you're going, you might not get

there.”

– Yogi Berra

Crandall, Croft & Associates,Evaluating Your Annual Fund

What an Audit will Accomplish:

Create a common understanding of development fundamentals/best practices

Set a precedence of continuous improvement within the development program

Start creating a pervasive culture of philanthropy

Crandall, Croft & Associates,Evaluating Your Annual Fund

Why Conduct an Audit?

It’s hard to plan where you're going if you don't know where

you've been.

Crandall, Croft & Associates,Evaluating Your Annual Fund

What an Audit will Accomplish:

Identify areas of strengths in fundraising

Identify areas of weaknesses in fundraising

Identify current giving patterns and donor preferences

Crandall, Croft & Associates,Evaluating Your Annual Fund

Why Conduct an Audit?

“If you can see things out of

whack, then you can see how things can be in whack.”

– Dr. SeussAin’t it GREAT to be a

Fundraiser?

Crandall, Croft & Associates,Evaluating Your Annual Fund

What an Audit will Accomplish:

Provide clarity on areas for improvement

Identify priorities for fundraising strategies by comparing current activities with accepted better/best practices

Set goals, organizationally and personally, that will move towards a comprehensive fundraising program

Crandall, Croft & Associates,Evaluating Your Annual Fund

Destination: A Strong and Consistent Fundraising Program

Crandall, Croft & Associates,Evaluating Your Annual Fund

Keys to Strong Annual Fundraising

Written Annual Fundraising Plan– With attainable goals and it is being followed

Case for Support– Provides a clear and compelling reason to

support the organization

Regular Donor Communications– Clearly demonstrates how support makes a

difference

Know Thy Donors

Crandall, Croft & Associates,Evaluating Your Annual Fund

Keys to Strong Annual Fundraising

Strong Board Support– Including financial

CEO Actively Involved in FundraisingVolunteer Fundraisers

– Volunteers make the best fundraisers!

Keep Records– Donor software program

Crandall, Croft & Associates,Evaluating Your Annual Fund

Different Levels of Audit

“Global Audit” – similar to S.W.A.T. analysis– Governance/Organizational Structure– External Environment– Fundraising Track Record– Constituency Analysis– Program Maturity– Resource Availability– Fundraising Culture– Donor Perspective

Audit Tool Available:http://www.guymallabone.com/resources

Crandall, Croft & Associates,Evaluating Your Annual Fund

Different Levels of Audit

Basic and Effective Audit:– Leadership Review: Board, CEO, Staff– Constituency Review– Fundraising Activities Review– Availability of Resources

Crandall, Croft & Associates,Evaluating Your Annual Fund

Leadership Review

BoardCEO/Executive

DirectorDevelopment

Staff

Crandall, Croft & Associates,Evaluating Your Annual Fund

Board’s Role in Fundraising

Believe strongly in the organization's mission in order to convince others of its merit.

Contribute to the organization financially to the fullest of their personal capabilities as an indicator of commitment.

Open doors to prospects and serve as an Ambassador for the organization.

Make direct cultivation and solicitation calls by mail, telephone, or in-person.

- Source: Association of Fundraising Professionals

Crandall, Croft & Associates,Evaluating Your Annual Fund

Board’s Role in Fundraising

Additionally, as a group the board:Approves all fundraising plans and budgets.Monitors revenue streams - the funds flowing into

the organization. Identifies and rates potential donors.Hosts/Assists with cultivation events such as tours,

socials, meetings, and presentations.

- Source: Association of Fundraising Professionals

Crandall, Croft & Associates,Evaluating Your Annual Fund

Key Questions @ Board

Do all board members contribute financially as a sign of commitment?

Do board members actively participate in the fund development process?

Is there a development committee?

The “culture of fundraising” begins

with the board!!

Crandall, Croft & Associates,Evaluating Your Annual Fund

Questions @ CEO/Executive Director?

Does the CEO understand the importance of development to the organization?

What is the CEO’s role in fundraising?

Is the CEO engaged in building relationships and soliciting major gifts?

CEO is the Chief Fundraising Officer!

Crandall, Croft & Associates,Evaluating Your Annual Fund

Questions @ Development Staff

Are staff professional and adequately knowledgeable?

Is there a commitment to regular professional training and education?

Are development staff roles clearly defined and focused only on fundraising?

Do staff maintain ethics in fundraising?Are staffing levels adequate to meet

fundraising needs?

Crandall, Croft & Associates,Evaluating Your Annual Fund

Constituency Analysis

Crandall, Croft & Associates,Evaluating Your Annual Fund

Constituency Analysis

Create a list of your donor/prospect audiences?– Individuals, Corporations, Foundations, Churches,

Alumni, Former Clients, Volunteers– Basic Demographics of donor base?

List how you are connecting with these audiences? How are you cultivating?– News, newsletters, speaking engagements,

special events, friends, volunteer opportunities, etc

Crandall, Croft & Associates,Evaluating Your Annual Fund

Cultivation of Constituency

Do you know your top 100 donors?Do you have systems in place for identifying

prospects, acquiring new prospects?Do you conduct research on donors and

potential donors?Do you have a data management system in

place to keep donor/prospect records?

Crandall, Croft & Associates,Evaluating Your Annual Fund

Fundraising Activities Analysis

Crandall, Croft & Associates,Evaluating Your Annual Fund

Fundraising Activity Review

List all of your current fundraising activities:– Grant Writing– Direct Mail, Newsletter– Telephone– Recurring Giving Program– Planned Giving Program– Special Events– In-Kind donation drives– Personal Solicitation – Major Gift Program– Corporate Sponsorships

Crandall, Croft & Associates,Evaluating Your Annual Fund

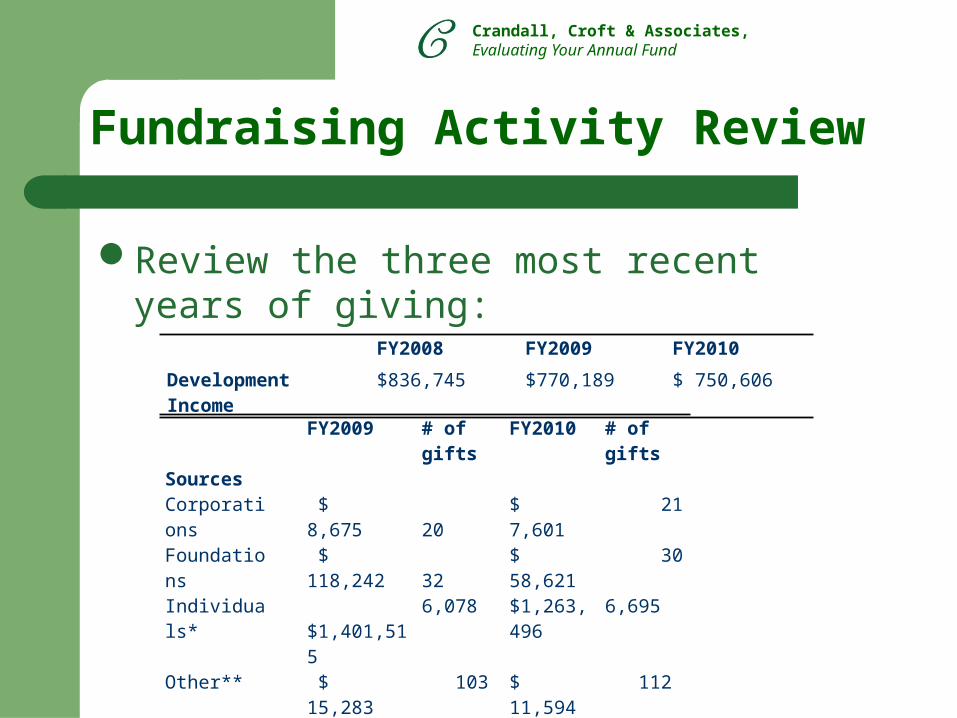

Fundraising Activity Review

Review the three most recent years of giving:

FY2008 FY2009 FY2010

Development Income $836,745 $770,189 $ 750,606

FY2009 # of gifts FY2010 # of gifts SourcesCorporations $ 8,675 20 $ 7,601 21 Foundations $ 118,242 32 $ 58,621 30 Individuals* $1,401,515 6,078 $1,263,496 6,695 Other** $ 15,283 103 $ 11,594 112

Crandall, Croft & Associates,Evaluating Your Annual Fund

Fundraising Review Questions

Is the fundraising program diverse?Are fundraising efforts systematic and

consistent?Are we utilizing established industry “best”

practices?What approaches work best for this

organization?

Crandall, Croft & Associates,Evaluating Your Annual Fund

Fundraising Review Questions

Do fundraising strategies reflect the mission and program activities?

What is the ROI for the overall program and for each activity? (Are you tracking cost per dollar raised?)

Crandall, Croft & Associates,Evaluating Your Annual Fund

Donor Software is COOL b/c…

Reports, reports and more reports

Crandall, Croft & Associates,Evaluating Your Annual Fund

Giving Dynamics Report

– What areas are strong?– What can be improved?

– Should also monitor donor segments (presidents circle, monthly donors, corporations, etc)

Crandall, Croft & Associates,Evaluating Your Annual Fund

Identify Weak Areas

Not many New Donors? Why? High attrition rate? Why?Donors Not Upgrading Support? Why?What can you do in each of these scenarios?

Crandall, Croft & Associates,Evaluating Your Annual Fund

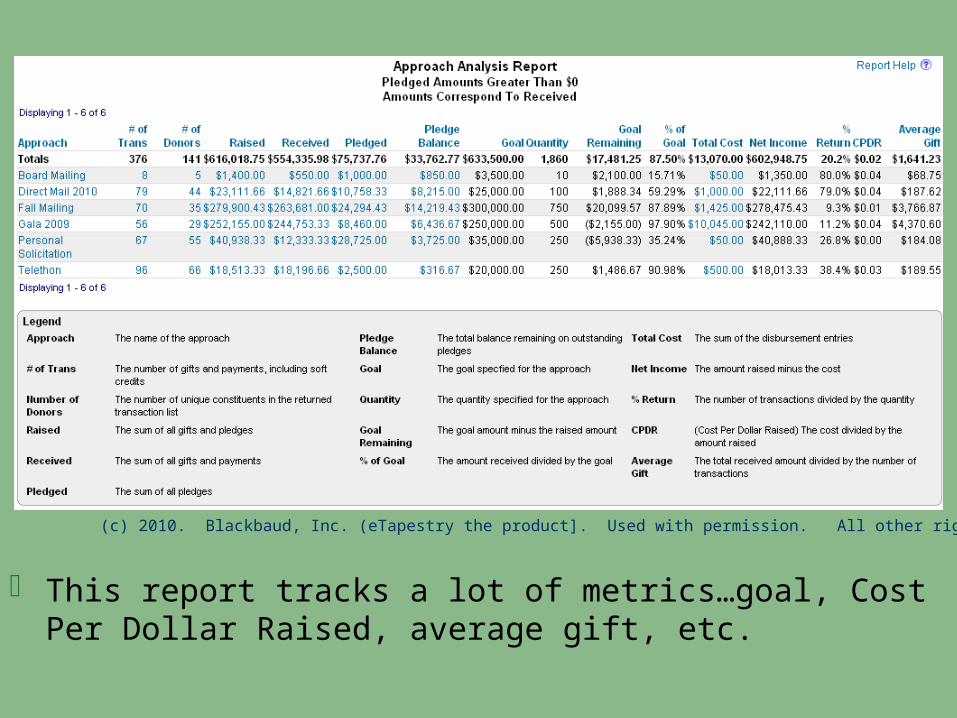

- This report tracks a lot of metrics…goal, Cost Per Dollar Raised, average gift, etc.

(c) 2010. Blackbaud, Inc. (eTapestry the product]. Used with permission. All other rights reserved.

Crandall, Croft & Associates,Evaluating Your Annual Fund

Fund Analysis ReportFund # of Donors # of Gifts Total Raised Average Gift

Annual Fund – Unrestricted 1,312 3,051 $726,624.98 $238.16

Client Sponsorship /Recurring Giving

303 1,494 $233,051.66 $155.99

Group Home Construction 82 188 $112,510 $598.46

Special Olympics 31 37 $7,028.60 $189.96

New Community Center 29 64 $266,735 $4,167.73

Music Therapy Program 10 12 $3,545 $295.42

Animal Therapy Program 5 5 $2,995 $599.00

Endowment Fund 5 5 $17,350 $3,470

Which area/program/giving option has the most donors? May indicate strongest appeal. Which has the highest average gift? Be sure to account for impact of major gifts.Compare with previous years and look for trends. May indicate a shift in interest in donor base.

Crandall, Croft & Associates,Evaluating Your Annual Fund

Focus on Effective StrategiesNow Consider Effective Strategies…

Crandall, Croft & Associates,Evaluating Your Annual Fund

Why is Annual Support Flat?

In non-recessionary environment, flat or declining annual fundraising is often due to:– Too much emphasis on inefficient methods or too

little emphasis on effective methods– Poor donor acquisition, or lack of planning or

budget for acquisition– Poor donor retention!!!– Neglecting to analyze results and adjusting

(usually from “tyranny of the urgent” and being understaffed)

Crandall, Croft & Associates,Evaluating Your Annual Fund

The Development Challenge

The Fundraising “Bucket”– Acquisition and Retention

Nonprofits lose 5 donors for every 6 they obtain - Fundraising Effectiveness Project

A 10% increase in donor retention can increase the lifetime value of the donor database by up to 200 percent. - IU Center on Philanthropy

Crandall, Croft & Associates,Evaluating Your Annual Fund

Top Focus: Donor Retention

Recent studies are showing that 9 out of 10 donors ARE NOT going to consider a gift supporting a new organization this year.

2011 FEP Study: NPOs gained more new or reactivated donors than they lost in lapsed donors in 2010, net increase of 1.7 percent in the number of donors. This compares favorably to a -3.2 percent average net loss of donors in 2009.

Crandall, Croft & Associates,Evaluating Your Annual Fund

Top Focus: Donor Retention

Where in the fundraising plan is donor stewardship and retention?

What can we do to renew and keep Donors?– Create a new donor process– Intentional renewal solicitations– Intentional stewardship to build trust

Crandall, Croft & Associates,Evaluating Your Annual Fund

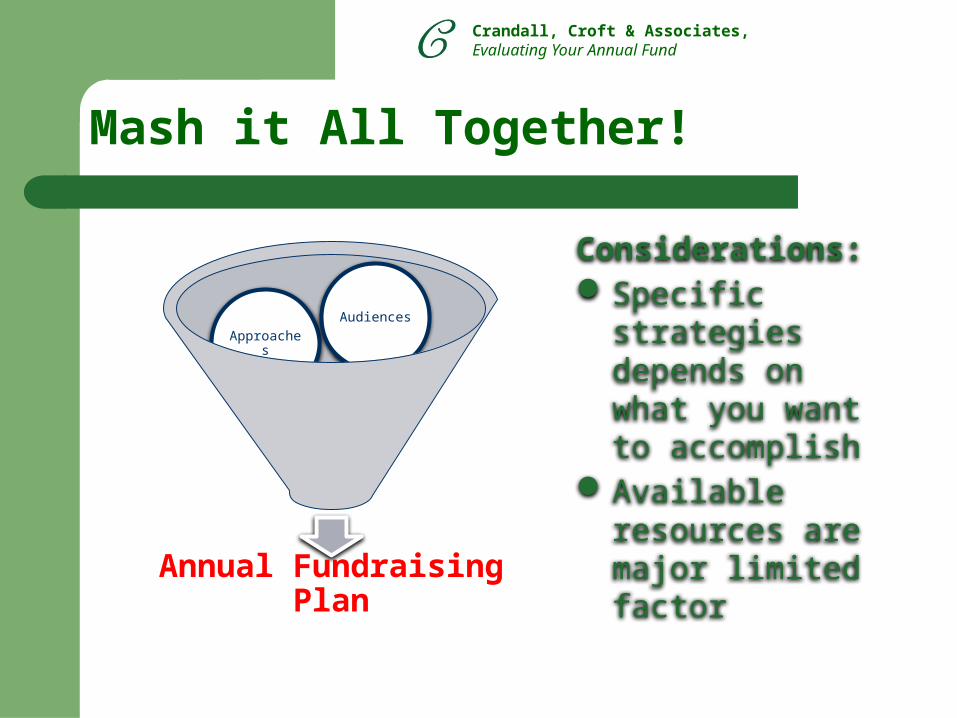

Mash it ALL Together!

Crandall, Croft & Associates,Evaluating Your Annual Fund

Mash it All Together!

Annual Fundraising Plan

Available Resources

Approaches

Audiences

Considerations:Specific strategies

depends on what you want to accomplish

Available resources are major limited factor

Crandall, Croft & Associates,Evaluating Your Annual FundAudiences - Donor Segments

Top Donors (Major Gifts)Staff Responsible: GaryObjective: To cultivate relationships and secure major gifts for annual support and for special projects or capital needs through personal contact. A specific cultivation and solicitation plan should be developed for each person within the major gift list, and a total annual goal from this group determined. This group must be a manageable list of donors who have demonstrated major gifts with previous giving to Rainbow Acres, or have been specifically identified as a major gift prospect, including rancher families. Should be no more than 25-50 donors. (A full time major gifts officer can only effectively cultivate about 80-120 individuals per year.) For the moment, Gary should identify individuals capable of completing Community Center Campaign and focus on a few individual major gifts for annual support. Activities:Develop specific and individualized cultivation and solicitation strategies for each donorFace to face visitsPhone callsPersonal notes, Birthday cards or calls, holiday cards, etcEmail when appropriateVIP Events (like reception during 35th anniversary)Individuals may be include in regular appeal letter mailings at CEO’s discretion, but must have a handwritten cover note.Solicitations should be specific whenever possibleTwice a year, the development team should intentionally review donor list and recent gifts for potential major gift prospects to add to this segment

Crandall, Croft & Associates,Evaluating Your Annual FundFundraising Activities (Approaches)

Direct Mail: 2009 Sybunt AppealsAugust 09 Appeal letter sent to all Sybunts who had given $1-$499Sept mail appeal letter to all Sybunts who had given $500 or more (636 individuals)ask to renew supportSegment by date of last gift (the further out the gift, the lower the gift array/request should be…goal is to recapture at any amount) Acquisition MailingsAcquisition efforts are critical to maintaining current donor levels to account for donor attrition, as well as adding to the donor base.Fall 2009 – An acquisition package may be created to mail in October targeting the 6,000 on the list who have never given. The theme could be around highlighting 35 years of ministry and accomplishments. Given current staff limitations, consideration may be given to drafting the Year end appeal message around this theme and then slightly adjust package and message for this group.Fall 2010 – A traditional acquisition approach should be planned for the Fall of 2010, including list rental options.

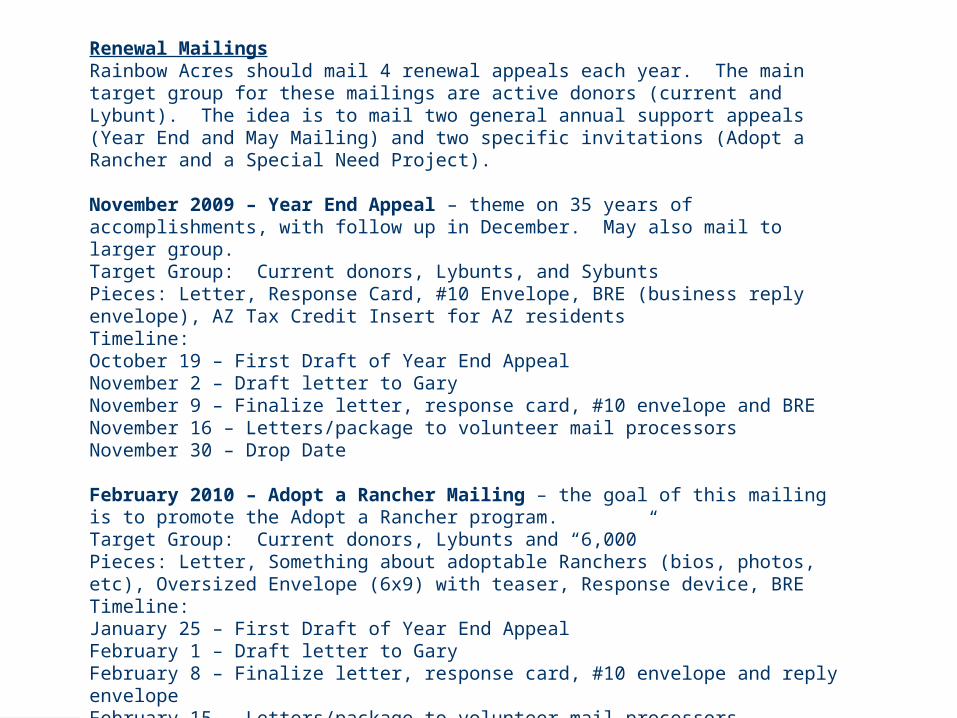

Crandall, Croft & Associates,Evaluating Your Annual FundRenewal Mailings

Rainbow Acres should mail 4 renewal appeals each year. The main target group for these mailings are active donors (current and Lybunt). The idea is to mail two general annual support appeals (Year End and May Mailing) and two specific invitations (Adopt a Rancher and a Special Need Project). November 2009 – Year End Appeal – theme on 35 years of accomplishments, with follow up in December. May also mail to larger group.Target Group: Current donors, Lybunts, and SybuntsPieces: Letter, Response Card, #10 Envelope, BRE (business reply envelope), AZ Tax Credit Insert for AZ residentsTimeline:October 19 – First Draft of Year End AppealNovember 2 – Draft letter to GaryNovember 9 – Finalize letter, response card, #10 envelope and BRENovember 16 – Letters/package to volunteer mail processors November 30 – Drop Date February 2010 – Adopt a Rancher Mailing – the goal of this mailing is to promote the Adopt a Rancher program. Target Group: Current donors, Lybunts and “6,000”Pieces: Letter, Something about adoptable Ranchers (bios, photos, etc), Oversized Envelope (6x9) with teaser, Response device, BRE Timeline:January 25 – First Draft of Year End AppealFebruary 1 – Draft letter to GaryFebruary 8 – Finalize letter, response card, #10 envelope and reply envelopeFebruary 15 - Letters/package to volunteer mail processorsFebruary 22 – Drop Date

Crandall, Croft & Associates,Evaluating Your Annual Fund

Annual Fundraising Plan

Direct Mail Communications Special Events Gary’s ScheduleSeptember 09 Sybunt Mailing –

$500 + prev. gift2010 CALENDAR

October Acquisition package to 6,000 never givers

35th Anniversary Event

35th Anniversary Event

November Year End Appeal (house list)- Tax Credit insert to AZ donors

Rainbow Promise (Highlight 35th, mail early Nov)

Host Desserts with Major Donor Prospects (continue thru 2010)

Individual/personal solicitations to top donors

December Current Renewal Appeal

Christmas Cards (non-solicitation)

…….. ……..

Follow up to Year End mailing

…….. ……..

2010January AAR Follow up to

non-responsesQ1 Rainbow Promise

……..

Tax Statements and Brief Annual Report

February Adopt a Rancher Package (house list plus “6,000”)

……..

March Church AAR promotional (mini-display)

……..

April Final follow up mailing to 6,000 never givers

Q2 Rainbow Promise

Blazin’ M Event

May General Appeal (house list)

Update Mailing Letter to Families

June

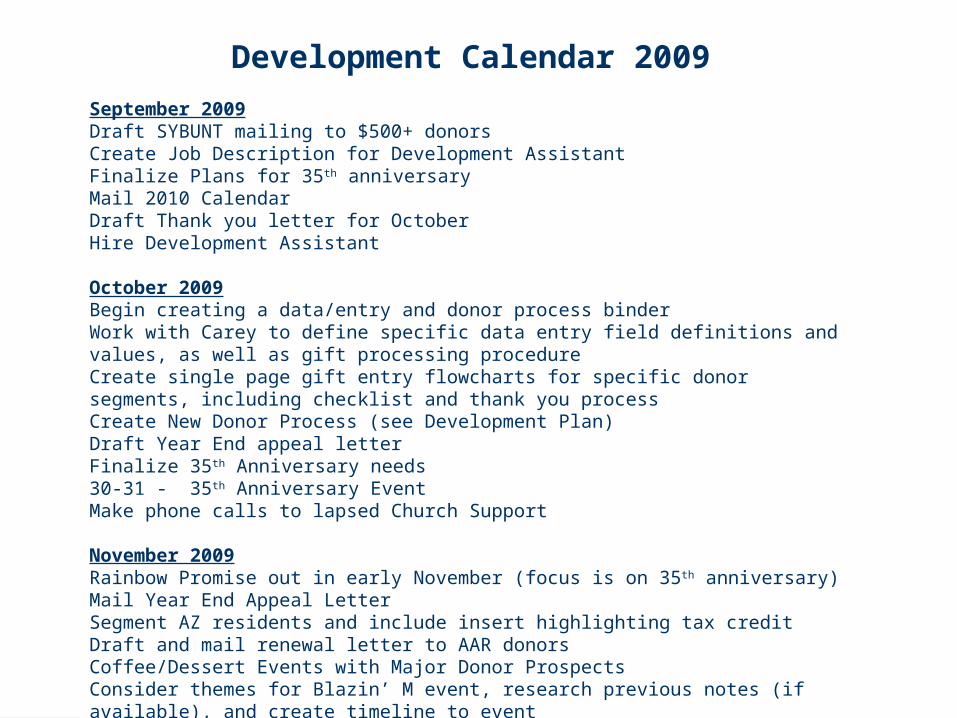

Crandall, Croft & Associates,Evaluating Your Annual FundDevelopment Calendar 2009

September 2009Draft SYBUNT mailing to $500+ donorsCreate Job Description for Development AssistantFinalize Plans for 35th anniversaryMail 2010 CalendarDraft Thank you letter for OctoberHire Development Assistant October 2009Begin creating a data/entry and donor process binderWork with Carey to define specific data entry field definitions and values, as well as gift processing procedureCreate single page gift entry flowcharts for specific donor segments, including checklist and thank you processCreate New Donor Process (see Development Plan)Draft Year End appeal letterFinalize 35th Anniversary needs30-31 - 35th Anniversary EventMake phone calls to lapsed Church Support November 2009Rainbow Promise out in early November (focus is on 35th anniversary)Mail Year End Appeal LetterSegment AZ residents and include insert highlighting tax creditDraft and mail renewal letter to AAR donorsCoffee/Dessert Events with Major Donor ProspectsConsider themes for Blazin’ M event, research previous notes (if available), and create timeline to event

Crandall, Croft & Associates,Evaluating Your Annual Fund

Annual Fundraising Plan

2011 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DECGroup A Newsltr Letter

from a child

Newsltr Appeal Newsltr Back to School Report

Appeal Newsltr Thank You Card

EOY Ltr

Group B Newsltr Program Recap Report

Newsltr Appeal Newsltr Letter from the President

Appeal Newsltr Thank You Card

EOY Ltr

Group C Newsltr State of the Org Ltr

Newsltr Appeal Letter with photos

Newsltr Appeal Newsltr Thank You Card

EOY Ltr

Group D Newsltr Letter from X

Newsltr Appeal Newsltr Private event

Appeal Newsltr Thank You Card

EOY Ltr

Source: Janet L. Hedrick, CFRE from “Near, Dear, and Clear” by Paul Lagasse in Advancing Philanthropy Nov/Dec 2010

Crandall, Croft & Associates,Evaluating Your Annual Fund

How Often to Evaluate?

Evaluate Overall Plan annually– Ideally, fundraising plan

will align with strategic planning

Evaluate each approach constantly

Crandall, Croft & Associates,Evaluating Your Annual Fund

Questions?