FDI in Retail Page No| 1 FDI in Retail- A Complete Story IntroductionJust back from first frenzied shopping experience in the UK, a four year old ever-inquisitive daughter asked to her father, ³Why do we not have a Harrods in Delhi? Shopping there is so much fun!´ Simple question for a four-year-old, but not so simple for her father to exp lain. As per the current regulatory regime, retail trading (except under single-brand product retailing ² FDI up to 51 per cent, under the Government route) is prohibited in India. Simply put, for a company to be able to get foreign funding, products sold by it to the general public should only be of a µsingle-brand¶; this condition being in addition to a few other conditions to be adhered to. That explains why we do not have a Harrods in Delhi. India being a signatory to World Trade Organization¶s General Agreement on Trade in Services, which include wholesale and retailing services, had to open up the retail trade sector to foreign investment. There were initial reservations towards opening up of retail sector arising from fearof job losses, procurement from international market, competition and loss of entrepreneurial opportunities. However, the government in a series of moves has opened up the retail sectorslowly to Foreign Direct Investment (³FDI´). In 1997, FDI in cash and carry (wholesale) with 100 percent ownership was allowed under the Government approval route. It was brought underthe automatic route in 2006. 51 percent investment in a single brand retail outlet was also permitted in 2006. FDI in Multi-Brand retailing is prohibited in India. Currently in 2011, UPA government proposed for allowing 51 percent investment in multi-brand retailing and 100 percent in si ngle brand retailing which due to lack of political consensus the decision is s till pending. Definition of RetailIn 2004, The High Court of Delhi defined the term µretail¶ as a sale for final consumption in contrast to a sale for further sale or processing (i.e. wholesale). A sale to the ultimate consumer. Thus,retailing can be said to be the interface between the producer and the individual consumerbuying for personal consumption. This excludes direct interface between the manufacturer and institutional buyers such as the government and other bulk customers retailing is the last link that connects the individual consumer with the manufacturing and distribution chain. A retailer is involved in the act o f selling goods to the individual consumer at a margin of profit.

Just back from first frenzied shopping experience in the UK, a four year old ever-inquisitivedaughter asked to her father, ³Why do we not have a Harrods in Delhi? Shopping there is somuch fun!´ Simple question for a four-year-old, but not so simple for her father to explain.

As per the current regulatory regime, retail trading (except under single-brand product retailing ² FDI up to 51 per cent, under the Government route) is prohibited in India. Simply put, for acompany to be able to get foreign funding, products sold by it to the general public should only be of a µsingle-brand¶; this condition being in addition to a few other conditions to be adhered to.That explains why we do not have a Harrods in Delhi.

India being a signatory to World Trade Organization¶s General Agreement on Trade in Services,which include wholesale and retailing services, had to open up the retail trade sector to foreigninvestment. There were initial reservations towards opening up of retail sector arising from fear of job losses, procurement from international market, competition and loss of entrepreneurialopportunities. However, the government in a series of moves has opened up the retail sector slowly to Foreign Direct Investment (³FDI´). In 1997, FDI in cash and carry (wholesale) with100 percent ownership was allowed under the Government approval route. It was brought under the automatic route in 2006. 51 percent investment in a single brand retail outlet was also permitted in 2006. FDI in Multi-Brand retailing is prohibited in India. Currently in 2011, UPAgovernment proposed for allowing 51 percent investment in multi-brand retailing and 100

percent in single brand retailing which due to lack of political consensus the decision is still pending.

Definition of Retail

In 2004, The High Court of Delhi defined the term µretail¶ as a sale for final consumption incontrast to a sale for further sale or processing (i.e. wholesale). A sale to the ultimate consumer.

Thus, retailing can be said to be the interface between the producer and the individual consumer buying for personal consumption. This excludes direct interface between the manufacturer andinstitutional buyers such as the government and other bulk customers retailing is the last link thatconnects the individual consumer with the manufacturing and distribution chain. A retailer isinvolved in the act of selling goods to the individual consumer at a margin of profit.

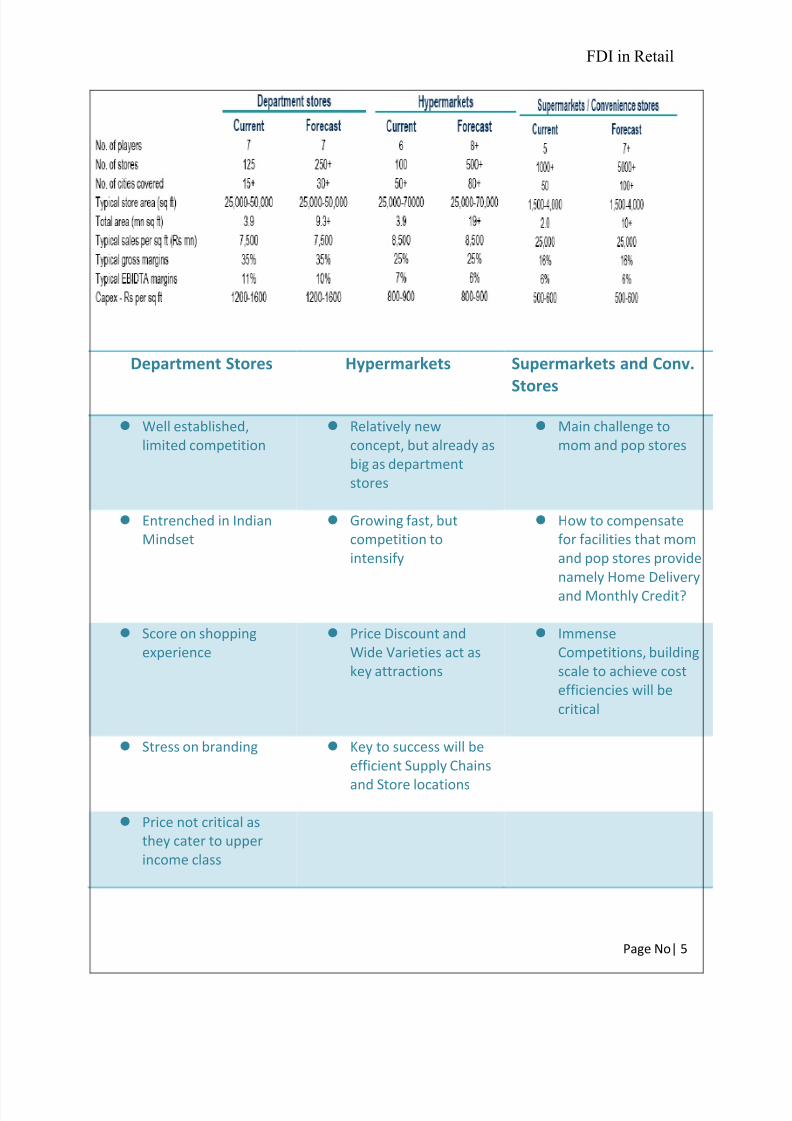

Division of Retail Industry ± Organized and Unorganized Retailing

The retail industry is mainly divided into: - 1) Organized and 2) Unorganized Retailing

Organized retailing refers to trading activities undertaken by licensed retailers, that is, those who

are registered for sales tax, income tax, etc. These include the corporate-backed hypermarketsand retail chains, and also the privately owned large retail businesses.

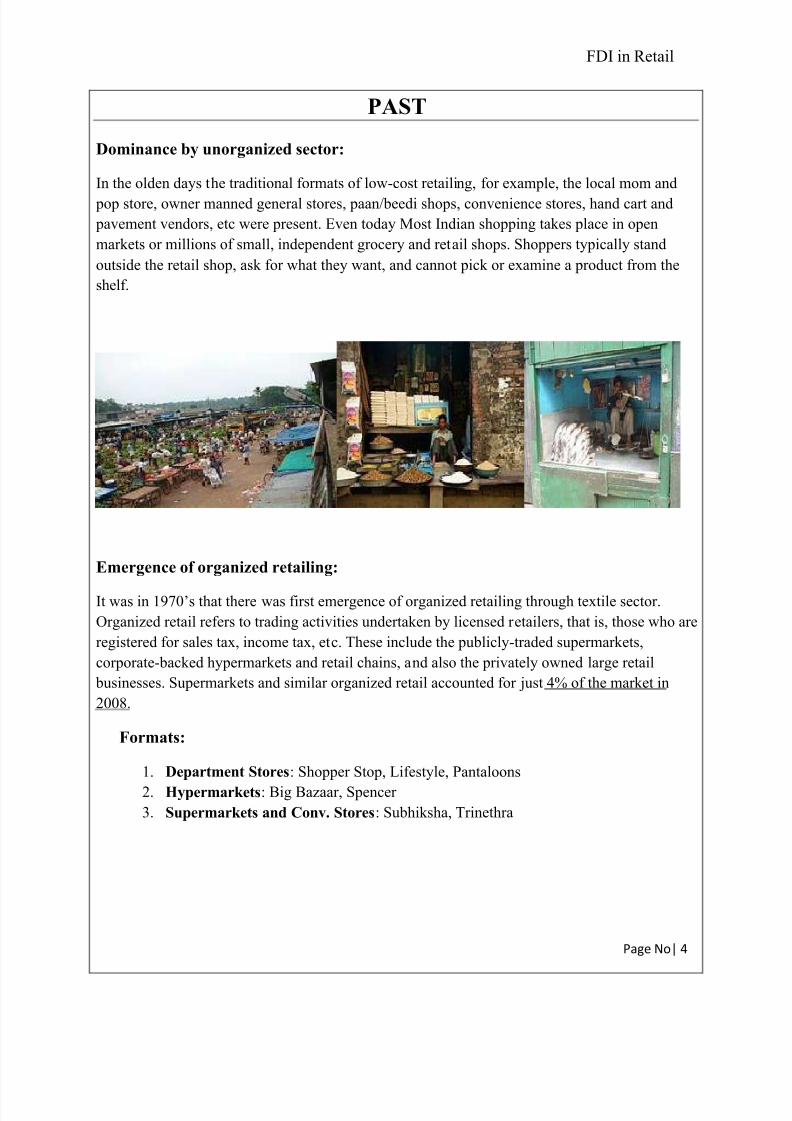

Unorganized retailing, on the other hand, refers to the traditional formats of low-cost retailing,for example, the local kirana shops, owner manned general stores, paan/beedi shops,convenience stores, hand cart and pavement vendors, etc.

The Indian retail sector is highly fragmented with 97 per cent of its business being run by theunorganized retailers. The organized retail however is at a very nascent stage. The sector is thelargest source of employment after agriculture, and has deep penetration into rural Indiagenerating more than 10 per cent of India¶s GDP.

Few facts about the Indian Retail sector:

1. Indian Retail sector is the fifth largest global retail destination. Offering a market of 1.2

billion people.

2. Indian retail business values at around US$ 450 billion

3. It is dominated by the unorganized sector with 97% of its business coming from the

traditional run family stores and corner stores.

4. It is estimated that the Indian retail market generates sales of about $470 billion a year, of which a miniscule $27 billion comes from the organized retail sector.

5. India's retail and logistics industry, organized and unorganized in combination, employs

about 40 million Indians (3.3% of Indian population)

6. The Economist forecasts that Indian retail will nearly double in economic value,

expanding by about $400 billion by 2020.

7. Its contribution to the economy accounts for about 15% of GDP.

8. The Indian retail market has been ranked by AT Kearney's eighth annual Global Retail

Development Index (GRDI), in 2009 as the most attractive emerging market for

investment in the retail sector.

9. More than 80% of the retail sector in the country is concentrated in the large cities. A

study reveals that among the more than 20 locations, for organized retail in India,

Mumbai was found to be the most preferred location followed closely by Bengaluru in

India permits 100% FDI in cash & carry and wholesale trading (which is business-to-business).

A cash n carry is a B2B format that refers to the purchasing of merchandise by customers which

consists of retailers, professional users, caterers, institutional buyers, etc. As the name suggests,

the payment is made in cash on the spot and the merchandise is carried away by the customersthemselves. No such service as µDelivery¶ exists in this retail format. These outlets do not make

sales to individual buyers.

Players in the business

Metro Cash and Carry India, a 100 per cent subsidiary of Metro Cash and Carry InternationalGmbH, Germany, were the first to foray onto the Indian shores more than seven years ago withtheir first store in Bengaluru. Besides this, another important player is UK¶s largest retailer Tesco. They have also set up cash & carry outlets in the country. The latest on the scene is BhartiWal-Mart Pvt. Ltd, the joint venture between Bharti Enterprises and Wal-Mart Stores Inc who

has just opened their second cash and carry outlet, µBest Price Modern Wholesale cash-and-carrystore¶ in Punjab.

FDI in Single Brand Retail

In single-brand retail, FDI up to 51 per cent is allowed, subject to Foreign Investment PromotionBoard (FIPB) approval and subject to the conditions mentioned in Press Note 3 that (a) onlysingle brand products would be sold (i.e., retail of goods of multi-brand even if produced by thesame manufacturer would not be allowed), (b) products should be sold under the same brandinternationally, (c) single-brand product retail would only cover products which are brandedduring manufacturing and (d) any addition to product categories to be sold under ³single-brand´

would require fresh approval from the government.

While the phrase µsingle brand¶ has not been defined, it implies that foreign companies would beallowed to sell goods sold internationally under a µsingle brand¶, viz., Reebok, Nokia, Adidas.Retailing of goods of multiple brands, even if such products were produced by the samemanufacturer, would not be allowed.

Going a step further, we examine the concept of µsingle brand¶ and the associated conditions:

FDI in µSingle brand¶ retail implies that a retail store with foreign investment can only sell one brand. For example, if Adidas were to obtain permission to retail its flagship brand in India,those retail outlets could only sell products under the Adidas brand and not the Reebok brand, for which separate permission is required. If granted permission, Adidas could sell products under the Reebok brand in separate outlets.

FDI in Multi Brand Retail

The government has also not defined the term Multi Brand. FDI in Multi Brand retail impliesthat a retail store with a foreign investment can sell multiple brands under one roof.

In July 2010, Department of Industrial Policy and Promotion (DIPP), Ministry of Commercecirculated a discussion paper on allowing FDI in multi-brand retail. The paper doesn¶t suggest

any upper limit on FDI in multi-brand retail. If implemented, it would open the doors for global

retail giants to enter and establish their footprints on the retail landscape of India. Opening upFDI in multi-brand retail will mean that global retailers including Wal-Mart, Carrefour andTesco can open stores offering a range of household items and grocery directly to consumers inthe same way as the ubiquitous ¶kirana¶ store.

As per the current regulatory regime, retail trading (except under single-brand product retailing ² FDI up to 51 per cent, under the Government route) is prohibited in India. Simply put, for acompany to be able to get foreign funding, products sold by it to the general public should only

be of a µsingle-brand¶; this condition being in addition to a few other conditions to be adhered to.

India being a signatory to World Trade Organization¶s General Agreement on Trade in Services,which include wholesale and retailing services, had to open up the retail trade sector to foreigninvestment. There were initial reservations towards opening up of retail sector arising from fear of job losses, procurement from international market, competition and loss of entrepreneurialopportunities. However, the government in a series of moves has opened up the retail sector slowly to Foreign Direct Investment (³FDI´). In 1997, FDI in cash and carry (wholesale) with100 percent ownership was allowed under the Government approval route. It was brought under the automatic route in 2006. 51 percent investment in a single brand retail outlet was also permitted in 2006. FDI in Multi-Brand retailing is prohibited in India.

FDI Policy with Regard to Retailing in India

a) FDI up to 100% for cash and carry wholesale trading and export trading allowed under the automatic route.

b) FDI up to 51 % with prior Government approval (i.e. FIPB) for retail trade of µSingleBrand¶ products (2006 Series)

c) FDI is not permitted in Multi Brand Retailing in India.

PROPOSED GOVERNMENT POLICY

a) FDI up to 100% in µsingle brand¶ retail b) FDI up to 51% in µmulti brand¶ retail

Though the above two recommendations come with riders like 50% of the investment and jobsshould go to the rural areas, 30% of the inputs should be sourced from medium and smallenterprises and investment in infrastructure.

FDI in retail is an economic reform, which would allow global chains like Wal-Mart Stores Incand Carrefour to own up to 51 percent of retail ventures. The policy would let foreign retailersown up to 51 percent of supermarkets and 100 percent of single-brand stores. The policy doesn'trequire parliamentary approval, but foreign retailers must get approval from state governments

where stores will be located.

Multi-brand retail in India is largely in the unorganised sector dominated by neighbourhoodkirana stores and there is a concern among political parties and traders that these stores would beaffected by the entry of global retailers.

The decision to increase FDI in single brand retail was taken by the Cabinet on November 24along with opening the gates for overseas investment in the multi-brand retail.

However, the government was forced to put on hold FDI in multi-brand retail by several political parties, including UPA ally Trinamul Congress.

MAJOR RETAIL PLAYERS IN INDIA

Growth of Retail Companies in India is still not yet in a matured stage with great potentialswithin this sector still to be explored. The retail industry is mainly divided into: -

y Organized and

y Unorganized Retailing

Organized retailing refers to trading activities undertaken by licensed retailers, that is, those whoare registered for sales tax, income tax, etc. These include the corporate-backed hypermarketsand retail chains, and also the privately owned large retail businesses.

Unorganized retailing, on the other hand, refers to the traditional formats of low-cost retailing,

for example, the local kirana shops, owner manned general stores, paan/beedi shops,convenience stores, hand cart and pavement vendors, etc.

According to a report by McKinsey & Co., the organized retail market in India is expected togrow to 14-18% by 2015 of the total retail market in India from 8% in 2008. Its value isestimated to be around US$450 billion by 2015.

The following are some major organized retailers in India:

1. Future Group

Future Group offers innovative offerings at affordable prices tailored to the needs of everyIndian household. Future Group strategy is based on a deep understanding of Indian consumers,the products they want, and making these products available in every city, in every store format.They are known as the ³Pioneers in the India¶s retail space´; their formats are household namesin more than 85 cities and 60 rural locations across the country. Their stores cover around 15million square feet of retail space and attract around 220 million customers each year.

Reliance Retail, Ltd. is a subsidiary company of Reliance Industries. RRL was founded in theyear 2006 in Mumbai. It is the second largest retailer in India. Its retail outlets offer foods,groceries, apparel and footwear, lifestyle and home improvement products, electronic goods, andfarm implements and inputs. RRL possesses brands like Reliance Fresh, Reliance Footprint,Reliance Time Out, Reliance Digital, Reliance Wellness, Reliance Trendz, Reliance Autozone,

Reliance Super, Reliance Mart, Reliance iStore, Reliance Home Kitchens, Reliance Market(Cash n Carry) and Reliance Jewel.

3. Shoppers'Stop

Shoppers Stop is an Indian department store chain promoted by the K Raheja Corp Group(Chandru L Raheja Group), started in the year 1991 with its first store in Andheri,Mumbai. Shoppers Stop Ltd has been awarded "the Hall of Fame" and won "the EmergingMarket Retailer of the Year Award", by World Retail Congress at Barcelona, on April 10,2008. Shoppers Stop is listed on the BSE. Till date, Shoppers Stop has put together 97 storesin India.

4. Aditya Birla Group

Aditya Birla Retail Limited, is the retail arm of Aditya Birla Group, a USD 28 billionCorporation. The Company ventured into food and grocery retail sector in 2007 with theacquisition of a south based supermarket chain. Subsequently Aditya Birla RetailLimited.expanded its presence across the country under the brand "more." with 2 formatsSupermarket & Hypermarket. Aditya Birla Retail Limited currently has employee strength of over 11,000.

Supermarket

³More´. ± Located in neighbourhood¶s, it sells a range of fresh fruits & vegetables, groceries, personal care, home care, general merchandise & a basic range of apparels. Currently, there areover 600 more. supermarkets across the country.

Hypermarket

more.MEGASTORE ± It sells a range of products across fruits and vegetables, groceries, FMCG products. more.MEGASTORE also has a strong emphasis on general merchandise, apparels &CDIT.

Currently, thirteen hypermarkets operate under the brand more.MEGASTORE in Mysore,Vadodara, Aurangabad, Indore, Bengaluru (3), Mumbai, New Delhi (2), Hyderabad, Nasik andVashi.

Private labelsAditya Birla Retail Limited provides customers products under its own labels. Private label FoodBrands include Feasters, Kitchen's Promise, and Best of India. Home & Personal care brandsinclude Enriche, 110%, Pestex, Paradise and Germex.

Subhiksha was an Indian retail chain with 1600 outlets selling groceries, fruits, vegetables,medicines and mobile phones. It began operations in 1997, and was closed down in 2009 owingto financial mismanagement and a severe cash crunch.

6. Spencer Group

Spencer's Retail is one of India¶s fastest growing retail stores.Spencer's is based on the 'FoodFirst' Format (it mainly offers fresh and packaged food). Many outlets though sport multipleformats for retailing food, apparel, fashion, electronics, lifestyle products, music and books. It isowned by the RPG Group, a major business house.

Established in 1996, Spencer¶s is one of the popular destinations for shoppers in Indiawith supermarkets, hypermarkets and dailies spread all over India.

7. Trent

Rent is the retail arm of the Tata group. Started in 1998, Trent operates Westside, one of themany growing retail chains in India based in Mumbai, Maharashtra.

Trent also operates the newly launched hypermarket, Star Bazaar which is situatedin Ahmedabad, Bangalore, Pune, Coimbatore, Chennai and Mumbai. In Aug, 2005 Trentacquired a 76% controlling stake in Landmark, a Chennai-based privately owned books andmusic retailer and completed 100% acquisition in April 2008. Landmark currently has 16 stores.

8. Tata ± Croma

Crom is an Indian retail chain for consumer electronics and durables. Tata GroupCompany Infiniti Retail runs Crom stores in India. Infiniti Retail Ltd is a 100% subsidiary of TATA Sons. Presently, there are a total of 71 Crom stores in India. The Crom Zip store is anoutlet for portable electronic items and meant for the mobile consumer. The first Zip store wasopened on Jun 22, 2007 at the Mumbai domestic airport. Crom claims to offer 6000 productsacross 8 categories.

Croma stores are spread across the states of Maharashtra (Mumbai, Pune, Aurangabad),Gujarat(Ahmedabad, Rajkot, Surat, Vadodara), DelhiNCR, Karnataka (Bangalore), Punjab(Amritsar, Jalandhar), Chandigarh, Tamil Nadu (Chennai) and Andhra Pradesh (Hyderabad).

9. Bharti

Bharti Retail Ltd. is a wholly owned subsidiary of Bharti Enterprises. Bharti Retail operates achain of multiple format stores. Recently the company has become more involved inthe food economic sectors, with a joint partnership in the agricultural company FieldFresh.

Bharti Enterprises tied-up with Wal-Mart for opening a chain of retail stores all over India.Though the retail chain store venture is yet to see the light, the two companies, in August 2007,

made a surprise statement that they have signed a wholesale cash-and-carry deal. The other retailcompanies of Bharti group are Bharti Retail (Holdings) Private Limited, Bharti Retail ResourcesPrivate Limited and Cedar Support Services Ltd.

10. McDonalds

McDonald's has a wide network of outlets throughout the country. The company started itsoperations in India in 1996. In India, it is a 50-50 joint venture partnership between McDonald¶sCorporation (US) and two Indian businessmen Amit Jatia and Vikram Bakshi.

GOVERNMENT VIEW IN FAVOUR OF FDI

The Indian government is keen to allow FDI in India supporting its argument with the following:

* Huge investments in the retail sector will see gainful employment opportunities in agro- processing, sorting, marketing, logistics management and front-end retail.

* At least 10 million jobs will be created in the next three years in the retail sector.

* FDI in retail will help farmers¶ secure remunerative prices by eliminating exploitativemiddlemen.

* Foreign retail majors will ensure supply chain efficiencies.

* Policy mandates a minimum investment of $100 million with at least half the amount to beinvested in back-end infrastructure, including cold chains, refrigeration, transportation, packing,sorting and processing. This is expected to considerably reduce post-harvest losses.

*This will have a salutary impact on food inflation from efficiencies in supply chain. This is also because food, which perishes due to inadequate infrastructure, will not be wasted.

* Sourcing of a minimum of 30% from Indian micro and small industry is mandatory. This will provide the scales to encourage domestic value addition and manufacturing, thereby creating amultiplier effect for employment, technology upgradation and income generation.

* A strong legal framework in the form of the Competition Commission is available to deal withany anti-competitive practices, including predatory pricing.

* There has been impressive growth in retail and wholesale trade after China approved 100%FDI in retail. Thailand has experienced tremendous growth in the agro-processing industry.

* In Indonesia, even after several years of emergence of supermarkets, 90% of fresh food and70% of all food is still controlled by traditional retailers.

* In any case, organized retail through Indian corporates is permissible. Experience of the lastdecade shows small retailers have flourished in harmony with large outlets.

OPPOSITIONS VIEW FOR OPPOSING FDI

The following are the reasons why the opposition is against allowing FDI in India.

* Move will lead to large-scale job losses. International experience shows supermarketsinvariably displace small retailers. Small retail has virtually been wiped out in developedcountries like the US and in Europe. South East Asian countries had to impose stringent zoningand licensing regulations to restrict growth of supermarkets after small retailers were gettingdisplaced. India has the highest shopping density in the world with 11 shops per 1,000 people. Ithas 1.2 crore shops employing over 4 crore people; 95% of these are small shops run by self-

employed people

* Global retail giants will resort to predatory pricing to create monopoly/oligopoly. This canresult in essentials, including food supplies, being controlled by foreign organizations.

* Fragmented markets give larger options to consumers. Consolidated markets make theconsumer captive. Allowing foreign players with deep pockets leads to consolidation.International retail does not create additional markets, it merely displaces existing markets.

* Jobs in the manufacturing sector will be lost because structured international retail makes purchases internationally and not from domestic sources. This has been the experience of most

countries which have allowed FDI in retail.

* Argument that only foreign players can create the supply chain for farm produce is bogus.International retail players have no role in building roads or generating power. They are onlyrequired to create storage facilities and cold chains. This could be done by governments in India.

* Comparison between India and China is misplaced. China is predominantly a manufacturingeconomy. It's the largest supplier to Wal-Mart and other international majors. It obviously cannotsay no to these chains opening stores in China when it is a global supplier to them. India incontrast will lose both manufacturing and services jobs.

After taking into account the government¶s view in favor of the FDI policy and the oppositionsview arguing against FDI, the following is our proposition.

y The government should not prevent anybody, Indian or foreign, from setting up any business unless there are very good reasons to do so. Hence, unless it can be shown that

FDI in retail will do more harm than good for the economy, it should be allowed.y A major argument given by opponents of FDI in retail is that there will be major job

losses. Big retail chains are actually going to hire a lot of people. So, in the short run,there will be a spurt in jobs. Eventually, there's likely to be a redistribution of jobs withsome drying up (like that of middlemen) and some new ones sprouting up.

y Fears of small shopkeepers getting displaced are vastly exaggerated. When domesticmajors were allowed to invest in retail, both supermarket chains and neighborhood pop-and-mom stores coexisted. It's not going to be any different when FDI in retail is allowed.Who, after all, will give home delivery? The local kirana. Why would anyone shun them?

y If anything, the entry of retail big boys is likely to hot up competition, giving consumersa better deal, both in prices and choices. Mega retail chains need to keep price points low

and attractive - that's the USP of their business. This is done by smart procurement andinventory management: Good practices from which Indian retail can also learn.

y The argument that farmers will suffer once global retail has developed a virtualmonopoly is also weak. To begin with, it's very unlikely that global retail will ever become monopolies. Stores like Wal-Mart or Tesco are by definition few, on the outskirtsof cities (to keep real estate costs low), and can't intrude into the territory of local kiranas.So, how will they gobble up the local guy? Secondly, it can't be anyone's case thatfarmers are getting a good deal right now. The fact is that farmers barely subsist whilemiddlemen take the cream. Let's not get dreamy about this unequal relationship.

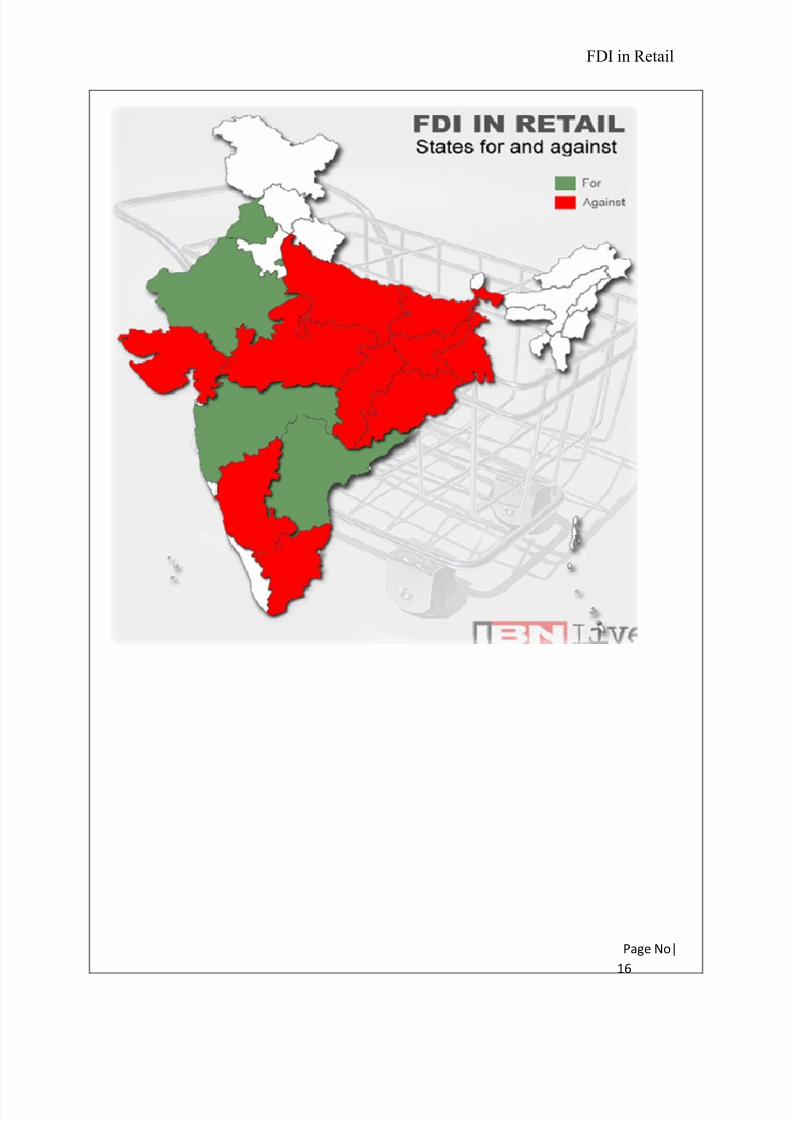

STATES FOR AND AGAINST FDI IN RETAIL

The states that are against FDI in retail are Uttar Pradesh, Madhya Pradesh, Gujarat, Karnataka,Tamil Nadu, Bihar, Jharkhand, Chhattisgarh, West Bengal and Orissa.The states that support allowing FDI in retail include Delhi, Rajasthan, Maharashtra, Punjab andAndhra Pradesh.The UPA government has cleared 51 per cent FDI in multi-brand retail and 100 per cent FDI insingle-brand retail, which means global giants like Walmart, Tesco can open outlets in India. BigMNCs can also jointly own Indian retail chains.

Allowing FDI in retail is a long-pending decision and one that is being seen as a positive step by

some sections of the retail industry. Experts say FDI in multi-brand retail will strengthen India¶sinefficient food distribution system, which causes food wastage, which in turn, leads to high foodinflation.

India has a high malnutrition rate and high food inflation because of wastage of food. India losesaround 30% to 40% of its food produce, because of lack of refrigerated transportation and coldstorage. The wastage of food creates an artificial scarcity, which in turn increases the prices of food articles.

The argument in favour of FDI in retail industry is that if foreign retailers such as Wal-Martopen shop in India, the investments they make in supply chain and logistics could bring down

food wastage and subsequently food inflation, which has been hovering around 10.5%, sinceDecember ¶10.

India¶s commerce minister Anand Sharma believes that besides reducing food wastage, the policy would have a³multiplier effect´ and tens of millions of people would gain jobs.

The reforms will ³give a fillip to job creation´, generating up to 10 million jobs over a three-year period in areas such as packaging, canning and transportation, Sharma told a news conferencerecently.

³We hope that an excess of four million jobs will be created and anywhere between five to six

million jobs will be created in logistics over a period of three years,´ Sharma said. Experts also believe that with the entry of foreign retailers, farmers will gain from better market access andfarmers¶ income will go up.

In fact, farmers have already benefited from direct purchase from farms by cash and carryretailers such as Bharti Wal-Mart, which has a store in Amritsar. Farmers say that such direct purchase gives them better returns than selling their produce in the local mandi.

Payments for the produce procured from farms are directly credited to the farmers¶ accounts,which free them from commission agents, who usually act as middlemen between farmers andthe retailers.

The government has also built in sufficient safeguards to allay fears of farmers and smallretailers. Commerce minister Sharma said the new rule would only apply to cities with a population of more than one million people. India has about 42 such cities.

Foreign retailers will have to invest a minimum of $100 million and half of this would have to beinvested in back-end infrastructure such as cold storage and refrigerated transport by them. Back-end, however, does not include investment in land and front-end stores.

The government will have the first right to procure farm products and foreign companiesinvesting more than 51% in single-brand retail stores must source at least 30% of themanufactured and processed products from small-scale Indian companies, a governmentstatement quoting the commerce minister said.

The government has also clarified that FDI in retail will benefit consumers, because it willincrease competition among retailers, which will improve quality of products and lower prices.

Currently, there is a huge gap between the retail price that is paid by a consumer and the price atwhich the product is procured from the farmers.

Once the retail sector is opened up for FDI, large retailers can save on commission costs by buying food produce directly from the farmers andthus buy products at a cheaper price.

Large foreign retailers, such as Wal-Mart and Tesco, which have lobbied for years, to buildstores in India have welcomed the government¶s FDI policy.

³This legal evolution should contribute to modernizing the Indian food supply chain and to fightagainst food inflation for the benefit of Indian customers. The decision will help farmers in Indiaand the nation¶s general economic development,´ Carrefour said in a statement.

Tesco also welcomed the decision. ³Allowing foreign direct investment in the retail sector would be good news for Indian consumers and businesses and we await further details on anyconditions,´ the company said in a statement.

A few of the multi-brand retailers are already present in India, though they do not sell directly toconsumers. US-based Wal-Mart has been operating in India as a wholesale retailer through a

50:50 joint venture, with Bharti Enterprises, since 2007.

France¶s Carrefour, is operating as a wholesale retailer in India since the year 2010. Similarly,UK¶s Tesco has a joint venture with the Tata group-led Trent for wholesale business sincearound 2008.

FDI in retail will also benefit domestic retailers such as Spencer¶s, Foodworld Supermarkets Ltd, Nilgiri¶s and ShopRite, which have been struggling to raise cash.

Effectively it will be more towards sourcing and logistics, if you see the best practices they have.So, when we are talking about logistics, it is also the supply chain and back-end practices which

they have that will be of a definite advantage for us. Foreignplayers would come with the best practices, which they have experienced but they will have adapted it to the country.

since 50% of the investment was proposed in the rural sector, it would help build infrastructure,including setting up of cold chains, which would help in cutting losses that arise out of wastageof food, due to lack of refrigerated storage facility.

The progression to FDI in multi-brand retailing cannot take place at the cost of vital concerns

raised in connection with this possible change by different groups; the question of adaptability of

the retailers in the unorganized sector, the question as to how the FDI in retailing can be

harnessed for the benefits of Indian agriculture and Medium and Small Enterprise and above allhow to impart into the economy a degree of resilience to withstand the changes that would be

ushered in the wake of introduction of FDI in retailing. All these concerns have to be addressed

not because the Left wing political parties and the media through their campaign have

necessitated such attention but because we are constitutionally bound to do so.

1. Indian agriculture has long been a source of livelihood for the teeming millions of the country

(provides employment to more than 50% of India¶s labor force) so much so that it is massively

over-crowded now. Besides, during the lean season even the productive farmer find themselves

unemployed. Although the manufacturing is a labor absorbing sector, its true potential has not

been harnessed as yet and it has been stagnating since the tenth five year plan. Retailing helps inabsorbing these shocks providing safety-net and opportunities to the superfluous labor to eke out

a living where all other sectors have not been able to. Critics fear that the inflow of FDI in

retailing will restrict the labor absorbing capacity of the retailing sector since the international

retailing giants employ labor saving machinery and knowhow both to add value to their service

as well as to enhance their profit. And given the fact that the manufacturing is not in a vibrating

state to absorb those who are displaced from the retailing by the advent of FDI, the poor and the

unemployed will find the going very difficult for them. There will be a hike in the rate of both

unemployment and underemployment.

2. It has also been said that the domestic organized retailing is underdeveloped and in anascent stage. Therefore, it is important that the domestic retailing sector is allowed to grow and

consolidate first before the sector is opened to FDI. FDI in retailing may also widen the rural -

urban divide in the sense that most of the retailing centers would be set up in the cities where

both the density of population and level of income of the people are high. These retail centers

would also attract cheap labor from the rural areas and thereby deplete the neighborhood of its

workforce. In addition, organized retailing with FDI would result in bevy of buildings and

multiplexes. Unless their constructions are regulated, they will also add to the chaotic muddle of

urbanscape.

3. It may bring down prices initially, but fuel inflation once multinational companies get astronghold in the retail market. These multi national brands will sell their produce at a very

cheap rate when the newly entre the market and the consumers will prefer their brands over

domestic brands because of the price difference, but eventually they will have a monopoly over

the entire market. The benefit is short term. The SME¶s will also get affected due to the

predatory pricing policies of multinational retailers