HDC Webinar Series Introduced by Dwayne Spradlin, CEO, Health Data Consortium Public Exchanges Go Live: Early Competitive Dynamics and Strategic Implications David Knott and Erica Hutchins Coe, McKinsey & Company

Transcript

HDC Webinar Series

Introduced by Dwayne Spradlin, CEO, Health Data Consortium

Public Exchanges Go Live:Early Competitive Dynamics and Strategic Implications

David Knott and Erica Hutchins Coe, McKinsey & Company

WORKING DRAFTLast Modified 12/9/2013 10:08 AM Eastern Standard TimePrinted 11/20/2013 10:37 AM Eastern Standard Time

PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Exchanges go live: earlytrends in competitor dynamics

Webinar document

McKinsey & Company | 3

McKinsey has conducted extensive research and client work on the impactof big data in health care and other industries

▪ Traditionally, the healthcare industry has lagged behind other industries in the use of bigdata—we believe that healthcare is now at a tipping point:– Demand for better data (driven by ever greater calls for demonstrable value)– Supply of relevant data at scale (claims, clinical data increasingly available)– Enhancements in technical capabilities (ability to combine and mine data sets)– Government catalyzing market change (liberating data sets, interoperability standards)

▪ Increased product, network, formulary, and pricing transparency brought about by publicexchanges will help accelerate the use and impact of big data in healthcare

▪ Public exchanges opened on October 1, 2013—we do not yet have access to broadenrollment data from public exchanges…

▪ …However, we can draw initial insights from rate filing data that is now available for everypublic exchange nationally

▪ Purpose of today’s conversation is to arm you with early insights to inform your strategiesand actions based on analysis of over 21,000 products offered in 50 states and DC

McKinsey & Company | 4

We have developed several proprietary tools to analyze competitor dynamicson the new public exchanges

Post-reform landscape▪ Rate filing database, with ~21,000 Public

Exchange plans across rating areas– 50 states and D.C. (as of October 16, 2013)– Pricing and network data– Carrier details– Cost sharing details

▪ Proprietary exchange simulation tool, with150,000 consumer data points

▪ Proprietary simulator to project expectedmarket dynamics

SOURCE: McKinsey Center for U. S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

McKinsey & Company | 5

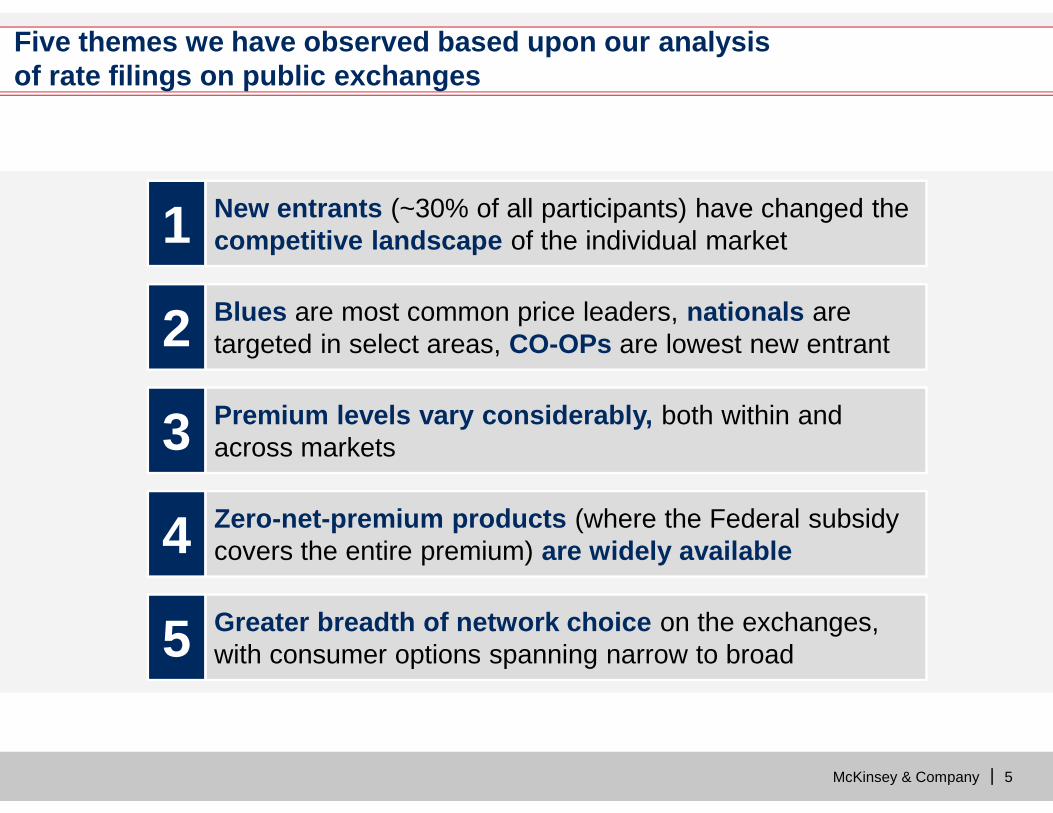

11 New entrants (~30% of all participants) have changed thecompetitive landscape of the individual marketNew entrants (~30% of all participants) have changed thecompetitive landscape of the individual market

22 Blues are most common price leaders, nationals aretargeted in select areas, CO-OPs are lowest new entrantBlues are most common price leaders, nationals aretargeted in select areas, CO-OPs are lowest new entrant

33 Premium levels vary considerably, both within andacross marketsPremium levels vary considerably, both within andacross markets

44 Zero-net-premium products (where the Federal subsidycovers the entire premium) are widely availableZero-net-premium products (where the Federal subsidycovers the entire premium) are widely available

55 Greater breadth of network choice on the exchanges,with consumer options spanning narrow to broadGreater breadth of network choice on the exchanges,with consumer options spanning narrow to broad

Five themes we have observed based upon our analysisof rate filings on public exchanges

McKinsey & Company | 6

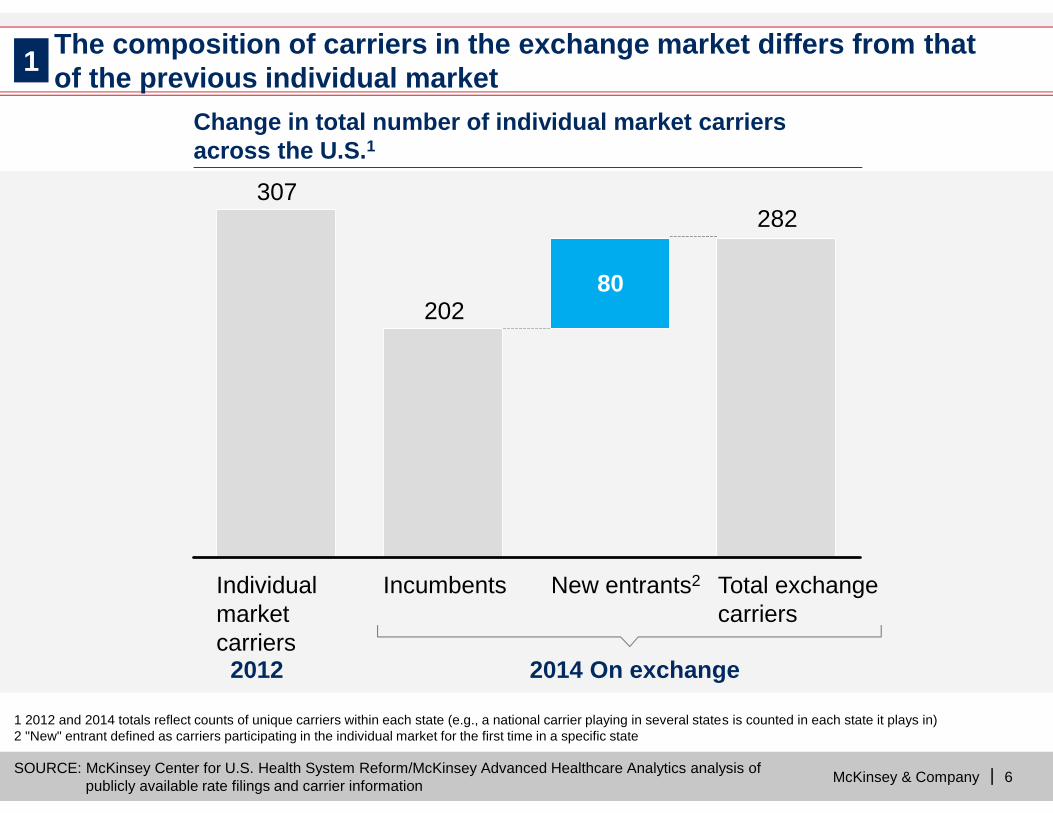

1 2012 and 2014 totals reflect counts of unique carriers within each state (e.g., a national carrier playing in several states is counted in each state it plays in)2 "New" entrant defined as carriers participating in the individual market for the first time in a specific state

2014 On exchange2012

The composition of carriers in the exchange market differs from thatof the previous individual market

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

1

282

202

307

Individualmarketcarriers

Incumbents Total exchangecarriers

New entrants2

80

Change in total number of individual market carriersacross the U.S.1

McKinsey & Company | 7

AL

ARAZ

CACO

CT

FL

GA

IA

ID

IL IN

KSKY

LA

MA

ME

MI

MN

MO

MS

MT

NC

ND

NE

NH

NM

NV

NY

OH

OK

OR

PA

SC

SD

TN

TX

UT

VA

VT

WA

WI

WV

WY

DCDEMD

NJ RI

HI

AK

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

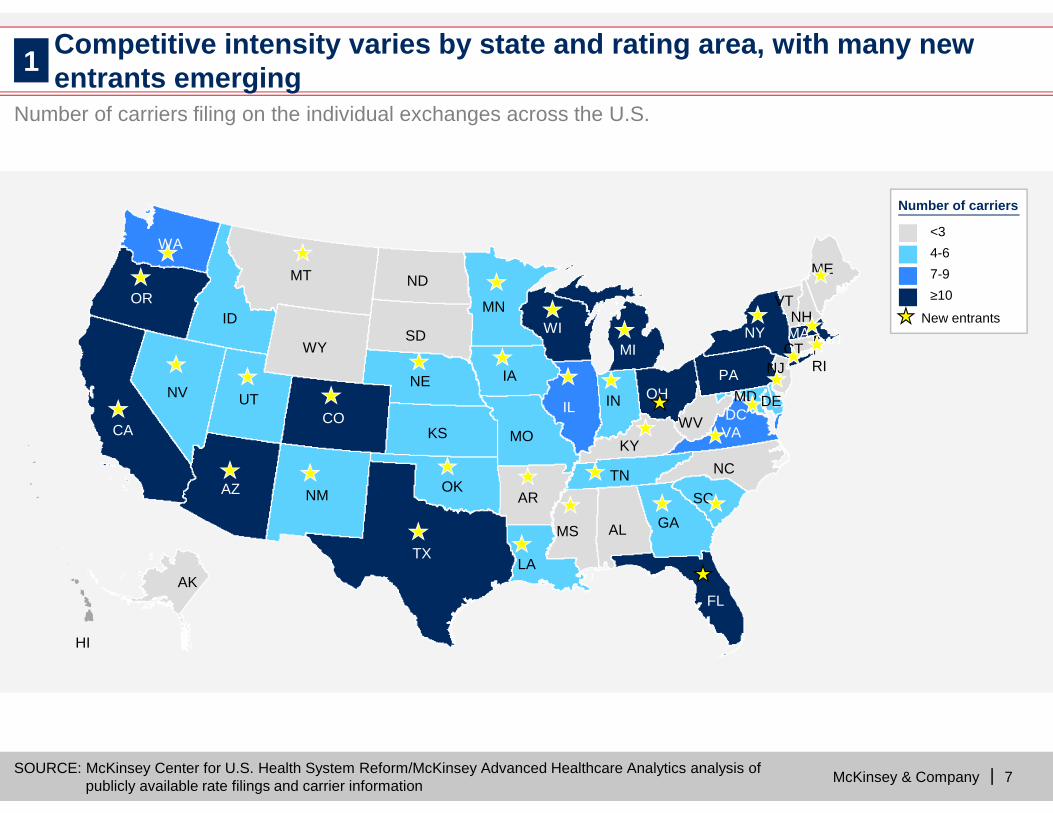

Number of carriers filing on the individual exchanges across the U.S.

Competitive intensity varies by state and rating area, with many newentrants emerging

<34-67-9≥10

Number of carriers

New entrants

1

McKinsey & Company | 8

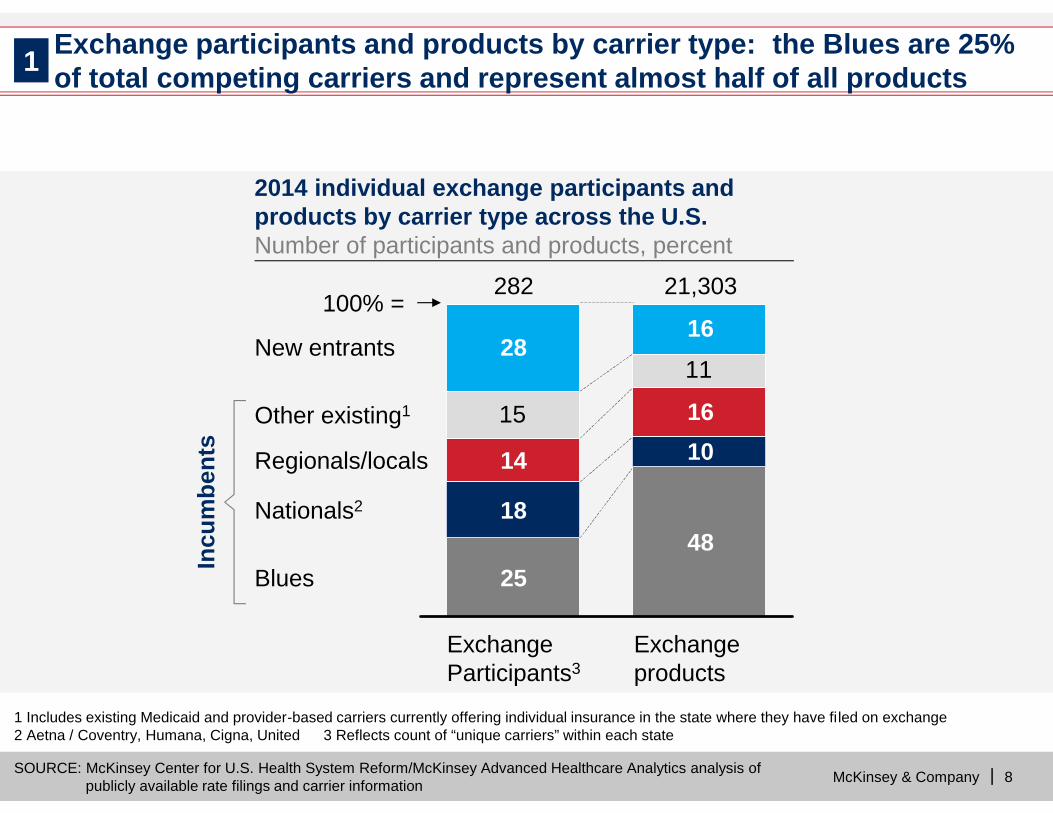

1 Includes existing Medicaid and provider-based carriers currently offering individual insurance in the state where they have filed on exchange2 Aetna / Coventry, Humana, Cigna, United 3 Reflects count of “unique carriers” within each state

Incu

mbe

nts

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

Exchange participants and products by carrier type: the Blues are 25%of total competing carriers and represent almost half of all products1

15

11

100% =

Blues

Nationals2

Regionals/locals

Other existing1

New entrants

Exchangeproducts

21,303

48

1016

16

ExchangeParticipants3

282

25

18

14

28

2014 individual exchange participants andproducts by carrier type across the U.S.Number of participants and products, percent

McKinsey & Company | 9

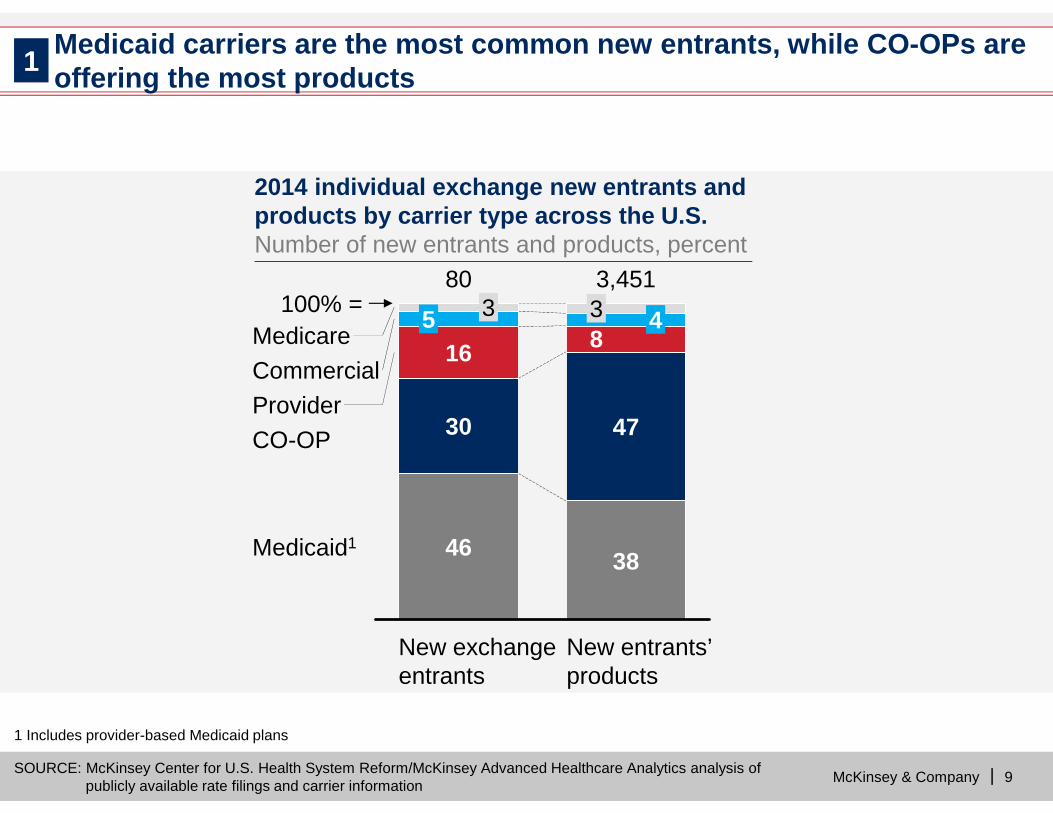

1 Includes provider-based Medicaid plans

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

Medicaid carriers are the most common new entrants, while CO-OPs areoffering the most products

3100% =

Medicaid1

CO-OPProviderCommercialMedicare

New entrants’products

3,451

38

47

84

80

46

30

165 3

New exchangeentrants

1

2014 individual exchange new entrants andproducts by carrier type across the U.S.Number of new entrants and products, percent

McKinsey & Company | 10

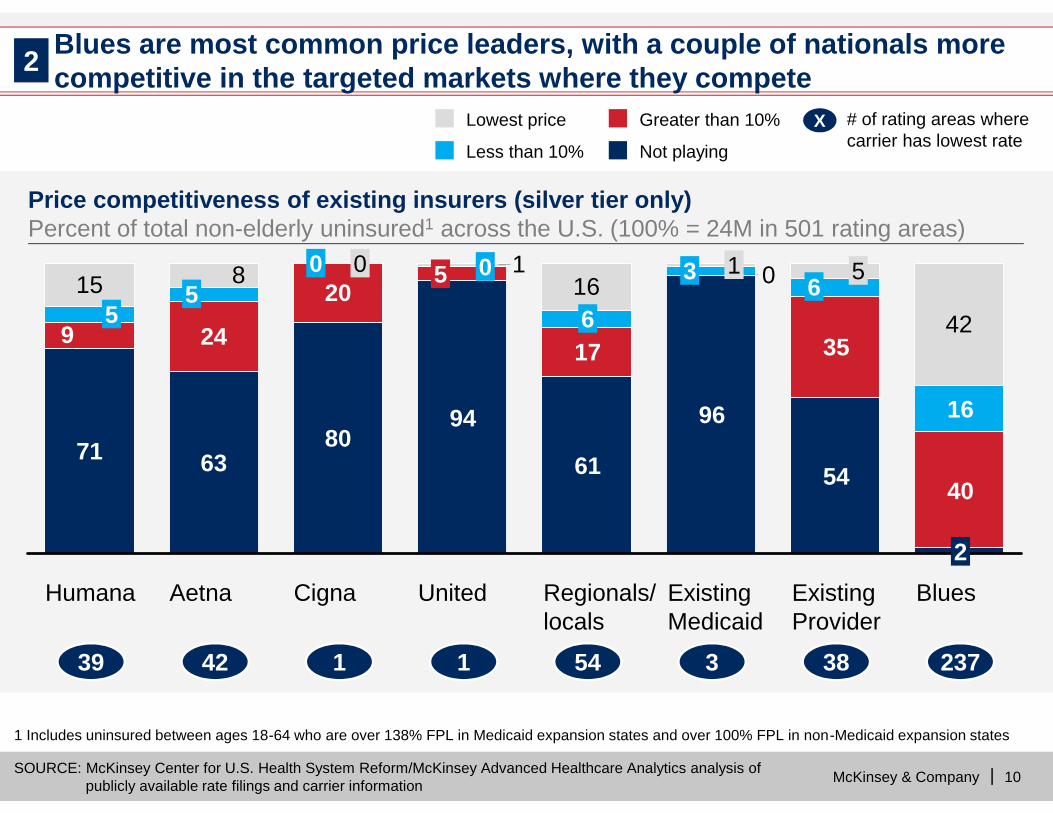

Blues are most common price leaders, with a couple of nationals morecompetitive in the targeted markets where they compete

1 Includes uninsured between ages 18-64 who are over 138% FPL in Medicaid expansion states and over 100% FPL in non-Medicaid expansion states

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

15 1642

018

Blues2

40

16

ExistingProvider

54

35

6 5

ExistingMedicaid

96

3 1

Regionals/locals

61

176

United

94

5 0

Cigna

80

200 0

Aetna

63

245

Humana

71

95

3939 2372374242 11 11 5454 33 3838

2

Not playing

Greater than 10%

Less than 10%

Lowest price XX # of rating areas wherecarrier has lowest rate

Price competitiveness of existing insurers (silver tier only)Percent of total non-elderly uninsured1 across the U.S. (100% = 24M in 501 rating areas)

McKinsey & Company | 11

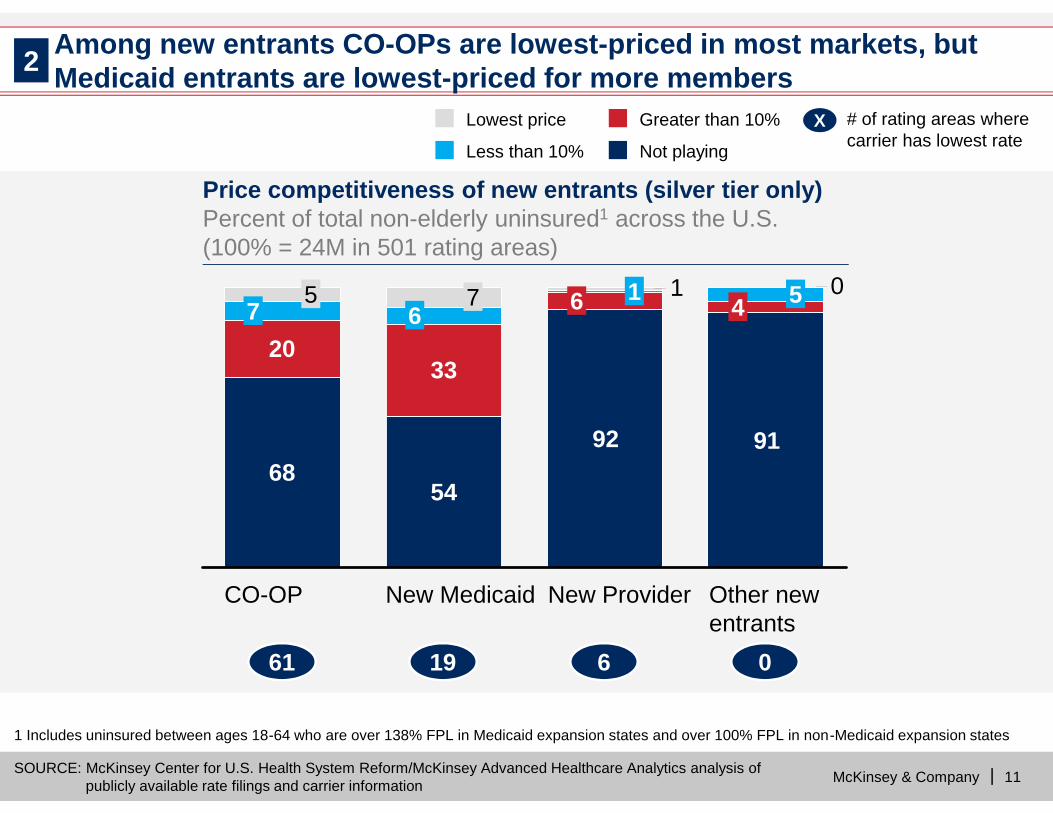

Among new entrants CO-OPs are lowest-priced in most markets, butMedicaid entrants are lowest-priced for more members

1 Includes uninsured between ages 18-64 who are over 138% FPL in Medicaid expansion states and over 100% FPL in non-Medicaid expansion states

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

016

7

CO-OP

68

Other newentrants

91

4 5

New Provider

92

6 1

New Medicaid

54

3320

7 5

6161 1919 66 00

2

XX # of rating areas wherecarrier has lowest rateNot playing

Greater than 10%

Less than 10%

Lowest price

Price competitiveness of new entrants (silver tier only)Percent of total non-elderly uninsured1 across the U.S.(100% = 24M in 501 rating areas)

McKinsey & Company | 12

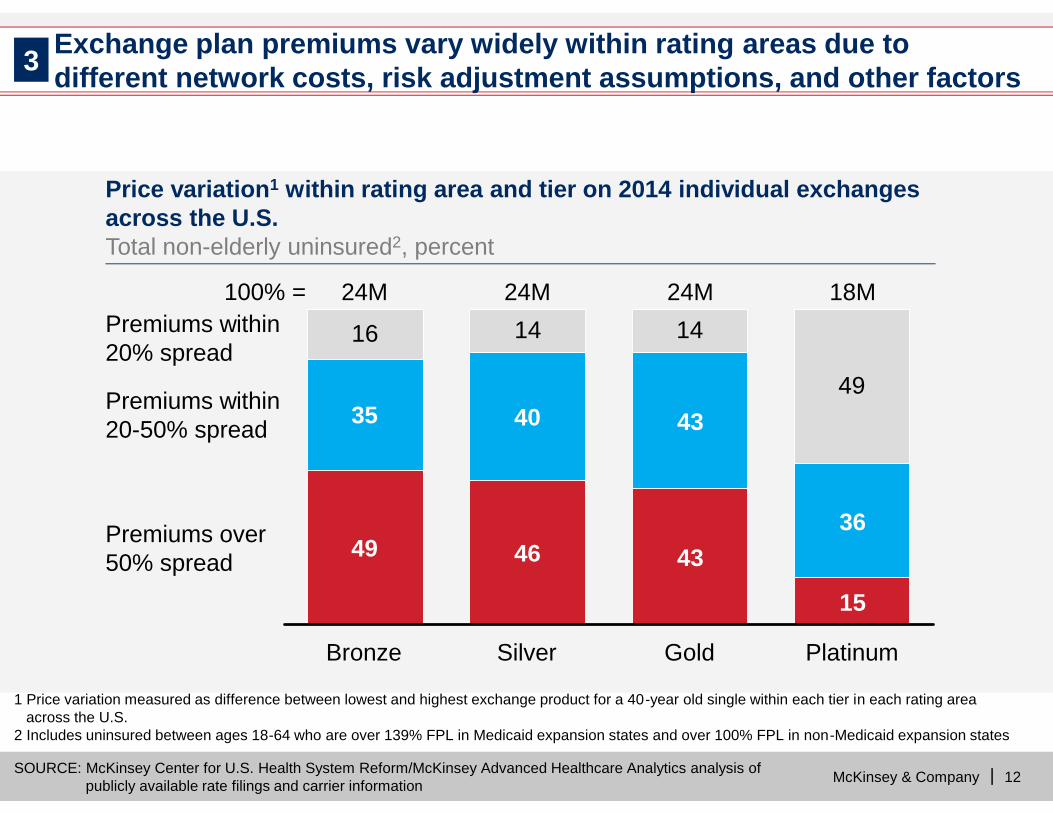

16 14 14

49

Gold

24M

43

43

Silver

24M

46

40

Bronze

24M

35

49

Premiums within20% spread

Platinum

18M100% =

Premiums over50% spread

Premiums within20-50% spread

15

36

1 Price variation measured as difference between lowest and highest exchange product for a 40-year old single within each tier in each rating areaacross the U.S.

2 Includes uninsured between ages 18-64 who are over 139% FPL in Medicaid expansion states and over 100% FPL in non-Medicaid expansion states

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

Exchange plan premiums vary widely within rating areas due todifferent network costs, risk adjustment assumptions, and other factors3

Price variation1 within rating area and tier on 2014 individual exchangesacross the U.S.Total non-elderly uninsured2, percent

McKinsey & Company | 13

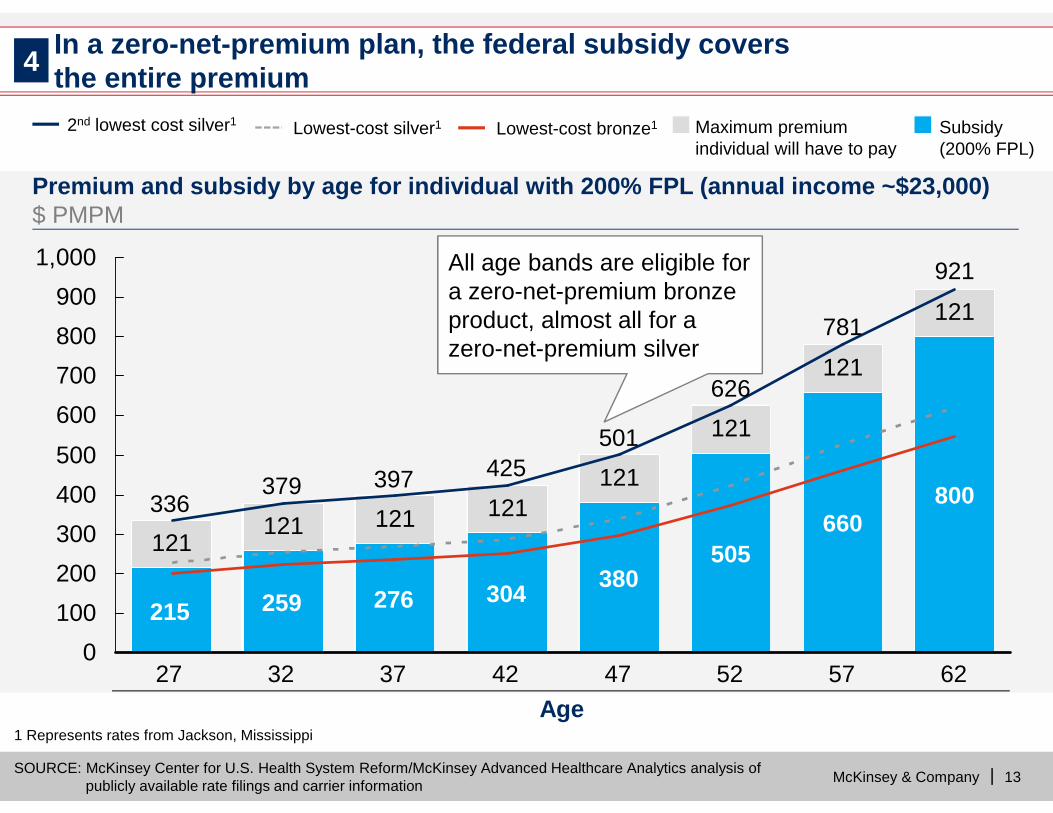

00

121121 121 121

121

121

121

121

0100200300400500600700800900

1,000

62

921

800

57

781

660

52

626

505

47

501

380

42

425

304

37

397

276

32

379

259

27

336

215

Age

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

In a zero-net-premium plan, the federal subsidy coversthe entire premium

1 Represents rates from Jackson, Mississippi

4

All age bands are eligible fora zero-net-premium bronzeproduct, almost all for azero-net-premium silver

Subsidy(200% FPL)

Lowest-cost silver1 Lowest-cost bronze1 Maximum premiumindividual will have to pay

2nd lowest cost silver1

Premium and subsidy by age for individual with 200% FPL (annual income ~$23,000)$ PMPM

McKinsey & Company | 14

AL

ARAZ

CACO

FL

GA

IA

ID

IL IN

KS

LA

MAMI

MN

MO

MS

NC

ND

NE

NM

NY

OK

OR

SCTN

TX

VA

VT

WA

WI

WV

WY

DCDE

NJ RI

AK

HI

MDNV UT

MT

SD

KY

OHPA

ME

NH

CT

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

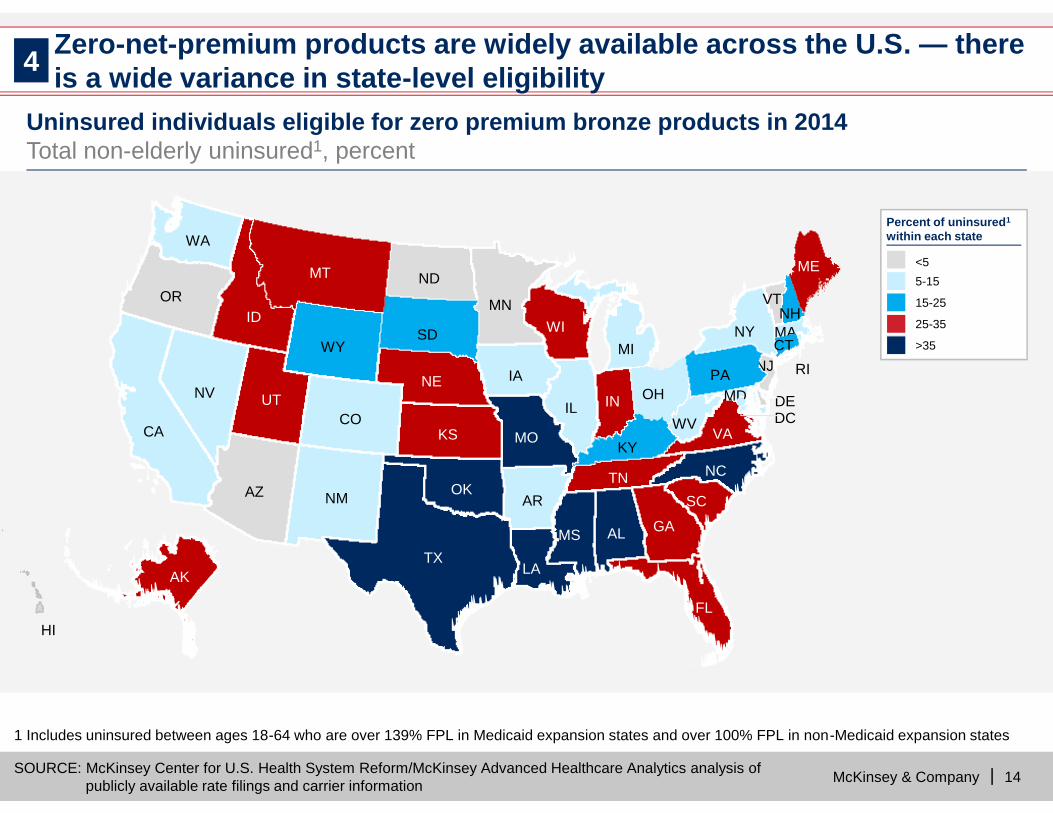

Zero-net-premium products are widely available across the U.S. — thereis a wide variance in state-level eligibility

<55-15

15-25

25-35

Percent of uninsured1

within each state

>35

1 Includes uninsured between ages 18-64 who are over 139% FPL in Medicaid expansion states and over 100% FPL in non-Medicaid expansion states

4

Uninsured individuals eligible for zero premium bronze products in 2014Total non-elderly uninsured1, percent

McKinsey & Company | 15

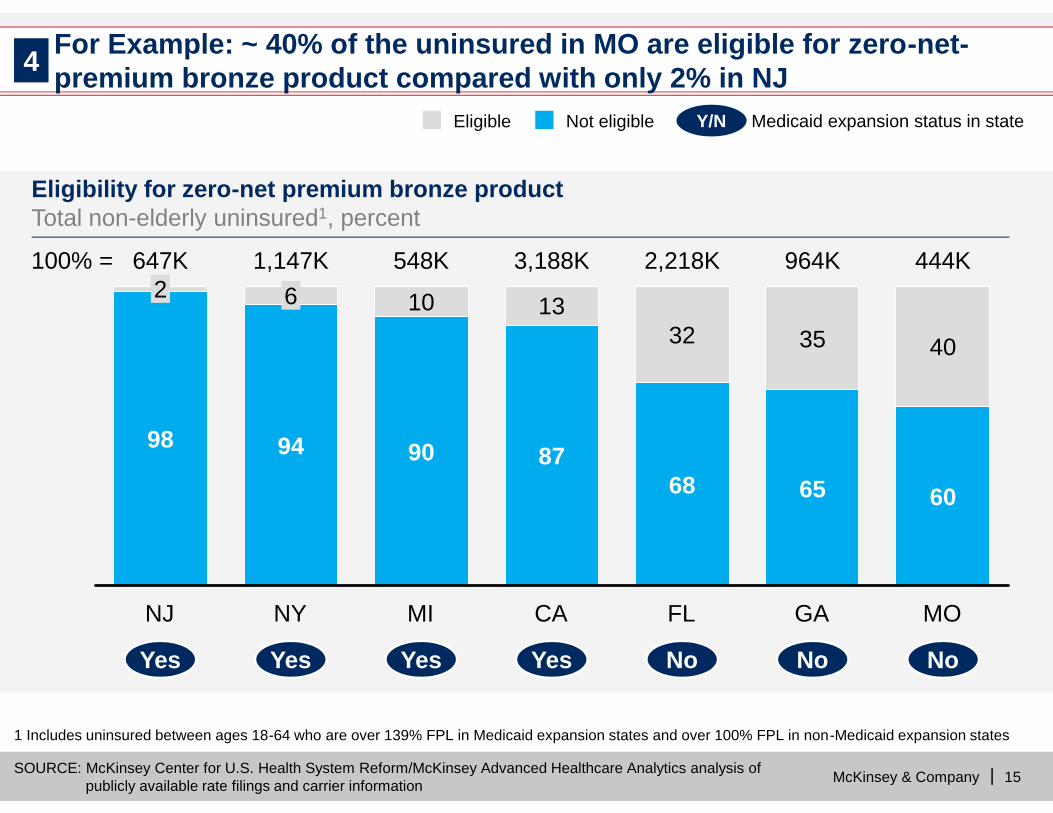

For Example: ~ 40% of the uninsured in MO are eligible for zero-net-premium bronze product compared with only 2% in NJ4

100% =

MO

444K

60

40

GA

964K

65

35

FL

2,218K

68

32

CA

3,188K

87

13

MI

548K

90

10

NY

1,147K

94

6

NJ

647K

98

2

1 Includes uninsured between ages 18-64 who are over 139% FPL in Medicaid expansion states and over 100% FPL in non-Medicaid expansion states

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

YesYes

Not eligibleEligible

YesYes YesYes YesYes NoNo NoNo NoNo

Y/NY/N Medicaid expansion status in state

Eligibility for zero-net premium bronze productTotal non-elderly uninsured1, percent

McKinsey & Company | 16

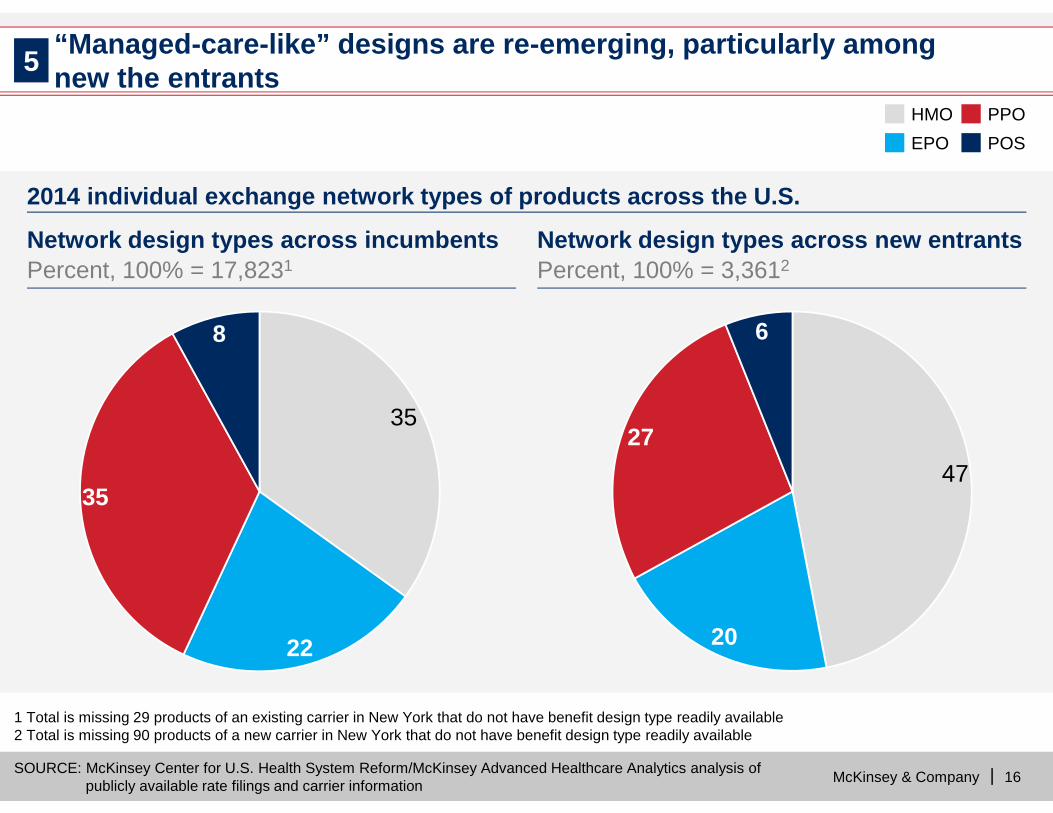

Network design types across incumbentsPercent, 100% = 17,8231

Network design types across new entrantsPercent, 100% = 3,3612

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

HMO PPOEPO POS

35

8

35

22

47

6

27

20

1 Total is missing 29 products of an existing carrier in New York that do not have benefit design type readily available2 Total is missing 90 products of a new carrier in New York that do not have benefit design type readily available

“Managed-care-like” designs are re-emerging, particularly amongnew the entrants5

2014 individual exchange network types of products across the U.S.

McKinsey & Company | 17

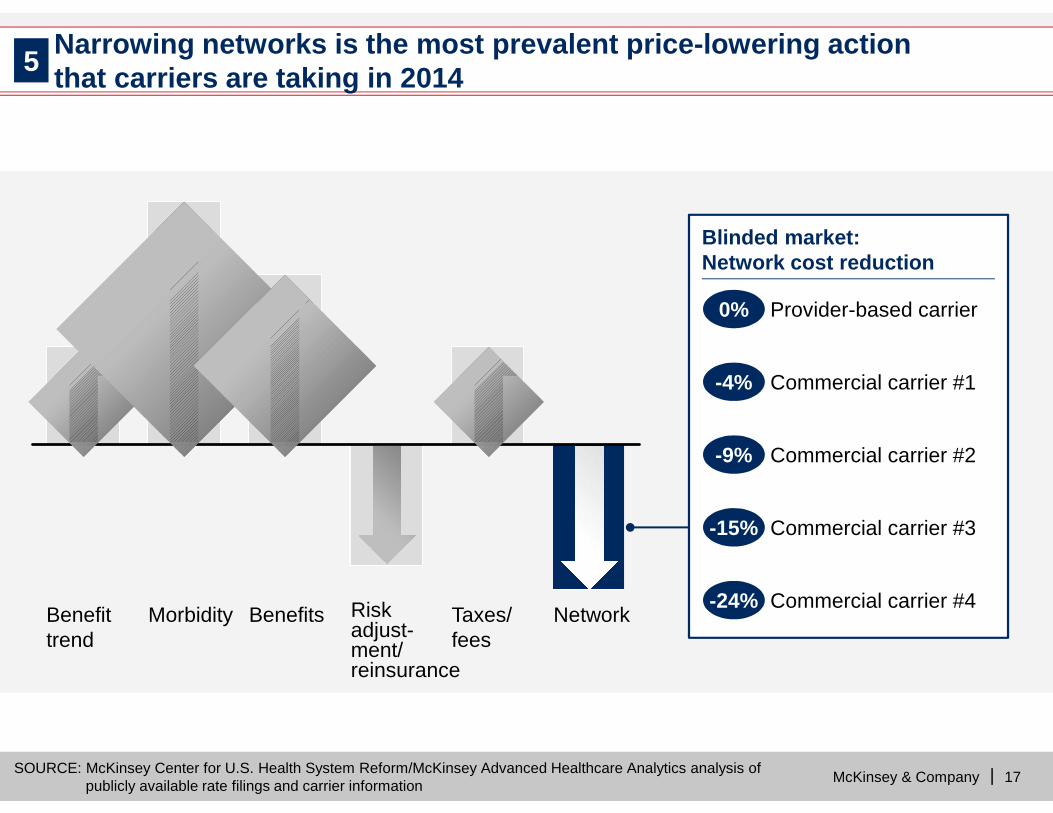

NetworkTaxes/fees

Riskadjust-ment/reinsurance

BenefitsMorbidityBenefittrend

Blinded market:Network cost reduction

Commercial carrier #4-24%-24%

Commercial carrier #3-15%-15%

Commercial carrier #2-9%-9%

Commercial carrier #1-4%-4%

Provider-based carrier0%0%

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analytics analysis ofpublicly available rate filings and carrier information

Narrowing networks is the most prevalent price-lowering actionthat carriers are taking in 20145

McKinsey & Company | 18

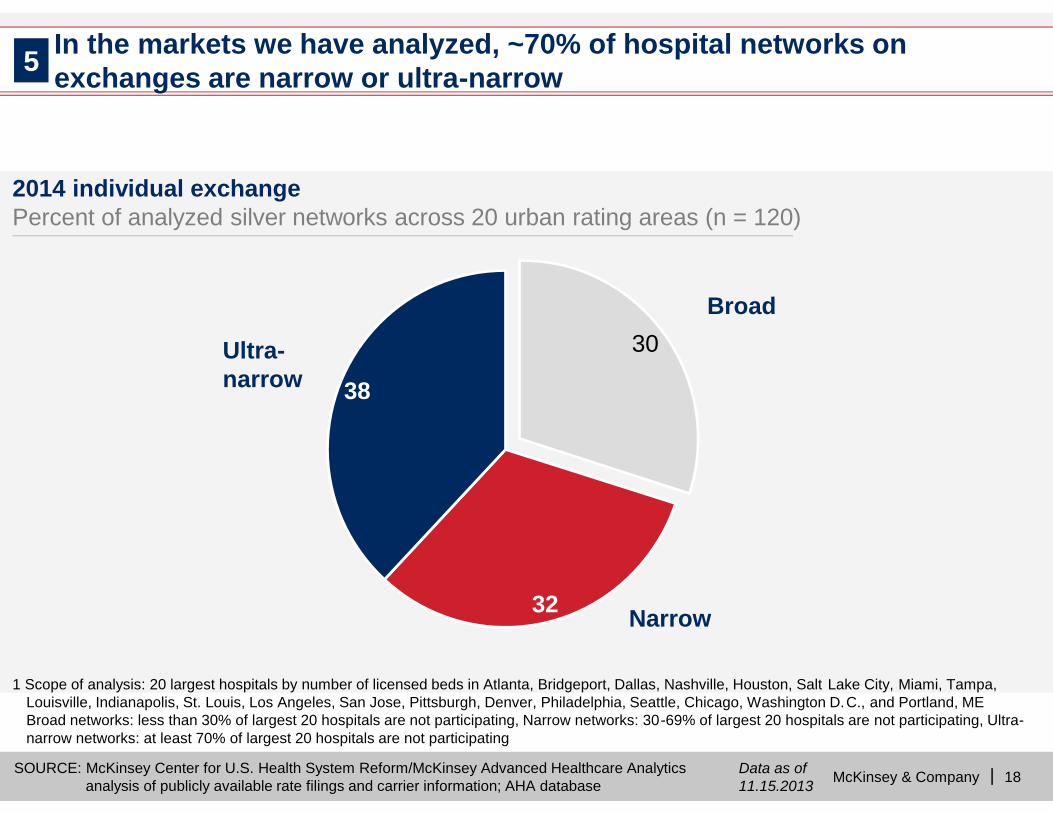

1 Scope of analysis: 20 largest hospitals by number of licensed beds in Atlanta, Bridgeport, Dallas, Nashville, Houston, Salt Lake City, Miami, Tampa,Louisville, Indianapolis, St. Louis, Los Angeles, San Jose, Pittsburgh, Denver, Philadelphia, Seattle, Chicago, Washington D.C., and Portland, MEBroad networks: less than 30% of largest 20 hospitals are not participating, Narrow networks: 30-69% of largest 20 hospitals are not participating, Ultra-narrow networks: at least 70% of largest 20 hospitals are not participating

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analyticsanalysis of publicly available rate filings and carrier information; AHA database

Data as of11.15.2013

30

38

32

Broad

Narrow

Ultra-narrow

2014 individual exchangePercent of analyzed silver networks across 20 urban rating areas (n = 120)

5 In the markets we have analyzed, ~70% of hospital networks onexchanges are narrow or ultra-narrow

McKinsey & Company | 19

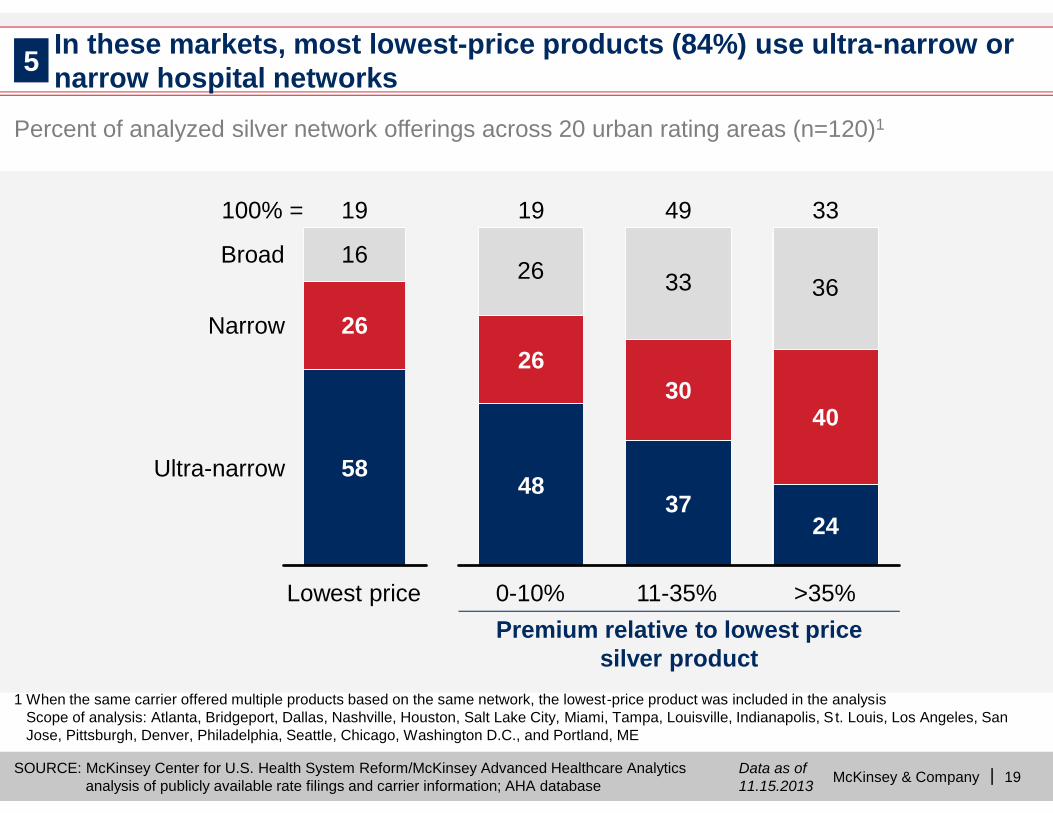

Percent of analyzed silver network offerings across 20 urban rating areas (n=120)1

1 When the same carrier offered multiple products based on the same network, the lowest-price product was included in the analysisScope of analysis: Atlanta, Bridgeport, Dallas, Nashville, Houston, Salt Lake City, Miami, Tampa, Louisville, Indianapolis, S t. Louis, Los Angeles, SanJose, Pittsburgh, Denver, Philadelphia, Seattle, Chicago, Washington D.C., and Portland, ME

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analyticsanalysis of publicly available rate filings and carrier information; AHA database

Data as of11.15.2013

In these markets, most lowest-price products (84%) use ultra-narrow ornarrow hospital networks5

26 33 36

0-10% >35%

33

24

40

11-35%

49

37

30

19

48

26

Lowest price

19

58

26

16

100% =

Ultra-narrow

Narrow

Broad

Premium relative to lowest pricesilver product

McKinsey & Company | 20

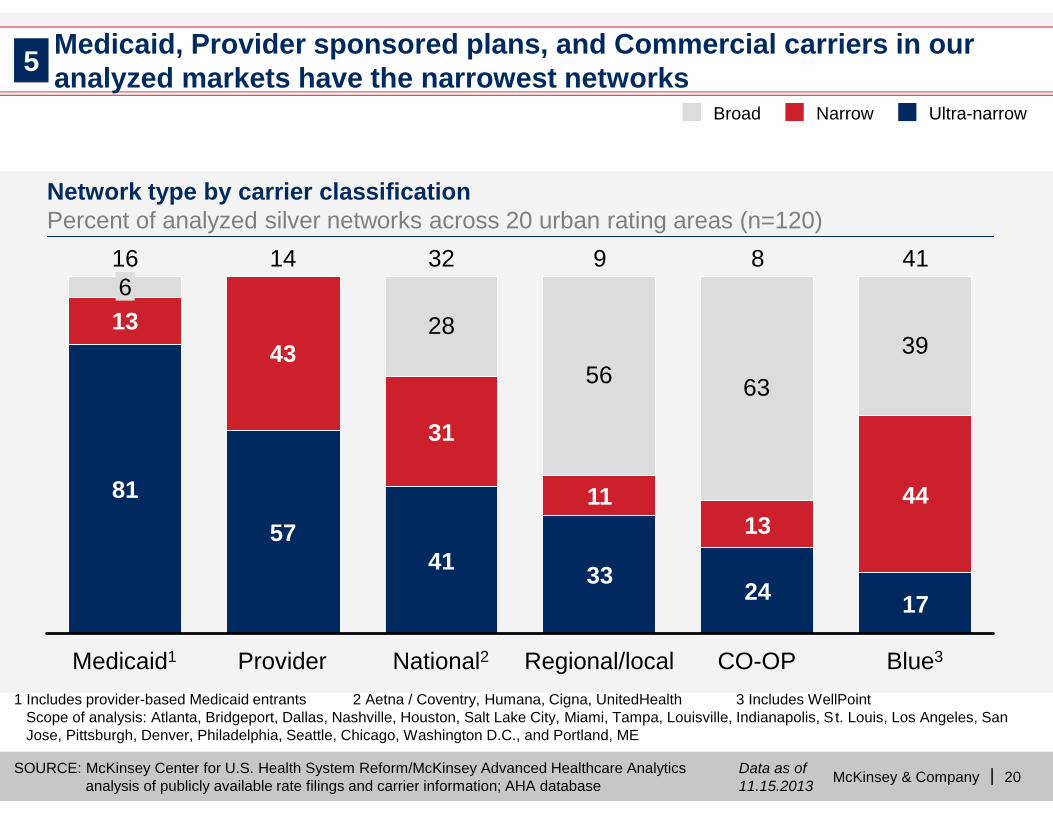

28

56 63

3913

41

31

Provider

14

57

43

Medicaid1

16

81

6

Blue3

41

17

44

CO-OP

8

24

13

Regional/local

9

33

11

National2

32

Ultra-narrowNarrowBroad

5

SOURCE: McKinsey Center for U.S. Health System Reform/McKinsey Advanced Healthcare Analyticsanalysis of publicly available rate filings and carrier information; AHA database

Data as of11.15.2013

1 Includes provider-based Medicaid entrants 2 Aetna / Coventry, Humana, Cigna, UnitedHealth 3 Includes WellPointScope of analysis: Atlanta, Bridgeport, Dallas, Nashville, Houston, Salt Lake City, Miami, Tampa, Louisville, Indianapolis, S t. Louis, Los Angeles, SanJose, Pittsburgh, Denver, Philadelphia, Seattle, Chicago, Washington D.C., and Portland, ME

Medicaid, Provider sponsored plans, and Commercial carriers in ouranalyzed markets have the narrowest networks

Network type by carrier classificationPercent of analyzed silver networks across 20 urban rating areas (n=120)

McKinsey & Company | 21

Our rate filing analyses suggest a number of early observations regardingthe new public exchange space

▪ The competitive landscape appears to have evolved with roughly a third ofincumbents not participating and significant number of new entrants emerging

▪ The Blues are the most common price leaders, nationals are price leaders intargeted markets, and CO-OPs are most often lowest priced among new entrants

▪ There is high degree of variation in prices both within and across markets,potentially driven by varying pricing assumptions by different carriers

▪ Zero-net-premium products (where the Federal subsidy covers the entire premium)are widely available which could have significant impact on uptake

▪ Our exchange simulations have indicated that price is the primary decision driver forconsumers. To reduce product cost, many carriers have used narrow networks

▪ Broader networks are also still often available, leaving the access and price tradeoffup to the consumer; this proliferation of products with varying breadths of hospitalnetworks is consistent with most well-functioning consumer markets – a variety ofchoices comprising different value propositions at different price points

We will continue to analyze consumer and competitor dynamics onpublic exchanges as these marketplaces unfold in 2014 and beyondWe will continue to analyze consumer and competitor dynamics onpublic exchanges as these marketplaces unfold in 2014 and beyond