Page 1

Fact Book 2010 |

© Continental AG

1

1

Fact Book Fiscal Year 2010

2

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive GroupV.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

Page 2

Fact Book 2010 |

© Continental AG

2

3

Continental at a Glance

140 Years of Progress and Achievement

Merger with major companies of

the German rubber industry to

form Continental Gummi-Werke

AG.

Acquisition of a US company’s

Automotive Brake & Chassis

unit, the core of which is Alfred

Teves GmbH in Frankfurt.

Continental-Caoutchouc- and

Gutta-Percha Compagnie is

founded in Hanover, Germany.

Continental strengthens its

position in the ASEAN region

and Australia by establishing

its Continental Sime Tyre joint

venture.

Takeover of the European tire operations of Uniroyal,

the tire operations of the Austrian company Semperit,

the North American tire manufacturer General Tire.

Continental reinforces its activities by

acquiring Temic, the international

electronics specialist.

Continental acquires Siemens VDO

Automotive AG and advances to

among the top five suppliers in the

automotive industry worldwide, at the

same time boosting its market position

in Europe, North America and Asia.

Continental expands its activities in

telematics, among other fields, with

the acquisition of the automotive

electronics business from Motorola.

Through the acquisition of Phoenix

ContiTech becomes the world‟s largest

specialist for rubber and plastics

technology outside the tire industry.

1871

1929

1979

1985

1987 1998

2001

2003 2004

2006

2007

Continental acquires a majority interest in

the Slovak company Continental Matador

Rubber s.r.o. and expands its position for

the Tires and ContiTech divisions in central

and eastern Europe.

4

6,743

9,132

10,115

11,233 11,408 11,534

12,597

13,837

14,887

16,619

24,239

20,096

26,047

398 607 533

33

694 855 1,157

1,507 1,602 1,676

-296 -1,040

1,935

138 235 205 -258

226 314 716 930 982 1,021

-1,124 -1,649

576

0

5,000

10,000

15,000

20,000

25,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007³ 2008 2009 2010

Sales

EBIT

NIAT2)

US GAAP IFRS

Continental at a Glance

Continental Corporation – Sales, EBIT & Net Income1)

1) From 1998 until 2003 US GAAP / from 2004 onwards IFRS

2) Net income attributable to the shareholders of the parent under IFRS since 2004

3) Since December 1, 2007, including Siemens VDO

(in € million)

Page 3

Fact Book 2010 |

© Continental AG

3

5

Continental at a Glance

Executive Board – Together more than 170 Years of ExperienceA

UT

OM

OT

IVE

GR

OU

P

Supervisory Board headed by Prof. Dr. Wolfgang Reitzle

Chief Financial Officer

Finance; Controlling; Law; IT

24 years of experience

Passenger and Light Truck Tires Division

14 years of experience

Commercial Vehicle Tires Division

Purchasing

21 years of experience

ContiTech Division

Director of HR and Labor Relations

31 years of experience

Wolfgang Schäfer

Nikolai Setzer

Dr. Hans-Joachim Nikolin

Heinz-Gerhard Wente

RU

BB

ER

GR

OU

P

Chassis & Safety Division

15 years of experience

Dr. Ralf Cramer

Powertrain Division

26 years of experience

José Avila

Interior Division

24 years of experience

Helmut Matschi

Chairman of the Executive Board

Quality & Environment; Corp. Comm.

18 years of experience

Dr. Elmar Degenhart

6

Evolution 2000–2010

EU 27 road fatalities

CO2 targets EU, US & China (g/km)

(1) China fuel consumption standard III is estimated at 20% further

saving /Sources: GS Research, Gao Hua Securities Research

estimates

Safety - vision zero

Environment - clean power Information - always on

Affordable Cars - mobility for everyone

Infotainment

11.0

15.3

2010 2015E

A&B segment in BRIC (million units)

Multimedia

GPS / Galileo

Infrastructure Other Cars

75.426

70.731

65.44163.90363.155

59.40960.26758.982

57.69156.427

54.30253.342

50.351

47.29045.346

43.10442.500

38.900

34.500

54.302

51.285

48.268

45.252

42.235

39.218

36.201

33.185

30.168

27.151

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EU road fatalities

EU fatalities EU target to halve the number of fatalities by 2010EU fatalities EU target to halve the number of fatalities by 2010

158130

95

198 198167

214

155 155

2008 2012E 2020E

EU US China

Source: CSM March 2011

Continental Strategy

Megatrends in the Automotive Industry

Page 4

Fact Book 2010 |

© Continental AG

4

7

6.8

12.9

2008 2015E

Continental at a Glance

Leading Global Position in Key Automotive Electronics Applications

Source: Global Insight, The Freedonia Group

1) ESC: Electronic Stability Control is a type of electronic brake system

2) Source: Frost & Sullivan, December 2009

Actuation

Advanced driver assistance

systems

Airbag electronics

Electronic brake systems (EBS)

Foundation brake systems

Diesel injection systems

Gasoline injection systems

Transmission control units

Double clutch transmission

control units

Body & security products

CV interiors

Device connectivity & telematics

units

Instrumentation and displays &

human machine interfaces

Sales 2010 €5,775 mill.

% of total 22%

Sales 2010 €4,731 mill.

% of total 18%

Sales 2010 €5,518 mill.

% of total 21%

ESC1 installation rate by region (%)

Gasoline direct injection systems

installation rate by region (%) Telematics market2 (in $ billion)

Chassis & Safety Powertrain Interior

13%

28%

9%

33%

2010 2015E

EU NAFTA

63%

86%85%

98%

2010 2015E

EU NAFTA

8

Sales 2010 €3,095 mill.

% of total 12%

Continental at a Glance

Leading Global Position in Tire and Non-Tire Rubber

Sales breakdown (%)

Europe overall

Europe OE

Europe winter tires

North America among Top 5

Europe overall

Europe OE

Europe industrial tires

North America among Top 5

Automotive hoses & hose lines

Automotive interior trim

Conveyor belts

Marine & oil hoses & hose lines

Multiple V-ribbed belts & timing belts

Railway air springs

Truck & bus air springs

Sales 2010 €5,821 mill.

% of total 22%

Sales 2010 €1,428 mill.

% of total 5%

Passenger & Light Truck Tires Commercial Vehicle Tires ContiTech

Sales breakdown (%) Sales breakdown (%)

OE25%

Non-OE

75%

OE18%

Non-OE

82%OE

54%

Non-OE

46%

Page 5

Fact Book 2010 |

© Continental AG

5

9

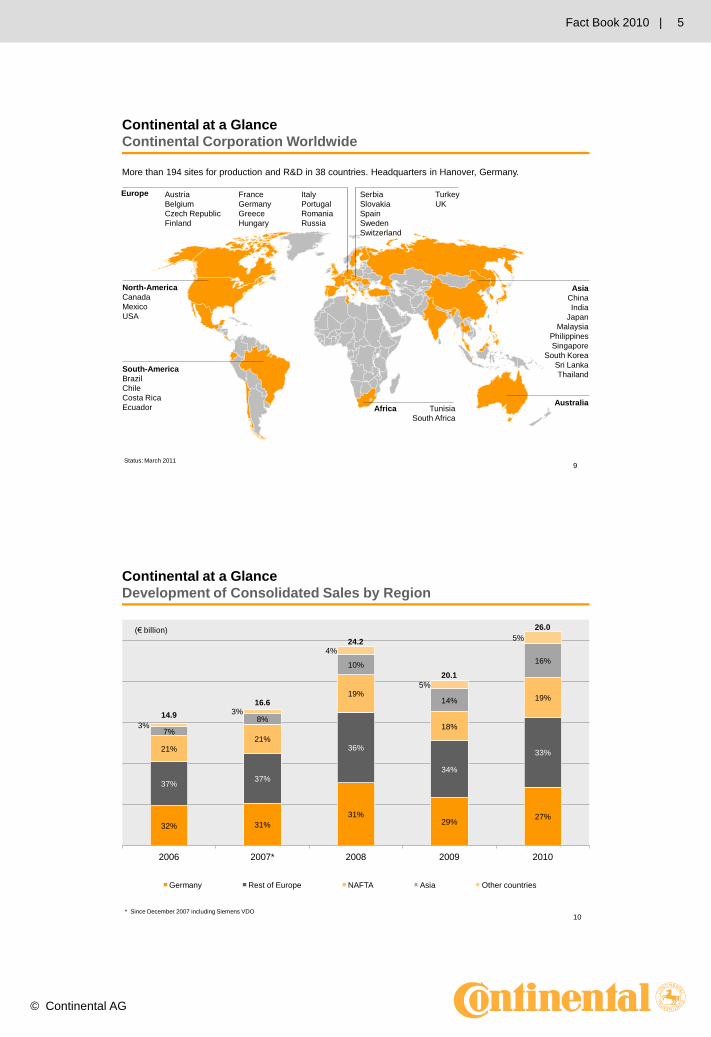

Continental at a Glance

Continental Corporation Worldwide

More than 194 sites for production and R&D in 38 countries. Headquarters in Hanover, Germany.

Status: March 2011

Europe

South-America

Brazil

Chile

Costa Rica

Ecuador

Asia

China

India

Japan

Malaysia

Philippines

Singapore

South Korea

Sri Lanka

Thailand

Tunisia

South Africa

AfricaAustralia

Austria

Belgium

Czech Republic

Finland

France

Germany

Greece

Hungary

Serbia

Slovakia

Spain

Sweden

Switzerland

Turkey

UK

North-America

Canada

Mexico

USA

Italy

Portugal

Romania

Russia

10

Continental at a Glance

Development of Consolidated Sales by Region

* Since December 2007 including Siemens VDO

32% 31%

31%29%

27%

37%37%

36%

34%

33%21%

21%

19%

18%

19%

7%

8%

10%

14%

16%

3%

3%

4%

5%

5%

14.9

16.6

24.2

20.1

26.0

2006 2007* 2008 2009 2010

(€ billion)

Germany Rest of Europe NAFTA Asia Other countries

Page 6

Fact Book 2010 |

© Continental AG

6

11

Continental at a Glance

Development of Consolidated Sales by Division

* Since December 2007 including Siemens VDO

** Automotive Systems until 2006

9%

24%21%

21%7%

16%

17%

18%

28%

21%

22%

22%

40%

31%

29%

21%

23%

22%

10%

9%

6%

5%

5%

19%

18%

12%

12%

12%

14.9

16.6

24.2

20.1

26.0

2006 2007* 2008 2009 2010

(€ billion)

Interior Powertrain Chassis & Safety Automotive Systems** Passenger and Light Truck Tires Commercial Vehicle Tires ContiTech

12

35%

34%33% 33% 31%

32%

32%

33%33%

32%17%

17%

16%14%

14%

11%

12%

13%14%

16%

5%

5%

5%6%

7%

85,224

151,654

139,155134,434

148,228

2006 2007* 2008 2009 2010

Germany Rest of Europe NAFTA Asia Other Countries

Continental at a Glance

Number of Employees by Region

* Since December 2007 including Siemens VDO

Page 7

Fact Book 2010 |

© Continental AG

7

13

Continental at a Glance

Number of Employees by Division

* Since December 2007 including Siemens VDO

** Automotive Systems until 2006

22% 22% 20% 20%

21%18%

18%18%

18%19%

20%

21%

35%

29%

17%19%

20%

19%

10%

6%6%

6%

5%

26%

16%

16%

16%

17%

151,654

139,155

134,434

2006 2007* 2008 2009 2010

Interior Powertrain Chassis & Safety Automotive Systems** Passenger and Light Truck Tires Commercial Vehicle Tires ContiTech

85,224

148,228

14

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive GroupV.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

Page 8

Fact Book 2010 |

© Continental AG

8

15

Continental Strategy

We Shape the Megatrends in the Automotive Industry

Information - Always on Affordable Cars - Mobility for everyone

Environment – Clean powerSafety – Vision zero

16

Continental Strategy – Megatrend Environment

Initiatives in EU, USA and Japan – Towards Cleaner Mobility

EU sets average CO2 emissions

from 2012 at 130 g/km (currently

160 g/km) by means of improvement

in vehicle technology

From 2020 onwards, the target is

95 g CO2/km for the new car fleet

From 2012 onwards, excess

emissions premium if not meeting

targets

EU1

1) Regulation (EC) No. 443/2009

2) Refers to the joint proposal of NHTSA and EPA, May 2009, and President Obama´s NFPE; The White House, May 19, 2009

3) Refers to “Law on Rationalization of Energy Use” of the Ministry of Economics, Trade and Industry

4) NHTSA: National Highway Traffic Safety Administration

5) EPA: Environmental Protection Agency

6) CAFE: Corporate Average Fuel Economy

7) ECCJ: Energy Conservation Center Japan

Emerging markets likely to follow Europe/USA/Japan on fuel efficiency standards

NHTSA4 and EPA5 to establish a

National Fuel Efficiency Policy (NFEP):

Increase CAFE6 from 25 mpg to

35.5 mpg by 2016 for passenger

cars and light trucks combined

Target is equivalent to a reduction in

CO2 from 210 g/km to 180 g/km

From 2020 onwards, the CAFE6

target is equivalent to 130g/km

USA2

ECCJ7 targets to improve fuel

efficiency standards by 23.5% by 2015

vs. 2004:

Increase average level of fuel

efficiency from 13.6 km/l to 16.8 km/l

for passenger cars

Target is equivalent to a reduction in

CO2 from 170 g/km to 140 g/km

Japan3

Page 9

Fact Book 2010 |

© Continental AG

9

17

Continental Strategy – Megatrend EnvironmentReduction of CO2 Emissions1: Solutions by Continental

Hybrid electric vehicle

Piezo common rail injection

Gasoline direct injection

Engine downsizing and turbocharger

SCR² systems/DDS³

Telematics, ACC, ADAS

Energy management (AES⁴)

Tires (rolling resistance, TPMS)

Double clutch transmission

Transmission (POD⁵)

Energy management (POD⁵)

Brake systems Min Max

~25%

~25%

15-20%

~15%

5%

5%

2-5%

3%

3%

1-2%

1-2%

1) Saving potential compared with gasoline port fuel injection Euro 4

2) Selective Catalytic Reduction

3) DEKA injector for diesel dosing into exaust gas

4) Advanced Energy Supply

5) Power-on-demand

5%

18

Continental Strategy – Megatrend Environment

Roadmap towards “Clean Power”: Selection of Technologies

Turbo Charger

Downsizing

2010 20202015

CO2 Reduction

Start-

Stop

Hybrid

Technology

Range

Extender

Full EV

Injection

Technology

Variable

Compression

RatioExhaust

Heat

Recovery

Time

Page 10

Fact Book 2010 |

© Continental AG

10

19

Continental Strategy – Megatrend Environment

ContiTech – Green Technologies

Pure printing

Designed

Green*

Lightweight

construction*

Perfect swing

for wind power

Ecological

pioneer*

Climate-

friendly

mining

SCR

technology:

Zero

emissions*

Energy

efficiency

in our

production

Tapping

regenerative

energies

Full power for

the solar

industry

* Technologies supplied to the automotive industry

20

Continental Strategy – Megatrend Safety

Initiatives in EU, USA and Japan – Towards Safer Mobility

Electronic stability control (ESC)

mandatory by •November 2011 for all new types of

passenger cars •November 2014 for all new passenger

cars1

Tire pressure monitoring system (TPMS)

mandatory by •November 2012 for all new types of

passenger cars •November 2014 for all new passenger

cars1

Advanced emergency braking system

and lane departure warning mandatory by •November 2013 for all new types of heavy

commercial vehicles and buses •November 2015 for all new heavy

commercial vehicles and buses2

Brake assist system mandatory for all new

passenger cars by November 20113

Framework to be established for the

deployment of intelligent transportation

systems4

EU

Electronic stability control (ESC)

mandatory by 2011 for all new light

vehicles5

Tire pressure monitoring system (TPMS)

mandatory for all new light vehicles since

September 20076

USA

Electronic stability control (ESC)

mandatory by

•October 2012 for all new types of

passenger cars

•October 2014 for all new passenger cars7

Advanced emergency braking system

and lane departure warning mandatory by

•November 2013 for all new types of heavy

commercial vehicles and buses

•November 2015 for all new heavy

commercial vehicles and buses

Japan

1) Regulation (EC) No. 661/2009

2) Regulation (EC) No. 661/2009

3) Regulation (EC) No. 78/2009; refers to passenger cars for maximum 8 passengers plus driver

4) Directive 2010/40/EU of the European Parliament and of the Council of July 2010

5) Federal Motor Vehicle Safety Standard No. 126 of the National Highway Traffic Safety Administration (NHTSA);

refers to vehicles with a gross vehicle weight of ≤4.536 t

6) Federal Motor Vehicle Safety Standard No. 138 of the National Highway Traffic Safety Administration (NHTSA);

refers to vehicles with a gross vehicle weight of ≤4.536 t

7) Source: Ministry of Land, Infrastructure, Transport and Tourism (MLIT) in Japan

Emerging markets likely to follow EU/USA on ESC regulation

Page 11

Fact Book 2010 |

© Continental AG

11

21

75,426

70,731

65,44163,90363,155

59,40960,26758,982

57,69156,427

54,30253,342

50,351

47,29045,346

43,10442,500

38,900

34,500

54,302

51,285

48,268

45,252

42,235

39,218

36,201

33,185

30,168

27,151

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EU road fatalities

EU fatalities EU target to halve the number of fatalities by 2010

Continental Strategy – Megatrend Safety

Development of Road Safety in Europe

Source: CARE (EU road accident database)

22

Continental Strategy – Megatrend Safety

ContiGuard®: 5 Cornerstones of Comprehensive Vehicle Safety

Active Safety Safety Telematics

Passive Safety

Sensor fusion (beam/camera)

Short range Lidar

Mid range radar 24 GHz

Long range radar 77GHz

Camera

Telematics control unit

E-Horizon

Car-to-X Communication

Electric power steering

Active rear axle kinematics

Chassis & safety controller

Electronic air suspension

Electronic stability control

Sensors

AFFP®

Accelarator

Force

Feedback

Pedal

Airbag control unit

Crash impact sound sensing

Pressure and acceleration satellites

Occupant classification systems

In crash

Pre crash Post crash

Traffic hazard

Vehicle Surrounding Sensors

HMI

Page 12

Fact Book 2010 |

© Continental AG

12

23

Continental Strategy – Megatrend Safety

Winter Tire Regulation1

Austria

Estonia

Finland

Germany

Europe: Winter tires mandatory

Latvia

Lithuania

Romania

Sweden

Slovakia

Slovenia

November 1 to April 15 when winter weather conditions apply

December 1 to end of February

December 1 to end of February

December 1 to end of February

November 1 to April 1

December 1 to March 31

Mandatory when winter weather conditions apply

November 1 to March 31

November 15 to March 15 when winter weather conditions

apply (winter tires or radial tires with min. tread depth of 3 mm)

The snowflake symbol: This symbol can be displayed on a tire if it tests seven percent better than a reference standard tire with

M+S² marking when ABS-braking on snow.

November 15 to March 31 when roads are snowy/icy

Norway

Mandatory when winter weather conditions apply

Europe: Winter tires partly mandatory

Czech Republic

November 1 to March 31 on certain motorways

France

Mandatory on certain roads – marked with signs

Italy

Mandatory on certain roads – marked with signs

Switzerland

Driver may be held liable if they cause an accident with

summer tires mounted when winter weather conditions apply

Canada: Winter tires partly mandatory

1) Source: Continental AG and websites of country ministries and automobile associations 2) Mud + snow

Mandatory in Québec December 15 to March 15;

mandatory on certain roads in the mountains of Canada when winter weather conditions applyCanada

24

Continental Strategy – Megatrends Safety & Environment

Initiatives in EU, USA and Japan on Labeling of Tires1

EU² USA³ Japan⁴

Fuel

efficiency

Noise

performance

Wet

grip

1) Similar initiative present in South Korea

2) Regulation (EC) No 1222/2009

Starting November 2012, passenger and

van tires must be classified and labelled for

fuel efficiency, wet grip and noise

performance (external rolling noise)

EU member states are responsible for the

market surveillance and specification of

penalties for non-compliance and can

provide incentives for tires of class C or

better (wet grip and fuel efficiency)

EU Commission must review this

regulation within five years

The NHTSA** Tire Fuel Efficiency

Consumer Information Program proposes

to inform consumers about the effect of

tires on fuel efficiency, safety, and

durability

The program aims to implement a national

tire fuel efficiency rating system for

replacement tires, with the information

provided to consumers at the point of sale

and online

Following the establishment of a council by

the Japanese government to promote fuel

efficient tires in 2008, the Japan

Automobile Tyre Manufacturers

Association (JATMA) introduced a

voluntary tire labelling system in 2010.

The labelling applies to replacement

summer tires for passenger cars and has

information on rolling resistance and wet

grip performance

Tires with a grading of A and above for

rolling resistance performance are defined

as “fuel efficient tires” and are marked with

an additional symbol:

Rolling

resistance

Wet grip

The tire rating label proposed by NHTSA**

3) Source: National Highway Traffic Safety

Administration (NHTSA)

4) Source: Japan Automobile Tyre Manufacturers

Association

Page 13

Fact Book 2010 |

© Continental AG

13

25

Continental Strategy – Megatrends Safety & Environment

Truck Tire Technology for Lowest Overall Driving Costs

*Compared to previous truck tire generation of the Continental brand

Savings thanks to low rolling resistance

Kilometers driven per year: 120,000

Diesel price (net):

€1.15 per literFuel savings* in total:

€2,584.1

In 2007 Continental started an initiative to launch new products

Latest truck tire generation of the Continental brand reduced rolling resistance significantly

Continental‟s focus is on overall driving costs

ContiCostCalculator (CCC) is a tool certified by DEKRA (a worldwide certification authority) to calculate the

overall operational costs for fleet customers

By taking into account mileage, retreads, fuel consumption and payload, the CCC tool shows that

Continental‟s new products lead to the lowest overall driving costs compared to competitors

26

Multimedia Devices

GPS / Galileo

Infrastructure

Other Cars

Infotainment

Continental Strategy – Megatrend Information

The Car will be Connected to its Environment!

Page 14

Fact Book 2010 |

© Continental AG

14

27

Continental Strategy – Market Trend Affordable Cars

Definition of “Affordable Cars”

Western Europe Eastern Europe China India

Dacia Logan €7,000

Chery QQ €3,500

Tata Nano €1,700

Maruti 800 €3,430

Low Cost Car

Mature Market

Low Cost Car

Emerging Market

€5,000

€10,000

€1,700

VW Fox €10,725

28

CAGR Product portfolio of

Low-cost OEM embedded navigation 68% Interior

Selective catalytic reduction 65% Powertrain/ContiTech*

Battery propulsion systems 44% Powertrain

Synchronous motors 31% Powertrain

Start stop systems 31% Powertrain*

Mobile phone navigation 29% Interior

Variable valve train 23%

eCall 16% Interior

Gasoline direct injection 16% Powertrain

Turbocharger 15% Powertrain

Blind spot detection 15% Chassis & Safety

Adaptive cruise control 14% Chassis & Safety

Lane departure warning 14% Chassis & Safety

Curtain airbag 14% Chassis & Safety*

Stolen vehicle tracking 14% Interior

Ambient lighting 11% Interior*

Electric power steering 10% Chassis & Safety

*Multifunctional switches 10% Interior*

Xenon headlamps 10% Chassis & Safety**

Park assist systems 8% Chassis & Safety

Electric stability control 7% Chassis & Safety

TPMS 6% Interior

OEM embedded navigation 5% Interior

Semi active damping 5% Chassis & Safety

Anti-lock braking systems 4% Chassis & SafetySource: Frost & Sullivan, December 2009, based on 2008 data

* no complete system but electronics or components

** washer systems

AHigh growth

CAGR 16% -70%

BMedium growth

CAGR 10% -15%

CLow growth

CAGR 3% -10%

CA

GR

Expected worldwide revenue development in %

(CAGR 2008-2015)

Continental Strategy50% of the Automotive Products are amongst the 25 Fastest Growing Technologies

Page 15

Fact Book 2010 |

© Continental AG

15

29

* Based on sales

**Based on units

Continental Strategy

Cost Consciousness – Production in Best-Cost Countries

27%

15%20%

60%69%

23%30%

13%

27%

68%

85%

26%32%

19%

32%

67%

100%

29%

Chassis & Safety * Powertrain * Interior * PLT ** CVT ** ContiTech *

Europe

57%

31%

65% 65%

23%

45%

62%

45%

72%68%

19%

51%

61%

45%

81%

65%

23%

57%

Chassis & Safety * Powertrain * Interior * PLT ** CVT ** ContiTech *

Rest of World

2008 2009 2010

30

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive GroupV.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

Page 16

Fact Book 2010 |

© Continental AG

16

31

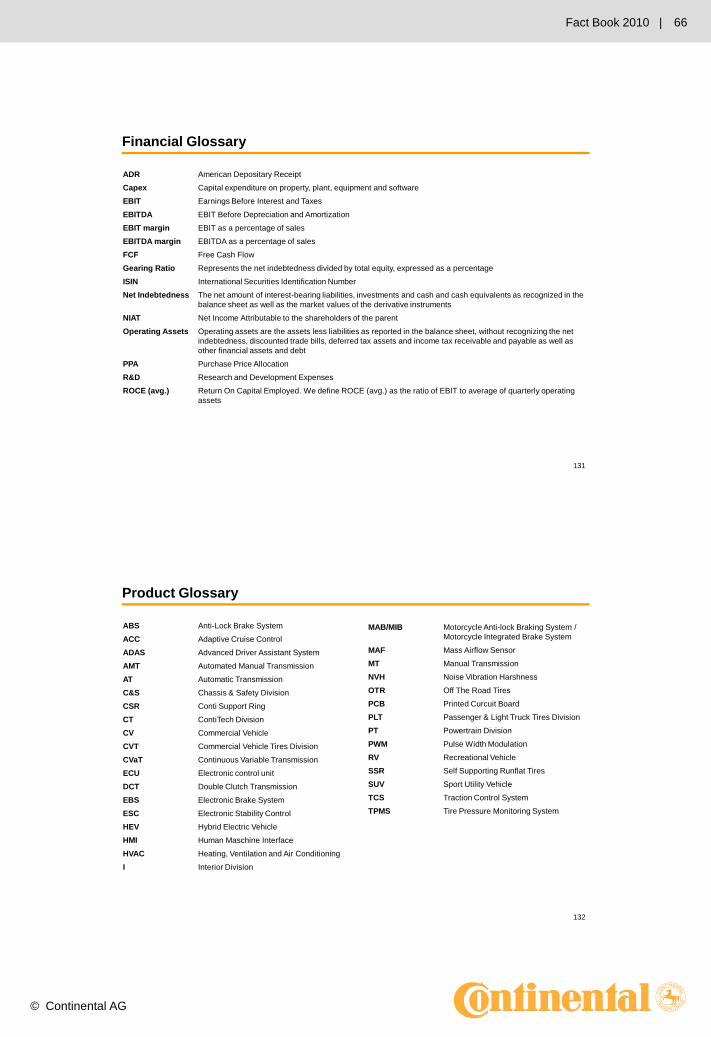

(in € million) 2008 2009 2010

Sales 24,238.7 20,095.7 26,046.9

EBITDA 2,771.4 1,591.2 3,587.6

EBIT -296.2 -1,040.4 1,935.2

EBIT adjusted 1 1,180.5 2,516.8

in % of sales 1 5.9 9.7

Net interest expense -706.7 -720.8 -697.2

Income tax expense -75.0 154.3 -592.1

Non-controlling interests -45.6 -42.3 -69.9

NIAT² -1,123.5 -1,649.2 576.0

Undiluted earnings per share (in €) -6.84 -9.76 2.88

Operating Assets (avg.) 19,117.0 16,024.1 15,580.0

RoCE (avg.) in % -1.5 -6.5 12.4

R & D expense 1,498.2 1,356.3 1,450.4

in % of sales 6.2 6.7 5.6

Capex³ 1,595.2 860.1 1,296.4

in % of sales 6.6 4.3 5.0

Depreciation & amortization 4 3,067.6 2,631.6 1,652.4

in % of sales 12.7 13.1 6.3

thereof impairment⁵ 1,341.4 993.0 57.7

Free cash flow 628.5 1,640.3 566.9

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Net income attributable to the shareholders of the parent

3) Capex including software

4) Excluding impairments on financial investments

5) 2008: including goodwill impairment of €1,230.0 mill.

2009: including goodwill impairment of €875.8 mill.

Continental Corporation

Consolidated Key Figures

31

32

6,639 6,615

5,892

5,093

4,3024,761

5,3375,696

5,997

6,658 6,4906,903

-37

285

419

513

605

701

485

726

Q1/08 Q2/08 Q3/08 Q4/08 Q1/09 Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10

Sales (in € million) adj. EBIT* (in € million)* Before amortization of intangibles from PPA, consolidation and special effects

Continental Corporation

Sales and Adjusted EBIT* by Quarter

Sales €24,239 mill. Sales €20,096 mill.

adj. EBIT* €1,181 mill.

Sales €26,047 mill.

adj. EBIT* €2,517 mill.

Page 17

Fact Book 2010 |

© Continental AG

17

33Note: Trailing ROCE is calculated as reported EBIT for the last twelve month (LTM) divided by average Operating Assets (OA)

Continental Corporation

Back to Value Creation1

9,4

94

19

,53

8

19

,60

7

19

,11

7

18

,58

6

17

,78

0

16

,70

0

16

,02

4

15

,50

8

15

,35

3

15

,40

5

8.7% 8.6%7.2%

-1.5%-4.9%

-7.5%

-14.4%

-6.5%

-2.5%

0.6%

8.9%

12.4%

19.5%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q4

2008 2009 2010 2010

trailing OA (in € million) Goodwill (in € million) trailing ROCE (in %)

15,58015,580

34

1) Amounts shown may contain rounding differences

2) Adjusted EBITDA before special effects excluding impairments

3) Includes change in inventory, trade receivables, trade payables and discounted notes

4) Includes dividends received, at-equity share in earnings of associates and income from other investments incl. impairments, gains and losses from disposals, other non-

cash items as well as changes in pension and post-employment provisions (including effects from transactions regarding contractual trust arrangements (CTA) in 2006

and 2009) and in other assets and liabilities

5) Adj. EBITDA to net cash interest paid

Continental Corporation

Key Historical Financials and Credit Metrics

(in € million )1 2006 2007 2008 2009 2010

Cash flow statement

Adjusted EBITDA2 2,339 2,568 3,001 2,354 3,662

Reported EBITDA 2,302 2,491 2,771 1,591 3,588

Net cash interest paid (78) (88) (519) (727) (703)

Tax paid (452) (484) (282) (205) (493)

Change in net working capital3 (184) (83) 275 595 (497)

Other 4 (765) 78 (360) 1,173 (46)

Cash flow provided by operating activites 823 1,914 1,885 2,427 1,849

Cash flow used for investing activities (1,464) (12,539) (1,256) (787) (1,282)

- thereof capex for PPE and intangibles (806) (904) (1,621) (911) (1,324)

Cash flow before financing actitivies (641) (10,626) 629 1,640 567

Balance sheet

Cash and cash equivalents 571 2,199 1,569 1,713 1,471

Derivative instruments and interest-bearing investments 33 71 64 104 202

Total indebtedness 1,785 13,127 12,117 10,713 8,991

Net indebtedness 1,181 10,856 10,484 8,896 7,317

Credit ratios

Net indebtedness / adj. EBITDA2 0.5x 4.2x 3.5x 3.8x 2.0x

Net cash interest paid coverage (ratio)5 30.1x 29.2x 5.8x 3.2x 5.2x

Page 18

Fact Book 2010 |

© Continental AG

18

35

Continental Corporation

Development of Net Indebtedness and Gearing Ratio

618 518 525 33 30 28 20 7 0.4 0.1 0.1 14 0.1 1 0.2 7

2,601

1,899

1,169881 493

1,181

10

,85

6 10

,48

4

11

,04

2

9,7

47

9,4

65

8,8

96

8,2

32

8,0

17

8,0

92

7,3

17

168%

111%

59%

30%13%

25%

158%

190%

210%186%

226%219%

145%133%138%

118%

YE YE YE YE YE YE YE YE Q1 H1 9M YE Q1 H1 9M YE

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Net indebtedness (in € million)

Off balance sheet debt (in € million)

Gearing Ratio (in %)

36

8,896 0

1,324611

443 564

1,652

684

1,056

7,317

Ne

t de

bt

(FY

20

09

)

Div

ide

nd

20

09

Ca

pe

x*

Ch

g. i

n

rece

iva

ble

s

Ch

g. i

nin

ve

nto

rie

s

Ch

g. i

np

aya

ble

s

De

pre

cia

tion

&

am

ort

iza

tio

n

Oth

er C

F

Ca

pita

lin

cre

ase

Ne

t de

bt

(FY

20

10

)Continental Corporation

Net Indebtedness Walk-down

€490 mill. burden from

change in working capital219%

118%

(in € million)

* According to CF statement including intangible assets

Page 19

Fact Book 2010 |

© Continental AG

19

37

VDO facility

(Tranche C)Aug 2012,

3,985

VDO facility

(Tranche D,Revolver)

Aug 2012, 303

Bond

Jul 2015 (8.5%), 750

Bond

Jan 2016 (6.5%), 625

Bond

Sept 2017 (7.5%), 1,000

Bond

Oct 2018 (7.125%), 625

Various other

bank lines, 857

Other

indebtedness, 846

Continental Corporation

Gross Indebtedness by Sources

Gross indebtedness

at Dec. 31, 2010,

of €8,991 mill.

(PY: €10,713 mill.)

Cash of €1,471 mill.

(PY: €1,713 mill.)

Net indebtedness

at Dec. 31, 2010,

of €7,317 mill.

(PY: €8,896 mill.)

Available and fully

committed credit lines

of €2,774 mill.

(PY: €2,196 mill.)

(in € million)VDO facility

Bonds

Various other bank lines

Other indebtedness

Note: bond values and the values for the VDO facilities are nominal values, all others book values

38

1,238.1

4,596.3

71.3 15.8

768.3

2,300.7

2011* 2012 2013 2014 2015 later

Continental Corporation

Maturity Profile at December 31, 2010

(in € million)

* Including maturities under the revolving credit facility currently drawn at nominal €303 million,

Page 20

Fact Book 2010 |

© Continental AG

20

39

100

100

87

25

18

54

13

75

82

46

Chassis & Safety(22% of total sales)

Powertrain(18% of total sales)

Interior(21% of total sales)

Passenger & Light Truck Tires

(22% of total sales)

Commercial Vehicle Tires(5% of total sales)

ContiTech(12% of total sales)

Continental Corporation

Sales OE/Non-OE

Non-OE28%

Chassis & Safety22%

Powertrain18%

Interior19%

PLT1

6%CVT²1%

ContiTech6%

28% of sales outside OE in 2010

1) PLT = Passenger and Light Truck Tires

2) CVT = Commercial Vehicle Tires

OE Non-OE

40

Continental Corporation

Purchasing – Production Materials 2010

Oil Based Chemicals1

12%

Electronics21%

E-Mechanics2

17%

Mechanics3

25%

Others4

19%

NaturalRubber

6%

Total production material purchased in 2010

€12.9 bn (74% of total purchased volume)

Purchasing Contracts

We aim for long-term contracts with our

strategic suppliers.

The purchase of oil derivatives for

chemical products cause a time

difference until realization in P&L of 2-6

months from spot price.

Main sources for natural rubber are

Thailand, Malaysia and Indonesia.

Continental has a wide range of

worldwide sources for production

materials.

1) E.g. synthetic rubber, carbon black

2) E.g. printed circuit boards, connectors, motors

3) E.g. stamping parts, turn parts, castings

4) E.g. textiles, plastics, brake pads

Page 21

Fact Book 2010 |

© Continental AG

21

41

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive GroupV.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

42

Market Data

Increasing Installation Rates of Electronic Brake Systems

Source: Continental estimates

ABS/TCS ESC Total EBS

0%

20%

40%

60%

80%

100%

Europe

North America

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Japan

2008 2009 2010 2011 2012 2013 2014 2015

China

Page 22

Fact Book 2010 |

© Continental AG

22

43

0%

20%

40%

60%

80%

100%Europe

Market Data

Installation Rates of Fuel Injection Systems*

Source: Continental estimates

*Based on production of diesel and gasoline engines for passenger cars & light vehicles

Gasoline direct injection Gasoline port fuel injection Diesel injection

2008 2009 2010 2011 2012 2013 2014 2015

China

North America

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Japan

44

Market Data Increasing Installation Rates of Double Clutch Transmission*

Source: Continental estimates

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2008 2009 2010 2011 2012 2013 2014 2015

Europe North America

Japan China

Double Clutch Transmission

Automated Manual Transmission

Continous Variable Transmission

Automatic Transmission

Manual Transmission

* Based on production of gearboxes for passenger cars and light vehicles

Page 23

Fact Book 2010 |

© Continental AG

23

45

0%

10%

20%

30%

40%

2008 2009 2010 2011 2012 2013 2014 2015

Market Data

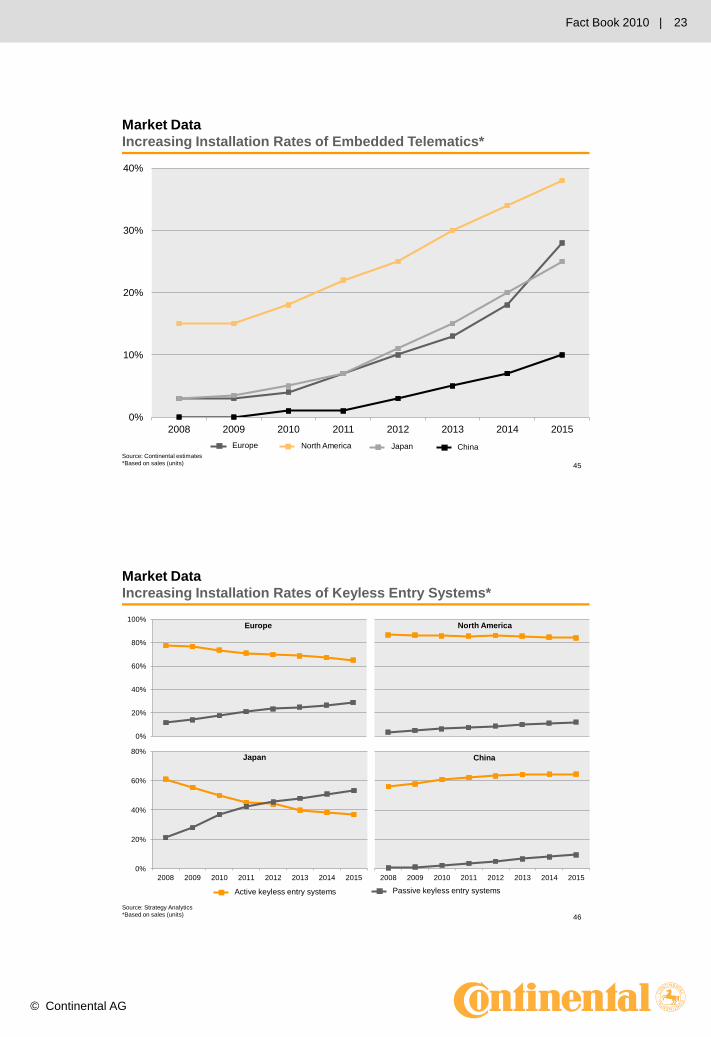

Increasing Installation Rates of Embedded Telematics*

Source: Continental estimates

*Based on sales (units)

JapanEurope North America China

46

Market Data

Increasing Installation Rates of Keyless Entry Systems*

Source: Strategy Analytics

*Based on sales (units)

0%

20%

40%

60%

80%

100%Europe North America

0%

20%

40%

60%

80%

2008 2009 2010 2011 2012 2013 2014 2015

Japan

2008 2009 2010 2011 2012 2013 2014 2015

China

Active keyless entry systems Passive keyless entry systems

Page 24

Fact Book 2010 |

© Continental AG

24

47

Market Data

Increasing Installation Rates of Multimedia Systems*

Source: Continental estimates

* Navigation stand-alone system and navigation systems with enriched multimedia functions

Radio Multimedia

0%

20%

40%

60%

80%

100%Europe

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Japan

North America

2008 2009 2010 2011 2012 2013 2014 2015

China

48

Source: Continental estimates

*Contains: adaptive cruise control, collision mitigation, lane departure warning, blind spot detection, intelligent lighting, night vision, traffic sign recognition

Market DataIncreasing Installation Rates of Advanced Driver Assistance Systems*

0%

5%

10%

15%

20%

25%

2008 2009 2010 2011 2012 2013 2014 2015

Europe NAFTA Japan

Page 25

Fact Book 2010 |

© Continental AG

25

49

Market Data Production of Light Vehicles 2009 - 2012

Source: CSM

* Estimates for passenger cars and light trucks < 6 tons (including vans)

2009 2010* 2011* 2012*

Americas 12.3 16.0 17.3 18.5

NAFTA 8.6 11.9 12.9 13.9

South America 3.7 4.1 4.3 4.6

Europe 16.3 18.6 18.7 19.6

Western Europe 11.8 13.0 13.0 13.4

Eastern Europe 4.5 5.6 5.7 6.3

Asia 27.8 35.1 37.3 40.6

Africa & Middle East 1.8 2.1 2.2 2.4

Total 58.2 71.8 75.5 81.2

(in million units)

50

Source: Global Insight

* Estimates for trucks > 6 tons

Market Data

Production of Heavy Vehicles 2009 - 2012

2009 2010* 2011* 2012*

Americas 394 501 576 713

NAFTA 217 254 328 446

South America 177 247 248 267

Europe 270 395 550 707

Western Europe 205 283 402 514

Eastern Europe 65 112 148 193

Asia 1,554 2,342 2,332 2,485

Total 2,267 3,238 3,459 3,905

(in thousand units)

Page 26

Fact Book 2010 |

© Continental AG

26

51

Market Data

World Passenger Light Vehicle Tire Sales Forecast 2009 - 2012

Source: LMC World Tyre Forecast Service 2010

* Estimates for OE and replacement

(in million units) 2009 2010* 2011* 2012*

Americas 350 380 405 429

NAFTA 283 306 326 346

South America 67 73 78 83

Europe 341 365 377 394

Western Europe 259 274 280 287

Central Europe 35 36 36 40

Eastern Europe 46 55 61 67

Asia 358 410 451 501

Oceania 20 21 22 23

Africa 32 34 36 38

Middle East & Turkey 62 69 75 81

Total 1,163 1,279 1,366 1,466

52

Source: LMC World Tyre Forecast Service 2010

* Estimates for OE and replacement

Market DataMedium and Heavy Truck Tire Sales 2009 - 2012

2009 2010* 2011* 2012*

Americas 31 34 38 40

NAFTA 19 21 24 25

South America 12 13 14 15

Europe 19 22 25 28

Western Europe 9 11 12 14

Central Europe 2 2 2 3

Eastern Europe 7 9 10 11

Asia 74 82 87 92

Oceania 2 2 2 2

Africa 5 6 6 7

Middle East & Turkey 10 11 12 12

Total 140 157 169 182

(in million units)

Page 27

Fact Book 2010 |

© Continental AG

27

53

Source: LMC World Tyre Forecast Service 2010

* Estimates

Market Data

Replacement Passenger, Light Truck and 4x4 Tires 2009 - 2012

2009 2010* 2011* 2012*

Americas 292 307 321 335

NAFTA 243 255 266 276

South America 48 52 55 58

Europe 262 280 293 306

Western Europe 200 212 219 226

Eastern/Central Europe 62 68 74 80

Asia 215 239 268 299

Oceania 18 19 20 21

Africa 30 31 32 34

Middle East & Turkey 50 56 61 66

Total 866 933 994 1,060

(in million units)

54

Market Data

Replacement Truck Tires 2009 - 2012

Source: LMC World Tyre Forecast Service 2010 and Continental estimates

* Estimates

2009 2010* 2011* 2012*

Americas 27 30 31 33

NAFTA 16 18 19 20

South America 11 12 13 14

Europe 15 18 19 21

Western Europe 7 8 9 9

Eastern/Central Europe 8 10 11 12

Asia 60 66 71 75

Oceania 2 2 2 2

Africa 5 5 6 6

Middle East & Turkey 9 10 11 12

Total 117 131 140 149

(in million units)

Page 28

Fact Book 2010 |

© Continental AG

28

55

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive GroupV.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

56

Automotive Group

Key Figures

(in € million) 2008 2009 2010

Sales 14,900.0 12,042.4 15,917.0

EBITDA 1,428.8 608.9 1,779.1

in % of sales 9.6 5.1 11.2

EBIT -1,205.8 -1,561.6 567.9

in % of sales -8.1 -13.0 3.6

EBIT adjusted 1 203.7 1,068.6

in % of sales 1 1.7 6.7

Operating Assets (avg.) 14,734.3 12,015.9 11,512.0

RoCE (avg.) in % -8.2 -13.0 4.9

R & D expense 1,276.2 1,144.3 1,227.1

in % of sales 8.6 9.5 7.7

Capex 2 1,095.6 538.1 739.8

in % of sales 7.4 4.5 4.6

Depreciation & amortization 3 2,634.6 2,170.5 1,211.2

in % of sales 17.7 18.0 7.6

thereof impairment 4 1,327.5 949.0 35.6

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Capex including software

3) Excluding impairments on financial investments

4) 2008: including goodwill impairment of €1,230.0 mill.

2009: including goodwill impairment of €875.8 mill.

Page 29

Fact Book 2010 |

© Continental AG

29

57

5,775

4,731

5,518 107 15,917

C&S PT I cons. AutomotiveGroup

organic growth (%)

26.7%

36.2%

22.4% 28.0%

Automotive Group

Sales and Adjusted EBIT* by Division

Automotive Group Sales (in € million) Automotive Group adj. EBIT* (in € million)

-

* Before amortization of intangibles from PPA, consolidation and special effects

630

26

412 0 1,069

C&S PT I cons. AutomotiveGroup

adj. EBIT* margin (%)

10.9%

0.6%

7.5% 6.7%

58

Automotive Group

Sales by Region

Germany29%

Europe (excluding Germany)

26%

Asia21%

NAFTA20%

Other countries

4%

Sales in 2010: €15.9 bn

(2009: 5%)(2009: 18%)

(2009: 28%)

(2009: 31%)

(2009: 18%)

Page 30

Fact Book 2010 |

© Continental AG

30

59

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive Group – 1. Chassis & Safety Division V.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

60

Chassis & Safety

Business Unit Structure

Hydraulic electronic

control units (HECU)

ABS

ESC

Software functions

Adaptive cruise control

Regenerative brake

system

Active front steering

Hill start assist,

hill descent control

Deflation detection

system

Hydraulic brake assist

Trailer stability assist

Calipers and discs

Drum brakes

Brake hoses

Boosters

Tandem master cylinders

Electric parking brakes

Pedal modules

Brake pressure regulators

Electric vacuum pump

Steering angle and

torque sensors

Wheel speed sensors

Engine/transmission

speed and position

sensors

Chassis sensors

Acceleration sensor

Height sensor

Pedal angle sensor

Pedal travel sensor

Sensor clusters

Inertial measurement

unit (IMU)

Airbag control units

Crash sensors

Occupant classification

systems (OCS)

Driver assistance

systems

Radar

Lidar

Camera

Chassis electronics

Electronic components

Steering systems

Suspension systems

Washer systems

Electronic Brake Systems Hydraulic Brake Systems Sensorics Passive Safety & ADAS Chassis Components

Page 31

Fact Book 2010 |

© Continental AG

31

61

India▐ Bangalore▐ Gurgaon

(New Delhi)▐ Manesar

Brazil▐ Salto▐ Varzea Paulista

China▐ Shanghai▐ Changchun▐ Changshu▐ Heihe▐ Lian Yun Gang

Chassis & Safety

Locations Worldwide

Mexico▐ Ayala Morelos (Cuautla)▐ Guadalajara▐ Las Colinas▐ Silao

USA▐ Auburn Hills▐ Brimley▐ Culpeper▐ Henderson▐ Morganton

Malaysia▐ Penang

Japan▐ Asahi▐ Hamakita▐ Hiroshima▐ Monbetsu▐ Yokohama

South Korea▐ Cheongwon▐ Icheon

Philippines▐ Calamba▐ Manila

▐ Korbach

▐ Lindau

▐ Nuremberg

▐ Regensburg

▐ Rheinböllen

▐ Schwalbach

Europe France▐ Boussens

▐ Toulouse

Hungary▐ Budapest

▐ Veszprém

Italy▐ Cairo Montenotte

Belgium▐ Mechelen

Czech Republic▐ Adrspach

▐ Frenstat

▐ Jicin

Portugal▐ Palmela

Romania▐ Iasi

▐ Sibiu

▐ Timişoara

Slovakia▐ Zvolen

Spain▐ Bergara

Sweden▐ Arvidsjaur

UK▐ Ebbw Vale

▐ Production

Germany▐ Alzenau

▐ Bebra

▐ Frankfurt

▐ Gifhorn

▐ Hanover

▐ Ingolstadt

▐ Karben

▐ Joint Ventures < 50%

57 sites for production and R&D in 19 countries. Divisional headquarters in Frankfurt/Main, Germany.

62

Chassis & Safety

Key Figures

(in € million) 2008 2009 2010

Sales 5,134.0 4,373.6 5,775.4

EBITDA 789.9 601.6 891.7

in % of sales 15.4 13.8 15.4

EBIT 303.1 -102.5 569.0

in % of sales 5.9 -2.3 9.9

EBIT adjusted 1 352.8 630.2

in % of sales 1 8.1 10.9

Operating Assets (avg.) 4,494.4 4,034.0 3,997.0

RoCE (avg.) in % 6.7 -2.5 14.2

R & D expense 423.6 380.8 422.3

in % of sales 8.3 8.7 7.3

Capex 2 336.0 159.5 247.1

in % of sales 6.5 3.6 4.3

Depreciation & amortization 3 486.8 704.1 322.7

in % of sales 9.5 16.1 5.6

thereof impairment 4 150.6 370.4 3.8

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Capex including software

3) Excluding impairments on financial investments

4) 2008: including goodwill impairment of €145.2 mill.

2009: including goodwill impairment of €367.0 mill.

Page 32

Fact Book 2010 |

© Continental AG

32

63

Chassis & Safety

Sales by Region

Germany30%

Europe (excluding Germany)

24%

NAFTA19%

Asia23%

Other countries

4%(2009: 20%)

(2009: 16%)

(2009: 26%)

Sales in 2010: €5.8 bn

(2009: 3%)

(2009: 35%)

64

Chassis & Safety

Market Position for Electronic Brake Systems 2010

Continental33%

Continental25%

Continental26%

Continental36%

Continental42%

Bosch30%

Bosch19%

Bosch49%

Bosch31%

Bosch42%

8%

3%

14%

13%

10%

Advics10%

Advics20%

Advics9%

5%

9%

5%

6%

9%

7%

4%

7%

5%

Others11%

2%

4%

Others6%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

TRW Mando Nissin Kogyo Mobis

Source: Continental estimates

Page 33

Fact Book 2010 |

© Continental AG

33

65

Chassis & Safety

Market Position for Foundation Brake Systems 2010

Continental21%

Continental11%

Continental56%

Continental15%

Continental34%

Bosch9%

5%

Bosch9%

Bosch15%

Bosch12%

TRW25%

TRW12%

TRW32%

TRW20%

TRW45%

Advics10%

Advics17%

Advics12%

Mando6%

Mando10%

Mando6%

9%

12%

16%

Others20%

Others33%

3%

Others16%

Others9%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Akebono

Source: Continental estimates

66

Chassis & Safety

Market Position for Actuation 2010

Continental25%

7%

Continental52%

Continental30%

Continental45%

Bosch20%

Bosch20%

Bosch22%

Bosch22%

Bosch20%

TRW13%

TRW5%

TRW24%

TRW14%

TRW22%

Advics10%

Advics16%

Advics11%

6%

13%

5%

5%

9%

4%

3%

5%

7%

3%

7%

Others15%

Others18%

2%

Others7%

Others13%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Mando Akebono KDAC SABS

Source: Continental estimates

Page 34

Fact Book 2010 |

© Continental AG

34

67

Chassis & Safety

Market Position for Airbag Electronics 2010

Continental27%

Continental21%

Continental43%

Continental22%

Continental38%

Bosch19%

Bosch16%

4%

Bosch12%

Bosch28%

TRW15%

TRW11%

TRW16%

TRW24%

TRW14%

Autoliv16%

Autoliv10%

Autoliv10%

Autoliv24%

Autoliv17%

12%

26%

6%

7%

8%

3%

7%

14%

Others8%

Others9%

Others6%

4%

3%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Denso Delphi Keihin

Source: Continental estimates

68

Continental20%

6%

Continental10%

Continental39%

10%

Bosch23%

7%

7%

12%

6%

Denso18%

Denso51%

Denso9%

7%

4%

14%

6%

Gentex6%

Gentex8%

Gentex10%

5%

3%

9%

6%

17%

4%

4%

12%

3%

6%

23%

3%

Others11%

Others17%

4%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

North America

Europe

Autoliv Delphi Hella Hitachi Honda Elesys Valeo

Chassis & Safety

Market Position for Advanced Driver Assistance Systems 2010

Source: Continental estimates

Page 35

Fact Book 2010 |

© Continental AG

35

69

ABS/TCS

ESC

0

5

10

15

20

25

Source: Continental estimates

Chassis & Safety Growing Sales Volume for Electronic Brake Systems

Europe

BMW 1 Series / 3 Series

Landrover Freelander

Mercedes C Class / S Class

Ford Focus / Fiesta

Opel Astra

VW Golf

Peugeot 207

Seat Altea

Volvo S80 / V70

NAFTA

Dodge Caravan / Voyager

Ford Explorer / Escape

Jeep Wrangler

GM Cruze / Equinox

Nissan Frontier

Toyota Tundra

VW Jetta / New Beetle

BMW X3

Asia

Daewoo Windstorm

Honda Accord

Mazda Axela

Suzuki Wagon R

Mitsubishi Lancer / Outlander

Subaru Legacy

Model Selection

(in million units)

70

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive Group – 2. Powertrain DivisionV.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

Page 36

Fact Book 2010 |

© Continental AG

36

71

Powertrain

Business Unit Structure

Engine management

systems and fuel

components for

Diesel piezo common

rail injection systems

Gasoline piezo direct

injection

Gasoline solenoid

direct injection

Gasoline port injection

Liquefied petroleum

gas (LPG) and

compressed natural

gas (CNG)

Aftertreatment

Engine management

systems /aftertreatment

products for commercial

vehicle applications

Turbocharger

Engine Systems Transmission Hybrid Electric Vehicle Sensors & Actuators Fuel Supply

Control units for

Automatic

transmission

Double clutch

transmission

Automated manual

transmission

Continuously variable

transmission

Control units for four-

and all wheel drive

applications

Transfer cases

Differentials

Limited slip coupling

Clutch systems

Actuators for powertrain

applications

Components and

modules for emission

management

Sensors for powertrain

applications

NOx, MAF,

transmission sensor

modules, position

sensors

Pressure,

temperature, knock,

cylinder pressure

Flexible fuel, oil

quality, oil level

Door handle sensors

Systems/ components

for hybrid and electric

vehicle applications

Power electronics

Electric motors

Battery systems

Energy management

Power net systems

Fuel supply units

Fuel level sensors

Fuel pumps

Control electronics for

fuel pumps

72

India▐ Bangalore▐ Pune▐ Manesar

Brazil▐ Guarulhos▐ Salto

China▐ Shanghai▐ Changchun▐ Tianjin▐ Wuhu

Powertrain

Locations Worldwide

Mexico▐ Ayala Morelos (Cuautla)▐ Guadalajara▐ Juarez

USA▐ Auburn Hills▐ Dearborn▐ Deer Park▐ Newport News▐ Seguin

Malaysia▐ Penang

Japan▐ Yokohama

South Korea▐ Cheongwon▐ Icheon

Australia▐ Bundoora

▐ Limbach-Oberfrohna/Stollberg

▐ Lohmar

▐ Nuremberg

▐ Regensburg

▐ Roding

▐ Schwalbach

Europe France▐ Boussens

▐ Foix

▐ Toulouse

Hungary▐ Budapest

Italy▐ Pisa

Czech Republic▐ Adrspach

▐ Brandys

▐ Frenstat

▐ Trutnov

Romania▐ Iasi

▐ Sibiu

▐ Timişoara

▐ Production, R&D

Germany▐ Bebra

▐ Berlin

▐ Dortmund

▐ Gifhorn

▐ Grünstadt

▐ Karben

▐ Joint Ventures < 50%

Philippines▐ Calamba

Canada▐ Chatham

Thailand▐ Amata City

Russia▐ Kaluga

60 sites for production and R&D in 22 countries. Divisional headquarters in Regensburg, Germany.

Page 37

Fact Book 2010 |

© Continental AG

37

73

Powertrain

Key Figures

(in € million) 2008 2009 2010

Sales 4,040.0 3,399.2 4,730.8

EBITDA 81.6 -13.3 268.2

in % of sales 2.0 -0.4 5.7

EBIT -1,046.2 -943.2 -198.1

in % of sales -25.9 -27.7 -4.2

EBIT adjusted 1 -206.3 26.0

in % of sales 1 -6.2 0.6

Operating Assets (avg.) 4,610.8 3,401.8 3,112.2

RoCE (avg.) in % -22.7 -27.7 -6.4

R & D expense 420.1 328.8 396.9

in % of sales 10.4 9.7 8.4

Capex 2 494.4 247.2 301.5

in % of sales 12.2 7.3 6.4

Depreciation & amortization 3 1,127.8 929.9 466.3

in % of sales 27.9 27.4 9.9

thereof impairment 4 653.3 488.0 36.6

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Capex including software

3) Excluding impairments on financial investments

4) 2008: including goodwill impairment of €609.6 mill.

2009: including goodwill impairment of €447.4 mill.

74

Germany26%

Europe (excluding Germany)

31%

NAFTA20%

Asia22%

Other countries

1%

(2009: 30%)

Powertrain

Sales by Region

Sales in 2010: €4.7 bn

(2009: 1%)

(2009: 28%)

(2009: 20%)

(2009: 21%)

Page 38

Fact Book 2010 |

© Continental AG

38

75Source: Continental estimates

Powertrain

Market Position for Diesel Injection Systems* 2010

* For passenger cars & light trucks ** Japan, South Korea, China, India, Thailand

Continental16%

2%

Continental20%

Bosch55%

Bosch44%

Bosch58%

12%

33%

5%

Delphi14%

Delphi18%

Delphi14%

3%

3%

3%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific**

Europe

Denso Others

76

Powertrain

Market Position for Gasoline Injection Systems* 2010

Source: Continental estimates * For passenger cars & light trucks ** Japan, South Korea, China, India, Thailand

Continental22%

Continental13%

4%

Continental27%

Continental33%

Bosch29%

Bosch26%

Bosch23%

Bosch16%

Bosch42%

17%

29%

18%

3%

5%

5%

20%

10%

6%

7%

14%

Hitachi10%

Hitachi9%

Hitachi9%

Hitachi9%

4%

34%

7%

Others7%

Others11%

Others19%

6%

Others6%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific**

South America

North America

Europe

Denso Delphi Keihin Magneti Marelli

Page 39

Fact Book 2010 |

© Continental AG

39

77

Powertrain

Market Position for Transmission Control Units* 2010

Source: Continental estimates * For passenger cars & light trucks ** Japan, South Korea, China, India

Continental45%

Continental29%

Continental35%

Continental70%

Bosch19%

Bosch10%

Bosch34%

Bosch16%

4%

9%

3%

5%

Delphi16%

6%

11%

4%

8%

19%

3%

11%

17%

5%

11%

2%

5%

3%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific**

North America

Europe

Denso Delphi Keihin Hitachi Aisin Visteon Others

78

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive Group – 3. Interior Division V.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

Page 40

Fact Book 2010 |

© Continental AG

40

79

Interior

Business Unit Structure

Instrument clusters

Secondary displays

Head-up displays

Climate controls

Faceplates

Central input devices

Roof controls

Integrated centerstacks

Cockpit modules

Instrumentation & Driver HMI Infotainment & Connectivity Body & SecurityCommercial Vehicles & Aftermarket

Radios

Connected radio & entry

navigation

Multimedia systems

Embedded telematics

Device connectivity

Software & special solutions

Body control units

Exterior light control units

Power closures

Seat comfort systems

Battery & energy management

Access control systems

Tire information systems

Intelligent antenna modules

Tachographs, telematics &

services

Visual human machine

interface

Haptical human machine

interface

Connectivity solutions

Powertrain control

Transmission electronics

Chassis electronics

Body electronics

Wear parts, spare parts &

services for the independent

aftermarket

Original equipment services

80

Interior

Locations Worldwide

India▐ Bangalore▐ Chennai▐ Haryana▐ Manesar▐ Pune

Brazil▐ Barueri▐ Campinas ▐ Gravatai▐ Guarulhos

China▐ Hong Kong▐ Jinan▐ Shanghai▐ Changchun▐ Tianjin▐ Wuhu

Mexico▐ Ayala Morelos (Cuautla)

▐ Guadalajara▐ Nogales

USA▐ Allentown▐ Auburn Hills▐ Cedar Rapids▐ Deer Park▐ Elma▐ Huntsville▐ Seguin▐ Troy

Malaysia▐ Penang▐ Sha Alam

Japan▐ Yokohama

South Korea▐ Cheongwon-gun▐ Icheon-city▐ Seoul

Philippines▐ Manila

▐ Markdorf

▐ Nuremberg

▐ Regensburg

▐ Schwalbach am Taunus

▐ Villingen-Schwenningen

▐ Wetzlar

Europe France▐ Foix

▐ Guyancourt

▐ Hambach

▐ Rambouillet

▐ Toulouse

Hungary▐ Budapest

Austria▐ Vienna

Czech Rep.▐ Brandys

▐ Frenstat

Italy▐ Novate

Milanese

Netherlands▐ Eindhoven

Romania▐ Iasi

▐ Sibiu

▐ Timişoara

Spain▐ Alcobendas

▐ Rubi

Sweden▐ Arvidsjaur

Switzerland▐ Rüthi

UK▐ Birmingham

Germany▐ Babenhausen

▐ Eschborn

▐ Frankfurt a. M.

▐ Ingolstadt

▐ Karben

Costa Rica▐ Alajuela

▐ Manaus▐ Resende▐ Sao Bernardo

do Compo

Tunesia▐ Bizerte

▐ Singapore

Australia▐ Bundoora▐ Campbellfield

Thailand▐ Bangkok

Russia▐ Chistopol▐ Kaluga▐ Moscow

60 sites for production and R&D in 23 countries. Divisional headquarters in Regensburg, Germany.

Page 41

Fact Book 2010 |

© Continental AG

41

81

Interior

Key Figures

(in € million) 2008 2009 2010

Sales 5,856.7 4,362.7 5,518.1

EBITDA 557.3 20.4 619.1

in % of sales 9.5 0.5 11.2

EBIT -462.6 -516.0 197.0

in % of sales -7.9 -11.8 3.6

EBIT adjusted 1 57.0 412.4

in % of sales 1 1.3 7.5

Operating Assets (avg.) 5,629.1 4,580.1 4,402.8

RoCE (avg.) in % -8.2 -11.3 4.5

R & D expense 432.5 434.7 407.9

in % of sales 7.4 10.0 7.4

Capex 2 265.2 131.3 191.3

in % of sales 4.5 3.0 3.5

Depreciation & amortization 3 1,019.9 536.4 422.1

in % of sales 17.4 12.3 7.6

thereof impairment 4 523.6 90.6 -4.8

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Capex including software

3) Excluding impairments on financial investments

4) 2008: including goodwill impairment of €475.2 mill.

2009: including goodwill impairment of €61.4 mill.

82

Interior

Sales by Region

Sales in 2010: €5.5 bn

Germany31%

Europe (excluding Germany)

24%

NAFTA19%

Asia18%

Other countries

8%

(2009: 31%)

(2009: 7%) (2009: 14%)

(2009: 28%)

(2009: 20%)

Page 42

Fact Book 2010 |

© Continental AG

42

83

Interior

Market Position for Body & Security 2010

Source: Continental estimates

Continental21%

Continental14%

Continental17%

Continental22%

Continental27%

5%

3%

Bosch7%

Bosch5%

Bosch7%

10%

18%

4%

9%

3%

8%

5%

18%

9%

9%

6%

4%

12%

3%

10%

6%

5%

8%

7%

3%

5%

6%

4%

8%

4%

3%

6%

4%

3%

6%

3%

3%

5%

Others28%

Others31%

Others32%

Others33%

Others31%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Denso Delphi Hella Lear Valeo Omron Calsonic Kansei Sumitomo HACO

84

Interior

Market Position for Instrumentation & Driver HMI* 2010

Source: Continental estimates * Excluding cockpit modules

Continental19%

Continental13%

Continental29%

Continental14%

Continental25%

Denso12%

Denso19%

Denso13%

Denso16%

3%

JCI6%

JCI4%

JCI5%

JCI10%

3%

8%

3%

4%

4%

5%

16%

9%

6%

9%

3%

10%

3%

4%

4%

4%

6%

7%

5%

4%

5%

3%

Others41%

Others50%

Others25%

Others36%

Others35%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Delphi Calsonic Kansei Magneti Marelli Nippon Seiki Valeo Visteon Yazaki

Page 43

Fact Book 2010 |

© Continental AG

43

85

Interior

Market Position for Infotainment & Connectivity 2010

Source: Continental estimates

9%

2%

Continental16%

Continental12%

Continental17%

6%

Bosch9%

Bosch16%

7%

9%

9%

4%

4%

6%

9%

3%

8%

3%

6%

13%

10%

14%

6%

11%

5%

10%

3%

3%

23%

7%

5%

13%

6%

7%

11%

9%

Others34%

Others43%

Others55%

Others34%

Others23%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Denso Delphi Magneti Marelli Aisin Panasonic Harman Alpine Clarion

86Source: Continental estimates

Interior

Market Position for Commercial Vehicle* 2010

* Market shares for commercial vehicle business as described in BU structure excluding automotive aftermarket

Continental37%

Continental16%

Continental58%

Continental25%

Continental34%

4%

Bosch9%

10%

6%

Stoneridge26%

10%

4%

9%

4%

9%

4%

Yazaki7%

Yazaki25%

9%

3%

Hella9%

9%

Phoenix9%

3% 4% 3%

Others31%

Others49%

Others36%

Others27%

Others11%

0% 20% 40% 60% 80% 100%

World

Asia/Pacific

South America

North America

Europe

Bosch Stoneridge Wabco Actia Ametek Yazaki Hella Phoenix Calsonic Kansei Harbin DETC

Page 44

Fact Book 2010 |

© Continental AG

44

87

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive Group V.

Rubber GroupVI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

88

(€ million) 2008 2009 2010

Sales 9,353.9 8,068.3 10,152.5

EBITDA 1,415.9 1,114.5 1,851.5

in % of sales 15.1 13.8 18.2

EBIT 984.9 655.7 1,413.1

in % of sales 10.5 8.1 13.9

EBIT adjusted 1 1,038.5 1,513.4

in % of sales 1 12.9 15.0

Operating Assets (avg.) 4,369.5 3,989.8 4,112.1

RoCE (avg.) in % 22.5 16.4 34.4

R & D expense 222.0 212.0 223.3

in % of sales 2.4 2.6 2.2

Capex 2 499.1 321.7 555.8

in % of sales 5.3 4.0 5.5

Depreciation & amortization 3 431.0 458.8 438.4

in % of sales 4.6 5.7 4.3

thereof impairment 13.9 44.0 22.1

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Capex including software

3) Excluding impairments on financial investments

Rubber Group

Key Figures

Page 45

Fact Book 2010 |

© Continental AG

45

89

3,095

5,821

1,428

191

10,153

CT PLT CVT cons. Rubber Group

organic growth (%)

26.4%

18.2%

25.8%20.7%-

397

1,031 86

0

1,513

CT PLT CVT cons. Rubber Group

adj. EBIT* margin (%)

12.9%

17.9% 6.1%15.0%

Rubber Group

Sales and Adjusted EBIT* by Division

Rubber Group Sales (in € million) Rubber Group adj. EBIT* (in € million)

* Before amortization of intangibles from PPA, consolidation and special effects

90

Rubber Group Sales by Region

Germany25%

Europe (excluding Germany)

43%

NAFTA17%

Asia8%

Other countries

7%

Sales in 2010: €10.2 bn

(2009: 26%)

(2009: 5%)

(2009: 8%)

(2009: 17%)

(2009: 44%)

Page 46

Fact Book 2010 |

© Continental AG

46

91

Topics

A. Continental at a GlanceI.

B. Continental StrategyII.

C. Continental CorporationIII.

D. Market DataIV.

Automotive Group V.

Rubber Group – 1. Passenger and Light Truck Tires Division VI.

Corporate Social Responsibility at ContinentalVII.

Share & Bond InformationVIII.

GlossaryIX.

92

* Except NAFTA Region, Colombia, Peru

** Trademark rights for Malaysia, Singapore and Brunei

Passenger and Light Truck TiresBusiness Unit Structure

Tires for :

Compact, medium-size &

full-size cars

4x4 and SUVs

Vans, light trucks & RVs

Extended mobility systems:

SSR

CSR

ContiComfortKit

ContiMobilityKit

ContiSeal

NVH engineering services

Brands:

Tires for:

Compact, medium-size

and full-size cars

4x4 and SUVs

Vans, light trucks & RVs

High- and ultra-high-

performance tires

Brands:

Tires for:

Compact, medium-size

and full-size cars

4x4 and SUVs

Vans, light trucks & RVs

High- and ultra-high-

performance tires

Brands:

Tires for:

Compact, medium-size

and full-size cars

4x4 and SUVs

Vans, light trucks & RVs

High- and ultra-high-

performance tires

Brands:

Bicycle tires

High-performance

bicycle racing tires

Motorcycle and scooter

tires

High-performance

motorbike tires

Brands:

Original EquipmentReplacement Business

EMEA

Replacement Business

The Americas

Replacement Business

Asia-PacificTwo-Wheel Tires

*

**

**

Page 47

Fact Book 2010 |

© Continental AG

47

93

(in € million) 2008 2009 2010

Sales 5,100.3 4,696.4 5,820.8

EBITDA 873.5 793.1 1,241.0

in % of sales 17.1 16.9 21.3

EBIT 626.4 536.4 993.3

in % of sales 12.3 11.4 17.1

EBIT adjusted 1 774.4 1,030.5

in % of sales 1 16.5 17.9

Operating Assets (avg.) 2,488.1 2,348.4 2,422.9

RoCE (avg.) in % 25.2 22.8 41.0

R & D expense 119.5 113.5 120.8

in % of sales 2.3 2.4 2.1

Capex 2 292.7 198.3 404.3

in % of sales 5.7 4.2 6.9

Depreciation & amortization 3 247.1 256.7 247.7

in % of sales 4.8 5.5 4.3

thereof impairment 13.1 24.6 7.2

1) EBIT before amortization of intangibles from PPA, consolidation and special effects; sales before changes in the scope of consolidation

2) Capex including software

3) Excluding impairments on financial investments

Passenger and Light Truck Tires

Key Figures

94

Passenger and Light Truck Tires Sales by Region

Germany21%

Europe (excluding Germany)

49%

NAFTA19%

Asia5%

Other countries

6%

Sales in 2010: €5.8 bn

(2009: 21%)

(2009: 52%)

(2009: 5%)

(2009: 4%)(2009: 18%)

Page 48

Fact Book 2010 |

© Continental AG

48

95

6%

Continental21%

Michelin19%

Michelin19%

Goodyear/Sumitomo

20%

Goodyear/Sumitomo

18%

Bridgestone/Firestone

19%

Bridgestone/Firestone

12%

Pirelli7%

Cooper9%

Others27%

Others23%

0% 20% 40% 60% 80% 100%

North America

Europe

Source: Continental estimates

* OE & replacement

Passenger and Light Truck TiresMarket Share for Passenger and Light Truck Tires* 2010

96

* Until 2004 consolidated in CVT Division

** Since July 2009

(million units)

Passenger and Light Truck Tires

Worldwide Passenger and Light Truck Tire Production 2010

Mount Vernon

San Luis Potosí

Cuenca**

Camaçari

Port Elizabeth

Alor Star /

Petaling Jaya*

9

5

15

3

3

(US)

(MX)

(EC)

(BR)

(ZA)

(MY)

Page 49

Fact Book 2010 |

© Continental AG

49

97

Lousado

15

Sarreguemines

10

Aachen

9

Korbach

10

Passenger and Light Truck Tires

European Passenger & Light Truck Tire Production 2010

Otrokovice

21

Puchov

8

Timişoara

14

(million units)

(PT)

(DE)

(FR)

(RO)

(CZ)

(SK)

98

11%

21%

26%

28%

34%

36%

42%

60%

66%

94%

100%

100%

0% 20% 40% 60% 80% 100% 120%

Malaysia

Romania

Ecuador

Brazil

South Africa

Slovakia

Czech Republic

Mexico

Portugal

USA

France

Germany

Passenger and Light Truck Tires

Cost of Labor at Continental Manufacturing Sites*

* Based on average FX rates 2010

Page 50

Fact Book 2010 |

© Continental AG

50

99

Passenger and Light Truck Tires

Unit Sales 2005 - 2010

* From 2006 - 2007 Asia included in Europe

** North America; since 2007 including Latin America

80 83 84 8475

86

26 24 24 23

20

25

4

4

4

2005 2006 2007 2008 2009 2010

(in million units)

Europe (incl. ROW)* The Americas** Asia/Pacific