EXAMINATION OF THE COMPONENTS OF THE INTERIM FISCAL POLICY PAPER WHICH WAS LAID BEFORE THE HOUSES OF PARLIAMENT ON SEPTEMBER 26, 2017 INDEPENDENT AUDITOR’S REPORT THE AUDITOR GENERAL OF JAMAICA APRIL TO JULY 2017

Transcript

EXAMINATION OF THE COMPONENTS OF THE INTERIM FISCAL POLICY PAPER WHICH WAS LAID BEFORE THE HOUSES OF PARLIAMENT

ON SEPTEMBER 26, 2017

INDEPENDENT AUDITOR’S REPORT THE AUDITOR GENERAL OF JAMAICA

APRIL TO JULY 2017

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

2

The Auditor General is appointed by the Governor General and is required by the Constitution, Financial Administration and Audit Act, other sundry acts and letters of engagement, to conduct audits at least once per year of the accounts, financial transactions, operations and financial statements of central government ministries and departments, local government agencies, statutory bodies and government companies. The Department is headed by the Auditor General, Pamela Monroe Ellis, who submits her reports to the Speaker of the House of Representatives in accordance with Section 122 of the Constitution of Jamaica and Section 29 of the Financial Administration and Audit Act. This report was prepared by the Auditor General’s Department of Jamaica for presentation to the House of Representatives.

Part A: Fiscal Management ............................................................................................................................. 9

Total Debt ................................................................................................................................................... 9

Bauxite Levy .............................................................................................................................................. 11

Wages and Salaries .................................................................................................................................. 14

Capital Expenditure .................................................................................................................................. 17

Part B: Deviation of the Fiscal Indicators ..................................................................................................... 20

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

4

This page is intentionally left blank

Bauxite Alumina Aluminium

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

5

The Auditor General’s Review

1. I have examined the components of the Fiscal Policy Paper FY2017/18 Interim Report. The Fiscal

Policy Paper FY2017/18 Interim Report was tabled in Parliament on September 26, 2017, within

six months of the passage of the Appropriation Act, in keeping with the requirement of the

Financial Administration and Audit (FAA) Act.

2. The report comprised the Fiscal Responsibility Statement, Macroeconomic Framework and Fiscal

Management Strategy. I reviewed the outturn for FY2016/17, the fiscal performance for April to

July 2017 and projections to end FY2017/18 and medium-term.

Responsibilities of the Minister of Finance

3. Section 48B(2) of the FAA Act provides that:

“Upon presentation of the annual Estimates of Revenue and Expenditure, the Minister shall lay

before both Houses of Parliament –

a) a Fiscal Policy Paper containing the information specified in the Third Schedule and setting out, in accordance with this section – i. a Fiscal Responsibility Statement;

ii. a Macroeconomic Framework; and iii. a Fiscal Management Strategy.”

4. Section 48E of the Financial Administration and Audit (FAA) (Amendment) Act requires that the

Minister shall cause to be tabled in both Houses of Parliament within six months of the passage

of the Appropriation Act for the financial year to which the relevant Estimates of Revenue and

Expenditure relate, a Fiscal Policy Paper which shall, in addition to the matters set out in the

Third Schedule, include:

b) The outturn of the previous financial year;

c) The performance of the first quarter of the financial year;

d) Projections to the end of the current financial year; and

e) Projections for the succeeding financial year and medium-term.

5. Section 48B (5(d) (ii) of the FAA Act requires the Minister to compare the outcome of the fiscal

indicators with the targets established for the previous financial year and give reasons for any

deviations.

6. Section 48D of the FAA Act requires that, the Minister shall act in conformity with the following fiscal management principles:

a) The total debt is to be reduced to, and thereafter maintained at a prudent and sustainable level;

b) Fiscal risks are to be managed prudently with particular reference to their quality and level;

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

6

c) Borrowings are to be geared toward investment activities that support productivity and economic growth; and

d) Expenditure is to be managed in a manner that is consistent with the level of revenue.

Responsibilities of the Auditor General 7. My responsibility, as set out in Section 48B (6) of the FAA Act, is to examine the components of

the Fiscal Policy Paper and provide a report to the Houses of Parliament indicating whether:-

a) the conventions and assumptions underlying the preparation of the Fiscal Policy Paper

comply with the principles of prudent fiscal management specified in Section 48D;

b) the reasons given, pursuant to subsection (5) (d) (ii) are reasonable having regard to the

circumstances;

c) pursuant to my application of criteria prescribed pursuant to regulations made under

Section 50 (1), there are public bodies that do not form part of the specified public

sector, and identifying those bodies (if any) which in the preceding financial year formed

part of the specified public sector;

d) a public private partnership involves only minimal contingent liabilities accruing to the

Government.

Methodology 8. In examining the FPP FY2017/18 Interim report, I reviewed the following:

The Fiscal Policy Paper for FY2017/18 and Errata (February 2017);

The outturn for FY2016/17 relative to budget in the context of projections at February

2017 and September FY2016/17; as well as the evidence and clarifications provided by

the Ministry of Finance and Public Service (MoFPS) regarding deviation from targets;

Projections provided to end FY2017/18 and the medium-term including an assessment of

fiscal risks; and

Other information from the MoFPS and publications from other external sources.

9. I also performed other procedures considered necessary to enable the review process. In the

conduct of my review of the FPP FY2017/18 Interim report, I adhered to the standards issued by

the International Association of Supreme Audit Institutions and International Standard on

Assurance Engagement (ISAE) 3000 – Assurance Engagements Other than Audits or Reviews of

Historical Information, issued by the International Auditing and Assurance Standards Board.

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

7

Key Comments

10. My comments are largely related to the information provided on central government

performance; supported by information from other credible sources, where applicable. Notably,

the Interim FPP Report was provided for my review on October 2, 2017, one week after tabling.

11. The Interim Report contained the outturn for FY2016/17 compared to budget, the performance

for April to July 2017 and projections to the end of FY2017/18 and the medium-term. Whereas I

am required under Section 48B (6) (b) of the FAA Act to confirm that the reasons given for

deviations are reasonable, I could not verify this for Non-Tax revenue as no explanation was

provided for the wide variation between the actual outturn and the estimate in the February FPP.

Non-Tax revenue was estimated to exceed budget for FY2016/17 by 13.4 per cent, whereas the

Interim FPP reported actual Non-Tax Revenue as being below budget by 7.2 per cent.

12. In conducting my assessment of the February FY2017/18 FPP, I had sought to clarify whether

there was a change in the bauxite levy regime as stated in that report. Although the Ministry

subsequently responded that there was no change, the Interim FPP FY2017/18 indicates that a

decline in the FY2017/18 budget for Bauxite Levy reflects the GOJ’s decision to enter into a

profit-sharing arrangement as part of a temporary change in the bauxite levy regime. This is

contrary to the Ministry’s previous response. In correspondence dated October 23, 2017, the

Ministry stated, “the Bauxite Levy Act had not been removed or repealed. So the provisions of

the Bauxite Levy Act can be re-imposed by the Minister subject to terms and conditions of MOUs

with the particular bauxite entity.”

13. The Interim FPP FY2017/18 report indicated that the final wage settlement for public sector

workers could exceed the contingency provision in the budget. This is a risk to the expenditure

budget and the overall fiscal programme, which requires the attainment of the legislated target

of 9 per cent of GDP by FY2018/19. Of note, Section 48D of the FAA Act requires that fiscal risks

are to be managed prudently with particular reference to their quality and level.

14. The Interim FY2017/18 FPP ascribed the continued reduction in debt servicing costs for

FY2016/17 and for the April to July 2017 period, mainly to the execution of liability management

operations, delays in debt management operations and a stronger than expected Jamaica Dollar.

However, the Report did not provide a value for the savings in interest payments arising from

liability management operations to enable an assessment of reasonableness.

15. Reference was made to Public Private Partnerships (PPPs) transactions in progress and further,

that the Enterprise Team had approved the Business Case and Procurement Plan for the Schools

Solar Energy PPP in August 2017. In accordance with the FAA Act, I am required to assess

whether ‘a public private partnership involves only minimal contingent liabilities accruing to the

Government’. This assessment would be undertaken once the business case and financial

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

8

arrangements are finalized. However, in a context where the Schools Energy project is a

‘Government Pays PPP’1, an assessment for contingent liability risk would not be relevant, as the

contingent liability risk is explicit with clear fiscal implications for the GOJ.

Recommendation

16. In the interest of transparency and in accordance with the FAA Act, the Ministry should ensure

that it provides reasonable explanations for deviations particularly where outturns are

significantly at variance with previous estimates indicated in the FPPs.

Pamela Monroe Ellis, FCCA, FCA, CISA Auditor General

1 Government Pays– Project that requires GOJ funding/ support for operations, e.g. schools or hospitals. This will be covered in

the budget as well as the public debt ceiling.

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

9

Part A: Fiscal Management

Total Debt

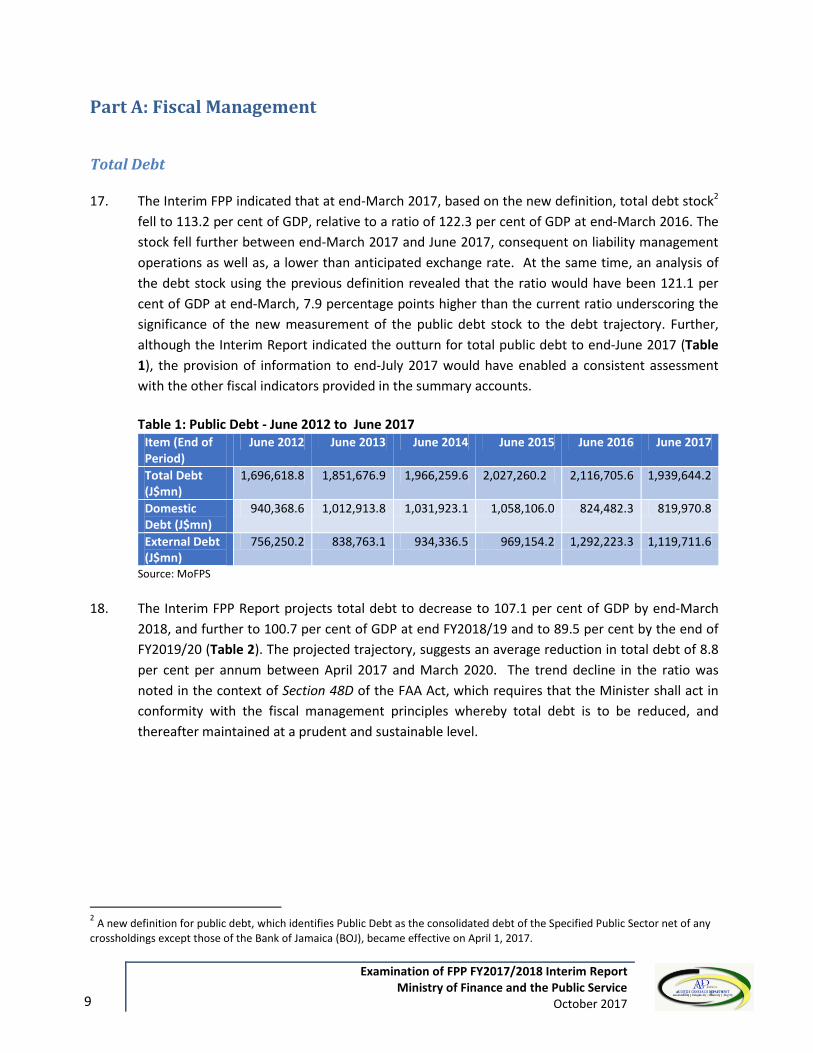

17. The Interim FPP indicated that at end-March 2017, based on the new definition, total debt stock2

fell to 113.2 per cent of GDP, relative to a ratio of 122.3 per cent of GDP at end-March 2016. The

stock fell further between end-March 2017 and June 2017, consequent on liability management

operations as well as, a lower than anticipated exchange rate. At the same time, an analysis of

the debt stock using the previous definition revealed that the ratio would have been 121.1 per

cent of GDP at end-March, 7.9 percentage points higher than the current ratio underscoring the

significance of the new measurement of the public debt stock to the debt trajectory. Further,

although the Interim Report indicated the outturn for total public debt to end-June 2017 (Table

1), the provision of information to end-July 2017 would have enabled a consistent assessment

with the other fiscal indicators provided in the summary accounts.

Table 1: Public Debt - June 2012 to June 2017

Item (End of Period)

June 2012 June 2013 June 2014 June 2015 June 2016 June 2017

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

20

Part B: Deviation of the Fiscal Indicators 46. I have reviewed the explanations provided in the FPP FY2017/18 Interim Report. In making a

determination of reasonableness of the explanations provided by the Minister of Finance, the

following were undertaken:

a) A review of the macroeconomic framework provided in the Interim Report in context of

Budget Assumptions indicated in the FPP FY2017/18 February 2017;

b) A review of estimated revenue gains/losses from the FY2017/18 Revenue Measures;

c) A review of risks in the FY2017/18 Fiscal Policy Paper and Debt Management Strategy to

determine if any has materialized or were excluded from initial projections;

d) A review of emerging risks discussed in the Interim Report;

e) Confirmation where possible, of the Minister’s explanations with observed data.

47. My comments on variances provided in Table 19 are confined to those elements for which

adequate information was provided in the FY2017/18 Interim FPP and by the Ministry of Finance.

Table 19: Comments on the Explanations for the Fiscal Deviations for April to July 2017 relative to Budget (J$mn)

Key Tax Types Provisional Budget Deviation from budget projection (%)

Share of Tax Revenue

GOJ's Explanation Stated in FPP FY2017/18 Interim

Audit Comments Ministry's Response

Tax Revenue April-July

$153,626.6 $148,175.4 3.7 The over-performance was attributable to the approved revenue measures announced in February 2017 and the continued strengthening of administrative procedures.

The measures tabled in March 2017 exceeded the budget gap. Hence, the Interim report should have explained how these measures performed for April to July relative to target.

Revenue Measures for the current FY would not be included in the FPP. These would be tabled in a Ministry Paper.

Income & Profits

$34,548.7 $32,981.9 4.8 23.1 Over-performance in Corporate Taxes influenced better than budgeted performance.

Other Companies

$13,139.2 $9,835.4 33.6 8.6 Improved compliance, increased profitability of the companies and growth in the number of tax paying companies.

The number of companies paying CIT increased to 776 in July from 700 in April.

Agreed

PAYE $17,007.2 $17,825.7 -4.6 11.1 The Ministry assumed that this resulted from increase in employment of persons below the personal income tax threshold.

Production & Consumption

$59,504.5 $54,252.2 9.7 38.8 Improvements in the real sector.

Despite overall downturn in real GDP, Manufacture;

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

22

Key Tax Types Provisional Budget Deviation from budget projection (%)

Share of Tax Revenue

GOJ's Explanation Stated in FPP FY2017/18 Interim

Audit Comments Ministry's Response

Food, Beverage & Tobacco subsectors increased, which are key components for SCT (local)

SCT (local) $11,320.1 $7,868.7 43.9 7.4 Partly attributable to greater than projected production at the local petroleum refinery.

Petroleum production for April to July 2017 was below amount for corresponding period in 2016, and the last five years.

The better performance was due to PetroJam having no credits to set off against local amounts due, as well as higher production taking place in April to July.

GCT (local) $28,750.6 $28,130.7 2.2 18.7 The Interim report did not provide an explanation for variance.

An oversight. This tax type benefited from improvements in Administrative Systems

Education Tax $8,675.5 $7,907.0 9.7 5.6 Higher levels of employment and personal income.

This is consistent with increase in employment.

International Trade

$59,573.3 $60,941.3 -2.2 38.8 Shortfalls in SCT (imports) was the main contributor.

GCT (imports) $25,477.4 $25,589.0 -0.4 16.6 The Interim report did not provide an explanation for variance.

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service

October 2017

23

Key Tax Types Provisional Budget Deviation from budget projection (%)

Share of Tax Revenue

GOJ's Explanation Stated in FPP FY2017/18 Interim

Audit Comments Ministry's Response

SCT (Imports) $13,799.5 $16,642.3 -17.1 9.0 Notable shifts in preferences for cars with smaller engine capacity possibly due to their mileage efficiency and affordability.

We could not validate this explanation.

Customs Duty $12,059.5 $11,569.8 4.2 7.8 The Interim report did not provide an explanation for variance.

An oversight. Customs duty was driven by increased volumes and higher CIF values.

Bauxite Levy $125.7 $131.0 -2.7 0.1 Profit sharing regime that forms part of the temporary bauxite levy modification for the sector. Slower than projected depreciation of the exchange rate.

Minor deviation was due to lower than projected exchange rate outturn for the period.

Non-Tax Revenue

$10,363.6 $10,309.2 0.5 6.7 The Interim report did not provide an explanation for variance.

This was broadly in line with budget with a variance of less than 1%.

Grants $1,838.2 $1,389.4 32.3 1.2 The Interim report did not provide an explanation for variance.

An oversight. The performance was due to improvements in the execution of capital projects.

Examination of FPP FY2017/2018 Interim Report Ministry of Finance and the Public Service