21

1 February, 2018 Emerging Markets Journal Location: United Arab Emirates Indian migrant workers walk to their construction site after a lunch break Featuring: Peru, South Africa & Norway

1

February, 2018

Emerging Markets Journal

Location: United Arab Emirates Indian migrant workers walk to their construction site after a lunch break

Featuring: Peru, South Africa & Norway

2

Table of Contents

Overview: Introduction to EM Journal.………………………………………………………………….3

Peru: Uncovering Peruvian Economic Influences…………………………………………………….4

South Africa: Growth Turbulence……………………………………………………………………….9

Norway: Developed Nation Support to Emerging and Frontier Markets ………………………….13

2018 Outlook…………………………………………………………………………………………….20

3

Introduction

Welcome to the Emerging Markets Club’s February, 2018 issue on international

development, geopolitical risks, and global finance fueling growth of developing nations.

The Emerging Markets Club is a student run, faculty assisted organization designed to

expose students to international markets alike. We observe economic trends impacting

business and sovereign nation growth. An emerging market is one which seeks to

increase consumption to those of developed countries through productivity and

government policy reform that lead to GDP growth. More importantly, GDP per Capita is

the true measure of a nation’s wealth.

2017-18 EMC Officers

President: Alexander Russo

Vice President (Internal): Kush Aggarwal

Vice President (External): Ethan Miller

Treasurer: Griffin Berenske

Chief Editor: Max Milejczak

Marketing Chair: Hyeseon Oh (Claire)

Secretary: Alex Gillespie

EMC Staff

Faculty Advisor: Alison Kvetko (Kelley Business Honors Program)

Kelley Student Gov’t Rep: Daniel Mayer

4

Uncovering Peruvian Economic Influences

Authors: Nicole Cadarso & Maria Laura Castedo

To discover the complexities of Peru’s economic situation, we have decided to conduct

some in-depth research about significant economic growth. Over the past few years, Peru has had

significant economic growth, it is one of the fastest growing economies in the world, classifying

as the 39th largest GDP in the world and 6th in South America. Although Peru is economically

improving more and more every day, there is a high economic informality with how they handle

their economy resulting in a weak education system, low productivity in many sectors and a

corrupt government. Furthermore, 75% workforce is associated with the informal sector resulting

in lack of social benefits for the lower class and missed opportunities for the government to earn

potential tax revenue. Although Peru is a growing economy, informality is a persistent problem

in Peru because it is the most profitable economic opportunity for poor citizens. We will, later

on, uncover the factors that lead to this issue and how it affects the socio-political and economic

areas in diverse ways.

In the past decade, Peru’s economy

has experienced a significant boom. It

successfully doubled the size of its economy

in just ten years and reached one of the

highest GDP growth rates in the region.

Because of this, people think Peru’s

population now lives in better conditions.

However, that is not the case. The majority

of Peru’s workforce, 73%, is still under the informal economy. The informal economy can best

be defined as all the economic activities that contribute to the nations GDP but isn’t registered.

Which leads to a lot of its recognition and benefits in the workforce to be unacknowledged. The

informal sector feeds jobs for a significant portion of Peru’s population which may sound like a

good thing, but in reality, it is just hurting the economy and is avoiding it to grow to its full

potential. These informal sectors are all due to the high levels of poverty, income inequality, and

social exclusion. There are two main groups of bodies who make the informal economy a

reality. The people who participate in order to provide for their families and survive, and the

5

people who participate with the primary goal to make a profit out of it. These primarily include

private businesses who don’t provide the formal documentation that the government requires and

don’t pay social contributions.

The informal economy in general, whether speaking of Peru’s or any other Country

prominent in it, is vast and complex. Its main causes are made of a combination of uncontrollable

factors, but specifically speaking about Peru’s high informality, we can narrow it down to two

factors. One is the survivalist segment, and another is the entrepreneurial drive of citizens.

In one hand we have the survivalists, whose struggle is the incapacity to acquire human capital.

On the other side, for entrepreneurial participants, their struggle is the inability to overcome the

forces that serve as boundaries for individuals to enter the formal sector. What this means is

there is not an easy way to enter the formal market, and it takes more than it seems to entirely

leave the informal sector once in it, since the informal field has so many temptations as

government regulation, taxation, and corruption. These factors, being government regulation the

most vital, are what led the start of what is now known as a high informal sector in Peru.

Moreover, the high demand of informality also has a profound impact on Peru’s general

education systems. The fact that there are policies that favor investment in human capital which

includes cutting the cost of education and security are extremely affecting the priorities of all the

limited funds for education. Having this financial burden is not allowing the 43.8 poor

population rate in Peru to educate children. The government doesn’t provide public schools with

enough fund and resources to teach kids all the things they need to learn in school. Education is

one of the most demanding components to success and in order to receive a good one in Peru

kids must be enrolled in private schools costing an average of $20,000 per year. This cost is

impossible for people from less developed areas to afford which results in them having their kids

attend public school where they are not receiving a proper education. Due to this lack of

knowledge, data tells us thatches adolescents will most likely automatically fall into the informal

sector. The development of human Capital, as education is a critical point that will leverage

Peru’s competitiveness.

Furthermore, having uncovered what Peru's informal area is made out of, it leads us to

ask ourselves how do these factors makeup to become the root and reason behind low

productivity, and thus hurts the economy. Findings from a World Bank study named "Doing

Business 2016" state that Peru's rank on "ease of paying taxes" is as the 50th and its "total tax

6

burden of 35.9% of profits" are way weaker than "41.2% average in developed countries."

Nevertheless, when Peruvian businesses come to preparing, filing and paying the taxes and

social contributions, the study states that "these firms on average spend 260 hours per year

compared to 176-hour average in developed countries." (World Bank). This significant variation

of rakings and percentages happens because of the tax filing process, inspired by all the stringent

government regulation and untidy legislative policies as found in the study and as identified in

all research of low productivity as the common ground. Nonetheless, despite the fact that we

have a common ground on the problem, sources of productivity are known to vary between both

sectors. This has to do mainly with the fact that informal companies cannot reach other markets

and services. The informal firms/businesses indeed bypass the social security payments, taxes,

and could benefit from adjustable employment, which are the costs of operating formally, but

regardless, they are still much less productive than formal firms.

On the other hand, researchers from the Department of Economics in Middle East

Technical University found that "the lack of access to credit provided by state-owned or private

banks may have a detrimental impact on productivity." Aforementioned, this is because of the

prominent downscale that "capitals constraining informal firms" will have because they will be

operating beneath the practical scale of production. Lastly, all these factors mentioned will cause

informal firms to find themselves having a lower capital intensity, labor production, and high

costs of capital limited outside financing that will demand them to replace their labor for

physical capital.

The main reason why business’ in

Peru can go along with such an informal

economy and so many informal sectors is

that of the corrupt government that’s in

place. Peru placed as the 101st most

corrupt country out of 176 while other

Southern American countries such as

Chile and Uruguay placed 24th and 21st.

Peru’s corruption is the direct source as to

why the country is the way it is. For as long as Peru can remember its government has used most

of their profits on themselves rather than focusing on making Peru a better nation to be a part of.

7

Studies have shown that this has resulted in businesses keeping extra money off the books to be

able to support their families just in case the government was to do something unexpected

someday putting them in harm. For example, when Ollanta Humala was elected president in

2011 there were infamous scandals. After becoming president, Humala once said one car was

only going to be allowed per family. Meaning that families of high income who have multiple

cars would have their 2nd, 3rd, 4th car taken away by the government and given to families of

lower income. This, of course, didn’t end up happening but the speculation that it could and

possibilities of what else he could only give business’s more motivation to keep things off the

books. Another factor that leads to such informality is the fact that the government openly

received bribes whether it be for something as simple as getting off a driving ticket to bribing a

judge to keep a loved one out of jail. The fact that the government promotes this behavior has

set the example for the nation as if it’s something they can openly do as well.

The critical condition Peru’s economy is something that requires immediate action. If

this isn’t something that is taken care of soon, the informal sector will continue to drag on the

nation's economic state and will permanently determine its future. Peru must address its

informal industries and integrate it with formal jobs with equal benefits to break the barrier that’s

keeping the country on hold. By doing this, Peru won’t only reduce informal sectors, but it will

increase the economy, strengthen the education system, raise productivity and most importantly,

reform the government ways. This will improve the lives of millions of its citizens and will

eventually lead to Peru not only increasing its GDP but growing together as a whole rather than

everyone on its own. Local people who drive the buses, or as they’re called in Peru ‘the micros,’

will be able to register their vehicle making it easier for them to expand their business and make

a bigger profit while doing the same amount of work. By registering, the self-employed street

vendors will now have a better opportunity to gain capital. 73% of the population will finally be

able to have access to healthcare, proper housing, real education, and most importantly a better

lifestyle for them and their families. Investing in the locals is the way to invest in Peru’s future.

8

Work Cited

Finn, Korey. e Informal Economy in Peru: A Blueprint for Systemic Reform. Vol. 35,

Lehigh University ,2017.

Hughes, Barry B, and John Evans. Economía Informal En Perú: Situación Actual y

Perspectivas. Derechos Reservados, 2016.

Loayza, Norman. “The Economics of the Informal Sector: a Simple Model and Some

Empirical Evidence from Latin America.” Carnegie-Rochester Conference Series on Public

Policy, North-Holland, 8 Dec. 1999,

www.sciencedirect.com/science/article/pii/S0167223196000218.

Portes, Alejandro, and Richard Schauffler. Competing Perspectives on the Latin America

Informal Sector. Vol. 19, 1993.

Saavedra, Jaime, and Alberto Chong. Structural Reform, Institutions and Earnings:

Evidence from the Formal and Informal Sectors in Urban Perú. 2007.

Taymaz, Erol. Informality and Productivity Differentials between Formal and Informal

Firms in Turkey. 2009.

9

South Africa Growth Turbulence

Authors: Brendan Smith, Drew Vesling, Jack Brzakala

South Africa is a country of 55 million people, that has relative macroeconomic stability

and a largely pro-business environment. South Africa is the most advanced, diversified and

productive economy in Africa. However, its actual growth does not match that of other African

economies. In 2016, its gross domestic product (GDP) grew by 0.5% to an estimated $ 736.3

billion. The nature of the South African economy is reflected in the mix of economic sectors:

Primary (including agriculture, fishing and mining) includes 10% of the GDP, Secondary

(manufacturing, construction and utilities) comprises 21% of the GDP, and Tertiary (trade,

transport and services) includes 69% of the GDP. The country covers 1.22 million square

kilometers and is the world’s largest producer of platinum, vanadium, chromium and manganese.

South Africans unfortunately have 6.2

million people of working age without jobs.

Workers out of school are finding it very

challenging to secure a job. This can be

shown in the graphic below with data from the

Statistics South Africa. Women also remain

the most vulnerable to the forces of the labor,

especially women of color who mainly hold

low-skilled jobs. These women struggle because of the 30% difference in wages between men

vs. women. Community and social services, which include the government, is the largest sector

in the economy. Agriculture jobs declined by 44,000 and employment in trade by 15,000, the

statistics office said.

South Africa’s business management environment (legal, publicity, marketing,

accounting, forensics, process outsour cing, etc.) is arguably the best in Africa, and boasts many

advantages. The Johannesburg Stock Exchange (JSE) ranks among the top emerging market

exchanges in the world, helping establish South Africa’s position as an entryway to other

10

countries and markets in sub-

Saharan Africa. Democratic life

is well-established with

transparent and contested

elections, an appreciation for the

rule of law, and citizens

maintaining significant pride in

the constitution and the peaceful

formation of the post-Apartheid

state. The graphic expresses the

relative strength of the economy in comparison with other African countries with data from the

World Bank.

Some of the main challenges endured in the South African Economy include:

corruption/ineptitude in high government circles, significant unemployment, violent crime,

insufficient infrastructure, and poor government service delivery to impoverished communities.

There is also a trade agreement with the European Union enables many European products to

enter South Africa duty-free or at lower rates than U.S. products. The documentation of these

risks can be seen with data provided by Allianz Global Corporate and Specialty.

Since the abolishment of Apartheid, the wages of whites and Asians, primarily of Indian

descent, have increased while the wages of black-Africans have remained relatively flat. Since

corruption is an issue, private interests are capturing contracts to secure state-owned resources.

Ten percent of All South Africans - the majority white - owns more than 90 percent of national

11

wealth, according to a 2016 research paper by Anna Orthofer, a graduate student at Stellenbosch

University. As seen in the graphic; the Black African and Coloured groups are characteristically

defined with a high percentage of low-skilled jobs and conversely, Whites and Indian/Asian

groups have higher percentages of their population in high-skilled or semi-skilled occupations.

The President stated the government will pursue economic transformation by ensuring that 30%

of government’s spending goes to black businesses, but still not enough when four out of every

five individuals in South Africa are included in this category. The best possible way of

combating income inequality is through increasing the minimum wage. South Africa has already

adopted a minimum wage which is R3500 per month and R20 per hour however, the problem is

that this minimum wage is below the poverty line. Because average monthly earnings of

Africans are not increasing at the same pace as of white counterparts the government should

implement policies that will focus on household income level in regard to minimum wage and

prioritize increasing wages for people who are in the lowest income order.

12

Work Cited

Anna Orthofer Economics PhD Candidate, Stellenbosch University. “South Africa needs to fix

its dangerously wide wealth gap.” The Conversation, 5 Feb. 2018, theconversation.com/south-

africa-needs-to-fix-its-dangerously-wide-wealth-gap-66355.

“How Inequalities undermine Social Cohesion: A Case study of South Africa.” G20 Insights, www.g20-insights.org/policy_briefs/inequalities-undermine-social-cohesion-case-study-south-africa/. “Race,Class,Gender in an unequal South Africa.” News24, 18 Jan. 2016, www.news24.com/MyNews24/raceclassgender-in-an-unequal-south-africa-20160118. Sedghi, Amy, and Mark Anderson. “African rich get richer even as poverty grows and inequality deepens | Ami Sedghi and Mark Anderson.” The Guardian, Guardian News and Media, 31 July 2015, www.theguardian.com/global-development/datablog/2015/jul/31/africa-wealth-report-2015-rich-get-richer-poverty-grows-and-inequality-deepens-new-world-wealth.

13

Norway: Supporting Emerging and Frontier Markets

Author: Alex Russo

WTO Trade Policy Review

To provide a backdrop of the Norwegian economy, an analysis of the Norway’s Trade

Policy Review by the World Trade Organization was done. The country eliminated its “most-

favored nation” policy on a majority of manufactured goods. This meant certain trade partners

previously received better tariff standards. In terms of bound rates, Norway tops out at 11 to 14%

in order to enhance production quality with a small population of 5.2 million. The public has

created an economy built on high standards relevant to its competing position and cultural ideals.

One example is increasing fish diets in developed nations. The demand in arctic water delicacies

is attracting consumers around the globe. Norway also justifies these rates with efficient dispute

settlements in its multilateral trade system. Trade disputes are settled in Geneva at the WTO

headquarters. Their role as an European Free Tarde Association (EFTA) member appears as a

discrimination loophole around GATT (General Agreement on Tariff and Trade) policy and

allow Norway to trade with regional partners over others. In further support of bound rates for

developed countries, Norway provides duty and quota free benefits for countries considered

‘low-income’; These are commonly referred to as Least Developed Countries (LDCs).

Supporting such classified nations is building future trade partners and international support,

much like China’s initiative to enter African and the Middle-East regions for pure economic

operations. To the contrary, Norway is not structuring vast debt financing that will have systemic

risk to its domestic economy (NY Times, May 2017).

Asia-Pacific nations have begun to seek

Norway’s resources, especially fresh fish

thriving in the waters off its impeccable coast.

It’s an essential area for Norway who heavily

relies on petroleum exports at 25% of GDP

(OECD 2017). Fish and aquaculture sit at just

about 1% due to its low cost and EU import

14

quotas for specific seafood products. As its fish exports become prevalent in more global

regions, the country could begin increasing toward bound rate levels. We will explore these

Asian trade agreements in the next section. They can claim environmental damages under the

GATT and charge all trade partners a greater price. Though price is the most delicate economic

tool, small increases to combat domestic and global inflation may become necessary.

According to the WTO Trade Policy Review in 2012, no significant changes have

occurred in Norway’s general framework since the last review in 2004. Lingering issues from the

global financial crisis have left a potential asset bubble in the housing market as interest rates

were left low for quite some time. More dramatically, as of February 2018, the European Central

Bank interest rates still remain near zero. A similar situation to Norway is currently happening in

the US. They see a shortage of affordable housing with baby-boomers retiring and Millennial

first-time buyers. Low inflation will play a major role to come as wage growth was absent in

2016-17. Norway’s true liquid gold is its vast ecosystem of lakes, rivers, and waterfalls.

Hydropower and fresh water extractions are scattered between beautiful fjords. Environmental

constraints remain in supporting tourism growth but managing the precious resource. It could be

an effective way to off-set reliability on crude oil and natural gas. The European Union has an

ease of access with their Regional Trade Agreement (RTA) but will see competition from other

Norwegian RTAs.

Regional Trade Agreements

At the time of Norway’s last TPR review in August of 2012, the country was approaching

full-economic capacity. Unemployment was nearing 3% and taxation of petroleum and crude oil

companies allowed assets under management to sustain through the financial crisis and recovery

period. Like the United States, pension liabilities will be difficult to fulfill even with these funds

are managed effectively. Many of the high tariff rates are expected to protect domestic industries

and help areas like consumer goods prices remain low through trade agreements. According to

Norway.no, Norway continues to work with the WTO in Geneva and assist other nations in

trade. The site outlines direct communication with developing and Least Developed Country

(LDC) to establish trade relations.

The Norwegian government is set up in a democratic style like the US. The main

difference is a legislative process known as ‘Storting’. A group of 169 representatives decide

15

custom tariffs on an annual basis. All international agreements are reviewed with the foreign

affairs committee. However, it is the Ministry of Foreign Affairs who is responsible for all trade

policy. They also oversee all multi-national trade and represent Norway at the WTO. Assisting

the Ministry of Foreign Affairs is Siv Jensen. She is the current Minister of Finance and is

responsible for planning and implementing economic policy (Regjeringen, 2017). This involves

work with the fiscal budget, which includes investing the trade surplus into the Sovereign Wealth

Fund. Regarding trade, Norway benefits from EU inclusion through the European Free Trade

Association (EFTA). They are given access to the internal market without being a member of the

EU. The two institutions have been working together with the WTO. Their cooperation is

focused on opening trade with smaller economies across the globe. A number of regional trade

agreements have been formed with the EFTA while led by Norway. Their participation in the

European Economic Area (EEA) means they adopt most legislation from the EU regarding the

single market, removing internal borders and regulatory obstacles. However, agriculture and

fisheries are excluded.

The significant economic feature that lies with Norway may just be the fishery market.

While the United Kingdom and the European Union battle over Brexit, it is raising major

concerns over shared fishing areas. Norway has little to worry. Their exclusion within the EFTA

retains their water rights, placing a strategic card in their hand to maintain world trade, including

Asia. An early announcement has been made for a China-Norway free trade agreement (FTA).

Negotiations began in 2008 and have since held 9 rounds before finally being signed by both

parties (fta.mofcom.gov). This is intriguing considering that the EFTA has a bilateral RTA with

Hong Kong and China since 2012. It may explain the length negotiations took. A noticeable

difference in the two agreements is the inclusion of “E-commerce” stated in the new Norway

RTA (EFTA.int, Nov 2017). This is the only pure bilateral deal Norway has made since its first

trade deal with the Faroe Islands in 1992; Those not-considered ‘pure’ are those through the

EFTA and EU. Another agreement recently announced through the EFTA is

Russia/Belarus/Kazakhstan, of whom not all are WTO members. The EFTA also announced

individual Indo-Pacific deals with India, Indonesia, Vietnam, and the Philippines, as well as a

middle-east deal slated to the WTO.

Referred to as a “fax democracy”, Norway implements the so-called “1st pillar of the

EU”. This is when legislation is sent through fax by the European Commission. The Prime

16

Minister of Norway reports receiving roughly 5 pieces each day (Politico, May 2016) The

Norwegians do not participate in the European Commission or European Parliament but are

consulted at various points in time during the drafting process. Aspects of the 1st pillar of the EU

include the union’s social policy, consumer protection, environment and company law. Between

free trade access with large economies and sole protection of its fisheries and agriculture,

Norway is in a unique position as an EFTA member. They benefit without direct participation in

all of the European Union.

Norway is a ‘founding father’ of the GATT and considered an original member of the

WTO. They have made long strides in every round and never had a complaint ruled against

them. In one issue resolved, Norway objected the EU, South American, and Asian nations

regarding “MFN” importation of processed and unprocessed seal products by the EU. They won

this Dispute Settlement Resolution (DSR), which solidified the provision as an EFTA member. It

states their right to deal seal products at their effective tariff. Outside of Europe, Norway has

made strides in the last decade to grow their trade network. They are importing low-cost

consumer goods from Asia and trading fishery stock in exchange. They also continue to invest in

least-developed countries, seeking to build personal bilateral and regional agreements in decades

to come. They can solidify themselves from full-fledged EU membership and prosper in

economic growth.

Use of Account Surplus

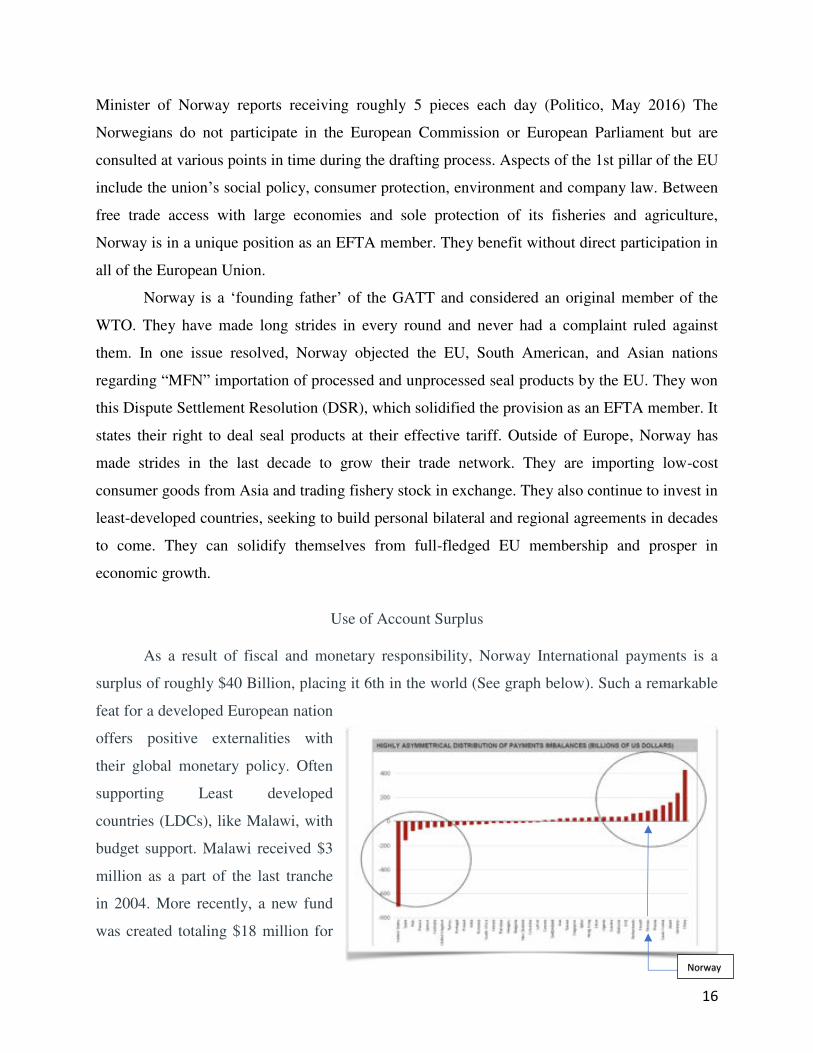

As a result of fiscal and monetary responsibility, Norway International payments is a

surplus of roughly $40 Billion, placing it 6th in the world (See graph below). Such a remarkable

feat for a developed European nation

offers positive externalities with

their global monetary policy. Often

supporting Least developed

countries (LDCs), like Malawi, with

budget support. Malawi received $3

million as a part of the last tranche

in 2004. More recently, a new fund

was created totaling $18 million for

Norway

17

a just phase 2 of the Enhanced Integrated Framework (EIF) in order to develop trade. Initiatives

like this allow payment imbalance shortfalls of small economies generate growth and establish

positive relations with other countries. Sub-Saharan nations struggle to meet budget constraints

because they lack the control over prices of natural resources, which most often are traded cross-

border below market value. Foreign powers often arm-strangle LDC’s as they know the countries

must export to offset high import levels.

China has expanded its global reach in the last decade, targeting Middle-east and African

countries. They offer migrant workers and infrastructure projects in exchange for access to

natural resource concessions. While the infrastructure is extremely poor, migrant workers force

up unemployment, which lowers government revenue and increases expenditures for social

welfare. Additionally, these projects keep the countries indebted even on 2% loans from the

Chinese government. They favor these for two reasons. The interest rates are lower, helping

decrease payment imbalances, and China promises a don’t ask, don’t tell philosophy regarding

how the governments create policy. Partnering with China has become popular for many

developing countries. China finances capital projects, sends migrant Chinese workers, and

usually requires concessions for lower rates. An example is the rights to most Cobalt that comes

from the Democratic Republic of Congo. Cobalt is the essential commodity used in lithium-ion

batteries for electric cars. This is an illustration of economic abuse by a more advanced

economy. The Congo has been forced to request China stop exporting the raw copper and cobalt

before processing (Reuters, 2017). Without being processed, the minerals are of significantly

lower value. An argument for this foreign direct investment (FDI) is the economic cycle

compared to developed countries. According to the figure, EM is in the early cycle where DM is

in the late cycle, signaling a pullback in leverage toward EM with lower debt-GDP ratios.

Conclusion

Norway understands emerging and least developed countries face fiscal obstacles. They

are prepared to lend support and meet IMF regulatory measures into the distant future. A right-

leaning party recently took control as PM with parliament support. This makes it difficult for

migrants to travel into Norway and remain settled. Pro-business policies will spur continued

economic growth through shifting resource exporting to more sustainable measures for the

region. The sovereign wealth fund is being put to use improving infrastructure, supporting social

18

programs, and investment abroad in equity and debt capital markets. Their investments have

return modestly, helping support sovereign wealth fund contributions.

19

Work Cited

https://atlas.media.mit.edu/en/profile/country/nor/ https://data.oecd.org/trade/trade-in-goods-and-services.htm http://ec.europa.eu/trade/policy/countries-and-regions/countries/norway/ https://www.nytimes.com/2017/05/13/business/china-railway-one-belt-one-road-1-trillion-plan.html http://www.worldstopexports.com/norways-top-10-exports/ http://www.nytimes.com/2005/10/27/world/europe/in-norway-eu-pros-and-cons-the-cons-still-win.html http://rtais.wto.org/UI/PublicSearchByMemberResult.aspx?MemberCode=578&lang=1&redirect=1 https://www.wto.org/english/tratop_e/region_e/rta_participation_map_e.htm https://www.wto.org/english/tratop_e/dispu_e/cases_e/1pagesum_e/ds401sum_e.pdf https://www.regjeringen.no/en/dep/fin/id216/

http://rtais.wto.org/UI/PublicSearchByMemberResult.aspx?MemberCode=578&lang=1&redirec

t=1

https://www.norway.no/en/missions/wto-un/our-priorities/trade/norwegian-

priorities/norwegian-priorities2/

https://www.wto.org/english/tratop_e/region_e/rta_participation_map_e.htm

http://fta.mofcom.gov.cn/english/

http://www.efta.int/free-trade/free-trade-agreements/hong-kong

http://www.ssb.no/en/nasjonalregnskap-og-konjunkturer/nokkeltall/economic-and-financial-data-for-norway https://www.wto.org/english/news_e/news16_e/if_20dec16_e.htm http://www.irinnews.org/news/2004/10/06/norway-releases-balance-payments-aid https://tradingeconomics.com/norway/balance-of-trade http://www.ssb.no/en/ur http://www.imf.org/en/News/Articles/2016/11/17/MS111716-Norway-Staff-Concluding-Statement-of-an-IMF-Staff-Visit

20

2018 Outlook

Large sums of capital have flowed into EM and

international markets in the past year. Institutional

investors, once again, were the first to begin shifting

asset allocations as banks struck record total bond

offerings since before the financial crisis. The

Emerging Markets Club does agree with economists’

view that growth is slowing in many developing

countries, but we do see healthy signs in a couple regions.

The Asia-Pacific has seen an increase in productivity with help from Singapore

continuing its rivalry with Hong Kong as the financial capital. Fintech is assisting local

businesses to better handle money and secure funding on local market exchanges. China’s

corporate debt is of concern at 230% of GDP. India appears a better alternative with GDP growth

accelerating. Thailand geopolitical risk remains with the welcome of its new King atop its

Monarchy who has close control over the

military government.

Peru is another growth prospect,

given recent reforms will remain in place

and stabilize the federal government. Its

ability to limit illegal trade within the

country borders can increase government

revenue for capital projects. In turn, better

infrastructure will move goods and services

efficiently across regions.

Developed market investors are chasing yields and have shifted from equity to debt as

well. This demand is already forcing US equity dividend rate to increase and maintain pace.

Cobalt was one mineral mentioned but global commodity prices have been subdued and are

21

primed for an increase. A rise in inflation is expected and would further boost prices. A

weakening dollar assists emerging economies to export to the US as it is cheaper for Americans.

Overall, we like what we see in the emerging market cycle and suggests exposure to

South American commodities and Asia-pacific manufacturing excluding China.