16

Oil pressure Potential for consolidation in the oilfield services sector

Oil pressurePotential for consolidation in the oilfield services sector

1 Oil pressure

2Oil pressure

There are many factors putting pressure on oil price

Geopolitical changes and political unrest

Restrictive legislation and sanctions

DemandChinese growth narrative

Central bank decisions

OPEC decisions

Additional producer countries

Over productionReserves and spare capacity

Significant weather events and disasters i.e. hurricanes and oil spills

Changing cost metrics

Additional resources i.e. American shale and deep water

Market sentiment

Dollar FX rates

Oilfield services companies are responding by cutting costs, however more fundamental change is required to protect the sector’s future.

Whilst the oilfield services sector has benefitted in recent years through strong oil prices, companies are now experiencing major change and must address the consolidation opportunities this presents.

There will continue to be multiple variable factors that contribute to the volatility of oil prices and it is almost impossible to identify the new normal. Oilfield services companies are under pressure as a result of the price impact on their upstream oil company customers.

3 Oil pressure

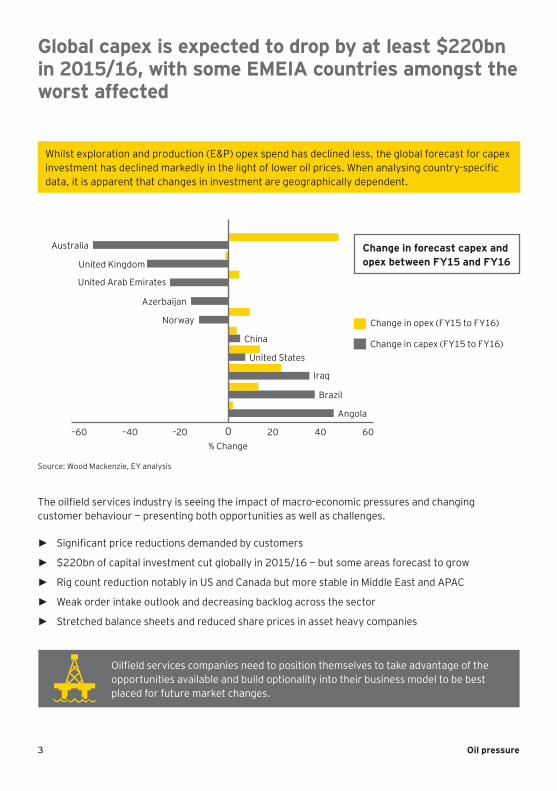

Global capex is expected to drop by at least $220bn in 2015/16, with some EMEIA countries amongst the worst affected

Whilst exploration and production (E&P) opex spend has declined less, the global forecast for capex investment has declined markedly in the light of lower oil prices. When analysing country-specific data, it is apparent that changes in investment are geographically dependent.

Change in opex (FY15 to FY16)

Change in capex (FY15 to FY16)

% Change

Australia

United Kingdom

United Arab Emirates

Norway

Azerbaijan

China

Iraq

Brazil

United States

0

Angola

20–20 40–40 60–60

Source: Wood Mackenzie, EY analysis

Oilfield services companies need to position themselves to take advantage of the opportunities available and build optionality into their business model to be best placed for future market changes.

Change in forecast capex and opex between FY15 and FY16

The oilfield services industry is seeing the impact of macro-economic pressures and changing customer behaviour — presenting both opportunities as well as challenges.

► Significant price reductions demanded by customers

► $220bn of capital investment cut globally in 2015/16 — but some areas forecast to grow

► Rig count reduction notably in US and Canada but more stable in Middle East and APAC

► Weak order intake outlook and decreasing backlog across the sector

► Stretched balance sheets and reduced share prices in asset heavy companies

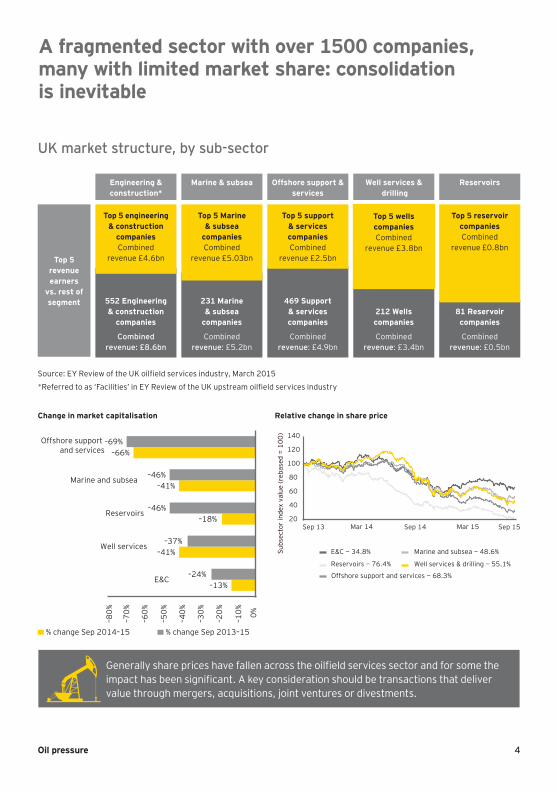

Generally share prices have fallen across the oilfield services sector and for some the impact has been significant. A key consideration should be transactions that deliver value through mergers, acquisitions, joint ventures or divestments.

4Oil pressure

552 Engineering & construction

companies

Combined revenue: £8.6bn

A fragmented sector with over 1500 companies, many with limited market share: consolidation is inevitable

UK market structure, by sub-sector

20

40

60

80

100

120

140

Sep 13 Mar 14 Sep 14 Mar 15 Sep 15

Subs

ecto

r in

dex

valu

e (r

ebas

ed =

100

)

E&C − 34.8% Marine and subsea − 48.6%

Offshore support and services − 68.3%

Reservoirs − 76.4% Well services & drilling − 55.1%

–13%

–41%

–18%

–41%

–66%

–24%

–37%

–46%

–46%

–69%

–80%

–70%

–60%

–50%

–40%

–30%

–20%

–10% 0%

E&C

Well services

Reservoirs

Marine and subsea

Offshore support and services

% change Sep 2013–15% change Sep 2014–15

Change in market capitalisation Relative change in share price

Top 5 revenue earners

vs. rest of segment

Marine & subsea Offshore support & services

Well services & drilling

Reservoirs

Source: EY Review of the UK oilfield services industry, March 2015

*Referred to as ‘Facilities’ in EY Review of the UK upstream oilfield services industry

231 Marine & subsea

companies

Combined revenue: £5.2bn

469 Support & services companies

Combined revenue: £4.9bn

Engineering & construction*

Top 5 engineering & construction

companies Combined

revenue £4.6bn

212 Wells companies

Combined revenue: £3.4bn

Top 5 Marine & subsea

companies Combined

revenue £5.03bn

Top 5 support & services companies Combined

revenue £2.5bn

Top 5 wells companies Combined

revenue £3.8bn

81 Reservoir companies

Combined revenue: £0.5bn

Top 5 reservoir companies Combined

revenue £0.8bn

5 Oil pressure

6Oil pressure

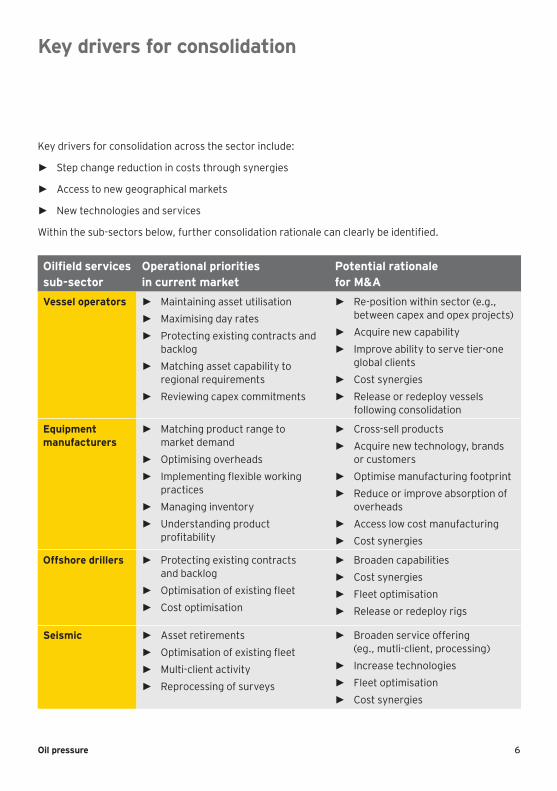

Key drivers for consolidation

Oilfield services sub-sector

Operational priorities in current market

Potential rationale for M&A

Vessel operators ► Maintaining asset utilisation ► Maximising day rates ► Protecting existing contracts and

backlog ► Matching asset capability to

regional requirements ► Reviewing capex commitments

► Re-position within sector (e.g., between capex and opex projects)

► Acquire new capability ► Improve ability to serve tier-one

global clients ► Cost synergies ► Release or redeploy vessels

following consolidation

Equipment manufacturers

► Matching product range to market demand

► Optimising overheads ► Implementing flexible working

practices ► Managing inventory ► Understanding product

profitability

► Cross-sell products ► Acquire new technology, brands

or customers ► Optimise manufacturing footprint ► Reduce or improve absorption of

overheads ► Access low cost manufacturing ► Cost synergies

Offshore drillers ► Protecting existing contracts and backlog

► Optimisation of existing fleet ► Cost optimisation

► Broaden capabilities ► Cost synergies ► Fleet optimisation ► Release or redeploy rigs

Seismic ► Asset retirements ► Optimisation of existing fleet ► Multi-client activity ► Reprocessing of surveys

► Broaden service offering (eg., mutli-client, processing)

► Increase technologies ► Fleet optimisation ► Cost synergies

Key drivers for consolidation across the sector include:

► Step change reduction in costs through synergies

► Access to new geographical markets

► New technologies and services

Within the sub-sectors below, further consolidation rationale can clearly be identified.

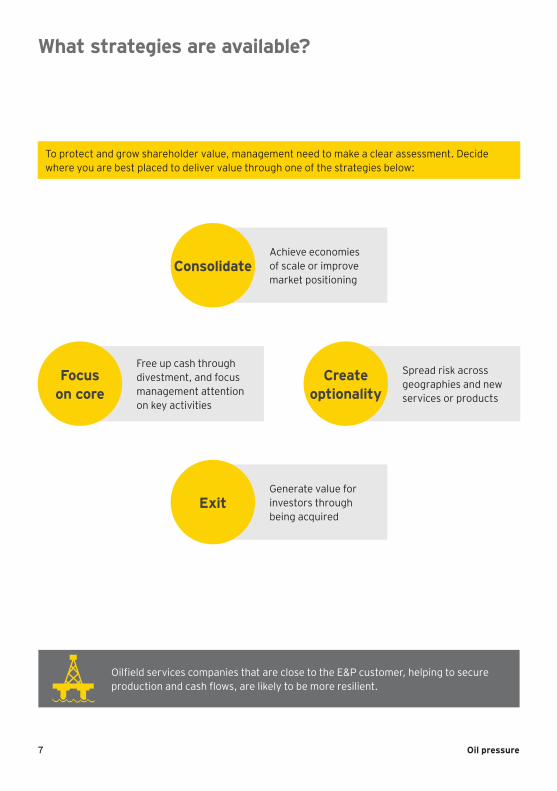

Achieve economies of scale or improve market positioning

Consolidate

Generate value for investors through being acquired

Exit

Spread risk across geographies and new services or products

Create optionality

Free up cash through divestment, and focus management attention on key activities

Focus on core

7 Oil pressure

What strategies are available?

To protect and grow shareholder value, management need to make a clear assessment. Decide where you are best placed to deliver value through one of the strategies below:

Oilfield services companies that are close to the E&P customer, helping to secure production and cash flows, are likely to be more resilient.

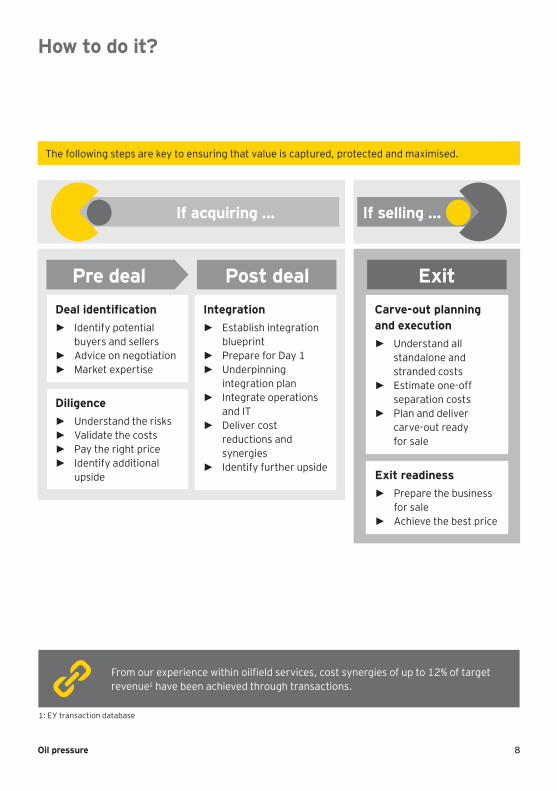

Pre deal Post dealDeal identification

► Identify potential buyers and sellers

► Advice on negotiation ► Market expertise

Integration ► Establish integration

blueprint ► Prepare for Day 1 ► Underpinning

integration plan ► Integrate operations

and IT ► Deliver cost

reductions and synergies

► Identify further upside

Carve-out planning and execution

► Understand all standalone and stranded costs

► Estimate one-off separation costs

► Plan and deliver carve-out ready for sale

Exit readiness ► Prepare the business

for sale ► Achieve the best price

Diligence ► Understand the risks ► Validate the costs ► Pay the right price ► Identify additional

upside

If acquiring … If selling …

Exit

1: EY transaction database

8Oil pressure

How to do it?

The following steps are key to ensuring that value is captured, protected and maximised.

From our experience within oilfield services, cost synergies of up to 12% of target revenue1 have been achieved through transactions.

9 Oil pressure

EY brings you a wealth of experience, global reach and has proven ability in supporting oilfield services companies during transactions

EY has over

10,000 Oil & Gas industry specialists across the globe, with

a wealth of industry and functional knowledge

1

3

6

Divestment of a global marine contractor business

EY advised a global offshore contractor on its acquisition of a North Sea/GoM deepwater SURF and floater installation company. The target was carved out from a global OFS company

1

Merger of two major oilfield services companies

EY supported client and target company management to plan and execute the integration

2

Acquisition of a global EPC business

EY advised a global engineering services company in its key acquisition of a global O&G E&C company. The acquisition materially increased the size of the workforce from 30,000 to 45,000 and was a key milestone in the company’s transition from turnaround to growth

3

10Oil pressure

EY brings you a wealth of experience, global reach and has proven ability in supporting oilfield services companies during transactions

4

1

1 5

3

2

6

Acquisition of a well intervention services company

EY assisted the client with reorganising its existing European well intervention services business ahead of the acquisition of a middle-eastern competitor

4

Carve out of a subsea products business

EY planned and supported the reorganisation and sale of a subsea products business

5

Merger of two global EPC businesses

EY advised a major international engineering and consultancy company in its acquisition of another publicly listed E&C business. The transaction expands the client’s offering and geographic footprint, and allows for efficiency savings in reduced overheads

6

11 Oil pressure

Contacts

Andy Brogan

Partner — Global Head of Oil & Gas Transactions

Tel: + 44 20 7951 7009Email: [email protected]

Glenn Peters

Partner — Restructuring

Tel: + 44 20 7951 4423Email: [email protected]

Eraj Weerasinghe

Director — TAS, Valuation & Business Modeling

Tel: + 44 20 7951 0565Email: [email protected]

Tim Bunnell

Director — Operational Transaction Services

Tel: + 44 20 7951 4708Email: [email protected]

Barry Fraser

Executive Director — Lead AdvisoryTel: + 44 122 4653 255Email: [email protected]

Michael McCartney

Director — Capital & Debt Advisory

Tel: + 44 20 7951 3263Email: [email protected]

Céline Delacroix

Executive Director — Oilfield Services Corporate Finance

Tel: + 44 20 7806 9204Email: [email protected]

Michel Driessen

Partner — Operational Transaction Services

Tel: + 44 20 7951 8792Email: [email protected]

David Rees

Executive Director — Operational Transaction Services

Tel: + 44 20 7951 2171Email: [email protected]

Stuart White

Director – TAS Transaction Diligence

Tel: + 44 122 4653 9199Email: [email protected]

12Oil pressure

13 Oil pressure

Notes

14Oil pressure

Notes

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2015 EYGM Limited. All Rights Reserved.

EYG No. DE0644

29667.indd (UK) 11/15. Artwork by Creative Services Group Design.

ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/oilandgas