32

1 Exchange Rates

1

Exchange Rates

2Exchange Rate: Definition

The exchange rate is the price of a currency in terms of another currency. Thud the exchange rate for the US dollar can be expressed in the amount of British pounds, EURO or Mexican pesos needed to but one dollar.

If $US1 = €0.82, then the exchange rate for EURO = (1/0.82) = $US 1.22

Q: The exchange rate for the US dollar is 7.5 Swedish Crowns (SEK), What is the exchange rate for the SEK?

A: 1 SEK = $ US 0.133

3Currencies are bought and sold on a foreign exchange market. The demand for a currency is a function of three main variables:

1.The demand for other countries’ goods and services

2.The demand for foreign direct investment and portfolio investment in another country

3.Speculative demand

People and import/ export firms will buy currencies from banks and foreign exchange offices to conduct international transactions. Foreign exchange brokers will in turn be used by banks to supply needed currencies and to cash-in unneeded currencies. Finally the central banks of trading countries may intervene on the currency market by adding to the foreign reserves in order to adjust the exchange rate.

4

The Supply curve for currencies is upward sloping because a higher price of

currency X would-ceteris paribus- would enable citizens of that country (X) (to

buy more goods of country Y. In doing more currency X will be available in

country Y’s market.

5EXPLANATION

When the value of the rupee increases in terms of dollars; rupee

appreciates, you will be able to buy more from the same amount of

rupees spent, therefore the supply of rupees will increase.

6DEMAND CURVE

The demand curve is downward sloping to indicate that citizens of country X will

buy more currency Y when they get more of it – and more goods- for their

currency X.

7EXPLANATION

When the rupee value falls in terms of other currencies ,say dollar,

we would need more rupees to buy same amount of goods,

demand for rupees would increase.

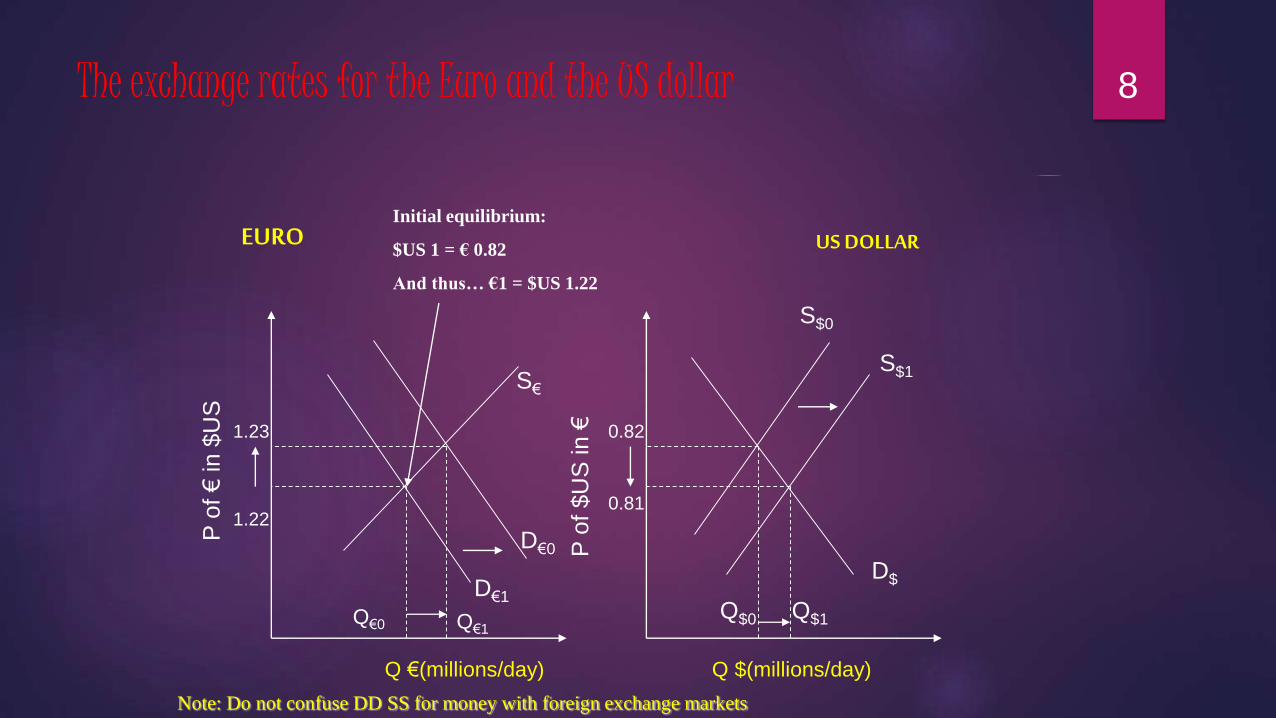

8The exchange rates for the Euro and the US dollar

P o

f €

in $

US

P o

f $

US

in €

Q €(millions/day) Q $(millions/day)

Initial equilibrium:

$US 1 = € 0.82

And thus… €1 = $US 1.22

EURO

S$0

S$1

0.82

0.81

Q$0 Q$1Q€0 Q€1

D$

D€0

D€1

S€

1.22

1.23

US DOLLAR

Note: Do not confuse DD SS for money with foreign exchange markets

9Fixed exchange rates

We know that exchange rates are established by market forces of demand and supply. When a group of countries instead keep their exchange rate constant thus establishing a fixed exchange rate.

Such countries use the central government to intervene on the foreign exchange market in order to keep exchange rate within a narrow band-much like the mechanism used in a buffer stock mechanism.

The central government can affect the exchange rate in the short run by buying or selling its own currency on the foreign exchange market, and by adjusting the interest rate to influence investors’ demand for the currency.

In the long run, governments might intervene using fiscal policies, supply-side measures and protectionism to adjust national income in order to increase or decrease exports and citizens’ propensity to import.

Types of Fixed exchange rates The Gold Standard

The Bretton Woods exchange rate system

10How a Fixed Exchange Rate Works

Ceiling

LR equilibrium

Floor

Outside the band

Q1 Q2 Q3Q4

2.84

2.82

2.80

2.78

P o

f £

in

US

$

Q £(millions/day)

D£1D£0

B

D£2

A

C

D

S£1

S£0

When exchange rate rises above

2.82 the Bank of England will have

to sell Q1Q3 (S£0 shifts to S£1)

on the foreign exchange market to

keep the pound within the band

Keeping the pound down

* (For ‘keeping the pound up’) refer pg 565 of textbook)

11Other tools affecting Exchange Rates

Central banks are not limited to buying and selling their currencies in order to influence the exchange rate. There are two alternatives in the short term:

1) The central bank can change the interest rate. If it wishes to increase the exchange rate, the interest rate could be raised. This would influence the demand for the home currency as foreign investors/ speculators would see a higher rate of return in holding the currency –demand for the home currency would rise.

2) The central bank could borrow from the International Monetary Fund. The IMF was created to aid countries having difficulty keeping a stable exchange rate. When a country’s currency falls, and the central bank runs out of foreign exchange to buy up the home currency, the central bank can borrow funds from the IMF to get over the crisis.

12Floating Exchange Rates

When a currency’s value is totally determined by market forces – e.g. supply and demand for the home currency – there is a floating exchange rate.

A currency ‘floats’ amongst the other currencies on the market and the price is set in accordance with the mechanisms of supply and demand outlined earlier.

The demand for a currency is derived from demand of goods, services and investments in other countries. There is also speculation in currency – which is perhaps the main short run determinant of exchange rates – which is based on the predictions/ emotions of currency speculators ‘betting’ on changes in exchange rates

In a floating exchange rate system, perfect information is an important issue.

Central banks have a tendency to intervene to correct what is considered to be disequilibrium in a floating exchange rate. This is called managed float or dirty float. Dirty float implies that impure market forces (central bank interventions) are present.

13Managed Exchange Rates

When currencies are allowed to fluctuate within a narrow band in the short run, and allowed to be realigned in the long run, there is a managed exchange rate. The most common version is when a government pegs its currency to another.

Completely fixed rates cause a problem of inflexibility, since economies have different fundamentals such as growth rates and inflation rates.

In the long run it could be very costly for a country with a weakening currency to defend its links with other countries.

That is why we have managed exchanged rates

14An example

When the exchange rate exceeds the ceiling of $US 0.12082 per Yuan, points A in the diagram,

the Chinese central bank sells Yuan (by buying foreign currencies) in order to increase the

supply and lower the exchange rate.

When the rate falls below the floor level of $US 0.12024 per Yuan, points B, the central bank

buys Yuan (with foreign currencies) which increases demand for Yuan and therefore the

exchange rate for Yuan goes up.

15A managed exchange rate

Revalu

ation

Devalu

ation

Ceiling

CeilingCeiling A

A

A

B

B

B Floor

Floor

Floor

0.12024

0.12048

0.12082

1995 2004

t1 t2

P o

f Y

uan in $

US

time

• If there is fundamental

upward movement in the Yuan

i.e. the managed rate is below

the long run rate the market

sets, the Chinese central bank

can realign the currency by

revaluating the Yuan: time t1.

•Conversely, a fundamental

overvaluation of the Yuan,

shown at time t2, might cause

massive purchasing of the Yuan

and running down the foreign

reserves.

16Appreciation and Depreciation

When the exchange rate of a freely floating currency rises, the currency has appreciated.

A fall in the value of a floating currency means the currency has depreciated.

Revaluation and devaluation

When the government re-pegs a fixed/ pegged currency, the currency has

been revalued.

When a fixed or pegged currency is realigned to a lower value, the currency

has devalued.

17Effects on exchange rates

Main determinants of the exchange rate

Two main assumptions:

The currency in question (the US dollar) is not only floating but also freely floating-there is no intervention by the US central bank

Each of the determinants mentioned later are operating under the ceteris paribus conditions-a change in interest rates is not accompanied by a change in another variable

18Trade Flow

When American exports increase, there will be an increased demand for the dollar as importers in other countries will need more dollars to buy the American goods. Increased exports will increase the demand for the dollar, causing the shift in the demand curve on slide 18 from D$0 to D$1 and subsequently an appreciation of the dollar from x 0to x 1. (x = ex; delta = change).

An increase in imports or an increase in American tourism abroad would imply increased trade of dollars for goods/ services causing an increase in supply of dollars on the market – S$’0 to S$’2 – and the dollar depreciates from x’ 0 to x’ 2 (slide 18)

=> US exports ↑demand for $US ↑x for $US↑ (and vice versa)

=> US imports ↑supply of $US ↑ x for $US↓ (and vice versa)

19Capital Flows/ Interest rate changes

*

Inflows of investment to the US demand for the $ US ↑ x for the $US↑

(and vice versa)

US investment abroad↑ supply of $US↑ x for $US↓ (and vice versa)

20Variables affecting the exchange rate for the US dollar

D$2

D$1

D$0

S’$1

S’$0

S’$2

S$

D’$

US dollar US dollar

Q2 Q0 Q1 Q’1 Q’0 Q’2

P o

f $U

S (

TW

I)

P o

f $U

S (

TW

I)Q$ (millions/day) Q$ (millions/day)

x 1

x 0

x 2

x ’1

x ’0

x ’2

21

Increase in demand for the US

dollar:

Increase in supply of the US

dollar:

↑ US exports of goods/ services

↑ in foreign investment in US

↑ in US interest rates

↓ in US inflation rate

Speculative buying of US dollar

US central bank buys dollars (= decrease

in foreign reserves)

↑ US imports of goods/ services

↑ in US foreign investment abroad

↑ in foreign interest rates

↓ in foreign inflation rates

Speculative selling of US dollar

US central bank sells dollars (= increase

in foreign reserves)

Decrease in demand for the US

dollar:

Decrease in supply of the US

dollar:

↓ US exports of goods/ services

↓ in foreign investment in US

↓ in US interest rates

↑ in US inflation rate

↓ US imports of goods/ services

↓ in US foreign investment abroad

↓ in foreign interest rates

↑ in foreign inflation rate

22Inflation

Ceteris Paribus:

Relative inflation in US↑ demand for US exports &

US demand for imports ↓ demand for US dollar ↓ &

supply of US dollar↑ x for the $US ↓

Relative inflation in US↓ demand for US exports↑ &

US demand for imports ↓ demand for US dollar ↑ &

supply of US dollar↓ x for $US ↑

23Speculation

Speculative belief that the US dollar will depreciate US dollar is sold supply

of the US dollar↑ x for $US↓

Speculative belief that the US dollar will appreciate US dollar is bought

demand for the US dollar ↑ x for the $US↑

24Use of foreign exchange reserves

Governments can intervene on the foreign currency market via the foreign currency reserves held in the central bank

US dollar depreciates ‘too much’ US central bank intervenes by buying the US dollar demand for dollar ↑ x for the $US ↑ (decrease in US foreign reserves & inflow to US capital account)

US dollar appreciates ‘too much’ US central bank intervenes by selling the US dollar supply of the US dollar ↑ x for $US ↓ (decrease in the US foreign reserves & inflow to the US capital account)

25Fixed exchange rates

Advantages:

Predictability and certainty

Exchange rate stability encourages trade

Fiscal/ monetary discipline domestically

Less risk of speculation

Disadvantages:

Loss of domestic monetary policy freedom

Need of large foreign reserves

Possibility of increased unemployment

Possibility of imported inflation

26Floating exchange rates

Advantages:

The balance of payments automatically adjusts

No large foreign reserves necessary

Freedom in domestic/ monetary policies

Reduced Speculation

Less risk of imported inflation

Disadvantages:

Instability and lack of predictability

Lack of monetary/ fiscal prudence

Loss of competitiveness and efficiency

27Monetary Integration (single currencies)

Information:

In 1999 the EURO technically came into being and during 2001 (from all 15 members except UK, Denmark, Sweden and Greece) were ‘locked’ in place in exchange terms. A European central bank took over the task of setting and implementing monetary policies for all EMU countries. This project created one of the largest shifts in economic power in history.

In order for each country wishing to join to be eligible, they had to adjust domestic fiscal and monetary policies to fulfill the following criteria:

Inflation could be no more than 1.5 percentage points above the average inflation of the three countries with the lowest inflation

Interest rates had to be within 2 percentage points of the average of the three countries with the lowest interest rates

A maximum budget deficit of 3% of GDP

Exchange rates had to be kept within a narrow band for 2-3 years

The national debt had to be lower than 60% of GDP

28EMU: COSTS AND BENEFITS

Benefits:

Trade creation

Increased efficiency due to increased competition

Benefits of scale

Lower transaction costs

Costs:

Loss of domestic monetary policy

Restrictions on domestic fiscal policy

Regional unemployment

29Purchasing Power Parity*

The theory of purchasing power parity states that exchange rates will in the long run adjust to

different inflation rates in countries, leading to equilibrium where a given amount of home currency

traded for a foreign currency will buy an equally-sized bundle of goods.

*Refer to textbook for limitation of this theory

30Understand this situation – Arbitrage and the law of one price

Assume two countries, X and Y, side-by-side which have no trade barriers; mo transaction costs; no transport costs; homogenous goods; identical expenditure taxes; and a floating exchange rate.

Country X can buy a kilo of flour for 2 ($X) domestically.

Country Y can buy a kilo of flour for 3 ($Y) domestically

The exchange rate is $X1 = $Y2; or $Y2 = $X0.5

The following two things will happen:

(i) Citizens from X will cross over to Y to buy flour, seeing as how $X2 they pay at home would get them $Y4 and then 1.33 kilos of flour;

(ii) There would be arbitrage, as enterprising people in Y would buy flour domestically and sell it in X for just under $X2 per kilo.

The result:

Increased demand for the Y dollar will cause the $Y to appreciate.

Also, the traders from Y will exchange their X dollars for Y dollars, thereby increasing supply of $X and causing a depreciation of the $X.

31

Law of one price:Assuming that there are no imperfections, two

homogenous goods must ultimately have the same

price on a market

Demand for Y flour will cease and arbitrage activities will

end when the exchange rate between the two countries is

such that the price is the same for both countries.

i.e. 1 kilo flour in X = $X2 = $Y3= 1 kilo flour in Y

32The law of one price and the PPP theory

Consider our previous situation. What if the inflation rates in X & Y would differ, exchange rate remaining constant.

Say for e.g. 10% inflation in Y and 0 in X.

The answer: 1 kilo of flour would cost $Y3.3 in Y but still $X2 in X. If the exchange rate remained unchanged, Y citizens would get more flour for their money in X and arbitrage would be conducted in the other direction – Y would import flour now. This would continue until a new exchange rate came in that gave both X & Y equal PPP.

2$X = 3.3$Y 1$X = 1.65$Y, or 1$Y = 0.60$X.

The X dollar has appreciated by 10% and the Y dollar has depreciated by 10%.

This is essentially the PPP theory.