SV\/P672 Evaluation of Financial Policy Credit Allocation in Bangladesh Arvind Virmani WORLD BANK STAFF WORKING PAPERS Number 672 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

All rights reservedManufactured in the United States of AmericaFirst printing October 1984

This is a working document published informally by the World Bank. To presentthe results of research with the least possible delay, the typescript has not beenprepared in accordance with the procedures appropriate to formal printed texts, andthe World Bank accepts no responsibility for errors. The publication is supplied at atoken charge to defray part of the cost of manufacture and distribution.

The World Bank does not accept responsibility for the views expressed herein, whichare those of the author and should not be attributed to the World Bank or to itsaffiliated organizations. The findings, interpretations, and conclusions are the resultsof research supported by the Bank; they do not necessarily represent official policy ofthe Bank. The designations employed, the presentation of material, and any maps usedin this document are solely for the convenience of the reader and do not imply theexpression of any opinion whatsoever on the part of the World Bank or its affiliatesconcerning the legal status of any country, territory, city, area, or of its authorities, orconcerning the delimitation of its boundaries, or national affiliation.

The full range of World Bank publications, both free and for sale, is described in theCatalog of Publications; the continuing research program is outlined in Abstracts ofCurrent Studies. Both booklets are updated annually; the most recent edition of each isavailable without charge from the Publications Sales Unit, Department T, The WorldBank, 1818 H Street, N.W., Washington, D.C. 20433, U.S.A., or from the EuropeanOffice of the Bank, 66 avenue d'I6na, 75116 Paris, France.

Arvind Virmani is an economist in the Development Research Department of theWorld Bank.

Library of Congress Cataloging in Publication Data

Virmani, Arvind, 1949-Evaluation of financial policy.

(World Bank staff working papers ; no. 672)1. Credit control--Bangladesh. 2. Finance--Bangladesh.

I. Title. II. Series.HG3711.B3V57 1984 332.7'09549'2 84-20985ISBN 0-8213-0429-1

Abstract

The Bangladesh Goverrnment has used a variety of policies to

influence the allocation of credit to specific borrower groups like poor

farmers, uses such as housing, and sectors such as agriculture. These

policies have also been used tc reduce allocation for certain uses such

as inventory holding ("speculative purposes"). The policies used have

included interest controls credit guarantees, refinance and margine

requirements. This paper attempts a systematic analysis of all the

policies used by the Bangladesh government in the light of the explicit

or implicit objectives of the government. The effect of each of the

policies used, alone or in combination, is analysed with a view to

evaluating their usefulness and efficiency. The analysis then provides

the basis for suggested policy charges in Bangladesh, as well as lessons

for financial policy makers in other countries.

ABREGE

Le Gouvernement du Bangladesh, souhaitant orienter les pratiquesdu credit bancaire de maniere a favoriser certaines categories d'emprunteurstels que les agriculteurs defavorises et certains secteurs comme le logementet l'agriculture, ou, au contraire, a d6courager le detention de stocks ades fins speculatives, a mis en oeuvre tout un eventail de mesures. C'estainsi qu'il agit notamment sur les taux d'int6r&t, les garanties de creditet les criteres regissant les refinancements et les marges ben6ficiaires.Le present document s'efforce de proc6der a une analyse systematique detoutes les mesures appliquees par le Gouvernement, a la lumiere de sesobjectifs explicites ou implicities. II examine l'impact de chacune deces politiques, utilisee isolement ou en association avec d'autres, afinde juger de son utilit6 et de son efficacit6. Sur la base de cette etudecritique, il propose des modifications et tire un certain nombre deconclusions dont peuvent slinspirer les responsables de la politiquefinanciere d'autres pays.

Extracto

El Gobierno de Bangladesh ha utilizado diversas politicas parainfluir en la asignaci6n del credito a grupos especificos de prestatarios,como los agricultores pobres, iy a ciertos usos y sectores, como la vivienday la agricultura. Estas polit-icas se han utilizado ademas para reducir laasignaci6n del cr6dito a deterrninados usos, como el mantenimiento de exis-tencias ("fines especulativos"). Entre las politicas aplicadas cabe citarel control de los intereses, garantias de creditos, refinanciamiento y exi-gencias de margenes. En este trabajo se intenta hacer un analisis sistema-tico de todas las politicas ap]Licadas por el Gobierno de Bangladesh a la luzde los objetivos explicitos o implicitos del mismo. Se analiza el efecto decada una de las politicas util:izadas, por si sola o en combinaci6n conotras, con vistas a evaluar su utilidad y eficacia. El analisis proporcionaluego la base para sugerir cambios de politicas en Bangladesh, asi como paraextraer ensenianzas de posible utilidad para los responsables de elaborar laspoliticas financieras en otros paises.

CURRENCY EQUIVALENTS

The Bangladesh Taka (abreviated TK) is fixed in relation to abasket of reference currencies, with the Pound Sterling serving asintervention currency. On January 11, 1982, the exchange rate was setat TK 38.372 buying and TK 38.472 selling per Pound Sterling. Dependingon exchange rate movements between Sterling and the US Dollar, theTaka/Dollar cross-rate is subject to change. In recent months, thisrate has fluctuated between TK 19 and TK 20.9 per US$.

MEASURES

1 Crore = 10 million

1 Lakh = 100 thousand

FISCAL YEAR

The Bangladesh Fiscal Year (FY) runs from July 1 to June 30.

Chapter Table of Contents Page

I., Introduction 1

1.1 Objectives - Explicit 1

1.2 Objectives - Implicit 1

1.3 Types of Policies 2

1.4 Overall Allocation 3

II. Interest Rate Policy 8

2.1 First Major Revision 8

2.2 Second Major Revision 8

2.3 Effect of Credit Ceilings 10

2.4 Guarantees and Collateral 11

2.5 Distributional Effects 15

2.6 Speculative Credit 16

2.7 Interest Ceilings and Interest Subsidy 16

2.8 Penalty Interest Rates 17

2.9 Objectives and EfEfects of Second Revision 19

2.10 Intra-Bank Lending Rates 22

2.11 Real and Nominal Interest Rates 23

III. Credit Allocation Polic 24

3.1 Overview 24

3.2 The Target Approach 25

3.3 Ceilings and Prohibitions 30

3.4 Margin Requirements: Overview and Analysis 32

3.5 Margin Requirements: Differential Impact 37

3.6 Refinance and Counter Finance: Overview 47

Table of Contents (continued) Page

3.7 Refinance Usage, Intentive Effects and Usefulness 52

3.8 Guarantee Programs 62

3.9 Urban-Rural Branch Licensing 64

IV. Issues of Financial Policy 69

4.1 Efficiency or Inefficiency in Credit Markets 69

4.2 Welfare Objectives and Credit Markets 70

4.3 Differential Interest Rates: Availability vs. Cost 72

4.4 Financing of Specialized Banks: Refinance, Debentures 73or Deposits

4.5 Buffer Stocks: Alternative for Margin Requirements 79and Refinance

4.6 Term Finance 80

V. Agricultural Credit 81

5.1 Introduction 81

5.2 Expected Marginal Product of Loans 82

5.3 Targets and Disbursements; Differential Performance 85

5.4 The Special Agricultural Program and Commercial 88Bank Performance

5.5 Introduction of Urban Organized Banks into 91Agricultural Lending

5.6 Interest Ceilings and BKB Performance 92

5.7 Recovery Performance 94

5.8 Bad Debts vs. Liquidity Problems 101

Footnotes 103

References 103

List of Tables

Table Number Page

1. Sectoral Distr.Lbution of Advances by 4Scheduled Banks

2. GDP in Current Prices by Sectors 6

3. Credit Allocation Index 7

4. Interest Rates on Loans and Advances 9

5. Advances Classified by Size of Accounts 12

6. Advances Classified by Securities 13

7. Loans to Agricuiltural Hunting, Forestry, 14Fishing

8. Advances Classified by Rates of Interest 18

9. Advances to Small Loans and Small Industry, 27House Building and Transport

10. Rates of Growth of Prices and Imposition 33of Margin Requirements

11. Distribution of Advances by Margins for 38Specified Securities, and Average Loan Sizeby Margin for the same Securities

12. Distribution of Advances by Rates of Margin 40for Related Securities

13. Distribution of Advances by Rates of Margin 41

14. Distribution of Advances by Securities 44

15. Distribution of Advances by Economic Purpose 46

16. Use of Refinancie by Bangladesh Krishi Bank 48(BKB) and Bangladesh Samabya Bank (BSB)

17. Average (weighted) Deposit Rate 53

18. Refinance: Usage as a Percentage of 57Entitled Limits

19. Advances and Deposits of Scheduled Banks 59excluding BKB and BSB

List of Tables (continued) Page

20. Payment of Government Guarantees to the 63Banks Under Special Agricultural Credit Program

21. Rural Branch Expansion 65

22. Administrative Costs of Rural Branches 67

23. Sonali Bank Statistics 68

24. Credit-Deposit Ratio by District 78

25. Marginal Product of Loans in Agriculture 83

26. Agricultural Credit 86

27. Special Agricultural Credit Program 89

28. Bangladesh Krishi Bank Borrower Characteristics 93

List of Figures

1. Rationing Equilibrium 36

2. Recovery Profiles by Banks for the Special 96Agricultural Credit Program

3. Recovery Profiles: BKB, Sonali, Agrani and 97Janata Banks

Bangladesh Bank (BB): The Central Bank of Bangladesh.

Co-operative Banks: Consist of an apex co-operative bank and 62central co-operative banks.

Bangladesh Samabaya Bank Limited (BSBL): The apex co-operative bank;sometimes referred to as the Bangladesh Jatiya Bank (BJSB).

Scheduled Banks: Banks permitted to carry out all normal bankingoperations including the taking of deposits from thepublic. They are therefore subject to reserve requirements.

Nationalized Commercial Banks (NCBs): The six commercial banks(Sonali, Janta, Agrani, Rupali, Pubali, Uttara) owned by thegovernment.

Specialized (Scheduled) Banks: Special Purpose Banks which areallowed to take deposits. Consist of:

Bangladesh Krishi Bank (BKB): The Agricultural development bank;Bangladesh Shilpa Bank (BSB): Specialized bank for making medium

and long term loans to industry.

Foreign Commercial Banks': 'Branches of foreign owned banks.

Bangladesh Shilpa Rin Sangst'ha (BSRS): Specialized Institution formaking long and medium-term loans to heavy-mediumindustries. Not a sc'heduled bank.

House Building Finance Corporation (HBFC): Specialized Institutionfor making loans for Housing.

Integrated Rural Development Program (IRDP): A two-tier co-operative system separate from and independent of the co-operative banks. Financed through the Sonali Bank.

PREFACE

This paper applies thet analytical framework developed earlier

by the author in The Nature of Credit Markets in Developing Countries:

A Framework for Policy Analysis, (World Bank Staff Working Paper

No.524). The paper was prepared originally as a report for the

Bangladesh Financial Sector Review Mission. Many of the issues before

this mission and its objectives were similar to those which motivated

the author's earlier work. The current paper was therefore conceived

from inception as a practical application of this policy framework.

A distinction between empirical testing and practical

application needs to be borne in mind in reading the paper. The former

was not attempted, given the data limitations and time constraints under

which the paper was written. It is presented more as a practical guide

to others wishing to apply the siame framework in the context of similar

limitations.

Arvind Virmani

I. INTRODUCTION

1.1 Objectives - Explicit

The Bangladesh government has outlined three operational objectives

of financial policy. These are-I/

(a) Macro-Economic Objective:

To control the expansion of bank credit so as to contain inflation

while stimulating production and investment. As with most governments no

explicit trade-off is considered and the relative emphasis on one or other

sub-objective has varied with economic and social conditions.

(b) Credit Allocation Objective:

To channel credit into priority and essential sectors and away from

speculative activities and hoarding. Agriculture, small industry and exports

were the earliest sectors to be defined as priority sectors. The emphasis on

agriculture as a priority/essential sector has remained throughout. The

emphasis given to other sectors has varied however. Small industry expanded

to include small businesses and trade, new sectors like residential housing

and Transport were added and then detleted from the list.

(c) Institutional Objective:

To consolidate and strengthen the banking system, to provide new

financial institutions and to promote money markets.

1.2 Objectives - Implicit

Underlying these explicit or apparent objectives of financial policy

are deeper or implicit objectives which guide their application. This is

particularly true of the credit allocation and institutional objectives. The

implicit objectives are:

- 2 -

(a) Efficiency Objective:

To correct imperfections in the credit market which lead to

economically or socially inefficient use of credit. This clearly influences

the choice of sectors and borrower categories for both positive and negative

credit allocation measures. It also influences the institutional objectives.

(b) Welfare Objective:

To provide welfare subsidies to target groups, to transfer income

between different groups of borrowers, and to change the division of gains in

transactions between traditional lenders and borrowers.

(c) Subsidy Objective:

To correct imperfections or impediments in other markets, or to

mitigate these effects, by providing subsidies through the credit system.

1.3 Types of Policies

The most important financial policies used to meet the overall

objectives can be divided broadly into three groups. This is done on the

basis of the sub-set of the objectives they are primarily directed towards.

They can and often do have effects on other objectives, but it is useful as a

first step to make the categorisation, as follows:

(a) Credit Ceilings and Prohibitions:

These were directed primarily at controlling the flow of total

credit, but often have an allocation component. They include ceilings on

total lending by individual banks, lending to private and public sectors,

lending to different loan size classes, and lending for certain economic

purposes. The allocation component is designed primarily to countervene the

likely allocational impact of overall credit control policies.

-3 -

(b) Allocational Instruments-

These included lending targets and guidelines, margin requirements,

refinance policies, government guarantees, and linking to new urban and rural

branches. Specialized banks when coupled with refinance policy have been

another instrument for this purpose. Further the effects of refinance policy

have been most strongly influenced by the credit ceiling instrument.

(c) Int:erest Rate Policy:

Interest rate policies, including the use of penalty rates, of

course have the broadest ramifications. Ceillgns on (loan) interest rates

have been directed primarily towards the welfare and subsidy objectives. A

secondary objective has beenm the stimulation of investment. Interest rate

policies of course influence the allocation of credit, and the viability of

financial institutions. The use of penalty rates of interest on loan

overdues, has been used as an indirect means of couiiteracti g some of these

secondary effects.

1.4 Overall Allocation

The present paper focuses on the post 1975 period, and on the issue

of credit allocation. Clearly however issues can seldom be so neatly

compartmentalized. To the extent that Macro-economi and institutional issues

interact with credit allocation Issues they will be dealt with.

Table 1 gives an overview of the allocation of credit by broad

economic sectors. Over the period from June 1975 to December 1975 the

proportion of total advances to the agricultural sector rose from 10.8% to

18.6%, while those to manufacturin;v declined from 52.4% to 40.0%. The

proportion of advances going to the transport eector also showed a declining

trend while those to the construction sector in reased. The proportion of

advances going to wholesale and retail trade fluctuated considerably over the

Table 1: Sectoral Distribution of Advances by Scheduled Banks

Transport and Communications 4.49 6.17 6.96 6.77 6.59 6.68

Trade & Catering 8.73 10.00 9.86 9.85 10.80 11.05

Soulrce: "Bangladesh: Recent Economic Dlevelopments and Selected Development Issues,"' March 3, 1982.(This is an internal document with restricted circulation.)

Table 3: Credit Allocation Index; Ratio of Advance Proportions to GD? Proportions

1974-75 1975-76 1976-77 1977-78 1978-79 1979-80

Sector

Agriculture .172 .201 .222 .255 .306 .344

Manufacturing 7.865 6.403 5.330 5.922 5.635 5.520

Construction .168 .135 .207 .290 .628 .265

Transportation .793 .793 .565 .570 .549 .475

Trade 2.702 2.750 2.803 2,329 2.424 2.337

Source: Tables 1 and 2.

II. INTEREST RATE POLICY

2.1 First Major Revision

Table 4 gives an overview of changes in interest rate ceilings on

loans and advances. Over the period there have been two major changes in loan

interest ceilings. The one in May 1977 reduced the nominal ceilings on almost

all loans by one percentage point; from 13% to 12% on general borrowing and

from 11.5 to 10.5 on exports. The exceptions to this were the rates on Jute,

Jute goods and Tea and rates charged by the specialised banks and co-

operatives, which remained essentially unchanged. The effect of this way to

reduce the gap between the interest charged by these institutions and by

others, with the exception of the Bangladesh Samabaya Bank (BSB).

Interestingly BSB which makes medium to long-term loans retained a higher

ceiling rate of 13%.

The professed objective of this reduction in ceilings was to provide

a stimulus to economic activity, particularly to commerce and trade. Credit

ceilings had been in effect since the IMF borrowing in 1974-74. These had

been raised periodically. In particular they had been raised some months

before the lowering of the interest rate ceilings. Credit ceilings were

therefore not on effective constraint in the succeeding period. In 1975-76

and 1976-77 the implicit GDP deflator declined by 23.9% and 3.2% respectively

indicating a strong though decelerating deflation. In 1977-78 this process

was reversed by an inflation rate of 14.9%.

2.2 Second Major Revision

The other major change in interest rate policy occured in October

1980 (also Table 4). The effect of this set of changes was to differentiate

loan interest ceilings by economic sectors. Thus intra-sectoral rates were

unified while intersectoral ceilings were made different for agriculture and

Table 4: Interest Rates on Loans and Advances (Scheduled Banks)

Since Since SinceJuly 1974 July 1976 May 1977 1978/79 October 1980 1981

General Borrowers 12.0-13.0% * 11.0-12.0% * 15.5% 16.0(i.e. all those notseparately specified)

to the public sector Jute industry were rescheduled. This was followed in

1977-78 by rescheduling and restructuring of the debt of the public sector

Jute and Tea industry. This was done under the condition that the debt would

now be backed by government guarantees. The change in the nature of

securities therefore primarily represents a reclassification of this debt from

fixed capital as collateral to government guarantees as collateral.

2.5 Distributional Effects

The distributional effects of credit ceilings, arising from the

unequal distribution of wealth and consequently of collateral among households

are best demonstrated for the agricultural sector. In this sector there is a

high co-relation between the distribution of land and the distribution of

wealth. land is of course the best form of implicit or explicit collateral in

agriculture. In addition, productivity and credit requirements would also be

linked to the value of land. Therefore among the land owners we would expect

small landowners to obtain smaller loans, while most of the landless creditors

would fall in the smallest category.

Table 7 gives the allocation of credit to the agricultural sector,

by loan size. Between June 1.977 and June 1978 there was a sharp reduction in

the proportion of loans of less than TK 1000 from 36.6% to 28.9%. Some of

these were shifted into the next loan size category of TIC 1000 to TK 3000,

which increased from 32.7% to 36.2%. However the table of cumulative

percentages shows clearly the decrease in the proportion of total loans going

to smaller loan categories. As our analysis indicated this would be the

direct effect of a decrease in interest ceiling. A word of caution is in

order, however: As the loan classes are in monetary terms, a proportional

increase in the size of all loans, for example due to inflation, would shift

the entire distribution to higher loan sizes. This would result in a

- 16 -

reduction of the proportion of loans in the lowest and a rise in that of the

highest size classification. The proportions in the other loan size groups

would remain approximately the same. This is not however the pattern in Table

7. Otherwise a Gini type coefficient is to be preferred.

2.6 Speculative Credit

An analysis of pure speculative credit is somewhat different from

that of productive credit as applied above. The speculator/trader is assumed

to use his own funds as well as any borrowed funds for buying a commodity

stock. The return to this stock arises purely from the anticipated increase

in its price. In effect we separate out the productive aspects of trade from

this analysis. The traders own contribution or margin constitutes the

security or collateral as far as the bank is concerned. It can be shown that

a reduction in credit ceilings in this case will tend to eliminate credit for

the less speculative commodities: That is the commodities for which price

rises are expected to be low may not obtain any credit.

In tables 1 and 3 and the accompanying discussion it was pointed out

that the reduction in credit ceilings in May 1977 led to a downward kink in

the rising share of output-adjusted credit going to the trade sector. This is

consistent with the above analysis.

2.7 Interest Ceilings and Interest Subsidy

It is useful at this point to draw a distinction between interest

ceilings and interest subsidies. Both may be motivated by a desire to provide

subsidies, as for example the lower than average credit ceilings on Jute, Jute

goods and Tea and on other export goods which prevailed before October 1980

(Table 4). However they can have quite different effects on the efficiency of

credit use and on the distribution of credit. As already indicated interest

ceilings have negative consequences in both these cases. On the other hand,

- 17 -

that when the banking system is inefficient in allocating credit to specific

sub-sectors or sets of borrowers, an interest subsidy to the bank can remove

this inefficiency [see Virmani (1982)]. In such a situation an interest

subsidy increases loans to the neglected sector and to borrowers with

inadequate collateral (wealth). However this policy has not been tried in

Bangladesh.

2.8 Penalty Interest Rates

In February 1979 the government introduced a system of penalty rates

of interest on overdue loans. Scheduled banks were allowed under the system,

to charge a penalty rate of interest, which could be incremented by 1% every

month, until total rate (normal plus penalty) became 20%. The objective of

this penalty was to decrease the disincentive for lending to sectors where

repayment of loans has been a problem. Loan overdues can create a liquidity

problem in addition to reducing the expected return to the bank. As borrowers

who are delaying payments are likely to be the more risky customers it is

logical to charge them a higher rate. The penalty rate does this without

imposing a cost on good borrowers and is therefore an efficient mechanism for

doing so.

The application of penalty rates, particularly in agriculture, has

been somewhat erratic, with differeni: banks having different rules. Thus

Sonali bank charges the full penalty while BKB limits itself to a maximum

penalty rate of 2.5% and Pubali to 11'. It is also reported that in other

economic sectors, banks often charge penalty rates only to the public sector

borrowers and seldom to the private sector. However this is quite consistent

with the rationale given above, if the public sector is more erratic and

deficient in its repayment performance than the corresponding private sector

borrowers.

Table 8: Advances Classif ied by Rates of Interest All Banks(Percent of total Loans)

30-6-76 30-6-77 30-6-78 30-6-79 30-6-80

Interest Rate

110,0%: 0.19 0.28 0.15 6.79 0.12 0.11

10.5% 26.41 23.31 16.34 18.93 25.25 19,86

11.0% 1.78 1.68 3.49 6.79 7.40 10.20

11.5- 7.28 5.85 5.87 5.49 8;38 7.26

12.O% 16.10 15.66 41.52 38,39 38.10 37.56

> 12.0 to < 13.0% 2.37 2.53 1,32 1.19 0.69 0,53 H

13.0% 33.38 40.57 17.46 9.04 5.01 3.89

> 13.0% 0 0 0 0.07 3.80 3.29

- 19 -

Table 8, giving the disl:ribution of advances by rate of interest,

shows that the proportion of loans carrying a rate of interest rate of more

than 13% jumped from .07% of total advances in June 1978 to 3.8% in June

1979. They remained at approximately that level in June 1980. A small

proportion of these of course constitute high interest loans under the Rural

Finance Experimental Project. The rest are due to the use of penalty rates

and give an approximate measure of the extent of usage of such rates.

As late repayment is a major problem in the agricultural sector,

penalty rates will be discussed further under agricultural credit. Such rates

can be a very useful instrument of policy, when the repayment period is

carefully defined to take account of natural agricultural fluctuations.

2.9 Objectives and Effects of the Second Revision

Detailed data of the kind used above is not available for June , so

the effects of the October 1980 revision of interest ceilings are not fully

visible. However some preliminary conclusions can be drawn. As previously

noted this revision involved a change-over to a sectorally oriented system of

interest ceilings. This involved the setting up of an implicit hierarchy of

sectors; agriculture and exports are on top with a ceiling rate of 12%,

followed by manufacturing with a ceiling of 14%, while all other sectors have

a ceiling rate of 15.5%. Small loans and loans in less developed areas, which

do not fit into the sectoral classiLfication, fall between the ceiling rates

for the agricultural and the manufacturing sectors, with a ceiling rate of

13%.

There are two possible justifications for this hierarchy. One is

based on the supposition that production and investment are sufficiently

sensitive to interest rates, and that the economic rate of return has the

hierarchical pattern postulated. T'hrough a plausible case can be made for the

- 20 -

second proposition, the first is highly dubious. However even if it has some

merit it must be questioned whether the provision of implicit subsidies to

creditors is the appropriate means of providing incentives. Thus it is

necessary to look more closely at other policies, like exchange rates and

tariffs, which directly affect exports and manufacturing.

The other possible justification is to provide welfare subsidies to

target groups. Thus the largest numbers of poor are thought to be in the

rural areas, and lower interest rates to agricultural creditors may be thought

of as providing a subsidy. However even if these justifications are accepted

credit ceilings can have unexpected and harmful effects. To understand this

it is very important to draw a distinction between interest ceilings and

interest subsidies, and between cheaper credit and sufficient credit.

Many policy makers and even economic analysts may see the

differential interest rate ceilings as a cross-subsidisation scheme from

general creditors to farmers, exporters, small loanees and industrial

borrowers. This is quite misleading. A true cross subsidisation scheme would

involve an interest tax (or a tax per loan) on all bank lending to general

borrowers and an appropriate interest subsidy (or subsidy per loan) on the

favoured borrowers. This would provide the correct incentives for channeling

credit into the desired sectors. The effect of the differential credit

ceilings will be to redirect credit away from agriculture and exports and to a

lesser extent from industry into general lending. This perverse effect would

be accompanied by redirection of credit within each sector to those with

sufficient collateral and away from those with little collateral. Thus the

poor would tend to get relatively less credit than they would in the absence

of effective credit ceilings. Though adverse intersectoral flows may be

partly stemmed by forced lending through specification of targets, this has

- 21 -

its own limitations. Among these are ineffectiveness against adverse

distributional effects and the fungability problem (discussed in a later

section).

Two observed effects of the differential credit ceiling support the

above analysis. Firstly these havre a differential impact among the

Nationalized Commercial Banks (NCBs). A rise in deposit interest rates also

raises the interest costs of all banks, and may have a differential impact

across banks depending on the distribution of each bank's deposits.

Profitability is more strongly affected, however, by the sectoral distribution

of a bank-s existing loan portfolio. Thus the Pubali Bank which was strongly

oriented towards small loans, exports and fisheries will now earn 12% or 13%

on most of its loans. This has put a profit squeeze and provided a

disincentive to expand further into these sectors. Thus, it is being forced

to expand into areas of related expertise in industry and trade in which

higher interest rates are allowed.

A similar reduction in profits is taking place for the specialized

banks such as the Bangladesh Krishi Bank (BKB). Though the rise in deposit

rates affects only a small fraction of its funds, the relative profitability

of agricultural lending vis a vis agriculture related commercial lending has

declined. Given that in 1979 approximately 70% of its loans went to

agriculture the lower interest rate of 12% on such loans puts a profit squeeze

on the BKB (discussed further in agricultural section). As a result the BKB

is planning to reduce the proportion of agricultural loans to 60% and to

expand faster into sectors like agro-industries, storage, transport and

banking to which higher credit ceilings are applicable.

- 22 -

2.10 Intra-Bank Lending Rates

The rates charged by banks on their internal transfer of funds

between branches and between branches and headquarters are of course not

directly relevant to final borrowers. They affect the incentive structure of

banks, however, and can affect credit flows to final borrowers. For

commercial banks, these rates vary from 11% to 14% at the present time, as

shown below

Bank Headquarters to Branch Branch to Headquarters

Sonali 11% 11%

Janata and Agrani 12% 12%

Pubali 14% 13%

Thus Pubali bank branches have clearly no incentive to borrow funds from

headquarters for lending to agricultural and export sectors (12%) and for

socioeconomic purposes (13%), and little incentives for lending to industry

(14%). If the average administrative costs for all lending operations (1 to

2%) are taken account of, even Sonali bank branches have little or no

incentive to borrow internally for lending to these sectors.

Banks should of course be free to set intra-bank lending rates

according to their particular circumstances. Given the current structure of

interest rates, however, we can calculate the approximate range in which these

rates should lie. The average interest cost of deposits is currently about 7%

of total business. The average administrative costs of lending are about 4%,

though the administrative costs of rural lending by commercial banks are

somewhat higher at about 5%. As the lowest loan rate is 12%, and taking the

4% cost as divided equally between the deposit and lending sides intra-bank

lending rates should be approximately 9 to 10%.

- 23 -

2.11 Real and Nominal Interest Rates

The anlysis presented in this chapter, as in the rest of the paper,

is in nominal interest rate terms. Given the established practice of using a

rate constructed by subtracting actual or expected inflation from the nominal

rate (the 'real' rate) this requires an explanation. The framework on which

the analysis of the paper is based, divides the basic financial market into

two submarkets: The deposit marlket and the loan market. The former is

supplied with funds by depositors and has banks as demanders of funds. In

conventional terms this is the savings side of the market. When savings are

treated in aggregate clearly a 'real' rate of interest must be used in the

analysis. If deposit markets are perfect, changes in the rate of inflation

have no effect on aggregate saving. If deposit rates are controlled by the

government, however, changes in ithe rate of inflation will influence both the

total amount of savings and the amount flowing into deposits. This in turn

will affect the opportunity shadow cost of funds to the banks (termed s in the

present paper).

our analysis focuses on the loan sub-market. The shadow

(opportunity) cost of funds (s) is of curse an input into this market. In the

loan market, competitive banks will make a loan to a borrower as long as their

expected profits are positive; the loan amount, the loan interest rate and

other variables are all expressed in nominal terms. The firm similarly

maximizes its expected profit evaluated in nominal terms. In deciding whether

to take a loan or not it merely compares these net profits with the nominal

opportunity cost of own funds. The terms of the loan contract, including the

loan interest rate, will differ for firms with different characteristics (e.g.

returns). The allocation of loans will therefore be determined by the

distribution of these characteristics across firms. If we compare two

- 24 -

situations; one in which all prices are double that in the other, there is no

reason to expect any difference in the distribution of these characteristics

across firms. Therefore the allocation of credit should not be affected if

other things remain unchanged.

If the deposit interest rate is controlled, however, the flow of

deposits into the banking system might fall. This in turn would raise the

shadow cost of funds to the banks. Our analysis shows that in this case loan

amounts must fall and loan interests rates rise for every existing borrower.

In addition collateral requirements may rise or fall for each borrower, and

this could affect the distribution of loans. Without more detailed

information, however, it is not possible to determine the direction of change

for any particular borrower. The first order approximation is therefore to

assume no effect of inflation on credit allocations; the analysis can be

carried out in nominal terms.

III. CREDIT ALLOCATION POLICY

3.1 Overview

Several different policy instruments have been used for different

sectors at different times. Among these are targets, prohibitions and

ceilings, margin requirements, refinance or counter finance, guarantees and

urban-rural branch approval. One way of organizing these instruments is in

terms of positive and negative instruments. The negative instruments are

designed to reduce or eliminate the flow of credit to certain individuals or

for certain purposes. Ceiling and prohibitions and margin requirements fall

into this category. The positive instruments are designed to channel the flow

of credit into specified areas. All the other instruments mentioned fall into

this category. Logically of course the categories are complementary in the

- 25 -

sense that if a negative instrunient is successful it must have a positive

aggregate effect on the unspecified areas, and similarly for a positive

instrument.

The banking system (i.e. the financial system excluding the Central

Bank and the government) can be conceptually seen as having an inflow of funds

on the deposit side and an outflow of funds on the loan side. In other words,

instruments can be classified in terms of how far they are from the final

borrower. Right on the outflow side are instruments like lending targets,

lending ceilings and prohibitions, exemptions from overall credit ceilings,

and margin requirements. In the middle are collateral guarantees and urban-

rural linked branch expansion. Farthest away, on the inflow side, are

instruments like refinance and liquidity guarantees.

3.2 The Target Approach

Loans to small businesses, small loans and exports were the earliest

to be designated as priority sectors (1973). In February 1975 banks were

notified that the small loan category be given priority in any credit

allocation following from an increase in deposits. In September 1975 a

lending target of TK 1 crore per bank was fixed for nationalised commercial

banks' lending to this category. During the same financial year (1975-76)

restrictions on housing loans were lifted.

In 1976-77, deposit-linked targets were imposed on each nationalised

commercial bank. The targets were 1 1/2% of deposits (as on June 1976) to be

loaned to the small loan category, 1 1/2% to the transport sector, and 1% of

deposits for residential housing. Informal guidelines were also issued for

increased lending in less developed areas at a controlled rate one percent

below the general interest rate ceilings (i.e. initially at 12%). In 1977-78,

the loan target for small loans was raised to 2% and maintained at that level

- 26 -

for the next three years. In contrast, targets for house building and

transport were maintained at the same level in 1977-78 and then eliminated the

following year. In 1977-78 loan interest ceilings of 11% on loans for rural

housing and 5% on loans for multistoried buildings were imposed. These

compared with the general ceiling of 12%.

Table 9 shows, for the three nationalised commercial banks the loans

made to the three targeted sectors as a percentage of their total loans and as

a percentage of target. The data for the three banks suggest that banks were

quite successful in meeting the small loan targets, but not those for housing

and transport. There is some variation among banks however: Sonali bank was

successful in small loans and unsuccessful in the other two; Agrani bank was

successful in transport and partially unsuccessful in small loans and housing;

and Janta bank was successful in both small loans and transport.

This variability in success (as measured against targets) suggests

that it is not useful to impose uniform targets on banks. Each bank has its

own special orientation and expertise. Given the different sources of

information and information links the banks would tend to specialise in

special segments. Uniform targets reduce the flexibility of the system. A

recognition of this probably lead to the elimination of targets on house

building and transport loans after a trail period of two years.

Table 9 also gives the allocation of credit to each priority sector

as a proportion of the total advances of each bank. In table 1, the share of

advances of all scheduled banks going to the transport sector showed a

declining trend over the 1978-80 period; it went from 4.3% in 1975 to 3.1%. in

1980. The allocation of credit by the three commercial banks in table 9, is

_ 27 -

Table 9: Advanees to Small toans rnd Smatl Tndtstry. HouRse Pu1ldfnr andTransport as a proportion of targeted amounts - Three Banks

kec. 1975 Dec. 1976 Dec. 1977 Dec. 1978 Dec. 1979 Dec. 19801. SONALI BANK (S)

Small loan. and small lndustryAs a percentage of total advanceti 2.19 2.o9 2.44 2.72 2.43 2.25As percentage of target: N.A. 701.00 126.56 109.51 97.82 98.80

House Building

Percentage of total advances .07 .17 .46 .74 .64 .54Percentage of target IIA. N.A. 36.46 59.55 N.A. N.A.

Trans porlt

As a percentage of total advanceo .82 .89 .71 .94 .49 .37As a percentage of target. NA. N.A. 36.89 50.26 N.A. NA.

2. AGRANI BANK (A)

Small loans

As a percentage of total advanceis .80 1.91 3.63 2.43 1.61 1.38As a percentage of target N.A. 291.00 201.18 95.67 62.47 53.15

Rouse Building

As percentage of total advances a .07 .91 1.29 1.26 2.13As percentage of target N.A. N.A. 75.34 101.48 N.A. N.A.

Transport

is percentage of total advance. * 1.14 1.18 1.27 1.00 1.10as percentage of target N.A. N.A. 65.54 67.02 N.A. .A.

3. JANATA BANK (J)

small Loans

As percentage of total advances .0 1.71 1.87 2.59 2.19 *As percentage of target N.A. 608.00 117.91 129.77 112.09 a

Rouse Building

As percentage of total advances a * * .89 1.56 *As percentage of target N.A. N.A. C 89.03 N.A. N.A.

Traaport

As percentage of total advances 2.72 2.11 1.89 1.92 1.91 aAs percentage of target N.A. N.A. 118.89 128.67 N.A. N.A.

4. ThREE BANKS (S. J, A)

Smll Loana (S, J, A)

As percentage of total advances .96 1.45 2.43 2.61 2.18 aAs percentage of target V.A. 364.00 138.58 114.02 95.71 a

House building (S & A only)

A percentage of total advances a .13 .63 .93 .83 .98As percentage of target N.A. N.A. 49.97 74.09 N.A. N.A.

Transport (S, J, A)

As percentage of total advances a 1.52 1.33 1.42 1.16 aAs percentage of target N.A. N.A. 75.84 83.04 N.A. N.A.

N.A. a Not applicablea - Data not availableSorce: Annual Reports of the respective banks

- 28 -

broadly consistent with this trend. It can be concluded therefore that the

setting of a formal lending target for the transport sector had little effect

on this down-trend.

Loans for housebuilding, by Sonali and Agrani banks, rose fairly

rapidly from 0.13% of advances in December 1976 to 0.93 of advances in

December 1978 (Table 9). This rising trend was maintained by the Agrani Bank

during the next year, while that of Sonali Bank was reversed leading to a

i small overall decline. Clearly the increase is not solely due to targeting

policy, as the removal in 1975-76 of restrictions on lending to this sector,

would have led to some re-allocation towards it.

The earlier analysis of loan rate ceilings also suggests that

differentially lower ceilings on rural housing loans (-1%) and multistoreyed

housing (-6%) might have been responsible for breaking the uptrend in housing

loans. However rural housing loans were an insignificant part of the

institutional loans for housing, before the special scheme was introduced in

1977-78. Similarly multistoreyed housing is a relatively new phenomenon in

the housing market and would not have had an immediate impact on total housing

credit. This is consistent with the different effect on the three banks.

I have shown elsewhere [Virmani (1982)] that there are certain problems

of information flows and interpretation which can lead to inefficiency in the

form of exclusion of certain types of borrowers and certain types of economic

activity. The analysis suggests that there may be a discrepancy between the

social and private returns to loans which requires a short term subsidy to the

banks. It is also suggested there that the subsidy will (probably) have to be

linked with a requirement to lend to the identified borrower categories. Any

element of forced lending, must however be only for a short introductory

period. This induces banks to collect information and generate links with the

- 29 -

neglected sector, a kind of forced learning by doing. A policy of

targeting/guidelines when accompanied by appropriate incentives can therefore

be justified for short periods for new and unfamiliar activities. Thus the

initial success in increasing the share of house building loans may have been

partly due to the guideline targeting approach.

This analysis is also supported by the differential performance of

banks in terms of loan share of the small loan category. Thus targeting had

little effect in the case of Sonali bank which already had a proportion of its

advances going to this sector, and already had information links. On the

other hand the Agrani and Janata banks had only .8% and 0% respectively of

their loan portfolio going to the small loan category on December 1975. This

had increased to 3.63% for Agrani by December 1977 and 2.59% for Janata by

December 1978. In both cases it declined after the peak. Three years in one

case and four years in the other was probably more than enough time for the

initial information links and learning to take place. Normal criteria would

eventually begin to apply. Thus the final stable level of lending to this

sector represents a relatively efficient level of lending compared both to the

low initial levels as well as to the peaks reached under pressure.

In 1979-80 banks were asked to raise their credit deposit ratios in

less developed areas, including the Chittagong Hill-Tracks to 75%. It is

highly unlikely that general development problems can be addressed solely or

even primarily by forced lending. Widespread experience, including that of

many banks in Bangladesh, indicates that a package of inputs and programme

(technology, marketing etc.) is necessary. Moreover with the interest changes

in October 1980, interest ceilings for these areas are at 13%, that is 2.5%

below the general rate. This provides a disincentive to bank lending.

Further as the target is linked to deposits from the same areas, if the target

- 30 -

is forcefully imposed, this would also provide a disincentive for raising

deposits from these areas.

A target of 1% of bank deposits for lending for non-traditional

exports was introduced in 1979-80 and continued thereafter. Policies directly

related to export profitability need to be examined very carefully as

suggested in the introduction. If there are also information problems in

export lending, guidelines and targets can be useful for a few years if

accompanied by adequate incentives. However from October 1980 the interest

ceiling for export lending at 12% was 3.5% below the general ceiling.

Informal targets were also set for agricultural lending. However as

target setting was not the major policy tool for agriculture, credit to this

sector will be considered in the section of the primary policy tool used.

3.3 Ceilings and Prohibitions

In the pre-1975 period of high inflation, there were many

restrictions on the use of various types of financial securities, capital

equipment and real estate as collateral. These were gradually lifted. In the

absence of interest rate ceilings such restrictions tend to raise interest

costs to borrowers (see Virmani 1982). Thus credit would be shifted from

those borrowers whose interest rates were previously against the ceiling to

those who were below. The latter would now be paying higher rates but getting

relatively more credit. Inefficiency is increased and credit tends to shift

from unfamiliar, more risky borrowers to familiar less risky borrowes as

perceived by the bank. Such restrictions would also tend to shift credit from

productive to speculative purposes as the latter are less likely to be based

on explicit collateral than on implicit collateral; for example, the margin of

stock value constituting the borrowers equity in a commodity stock. Implicit

collateral (e.g. the value of accounts receivable) can of course be used even

- 31 -

on production loans; but this is done only for a bank's best or prime

customers.

The most widely used ceilings, usually in times of general

inflation, are those on credit to large borrowers, or to all borrowers. Thus

for example in February 1979 banks were exhorted to limit credit to borrowers

and reduce it where possible. Later in the year inventory norms were set and

the banks were told to reduce credit gradually in accordance with these

norms. The objective was to reduce credit to those with high inventories and

large credit. For producers this acts basically as a loan amount ceiling. In

December 1979 formal ceilings were imposed on all borrowers. Industrial

borrowers were limited to 90% of their maximum outstandings in the previous

year. Traders were limited to 85% while export finance, term finance and

special programmes were exempt. In August 1980 the cuts were withdrawn.

Though credit ceilings are usually used for controlling general credit

expansion they have allocational effects which are the primary focus of our

paper. Credit ceiling may also be applied selectively; to mitigate the harsh

effect of general ceilings on particular sectors or borrowers. To this extent

they can be seen directly as an allocational instrument. I have shown

elsewhere (Virmani, 1982) that ceilings on loan amounts to producers, when

effective, reduce the cost of loans to the borrower, through a lowering of

interest rates. Further they are likely to be more effective against the

larger, more organised better placed borrowers, mainly because they are easier

for a government to police. Thus they are likely to have perverse welfare

effects within the set of borrowers. When applied to all existing borrowers

they are likely to channel loans away from current borrowers to new less

productive borrowers. When applied to a subset of borrowers they will tend to

shift credit to those not subject to these restrictions, while lowering

- 32 -

interest rates to the former. But a better way of rechanelling without

adverse distributional effects is to put an interest tax on lending to non-

favored borrowers. Overall efficiency in use of credit will deteriorate under

both policies, unless all favored creditors were previously getting less than

the efficient amount of credit. This is unlikely to be true.

Loan ceilings on credit which is going into stocking for speculative

purposes has somewhat different effects. In this case it can be shown that an

effective ceiling on loan amounts per borrower will increase the interest rate

on loans. However if these rates cannot be raised because of interest rate

ceilings then no loans will be made to the potential borrowers. Loan ceilings

can therefore be useful in this case if they are effective.

3.4 Margin Reguirements: Overview and Analysis

In Bangladesh, as in many other countries, government setting of

minimum margin requirements have been used primarily as an instrument for

controlling "speculation and hoarding", in specific commodities. Thus they

were in most active use when prices of particular commodities considered to

have large adverse social consequences started to rise very rapidly. Among

the specific commodities have been rice and paddy, sugar, oil and oil seeds,

jute and jute goods, onions and chillies, salt, cotton yarn and textiles, and

synthetic yarn and textiles.

As shown in Table 10, at the start of the period under consideration

the margin requirement on Jute and Jute goods was implicitly 100% as all

lending for this purpose was banned. This was motivated by the high rates of

growth of prices, which rose by 63% in 1974-75. As price growth eased to 4.4%

in 1975-76, credit was allowed to this sector. However a sharp rise of 40% in

the prices of these goods in 1977-78 following on the heels of a rise of 11%

the previous year does not seem to have led to an increase in margin

Table 10: Rate of Growth of Prices and Imposition of Margin Requirements (In percentages)

1974-75 1975-76 1976-77 1977-78 1978-79 1979-80

1. Jute and Jute GoodsMargin 100. 0(?)Rate of price growth 63.00 4.37 11.32 39.99 1.18

Mustard Oil Prices (Rate of Growth) -32.18 -15.00 35.20 -0.20

5. Cotton, Yarn & Textiles and 50 0 50Synthetic Yarn & TextilesRates of Growth in;Sari Prices -0.47 -1.45 10.65 26.49 2.81WPI for Manufactures 49.73 -43.07 -2.63 5.97 7.41

6. General Merchandise TradeMargins 0(?) 50 60

Rate of Growth ofCOL Index for Middle Income Groups 67.17 -8.40 2.40 12.60 8.30 18.50COL Index for Non-Food 52.10 11.40 4.40 9.50 9.30 14.60COL Index for Food -16.00 1.05 15.64 6.80 20.96

a/ There were informal guidelines in margins during this period.b/ Informal norms were prescribed to banks.

Sources: Resume of Financial Institutions, Finance Ministry, Various Issues.Bangladesh Bank, Annual Reports.Statistical Absgract of the Bangladesh (-ov,rnmnt.

- 34 -

requirements. Thus the use of this instrument seems to decline over time,

perhaps corresponding to a decline in concern over hoarding. Similarly the

margin requirement of 50% on advances against salt was accompanied in 1974-75

by rate of growth of 751% in salt prices. These margin requirements were

eliminated the next year as prices fell by 66.8%. Guidelines were issued in

1976-77 as prices again rose by 20.5% and inventory-credit norms were

established the following year. The sharp decline of 18% in salt price in

1978-79 led to some positive credit measures. Lending, for sugar alloted by

the food department, could be done at 50% margin in 1977-78. As sugar prices

were controlled throughout the period, the best available (though imperfect)

measure of tightness or rationing in the sugar market was gur prices

(jaggery). Thus gur prices, after falling by 21.1% in 1976-77 increased by

1.6% in 1977-78 suggesting a corresponding increase in demand pressure

relative to supply in the sugar market. This is confirmed by the still higher

price rise of 12% in gur prices in 1978-79.

Credit margins on borrowing by oil mills against local oil seeds and

oils were put at 50% in 1977-78. Similarly a 25% margin requirement was

specified on imported oils and oil seed during the same year. Prices of

mustard oil, which constitutes the most important local oil, provide the

answer. Price declines of 32% and 15% in 1975-76 and 1976-77 were followed by

a price rise of 35% causing alarm to the government. A decline of 0.2% in

mustard oil prices in 1978-79 led to a removal of margin requirements on

imported oils and seeds and a fall in margin requirement to 50% on finished

products of oil mills.

Margin requirements seem to have been directed primarily against

agricultural commodities, and within that primarily on goods of common

consumption. Thus, for example, lending to private rice and paddy traders has

- 35 -

been banned for most of this period, giving an effective margin requirement of

100%. The other major good in the consumption basket is clothing. As we

might expect both cotton yarn and textiles and synthetic yarn and textiles

have been subject to margin requirements (Table 10). The early period also

witnessed wider use of margin requirements on industrial inputs suggesting use

of margin requirement as a more general credit control and inflation fighting

device. As recently as 1978-79 margin requirements on general merchandise

trade were raised from 50% to 60%, following observation of accelerating

inflation in 1977-78 and 1978-79 (Table 10).

Before determining the effects of this policy instrument in

different contexts, it is useful Ito analyse the effect of margin requirements

in a simplified context. Consider a situation in which credit is being used

purely for speculative purposes, that is to buy and hold commodity stocks in

anticipation of a price rise. Consider a bank and a speculator who are

neutral in their attitude to risk and are therefore interested only in the

expected returns. To begin with we assume that the speculator has a fixed

amount of outside funds or equity available to him for purchase of

commodities. Given this equity, we can define a loan supply curve for each

borrower-lender pair which is limited at one end by the condition that banks'

have positive expected profits. The speculator's demand curve is perfectly

elastic; if at any interest rate it is profitable for him to borrow it will be

profitable to borrow an infinite amount. Thus a 'rationing equilibrium' can

emerge as shown below (r*, L*), if banks act competitively. In such a

situation, if government imposes a margin requirement m (m > e which ise + L* e wi is

effective, it is equivalent to a loan ceiling

- 36 -

Figure 1

LS

L~~~~~~~~~~LE ~ ~~~~ X

, .~~~~~~~~~~~~~~~~~~~~.

1~~ e

L = e (--1) (from m = e+ L , e is the value of the stock). As shown in the

ceilings exist, and the new interest required is higher than these ceilings no

loans will be made.

Even when the effect of government imposed margin requirements falls

on loans for productive purposes, it still acts as a loan ceiling. The effect

of loan ceilings has been shown above (section 12). When commodity stocks are

used as collateral by producers, the ratio of the loan value to the collateral

is of course referred to by banks as the 'margin'. This ratio, or bank set

,margin requirement' will, in general, be different for different producers,

even for the same collateral commodity. This is because the returns from and

riskiness of the productive activity in which the loan is used varies across

borrowers. All the terms of the loan contract will therefore differ: more

productive borrowers will obtain better terms than less productive ones. This

will tend to result in lower effective margins for the former than for the

latter.

Returning to the case of speculator borrowing, the speculator's

equity contribution may not be fixed as assumed. If, instead, the speculator

has a rising marginal cost of equity funds, similar results are obtained. The

- 37 -

only difference is that an effective margin requirement raises the marginal

return to speculator equity and therefore brings forth additional equity funds

into speculation. As a result interest rates do not rise as much as in the

fixed equity case, and the number of eliminated borrowers will be smaller.

Thus effective margin requirements can reduce the flow of funds for

speculative purposes and raise the cost to current borrowers.

3.5 Margin Requirements: Differential Impact

In Table 11 and 12 we present data on the distribution of credit by

margin requirements for some of the commodities reviewed above for which data

is available for the relevant time periods. These statistics relate to

Nationalised Commercial banks (NCBs). The results for sugar, and oil and oil

seeds are broadly consistent with the above analysis. Thus for sugar the

imposition of a 50% margin requirement in April 1978 resulted in a substantial

change: Between June 1977 and June 1978, the proportion of credit with no

margin requirements, went from 84% to 53%, while that with 50% margin

requirement went from 5% to 28%. This was accompanied by an increase in

proportion of credit subject to 25% margin. As this credit includes credit

going to public sector sugar mills, this represents a fairly effective

shift. This shift in the allocation of credit by margins was accompanied by a

fall in loan size per borrower from TK 6280 to TK 1040. Total loans against

sugar also declined from TK 408 thousand to TK 281 thousand. Both these are

consistent with our analysis.

By June 1979 however virt:ually no loans were at 50% margin, with

about 90% of the loans being at margins of 25% or less. The average loan size

had increased back to TK 5820, evert though total loans against sugar were

still at a reduced level of TK 245 thousand.

- 38 -

Table 11: Distribution of Advances by MarpinR for Specified Securities, and Average Loan Sizeby tlrgl, for saae Seeurities

1/ It is not entirely clear from the data whether disbursements are for agricultural credit alone or alsoinclude trade, storage marketing of agricultural goods.

Source: Bangladesh Bank, Annual Reports

- 49 -

sanctions for the first time and in 1980-81 this reversal become more

pronounced. This peculiar situation arises because of delay in disbursement

of loans committed in the previous year.

The proportion of refinancing actually provided can be measured

approximately by the loans disbursed by the Central Bank divided by the

entitlement, as measured by the agricultural banks advances for the year.

These rise to a peak of 117% in 1977-78 and then decline to 79% in 1980-81.

Because of the carry-over of previously committed loans and the partial carry

over of previously sanctioned loans, a better (but still approximate; because

of the abrupt start at 1974-75) measure is the cumulative disbursement divided

by the cumulative entitlement. This shows refinance proportion rising from

87% in 1975-76 to 101% in 1977-78, suggesting that most backlogs were cleared

by this time. Refinance remained aLt the fairly high level of 96% in 1979-80

but fell sharply to 90% in 1980-81. This suggests that even though actual

refinancing by the Bangladesh bank may have fallen below 100%, due to the

application of constraints ona general credit expansion, the goal remained at

100%. In contrast, in 1979-80 and 1980-81 loan sanctions are actually below

loan entitlements for the first time, suggesting an implicit movement away

from the goal of 100% refinancing of agricultural banks.

The commercial banks, and the BKB for its non-agricultural lending,

are entitled to refinance on a wide variety of items. The current rates of

refinance are as follows:

Food and Fertilizers (BADC), Petroleum and Petroleum Corp. 100

Exports Non-Traditional 100%

Traditional 50%

Small Loans 0% (100% until late )Sugar 50%

Jute 50%

SACP 50%

- 50 -

The refinance rate for the special agricultural programe (SACP),

like the agricultural lending of BRB and BSBL, carried a 2% subsidy on the

Bangladesh bank rate. All other sectors got refinace at the discount rate

which was 8% between June 1974 and October 1980 and 10.5% thereafter (Table

4).

The total amount of refinance taken under these catagories rose

steadily from 251.53 lakhs in 1979 to 703.88 lakhs in December , a growth of

180%. The annual compound growth rate from June 1979 to June was 67% a year,

representing a fairly substantial increase in refinance. Jute was the largest

user of refinance throughout the period, but grew by only 23.5% from 119 lakhs

in June 1979 to 146.98 lakhs in December . Refinance to the petroleum

corporation started in December 1979 and has been the second largest since

December 1980. Food and fertilizer have changed places for the next position.

Given the diverse items for which refinance is provided it is useful

to look at some of the explicit and implicit objectives. Both food and jute

are subject to annual fluctuations in production. Refinance is seen as a

means of providing credit for holding stocks in a deflationary situation. Our

earlier analysis of speculative credit suggests that commercial banks would

tend to provide little credit in this situation. But this question really

needs to be looked at in terms of the buffer stocking policy of the

government. Macroeconomic issues are also important. A properly worked out

buffer stocking policy would trade off sectoral effects and macro economic

effects, and work out a self supporting buffer-stock policy. Any desired

subsidies, should in general go direct to the producer and not to private

traders.

Sugar production has a strong seasonal pattern. Both lender banks

and potential borrowers know that prices will fluctuate in a seasonal pattern

- 51 -

over the year. The analysis of speculative credit does not indicate that

banks will not provide credit in this situation. However a seasonal buffer

stocking policy which is self-supporting could be worked out if necessary. If

it is thought necessary to provide subsidies to producers or consumers these

could be provided directly.

Provision of refinance to the petroleum corporation is used

essentially to fill the gap between the rise in oil prices and the rise of

final product prices. Thus it can be seen as a means of providing a

consumption subsidy to oil consumers. Even if such a subsidy is to be given

there does not appear to be significant reasons for using the banking system

for this purpose. The provision of refinance to BADC for fertilizer has a

completely different purpose. Subsidies are provided explicitly through the

budget: Delays in receipt of the subsidy or short term liquidity problems are

however met by providing 100% refinance to banks for their lending to BADC.

This appears to be a more satisfactory method for achieving a similar purpose.

In the case of non-traditional exports information problems can

effect the flow of credit, as I have shown elsewhere (Virmani 1982). A

determination must be made, however, whether this is the primary, or even a

major problem. This requires a prior examination of the foreign exchange

markets and the policies which impinge directly on exports and imports. In

addition one should also look at more general agricultural or industrial

policies which impinge on sectors which are potential exporters. Given

appropriate policies in these areas, credit policies can be used to remove any

inefficiencies in loan markets. These generally relate to new export products

with which bankers are unfamiliar. Credit policies when used for an initial

period can be useful in removing inefficiences.

- 52 -

3.7 Refinance Usage, Incentive Effects and Usefulness

The use of refinance policy as an instrument for redirecting credit

allocation can be examined in the context of the analysis in Virmani (1982). We

start by considering the simplest case of a perfect deposit market, in which a

bank acts as a price taker at a deposit interest rate of i (a more realistic

case is considered below). Let the refinance proportion be h and the

refinance rate p. If the refinance rate is greater than or equal to the

deposit rate, no refinance would be availed of and refinance provides no

incentive. If the refinance rate is less than the deposit rate, the cost of

funds for the refinanced sector becomes i = hp + (1 + h)i which is less than

i the deposit rate. I have shown that the direct effect of this is to

increase loan amounts and reduce interest rates to borrowers. Loans would

also be made for the first time to previously marginal potential borrowers.

Both these would shift credit allocation towards the refinanced sectors.

If interest ceilings exist, the effect of refinancing is to reverse,

partially, the harmful effects of such ceilings. The lowering of the 'free'

interest rate on loans means that on the margin borrowers are shifted from

having an effective credit ceiling to not having one. The effect of refinance

policy on collateral requirements is uncertain, as these may rise or fall. For

those borrowers who are still constrained by the loan interest ceilings, the

adverse distributional consequences of interest ceilings on the poor (little

wealth), may be countered or enhanced by refinance policy.

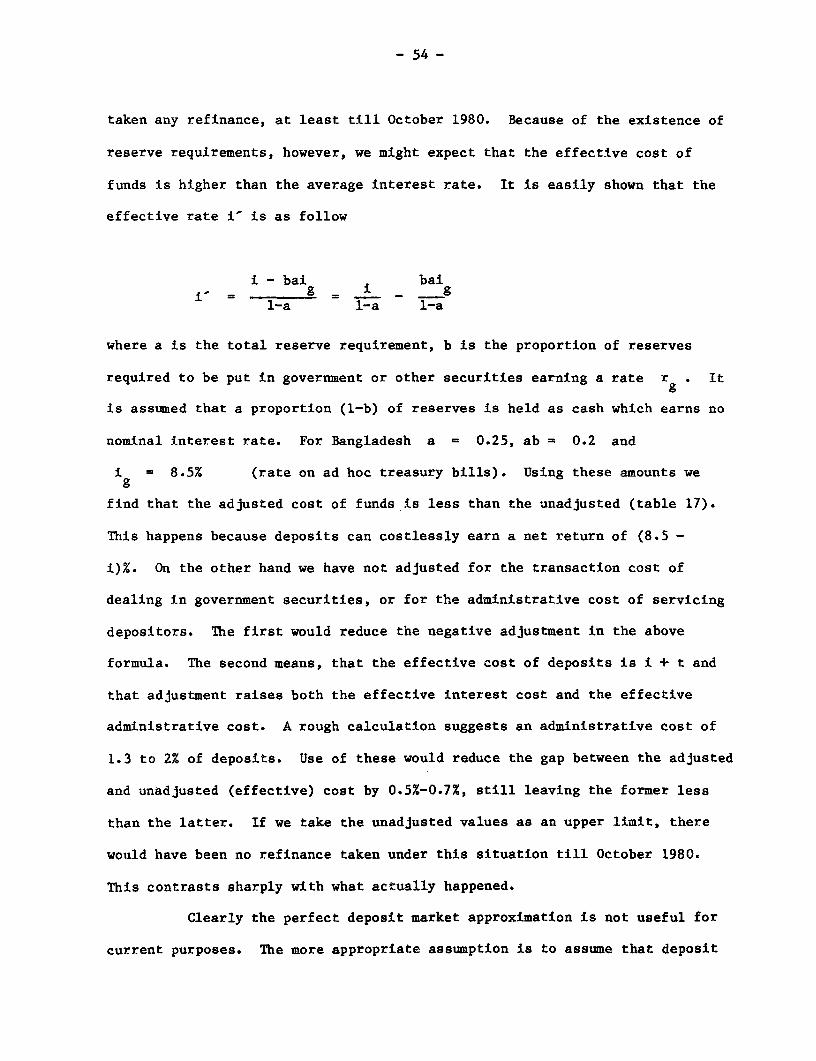

Table 17 gives the average weighted deposit costs over the period.

The refinance rate for the agricultural banks has been 6% since 1974. (The

refinance rate is of course 8.0/10.5 for the other sectors). This compares

with a interest rate of 3.5 to 4.3% till 1980 and 7.0% in respectively.

Under such a situation our analysis suggests that these banks would not have

Note: The national average for the size of business of a Sonali branch was16,669 (Thousand Taka) in 1979 and 19,164 (Thousand Taka) in 1980; theadministrative cost as a percentage of business was about 1.8% for thetwo years.

* Computed from a sample of 10 rural branches that have been inoperations since 1978 or earlier. -

** Size of Business is defined as the sum of total deposits andoutstanding advances.

Table 23: Sonali Bank Statistics(in 1000 Taka or p.9 as applicable)

these branches. If rural branches were transferred to BKB the primary

responsibility for providing funds; to BSBL and IRDP would be transferred to

BKB.

An alternative method for linking the flow of funds to agricultural

banks with rural deposit mobilization is to make it mandatory for nationalized

banks to transfer all excess reserves from their rural operations to BKB, BSBL

and IRDP. This transfer would be in the form of loans at rates which take

account of interest payments and administrative costs. In other words BKB,

BSBL and IRDP would have the right to borrow from the NCBs the difference

between the loanable funds generated by rural deposits and the loans made in

rural areas. This proposal is likely to be more acceptable to NCBs, but more

difficult to implement because of the problem of defining rural areas and

rural loans. Some mix of the two maethods may prove to be more feasible.

4.5 Buffer Stocks: Alternative for Margin Requirements and Refinance

When analysing margin requirements it was suggested that they may be

useful for agricultural commodities. As buffer stocks fulfill the same price

stabilizaton function it is useful to briefly consider the two together. As a

general principle buffer stock policy is more relevant for commodities whose

prices fluctuate regularly on a seasonal and/or annual basis. Margin

requirement changes are more appropriate for unexpected and temporary changes

in prices. Put somewhat differently buffer stocks are more appropriate when

production fluctuates from year to year or when havesting is concentrated at

one point in a year, resulting in a strong seasonal fluctuation in prices

(i.e., demand is uniform). Margin requirements are more appropriate when

unexpected economic events lead to strong speculative demand.

Buffer stocking and refinance are not as clearly separable. Buffer

stocking would itself give rise to a cyclical, seasonal or annual, pattern of

- 80 -

demand for credit. In the seasonal case the cycle is exactly the inverse of

the demand for credit for agricultural production of the corresponding

commodity. Therefore if both sets of borrowers were supplied from an

integrated financial system, cyclical demand fluctuation would be eliminated

and there would be no need for special refinance. On the other hand annual

cycles would still lead to annual fluctuation in credit demand from the

stocking agency. If the buffer stocking operation is self supporting (after

taking account of explicit budgetary subsidies) the banking system woud

generally be willing to supply the required credit.

4.6 Term Finance

In the agriculture area there is strong push for providing medium,

and long term finance for irrigation improvement. In industry the specialised

banks, Bangladesh Shilpa Bank (BSB) and Bangladesh Shilpa Rin Savings (BSRS),

are there specially for providing term finance. I have shown elsewhere that

term lending creates special problems for banks because of the difficulty of

distinguishing between productive and unproductive, and honest and dishonest

borrowers. Both problems have arisen in the case of term lending for

industry. Industrial lenders can borrow up to 70% of the cost of a new

project from BSB. Additional loans of up to 15% can be obtained from ICB and

IFC. By inflating the cost of imported machinery (overinvoicing) and of land,

and covering the difference from the public (shares) the promoters can end up

by not using any of their own funds. Thus they may have little commitment to

the success of the project, resulting in poor repayment performance.

As I have shown it is necessary in such situations to develop

procedures for distinguishing between productive and honest borrowers and the

rest, and restricting loans to the former. A World Bank research project on

Kenya is attempting to develop such procedures. Similar work has also been

- 81 -

done in a neighboring country. Use should be made of these and other

attempts, to do the same thing in Bangladesh. Other suggestions are made in

the financial review of Industrial Sector lending.

V. AGRICULTURAL CREDIT

5.1 Introduction

The explicit purpose of agricultural credit policy has been to

promote the growth of output and the welfare of farmers. The first goal

implies either that rural credit markets are inefficient or that credit is an

effective means of providing a production/investment subsidy to

agricultural. If rural credit markets are inefficient, then effective

intervention could promote output growth by improving efficiency. On the

other hand a determination of whether a production subsidy should be provided

through credit requires a prior exaLmination of the incidence of taxes and

subsidies on fertilizer, irrigation water, irrigation equipment and output.

Once a neutral policy environment is created, it cannot be ruled out a priori

that an explicit credit subsidy (not interest ceilings) may be one component

of an integrated subsidy package.

The second policy objective of increasing farmer welfare can relate

to the entire agricultural sector, or to sub-sets of farmers, usually the poor

and landless. An appropriate production subsidy package is one means of

increasing farmer welfare if accompanied by measures to market the output and

minimize any adverse impact on output prices. The other welfare question

relates to the distribution of gains between traditional lenders and farmer

borrowers. This has been addressed earlier.

Returning to the question of credit market efficiency, there are two

opposing views on the matter. One view is that if agricultural productivity

- 82 -

increases due to introduction of HYVs enough credit will be generated to meet

demand. In other words the existing level of technology and non-credit

related constraints-risk, availability of water, technical knowledge etc., are

significantly more important factors. The other view is that rural credit

markets are very fragmented, and excess funds do not flow smoothly from

surplus to deficit areas. This causes inefficiencies in credit markets.

5.2 Expected Marginal Product of Loans

In an earlier paper I have given a method for measuring the degree