PRIME INVESTMENT RESEARCH AUTOMOTIVE |EGYPT GB AUTO – INITIATION OF COVERAGE JANUARY, 14 TH 2016 PRIME INVESTMENT RESEARCH BUILDING MATERIALS |EGYPT EZZ STEEL – INITIATION OF COVERAGE JANUARY, 24 TH 2016 WE INTIATE COVERAGE FOR … EZZ STEEL … ASSIGNING A “BUY” RATING EGYPT’S STEEL DEMAND IS SOLID AND PERFORMING WELL, SUPPORTED BY THE LARGEST AND GROWING POPULATION IN THE MENA REGION, STRONG DEMAND FOR RESIDENTIAL UNITS AND PLANS OF MEGA PROJECTS. SLOWDOWN IN THE CHINESE ECONOMY WEIGHS ON THE GLOBAL STEEL INDUSTRY AND ACCORDINGLY, THE DOMESTIC ONE. CONTINUITY OF OVERSUPPLY OF IRON ORE OVER THE SHORT-TERM, WILL MAINTAIN GLOBAL PRICE UNDER PRESSURE AND PREVENTING LOCAL PLAYERS FROM PASSING FULL INCREASES IN COGS TO END CONSUMERS, ESPECIALLY WITH THE AVAILABILITY OF CHEAPER IMPORTED STEEL. EZZ STEEL SHOWED SOLID OPERATING PERFORMANCE IN THE PAST YEARS DESPITE THE POLITICAL UNREST IN EGYPT. AL EZZ AL DEKHILA IS THE CORNERSTONE FOR THE GROUP, WHEN IT FALLS THE WHOLE GROUP COLLAPSE. NEW DRI PLANT TO ENHANCE MARGINS IN BOTH EFS & ESR, AND ACCORDINGLY THE WHOLE GROUP OVER THE MEDIUM TERM. WE INITIATE COVERAGE FOR EZZ STEEL AT A FAIR VALUE OF EGP 11.22/SHARE IMPLYING A 69% UPSIDE POTENTIAL. HENCE, WE ASSIGN ESRS A “BUY” RATING.

Transcript

PRIME INVESTMENT RESEARCH AUTOMOTIVE |EGYPT

GB AUTO – INITIATION OF COVERAGE JANUARY, 14TH

2016

PRIME INVESTMENT RESEARCH

BUILDING MATERIALS |EGYPT EZZ STEEL – INITIATION OF COVERAGE

JANUARY, 24TH 2016

WE INTIATE COVERAGE FOR … EZZ STEEL … ASSIGNING A “BUY” RATING

EGYPT’S STEEL DEMAND IS SOLID AND PERFORMING

WELL, SUPPORTED BY THE LARGEST AND GROWING

POPULATION IN THE MENA REGION, STRONG

DEMAND FOR RESIDENTIAL UNITS AND PLANS OF

MEGA PROJECTS. SLOWDOWN IN THE CHINESE ECONOMY WEIGHS ON

THE GLOBAL STEEL INDUSTRY AND ACCORDINGLY, THE

DOMESTIC ONE. CONTINUITY OF OVERSUPPLY OF IRON ORE OVER THE

EGYPT. AL EZZ AL DEKHILA IS THE CORNERSTONE FOR THE

GROUP, WHEN IT FALLS THE WHOLE GROUP COLLAPSE. NEW DRI PLANT TO ENHANCE MARGINS IN BOTH EFS

& ESR, AND ACCORDINGLY THE WHOLE GROUP OVER

THE MEDIUM TERM.

WE INITIATE COVERAGE FOR EZZ STEEL AT A FAIR

VALUE OF EGP 11.22/SHARE IMPLYING A 69%

UPSIDE POTENTIAL. HENCE, WE ASSIGN ESRS A “BUY” RATING.

2

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

Ezz Steel is the leading steel producer in Egypt and the MENA region. The company dominated the local steel market for many years and will likely dominate it for many years coming. Ezz steel has managed to occupy half of the local market for long steel with a production capacity of 3.5mn ton. It also occupies almost the half of local market for flat steel with production capacity of 1mn ton. Moreover, EFS operates a flexible capacity of 1.3mn ton whether long or flat. In addition to its directly owned company, Ezz Steel Rebars with a capacity of 1mn ton of long steel, Ezz steel holding company has three subsidiaries, 1- Al Ezz Al Dekhila (2mn ton long steel, 1mn ton flat steel & 3.2mn ton DRI). 2- Al Ezz Flat Steel (1.3mn ton flexible capacity). 3- Al Ezz Rolling Mills (500k ton of long steel).

One of the main advantages that differentiate Ezz Steel from its peers is using the highly efficient production method of Direct Reduced Iron (DRI). This production method depends on the lower cost iron ore and natural gas as main factors of production. The alternative methods use raw materials as scrap and coal which are more expensive relative to iron ore and natural gas. This gives Ezz steel a high cost advantage against its peers. The existing DRI plant is owned and operated by Ezz Al Dekhila with a production capacity of 3.2mn tons of DRI. In addition, Ezz steel enjoys a good reputation in Egypt’s market, through offering high quality products. Ezz Steel to duplicate EZDK business model in EFS & ESR, through a new DRI plant owned by Al Ezz Rolling Mills with a production capacity of 1.9mn ton. The new DRI plant will mainly supply Ezz Flat Steel with the required DRI for production, the remainder DRI will be supplied to Ezz Steel Rebar. The new DRI plant started production in December 2015, supplying Ezz Flat Steel with required raw materials, leading to a limited improve in margins. We believe the new DRI plant will improve EFS & ESR’s margins through providing raw materials, leading to an increase in utilization rates. Meanwhile, the company’s decision to make the new DRI plant under ERM’s control will boost revenues and margins of ERM through selling DRI to EFS & ESR. Therefore, we believe the new DRI will take Ezz Steel to new levels of revenues over the short term and margins over the medium term, in conjunction with the stability in global steel industry. However, we expect Ezz Steel to keep recording net losses till 2018. Our expectation is attributed to the high levels of Ezz Steel’s interest expenses as Ezz has a high level of debt. World’s steel industry is in pain. The sluggish steel demand by China, the largest producer and consumer of steel in the world, led to steel glut in the country. Steel producers in China dumped the rest of the world with that glut leading to plunging prices and suffering high cost producers. Commodities prices also plunged with the lowest iron ore and coking coal prices in more than 7 years. A market share war between iron ore producers led to higher supply and lower prices. The golden age of steel industry is over. The coming years are carrying bad news for the global industry; China’s demand has finally reached its peak when no one was ready, slowing economic growth will make things worse. Prices will keep declining until the situation in China stabilizes leading to stabilizing steel prices, but not booming. With global steel industry suffering, local industry was not any better. An energy crisis arises making it impossible for steel mills to operate. Higher cost of energy since the mid of 2014 coupled with declining steel global prices, has pressured local prices. Unlike global industry, local industry is healing, however, in a slow pace. The energy situation is getting better, and by 2018 we expect the crisis to end. But till then, the crisis will take its time to disappear.

We reached a Fair Value of EGP 11.22 with a “Buy” recommendation, driven from an upside potential of 69%, Using Sum of Parts valuation (SOPT) method. We see Ezz Steel as a very efficient organization but it is faced by many obstacles that tumble its performance.

EZZ STEEL … EFFICIENCY, INTEGRATION & COST ADVANTAGE ….. STILL NOT ENOUGH

Stock Data Outstanding Shares [in mn] 543.26 Mkt. Cap [in mn] 3,536.7 Bloomberg – Reuters ESRS EY / ESRS.CA 52-WEEKS 6.11-16.91 DAILY AVERAGE TURNOVER [in mn] 9.97

Report Contents Valuation & Risks 3-6 Financial Statements 7 Industry Overview 8 Supply Side 9 Consumption 10 Outlook 11 Raw Materials 12-14

Iron Ore Scrap Coking Coal

Global Steel Price 14 Egypt’s Steel Industry 16

Domestic Supply 17 Consumption 19 Price 19

Company Profile 20 Financial Overview 23 Disclaimer 26

0 2 4 6 8

10 12 14 16 18

05-

Jan

-15

05-

Feb

-15

05-

Mar

-15

05-

Ap

r-15

05-

May

-15

05-

Jun

-15

05-

Jul-1

5

05-

Au

g-1

5

05-

Se

p-1

5

05-

Oct

-15

05-

No

v-15

05-

De

c-15

05-

Jan

-16

ESRS EGX - rebased

3

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

PRICE

SOURCE: EZZ STEEL & PRIME ESTIMATES

Valuation

We initiate Ezz Steel with a Fair Value

of EGP 11.22, with a “Buy”

recommendation, using sum of parts

(SOPTs) valuation method. In sum of

parts we conducted separate valuation

models for each company on a standalone

basis.

Despite the global challenges, we are bullish on the Egyptian steel industry, supported by the domestic

demand, which is expected to maintain its powerful for the following,

1- The Largest population in MENA region which hit 90mn in December 2015, with an annual growth rate of

2%. Additionally, Egypt enjoys a young population, with 60% of population are under age of 30 years old.

2- The political stability in Egypt through elections of the parliament members, represents a strong factor in

the process of attracting FDI’s.

3- Massive mega projects in Egypt declared in 2015 presents a strong incentive for the local steel demand

growth in the coming years.

4- With more than one million marriages per annum, the rate of marriages in Egypt increased by 5% in 2014

compared to 2013, which increases demand for residential units as the main engine of steel industry in

Egypt, supporting our positive outlook for the local demand.

5- Mortgage finance in Egypt increased by 54% in the first 10 months of 2015 to register EGP 732mn compared

to EGP 474mn in the same period last year. However, mortgages still represent only 1% of GDP. The CBE

targets increasing this percentage, as it recently introduced amendments to facilitate and increase

mortgages provided for low income segment. The increase in mortgages, which in turn will boost demand

for residential units, will support domestic demand for steel.

6- In addition to the above mentioned factors, Shortage of NG supply will ease starting 2016. We expect Ezz

Steel’s DRI plants to get 50% of NG required for production in 2016. We believe NG supply to plants will

increase gradually.

Ezz steel is not immune from the global plunge in steel

prices. We expect global prices to remain depressed and

will likely decline further in the upcoming 2 years,

however, it will pick up gradually in the long run. As we

expect supply of iron ore will ease through the exit of

small producers from the Chinese market, leading iron

ore prices up. This in turn, will lead to minimize steel

oversupply in Chinese market, and hence in the whole

world. However, local prices will not be highly affected

by this drop for three main reasons: 1- we expect

government to impose higher import tariffs on steel

imports, in response to requests of domestic

manufacturers. 2- Imports restrictions by the CBE on a

lot of the “unnecessary imports” according to the CBE governor, which will limit FX amount allocated to

steel importers & hence reduce imported amount.

3- The devaluation of the local currency.

These reasons will allow Ezz steel to sell at a premium in the domestic market relative to global prices.

Company Equity Value Ownership Contribution

EZDK 6,599,506 55% 3629728.565

ESR/ERM 2,273,731 100% 2273731.47

EFS 563,354 34% 191540.5018

EV 6,095,001

No. of Shares 543,265

Fai Value 11.22

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2015E 2016F 2017F 2018F 2019F 2020F

EG

P/T

on

Global Price (EGP/ton) Ezz price (EGP/ton)

4

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

BEFORE NEW DRI PLANT AFTER NEW DRI PLANT

SOURCE: EZZ STEEL & PRIME ESTIMATES

The new DRI plant will help in diversifying the risk of depending on EZDK as the main source of profit for Ezz

Steel group. With EFS starting production using DRI, it will be transferred to higher levels of margins. The

total DRI production capacity within Ezz group will reach 5.1mn tpa, through adding a new 1.85mn tpa in

ERM to the existing 3.2mn tpa in EZDK.

But with the current energy crisis in Egypt, how the plant would work? According to Ezz steel, they had agreed with

the local government to provide 60-65% of the plant’s needs of NG in 2016, which is sufficient to provide enough DRI

to operate EFS with full capacity. Even if the problem of natural gas continued, operations in facilities will be

maintained. Scrap prices declined from USD 425/ton in 1st of January 2014 to USD 250/ton in Jan 1st

2016 with a

decline of 41%. So we believe that, even if the case of natural gas supply shortage appeared again in 2016 the effect

on operations of Ezz Steel will not be as severe as before, but this will result in recording lower profitability margins as

we saw in EZDK results in 2014 & 2015, due to the higher contribution of scrap in production process to replace DRI.

Process EZDK ESR+ERM EFS

DRI (Mtpa) 3.2 0 0

Meltshop (Mtpa) 3 0.85 1.3

Final product (Mtpa) 3 1.5 1.3

Process EZDK ESR+ERM EFS

DRI (Mtpa) 3.2 1.9 0

Meltshop (Mtpa) 3 0.85 1.3

Final product (Mtpa) 3 1.5 1.3

Source: Prime Calculations

5

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

SOURCE: EZZ STEEL & PRIME ESTIMATES

SOURCE: EZZ STEEL & PRIME ESTIMATES

DRI PRODUCTION & UTILIZATION RATES

SOURCE: EZZ STEEL & PRIME ESTIMATES

EZDK

EZDK is the real deal for Ezz group as

mentioned earlier, so when EZDK faced

problems the whole group was suffering.

The average utilization rates of EZDK for

the three lines of production are

expected to improve in the coming

years, with the expected gradual

increase in NG supply.

We expect that, DRI plant will get higher supply of NG

than previously, which will improve utilization rates and

margins. Our forecast is backed by the improvements in

oil & gas sector and the new discoveries in the

Mediterranean area. In addition, the government started

to pay its debts to foreign oil companies, which will

encourage them to restore their discoveries in the

country.

Nonetheless, we expect low selling prices to put

revenues on the declining trend over the short term and

to pick up gradually. On the other hand, margins will

improve as a result of the higher percentage of DRI used

in production process.

EFS

We are optimistic about EFS and we consider it as the new story. The new DRI plant is finally online and, according

to the company, it started production in December 2015. The new plant owned by ERM will mainly feed EFS with its

needs of DRI, which will turn EFS into an integrated facility; this will boost utilization rates in EFS pushing up sales

revenues for levels that EFS did not witness before. Gross profit margins are expected to improve, because of the cost

advantage of using DRI relative to scrap. However, EFS will not get the full advantage of using DRI, since it will get DRI

supply at prices close to that of scrap. This is one of the reasons we do not see EFS booming the way for Ezz group like

EZDK. Still, it will enhance operation margins, enabling the company to start repaying its debts and helping the group

to reduce high debts level.

EZDK 2014a 2015e 2016f 2017f 2018f

Utilization Rate 80% 67% 75% 79% 83%

Revenues 12,131 11,035 10,712 10,954 11,656

Cogs/Sales 92% 94% 92% 88% 87%

EBITDA Margin 7% 5% 8% 12% 13%

Net Income 36 -241 -155 255 423

NPM 0.3% -2.2% -1.4% 2.3% 3.6%

Dividend Yield 7% 0% 0% 3% 8%

P/B 1.20 1.47 1.57 1.41 1.28

EFS 2014a 2015e 2016f 2017f 2018f

Utilization Rate 30% 25% 70% 75% 85%

Revenues 1,946 1,301 3,811 4,081 4,846

Cogs/Sales 107% 108% 88% 89% 86%

EBITDA Margin -9% -10% 10% 9% 12%

Net Income -438 -399 -41 -73 99

NPM -23% -31% -1% -2% 2%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

0

500

1,000

1,500

2,000

2,500

3,000

2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Th

ou

san

d T

on

DRI Production Utilization Rate in NG

6

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

SOURCE: EZZ STEEL & PRIME ESTIMATES

ESR/ERM

We do not expect profitability margins to enhance significantly in ESR/ERM. The New DRI plant, located in Al Ein

Sokhna, is owned by ERM. Sales revenues from the DRI will boost ERM reported revenues, through selling DRI at

prices near that of scrap, however, margins

will not be enhanced since ERM will still

depends on high cost raw materials in

operating its own 0.5mn tpa of rebar steel.

The main production of the DRI plant will

mainly support EFS with its needs and the

remainder will be allocated to ESR. So that

is why we believe ESR’s margins will not

boom too, as it will buy DRI near scrap

prices, similar to EFS’s case.

Upside Risks

Higher than anticipated steel demand by China leading to a pickup in prices and decline in oversupply.

More NG supply to DRI plants, hence pushing utilization rates margins up.

Higher than expected import tariffs, allowing Ezz Steel to control prices with no pressure.

Lower than expected devaluation of the EGP against USD, reducing the cost of importing raw materials.

Downside Risks

Easing FX crisis, making it easier to import steel leading to availability of cheaper imported steel and

accordingly more aggressive competition.

Lower than expected import tariffs or removal of import barriers by the government. Lower NG supply to DRI plants, leading to lower utilization rates and higher cost of production.

Slowdown in local steel demand.

ESR/ERM 2014a 2015e 2016f 2017f 2018f

Utilization Rate 76% 83% 86% 86% 90%

Revenues 5,321 6,900 8,598 9,120 9,938

Cogs/Sales 96% 93% 91% 92% 93%

EBITDA Margin -1% 1% 3% 2% 1%

Net Income -433 -306 -556 -820 -521

NPM -8% -4% -6% -9% -5%

7

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

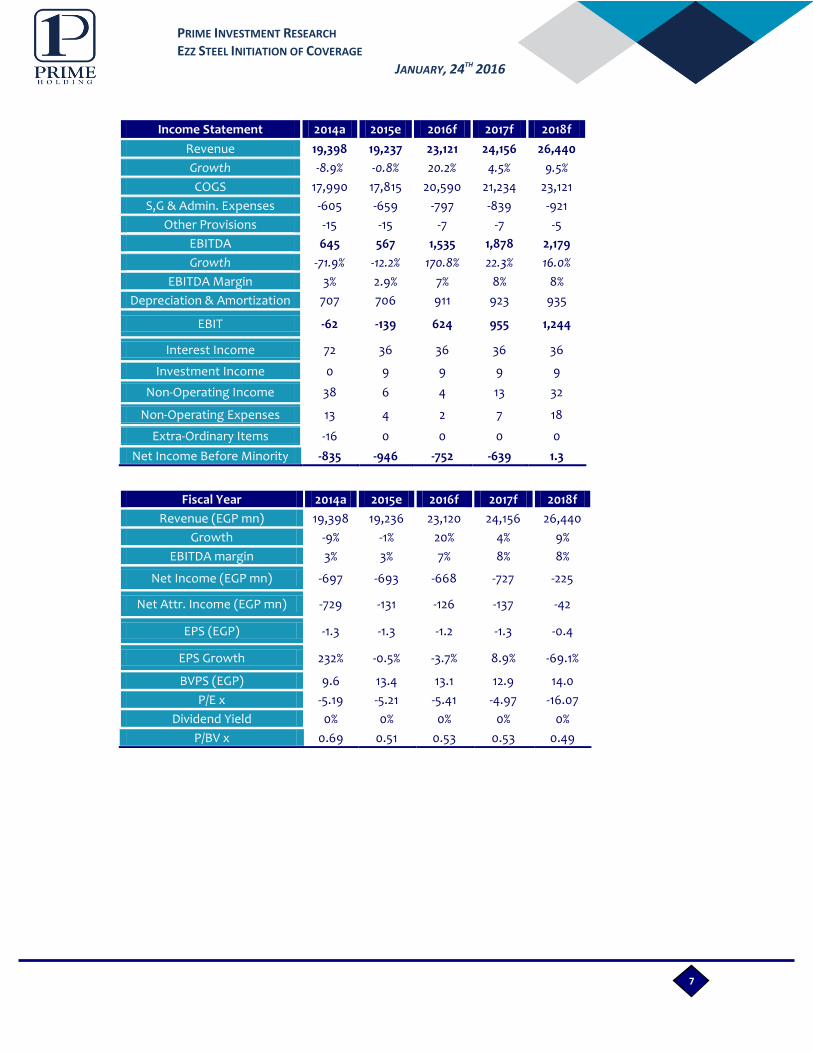

Income Statement 2014a 2015e 2016f 2017f 2018f

Revenue 19,398 19,237 23,121 24,156 26,440

Growth -8.9% -0.8% 20.2% 4.5% 9.5%

COGS 17,990 17,815 20,590 21,234 23,121

S,G & Admin. Expenses -605 -659 -797 -839 -921

Other Provisions -15 -15 -7 -7 -5

EBITDA 645 567 1,535 1,878 2,179

Growth -71.9% -12.2% 170.8% 22.3% 16.0%

EBITDA Margin 3% 2.9% 7% 8% 8%

Depreciation & Amortization 707 706 911 923 935

EBIT -62 -139 624 955 1,244

Interest Income 72 36 36 36 36

Investment Income 0 9 9 9 9

Non-Operating Income 38 6 4 13 32

Non-Operating Expenses 13 4 2 7 18

Extra-Ordinary Items -16 0 0 0 0

Net Income Before Minority -835 -946 -752 -639 1.3

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

WORLD’S CONSUMPTION CHINA’S CONSUMPTION

SOURCE: WSA & PRIME CALCULATIONS

GLOBAL CONSUMPTION

APPARENT CONSUMPTION

SOURCE: WSA & PRIME CALCULATIONS

Consumption

On the other hand, steel consumption also increased remarkably in the last 10-15 years. The key driver for that

growth was also China. Whereas, many countries and regions, specially developed ones, witnessed declining levels of

consumption. However, all of these declines combined were lower than the increasing demand in China, which drove

steel consumption to unprecedented rates in the last decade. The difference in steel consumption growth is depicted

in the below graphs. It is so clear that, if it wasn’t for China’s demand growth, steel industry would have shrunk a lot.

According to WSA estimates, steel consumption is estimated to decline by 1.7% in 2015 to be 1.513bn ton.

China, on its own, consumes almost the half of the world’s total consumption with 711mn ton. The rest of Asian countries except for China, India and Japan, constitutes about 10% and then comes the EU with 9.55%.

Country 2014 mtpa %

China 711 46.24%

India 75 4.90%

Japan 68 4.39%

NAFTA 145 9.41%

EU 147 9.55%

Other Asia 155 10.06%

Other Europe 73 4.75%

CIS 57 3.68%

Africa 64 4.16%

Middle East 52 3.38%

Central and south America 48 3.13%

Australia & New Zealand 7 0.48%

World 1,537 100%

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

2008 2014

Mn

To

n

-34%

0

100

200

300

400

500

600

700

800

2008 2014

Mn

To

n

59%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

2014

2004

11

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

CHINA’S GDP AND STEEL PRODUCTION CORRELATION

SOURCE: WSA & PRIME ESTIMATES

GLOBAL STEEL PRODUCTION & CONSUMPTION

SOURCE: WSA & PRIME CALCULATIONS

Outlook

However, the outlook for steel Industry is not as good as

its history. As mentioned before, global steel industry

mainly depends on China as its main engine. In 2014

Chinese steel demand declined for the first time since

1995. This was a result of the slowdown in the real estate

sector, which accounts for almost half of steel demand in

China. Accordingly, global steel demand declined, prices

crashed and the world found itself with steel glut. The

relationship between global steel market and Chinese

economic growth is depicted in the graph. Any slowdown

in China’s real GDP growth rates is accompanied with

lower steel production, when we calculated the

correlation between GDP growth in China and global steel prices; it was 0.9, which refers to a very high correlation

between the both. In the short run, we believe conditions will be the same in China with declining steel demand or in

best cases a flat one. Our view is backed by the expectations of China’s GDP to continue slowing down to 6.3% in

2016 compared to 6.8% in 2015. Accordingly, we see the economic slowdown in China to weigh negatively on global

steel industry. The even worst case scenario is that, economic growth in China is turning to be at a normal level of

4.5%, which will be another shock for the global market. With estimations that steel demand in China is decreased by

3.3% in 2015 and expected to decrease by 1.9% in 2016, we do not expect a strong rebound in the market in the short

term; however, industry will stabilize at lower rates relative to its history. Our opinion is stemmed from the believe

that; what is happening now in China is a normalization stage that all developed markets have been through before

when they turned from developing markets into developed ones. The historical booming in the industry was

abnormal; we saw that without China, the global steel production and consumption would not grew in these

remarkable levels. Hence, we believe that with China’s economy normalizing, global steel industry will normalize too.

Source: Bloomberg & Prime Research

-10%

-5%

0%

5%

10%

15%

20%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Th

ou

san

d T

on

Steel Production Steel Consumption % Change in Production % Change in Consumption

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

2005 2007 2009 2011 2013 2015

China’s GDP Growth % Steel production Growth %

12

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

SOURCE: WORLD BANK & PRIME CALCULATION

IRON ORE PRODUCERS

SOURCE: WORLD BANK & PRIME CALCULATION

So the simple question now is, has China reached its peak? All indicators show that it is already there and the curve is

declining until it reaches normality. In addition, China is beginning to depend on demand and supply as the main

market factors instead of depending on centrally planned investment, which was concentrated on mass real estate

constructions. And these are not the only bad news, China’s population growth rates are turning downside for the

first time since 2010 and it seems that, it is more of a stable decline not a sudden one, which is, according to experts,

a normal decline and the population growth would have taken a downside route sooner or later.

However, there is still a hope for more future demand since the

percentage level of china’s urbanized population still lags that of the

developed nations. As shown in the table China’s urbanized population

percentage of the total population is still very low compared to other

developed nations. This is an indicator that; there are still great

demand incentives in the largest populated nation, so things will not

crash but rather normalize.

According to the World Steel Association (WSA), the world’s total demand is expected to grow by 2.9% in 2016

compared to a decline by 0.2% in 2015. These expectations are based on china’s economy to stabilize in 2016 and not

to decline even further. WSA expects steel demand in China to contract by 2% in 2016 after a decline of 3.3% and

3.5% in 2014 and 2015, respectively. WSA analysts believe that, emerging markets like India and Mexico in addition to

the MENA region are expected to witness positive demand growth rates in 2016 and in the medium term. Developed

countries are expected to witness positive growth in 2016 by 1.8% compared to a negative one in 2015 by 2.1%. With

US Fed increased interest rates for the first time after the global crisis in 2008 and with another 4 expected hikes in

2016 leading to a dollar appreciation and lower investments, USA is expected to see lower steel demand.

The lower commodity prices caused by China’s slowdown had a negative effect on a lot of markets, Specially

emerging, around the world, lower investments and crashing security markets are all reasons to make us believe that,

in contrast to WSA expectations, world’s total steel demand will grow at slower rate in 2016 than that of WSA, as we

believe that Chinese economy is unlikely to stabilize in 2016.

Raw Materials

As we mentioned earlier, major raw materials in steel Production process are:

Iron Ore

When it comes to iron ore demand, pricing and supply, all eyes turn to China. Since integrated steel making (non recycled steel) is mainly based on iron ore, iron ore demand in China has been growing rapidly in the past years. Seaborne iron ore demand from China increased by 10% per year in the past three years to reach about 700mn tons by 2014. To meet this increasing demand, iron ore miners have significantly increased supply capacity. This means that any drop of China’s demand will have a direct effect on iron ore prices, which really happened. About 98% of mined iron ore is used in steel production and it is one of the most abundant metallic where it makes up about 5% of the earth’s crust. The standard Fe content in iron ore (which is the amount of pure iron exists in iron ore) is 60- 65%, except for Chinese iron ore that is of inferior grade with Fe content of 17-20%. The majority of iron ore is mined in Brazil, Australia, China, India, Russia and US.

Country 2011 2012 2013 2014

China 51% 52% 53% 54%

US 81% 81% 81% 81%

Germany 74% 75% 75% 75%

UK 82% 82% 82% 82%

France 79% 79% 79% 79%

0

100

200

300

400

500

600

700

Mn

To

n

2013

2014

*Note: Chinese production here is converted to correspond with the world average Fe content.

13

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

IRON ORE EXPORTERS IRON ORE IMPORTERS

SOURCE: WSA & PRIME CALCULATIONS

IRON ORE PRICE

SOURCE: BLOOMBERG

Iron ore top producer is Australia followed by Brazil; the two countries together constitute about 50% of iron ore production around the world. Therefore, the largest iron ore producing companies Rio Tinto, Vale and BHP Billiton are located in both Australia and Brazil. China comes third in production by 15% of total production followed by India 8%, Russia 5%, Ukraine 4% and then U.S with 3%.

As the main producers, Australia and Brazil are also the top exporters of iron ore. Both countries constitute together

70% of the total iron ore exports. On the other hand, China dominates imports of iron ore, accounting for more than

60% of the world’s total imports of Iron ore.

With lower demand on iron ore by the main importer China, iron ore prices crashed from USD 133/ton in Jan 1st

2014

to USD 39.58/ton in January 1st

2016, declining by 70%. We expect that; iron ore prices will stay in the thirties for a

while and prices will not be lifted above the thirties before 2017. Our view is backed by the market share war

between the largest iron ore producers and the Chinese small ones. With the lowest cost producers BHP Billiton, Vale

and Rio Tinto want to dominate the Chinese market and throw small producers out of the market completely.

The main sources of iron ore supply to China are Vale (Brazilian company) ,Rio Tinto & BHP Billiton (Australian

companies); presenting about 60% of China’s iron ore imports which gave them a monopolistic pricing power over

iron ore. Iron ore supply increased, although

expectations of cuts in production in response to the

decline in Chinese demand. Large companies mainly

depended on cost cuts in order to meet plunging prices.

BHP Billiton increased its output of iron ore in the

second half of 2015 by 4%, although it reduced its

output of all other commodities like coal and copper.

Rio Tinto also showed increase in both iron ore

production and shipments by 11% in 9m 2015

compared to 9m 2014. The case was not so different

for Vale which increased its iron ore production by 5%

in 2015 compared to the same period in 2014. So if this

case of market share war maintained in 2016 coupled

with the lower Chinese demand for steel, we expect

that iron ore prices will plunge even more for 2016 and

start stabilizing by 2017, with the exit of high cost minors.

Source: WSA & Prime Calculations

Australia 46%

Brazil 24%

south africa 5%

Canada 3%

Ukraine 3%

Russia 2%

Other Countries

17%

China 64%

Rest of the world

36%

0

20

40

60

80

100

120

140

US

D/T

on

14

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

STEEL SCRAP PRICE

SOURCE: BLOOMBERG

COKING COAL IMPORT PRICE IN CHINA

SOURCE: BLOOMBERG

GLOBAL STEEL PRICE

SOURCE: BLOOMBERG

Scrap

In the meantime, steel scrap did not survive the

shrinkage in steel industry; steel scrap prices sought

a huge plunge in its prices from USD 425/ton in 1st

of January 2014 to USD 250/ton in January 1st

2016

with a decline of 41%. We expect steel scrap price

will not collapse as iron ore, since it is not an

abundant commodity as iron ore.

Coking Coal

Being one of the main raw materials in steel

production in China, coking coal did not survive the

hit. China is reducing its use of coal and plans to

impose more restrictions on the use of coal starting

2016 until it reaches its lowest level of coal

consumption by 2025. This move comes due to the

climate change crisis that hits the world, in addition

to the high level of pollution in a country that mainly

depends on coal in each aspect of energy use. With

the economic slowdown, coal consumption in China

already started to decline. Coal import price in China

reached USD 75/ton by October 2015 which is the

lowest in more than 7 years. The lower demand on

coking coal by China due to both the economic

slowdown and the Chinese government efforts to

reduce coal consumption will lead to lower coal

prices which represent a threat for cheaper steel by China, even cheaper than now.

Global Steel Price

Steel Glut led to lower prices. With unexpected

lower demand levels in 2014, China founded itself

loaded with oversupply of steel since producers did

not decrease their production in response to slowing

economic growth. So it simply dumped this

oversupply to the world in cheap prices supported by

the government’s subsidies, devalued currency, low

cost of labor and increasing supply of iron ore despite

of its declining price. This led prices of steel to decline

with about 42% from USD 675/ton in the beginning of

2014 to USD 391/ton as of 31st

December 2015.

0

20

40

60

80

100

120

140

160

180

Jan

/11

May

/11

Se

p/1

1

Jan

/12

May

/12

Se

p/1

2

Jan

/13

May

/13

Se

p/1

3

Jan

/14

May

/14

Se

p/1

4

Jan

/15

May

/15

Se

p/1

5

US

D/T

on

0

100

200

300

400

500

600

700

800

US

D/T

on

0

50

100

150

200

250

300

350

400

450

Jan

-14

Mar

-14

May

-14

Jul-1

4

Se

p-1

4

No

v-14

Jan

-15

Mar

-15

May

-15

Jul-1

5

Se

p-1

5

No

v-15

US

D/T

on

15

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

STEEL PRODUCTION IN CHINA

SOURCE: BLOOMBERG & PRIME CALCULATIONS

In other words, while demand was faltering, steel production was not reduced enough in response to that.

Consequently, imported steel became attractive in many countries despite high freight costs. The increase in Chinese

steel exports is attributed to many reasons: 1- declining levels of demand in China. 2- Subsidies given to exporters

that reached 256% in some countries like USA. 3- Crashes in all raw materials costs. Noting that steel production in

China declined by only 1.9% in the first 11m of 2015 compared to the same period for 2014. For steel prices the

situation is unlikely to change soon. With declining Chinese demand for steel and increasing levels of steel

production and iron ore supply, global prices are expected to stay on the declining trend.

Backed by the depressed global prices, many steel producers suffered from the lower cost excess capacity of China,

which threatened the domestic production of steel in these countries. Thousands of workers lost their jobs in steel

mills around the world, many companies had to reduce capacities and shutting down mills whether temporarily or

permanently like Wisconsin steel in the United States. Chinese steel exports are estimated to be 100mn tons in 2015.

This spurred steel producers around the world to seek governmental intervention to protect the local industry, many

governments responded to steel makers and imposed tariffs on imported steel. Egypt imposed 8% tariff on imported

steel from China and Turkey, Brazil is considering hiking its tariff rate on steel from 8-14% to 5-20%. With 34% of US

mills became idle in 2015; the country is considering a plan to impose 256% tariffs on imported steel from China that

gets 256% subsidies from the Chinese authority. In the meantime, the EU imposed 5 year trade protection against

electric steel products from 5 countries namely; US, Russia, Japan, China and South Korea in order to curb

competition in the local markets.

Although the Chinese government signaled that it intends

to cut excess steel capacity to reduce the oversupply, we

expect that this is unlikely to happen at least in the short

run. And even if it happened it won’t be big enough to

curb massive exports by Chinese steel mills and lift prices

up again. With the end of the Chinese unprecedented

growth cycle that boosted steel demand for the last

decade it is uncertain what will take its place. The low

Chinese demand growth rates are expected to continue

for a long time, since it is very difficult to witness another

booming growth cycle as the one that we witnessed in

China and even if this happened it will take time to help in

the rebound process of steel market. However, many experts see India as the coming force that will take china’s place

and help boosting steel demand. This is unlikely in our opinion due to the huge differences between the two

countries, like political differences in the way that the country is ruled since China is a communist country where the

government controls all the resources which allows it to plan the required production instead of being based on

demand and supply. Planned economy in China allowed the government to direct resources for industrialization

sector to boost GDP growth, however, an economy that is more based on supply & demand will not do that.

Hence, we believe that, the current situation will be maintained for a while, with markets will take some time to get

used to the new demand levels in China and the low commodity prices especially for countries that mainly depends

on some of these commodities as a main source of income such as Australia with iron ore.

56 000

58 000

60 000

62 000

64 000

66 000

68 000

70 000

72 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Th

ou

san

d T

on

2014

2015

16

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

Egypt’s Steel Industry

An industry fighting too many opponents. Although the Egyptian steel market has a lot of advantages like; low cost

manpower and strong domestic demand, it is still faced by many obstacles. The Egyptian steel industry is currently in

a deadlock as it is struggling to survive faced by many challenges; we can set them as follows:

Energy crisis is the big deal here, the country is in a big trouble concerning natural gas supply after 25th of

January 2011 revolution, with the instability of the country causing investors to fly out of it. The main reason of

the crisis is the inability of the government to pay dues owed to foreign oil companies due to the depletion of

foreign reserves. This was faced by the suspension of production and exploration in Egypt by these companies.

The country is facing a real energy crisis since 2012 that reached its peak in 2014 and 2015. Many factories were

not able to operate specially in 3Q 2014 and some factories halted production for many days including EZDK’s

DRI facility that stopped operations for more than 50 days.

The government took a decision in 2014 to remove subsidies on energy sources over the upcoming five years

starting 2014. The decision included the increase of natural gas price for steel industry by 75% from 4

USD/mmbtu to 7 USD/mmbtu and electricity to be 33 piaster/kwh instead of 30 piaster/kwh and it will increase

gradually for 5 years till 2019.

Capital restrictions introduced in February to crush the FX black market, while firms struggled to open letters of

credit to import raw materials. In addition, the devaluation of the Egyptian pound increased cost of raw

materials for any industry that depends on imported raw materials. Not to mention the FX shortage in 2015

made it difficult to import raw materials.

Domestic steel manufacturers were not able to reap the fruits of declining raw material prices. As the cost of

production in the Egyptian steel market increased due to; subsidies removal, depreciated EGP and shortage of

NG, which led to a drop in utilization rates. In addition, declining global steel prices prevented local producers

from passing full increases in cost of production to the end consumer.

Chinese, Ukrainian and Turkish steel imports increased last year to be more than 600k tons. Turkish steel has

the main advantage over the other exporters to Egypt and over the local industry, as it is sold in relatively lower

prices considering of course the low transportation and freight costs since the distance between Egypt and

Turkey is only 1,100 kilometers. Price per ton of Turkish steel reached EGP 5,000 (post the devaluation of the

Egyptian pound against US dollar) after tariffs, transportation and freight costs compared to local steel which

was sold at more than EGP 5,200 (post the devaluation too).

Turkey’s new policy focuses on increasing exports to MENA region to cover the loss of markets like Iraq, where

its exports declined by more than 60% and other markets where Chinese steel exports dumped in with lower

prices. Note that imported steel from Turkey increased by 70% in the first nine months of 2015 to reach 359k

ton with further expectations that it will increase even more. This urged local companies to pressure the

government to impose tariffs on imported steel, the government finally responded and imposed import tariff of

8% on steel rebar for three years with at least EGP 408/ton in the first year and decreasing gradually in the

second and third years. This rate of tariff is considered not enough for local producers who called to impose

anti-dumping tariffs reaching 40% on rebar. We expect that, the government will respond to companies and will

impose higher tariffs on imported steel in the near future as almost all countries around the world took or

planning to take the same step, US for example is planning to impose imported tariffs reaching 256% as

mentioned before.

17

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

EGYPT’S STEEL PRODUCTION

SOURCE: WSA & PRIME CALCULATIONS

EGYPT’S MONTHLY STEEL PRODUCTION

SOURCE: WSA & PRIME CALCULATIONS

SOURCE: WSA & PRIME CALCULATIONS

WORLD STEEL PRODUCTION

Domestic Supply

Egypt’s steel industry did not suffer as expected

after the 25th

of Jan revolution; this was due to

the stability in local demand, which was

stimulated by the mass illegal constructions due

to the absence of the security power. Even in the

years followed the revolution with all the political

unrest in Egypt, steel production was almost

stable. Things really got bad for production in

2014 due to the energy crisis especially in

October, when many factories had to stop

production because of the shortage in natural gas

supplied by the government. In 2015 things got

even worst with lower NG supply and FX crisis, as

production declined further by 14% in the first 11

months of 2015 compared to the same period in 2014.

In 2014 Egypt was ranked 25th amongst the total steel producers with about 6.5mn ton representing about 0.39% of the world’s steel production.

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

FX shortage is not that bad. Despite all the negativity concerning the currency crisis, we believe that there is

something positive about it. Backed by this shortage of foreign currency, and Spurred by the desire to reduce imports

bill and achieve more control on it, the CBE issued some regulations: 1- Capital restrictions introduced in February. 2-

Increasing the required amount to be deposited in EGP to cover letters of credit up to 100% of the total value of letter

of credit from 50%. We believe that, even if local steel industry was affected by this, it had a much more severe effect

on steel importers. For example, a company like Ezz steel would face serious problems to get FX required from banks

to import raw materials, but as compared to importers of steel, Ezz steel is in a much better situation. As banks

provide foreign currency based on priority, where raw materials importers, like Ezz steel is in an advanced position

relative to finished steel importers. This will help curbing lower cost steel imports and will ease some of the pressure

on local steel prices.

The energy crisis is easing, that is what we believe. The government started to pay portions of the dues owed to

foreign oil firms, which reached more than USD 3bn in 2015 declining from more than USD 6bn in 2014. This spurred

many oil firms to restore their activities in the country, whether exploration or production. We believe that; the

energy crisis reached its peak in 2015, and factories will be able to operate in 2016 better than 2015, taking in

consideration low oil prices trading below USD 30 now, with expectations that it might reach USD 20 in 2016 (with

Iran resume exporting). These low prices helped to ease the cost of energy for the local government, allowing it to

import more NG shipments at lower cost. President El Sisi declared in November 2015, that; NG supply shortage is

over and factories will be able to operate normally starting November. In addition, household consumption eased in

4Q 2015 because of the end of summer overload, allowing the government to allocate more NG to industrial sector.

But would it be enough to return to the normal production levels and for factories to operate and make profits? Well

there are other problems like the devaluation of the Egyptian pound and the shortage of the US dollar that continue

to be main obstacles for companies that import raw materials.

Zohr an Industry Resurrection. The hopes to end the energy crisis got really high after ENI, an Italian energy group,

announced in August that; it had discovered the largest known gas field in the Mediterranean off the Egyptian coast

called “Zohr” field that could hold 30tn cubic feet of gas covering an area of about 100sq kilometers, with the

company adjusting later that it could be even bigger than expected. The government agreed with ENI’s CEO that; the

discovery will be completely allocated to the internal market in order to cover all the local needs and the stage of

exporting will probably come later. ENI’s plan was to start production by 2018, but the Egyptian government stated it

hopes that the production will start by 2017. The production will begin at 700mn to 1bn cubic feet per day increasing

to 2.7bn cubic feet per day by 2019. It is expected that the field will satisfy all the needs in the local market by 2018,

so we still believe that in the short run the shortage will continue to hit the industry but with less severity, as we

believe that; the government will prioritize household sector over the industrial one.

19

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

EGYPT’S STEEL CONSUMPTION

SOURCE: WSA & PRIME CALCULATIONS

STEEL PRICES

SOURCE: CBE, BLOOMBERG & PRIME CALCULATIONS

STEEL EXPORTS

SOURCE: CBE & PRIME CALCULATIONS

Consumption

Egypt’s consumption of steel is about 0.66% of the world’s total consumption, with 10mn tons in 2014 ranked 23

rd amongst the

global steel consumers. The key driver for this consumption is real estate sector since Egypt is one of the heavy populated countries in the MENA region with population that reached about 90mn people by December 2015. Although our negative outlook for global steel demand especially in China, we have positive outlook for steel demand in Egypt. We expect demand to witness moderate growth rates, not booming of course, or worst case to be flat but it will maintain its high levels. Egypt witnessed a strong demand in the past years, although political and economical unrest. We are positive on local demand outlook and we believe that the problem is not in demand; however, the problem is in the local industry’s ability to meet this demand which led to massive imports of steel from countries like China and Turkey.

Local Steel Prices

Prices increased largely in 2013 by 11%, caused mainly by the devaluation of the local currency against US dollar by more than 70 piaster. In 2014 the local price stood at the same levels as 2013, affected by the plunge in global prices and competition by imported steel from China and Turkey in relatively lower prices. The lower raw materials cost in 2015 pushed prices down even further; however, Egypt’s steel is still selling at a premium reaching 20% relative to global steel price coupled with the devaluation in EGP. In relation, cheap imported steel, especially from Turkey, helped to depress the local prices. Although the lower raw materials cost can be considered as an advantage for the local steel mills, but this advantage cannot be felt by the companies because of their inability to increase prices to cover the increase in both energy and electricity prices.

Exports are not any better, after 25th of January 2011 revolution exports of steel declined with about 50% and things did not get any better after that, with our expectations that exports will decline even further this year 2015 and will stay low for many years to come, due to higher cost of producing steel locally than in exporting countries.

Country 2014 %

China 711 46.24%

India 75 4.90%

Japan 68 4.39%

NAFTA 145 9.41%

EU 147 9.55%

Other Asia 155 10.06%

Other Europe 73 4.75%

CIS 57 3.68%

Africa 64 4.16%

Middle East 52 3.38%

Central and south America 48 3.13%

Egypt 10 0.66%

Australia & New Zealand 7 0.48%

World 1,537 100%

0

1000

2000

3000

4000

5000

6000

2009 2010 2011 2012 2013 2014 2015

Local Price EGP/Ton Global Price EGP/Ton

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

Mn

US

D

20

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

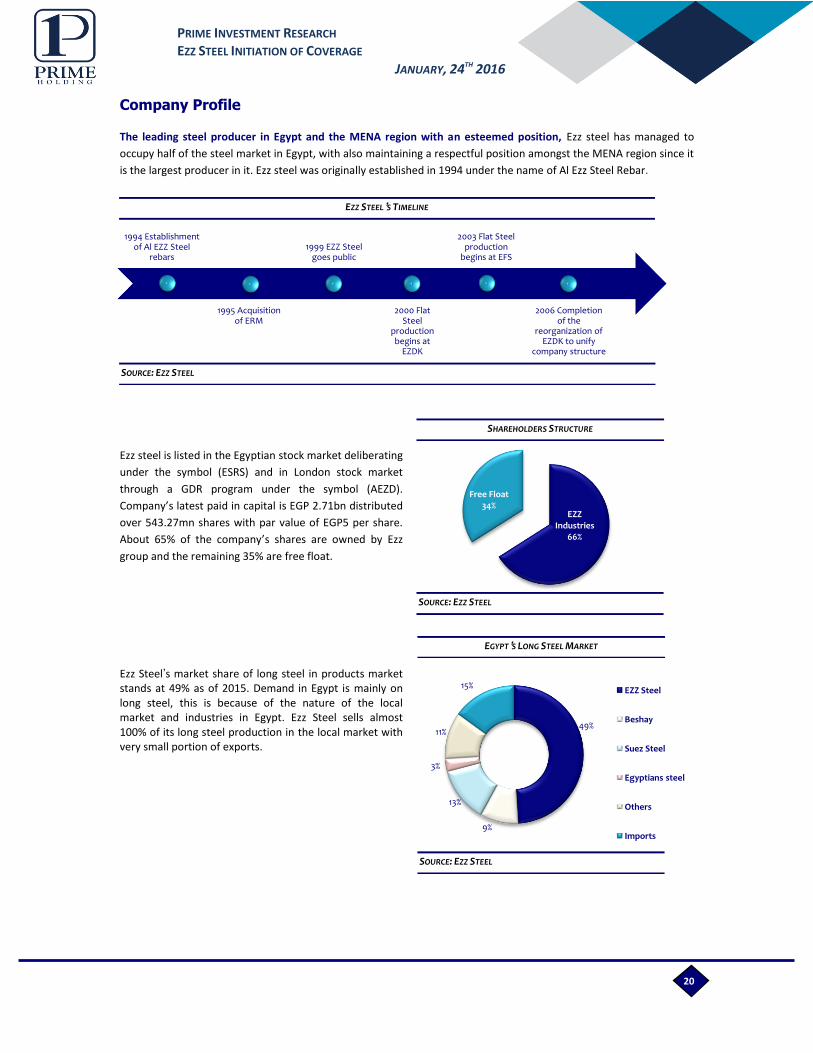

EZZ STEEL’S TIMELINE

SOURCE: EZZ STEEL

SHAREHOLDERS STRUCTURE

SOURCE: EZZ STEEL

EGYPT’S LONG STEEL MARKET

SOURCE: EZZ STEEL

Company Profile

The leading steel producer in Egypt and the MENA region with an esteemed position, Ezz steel has managed to

occupy half of the steel market in Egypt, with also maintaining a respectful position amongst the MENA region since it

is the largest producer in it. Ezz steel was originally established in 1994 under the name of Al Ezz Steel Rebar.

Ezz steel is listed in the Egyptian stock market deliberating

under the symbol (ESRS) and in London stock market

through a GDR program under the symbol (AEZD).

Company’s latest paid in capital is EGP 2.71bn distributed

over 543.27mn shares with par value of EGP5 per share.

About 65% of the company’s shares are owned by Ezz

group and the remaining 35% are free float.

Ezz Steel’s market share of long steel in products market stands at 49% as of 2015. Demand in Egypt is mainly on long steel, this is because of the nature of the local market and industries in Egypt. Ezz Steel sells almost 100% of its long steel production in the local market with very small portion of exports.

1994 Establishment of Al EZZ Steel

rebars

1995 Acquisition of ERM

1999 EZZ Steel goes public

2000 Flat Steel

production begins at

EZDK

2003 Flat Steel production

begins at EFS

2006 Completion of the

reorganization of EZDK to unify

company structure

EZZ Industries

66%

Free Float 34%

49%

9%

13%

3%

11%

15% EZZ Steel

Beshay

Suez Steel

Egyptians steel

Others

Imports

21

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

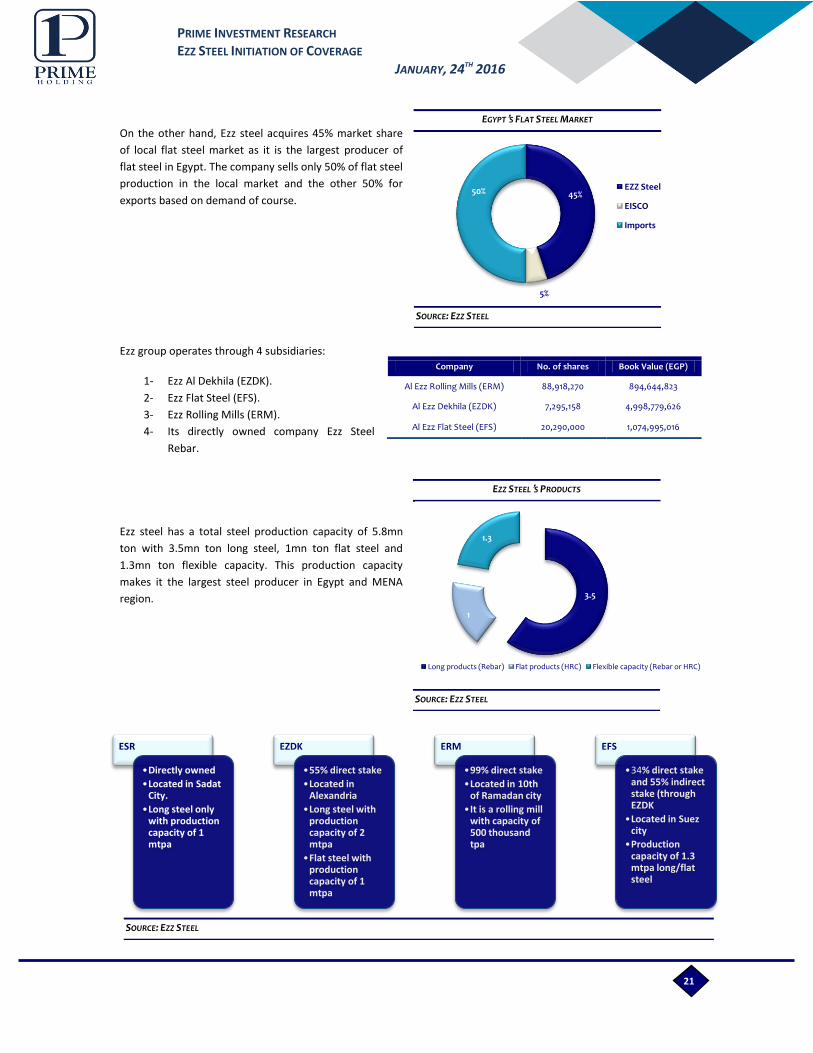

EGYPT’S FLAT STEEL MARKET

SOURCE: EZZ STEEL

EZZ STEEL’S PRODUCTS

SOURCE: EZZ STEEL

SOURCE: EZZ STEEL

On the other hand, Ezz steel acquires 45% market share

of local flat steel market as it is the largest producer of

flat steel in Egypt. The company sells only 50% of flat steel

production in the local market and the other 50% for

exports based on demand of course.

Ezz group operates through 4 subsidiaries:

1- Ezz Al Dekhila (EZDK).

2- Ezz Flat Steel (EFS).

3- Ezz Rolling Mills (ERM).

4- Its directly owned company Ezz Steel

Rebar.

Ezz steel has a total steel production capacity of 5.8mn

ton with 3.5mn ton long steel, 1mn ton flat steel and

1.3mn ton flexible capacity. This production capacity

makes it the largest steel producer in Egypt and MENA

region.

Company No. of shares Book Value (EGP)

Al Ezz Rolling Mills (ERM) 88,918,270 894,644,823

Al Ezz Dekhila (EZDK) 7,295,158 4,998,779,626

Al Ezz Flat Steel (EFS) 20,290,000 1,074,995,016

Source: Company Data

3.5

1

1.3

Long products (Rebar) Flat products (HRC) Flexible capacity (Rebar or HRC)

ESR

•Directly owned

•Located in Sadat City.

•Long steel only with production capacity of 1 mtpa

EZDK

•55% direct stake

•Located in Alexandria

•Long steel with production capacity of 2 mtpa

•Flat steel with production capacity of 1 mtpa

ERM

•99% direct stake

•Located in 10th of Ramadan city

•It is a rolling mill with capacity of 500 thousand tpa

EFS

•34% direct stake and 55% indirect stake (through EZDK

•Located in Suez city

•Production capacity of 1.3 mtpa long/flat steel

45%

5%

50% EZZ Steel

EISCO

Imports

22

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

EZDK SHAREHOLDERS STRUCTURE

SOURCE: EZZ STEEL

EFS BUSINESS STRUCTURE

SOURCE: EZZ STEEL

Ezz Al Dekhila (EZDK) is the major source of profit for Ezz group; it represents about 52% of Ezz steel’s total

production capacity and deliberates in the Egyptian Stock Market under the symbol (IRAX). It is the only fully

integrated steel producer in Ezz group and Egypt backed by 3.2mn tpa production capacity of DRI supporting 3mn tpa

of steel production (2mn tpa Rebar and 1mn tpa HRC).

EZDK adapts a high efficient unique production process not

only in Egypt but in the whole world where only about 4% of

the world steel producers use the same technique. This

process is called DRI method; where iron ore pellets are

introduced to a direct reduction plant where a certain

chemical process happens that ends with Direct Reduced Iron

or DRI. The DRI then is melted in the melt shop, resulting in

slabs or billets that then get to rolling mills to give long or flat

steel. The main advantage of this production process is that it

mainly depends on the cheaper available raw materials; iron

ore and natural gas compared to steel scrap and coal.

The DRI lower cost advantage compared to scrap makes EZDK achieve the highest profit margins compared to its

peers and other subsidiaries of Ezz steel. EZDK is the only facility that exports steel, the level of exports deteriorated

in 2014 to record 17% of sales only as result of the local crisis in production and the slowdown in the global demand.

EZDK was affected the most by the energy crisis. DRI plants depend on natural gas as a factor of production not a

source of energy, so NG cannot be replaced by coal or any other source of energy. With the unavailability of NG, EZDK

was unable to produce DRI; hence, it had to import higher cost scrap to continue production which led to higher cost

of production affecting the company’s profitability.

Ezz Flat Steel (EFS) was mainly designed to target exports

through the production of Flat Steel with production capacity

of 1.3mn tpa, but with the lower demand on flat steel and

higher production costs due its dependence on scrap as the

main raw material it was upgraded in 2012 to produce long

steel too with the same production capacity, so it has flexible

production of 1.3mn tpa of long steel or flat steel.

Even with the flexibility in production EFS still incur losses

because of its dependence on the high cost scrap. A new DRI

plant was constructed to support EFS with its required DRI

which is supposed to increase utilization rates and lowering

costs of production.

Ezz Steel Rebar (ESR) is the directly owned factory by Ezz Steel with a production capacity of one million tpa, while Ezz

Rolling Mill (ERM) is a rolling mill that purchase billets and turn it into long steel with an annual capacity of 0.5mn

ton. As EFS, ESR depends on scrap as the main raw material in production.

Ezz secured two additional DRI licenses with EGP 660mn in the beginning of 2014 (one of them is returned to the

government), construction of one DRI plant at El Ain El Sokhna is over with investments costs of about USD 550mn

financed through 70% debt and 30% equity. The new DRI facility is expected to add an additional production capacity

of DRI equals to 1.9mn tpa that will mainly support production of EFS and the remainder will support ESR. This will

increase the level of integration in the two facilities to be fully integrated as EZDK.

55%

11%

6%

6%

23%

Ezz steel

National Investment bank

Al Ahly Capital Holding

Governmental Social Insurance Fund

Others

55%

34%

11%

EZDK

Ezz Steel

state owned banks (NBE,BM)

23

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

STEEL SALES STEEL PRODUCTION

SOURCE: EZZ STEEL

COGS & COGS/SALES COGS/SALES

SOURCE: EZZ STEEL

Financial Overview

Poor Performance reflecting industry obstacles, Ezz steel showed poor performance in the first 9 months of 2015.

Total sales value declined by 14% in 9M2015 to record EGP 12.759bn compared to EGP 14.88bn in 9M2014. Lower

sales value is ascribed to: 1- lower selling prices. 2- Lower production. Rebar production declined by 13.67%

recording 2.4mn ton in the first 9M of 2015 compared to 2.78mn ton for the same period in 2014, Flat steel

production also declined to be 0.52mn ton in 9M2015 compared to 0.57mn ton in 9M2014. Hence, rebar sales

volume declined by 9% in 9M2015 to be 2.4mn ton compared to 2.63mn ton in 9M2014. Flat steel sales volume also

declined by 17% to be 516k ton in 9M2015.

Gross profit margin recorded 4.6% in the first 9M of 2015 compared to 3.4% in the same period 2014, leading to an increase of 14% in gross profit from EGP 512mn in 9M2014 to EGP 585mn in 9M2015. Although the increase in Energy prices, cogs decreased in 9M2015, this was mainly due to the huge plunge in cost of raw materials, whether scrap or iron ore, and lower purchased quantity due to unavailability of FX & NG.

0

1

2

3

4

5

6

7

-

5,000

10,000

15,000

20,000

25,000

2012 2013 2014 9m 2014 9m 2015

Slaes value (EGP) Sales Volume (Million Ton)

Source: Company Data

0

0.5

1

1.5

2

2.5

3

Rebar Flat steel M

n T

on

9m 2014

9m 2015

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2012 2013 2014 9m 2014 9m 2015

Mn

EG

P

COGS COGS Margin

115.50%

92.80% 98.50%

134%

94% 91%

EFS EZDK ESR/ERM

9m 2014 9m 2015

24

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

EBITDA & EBITDA MARGIN

SOURCE: EZZ STEEL

NET PROFIT & NET PROFIT MARGIN

SOURCE: EZZ STEEL

DEBT/EQUITY

SOURCE: EZZ STEEL

EBITDA recorded EGP 533mn for 9M2015 compared to EGP 504mn for 9M2014, an increase of %5.75 y.o.y. Accordingly, EBITDA margin increased to be 4.17% from 3.38% in the same period 2014. This is mainly because of the lower cost of raw materials leading to lower cogs.

The company’s net loss after minority recorded EGP

509mn in 9M2015 compared to EGP 461mn in

9M2014. Despite the higher GPM in 9M2015

compared to that of 9M2014, the company made

higher net loss. This is because of the increase in

interest expenses by EGP 200mn to record EGP

872mn.

High leverage risk. In 9M2015 debt/equity ratio

registered 2.89x compared to 2.04x in 9M2014. There

is no doubt that one of the major risks of Ezz steel is

its heavy weight of debt; which was increasing

through time with more capex used to finance the

new DRI plant. But with the completion of the DRI

plant and with no further expectations for major

investments we expect that, these high levels of debts

will ease through time with higher levels of debts

serving, which will also affect negatively our expected

bottom line over the coming three years.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

-

500

1,000

1,500

2,000

2,500

2012 2013 2014 9m 2014 9m 2015

Mn

EG

P

EBITDA EBITDA Margin

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

(1,000)

(800)

(600)

(400)

(200)

-

200

400

600

2012 2013 2014 9m 2014 9m 2015

Mn

EG

P

Net profit(loss) Net profit(loss) margin

0

0.5

1

1.5

2

2.5

3

3.5

2012 2013 2014 9m 2015

25

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

JANUARY, 24TH 2016

26

PRIME INVESTMENT RESEARCH EZZ STEEL INITIATION OF COVERAGE

HEAD OFFICE PRIME SECURITIES S.A.E. 2 Wadi El Nil St., Liberty Tower, 7th-8th Floor, Mohandessin, Giza, Egypt Tel: +202 33005700/770/650/649 Fax: +202 3760 7543

Disclaimer Information included in this report has no regard to specific investment objectives, financial situation, advices or particular needs of the report users.

The report is published for information purposes only and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Unless specifically stated otherwise, all price information is only considered as indicator.

No express or implied representation or guarantee is provided with respect to completeness, accuracy or reliability of information included in this report.

Past performance is not necessarily an indication of future results. Fluctuation of foreign currency rates of exchange may adversely affect the value, price or income of any products mentioned in this report.

Information included in this report should not be regarded by report users as a substitute for the exercise of their own due diligence and analysis based on own assessment and judgment criteria. Any opinions given are subject to change without notice and may significantly differ or be contrary to opinions expressed by other Prime business areas as a result of using different assumptions and criteria. Prime Group is under no obligation responsible to update or keep current the information contained herein.

Prime Group, its directors, officers, employees or clients may have or have had interests or long or short positions in the securities and/or currencies referred to herein, and may at any time make purchases and/or sales in them as principal or agent.

Prime Group, its related entities, directors, employees and agents accepts no liability whatsoever for any loss or damage of any kind arising from the use of all or part of these information included in this report. Certain laws and regulations impose liabilities which cannot be disclaimed. This disclaimer shall, in no way, constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

Furthermore, Prime Group or any of the group companies may have or have had a relationship with or may provide or have provided other services, within its objectives to the relevant companies. Prime Group 2016 all rights reserved. You are hereby notified that distribution and copying of this document is strictly prohibited without the prior approval of Prime Group.