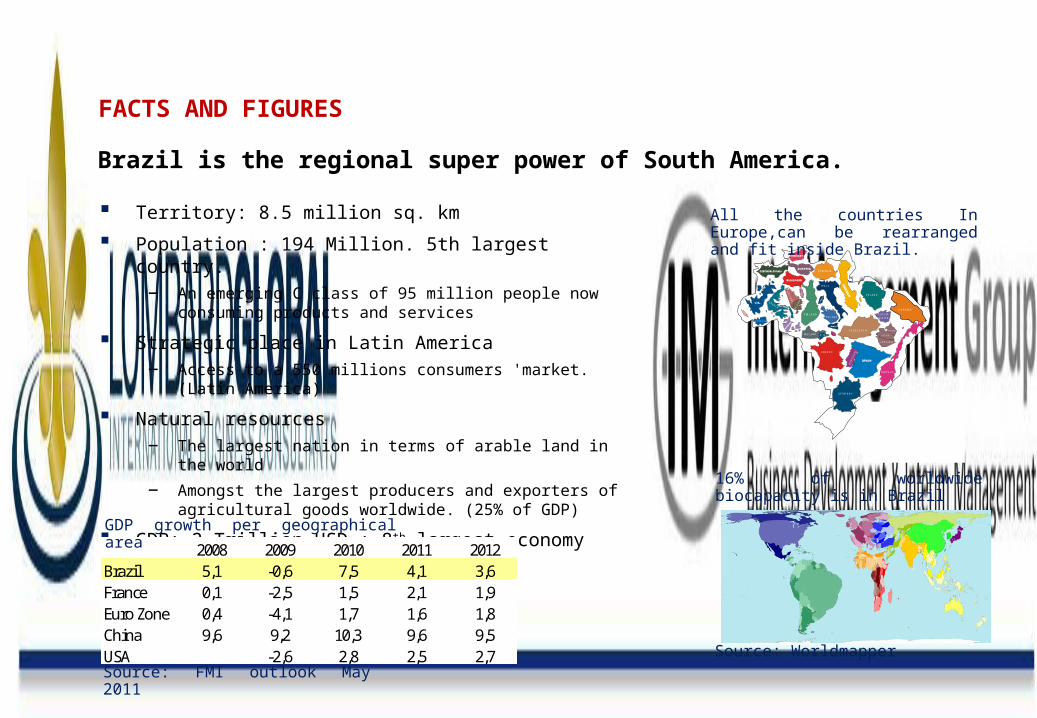

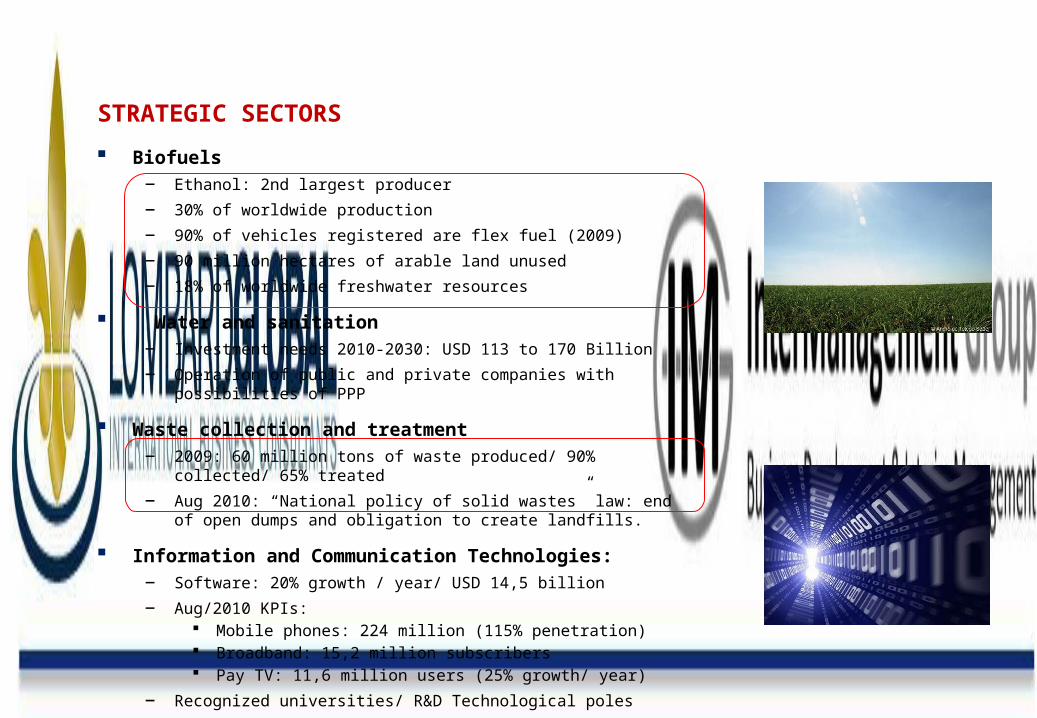

FACTS AND FIGURES Territory: 8.5 million sq. km Population : 194 Million. 5th largest country. − An emerging C class of 95 million people now consuming products and services Strategic place in Latin America − Access to a 550 millions consumers 'market. (Latin America) Natural resources − The largest nation in terms of arable land in the world − Amongst the largest producers and exporters of agricultural goods worldwide. (25% of GDP) GDP: 2 Trillion USD : 8 th largest economy of 3.3 million square miles, the c ountry is large r than the continental ROMANIA ICELAND P O RT U GAL H O L L AN D BE LG IU M SW ITZER LAN D C YPRU S G R EECE ITA L Y Y U G O S L AV IA IRELAND N. IRL. POLAND UKRAINE FRANCE NORWAY LITH UAN IA LATVIA ES T O N IA GERMANY R U S SIA (W HITE) FIN LA N D All the countries In Europe,can be rearranged and fit inside Brazil. 16% of worldwide biocapacity is in Brazil Source: Worldmapper 2008 2009 2010 2011 2012 Brazil 5,1 -0,6 7,5 4,1 3,6 France 0,1 -2,5 1,5 2,1 1,9 Euro Zone 0,4 -4,1 1,7 1,6 1,8 China 9,6 9,2 10,3 9,6 9,5 USA -2,6 2,8 2,5 2,7 GDP growth per geographical area Brazil is the regional super power of South America. Source: FMI outlook May 2011

Transcript

FACTS AND FIGURES

Territory: 8.5 million sq. km

Population : 194 Million. 5th largest country.

− An emerging C class of 95 million people now consuming products and services

Strategic place in Latin America

− Access to a 550 millions consumers 'market. (Latin America)

Natural resources

− The largest nation in terms of arable land in the world

− Amongst the largest producers and exporters of agricultural goods worldwide. (25% of GDP)

GDP: 2 Trillion USD : 8th largest economy

EURO PE IN BRAZIL

All the c o untrie s in Eu ro p e ,inc lud ing p a rt o f th e e x-So vie tUnio n , c a n b e re a rra ng e d tofit insid e Bra zil. W ith a te rrito ry

o f 3.3 m illio n sq ua re m ile s, th e c o un try is la rg e r tha n the c o ntin e n ta l

Unite d Sta te s.

R OM A N I A

ICELAND

PO

RT

UG

AL

HO

LLA

ND

BE

LGIU

M

SWITZERLAND

CYPRU

S

GREECE

M A L T A

I TA L Y

Y U GO S L AV IAIR E L A N D N . IR L .

P O L A N D

U K R A I N E

F RA N C E

N OR W AY

L ITH UAN IA

LAT VIA

ESTONIA

G E R M A NY

R U S S IA(W HI T E )

F IN L A N D

All the countries In Europe,can be rearranged and fit inside Brazil.

− Luxury: 2002 -2010 Class A revenue grown 48% Promising sector. Growth rate 20%/ year over last 5 years Evolution of millionaires forecasted 2010-2017: 330%

BRAZIL OUTLOOK, AGENDA

Brazil Today

Strategic Sectors

Foreign Investments

Cultural aspects

Cases of success and failure

Interim Management in Brazil

FOREIGN DIRECT INVESTMENTS

Brazil: Modern and each time more open to foreign countries

Brazil: 4,3% of global Foreign Direct Investments in 2010 (4th largest)

Investment Grade from Standars & Poors in 2008 and Moody´s in 2009

850 of the 1000 world’s largest corporations are present in Brazil, by joint-venture or with subsidiary.

Since privatization programs in 2000, FDI above 15 Billion USD/ year (expect 2002/3) [?]

Growth of FDI in primary sector (Oil & Gas)

16%13%

10% 9% 8%6%

USA Luxembourg Netherland Japan Spain France

Direct Investment in Brazil per origin. 2009

Source: Banco Central do Brasil, Oct 2010

FRENCH INVESTMENTS

The presence of French companies in Brazil’s FDI is important

37 of the CAC 40 companies have at least one subsidiary in Brazil

450 subsidiaries of French companies in Brazil

60% in SP ; 20% in Rio (Others in Minas Gerais and Paraná)

All sectors are present (out of civil construction)

21%

6%

54%

8%

11%

Importation/Exportation

Representation Desk

Subsidiary/Industrial unit

JV/ Partnership

Others

How do french corporations invest in Brazil?

Source:Ubifrance/ Crescendo Consultoria,

BRAZIL OUTLOOK, AGENDA

Brazil Today

Strategic Sectors

Foreign Investments

Cultural aspects

Cases of success and failure

Interim Management in Brazil

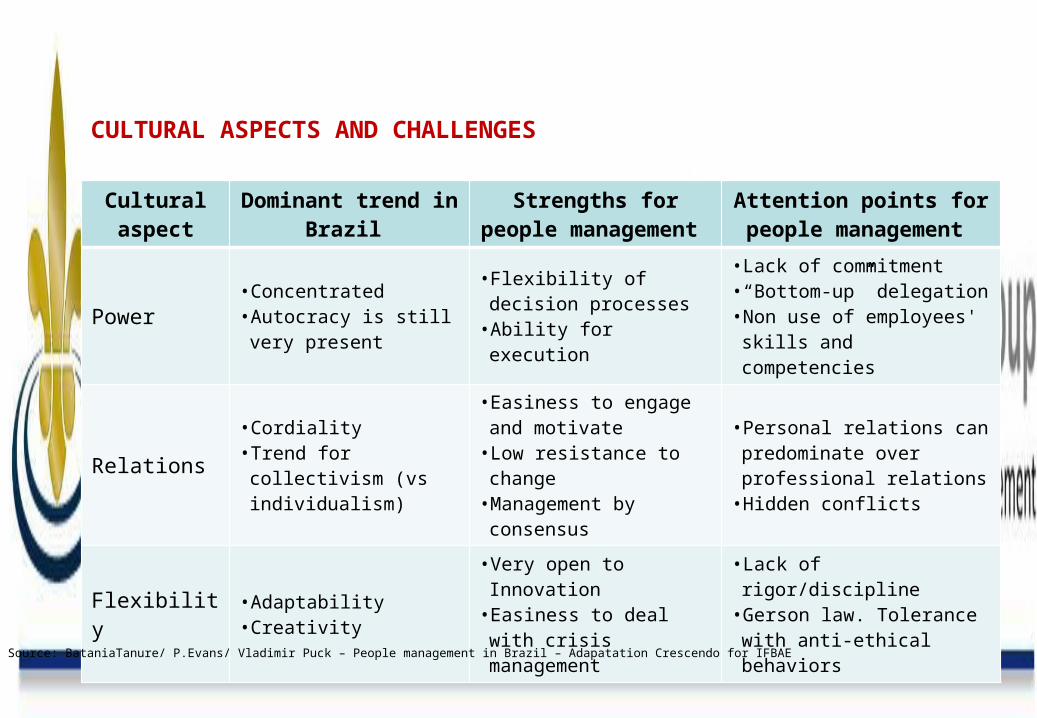

CULTURAL ASPECTS AND CHALLENGES

Cultural aspect

Dominant trend in Brazil

Strengths for people management

Attention points for people management

Power• Concentrated • Autocracy is still very present

• Flexibility of decision processes

• Ability for execution

• Lack of commitment• “Bottom-up” delegation• Non use of employees' skills and competencies

Relations • Cordiality• Trend for collectivism (vs individualism)

• Easiness to engage and motivate

• Low resistance to change• Management by consensus

• Personal relations can predominate over professional relations

• Hidden conflicts

Flexibility • Adaptability• Creativity

• Very open to Innovation • Easiness to deal with crisis management

• Lack of rigor/discipline• Gerson law. Tolerance with anti-ethical behaviors

Source: BataniaTanure/ P.Evans/ Vladimir Puck – People management in Brazil – Adapatation Crescendo for IFBAE

BRAZIL OUTLOOK, AGENDA

Brazil Today

Strategic Sectors

Foreign Investments

Cultural aspects

Cases of success and failure

Interim Management in Brazil

SUCCESS CASE: ACCOR BRASIL 1976 -2006

Latin America leader in Hotel industry

− 140 hotel – 25. 500 rooms

1st largest (LA and world) in services

− 4 million users/ day service tickets in Brazil

1st largest in Brazil for corporate meals

− 800.000 meals en 1.400 restaurants

1st largest in Latin America for business trips

− 1.000.000 passengers per year in Brazil

Source: Presentation Firmin Antonio CCFB 29/09/2010

1976

U$ 200.000

2006

Leader in all of its activities

SUCCESS CASE: ACCOR BRASIL 1976 -2006

2 decisive pillars for ACCOR success:

− A robust and rigorous strategic plan “Plan the future, to resist to periods of uncertainty, valuing people and team work,

and, above all, be always attentive to opportunities to continue investing to grow” To succeed in Brazil our company had to:

− THINK BIG− HAVE ROBUST BASE − BE CLIENT ORIENTED − BE MODERN AND FLEXIBLE− LIVE IN PERMANENT CHANGE

Adopted the Balanced Score Card as strategic tool

− A strong corporate culture The corporate culture makes the difference to motivate people Corporate project built on 3 pillars: Profit; Service; People (PSP) “Technology and products can be copied or bought, but culture is unique” “live a human adventure in the corporate adventure”

Source: Presentation Firmin Antonio CCFB 29/09/2010

− Thinking that the French ambassador could solve the principal questions of institutional relationship of the corporation in Rio

It took a very long time to understand the social context and to react against the phenomenon of “gatos” in Rio´s favelas that resulted in huge losses. Non Technical Losses (PNTs) went as far as representing 23 of total billing.

− Lack of corporate project and good management practices Old habits of the public owned Light were maintained (Lack of meritocracy) Lack of long term alignment of shareholders. It was a short-term opportunistic

alliance Organizational structure divided in bins

− Lack of preparation of key managers French expatriates unprepared for Brazilian cultural challenge.

Source: Crescendo presentation IFBAE

OTHER EXAMPLES OF SUCCESS OF FRENCH COMPANIES

1. Tropicalization of the offer 2. Long term vision

3.Penetration of historically closed markets 4.Tropicalization of the management

BRAZIL OUTLOOK, AGENDA

Brazil Today

Strategic Sectors

Foreign Investments

Cultural aspects

Cases of success and failure

Interim Management in Brazil

INTERIM MANAGEMENT IN BRAZIL

Consummer GoodsCommercial Juridical HR Director Financial Industrial President

Base salary 601.000 493.000 580.000 616.000 511.000 1.331.000Short term 392.000 240.000 367.000 410.000 307.000 1.483.000Long term 263.000 275.000 428.000 445.000 198.000 1.879.000Total remuneration 1.256.000 1.008.000 1.375.000 1.471.000 1.016.000 4.693.000

Capital IntensiveCommercial Juridical HR Director Financial Industrial President

Base salary 553.000 539.000 531.000 630.000 581.000 1.462.000Short term 332.000 398.000 333.000 371.000 329.000 1.263.000Long term 468.000 468.000 290.000 523.000 304.000 1.140.000Total remuneration 1.353.000 1.405.000 1.154.000 1.524.000 1.214.000 3.865.000

Infrastructure Commercial Juridical HR Director Financial Industrial President

Base salary 565.000 492.000 547.000 580.000 526.000 1.151.000Short term 384.000 315.000 287.000 391.000 331.000 1.165.000Long term 409.000 399.000 370.000 489.000 380.000 646.000Total remuneration 1.358.000 1.206.000 1.204.000 1.460.000 1.237.000 2.962.000

Chemical and PetrochemicalCommercial Juridical HR Director Financial Industrial President

Base salary 497.000 5.140.000 466.000 519.000 474.000 988.000Short term 315.000 470.000 315.000 414.000 232.000 867.000Long term 144.000 168.000 138.000 162.000 141.000 384.000Total remuneration 956.000 5.778.000 919.000 1.095.000 847.000 2.239.000

Services Commercial Juridical HR Director Financial Industrial President

Base salary 516.000 500.000 546.000 610.000 618.000 1.106.000Short term 318.000 459.000 313.000 431.000 250.000 1.166.000Lon term 354.000 330.000 325.000 424.000 88.000 1.208.000Total remuneration 1.188.000 1.289.000 1.184.000 1.465.000 956.000 3.480.000

Remuneration of six key executives functions per sector of actuation (in BRL)

“Are you ready for your Brazil Country Manager to earn more than the CEO

of the corporation?” Exame. Sept. 2011C

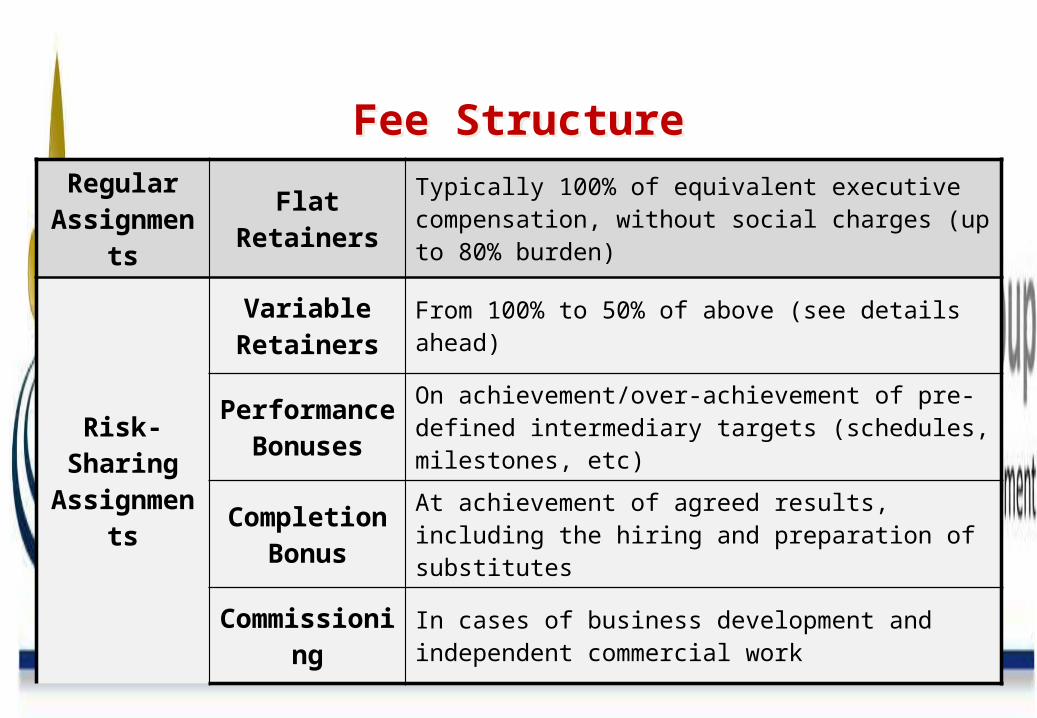

Interim management: The most cost efficient

solution for transition situations

Source: Exame Sept 2011

Corporate BackgroundCorporate Background

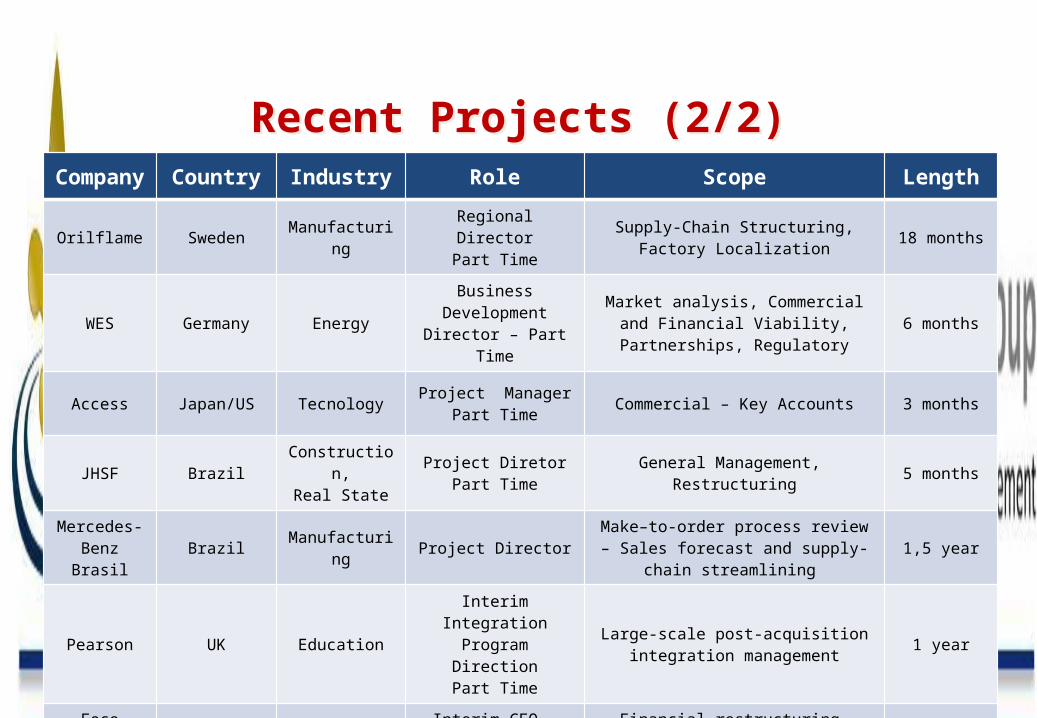

Recent Projects (1/2)Recent Projects (1/2)Company Country Industry Role Scope Length

Effortel Belgium Telecom Country ManagerPart Time Planning, Partnerships, Legal, Regulatory 1,5 year

MobileGlobe France Telecom Country ManagerPart Time

Planning, Partnerships, Legal, Regulatory, Operation Management 1 year

Proudfoot Consulting USA Consulting VP – Full Time Management, Sales 1 year

Credipar Brazil Financial Services

Interim CEO - Full TimeInterim CFO – Part Time

General Management, Restructuring, Financial processes, Funding

5 months7 months

AEC Canada Energy Business Development Director – Part Time

Market analysis, Commercial and Financial Viability, Partnerships, Financiang 1 year

Azevedo Brazil Manufacturing Consulting Part Time Market Development 6 months

Orilflame Sweden Manufacturing Regional DirectorPart Time