The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Presenting a live 90-minute webinar with interactive Q&A FCPA in India 2016: Compliance Strategies for India's Unique Cultural and Governmental Intricacies Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific TUESDAY, JANUARY 12, 2016 Jay Holtmeier, Partner, Wilmer Cutler Pickering Hale and Dorr, New York Elizabeth D. Keating, Vice President, Global Investigations Counsel, Johnson Controls, Milwaukee, Wis. Michael Stavridis, Partner, Ernst & Young, Chicago

Transcript

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Industry-Specific Risks (e.g., probe of banks’ Asian hiring practices)

Increasing Cooperation with and Enforcement by Non-US Authorities

Collateral Civil Litigation 6

Enforcement by Indian Authorities

Lokpal Act of 2013 created a new agency to investigate and prosecute civil servants accused of corruption.

Black Money Act came into effect in July 2015 and aims to curb “black money,” i.e., undisclosed foreign assets and income, and it imposes tax and penalty on such income.

Pending amendments to the Prevention of Corruption Act of 1988 include tougher prison terms for individuals convicted under the Act; liability for commercial entities that induce public servants; an expansion of the types of corruption covered under the Act; and a “speedy trial” provision aimed at reducing the trial period for cases brought under the Act from an average of eight years to two years.

7

Enforcement by Indian Authorities (cont.)

Recent Supreme Court ruling expands power of Comptroller & Auditor

General to audit transactions with government.

Parliament recently passed a whistleblower protection bill.

High-profile investigations reported publicly:

– National Herald graft case continues against Sonia Gandhi, head of India’s main opposition Congress Party, and her son Rahul, for misappropriating $300M through the purchase of a non-profit newspaper company.

– Bribery in helicopter procurement led to India’s suspension of $750M contract with AgustaWestland and criminal charges against former Indian Air Force Chief.

– India’s Defense Ministry has suspended all contracts with Rolls-Royce pending inquiry of bribery allegations by India’s Central Bureau of Investigation.

– In July 2015, the Supreme Court of India transferred the ongoing Vyapam case involving widespread corruption in a state government examination board to the Central Bureau of Investigation. By July 2015, more than 2,000 individuals had been charged in the case. 8

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Louis Berger International, Inc. (2015) – Payments to Government Officials Through Third-Party Vendors

– LBI is a New Jersey-based construction management company.

– The DOJ alleged that between 1998 and 2010 LBI paid $3.9M in bribes to officials in India, Indonesia, Vietnam, and Kuwait to secure construction management contracts in those countries.

LBI concealed the payments by characterizing them as “commitment fees,” “counterpart per diems,” “marketing fees,” and “field operation expenses.”

Third-party vendors submitted false invoices to generate payments from LBI; payments tracked on a spreadsheet.

– James McClung, Senior Vice-President in charge of LBI’s India operations, pleaded guilty to violating the FCPA by participating in the scheme.

– LBI entered into a deferred prosecution agreement and paid a $17.1 million criminal penalty; a compliance monitor was imposed for three years.

9

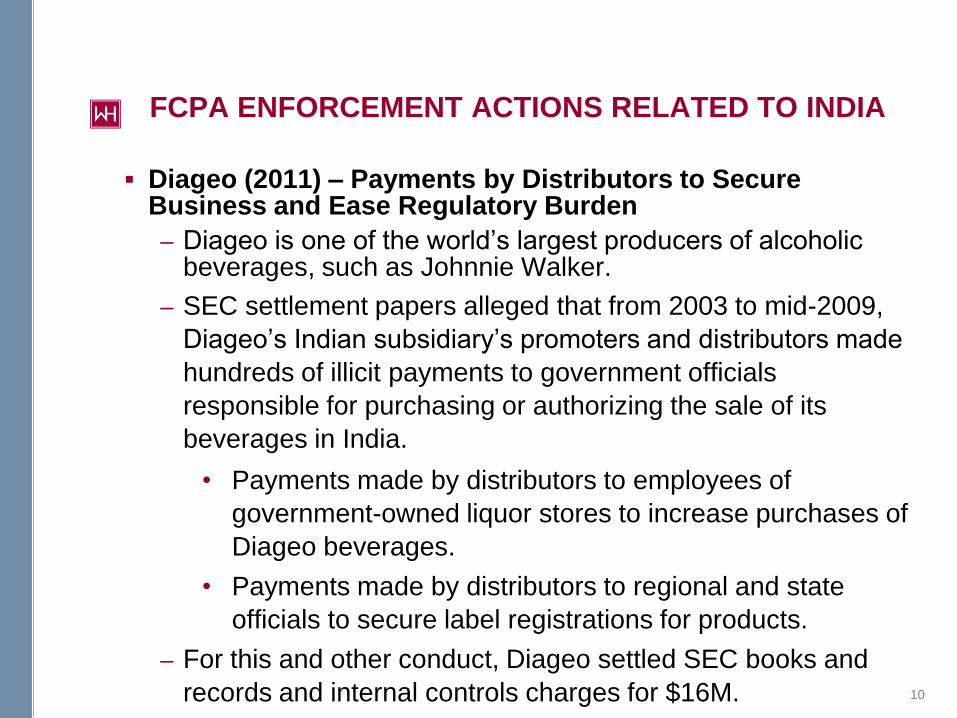

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Diageo (2011) – Payments by Distributors to Secure Business and Ease Regulatory Burden

– Diageo is one of the world’s largest producers of alcoholic beverages, such as Johnnie Walker.

– SEC settlement papers alleged that from 2003 to mid-2009,

Diageo’s Indian subsidiary’s promoters and distributors made

hundreds of illicit payments to government officials

responsible for purchasing or authorizing the sale of its

beverages in India.

• Payments made by distributors to employees of

government-owned liquor stores to increase purchases of

Diageo beverages.

• Payments made by distributors to regional and state

officials to secure label registrations for products.

– For this and other conduct, Diageo settled SEC books and

records and internal controls charges for $16M. 10

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Baker Hughes (2001) – Payments by Agent to Ease Regulatory Burden

– Baker Hughes’ former subsidiary Western Geophysical (WG)

provided geophysical exploration services.

– In order to provide these services in the Bay of Canby, India,

WG needed authorization from the Director General of

Shipping to use a foreign-flagged vessel.

– According to the SEC’s papers, WG’s agent told a WG

manager that permits could be issued for $15k. WG manager

told the agent to “take care of it.”

– WG later authorized a $15k reimbursement for the agent

without adequate inquiry to ensure that the payment did not

violate the FCPA.

– WG accounting staff improperly described the payment as

“Shipping Permit.”

– SEC issued cease and desist order.

11

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Oracle (2012) – Side Funds Maintained by Distributors

– Oracle is a California-based computer technology company.

– Oracle’s Indian subsidiary sells its products through

distributors that retain the margin between the amount paid by

the customer and the amount paid to the subsidiary.

– According to the government, the subsidiary structured

transactions to create extra margins for distributors in certain

instances, essentially creating off-the-books side funds.

– Subsidiary employees then directed distributors to make

payments from the side funds to sham entities.

– No allegation of bribery.

– Oracle settled SEC books and records and internal controls

charges for $2 million.

12

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Dow Chemical (2007) – Payments Through Side Funds and Petty Cash to Ease Regulatory Burden

– Dow’s Indian majority-owned, fifth-tier subsidiary DE-Nocil

manufactures pesticides and other products.

– SEC alleged that DE-Nocil structured transactions such that

off-the-books funds were held by the company’s contractors.

As directed by DE-Nocil, the contractors disbursed funds

directly to DE- Nocil or to a third party that would bribe a

Central Insecticides Board official.

– Bribes resulted in expedited regulatory registration for DE–

Nocil’s products.

– DE-Nocil also used petty cash to make improper payments to

other officials, such as state inspectors.

– Dow settled SEC books and records and internal controls

charges and agreed to pay a $325K civil penalty. 13

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Pride Int’l (2010) – Payments to Judicial Officer Through Third-Party Bank Account

– Pride International is an oil and gas services company.

– Government settlement papers alleged that managers at

Pride’s French subsidiary (including the legal director)

authorized payment of $500K to a judge of the Indian

Customs, Excise, and Gold Appellate Tribunal to secure a

favorable determination in a customs duties and penalties

dispute.

– Payments were made through a third-party company’s bank

accounts in Dubai.

– The estimated value of the favorable decision was $10M.

– Pride’s French subsidiary pleaded guilty; Pride International

entered into a DPA with DOJ.

• For this and other conduct, Pride entities paid DOJ/SEC

$56.2M.

14

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Westinghouse Air Brake Technologies (2008) – Payments to Secure Business and Ease Regulatory Burden

– WABTEC manufactures brake subsystems for locomotives,

freight cars, and passenger transit vehicles.

– Government’s papers state that WABTEC’s Indian

subsidiary’s employees and agents made payments to Indian

Railway Board and other government officials to:

• Obtain business during the IRB tender process;

• Schedule pre-shipping product inspections;

• Have certificates of product delivery issued; and

• Curb tax audits.

– To generate cash for these payments, the subsidiary engaged

third-party “marketing agents” to create false invoices. When

the subsidiary paid the invoices, the “marketing agents”

returned the cash to the subsidiary.

– Payment of $677K to DOJ/SEC.

15

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Textron, Inc. (2007) – Payment to Secure Business with a Commercial Customer

– Textron is a conglomerate in the aircraft, defense,

manufacturing, and financial industries.

– According to the government’s papers, a subsidiary paid

approximately $52K to an employee of a non-government

customer to secure business in India.

– The payment was described as a “commission” in the

subsidiary’s records.

– Identified by an internal investigation in response to

allegations of kickbacks related to the UN’s Oil for Food

Program.

– For this and other conduct, Textron entered into a NPA with

DOJ and agreed to pay a total of $4.7M to DOJ/SEC.

16

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Electronic Data Systems (2007) – Payments to Secure Business

– EDS is one of the world’s largest technology companies.

– SEC’s papers allege that between 2001 and 2003, EDS’

Indian subsidiary had difficulty performing its contractual

obligations for two Indian government-owned clients.

– The subsidiary’s president authorized payments and gifts of

over $720K to employees of the Indian government-owned

clients.

– The payments resulted in the subsidiary retaining the

business of the two clients.

– For this and other conduct, EDS settled with the SEC for

$491K. The subsidiary’s president also settled with the SEC

and paid a $70K penalty.

17

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Control Components, Inc. (2009) – Payments to Secure Business

– CCI designs and manufactures valves used in the power, oil

and gas, and nuclear industries.

– CCI made payments of at least $4.9M from 2003 – 2007 to

employees of private companies and state-owned companies

in several countries, including in India to the Maharashtra

State Electricity Board.

– For this and other conduct, CCI pleaded guilty to criminal anti-

bribery and Travel Act charges and paid an $18.2M fine.

18

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Indictment

Six Foreign Nationals (2013)

– USAO in N.D. Ill. alleged that six foreign nationals engaged in

international racketeering conspiracy involving bribes of Indian

government officials in exchange for titanium mining licenses and

– Conspiracy included sale of titanium products to unnamed “Company

A” headquartered in Chicago.

– Defendants include two Ukrainians, a Hungarian, a Sri Lankan, and

two Indians (one of whom is a US Green Card holder and the other is

an Indian MP).

– 5 out of 6 defendants remain at large; an Indian court stayed the

arrest of one of the Indian nationals, and an Austrian court refused to

extradite one of the Ukrainian defendants to the U.S., calling the

request “politically motivated.” 19

PUBLICLY REPORTED FCPA INVESTIGATIONS IN INDIA

Rolls Royce

– DOJ is investigating Rolls Royce for bribes in connection with contracts in Indonesia, China, and India. The UK SFO and India’s CBI are also investigating the allegations. In September 2014, India lifted its military procurement ban on the company.

Anheuser-Busch InBev

– Both DOJ and SEC are investigating the brewing company in connection with its Indian joint venture, InBev Indian Int’l Private Ltd. In February 2015, AB InBev ended ties with the joint venture in India that is the subject of the investigation.

Wal-Mart

– Continuing global FCPA investigation, including of Wal-Mart’s Indian joint venture with Bharti Enterprises. In late 2013, the companies announced the breakup of the joint venture.

20

OTHER PUBLICLY REPORTED DEVELOPMENTS

Alstom Network UK

– In July 2014, the UK Serious Fraud Office brought criminal charges against the British subsidiary of the company, as well as two British nationals, for corrupt practices involving transport projects in India, Poland, and Tunisia. The company allegedly paid €3.3M in bribes disguised as consultancy fees to secure infrastructure contracts relating to Delhi Metro construction.

Yara International

– In January 2014, Norwegian authorities fined the fertilizer company $48M for bribing officials in India and Libya and making corrupt payments to a supplier in Russia. Yara allegedly agreed to pay $3M in bribes to the relative of an Indian government official in connection with a joint venture with an Indian government controlled entity. Norwegian Authorities also indicted four Yara executives, who in July 2015 were sentenced to prison terms ranging from 2 to 3 years.

21

OTHER PUBLICLY REPORTED DEVELOPMENTS (CONT.)

Cryptometrics Agent

– In August 2013, Nazir Karigar, a former agent of Cryptometrics, became the first individual to be convicted of violating Canada’s Corruption of Foreign Public Officials Act. Authorities alleged that Karigar offered to bribe Indian officials to rig the bidding process for Air India contracts.

Bunge

– In June 2013, five executives of the Indian unit of the American food company Bunge resigned amid an internal audit related to the subsidiary’s purchase of land in Kandla, India.

22

CONTACTS WITH GOVERNMENT OFFICIALS IN INDIA

Public procurement/contracting with government agencies

Customs clearance/importation of goods

Immigration processes

Real estate (both purchasing and leasing land)

Tax administration (excise and sales taxes, audits)

Obtaining certificates, registrations, permits, and licenses (approval from multiple officials often required to obtain one permit/license)

Gifts and entertainment (especially during religious festival, Diwali)

Communicate expectations to vendors re ethics and anti-bribery/anti-corruption training for all high

risk vendors

Training to include discussion of India Prevention of Corruption Act

Copy of Code of Conduct

Johnson Controls, Inc. - Confidential 41

Navigating the Risks

Financial Controls

Establish monitoring process to ensure vendor transactions are for legitimate services

Red flag/warning sign training for AP function

Stringent controls around employee advances and petty cash

Evaluate use of “miscellaneous vendor codes”

Red Flag training for all finance personnel

Government Interfacing Activities

Establish “Compliance Task Force” to handle all licensing, permitting and inspection requirements

Only “Task Force’ will interface with government agencies

Administers, manages and enforces all statutory compliance activities

Communication to Customers

Need to communicate to customers that the refusal to make improper payments may slow the

process of obtaining government approvals necessary to operate

Monitor all Licensing/Permitting Activities

Review all licenses and permits necessary to conduct business

Monitoring and Auditing

Regular and periodic forensic reviews of business practices and control environment

Johnson Controls, Inc. - Confidential 42

Navigating the Risks – Monitoring/Auditing

RED FLAGS

Rumors regarding unethical or suspicious conduct by an employee, marketing representative, consultant or other business partner, or a government official

Unnecessary third-parties or multiple intermediaries

Requests for payments to a third-party rather than the consultant

Requests for payments in a third country

Business in a country with bribery problems

Requests for payment in cash

Requests for unusually large commissions or other payments, or payments that appear excessive for the service rendered

Non-government organizations, lobbying costs, public relations expenditure, political contributions etc.

Requests for reimbursement of expenses that are poorly documented

Incomplete or inaccurate information in required disclosures

Refusal to certify compliance

Government end-users

Government touch points such as customs, taxes, licenses, etc.

Previous issues, incidents

Monitoring FCPA risks in India January 2016

Michael Stavridis

44

Perceived as most corrupt sectors

Presentation title

Infrastructure and

real estate Metals and

mining

“According to 73% of the respondents from PE

firms, a company operating in a sector that is

perceived as highly corrupt, may lose ground

when it comes to a fair valuation of its business,

as it bargains hard and factors in the cost of

corruption in the sector during a transaction.”

Aerospace

and defense

Power and

utilities

45

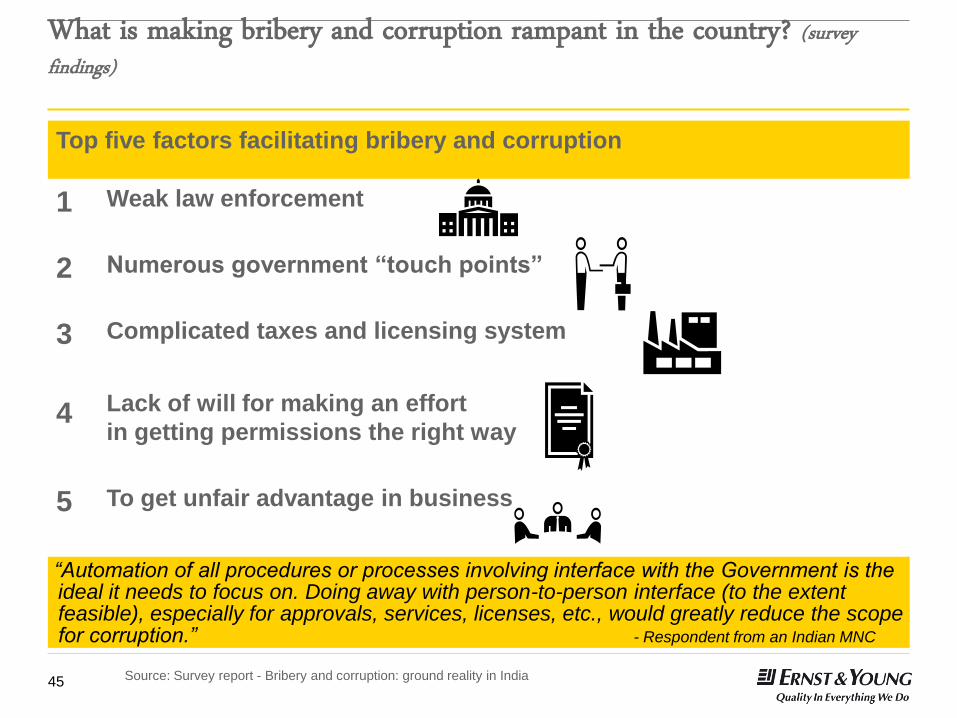

What is making bribery and corruption rampant in the country? (survey findings)

Top five factors facilitating bribery and corruption

1 Weak law enforcement

2 Numerous government “touch points”

3 Complicated taxes and licensing system

4

Lack of will for making an effort

in getting permissions the right way

5

To get unfair advantage in business

“Automation of all procedures or processes involving interface with the Government is the ideal it needs to focus on. Doing away with person-to-person interface (to the extent feasible), especially for approvals, services, licenses, etc., would greatly reduce the scope for corruption.” - Respondent from an Indian MNC

Source: Survey report - Bribery and corruption: ground reality in India

46

Production

Sourcing

Logistics

Customs CHA

Police

Labour law

officials

FDA

Municipal

dept.

Octroi

Excise

W&M

Labour

law

Shops &

Establishment

Fire

department

Sales tax

Income

tax Service

tax

Road

permits

Companies

Act

Electricity

board

Pollution Control Board

DGFT

Local + imports

Imports

Lift

license

Tax compliance

Manufacturing

a a

a a

a

a

a a

a a

a a

a a a a

a a

a

a

Indian

company

Government interaction at a glance

47

Step 1

Step 2

Step 3

Step 4 Step 5

Conversion of land

and change of land

use

Pre-approval NOCs

and clearance from

agencies

Plan sanction

Occupancy certificate

Some of the permits required

Conversion of land use

Sanction of development plan

NOC from electricity board

NOC from fire service department

NOC from Airport Authority of India

NOC from Ministry of Environment and Forest Clearance

57

172

40

Number of approvals a

builder needs to construct

a property

Number of documents a

builder has to produce

Number of departments

of central and state

governments and

municipal corporations a

builder engages

Example of licenses and permits challenges

48

Proactive

Sample FCPA compliance program framework

Reactive

Proactive

Setting the Proper Tone

Code of Ethics

FCPA Prevention Policies

FCPA Risk Assessment

FCPA Controls Monitoring

FCPA Awareness Training

Response Plan

Conduct FCPA Risk Assessment

FCPA Monitoring

Program assessment

Implementation review

Substantive review

Results drive

monitoring

49

FCPA compliance program Risk assessment criteria

Government end-users;

sales intermediaries/

direct sales

High risk geographic

markets

Significant movement of

goods/ imports/ exports/

certifications Government touch points –

VAT/ taxes/ licenses/ etc.

Travel, entertainment

and gifts, customer travel,

petty cash

50

How to monitor for corruption risks?

► What kind of testing should be conducted?

► Controls testing versus substantive testing

► Controls alone may not prevent irregularities; control testing alone may not

detect irregularities

► The DOJ/SEC guidance to the FCPA states that a compliance program that is

“followed in practice will inevitably uncover compliance weaknesses and require

enhancements” and that programs that employ a “check-the-box” approach may be

inefficient and, more importantly, ineffective”

► “DOJ and SEC evaluate whether companies regularly review and improve their

compliance programs and not allow them to become stale.”

► The UK MOJ guidance to the UK Bribery Bill requires organizations to “monitor the

ethical quality of transactions”.

51

How to monitor for corruption risks? continued

► How to choose a sampling methodology? Where and how are potential

problem payments recorded?

► Understand the business? Where are the customers? Where are the

government touch points?

► Choose accounts that could have risk – Commissions, permits, licenses,

consultants, freight forwarding, customs clearance, etc. as well as major

Government or SOE contracts/projects

► Choose T&E reports from individuals who direct or touch the risk Who manages imports/exports?

Who entertains our big Government clients?

► Controls over cash?

52

How to monitor for corruption risks? continued

► How can we leverage technology to find higher risk transactions?

► Analytics

► Key word searches on text fields in GL or T&E systems

► Who should conduct these audits?

► Experience (how many of the auditors have ever seen a bribe?)

► Local expertise (how many have ever seen a bribe in India?)

► Training

► Who should be interviewed?

► Employees

► Vendors?

53

Higher risk ledger accounts and expenses

► Obtain listing of major customers and identify potentially high risk customer

contracts

► From the chart of accounts and trial balance, select higher risk accounts for