FATCA Highlights FATCA Final Regulations Released Translating Aspects of the 544 Pages into Business As Usual Processes Released February 2013 Volume 8 By Ellen Zimiles, Jeffrey Locke, Richard Kando and Courtland Hillman GLOBAL INVESTIGATIONS & COMPLIANCE

Transcript

FATCA Highlights FATCA Final Regulations Released Translating Aspects of the 544 Pages into Business As Usual Processes

Released February 2013 Volume 8

By Ellen Zimiles, Jeffrey Locke, Richard Kando and Courtland Hillman

G L O B A L I N V E S T I G A T I O N S & C O M P L I A N C E

FATCA HIGHLIGHTS | VOLUME 8

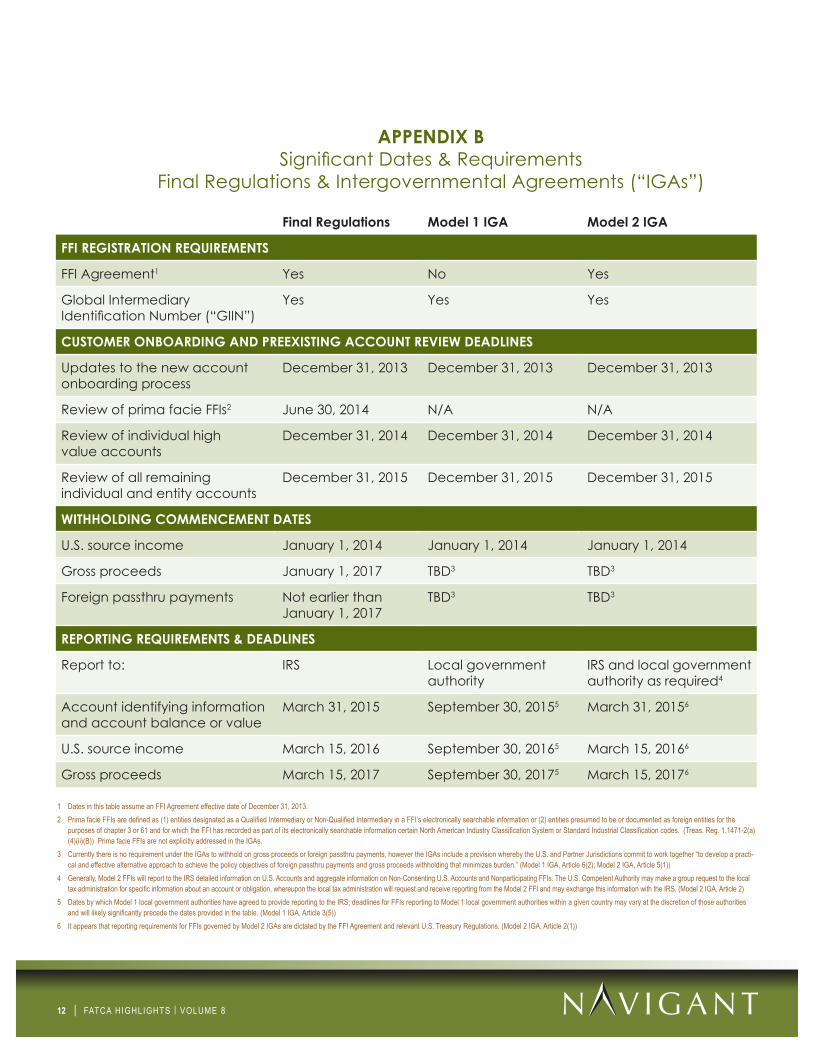

TABLE OF CONTENTS

I. Introduction..............................................................................................................................................1

II. Overview of FATCA........................................................................................................................................................................1

III. Registration Process........................................................................................................................................................................2

IV. Pre-Existing Account Analysis........................................................................................................................................................2

V. On-boarding of New Accounts....................................................................................................................................................7

VI. Reporting...........................................................................................................................................................8

VII. ResponsibleOfficerCertification&Governance.......................................................................................................................9

VIII. Conclusion.................................................................................................................................................10

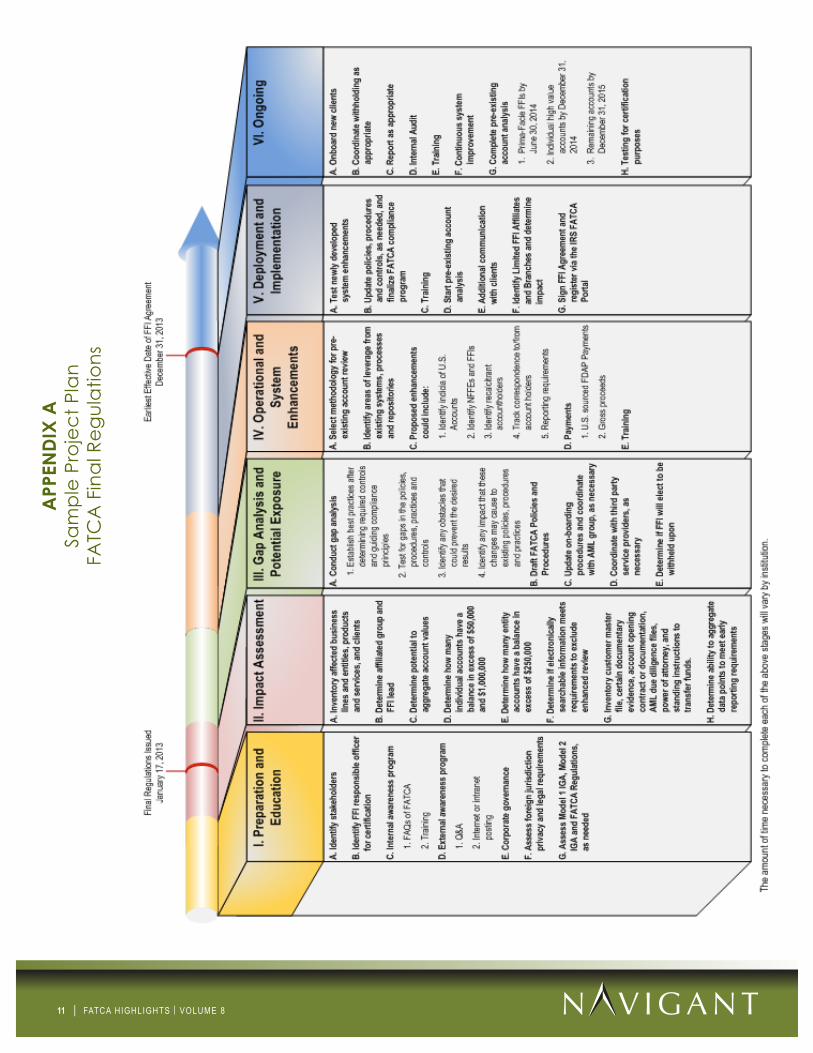

Appendix A - Sample Project Plan.....................................................................................................................................................11

I. INTRODUCTIONOn January 17, 2013, the United States Treasury and theInternalRevenueService(“IRS”)releasedthefinalregulations for the Foreign Account Tax Compliance Act (“FATCA”).1Thepreambleandfinalrulesare544pageslong.Generally,theFATCAFinalRegulationsprovidesomeadditionalrelieftofinancialinstitutionsand account for and accept many of the sugges-tionsmadebythefinancialservicesindustryasawhole.2

Below we provide a summary of the highlights of the FATCA Final Regulations as they relate to registration, duediligence,newFATCAreportingandcertifica-tionsthathavetobemadebytheresponsibleofficeroftheforeignfinancialinstitution(“FFI”).3

II. OVERVIEW OF FATCAOn March 18, 2010, FATCA was signed into law as part of the Hiring Incentives to Restore Employment Act (the “HIRE Act”). Over the last three years, the U.S. Treasury and the IRS have issued three Notices, proposed FATCA regulations on February 8, 2012, asked for and received numerous comments from thefinancialservicesandrelatedindustriesandheldmanymeetingswithfinancialinstitutionsandtheirrepresentatives. At the same time, the U.S. Treasury and the IRS met with representatives of foreign gov-ernments to try and devise a solution to implement FATCA, while minimizing implementation costs and not violating local laws in different countries.

The culmination of these efforts is two different tracks for FFIs to comply with FATCA depending on the loca-tion of the FFI: 1) the U.S. Treasury’s FATCA Final Regu-lationsand2)intergovernmentalagreements(“IGAs”).

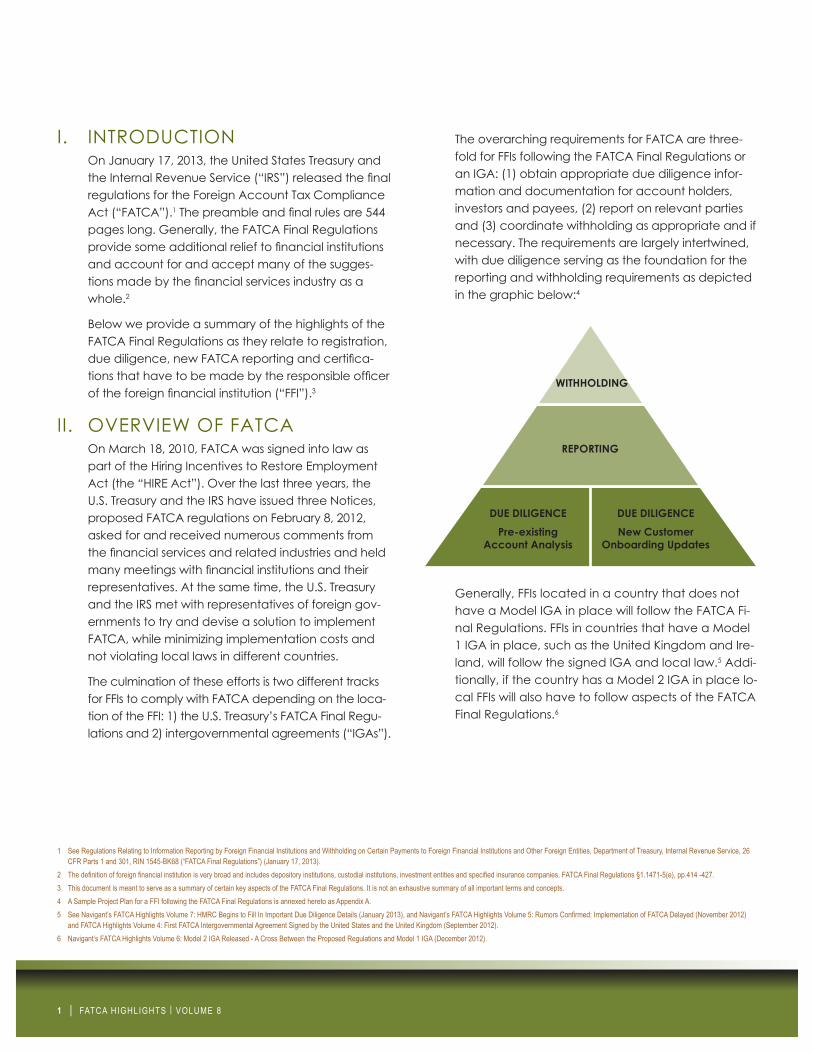

The overarching requirements for FATCA are three-fold for FFIs following the FATCA Final Regulations or anIGA:(1)obtainappropriateduediligenceinfor-mation and documentation for account holders, investors and payees, (2) report on relevant parties and (3) coordinate withholding as appropriate and if necessary. The requirements are largely intertwined, with due diligence serving as the foundation for the reporting and withholding requirements as depicted in the graphic below:4

1 See Regulations Relating to Information Reporting by Foreign Financial Institutions and Withholding on Certain Payments to Foreign Financial Institutions and Other Foreign Entities, Department of Treasury, Internal Revenue Service, 26 CFR Parts 1 and 301, RIN 1545-BK68 (“FATCA Final Regulations”) (January 17, 2013).

2 The definition of foreign financial institution is very broad and includes depository institutions, custodial institutions, investment entities and specified insurance companies. FATCA Final Regulations §1.1471-5(e), pp.414 -427.3 This document is meant to serve as a summary of certain key aspects of the FATCA Final Regulations. It is not an exhaustive summary of all important terms and concepts.4 A Sample Project Plan for a FFI following the FATCA Final Regulations is annexed hereto as Appendix A.5 See Navigant’s FATCA Highlights Volume 7: HMRC Begins to Fill In Important Due Diligence Details (January 2013), and Navigant’s FATCA Highlights Volume 5: Rumors Confirmed: Implementation of FATCA Delayed (November 2012)

and FATCA Highlights Volume 4: First FATCA Intergovernmental Agreement Signed by the United States and the United Kingdom (September 2012).6 Navigant’s FATCA Highlights Volume 6: Model 2 IGA Released - A Cross Between the Proposed Regulations and Model 1 IGA (December 2012).

WITHHOLDING

REPORTING

DUE DILIGENCEPre-existing

Account Analysis

DUE DILIGENCENew Customer

Onboarding Updates

Generally,FFIslocatedinacountrythatdoesnothaveaModelIGAinplacewillfollowtheFATCAFi-nal Regulations. FFIs in countries that have a Model 1IGAinplace,suchastheUnitedKingdomandIre-land,willfollowthesignedIGAandlocallaw.5 Addi-tionally,ifthecountryhasaModel2IGAinplacelo-cal FFIs will also have to follow aspects of the FATCA Final Regulations.6

2 | FATCA HIGHLIGHTS | VOLUME 8

I I I . REGISTRATIONPROCESSThefinalregulationsgivemuchneededguidanceconcerning the registration process for FATCA. Cer-taintypeoffinancialinstitutions,includingparticipat-ing FFIs, deemed-compliant FFIs, and FFIs in countries thatsignedtheModel1andModel2IGAwillhavetoregisterwiththeU.S.Governmentthoughawebsitere-ferredtoasthe“FATCAPortal.”EachofthesefinancialinstitutionswillreceiveaGlobalIntermediaryIdentifica-tionNumber(“GIIN”),whichwillbeauniqueidentifierthattheFFIwillhavetosupplytootherfinancialinstitu-tions where they maintain accounts or act as payees. The FATCA Portal will become available July 15, 2013 andGIINswillbeassignedstartingnolaterthanOcto-ber 15, 2013. Additionally, all FFIs will manage their FFI account on-line. These dates are important because the earliest effective date of a FFI Agreement is De-cember 31, 2013 and withholding could begin shortly thereafter on non-participating FFIs.7

IV. PRE-EXISTINGACCOUNTANALYSISThe process to complete the pre-existing account analysis is similar in it’s methodology when com-pared to the FATCA proposed regulations although there are some important changes.8 Below is an outline of the important steps to completing the pre-existing account analysis for individual and en-tity account holders.9

A. In-Scope Accounts

Before starting the review of accounts, the FFI should determine which accounts are in-scope. AFFIonlyhastoreviewfinancialaccountsasdefinedbyFATCA.10 There are some important exclusionstoFATCA’sdefinitionoffinancialac-count, including certain retirement funds, non-retirement savings accounts and certain term life insurance contracts.11 There are also accounts that are out of scope based on their balance

orvalue.Thefollowingfinancialaccountsareexcluded from the pre-existing account review, until and if the aggregate account balance or value is in excess of $1,000,000:

1. Individual accounts with a year-end aggre-gated balance or value of $50,000 or less;

2. Cash value insurance or annuity contracts with an aggregated value of $250,000 or less and

3. Entity accounts with a year-end aggregated balance or value of $250,000 or less.

It is important to note that the dollar amount ex-clusions only occur after the aggregated account balance or value, discussed below, is determined.

B. Aggregation

Implementing a process to aggregate account balancesorvaluesmaybedifficultforfinancialinstitutions. In general, FFIs are required to con-duct two types of aggregation: (1) electronic and (2) based on relationship manager knowledge.12 Both aggregations processes should occur, when possible, throughout the FFI and the expanded af-filiatedgroup.

1. Electronic Aggregation

FFIs are required to aggregate accounts electronically “only to the extent that the financialinstitution’scomputerizedsystemslink the accounts by reference to a data ele-ment, such as client number, EIN, or foreign tax identifying number, and allow the ac-count balances of such accounts to be ag-gregated.”13 It is important to note the last clause, “allow the account balances ... to be aggregated”, as it does not state that the values are already aggregated, but instead, can be aggregated.

7 A table comparing and contrasting requirements for FFIs that will follow a Model IGA and the FATCA Final Regulations is annexed hereto as Appendix B.8 Generally, a pre-existing account is any account maintained by the FFI as of December 31, 2013, assuming that is the FFI’s effective date for its FFI Agreement. FATCA Final Regulation §1.1471.4 (c)(3), p.323.9 It is also important to note that pre-existing accounts, both individual and entity, will have to be monitored in the future for potential changes of circumstance.10 FATCA Final Regulations §1.1471.5 (b), p. 395.11 FATCA Final Regulations §1.1471.5 (b)(2)(i-vi), pp.397-401.12 Under FATCA a relationship manager is defined as: an officer or other employee of an FFI who is assigned responsibility for specific account holders on an ongoing basis (including as an officer or employee that is a member of an FFI’s private banking department), advises account holders regarding their

banking, investment, trust, fiduciary, estate planning, or philanthropic needs, and recommends, makes referrals to, or arranges for the provision of financial products, services, or other assistance by internal or external providers to meet those needs. Notwithstanding the previous sentence, a person is only a relationship manager with respect to an account that has a balance or value of more than $1,000,000” after aggregation. FATCA Final Regulations §1.1471-1 (b)(106), p.163.

13 FATCA Final Regulations §1.1471-5(b)(4)(iii)(A) and (B), p. 410.

3 | FATCA HIGHLIGHTS | VOLUME 8

2. Relationship Manager Knowledge

FFIs are “required to aggregate all accounts that a relationship manager knows are di-rectly or indirectly owned, controlled, or es-tablished … by the same person” as well as accounts that the relationship manager can associate with other accounts through dif-ferent codes.14 This step will require each re-lationship manager be asked whether he or she is aware of additional accounts associ-ated with an account holder beyond those identifiedduringelectronicaggregation.Theresponse to these questions must be tracked andretained.Somefinancialinstitutionshavethousands of relationship managers each of whom may have hundreds of accounts for which they are responsible.

Asking relationship managers these aggrega-tion questions may be the easy part com-pared to determining if accounts should actually be aggregated. For example, a re-lationship manager may provide a response thatislessthandefinitive,suchasnaminga country where the relationship manager believes the account holder may maintain another account, but where certain privacy and data protection laws do not allow the relationship manager to access account in-formation in such country. Determining what constitutes knowledge in this instance will be of utmost importance and may not be a bright line.

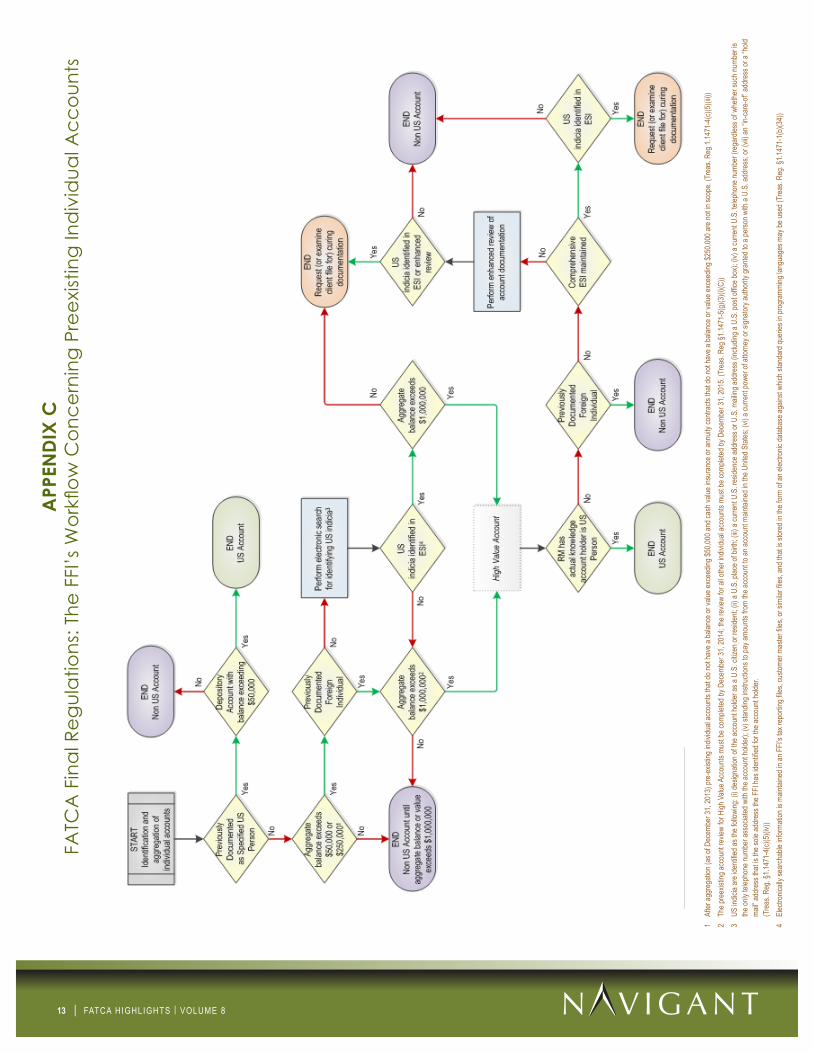

14 FATCA Final Regulations §1.1471-5(b)(4)(iii)(A) and (B), p. 410-411.15 For a pictorial workflow see FATCA: The FFIs Workflow Concerning Pre-existing Individual Accounts annexed hereto in Appendix C.16 There are seven U.S. indicia for individuals and they are: 1. Designation of the account holder as a U.S. citizen or resident; 2. A U.S. place of birth; 3. A current U.S. residence address or U.S. mailing address (including a U.S. post office box); 4. A current U.S. telephone number (regardless of whether such number is the only telephone number associated with the account holder; 5. Standing instructions to pay amounts from the account to an account maintained in the United States; 6. A current power of attorney or signatory authority granted to a person with a U.S. address; or 7. An “in-care-of” address or a “hold mail” address that is the sole address the FFI has identified for the account holder.

FATCA Final Regulations §1.1471.-4 (c)(5)(iv) (B), pp. 333-334.17 A recalcitrant account holder is an account holder who does not provide information or a waiver of local privacy laws as requested by the FFI. FATCA Final Regulations §1.1471-5(g), p.453.

C. Individual Accounts15

Ingeneral,afinancialinstitutionmustreviewitsin-scope pre-existing individual accounts for U.S. indicia, which include U.S. citizenship, residency, and/or a U.S. residence address or telephone number.16WhenU.S.indiciaareidentified,TheFFImust either already possess or request curing doc-umentation for the account holder. The curing documentation will provide evidence to deter-mine if the account holder is a U.S. taxpayer. If the account holder does not respond to requests for curing documentation, the account holder must beclassifiedasrecalcitrant,17 which means the FFI will have to withhold on select payments to the account holder.

There are two basic categorizations of individual accounts subject to the pre-existing account re-view: (1) accounts with an aggregated balance or value in excess of $50,000 up to and including $1,000,000 (“Low Value Accounts”) and (2) ac-counts with an aggregated balance or value in excess of $1,000,0000 (“High Value Accounts”). The aggregate balance or value dictates both the type of review required and the date by which this review must be completed. High Value Accounts have to be reviewed by December 31, 2014 and Low Value Accounts have to be re-viewed by December 31, 2015, assuming the FFI Agreement is effective December 31, 2013.

4 | FATCA HIGHLIGHTS | VOLUME 8

1. Low Value Accounts

FFIs must review their electronically search-able information for the seven indicia of U.S. person status for Low Value Accounts. To start FFIs have to determine what electronic data they have that can be categorized as electronically searchable information. Elec-tronicallysearchableinformationisdefinedas information “that is stored in the form of an electronic database against which stan-dard queries in programming language … may be used.” It is important to note that information is “not electronically searchable merely because [it] is stored in an image re-trieval system (such as portable document format (.pdf) or scanned documents).”18 If no U.S. indicia are found, the account is classi-fiedasanon-U.S.account.IfU.S.indiciaarefound, the FFI has to collect more information from the account holder to determine if the account holder is a U.S. person.

2. High Value Accounts

For High Value Accounts, FFIs must review not only their electronically searchable in-formation for U.S. indicia, but also hard copy documents if the required information is not part of the electronically searchable infor-mation.19 Assuming the electronically search-able information does not meet all of the requirements, the FFI is required to review the customermasterfileandtotheextentnotmaintainedinthecustomermasterfile,theFFI must also review the following if obtained inthelastfiveyears:

a. Themostrecentwithholdingcertificate,written statement, and documentary evidence;

b. The most recent account opening contract or documentation;

c. The most recent documentation ob-tained by the participating FFI for purpos-es of anti-money laundering (“AML”) due diligence or for other regulatory purposes;

d. Any power of attorney or signature au-thority forms currently in effect; and

e. Any standing instructions to pay amounts to another account.20

FFIs must also ask the account holder’s re-lationship manager if he or she has actual knowledge that the account holder is a U.S. citizen or resident.

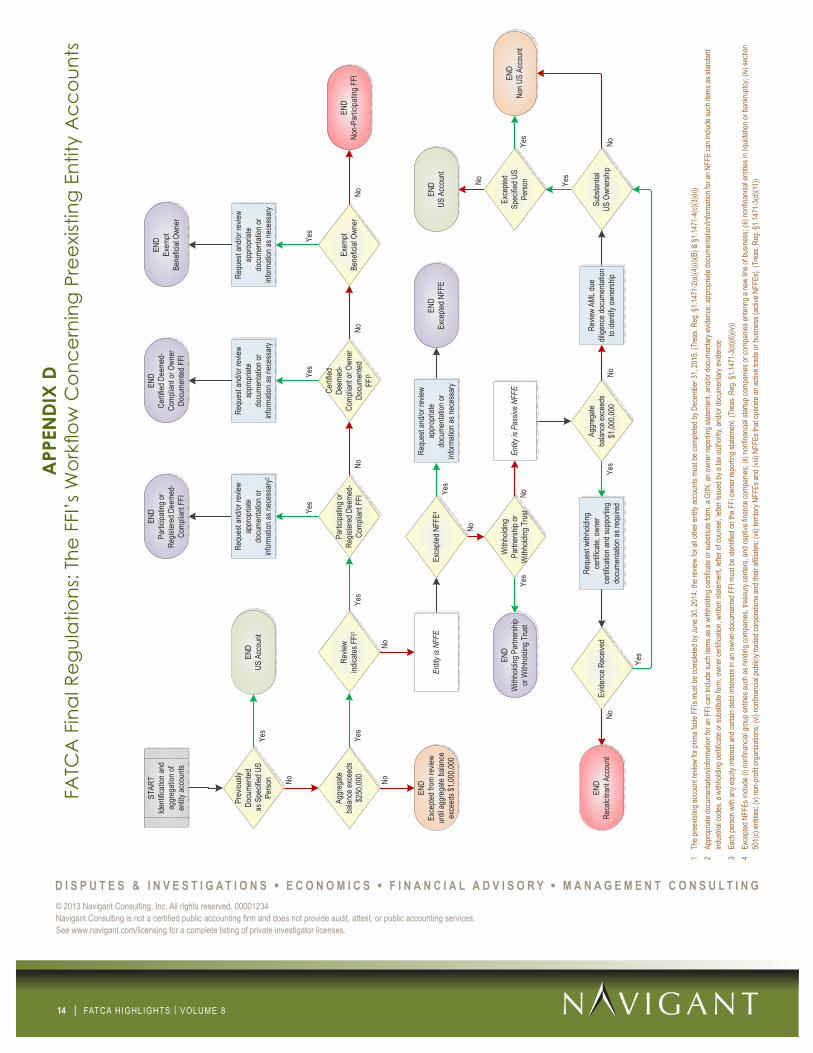

D. Entity Accounts21

In general, a FFI has to classify all of its in-scope entity account holders. The primary division for foreign entity account holders is whether the for-eignentityaccountholderisaFFIoranon-finan-cial foreign entity (“NFFE”). NFFEs are all non-U.S. entities that are not FFIs and generally include entitiessuchasthoseoperatingnon-financialac-tive trades or businesses. As part of the review of both FFI and NFFE account holders, FFIs are required to look for certain entities that are ex-empt or excepted from FATCA because the U.S. government believes they pose a low risk for tax evasion, among other reasons. Some examples of such entities include: foreign governments, in-ternational organizations and companies oper-atinganon-financialactivetradeorbusiness.Allentity accounts except prima facie FFIs have to be reviewed by December 31, 2015. Prima facie FFIs have to be reviewed by June 30, 2014.22 Both deadlines for review assume an effective date of the FFI Agreement of December 31, 2013.

18 FATCA Final Regulations §1.1471-1(b)(34), p. 150.19 FATCA Final Regulations §1.1471-4(c)(5)(iv)(D)(4), pp. 339 -340.20 FATCA Final Regulations § 1.1471-4(c)(5)(iv)(D)(4), pp. 338-339.21 For a pictorial workflow see FATCA: The FFIs Workflow Concerning Pre-existing Entity Accounts annexed hereto in Appendix D.22 FATCA Final Regulations §1.1471-2 (a)(4)(ii)(B), pp.178 – 180.

5 | FATCA HIGHLIGHTS | VOLUME 8

1. FFIs

Ingeneral,forfinancialinstitutionaccountholders a FFI will have to collect, or already have,awithholdingcertificate,suchaW-8BEN-E, that contains the account holder FFI’sGIIN.TherearedifferentgroupsofFFIsthat signify compliance with FATCA including:

a. participating FFIs;

b. registered deemed compliant FFIs;

c. certifieddeemedcompliantFFIs;and

d. FFIs that are excepted or exempted from FATCA.

A non-complying FFI will be categorized as a non-participating FFI. FFIs are required to withhold and report on select payments to non-participating FFIs, such as U.S. sourced dividends and interest payments.

2. NFFEs

In general, FFIs must have or collect docu-mentation on their NFFE account holders, whichcanbeclassifiedeitheraspassiveoras excepted NFFEs. FFIs should be most con-cerned about passive NFFEs, which could be analogous to a shell company for anti-money laundering purposes. For passive NFFEs with an aggregate balance or value of $1,000,000 orless,theFFIcanreviewitscurrentAML/KYCfileforinformationonsubstantialU.S.own-ers, which are generally any U.S. persons that own more than 10% of the Passive NFFE. For passive NFFEs with an aggregate balance or value of more than $1,000,000 the FFI has to gather information from the account holder concerning its substantial U.S. owners, if it has any. If the FFI is unable to gather the informa-

23 FATCA Final Regulations §1.1471-3(c)(5)(ii)(B), p. 211. 24 U.S. indicia for entities are: (1) classification of an account holder as a U.S. resident in the withholding agent’s customer files, (2) current U.S. residence address or U.S. mailing address; (3) with respect to an offshore obligation, standing

instructions to pay amounts to a U.S. address or an account maintained in the U.S., (4) A current telephone number for the entity in the United States but no telephone number for the entity outside the United States, (5) a current telephone number for the entity in of the United States in addition to a telephone number for the entity outside the United States, (6) a power of attorney or signatory authority granted to a person with a U.S. address and (7) an “in-care-of” address or “hold mail” address that is the sole address provided for the entity. FATCA Final Regulations §1.1471-3(e)(4)(v)(a), p. 291

tion from the account holder, the account holder is deemed to be recalcitrant and the FFI must report and withhold on select U.S. sourced payments.

Excepted NFFEs are NFFEs that generally have been deemed to pose a low risk of tax evasion. Excepted NFFES include Active NFFEs, which are companies that operate non-financialactivetradesorbusinesses.Thelocal children’s clothing store formed and operating in Canada that generates the ma-jority of its income from the sale of clothing is an example of an entity that may have an ActiveNFFEclassification.

3. TypesofProoftoShowaFATCAClassification

An important change from the Proposed Regulations to the FATCA Final Regulations is the type of proof needed to classify an entity according to FATCA. In the FATCA Fi-nal Regulations the documentation require-mentshavebeensimplifiedsomewhat.Forexample, in select situations, such as for an entityoperatinganon-financialactivetradeor business, the FFI can rely on any standard-izedindustrycodeoranyclassificationintheFFI’s records with respect to the payee to classify the entity that was determined based on documentation supplied by the payee.23 Torelyontheclassificationcode,theFFIhasto make sure other requirements are met, including the non-existence of entity U.S. indi-cia.24 In practice, this means that if a FFI clas-sifiesanentityusingaclassificationcode,theFFIwillhavetoreviewthefilefortheentitytomake sure it contains no entity U.S. indicia. Requiring this search for U.S. indicia substan-tially decreases the value of the reliance on an industry code.

6 | FATCA HIGHLIGHTS | VOLUME 8

E. IRS Forms Not Needed for Offshore Accounts to Cure Individual U.S. Indicia or for Entity Classification

The Final FATCA Regulations ease the documen-tation requirements for a FFI in certain situations. For example, IRS forms are not explicitly required (1) to establish an individual account holder’s status as a foreign person when U.S. indicia have beenidentifiedand(2)toproperlyclassifyenti-ties under FATCA. Rather, an FFI may provide a substitutewithholdingcertificateprovidedthatitcontains provisions that are substantially similar to those in the IRS forms.

1. Substitute Individual Form

Specifically,forindividualsthesubstitutewith-holdingcertificatemustcontaintheindivid-ual account holder’s name and address, all countries in which the individual is resident for tax purposes and associated TINs where ap-plicable, and the city and country of birth.25 In general, the substitute withholding certi-ficationmustbesignedanddatedunderpenalties of perjury; however, the substitute form need not be signed under penalties of perjury if it is accompanied by documentary evidence that supports the individual’s claim of foreign (non-U.S.) status. It is important to notethatthesubstitutewithholdingcertifica-tion may also request information required for non-FATCA purposes, such as tax or AML due diligence. Thus, to the extent that an FFI’s tax and AML programs capture this informa-tion, an FFI may rely on such information for FATCA purposes.

2. Substitute Entity Form

Afinancialinstitutionmakingapaymentwithrespect to an offshore obligation, in certain situations,canrelyuponawrittennotifica-tion instead of Form W-8 “that indicates the person’sentityclassification…unlessthewithholding agent has reason to know … it is incorrect.”26Thewrittennotificationdoesnothave to be signed. For example, for an Ac-tiveNFFEtheFFImayrelyonawrittennotifi-cation in certain circumstances.

3. Validity Period

One historic area of frustration for FFIs with regard to the FATCA proposed regulations en-tailed the expiry of documents and the subse-quent necessity to refresh due diligence. The FATCA Final Regulations address the FFIs’ con-cern by allowing certain documents to remain validindefinitely.Suchdocumentsinclude:

a. Awithholdingcertificateorwrittenstate-ment provided by a participating FFI that hasfurnishedavalidGIINthathasbeenverified;

b. Awithholdingcertificateordocumen-tary evidence provided by an individual claiming non-U.S. taxpayer status if the FFI does not have a current U.S. resi-dence or mailing address or U.S. tele-phone as the sole telephone number on file,anddoesnothavestandinginstruc-tions to make a payment in the United States and

c. Awithholdingcertificate,writtenstate-ment or documentary evidence provid-ed certain entities such as a retirement fund,anon-profitorganization,aNFFEthat is publicly traded and a NFFE oper-atinganon-financialtradeorbusinessforwhich AML due diligence does not indi-cate that determination is incorrect.27

25 FATCA Final Regulations §1.1471-3 (c)(6)(ii)(C), pp. 222-223.26 FATCA Final Regulations § 1.1471-3(b)(2), pp. 195-196.27 FATCA Final Regulations §1.1471-3(c)(6)(ii)(B) and (C), p. 213.

7 | FATCA HIGHLIGHTS | VOLUME 8

28 There is an exception for depository accounts under or equal to $50,000 as these accounts even if held by a U.S. taxpayer are still not U.S. accounts. §1.1471-4 (c)(4), p.326 and see §1.1471-5 (a)(4)(i), p.394. It also appears if these ac-counts are excluded from the review, the accounts will have to be reviewed when they cross $50,000. Thus, it may make sense for most FFIs to elect not to apply this exception.

29 The IRS may approve certain documents, on a country by country basis, to serve as documentary evidence for QIs located in that country. The IRS website (www.irs.gov) provides a list of documentation for each approved country. 30 FATCA Final Regulations §1.1471-3(c)(5)(i)(A) and (B), p. 209-210.31 FATCA Final Regulations §1.1471-3(c)(5)(i)(A) and (B), p. 209-210.32 FATCA Final Regulations §1.1471-3 (e), pp. 284-286.33 FATCA Final Regulations §1.1471-4 (c)(3)(i), pp. 323-324.34 FATCA Final Regulations §1.1471-4 (c)(3)(i), p. 324.35 It is important to note that foreign passthru payment is still undefined in the Final FATCA Regulations and the earliest it would go into effect is January 1, 2017.

V. ON-BOARDINGOFNEWACCOUNTSFFIs will be required to onboard new accounts in a FATCA compliant manner as early as January 1, 2014.

A. Individual Account Holders

Financial institutions must collect certain types of documentary evidence to determine if an indi-vidual is a U.S. or non-U.S. taxpayer.28 Examples of documentary evidence to support a claim of foreign status for an individual include:

1. Certificateofresidence;

2. Individualgovernmentidentification;

3. SelectQualifiedIntermediary(“QI”) documentation29 and

4. Select third-party credit reports.30

To support a claim of foreign status, the docu-mentary evidence must contain a permanent residence address for the person named on the documentation or indicate the country in which the individual is a resident or citizen.31 After receiv-ing documentary evidence the FFI has to review other information collected by the FFI to deter-mine if the documentation provided is reliable in the context of other information known to the FFI about the account holder. When reviewing the documentary evidence the FFI must look for a number of things including a U.S. address or U.S. telephone number (as the only telephone number provided), which are part of the seven U.S. indicia for the pre-existing individual account analysis.32 If this information is found, the FFI has to collect more information to prove foreign status.

B. Entity Accounts and Payees

The FFI has to properly classify its entity account holders and payees. The goal is to determine “if the account is a U.S. account or an account held by a recalcitrant account holder or non-partici-pating FFI … and to establish the chapter 4 status of each account holder and each payee re-gardless of whether the participating FFI makes a payment to the account…”33 Additionally, if the account holder receiving the payment is not the payee, the FFI may have to look through the ac-count holder to determine who the actual payee is where withholding apply.34 For example, if the account holder is holding the account on behalf of a third party, the FFI may be required to obtain theFATCAclassificationofthethirdparty.

It should be noted that many of the documenta-tion exceptions allowed for pre-existing entity ac-counts do not apply to new accounts. For most new accounts the FFI will have to obtain a with-holdingcertificateoritssubstituteforproperclas-sification.FFIshave90daysoruntilthetimeawith-holdable or passthru payment is made to classify the entity, whichever is earlier.35

8 | FATCA HIGHLIGHTS | VOLUME 8

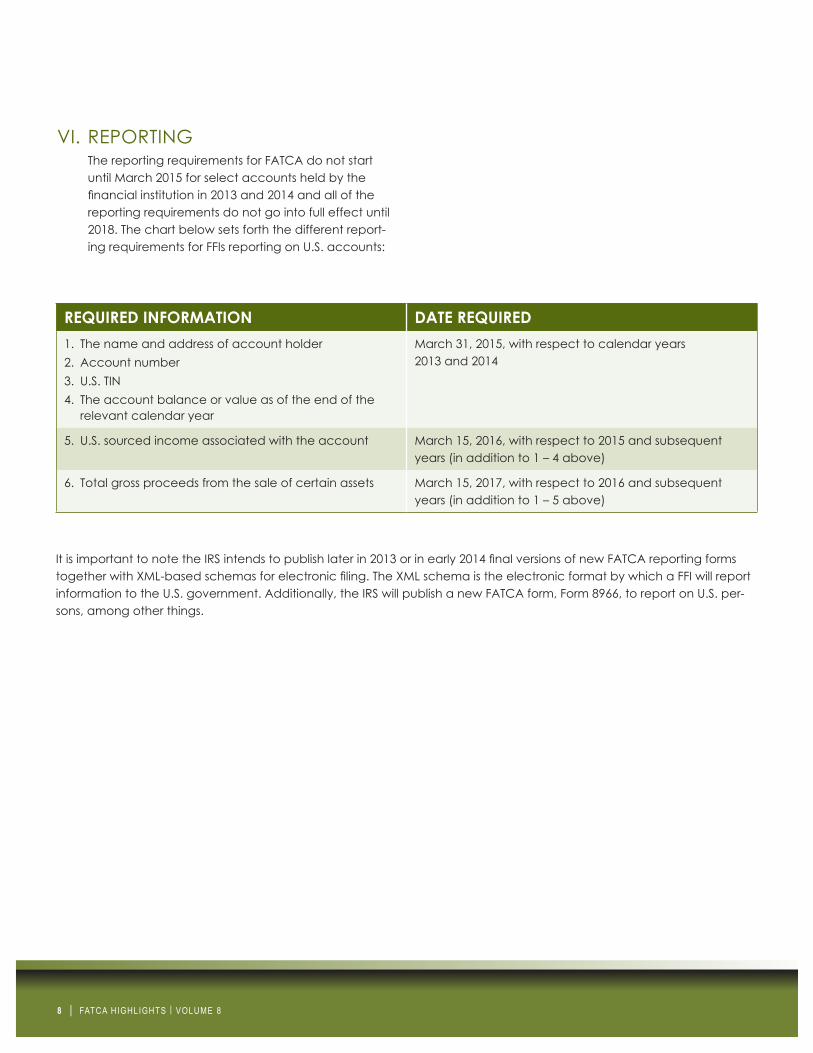

VI.REPORTINGThe reporting requirements for FATCA do not start until March 2015 for select accounts held by the financialinstitutionin2013and2014andallofthereporting requirements do not go into full effect until 2018. The chart below sets forth the different report-ing requirements for FFIs reporting on U.S. accounts:

REQUIRED INFORMATION DATE REQUIRED1. The name and address of account holder2. Account number 3. U.S. TIN 4. The account balance or value as of the end of the

relevant calendar year

March 31, 2015, with respect to calendar years 2013 and 2014

5. U.S. sourced income associated with the account March 15, 2016, with respect to 2015 and subsequent years (in addition to 1 – 4 above)

6. Total gross proceeds from the sale of certain assets March 15, 2017, with respect to 2016 and subsequent years (in addition to 1 – 5 above)

ItisimportanttonotetheIRSintendstopublishlaterin2013orinearly2014finalversionsofnewFATCAreportingformstogetherwithXML-basedschemasforelectronicfiling.TheXMLschemaistheelectronicformatbywhichaFFIwillreportinformationtotheU.S.government.Additionally,theIRSwillpublishanewFATCAform,Form8966,toreportonU.S.per-sons, among other things.

9 | FATCA HIGHLIGHTS | VOLUME 8

37 If the participating FFI has not received the necessary documentation from the account holder, the FFI must treat the account holder as a recalcitrant account holder or other presumed classification, as necessary, to make the required certifications. FATCA Final Regulations, §1.1471-4(c)(7), p.342.

38 FATCA Final Regulations §1.1471-4(c)(7), p. 342.39 FATCA Final Regulations §1.1471-4(f), p. 375.40 FATCA Final Regulations §1.1471-4(c)(7), p. 343.

VII.RESPONSIBLE OFFICER CERTIFICATION&GOVERNANCEConsistent with the proposed regulations, the FATCA Final Regulations require a participating FFI to ap-pointaresponsibleofficertocertifycompliancewiththe FFI Agreement.

A. Required Certifications

Thecertificationsaresponsibleofficermust make include:

1. The participating FFI has completed the re-view of all pre-existing High Value Accounts;

2. The participating FFI has completed the re-view of all other pre-existing accounts37 and

3. The participating FFI did not have any formal or informal practices or procedures in place from August 6, 2011 through the date of certi-ficationtoassistaccountholderavoidFATCAdetection.38

Tomakethesecertifications,theFATCAFinalRegulations mandate the participating FFI adopt a compliance program under the authority of theresponsibleofficertoallowtheresponsibleof-ficertocertifycompliance.Thecompliancepro-gram must include policies, procedures and pro-cessessufficienttosatisfytherequirementsoftheFFIAgreement.Theresponsibleofficermustre-viewthesufficiencyofthecomplianceprogramand certify it every three years.39Thecertificationprocess will occur in the FATCA Portal the IRS is setting up to allow FFIs to register with the IRS.

B. Conducting a Reasonable Inquiry

According to the FATCA Final Regulations, a rea-sonable inquiry to determine if there have been policies in place to avoid FATCA detection con-sists of a review of the procedures and a writ-ten inquiry. A written inquiry could include email requests to relevant business lines that require responses from onboarding and management personnel regarding not having any formal or in-formal practices or procedures to assist account holders avoid FATCA detection.40

The above sounds simple, but when push comes to shove regarding actually certifying compli-ancewithFATCAtotheUnitedStatesGovern-ment, many more audit and testing steps will most likely be necessary and could be dictated bytheresponsibleofficer.ConsistentwithAMLtesting, the FFI may want to take a risk-based approach to allow for greater assurance. For ex-ample, certain geographies, based on historical U.S.Governmentactions,maybemoresuscep-tible to facilitating tax evasion, which may lead to higher risk for FATCA compliance. The FFI re-sponsibleofficermayrequestadditionaltestingresources be utilized in a certain geography to providegreatercomfortcomecertificationtime.

10 | FATCA HIGHLIGHTS | VOLUME 8

CONTACTS »

Ellen Zimiles Managing Director Head,GlobalInvestigations&Compliance +1.212.554.2602 [email protected]

Richard Kando Director, FATCA Task Force Leader, GlobalInvestigations&Compliance +1.212.554.2698 [email protected]

Salvatore LaScala Managing Director GlobalInvestigations&Compliance +1.212.554.2611 [email protected]

Dr. Ray Nulty Managing Director Financial Services +44 (0) 788 750 3854/ +353 (0) 87 0541416 [email protected]

David Brown Director GlobalInvestigations&Compliance +1.416.777.2438 [email protected]

VIII.CONCLUSIONGaininganunderstandingofmanyoftheconceptsof the FATCA Final Regulations in earnest is critical considering many FFIs around the globe still need to implement a workable compliance program. Strik-ing the balance between engineering a complex process and making that process manageable so as to become business as usual will be of utmost importance over the next 11 months leading up to FATCA’s go-live date of December 31, 2013.

CUSTOMER ONBOARDING AND PREEXISTING ACCOUNT REVIEW DEADLINES

Updates to the new account onboarding process

December 31, 2013 December 31, 2013 December 31, 2013

Review of prima facie FFIs2 June 30, 2014 N/A N/A

Review of individual high value accounts

December 31, 2014 December 31, 2014 December 31, 2014

Review of all remaining individual and entity accounts

December 31, 2015 December 31, 2015 December 31, 2015

WITHHOLDING COMMENCEMENT DATES

U.S. source income January 1, 2014 January 1, 2014 January 1, 2014

Grossproceeds January 1, 2017 TBD3 TBD3

Foreign passthru payments Not earlier than January 1, 2017

TBD3 TBD3

REPORTING REQUIREMENTS & DEADLINES

Report to: IRS Local government authority

IRS and local government authority as required4

Account identifying information and account balance or value

March 31, 2015 September 30, 20155 March 31, 20156

U.S. source income March 15, 2016 September 30, 20165 March 15, 20166

Grossproceeds March 15, 2017 September 30, 20175 March 15, 20176

1 Dates in this table assume an FFI Agreement effective date of December 31, 2013. 2 Prima facie FFIs are defined as (1) entities designated as a Qualified Intermediary or Non-Qualified Intermediary in a FFI’s electronically searchable information or (2) entities presumed to be or documented as foreign entities for the

purposes of chapter 3 or 61 and for which the FFI has recorded as part of its electronically searchable information certain North American Industry Classification System or Standard Industrial Classification codes. (Treas. Reg. 1.1471-2(a)(4)(ii)(B)) Prima facie FFIs are not explicitly addressed in the IGAs.

3 Currently there is no requirement under the IGAs to withhold on gross proceeds or foreign passthru payments, however the IGAs include a provision whereby the U.S. and Partner Jurisdictions commit to work together “to develop a practi-cal and effective alternative approach to achieve the policy objectives of foreign passthru payments and gross proceeds withholding that minimizes burden.” (Model 1 IGA, Article 6(2); Model 2 IGA, Article 5(1))

4 Generally, Model 2 FFIs will report to the IRS detailed information on U.S. Accounts and aggregate information on Non-Consenting U.S. Accounts and Nonparticipating FFIs. The U.S. Competent Authority may make a group request to the local tax administration for specific information about an account or obligation, whereupon the local tax administration will request and receive reporting from the Model 2 FFI and may exchange this information with the IRS. (Model 2 IGA, Article 2)

5 Dates by which Model 1 local government authorities have agreed to provide reporting to the IRS; deadlines for FFIs reporting to Model 1 local government authorities within a given country may vary at the discretion of those authorities and will likely significantly precede the dates provided in the table. (Model 1 IGA, Article 3(5))

6 It appears that reporting requirements for FFIs governed by Model 2 IGAs are dictated by the FFI Agreement and relevant U.S. Treasury Regulations. (Model 2 IGA, Article 2(1))

![Emarketing [repaired]](https://static.documents.pub/doc/80x56/555122efb4c9052d0e8b54a2/emarketing-repaired.jpg)