20

EXECU TAX M UTIVE R MANAG RES Novem REPORT EMENT SEARCH mber 15, 20 SUMMA SYSTEM H 013 ARY MS

EXECU

TAX M

UTIVE R

MANAG

RES

Novem

REPORT

EMENT

SEARCH

mber 15, 20

SUMMA

SYSTEM

H

013

ARY

MS

2

TABLE OF CONTENTS

Background Research & Methodology .......................................................................... 3

Executive Summary ....................................................................................................... 4

Section I—General Information .................................................................................... 6

Population of Counties .............................................................................................. 6 Functions Tax Office Provides ................................................................................... 7 Number of Real Property Tax Bills ............................................................................. 8 Number of Personal Property Tax Bills ....................................................................... 9 Amount of Real Property Tax Dollars ....................................................................... 10 Real Property Tax Dollars as Percent of Jurisdiction’s Total Revenue ......................... 10 Changes in the Size of Office Staff ........................................................................... 11 Public Access Over the Internet to Property Tax Information .................................... 12 Tax Transactions on the Internet ............................................................................ 13 Present Tax Management System Integration with Other Offices ............................... 14 County Offices with which Tax Software Management Systems are Integrated ........... 15

Section II—Views on Tax Management Systems ........................................................ 16

Needs a Tax Management System is Required to Meet ............................................. 16 Technology Innovations and Trends of Value .......................................................... 17 Issues of Importance When Selecting a Vendor ...................................................... 18

3

BACKGROUND RESEARCH & METHODOLOGY

Advanced Analytics (AA), a division of Hidalgo & DeVries, Inc., was commissioned to conduct the jointly sponsored, Second Annual Thomson Reuters-National Association of Counties (NACo) Tax Systems Research Study (in association with the National Association of County Collectors, Treasurers and Finance Officers—NACCTFO), amongst tax officials in U.S. counties. On May 21, 2013, a self-administered online questionnaire was emailed to tax officials in counties across the country. The e-mailing database of 3,395 names was generated by NACo. As in last year’s study, a major objective of the research was to investigate the present views and future needs of tax officials, and to compare, where appropriate, 2013 results with those obtained in the 2012 study. The research topics covered both general information descriptive of the processes used, and services offered by the officials’ offices, as well as specifics regarding their views and ratings of various tax systems and their features and benefits. By the cutoff date of June 24, 2013, a total of 230 (6.8% response) questionnaires had been completed online. The information contained in the total number of completed questionnaires, forms the basis for this report. The following information presents a summary analysis of that data. About the Sponsors of this Study Thomson Reuters, the provider of Aumentum Tax—a leading software system in use in jurisdictions across the country—is the world's leading source of intelligent information for governments, businesses, and professionals. Combining industry expertise with innovative technology, we deliver critical information to leading decision makers. Aumentum simplifies the revenue management lifecycle for governments around the world. Our unique combination of technology enhanced by experience enables you to optimize revenue generation, support sustainable growth and improve services to the public. For more information about Aumentum Tax, visit tax.thomsonreuters.com/aumentum The National Association of Counties (NACo) is the only national organization that represents county governments in the United States. Founded in 1935, NACo provides essential services to the nation’s 3,068 counties. NACo advances issues with a unified voice before the federal government, improves the public's understanding of county government, assists counties in finding and sharing innovative solutions through education and research, and provides value-added services to save counties and taxpayers money. For more information about NACo, visit www.naco.org. Research Notes: Specific counties and county official are not identified in this report. E-mail addresses are not, and have not been matched to completed surveys, only recorded in order to provide an Executive Report of findings to all respondents who made such requests. All information is presented in aggregate form, with additional cross-tabs by county population where appropriate.

4

EXECUTIVE SUMMARY A. About the Respondents Size of Counties: Population size of responding counties ranged from less than 10,000 for the smallest responding county to a high of over one million for the largest. When grouped by size according to NACo’s grouping guidelines, responding counties offer a fair representation of the average population range of counties across the United States.

63% of responding counties=populations of <50K compared to 70.5%* nationally 12% of responding counties=populations of 50-100K compared to 12.5%* nationally 13% of responding counties=populations of 100-250K compared to 9.7%* nationally 12% of responding counties=populations of 250K> compared to 7.3%* nationally

*Source NACo

B. General Information Functions Provided: Nine in ten of respondent’s offices are responsible for collection/cashiering (97%) and property tax billing (87%). Seven in ten (73%) are responsible for revenue distribution and personal property tax billing (72%) and six in ten development of tax bills (59%). Property Tax Bills: When measured against the last reporting period, six in ten (57%) of respondents indicated an increase in the number of real property tax bills their office sent, with an average increase of 1.5% for all respondents reporting an increase. And while 38% of respondents reported no change in the number of real property tax bills sent by their offices, only 5% of respondents indicated a decrease which averaged 2.0% for this group. Property Tax Collected: When measured against the last reporting period, more than six in ten (65%) of respondents’ offices indicated an increase in the number of real property tax dollars collected, with an average increase of 2.0% for all respondents. And while 21% of respondents reported no change in the number of real property tax dollars collected by their offices, a low of 14% of respondents indicated a decrease which averaged 2.0% for this group.

Staff Size: When compared to the previous year there was a decrease of 28 basis points in offices reporting staff reductions—12% vs. 40%, with eight in 10 (83%) of respondents’ reporting no change in the size of office staff, and 5% indicating an increase averaging 1.5% FTE’s. The continued trend of decrease of staff reductions which began the previous year, combined with an increase—albeit modest, in hiring point to not only market stabilization, but growth.

5

Access to Data: Eight in ten (80%) of respondents provide access to property tax information over the internet. Of the respondents that allow public access to property tax information over the internet, 82% indicated they allow transactions such as payments of taxes—resulting in an average of 10% of taxes paid over the internet.

Integration with Other Offices: With no change since the last reporting period, more than three quarters (78%) of respondents indicated that their Tax system is integrated with other county office systems—Assessor (86%), Treasurer (68%), GIS (50%), and Auditor (50%).

C. Views on TAX Systems Needs System Must Meet: When ranking the most important jurisdictional needs that a TAX system must meet, the majority (65%) of respondents identified: Improving accuracy of tax bills as their first or second need, followed by improvement on efficiency and productivity of staff (52%), and improving reliability of data (43%).

New Technology: Based on what they believe to be the most valuable technology trends to their offices, respondents ranked Mobile highest at 75%, followed by eGovernment (42%) and Cloud (31%).

Vendor Selection Issues: When ranking the issues that are “Very Important” or “Important” to their jurisdictions when selecting a vendor, all (100%) of respondents ranked support after installation and training quality first, followed by Tax Domain Knowledge and Experience (99%), Conversion Expertise (97%), Periodic System Enhancements Provided (97%), Cost (95%), Leading Edge Technology (90%), and Certified Project Management Expertise (89%).

Populat Six in tenwith 46%the balanof responpopulatio250,000

tion of Coun

n (63%) of r% of those rence indicatedndents reporons above 10(13%), 250,

Se

nties

respondents eporting a pod a populatiorted a popula00K amount,001 to 500,

ection I—G

reported theopulation beon between ation betweeed to almost,000 (5%), a

6

General Info

e populationetween 10,0025,001 and en 50,001 at one fourth and 500,001

ormation

n of their cou01 and 25,050,000. Slignd 100,000, (24%) of a

1 to 2,000,00

unty to be 5000 and less ghtly over on, while counll responden00 (6%).

50,000 or lesthan 10,000

ne in ten (12ties reportin

nts—101,001

ss, 0 and 2%) ng 1 to

TaxDevProPerColRevMotBusSpeTaxOth

Function Nine in teBilling (8Personal Functions(45%), M(22%), a

x Assessmenvelopment ooperty Tax Birsonal Propelection/Cashvenue Distribtor Vehicle Tsiness Tax oecial Assessmx Sales her self-repo

ns Tax Offi

en of respon7%) are funProperty Tas indicated bMotor Vehicleand Taxes As

Fun

nt of Tax Bills illing rty Tax Billin

hiering bution Tags r Licenses ment Tax

orted taxes

ce Provide

ndents indicanctions withiax Billing (72by less than e Tags (26%ssessment (1

nctions Tax

ng

es

ated that Con their office

2%), Developfive out of t

%), other sel17%).

x Office Pro

Less tha50,000

18%52%90%73%95%76%28%23%41%46%20%

7

ollection/Cashes, followed pment of Taten respondef-reported ta

ovides (By C

an 0

50,10

hiering (97%by Revenue

ax Bills (59%ents were Spaxes (23%),

County Pop

,001 to 00,000 19% 57% 82% 79% 93% 71% 19% 10% 38% 57% 29%

%) %) and Pe Distribution

%), and Tax Special Asses, Business T

pulation)

100,000 250,00

13% 87% 93% 83% 100% 70% 30% 26% 57% 65% 26%

Property Taxn (73%), Sales (50%)sment Tax ax or Licens

to 0 25

x

).

ses

50,000+

11% 74% 81% 74% 100% 87% 21% 21% 15% 47% 37%

Les10,25,50,1012505007501,0

Number

More thaby their onumber tless thanthe numbthe numbbetween

ss than 10,00001 to 25, 0001 to 50,00001 to 100,01,001 to 2500,001 to 5000, 001 to 7500,001 to 1,0000,000 +

Increase

Almost siTax bills of 1.5%)sent. Onl

r of Real Pr

an half (55%office duringto be betwee

n 10,000 billsber to be beber of Real P100,001 an

Numb

00 000 00 000 0,000 0,000 0,000 00,000

e vs. Decre

ix in ten (57that their of

), while 38%ly 5% of res

roperty Tax

%) of all respg the last billen 10,001 as sent last bietween 25,00Property Taxd 1,000,000

ber of Real Less than

50,000 37% 43% 20% 1% 0% 0% 0% 0% 0%

ease

%) of respoffice sent du

% of respondespondents in

x Bills

ondents estiing period tond 25,000 willing period.01 and 100,0x bills sent b0+.

Property T 50,00

ondents indicring 2012 bients reportedicated a de

8

imated the no be less tha

with the rema. About four 000. The rem

by their office

Tax bills (B

01 to 100,0

10% 14% 43% 33% 0% 0% 0% 0% 0%

cated an incrilling period ed no changeecrease whic

number of Ran 25,000. Oaining 25% in ten (36%

maining 9% e during the

By County P

000

rease in the compared toe in the numch averaged

Real PropertyOf those, 30indicating th

%) of responof responde

e last billing p

Population)100,000 t

250,0000% 4% 9% 78% 9% 0% 0% 0% 0%

number of o 2011 (an a

mber of real 2.0% for th

y Tax bills se% indicatedhe number tdents indicaents estimatperiod to be

) to 0 25

Real Propertaverage incrproperty tax

his group.

ent the to be ated ted e

50,000+

5% 5% 11% 11% 32% 32% 5% 0% 0%

ty rease x bills

Less1,002, 55,007,5010,0

Number Nearly hanumber o1,000. Thbetween 4% betw

s than 1,000 01 to 2,500 501 to 5,000 01 to 7,500 00 to 10,000 000 +

Increase

Two thirdsent durioffices re

r of Person

alf (48%) ofof personal phe remaining1,001 and 2

ween 7,501 a

Numb

e vs. Decre

ds of offices ng the 2012

eported an a

al Property

f respondentproperty taxg 52% of res2,500, 11% and 10,000.

ber of PersoLess than

50,000 61% 16% 8% 4% 1% 10%

ease

(65%) repo2 billing perioaverage incre

y Tax Bills

ts—a 20% inx bills sent byspondents inbetween 2,5

onal Property

50,0

orted no chaod comparedease of 1.5%

9

ncrease fromy their officendicated the501 and 5,00

y Tax Bills (

01 to 100,0

26% 5% 32% 21% 5% 11%

nge in the nd to the 201

% while 16%

m the previoue for the laste following: 100, 9% betw

(By County P

000 100

number of pe11 billing per% reported a

us year—indt billing perio16% sent ouween 5,001 a

Population)

0,000 to 25

32% 9% 14% 23% 9% 14%

ersonal propriod. Of the b decrease, a

dicated the od are less tut 10,001+, and 7,500, a

0,000 25

perty tax billsbalance, 19%also of 1.5%

than 12%

and

50,000+

16% 0% 11% 11% 11% 53%

s % of

%.

Amount

More thatotal amothe 2011

Real Pro

Increase DecreaseNo Chang

Real Pro

Perc

t of Real Pr

an six in ten ount of Real billing perio

operty Tax

R

e ge

operty Tax

cent of Resp20% 29% 24% 27%

roperty Tax

(65%) of reProperty Ta

od—while 14

Dollars Inc

Real PropeLess th

50,0068%10%22%

Dollars as

pondents

x Dollars Co

espondents’ oax dollars co4% indicated

crease/Dec

erty Tax Dohan 00

5

% % %

Percent of

% of Tota0-265176-

10

ollected

offices indicallected durind a decrease

crease by C

ollars (By C50,001 to 100,000

68% 11% 21%

f Total Cou

al Revenue-25 6-50 -75 -100

ated an increng the 2012 e also averag

County Pop

County Pop100,0

250,572419

nty Revenu

ease averagbilling perio

ging 2%.

pulation

ulation) 000 to ,000 % % %

ue

ging 2% in tod compared

250,000

58% 26% 16%

the d to

+

Changes

When coreportingchange incontinuedan increa

Reasons

AccordingCuts (41%saw an inTechnolo

Increa

No ChangDecreaseIncrease

s in the Siz

mpared to tg staff reductn the size ofd trend of dease—albeit m

s for Chang

g to respond%), Retiremncrease in stogy (29%).

ase/Decrea

ge e

ze of Office

he previous tions—12% f office staff,ecrease of s

modest, in hi

ges in Staff

dents who sament (29%), taff size, the

ase of Size Less t

50,091%7%2%

e Staff

year there wvs. 40%, w

, and 5% indstaff reductioiring point to

f Size

aw a decreaand Use of T

e leading rea

of Office Sthan 000

5

% % %

11

was a decreaith eight in 1dicating an ions which beo not only m

se in staff siTechnology asons were:

Staff During50,000 to 100,000

87% 7% 7%

ase of 28 ba10 (83%) ofncrease aveegan the pre

market stabili

ize, the lead(29%). AccoIncreased W

g 2012(By 100,00

250,058%37%5%

asis points inf respondenteraging 1.5%evious year, ization, but g

ding reasonsording to res

Workload (86

County Po00 to 000 2

% % %

n offices ts’ reporting

% FTE’s. Thecombined wgrowth.

were: Budgspondents w6%) and Use

opulation)

250,000+

68% 16% 16%

no e with

get who e of

Public A

Eight in tover the

Public A

Yes

No

Access Over

ten (79%) ointernet.

Access Ove

r the Intern

f all respond

er the InterLess th

50,0073%

27%

net to Prop

dents’ offices

rnet to Prophan 00

5

%

%

12

perty Tax I

s allow the p

perty Tax I50,001 to 100,000

73%

27%

Information

public to acc

Informatio100,0

250,95

5%

n

cess property

on (By Coun000 to ,000 %

%

y tax inform

nty Populat

250,000

100%

0%

ation

tion)

+

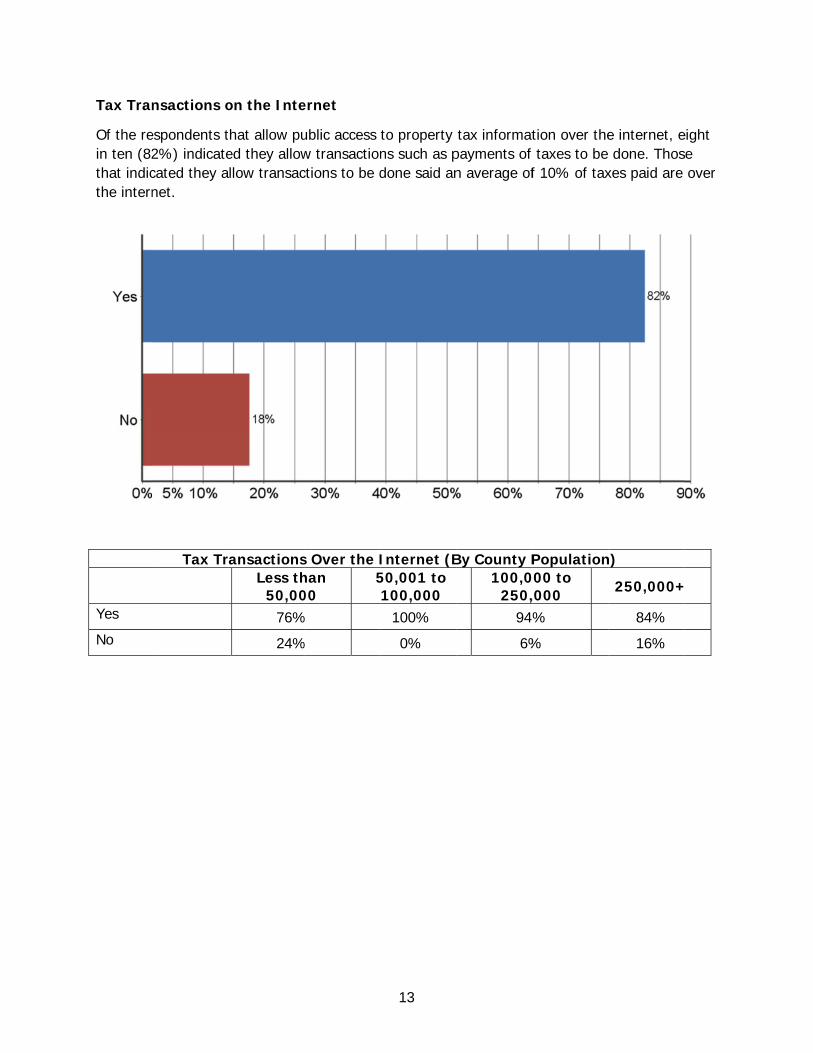

Tax Tran

Of the rein ten (82that indicthe intern

Yes

No

nsactions o

espondents t2%) indicatecated they anet.

Tax Tr

on the Inte

that allow pued they allowllow transac

ransactionsLess th

50,0076%

24%

ernet

ublic access w transactionctions to be d

s Over the Ihan 00

5

%

%

13

to property ns such as pdone said an

Internet (B50,001 to 100,000

100%

0%

tax informatpayments of n average of

By County P100,0

250,94

6%

tion over thetaxes to be

f 10% of tax

Population000 to ,000 %

%

e internet, edone. Thos

xes paid are

n)

250,000+

84%

16%

eight se

over

+

Present

Nearly eiother jur

Present

Yes No

Tax Manag

ght in ten (7isdictional of

t Tax Syste

gement Sy

78%) of all rffices.

m IntegratLess than

50,000 82% 18%

ystem Integ

respondents

tion with On 50

10

14

gration wit

indicated th

Other Count0,001 to 00,000 67% 33%

th Other Of

hey have int

ty Offices (100,00

250,079%21%

ffices

tegrated thei

(By County00 to 000 % %

ir TMS with

y Populatio

250,000+

67% 33%

on)

County

Of those with counTreasure

Offices wit

respondentsnty offices, t

er (68%), GI

th which Ta

s that indicathe majority S (50%), an

ax Softwar

ated integrat(86%) said

nd Auditor (5

15

re Managem

ting their pretheir system

50%) followe

ment Syste

esent tax sofm is integrated.

ems are Int

ftware manated with an A

tegrated

agement sysAssessor.

stems

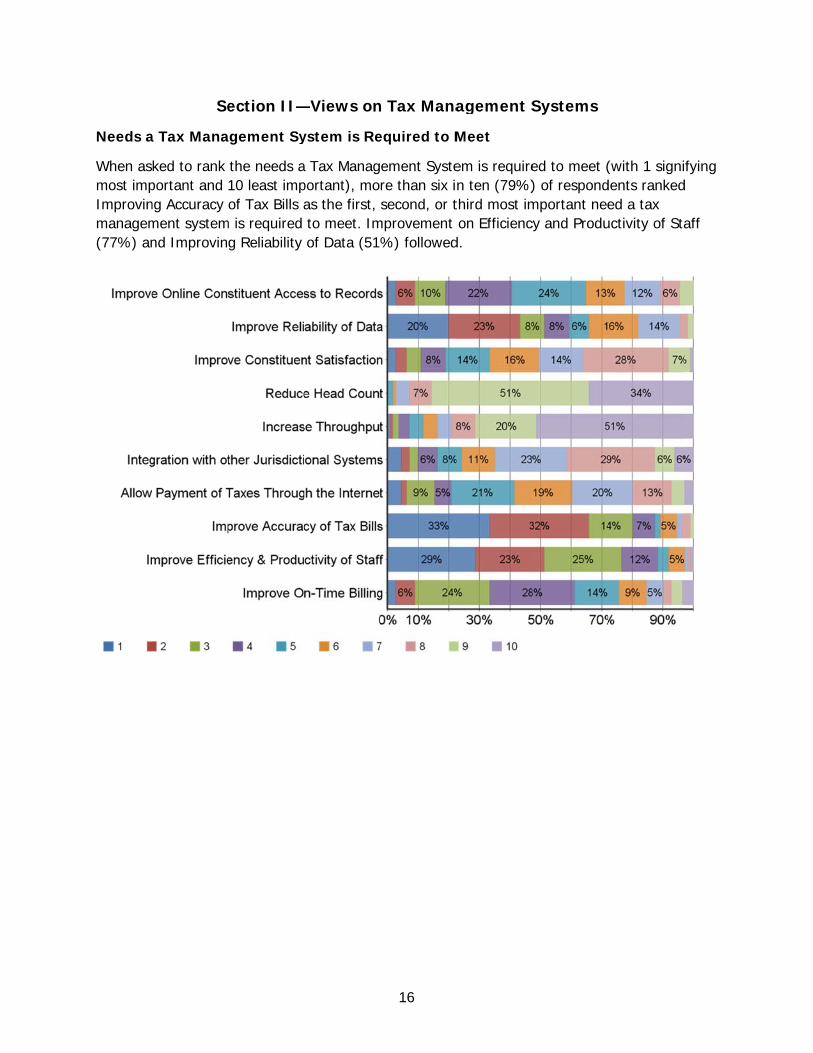

Needs a

When asmost impImprovinmanagem(77%) an

Se

a Tax Mana

ked to rank portant and ng Accuracy ment systemnd Improvin

ection II—

agement Sy

the needs a10 least impof Tax Bills a

m is required g Reliability

—Views on

ystem is Re

a Tax Managportant), moas the first,to meet. Imof Data (51

16

n Tax Mana

equired to M

ement Systere than six isecond, or t

mprovement %) followed

agement S

Meet

em is requiren ten (79%)third most imon Efficienc

d.

Systems

ed to meet () of respondmportant neecy and Produ

(with 1 signidents rankeded a tax uctivity of Sta

fying d

aff

Technol

When asand 10 lefirst, secoand eGov

logy Innova

ked to rank east importaond, or thirdvernment (5

ations and

the most imnt), more th

d most valua51%).

Trends of

mportant techhan eight in able technolo

17

Value

hnology trenten (84%) oogy innovatio

nds (with 1 sof respondenon or trend,

signifying monts ranked M followed by

ost importanMobile as they Cloud (54%

nt e %)

Issues o

Respondemanagemfollowed Periodic Sand Certi

of Importan

ents indicatement systemby Tax DomSystem Enhaified Project

nce When

ed that the km provider armain Knowledancements PManagemen

Selecting a

key issues (Vre: Support Adge and ExpProvided (97nt Expertise

18

a Vendor

Very ImportaAfter Installaperience (997%), Cost (9(89%).

ant or Impoation and Tr%), Convers

95%), Leadin

rtant) when aining Qualision Expertisng Edge Tec

selecting a ty (100%), se (97%), chnology (90

tax

0%),

19

Issues of Importance When Selecting a Vendor (By County Population)

Less than 50,000

50,001 to 100,000

101,001 to 250,000 250,000+

Provides a Scalable System Very Important 27% 42% 23% 19% Important 59% 25% 46% 63% Somewhat Important 11% 33% 23% 19% Not Important 3% 0% 8% 0%

No “Offshoring” of Design and Development Very Important 43% 50% 54% 44% Important 41% 25% 31% 19% Somewhat Important 13% 25% 8% 31% Not Important 3% 0% 8% 6%

Provides Periodic System Enhancements Very Important 64% 358% 69% 63% Important 31% 42% 31% 38% Somewhat Important 3% 0% 0% 0% Not Important 1% 0% 0% 0%

Local Sales/Support Representation Very Important 57% 42% 38% 38% Important 27% 25% 31% 25% Somewhat Important 16% 25% 23% 19% Not Important 0% 8% 8% 19%

Ability to Host Solution Very Important 56% 42% 23% 6% Important 31% 25% 23% 50% Somewhat Important 9% 33% 38% 38% Not Important 4% 0% 15% 6%

Cost Very Important 77% 75% 62% 44% Important 21% 8% 38% 44% Somewhat Important 1% 17% 0% 13% Not Important 0% 0% 0% 0%

Robust Base of Successful Deployments Very Important 37% 42% 54% 56% Important 47% 50% 46% 31% Somewhat Important 14% 8% 0% 13% Not Important 1% 0% 0% 0%

Certified Project Management Expertise Very Important 46% 50% 38% 50% Important 44% 42% 54% 31% Somewhat Important 6% 8% 8% 13% Not Important 4% 0% 0% 6%

Tax Domain Knowledge & Experience Very Important 86% 92% 69% 88% Important 13% 8% 31% 13% Somewhat Important 1% 0% 0% 0% Not Important 0% 0% 0% 0%

Training Quality Very Important 91% 83% 69% 69% Important 9% 17% 31% 31% Somewhat Important 0% 0% 0% 0% Not Important 0% 0% 0% 0%

Conversion Expertise Very Important 79% 75% 85% 75% Important 21% 25% 15% 6% Somewhat Important 0% 0% 0% 19% Not Important 0% 0% 0% 0%

Support After Installation Very Important 94% 83% 92% 94% Important 6% 17% 8% 6% Somewhat Important 0% 0% 0% 0% Not Important 0% 0% 0% 0%

Prior Experience with Your Jurisdiction Very Important 39% 25% 23% 25% Important 34% 8% 23% 38% Somewhat Important 21% 42% 38% 31% Not Important 6% 25% 15% 6%

Local vs. National Presence Very Important 36% 25% 31% 13% Important 36% 17% 23% 44% Somewhat Important 20% 50% 38% 31% Not Important 9% 8% 8% 13%

Leading Edge Technology Very Important 50% 42% 69% 44% Important 39% 50% 23% 50% Somewhat Important 10% 8% 8% 6% Not Important 1% 0% 0% 0%

20

![Architecture Portfolio [2012-2015] Ileana Cristina Balan](https://static.documents.pub/doc/80x56/57906d3c1a28ab68748f1cef/architecture-portfolio-2012-2015-ileana-cristina-balan.jpg)