36

Exemptions and Excise Helpful information for Clerks

Exemptions and ExciseHelpful information for Clerks

Qualifications for all Real Estate Personal Exemptions

• Applicants must file an application for each fiscal year with the assessors in

the city or town where their property is located. The application is due on

December 15, or three months after the actual tax bills are mailed,

whichever is later.

• Applicants can only be granted one statutory exemption for each Fiscal

year except Clauses 18, 18A, 41A, & 45. If they qualify for more than 1

exemption they would be granted the Exemption that provides the greatest

benefit for them.

• Own the property as of July 1st

For properties held in a Trust the applicant must have both legal and

beneficial interest in the property

For properties in a Life Estate the applicant must be the life tenant of

the property

• Occupy the property as of July 1st as their domicile

• Meet statutory requirements for the exemption they are applying for.

Qualifications for all Real Estate Personal Exemptions, cont’d

• A married couple can qualify for 2 exemptions.

– Example – Husband is a Veteran with a service-connected disability. The wife qualifies under clause 41C. They each must qualify according to the requirements of the clause exemption for which they are applying.

– Example – Two owners, tenants in common, not married, can also qualify for 2 different exemptions . The Veteran will receive 100% of the exemption, however the co-owner will only receive 50% of Clause 41C exemption provided the co-owner meets all statutory requirements of the exemption for which application is made.

– Exception – If both husband and wife are owners and qualified Veterans, each can receive a Clause 22 $400 veterans exemption.

REAL ESTATE EXEMPTIONS FOR SENIORS

Clause 41

Statutory Exemptions Clause 41

• Documentation requirements may include but are not limited to: – Birth Certificate

– Evidence of ownership, domicile & occupancy

– Income tax returns, income statements & bank and other asset account statements

• Age Requirements: Must be 70 years or older as of July 1st. Local option can change the age requirement to no less than 65 years. – Clause 41C & 41C-1/2

• Additional ownership requirements: – Must have had a domicile in MA for the 10 preceding years & owned the property or any

other property in MA for any 5 years. (The 10 year continuous domicile requirement for Clause 41C½ may be reduced to 5 years by vote of the legislative body of your city or town.)

– If property is owned with someone besides the applicant that is not the applicant’s spouse, the exemption granted will be equal to the percentage of the ownership interest in the property. The co-owners must also meet the income and asset requirements. If they do not qualify for Clause 41 they may be eligible for Clause 17.

Statutory Exemptions Clause 41 -continued

• Income Limits: Gross receipts from all income sources for the previous calendar year cannot exceed the specified limit.

– Combined income of the applicant and their spouse, if applicable.

– Ordinary business expenses and losses are deducted but personal or family expense are not.

– The minimum social security allowance that is set by the DOR is deducted.

• Asset Limits: Whole Estate as of July 1st cannot exceed the specified limit.

– Not including the value of your home, unless it exceeds two dwelling units (i.e. three family).

– This does include all money in the bank, stocks, bonds, IRAs, any other real estate, etc.

SURVIVING SPOUSE, SURVIVING MINOR & ELDERLY

Clause 17

Statutory Exemptions Clause 17

• Documentation requirements may include but are not limited to: – Death Certificate

– Birth Certificate

– Evidence of ownership, domicile & occupancy

– Bank and other asset account statements

• Status Requirements: (Must meet one of the below requirements as of July 1st)

– Widow/Widower

– Minor child of a deceased parent

– Person 70 years or older (That have owned & occupied the property as their domicile for not less than 10 years or 5 if local option was accepted)

• Asset Limits: Whole Estate as of July 1st cannot exceed the specified limit.– Under Clause 17D, it does not include the value of your home, unless it produces

income and exceeds two dwelling units. (i.e. three family).

– This does include all money in the bank, stocks, bonds, IRAs, automobiles, any other real estate, etc.

Exemption LimitsBased on Chapter 59, Section 5C.

• No exemption can reduce the amount of taxable value to less than 10 percent of the total Full & Fair Cash Value.

SENIOR WORK-OFF PROGRAMSCan vary from Town to Town.

Acceptance of statue is a vote of the town meeting, town council or city council with mayor’s approval where required by law.

Senior Work Property Tax Work off AbatementGL Chapter 59, Sec.5K

SCOPE OF ABATEMENT:

1. AGE- Must be 60 years of age or older.

2. OWNERSHIP – Must be the assessed owner of the property on which the tax is assessed or acquired ownership before the work is performed and the abatement applied.

3. MAXIMUM ABATEMENT AND HOURLY RATE: Maximum abatement they may earn is $1,000. Hourly rate cannot be higher than minimum wage allowed by the state. As of January 1, 2015-that rate is $9.00 per hr. & Fed. rate is $ 7.25 an hr-since 2009.

4. PERSONAL EXEMPTIONS AND DEFERRALS: Taxpayers may earn abatements under the work-off program in addition to any property tax exemptions they may be eligible for under other statues. And then they may also defer the balance of their taxes if eligible!!

IGR No. 02-210 on Senior Work ProgramDetails of the Senior tax work-off abatement

• Website has detailed information.

• MODEL of a Certificate of Completion for taxpayer.

• http://www.mass.gov/dor/docs/dls/publ/igr/2002/02-210.pdf

EXEMPTION FOR THE BLIND

Clause 37

Statutory Exemptions Clause 37

• Documentation requirements may include but are not limited to:

– Evidence of ownership, domicile & occupancy

– Current Massachusetts Commission for the Blind Certificate

– Letter from doctor indicating blind status as of July 1st , this is only required for the first year of applying and only if the applicant does not have the above certificate.

• Status Requirements: Must be legally blind as of July 1st.

VETERAN EXEMPTIONS

Clause 22

Statutory ExemptionsFor all Veterans Exemptions

• Documentation requirements may include but are not limited to: – Evidence of ownership, domicile & occupancy

– DD214

– Current MA Tax Exemption Letter from the Department of Veterans Affairs

• Additional ownership requirements: – 22, 22A, 22B, 22C, 22E & 22F- Domiciled in MA for 6 consecutive months before entering the

service or 5 consecutive years (1 year if locally adopted) before the application date.

– 22D- Domiciled in MA for 5 consecutive years (1 year if locally adopted) before the application date or deceased spouse domiciled in MA for 6 consecutive months before entering the service.

• Discharge requirements: – Last discharge or release from the armed forces was (medical, honorable, etc.) anything except

dishonorable conditions.

Clauses 22A, B, C, E & F: exemptions are prorated for a domicile greater than a single-family

house. (I.E. The applicant owns 2 family with another owner that is not their spouse they would be granted 50% of the exemption amount.)

Statutory Exemptions Clause 22’s

• Clause 22 allows for a $400 tax exemption for the following:

– Minimum 10% (up to 99%) service connected disabled veteran

– Purple Heart recipient

– Gold Star mothers & fathers

– Spouse of veteran entitled under Clause 22

– Surviving spouse of veteran who does not remarry

• Clause 22A allows for a $750 tax exemption if the veteran has:

– Lost use of one hand above the wrist, or one foot above the ankle, or one eye

– A Congressional Medal of Honor

– A Distinguished Service Cross

– A Navy Cross or an Air Force Cross

• Clause 22B allows for a $1,250 tax exemption if the veteran has: – Lost use of both hands or both feet

– Lost use of one hand and one foot

– Lost use of both eyes (blind)

• Clause 22C allows for a $1,500 tax exemption if the veteran: – Is rated by the VA to be permanently and totally disabled

– And has specially adapted housing

• Clause 22D allows for a full exemption: – For surviving spouses (who have never remarried) of active duty military personnel

(including National guardsmen on active duty) who, on or after September 11, 2001, were

• Killed or went missing in action and are presumed to have been killed in a combat zone

• Or died as a proximate result of injuries sustained or diseases contracted in a combat zone

Statutory Exemptions Clause 22’s continued

• Clause 22E $1,000 tax exemption for veterans that are: – 100% disabled as determined by the VA

• Clause 22F Full Exemption: – Paraplegic veterans, those with service-related injuries as determined by the VA, or their

surviving spouses, are eligible for total exemption on their property taxes.

Statutory Exemptions Clause 22’s continued

Veterans Work Off ProgramActs of 2012- Chapter 108 Section 8A

Veteran Work-off Abatemenet Program

NEW-Veteran Work-off AbatementChapter 108 Sec. 8A (Adds new local acceptance to GL-59 Sec.5 N)

Adds a NEW local acceptance Statue -to GL c.59 –S 5N -in 2012-to allow city and towns to create work off programs for veterans.

Statue is almost IDENTICAL to GL c59 S 5K for the Senior Work-off Abatement program.

SET UP BY COMMUNITIES:

-Acceptance is by Vote of the legislative body of the city or town.

-Veterans may earn “abatements” of their property taxes by working for the community.

-COMMUNITY will set its own program and eligibility requirements.

-WAGES may not exceed $1,000 or if voted by community 125 hours of service.

-Earned Abatement is NOT income for state tax and worker’s compensation programs.

Website for Veteran Publication on Work Program

• http://www.mass.gov/dor/docs/dls/publ/bull/2013/2013-03b.pdf

MASS.GOV-WEBSITE FOR ALL FORMS AND BROCHURES

• Forms and Brochures

• http://www.mass.gov/dor/local-officials/municipal-finance-law/forms-and-brochures.html

Everything you wanted to know about Excise Tax!

For New and Older cars!!

What is the motor vehicle and trailer excise?

• An excise is a tax upon an event or privilege. A motor vehicle and trailer excise is in lieu of a tangible personal property tax and is levied for the privilege of registration. M.G.L. Ch. 60A, which is the statutory basis for the excise, uses the motor vehicle itself as a means to measure this privilege. Revenue derived from the excise can be used by cities and towns for any lawful purpose.

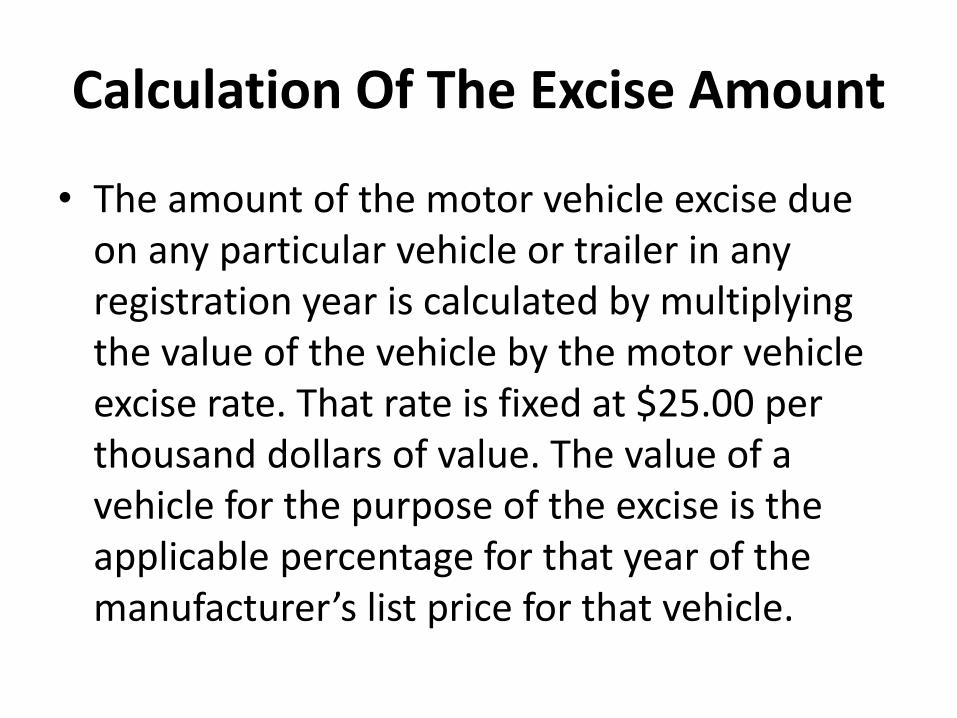

Calculation Of The Excise Amount

• The amount of the motor vehicle excise due on any particular vehicle or trailer in any registration year is calculated by multiplying the value of the vehicle by the motor vehicle excise rate. That rate is fixed at $25.00 per thousand dollars of value. The value of a vehicle for the purpose of the excise is the applicable percentage for that year of the manufacturer’s list price for that vehicle.

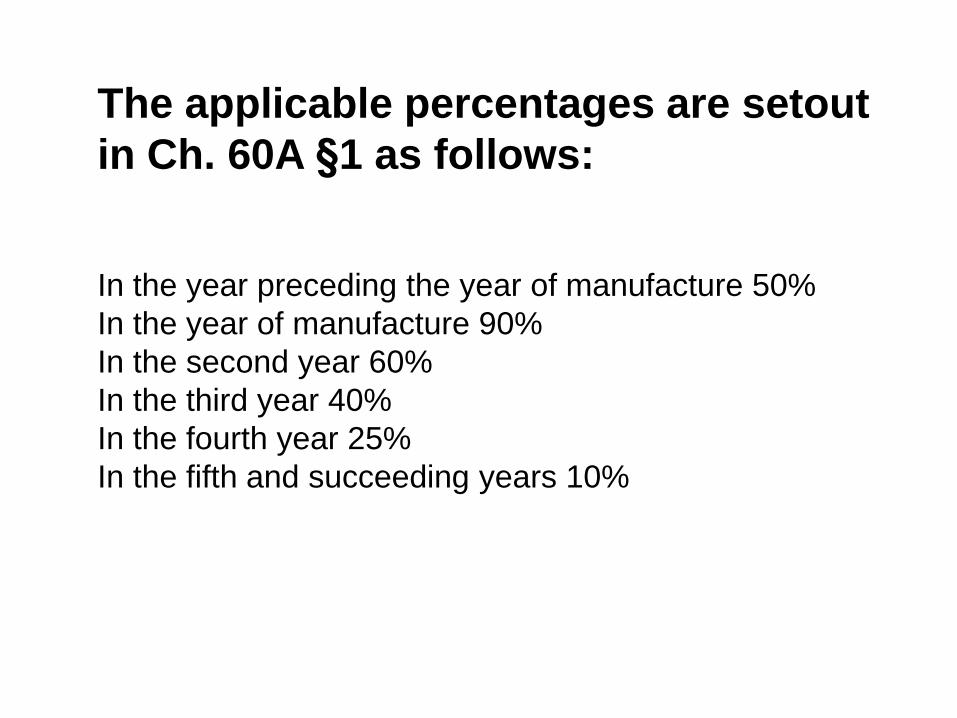

The applicable percentages are setout

in Ch. 60A §1 as follows:

In the year preceding the year of manufacture 50%

In the year of manufacture 90%

In the second year 60%

In the third year 40%

In the fourth year 25%

In the fifth and succeeding years 10%

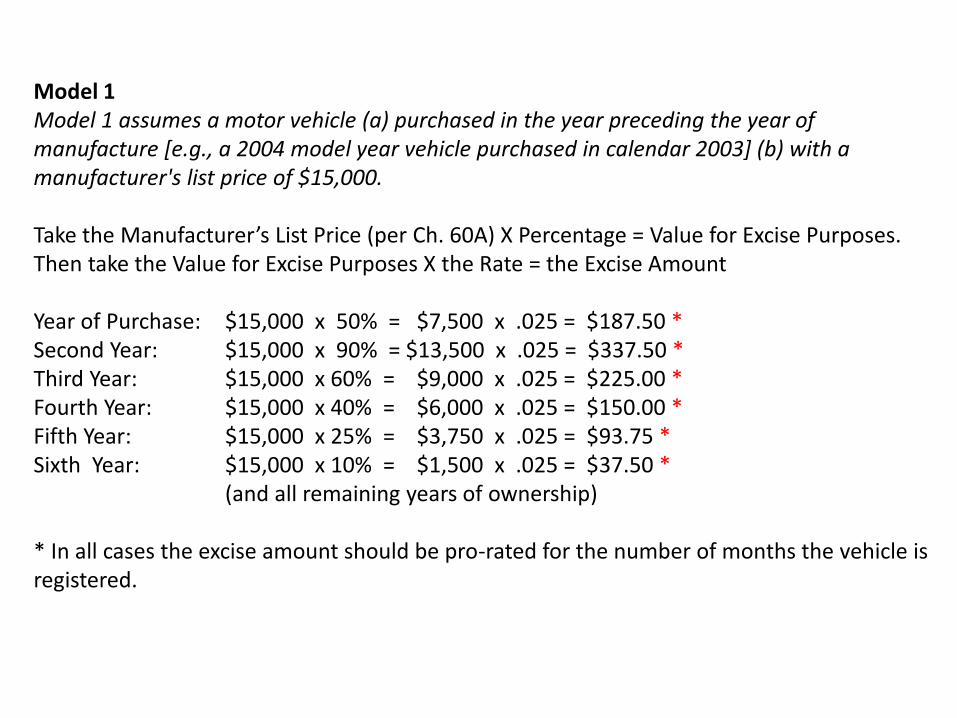

Model 1Model 1 assumes a motor vehicle (a) purchased in the year preceding the year ofmanufacture [e.g., a 2004 model year vehicle purchased in calendar 2003] (b) with amanufacturer's list price of $15,000.

Take the Manufacturer’s List Price (per Ch. 60A) X Percentage = Value for Excise Purposes. Then take the Value for Excise Purposes X the Rate = the Excise Amount

Year of Purchase: $15,000 x 50% = $7,500 x .025 = $187.50 *Second Year: $15,000 x 90% = $13,500 x .025 = $337.50 *Third Year: $15,000 x 60% = $9,000 x .025 = $225.00 *Fourth Year: $15,000 x 40% = $6,000 x .025 = $150.00 *Fifth Year: $15,000 x 25% = $3,750 x .025 = $93.75 *Sixth Year: $15,000 x 10% = $1,500 x .025 = $37.50 *

(and all remaining years of ownership)

* In all cases the excise amount should be pro-rated for the number of months the vehicle is registered.

Model 2

Model 2 assumes a motor vehicle (a) purchased two years succeeding the year ofmanufacture (b) with a manufacturer’s list price of $19,000.

Manufacturer’s List Price-Ch. 60A X Percentage = Value for Excise Purposes Then take the Value for Excise Purposes X Rate = Excise Amount

Year of Purchase: $19,000 x 40% = $7,600 x .025 = $190.00Second Year: $19,000 x 25% = $4,750 x .025 = $118.75Third Year: $19,000 x 10% = $1,900 x .025 = $47.50(and all remaining years)

How to handle those Dealership plates!!

DEALER PLATE SPECIAL EXCISEG.L. Ch. 60A Sec. 1

SUMMARY:

This legislation exempts motor vehicles operated with dealer plates from the customary motor vehicle excise under Chapter 60A of the General Laws and, instead, imposes on each motor vehicle dealer a special excise of $100.00 for every dealer registration plate issued to that dealer by the Registrar of Motor Vehicles.

Trailers operated with dealer plates continue to be subject to the usual excise provisions prescribed by G.L. Ch. 60A. That is to say, such trailers may not be operated with dealer plates for personal use.

Motor vehicles may be operated with dealer plates for exclusively business reasons by any person. However, they may be utilized for personal use only by a dealer, a dealer’s spouse, a co-owner who holds at least a 40% proprietary interest in a motor vehicle dealership, a co-owner’s spouse and by dealership employees who work at least 20 hours a week for the dealership and whose duties involve the sale of motor vehicles.

ASSESSMENT PROCESS

• A. Per Plate Assessment• Beginning in calendar year 1999, local assessors must assess a special

excise upon each motor vehicle dealer of $100.00 per plate for every dealer plate issued to that dealer for the respective calendar year.

• B. Registry List• Assessors should assess this special excise using dealer plate lists

provided by the Registry of Motor Vehicles to every city and town. Each municipality’s list will identify all persons in that city or town to whom the Registry has issued dealer plates. In addition, the list will state the number of plates issued to each dealer.

• C. Time of Delivery of Registry List• The Registry issues dealer plates annually, for the period beginning each

April 1st and ending the following March 31st.

ABATEMENTS

HI…I BOUGHT A NEW CAR…..

CAN YOU PUT THE EXCISE TAX FROM MY OLD CAR ON THE NEW CAR????

For what reasons may I get an abatement of a motor vehicle excise?

• A taxpayer may file an abatement application and receive an abatement for any of the following reasons:

• Sale of the vehicle and cancellation of the registration or the trade of the subject vehicle for another and the transfer of the registration.

• Transfer of the registrant and the vehicle to another state with proof of registration in that state and cancellation of the Massachusetts registration;

• Overvaluation of the vehicle;• Subsequent registration of the same vehicle in the same year by the same person

(e.g., vehicle is later registered with a Vanity Plate).• Theft of the vehicle, if the local police authorities are notified within 48 hours of

the discovery of the theft and the certificate of registration is surrendered no sooner than thirty days after the theft and the registrant has received a certificate of cancellation of registration signed by the Registrar of Motor Vehicles or his authorized agent setting forth that the subject vehicle was stolen.

• Applications for abatement must be filed with the local board of assessors within 3 years after the date the excise was due, or 1 year after the excise was paid, whichever is later. If the taxpayer's application for abatement is denied, there can be an appeal to the Appellate Tax Board (ATB) within three months of the denial.

RMV – Section 5

• Section 5 license plates are farm plates, dealer plates.

• When confronted with Section 5 license plates call Sabrina Brown. She is the person with the knowledge to help you. Her phone # is (857) 368-8030, or email her at [email protected]

• If, after the town has followed all statutory collection procedures and the owners remain tax delinquent, the Tax Collector can file a Notice of Excise Tax Delinquency which will prevent renewal of the Section 5 plates.

• This notice can be found on the RMV website: www.massrmv.com/rmv/forms/section5.htm

WEBSITE TO MASS.GOV

Website:http://www.mass.gov/dor/local-officials/municipal-finance-

law/frequently-asked-questions-motor-vehicle-excise.html#q11

MASS RMVHELP LINE NUMBER FOR CLERKS ONLY: 857-368-8181

WEBSITE ADDRESS: http://www.massrmv.com/

HELP LINE FOR PUBLIC:857-368-8180