34

1

A mature company that still has much to offer

Societatea Energetica Electrica SA (EL) is the most important player in the field of distribution, supply and other energy-related services in Romania. Established in 1998, EL has a 40.3% market share of electricity distribution and a 22% of electricity supply as measured by terawatt-hours [TWh] volumes.

1

We issue a BUY recommendation for Societatea Energetica Electrica SA, with a one-year target price of RON16.74. This is equivalent to a 19.7% upside from the closing price of RON13.98 on February 9

th, 2017. We base our decision on a Discounted Free Cash Flow

to Equity Model, a Relative Valuation through Peer Multiples Comparison and a Monte Carlo simulation validation. Our recommendation is based on the following: Steady revenue stream from distribution EL has exclusive distribution rights over a good portion of the regions in Romania. This secures predictability of revenues, cash flows and returns. The supply part of the business synergises greatly with the distribution part, and the company is looking forward to improve the services it offers. Strong overall financial position The company has substantial cash holdings, proceeds from the IPO, and little to no financing through debt, with a capital structure consisting of more than 94% equity. One important objective of the company’s management is currently improving the margins through new investments.

Little impact of liberalisation Taking a look at the almost non-existent impact of the natural gas market liberalisation in Romania as well as at the effects of liberalisation in other European electricity markets we concluded that the full electricity market liberalisation in 2018 would not fundamentally change any factors that contribute to the value of Electrica. Fondul Proprietatea There is optimism surrounding a deal of acquiring the 22% non-controlling interest in four of EL’s subsidiaries. Even though the last year’s negotiations haven’t concluded in a transaction, both parties admitted they are open to new talks. This could mean higher dividend yields, EPS and, as a consequence, a higher share price for Electrica. We study this possibility in the report, and the numbers that result.

Income statement in thousands RON 2013 2014 2015 2016e

Total revenues 5,511,135 5,220,237 5,713,956 5,972,143 Total expenses (4,839,997) (4,351,093) (4,792,135) (4,977,816)

EBITDA 671,138 869,144 921,821 994,327 Impairment, depreciation & amortisation (325,688) (358,512) (353,181) (405,005) Interest and taxes (29,803) (97,727) (86,480) (108,909) Profit to Minority Interest (71,235) (116,099) (119,485) (132,026) Profit attributable to Shareholders 244,412 296,806 362,675 348,387

Balance sheet in thousands RON 2013 2014 2015 2016e

Current Assets 4,115,781 3,765,253 3,843,116 3,492,404 Non-current Assets 4,307,209 4,382,414 4,548,169 4,786,055

Total Assets 8,422,990 8,147,667 8,391,285 8,278,459

Current Liabilities 1,365,986 1,249,863 1,408,394 1,315,191 Long-Term Liabilities 611,386 609,096 540,301 509,265

Total Liabilities 1,977,372 1,858,959 1,948,695 1,824,456

Total Equity 6,445,618 6,288,708 6,442,590 6,454,004

Total Equity and Liabilities 8,422,990 8,147,667 8,391,285 8,278,459

10.5

11

11.5

12

12.5

13

13.5

14

14.5

03/07/2014 03/07/2015 03/07/2016

Fig.1 Market Info, Valuation Results

and Stock Chart

Market Data 52-Week Low 52-Week High Average Price Shares Outstanding Mkt Cap(RON) Dividend Yield P/E IPO

RON 11.16 RON 14.16 RON 14.00

345,939,929 4,870,834,200

5.99 16.19

4 Jul 2014

Source: Bucharest Stock Exchange

Valuation methods

DCF Multiples Target Price

(50%) (50%)

RON16.78 RON16.69 RON16.74

Recommendation BUY

Target Price(RON) Closing Price(RON) Feb 09, 2017

Upside(%) (excl. Dividends) 1RON Feb 09, 2017

16.74 13.98

19.7

0.22EUR 0.24USD

Alexandru Ioan Cuza University of Iasi - Student Research This report is published for educational purposes only by students competing in the CFA Institute Research Challenge

Industrial Sector, Utilities Industry

Bucharest Stock Exchange

ISIN code: ROELECACNMOR5 Bloomberg: EL RO Societatea Energetica Electrica Reuters: ROEL.BX

2

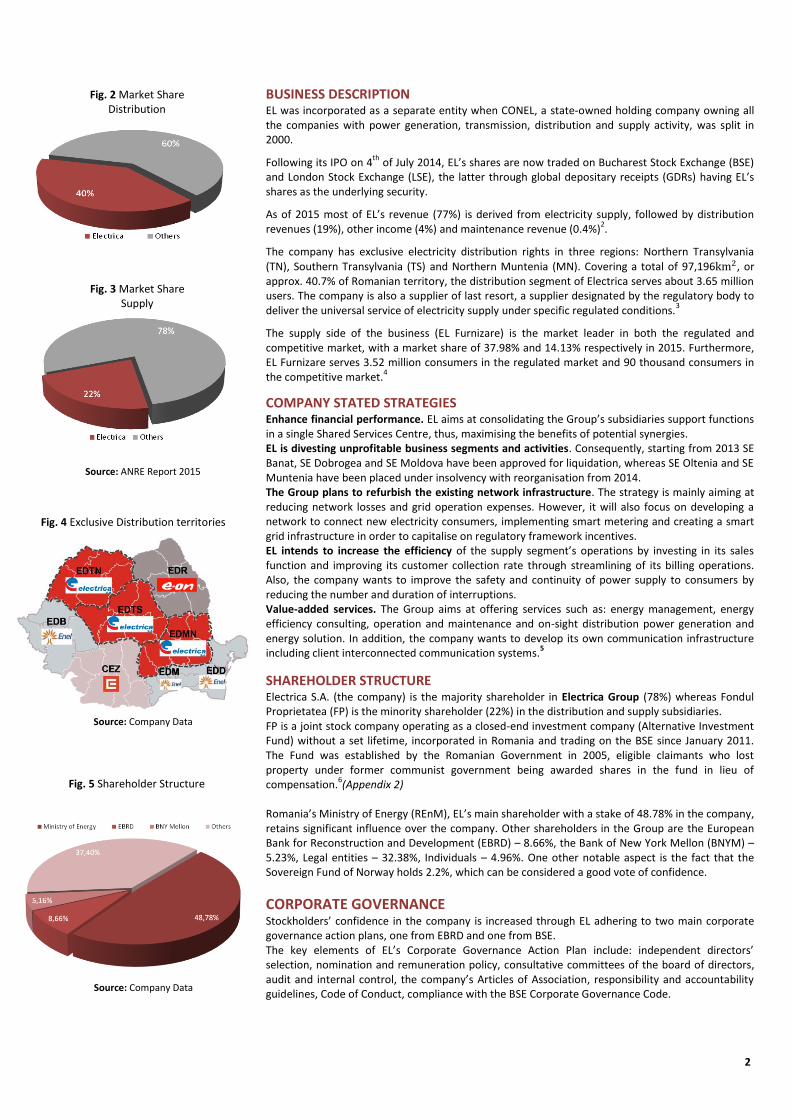

BUSINESS DESCRIPTION EL was incorporated as a separate entity when CONEL, a state-owned holding company owning all the companies with power generation, transmission, distribution and supply activity, was split in 2000.

Following its IPO on 4th

of July 2014, EL’s shares are now traded on Bucharest Stock Exchange (BSE) and London Stock Exchange (LSE), the latter through global depositary receipts (GDRs) having EL’s shares as the underlying security.

As of 2015 most of EL’s revenue (77%) is derived from electricity supply, followed by distribution revenues (19%), other income (4%) and maintenance revenue (0.4%)

2.

The company has exclusive electricity distribution rights in three regions: Northern Transylvania (TN), Southern Transylvania (TS) and Northern Muntenia (MN). Covering a total of 97,196km2, or approx. 40.7% of Romanian territory, the distribution segment of Electrica serves about 3.65 million users. The company is also a supplier of last resort, a supplier designated by the regulatory body to deliver the universal service of electricity supply under specific regulated conditions.

3

The supply side of the business (EL Furnizare) is the market leader in both the regulated and competitive market, with a market share of 37.98% and 14.13% respectively in 2015. Furthermore, EL Furnizare serves 3.52 million consumers in the regulated market and 90 thousand consumers in the competitive market.

4

COMPANY STATED STRATEGIES

Enhance financial performance. EL aims at consolidating the Group’s subsidiaries support functions in a single Shared Services Centre, thus, maximising the benefits of potential synergies. EL is divesting unprofitable business segments and activities. Consequently, starting from 2013 SE Banat, SE Dobrogea and SE Moldova have been approved for liquidation, whereas SE Oltenia and SE Muntenia have been placed under insolvency with reorganisation from 2014. The Group plans to refurbish the existing network infrastructure. The strategy is mainly aiming at reducing network losses and grid operation expenses. However, it will also focus on developing a network to connect new electricity consumers, implementing smart metering and creating a smart grid infrastructure in order to capitalise on regulatory framework incentives. EL intends to increase the efficiency of the supply segment’s operations by investing in its sales function and improving its customer collection rate through streamlining of its billing operations. Also, the company wants to improve the safety and continuity of power supply to consumers by reducing the number and duration of interruptions. Value-added services. The Group aims at offering services such as: energy management, energy efficiency consulting, operation and maintenance and on-sight distribution power generation and energy solution. In addition, the company wants to develop its own communication infrastructure including client interconnected communication systems.

5

SHAREHOLDER STRUCTURE Electrica S.A. (the company) is the majority shareholder in Electrica Group (78%) whereas Fondul Proprietatea (FP) is the minority shareholder (22%) in the distribution and supply subsidiaries. FP is a joint stock company operating as a closed-end investment company (Alternative Investment Fund) without a set lifetime, incorporated in Romania and trading on the BSE since January 2011. The Fund was established by the Romanian Government in 2005, eligible claimants who lost property under former communist government being awarded shares in the fund in lieu of compensation.

6(Appendix 2)

Romania’s Ministry of Energy (REnM), EL’s main shareholder with a stake of 48.78% in the company, retains significant influence over the company. Other shareholders in the Group are the European Bank for Reconstruction and Development (EBRD) – 8.66%, the Bank of New York Mellon (BNYM) – 5.23%, Legal entities – 32.38%, Individuals – 4.96%. One other notable aspect is the fact that the Sovereign Fund of Norway holds 2.2%, which can be considered a good vote of confidence.

CORPORATE GOVERNANCE Stockholders’ confidence in the company is increased through EL adhering to two main corporate governance action plans, one from EBRD and one from BSE. The key elements of EL’s Corporate Governance Action Plan include: independent directors’ selection, nomination and remuneration policy, consultative committees of the board of directors, audit and internal control, the company’s Articles of Association, responsibility and accountability guidelines, Code of Conduct, compliance with the BSE Corporate Governance Code.

Source: ANRE Report 2015

Fig. 5 Shareholder Structure

Source: Company Data

Fig. 4 Exclusive Distribution territories

Source: Company Data

Fig. 3 Market Share Supply

Fig. 2 Market Share Distribution

3

Shareholders must approve through vote (in proportion of at least 55%) any investment in excess of EUR30m, the company’s CAPEX plan, any M&A transactions contemplated, any amendment of the Constitutive Act, and any major donations made by the company.

7

EL is governed through the help of three main corporate bodies: the General Meeting of Shareholders (GMS), which is the highest decision-making forum in the company, The Board of Directors (BoD) comprised of seven non-executive members, and the General Manager, having a four-year mandate. The Board of Directors has three consultative committees: Audit and Risk Committee, Nomination and Remuneration Committee and Strategy, Restructuring & Corporate Governance Committee.

8

EBRD’s involvement has contributed to EL’s decision to create a corporate governance structure that is appealing to private investors. The REnM was only allowed to nominate two board members, with the other 3 board members entirely independent and nominated by the other shareholders. Although this was the case following its IPO, the REnM proposed and enforced a decision to have a total of 7 members in the BoD, nominating three of them since December 14

th, 2015.

9

There is a trend towards adopting equity-type compensation, as documented by another Romanian EBRD investment in Romgaz, where a performance and merit based system, linked to both earnings and share price was implemented. This will likely align the interests of both the management and shareholders, producing in the end sustainable continuing value. As of December 2016, 6 executive members hold 0.02% of outstanding shares.

The General Manager of EL, Dan Catalin Stancu, started his mandate on October 24, 2016. He has over 19 years of experience in the group from 1990, and has occupied several management positions including Director of Business Development and Privatization and had board membership in EDMN, EDTN and CEZ Oltenia when EL still had ownership stake in it.

10 From 2009 he held

positions in E.On, the distributor from Eastern region of Romania, as Director of Strategy and Business Development, and he was a member of E.On Distributie and E.On Renewable Romania boards of directors.

Social Responsibility EL aims at carrying out its operations as a responsible player on the energy market. Furthermore, social involvement is a core part of the company’s strategy, as documented by its Code of Ethics and Professional Conduct. EL has participated mainly in culturally and educationally sustainable projects with a long-term impact including: “Hospices of Hope”, ”Save the Children”, ”Because we care”, ”Let’s do it Romania”, “The Story of Light”. It is also a partner of the George Enescu Classical Music Festival.

11

INDUSTRY OVERVIEW Macroeconomics According to IMF, Romania showed a strong GDP growth during 2013-2015. The country’s 3.66% growth in 2015 in contrast to EU countries’ average of 2.2% has put Romania amongst the highest-growing economies in the EU. With Romania’s GDP growth in 2016 at 5%, analysts from World Bank are projecting a high future growth for the country annually averaging 3.20% towards 2020.

12

Due to the fading impact of VAT rate cuts, fiscal policy easing and the rising wage costs, Romanian inflation is forecasted to remain stable within the interval 1.5%-3.5% from 2017 onward.

Romanian and EU Electricity Market In Romania the price of electricity for industry and households (excluding taxes and levies) is about 24% and 32%, respectively, lower than in the European Union. The country is also the third most energy independent country in the EU after Denmark and Estonia. On average EU countries are 54% dependent on energy, whereas Romania is importing only 17% of gas and oil from Russia, as of 2015.

13

Political Situation Uncertainty arises after an unexpected election result putting the Socialist Democrat party in charge of Romania’s parliament with more than 45% of the seats as of December 2016. Populist agenda items could arise and interfere with market liberalisation and regulation. Consequently, the ruling party plans to impose a higher threshold of obligatory dividend distribution and a minimum quota of 90% on net realized income.

14 Furthermore, the Ministry of Economy has

restructuring plans for energy companies’ state ownership, such as EL.15

To further exacerbate the matters, according to the central bank of Romania (BNR), the current government budget is based on an over-estimated future economic growth of 5%.

Board Member Independent Term (2016)

Cristian Busu No 1 year

Arielle Malard de Rothschild

Yes 4years

Ioana Dragan No 4years

Corina Popescu No 4years

Bogdan Iliescu Yes 4years

Willem Schoeber

Yes 4years

Pedro Mielgo Alvarez

Yes 4years

Leadership % of Outstanding Shares

Board of Directors 0% Executive Officers 0.02%

Leadership Compensation(2015)

Top Executives (4 disclosures)

RON5,540 thou.

Members of BoD RON5,362 thou.

Fig. 6 Subsidiaries’ Ownership

Source: Company Data

Source: Company Data

Fig. 7 Board of Directors

Fig. 9 Equity Compensation

Fig. 10 GDP Growth - RO/EU28

Source: Eurostat

Source: Company Data

Source: Company Data

Fig. 8 Leadership Compensation

4

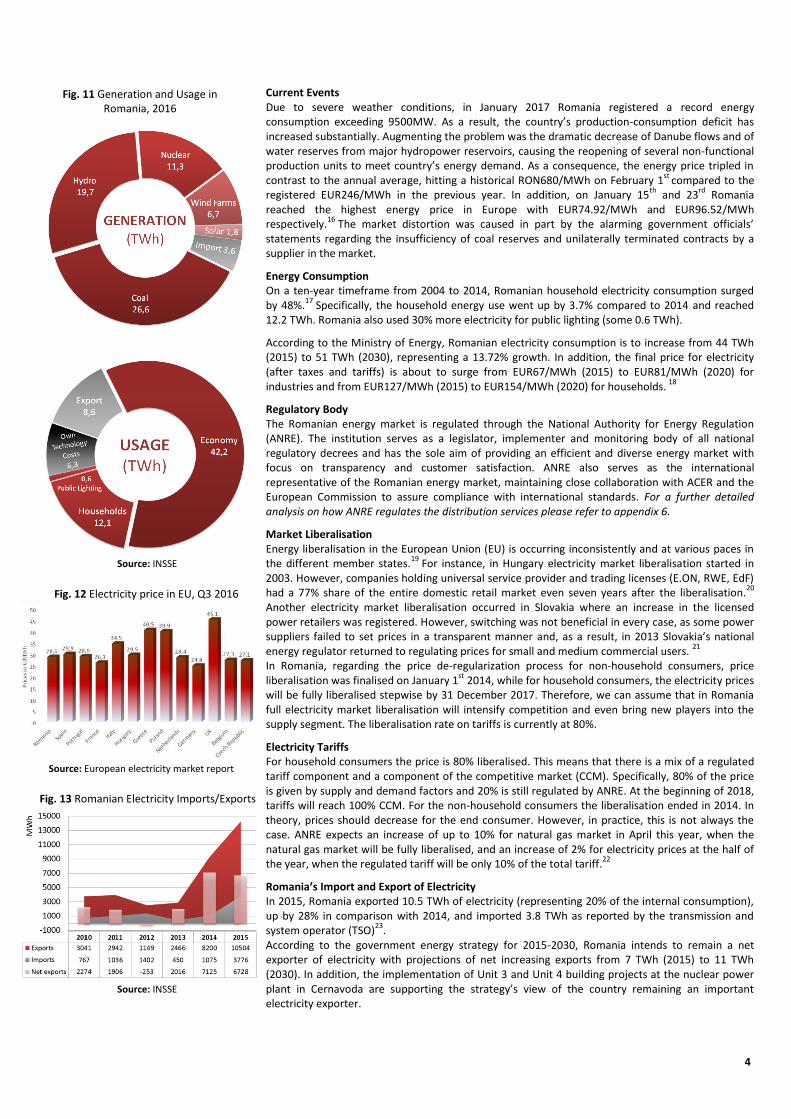

Current Events Due to severe weather conditions, in January 2017 Romania registered a record energy consumption exceeding 9500MW. As a result, the country’s production-consumption deficit has increased substantially. Augmenting the problem was the dramatic decrease of Danube flows and of water reserves from major hydropower reservoirs, causing the reopening of several non-functional production units to meet country’s energy demand. As a consequence, the energy price tripled in contrast to the annual average, hitting a historical RON680/MWh on February 1

st compared to the

registered EUR246/MWh in the previous year. In addition, on January 15th

and 23rd

Romania reached the highest energy price in Europe with EUR74.92/MWh and EUR96.52/MWh respectively.

16 The market distortion was caused in part by the alarming government officials’

statements regarding the insufficiency of coal reserves and unilaterally terminated contracts by a supplier in the market.

Energy Consumption On a ten-year timeframe from 2004 to 2014, Romanian household electricity consumption surged by 48%.

17 Specifically, the household energy use went up by 3.7% compared to 2014 and reached

12.2 TWh. Romania also used 30% more electricity for public lighting (some 0.6 TWh).

According to the Ministry of Energy, Romanian electricity consumption is to increase from 44 TWh (2015) to 51 TWh (2030), representing a 13.72% growth. In addition, the final price for electricity (after taxes and tariffs) is about to surge from EUR67/MWh (2015) to EUR81/MWh (2020) for industries and from EUR127/MWh (2015) to EUR154/MWh (2020) for households.

18

Regulatory Body The Romanian energy market is regulated through the National Authority for Energy Regulation (ANRE). The institution serves as a legislator, implementer and monitoring body of all national regulatory decrees and has the sole aim of providing an efficient and diverse energy market with focus on transparency and customer satisfaction. ANRE also serves as the international representative of the Romanian energy market, maintaining close collaboration with ACER and the European Commission to assure compliance with international standards. For a further detailed analysis on how ANRE regulates the distribution services please refer to appendix 6.

Market Liberalisation Energy liberalisation in the European Union (EU) is occurring inconsistently and at various paces in the different member states.

19 For instance, in Hungary electricity market liberalisation started in

2003. However, companies holding universal service provider and trading licenses (E.ON, RWE, EdF) had a 77% share of the entire domestic retail market even seven years after the liberalisation.

20

Another electricity market liberalisation occurred in Slovakia where an increase in the licensed power retailers was registered. However, switching was not beneficial in every case, as some power suppliers failed to set prices in a transparent manner and, as a result, in 2013 Slovakia’s national energy regulator returned to regulating prices for small and medium commercial users.

21

In Romania, regarding the price de-regularization process for non-household consumers, price liberalisation was finalised on January 1

st 2014, while for household consumers, the electricity prices

will be fully liberalised stepwise by 31 December 2017. Therefore, we can assume that in Romania full electricity market liberalisation will intensify competition and even bring new players into the supply segment. The liberalisation rate on tariffs is currently at 80%.

Electricity Tariffs For household consumers the price is 80% liberalised. This means that there is a mix of a regulated tariff component and a component of the competitive market (CCM). Specifically, 80% of the price is given by supply and demand factors and 20% is still regulated by ANRE. At the beginning of 2018, tariffs will reach 100% CCM. For the non-household consumers the liberalisation ended in 2014. In theory, prices should decrease for the end consumer. However, in practice, this is not always the case. ANRE expects an increase of up to 10% for natural gas market in April this year, when the natural gas market will be fully liberalised, and an increase of 2% for electricity prices at the half of the year, when the regulated tariff will be only 10% of the total tariff.

22

Romania’s Import and Export of Electricity In 2015, Romania exported 10.5 TWh of electricity (representing 20% of the internal consumption), up by 28% in comparison with 2014, and imported 3.8 TWh as reported by the transmission and system operator (TSO)

23.

According to the government energy strategy for 2015-2030, Romania intends to remain a net exporter of electricity with projections of net increasing exports from 7 TWh (2015) to 11 TWh (2030). In addition, the implementation of Unit 3 and Unit 4 building projects at the nuclear power plant in Cernavoda are supporting the strategy’s view of the country remaining an important electricity exporter.

Fig. 11 Generation and Usage in Romania, 2016

Source: INSSE

Fig. 12 Electricity price in EU, Q3 2016

Source: European electricity market report

Fig. 13 Romanian Electricity Imports/Exports

Source: INSSE

5

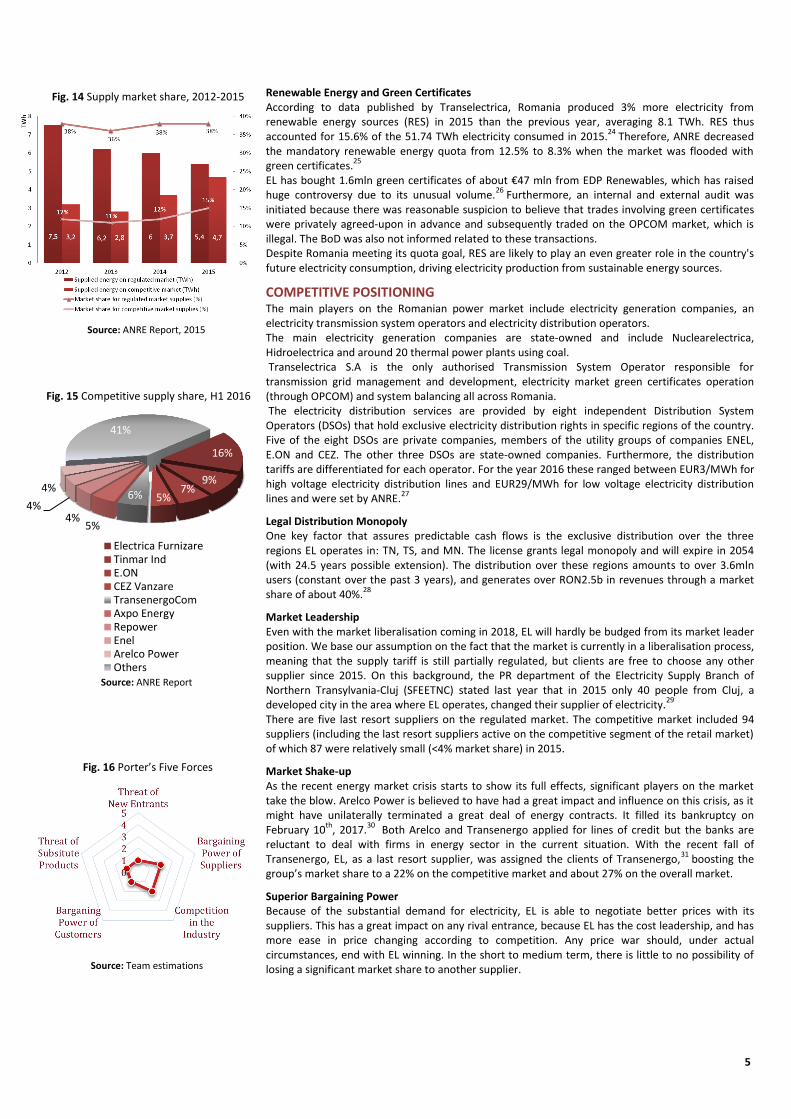

Renewable Energy and Green Certificates According to data published by Transelectrica, Romania produced 3% more electricity from renewable energy sources (RES) in 2015 than the previous year, averaging 8.1 TWh. RES thus accounted for 15.6% of the 51.74 TWh electricity consumed in 2015.

24 Therefore, ANRE decreased

the mandatory renewable energy quota from 12.5% to 8.3% when the market was flooded with green certificates.

25

EL has bought 1.6mln green certificates of about €47 mln from EDP Renewables, which has raised huge controversy due to its unusual volume.

26 Furthermore, an internal and external audit was

initiated because there was reasonable suspicion to believe that trades involving green certificates were privately agreed-upon in advance and subsequently traded on the OPCOM market, which is illegal. The BoD was also not informed related to these transactions. Despite Romania meeting its quota goal, RES are likely to play an even greater role in the country's future electricity consumption, driving electricity production from sustainable energy sources.

COMPETITIVE POSITIONING The main players on the Romanian power market include electricity generation companies, an electricity transmission system operators and electricity distribution operators. The main electricity generation companies are state-owned and include Nuclearelectrica, Hidroelectrica and around 20 thermal power plants using coal. Transelectrica S.A is the only authorised Transmission System Operator responsible for transmission grid management and development, electricity market green certificates operation (through OPCOM) and system balancing all across Romania. The electricity distribution services are provided by eight independent Distribution System Operators (DSOs) that hold exclusive electricity distribution rights in specific regions of the country. Five of the eight DSOs are private companies, members of the utility groups of companies ENEL, E.ON and CEZ. The other three DSOs are state-owned companies. Furthermore, the distribution tariffs are differentiated for each operator. For the year 2016 these ranged between EUR3/MWh for high voltage electricity distribution lines and EUR29/MWh for low voltage electricity distribution lines and were set by ANRE.

27

Legal Distribution Monopoly One key factor that assures predictable cash flows is the exclusive distribution over the three regions EL operates in: TN, TS, and MN. The license grants legal monopoly and will expire in 2054 (with 24.5 years possible extension). The distribution over these regions amounts to over 3.6mln users (constant over the past 3 years), and generates over RON2.5b in revenues through a market share of about 40%.

28

Market Leadership Even with the market liberalisation coming in 2018, EL will hardly be budged from its market leader position. We base our assumption on the fact that the market is currently in a liberalisation process, meaning that the supply tariff is still partially regulated, but clients are free to choose any other supplier since 2015. On this background, the PR department of the Electricity Supply Branch of Northern Transylvania-Cluj (SFEETNC) stated last year that in 2015 only 40 people from Cluj, a developed city in the area where EL operates, changed their supplier of electricity.

29

There are five last resort suppliers on the regulated market. The competitive market included 94 suppliers (including the last resort suppliers active on the competitive segment of the retail market) of which 87 were relatively small (<4% market share) in 2015.

Market Shake-up As the recent energy market crisis starts to show its full effects, significant players on the market take the blow. Arelco Power is believed to have had a great impact and influence on this crisis, as it might have unilaterally terminated a great deal of energy contracts. It filled its bankruptcy on February 10

th, 2017.

30 Both Arelco and Transenergo applied for lines of credit but the banks are

reluctant to deal with firms in energy sector in the current situation. With the recent fall of Transenergo, EL, as a last resort supplier, was assigned the clients of Transenergo,

31 boosting the

group’s market share to a 22% on the competitive market and about 27% on the overall market.

Superior Bargaining Power Because of the substantial demand for electricity, EL is able to negotiate better prices with its suppliers. This has a great impact on any rival entrance, because EL has the cost leadership, and has more ease in price changing according to competition. Any price war should, under actual circumstances, end with EL winning. In the short to medium term, there is little to no possibility of losing a significant market share to another supplier.

16%

9% 7%

5% 6%

5% 4%

4%

4%

41%

Electrica FurnizareTinmar IndE.ONCEZ VanzareTransenergoComAxpo EnergyRepowerEnelArelco PowerOthers

Source: ANRE Report, 2015

Fig. 14 Supply market share, 2012-2015

Source: ANRE Report

Fig. 15 Competitive supply share, H1 2016

Source: Team estimations

Fig. 16 Porter’s Five Forces

6

INVESTMENT SUMMARY Steady Growth of Revenue According to recent breakthroughs in statistical modelling and satellite imagery, advancements in a very interesting field have been made – forecasting human well being with the help of night-time lights.

32 A company from Japan is employing these practices and already forecasts inflation and GDP

according to images from satellite. Knowing some specifics about the modelling and correlations behind, we believe that EL will perform in line with Romania’s economy growth.

33(Appendix 8)

Costs Optimization The management is targeting to employ a 2% yearly decrease in operational costs. This will be achieved through the intended transition to Smart Grids, smart metering and implementation of systems such as SCADA and SAD in order to assure operational efficiency, reduction of losses and improvement of grid flexibility. Cost optimization and reduction in network losses are a focal point of the company because of the regulations’ efficiency targets and profit incentives for optimization. Since 1.75% is the efficiency target set by ANRE, we will assume they will neither lose nor win from meeting or exceeding it.

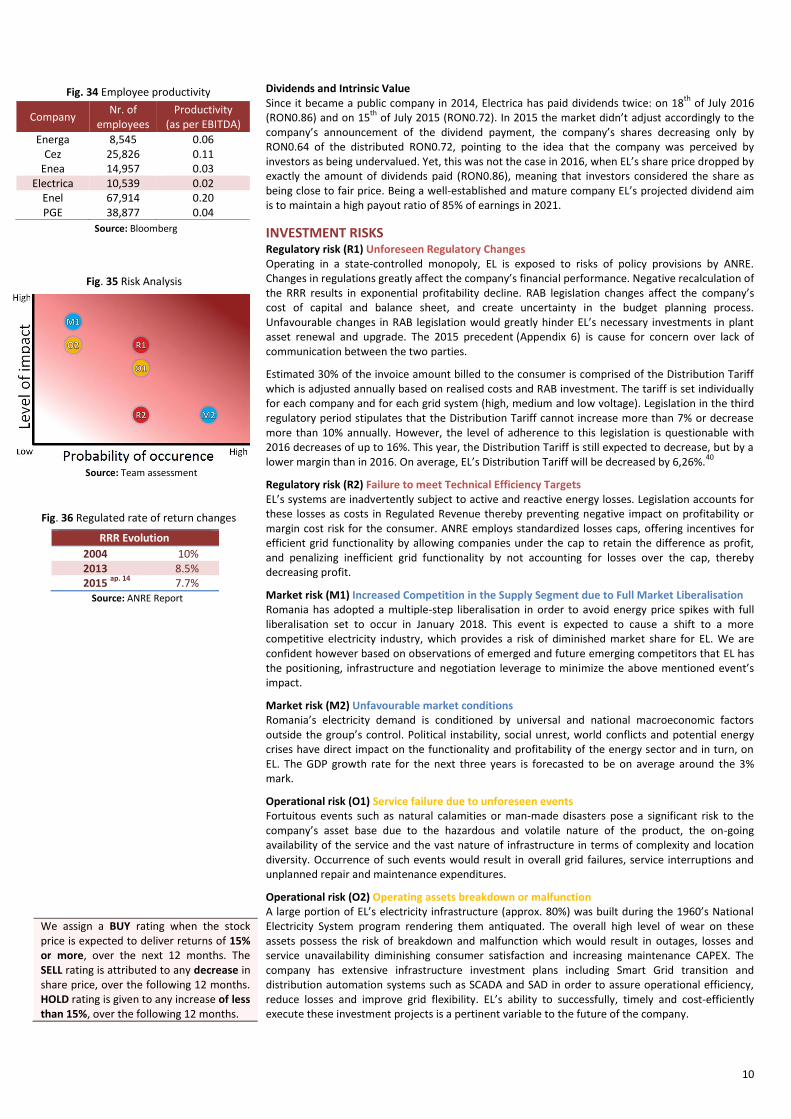

Sound Cash Position With over RON2.5bln in cash and other investment vehicles, most of the holdings coming in the form of proceeds from the IPO, it is undeniably clear that there is a large array of possibilities to increase the future cash flows. Thus, not only can EL stick to its investment plan, but also, the company can acquire the minority interest of 22% from FP in four of its subsidiaries. The DPS would then increase in 2017 from 0.88 to 1.13, resulting in a dividend yield of 7.45 from 6.11, and earnings per share attributable to shareholders of 1.39 from 1.09. As a bottom line, we estimate the share price to reach the mid RON19. Since the market is shaken up from the recent events in the energy sector, the probability of EL taking an M&A decision seems more possible than ever. Last year, EL had a chance to buy 30% ownership in E.ON, the distributor on the Eastern region of Romania, since the present CEO of EL was also the Director of Strategy and Business Development in the recent years of E.ON and member of E.ON’s BoD.

Effortless Increase in Market Share An easy 4% overall market share increase (competitive and regulated market cumulated - Transenergo had 6% on the competitive market in 2015)

34 was achieved by EL after the bankruptcy

filing of the above mentioned important market player on the competitive market. The clients have limited choices, and even if some might migrate to other competitors, such an easy and almost effortless upgrade of revenue streams has to be taken in consideration.

Bond Behaviour According to Bloomberg Default Risk, EL has a 0.0064% probability to default on its debt within a year, earning the company an Investment grade rating of IG3 (the AA equivalent for S&P/Fitch).

35

From this perspective, holding EL in your portfolio is similar to holding High Credit Quality bonds. Such bonds have low interest rate payments since the risk of them defaulting is low. Yet, one would prefer EL shares to bonds, since for the same amount of risk or even less the company provides owners with the benefits of steady returns and dividends growth.

Strong Dividend Policy The management states that they plan an 85% dividend pay-out ratio, and considering the 82.44% dividend pay-out ratio in 2014 and 80.40% in 2015, they can deliver on this promise. It is a consistent source of returns for investors, with a dividend yield of about 6%, above the peer median.

Equity Index Outperformance It is worth mentioning that the stock has an annualized return almost three times above the BET Index, the Romanian index that comprises the 10 most traded companies on BSE (excluding financial investment firms and including EL with a weight of 8.3%). Together with the safety of the investment mentioned above, and market outperforming returns, EL is shaping to be a must-have in every investor’s portfolio looking to invest in Romanian equity markets. Because of the current potential instability in the fiscal governance of Romania we are testing how sensitive our model is to changes in total amount of taxes paid, and how much does the long-term growth change if the weights of inflation and GDP growth in explaining the revenue growth differ.

2017 FP Sells FP Stays

EPS 1.39 1.09

DPS 1.13 0.88

Dividend Yld 7.45 6.11

Fig. 17 Romania and The Republic of Moldova 1992&2003

Night-time lights heat-map

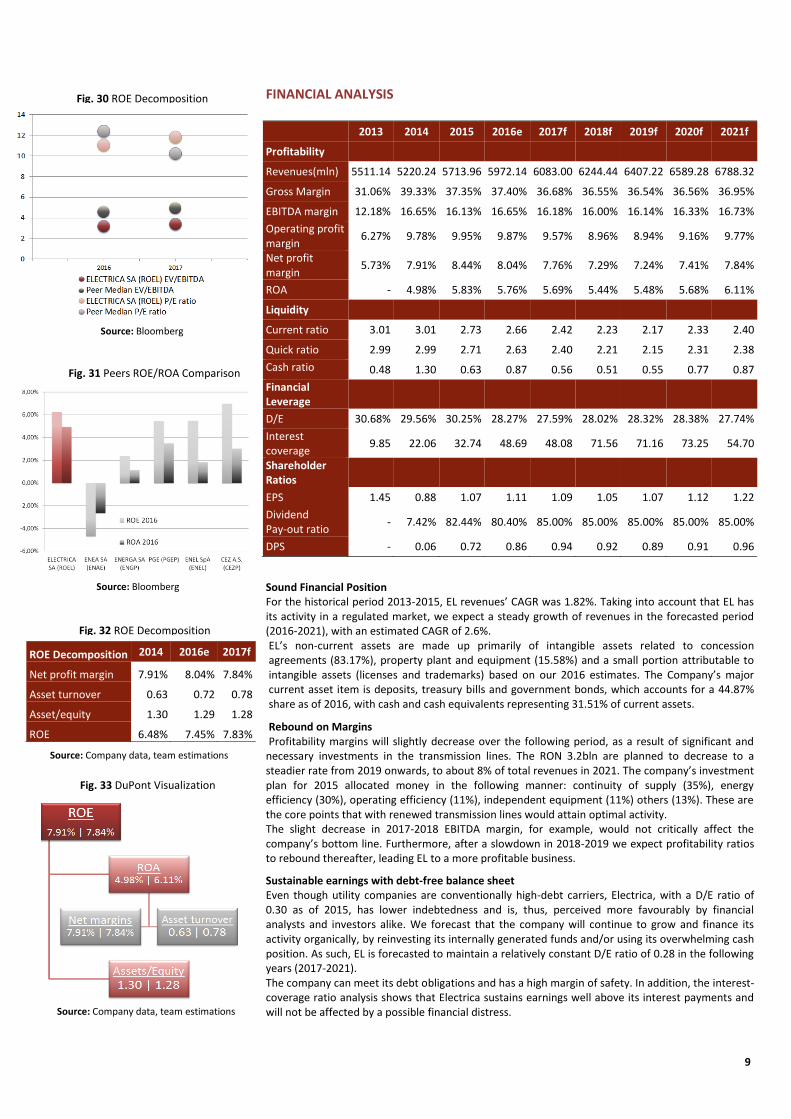

Fig. 18 Correlations between IC&T development estimate-official IC&T data-GDP

Fig. 19 Scenario analysis on minority interest

Source: NOAA Geophysical Data centre

Source: Univ.of Colorado & Denver Thesis

Source: Team calculations

7

Weight of Growth explained by GDP Growth

To

tal E

ffec

tive

Tax

70.0% 75.0% 80.0% 86.0% 90.0% 95.0% 100.0%

17.0% 17.27 17.30 17.34 17.38 17.41 17.45 17.49

18.0% 17.07 17.10 17.14 17.18 17.21 17.25 17.28

19.0% 16.87 16.90 16.94 16.98 17.01 17.05 17.08

20.0% 16.67 16.70 16.74 16.78 16.81 16.84 16.88

21.0% 16.47 16.50 16.54 16.58 16.61 16.64 16.67

22.0% 16.27 16.30 16.34 16.38 16.40 16.44 16.47

23.0% 16.07 16.11 16.14 16.18 16.20 16.24 16.27

Source: Team calculations

VALUATION We evaluated EL using three models: Discounted Cash-Flow Model (DCF), Relative Valuation Multiples Analysis and checked our assumptions through a Monte Carlo Simulation, based on our valuation assumptions. Our investment decision is based on proportional weighting of the methods used, 50% multiples’ resulted price and 50% DCF analysis resulted price.

Discounted Cash-Flow Model To value the company, we used DCF Model with a five-year forecast period after which a terminal free cash flow with a perpetual growth of 3% (GDP growth forecasted) was employed. Our valuation generated a Target Price of RON 16.78 per common share. Our DCF model relies heavily on the following factors and assumptions:

Total revenues We can easily predict a general direction for the revenues, since it’s a defensive business. As we’ve mentioned, the exclusive rights to distribute on the three regions make it easy to forecast the distribution activity of EL, which is roughly 18% of total revenues. Taking into consideration the satellite imagery statistical relationships, we assume a revenue growth rate above inflation rate that is roughly 2.6% from 2018 onwards, and in line with the GDP growth rate, considering the strong relationship – approx. 87% correlation - between the IC&T development index (IDI official data) estimation through satellite imagery and GDP growth, which is approx. 3.2% from 2018 onwards.

36

Non-household Migration Rates The migration rate of large non-household consumers from one supplier to another has increased from 9.4% in 2014 to 13.3% in 2015. These customers amount to 55.4% from the supply revenues in 2015. Extrapolating from 2015 data, but rounding to 15% migration rate, together with the 22% supply market share in 2015, we estimate the impact on the revenues to be 2% at most yearly, together with some margin of error, 1.62% being the impact in 2015.

Market Liberalisation Impact on Supply Business For the supply we estimate an initial decrease of 2% from total growth in 2018. We then decrease supply revenues, as stated above, with 2%, about 1.85% coming from non-household migration rate and the rest of 0.15% from households. This would translate into a 3.5% household migration assumption, and we based it on past estimations and reports. One such report from ANRE states the fact that, as a result of market liberalisation of natural gas market in 2007, until 2011, in a three years span, only fewer than 100 households decided to switch their gas supplier.

37

CAPEX Because of the wear level of the existing equipment, the firm has to invest heavily in the following period, with a budget approved by ANRE of RON3.2bln. EL will thus undergo significant improvements and optimizations, which translates to a plan of RON3.2bln up to the end of the regulatory period, the end of 2018.

38 This also means that for each years’ amount of CAPEX, EL has a

RRR on RAB of 7.7% the following year. We are gradually increasing capital expenditures up to 2019 when we consider they will level, and following the regulatory period EL will primarily invest in maintenance.

Long-term Growth Rate Our 3% assumption is based on the increasing GDP growth rate. Romania has one of the highest European GDP growth rates in the recent years, the highest after Poland, and in 5 years it is unlikely for it to diminish, excluding a black swan event.

39 World Bank estimates the GDP growth from 2018

to be 3.26%. It is explained by 83% share GDP growth and 17% inflation, as of the statistical model.

Source: Company data, Team calculations

Source: Team calculations

Fig. 20 Stock performance compared to index since IPO

Fig. 21 Sensitivity analysis on amount of taxes/long-term growth assumption

Fig. 22 Revenue projection

Fig. 23 Revenue breakdown

Source: Company data, Team calculations

Source: Company data, Team calculations

Fig. 24 Fixed assets/CAPEX evolution

8

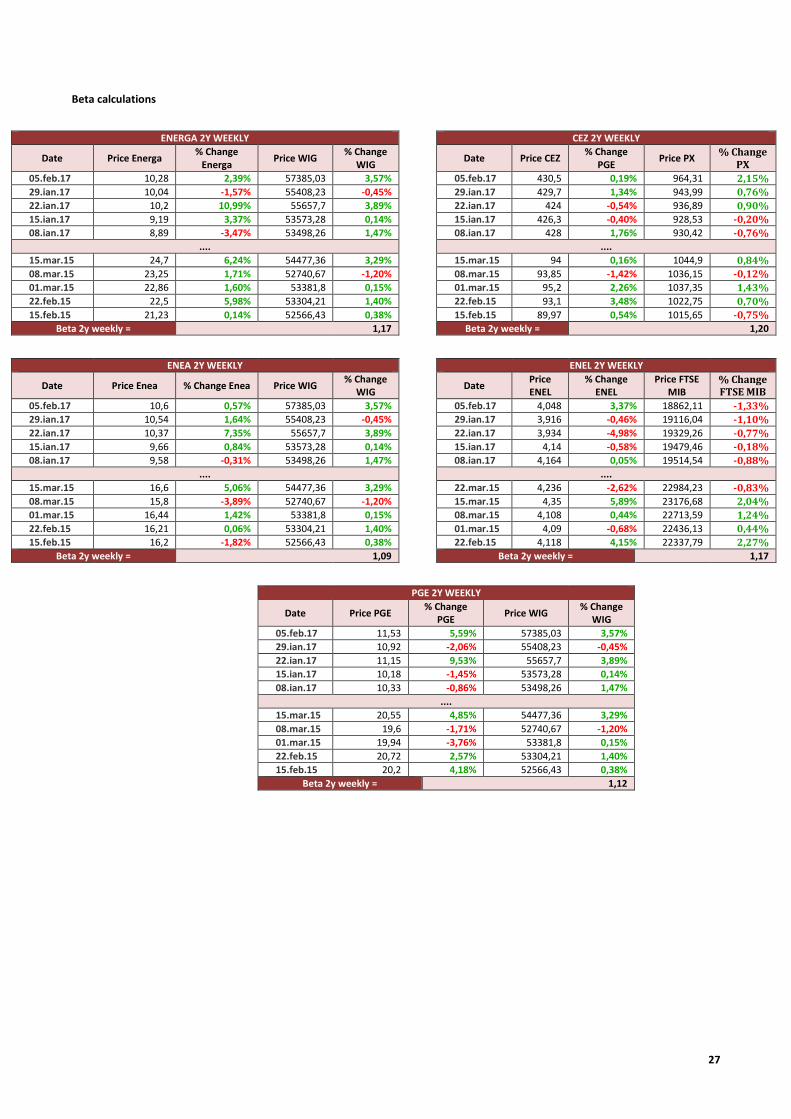

Weighted Average Cost of Capital For the computation of WACC we used a target capital structure of 6%/94% Debt/Equity. The cost of equity was calculated using the CAPM model. For the risk free rate we used the 10-year Romanian Government Bond YTM rate of 4.00%, highest during the month. The risk free rate plus an AAA credit spread (according to Damodaran, based on interest coverage ratio of the company) was used to calculate cost of debt, 4.60%. Beta was computed as the median value of the unlevered beta coefficients observed weekly during a 2-year period for the chosen peer companies in comparison with each their respective market index. Levered beta using the target D/E is 0.76. The market risk premium is 7.95% based on Damodaran’s two estimations methods. According to the aforementioned data, we derived a levered cost of equity of 10.05%. Based on our computation, the WACC for EL is 9.70%. (Appendix 10)

Debt EL, in the past recent years, uses mostly short-term debt, such as overdrafts. As of December 2016, the capital structure of EL is 5.1:94.9(%) Debt/Equity. The management stated that they tend to be debt adverse, and we can observe that in the recent years they have little to no long-term debt. We assume that in the mid-term horizon, they will require additional financing since large finance new investments from internal sources, organically, as we set a target debt of 6.00%.

Terminal Value Long-term Growth Rate

Wei

ghte

d A

vera

ge C

ost

of

Cap

ital

2.1% 2.4% 2.7% 3.0% 3.3% 3.6% 3.9%

8.8% 18.62 18.73 18.84 18.97 19.10 19.25 19.42

9.1% 17.92 18.00 18.08 18.17 18.27 18.37 18.48

9.4% 17.28 17.34 17.39 17.45 17.51 17.57 17.64

9.7% 16.68 16.71 16.75 16.78 16.83 16.86 16.90

10.0% 16.15 16.16 16.18 16.19 16.20 16.21 16.21

10.3% 15.60 15.61 15.62 15.63 15.64 15.64 15.64

10.6% 15.04 15.07 15.10 15.12 15.14 15.16 15.18

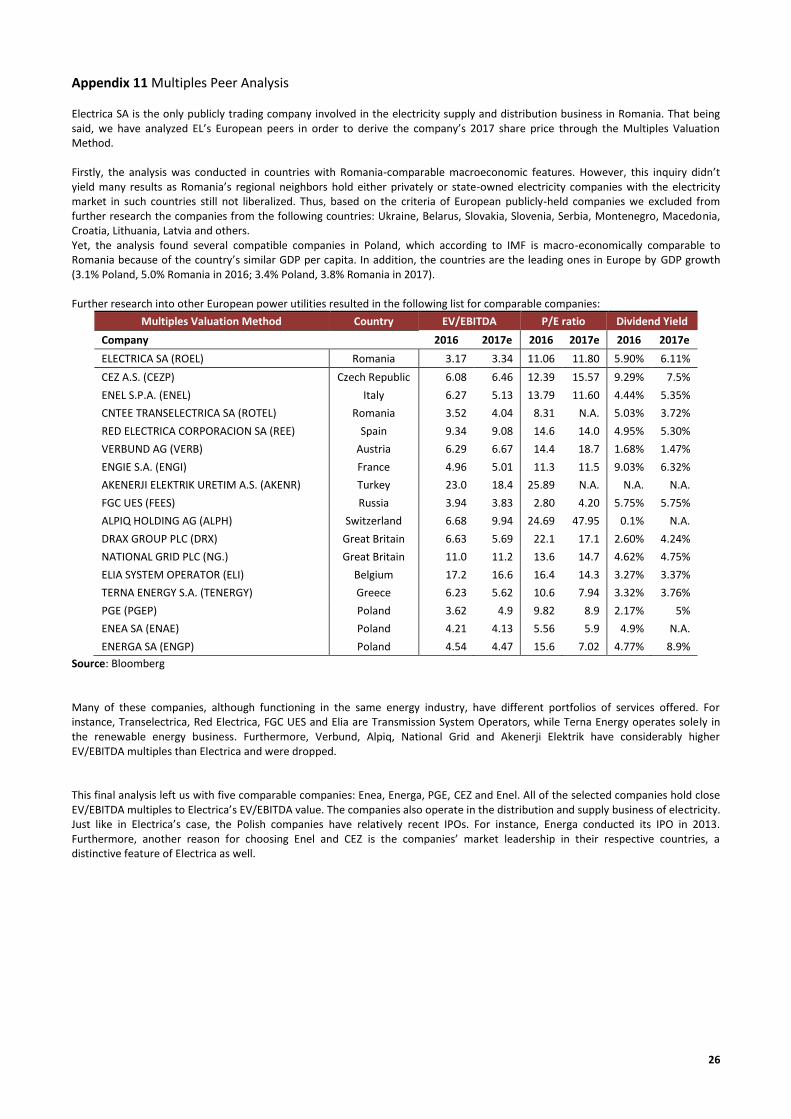

Relative Valuation – Multiples Approach

Multiples Valuation Method Country EV/EBITDA P/E ratio Dividend Yield

Company 2016 2017e 2016 2017e 2016 2017e

ELECTRICA SA (ROEL) Romania 3.17 3.34 11.06 11.80 5.90% 6.11%

PGE (PGEP) Poland 3.62 4.9 9.82 8.9 2.17% 5%

ENEA SA (ENAE) Poland 4.21 4.13 5.56 5.9 4.9% N.A.

ENERGA SA (ENGP) Poland 4.54 4.47 15.6 7.02 4.77% 8.9%

CEZ A.S. (CEZP) Czech Republic 6.08 6.46 12.39 15.57 9.29% 7.5%

ENEL S.P.A. (ENEL) Italy 6.27 5.13 13.79 11.60 4.44% 5.35%

Peer Median 4.54 4.90 12.39 8.90 4.77% 6.43%

Source: Bloomberg

As a crosscheck for the DCF Valuation method, we have also evaluated EL’s industry standing in comparison with its peers. The companies’ selection methodology yielded five appropriate companies for the Multiples Valuation. (Appendix 11) In order to arrive at an estimated equity or firm value, for each category of multiples a median was calculated. Statistically, the median represents a more appropriate measure than the mean because an average can be skewed by data from sample outliers. Consequently, we have derived a median of 4.90 for the 2017

EV/EBITDA multiple.

The forward-looking peer multiple of Enterprise Value to EBITDA was used for estimating EL’s price in 2017. The rationale for using this method is that it essentially eliminates the distorting effect of different capital structures, non-operating assets, and non-operating income statement items. Following this method we obtained a price per share of 16.69 RON for 2017. This result reinforced our bullish perspective on the stock, since currently the company’s shares are traded at 13.98 RON. The P/E ratio of EL at 11.8 for 2017 is far from its 8.9 industry median, while EL’s dividend yield for 2017 (6.11%) is slightly lower than the comparable companies’ median (6.43%). However, as EL has pledged to raise its dividend pay-out ratio to 85% this difference will likely be eliminated in the following years.

WACC Components

10yrs YTM RO Gov. bonds 4.00%

EL credit spread (AAA) 0.60%

Cost of debt 4.60%

Target D/E ratio 6.00%

Levered beta 0.76

Market risk premium 7.95%

Cost of equity, levered 10.05%

Debt-to-value 5.66%

Equity-to-value 94.34%

Marginal tax rate 16.00%

WACC 9.70%

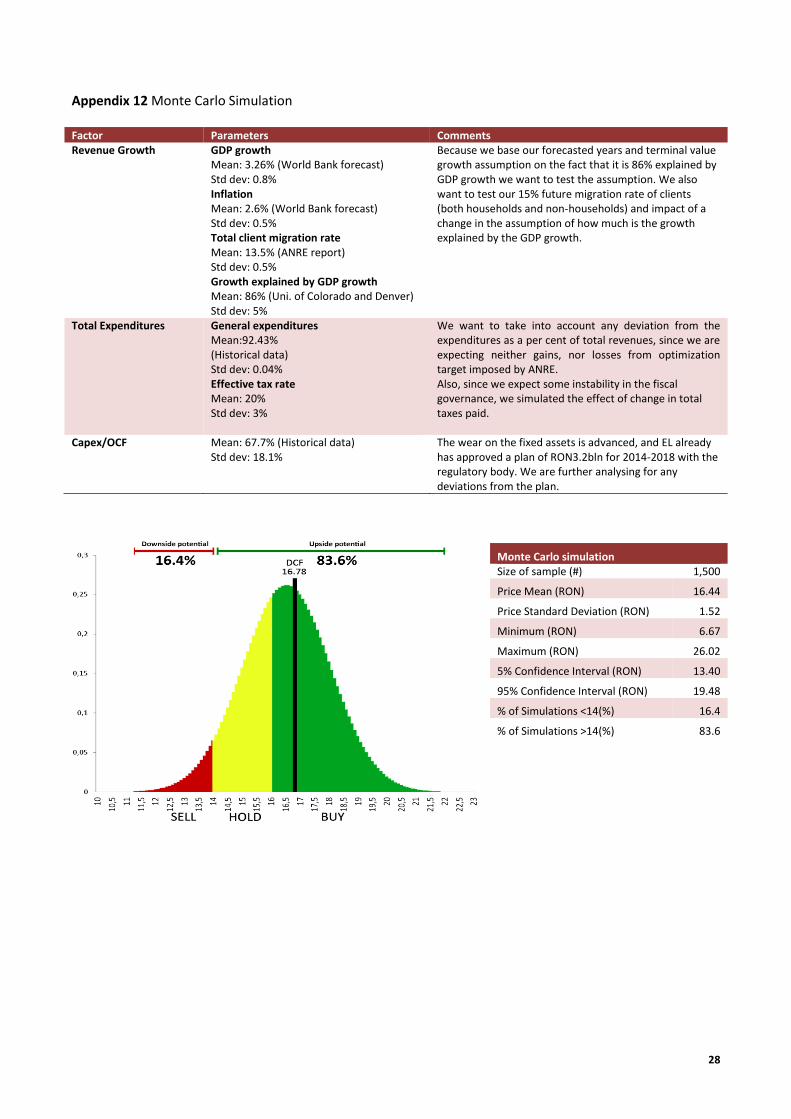

Monte Carlo simulation Size of sample (#) 15,000

Price Mean (RON) 16.44 Price Standard Deviation (RON) 1.52

Minimum (RON) 6.67

Maximum (RON) 26.02 5% Confidence Interval (RON) 13.40 95% Confidence Interval (RON) 19.48 % of Simulations <14(%) 16.4 % of Simulations >14(%) 83.6

Fig. 27 – Sensitivity analysis WACC/TV growth rate

Fig. 28 – Multiples analysis

Fig. 26 Monte Carlo Descriptive Statistics

Source: Team calculations

Fig. 29 Monte Carlo Descriptive Statistics

Source: External historical data (Appendix 12), Team calculations

Fig. 25 Weighted Average Cost of Capital

Source: Team calculations

9

FINANCIAL ANALYSIS

2013 2014 2015 2016e 2017f 2018f 2019f 2020f 2021f

Profitability

Revenues(mln) 5511.14 5220.24 5713.96 5972.14 6083.00 6244.44 6407.22 6589.28 6788.32

Gross Margin 31.06% 39.33% 37.35% 37.40% 36.68% 36.55% 36.54% 36.56% 36.95%

EBITDA margin 12.18% 16.65% 16.13% 16.65% 16.18% 16.00% 16.14% 16.33% 16.73%

Operating profit margin

6.27% 9.78% 9.95% 9.87% 9.57% 8.96% 8.94% 9.16% 9.77%

Net profit margin

5.73% 7.91% 8.44% 8.04% 7.76% 7.29% 7.24% 7.41% 7.84%

ROA - 4.98% 5.83% 5.76% 5.69% 5.44% 5.48% 5.68% 6.11%

Liquidity

Current ratio 3.01 3.01 2.73 2.66 2.42 2.23 2.17 2.33 2.40

Quick ratio 2.99 2.99 2.71 2.63 2.40 2.21 2.15 2.31 2.38

Cash ratio 0.48 1.30 0.63 0.87 0.56 0.51 0.55 0.77 0.87

Financial Leverage

D/E 30.68% 29.56% 30.25% 28.27% 27.59% 28.02% 28.32% 28.38% 27.74%

Interest coverage

9.85 22.06 32.74 48.69 48.08 71.56 71.16 73.25 54.70

Shareholder Ratios

EPS 1.45 0.88 1.07 1.11 1.09 1.05 1.07 1.12 1.22

Dividend Pay-out ratio

- 7.42% 82.44% 80.40% 85.00% 85.00% 85.00% 85.00% 85.00%

DPS - 0.06 0.72 0.86 0.94 0.92 0.89 0.91 0.96

Sound Financial Position For the historical period 2013-2015, EL revenues’ CAGR was 1.82%. Taking into account that EL has its activity in a regulated market, we expect a steady growth of revenues in the forecasted period (2016-2021), with an estimated CAGR of 2.6%. EL’s non-current assets are made up primarily of intangible assets related to concession agreements (83.17%), property plant and equipment (15.58%) and a small portion attributable to intangible assets (licenses and trademarks) based on our 2016 estimates. The Company’s major current asset item is deposits, treasury bills and government bonds, which accounts for a 44.87% share as of 2016, with cash and cash equivalents representing 31.51% of current assets.

Rebound on Margins Profitability margins will slightly decrease over the following period, as a result of significant and

necessary investments in the transmission lines. The RON 3.2bln are planned to decrease to a steadier rate from 2019 onwards, to about 8% of total revenues in 2021. The company’s investment plan for 2015 allocated money in the following manner: continuity of supply (35%), energy efficiency (30%), operating efficiency (11%), independent equipment (11%) others (13%). These are the core points that with renewed transmission lines would attain optimal activity. The slight decrease in 2017-2018 EBITDA margin, for example, would not critically affect the company’s bottom line. Furthermore, after a slowdown in 2018-2019 we expect profitability ratios to rebound thereafter, leading EL to a more profitable business.

Sustainable earnings with debt-free balance sheet Even though utility companies are conventionally high-debt carriers, Electrica, with a D/E ratio of 0.30 as of 2015, has lower indebtedness and is, thus, perceived more favourably by financial analysts and investors alike. We forecast that the company will continue to grow and finance its activity organically, by reinvesting its internally generated funds and/or using its overwhelming cash position. As such, EL is forecasted to maintain a relatively constant D/E ratio of 0.28 in the following years (2017-2021). The company can meet its debt obligations and has a high margin of safety. In addition, the interest-coverage ratio analysis shows that Electrica sustains earnings well above its interest payments and will not be affected by a possible financial distress.

ROE Decomposition 2014 2016e 2017f

Net profit margin 7.91% 8.04% 7.84%

Asset turnover 0.63 0.72 0.78

Asset/equity 1.30 1.29 1.28

ROE 6.48% 7.45% 7.83%

Fig. 31 Peers ROE/ROA Comparison

Fig. 32 ROE Decomposition

Source: Company data, team estimations

Fig. 33 DuPont Visualization

Source: Company data, team estimations

Source: Bloomberg

Fig. 30 ROE Decomposition

Source: Bloomberg

10

Dividends and Intrinsic Value Since it became a public company in 2014, Electrica has paid dividends twice: on 18

th of July 2016

(RON0.86) and on 15th

of July 2015 (RON0.72). In 2015 the market didn’t adjust accordingly to the company’s announcement of the dividend payment, the company’s shares decreasing only by RON0.64 of the distributed RON0.72, pointing to the idea that the company was perceived by investors as being undervalued. Yet, this was not the case in 2016, when EL’s share price dropped by exactly the amount of dividends paid (RON0.86), meaning that investors considered the share as being close to fair price. Being a well-established and mature company EL’s projected dividend aim is to maintain a high payout ratio of 85% of earnings in 2021.

INVESTMENT RISKS Regulatory risk (R1) Unforeseen Regulatory Changes Operating in a state-controlled monopoly, EL is exposed to risks of policy provisions by ANRE. Changes in regulations greatly affect the company’s financial performance. Negative recalculation of the RRR results in exponential profitability decline. RAB legislation changes affect the company’s cost of capital and balance sheet, and create uncertainty in the budget planning process. Unfavourable changes in RAB legislation would greatly hinder EL’s necessary investments in plant asset renewal and upgrade. The 2015 precedent

(Appendix 6) is cause for concern over lack of

communication between the two parties.

Estimated 30% of the invoice amount billed to the consumer is comprised of the Distribution Tariff which is adjusted annually based on realised costs and RAB investment. The tariff is set individually for each company and for each grid system (high, medium and low voltage). Legislation in the third regulatory period stipulates that the Distribution Tariff cannot increase more than 7% or decrease more than 10% annually. However, the level of adherence to this legislation is questionable with 2016 decreases of up to 16%. This year, the Distribution Tariff is still expected to decrease, but by a lower margin than in 2016. On average, EL’s Distribution Tariff will be decreased by 6,26%.

40

Regulatory risk (R2) Failure to meet Technical Efficiency Targets EL’s systems are inadvertently subject to active and reactive energy losses. Legislation accounts for these losses as costs in Regulated Revenue thereby preventing negative impact on profitability or margin cost risk for the consumer. ANRE employs standardized losses caps, offering incentives for efficient grid functionality by allowing companies under the cap to retain the difference as profit, and penalizing inefficient grid functionality by not accounting for losses over the cap, thereby decreasing profit.

Market risk (M1) Increased Competition in the Supply Segment due to Full Market Liberalisation Romania has adopted a multiple-step liberalisation in order to avoid energy price spikes with full liberalisation set to occur in January 2018. This event is expected to cause a shift to a more competitive electricity industry, which provides a risk of diminished market share for EL. We are confident however based on observations of emerged and future emerging competitors that EL has the positioning, infrastructure and negotiation leverage to minimize the above mentioned event’s impact.

Market risk (M2) Unfavourable market conditions Romania’s electricity demand is conditioned by universal and national macroeconomic factors outside the group’s control. Political instability, social unrest, world conflicts and potential energy crises have direct impact on the functionality and profitability of the energy sector and in turn, on EL. The GDP growth rate for the next three years is forecasted to be on average around the 3% mark.

Operational risk (O1) Service failure due to unforeseen events Fortuitous events such as natural calamities or man-made disasters pose a significant risk to the company’s asset base due to the hazardous and volatile nature of the product, the on-going availability of the service and the vast nature of infrastructure in terms of complexity and location diversity. Occurrence of such events would result in overall grid failures, service interruptions and unplanned repair and maintenance expenditures.

Operational risk (O2) Operating assets breakdown or malfunction A large portion of EL’s electricity infrastructure (approx. 80%) was built during the 1960’s National Electricity System program rendering them antiquated. The overall high level of wear on these assets possess the risk of breakdown and malfunction which would result in outages, losses and service unavailability diminishing consumer satisfaction and increasing maintenance CAPEX. The company has extensive infrastructure investment plans including Smart Grid transition and distribution automation systems such as SCADA and SAD in order to assure operational efficiency, reduce losses and improve grid flexibility. EL’s ability to successfully, timely and cost-efficiently execute these investment projects is a pertinent variable to the future of the company.

Company Nr. of

employees Productivity

(as per EBITDA)

Energa 8,545 0.06 Cez 25,826 0.11

Enea 14,957 0.03 Electrica 10,539 0.02

Enel 67,914 0.20 PGE 38,877 0.04

Fig. 35 Risk Analysis

We assign a BUY rating when the stock price is expected to deliver returns of 15% or more, over the next 12 months. The SELL rating is attributed to any decrease in share price, over the following 12 months. HOLD rating is given to any increase of less than 15%, over the following 12 months.

Fig. 34 Employee productivity

Source: Bloomberg

Source: Team assessment

RRR Evolution

2004 10% 2013 8.5% 2015

ap. 14 7.7%

Source: ANRE Report

Fig. 36 Regulated rate of return changes

11

APPENDICES

APPENDIX 1 Financial Statements A. Balance Sheet

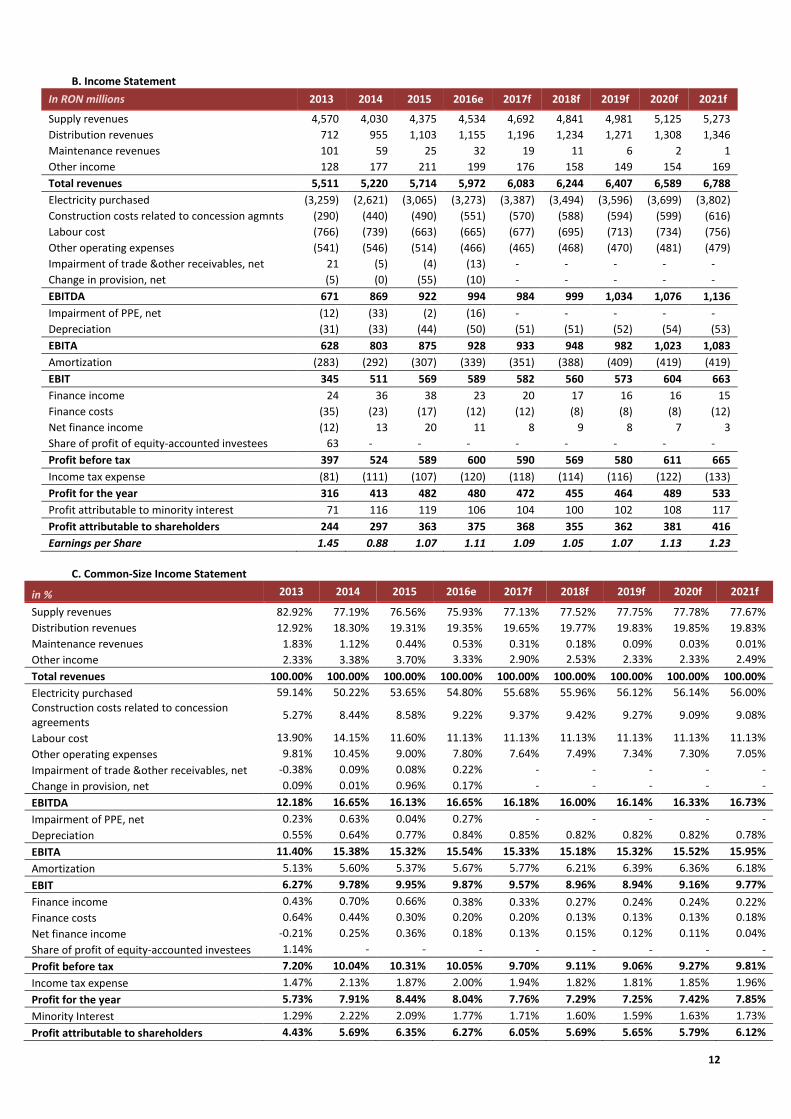

In RON millions 2013 2014 2015 2016e 2017f 2018f 2019f 2020f 2021f

Assets

Instangible asstes 3,345 3,510 3,715 4,014 4,441 4,683 4,793 4,711 4,752

Property, plant & equipment, net 876 805 779 735 730 749 769 725 747

Deffered tax assets 85 60 51 33 33 32 31 31 30

Other non-current assets 1 8 4 3 3 3 3 3 3

Accounts receivable 1,145 805 875 796 811 833 854 879 905

Cash & cash equivalents 651 1,630 893 1,142 740 725 807 1,150 1,265

Deposits, treasury bills and government bonds 0 1,221 1,988 1,493 1,521 1,374 1,281 1,186 1,086

Inventories 34 24 23 28 29 30 31 31 32

Prepayments 6 9 9 5 6 6 6 6 6

Green certificates 0 54 31 4 4 4 4 5 5

Income tax receivables 37 23 23 23 23 22 22 24 26

Assets held for distribution 2,243 0 0 0 0 0 0 0 0

Total assets 8,423 8,148 8,391 8,278 8,340 8,461 8,602 8,750 8,858

Equity and liabilities

Share capital 2,509 3,814 3,814 3,814 3,814 3,814 3,814 3,814 3,814

Retained Earnings 1,937 1,247 1,355 1396 1,484 1,562 1,662 1,779 1,896

Minority interests 764 804 829 842 842 842 842 842 842

Share Premium 0 103 103 103 103 103 103 103 103

Treasury shares reserve 0 (75) (75) (75) (75) (75) (75) (75) (75)

Other 1,235 396 417 374 374 374 374 374 374

Total equity 6,446 6,289 6,443 6,454 6,542 6,619 6,720 6,837 6,954

Liabilities

Financing for network construction related to concession agreements

272 251 222 233 238 244 250 257 265

Finance lease 1 0 0 0 0 0 0 0 0

Deferred tax liabilities 201 184 181 184 183 183 184 184 184

Employee benefits operating 152 147 135 85 87 89 91 94 97

Employee benefits nonoperating 213 220 194 162 165 169 173 178 184

Short-term debts 0 0 60 2 0 0 0 0 0

Bank overdrafts 80 48 66 175 115 118 121 110 57

Accounts payable 955 919 949 817 845 872 897 923 950

Deferred revenues 3 3 4 5 5 5 5 6 6

Provisions 85 73 128 149 149 149 149 149 149

Current income tax liability 15 14 11 12 12 12 12 12 12

Total liabilities 1,977 1,859 1,949 1,824 1,798 1,841 1,883 1,913 1,903

Total equity and liabilities 8,423 8,148 8,391 8,278 8,340 8,461 8,602 8,750 8,858

12

B. Income Statement

In RON millions 2013 2014 2015 2016e 2017f 2018f 2019f 2020f 2021f

Supply revenues 4,570 4,030 4,375 4,534 4,692 4,841 4,981 5,125 5,273

Distribution revenues 712 955 1,103 1,155 1,196 1,234 1,271 1,308 1,346

Maintenance revenues 101 59 25 32 19 11 6 2 1

Other income 128 177 211 199 176 158 149 154 169

Total revenues 5,511 5,220 5,714 5,972 6,083 6,244 6,407 6,589 6,788

Electricity purchased (3,259) (2,621) (3,065) (3,273) (3,387) (3,494) (3,596) (3,699) (3,802)

Construction costs related to concession agmnts (290) (440) (490) (551) (570) (588) (594) (599) (616)

Labour cost (766) (739) (663) (665) (677) (695) (713) (734) (756)

Other operating expenses (541) (546) (514) (466) (465) (468) (470) (481) (479)

Impairment of trade &other receivables, net 21 (5) (4) (13) - - - - -

Change in provision, net (5) (0) (55) (10) - - - - -

EBITDA 671 869 922 994 984 999 1,034 1,076 1,136

Impairment of PPE, net (12) (33) (2) (16) - - - - -

Depreciation (31) (33) (44) (50) (51) (51) (52) (54) (53)

EBITA 628 803 875 928 933 948 982 1,023 1,083

Amortization (283) (292) (307) (339) (351) (388) (409) (419) (419)

EBIT 345 511 569 589 582 560 573 604 663

Finance income 24 36 38 23 20 17 16 16 15

Finance costs (35) (23) (17) (12) (12) (8) (8) (8) (12)

Net finance income (12) 13 20 11 8 9 8 7 3

Share of profit of equity-accounted investees 63 - - - - - - - -

Profit before tax 397 524 589 600 590 569 580 611 665

Income tax expense (81) (111) (107) (120) (118) (114) (116) (122) (133)

Profit for the year 316 413 482 480 472 455 464 489 533

Profit attributable to minority interest 71 116 119 106 104 100 102 108 117

Profit attributable to shareholders 244 297 363 375 368 355 362 381 416

Earnings per Share 1.45 0.88 1.07 1.11 1.09 1.05 1.07 1.13 1.23

C. Common-Size Income Statement

in % 2013 2014 2015 2016e 2017f 2018f 2019f 2020f 2021f

Supply revenues 82.92% 77.19% 76.56% 75.93% 77.13% 77.52% 77.75% 77.78% 77.67%

Distribution revenues 12.92% 18.30% 19.31% 19.35% 19.65% 19.77% 19.83% 19.85% 19.83%

Maintenance revenues 1.83% 1.12% 0.44% 0.53% 0.31% 0.18% 0.09% 0.03% 0.01%

Other income 2.33% 3.38% 3.70% 3.33% 2.90% 2.53% 2.33% 2.33% 2.49%

Total revenues 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Electricity purchased 59.14% 50.22% 53.65% 54.80% 55.68% 55.96% 56.12% 56.14% 56.00%

Construction costs related to concession agreements

5.27% 8.44% 8.58% 9.22% 9.37% 9.42% 9.27% 9.09% 9.08%

Labour cost 13.90% 14.15% 11.60% 11.13% 11.13% 11.13% 11.13% 11.13% 11.13%

Other operating expenses 9.81% 10.45% 9.00% 7.80% 7.64% 7.49% 7.34% 7.30% 7.05%

Impairment of trade &other receivables, net -0.38% 0.09% 0.08% 0.22% - - - - -

Change in provision, net 0.09% 0.01% 0.96% 0.17% - - - - -

EBITDA 12.18% 16.65% 16.13% 16.65% 16.18% 16.00% 16.14% 16.33% 16.73%

Impairment of PPE, net 0.23% 0.63% 0.04% 0.27% - - - - -

Depreciation 0.55% 0.64% 0.77% 0.84% 0.85% 0.82% 0.82% 0.82% 0.78%

EBITA 11.40% 15.38% 15.32% 15.54% 15.33% 15.18% 15.32% 15.52% 15.95%

Amortization 5.13% 5.60% 5.37% 5.67% 5.77% 6.21% 6.39% 6.36% 6.18%

EBIT 6.27% 9.78% 9.95% 9.87% 9.57% 8.96% 8.94% 9.16% 9.77%

Finance income 0.43% 0.70% 0.66% 0.38% 0.33% 0.27% 0.24% 0.24% 0.22%

Finance costs 0.64% 0.44% 0.30% 0.20% 0.20% 0.13% 0.13% 0.13% 0.18%

Net finance income -0.21% 0.25% 0.36% 0.18% 0.13% 0.15% 0.12% 0.11% 0.04%

Share of profit of equity-accounted investees 1.14% - - - - - - - -

Profit before tax 7.20% 10.04% 10.31% 10.05% 9.70% 9.11% 9.06% 9.27% 9.81%

Income tax expense 1.47% 2.13% 1.87% 2.00% 1.94% 1.82% 1.81% 1.85% 1.96%

Profit for the year 5.73% 7.91% 8.44% 8.04% 7.76% 7.29% 7.25% 7.42% 7.85%

Minority Interest 1.29% 2.22% 2.09% 1.77% 1.71% 1.60% 1.59% 1.63% 1.73%

Profit attributable to shareholders 4.43% 5.69% 6.35% 6.27% 6.05% 5.69% 5.65% 5.79% 6.12%

13

APPENDIX 2 Company and Ownership Structure

Shareholder (22/11/16) Percent of share capital Romanian State 48.78% EBRD 8.66% BNY Mellon DRS-LSE 5.16% Grantham Mayo van Otterloo 2.66% Norges Bank 1.63% NN Group NV 1.27% Blackrock 0.93% Total 100%

Source: Bloomberg

Geographic Percent of shares Romania 67.55% Britain 13.08% United States 11.67% Norway 2.22% Luxembourg 2.14% Ireland 1.07% Other 1.68% Source: Bloomberg

14

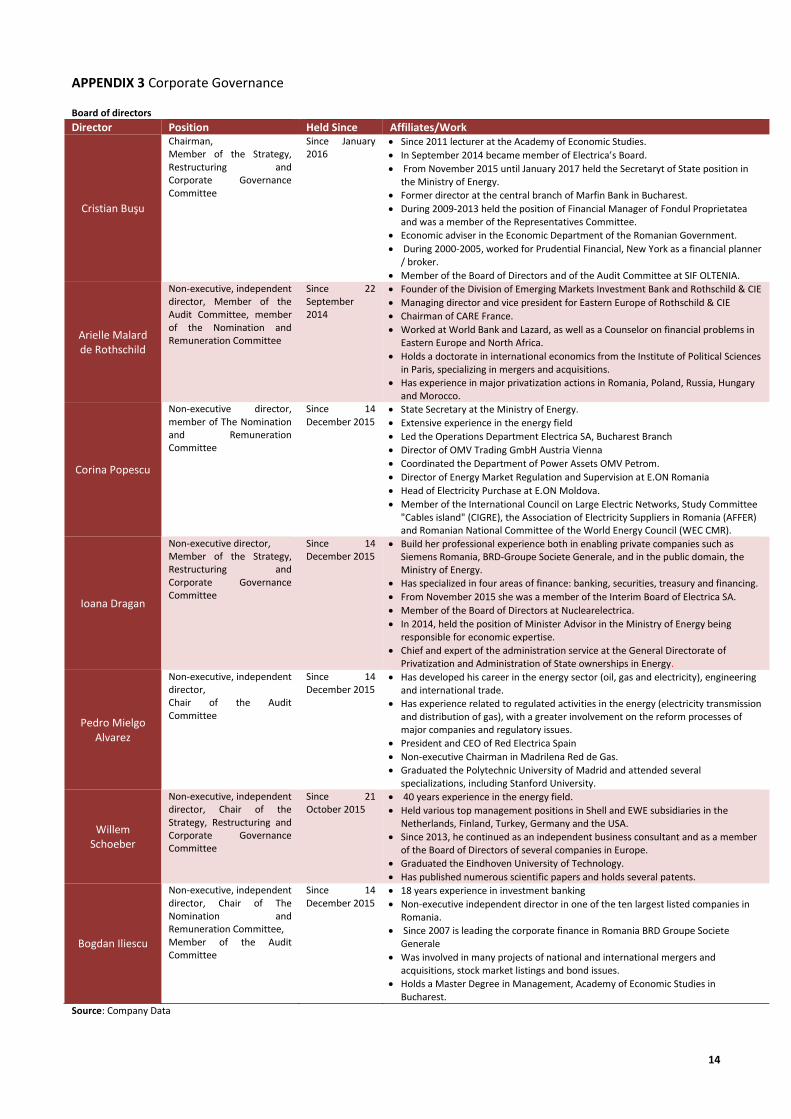

APPENDIX 3 Corporate Governance Board of directors

Director Position Held Since Affiliates/Work

Cristian Buşu

Chairman, Member of the Strategy, Restructuring and Corporate Governance Committee

Since January 2016

Since 2011 lecturer at the Academy of Economic Studies.

In September 2014 became member of Electrica’s Board.

From November 2015 until January 2017 held the Secretaryt of State position in the Ministry of Energy.

Former director at the central branch of Marfin Bank in Bucharest.

During 2009-2013 held the position of Financial Manager of Fondul Proprietatea and was a member of the Representatives Committee.

Economic adviser in the Economic Department of the Romanian Government.

During 2000-2005, worked for Prudential Financial, New York as a financial planner / broker.

Member of the Board of Directors and of the Audit Committee at SIF OLTENIA.

Arielle Malard de Rothschild

Non-executive, independent director, Member of the Audit Committee, member of the Nomination and Remuneration Committee

Since 22 September 2014

Founder of the Division of Emerging Markets Investment Bank and Rothschild & CIE

Managing director and vice president for Eastern Europe of Rothschild & CIE

Chairman of CARE France.

Worked at World Bank and Lazard, as well as a Counselor on financial problems in Eastern Europe and North Africa.

Holds a doctorate in international economics from the Institute of Political Sciences in Paris, specializing in mergers and acquisitions.

Has experience in major privatization actions in Romania, Poland, Russia, Hungary and Morocco.

Corina Popescu

Non-executive director, member of The Nomination and Remuneration Committee

Since 14 December 2015

State Secretary at the Ministry of Energy.

Extensive experience in the energy field

Led the Operations Department Electrica SA, Bucharest Branch

Director of OMV Trading GmbH Austria Vienna

Coordinated the Department of Power Assets OMV Petrom.

Director of Energy Market Regulation and Supervision at E.ON Romania

Head of Electricity Purchase at E.ON Moldova.

Member of the International Council on Large Electric Networks, Study Committee "Cables island" (CIGRE), the Association of Electricity Suppliers in Romania (AFFER) and Romanian National Committee of the World Energy Council (WEC CMR).

Ioana Dragan

Non-executive director, Member of the Strategy, Restructuring and Corporate Governance Committee

Since 14 December 2015

Build her professional experience both in enabling private companies such as Siemens Romania, BRD-Groupe Societe Generale, and in the public domain, the Ministry of Energy.

Has specialized in four areas of finance: banking, securities, treasury and financing.

From November 2015 she was a member of the Interim Board of Electrica SA.

Member of the Board of Directors at Nuclearelectrica.

In 2014, held the position of Minister Advisor in the Ministry of Energy being responsible for economic expertise.

Chief and expert of the administration service at the General Directorate of Privatization and Administration of State ownerships in Energy.

Pedro Mielgo Alvarez

Non-executive, independent director, Chair of the Audit Committee

Since 14 December 2015

Has developed his career in the energy sector (oil, gas and electricity), engineering and international trade.

Has experience related to regulated activities in the energy (electricity transmission and distribution of gas), with a greater involvement on the reform processes of major companies and regulatory issues.

President and CEO of Red Electrica Spain

Non-executive Chairman in Madrilena Red de Gas.

Graduated the Polytechnic University of Madrid and attended several specializations, including Stanford University.

Willem Schoeber

Non-executive, independent director, Chair of the Strategy, Restructuring and Corporate Governance Committee

Since 21 October 2015

40 years experience in the energy field.

Held various top management positions in Shell and EWE subsidiaries in the Netherlands, Finland, Turkey, Germany and the USA.

Since 2013, he continued as an independent business consultant and as a member of the Board of Directors of several companies in Europe.

Graduated the Eindhoven University of Technology.

Has published numerous scientific papers and holds several patents.

Bogdan Iliescu

Non-executive, independent director, Chair of The Nomination and Remuneration Committee, Member of the Audit Committee

Since 14 December 2015

18 years experience in investment banking

Non-executive independent director in one of the ten largest listed companies in Romania.

Since 2007 is leading the corporate finance in Romania BRD Groupe Societe Generale

Was involved in many projects of national and international mergers and acquisitions, stock market listings and bond issues.

Holds a Master Degree in Management, Academy of Economic Studies in Bucharest.

Source: Company Data

15

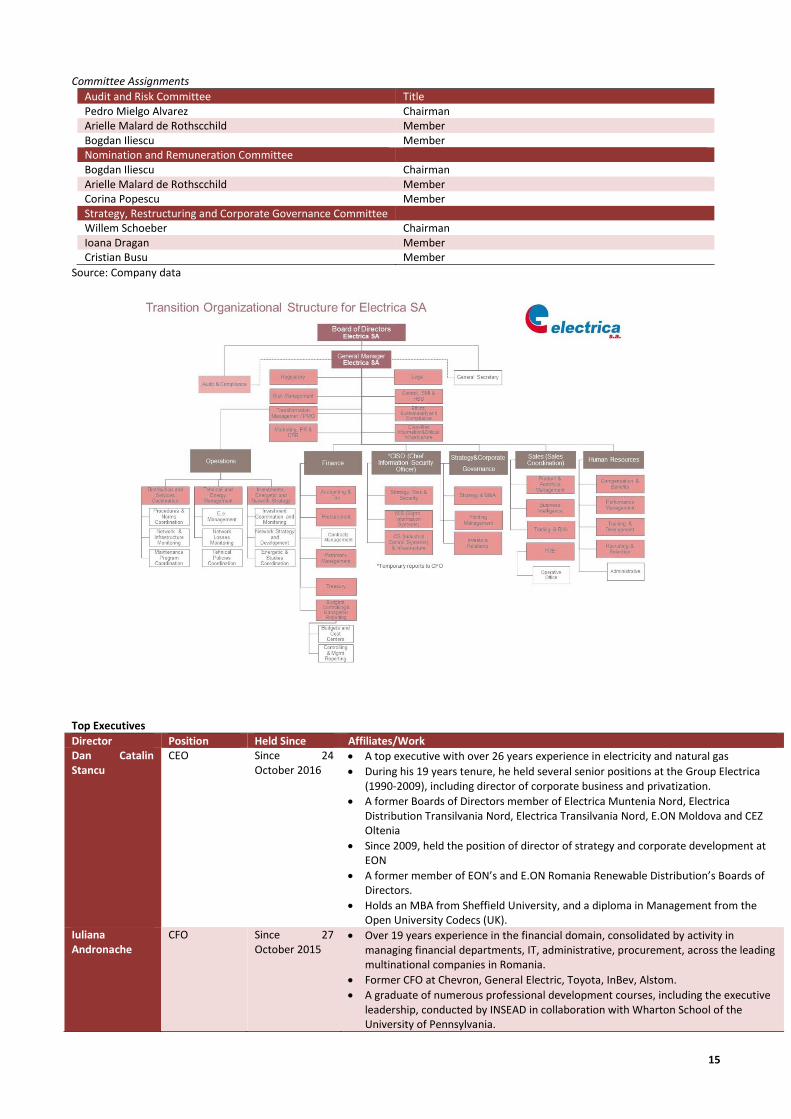

Committee Assignments

Audit and Risk Committee Title Pedro Mielgo Alvarez Chairman Arielle Malard de Rothscchild Member Bogdan Iliescu Member Nomination and Remuneration Committee Bogdan Iliescu Chairman Arielle Malard de Rothscchild Member Corina Popescu Member Strategy, Restructuring and Corporate Governance Committee Willem Schoeber Chairman Ioana Dragan Member Cristian Busu Member

Source: Company data

Top Executives

Director Position Held Since Affiliates/Work Dan Catalin Stancu

CEO Since 24 October 2016

A top executive with over 26 years experience in electricity and natural gas

During his 19 years tenure, he held several senior positions at the Group Electrica (1990-2009), including director of corporate business and privatization.

A former Boards of Directors member of Electrica Muntenia Nord, Electrica Distribution Transilvania Nord, Electrica Transilvania Nord, E.ON Moldova and CEZ Oltenia

Since 2009, held the position of director of strategy and corporate development at EON

A former member of EON’s and E.ON Romania Renewable Distribution’s Boards of Directors.

Holds an MBA from Sheffield University, and a diploma in Management from the Open University Codecs (UK).

Iuliana Andronache

CFO Since 27 October 2015

Over 19 years experience in the financial domain, consolidated by activity in managing financial departments, IT, administrative, procurement, across the leading multinational companies in Romania.

Former CFO at Chevron, General Electric, Toyota, InBev, Alstom.

A graduate of numerous professional development courses, including the executive leadership, conducted by INSEAD in collaboration with Wharton School of the University of Pennsylvania.

16

Alexandra Borislavschi

Director of Strategy and Corporate Governance

Since 4 August, 2015

In 2013 was a director of the Economic Department and Business Development

In February 2014 served as Director of Corporate Governance and Corporate Finance.

The most important project she managed was Electrica’s Initial Public Offer (IPO) of 105% of the share capital during the period October 2013 - July 2014.

Worked at BRD-Groupe Societe Generale from 2003 to 2013.

Project Coordinator in the Investment Banking department at BRD-Groupe Societe Generale.

Livioara Sujdea Distribution CEO

Since 1 February, 2017

Over 20 years experience in the energy market

Occupied various senior management positions including deputy General Director and Member of the Board of Directors at E.ON Moldova Distribution, E.ON Gas Distribution, Distribution E.ON Romania, Director Operation and Deputy General Director and member of the Board of Directors at E.ON Energie.

Holds an Executive MBA with specialization in General Management at the University of Sheffield U.K. and a Diploma in Strategic Management and Leadership from the Chartered Management Institute London, U.K.

Source: Company data

APPENDIX 4 Supply Chain

17

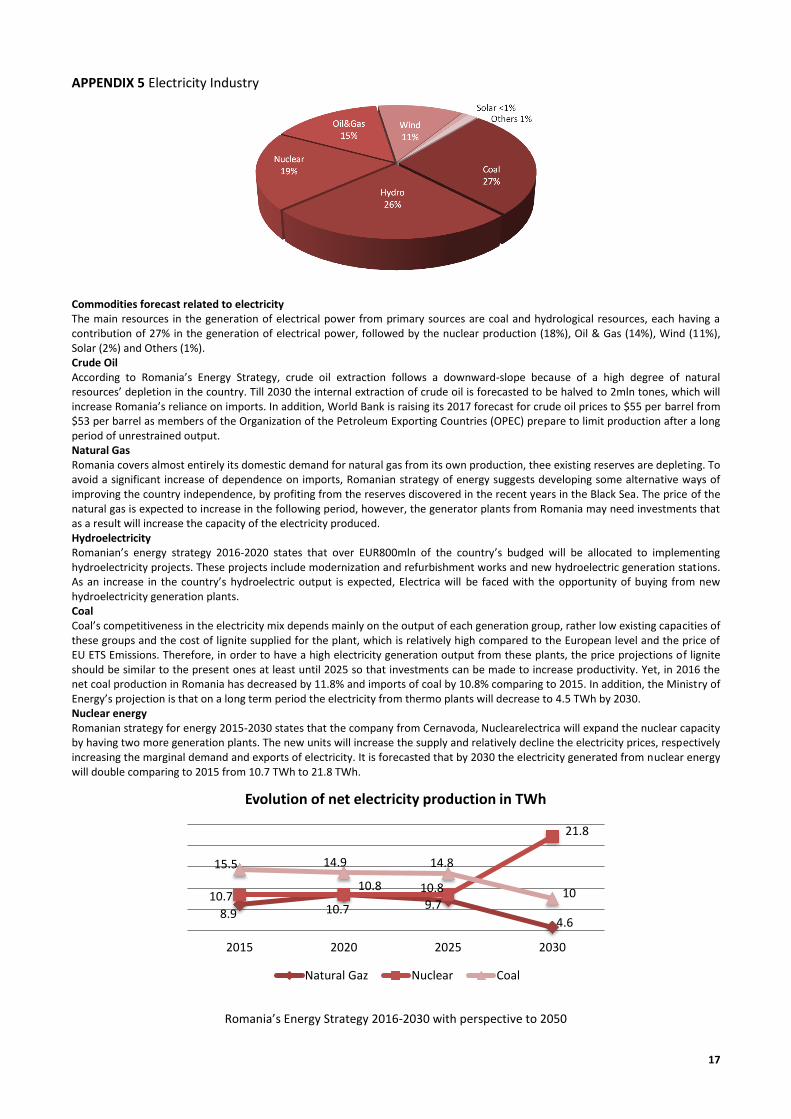

APPENDIX 5 Electricity Industry

Commodities forecast related to electricity The main resources in the generation of electrical power from primary sources are coal and hydrological resources, each having a contribution of 27% in the generation of electrical power, followed by the nuclear production (18%), Oil & Gas (14%), Wind (11%), Solar (2%) and Others (1%). Crude Oil According to Romania’s Energy Strategy, crude oil extraction follows a downward-slope because of a high degree of natural resources’ depletion in the country. Till 2030 the internal extraction of crude oil is forecasted to be halved to 2mln tones, which will increase Romania’s reliance on imports. In addition, World Bank is raising its 2017 forecast for crude oil prices to $55 per barrel from $53 per barrel as members of the Organization of the Petroleum Exporting Countries (OPEC) prepare to limit production after a long period of unrestrained output. Natural Gas Romania covers almost entirely its domestic demand for natural gas from its own production, thee existing reserves are depleting. To avoid a significant increase of dependence on imports, Romanian strategy of energy suggests developing some alternative ways of improving the country independence, by profiting from the reserves discovered in the recent years in the Black Sea. The price of the natural gas is expected to increase in the following period, however, the generator plants from Romania may need investments that as a result will increase the capacity of the electricity produced. Hydroelectricity Romanian’s energy strategy 2016-2020 states that over EUR800mln of the country’s budged will be allocated to implementing hydroelectricity projects. These projects include modernization and refurbishment works and new hydroelectric generation stations. As an increase in the country’s hydroelectric output is expected, Electrica will be faced with the opportunity of buying from new hydroelectricity generation plants. Coal Coal’s competitiveness in the electricity mix depends mainly on the output of each generation group, rather low existing capacities of these groups and the cost of lignite supplied for the plant, which is relatively high compared to the European level and the price of EU ETS Emissions. Therefore, in order to have a high electricity generation output from these plants, the price projections of lignite should be similar to the present ones at least until 2025 so that investments can be made to increase productivity. Yet, in 2016 the net coal production in Romania has decreased by 11.8% and imports of coal by 10.8% comparing to 2015. In addition, the Ministry of Energy’s projection is that on a long term period the electricity from thermo plants will decrease to 4.5 TWh by 2030. Nuclear energy Romanian strategy for energy 2015-2030 states that the company from Cernavoda, Nuclearelectrica will expand the nuclear capacity by having two more generation plants. The new units will increase the supply and relatively decline the electricity prices, respectively increasing the marginal demand and exports of electricity. It is forecasted that by 2030 the electricity generated from nuclear energy will double comparing to 2015 from 10.7 TWh to 21.8 TWh.

Romania’s Energy Strategy 2016-2030 with perspective to 2050

8.9 10.7 9.7

4.6

10.7 10.8 10.8

21.8

15.5 14.9 14.8

10

2015 2020 2025 2030

Evolution of net electricity production in TWh

Natural Gaz Nuclear Coal

18

APPENDIX 6 Regulation The Electricity Distribution Sector in Romania is a government-regulated monopoly based on concession agreements with a 49-year old duration with a possible extension of 24.5 years at contract expiration. Electrica’s current contract expiration year is 2054. In order to prevent monopolistic practices, distribution is regulated through a Tariff Basket Cap based on a Regulated Asset Base. Per ANRE methodology, a company’s annual allowed revenue is calculated employing the following formula:

𝑂𝑃𝐸𝑋 + 𝑁𝐿 + 𝑊𝐶 + 𝐷𝐸𝑃 + 𝑅𝑒𝑡. 𝑅𝐴𝐵 − 𝑅𝐸𝑅 = 𝐴𝑙𝑙𝑜𝑤𝑒𝑑 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 OPEX= Operating expenditures NL= Cost of Network Losses WC= Working Capital DEP= Depreciation Ret. RAB= Return on RAB RER= Reactive Electricity Romania employs a regulated rate-of-return on RAB, with constant rebasing to avoid imbalances. An over based RRR results in financial pressure on the consumer while an under based RRR results in financial pressure on the company due to potential difficulties in securing capital. A proficient regulated rate of return guarantees an attractive return on investment while protecting consumers from monopolistic price gauging. The regulated rate of return is set employing the following formula:

𝑅𝑅𝑅 = 𝑊𝐴𝐶𝐶 ∙𝐸

1 − 𝑇+ 𝐶𝐷 ∙ 𝐷

RRR= Rate of Regulated Return WACC= Weighted Average Cost of Capital E= the weight of equity in total capital T= Tax rate CD= Cost of debt D= the weight of debt in total capital The Distribution Tariff is the fee charged to the final consumer for the transportation of electric energy from the supplier to the aforementioned consumer. The Tariff is regulated and adjusted individually for each distributer and for each type of distribution grid

𝐷𝑖𝑠𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛 𝑇𝑎𝑟𝑖𝑓𝑓 =𝐴𝑙𝑙𝑜𝑤𝑒𝑑 𝑅𝑒𝑣𝑒𝑛𝑢𝑒

𝑃𝑟𝑜𝑗𝑒𝑐𝑡𝑒𝑑 𝑉𝑜𝑙𝑢𝑚𝑒𝑠

Analysing aforementioned information entitles us to identify a couple of value maximizing drivers and build a more comprehensive profit model:

𝑅𝑅𝑅 ∙ 𝑁𝑒𝑤 𝑅𝐴𝐵 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡𝑠 + 𝑂𝑃𝐸𝑋 ∙ (𝑅𝑒𝑎𝑙𝑖𝑠𝑒𝑑 𝑂𝑃𝐸𝑋 𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡 − 𝑇𝑎𝑟𝑔𝑒𝑡 𝑂𝑃𝐸𝑋 𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡 + 𝐶𝑜𝑠𝑡 𝑜𝑓 𝑁𝑒𝑡𝑤𝑜𝑟𝑘 𝐿𝑜𝑠𝑠𝑒𝑠 ∙ (𝑅𝑒𝑎𝑙𝑖𝑠𝑒𝑑 𝑁𝑒𝑡𝑤𝑜𝑟𝑘 𝐿𝑜𝑠𝑠𝑒𝑠 − 𝑇𝑎𝑟𝑔𝑒𝑡 𝑁𝑒𝑡𝑤𝑜𝑟𝑘 𝐿𝑜𝑠𝑠𝑒𝑠)

A Somewhat Dysfunctional Marriage Transparency, negotiation and trust are crucial in order to establish a good level of communication in the relationship between the regulator and the regulated party. Precedent conflicts exist which seem to question the previously mentioned necessary features of the relationship. ANRE’s directive 146/2014 for the third regulatory period stipulated a negative recalculation of the RRR from 8,52% to 7,45%. This 107 basis point proposed drop sparked large amounts of negative backlash from Electrica and its investors, with the parties filling legal injunctions against the order. In a statement from minority-interest holder “Fondul Proprietatea”, the negative recalculation would drastically affect company profitability, forecasting an approximate 12,5% decline from the previous period. ANRE defended its directive as the result of huge network losses of approximately EUR1bln, despite increases in the distribution tariff by approximately 13% in the second regulatory period. The parties reached a compromise after long sessions of negotiation with the RRR currently residing at 7,7%.

19

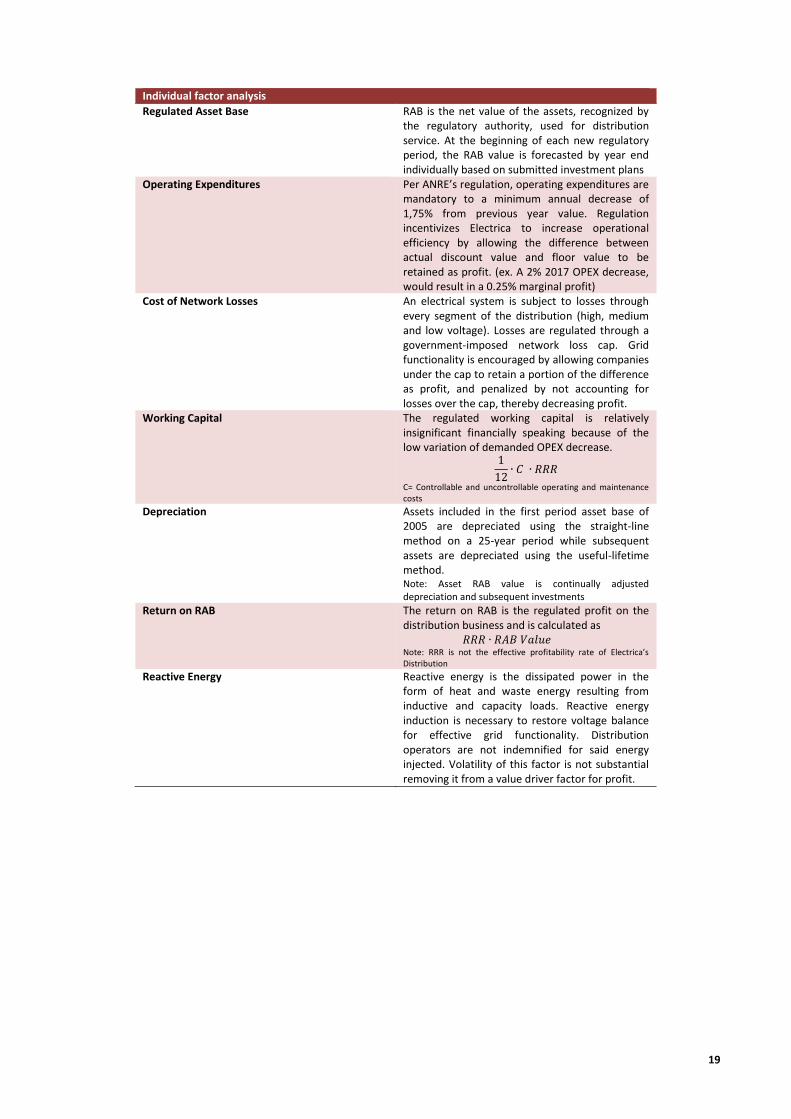

Individual factor analysis

Regulated Asset Base RAB is the net value of the assets, recognized by the regulatory authority, used for distribution service. At the beginning of each new regulatory period, the RAB value is forecasted by year end individually based on submitted investment plans

Operating Expenditures Per ANRE’s regulation, operating expenditures are mandatory to a minimum annual decrease of 1,75% from previous year value. Regulation incentivizes Electrica to increase operational efficiency by allowing the difference between actual discount value and floor value to be retained as profit. (ex. A 2% 2017 OPEX decrease, would result in a 0.25% marginal profit)

Cost of Network Losses

An electrical system is subject to losses through every segment of the distribution (high, medium and low voltage). Losses are regulated through a government-imposed network loss cap. Grid functionality is encouraged by allowing companies under the cap to retain a portion of the difference as profit, and penalized by not accounting for losses over the cap, thereby decreasing profit.

Working Capital The regulated working capital is relatively insignificant financially speaking because of the low variation of demanded OPEX decrease.

1

12∙ 𝐶 ∙ 𝑅𝑅𝑅

C= Controllable and uncontrollable operating and maintenance costs

Depreciation Assets included in the first period asset base of 2005 are depreciated using the straight-line method on a 25-year period while subsequent assets are depreciated using the useful-lifetime method. Note: Asset RAB value is continually adjusted depreciation and subsequent investments

Return on RAB The return on RAB is the regulated profit on the distribution business and is calculated as 𝑅𝑅𝑅 ∙ 𝑅𝐴𝐵 𝑉𝑎𝑙𝑢𝑒 Note: RRR is not the effective profitability rate of Electrica’s Distribution

Reactive Energy Reactive energy is the dissipated power in the form of heat and waste energy resulting from inductive and capacity loads. Reactive energy induction is necessary to restore voltage balance for effective grid functionality. Distribution operators are not indemnified for said energy injected. Volatility of this factor is not substantial removing it from a value driver factor for profit.

20

APPENDIX 7 Market Data

Distribution System Operator Concentration in EU Countries

Source: EU-Electric

We can see that in the majority of EU countries the market of distribution is mostly sparse. This data reinforces our choice regarding the peers, with respect to countries they have activity in.

Market Tariff Liberalization Process

Source: ANRE

21

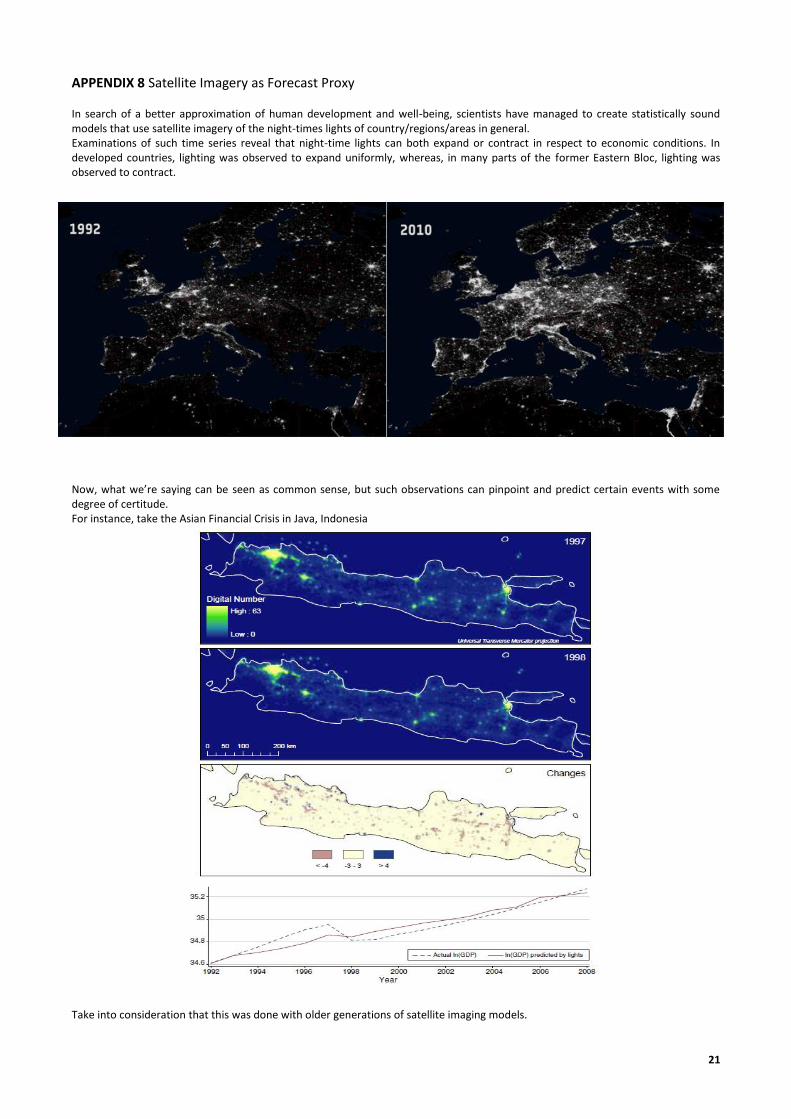

APPENDIX 8 Satellite Imagery as Forecast Proxy In search of a better approximation of human development and well-being, scientists have managed to create statistically sound models that use satellite imagery of the night-times lights of country/regions/areas in general. Examinations of such time series reveal that night-time lights can both expand or contract in respect to economic conditions. In developed countries, lighting was observed to expand uniformly, whereas, in many parts of the former Eastern Bloc, lighting was observed to contract.

Now, what we’re saying can be seen as common sense, but such observations can pinpoint and predict certain events with some degree of certitude. For instance, take the Asian Financial Crisis in Java, Indonesia

Take into consideration that this was done with older generations of satellite imaging models.

22

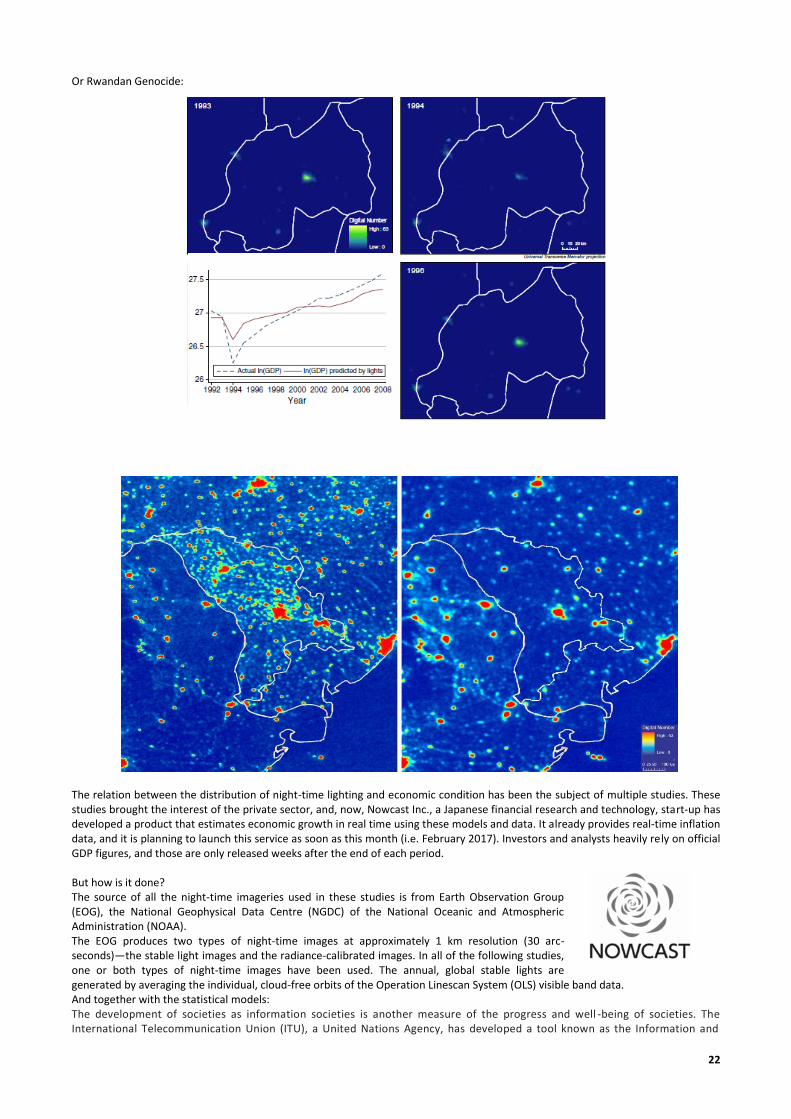

Or Rwandan Genocide:

The relation between the distribution of night-time lighting and economic condition has been the subject of multiple studies. These studies brought the interest of the private sector, and, now, Nowcast Inc., a Japanese financial research and technology, start-up has developed a product that estimates economic growth in real time using these models and data. It already provides real-time inflation data, and it is planning to launch this service as soon as this month (i.e. February 2017). Investors and analysts heavily rely on official GDP figures, and those are only released weeks after the end of each period. But how is it done? The source of all the night-time imageries used in these studies is from Earth Observation Group (EOG), the National Geophysical Data Centre (NGDC) of the National Oceanic and Atmospheric Administration (NOAA). The EOG produces two types of night-time images at approximately 1 km resolution (30 arc-seconds)—the stable light images and the radiance-calibrated images. In all of the following studies, one or both types of night-time images have been used. The annual, global stable lights are generated by averaging the individual, cloud-free orbits of the Operation Linescan System (OLS) visible band data. And together with the statistical models: The development of societies as information societies is another measure of the progress and well -being of societies. The International Telecommunication Union (ITU), a United Nations Agency, has developed a tool known as the Information and

23

Communication Technology Development Index (IDI) to measure the development of countries as information societie s. The IDI is a composite index made up of 11 indicators covering Information and Communication Technology (ICT) use, access, and skills . Most of the indicators included in the IDI were found to have a close relationship with GDP per capita.

And to make it even clearer that energy production and delivery has a close relationship; here we have a regression of Night light development index (NLDI) and energy consumption per capita:

Development in a picture

24

APPENDIX 9 Default Risk In addition to assessing a company’s default probability within one year Bloomberg Default Risk comes up with data on a synthetically created Credit Default Swap (CDS). This financial instrument for protection against default is based on the company’s equity and debt position. Furthermore, Bloomberg assesses Electrica’s synthetic CDS with a 5-year maturity trading at 76 basis points (bps), while the same synthetically modelled CDS instrument for Romania is assessed to be trading at 111 bps. Hypothetically, one would need to pay more (111bps) for protection against Romania’s default since the risk of this event happening is modelled to be greater than the risk of Electrica’s default (64bps). In essence, this would mean that Electrica is a safer investment than the sovereign country. Even more than that, Electrica significantly outperforms its national and international peers in terms of credit default on both the possibility of defaulting within one year and the synthetically modelled 5-years CDS as exemplified by the following table:

Company Bloomberg 1-Year Default Risk Rating

S&P/Fitch rating equivalent

Interpretation Default

probability (in a year)

5-Years Synthetic CDS Model

trading at:

Electrica IG3 AA High Credit Quality 0.0064% 76 bps

Transelectrica IG4 AA- High Credit Quality 0.0249% 88 bps

Nuclearelectrica IG6 A Medium-high grade with

low credit Risk 0.0517% -

PGE IG8 BBB+ Moderate Credit Risk 0.1027% 152 bps

Energa IG9 BBB Moderate Credit Risk 0.2249% 183 bps

Enel SpA IG8 BBB+ Moderate Credit Risk 0.1104% 74 bps

Enea IG9 BBB Moderate Credit Risk 0.2130% 181 bps

CEZ a.s. IG7 A- Medium-high grade with

low credit Risk 0.0772% 142 bps

E.On (Belgium) IG10 BBB- Moderate Credit Risk 0.3730% -

Source: Bloomberg

Appendix 10 DCF Model

Weighted average cost of capital

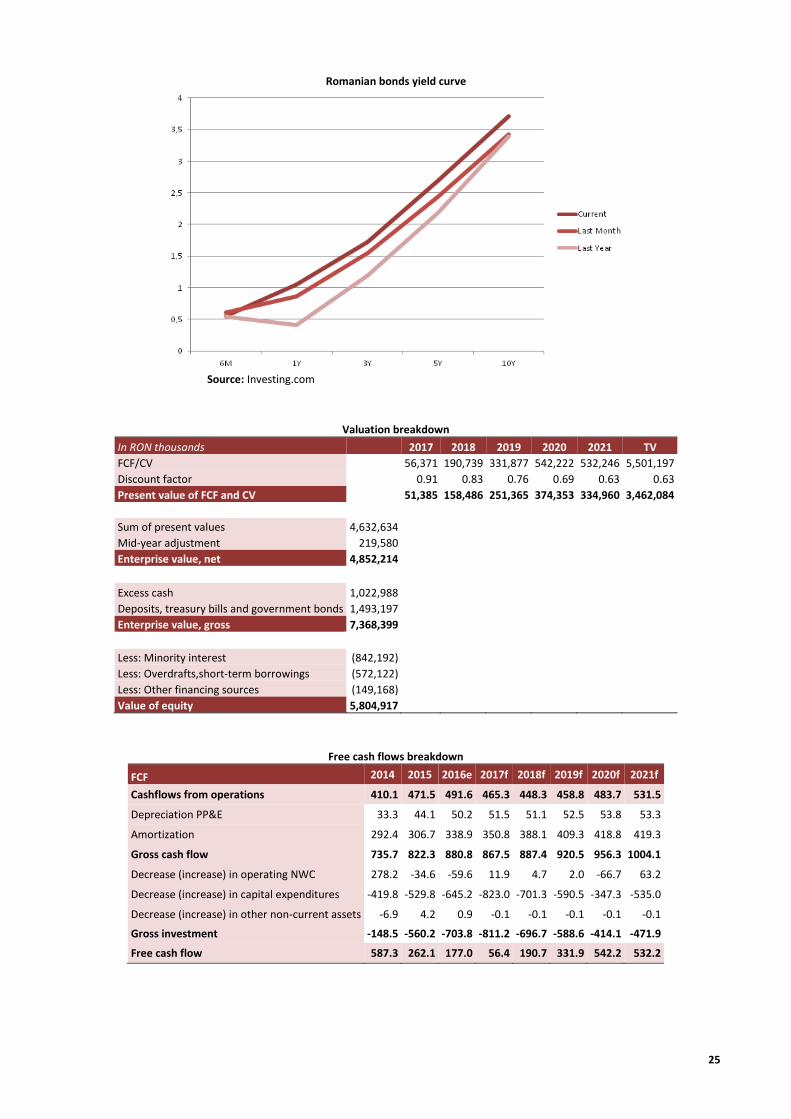

Risk free We took as the Risk free rate the Romanian 10Y Government Bonds YTM. Recently, in the past month the highest point was at 4.00%. We noticed there is upward pressure on the yield curve.

Equity market risk premium