12

Consumer attitudes toward energy provision Spring 2015

Consumer attitudes toward energy provisionSpring 2015

This group has dominated the retail energy business in the UK since the introduction of liberalisation in the late 1990s. However, in recent years, there has been a raft of new entrants, some of which are well placed to challenge that market domination.

In the wake of the recession, and stimulated by political and other interventions, UK householders are now more mindful of their energy costs, and many of the smaller firms have been able to offer cheaper bills than their more established rivals. As a result, the challengers’ share of the household market has risen from 2% to almost 9% since 2012.

To explore this area further, we commissioned a survey to look at consumers’ attitudes toward energy provision, their energy suppliers, their bills and their willingness to switch providers when they are dissatisfied with any of the aforesaid.

Our survey, conducted by market researcher OnePoll in February 2015 among 2,000 UK consumers, revealed that almost one-quarter of consumers (24%) switched gas or electricity supplier in 2014. The same survey shows that this trend is likely to continue, with almost one-quarter of consumers (22%) stating that they are likely to switch supplier in 2015.

Our survey suggests that it is inertia, rather than loyalty, that has kept many consumers tied to their existing energy suppliers as many express a willingness to switch if they think doing so would result in cheaper bills.

Key findings include:

• Almost one-quarter of UK consumers (24%) switched gas or electricity supplier in the last year — and more than 8 in 10 (81%) of this group would consider switching again in the near future.

• Thirty-nine percent of respondents identified billing errors by their existing supplier as the most likely reason to cause them to look for an alternative supplier.

• More than three-quarters (78%) of consumers stated that price was the single most important factor they would consider when choosing a new supplier.

• Only 12% of consumers have a completely clear understanding of what their energy bill means in terms of energy supply and affordability.

• Nearly one-third of respondents (29%) said that their energy bill is the household bill that they worry most about being able to afford.

With price dominating the drive to switch, and more than one-third of consumers (42%) believing that the increases in energy bills were being driven by the desire by energy companies to increase their profits, energy suppliers need to understand what these changing consumer attitudes might mean for them.

The UK’s large energy suppliers currently provide gas and electricity to around 26 million UK homes.

Our survey also looked at why consumers switch energy suppliers, along with the importance of energy costs and environmental matters in their decision-making process.

Executive summary

Consumer attitudes toward energy provisionSpring 2015

Consumer attitudes 2 toward switching suppliers are changing

Why are consumers 3 switching suppliers?

Consumer attitudes 4 toward energy suppliers

Consumer attitudes 6 toward energy bills

Changing attitudes 8 toward the environment

Conclusion 9

Contents

Consumer attitudes toward switching suppliers are changing

Our survey found consistently high numbers of consumers across the whole of the UK have either switched supplier or are considering doing so, but the greatest number of changes were found in the East Midlands, where almost one-third of consumers (32%) have switched supplier in the last year.

A significant number of respondents in the North East and East Anglia (28%) and London (24%) have also changed supplier in the last year. By contrast, only 17% of consumers in Wales decided to switch in the last year. The regional differences can be attributed, in part, to the price differences across the country, where the cheapest supplier varies by area, and also by the success of some suppliers in maintaining loyalty or affinity.

Looking forward to 2015, over one-third of Londoners (35%) are considering moving to a different supplier for their gas and electricity. Energy consumers in the North West, West Midlands and the South West are the most likely to switch.

Almost a quarter of UK consumers (24%) switched gas or electricity supplier in the last year — and, strikingly, more than 8 in 10 (81%) of this group would consider switching again in the near future. This may suggest that a minority, but nonetheless very active, part of the customer base now sees switching as a norm, and the experience is worth repeating.

While energy companies might well expect those familiar with the process of switching to consider doing so again, they may be surprised by the relatively small proportion of consumers who are unlikely to switch supplier in the next 12 months, which stands at just 38%. This indicates that levels of brand loyalty are diminishing.

Despite the fact that more than three-quarters of consumers (76%) did not change gas or electricity supplier in 2014, there appears to be a strong appetite for switching.

32%

28%

24%

24%

17%

2

Why are consumers switching suppliers?

Comparatively, customer service was considered the most important factor when choosing a new supplier by only 9% of respondents, and brand was chosen by even fewer respondents (6%).

However, when asked what customer service elements would most likely cause them to switch their energy supplier, more than one-third (39%) of consumers cited inaccurate bills. Quality of service appears to be an insignificant factor when selecting a new supplier, yet the biggest reason for customers to decide to move on.

Households faced rising energy bills between mid-2013 and mid-2014 despite the cost of gas and electricity to energy

suppliers falling by up to 20%, according to the Department for Energy and Climate Change. Energy suppliers argue that increasing energy bills are largely caused by high or fluctuating costs in the wholesale market, but our research shows that this message has not been communicated effectively to consumers, with 42% believing that rising energy bills are designed to increase the profits of energy companies.

For this reason, perhaps, less than one-fifth of consumers (18%) would trust suppliers to provide them with advice on energy consumption. More than two-thirds (68%) feel that they themselves are most responsible for reducing the energy consumption in their own homes, while only 15% consider their energy supplier to be most responsible.

These results highlight the fact that consumers are trying to take more control over their energy consumption and costs but also reveal a lack of trust in their energy supplier. The challenge for the industry, therefore, is to invest in ways to restore the confidence and loyalty of its consumer base through innovative services and an enhanced and trouble-free customer experience, especially if they are unable to improve on price.

Our survey found that price dominates the drive to switch supplier; more than three-quarters (78%) of consumers stated that price was the single most important factor they would consider when choosing a new supplier.

12% long complaint processes were also among the top reasons that would trigger a decision to switch

16% received unfriendly service when calling the helpline

39% of consumers responded that inaccurate bills would lead them to switch providers

3Consumer attitudes toward energy provision Spring 2015

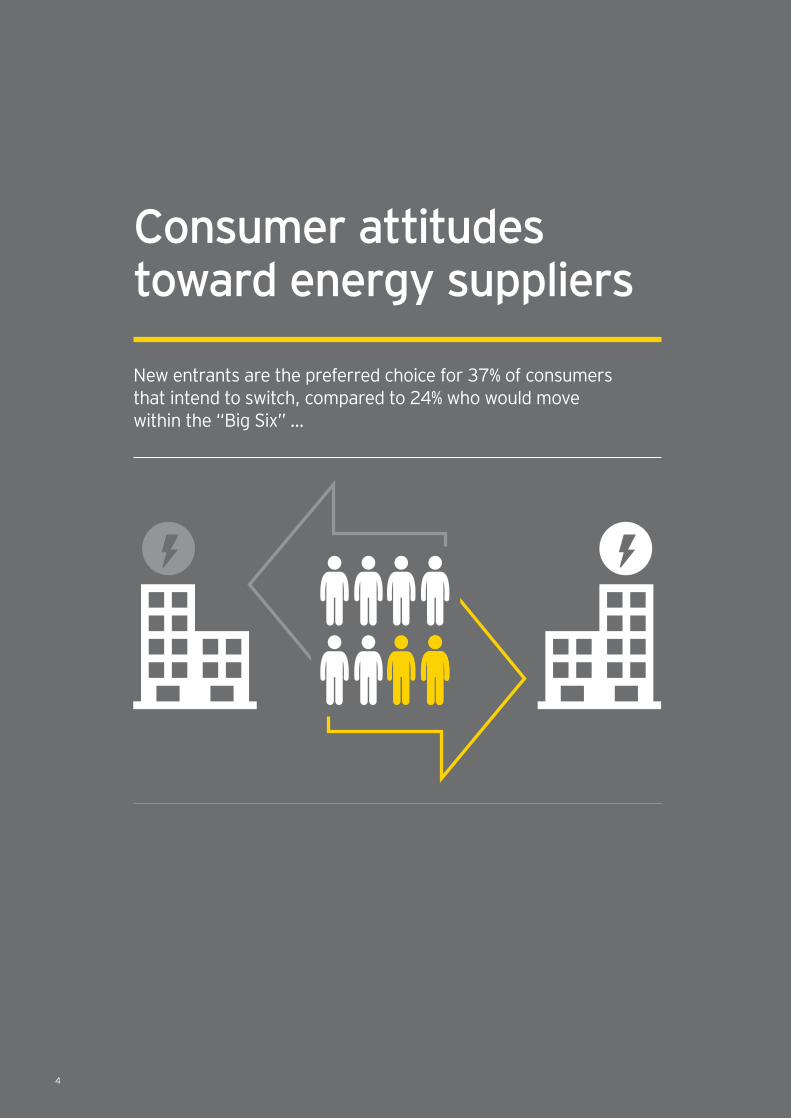

Consumer attitudes toward energy suppliers

New entrants are the preferred choice for 37% of consumers that intend to switch, compared to 24% who would move within the “Big Six” …

4

When consumers who were currently thinking of switching energy supplier were asked which energy company they would be most likely to choose, more than one-third (37%) selected a new entrant (smaller energy suppliers). Less than a quarter (24%) would be likely to switch to one of the large suppliers; however, almost 4 in 10 (39%) consumers remain unsure whether they would switch to a large supplier or a new entrant.

While the large suppliers currently hold the majority of the consumer market, the fact that more than three-quarters of consumers (76%) who would consider switching supplier would not automatically consider one of these suppliers is striking. This underscores the fact that there are significant opportunities for new entrants to the market to erode the market share of the large suppliers.

Equally, the large players still have the opportunity to find better ways of engaging with their consumers and retaining the “swing voters.”

33%of consumers stated that they believe the UK energy market needs more suppliers.

5Consumer attitudes toward energy provision Spring 2015

Consumer attitudes toward energy bills

This lack of understanding perhaps reflects the sense that consumers do not believe that energy suppliers are billing transparently, and also highlights the importance of regulators and energy suppliers alike finding better, clearer ways to communicate both pricing and the individual components of energy bills.

What do consumers want from their energy suppliers?

UK households appear to have little desire for energy suppliers to provide additional services, particularly those unrelated to energy provision.

When asked, nearly two-thirds (65%) of consumers replied that they would not be interested in purchasing additional services from their energy supplier. Fewer than 10% of consumers would be interested in purchasing insurance cover or mobile services, and only one in five (22%) would be interested in boiler care, even though this is directly related to their energy service.

Instead, our survey indicates that consumers appreciate greater control where their energy bills are concerned, with 62% reporting that they would like to receive their energy bills monthly or more frequently. Only 3% reported that they would like to receive their bills on less than a quarterly basis, which is the market standard.

It appears that consumers have a conservative attitude toward financial planning and feel more comfortable with predictable costs, even if they’re higher. As such, concerns remain about the fact that energy bills often fluctuate. Nearly one-third of respondents (29%) said that their energy bill is the household bill that they worry most about being able to afford, compared to only 18% of respondents who worry most about their mortgage and only 9% who worry most about their food bill.

However, despite their fears about energy costs, 85% of consumers can usually afford their bills and only 10% have missed a payment in the last year. The disparity between the apparent anxiety over the cost of energy bills and the reality of consumers’ ability to pay their bills may be linked to the fact that consumers are regularly presented with news that suggests that they are being overcharged, or that bills are contributing to an inappropriate level of profit for the energy companies.

The results of our survey indicate that while consumers want more control of their energy usage and bills, they want this in a straightforward manner. As such, energy suppliers must find a way of convincing consumers that they are acting transparently, and must also empower their customers to feel in control of their energy bills.

Currently, only 12% of consumers feel that they have a completely clear understanding of what their energy bill means in terms of energy supply and affordability, while half (50%) of the consumers are either unsure or unclear to a greater or lesser degree as to what their energy bill means.

6

50%of consumers are either unsure or unclear to a greater or lesser degree as to what their energy bill means.

7Consumer attitudes toward energy provision Spring 2015

Changing attitudes toward the environment

More than three-quarters (77%) of consumers surveyed now receive paperless bills through emails, smartphones or tablets, which is also a sign that consumers are more conscious of their impact on the environment, as well as a sign that they desire more immediate and accessible communication.

There are limits to the level of further costs consumers are willing to incur in order to be more environmentally friendly, however. While 20% would be willing to pay up to £10 extra per month to fund investment in renewable energy, a smaller number (15%) would be willing to pay this same amount to combat climate change or to fund essential energy infrastructure projects in their region. Just 1 in 10 respondents (10%) said they’d be willing to pay this amount each month to support the exploration of new forms of energy, such as fracking.

Finally, three-quarters (75%) of householders were familiar with the concept of a smart meter, which aims to help households cut down on their energy bills by enabling them to see their own energy use in real time.

26%of respondents would be willing to pay higher energy bills if the extra money were to go toward investment in renewable energy, and 22% would be equally willing if the extra money paid were to combat climate change.

Responses from consumers in our survey indicate that green issues remain important.

8

Conclusion

While the larger suppliers currently retain the dominant market share, there is an evident and growing appetite among customers to shop around for a better deal. The ongoing Competition and Markets Authority investigation may yet propose remedies that further encourage or enable “stuck” customers to benefit from more competitive tariffs.

A key problem for energy companies is that many customers believe that energy suppliers are quick to pass on higher costs, but rarely pass on price cuts, in order to protect their profits.

If energy companies can find a better way of communicating their pricing so that it is more easily understood by the customer, customers may be less likely to feel like they have received a poor deal.

The more transparent, error-free and flexible the billing process becomes for the consumer, the more likely consumers are to remain with their existing supplier. Conversely, where mistakes are made with bills, consumers will readily start to explore their options with other suppliers and will move based on price.

While protecting the environment is a concern for many customers, government should keep in mind that there are limits to the costs that consumers are willing to bear in order to find more environmentally friendly ways of producing energy.

The results of EY’s survey, Consumer attitudes toward energy provision, highlight the fact that energy suppliers will have to work harder to gain consumers’ trust and make their services appealing to them. Differentiation through service innovation is what will drive market share moving forward.

9Consumer attitudes toward energy provision Spring 2015

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2015 EYGM Limited. All Rights Reserved.

EYG no. DX0320

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

EY | Assurance | Tax | Transactions | Advisory

Follow us on Twitter: @EY_UK_Energy ey.com/energy

For further information, please contact the authors below

Tony WardPartner, Head of Power and Utilities for UK&[email protected] +44 [0]12 1535 2921

Yunus Ozler Partner, [email protected]+44 [0]20 7951 4524

For marketing and media relations enquiries, please contact:Kevin Corcoran Associate Director for Energy, Brand Marketing & [email protected]

Konstantinos Makrygiannis Energy Media Relations [email protected]