Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink. FPI_FAIS Compliance and Risk Management guide Page 1 of 15 FAIS Compliance and Risk Management Disclaimer This document serves as a mere guide and should not be used as the definitive and only source of information for advising a client and implementing any processes in your practice. Your due diligence must be done. The Financial Planning Institute (FPI) will not accept any liability that may arise out of the use of this document, consultation must be sought from a relevant expert. Request for comment This is an evolving document and therefore we do encourage constructive input. The next update is scheduled for 2015. We welcome comments from members and other stakeholders. These comments will be used to assess the Guide’s usefulness and to improve it prior to publishing another version. Please submit your comments to [email protected]FAIS licensing and requirements An FSP (Financial services provider) needs to obtain a licence if they will be rendering advice or intermediary services in terms of the FAIS Act. An individual carrying out the functions of an FSP needs to be authorised by the Registrar to act in that capacity. Section 8 provides details of the application for authorisation to act as an FSP. The registration process noted below is taken from the FSB website under New License Applications: Procedures to obtain a license o The call centre will be able to provide you with and electronic application form. (FSB call centre number 0800 110 443) o An FSP number will be allocated to you after submission of the application forms to the FSB. o The required fee must be paid prior to submission of the forms and proof of payment must accompany the application form. o Read the instructions on each form before completing the relevant forms and if required, make copies of the pages needed. o FSP 14A must be completed in full and be signed by the responsible person. o The applicant must appoint a compliance officer if it will have more than one key individual or representatives. o If an application for the approval of a compliance practice and/or officer (Form FSP 13) is not attached to your application, please ensure that your Compliance Officer is already approved as a Compliance Officer. Application form for financial services providers

Transcript

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 1 of 15

FAIS Compliance and Risk Management

Disclaimer

This document serves as a mere guide and should not be used as the definitive and only source of

information for advising a client and implementing any processes in your practice. Your due

diligence must be done. The Financial Planning Institute (FPI) will not accept any liability that may

arise out of the use of this document, consultation must be sought from a relevant expert.

Request for comment This is an evolving document and therefore we do encourage constructive input. The next update is scheduled for 2015. We welcome comments from members and other stakeholders. These comments will be used to assess the Guide’s usefulness and to improve it prior to publishing another version.

An FSP (Financial services provider) needs to obtain a licence if they will be rendering advice or

intermediary services in terms of the FAIS Act.

An individual carrying out the functions of an FSP needs to be authorised by the Registrar to act in

that capacity.

Section 8 provides details of the application for authorisation to act as an FSP. The registration

process noted below is taken from the FSB website under New License Applications:

Procedures to obtain a license o The call centre will be able to provide you with and electronic application form.

(FSB call centre number 0800 110 443) o An FSP number will be allocated to you after submission of the application forms to

the FSB. o The required fee must be paid prior to submission of the forms and proof of payment

must accompany the application form. o Read the instructions on each form before completing the relevant forms and if

required, make copies of the pages needed. o FSP 14A must be completed in full and be signed by the responsible person. o The applicant must appoint a compliance officer if it will have more than one key

individual or representatives. o If an application for the approval of a compliance practice and/or officer (Form FSP

13) is not attached to your application, please ensure that your Compliance Officer is already approved as a Compliance Officer.

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 2 of 15

Applying through the FSB directly:

The application is available in Word format, and can be obtained from our Contact Centre. A reference number will be issued to you as soon as you submit your application form to the FSB. (Please note that this number is not your FSP approved license number; it’s a temporary reference no. to record your enquiry and procedure of application.”

Applicants are requested to adhere to the numerical order of the document when filling out the forms.

1. FSP 1 - Business Information of Financial Services Provider

2. FSP 2 - Licence categories

3. FSP 3 - Directors, officers and applicable shareholders

4. FSP 4 - Key individuals / Applicant Sole proprietor

5. FSP 5 - Representatives

6. FSP 6 - Compliance officer of FSP

7. FSP 7 - Operational ability

8. FSP 8 - Financial soundness

9. FSP 9 - External auditor 10. FSP 10 - Nominee company or independent custodian of discretionary or

administrative FSP 11. FSP 11 - Clearing firm or foreign forex services provider of forex services provider

12. FSP 12 - Application for specific exemptions

13. FSP 13 - Application for the approval of a compliance officer (separate form)

14. FSP 14 - Attachments, list of all completed forms and declarations

15. FSP 15 - Hedge fund Application form

Prior to applying for a licence the business should already be registered with CIPC, SARS and a bank

account opened. This information will be required when completing the forms.

It is only the FSP that applies for registration as per the licence categories. The Key Individual,

Representative and compliance office work for the FSP and do not have to apply for registration,

however, the FSP is obliged to inform the FSB of the names and contact details of the individuals

mentioned. Representatives must be registered within 15 days of appointment, further all changes

must be reported to the in the same time frame, and it is important for the FSP to ensure that they

receive confirmation from the Registrar that the update has been effected.

The information you would have documented in your business plan would come in handy when

completing the forms pertaining to operational ability and financial soundness.

Applications may be submitted directly to the FSB or through a recognised representative body.

All FSPs, key individuals, compliance officers and representatives must comply with the

relevant fit and proper requirements before a licence will be granted by the FSB.

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 3 of 15

The Fit and Proper requirements (Board Notice 106 of 2008)

Honesty and Integrity requirements that are applicable to all FSPs, key individuals, representatives and compliance officers:

This is in terms of section 2(1) of Board Notice 106. In deciding on whether the individual is in fact honest and has integrity the registrar may refer to any information in their possession or if such information is brought to their attention. The individual has a fiduciary duty towards the client. S3 (a) lists various actions that would equate to contrary behaviour.

Competency requirements that consist of experience and qualification requirements that are applicable to all FSPs, key individuals and representatives:

Experience

Table a: category I experience requirements for an FSP and representative

Subcategory

Advice:

Minimum Experience

Service:

Minimum Experience

1.1 Long-term Insurance subcategory A 6 months 2 months

1.2 Short-term Insurance Personal Lines 1 year 6 months

1.3 Long-term Insurance

1.3.1 subcategory B1 1 year 6 months

1.3.2 subcategory B2 1 year 6 months

1.4 Long-term Insurance subcategory C 1 year 6 months

1.5 Retail Pension Benefits 1 year 6 months

1.6 Short-term Insurance Commercial Lines 1 year 6 months

1.7 Pension Fund Benefits 1 year 6 months

1.8 Securities and instruments: Shares 2 years 1 year

1.9 Securities and Instruments: Money market instruments

2 years 1 year

1.10 Securities and Instruments: Debentures and securitised debt

2 years 1 year

1.11 Securities and Instruments: Warrants, certificates and other instruments acknowledging debt

2 years 1 year

1.12 Securities and Instruments: Bonds 2 years 1 year

1.13 Securities and Instruments: Derivative instruments excluding warrants

2 years 1 year

1.14 Participatory Interests in one or more collective Investment schemes

1 year 1 year

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 4 of 15

1.15 Forex Investment Business 2 years 1 year

1.16 Health Service Benefits 2 years 2 years

1.17 Long-term Deposits 6 months 3 months

1.18 Short-term Deposits 6 months 3 months

1.19 Friendly Society Benefits 6 months 2 months

Table b: category II experience requirements for FSP and representative

Subcategory

Minimum Experience

2.1 Long-term Insurance

2.1.1 subcategory B1 2 years

2.1.2 subcategory B2 2 years

2.2 Long-term Insurance subcategory C 2 years

2.3 Retail Pension Benefits 2 years

2.4 Pension Fund Benefits 2 years

2.5 Securities and Instruments: Shares 3 years

2.6 Securities and Instruments: Money market instruments 3 years

2.7 Securities and Instruments: Debentures and securitised debt

3 years

2.8 Securities and Instruments: Warrants, certificates and other instruments acknowledging debt

3 years

2.9 Securities and Instruments: Bonds 3 years

2.10 Securities and Instruments: Derivative instruments excluding warrants

3 years

2.11 Participatory interests in one or more collective investment scheme

2 years

2.12 Forex Investment Business 3 years

2.13 Long-term deposits 1 year

2.14 Short-term deposits 1 year

(Taken from the Financial Services Board’s website [FSB])

Qualifications

Transitional period prior to 2009

Date of First Appointment(DOFA) Date by which qualifications must be obtained

KI’s approved and Reps appointed up to 2007 30 or 60 credits, depending on licence category, in a registered skills programme by 31/12/2009

KI’s approved and Reps appointed in 2008 and 2009

OPTIONS:

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 5 of 15

1. Qualification as defined in Board Notice 106 of 2008, Part 10(1) consisting of 30 or 60 credits (as above), by 31/12/2011; or

2. A Full Qualification as recognised by the Registrar by31/12/2013

New entrants from January 2010 onwards

KI’s approved in 2010 Recognised qualification as per the list of recognised qualifications in order to be approved as KI.

Reps appointed in 2010 under Supervision Entry level Matric /Grade 12 or School leaving certificate @ NQF level 4 (Excluding Cat 1.1 and 1.19 – minimum ABET Level 1)

A representative may only work for a period not exceeding six (6) years after date of first appointment under supervision, whilst obtaining the required experience, regulatory examination and recognised qualification as they apply.

List of recognised qualifications

List No.

List Name

List 1 Qualifications recognised for Category I FSPs

List 2 Specified subject(s) / module(s) / unit standard(s) based qualifications recognised for Category I FSPs

List 3 Qualifications recognised for Category I FSPs for the transitional period only

List 4 Qualifications recognised for Category II and IIA FSPs

List 5 Qualifications recognised for Category III FSPs

List 6 Qualifications recognised for Category III FSPs for the transitional period only

List 7 Qualifications recognised for Category IV FSPs

List 8 Specified subject(s) / module(s) / unit standard(s) based qualifications recognised for Category IV FSPs

List 9 Qualifications recognised for Category IV FSPs for the transitional period only

List 10 Qualifications recognised for Category II and IIA FSPs for the transitional period only

List 11 Specified subject(s) / module(s) / unit standard(s) based qualifications recognised for Category II and IIA FSPs

List 12 Specified subject(s) / module(s) / unit standard(s) based qualifications recognised for Category III FSPs

List 13 Qualifications recognised for Compliance Officers

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 6 of 15

List of appropriate subjects KIs and Reps The following subjects are deemed to meet the requirements for appropriateness, and will be used in combination with the list of generic qualifications as approved by the Registrar. “Generic qualification “means a qualification that addresses knowledge, skills and competence that are broadly applicable to the financial services industry, without addressing any specific type of narrow specialisation relating to a specific subcategory; “Specific qualification “means a qualification that addresses specific and/or specialised knowledge, skills and competence that is applicable to the financial services industry, and may address a specific type of specialisation and/or subcategory in the financial services industry;

Strategic Management Strategic Management Mercantile law

Taxation Taxation Network administration

Taxation law Taxation law Process Management (Process Modelling and Control)

Wealth management Wealth management Programming

Risk Management

Services Marketing

Statistics

Strategic Communication

Management Skills

Strategic Marketing

Strategy

Taxation

Taxation law

Wealth management

List of appropriate subjects for compliance officers

Subjects

Accounting Financial Planning

Auditing Financial/Securities Markets

Business Assurance Fraud Risk Management

Accounting Financial Planning

Auditing Financial/Securities Markets

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 8 of 15

Business Assurance Fraud Risk Management

Business Economics Health Care Benefits

Business Environment Informatics

Business Finance Insurance

Business Information Systems Interpretation of Statutes

Business Integration Law of Contract or Delict

Business Management Legal Environment

Commercial Law Mercantile Law

Companies Law Money Laundering Control

Compliance Management Network Administration

Computer Architecture Process Management (Process Modeling and Control)

Corporate Finance Retirement Planning

Corporate Governance Risk Management

Estate and Trust Law Strategic Communication Management Skills

Estate planning Strategic Management

Finance Strategy

Financial Management Wealth Management

[Taken from the FSB website]

The application forms and pathway can be obtained from the FSB website.

Regulatory Exams

These examinations are compulsory for anybody rendering financial services to a client.

List of Level 1 Regulatory Examinations (currently available)

Re No:

Regulatory Examination

Descriptor

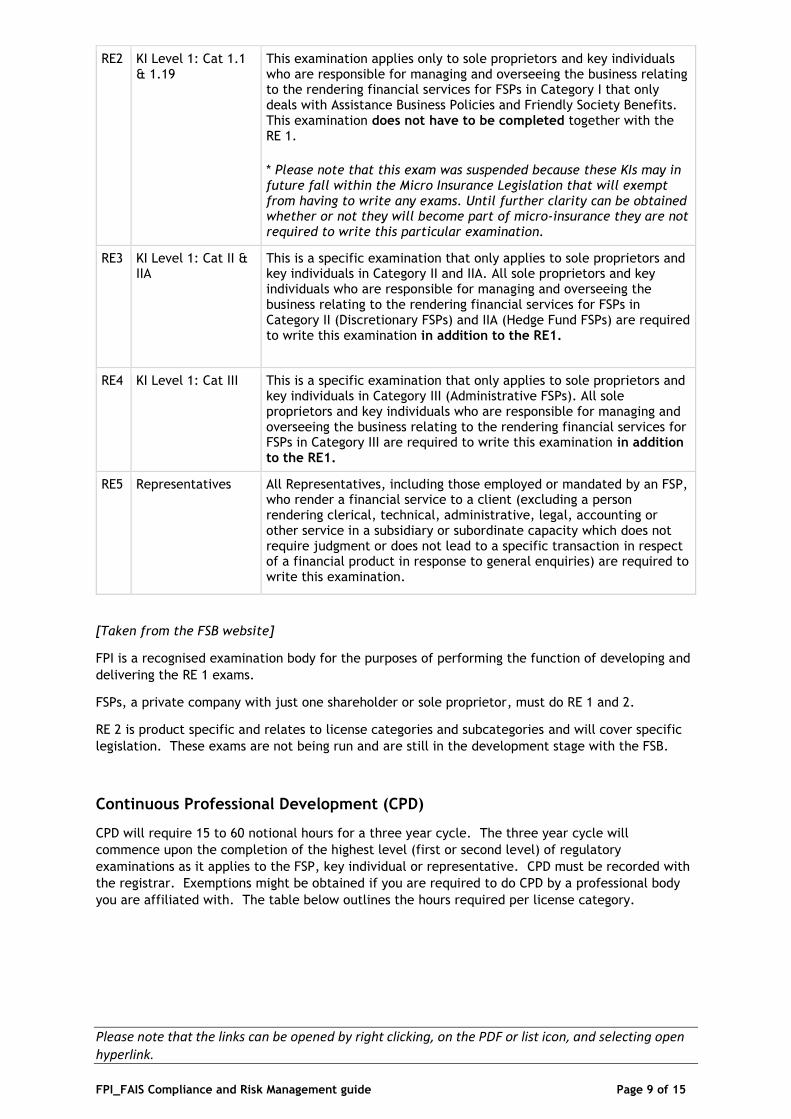

RE1 KI Level 1: Cat I, II, IIA, III and IV (General)

This is a general examination that applies to all key individuals and sole proprietors in all the Categories. This examination consists of 80 questions. All sole proprietors and key individuals who are responsible for managing and overseeing a business relating to the rendering financial services for FSPs in Category I, II, IIA, III and IV are required to write this examination.

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 9 of 15

RE2 KI Level 1: Cat 1.1 & 1.19

This examination applies only to sole proprietors and key individuals who are responsible for managing and overseeing the business relating to the rendering financial services for FSPs in Category I that only deals with Assistance Business Policies and Friendly Society Benefits. This examination does not have to be completed together with the RE 1.

* Please note that this exam was suspended because these KIs may in future fall within the Micro Insurance Legislation that will exempt from having to write any exams. Until further clarity can be obtained whether or not they will become part of micro-insurance they are not required to write this particular examination.

RE3 KI Level 1: Cat II & IIA

This is a specific examination that only applies to sole proprietors and key individuals in Category II and IIA. All sole proprietors and key individuals who are responsible for managing and overseeing the business relating to the rendering financial services for FSPs in Category II (Discretionary FSPs) and IIA (Hedge Fund FSPs) are required to write this examination in addition to the RE1.

RE4 KI Level 1: Cat III This is a specific examination that only applies to sole proprietors and key individuals in Category III (Administrative FSPs). All sole proprietors and key individuals who are responsible for managing and overseeing the business relating to the rendering financial services for FSPs in Category III are required to write this examination in addition to the RE1.

RE5 Representatives All Representatives, including those employed or mandated by an FSP, who render a financial service to a client (excluding a person rendering clerical, technical, administrative, legal, accounting or other service in a subsidiary or subordinate capacity which does not require judgment or does not lead to a specific transaction in respect of a financial product in response to general enquiries) are required to write this examination.

[Taken from the FSB website]

FPI is a recognised examination body for the purposes of performing the function of developing and

delivering the RE 1 exams.

FSPs, a private company with just one shareholder or sole proprietor, must do RE 1 and 2.

RE 2 is product specific and relates to license categories and subcategories and will cover specific

legislation. These exams are not being run and are still in the development stage with the FSB.

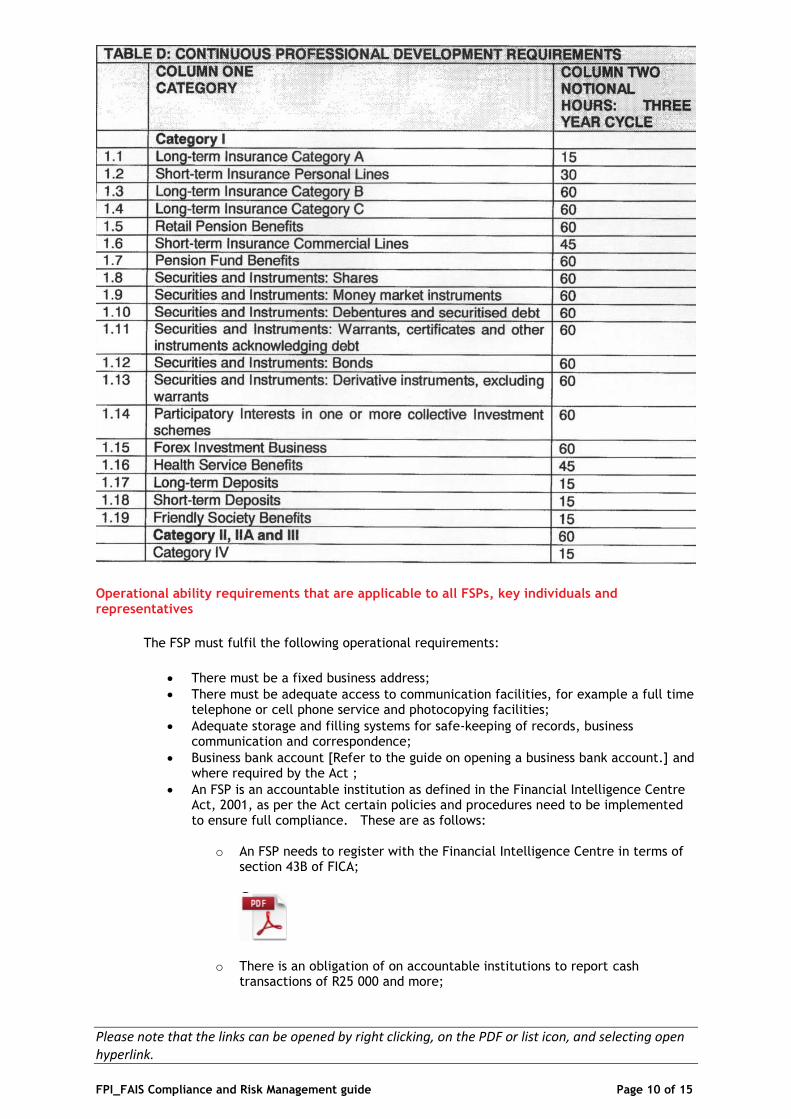

Continuous Professional Development (CPD)

CPD will require 15 to 60 notional hours for a three year cycle. The three year cycle will

commence upon the completion of the highest level (first or second level) of regulatory

examinations as it applies to the FSP, key individual or representative. CPD must be recorded with

the registrar. Exemptions might be obtained if you are required to do CPD by a professional body

you are affiliated with. The table below outlines the hours required per license category.

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 10 of 15

Operational ability requirements that are applicable to all FSPs, key individuals and representatives

The FSP must fulfil the following operational requirements:

There must be a fixed business address;

There must be adequate access to communication facilities, for example a full time telephone or cell phone service and photocopying facilities;

Adequate storage and filling systems for safe-keeping of records, business communication and correspondence;

Business bank account [Refer to the guide on opening a business bank account.] and where required by the Act ;

An FSP is an accountable institution as defined in the Financial Intelligence Centre Act, 2001, as per the Act certain policies and procedures need to be implemented to ensure full compliance. These are as follows:

o An FSP needs to register with the Financial Intelligence Centre in terms of section 43B of FICA;

o There is an obligation of on accountable institutions to report cash transactions of R25 000 and more;

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 11 of 15

o Preventing, detecting, monitoring and reporting confirmed, suspected, detected or prevented money laundering;

o Client identification and verification (copy of ID and proof of address); o Record keeping (this is also a requirement of FAIS and is discussed in more

detail below.); o Money laundering control training (Compliance will ultimately be the

responsibility of the key individual), however, staff members should also be aware of the requirements. Make sure that there are proper policies in place;

o Monitoring of accounts, activities, policies, procedures and plans.

There must be detailed service level agreements if an FSP outsources administrative or system functions to a third party;

Internal control structures (proper procedures and controls must be in place:

o Segregation of duties, roles and responsibilities where necessary; o Access Control; o Access rights and electronic data security; o Physical security of the providers assets and records; o Policies relating to business process, policies and controls and technical

requirements; o System application testing; o Disaster recovery and back-up procedures on electronic data; o Appropriate training for all key individuals and/or representatives regarding

the requirements of the Act; o A business continuity plan [The below link will take you to the FPI

Resources Centre, under Risk Committee portal, where you will find a template for a Business Continuity Plan and a template for an agreement with another FSP which allows for business continuity.];

A registered private company will continue irrespective of the shareholder or key individual. These individuals will have to be replaced in anything was to happen.

o Proper systems controls and compliance measures and to record all financial and systems procedures;

o Data Integrity; o Professional indemnity or fidelity insurance cover; o A key individual, in respect of an FSP, must have and be able to maintain

the operational ability to fulfil the responsibilities imposed by the Act on FSPs, including oversight of the financial services (regarding the giving of advice and rendering of intermediary services) provided by the representative of the FSP.

A lot of the operational requirements noted above relate to data integrity. Apart from the FAIS Act, there are more stringent requirements imposed by the Protection of Personal Information Act, these must be taken cognisance of in risk mitigation and the protection of client information. A guide to the Protection of Personal Information Act has been prepared for members.

Solvency requirements that are applicable to the FSP (Financial Soundness)

Please note that the links can be opened by right clicking, on the PDF or list icon, and selecting open hyperlink.

FPI_FAIS Compliance and Risk Management guide Page 14 of 15

Compliance Officer

FSPs are responsible for compliance with the legislation, it is not the responsibility of the compliance officer. The key individual is responsible to ensure compliance with the FAIS Act and representatives also have specific responsibilities in respect thereof. The compliance officer is responsible for the monitoring of compliance only.

Section 17 (4) of the FAIS Act requires that a compliance officer or, in the absence of such officer, the authorised financial services provider concerned, must submit compliance reports to the registrar.

In the case of a sole proprietor who has not appointed any representatives or a second key individual, the annual compliance report must be completed and submitted by the sole proprietor.

Where the FSP has appointed a compliance officer, the report must be completed and submitted by the compliance officer (the key individual is still required to review the completed compliance report and sign the declaration attached to the report).

The FSB has to approve the compliance officer appointed by the FSP.

The compliance report must be submitted annually. The compliance report comprises of a questionnaire that is prepared by the FSB. The compliance report can be submitted in “hard copy” or online. Under the heading Supervision Department select the compliance reports option. The reporting date is dependent on the type of license that was granted. If an FSP has more than one licence only one report needs to be submitted.

An FSP that has just been authorised when the reporting period is due, is required to still submit a fully completed report. The FSP can indicate on the compliance report that it has just been authorised. The FSP must state what actions are being taken to ensure that they will be fully compliant by the next reporting period.

Submission of Financial Statements

FSPs need to submit financial reports (section 19(2) of the FAIS Act) in order for the FSB to

ascertain if they still meet the financial soundness requirements in terms of the Fit and Proper

Requirements (BN 106 of 2008).

There are a number of exemptions that apply regarding the submission of financial statements:

Board Notice 85 of 2004 – only applies to Category I FSPs that are funeral parlours and

collect client’s premiums;

Newly authorised FSPs must, if you a company, provide a letter from the external auditor

stating the background and reasons for lack of business activity.

The financial statements must be submitted within four months after the FSPs financial year end.

The financial statements can be submitted by hand, posted or submitted online.

For more information on submission of statutory returns click here.