25

Prezentáció címe Eva Rez Principal, Day One Capital February 2017 CEE FINTECH Report 2016

| Date post: | 09-Feb-2017 |

| Category: |

Economy & Finance |

| Upload: | rezeva |

| View: | 178 times |

| Download: | 0 times |

Prezentáció címe

Eva Rez

Principal, Day One Capital

February 2017

CEE FINTECH Report

2016

Summary based on the below Deloitte report

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/central-

europe/ce-fintech-in-cee-region-2016.pdf

a

Hungary is the 7th out of 9 countries

Source: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/central-europe/ce-fintech-in-cee-region-2016.pdf

Net FDI inflow as a % of GDP is the highest in Hungary

Source: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/central-europe/ce-fintech-in-cee-region-2016.pdf

Key Trends

What is hot?

– Mainly solutions for the banking sector developed in-house or fromvendors

– Payment services are the hottest especially in Poland and the CzechRepublic

– PFM, P2P lending quite developed in the region except Hungary

– Cybersecurity is gaining momentum but mainly provided by globalplayers

What is not so hot?

– Insurance and asset management lag behind

Key barriers: demand, regulation, competition

Potential facilitators: favourable business environment, growingfintech community

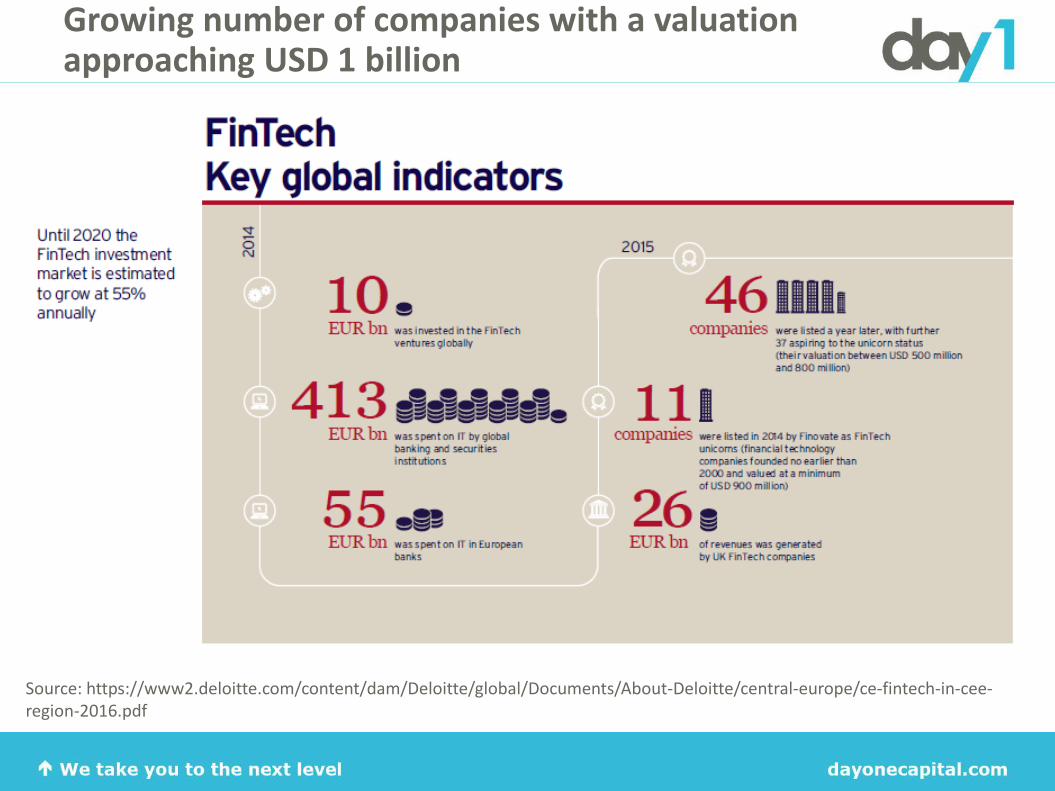

Growing number of companies with a valuation approaching USD 1 billion

Source: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/central-europe/ce-fintech-in-cee-region-2016.pdf

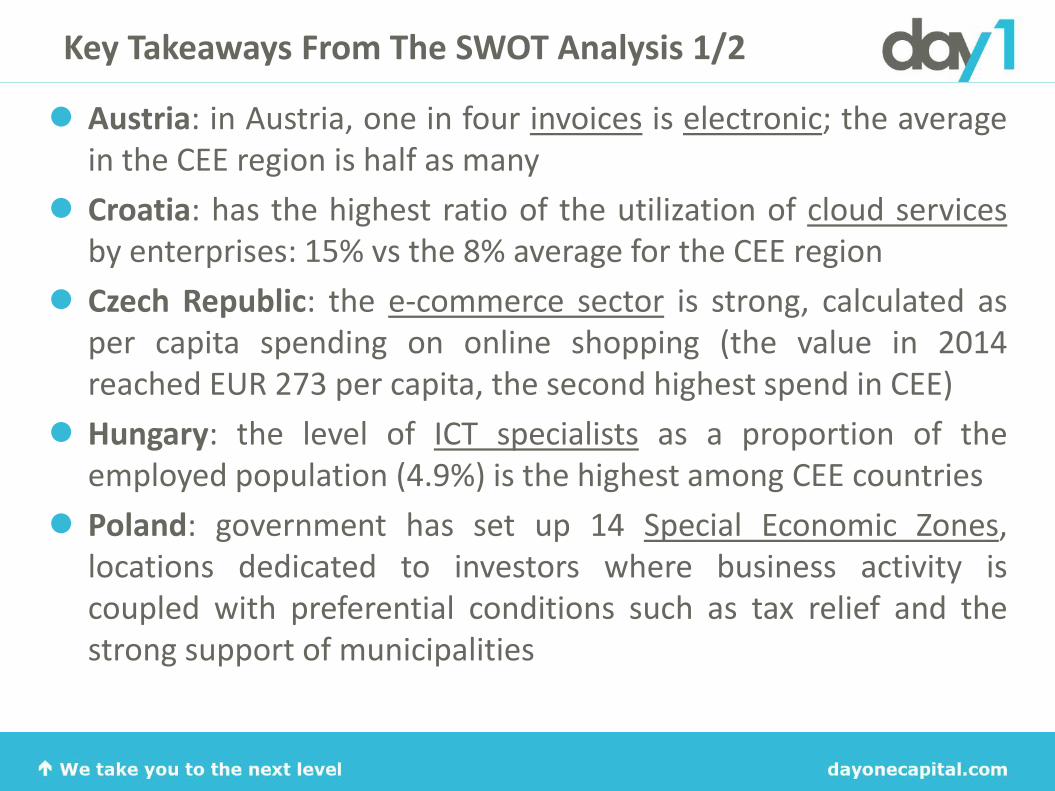

Key Takeaways From The SWOT Analysis 1/2

Austria: in Austria, one in four invoices is electronic; the averagein the CEE region is half as many

Croatia: has the highest ratio of the utilization of cloud servicesby enterprises: 15% vs the 8% average for the CEE region

Czech Republic: the e-commerce sector is strong, calculated asper capita spending on online shopping (the value in 2014reached EUR 273 per capita, the second highest spend in CEE)

Hungary: the level of ICT specialists as a proportion of theemployed population (4.9%) is the highest among CEE countries

Poland: government has set up 14 Special Economic Zones,locations dedicated to investors where business activity iscoupled with preferential conditions such as tax relief and thestrong support of municipalities

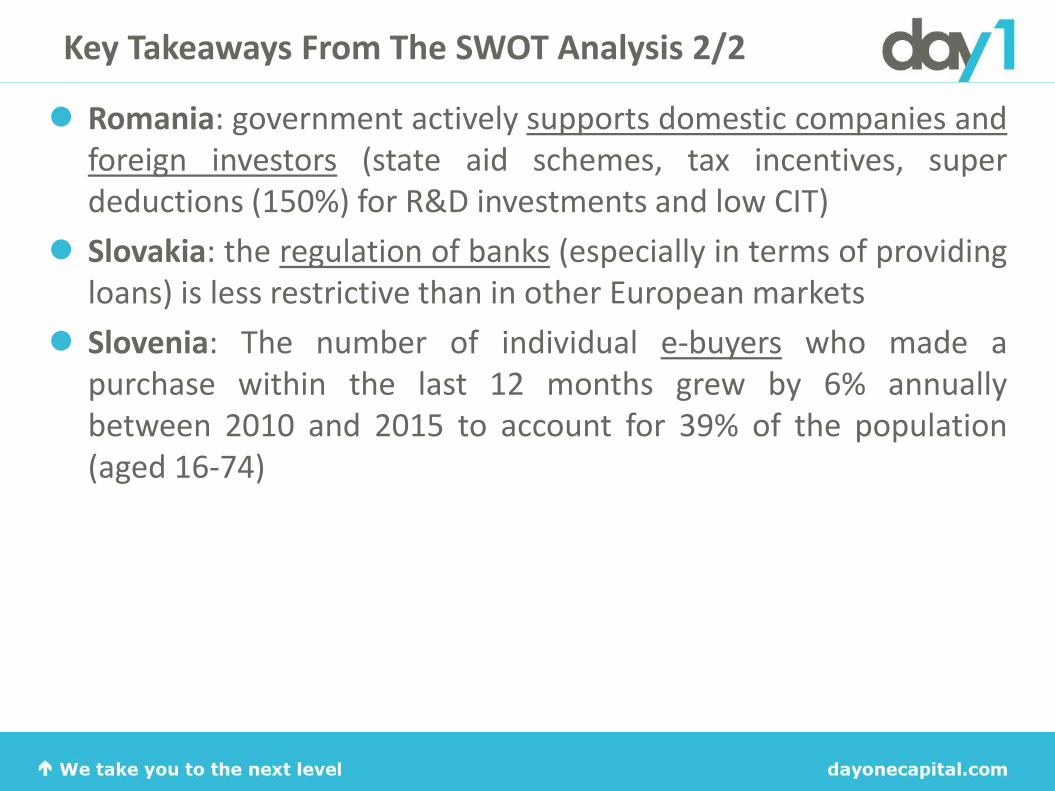

Key Takeaways From The SWOT Analysis 2/2

Romania: government actively supports domestic companies andforeign investors (state aid schemes, tax incentives, superdeductions (150%) for R&D investments and low CIT)

Slovakia: the regulation of banks (especially in terms of providingloans) is less restrictive than in other European markets

Slovenia: The number of individual e-buyers who made apurchase within the last 12 months grew by 6% annuallybetween 2010 and 2015 to account for 39% of the population(aged 16-74)

The lowest trust in banks in the region

Source: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/central-europe/ce-fintech-in-cee-region-2016.pdf

Fintech in Austria - Conservative

Banking sector

– Austrian IT companies serving banks usually are themselves part of bankinggroups

– There are numerous fintech companies co-operating and competing with theestablished financial sector (e.g. Number 26)

Insurance sector

– Innovations that have appeared in the market have not gained widespreadpopularity to date

Capital market

– Developing solutions for individual investors seems to be the futuredevelopment direction for the Austrian fintech market (e.g. Wikifolio)

Payments

– Austria is catching up with the CEE region

– Society needs to realise the benefits of online and m-payments

Data analytics

– Banks mostly choose international players to provide them with analyticssolutions

Fintech in Bulgaria - Follower

Banking sector– Most of the banks belong to global groups and inherit technology solutions from them

– Banks concentrate on mobile technologies, CRM systems, data and analytics solutionsand virtualisation

Insurance sector– Bulgarian insurers understand the need for digital transformation and automated sales

processes (e.g. Generali Bulgaria)

– Development is slower than in the banking industry

Capital market– The crowdfunding market is relatively saturated

– The lack of regulation of crowdfunding activities raises concerns over factors includingintellectual property and the contractual relationships between investors and platforms

Payments– Low smartphone penetration hampers the wide uptake of mobile payment solutions

– The Bulgarian payments market is set for strong growth

Fintech in Croatia - Small

Banking sector– Online banking penetration is among the lowest in CEE

– The biggest bank in Croatia (Zagrebacka banka) is one of the most innovative ones

Insurance sector– The market is at an early stage of development

– Croatian insurers have already started considering financial technology innovation,especially in the area of digital distribution channels

– The high willingness of insurers to work with local IT companies is a barrier to the entry offoreign players

Capital market– The dominance of banks in terms of capital raising could hamper the market entry of

non-banking players who specialise in personal loans and micro-finance

Payments– The low usage of non-cash payment methods may impede the implementation of

payments-related products and services

Personal finance– Oradian!

Fintech in Czech Republic – Competitive 1/2

Banking sector– One of the most innovative of all CEE countries (e.g. contactless cards)

– Current IT architecture is based on legacy systems built by globally known IT vendors,which makes it harder for new fintech entrants

– Security concerns and data protection are still hampering the wide uptake of cloud-basedsolutions

Payments– Due to the strong e-commerce market digital payment solutions will further expand

– Strong position of banks but some startups showed up especially for routine transactions(e.g. Twisto – one-stop-shop solution for payments)

– Several innovative Bitcoin-related solutions (e.g. display device that enables offlinepayments using Bitcoin)

Personal finance– Banks are implementing tools for personal finance management (both in-house solutions

and off-the-shelf solutions from startups)

– P2P lending market is quite well developed, both for individual borrowers and SMEs

– Education more in focus

Fintech in Czech Republic – Competitive 2/2

Cybersecurity– Banks are starting to consider biometrics as the emerging global trend and centralised

authentication security solutions

Enterprise solutions– RPA (Robotic Process Automation) software is gaining more and more attention

– One of the few CEE markets where a common standard for exchanging paymentinformation embedded in QR codes has been successfully implemented. It can be nowintegrated within most accounting systems.

Fintech in Hungary – Regulated 1/2

Banking sector– The penetration of mobile and internet banking currently remains low

– Banks are committed to innovation – digitisation (e.g. digitalisation of branches) is a hottopic in the C-suite

– IT budgets in Hungarian banks are among the lowest in the CEE region but someimprovements are expected

Insurance sector– The insurance sector is still not set to digitise, while customers are very price-sensitive

– As an exemption telematics are used within the market (e.g. Vemoco – pay as you drive)

– The most pressing issues are going paperless, automating the underwriting process,simplifying product development and introducing an omni-channel view

Payments– Hungary has one of the lowest regional penetrations of contactless smart cards

– Mobile payments are only just beginning to enter the payment landscape in Hungary

– MobilTarca is the first NFC scheme in the country

– There are only around 10 Hungary-based mobile payment apps (e.g. iCsekk, Buxa, Barion)

– There is a strong belief that global solutions from the likes of Apple or Samsung candominate the market

Fintech in Hungary – Regulated 2/2

Asset management– Growing savings per capita and customer education may create a deeper market

Capital market and Personal finance– P2P lending, crowdfunding, micro lending and other such solutions are not possible in the

current legal environment

Fintech in Poland – Open to innovation 1/3

Banking sector– A regional leader in technologically advanced, pioneering solutions sector (e.g. mobile

banking, contactless functionality or the branchless model by mBank (Commerzbank))

– The digital maturity of Polish banks and the many interesting solutions offered to theirclients may limit the development of non-banking innovators (e.g. for cooperation:Finanteq)

– Highly regulated and also trusted by society

Insurance sector– Focus is mainly on back-office and direct sales channels

– Insurers will turn their attention to young businesses delivering high level of automationand as-a-service delivery model

– Internet of Things and gamification are two key trends in Poland (e.g. Link4)

Payments– Wide acceptance of contactless cards drives the dynamic development of the POS

infrastructure

– The value of m-commerce grew more than fourfold between 2013 and 2015 and isforecasted to grow at an annual rate of around 40% in years to come

Fintech in Poland – Open to innovation 2/3

Payments– The best known internet payment companies were created by Polish companies: PayU (a

subsidiary of Allegro – the biggest e-commerce company in Poland – currently owned bythe South African Naspers), DotPay, Przelewy24 and Tpay

– HCE (Host Card Emulation: payment data is stored on the bank’s servers and the details ofpayment card are kept in the mobile app) adopted by 5 banks already: Pekao SA, PKO BP,BZ WBK, Eurobank and Getin

– Bitcoin and Blockchain technology are popular

– PSD2 is likely to shift the centre of gravity towards new entrants, including global players

Capital market and Personal finance– Demand for consumer loans in Poland is rising, thus lending platforms are gaining

momentum

– Despite legal ambiguities (e.g. maximum level of credit cost), crowdfunding remains apromising area

Cybersecurity– Ensuring the security of mobile banking and cloud-based solutions is a future trend, with

little recognition for biometrics on the Polish market

– Regulatory bodies are placing special emphasis on the issue of security

Fintech in Poland – Open to innovation 3/3

Data analytics– Polish banks are mainly focused on basic issues related to data quality because of the

process of consolidation in the industry

– Regulations concerning data management may be a significant challenge for many financialinstitutions

Enterprise solutions– SMEs are increasingly interested in automated and cloud-based solutions for the

management of their finances

Fintech in Romania – Digitally divided 1/2

Banking sector– The penetration of online banking in Romania is currently at a negligible 6%

– Key players (e.g. OTP Bank Romania) follow European trends and deliver a high-quality userexperience to their customers

– In most cases the deployment of a cloud computing solution will mean “outsourcing ofsignificant activities”, thus becoming subject to the obligation to notify the National Bankof Romania

– Different challenges than in other CEE countries: e.g. stronger focus on regulatory issuesthan on customer experience

Insurance sector– Low level of development

Payments– Cash payments currently dominate the Romanian payments sector but the country is

encouraging the popularisation of non-cash payments (e.g. anti-corruption initiatives,GarantiBank’s innovations)

– Education appears to be key to the nationwide adoption of non-cash payments

– International transfers are particularly important in Romania with 16.5% of its populationliving abroad

Fintech in Romania – Digitally divided 2/2

Payments– Currently, the market is fragmented, with small alliances connecting some banks and some

merchants

– Significant potential for Romania’s ATM-related business due to its multifunctional nature

Capital market and Personal finance– There is strong demand for loans as reported both by banks and non-banking institutions

– Online lending with price-comparison functionality is becoming popular

– Crowdfunding activity faces stricter regulatory barriers and people do not trust the concept

Fintech in Slovakia – Open to innovation 1/2

Banking sector– The banking sector in Slovakia is open to new, innovative solutions

– The sector’s current leader is Tatra banka

– Slovak banks often serve as a testing environment for global innovations, while non-banking institutions pose strong competition

Insurance sector– Unlike in most CEE countries, insurance is not lagging behind banking in terms of

innovation

– Focus on online policy sales and telematics

Payments– Slovakia is perceived internationally as a rapid adopter of innovative payment solutions,

leaving the UK and most of Europe behind

– Bratislava has recently become the second European city (after Bristol in the UK) wherepeople can use a local electronic currency to make payments

– Due to its high level of innovative capability, the payments market is already facingconsolidation: only best-in-class solutions remain on the market

Fintech in Slovakia – Open to innovation 2/2

Capital market and Personal finance– Alternative lending is as yet not strictly regulated, and spells opportunities for new entrants

to experiment with various business models

– However, a new law that came into force in mid-2015 requires consumer finance lenders toobtain a licence and retain a minimum level of basic capital

– Crowdfunding in Slovakia is still in its infancy

Enterprise solutions– Automated and robotic finance management is not as yet popular in Slovakia (exception:

Archiles, Datamolino)

Fintech in Slovenia – Small

Banking sector– The inventiveness of Slovenian banks is average, based mainly on solutions already popular

in most banks in Western Europe (e.g. mobile, contactless cards)

– The small market size may constrain banks’ investment in technologies supporting newproduct development

Payments– Slovenia has emerged as a CEE Bitcoin hub thanks to many start-ups providing platforms

for Bitcoin transactions or trading (e.g. Bitstamp: 16% market share)

– Payments in Bitcoins are spreading due to increasing number of merchants accepting thiscryptocurrency (second in the global league table of Bitcoin merchant adoption)

Capital market and Personal finance– Mid-sized Slovenian companies are starting to exchange their receivables on a dedicated

marketplace (e.g. Borza Terjatev/Invoice Exchange)

Thank you!a

https://medium.com/@evarez

www.dayonecapital.comhttp://www.dayonecapital.com/subscribe-to-our-

newsletter/

https://twitter.com/DayOneCapitalhttps://www.facebook.com/dayonecapital