19

Factor Analysis Advanced Financial Accounting II Åbo Akademi School of Business

| Date post: | 06-Sep-2018 |

| Category: |

Documents |

| Upload: | truongtuyen |

| View: | 220 times |

| Download: | 0 times |

Factor Analysis

Advanced Financial Accounting II

Åbo Akademi School of Business

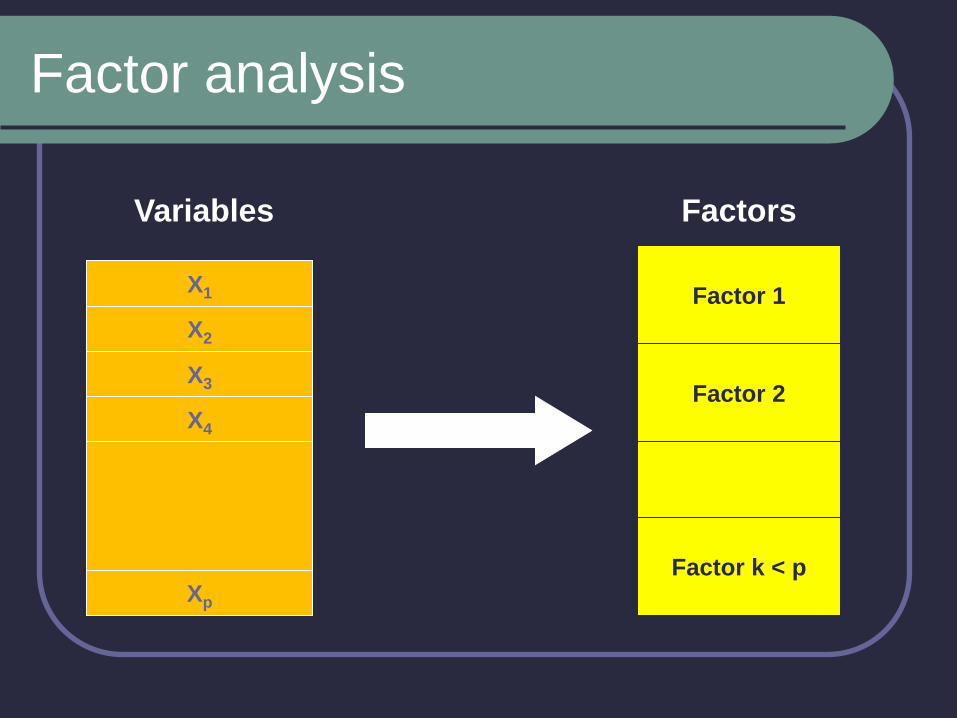

Factor analysis

A statistical method used to describe variability among observed variables in terms of fewer unobserved variables called factors

The observed variables are modeled as linear combinations of the factors plus error terms

The information gained about the interdependen-cies can be used later to reduce the set of variables in a dataset

Related to principal component analysis (PCA) PCA performs a variance-maximizing rotation of the variable

space, i.e. takes into account all variability in the variables

Factor analysis estimates how much of the variability is due to common factors

Factor analysis

X1

X2

X3

X4

Xp

Variables

Factor 1

Factor 2

Factor k < p

Factors

Factor analysis - an example:

Financial ratios

DSales

DAssets

EBIT-%

ROI

CR

Variables

Growth

Profitability

Solidity

Factors

ROE

CF/Sales

Equity Ratio

QR

Types/purposes of factor analysis

Exploratory factor analysis Used to uncover the underlying structure of a

relatively large set of variables

A priori assumption is that any indicator may be associated with any factor

No prior theory, factor loadings are used to intuit the factor structure of the data

Confirmatory factor analysis Seeks to determine if the number of factors and the

loadings of the measured variables on them confirm to what is expected on the basis of a pre-established theory

Factor analysis with SPSS

Analyze

⇒ Dimension Reduction

⇒ Factor

Extraction method, several alternatives e.g. Principal Components (the most common)

Maximum Likelihood

Number of factors Statistically defined (based on eigenvalues)

Used defined (Fixed) when prior assumption on factor structure

Rotation in order to extract a clearer factor pattern, several alternatives, e.g. Varimax

Oblimin

Confirmatory Factor analysis - an example:

Financial Ratios for Finnish listed companies

9 variables

DSales, DAssets, EBIT-%, ROI, ROE, Cash

Flow(Operations)/Sales, Equity Ratio, Quick Ratio

Current Ratio

Fixed number of factors: 3

Predefined assumption on three factors: Growth,

Profitability and Solidity

Extraction method: Principal Components

Analysis

Rotation method: Varimax

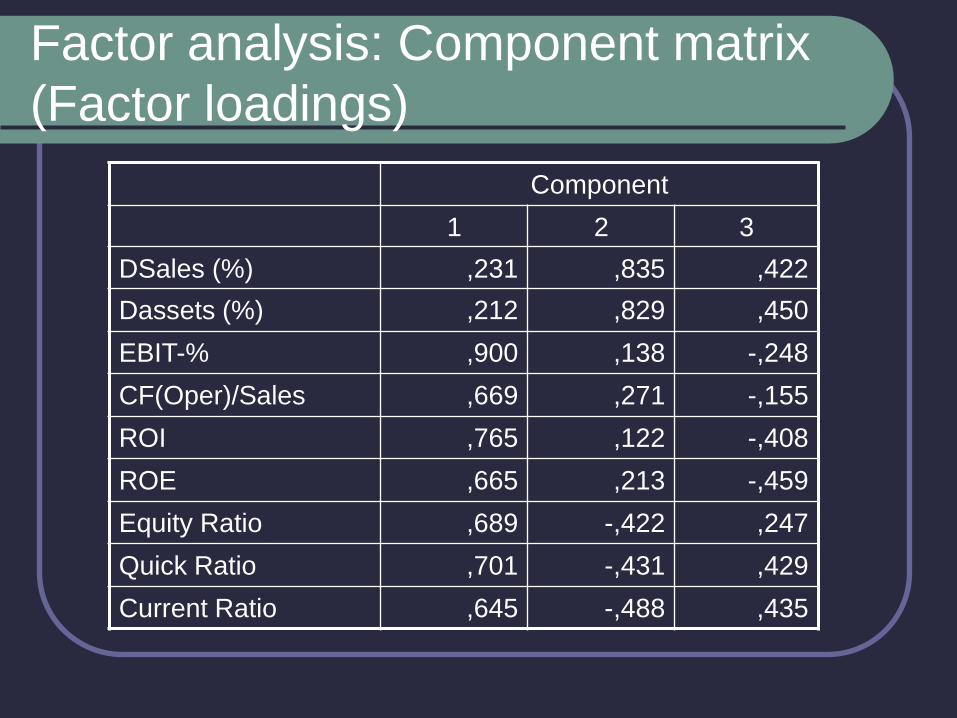

Factor analysis: Component matrix

(Factor loadings)

Component

1 2 3

DSales (%) ,231 ,835 ,422

Dassets (%) ,212 ,829 ,450

EBIT-% ,900 ,138 -,248

CF(Oper)/Sales ,669 ,271 -,155

ROI ,765 ,122 -,408

ROE ,665 ,213 -,459

Equity Ratio ,689 -,422 ,247

Quick Ratio ,701 -,431 ,429

Current Ratio ,645 -,488 ,435

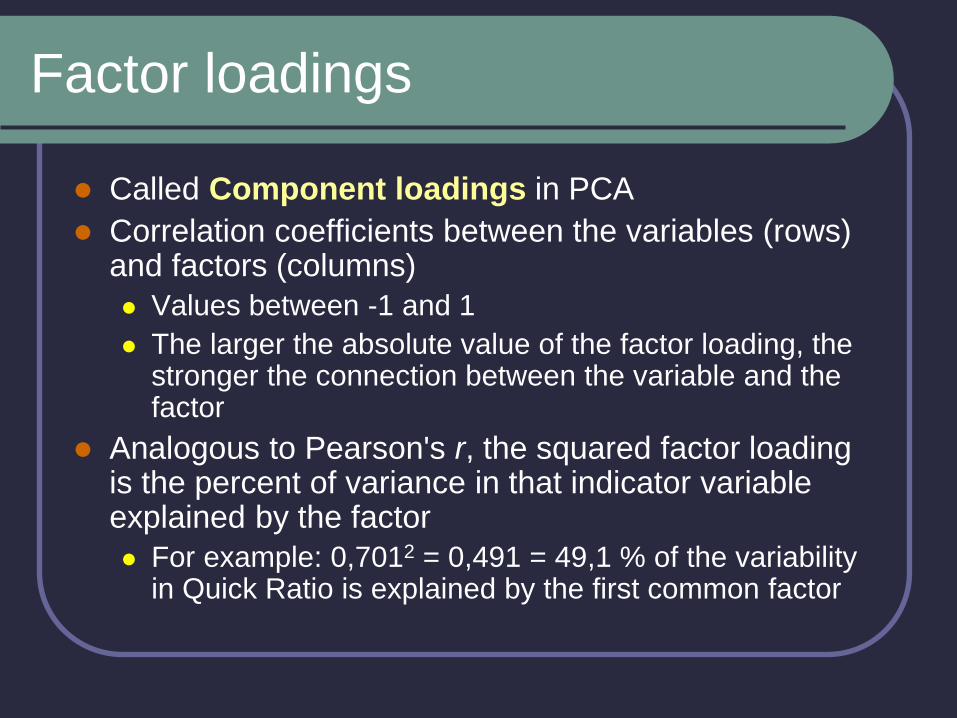

Factor loadings

Called Component loadings in PCA

Correlation coefficients between the variables (rows) and factors (columns)

Values between -1 and 1

The larger the absolute value of the factor loading, the stronger the connection between the variable and the factor

Analogous to Pearson's r, the squared factor loading is the percent of variance in that indicator variable explained by the factor

For example: 0,7012 = 0,491 = 49,1 % of the variability in Quick Ratio is explained by the first common factor

Interpreting the factor loadings and

rotating the loadings matrix

A common problem in interpreting the unrotated factor loadings matrix is that all the most significant loadings are concentrated in one or two first factors

One way to obtain more interpretable results is to rotate the solution

The most common rotation method is Varimax rotation

An orthogonal rotation (Rotated factors uncorrelated)

Maximizes the variance of the squared loadings of a factor on all the variables in the matrix

Each factor will tend to have either large or small loadings of any particular variable

Yields results that make it as easy as possible to identify each variable with a single factor

Factor analysis: Varimax-rotated

component matrix

Component

1 2 3

DSales (%) ,132 -,055 ,953

DAssets (%) ,100 -,048 ,960

EBIT-% ,869 ,344 ,128

CF(Oper)/Sales ,671 ,183 ,248

ROI ,875 ,177 ,003

ROE ,834 ,037 ,031

Equity Ratio ,274 ,795 -,086

Quick Ratio ,173 ,911 ,011

Current Ratio ,111 ,911 -,042

Factor analysis - an example: Financial ratios

for Finnish listed companies

The three pre-assumed factors – Growth, Profitability and Solidity - may be clearly identified in the rotated component matrix

For example Growth is represented by component 3 combining the major part of ratios DSales and DAssets with minor influences from the other seven variables

In the same manner Profitability is represented by component 1 and Solidity by component 2

The component matrix may be further transformed into a Component score coefficient matrix to be used to create new ratios describing the factors

Factor analysis: Communalities

Initial Extraction

DSales (%) 1,000 ,928

DAssets (%) 1,000 ,934

EBIT-% 1,000 ,890

CF(Oper)/Sales 1,000 ,545

ROI 1,000 ,766

ROE 1,000 ,698

Equity Ratio 1,000 ,715

Quick Ratio 1,000 ,861

Current Ratio 1,000 ,843

Communalities

The communalities for a variable are computed by

taking the sum of the squared loadings for that

variable

May be interpreted as multiple R2 values for

regression models predicting the variables of interest

from the factors

The sum of the squared factor loadings for all factors

for a given variable (row) is the variance in that

variable accounted for by all the factors For example 86.1 % of the variation in Quick Ratio is explained by

the three common factors, 13.9 % is left unexplained

Communalities...

One assessment of how well the model is doing can

be obtained from the communalities

Values close to one indicate that the model explains

most of the variation for the variables

Adding up the communality values for individual

variables gives the Total communality of the model

In the example case we have total communality of 7.182

Dividing total communality by the number of variables

gives the percentage of variation explained in the

model

In the example case 7.182/9 = 79.8 %

SPSS: Total Variance Explained

Compo-

nent

Initial Eigenvalues Extraction Sums of Squared

Loadings

Total % of

Variance

Cumulative

%

Total % of

Variance

Cumulative

%

1 3,765 41,832 41,832 3,765 41,832 41,832

2 2,139 23,764 65,595 2,139 23,764 65,595

3 1,277 14,184 79,780 1,277 14,184 79,780

4 ,708 7,871 87,651

... ... ... ...

9 ,103 1,143 100,000

Total variance

explained by the

three factor model

79.78 %

Even an Explorative Factor

Analysis with the default

eigenvalue limit 1,0 in SPSS

would have resulted in extractíng

three factors

Factor analysis: Computing factor

scores

The observed nine ratios for Alma Media 2005 were

DSales - 0.3846

DAssets - 0.2580

EBIT-% 0.1480

Cash Flow(Oper.)/Sales 0.1179

ROI 0.2610

ROE 0.2840

Equity Ratio 0.5201

Quick Ratio 1.7119

Current Ratio 2.9000

Factor analysis: Computing factor scores…

The nine variables may be summarized in three new

variables Profitability, Solidity and Growth by

multiplying the observed ratio values with component

scores:

Profitability = -0.053 × (-0.3846) - 0.071 × (-

0.2580) + 0.314 × 0.1480 + 0.240 × 0.1179 + 0.360

× 0.2610 + 0.374 × 0.2840 - 0.025 × 0.5201- 0.108

× 1.7119 - 0.129 × 2.9000 = -0.129

Solidity = 1.230

Growth = - 0.189

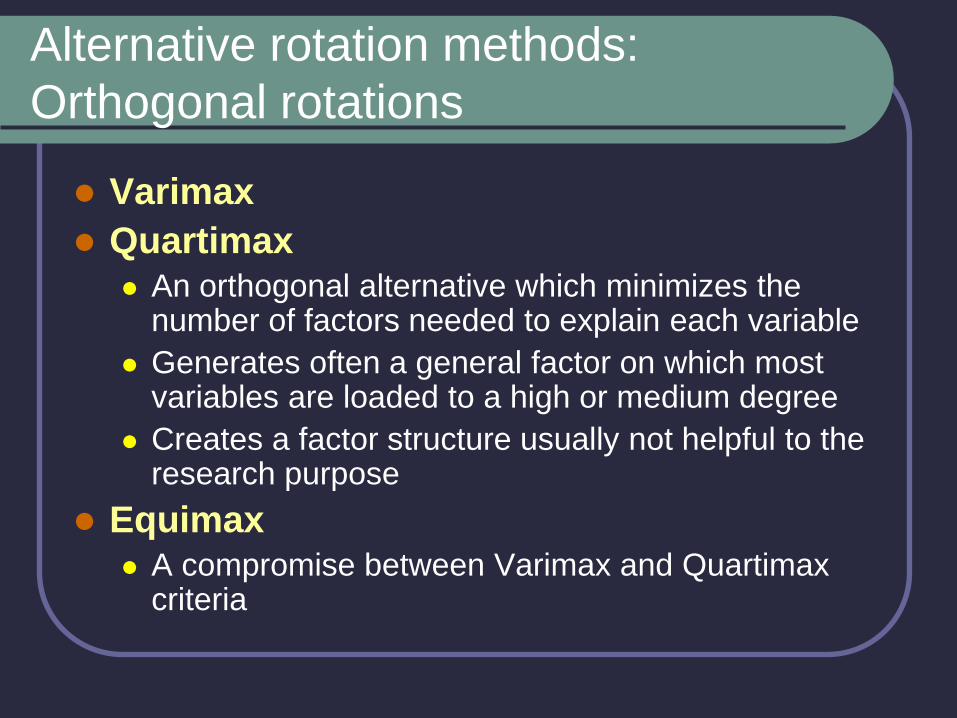

Alternative rotation methods:

Orthogonal rotations

Varimax

Quartimax An orthogonal alternative which minimizes the

number of factors needed to explain each variable

Generates often a general factor on which most variables are loaded to a high or medium degree

Creates a factor structure usually not helpful to the research purpose

Equimax A compromise between Varimax and Quartimax

criteria