Page 1

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 345

FEBRUARY 2013

VOL 4, NO 10

Factors affecting Total Quality management (TQM) implementation in

Jordanian Commercial Banks

ABLA SAEED SOUD TAHTAMOUNI

Banking and Finance Department

Faculty of Economic and Administrative Sciences

Hashemite University , Zarqa – Jordan

AMEEN AHMED MAHBOB AL MOMANI.

Department of Tourism and Archaeology

Faculty of Art , Hail‘University

Kingdom of Saudi Arabia –Hail

NADERA NOFAN MRYAN

Economic Department

Faculty of Economic and Administrative Sciences

Hashemite University , Zarqa – Jordan

Abstract

The aim of this study is to analysis the factors affecting Total Quality management (TQM) implementation in

Jordanian Commercial Banks. 160 branch manager were selected as viable for the study once it was determined that

sufficient information could be found in order to meet the research objectives. 46.9% of the sample have Batchelor

degree, 50.0% attend 2 training programmes, 56.9 % are located in Amman, 56.9% are male and 29.4% have 15

years and more of experience. Data have been processed and analyzed through the use of “SPSS” program in order

to obtain means, standard deviations, and percentages for the demographic characteristics of the sample. Moreover,

analysis of variance (ANOVA) is conducted to test if there are any statistical evidences of the existence of

difference between factors affecting Total Quality management (TQM) implementation in Jordanian Commercial

Banks and the independent variables.

Keywords: Total Quality management, Commercial Banks, Means, ANOVA

Introduction

TQM is a concept that has evolved over time and continues to evolve. It is a concept that overlaps with similar

concepts like that of the 'Quality Management Systems' laid out in the International Organization for Standardization

(ISO 9000 series), which provides world standards for management best practices. The Six Sigma concept and its

principles evolved out of a similar history with TQM. Many Six Sigma concepts are synonymous with TQM, as are

some of the principles of the Lean Manufacturing concept

TQM have changed the face of business as we know it today. Even though the bottom line for business has always

been focused on profit as a benchmark for success, much disagreement and confusion has existed from the time of

the industrial revolution to present on how to achieve that goal. How does a company make a great profit? By

making a good-quality product that sells itself and works reliably for the customer, resulting in customer satisfaction

while maintaining the lowest costs possible and selling at the best price the market will bear. TQM principles have

determined that individual ownership and pride in workmanship for all departments and employees results in a

better product.( Kasim Randeree, Ashish Mahal, Anjli Narwani, 2012).

Page 2

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 346

FEBRUARY 2013

VOL 4, NO 10

Total quality management represents a formidable challenge for bank marketers seeking to understand what makes

their bank shine in the eyes of their customers.

Is it plenty of parking spaces? An accurate statement? Convenient ATMs? A handshake at the door? Or, a

sophisticated investment product?

As banks move from the realm of quality service into the domain of total quality management, they are asking

themselves some serious questions about the way they do business. Their probing extends beyond sales and service

to include the total management philosophy.

"Banks are opening up their definition of quality management and considering what their customers expect and

experience, rather than just what the bank provides," says Diane Sauter, president of Strategic Solutions, Golden,

Colo. "There are a lot of factors that go into total quality that the customer never sees, yet considers important, such

as accuracy in processing or up time for ATMs."

Both internal and external procedures are being examined, measured and improved to deliver quality service that is

consistent throughout the bank. Sometimes referred to as re-engineering or strategic management, total quality

management programs empower employees to participate more in the decision process.(

http://www.highbeam.com/doc/1G1-16745395.html)

Review of Related Literature

Saman Yapa ,2012, the purpose of his paper is to report the results of an investigation on the use of total quality

management (TQM) tools, techniques and concepts among Sri Lankan service organizations. The findings of the

paper will provide information to the practitioners to implement TQM in their organizations and to academics to

design courses in TQM.

Lukasz Skowron, Kai Kristensen, 2012, the paper was about the the impact of the recent banking crisis on

customer loyalty in the banking sector: Developing versus developed countries. The paper consists of two parts:

theoretical and empirical. In the theoretical part the authors discuss the nature of the banking and financial crises, the

historical perspective of banking crises occurrence and main causes and consequences of those crises. The second

part of the paper demonstrates statistical analysis of the obtained data from the Polish and European banking sector.

The authors also present socio-demographic characteristic of the research samples and the character of the bank-

client relations, comparative analysis of customer satisfaction index changes in the European banking sector and

structural equation modes for the Polish banking sector for the years 2007-2009. The analyses allowed the authors to

confirm the main research hypotheses: first, clients of developing European countries demonstrate generally lower

satisfaction and loyalty levels than clients of banks in Western Europe. Second, the recent banking crisis has

affected the level of customer satisfaction much more strongly in developing European countries than in developed

ones. Third, the recent banking crisis has changed the character of the process of building customer satisfaction and

loyalty in Poland by strengthening the influence of the image area.

Kasim Randeree, Ashish Mahal, Anjli Narwani, 2012 ,study Organisations utilise Business Continuity

Management (BCM) to support sustained performance of electronic systems on which their core activities are based.

These organisations require a tool that can be used to assess the maturity of their existing BCM processes. Through

the examination of the banking sector of the United Arab Emirates, the purpose of this paper is to address the need

for a BCM maturity model. The research found that the provision of a standard maturity model for BCM as a

situational analysis tool for the banking sector is functional and can be the basis of a tool to address the gap in

organisations in general to assess the maturity level of their BCM processes.

Billy T.W. Yu, W.M. To, Peter K.C. Lee ,2012, the paper aims to explore the practice of quality management

framework as a strategic tool for public management. The paper starts with a basic process-based model; it then

enhances the model with the quality management principles for continuous improvement. With identification of

concerned factors from the literature, it examines their usefulness in the quality management system. An empirical

Page 3

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 347

FEBRUARY 2013

VOL 4, NO 10

analysis on the framework identifies eight factors: factual approach to decision making, use of quality tools,

customer focus, leadership, involvement of people, process approach, mutually beneficial supplier partnership and

internal results. The framework shows that leadership and customer focus are much more important than previously

anticipated for successful implementation of quality management system.

Faisal Talib, Zillur Rahman, M.N. Qureshi,2011, the analysis revealed the significance and usage of TQM in

Indian service industries. The results also suggested that the Indian service industries are well aware of the TQM

program, though more efforts need to be focused on implementing it properly, use of TQM models and frameworks,

and continuously improving the ongoing TQM practices. Indian service managers show a stronger familiarity with

TQM concepts and practices and they believe that TQM is a way of guaranteeing high quality products and services.

Therefore, service companies should invest in TQM, as this could help them to improve competitiveness in the

marketplace. Further, the Indian service managers and practitioners must be more concerned about the maintenance

of standards and take a more dynamic approach towards TQM, thus preparing their company more effective for

future challenges.

Keng-Boon Ooi, Binshan Lin, Boon-In Tan, Alain Yee-Loong Chong,2011 ,examine the relationship between

total quality management (TQM) practices and customer satisfaction and also to investigate the association between

TQM practices and service quality within the context of Malaysia's small service organizations. The paper uses data

from the perceptions of sales and marketing managers in 108 small service organizations in Malaysia. Data were

analyzed by employing correlation and multiple regression analysis to test the relationship between TQM practices,

customer satisfaction and service quality.

Naser A. Aboyassin, Marwan Alnsour, Moayyad Alkloub,2011, The study provides useful information and

impartial advice for managers in the insurance business in Jordan. It also suggests new business practices for the

sector. This study attempts to fill gaps in the literature on Arabian management practices. It may also contribute to

developing management practices cross-culturally.

Xingxing Zu, Huaming Zhou, Xiaowei Zhu, Dongqing Yao,2011,the purpose of this study is to investigate the

underlying characteristics that influence quality management implementation at manufacturing companies operating

in China. The results show that in general, there is no significant difference in implementing quality management

practices among companies of different operating characteristics in terms of company size, industry, ownership, and

production process. This study reveals that cultural profile is a distinguishing factor to explain the difference in

quality management implementation among the companies.

Hatice Camgöz Akdag, Mosad Zineldin,2011, the aim of this paper is to investigate and define the competitive

positioning of banks including state-owned, domestic and foreign banks operating in Istanbul, Turkey. The aim is to

check the competitive marketplace and to identify the major quality attributes, which bankers themselves and their

customers used in determining the overall perception of a given bank and services offered. The investigation was

held in Istanbul, Turkey. In total, 30 banks were included in the research, which includes state-owned, local and

foreign-owned banks. A total of 1,530 questionnaires were submitted, answers collected and analyzed. Reliability

test and frequency analysis were used to analyze the data.

Satish Mehra, Aaron D. Joyal, Munsung Rhee,2011, the paper seeks to study the impact of adopting quality

orientation as a business operations philosophy to enhance a firm's performance. Specifically, it aims to identify

various indicators that make up a quality orientation philosophy, and to research their role in improving business

performance in the banking sector of the service industry. The paper surveyed retail banking firms for this study,

and used path analysis and structure equation modeling (SEM) to develop the study model. This model was tested to

develop the process by which quality orientation philosophy, if adopted, can impact a business's performance.

Siti Zaleha Abdul Rasid, Abdul Rahim Abdul Rahman, Wan Khairuzzaman Wan Ismail, 2011 ,the purpose of

the paper is to examine the link between management accounting and risk management. The paper measures the

extent to which management accounting practices help in managing risks and the extent of the integration between

Page 4

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 348

FEBRUARY 2013

VOL 4, NO 10

these two important managerial functions. The study used a mail survey of financial institutions listed in the

Malaysian Central Banks' web site. The respondents to whom 106 questionnaires were sent were the chief financial

officers; the response rate was 68 percent. A total of 16 post-survey semi-structured interviews were also conducted

with selected respondents to gain further insights into the survey findings.

Gurjeet Kaur, R.D. Sharma, Nitasha Seli , 2009 ,the study is based on primary research conducted with data

gathered from 611 internal customers and 37 internal suppliers of an Indian private sector bank.

The results indicate that all the three components of market orientation mentioned above determine the IMO level.

Furthermore, the continuous emphasis on IMO by internal suppliers results in organizational commitment and job

satisfaction among internal customers.

Anita Lifen Zhao, Stuart Hanmer-Lloyd, Philippa Ward, Mark M.H. Goode,2008 , the purpose of the paper is

to identify risk factors that discourage Chinese consumers from adopting internet banking services (IBS). This

market is experiencing fast growth; however, an in-depth understanding of Chinese consumers within this is lacking.

Perceived risk is a key construct in Western consumer decision making, whereas whether this is true in China's IBS

market is rarely researched. An exploration of this dynamic market is therefore critical to develop theoretical and

practical implications.

Research problem

The research attempts to provide an in-depth empirical analysis of the factors affecting Total Quality management

(TQM) implementation in Jordanian Commercial Banks

A sample of bank manager in different banks location was randomly selected followed by an interview conducted

with 160 branch manager. A survey questionnaire was the data collection tool for the descriptive part of this study.

Research aims

The aim of the study was to explore the factors affecting Total Quality management (TQM) implementation in

Jordanian Commercial Banks

The key concepts in this study are (TQM) and factors affecting it.

The research question is as follows: what are the factors affecting Total Quality management (TQM)

implementation in Jordanian Commercial Banks? This research is an attempt to present data based on this question.

The measuring instrument

A questionnaire was developed to measure each of the the factors affecting Total Quality management (TQM)

implementation in Jordanian Commercial Banks. Each factor was measured using multi-item scales linked to a 5-

point Likert-type scale, ranging from strongly agrees to strongly disagree. Where possible, previously used

measuring instruments with proven reliability and validity were used.

Validity:

The questionnaire has been evaluated by instructors from the Jordanian universities. These instructors are expertise

in research in general and questionnaire developers in particular. Their remarks and comments were taken into

consideration.

Reliability:

Reliability with composite measures is evaluated for the internal consistency through the “Cronbach’s Alpha”

measure. The Alpha’s for the items are not below (0.78). Therefore, it can be concluded that the reliability of the

questionnaire is high.

Sampling

The population of the study is all commercial banks in Jordan

Page 5

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 349

FEBRUARY 2013

VOL 4, NO 10

A sample of branch manager was chosen using information available about banks branch manager

Non-probability, convenience and purposive sampling was then used to ensure that sufficient information available

on each of the branch manager chosen, and that the information gathered would be as rich and informative as

possible. A total of (160) useable questionnaires were obtained

Participants

160 branch manager were selected as viable for the study once it was determined that sufficient information could

be found in order to meet the research objectives.

46.9% of the sample have Batchelor degree, 50.0% attend 2 training programmes, 56.9 % are located in Amman,

56.9% are male and 29.4% have 15 years and more of experience (table 1)

Table (1): Sample Distribution in Commercial Banks

Variable Frequency %

Qualifications of bank

manager:

Batchelor degree

75 46.9

Master degree

64 40.0

Ph.D degree

21 13.1

Number of training

programmes that attend in

QM:

Non

37 23.1

2 training programmes

80 50.0

More than 2 training

programmes 43 26.9

Location of the bank:

Amman 91 56.9

Irbid 32 20.0

Zarqa 37 23.1

Gender:

Male 120 75.0

Female 40 25.0

Years of experience of bank

manager:

Less than (5) years 31 19.4

(5) to less than (10) years 37 23.1

(10) to less than (15) years 45 28.1

15 years and more 47 29.4

Page 6

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 350

FEBRUARY 2013

VOL 4, NO 10

Procedure

A sample was randomly selected. A survey questionnaire was the data collection tool for the descriptive part of this

study. The questionnaire has been adopted from the research conducted by the researchers

Salaheldin Ismail Salaheldin and Banan A. Mukhalalati,2009," The Implementation of TQM in the Qatari

Healthcare Sector" Journal of Accounting – Business & Management vol. 16 no. 2 (2009) 1-14

Research limitations

The main limitation of this study is that the sample was small. The questionnaire has been adopted from the research

conducted by others. The data and generalizability of the findings should be viewed while considering these

limitations. It is restricted to the employees working in the Jordanian commercial banks in Amman, Zarqa, and Irbid

governorate. It has been conducted within a short period of time which may not reflect an accurate and valid profile

about work stress in organizations.

Terminology of the Study:

Total Quality management (TQM): is an integrative philosophy of management for continuously improving the

quality of products and processes

Data Collection:

The study adopts two sources of data: secondary and primary data. Secondary data are obtained from literature

published in this subject including previous studies. The primary data are collected from field study conducted

through a questionnaire. The questionnaire consists of two parts: The first part included general data of personal

variables (Location of the bank, Years of experience of bank manager, Gender, Qualifications of bank manager and

Number of training programmes that attend in QM). The second part included (19) items representing the factors

affecting Total Quality management (TQM) implementation in implementation in Jordanian Commercial Banks

Data Analysis Methods:

Ready statistical software was chosen to analyze the collected data. It is the Statistical Package for Social Sciences

(SPSS) which is usually used in the social sciences studies: Descriptive statistics, to describe the characteristics of

the sample depending on frequencies, percentages, means, and standard deviation, “t-test” and “Sheffe test” for prior

comparisons, ANOVA to measure the effects of the independent variables on the dependent variable.

Hypothesis

The following hypotheses were examined:

H1: There are no statistical differences (α≤0.05) between managers due to the location of the banks towards the

factors affecting Total Quality management (TQM) implementation in Jordanian Commercial Banks H2: There are no statistical differences (α≤0.05) between managers due to the Years of experience towards the

factors affecting Total Quality management (TQM) implementation in Jordanian Commercial Banks H3: There are no statistical differences (α≤0.05) between managers due to the Gender towards the factors affecting

Total Quality management (TQM) implementation in Jordanian Commercial Banks H4: There are no statistical differences (α≤0.05) between managers due to the Qualifications of bank manager

towards the factors affecting Total Quality management (TQM) implementation in Jordanian Commercial Banks

H5: There are no statistical differences (α≤0.05) between managers due to the number of training programmes that

attend in QM towards the factors affecting Total Quality management (TQM) implementation in Jordanian

Commercial Banks

Page 7

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 351

FEBRUARY 2013

VOL 4, NO 10

Statistical results

What are the factors affecting Total Quality management (TQM) implementation in Jordanian Commercial Banks?

To answer this question we find the mean for each variable (table 2). A quick review of the result in table 2 reveals

clearly that variables 1 and 5 have the highest mean value (4.9938) and this means that the effective management

decisions and operating systems and customers satisfaction level are some of the factors that affecting Total

Quality management (TQM) implementation in Jordanian Commercial Banks

Variable 7 has the least mean value, which means that the bank manager do not feel that the product/service quality

level is one of the factors that affecting Total Quality management (TQM) implementation in Jordanian

Commercial Banks (table 2)

Table (2): Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

q1 160 4.00 5.00 4.9938 .07906

q2 160 1.00 5.00 4.7063 .66915

q3 160 1.00 5.00 4.6938 .68218

q4 160 3.00 5.00 4.8188 .44682

q5 160 4.00 5.00 4.9938 .07906

q6 160 1.00 5.00 4.8688 .66467

q7 160 1.00 5.00 4.4813 .94484

q8 160 3.00 5.00 4.8250 .44226

q9 160 3.00 5.00 4.7938 .46374

q10 160 2.00 5.00 4.8000 .52365

q11 160 2.00 5.00 4.8313 .50434

q12 160 2.00 5.00 4.7313 .59051

q13 160 3.00 5.00 4.8250 .44226

q14 160 3.00 5.00 4.7938 .49011

q15 160 3.00 5.00 4.8000 .48629

q16 160 2.00 5.00 4.7938 .52721

q17 160 3.00 5.00 4.8438 .38111

q18 160 4.00 5.00 4.9875 .11145

q19 160 4.00 5.00 4.9688 .17454

Valid N (listwise) 160

Testing the Hypothesis

To test hypothesis 1 we used SPSS and One-Way Analysis of Variance ANOVA, we found that there were

statistical differences towards the factors affecting Total Quality management (TQM) implementation in Jordanian

Commercial Banks due to the location of the banks in statements 2,7,11 and 13. Table (3)

Page 8

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 352

FEBRUARY 2013

VOL 4, NO 10

Table (3): ANOVA test for location of the banks level

Sum of Squares df Mean Square F Sig

q2 Between Groups 8.149 2 4.075 10.147 .000

Within Groups 63.045 157 .402

Total 71.194 159

q7 Between Groups 7.564 2 3.782 4.418 .014

Within Groups 134.380 157 .856

Total 141.944 159

q11 Between Groups 2.696 2 1.348 5.607 .004

Within Groups 37.748 157 .240

Total 40.444 159

q13 Between Groups 1.853 2 .926 4.973 .008

Within Groups 29.247 157 .186

Total 31.100 159

To know which group is significant we ran the Scheffe test. . Table (4)

Table (4): Scheffe test for the location of the banks

Multiple Comparisons

Schef fe

.06490 .13024 .883 -.2569 .3868

.54886* .12355 .000 .2435 .8542

-.06490 .13024 .883 -.3868 .2569

.48395* .15298 .008 .1059 .8620

-.54886* .12355 .000 -.8542 -.2435

-.48395* .15298 .008 -.8620 -.1059

.42033 .19014 .090 -.0496 .8902

.45411* .18039 .045 .0083 .8999

-.42033 .19014 .090 -.8902 .0496

.03378 .22334 .989 -.5182 .5857

-.45411* .18039 .045 -.8999 -.0083

-.03378 .22334 .989 -.5857 .5182

-.00515 .10077 .999 -.2542 .2439

.30650* .09560 .007 .0702 .5428

.00515 .10077 .999 -.2439 .2542

.31166* .11837 .034 .0191 .6042

-.30650* .09560 .007 -.5428 -.0702

-.31166* .11837 .034 -.6042 -.0191

-.12260 .08871 .387 -.3418 .0966

.19751 .08415 .067 -.0105 .4055

.12260 .08871 .387 -.0966 .3418

.32010* .10419 .010 .0626 .5776

-.19751 .08415 .067 -.4055 .0105

-.32010* .10419 .010 -.5776 -.0626

(J) location

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

(I) location

1.00

2.00

3.00

1.00

2.00

3.00

1.00

2.00

3.00

1.00

2.00

3.00

Dependent Variable

q2

q7

q11

q13

Mean

Dif f erence

(I-J) Std. Error Sig. Lower Bound Upper Bound

95% Conf idence Interv al

The mean dif f erence is signif icant at the .05 lev el.*.

Page 9

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 353

FEBRUARY 2013

VOL 4, NO 10

We found the managers who work in Irbid reports and feel more than those who working in Amman and Zarka that

factors affecting TQM implementation in banks are: Management philosophy and practice which ensure effective

and efficient use of all available resources, product/service quality leve, Proper policies in Place and Adopting an

accreditation system

So we rejected the hypothesis.

To test hypothesis 2 we used SPSS and One-Way Analysis of Variance ANOVA, we found that there were

statistical differences towards the factors affecting Total Quality management (TQM) implementation in Jordanian

Commercial Banks due to the Years of experience in statements 3,6,7,11and 15. Table (5)

Table (5): ANOVA test for Years of experience

ANOVA

Sum of

Squares df

Mean

Square F Sig

q3 Between Groups 7.022 3 2.341 5.452 .001

Within Groups 66.972 156 .429

Total 73.994 159

q6 Between Groups 4.078 3 1.359 3.205 .025

Within Groups 66.166 156 .424

Total 70.244 159

q7 Between Groups 35.355 3 11.785 17.248 .000

Within Groups 106.588 156 .683

Total 141.944 159

q11 Between Groups 2.990 3 .997 4.151 .007

Within Groups 37.454 156 .240

Total 40.444 159

q15 Between Groups 5.594 3 1.865 9.089 .000

Within Groups 32.006 156 .205

Total 37.600 159

To know which group is significant we ran the Scheffe test. . Table (6)

Page 10

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 354

FEBRUARY 2013

VOL 4, NO 10

Table (6) Scheffe test for the Years of experience

Multiple Comparisons

Schef fe

-.38535 .15954 .125 -.8362 .0655

-.57634* .15293 .003 -1.0086 -.1441

-.51819* .15160 .010 -.9466 -.0897

.38535 .15954 .125 -.0655 .8362

-.19099 .14541 .632 -.6019 .2200

-.13283 .14400 .837 -.5398 .2742

.57634* .15293 .003 .1441 1.0086

.19099 .14541 .632 -.2200 .6019

.05816 .13665 .981 -.3281 .4444

.51819* .15160 .010 .0897 .9466

.13283 .14400 .837 -.2742 .5398

-.05816 .13665 .981 -.4444 .3281

-.14385 .15857 .844 -.5920 .3043

-.38710 .15201 .095 -.8167 .0425

-.38710 .15069 .090 -.8130 .0388

.14385 .15857 .844 -.3043 .5920

-.24324 .14453 .421 -.6517 .1652

-.24324 .14313 .412 -.6478 .1613

.38710 .15201 .095 -.0425 .8167

.24324 .14453 .421 -.1652 .6517

.00000 .13583 1.000 -.3839 .3839

.38710 .15069 .090 -.0388 .8130

.24324 .14313 .412 -.1613 .6478

.00000 .13583 1.000 -.3839 .3839

.89974* .20126 .000 .3309 1.4686

-.16272 .19294 .870 -.7080 .3826

-.32395 .19125 .415 -.8645 .2166

-.89974* .20126 .000 -1.4686 -.3309

-1.06246* .18344 .000 -1.5809 -.5440

-1.22369* .18167 .000 -1.7371 -.7102

.16272 .19294 .870 -.3826 .7080

1.06246* .18344 .000 .5440 1.5809

-.16123 .17240 .831 -.6485 .3260

.32395 .19125 .415 -.2166 .8645

1.22369* .18167 .000 .7102 1.7371

.16123 .17240 .831 -.3260 .6485

.34612* .11931 .042 .0089 .6833

.01219 .11437 1.000 -.3110 .3354

.18051 .11337 .471 -.1399 .5009

-.34612* .11931 .042 -.6833 -.0089

-.33393* .10874 .027 -.6413 -.0266

-.16561 .10769 .502 -.4700 .1387

-.01219 .11437 1.000 -.3354 .3110

.33393* .10874 .027 .0266 .6413

.16832 .10219 .441 -.1205 .4571

-.18051 .11337 .471 -.5009 .1399

.16561 .10769 .502 -.1387 .4700

-.16832 .10219 .441 -.4571 .1205

-.19878 .11029 .358 -.5105 .1129

-.18136 .10572 .403 -.4802 .1174

.24228 .10480 .153 -.0539 .5385

.19878 .11029 .358 -.1129 .5105

.01742 .10052 .999 -.2667 .3015

.44106* .09955 .000 .1597 .7224

.18136 .10572 .403 -.1174 .4802

-.01742 .10052 .999 -.3015 .2667

.42364* .09447 .000 .1566 .6906

-.24228 .10480 .153 -.5385 .0539

-.44106* .09955 .000 -.7224 -.1597

-.42364* .09447 .000 -.6906 -.1566

(J) experience

2.00

3.00

4.00

1.00

3.00

4.00

1.00

2.00

4.00

1.00

2.00

3.00

2.00

3.00

4.00

1.00

3.00

4.00

1.00

2.00

4.00

1.00

2.00

3.00

2.00

3.00

4.00

1.00

3.00

4.00

1.00

2.00

4.00

1.00

2.00

3.00

2.00

3.00

4.00

1.00

3.00

4.00

1.00

2.00

4.00

1.00

2.00

3.00

2.00

3.00

4.00

1.00

3.00

4.00

1.00

2.00

4.00

1.00

2.00

3.00

(I) experience

1.00

2.00

3.00

4.00

1.00

2.00

3.00

4.00

1.00

2.00

3.00

4.00

1.00

2.00

3.00

4.00

1.00

2.00

3.00

4.00

Dependent Variable

q3

q6

q7

q11

q15

Mean

Dif f erence

(I-J) Std. Error Sig. Lower Bound Upper Bound

95% Conf idence Interval

The mean dif f erence is signif icant at the .05 lev el.*.

Page 11

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 355

FEBRUARY 2013

VOL 4, NO 10

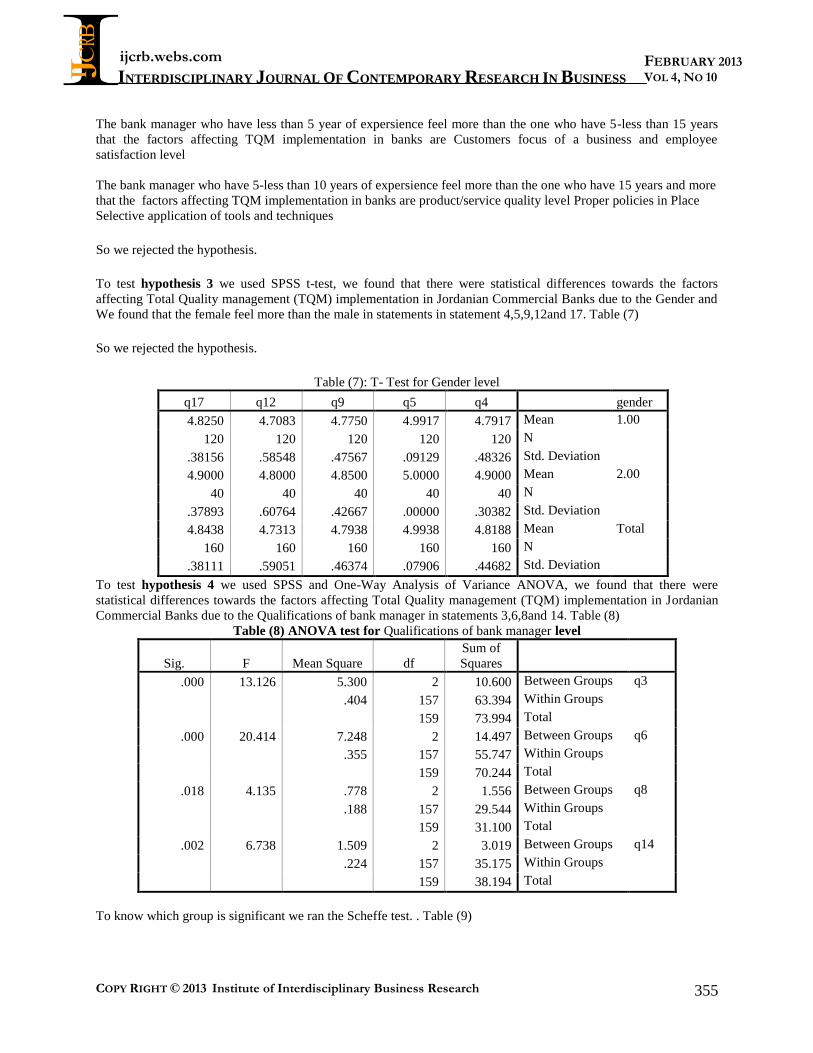

The bank manager who have less than 5 year of expersience feel more than the one who have 5-less than 15 years

that the factors affecting TQM implementation in banks are Customers focus of a business and employee

satisfaction level

The bank manager who have 5-less than 10 years of expersience feel more than the one who have 15 years and more

that the factors affecting TQM implementation in banks are product/service quality level Proper policies in Place

Selective application of tools and techniques

So we rejected the hypothesis.

To test hypothesis 3 we used SPSS t-test, we found that there were statistical differences towards the factors

affecting Total Quality management (TQM) implementation in Jordanian Commercial Banks due to the Gender and

We found that the female feel more than the male in statements in statement 4,5,9,12and 17. Table (7)

So we rejected the hypothesis.

Table (7): T- Test for Gender level

gender q4 q5 q9 q12 q17

1.00 Mean 4.7917 4.9917 4.7750 4.7083 4.8250

N 120 120 120 120 120

Std. Deviation .48326 .09129 .47567 .58548 .38156

2.00 Mean 4.9000 5.0000 4.8500 4.8000 4.9000

N 40 40 40 40 40

Std. Deviation .30382 .00000 .42667 .60764 .37893

Total Mean 4.8188 4.9938 4.7938 4.7313 4.8438

N 160 160 160 160 160

Std. Deviation .44682 .07906 .46374 .59051 .38111

To test hypothesis 4 we used SPSS and One-Way Analysis of Variance ANOVA, we found that there were

statistical differences towards the factors affecting Total Quality management (TQM) implementation in Jordanian

Commercial Banks due to the Qualifications of bank manager in statements 3,6,8and 14. Table (8)

Table (8) ANOVA test for Qualifications of bank manager level

Sum of

Squares df Mean Square F Sig.

q3 Between Groups 10.600 2 5.300 13.126 .000

Within Groups 63.394 157 .404

Total 73.994 159

q6 Between Groups 14.497 2 7.248 20.414 .000

Within Groups 55.747 157 .355

Total 70.244 159

q8 Between Groups 1.556 2 .778 4.135 .018

Within Groups 29.544 157 .188

Total 31.100 159

q14 Between Groups 3.019 2 1.509 6.738 .002

Within Groups 35.175 157 .224

Total 38.194 159

To know which group is significant we ran the Scheffe test. . Table (9)

Page 12

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 356

FEBRUARY 2013

VOL 4, NO 10

Table (9) Scheffe test for the Qualifications of bank manager

Multiple Comparisons

Schef fe

.23708 .10813 .094 -.0301 .5043

.79810* .15688 .000 .4104 1.1858

-.23708 .10813 .094 -.5043 .0301

.56101* .15980 .003 .1661 .9559

-.79810* .15688 .000 -1.1858 -.4104

-.56101* .15980 .003 -.9559 -.1661

.03125 .10140 .954 -.2193 .2818

.90476* .14711 .000 .5412 1.2683

-.03125 .10140 .954 -.2818 .2193

.87351* .14985 .000 .5032 1.2438

-.90476* .14711 .000 -1.2683 -.5412

-.87351* .14985 .000 -1.2438 -.5032

.00729 .07382 .995 -.1751 .1897

.29524* .10710 .024 .0306 .5599

-.00729 .07382 .995 -.1897 .1751

.28795* .10909 .033 .0183 .5575

-.29524* .10710 .024 -.5599 -.0306

-.28795* .10909 .033 -.5575 -.0183

-.19083 .08055 .063 -.3899 .0082

.22286 .11686 .166 -.0659 .5116

.19083 .08055 .063 -.0082 .3899

.41369* .11904 .003 .1195 .7079

-.22286 .11686 .166 -.5116 .0659

-.41369* .11904 .003 -.7079 -.1195

(J) qualif ication

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

(I) qualif ication

1.00

2.00

3.00

1.00

2.00

3.00

1.00

2.00

3.00

1.00

2.00

3.00

Dependent Variable

q3

q6

q8

q14

Mean

Dif f erence

(I-J) Std. Error Sig. Lower Bound Upper Bound

95% Conf idence Interv al

The mean dif f erence is signif icant at the .05 lev el.*.

The bank manager who have ph.d feel more than the one who have Batchelor and Master degree that the factors

affecting TQM implementation in banks are Customers focus of a business and employee satisfaction level, delivery

time and engineer in foundation of businesses plan stage

So we rejected the hypothesis.

To test hypothesis 5we used SPSS and One-Way Analysis of Variance ANOVA, we found that there were

statistical differences towards the factors affecting Total Quality management (TQM) implementation in Jordanian

Commercial Banks due to the training programmes that attend in QM in statements 3,6,7and 13. Table (10)

Page 13

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 357

FEBRUARY 2013

VOL 4, NO 10

Table (10) ANOVA test for training programmes level

Sum of Squares df Mean Square F Sig.

q3 Between Groups 6.574 2 3.287 7.654 .001

Within Groups 67.420 157 .429

Total 73.994 159

q6 Between Groups 9.163 2 4.581 11.776 .000

Within Groups 61.081 157 .389

Total 70.244 159

q7 Between Groups 13.820 2 6.910 8.468 .000

Within Groups 128.123 157 .816

Total 141.944 159

q13 Between Groups 1.677 2 .838 4.474 .013

Within Groups 29.423 157 .187

Total 31.100 159

To know which group is significant we ran the Scheffe test. Table (11)

Table (11) Scheffe test for the training programmes

Multiple Comparisons

Schef fe

-.47568* .13028 .002 -.7976 -.1537

-.48963* .14694 .005 -.8528 -.1265

.47568* .13028 .002 .1537 .7976

-.01395 .12391 .994 -.3202 .2923

.48963* .14694 .005 .1265 .8528

.01395 .12391 .994 -.2923 .3202

-.56757* .12401 .000 -.8740 -.2611

-.56757* .13987 .000 -.9132 -.2219

.56757* .12401 .000 .2611 .8740

.00000 .11794 1.000 -.2915 .2915

.56757* .13987 .000 .2219 .9132

.00000 .11794 1.000 -.2915 .2915

-.46047* .17960 .040 -.9043 -.0166

-.83344* .20257 .000 -1.3340 -.3328

.46047* .17960 .040 .0166 .9043

-.37297 .17082 .096 -.7951 .0492

.83344* .20257 .000 .3328 1.3340

.37297 .17082 .096 -.0492 .7951

-.20135 .08607 .068 -.4141 .0113

-.28158* .09707 .017 -.5215 -.0417

.20135 .08607 .068 -.0113 .4141

-.08023 .08186 .619 -.2825 .1221

.28158* .09707 .017 .0417 .5215

.08023 .08186 .619 -.1221 .2825

(J) teraining

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

2.00

3.00

1.00

3.00

1.00

2.00

(I) teraining

1.00

2.00

3.00

1.00

2.00

3.00

1.00

2.00

3.00

1.00

2.00

3.00

Dependent Variable

q3

q6

q7

q13

Mean

Dif f erence

(I-J) Std. Error Sig. Lower Bound Upper Bound

95% Conf idence Interv al

The mean dif f erence is signif icant at the .05 lev el.*.

Page 14

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 358

FEBRUARY 2013

VOL 4, NO 10

We found the managers who do not attend any training programmes feel more than the one attend 2 training

programmes and more that factors affecting TQM implementation in banks:Customers focus of a business.

employee satisfaction level product/service quality level and Adopting an accreditation system

So we rejected the hypothesis.

Conclusions:

The main results and conclusions of this study are summarized as follows:

There are significant statistical evidences that differences between factors that affecting Total Quality management

(TQM) implementation in Jordanian Commercial Banks. These differences are due to the following factors:

1. Location of the bank:

we found the managers who work in Irbid reports and feel more than those who working in Amman and Zarka that

factors affecting TQM implementation in banks are: Management philosophy and practice which ensure effective

and efficient use of all available resources, product/service quality leve, Proper policies in Place and Adopting an

accreditation system

2.Years of experience of bank manager:

The bank manager who have less than 5 year of expersience feel more than the one who have 5-less than 15 years

that the factors affecting TQM implementation in banks are Customers focus of a business and employee

satisfaction level

The bank manager who have 5-less than 10 years of expersience feel more than the one who have 15 years and more

that the factors affecting TQM implementation in banks are product/service quality level Proper policies in Place

Selective application of tools and techniques

3. Gender:

We found that the female feel more than the male in statements in statement 4,5,9,12and 17

4. Qualifications of bank manager:

The bank manager who have ph.d feel more than the one who have Batchelor and Master degree that the factors

affecting TQM implementation in banks are Customers focus of a business and employee satisfaction level, delivery

time and engineer in foundation of businesses plan stage

5. Number of training programmes that attend in QM

we found the managers who do not attend any training programmes feel more than the one attend 2 training

programmes and more that factors affecting TQM implementation in banks:Customers focus of a business.

employee satisfaction level product/service quality level and Adopting an accreditation system

Recommendations:

(1) Developing recruitment and employment methods to place the appropriate person for the

appropriate job.

(2) Conducting training courses based on identification of training needs, to provide employees with

the required information, and to develop their abilities, skills, and attitudes.

Future Studies:

Conclusions of the previous studies, as well as the conclusions of this study, are worth investigation and revision by

researchers; hence the researchers recommend conducting the following studies: factors affecting TQM

implementation in banks

Page 15

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 359

FEBRUARY 2013

VOL 4, NO 10

Questionnaire

Factors affecting TQM implementation in banks

Part One – Personal Data:

1. Location of the bank:

- Amman

- Zarka

- Irbid

2.Years of experience of bank manager:

- less than 5 years.

- 5-less than 10 years.

- 10-less than 15 years.

- 15 years and more

3. Gender:

-Male.

-Female.

4. Qualifications of bank manager:

- Batchelor degree

- Master

- Ph.D

5. Number of training programmes that attend in QM

- Non

- 2 training programmes

- More than 2 training programmes

Part Two – Questionnaire statements:

Put the sign (√) in front of each item of the following on the right column:

No.

Factors affecting TQM implementation in

banks

Strongly

agree

Agree Neutral

Not

agree

Strongly

not agree

1. Effective management decisions and

operating systems

2. Management philosophy and practice

which ensure effective and efficient use

of all available resources

3. Customers focus of a business.

4. Teamwork and participation as continues

improvement culture

5. Customers satisfaction level

6. employee satisfaction level

7. product/service quality level

8. delivery time

9. Supplier involvement

10. Quality systems standards such as ISO

9000

11. Proper policies in Place

12. A work environment through

management-worker partnership.

13. Adopting an accreditation system

Page 16

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 360

FEBRUARY 2013

VOL 4, NO 10

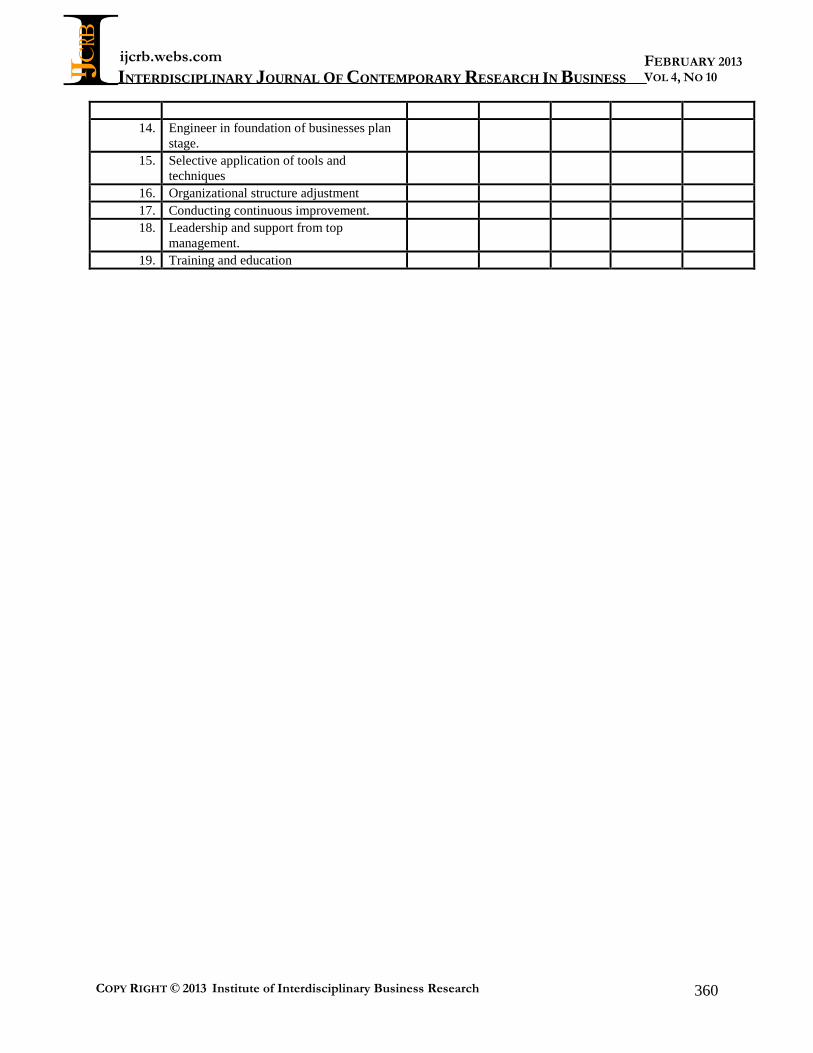

14. Engineer in foundation of businesses plan

stage.

15. Selective application of tools and

techniques

16. Organizational structure adjustment

17. Conducting continuous improvement.

18. Leadership and support from top

management.

19. Training and education

Page 17

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 361

FEBRUARY 2013

VOL 4, NO 10

References

Ahire, S. L. 1997. Management Science- Total Quality Management interfaces: An integrative framework.

Interfaces 27 (6) 91-105.

Anita Lifen Zhao, Stuart Hanmer-Lloyd, Philippa Ward, Mark M.H. Goode,2008,"

Assessing the awareness of total quality management in Indian service industries: An empirical investigation",Asian

Journal on Quality Volume: 12 Issue: 3

Billy T.W. Yu, W.M. To, Peter K.C. Lee,2012," Quality management framework for public management decision

making", Management Volume: 50 Issue: 3

Faisal Talib, Zillur Rahman, M.N. Qureshi,2011,"

Gurjeet Kaur, R.D. Sharma, Nitasha Seli,2009," Internal market orientation in Indian banking: an empirical

analysis",Managing Service Quality Volume: 19 Issue: 5

Hatice Camgöz Akdag, Mosad Zineldin,2011," Strategic positioning and quality determinants in banking

service",The TQM Journal Volume: 23 Issue: 4

Kasim Randeree, Ashish Mahal, Anjli Narwani,2012," A business continuity management maturity model for the

UAE banking sector",Business Process Management Journal Volume: 18 Issue: 3

Keng-Boon Ooi, Binshan Lin, Boon-In Tan, Alain Yee-Loong Chong,2011,' Are TQM practices supporting

customer satisfaction and service quality?

Type: Research paper",Journal of Services Marketing Volume: 25 Issue: 6

Lukasz Skowron, Kai Kristensen,2012," The impact of the recent banking crisis on customer loyalty in the banking

sector: Developing versus developed countries", The Volume: 24 Issue: 6

Naser A. Aboyassin, Marwan Alnsour, Moayyad Alkloub,2011,' Achieving total quality management using

knowledge management practices: A field study at the Jordanian insurance sector",International Journal of

Commerce and Management Volume: 21 Issue: 4

Perceived risk and Chinese consumers' internet banking services adoption"International Journal of Bank Marketing

Volume: 26 Issue: 7

Saman Yapa, 2012," Total quality management in Sri Lankan service organizations

",The TQM Journal Volume: 24 Issue: 6

Satish Mehra, Aaron D. Joyal, Munsung Rhee,2011," On adopting quality orientation as an operations philosophy to

improve business performance in banking services",International Journal of Quality & Reliability Management

Volume: 28

Siti Zaleha Abdul Rasid, Abdul Rahim Abdul Rahman, Wan Khairuzzaman Wan Ismail,2011," Management

accounting and risk management in Malaysian financial institutions: An exploratory study",Managerial Auditing

Journal Volume: 26 Issue: 7

Xingxing Zu, Huaming Zhou, Xiaowei Zhu, Dongqing Yao,2011," Quality management in China: the effects of firm

characteristics and cultural profile",International Journal of Quality & Reliability Management Volume: 28 Issue: 8

http://www.highbeam.com/doc/1G1-16745395.html