33

Fairchild Semiconductor International, Inc. October 2005 Investor Presentation

Fairchild SemiconductorInternational, Inc.

October 2005 Investor Presentation

2

Notes on Forward Looking Statements and Non-GAAP Measures

• Comments in this presentation other than statements of historical fact may constitute forward looking statements.

• Forward looking statements are based on Fairchild management’s estimates and projections and are subject to various risks and uncertainties.

• These risks and uncertainties are described in the Company’s periodic reports and other filings with the Securities and Exchange Commission (see the Business Risks section) and are available at http://www.sec.gov and investor.fairchildsemi.com.

• Actual results may differ materially from those projected in the forward looking statements.

• Some data in this presentation may include non-GAAP measures that we believe provide useful information about the operating performance of our businesses that should be considered by investors in conjunction with GAAP measures that we also provide. You can find a reconciliation of non-GAAP to comparable GAAP measures at the Investor Relations section of our web site at http://investor.fairchildsemi.com

Recent additions to our website at http://investor.fairchildsemi.comUpdated Financials (through 2005 Q3, with segment revenue/gross margin breakouts)

• Quarterly Fact Sheet with 2005 Q3 highlights

• This investor presentation

3

Fairchild: A Solid Foundation

• Market share leader in the $15B TAM power semiconductor market

• World-class silicon and packaging processes and capabilities

• MOSFET

• Analog

• Multi-chip packaging

• Global supply chain

• Worldwide customer base with tier 1 customers

• The employee talent to succeed

• Healthy balance sheet

4

Focus Areas for 2005

• Tune up the organization

• Clear responsibilities

• Strengthen management team

• Focus on distribution channel re-sales

• Incentives for distributors and our sales force now based on re-sales

• Selective programs to reduce slow moving inventory

• Operational changes get us 95% of the benefit

5

Focus Areas for 2005 (cont.)

• Get closer to the customer

• Strengthen technical sales…more FAE’s

• Senior management sponsors

• Increase investment in analog

• Shift spending to self-fund higher R&D

• Stronger management team

6

Focus Areas for 2005 (cont.)

• Focus on quality of business

• Rationalize product lines…identify products that do not meet our target gross margins

• Discontinue/divest low margin products as appropriate

• Plan for gradual phase out of low margin products as higher margin, new products ramp

www.fairchildsemi.com

Fairchild Overview

8

Colorado Springs, COAnalog Design

Mountaintop, PAWafer Fab

South Portland, MEHeadquarters, WaferFab, North AmericanSales Headquarters

Wootton Bassett, EnglandEurope Sales Headquarters

Penang, MalaysiaAssembly and Test

Bucheon, South KoreaWafer FabKorea Sales Headquarter

Suzhou, ChinaAssembly and Test

Irving, TXCustomer ServiceCenter

Salt Lake City, UTWafer Fab

San Jose, CAAnalog & Discrete Design

Hong KongAsia-Pacific SalesHeadquarters

Tokyo, JapanJapan Sales Headquarters

SingaporeAsia Ops MgmtWafer Fab

Cebu, PhilippinesAssembly and Test

Geographic Footprint Overview

Regional Sales Headquarters,Customer Service Centers

Product Group and Design Centers,Manufacturing Locations

- 2004 sales: $1.6 billion

- 9000 employees worldwide

- 8 production facilities and 5 customer service centers

- 36 direct sales offices in 17 countries

9

Fairchild Semiconductor Overview

Power Analog/Std Linear

Power Discrete

All Other

High Performance Multi-Market Products

Memory

Processing

ASIC/SystemOnChip $29.2B$68.2B

$47.3B

$67.7B

$212.4B Semi TAM 2004

Source: WSTS, January, 2005

Fairchild’s 2004Served Available Market ~ $29.2B

Fairchild Q3 2005 Product Mix

Standard Products

26%

Power Discrete

56%Power Analog

18%

10

Source: Fairchild internal estimates

24%

14%

14%5%

24%

5%14%

: Computing

Industrial:Other

Consumer

Industrial:Power Supplies,

Adaptors

Cellular Handsets, Base StationsCentral Office SwitchesWireless NetworkingRouters/Hubs CD/DVD Players

Game ConsolesTV’s, VCRs, Set Top Boxes

PDA’s, MP3’s, CamerasWhite Goods, Appliances

Flat Panel DisplaysMonitors, CRTs

Desktops NotebooksDisk DrivesPrinters, CopiersMemory Modules

Power SuppliesDC-DC Power Bricks

Power AdaptorsVoltage Regulator Modules

Ignition, Engine ManagementEntertainmentBody ElectronicsNavigation, Safety

Displays

Communications

Auto

Factory AutomationATE, InstrumentationLighting, MedicalMotor Control

2005 Q3 Sales by End Market Segment

11

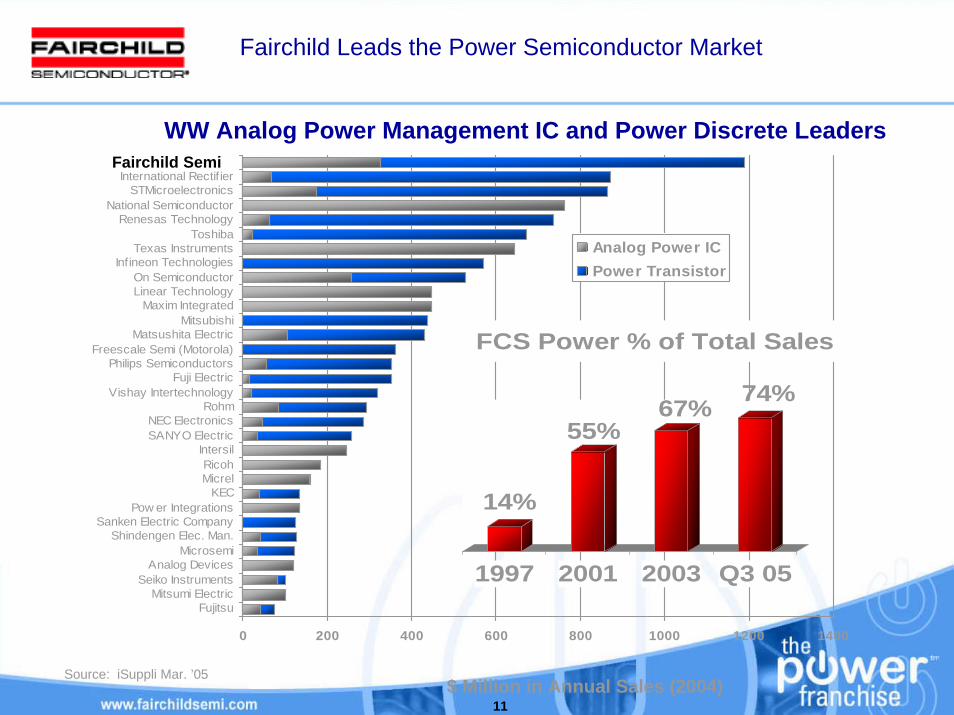

Fairchild Leads the Power Semiconductor Market

WW Analog Power Management IC and Power Discrete Leaders

0 200 400 600 800 1000 1200 1400

FujitsuMitsumi Electric

Seiko InstrumentsAnalog Devices

MicrosemiShindengen Elec. Man.

Sanken Electric CompanyPow er Integrations

KECMicrelRicoh

IntersilSANYO ElectricNEC Electronics

RohmVishay Intertechnology

Fuji ElectricPhilips Semiconductors

Freescale Semi (Motorola)Matsushita Electric

MitsubishiMaxim Integrated

Linear TechnologyOn Semiconductor

Infineon TechnologiesTexas Instruments

ToshibaRenesas Technology

National SemiconductorSTMicroelectronics

International Rectif ier

Analog Power ICPower Transistor

Source: iSuppli Mar. ’05$ Million in Annual Sales (2004)

14%

55%67% 74%

1997 2001 2003 Q3 05

FCS Power % of Total Sales

Fairchild Semi

www.fairchildsemi.com

Increasing the Quality of Business

13

Integrate power functions into single package solutions

Requires competencies in end market applications, power switch & analog control design, and advanced packaging

Degree of integration is also a function of the potential market size

Benefits to Our Customers• Shorter design-in cycle

• Lower system costs

• Less components – higher reliability

• Leverage our power systems expertise

Benefits to Fairchild• Shorter time to market

• Save silicon & packaging costs by optimized product design

• High barrier of entry

• Improves return on our R&D investment

Power Remains a Key Target MarketHigher Levels of Integration Drive Increased Margins

14

Increased Functionality in Power Solutions

Power Applications& System Knowledge

Control ICTechnology

Power DiscreteTechnology

PackagingTechnology

CustomerRelationships

Inputs OutputDecision MakingThought Process

System Partioning

Silicon Technology

Packaging Technology

Cost Tradeoff Analysis

Development Timing

Value Analysis

Application Size& Growth Rates

•Self Contained PowerBuilding BlockFunctions

•Extensible AcrossMarkets and Products

•High Customer Value

•Cost-Effective

•High Volume

Fairchild is One of a Few Power Semiconductor Companies,Worldwide, To Offer this Unique Mix of Capabilities Across

A Broad Range of Markets, Products, and Applications

15

Smart Power Modules (SPM™)

• Line-up : 600V / 1A, 2A, 3A, 5A, 10A, 15A, 20A, 30A • Low Thermal Resistance by Ceramic-based TMT Package• 2500V/1min Isolation and

1500V/1min Isolation • Built-in Thermistor (NTC)• For inverter high-side IGBTs

- Gate driving circuit (HVIC)- Control supply under-voltage

protection• For inverter low-side IGBTs

- Gate driving circuit- Short-circuit protection using sense-IGBTs

using external shunt - Control supply under-voltage protection

• Input interface: 5V/3.3V CMOS/LSTTL compatible • Vector control correspondence due to 3-N terminals

SPM : 60 x 31(mm)

SPM : 44 x 26.8(mm)

SPM : 29 x 12(mm)

Optimized for Motion Control

16

Application: Brushless DC Fan motor controllers for air conditioners and air cleaners

Features: • SPM + Control IC(ASIC) + Hall IC • Low Cost & High Performance, 180° Control • Motion sensors can be eliminated

SPM™ Success – Air Conditioning Fan Drivers

0.5 inch

From 3.5” to 2.5”Motor housing

PCB area reduced by 50% Motor enclosure size reduced by 20%

17

SPM™ Success - Switch Reluctance Motors (SRM) Vacuum Cleaner Drivers

Heat Sink Circuit Bd. SR Motor Built-in InverterSRM

Application: SRM vacuum cleaner controllers

Features: • SPM + micro-controllers• High reliability and high performance• High thermal characteristic, SC, UV protection functions

SRM delivers 50% more vacuum for the same space

18

SPM™ Success - White Goods

Assembling these parts might increase manufacturing time and cause low yields.

Protection circuit using analog components cause time delay and noise.

3-HVICs 1-LVICs

SPM’s built-in HVIC and LVIC with protection

circuit

SPM, which integrates all diverse components, enhances productivity while simplifying manufacturing

6-IGBTs

Fairchild’s SPM simplifies design through an integrated inverter-controlled variable speed driver for 3-phase induction motors, low power brushless dc (BLDC) motors, and switched reluctance motors.

Design Considerations

Manufacturing Impact

Integration of system components

19

Fairchild Green FPS

Green FPS Growth

0%

50%

100%

2003 2004

YoY

Gro

wth

(%)

• Integrated SenseFET and PWM IC Switches that meet low standby power regulations, simplify designs, reduce EMI emissions, and lowers costs

20

Fairchild is Also Committed to Developing Leadership Analog Signal Path Products

Source; iSupply, WSTS

Amplifiers $2.7B

Regulators $5.4B

Data Converters

$2.1B

Interface $2.0B

High Performance Analog $12.2B - 2004

Amplifiers $3.3B

Regulators $11.5B

Data Converters

$3.0B

Interface $2.8B

High Performance Analog $20.6B - 2009

14% CAGR

21

Fairchild Video Filters

• Video filters and drivers with superior integration enabling customers to reduce components count and bill of materials

Video Filter Growth

0%

35%

70%

2003 2004

YoY

Gro

wth

(%)

22

Fairchild Analog Switches

Analog Switch Growth

0%

25%

50%

2003 2004

YoY

Gro

wth

(%)

• Fairchild’s Analog Switches provide the best combination of low resistanceswitching and ultra-small packaging

23

Fairchild LED Drivers

• LED Drivers with high efficiency to maximize battery life in space efficient MLP packaging for ultra-portable applications

24

Fairchild uSerDesTM(micro serializers and deserializers)

• µSerDes™ is a proprietary serialization/ deserialization solution designed for use in portable products

Features:

uSerDes is 1/7 the size, 1/10 active power and 1/4000 standby power, and significantly less EMI than conventional SerDes solutions

Benefits:

uSerDes technology can enable reduction is system size, system cost, and faster Time to Market

www.fairchildsemi.com

Financials

26

Setting a New Direction for the Future Supporting Our Shift to Higher Value Products

• Adjust the business model to support our shift to more complex products

• Focus on internal metrics to measure progress…ROIC, distribution POS measures, margin optimization at the factory level

• Continue to generate strong cash flow to invest in the business, fund acquisitions and further de-lever

27

Gross Margin Improvement Plan

Drive ~30% gross margins at current sell-through revenue levels

• Increase utilization rate as inventories reach target…sell-in = sell-through…400 – 600 bps impact

• Lower capex and D&A expense…eventual 300 – 350 bps impact in Q1 05

Achieve mid-30’s gross margins on >50% fall-through in <24 months

• Reduce capex…lower D&A

• Aggressive margin/mix management

• Closer alignment of distribution sales in to sales out

• Cut infrastructure costs (Operations, IT)

• Sharpen focus on R&D spending

• Increase % of sales from new products

• Increase analog and power % of sales

• Possible divest/exit low margin products

28

Adjusting the Capital Expenditure Model

Leverage last 5 years of investments to reduce capex and D&A for at least the next few years

Capex % of Sales

0.00%

10.00%

20.00%

2000 2001 2002 2003 2004 2005+

6 – 8%

29

Sales Grow at or above the power market

Gross Margin Improving steadily to the mid-30’s & beyond

R&D Shift more spending to analog…gradual increase as percentage of sales

SG&A Shift spending from G&A to Selling...more technical support (FAE’s, design centers, etc.)

Capex Reduce capex to 6 - 8% of sales or lower

Utilization & Lead Times Maintain stable, shorter lead times on higher value focus products

Increasing Product ValueImplications to the Business Model

30

Q3 2005: Turning the Corner

• Demand was seasonally stronger…bookings up, sales flat QoQ…building backlog again

• Significant reduction in inventories again in Q3

• Distributors’ inventories reduced more than 1 week on higher re-sales

• Reduced internal inventories more than 11% from the prior quarter

• Pro forma gross margins were 21%, up 110 bps QoQ due primarily to lower depreciation expenses

• Utilization increased slightly to low-80%...lead times were up about a week to 6 – 8 weeks on average

• Bookings were strongest for products serving the computing and consumer end markets…especially for notebook, TV and DVD applications

• Record analog switch sales and bookings…sales up >40% QoQ

31

Strong Balance Sheet ManagementNet Debt <$150M…Lowest in our history

($ in millions) 9/25/2005 12/30/2001

Cash, marketable investments $504.6 $504.4

Total debt: $180M Revolver 0.0 0.0 $450M Term B Loan 447.7 0.0

10 1/8% notes due 3/07 0.0 285.010 3/8% notes due 10/07 0.0 300.010 1/2% notes due 2/09 0.0 350.05% Converts due 11/08 200.0 200.0Other 0.0 3.6Total debt $647.7 $1,138.6

Shareholders' equity $1,008.7 $808.0Debt / Equity 0.6x 1.4x

32

Forward Guidance

• We expect revenues to increase about 5% sequentially

• Gross margins forecast to increase 200 –300 bps sequentially

33

Fairchild: Setting a New Direction

• Build on our strengths…silicon and packaging processes, operations, worldwide customer base…

• New product execution…customer and application focus

• Adjust the business model to support a higher value business

• Continue reducing debt and lowering interest expense…strong cash flow