Feasibility Study provisional results: • 652,500oz @ 2.14g/t Au Mining Inventory • +/-90,000ozpa and 600,000oz life-of-mine production • 7 year initial mine-life • 91.1% average gold recovery and 5.7:1 waste to ore strip ratio • $697/oz cash operating cost (C1) • $830/oz all-in-sustaining cost* • $40Mpa average net operating cash flow (post tax) • $168M establishment capital cost plus $27M mining fleet Additional work planned to enhance overall returns: • Operating cost review to lift Mineral Resource-to-Mineral Reserve conversion • Julie plant configuration options to reduce operating costs, lower cut-off grade and increase Ore Reserves • Government engagement regarding regional specific and other concessions to reduce capital and operating costs and overall fiscal imposts • Continuation of exploration to boost Mineral Resources, mining inventory and mine life. Other attributes: • 2.0Moz Mineral Resource and considerable opportunity to expand • 15 year Mining Leases granted • Grid power, excellent access and infrastructure • Strong community support and no communities to relocate ASX & Media Release ASX Code – AZM 23 rd March 2015 www.azumahresources.com.au Investment Highlights: Wa Gold Project: • 2.0Moz Mineral Resource including 1.3Moz Measured & Indicated • 624,000oz Ore Reserves at 2.14 g/t plus 28,500oz ‘mining inventory’ • Feasibility Study completed • Initial 7yr mine-life at +/-90,000oz pa • Excellent Infrastructure (grid power, water, established roads, airport) • Mining Leases granted • 2,800km 2 licenses with >150km strike of prospective Birimian terrain. • 15% strategic investment in neighbour, Castle Minerals Limited (~10,000km 2 ) • Board and management team of successful explorers, mining and corporate professionals Issued Capital: 393.850M ordinary shares 6.075M performance rights 2.0M $1.00 Converting Notes Directors & Management: Chairman: Michael Atkins Managing Director: Stephen Stone Non-Executive Directors: Geoff M Jones Bill LeClair Company Secretary: Dennis Wilkins Contact: Stephen Stone Mb: +61 (0) 418 804 564 [email protected]Feasibility Study Status Update and Provisonal Results Wa Gold Project, Ghana • All-in-sustaining-costs (AISC) comprise all cash costs (C1) plus royalties and post- establishment capital costs related to sustaining production • All amounts are in US$ unless specifically stated • Rounding of numbers may result in minor inconsistencies Page 1 of 15

Transcript

Feasibility Study provisional results:

• 652,500oz @ 2.14g/t Au Mining Inventory

• +/-90,000ozpa and 600,000oz life-of-mine production

• 7 year initial mine-life

• 91.1% average gold recovery and 5.7:1 waste to ore strip ratio

• $697/oz cash operating cost (C1)

• $830/oz all-in-sustaining cost*

• $40Mpa average net operating cash flow (post tax)

• $168M establishment capital cost plus $27M mining fleet Additional work planned to enhance overall returns:

• Operating cost review to lift Mineral Resource-to-Mineral Reserve conversion

• Julie plant configuration options to reduce operating costs, lower cut-off grade and increase Ore Reserves

• Government engagement regarding regional specific and other concessions to reduce capital and operating costs and overall fiscal imposts

• Continuation of exploration to boost Mineral Resources, mining inventory and mine life.

Other attributes:

• 2.0Moz Mineral Resource and considerable opportunity to expand

• 15 year Mining Leases granted

• Grid power, excellent access and infrastructure

• Strong community support and no communities to relocate

ASX & Media Release

ASX Code – AZM 23rd March 2015

www.azumahresources.com.au

Investment Highlights:

Wa Gold Project:

• 2.0Moz Mineral Resource including 1.3Moz Measured & Indicated

• 624,000oz Ore Reserves at 2.14 g/t plus 28,500oz ‘mining inventory’

• Feasibility Study completed

• Initial 7yr mine-life at +/-90,000oz pa

• Excellent Infrastructure (grid power, water, established roads, airport)

• Mining Leases granted

• 2,800km2 licenses with >150km strike of prospective Birimian terrain.

• 15% strategic investment in neighbour, Castle Minerals Limited (~10,000km2)

• Board and management team of successful explorers, mining and corporate professionals

Issued Capital: 393.850M ordinary shares 6.075M performance rights

Azumah Resources Limited – Feasibility Study Update – March 2015

“Provisional Study results confirm a solid Project with no technical, social or environmental impediments to development, improved fundamentals such as mine-life, ore grade and strip-ratio plus operating and capital costs in-line with, if not better than, guidance provided when Ore Reserves were issued last year” said Azumah Managing Director Stephen Stone.

“Azumah is very conscious of the present commercial climate and prior to Study finalisation it is focusing on several areas that can better position the Project for financing and development”.

“The existing 2.0Moz Mineral Resources highlight that any further reductions in operating costs will translate to enlarged pits and higher gold production. Recent exploration results confirm the 2,800km2 Project’s underlying prospectivity and underpin our confidence that we will continue to increase Minerals Resources, convert these to Ore Reserves and increase mine-life”.

Perth-based gold explorer and developer Azumah Resources Limited (ASX:AZM) (“Azumah” or “the Company”) advises that the GR Engineering Limited (“GRES”) managed Feasibility Study (“Study”) for the Wa Gold Project (“Project”), northwest Ghana, West Africa has progressed to a stage where provisional results can be released and a plan to optimise the Study progressed.

Study progress and provisional operational results, which are generally in-line with or better than previous guidance issued at the time of the September 2014 Ore Reserve increase announcement, are now reported (refer ASX release dated 2nd September 2014).

These outputs and the Study finalisation, inclusive of final reporting of financial returns, are subject to several enhancement options now being evaluated and progressed. Individually or combined, they could have a materially positive impact on overall returns and better position the Project for financing and development in the prevailing commercial environment. These options are:

Opportunities to further reduce operating costs, which along with any increase in the gold price, will enlarge pits, increase the Mining Inventory and mine-life and reduce costs per ounce gold produced, without the need for further driling.

Julie mining and processing options including possibly a stand-alone processing capability at Julie. Under the present Study scope current costs include $11M for the installation of a haul road and $35M for Julie ore to be hauled to Kunche for processing. This has the present impact of increasing the Julie cut-off grade, reducing Julie Ore Reserves and increasing production costs.

The option of a stand-alone plant at Julie is one of the reasons that mining at Julie has been deliberately deferred to at least year 4, by which time there may also have been an increase in Mineral Resources and/or the gold price.

Advancing discussions with the Government of Ghana to co-operatively identify regional specific taxation and fixed impost concessions that could materially reduce capital and operating costs and improve bottom-line returns.

In addition, but not a part of the Study per se, Azumah will continue to explore its 2,800km2 tenure encompassing large tracts of fertile Birimian terrain in order to maintain its track-record of discovery and increasing Mining Inventory with a commensurate increase in mine-life and overall returns (refer ASX release dated 12th March 2015).

Provisional Study Results pending enhancement options

The Study comprises a rigorous technical review of the Project to assess the impact of a considerably increased Julie Mineral Resource, expanded Mining Inventory of 652,500oz and extensive confirmatory metallurgical test work.

Page 2 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

The Project is based on a conventional carbon in leach (CIL) gold plant located adjacent to the flagship 1.4km strike Kunche deposit which will treat 1.2Mtpa of primary ore and up to 1.8Mtpa of softer oxide and transition ore.

Ore will be sourced from the staged mining of a series of shallow open pits at Kunche, Bepkong and Aduane in the Wa Lawra district with ore from Julie and Collette in the Wa East area trucked on mostly public roads to the Kunche plant.

Provisional outputs comprise a life-of-mine (LOM) revenue of $732M from ~600,000oz of recovered gold at the average rate of +/-90,000oz per year ($1300/oz gold price).

Operating margins are healthy with average annual post-development net cash flows of ~$40M over the initial seven year mine-life (post tax).

Cash operating costs (C1) average US$697/oz (before royalty) and all-in-sustaining costs (AISC) are $830/oz.

Establishment capital costs of $168M (+15%/-5% accuracy) are in-line with previous guidance and include all plant, all infrastructure, EPCM and owners costs, pre-production costs, all taxes and duties including VAT, contingencies and working capital.

Azumah has also assumed the purchase of the core mining fleet for an additional $27.8M. The fleet would be externally operated and maintained under a hybrid contract mining arrangement with substantial offsetting savings in contract mining rates.

Deferred capital of $22.1M relates to the Julie flotation and regrind circuit addition to the Kunche plant plus haul road construction and other related Julie site costs in year 4.

Sustaining capital totals $20.6M with the majority required for the phased expansion of the tailings dam.

Importantly, the Study has confirmed that with the excellent infrastructure and services available there are no technical, logistical, social or environmental impediments to development. This includes high-voltage grid power to site which provides power at ~50% of self-generation alternatives.

With Mining Leases granted and Study technical work all but completed, the EPA permitting process can now proceed in earnest.

The following Appendix to this release details the provisional Study outputs and basis for their estimation. These may vary pending Study finalisation.

Graph 1: Summary of Wa Gold Project Life-Of-Mine Production and Grade (provisional)

NB: Average mill head grade is 2.14g/t Au

2.0g/tAu

90,000ozpa

Page 3 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

For further information on Azumah Resources Limited and its Project please visit its website at www.azumahresources.com.au

Stephen Stone Managing Director Tel: +61 (0)418 804 564 [email protected]

Nathan Ryan – Australia NWR Communications +61 (0)451 896 420 [email protected]

Joanna Longo – North America Terre Partners +1 416 238 1414 [email protected]

APPENDIX

PROJECT INTRODUCTION

The Project is located 50km from the regional town of Wa which serves as the administrative centre for the Upper West region in Ghana. The Project area comprises mostly uncultivated flat savannah bush with occasional subsistence level farmland and is generally sparsely populated.

Operations are based on a conventional carbon in leach (CIL) gold plant located adjacent to the flagship, 1.4km long, Kunche deposit which will treat 1.2Mtpa of primary ore and up to 1.8Mtpa of softer oxide and transition ore.

Ore will be sourced from the staged mining of a series of shallow open pits at Kunche, Bepkong and Aduane in the Wa Lawra district and from Julie and Collette in the Wa East area, which would be trucked 85km to the Kunche plant (Figure 1).

Study Parameters and Management

The Study was managed by Perth based GRES with Azumah co-ordinating geology, geotechnics, mining, environmental and financial modelling.

The Study has to date addressed: ore mineralogy and characterisation; metallurgical recovery; optimal flow sheet and processing plant design; resource estimation; geotechnics; mine optimisations and pit designs; Ore Reserve estimation and verification; mining and mining equipment; mine scheduling; tailings and waste management; site infrastructure and services requirements; capital and operating costs; fiscal matters and taxation; revenue and preliminary financial modelling; social and environmental issues; community and farmer compensation; haul road routing and design; Project implementation; and risks and opportunity assessments.

Specialist independent consultants and contractors were employed to contribute to the Study, many of which are regarded as leaders in their respective fields with the majority having recent experience in West Africa and specifically Ghana (Table 1).

Table 1: List of Study Contributors

Function Proponent Geology & Resource Models

CSA Global Pty Ltd & Brian Wolfe

Metallurgical Test-work Metpro, GR Engineering Services Limited & Bureau Veritas Process Flow-Sheet Design GR Engineering Services Limited Operating & Capital Cost GR Engineering Services Limited Mining & Ore Reserves Kirk Mining Consultants Social and Environmental SAL Consult (Ghana) Hydrology and Tailings Storage Knight Piésold Geotechnical George Orr and Associates & Coffey Mining Taxation & Fiscal Regime Ernst & Young (Ghana and Perth) Financial Modelling Azumah Resources Limited & Optimum Capital

Azumah Resources Limited – Feasibility Study Update – March 2015

Geology Azumah has completed over 540,000m of exploration, definition and infill drilling to discover and assess mineralisation for mining at the Project. Since the previous Feasibility Study (August 2012) the Company has:

• Drilled a further 217 RC and diamond holes for 12,274m and 3,486 auger drill holes for 15,294m. It has also collected 1,548 surface truck-mounted power auger based geochemical samples;

• Undertaken resource re-estimates for Kunche and more recently in August 2014 for Julie (Brian Wolfe) to reflect the considerably extended Julie deposit mineralisation and the use of the multiple indicator kriging (MIK) geostatistical estimation method at Julie;

• Re-logged all diamond core retained on site from the Kunche, Bepkong and Julie deposits to update and standardise the database lithology; and

• Undertaken extensive resampling of Julie deposit holes to assess sulphur distributions as support for flotation plant flow sheet design.

Figure 1: Wa Gold Project – Key Deposits and Prospects

The 0.75Moz, 1.4km striking, sub-vertical, sub-outcropping Kunche deposit is hosted by a north-north-west striking sinistral shear system within Birimian metasediments. Mineralisation is associated with silicification and pyrrhotite-arsenopyrite alteration in and around dark grey quartz veins and stringers. The veins are best developed in coarse greywacke units or in a broad 20-30m wide zone of interleaved greywackes and phyllites which is interpreted as the ‘Kunche Shear Zone’ that extends for some 40km and which has been a key focus for exploration. Page 5 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

The 0.25Moz, 0.56km striking Bepkong deposit is 2km north of Kunche and is covered by transported colluvium and alluvium which overlies the mottled zone of a truncated laterite profile and was therefore a ‘blind’ discovery by Azumah based on geochemical sampling. It is hosted by a north-south striking sinistral shear system within Birimian metasediments, the same meta-sedimentary package as Kunche, although carbonaceous phyllites are dominant over arenitic wacke units. It comprises up to six sub-parallel lodes of which two dominate. There is a close association between gold grade and pyrite - arsenopyrite content and zones of disseminated arsenopyrite always carry significant grade, but grade may also occur without arsenopyrite (or any sulphide). Pyrite content is variable. The satellite 0.09Moz Aduane deposit is 1km south of Bepkong and of a similar style.

The Wa East district hosts the 0.83Moz Julie deposit and is also host to many other smaller deposits most of which have yet to be converted to Ore Reserves. These include the 0.08Moz Collette deposit and the Josephine and Kjersti prospects. Julie comprises a series of shallow north-dipping ore shoots located along a ~6km east-west trending shear zone. Gold mineralisation occurs as micron-sized inclusions and free gold within fractures of euhedral pyrites that have precipitated within fracture controlled crystalline quartz-carbonate-tourmaline veins within the sheared meta-monzodiorite. Metallurgical test work indicates that to liberate the interlocking of fine gold particles in pyrite, a fine grind phase is required after sulphide flotation.

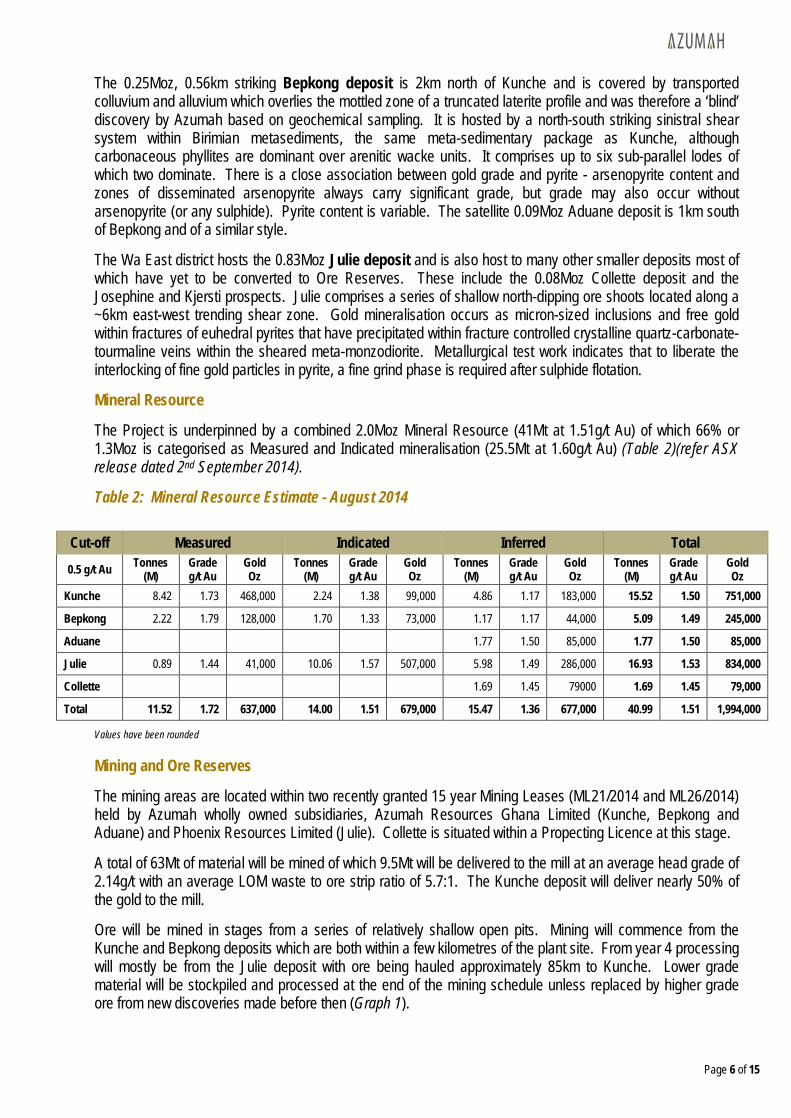

Mineral Resource

The Project is underpinned by a combined 2.0Moz Mineral Resource (41Mt at 1.51g/t Au) of which 66% or 1.3Moz is categorised as Measured and Indicated mineralisation (25.5Mt at 1.60g/t Au) (Table 2)(refer ASX release dated 2nd September 2014).

Table 2: Mineral Resource Estimate - August 2014

Cut-off Measured Indicated Inferred Total 0.5 g/t Au Tonnes

The mining areas are located within two recently granted 15 year Mining Leases (ML21/2014 and ML26/2014) held by Azumah wholly owned subsidiaries, Azumah Resources Ghana Limited (Kunche, Bepkong and Aduane) and Phoenix Resources Limited (Julie). Collette is situated within a Propecting Licence at this stage.

A total of 63Mt of material will be mined of which 9.5Mt will be delivered to the mill at an average head grade of 2.14g/t with an average LOM waste to ore strip ratio of 5.7:1. The Kunche deposit will deliver nearly 50% of the gold to the mill.

Ore will be mined in stages from a series of relatively shallow open pits. Mining will commence from the Kunche and Bepkong deposits which are both within a few kilometres of the plant site. From year 4 processing will mostly be from the Julie deposit with ore being hauled approximately 85km to Kunche. Lower grade material will be stockpiled and processed at the end of the mining schedule unless replaced by higher grade ore from new discoveries made before then (Graph 1).

Page 6 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

Figures 2 & 3: Kunche and Julie Resource Projections and Pit Outlines

The higher grade Julie deposit has been deferred in the mining sequence to preserve the option for a stand-alone Julie processing development which may be warranted with continued exploration success in the Wa Lawra and Wa East areas.

Under a hybrid contract mining arrangement, Azumah plans to own the core mining fleet and also provide fuel and explosives to a mining contractor which will undertake day-to-day mining operations including: drill and blast: excavate, load and haul; fleet maintenance; dewatering; and rehabilitation. This results in material mining cost savings and an average contract mining cost of $3.29/t mined (ore and waste) which will more than outweigh the upfront fleet capital cost. Haulage of Julie ore will also be undertaken by an external contractor at an estimated cost of $0.17/tkm.

The Mining Inventory of 652,500oz comprises Mineral Reserves of 624,000oz (9.1Mt at 2.14g/t Au) within designed pits at Kunche, Bepkong and Julie plus an additional 28,500oz gold contained as Inferred mineralisation within optimised pits at Aduane and Collette (Table 3 and 4).

The Mining Inventory and Ore Reserve are based on inputs to the Study (modifying factors) as at August 2014 including a gold price of US$1,300/oz and pit designs based on selected pit optimisation shells at a revenue factor of 0.95 (US$1,235).

A recent check of the Ore Reserves using the most recent Study modifying factors confirmed that there has been no material change in the size of the optimised pits and hence confirms the validity of the reported Ore Reserves.

The mining and processing schedules have an initial 7-year life with annual LOM gold production of +/- 90,000oz pa.

Increased Ore Reserves are expected through: completion of additional infill drilling and technical studies to upgrade the existing in-pit Inferred Mineral Resources at Aduane, Julie and Collette; additional discovery on Azumah’s 2,800km2 of licences including from a number of advanced exploration targets (refer ASX release dated 12th March 2015); and/or through conversion of more of Azumah’s existing 2.0Moz Mineral Resource with operating costs reductions, gold price increases and other Project enhancements.

Figures 3 & 4: Kunche - Bepkong and Julie Site Layouts

Page 8 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

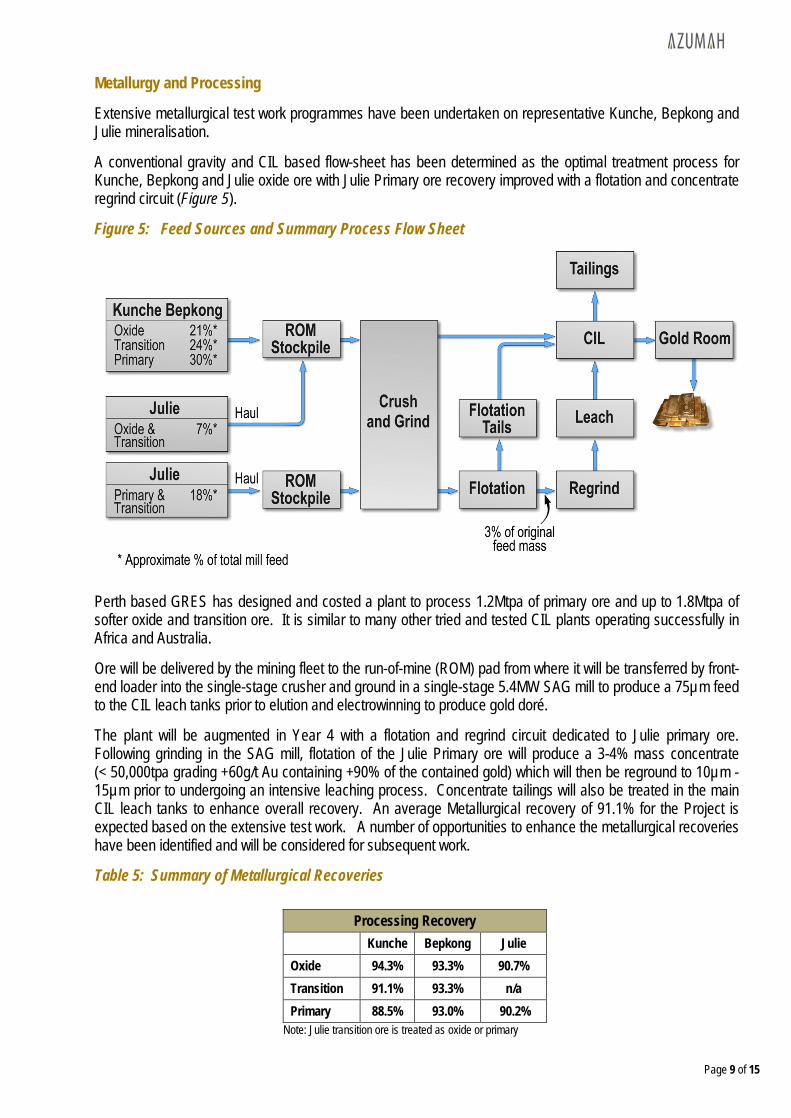

Metallurgy and Processing

Extensive metallurgical test work programmes have been undertaken on representative Kunche, Bepkong and Julie mineralisation.

A conventional gravity and CIL based flow-sheet has been determined as the optimal treatment process for Kunche, Bepkong and Julie oxide ore with Julie Primary ore recovery improved with a flotation and concentrate regrind circuit (Figure 5).

Figure 5: Feed Sources and Summary Process Flow Sheet

Perth based GRES has designed and costed a plant to process 1.2Mtpa of primary ore and up to 1.8Mtpa of softer oxide and transition ore. It is similar to many other tried and tested CIL plants operating successfully in Africa and Australia.

Ore will be delivered by the mining fleet to the run-of-mine (ROM) pad from where it will be transferred by front-end loader into the single-stage crusher and ground in a single-stage 5.4MW SAG mill to produce a 75µm feed to the CIL leach tanks prior to elution and electrowinning to produce gold doré.

The plant will be augmented in Year 4 with a flotation and regrind circuit dedicated to Julie primary ore. Following grinding in the SAG mill, flotation of the Julie Primary ore will produce a 3-4% mass concentrate (< 50,000tpa grading +60g/t Au containing +90% of the contained gold) which will then be reground to 10µm -15µm prior to undergoing an intensive leaching process. Concentrate tailings will also be treated in the main CIL leach tanks to enhance overall recovery. An average Metallurgical recovery of 91.1% for the Project is expected based on the extensive test work. A number of opportunities to enhance the metallurgical recoveries have been identified and will be considered for subsequent work.

Note: Julie transition ore is treated as oxide or primary

Page 9 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

Tailings

Tailings from the CIL process will be disposed of in a dedicated tailings storage facility (TSF) adjacent to the plant. The TSF will be fully lined with an HDPE geo-membrane to meet Ghana EPA requirements.

Mining Waste

Mined waste, after formation of the ROM pad and TSF, will be stored in waste dumps adjacent to each of the pits. Sub ore grade material or ‘mineralised waste’ will be stored in segregated areas of the waste dumps for possible later treatment. Sediment storage structures have been designed and will be built on appropriate drainage lines.

Water

Water for use in the plant and other mine requirements will be sourced from the adjacent Black Volta River, 5km to the west of the plant, from mine dewatering and from the TSF. The Black Volta forms the border with Burkina Faso to the west and the Project’s western licence boundary (Figure 6).

A 800,000m3 water storage dam has been incorporated to ensure year-round security of supply under low rainfall conditions.

A licence for the abstraction of water from the Black Volta has been granted by the Ghana Water Resources Commission. Water for Julie dust suppression will be sourced from pit dewatering and/or a borefield.

Power

Power will be accessed through a newly completed 161kV arterial transmission line which was re-routed by the Government owned power infrastructure company, GridCo, to service the Project. Pylons have been constructed by GridCo to the mine gate (Figure 7).

The availability of grid power is a major benefit to the Project and provides a considerable cost saving over the alternative diesel generated power.

Power supply costs in Ghana are set to become more competitive with the entry into the market of several independent power producers (IPPs). Supply discussions have commenced with these as well as the government owned Volta River Authority.

Figures 6 & 7: Black Volta River and Powerline Pylons to Site

Page 10 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

Roads and Transport

The Project has excellent access with sealed roads to within 5km of site. Unsealed roads in the areas are also well constructed and maintained by local authorities.

A 2km sealed airstrip at Wa services small to medium sized private and non-scheduled air services. Regular commercial services from Accra are proposed to commence in 2016.

Transport of ore from Julie and Collette for treatment at the plant adjacent to Kunche (~85km) will be via road trucks mostly on existing local roads and highways. However, some road upgrades are required together with construction of new roads sections and deviations around villages.

Accommodation

Operational staff accommodation will be provided at the Company’s existing 48 person Kalsegra camp, 8km from Kunche, which will be expanded accordingly with some staff also accommodated in surrounding villages. A separate camp at Julie, based on expanding the existing exploration camp, will be developed prior to the commencement of mining there.

Community and Regional Impact

No specific social impediments to development have been identified. At Kunche-Bepkong there are no villages to relocate with only one family nearby to Bepkong requiring relocation prior to Project commencement which will be undertaken in close liaison with local authorities and village chiefs. At Julie scattered houses and farming shelters will need to be relocated from within a buffer zone around the mine. Compensation for loss of access to agricultural land will be required and detailed plans for this are being devised based on farm surveys already carried out.

All community issues and decisions will be undertaken in accordance with Equator Principles and on a free, prior and informed consent basis.

Ghana’s Upper West region is largely under-developed and comprises mainly subsistence farming with no large established industries. The region will benefit enormously from the Project with all but a few of the estimated 205 permanent employees and 115 contractor staff being Ghanaian. During construction and pre-production mining the workforce will temporarily expand to in excess of 800 persons of which 96% will be Ghanaian.

Employment preference will be given to locals and, along with the various contracting groups, male and female Ghanaians will be provided with extensive educational and training opportunities by Azumah and its major contracting groups under the Company’s employment and gender policy.

Azumah has also implemented a local content purchasing policy.

Environmental and EPA Licencing

Azumah has established baseline environmental monitoring programmes since 2011. A draft Environmental Impact Statement (‘EIS’) was submitted in 2011 but was not actioned pending the formal granting of a Mining Lease, which has now been issued. The draft EIS is now being updated to reflect the larger plant, changes to the process flow sheet, lining of the TSF with an HDPE membrane and the much expanded operations at Julie.

Azumah has also completed detailed social studies in all areas including farm surveys, traffic surveys and extensive community consultation.

Site rehabilitation has been costed at around $5M (in addition to progressive mining/waste dump rehabilitation) and an environmental bond is also included in cash flows.

Page 11 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

General Services

Ghana has a well-developed mining industry and is supported by an extensive range of established service providers in-country covering mining, construction, operations support, goods and material supply, and transport services.

SUMMARY FINANCIALS (provisional and subject to revision):

The Study capital and operating costs have been estimated to an accuracy of -5% / +15% as at Q4 2014. Operating and capital costs were derived from bottom-up first principles or based on quotes from third parties.

Revenue

Operations will generate LOM revenue of $732M (Study revenue gold price of $1,300/oz and after government royalties of 5% plus refining and realisation charges) and provide considerable export income to Ghana. A major component of the revenue will be converted to Ghana cedi currency for payment of local expenses.

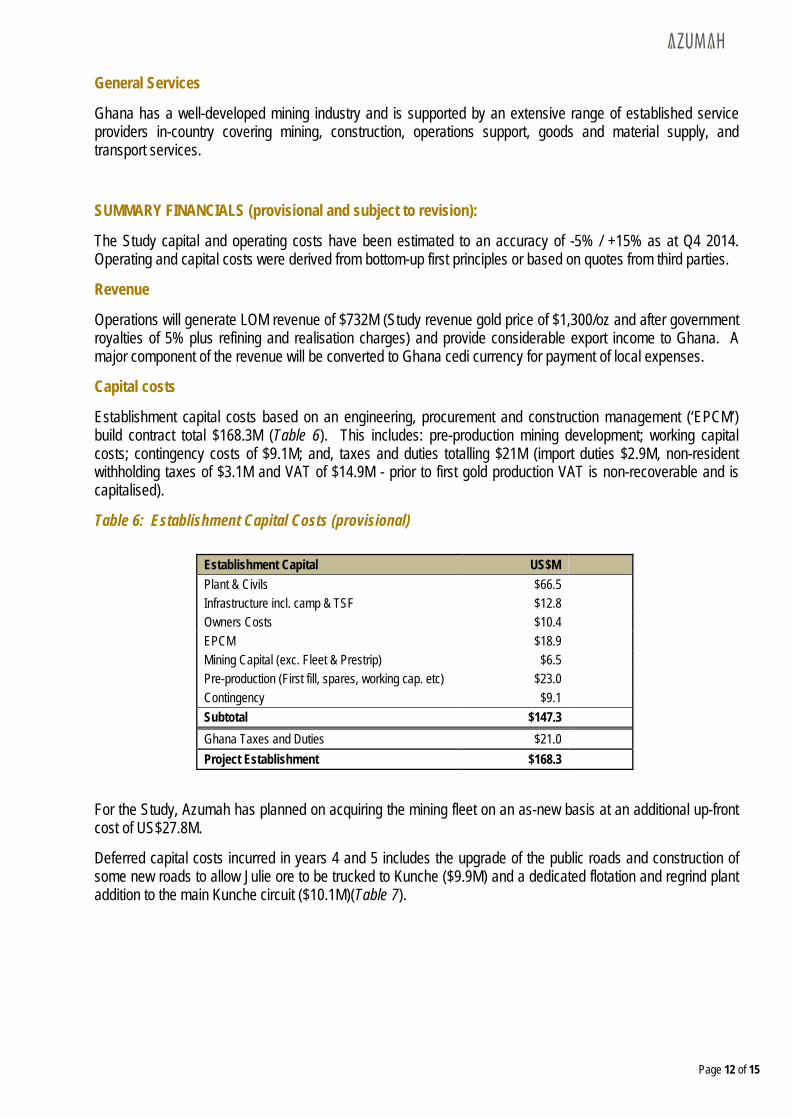

Capital costs

Establishment capital costs based on an engineering, procurement and construction management (‘EPCM’) build contract total $168.3M (Table 6). This includes: pre-production mining development; working capital costs; contingency costs of $9.1M; and, taxes and duties totalling $21M (import duties $2.9M, non-resident withholding taxes of $3.1M and VAT of $14.9M - prior to first gold production VAT is non-recoverable and is capitalised).

Table 6: Establishment Capital Costs (provisional)

For the Study, Azumah has planned on acquiring the mining fleet on an as-new basis at an additional up-front cost of US$27.8M.

Deferred capital costs incurred in years 4 and 5 includes the upgrade of the public roads and construction of some new roads to allow Julie ore to be trucked to Kunche ($9.9M) and a dedicated flotation and regrind plant addition to the main Kunche circuit ($10.1M)(Table 7).

Page 12 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

Table 7: Deferred and Sustaining Capital Costs

Deferred Capital US$M Flotation and Regrind $10.1 Julie Haul Road $9.9 Julie Mine Establishment $2.1 Total Deferred Capital $22.1 Sustaining Capital Tailings Storage Facility Lifts $16.0 Vehicles, Fleet and plant capital $4.6 Total Sustaining Capital (net) $20.6

Rehabilitation costs of $4.8m are included in the cash flows.

Operating Costs

Site cash operating costs (C1) average $697/oz over the LOM (excluding royalties of $65/oz based on 5% of $1300/oz) (Table 8).

Mining costs were derived from a mining contractor based on designed pits and mining schedules. Mining costs comprise 53% of C1 costs and average $3.29/t mined, plus haulage costs from Wa East for Julie and Collette ore. Mining costs include fuel priced at $1.00/ltr (currently ~$0.85/ltr) and are on the basis of Azumah’s preferred hybrid mining contract arrangements.

Processing costs averaging $15.10/t ore processed includes power costs of $0.15/kWh (~30% of total processing costs) based on supply from an independent power producer.

G&A costs of $5.6M pa (or approx. $4.07/t milled) includes administration labour, government fees, insurance, etc.

Table 8: Site Cash Costs (C1) (provisional)

Operating Cost Unit Mining Cost* $/t mined (ore and waste) $3.29

Processing Cost $/t ore average LOM $15.10

G&A $/t $4.07

Total Site Cost** (C1) US$/oz $697 *Excludes Julie haulage costs of $14.27/t **Excludes royalties of 5% but includes realisation costs of ~$4/oz

Cash Flows

All-in-sustaining-costs total $830/oz and the Project generates average annual positive cash flows of approximately $40M (post tax) over the 7 years of initial Project operation.

Ghana Fiscal

Total revenue to the Government of Ghana of $107M is based on the current fiscal regime and includes non-refundable VAT on construction costs ($14.9M), import duties, non-resident withholding taxes, PAYE taxation on employees (Azumah and contractors), government fees and royalties ($39M). It excludes dividend and interest withholding taxes, 10% free carried interest in the Project or any taxation on contractor income or indirect locally procured goods and services.

Page 13 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

PROJECT ENHANCEMENT OPPORTUNITIES

These outputs and Study finalisation, inclusive of reporting of financial returns, are subject to several outstanding items that Azumah will, using the now available definitive data, evaluate and progress on the basis that, in combination, they could have a materially positive impact on overall returns and better position the Project for financing and development in the prevailing commercial environment. These enhancement options are:

Opportunities to further reduce operating costs, which along with any increase in the gold price, will enlarge pits, increase the Mining Inventory and mine-life and reduce costs per ounce gold produced without the need for further driling.

Julie mining and processing options including possibly a stand-alone processing capability at Julie. Under the present Study scope current costs include $11M for the installation of a haul road and $35M for Julie ore to be hauled to Kunche for processing. This has the present impact of increasing the Julie cut-off grade, reducing Julie Ore Reserves and increasing production costs.

The option of a stand-alone plant at Julie is one of the reasons that mining at Julie has been deliberately deferred to at least year 4,by which time there may also have been an increase in Mineral Resources and/or the gold price.

Figure 8: Julie Cross-Section

Advancing discussions with the Government of Ghana to co-operatively identify regional specific taxation and fixed impost concessions that could materially reduce capital and operating costs and improve bottom-line returns.

In addition, but not a part of the Study per se, Azumah will continue to explore its 2,800km2 tenure encompassing large tracts of fertile Birimian terrain in order to maintain its track-record of discovery and increasing Mining Inventory with a commensurate increase in mine-life and overall returns (refer ASX release dated 12th March 2015).

Exploration, Mineral Resources and Mining Inventory increases

Recent auger rig based geochemical soil sampling, mapping and review of existing datasets has generated a number of high-priority targets close to and within trucking distance of the plant, some of which have been earmarked for follow-up drill testing (refer ASX release dated 12th March 2015)

Page 14 of 15

Azumah Resources Limited – Feasibility Study Update – March 2015

Azumah also has a strategic shareholding in neighbour Castle Minerals Limited which holds licences encompassing 10,000km2. Castle has reported combined Mineral Resources of 3.3Mt at 1.54g/t for 161,600oz in the vicinity of Azumah’s Julie deposit.

Competent Persons’ Statements

The scientific and technical information in this report that relates to the geology of the deposits and exploration results is based on information compiled by Mr Stephen Stone, who is a full-time employee (Managing Director) of Azumah Resources Ltd. Mr Stone is a Member of the Australian Institute of Mining and Metallurgy and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Stone is the Qualified Person overseeing Azumah’s exploration projects and has reviewed and approved the disclosure of all scientific or technical information contained in this announcement that relates to the geology of the deposits and exploration results.

The scientific and technical information in this report that relates to the in-situ Mineral Resource estimates for the Bepkong and Collette deposits is based on information compiled by Mr David Williams, who is a geological consultant employed by CSA Global Pty Ltd. Mr Williams is a Member of the Australian Institute of Geoscientists and the Australian Institute of Mining and Metallurgy and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Williams has reviewed and approved the disclosure of all scientific or technical information contained in this announcement that relates to the Bepkong and Collette Mineral Resource estimate.

The scientific and technical information in this report that relates to the in-situ Mineral Resource estimates for the Kunche and Aduane deposits is based on information compiled by Mr Dmitry Pertel, who a full-time employee (Manager - Resources) of CSA Global Pty Ltd. Mr Pertel is a Member of the Australian Institute of Geoscientists and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Pertel has reviewed and approved the disclosure of the relevant scientific or technical information contained in this announcement that relates to the Kunche and Aduane Mineral Resource estimates.

The scientific and technical information in this report that relates to Mineral Resources estimates for the Julie deposit is based on information compiled by Mr Brian Wolfe, a Competent Person who is a Member of the Australian Institute of Geoscientists. Mr Wolfe is a consultant to Azumah Resources Limited and is not an employee of the Company. Mr Wolfe has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Wolfe consents to the inclusion in the report of the Julie Mineral Resources in the form and context in which it appears.

The scientific and technical information in this report that relates to Ore Reserves estimates for the Kunche, Bepkong and Julie deposits is based on information compiled by Mr Linton Kirk, an independent consultant to Azumah Resources Limited. Mr Kirk is a Fellow of the Australasian Institute of Mining and Metallurgy. Mr Kirk has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Kirk consents to the inclusion in the report of the matters related to the Ore Reserve estimate in the form and context in which it appears.

The scientific and technical information in this report that relates to Process Metallurgy is based on information compiled by Mr Ian Thomas, an independent process consultant to Azumah Resources Limited. Mr Thomas is a member of the Australasian Institute of Mining and Metallurgy. Mr Thomas has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Thomas consents to the inclusion in the report of the matters related to the metallurgy, specifically the data represented in Table 3 in ASX release dated 2nd September 2014, in the form and context in which it appears.

Forward-Looking Statement

This release contains forward-looking information. Such forward-looking information is often, but not always, identified by the use of words such as “seek”, “anticipate”, “believe”, “plan”, “estimate”, “expect” and “intend”, and statements that an event or result “may”, “will”, “should”, “could”, or “might” occur or be achieved, and other similar expressions. In providing the forward-looking information in this news release, the Company has made numerous assumptions regarding: (i) the accuracy of exploration results received to date; (ii) anticipated costs and expenses; (iii) that the results of the feasibility study continue to be positive; and (iv) that future exploration results are as anticipated.

Management believes that these assumptions are reasonable. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from those contained in the forward-looking information. Forward-looking information is based on estimates and opinions of management at the date the statements are made.