51

Export market appraisal for broccoli and cauliflower Peter Gartrell Department of Agriculture & Food Western Australia Project Number: VG05028

Export market appraisal for broccoli and cauliflower

Peter Gartrell

Department of Agriculture & Food Western Australia

Project Number: VG05028

VG05028 This report is published by Horticulture Australia Ltd to pass on information concerning horticultural research and development undertaken for the vegetables industry. The research contained in this report was funded by Horticulture Australia Ltd with the financial support of the vegetable industry. All expressions of opinion are not to be regarded as expressing the opinion of Horticulture Australia Ltd or any authority of the Australian Government. The Company and the Australian Government accept no responsibility for any of the opinions or the accuracy of the information contained in this report and readers should rely upon their own enquiries in making decisions concerning their own interests. ISBN 0 7341 2093 1 Published and distributed by: Horticulture Australia Ltd Level 7 179 Elizabeth Street Sydney NSW 2000 Telephone: (02) 8295 2300 Fax: (02) 8295 2399 © Copyright 2009

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

1

Export Market Situation Analysis for the

Australian Cauliflower and Broccoli Industry

Peter Gartrell Department of Agriculture and Food, Western Australia Final Report for Project VG05028 March 2009

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

2

Project Team

Project Leader Peter Gartrell Regional Economist Department of Agriculture and Food WA PO Box 1231 Bunbury WA 6231 Tel – (08) 97806100 Fax – (08) 97806136 Email – [email protected] Team Members

Rachel Lancaster Dennis Phillips Research Officer Development Officer Department of Agriculture and Food WA PO Box 1231 Bunbury WA 6231

Department of Agriculture and Food WA Locked Bag 4 Bentley Delivery Centre WA 6983

Administrator

John Elliot Development Officer Department of Agriculture and Food WA Locked Bag 4 Bentley Delivery Centre WA 6983

Project Manager

Wayne Prowse Export Development Manager Horticulture Australia Limited Level 7, 179 Elizabeth Street Sydney NSW 2000 Email – [email protected]

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

3

Funding Sources

Funding for the investigation conducted by this project was provided by Horticulture Australia Limited (HAL) and the Department of Agriculture and Food, Western Australia.

Important Disclaimer

Any recommendations contained in this publication do not necessarily represent current HAL Limited policy. No person should act on the basis of the contents of this publication, whether as to matters of fact or opinion or other content, without first obtaining specific, independent professional advice in respect of the matters set out in this publication.

The Chief Executive Officer of the Department of Agriculture and Food and the State of Western Australia accept no liability whatsoever by reason of negligence or otherwise arising from the use or release of this information or any part of it.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

1

Index Page Number

Index 1

List of figures and tables 2

1. Media Summary 4

2. Technical Summary 5

3. Introduction, background and objective 6

4. Materials and methods

4.1 Overview 7

4.2 Methodology 8

5. Research and analysis

5.1 Australian industry evaluation 8

5.2 Australian market performance 14

5.3 World market profile 23

5.4 Export market brief 27

5.5 Competitor analysis 35

6. Position statement and discussion 38

7. Recommendations 44

8. References and further reading 46

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

2

List of figures and tables

Title Page

1 Australian total and domestic production of cauliflower and broccoli. 9

2 Australian production of cauliflower by State 2000-2007 9

3 Cauliflower production share by State for 2007 11

4 Australian production of broccoli by State 2000-2007 11

5 Broccoli production share by State for 2007 12

6 Cauliflower yields by Australian States 13

7 Broccoli yield by Australian States 14

8 Australian production, export volumes and values for cauliflower and broccoli 15

9 Annual export volumes and price 2000 to 2008 15

10 Trade weighted index for Australian exchange rate and average export price for

cauliflower and broccoli

16

11 Annual cauliflower export volumes by State 17

12 Average FOB export price for Australian cauliflower 17

13 Monthly cauliflower export volume for 2001 18

14 Monthly cauliflower export volumes by State for 2008 and Australia 2001 19

15 Annual broccoli export volumes by State 19

16 Average FOB export price for Australian broccoli 20

17 Monthly broccoli export volume for 2001 21

18 Monthly broccoli export volumes by State for 2008 and Australia 2001 21

19 Australian population and apparent consumption of cauliflower and broccoli

2000-2007

22

20 World production of cauliflower and broccoli 23

21 Selected countries export : production ratio for cauliflower and broccoli 24

22 Apparent consumption trend for cauliflower and broccoli for selected countries

and the world average (1990 – 2006)

25

23 Apparent consumption and GDP for India and China 25

24 Apparent consumption and GDP for Australia and the United Kingdom 26

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

3

Title Page

25 Annual Australian exchange rate history for selected countries 26

26 Singapore imports of broccoli from Australia and China 28

27 Singapore imports of cauliflower from Australia and China 28

28 Malaysian import volumes and price for cauliflower and broccoli 30

29 Japanese import volume and price for broccoli 31

30 Japanese domestic wholesale price for broccoli 32

31 Japanese broccoli import price and volume from China and US 32

32 Australian monthly exports of broccoli to the UAE 33

33 Import volume and price for cauliflower and broccoli for the UAE (2005) 34

34 Import volume and price for Dubai Direct 35

35 Cost of production outline for Australian broccoli and cauliflower 36

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

4

1. Media summary

The Australian fresh broccoli and cauliflower industries have experienced significant displacement in export markets. Exports for both products have declined rapidly in recent years. Export volumes of have collectively fallen by 92 per cent since its peak in 2001. Broccoli and cauliflower exports have primarily targeted the South East Asian and Japanese markets. Price is the key criteria in any export trade. Qualities such as shelf life and safety play a small part in markets such as Malaysia. More affluent consumers, such Singapore, have maintained a base level of demand for these criteria and the associated price premium. Australia still commands one third of the Singapore market for broccoli despite its apparent 100 per cent premium in price. The most significant shift in market dynamics has been the emergence of the Chinese vegetable industry. China now produces 45 per cent of the world’s cauliflower and broccoli. Its production has grown 51 per cent since the year 2000. Not surprisingly this corresponds to its increased export market presence. During this time countries such as Australia and the United States have reduced their exports, as a percentage of production, from approximately 30 to 5 per cent. China has a relatively low cost labour supply and subsequently a lower cost of production. Production growth and price competitiveness has been further spurred by government incentives such as tax relief and infrastructure support, particularly for export based business. Australian costs of production have been driven up primarily by wage, energy and fertilizer cost increases. Broccoli and cauliflower production systems have relatively high labour and low levels of mechanization throughout the supply chain. Exchange rates have further exacerbated export costs in recent times. Some gains in agronomic performance have softened these cost impacts. Australia’s collective yield performance for cauliflower and broccoli has increased by 1.5 per cent per annum since the year 2000. This includes the environmentally induced, substandard performances encountered by the traditionally largest producing State of Victoria. Australia’s production base for these products has collectively remained stable. Since the year 2000, cauliflower has declined 8.7 per cent in volume whilst broccoli has conversely increased 17.5 per cent. This increase in production, coupled with significant declines in exports, reveals a significant increase in apparent domestic consumption of approximately 3 per cent per annum. This exceeds the annual population growth of 1.4 per cent. The Australian cauliflower and broccoli industries need to consolidate by focusing on its strengths, particularly for the domestic and Singapore markets. Greater emphasis on cost competitiveness through agronomic and structural change is required. Continual monitoring of production and market competitiveness is required to steer these investments.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

5

2. Technical summary

From the year 2000 to 2007 Australian production of cauliflower fell by 8.7 per cent whilst broccoli increased by 17.5 per cent. Production has been dominated by Victoria and Queensland. In 2007 they collectively represented about two thirds of production of each product. Yield performances have been increasing by about 1.5 per cent per annum since 2000, despite some substandard performances in Victoria in recent times.

Australian domestic consumption has increased 20 percent or 0.89 kg per person since 2000. Apparent consumption of fresh cauliflower increased from 2.84 to 3.25 kg per capita. Fresh broccoli increased from 1.58 to 2.07 kg per capita. Domestic trends have dampened the impact of the decline in exports, particularly so for broccoli.

Cauliflower and broccoli exports represented approximately 30 per cent of production in the export peak of 2001. By 2007 this had declined to below 2 per cent. Export volumes of cauliflower and broccoli have collectively fallen by 92 per cent. Export value of fresh cauliflower and broccoli declined by $25.4m and $8.7m respectively from 2000 to 2008. Export FOB price for cauliflower increased by $0.44 per kilogram (36 per cent) and broccoli increased by $0.94 per kilogram (60 per cent). The price increase is the result of more favorable markets being maintained and increased opportunistic trade.

World production of cauliflower and broccoli was estimated to be 1.9 million metric tonnes in 2007. Since 2000 world production has increased 3.9 per cent per annum. China and India are the leading producers of cauliflower and broccoli with approximately 70 per cent of world production.

The export markets evaluated for broccoli and cauliflower included Singapore, Malaysia, the UAE and Japan. Collectively they showed unquestionable market dominance by Chinese exporters. It is clear that China has directly substituted Australian supplies. Chinese exports of these vegetables have grown value of market share from 15 per cent in 2003 to over 45 per cent in 2007. Chinese price is consistently 35 to 65 per cent cheaper than the Australian cost of supply in to the same markets. For some markets it is not possible to extract information at an individual product level. Cauliflower and broccoli are often aggregated making it difficult to ascertain the market trends. General data is often untimely and questionably accurate.

Exchange rates, Chinese cost of production, its government support and its proximity to Australia’s traditional markets have severely reduced Australian competitiveness. Labour and general input costs are significantly lower in China. The Australian cauliflower and broccoli industries need to consolidate by focusing on its strengths, particularly for the domestic and Singapore markets. Greater emphasis on cost competitiveness through agronomic and structural change is required. Continual monitoring of production and market competitiveness is required to steer these investments.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

6

3. Introduction, background and objectives The aims of the project were to identify the export market position for Australian fresh broccoli and cauliflower. The information produced by the project would provide an indication of markets which may be profitable destinations for the export produce. Markets that would be studied in detail include those in the Middle East (specifically the United Arab Emirates) and other traditional markets. Total production of Australian broccoli was estimated at 55,000 tonnes in 2003. This was an increase of approximately 38 per cent or 15,000 tonnes per annum from 5 years earlier. The main States for broccoli production were Queensland and Victoria. Together they accounted for over half of Australia’s production and nearly 40 per cent of exports. Total production of Australian cauliflower was estimated at 73,000 tonnes in 2003. This was an increase of approximately 12 per cent or 8,000 tonnes per annum from 5 years earlier. The main production States for cauliflower were Western Australia and Victoria with just over 50 per cent of production. Queensland was also a significant producer with 22 per cent of Australian production. Western Australia was clearly the most significant exporter with 84 per cent of exports. Australia exported approximately 5,000 tonnes of broccoli and 9,000 tonnes of cauliflower at the inception of the project. These markets were collectively valued at $23 million at that time. 5 years prior to the study their collective exports were 29,000 tonnes at a value of $40 million. Broccoli exports had declined almost 35 per cent or 4,000 tonnes per annum. Cauliflower had declined by a similar amount representing a 23 per cent decline over the 5 year period. Broccoli is exported to several countries, however almost three quarters of exports comprised the three main markets, being Japan (22 per cent), Singapore (39 per cent) and Malaysia (11 per cent). Cauliflower produced for export is reliant on limited markets in the South East Asian region, in particular, Singapore and Malaysia, with 94 per cent of exports being sent to these two countries. The decline in exports of both broccoli and cauliflower is obviously of concern to the brassica industry. A major cause of the decline, in addition to the high Australian dollar, is the increase in competition in Singapore and Malaysia from Chinese supplies. The quantity of Chinese product in these markets has risen substantially over the past three years, with continually improving quality and relatively low prices. The increased competition requires the brassica industry to look at other markets and mechanisms where Australian cauliflower and broccoli can be competitive. Primarily the objectives of the project were to provide an analysis of production and market performance for Australian broccoli and cauliflower industries. The project aimed to outline potential new markets and the competitive environment. It would also examine niche opportunities for fresh produce supplies into these and existing markets. As the project progressed the scope was reduced in light of the initial findings. It was decided, in

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

7

consultation with the funding bodies (Horticulture Australia and the Department of Agriculture and Food, WA), that the project be halted prematurely and reported. It was considered that investment in detailed market studies would be withdrawn in light of the initial findings.

4. Materials and methods

4.1 Overview A brief situation analysis was conducted and identified significant decline in the export market performance for cauliflower and broccoli. Opportunities to reinvigorate existing markets, and define new markets, were identified as an industry priority. A specialist team was identified and consulted. The project aim was to identity the competitive position for Australian product, particularly in the Middle East. The desktop survey of select countries aimed to identify markets which may have profitable potential for fresh Australian broccoli and cauliflower. An outline of the competitor’s active in these markets, with particular reference to those who are actively displacing Australian exports. The main output from this project will be a document that will outline the market opportunity for broccoli and cauliflower in the Middle East and Asian export markets. This will contain an interpretation of statistical information on the price and volume from suppliers to the selected markets. After the release of the document, industry will be able to use the data to reposition planning in relation to export markets for fresh cauliflower and broccoli. The outcome for this project is expected to be a more informed approach to supply chain assessment to assist in a directional guide for Australian cauliflower and broccoli producers. The initial objective of the project was to address the export decline of cauliflower and broccoli exports for Australian producers. From this outline, provide direction to reinvigorate the industry with the identification of new direction to capture export opportunities. From the primary capture of desktop data, priority market for examination would be identified. This was to be done by gathering relevant information on existing and potential markets. The information gathered would then be used to determine the markets most likely to be able to accept Australian product at an acceptable price for the producer. Employment of consultants in these identified markets would then sieve out the potential supply chain and its relevant components. Areas of investigation include indicative prices, product specifications, specific barriers or opportunities for trade, packaging requirements and alternative product handling options. The findings of the study were aimed to produce a handbook as a guide to the identified opportunities. This was revised to provide a situation analysis of the Australian cauliflower and broccoli export industries.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

8

4.2 Methodology The trade data for cauliflower and broccoli and its potential competitors for the Middle East and traditional markets would be examined to outline market history and position. The countries which have the most potential would be selected for more detailed study. Countries in North and South East Asia will be examined to determine if these have reasonable potential, however the Middle East will be the main focus of the project. Information collected would include current import data, current market suppliers and their capacities and trends. The future capacity of countries to continue imports or act as re-exporters of Australian product would also be examined. In the markets selected for more detailed examination, factors which would be considered include gathering wholesale data in small increments, determining the product specifications and packaging requirements of the importing countries, indicative prices and identification of potential contacts in the countries examined. The importance of aspects of Australian product such as low chemical application and product traceability will also be assessed. The size and diversity of the market segments in these countries would also be examined as this can have an impact on the price received for the product. Market segments include the wholesale markets, supermarkets, food service sector and processing sectors. A critical part of the project is the investigation of the actual state of markets compared to the statistical data collected throughout the project. It is intended where possible, to employ or identify local consultants in the target countries who can ‘ground truth’ the information gained from the statistics. This is necessary as various countries report their statistics by different methods, which can make the direct comparison of the information difficult. The consultants would also be able to provide contact details for companies interested in obtaining Australian product. The information gathered will be compiled into a reference report. The report will be freely available. The report can be used by those who may wish to investigate further the export of broccoli and cauliflower to new and traditional markets. An offer will be made to interested exporters and other industry personnel who may wish to further discuss the statistical information in the report. This could be presented at a national vegetable industry conference.

5. Research and analysis

5.1 Australian industry evaluation Total production of Australian cauliflower and broccoli has collectively shown a marginal fall since the year 2000. Broccoli production peaked during this period but declined in the later part to close at 46,031 tonnes per annum. This was an increase of 6,847 tonnes or 17.5 per cent (Figure 1). Over the same period cauliflower declined from 76,437 to 69,792 tonnes per annum. This is a decline of 6,644 tones or 8.7 per cent. Average annual production for cauliflower and broccoli since 2000 was 76,726 and 48,509 per annum.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

9

Figure 1 : Australian total and domestic production of cauliflower and broccoli

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2000 2001 2002 2003 2004 2005 2006 2007

Vo

lum

e -

ton

nes

Cauliflower Production Broccoli ProductionCauliflower domestic Broccoli domestic

Australian Bureau of Statistics

Figure 2 : Australian production of cauliflower by State 2000-2007

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2000 2001 2002 2003 2004 2005 2006 2007

Pro

du

ctio

n -

to

nn

es

WA NSW Vic Qld Other

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

10

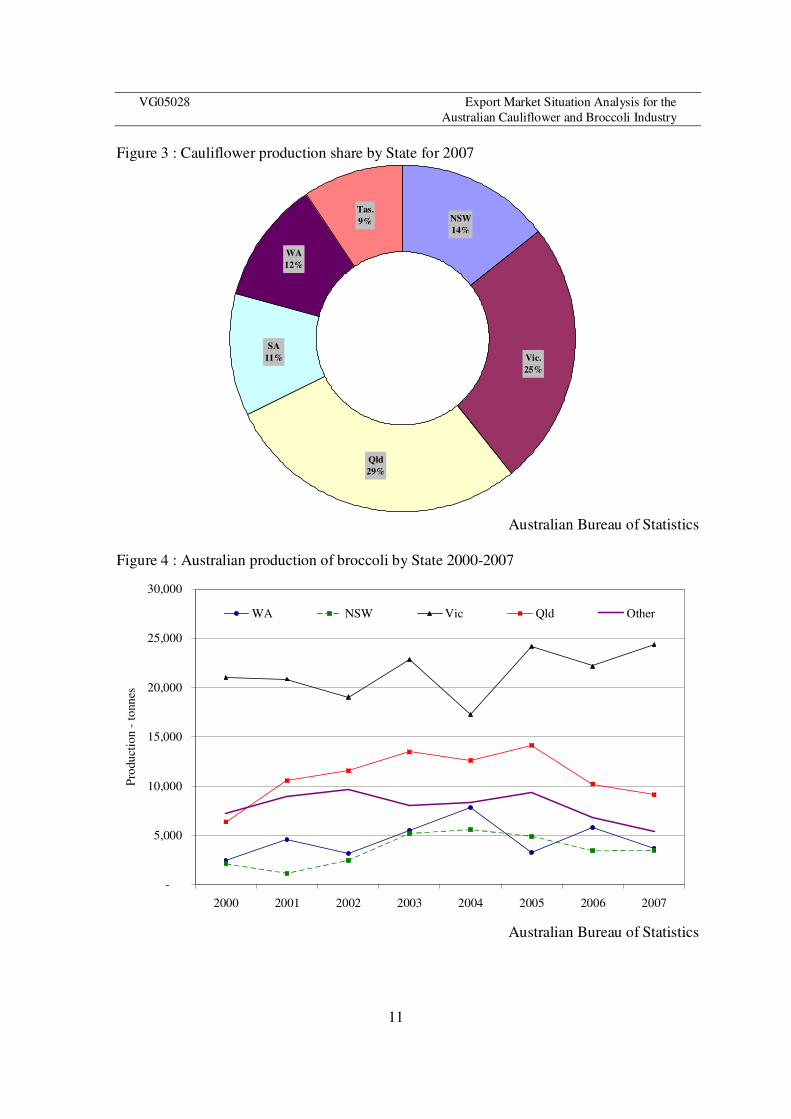

Apparent domestic supply of cauliflower increased 26.6 per cent, or 14,592 tonnes, at an average supply level of 64,925 tonnes per annum. Average domestic supply of cauliflower was 85 per cent of production. Broccoli domestic supply increased at nearly doubled that of cauliflower to realize an increased supply of 13,605 tonnes, or 44.6 per cent growth, since 2000. Annual supply averaged 41,879 tonnes per annum or 86 per cent of production for the period. The convergence of the production and domestic supply lines (Figure 1) highlight the fall in Australian fresh exports of cauliflower and broccoli. Cauliflower production in Australia has been led by Victoria which averaged approximately 21,000 tonnes or 27 per cent per annum since 2000. Recent market and environmental constraints have realized a decline in Victorian production with Queensland, and to a lesser extent Western Australia, responding to fill the void. New South Wales has a very domestically focused supply industry. It has remained relatively fairly static over this period. Western Australia has realized significant decline. It has fallen from 24 per cent of the national crop to only 12 per cent in 2007. This has been largely due to South East Asian market trade decline. Some recovery has been realized with increased interstate trade. Some of the increase could be partly attributed to product specifications for domestic versus export produce. That is the product now being traded domestically is recorded at greater weights due to the presentation of the product. Queensland has increased production of cauliflower by approximately 4,500 tonnes or 30 per cent to become the leading supplier of Australian cauliflower with 29 per cent of the national crop (Figure 3). The other smaller producing States have realized significant gains since 2000. This is from a modest average base of 13,393 tonnes per annum but is none the less significant. These have increased from 12.7 to 20.8 per cent of cauliflower production. South Australia and Tasmania share this segment in almost equal proportions. Australian production of broccoli is dominated by Victoria with more than half of Australian production. Victorian broccoli production has increased by around 10 per cent since 2000 equivalent to the national rate of growth. New South Wales has shown the greatest level of growth whilst all other States slowed after significant gains during the mid 2000’s. Domestic trade has dominated the growth in the broccoli industry and assisted in the alleviation of export declines. Domestic trade now accounts for about 44,000 tonnes per annum which is approximately 95 per cent of production. This up from the 77 per cent of production being for domestic use, back in 2000/01.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

11

Figure 3 : Cauliflower production share by State for 2007

Qld

29%

SA

11%

NSW

14%

Vic.

25%

Tas.

9%

WA

12%

Australian Bureau of Statistics

Figure 4 : Australian production of broccoli by State 2000-2007

-

5,000

10,000

15,000

20,000

25,000

30,000

2000 2001 2002 2003 2004 2005 2006 2007

Pro

du

ctio

n -

to

nn

es

WA NSW Vic Qld Other

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

12

Queensland accounted for 20 per cent of broccoli production in 2007. This State realized significant growth which saw it over double in the first 5 years, but retreated rapidly as export demand and domestic supplies slowed. At the same time Western Australia accounted for 8 per cent of production, but this varies significantly over time. Using 2000/01 production averages, Western Australia varied from a 10 per cent fall to a doubling of production during that 8 year period. Figure 5: Broccoli production share by State for 2007

Tas.

10%NSW

8%

Vic.

52%

Qld

20%

SA

2%

WA

8%

Australian Bureau of Statistics

The planted area of Australian cauliflower has averaged 3,700 hectares over the 2000 to 2008 period. The area planted, as a general trend, has declined over this period in the order of 10 to 15 per cent. During the same period apparent yield has increased by 20 to 25 per cent. Yields were around 18 tonnes per hectare and increased to just above 22 tonnes.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

13

Figure 6 : Cauliflower yields by Australian States

10.0

15.0

20.0

25.0

30.0

35.0

2000 2001 2002 2003 2004 2005 2006 2007

Yie

ld -

to

nn

es p

er h

ecta

re

WA NSW Vic QLD

Australian Bureau of Statistics

Victoria’s cauliflower’s poor yield performance in 2007 reduced the Australian average by over 1 tonne per hectare for the end of the period. Victoria had 38 per cent of area and only 24 per cent of production. New South Wales yields have generally been greater than those recorded for other States. This reflects the market presentation of domestic produce versus export. Domestic product per unit records a greater weight largely due to sales with leaves on, and the less stringent size and quality requirements relative to some export markets. This may also partly explain the sudden rise in Western Australian yield as the export supply ratio falls. It could also be argued that the more marginal producers of cauliflower have exited the market in the wake of increase cost/price pressure Australian planted area for broccoli has remained relatively stable since 2000. Apparent yield has increased over this period by 10 and 15 per cent on average. Yield for the whole period average 7.0 tonnes per hectare. This is an increase of 0.4 tonnes per hectare from the first half of the period 2000 to 2008 to the later. Inversely to cauliflower, Western Australia realizes a variable but superior yield performance than the other States. A typical yield range within each State varies by 2 to 2.5 tonnes between years. Western Australia’s short term average yield is 9.6 tonnes per hectare. Queensland and Victoria are relatively more stable and average in the vicinity of 7 tonnes per hectare. Given that these two States represent two thirds of supply they will dictate the national performance average. The New South Wales short term yield average is 4.4 tonnes per hectare. This is over half the performance of the leading State and substantially below the average. It is widely variable with a range of 1.5 to 7.2 tonnes per hectare as a State average yield.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

14

Figure 7 : Broccoli yield by Australian States

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2000 2001 2002 2003 2004 2005 2006 2007

Yie

ld -

to

nnes

per

hec

tare

WA NSW Vic QLD

Australian Bureau of Statistics

5.2 Australian market performance Production of cauliflower and broccoli in Australia has remained relatively stable since the year 2000. Inversely the export markets for both products have declined severely. Australian export volumes of cauliflower and broccoli from 2000 to 2009 declined by almost 30,000 tonnes or 33.5 per cent per annum. This equates to a collective loss in annual export earnings of $34.2 million per year over that period. Exports as a percentage of production fell from approximately 28 per cent in 2002/03 to 2 per cent in 2007. FOB (Free on Board) price receipts remained relatively static until 2005 and then escalated rapidly. This is a result of the broader market presence being redefined to relatively more expensive and opportunistic market participant. The increased use of air freight to fill these niche markets has contributed to further increase the cost of supply.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

15

Figure 8 : Australian production, export volumes and values for cauliflower and broccoli

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2000 2001 2002 2003 2004 2005 2006 2007

Volu

me

- to

nn

es

Cauli Prod Broc Prod Cauli Export Broc Export

Australian Bureau of Statistics

Figure 9 : Annual export volumes and price 2000 to 2008

-

5,000

10,000

15,000

20,000

25,000

30,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Vo

lum

e -

ton

nes

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Ex

po

rt P

rice

- F

OB

($

A)

Cauli Export Broc Export Cauli Price Broc Price

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

16

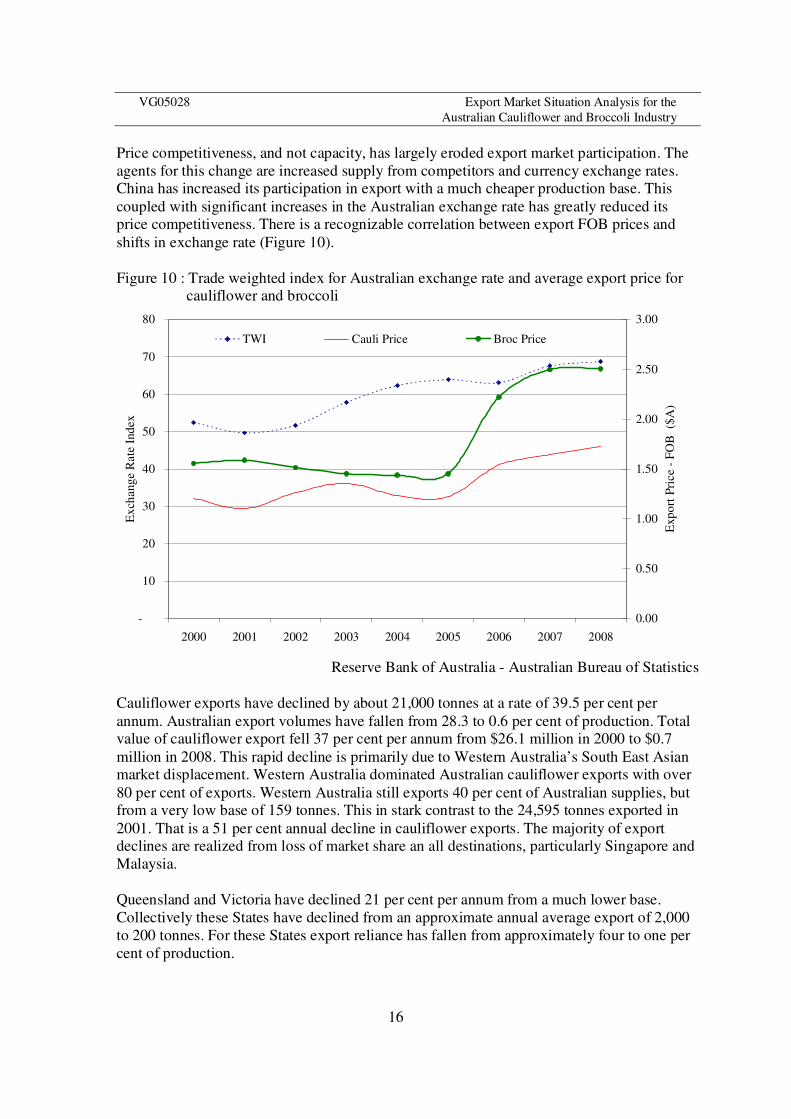

Price competitiveness, and not capacity, has largely eroded export market participation. The agents for this change are increased supply from competitors and currency exchange rates. China has increased its participation in export with a much cheaper production base. This coupled with significant increases in the Australian exchange rate has greatly reduced its price competitiveness. There is a recognizable correlation between export FOB prices and shifts in exchange rate (Figure 10). Figure 10 : Trade weighted index for Australian exchange rate and average export price for

cauliflower and broccoli

-

10

20

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008

Ex

chan

ge

Rat

e In

dex

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Exp

ort

Pri

ce -

FO

B ($

A)

TWI Cauli Price Broc Price

Reserve Bank of Australia - Australian Bureau of Statistics

Cauliflower exports have declined by about 21,000 tonnes at a rate of 39.5 per cent per annum. Australian export volumes have fallen from 28.3 to 0.6 per cent of production. Total value of cauliflower export fell 37 per cent per annum from $26.1 million in 2000 to $0.7 million in 2008. This rapid decline is primarily due to Western Australia’s South East Asian market displacement. Western Australia dominated Australian cauliflower exports with over 80 per cent of exports. Western Australia still exports 40 per cent of Australian supplies, but from a very low base of 159 tonnes. This in stark contrast to the 24,595 tonnes exported in 2001. That is a 51 per cent annual decline in cauliflower exports. The majority of export declines are realized from loss of market share an all destinations, particularly Singapore and Malaysia. Queensland and Victoria have declined 21 per cent per annum from a much lower base. Collectively these States have declined from an approximate annual average export of 2,000 to 200 tonnes. For these States export reliance has fallen from approximately four to one per cent of production.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

17

Figure 11 : Annual cauliflower export volumes by State

0

5,000

10,000

15,000

20,000

25,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Ex

po

rt v

olu

me

- to

nnes

WA NSW Vic QLD

Australian Bureau of Statistics

Figure 12 : Average FOB export price for Australian cauliflower

0.30

0.80

1.30

1.80

2.30

2.80

2000 2001 2002 2003 2004 2005 2006 2007 2008

Av

erag

e E

xpo

rt P

rice

- F

OB

($A

)

WA NSW Vic

QLD Other

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

18

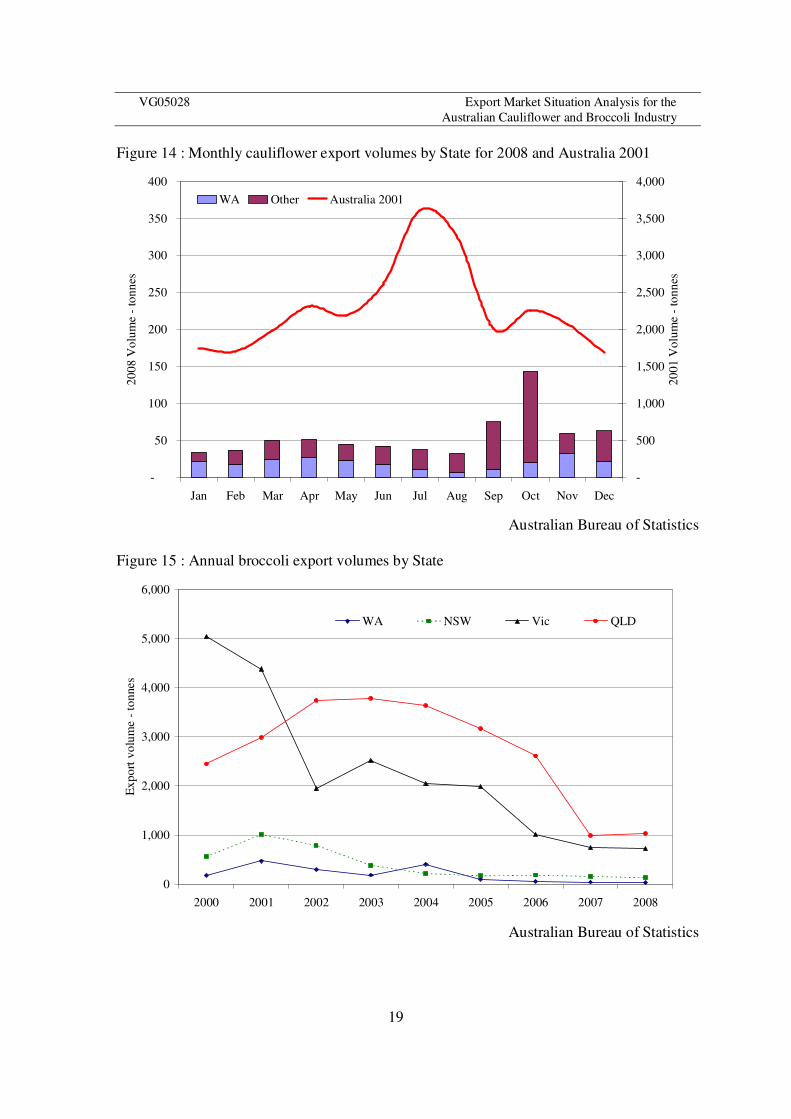

Annual average FOB price for Australian cauliflower has increased steadily since 2000. The major producing States of Western Australia and Queensland have realized steady increases in FOB price over time. For other minor export participants the FOB prices fluctuate considerably. This reflects both the volatile nature of opportunistic marketing and the reliability of data and error on small collections. Monthly export trade volumes of cauliflower from Australia typically peaked during the winter months June to August. Cauliflower produce specifications are generally larger at this time. This realizes less cost per unit of production and marginally less costs in irrigation supply. For all of 2001 (Figure 13) Western Australian exports were consistently ranged between 1,500 to 2,500 tonnes per month. This was the peak calendar year for export volume of Australian cauliflower. Other exporting States participated during the late winter early spring time. Supply would tend to peak at this time. With declining exports, the shape of monthly exports has averaged 30 tonnes in 2008 with a peak period in early spring (Figure 14). This is dominated by Queensland supplies with 45 per cent of annual supply. Singapore and Malaysia are still the primary export markets with 50 per cent of export value. Brunei and Indonesia collectively bring export representation to 70 per cent. In 2001 94 per cent of export went to Singapore and Malaysia. Over two thirds of that trade was with Malaysia. Figure 13 : Monthly cauliflower export volume for 2001

-

500

1,000

1,500

2,000

2,500

3,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Volu

me

- to

nn

es

WAOther States

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

19

Figure 14 : Monthly cauliflower export volumes by State for 2008 and Australia 2001

-

50

100

150

200

250

300

350

400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

20

08 V

olu

me

- to

nn

es

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

20

01 V

olu

me

- to

nn

es

WA Other Australia 2001

Australian Bureau of Statistics

Figure 15 : Annual broccoli export volumes by State

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Ex

po

rt v

olu

me

- to

nnes

WA NSW Vic QLD

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

20

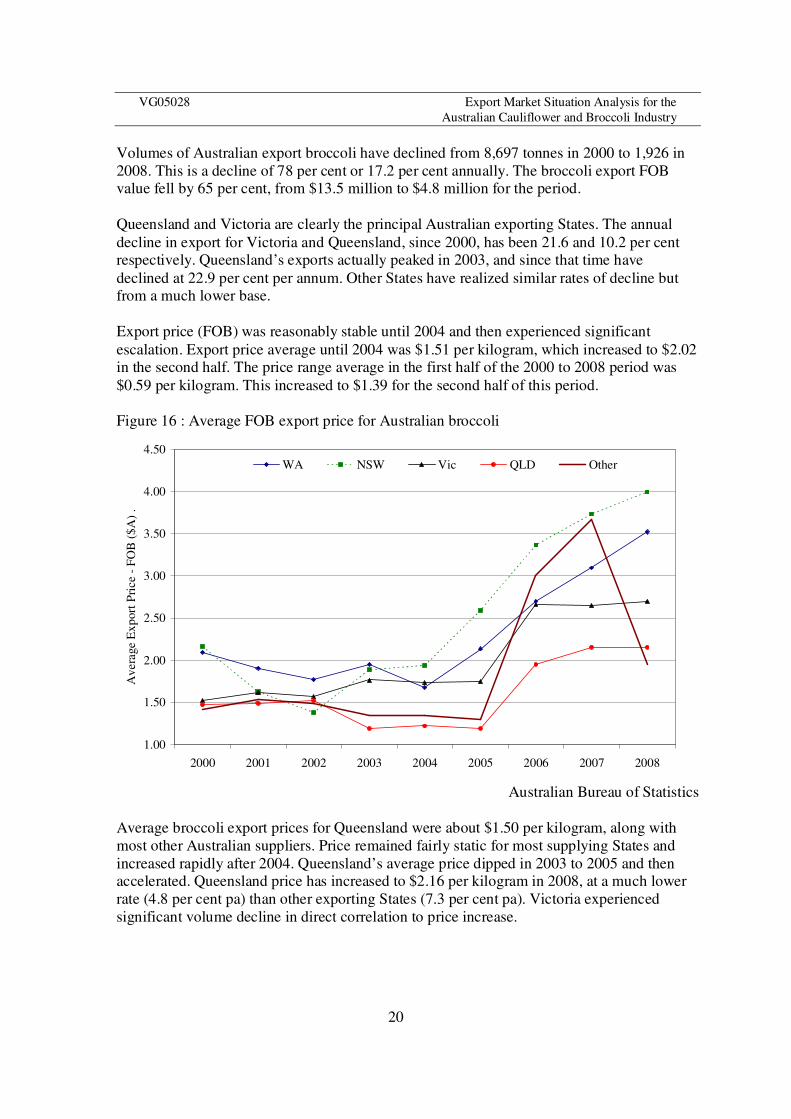

Volumes of Australian export broccoli have declined from 8,697 tonnes in 2000 to 1,926 in 2008. This is a decline of 78 per cent or 17.2 per cent annually. The broccoli export FOB value fell by 65 per cent, from $13.5 million to $4.8 million for the period. Queensland and Victoria are clearly the principal Australian exporting States. The annual decline in export for Victoria and Queensland, since 2000, has been 21.6 and 10.2 per cent respectively. Queensland’s exports actually peaked in 2003, and since that time have declined at 22.9 per cent per annum. Other States have realized similar rates of decline but from a much lower base. Export price (FOB) was reasonably stable until 2004 and then experienced significant escalation. Export price average until 2004 was $1.51 per kilogram, which increased to $2.02 in the second half. The price range average in the first half of the 2000 to 2008 period was $0.59 per kilogram. This increased to $1.39 for the second half of this period. Figure 16 : Average FOB export price for Australian broccoli

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

2000 2001 2002 2003 2004 2005 2006 2007 2008

Av

erag

e E

xp

ort

Pri

ce -

FO

B (

$A

) .

WA NSW Vic QLD Other

Australian Bureau of Statistics

Average broccoli export prices for Queensland were about $1.50 per kilogram, along with most other Australian suppliers. Price remained fairly static for most supplying States and increased rapidly after 2004. Queensland’s average price dipped in 2003 to 2005 and then accelerated. Queensland price has increased to $2.16 per kilogram in 2008, at a much lower rate (4.8 per cent pa) than other exporting States (7.3 per cent pa). Victoria experienced significant volume decline in direct correlation to price increase.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

21

Figure 17 : Monthly broccoli export volume for 2001

-

100

200

300

400

500

600

700

800

900

1,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Volu

me

- to

nn

es

QLD VIC Other

Australia Bureau of Statistics

Figure 18 : Monthly broccoli export volumes by State for 2008 and Australia 2001

-

200

400

600

800

1,000

1,200

1,400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Volu

me

- to

nn

es

QLD VIC Other Australia 2001

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

22

Annual exports of Australian broccoli peaked in 2001. At this time a clear supply pattern was evident. Australia realized low trade levels during the summer months. Queensland predominantly exported in the winter early spring periods and was flanked by Victorian supplies (Figure 17). Total Australian supply peaked during the winter months. Average monthly supplies were approximately 1,200 tonnes from April to October and 350 tonnes per month for the balance of the year. A similar pattern remained in 2008 but from a much lower base. During 2008 the monthly average volume for April to October was 220 tonnes whilst the balance was 76 tonnes per month. Australian population has increased from 19.3 million people in 2000 to 21.2 million in 2007. This is an average growth rate of 1.36 per cent per annum. For the same period apparent cauliflower consumption grew at a greater rate of 2.05 per cent per annum. This was up from 2.82 kilograms per capita in 2000 to 3.28 kilograms in 2007. Broccoli for the same time period was up 4.00 per cent per annum. In 2000 the apparent consumption was 1.58 kilograms per capita. This increased to 2.08 kilograms per capita in 2007. It is not possible to capture the domestic trade data accurately. The numerous, undocumented in-state trade avenues and interstate trade data make analyses of State based consumption difficult. Average annual Consumer Price Index (CPI) has averaged 3.0 per cent since 2001. The apparent vegetable price index has been approximately 4.1 per cent per annum. Applying these to wholesale market data suggests that broccoli has tracked with CPI but slightly behind the vegetable price index. Cauliflower wholesale price, in Western Australia for example, is approximately 16.6 per cent behind the CPI from 2001 to 2008. Figure 19 : Australian population and apparent consumption of cauliflower and broccoli

2000-2007

-

5,000

10,000

15,000

20,000

25,000

2000 2001 2002 2003 2004 2005 2006 2007

Au

stra

lian

po

pu

lati

on

- 0

00's

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Ap

par

ent

con

sum

pti

on

- k

g/h

d .

Population Cauliflower Broccoli

Australian Bureau of Statistics

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

23

5.3 World market profile World production of cauliflower and broccoli was estimated to be 1.9 million metric tonnes in 2007. International trade is estimated at $800 million per annum. Since 1980 world production has increased at 2.1 per cent. From the year 2000 it has accelerated to 3.9 per cent per annum. China and India are the leading producers of cauliflower and broccoli with approximately 70 per cent of world production and approximately 40 per cent of population. On a per capita basis China produces approximately 5.6 kilograms. Australia by comparison produces 6.5 kilograms per head per capita Since 1980 Chinese and Indian production has been increasing at 6.4 and 0.6 per cent per annum respectively. Since 2000 India has increased at 1.6 per cent whilst China has recorded an annual production increase of 6.9 per cent. Since 1992, China’s growth is unparalleled by any other producing nation or the world as a collective (Figure 20). Figure 20 : World production of cauliflower and broccoli

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Pro

du

cti

on

- t

on

nes

China India World Balance

FAO

Chinese production has increased 51 per cent since 2000. Unsurprisingly this resulted in an increase in Chinese exports from this time. Chinese exports represented approximately 2 to 3 per cent of its production. From 1990 to 2000 countries such as Australia and the United States of America increased their exports as a percentage of domestic production. From 2000 these fell in direct correlation to increases in Chinese exports (Figure 21). India’s participation in export is extremely low.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

24

Figure 21 : Selected countries export : production ratio for cauliflower and broccoli

0%

5%

10%

15%

20%

25%

30%

35%

40%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Pro

du

cti

on

Ex

porte

d -

per

cen

tage

Australia China India United States of America

FAO

The apparent world consumption is approximately 2.9 kilograms per capita. The apparent consumption in China has increased rapidly since 1990 (Figure 22). This is up from 1.6 to 6.0 kilograms per head from 1990 to 2007. China’s domestic consumption has increased 138 per cent since the year 2000. Over the same period population has increased by 3.7 per cent. Australian and United States consumption by comparison is 5.3 and 3.9 kilograms per head. Gross Domestic Product (GDP) per capita measures can be litmus to the demand shifts for various products. As per capita GDP increases consumption patterns change. In less developed countries the fundamental food products, such as cauliflower and broccoli, increase. GDP and consumption trends for China and India reasonably demonstrate this (Figure 23). When income or GDP increases, it will reach a level where substitution of basic products will take place. Generally more developed and growing economies will show a plateau or decline in basic produce demand. Price drivers will also alter consumption patterns. To a lesser extent product perception, such as product image or health benefits, can influence consumption. Australia and the United Kingdom have shown increases in GDP over the past two decades (Figure 24). Over this period consumption declined and then rose toward the end of this period. This could be due to the relative price competitiveness of these products since the year 2000. It also coincides with a lot of positive, health related publicity for both products.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

25

Figure 22 : Apparent consumption trend for cauliflower and broccoli for selected countries and the world average (1990 – 2006)

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

App

aren

t C

on

sum

pti

on -

kg

/cap

ita/

ann

um

Australia China United Kingdom World

FAO

Figure 23 : Apparent consumption and GDP for India and China

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1990 1992 1994 1996 1998 2000 2002 2004 2006

App

aren

t C

on

sum

pti

on -

kg

/cap

ita/

ann

um

-

500

1,000

1,500

2,000

2,500

GD

P -

$U

S

per

cap

ita

China India China GDP India GDP

China GDP trendline

China consumption trenline

India GDP trendline

India consumption trendline

FAO

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

26

Figure 24 : Apparent consumption and GDP for Australia and the United Kingdom

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1990 1992 1994 1996 1998 2000 2002 2004 2006

Ap

par

ent

Co

nsu

mp

tio

n -

kg

/cap

ita/

ann

um

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

GD

P -

per

cap

ita

Aust UK UK GDP Aust GDP

UK GDP trendline

Aust GDP Trendline

UK consumption trendline

Aust consumption trendline

FAO - USDA

Figure 25 : Annual Australian exchange rate history for selected countries

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 Jan-09

Au

stra

lian

Doll

ar B

uy

ing

40.00

45.00

50.00

55.00

60.00

65.00

70.00

75.00

Tra

de

Wei

ghte

d I

nd

ex

US Malay ChinaSingapore TWI

Reserve Bank of Australia

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

27

Many traditional markets and competitor currencies are closely linked to the United States of America (US) dollar. Exchange rates are a critical component of international trade competitiveness. The Australian dollar has fluctuated widely in recent times from around $0.50 to $0.95 US. As the Australian dollar increases against the target market currency produce price will be relatively higher for the importer. This is particularly so where the importing country and competitor suppliers are on a similar currency base. This is fundamentally the case with China and Malaysia. Conversely the cost of freight and some inputs for production should theoretically be improved.

5.4 Export market brief Australia’s primary fresh vegetable export markets include Singapore, Malaysia, Hong Kong, Japan and in more recent times the Middle East. The South East Asian destinations have been attractive due to their need to import many food products outside their producing capacity. As these economies have grown, so have their capacity to pay. The demand for quality and timeliness of produce has increased over time. This is not to under estimate the strong focus on produce price. Australia’s proximity to these markets and attention to quality parameters have realized a market opportunity. During the 1980’s, Australia began to increase exports as Taiwan lost capacity and became less price competitive. Australian presence in these markets peaked around 2001. At this time China responded to fiscal and policy signals to increase vegetable exports.

Singapore Singapore was historically the South East Asian trading hub for a significant amount of fresh produce. Re exports have declined as trade logistics have matured. Singapore has been a primary market for Australian cauliflower and broccoli. Up until the mid 1980’s Australia held 60 per cent of the market, Taiwan held the balance. During the mid to late 1990’s Australia held over 90 per cent of the cauliflower market. Singapore has a population of approximately 4.4 million people with a per capita GDP of nearly $US 35,000. Vegetable trade in 2008 was $390 million of which $19 million was cauliflower and broccoli. Cauliflower and broccoli accounted for $7 and $12 million respectively in 2008. Approximately $1million was re exported, primarily to Malaysia. This is a mature market for these products. Consumption and thus market growth has slowed significantly over the past decade. Consumption in of cauliflower in 1995 was approximately 1.6 kilograms per head. A decade later it was the virtually the same. Broccoli consumption has grown to 1.67 kilograms per capita in 2008.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

28

Figure 26 : Singapore imports of cauliflower from Australia and China

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2003 2004 2005 2006 2007 2008

CIF

Pri

ce -

$A

/ k

g

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Vo

lum

e -

ton

nes

China Vol Australia Vol China Australia

GTIS

Figure 27 : Singapore imports of broccoli from Australia and China

0.60

1.10

1.60

2.10

2.60

3.10

2003 2004 2005 2006 2007 2008

CIF

Pri

ce -

$A

/ k

g

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Vo

lum

e -

ton

nes

China Vol Australia Vol China Australia

GTIS

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

29

In 2008 over 95 per cent of Singapore’s cauliflower imports were supplied by China. Australia has decreased from 75 per cent of supply in 2003, to 2 per cent in 2008. Malaysia now exports double the volume of cauliflower to Singapore than Australia; this is primarily Chinese re exports. Broccoli imports for Singapore have increased steadily over the past decade. Market growth was 3.6 per cent per annum over the past decade. During this time, Australia has lost significant market share. Australian share is down to 15 per cent of volume, an annual decline of 13 per cent. This is a direct correlation with the Chinese increase in the market. China now supplies 82 per cent of Singapore’s broccoli. Singapore is a developed economy with high quality demands and is a health and safety conscious consumer. The market has a strong Chinese heritage and linkage. Quarantine restrictions are very low. These factors provide Chinese importers with a good opportunity, in conjunction with their competitive pricing. Some health, safety and consistency of supply have provided some limited opportunity in trade for Australian exporters. Singapore has a relative geographic advantage as an export destination, particularly for Western Australia. Produce is primarily a sea freighted from Australia for cost management reasons, generally with out major compromise in quality. Chinese competitors are geographically better positioned but the freight cost is only marginally less. Timeliness and frequency of shipping is improved. Strong links have been developed over time in many fresh food items. This provides some level of access with these existing linkages.

Malaysia The population of Malaysia exceeds 26 million people. GDP per capita is estimated at $US7,000 or approximately 20 per cent of that for Singaporeans. With a lower GDP or country wealth it is a more price sensitive market. Surveys show that price is the most important factor with a majority of Malaysian consumers. While Malaysia has a large population, the niche or wealthier segment is quite small. It is therefore difficult to target and these products do not carry a prestige image. Health and safety information regarding food is not readily promoted. Like Singapore, there is a strong Chinese link and influence in Malaysia. Quarantine requirements are relatively relaxed for Malaysia’s fresh produce imports. These are two elements that assist Chinese trade in Malaysia. Both the Malaysian and Chinese economies are closely linked to the US currency. Most cross currency confusion, risks and impacts are relatively diffused by this commonality. The Malaysian imports of vegetables in 2007 totaled more than $550 million and just over one million tonnes. Over 33,000 tonnes (3 per cent) of vegetable imports were cauliflower and broccoli. This market has grown at 7.4 per cent per annum since 2003. Taiwan used to be the most significant supplier of cauliflower and broccoli up until the early 1980’s, similar to the history with Singapore. Taiwan held the balance of trade for

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

30

cauliflower for longer than it did in Singapore. The price point of Taiwanese cauliflower was more competitive but lost market share due to capacity. In recent times China has expanded its market share for cauliflower and broccoli from 53 per cent in 2003 up to 95 per cent in 2008. Australia has conversely declined from 43 per cent to down 2 per cent in 2008. Malaysia represents 62 per cent of the value of Chinese cauliflower exports at an FOB value of $16.2 million in 2008. Broccoli represented $8.7 million or 23 per cent of the value of Chinese exports. From 2003 through to 2008 the CIF price for Chinese cauliflower and broccoli increased in response to other suppliers. Both Malaysia and China have currencies exchanges largely dictated by the US exchange rate. The change in price would therefore be due to an opportunistic response, a reflection of supply shift or an increase in costs such as freight. Australian prices have increased in parallel with its strengthening dollar. The fall in other supplier prices in response to the withdrawal of European and US suppliers. These supplies have been substituted by imports from South Africa and smaller Asian suppliers. South Africa has predominantly supplied during the second quarter of the previous 5 years. Other suppliers have remained at a low base of approximately 1,000 tonnes per annum. Figure 28 : Malaysian import volumes and price for cauliflower and broccoli

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

2002 2003 2004 2005 2006 2007

Impo

rt V

olu

me

- to

nnes

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Imp

ort

pri

ce -

$au

per

kil

og

ram

China Australia Other

China price Aust price Other price

GTIS

Japan Japan’s population is approximately 130 million people with a GDP per capita of an estimated $US 34,000. Vegetable consumption per capita in Japan is remarkably high but a wide range of vegetable products are consumed. Based on wholesale data consumption of

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

31

cauliflower and broccoli is approximately 0.24 and 0.76 kilograms per person per year. This does not represent all trade but is indicative of its lower per capita consumption. Japanese imports of cauliflower and broccoli have been declining over recent years. Only a very small amount of cauliflower is imported. This has fallen from 108 tonnes in 2005 down to 18 tonnes in 2007. Supply specifications for cauliflower are typically for a much smaller product than that of other Asian markets. This contributes to a higher cost product given the yield dilution to achieve these specifications. Broccoli imports have declined from 66,000 tonnes in 2003 to 32,400 tonnes in 2008. That is a decline of 13.3 per cent per annum. The United States of American is the primary supplier with 98 per cent of imports in 2008 up from 89 per cent in 2003. China has had a significant presence during the recent past, but has reduced rapidly in 2007/08 (Figure 29). Chinese price has remained fairly stable whilst US price has declined from an average of $2.36 to $2.04 per kilogram. The Australia average price has increased significantly based on very small volumes. Figure 29 : Japanese import volume and price for broccoli

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2003 2004 2005 2006 2007 2008

Volu

me

- to

nn

es

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Pri

ce -

$au

/kg

China AustraliaOther Log. (Australia price)Log. (Other price) Log. (China price)

GTIS

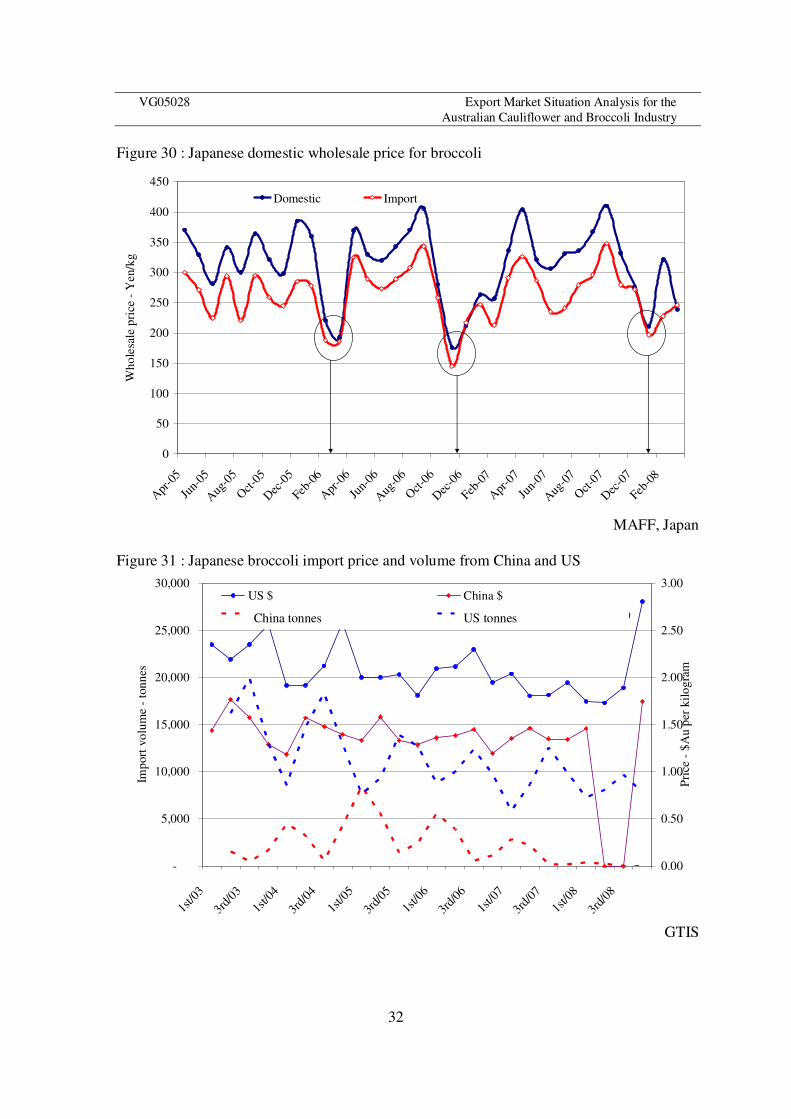

Broccoli price is variable through out the year with notable troughs in the early part of each year (Figure 30). The margin between the import and domestic price suggests a premium due cost of supply or consumer preference. United States imports also mirror this with volume falls during the first quarter of each year (Figure 31). China used to increases its market presence at this time. Price margin between China and the US has averaged 65 cents per kilogram, yet Chinese volumes have declined at a greater rate. This suggests that price is not the primary driver in this market.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

32

Figure 30 : Japanese domestic wholesale price for broccoli

0

50

100

150

200

250

300

350

400

450

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb-0

6

Apr

-06

Jun-

06

Aug

-06

Oct

-06

Dec

-06

Feb-0

7

Apr

-07

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb-0

8

Wh

ole

sale

pri

ce -

Yen

/kg

Domestic Import

MAFF, Japan

Figure 31 : Japanese broccoli import price and volume from China and US

-

5,000

10,000

15,000

20,000

25,000

30,000

1st/0

3

3rd/

03

1st/0

4

3rd/

04

1st/0

5

3rd/

05

1st/0

6

3rd/

06

1st/0

7

3rd/

07

1st/0

8

3rd/

08

Imp

ort

vo

lum

e -

ton

nes

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Pri

ce -

$A

u p

er k

ilo

gra

m

US $ China $

2 per. Mov. Avg. ( China) 2 per. Mov. Avg. ( United States)

GTIS

US tonnes China tonnes

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

33

United Arab Emirates The UAE comprises seven emirates including Dubai. The UAE has approximately 4.3 million people, Dubai 1.4 million. GDP per capita for the UAE was about $US 42,000. Dubai was chosen as the litmus indicator of this market. It has a higher income profile and expatriate population. It has a high immigrant labour force, most notably Indian. There is also an additional demand from a growing tourism population. The local production of vegetables is very limited and is therefore reliant on imports. Dubai is very often the distribution hub for other Gulf countries. The US, China, Chile, South Africa and Europe are all very active in this market. It is therefore still a very competitive market environment, but it is expanding and evolving. Figure 32 : Australian monthly exports of broccoli to the UAE

0

10

20

30

40

50

60

70

80

90

100

2000 Jan2001 Jan

2002 Jan2003 Jan

2004 Jan2005 Jan

2006 Jan2007 Jan

2008 Jan

Vo

lum

e -

To

nn

es

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Pri

ce -

$A

u p

er k

ilo

gra

m

Volume PricePoly. (Price) Poly. (Volume)

Australian Bureau of Statistics

Australian exports of broccoli have grown approximately 12.5 per cent per year since 2003, but are based on the low volume of 2003 of 237 tonnes. The total value of cauliflower and broccoli from Australia was $Au 1.2 million in 2008. Cauliflower represented small quantities of this trade in the recent past and was nil for 2007 and 2008. The UAE imported $Au620 million or just over one million tonnes of fresh vegetables in 2007. Just over 15 per cent of this was then re exported to near neighbour countries such as Iraq, Iran, Kuwait, Oman, Qatar and Saudi Arabia. In 2007 the UAE exported 1,100 tonnes of its own vegetables, mainly to Oman and Qatar.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

34

Dubai has little production capacity, but the 2005 census shows that cauliflower production was in excess of 9,000 tonnes and $Au 5.6 million. Total vegetable production area was over 13,000 hectares and $Au 235 million. Figure 33 : Import volume and price for cauliflower and broccoli for the UAE (2005)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jordan Saudi Arabia Syria Lebanon Iran Other

Vo

lum

e -

ton

nes

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Pri

ce -

$A

u p

er k

ilog

ram

Broccoli Volume Cauliflower Volume

Broccoli Price Cauliflower Price

Ministry of Economy, UAE

Cauliflower and broccoli imports for the UAE are approximately 15,000 tonnes per annum. This is approximately 3,000 tonnes of broccoli and 12,000 tonnes of cauliflower. Very minor amounts of these products are re exported. Supplies of broccoli and cauliflower come predominantly from other Middle Eastern sources. Jordan is the major primary produce supplier. In 2006 Jordan exported 24,000 tonnes of brassica, of which 45 per cent was sent to the UAE. This was a total FOB value of $Au4.5 million or $Au0.20 per kilogram. Given its relative geographic position, it is a low cost provider to this market. Average retail price of cauliflower in 2007 for the UAE was $Au1.65 per kilogram. Australian price has continued to escalate but has been able to maintain and even expand its market share. This is generally an extremely opportunistic and niche supply. The air freight percentage of Australian broccoli exports has increased each year. In 2006/07 100 per cent of broccoli was air freighted from Australia. By comparison China freight was all by sea.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

35

Figure 34 : Broccoli import volume and price for Dubai Direct

-

100

200

300

400

500

600

700

800

900

1,000

2001 2002 2003 2004 2005 2006 2007

Vo

lum

e -

ton

nes

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Pri

ce -

$A

per

kil

og

ram

China Australia Other

Other price Aust Price China Price

Dubai Direct

5.5 Competitive position statement

Volatile exchange rates, along with the increased cost of labour and other farm inputs, have had a significant impact on the Australian industry’s export competitiveness. Competitor suppliers have increased productive capacity and investment impetus. Collectively this scenario has aggressively eroded Australia’s market share for cauliflower and broccoli in its traditional export markets.

The Australia horticulture industry has tended to cope with cost price squeeze scenarios by increasing productivity or improving efficiency. These adjustments require an investment of time and finance. The scope and scale of recent changes have been greater than these incremental gains over recent years.

Australia’s primary competition in the cauliflower and broccoli export markets is China. China is the world’s largest producer of vegetables. China is a giant in the world vegetable industry. It produced approximately 8.5 million tonnes of cauliflower and broccoli in 2007. Production is geographically diverse, which spreads supply timing and risk. China is amongst the worlds lowest cost producers of vegetables. Low input costs, favorable exchange rates and government support policies provide a constructive platform for expansion through price competitiveness.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

36

Exchange rates and China’s comparative costs of production have severely impacted Australia’s price competitiveness. In order to better understand Australia’s cost competitiveness an analysis of costs chain elements were extracted and compared to competitor CIF price receipts. Australia’s indicative farm gate cost of production ranged from 31 to 44 cents per kg for cauliflower and 55 to 106 cents for broccoli. Post harvest costs for cauliflower ranged from 40 to 51 cents per kg and 65 to 71 cents for broccoli. Freight varied between source and destination. The data used was publicly available and is very generic. It does not account for seasonal performance or other agronomic and structural cost variations. Using Singapore as an example, CIF cost price for cauliflower exceeded the average Chinese CIF price receipts by 21 to 28 per cent. For broccoli it was 61 to 79 per cent. These percentages are the premiums price over Chinese produce that are required to breakeven. This dictates a premium of approximately 65 and 110 per cent of cost to provide financial incentive for industry participants.

Figure 35 : Cost of production outline for Australian broccoli and cauliflower

Western Australia New South Wales Queensland

Cauliflower Broccoli Cauliflower Broccoli Cauli Broccoli

Yield kg/ha 23,490 10,100 18,000 6,400 8,600

COP Plants/seed 3,190 3,557 1,045 2,400 3,000

$/ha Fertiliser/pests 1,600 1,860 784 1,534 “

Irrigation 550 260 90 150 “

Cultural 762 426 278 540 602

Other 915 905 160 56 700

Labour 1,999 2,200 3,510 2,088 2,500

Farm Gate Cost $/kg 0.38 0.91 0.33 1.06 0.79

Post harvest Packaging 0.13 0.23 0.11 0.28 0.23

Freight 0.13 0.21 0.08 0.15 0.21

Labour/energy/O’head 0.25 0.28 0.27 0.22 0.28

FOB Cost $/kg 0.89 1.62 0.78 1.70 1.50

Freight cost - Singapore 0.28 0.45 0.34 0.52 0.81

CIF Cost $/kg 1.17 2.07 1.11 2.22 2.31

% China CIF Singapore 128% 161% 121% 172% 179%

NSW Department of Agriculture; Queensland Department of Primary Industries; Department of Agriculture and Food, WA

China’s cost of production, that is Free on Board (FOB), is much lower than that of Australian producers for most fresh produce. This is primarily attributable to costs of labour.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

37

Many activities remain very labour intensive for this reason. As a percentage of production costs, labour is the most significant cost in Chinese production. Australian broccoli FOB cost is approximately $1.60 per kilogram. Chinese FOB price, not cost, for broccoli is indicatively $0.32 per kilogram or $0.25 at the point of wholesale. Chinese average price receipts for broccoli in Singapore are $1.38 per kilogram CIF compared to Australia’s $2.88 in 2008. Price differentiation of this magnitude is difficult to substantiate in a marginally differentiated product such as broccoli.

China has significant investment in on farm packing facilities. Approximately 80 per cent of vegetable production is performed by small family based businesses. The balance is a more corporate style structure with technologies, scale and investment to rival most developed world production systems. These style businesses have been partially escalated by government policy. The fundamental goals are to ensure that rural labour and its contribution to GDP are maximized. Examples of local and National government support mechanisms include taxation relief specific to vegetable producers (esp. export), subsidized inputs cost, on farm and general infrastructure subsidies and investments, rebates and finance discounts for large scale product managers, fully funded training, research and development. For the foreseeable future it is highly likely that the governments will continue to support the development of the vegetable industry and its associated infrastructures.

Freight is a significant component of export. Air freight is generally suitable for high value produce that can absorb the premium price paid (eg live seafood). Sea freight is most suited to produce such as cauliflower and broccoli. This mode is more affordable but a less timely method of transfer. The export markets of South East Asia are relatively close to Australia which increases competitiveness with suppliers such as South America. China holds a freight cost advantage for many of Australia’s traditional markets. The freight costs from China to key markets are lower but in the main are fairly inconsequential in comparison to other cost chain advantages. The timeliness of China’s shipping freight services is more frequent and the transit times are less. Environmental and resource restrictions could offer some obstacles for export expansion in China. In some areas water resources and land use changes will be evident, but in the main not a significant barrier. Issues such as environmental degradation and chemical residues are apparent. Chemical residue detections in produce have been evident. This is a market problem in terms of market access and consumer sentiment. With careful management and investment this could provide an opportunity for Chinese trade if it is rectified. Improved quality assurance programs are being implemented by the more corporate style businesses in China. China’s increasing domestic demand is not expected to exceed production capacity in the short to medium term. Domestic price for vegetables has increased significantly above the base CPI (Consumer Price Index) in recent years. Domestic price is very competitive with export prices received. Consumption of cauliflower and broccoli is already at developed world levels. Consumption per capita could reasonably be expected to slow or even plateau as substitution by the higher income earners occurs.

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

38

Australian cauliflower and broccoli industries hold some competitive advantages. Timing and consistency of supply is one example. Cauliflower production, in Western Australia in particular, managed whole of year supply. Whilst this is theoretically true, there is still a lot of division, particularly between States. Single source supplies are attractive to large retail chains in the goal of reducing category management cost and externalize the risk of supply. Quality assurance and compliance systems are another market instrument that Australian industry does possess. Whilst it adds some cost to the supply, it can also open the doors to risk evasive supermarket retailers. This is particularly useful in the wealthier and more health conscious markets. It does require some parallel promotion. This is often expensive and thus very small levels of investment have been made in this area. Some economies of scale, in terms of total export value, are required for such a task.

Other significant competitors include South Africa, New Zealand, USA and European countries. These are faced with the same levels of price disparity when compared to China. India does have the second highest production levels of cauliflower and broccoli. For the same reasons as China it should be carefully monitored as a potential competitor. Infrastructure, resources and investment base are very different to those that China enjoys, it does however have the base underlying capacity with labour cost and market proximity.

In some markets such as the UAE / Middle East, near neighbour suppliers, such as Jordan, must be monitored and understood. Jordan’s export price for cauliflower to the UAE has increased by 5.5 per cent per annum for the past decade. During the same period the productivity levels have improved and domestic prices have increased 5.3 per cent per annum. Jordan produces almost 80,000 tonnes of cauliflower and broccoli per year. This is similar to the annual production of Australia from a country with one third of the population. This demonstrates its export capacity and financial incentive. Freight advantage for Jordan is much greater.

6. Position statement and discussion The Australian cauliflower and broccoli industries have experienced unprecedented declines in exports since 2001. Exports for cauliflower fell by 21,000 tonnes and broccoli by 6,700 tonnes since the year 2000. Production has collectively remained static. Cauliflower production declined 6,600 tonnes, whilst broccoli increased 6,800 tonnes since the year 2000. Broccoli production in Australia has realized growth in the order of 2.3 per cent per annum since the year 2000. Broccoli exports represented 8,800 tonnes or 19 per cent of production in 2000 to 2003. This fell to approximately 1,900 tonnes or 3 per cent by 2008. Broccoli exports experienced a brief growth in exports during this period largely from trade from out of Queensland. Victoria realized a decline over that same period and continued to fall from 5,000 to 800 tonnes per annum export. This could be partly attributed to Victorian producers being required to reprioritize water resources and competitive improvements in Queensland. The reduction in supply corresponded with increased domestic price and an increase in inter

VG05028 Export Market Situation Analysis for the Australian Cauliflower and Broccoli Industry

39