62

FEBRUARY 2008 Globalisation and the changing UK economy

Department for Business, Enterprise and Regulatory Reform. www.berr.gov.ukFirst published February 2008. © Crown copyright. BERR/Pub 8693/02/08/NP. URN 08/607

FEBRUARY 2008

Globalisation and the changing UK economy

7480-BERR-Global UK economyCOV 31/1/08 16:26 Page bcoviv

FEBRUARY 2008

Globalisation and the changing UK economy

7480-BERR-Global UK economy 31/1/08 17:34 Page I

Contents

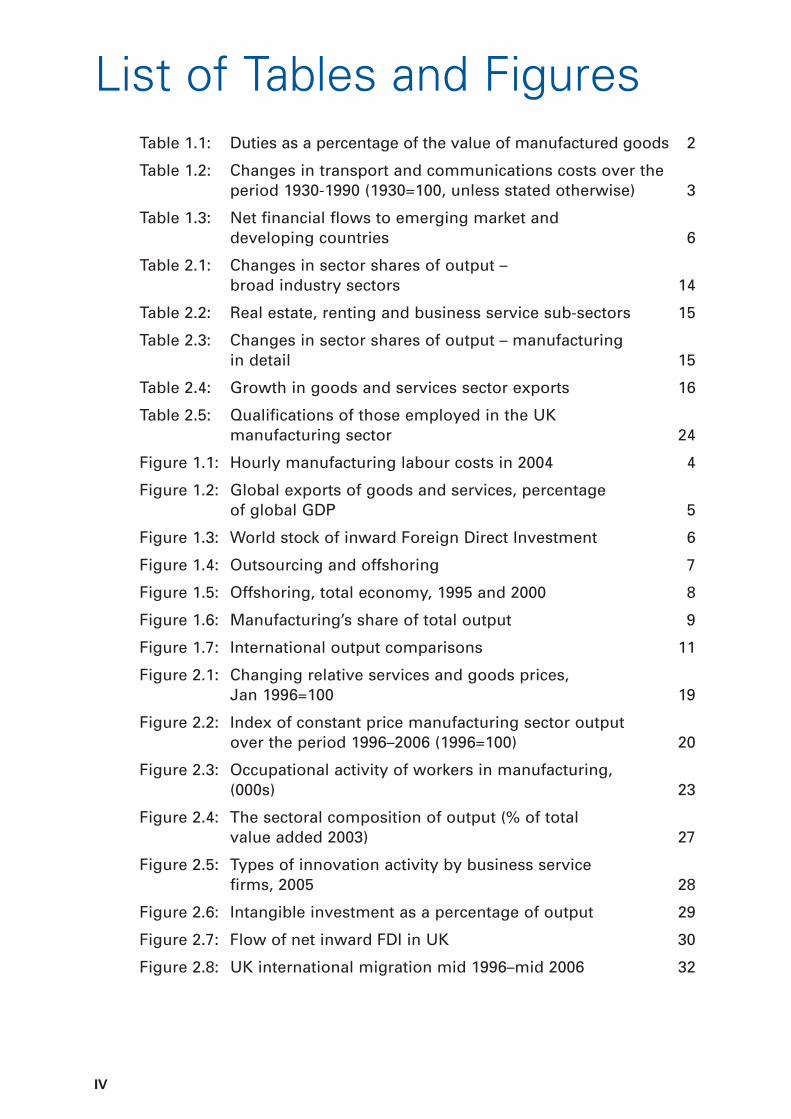

List of Tables and Figures IV

Foreword V

Executive Summary VII

1. The process of globalisation 11.1 Defining globalisation 1

1.2 Drivers of the latest wave of globalisation 2

1.3 Consequences of the latest wave of globalisation 5

2. The changing UK economy 132.1 Changes in output and employment shares 13

2.2 Export performance 16

2.3 Explaining the changing shape of the UK economy 18

3. The policy response to globalisation 333.1 Globalisation, trade openness and economic growth 33

References 49

III

7480-BERR-Global UK economy 31/1/08 17:34 Page III

List of Tables and FiguresTable 1.1: Duties as a percentage of the value of manufactured goods 2

Table 1.2: Changes in transport and communications costs over theperiod 1930-1990 (1930=100, unless stated otherwise) 3

Table 1.3: Net financial flows to emerging market and developing countries 6

Table 2.1: Changes in sector shares of output – broad industry sectors 14

Table 2.2: Real estate, renting and business service sub-sectors 15

Table 2.3: Changes in sector shares of output – manufacturing in detail 15

Table 2.4: Growth in goods and services sector exports 16

Table 2.5: Qualifications of those employed in the UK manufacturing sector 24

Figure 1.1: Hourly manufacturing labour costs in 2004 4

Figure 1.2: Global exports of goods and services, percentage of global GDP 5

Figure 1.3: World stock of inward Foreign Direct Investment 6

Figure 1.4: Outsourcing and offshoring 7

Figure 1.5: Offshoring, total economy, 1995 and 2000 8

Figure 1.6: Manufacturing’s share of total output 9

Figure 1.7: International output comparisons 11

Figure 2.1: Changing relative services and goods prices, Jan 1996=100 19

Figure 2.2: Index of constant price manufacturing sector output over the period 1996–2006 (1996=100) 20

Figure 2.3: Occupational activity of workers in manufacturing, (000s) 23

Figure 2.4: The sectoral composition of output (% of total value added 2003) 27

Figure 2.5: Types of innovation activity by business service firms, 2005 28

Figure 2.6: Intangible investment as a percentage of output 29

Figure 2.7: Flow of net inward FDI in UK 30

Figure 2.8: UK international migration mid 1996–mid 2006 32

IV

7480-BERR-Global UK economy 31/1/08 17:34 Page IV

Foreword Globalisation is changing the world’s economic landscape and the way we liveour lives. While globalisation, and the arguments that surround it, have ebbedand flowed for centuries, the wave of globalisation we are currentlyexperiencing is unique in terms of the speed and intensity of the political,economic, social and technological forces that have collided to create it. It hasunleashed a renewed wave of people, commerce and capital throughout theglobal economy and has powered the creation and transformation of markets,jobs and industries across the world, at ever increasing speeds.

This paper sets out how firms across the UK economy are taking advantage ofthe opportunities provided by globalisation in terms of new, rapidly-growingmarkets for producers and investors. It describes how many firms aresuccessfully responding to the challenge of low-wage competition by investingin innovation and skills in order to move up the value chain into morespecialised, high-quality goods and services.

The constant change that globalisation brings can create anxiety anduncertainty, as new technologies and methods of working appear to destroy jobsand skills almost overnight. The Government understands that this can bechallenging and daunting to workers who have to cope with a changing workenvironment and need to develop new skills. However, these are not reasons toturn our back on trade and revert to protectionist measures; the lesson of thefirst half of the twentieth century is that responding to economic uncertaintythrough protectionism only serves to undermine the process of innovation andeconomic growth, putting more pressure on jobs and living standards. TheGovernment has an important role to play in helping people to cope and toadjust to the changes brought by globalisation.

BERR’s role is to work with businesses to enable them to succeed in thischanging environment and help ensure that the benefits of globalisation are feltas widely as possible and across all regions. Key to this is ensuring thatindividuals develop the skills to enable them to adapt and prosper whateverfuture globalisation brings. For this reason the Government has set the UK theambition of being the world leader in skills by 2020. BERR is working as the voicefor business to ensure the concerns of business are understood throughoutGovernment on other priority areas such as planning, transport, innovation andtaxation. At the same time we remain committed to working with internationalpartners to open up trade and create opportunities for business both within theEU and beyond.

The Rt. Hon. John Hutton, Secretary of State for Business, Enterprise andRegulatory Reform, February 2008.

V

7480-BERR-Global UK economy 31/1/08 17:34 Page V

VII

Executive SummaryGlobalisation is transforming the face of the global economy. This paper seeksto examine in more detail exactly what globalisation involves, how the UKeconomy is being transformed, in part in response to globalisation, and thepolicies that the Government is putting in place to best enable businesses tomaximise the opportunities and meet the challenges of globalisation.

In the first chapter of this paper we describe how globalisation has increased thefree flow of ideas, people, goods, services and capital across borders and hasincreased the integration of economies and societies.

While globalisation is not a new phenomenon, with waves of globalisationdating back to the 1800s, the current wave of globalisation is unique in bringingtogether the following three factors:

� The adoption by a large number of countries of more open economic policiesin the post-WWII era. This has increased international trade in goods andservices, and cross-border flows of both capital and labour.

� Rapid technical progress, particularly developments in the field ofInformation and Communications Technology (ICT). This has sharply loweredtransport and communications costs and has increased the tradability ofgoods and services.

� The emergence of developing, low-wage economies. The arrival of thesecountries on the world stage stems mainly from political and economicchanges – notably China’s accession to the WTO in 2001 and economicreform in India.

The consequences of the latest wave of globalisation can be observed mostclearly in the massive growth in cross-border trade in goods and service duringthe post-WWII era, with international trade in intermediate inputs and cross-border trade in services growing particularly strongly in the last decade or so.Similarly, international capital flows – particularly Foreign Direct Investment(FDI) – have also increased markedly in the post-WWII era. These figures have,in part, been driven by growth in global value chains, whereby firms locatedifferent parts of the production process in different countries according torelative cost structures, which has led to increased international trade inintermediate inputs. Part of this process is offshoring, which involves firmsselecting and holding on to the stages of the value chain that they consider toadd the most value, while relocating the firm’s remaining activities to foreigncountries or to third parties in foreign countries. While offshoring has had a highand often negative media profile, research suggests that it has not had aparticularly significant impact on employment structures in a large number ofdeveloped countries, and has often allowed firms to increase productivity, withthe bulk of demand continuing to be met domestically.

7480-BERR-Global UK economy 31/1/08 17:34 Page VII

Nevertheless, the rise of low wage economies and associated growth in globalsupply chains have both contributed to a significant change in the compositionof most advanced economies’ structures in recent years. The rapid technologicalchanges and accompanying investment we have seen in manufacturing globallyhas facilitated strong productivity growth in the sector, resulting in falling pricesrelative to services and has facilitated a shift in the composition of both (currentprice) output and employment towards the services sector.

The current wave of globalisation has also changed the make up of the globaleconomy with, for example, China’s share of world output increasing from justover 2.6 per cent in 1980 to almost 5.5 per cent in 2006 and this is set to increasefurther according to International Monetary Fund (IMF) modelling. While this willprovide substantial potential opportunities for developed economies – with,amongst other things, new markets for their exporters and investors – it will alsoincrease the pressure on energy resources and the environment, withdeveloping economies expected to account for half of world energy demand by2012. Meeting the challenge of climate change, including reducing greenhousegas emissions, is clearly integral to how we manage internationally the ongoingprocess of globalisation.

Chapter 2 considers how the UK economy has been changing in recent years, inresponse to both developments in the global economy and domestic forces,such as population ageing and rising incomes. The chapter discusses how theUK economy has been able to take advantage of technological developmentswhich have made many services increasingly tradable and how the UK hasbecome a world leader in the growing export markets for many financial andbusiness services.

In common with many OECD economies, the UK has seen a fall in the share ofoutput measured in current prices accounted for by manufacturing. Part of thismay result from measurement difficulties associated with the increasinginteractions between manufacturing and service activities and subsequentoutsourcing and reclassification. The fall in the relative value of current pricemanufacturing output is also related to the global fall in the relative price ofmanufactured goods as producers all over the world have taken advantage ofimprovements in technology to lower costs and raise quality. Changes indomestic demand, in line with increased incomes and greater leisure time, havealso encouraged the more rapid expansion in some service sectors.

But the headline figure for the share of output accounted for by manufacturingalso hides the transformation that much of the sector has gone through in recentyears in response to both technological improvements and the emergence ofChina and India into the global economy. Within manufacturing, there has beena shift towards higher skilled professions, such as professional services andresearch and development, and in line with this an improvement in averagequalification levels. Case studies of the electronics and automotive sectors helpillustrate the changing role of the UK within increasingly global supply chains.

Globalisation and the changing UK economy

VIII

7480-BERR-Global UK economy 31/1/08 17:34 Page VIII

Similarly, in services, we note the extent to which UK service providers haveundertaken different types of innovation – including through intangibleinvestment in areas such as training, R&D and branding – in order to raisequality and lower costs, enabling the UK to become global leaders in many,increasingly tradable services.

The chapter also considers the importance of FDI and engagement with multi-national enterprises (MNEs) in helping the UK raise productivity and competesuccessfully in the global economy. There is a growing economic literaturewhich points to the important role for FDI and MNEs in assisting productivitygrowth, both through a direct effect on investment, and more indirectly throughthe spread of technological know-how and management best practice. Similarly,the increased net inward migration into the UK in recent years is considered,with the positive impact such migration has had on economic growth in recentyears noted, alongside the possible positive impact on long-term productivitygrowth.

The final chapter considers the UK Government’s policy response toglobalisaton. Globalisation is creating tremendous opportunities for businessthrough the opening up of new markets, access to new technologies andcheaper products for consumers. Economic theory and evidence also points tothe strong relationship between increased trade and rising prosperity as well asthe dangers of retreating into protectionism. But globalisation also createschallenges for the UK economy. Globalisation puts UK firms and workers incompetition with those from across the globe and reinforces the need for UKfirms to continue to innovate and offer higher quality goods and services. Andinevitably, given the rapid pace of change that globalisation brings about, thereare rising fears that globalisation will undermine UK competitive advantagesand lead to job losses and insecurity. Not all people and places will be well-equipped to take advantage of the opportunities of globalisation.

The policy response to recent trends in globalisation, and the associatedopportunities and threats to the UK economy, has centred on three key priorityareas.

� Firstly, in recognition of the potential benefits to be derived fromglobalisation and greater openness, the UK is committed to reducinginternational barriers to trade. At the same time, we need to work withinternational partners to ensure that international institutions such as the IMFare fully equipped to provide the necessary direction and support to theongoing process of globalisation.

Globalisation and the changing UK economy

IX

7480-BERR-Global UK economy 31/1/08 17:34 Page IX

� Secondly, the Government’s strategy of raising productivity through ensuringmacroeconomic stability and putting in place policies to strengthen theproductivity drivers (competition, investment, innovation, enterprise andskills) will also work to ensure that UK business is best placed to takeadvantage of the benefits of globalisation and compete effectively ininternational markets. In an increasingly competitive global economy, there isa renewed emphasis on having a world class risk-based regulatory regimewhich finds the right balance in supporting both competitiveness and widerobjectives.

� Thirdly, to ensure the benefits of globalisation are felt as widely as possible,the Government has a number of policies in place to help the UK economyadapt to its changing role in the global economy, as well as to reduce regionaleconomic performance differences and to protect the most vulnerableworkers through targeted labour market interventions.

Globalisation and the changing UK economy

X

7480-BERR-Global UK economy 31/1/08 17:34 Page X

1. The process ofglobalisation

Globalisation is transforming the face of the global economy. But what exactlydoes globalisation involve? In this chapter we define what globalisation is,noting, first, that is not a recent phenomenon, with waves of globalisation datingback to the 1800s and, second, that it is about much more than the location ofproduction in low wage economies.

The second section discusses the various drivers of the current wave ofglobalisation. We identify three relatively recent developments in particular – theadoption of more open economic policies, increasing technological innovation,and the emergence of developing, low-wage economies on the world stage – ascentral to the current wave of globalisation.

Having discussed the driving forces behind the current wave of globalisation, wego on to note that these developments have facilitated greater cross-bordertrade in goods and services, foreign direct investment, and migration. Unlikeprevious episodes of globalisation, the latest wave is also very closelyassociated with the development of globally-distributed production systems.These so-called global supply chains reflect the increasingly global distributionof the various stages in the production process, in turn partly the result ofoffshoring.

1.1 Defining globalisation

Numerous definitions – both economic and non-economic – of globalisationexist, but according to one of the most oft-cited definitions, that of theInternational Monetary Fund (IMF), globalisation is “the process through whichan increasingly free flow of ideas, people, goods, services and capital leads tothe integration of economies and societies”.1 Globalisation is, thus, about muchmore than the location of production in low wage economies.

Globalisation is not a recent phenomenon; it is possible to trace waves ofglobalisation back to the 1800s. The period 1870-1913, for example, saw asignificant increase in international trade, accompanied by cross-border flows oflabour and capital. The current wave of globalisation, the pace and scale ofwhich are probably without precedent, started as early as the 1950s.

Globalisation has the potential to benefit emerging countries, providing amechanism through which poverty can be reduced. The rapid growth of theseemerging economies also provides substantial potential opportunities fordeveloped economies – with new markets for exporters and investors, andcheaper, more diverse goods and services for consumers.

1

1 Köhler, H. (2002).

7480-BERR-Global UK economy 31/1/08 17:34 Page 1

1.2 Drivers of the latest wave of globalisation

The current wave of globalisation has been driven and facilitated by severaldevelopments which have not previously occurred together. These are:

� The adoption of more open economic policies – which have increasedinternational trade in goods and services, and cross-border flows of bothcapital and labour;

� Technological progress – which has sharply lowered transport andcommunications costs and has increased the tradability of goods andservices; and

� The emergence of developing, low-wage economies on the world stage –which has been led by China and India.

We discuss the three main drivers of the latest wave of globalisation in moredetail below, beginning with the adoption of more open economic policies in thepost-WWII era.

The adoption of more open economic policies

The period since WWII has seen a series of reductions in the tariffs levied onmanufactured goods, thanks in large part to the General Agreement on Tradeand Tariffs (GATT) and, latterly, the World Trade Organisation (WTO). Table 1.1,below, indicates the scale of these tariff reductions on manufactured goods.

Table 1.1: Duties as a percentage of the value of manufactured goods1913 1950 1990 2004

Germany 20 26 5.9 3.6

Japan 30 25 5.3 3.9

Italy 18 25 5.9 3.6

United States 44 14 4.8 4.0

Source: Acocella (2005).

In addition to tariff reductions on manufactured goods, the post-WWII era hasseen the gradual lowering of non-tariff barriers as well. Reductions wereparticularly marked in the regional trading blocs formed after WWII, such as theEuropean Union (EU) and North American Free Trade Area (NAFTA). Finally, thegradual elimination of restrictions on Foreign Direct Investment (FDI) put inplace after WWII liberalised international capital movements.

TECHNOLOGICAL PROGRESS

Recent technological progress has driven the current wave of globalisationthrough four main channels: transactions costs; productivity; modularisation;and dissemination.

Globalisation and the changing UK economy

2

7480-BERR-Global UK economy 31/1/08 17:34 Page 2

Technological progress, particularly developments in the field of Informationand Communications Technology (ICT), has had a very significant impact ontransactions costs. As Table 1.2 shows, in 1990, the cost of a three-minute phonecall between London and New York was roughly one-seventieth of what it wasin 1930; the cost of air passenger transport in 1990 was approximately one-sixthof what it was in 1930.

Table 1.2: Changes in transport and communications costs over theperiod 1930-1990 (1930=100, unless stated otherwise)

1930 1950 1960 1970 1990

Air transport costs per passenger mile 100 44 56 24 16

Cost of a three minute London-New York telephone call 100 22 19 13 1.4

Cost of using a satellite n/a n/a n/a 100 8

Source: Acocella (2005).

Even more recent developments – such as satellite and broadbandcommunications – have effectively increased the number of services it iseconomically feasible to trade. Here too there have also been significant costreductions – with the cost of using a satellite falling by 92 per cent between 1970and 1990.

But, beyond this, technological progress has also enabled the separation, orunbundling, of the production and consumption of information-intensive serviceactivities, such as Research and Development (R&D), inventory management,quality control, professional and technical services, banking and insurance, andgovernment administration. Now even services in which consumer-producerinteraction is very high can, in principle, be unbundled and traded acrossborders. Examples include remote education facilitated by onlinecommunication and multimedia systems, and the remote transmission ofmedical diagnostic services.

Additionally, technological progress has also made it possible to reduce thecomplexity of production. This has been done, in the main, through thedevelopment of production systems broken up into modules i.e.,modularisation. With complexity reduced, production develops a more distinctsupply chain, and modules can in some cases be outsourced, potentially to thebest global source of supply.2

Finally, technological progress has also facilitated the dissemination ofknowledge and technological progress and has made it vastly easier to benefitfrom spillovers from private investment in knowledge creation, such as R&D.Knowledge spillovers from R&D used to have a marked local bias, tending to

Globalisation and the changing UK economy

3

2 Modularisation does not lead automatically to outsourcing because in some cases it can create a greater need forinteraction, co-ordination and co-operation across workstreams.

7480-BERR-Global UK economy 31/1/08 17:34 Page 3

arise within local clusters through, for example, labour market turnover.However, the latest analysis of the geography of patents citations, a proxymeasure of knowledge transfer, suggests that the local bias of knowledgespillovers has fallen over time compared to earlier studies, with the local bias inthe most ICT-intensive sectors all but disappeared.

THE EMERGENCE OF DEVELOPING, LOW-WAGE ECONOMIES ON THE WORLD

STAGE

For most of the post-WWII period, it was the major, developed economies (withthe notable exceptions of a few outward-looking countries, like Japan, SouthKorea, and certain other Asian economies) that increased their economiclinkages. Over the last decade or so, however, some highly populous, low-wagedeveloping economies have emerged onto the world stage. China and Indiahave been at the forefront of this movement, with both nations greatlyincreasing their shares of global output, trade and foreign direct investment inthe recent past.

Figure 1.1: Hourly manufacturing labour costs in 2004

Source: Estimates from BLS (2004); China and India from Oxford Economic Forecasting in Olsen, K. (2006), TheChanging Nature of Manufacturing in OECD Countries. Notes: (1) Estimates of Chinese labour compensation may beunderestimated as Chinese workers may benefit from various types of non-monetary compensation, includingsubsidised accommodation. (2) Trade-weighted estimates, as shown in BLS (2004).

The arrival of these countries on the world stage stems mainly from recenteconomic and political changes: economic reform in China, leading to itsaccession to the WTO in 2001 and, different, but nevertheless important,economic reform in India. But the rise of these countries has also been driven bythe adoption of open, liberal economic policies in other parts of the world and

0

5

10

15

20

25

30

35

Denm

ark

Norway

Germ

any

Switzer

land

Belgiu

m

Finlan

d

Nether

lands

Austria

Sweden

EU-15 (

2)

Luxe

mbourgUS

Fran

ceUK

Japan

Australi

a

Canad

a

Irelan

d

Italy

Spain

New Z

ealan

d

Korea

Portugal

Chines

e Taip

ei

Hong Kong C

hina

Czech

Rep

ublic

Brazil

Mex

ico

India

China (

1)

$US

Globalisation and the changing UK economy

4

7480-BERR-Global UK economy 31/1/08 17:34 Page 4

technological progress which has made it possible to manage remoteproduction far more effectively.

1.3 Consequences of the latest wave of globalisation

TRADE IN GOODS AND SERVICES, INTERNATIONAL FDI, AND MIGRATION

HAVE ALL INCREASED AND PRODUCTION IS INCREASINGLY ORGANISED

ALONG GLOBAL VALUE CHAINS

Cross-border trade in goods has taken off since WWII. This has been particularlytrue of the recent past, with the total value of goods exports rising from$5,398,671m in 1996 to $11,982,932m in 2006. While goods exports havehistorically accounted for the bulk of total exports, trade in services is nowincreasingly important, accounting for 19 per cent of total world exports in 2006.

Growth in global exports of goods and services has, in fact, been so strong thatit has outpaced growth in world output in the recent past, leading to an increasein the ratio of global exports of goods and services to global GDP, as shownin Figure 1.2.

Figure 1.2: Global exports of goods and services, percentage ofglobal GDP

Source: IMF World Economic Outlook.

Mirroring this increase in cross-border trade in goods and services there hasbeen an increase in international capital flows since the Second World War –again, particularly in the more recent past. According to UNCTAD, there was amore than three-fold increase in the world’s stock of inward FDI, from$3,083,106m to $11,998,838m between 1996 and 2006, as Figure 1.3 shows.

0

5%

10%

15%

20%

25%

30%

35%

20062005200420032002200120001999199819971996

Globalisation and the changing UK economy

5

7480-BERR-Global UK economy 31/1/08 17:34 Page 5

Figure 1.3: World stock of inward Foreign Direct Investment

Source: UNCTAD, Handbook of Statistics.

Not only has the total stock of inward FDI increased greatly, the direction andnature of FDI has also changed in the recent past. Developing and emergingeconomies are now far more important in terms of FDI inflows than they werepreviously, with significant amounts of capital flowing from capital-abundantindustrialised countries to a few developing countries, as Table 1.3 shows,helping build up the latter’s production and trade capabilities. In the very recentpast, a handful of developing countries have become significant sources of FDIin their own right – with FDI flowing from these countries back to developedeconomies.

Table 1.3: Net financial flows to emerging market and developingcountries3

$USbn Average Average

1993–1998 1999–2004 2005 2006

Net private capital flows 158.0 120.8 271.1 220.9

Net direct investment 110.0 174.0 262.7 258.3

Net portfolio investmenta 71.1 -14.2 23.3 -111.9

Other net investmentb -23.0 -39.6 -17.0 73.6

Net official flows 11.2 -22.1 -146.4 -165.8

Total net flows 169.2 98.7 124.7 55.2

Change in reserves -71.1 -237.1 -595.3 -754.2

Source: International Monetary Fund (IMF), World Economic Outlook Database, October 2007. Notes: (a) Includingportfolio debt and equity investment; (b) Including short- and long-term bank lending.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

20062005200420032002200120001999199819971996

$US

bn

Globalisation and the changing UK economy

6

3 IMF classification includes Israel and Korea, Singapore, Taiwan and Hong Kong, normally counted among theadvanced economies.

7480-BERR-Global UK economy 31/1/08 17:34 Page 6

Looking at the nature of FDI flows in the recent past, it is clear that there hasbeen very rapid growth of FDI into the service sector since the 1990s, particularlyto developing countries’ service sectors. The share of services in the stock ofinward FDI in developing countries increased from 47 per cent in 1990 to 55 percent in 2002 thanks in large part to the rapid growth in the offshoring of services,and the opening of domestic financial activities.

Echoing greater trade in goods and services and FDI, migration – which has longbeen associated with globalisation – has also increased in the current round ofglobalisation. Migration flows have doubled since 1975 and around 3 per cent ofthe world’s population currently live outside their country of birth. Beyond this,the nature of migration has changed significantly, with temporary work-relatedand high-skilled migration accounting for an increasing share of migrationbetween OECD countries. Although migration is not central to the current waveof globalisation compared to previous episodes, some of its effects are stillimportant. For example, research suggests that migration flows have: supportedeconomic growth – particularly in the US; facilitated knowledge transfer –through, for example, the return of electronics engineers from the US to Indiaand China; and increased flows of remittances – which are important sources offunding for those developing countries which are not major recipients of privatecapital flows.

These figures – particularly the trade and FDI figures – have partly been drivenby the relatively recent emergence of global value chains – whereby firms locatedifferent parts of the production process in different countries according torelative cost structures. The development of global value chains has beenfacilitated by technological progress which has made it easier to supply servicesremotely, to modularise production activities and manage them remotely andhas resulted in a massive increase in cross-border trade in intermediates andbusiness services.

The emergence of global value chains is, in turn, associated with offshoring,which involves firms selecting and holding on to the stages in the value chainthat they consider to be ‘core’, whilst relocating the firm’s ‘non-core’ activities toforeign countries or to third parties in foreign countries.

Figure 1.4: Outsourcing and offshoring

Location

National International

Control Outsourced Domestic outsourcing International outsourcing

Insourced Domestic supply International insourcing

Source: Van Welsum, D. and Vickery, G. (2005).

Globalisation and the changing UK economy

7

7480-BERR-Global UK economy 31/1/08 17:34 Page 7

No official data on offshoring and global value chains exists, but the impact ofoffshoring on developed economies can be approximated using a proxy foroffshoring – the share of non-energy imported intermediate inputs in totalnon-energy intermediate inputs.4 A proxy measure of this type is reported inFigure 1.5.

Figure 1.5 shows that between 1995 and 2000, offshoring grew in almost allOECD countries, with significant increases in the sourcing of intermediatesabroad in a number of countries. Comparing OECD member states, it is clearthat, small increases between 1995 and 2000 notwithstanding, Japan and the USoffshore relatively little compared to other countries. It is also apparent thatsmaller countries like Ireland and Hungary) offshore quite a lot.

Figure 1.5: Offshoring, total economy, 1995 and 20005

Source: OECD, Input-Output Tables Database. Note: Australia 1995 and 1999; Canada 1997 and 2000; Greece 1995 and1999; Hungary 1998 and 2000; Norway 1995 and 2001; Portugal 1995 and 1999.

Despite having a high and often negative media profile in almost all OECDcountries, offshoring does not appear to have had a significant negativeeconomic impact on a large number of developed countries. Studies suggestthat there is not a significant link between offshoring and aggregate levels ofemployment. In most cases, the bulk of demand continues to be metdomestically. There are a number of reasons for this, including the fact that thedelivery of some services requires physical proximity to the customer,transactions costs are high, customer preferences, and competitive advantage.

0%

10%

20%

30%

40%

50%

Irelan

d

Hungary

Czech

Rep

ublic

Slova

k Rep

ublic

Belgiu

m

Austria

Switzer

land

Canad

a

Nether

lands

Portugal

Norway

Sweden

Greec

e

Denm

ark

Spain

Turk

ey

Poland

Finlan

d

Korea

Germ

any

UK

Italy

New Z

ealan

d

Australi

a

Fran

ceUS

Japan

1995 2000

Globalisation and the changing UK economy

8

4 This can be derived from input-tables, which contain information on the value intermediate goods and servicesimported from elsewhere.

5 Calculated as the share of non-energy imported intermediates in total non-energy intermediate inputs.

7480-BERR-Global UK economy 31/1/08 17:34 Page 8

PRODUCTIVITY-IMPROVING TECHNOLOGICAL PROGRESS HAS CHANGED THE

COMPOSITION OF MOST ADVANCED ECONOMIES’ OUTPUT AND EMPLOYMENT

Productivity-improving technological improvements have impacted on somedeveloped countries’ sectors (i.e., manufacturing) more than others (i.e.,personal services). This matters because it can be shown that, under certainassumptions, sectors which experience more rapid gains in productivity willexperience a fall in the relative price of their products, where price is determinedby marginal cost. Crucially, if the ensuing increase in demand is not sufficient tofully offset this fall in price the total value of output (i.e., price multiplied byquantity demanded) will fall and the sector’s share of total economy-wide outputmeasured in current prices will decline. This is the so-called Baumol effect,identified by William Baumol in the late 1960s.6

Relatively higher technology-driven productivity growth in developedeconomies’ manufacturing sectors compared to some service sectors, notablythe personal services sector, has led to a decline in the price of manufacturesrelative to services, and a decline in the manufacturing sector’s share of totaloutput measured in current prices in almost all developed economies. Thisphenomenon is illustrated in Figure 1.6 below. In several cases, these changeshave been accompanied by more-or-less equal and opposite growth in the shareof total output measured in current prices accounted for by the services sector.

Figure 1.6: Manufacturing’s share of total output

Source: UNCTAD. Note: Pre-1990 data for Germany unavailable.

0%

5%

10%

15%

20%

25%

30%

35%

200520001995199019851980

Japan Germany UK US France

Globalisation and the changing UK economy

9

6 Baumol, W. (1967).

7480-BERR-Global UK economy 31/1/08 17:34 Page 9

A corollary of the Baumol effect is that if we assume that wages are set in aneconomy-wide labour market, sectors that experience more rapid gains inproductivity (and, consequently, experience relative price declines) will accountfor a smaller share of total employment in the same way that they will accountfor a smaller share of total output if the increase in demand is not sufficient tofully compensate for the price effect.

Internationally comparable data shows that, in keeping with the Baumol effect,manufacturing’s share of total employment has also fallen off in most advancedeconomies with, for example, manufacturing employment falling by around 3million in the US and by almost 3 million in Japan since 1997. Again, this hasbeen accompanied by more-or-less equal and opposite growth in the share oftotal employment accounted for by the services sector.7

THE BALANCE OF ECONOMIC POWER IN THE GLOBAL ECONOMY HAS

CHANGED

The entry of highly populous, low-wage economies onto the world stage haschanged the make up of the global economy, particularly in terms of countries’shares of total world output.

Between 1980 and 2006, China’s share of world output increased from just over2.6 per cent to almost 5.5 per cent. India’s rise over the same period was slightlyless impressive, but India’s share of world output nevertheless increased from1.5 per cent to over 1.8 per cent. Both countries have grown particularly stronglyin the recent past: both India and China’s shares of world output have risen year-on-year since 1994.

Over time, however, the process of economic development usually leads to anincrease in a country’s real exchange rate. This combined with rises in realwages means that differences in labour costs tend to narrow. Such a pattern isalready evident in the case of China, according to the World Bank, whereaverage wages, on an internationally comparable basis, have trebled in the lastdecade.

Globalisation and the changing UK economy

10

7 The share of manufacturing employment in some major developing economies has also shrunk in recent years.Examples include China, Russia and Brazil. Alongside this, many of these countries have also seen rapid growth inmanufacturing output in recent years. This highlights the critical role of the differential productivity growth theory,a la Baumol (1967), in driving deindustrialisation in developing countries as well.

7480-BERR-Global UK economy 31/1/08 17:34 Page 10

Figure 1.7: International output comparisons

Source: BERR calculations based on FCO/IMF modelling.

Notwithstanding, according to an IMF/FCO model, recent trends look set tocontinue for some time to come. In particular, Chinese output (and China’s shareof total global output) is set to increase markedly through to 2020, as Figure 1.7shows.

The continued rise of developing economies on the world stage will providesubstantial potential opportunities for already developed economies – with,amongst other things, new markets for their exporters and investors. But thecontinued rise of these developing economies will also increase the pressure onenergy resources, with developing economies expected to account for half ofworld energy demand by 2012. The continued rise of these developingeconomies will also increase the pressures on the environment, notably throughclimate change. Meeting the challenge of climate change, including reducinggreenhouse gas emissions, is clearly integral to how we manage internationallythe ongoing process of globalisation.

ChinaChina

IndiaUK

EU27excl. UK

USUS

RoWRoW

EU27excl. UK

India

UK

Total Output 2006

$US48.2 trillion

Total Output 2020

$US77.8 trillion

Globalisation and the changing UK economy

11

7480-BERR-Global UK economy 31/1/08 17:34 Page 11

2. The changing UKeconomy

Chapter 1 examined the drivers of globalisation and how they are acting asforces for change in the global economy. This section considers how the UKeconomy has been changing in recent years, in response to both developmentsin the global economy and domestic forces such as population ageing and risingincomes.

The chapter discusses how the UK economy has been able to take advantage oftechnological developments which have made many services increasinglytradable and how the UK has become a world leader in the growing exportmarkets for many financial and business services.

While, in common with many OECD economies, the UK has seen a fall in theshare of output accounted for by manufacturing, this headline figure hides thetransformation that much of the sector has gone through in recent years inresponse to both technological improvements and the emergence of China andIndia into the global economy. Case studies of the electronics and automotivesectors help shed light on the changing role of the UK within increasingly globalsupply chains.

We highlight the importance of increasing investment in intangibles such asR&D, design and training, which also lies behind changes in both themanufacturing and service sectors.

2.1 Changes in output and employment shares

The UK economy has continued its long-term structural change during the pastten years with, broadly speaking, a continuing shift in terms of the shares ofoutput and employment from manufacturing towards services (although theshift away from manufacturing is more moderate in output terms than inemployment terms). As Table 2.1 illustrates, the growing prominence of servicesis underlined by the growing share of output and employment accounted for bythe wholesale and retail trade, financial intermediation, health and social work,education, other social and personal services, and hotels and restaurants.

13

7480-BERR-Global UK economy 31/1/08 17:34 Page 13

Table 2.1: Changes in sector shares of output – broad industry sectors

Output (GVA) share (%) Ppt change in

share of output

2006 1996 1996–2006

Real estate, renting and business services 24.8 19.1 5.7

Manufacturing 13.2 21.1 -7.9

Wholesale and retail trade 12.1 11.6 0.5

Financial intermediation (excl. FISIM) 9.4 6.5 2.9

FISIM 5.0 3.3 1.7

Health and social work 7.3 6.4 0.9

Transport, storage and communications 7.2 7.8 -0.6

Construction 5.7 5.1 0.6

Education 5.6 5.4 0.2

Other social and personal services 5.4 4.3 1.1

Public administration and defence 5.1 5.8 -0.7

Hotels and restaurants 3.1 2.7 0.4

Mining and quarrying 2.4 2.9 -0.4

Electricity, gas and water 2.7 2.3 0.4

Agriculture, forestry and fishing 0.9 1.8 -0.8

Source: ONS Blue Book (including experimental output statistics). Note: FISIM = Financial intermediation services,independently measured.

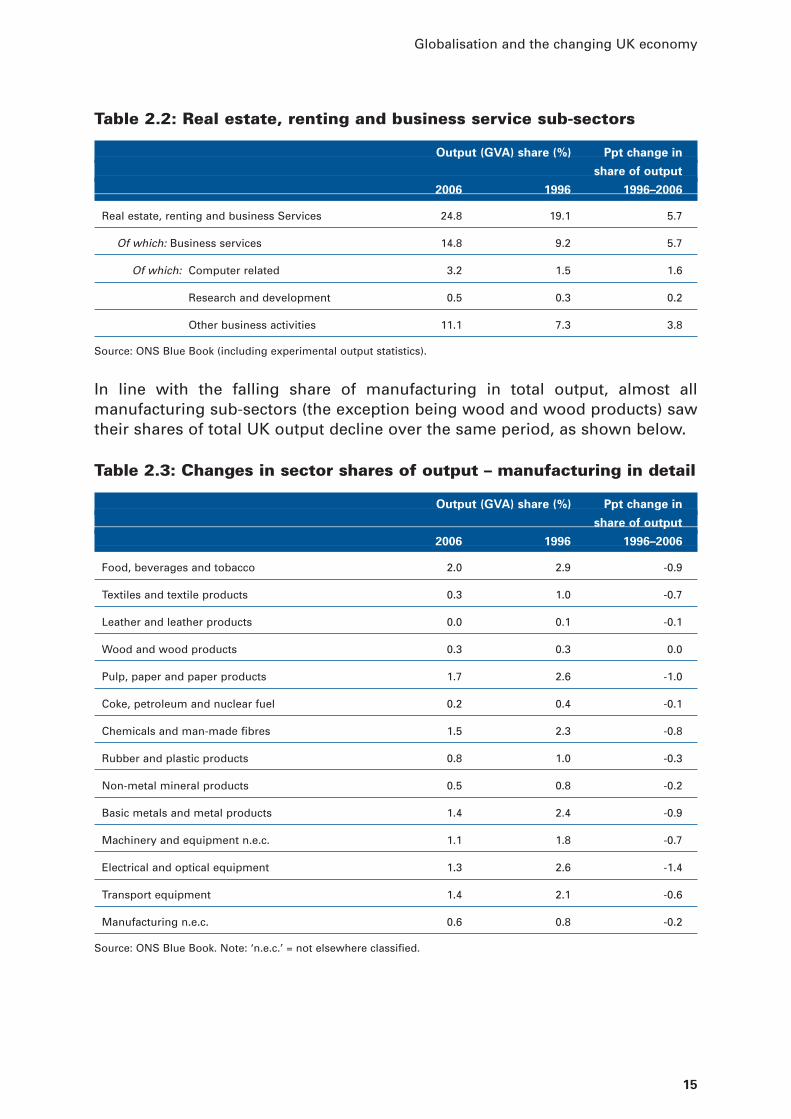

Growth in real estate, renting and business services, which increased its outputshare by 5.7 percentage points over the period 1996-2006, has been central togrowth in services. In turn, growth in business services has been central togrowth in the broader real estate, renting and business services sector, as Table2.2 shows. Business services include a diverse range of activities, from thecreative and technical, such as advertising, legal services and computing, toindustrial cleaning and call centres. In the past two decades business serviceshave doubled their share of GDP from 7 to 14 per cent, and account for almost1.7 million jobs more jobs than previously.

Globalisation and the changing UK economy

14

7480-BERR-Global UK economy 31/1/08 17:34 Page 14

Table 2.2: Real estate, renting and business service sub-sectors

Output (GVA) share (%) Ppt change in

share of output

2006 1996 1996–2006

Real estate, renting and business Services 24.8 19.1 5.7

Of which: Business services 14.8 9.2 5.7

Of which: Computer related 3.2 1.5 1.6

Research and development 0.5 0.3 0.2

Other business activities 11.1 7.3 3.8

Source: ONS Blue Book (including experimental output statistics).

In line with the falling share of manufacturing in total output, almost allmanufacturing sub-sectors (the exception being wood and wood products) sawtheir shares of total UK output decline over the same period, as shown below.

Table 2.3: Changes in sector shares of output – manufacturing in detail

Output (GVA) share (%) Ppt change in

share of output

2006 1996 1996–2006

Food, beverages and tobacco 2.0 2.9 -0.9

Textiles and textile products 0.3 1.0 -0.7

Leather and leather products 0.0 0.1 -0.1

Wood and wood products 0.3 0.3 0.0

Pulp, paper and paper products 1.7 2.6 -1.0

Coke, petroleum and nuclear fuel 0.2 0.4 -0.1

Chemicals and man-made fibres 1.5 2.3 -0.8

Rubber and plastic products 0.8 1.0 -0.3

Non-metal mineral products 0.5 0.8 -0.2

Basic metals and metal products 1.4 2.4 -0.9

Machinery and equipment n.e.c. 1.1 1.8 -0.7

Electrical and optical equipment 1.3 2.6 -1.4

Transport equipment 1.4 2.1 -0.6

Manufacturing n.e.c. 0.6 0.8 -0.2

Source: ONS Blue Book. Note: ‘n.e.c.’ = not elsewhere classified.

Globalisation and the changing UK economy

15

7480-BERR-Global UK economy 31/1/08 17:34 Page 15

2.2 Export performance

Table 2.4 illustrates how the UK has benefited in terms of higher exports fromthe rapid growth in world trade outlined in chapter 1. The UK has seenimpressive growth in many service sector exports. Financial services and otherbusiness services in particular have become significant contributors to overallUK export volumes in recent years. While other countries have also benefitedfrom the technological changes that have allowed increased trade in services,UK performance has been particularly strong. According to the IMF, the UK wasresponsible for 8.7 per cent of service exports in 2004, compared with Germany’s6.6 per cent share and France’s 5.1 per cent share. The UK is the global marketleader in financial services exports (24.4 per cent of world exports) and computerservices (13.7 per cent of world exports).

Table 2.4: Growth in goods and services sector exports

Service Good Growth Percentage share of Change in share

1996–2006 total exports 2006 of total exports

(%) (%) 1996–2006 (%)

Computer and information Services 495 1.8 1.3

Communications services 303 1.2 0.7

Construction services 280 0.2 0.1

Financial services 246 7.7 4.0

Non-oil fuels 224 0.6 0.3

Personal, cultural and recreational Services 162 0.5 0.3

Other business services 151 9.4 3.2

Oil 112 6.3 1.4

Basic materials 76 1.3 0.1

Royalties and license fees 74 2.0 0.1

Government services 62 0.6 0.0

Transportation services 53 4.5 -0.3

Finished manufactured goods 46 37.2 -4.7

Semi-manufactured goods 44 17.6 -2.5

Travel services 34 5.0 -1.1

Insurance services 33 1.0 -0.2

Food, beverages, tobacco -2 3.0 -2.0

Unspecified goods -33 0.4 -0.5

Total services 115 33.7 8.0

Total goods 47 66.3 -8.0

Source: ONS Pink Book.

Globalisation and the changing UK economy

16

7480-BERR-Global UK economy 31/1/08 17:34 Page 16

It is also noticeable that export volumes increased significantly in recent years inmany goods sectors. An examination of commodity exports at a more detailedlevel shows that the UK has a strong trade record in a number of smaller, morespecialised manufacturing sectors. These tend to be sectors providing lowvolume, high-technology, specialised or innovative products which may betailored to a specific consumer need. Examples include cultural items (art andprinted materials), pharmaceuticals, aircraft components, certain chemicals(particularly pharmaceutical) and instruments.

Europe remains the most important market for UK exporters, accounting for 56per cent of total trade and 63 per cent of British goods exports in 2006. Theaverage value of goods exported per firm is higher for EU exports (£4.9m) thanfor non-EU exports (£1.0m).8 However, the great majority of exporters trade withnon-EU markets. Of the approximately 70,000 UK firms who exported goods in2007, 65,100 exported outside the EU, and 16,700 within the EU9 (some firmsexport both within and outside the EU, hence these do not sum to the total).

Studies suggest that exporting has a positive effect on the UK economy.Exporters and MNEs tend to have above average productivity, and as theyexpand, average UK productivity rises. Exporting also acts as a stimulus tocompetition, which encourages innovation and drives up productivity. Analysisof the Community Innovation Survey (CIS4) indicates that exporters tend to bemore active in R&D than other firms: approximately 26 per cent of UKestablishments export but when only manufacturing firms which are R&D activeare considered, this rises to 72 per cent.10 Other positive effects on UKproductivity from exporting arise from increased access to new ideas andtechnologies and exposure to superior organisational skills which may be directthrough exposure to overseas markets or inward investors or indirect viaknowledge spillovers.

Although there are benefits from participating in international markets, barriersexist to doing so and Government support aims to assist firms in overcomingthem. Analysis suggests that such support is best focused on: strengtheningsocial networks which underpin international trade and investment flows;providing access to information and advice which the private sector alone willnot or cannot provide both to inward investors and UK firms seeking to export;and strengthening the internationalisation capabilities of innovative and high-growth businesses which would not otherwise fulfill their potential withoutexploiting overseas opportunities.11

A sub-set of SMEs, referred to as ‘born globals’ fall into this group of firms.These firms tend to be knowledge-intensive or knowledge-based and their

Globalisation and the changing UK economy

17

8 HMRC UK Regional Trade in Goods Statistics, 2007Q3 (data for 2007 is provisional).

9 HMRC UK Regional Trade in Goods Statistics, 2007Q3 (data for 2007 is provisional).

10 Harris, R. and Cher Li, Q. (2006).

11 DTI Economics Paper No 18 sets out in more detail the economic benefits for the UK of increased international tradeand investment, the evidence on market failure and the cost-effectiveness of Government intervention.

7480-BERR-Global UK economy 31/1/08 17:34 Page 17

products are so specialised that there is a limited domestic market for them.They thus have to target the global market to obtain sufficient scale to benefitfrom R&D and innovation.12 These young and innovative SME exporterscontribute crucially to the flexibility which allows the economy to respond toeconomic shocks and changes to the UK’s comparative advantage. In time, someof these dynamic SMEs and ‘born globals’ of today will become the large firmsin profitable mature sectors of the future.

2.3 Explaining the changing shape of the UK economy

CLASSIFICATION AND OUTSOURCING

Part of the shift in the value added shares from manufacturing to services is dueto measurement difficulties. Increasingly, firms do not consider themselves to bein ‘services’ or ‘manufacturing’ but providing solutions for customers thatinvolve a combination of products and services. Manufacturing firms oftenprovide both a physical product and an accompanying or complementaryservice. Similarly, service industries and functions are becoming moreindustrialised due to technological developments (e.g., ICT). The question is howfirms that are changing their orientation report their business activity to theOffice for National Statistics (ONS). If a firm that was previously focusedprimarily on manufacturing but had a small but significant service activity (e.g.,a small retailing presence) chose to focus solely on services and changes itsreporting from wholly manufacturing to wholly services then the officialstatistics would overstate the switch away from manufacturing. While ONSattempt to overcome such problems by allowing reporting units below the levelof the firm, there remains some uncertainty around the data. BERR analysisshows that between 1998 and 2006 firms switching classification frommanufacturers to service providers accounted for 120,000 jobs more than thosefirms switching the other way. This figure, which accounts for around 10 per centof the fall in manufacturing employment during the period, represents an upperbound for the number manufacturing job losses which might be overstated byofficial statistics due to reclassification issues.

In addition to reclassification, there is a second, related, issue aroundmanufacturing outsourcing service activities (such as cleaning) that wouldpreviously have been carried out in-house. However, while research suggestsoutsourcing of this nature has been an important trend in the UK, evidencesuggests that most outsourcing from manufacturing to services took placebetween 1984 and 1990, prior to the period under consideration.13

Globalisation and the changing UK economy

18

12 Harris, R. and Cher Li, Q. (2007).

13 For example, Abramovsky, L. and Griffiths, R. (2007).

7480-BERR-Global UK economy 31/1/08 17:34 Page 18

CHANGING RELATIVE PRICES

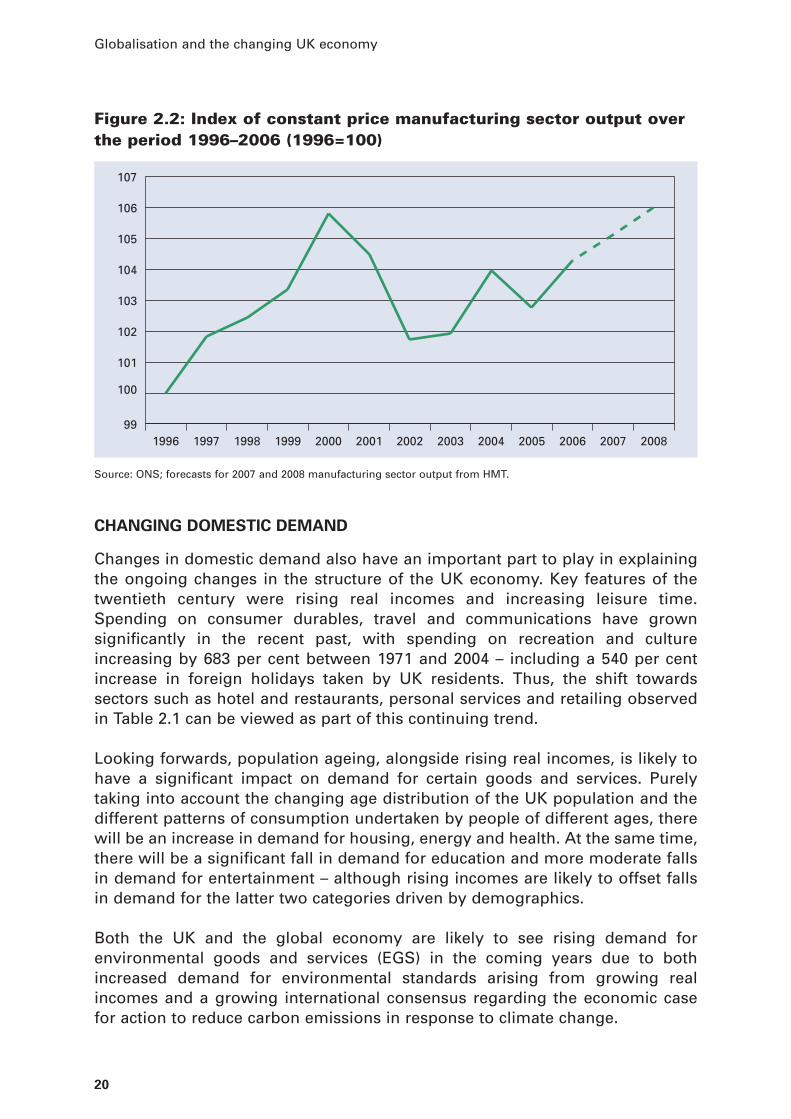

The shift towards services also reflects the decline in the average price ofmanufactured goods relative to services (Figure 2.1). This shift in relative priceshas occurred both as a result of global improvements in manufacturingproductivity driven by improvements in technology and related investment andas a result of the increased involvement of low-wage economies inmanufacturing rather than tradable services.14 As Figure 2.2 shows, the real(constant price) output of UK manufacturing (the value of output measured in1996 prices) has actually increased over the last 10 years. As discussed inchapter 1, there has been a trend towards manufacturing falling as a share ofoverall output in nearly all OECD economies over the last 10 years.

Figure 2.1: Changing relative services and goods prices, Jan 1996=100

Source: ONS.

80

90

100

110

120

130

140

150

160

Sep

–07

May

–07

Jan

–07

Sep

–06

May

–06

Jan

–06

Sep

–05

May

–05

Jan

–05

Sep

–04

May

–04

Jan

–04

Sep

–03

May

–03

Jan

–03

Sep

–02

May

–02

Jan

–02

Sep

–01

May

–01

Jan

–01

Sep

–00

May

–00

Jan

–00

Sep

–99

May

–99

Jan

–99

Sep

–98

May

–98

Jan

–98

Sep

–97

May

–97

Jan

–97

Sep

–96

May

–96

Jan

–96

All goods CPI inflation All services CPI inflation

Globalisation and the changing UK economy

19

14 This phenomenon of falling manufacturing relative prices is also driving the improvement in the terms of trade theUK has observed in recent years.

7480-BERR-Global UK economy 31/1/08 17:34 Page 19

Figure 2.2: Index of constant price manufacturing sector output overthe period 1996–2006 (1996=100)

Source: ONS; forecasts for 2007 and 2008 manufacturing sector output from HMT.

CHANGING DOMESTIC DEMAND

Changes in domestic demand also have an important part to play in explainingthe ongoing changes in the structure of the UK economy. Key features of thetwentieth century were rising real incomes and increasing leisure time.Spending on consumer durables, travel and communications have grownsignificantly in the recent past, with spending on recreation and cultureincreasing by 683 per cent between 1971 and 2004 – including a 540 per centincrease in foreign holidays taken by UK residents. Thus, the shift towardssectors such as hotel and restaurants, personal services and retailing observedin Table 2.1 can be viewed as part of this continuing trend.

Looking forwards, population ageing, alongside rising real incomes, is likely tohave a significant impact on demand for certain goods and services. Purelytaking into account the changing age distribution of the UK population and thedifferent patterns of consumption undertaken by people of different ages, therewill be an increase in demand for housing, energy and health. At the same time,there will be a significant fall in demand for education and more moderate fallsin demand for entertainment – although rising incomes are likely to offset fallsin demand for the latter two categories driven by demographics.

Both the UK and the global economy are likely to see rising demand forenvironmental goods and services (EGS) in the coming years due to bothincreased demand for environmental standards arising from growing realincomes and a growing international consensus regarding the economic casefor action to reduce carbon emissions in response to climate change.

99

100

101

102

103

104

105

106

107

2008200720062005200420032002200120001999199819971996

Globalisation and the changing UK economy

20

7480-BERR-Global UK economy 31/1/08 17:34 Page 20

BERR and DEFRA estimate15 that the UK EGS market will grow by 42 per centbetween 2005 and 2010, rising in value from £25bn to £34bn over the period.By 2015, the ESG market is expected to be worth £46bn. The sector is expectedto increase from 2.0 per cent of GVA in 2005 to 3.8 per cent of 2005 GVA by 2015.Particular sub-sectors driving this growth are expected to be energymanagement (£2bn in 1995, rising to £7bn by 2015), renewable energy (£1bn,rising to £8bn) and waste management (£8bn in 1995, rising to £17bn by 2015).

Global demand for environmental services is also expected to grow over thecoming years, with BERR and DEFRA estimating that the global market will growby approximately 33 per cent between 2005 and 2015 (from $600bn in 2005 tojust under $800bn by 2015). Opportunities exist in many of the new EU MemberStates, as well as emerging markets, in basic environmental infrastructures,such as water supply and waste management as these countries either continueto industrialise or need to clean up the legacy of previous industrialisation.

INCREASING TRADE OPENNESS AND THE CHANGING UK ECONOMY

While measurement difficulties around reclassification and outsourcing,technology-driven changes in relative prices and changing domestic demand allplay a part in explaining the changing structure of the UK economy, the changesin the UK economy have undoubtedly come in response, at least in part, to thechanging global economy.

As described in chapter 1, increasingly global value chains allow intermediateproducts to be sourced from abroad, leading to increased exports and importsof both intermediate inputs and final outputs. Such activity, whereby firms tradeinternationally within the supply chain, is often referred to as offshoring, and theextent to which it has affected a couple of leading UK sectors is considered indetail in Box 1. However, the fact that non-energy imported intermediate inputsas a share of total non-energy intermediate inputs was stable for the UK between1995 and 2000, as shown in Figure 1.5 in chapter 1 suggests that the increase inoffshoring has been limited and/or a very recent phenomenon. This, despite thestrong evidence that increased outsourcing (domestic trade in intermediates)has taken place in the UK, with intermediate consumption within manufacturingindustries in the UK increasing by almost 40 per cent between 1992 and 2004.The greatest proportion of these intermediate inputs come from themanufacturing sector itself – highlighting how production processes arebecoming increasingly fragmented.

Since 2000 there has been concern at a developing trend for service jobs tomove offshore. However, whilst the pace of service offshoring has increasedsince 2000, evidence suggests that the number of jobs being moved as a resultof restructuring16 or offshoring has been limited. Even in the occupationsregarded as most vulnerable to offshoring – IT and contact centres –

Globalisation and the changing UK economy

21

15 DTI/DEFRA (2006).

16 Rüdiger, K. (2007).

7480-BERR-Global UK economy 31/1/08 17:34 Page 21

employment growth over the period 2001 to 2004 was three times the overall UKemployment growth.17

There are reasons for expecting service offshoring to increase in the future.Whilst manufacturing offshoring is relatively mature, service offshoring is still arecent development. As with manufacturing, service providers are likely tocontinue to extend their use of global value chains to increase their efficiency.But there is likely to be a limit to this process. The costs and benefits ofoffshoring can be finely balanced and many employers are likely to seek to retainjobs onshore, especially as the cost of offshore locations rises. Many activities,requiring a wide range of skills and capabilities, either must be or are bestdelivered locally.

Whilst it is sometimes assumed that offshoring has a negative impact on theeconomy, the potential impact of offshoring on domestic employment andeconomic activity is uncertain. Jobs that move overseas are lost. But, the netimpact depends on how quickly people adjust and find new jobs and whetheroffshoring firms expand their home employment as a result of their improvedefficiency. Analysis so far suggests that offshoring hasn’t had a negative impacton overall UK employment.18 Studies also show no clear pattern as to howoffshoring affects productivity, with much depending on both sector and firm-specific characteristics.19

The UK has also been a beneficiary of offshoring by overseas companies. In2006, the UK was the second-largest recipient of FDI inflows globally and is asubstantial exporter of the services – business, financial, computing, informationand communications – that are most frequently offshored.

A wider academic debate remains ongoing regarding the relative importance ofincreased trade and improvements in technology in explaining the decline in theshare of manufacturing in many OECD economies. The seminal paper indisentangling the impact of trade from ‘internal factors’ was Rowthorn and Wells(1987), later updated in Rowthorn and Ramaswamy (1999), and Boulhol andFontagné (2007). Their main result was that trade with developing countries wasresponsible for less than a fifth of the relative decline of manufacturingemployment in the advanced economies (confirmed by Boulhol and Fontagné).Similarly, Hine and Wright (1998) found a limited impact of imports on UKemployment: around 6 per cent of job losses in the manufacturing sector overan earlier period (1981-91).

Whether as a result of increased trade or improvements in technology, it isundoubtedly the case that UK companies, particularly those engaged in

Globalisation and the changing UK economy

22

17 Heckley, G. (2005).

18 Hijzen, A. and Swaim, P. (2007).

19 Olsen, K. (2006).

7480-BERR-Global UK economy 31/1/08 17:34 Page 22

relatively high-volume, low-skilled activities, have had to adapt and respond inrecent years in order to remain competitive and take advantage of theopportunities created by globalisation, namely larger export markets, cheaperinputs, and improved access to technology.

Within manufacturing, there have been tremendous efforts to shift towardshigh-technology, high-skilled areas where low-wage economies are less able tocompete. While the overall fall in manufacturing employment has been welldocumented, within the sector, there has been a shift towards higher-skilledoccupations. Figure 2.3 shows that the majority of job losses have occurredamongst production occupations, with higher-skilled occupations, includingR&D and development, professional support and logistics and distribution,consequently now representing a much larger proportion of employment (R&Dand development employment actually increased in absolute terms between1994 and 2006).

Figure 2.3: Occupational activity of workers in manufacturing, (000s)

Source: ONS Labour Force Survey, 4 quarter averages.

Similarly, as Table 2.5 shows, qualifications data also point to considerableupskilling, with an increasing share of those working in the sector now holdingNVQ3 qualifications and the number of employees with degrees almostdoubling between 1994 and 2006.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

20061994

6.1%

10.2%

10.0%

16.3%

2.5%

Production

54.9%

50.1%

3.6%18.6%

9.4%11.5%7.0%

Logistics, distribution Sales and Marketing Support services, trades

Support services, professional R&D, development

Globalisation and the changing UK economy

23

7480-BERR-Global UK economy 31/1/08 17:34 Page 23

Table 2.5: Qualifications of those employed in the UK manufacturingsector

Proportion with NVQ level Proportion with degree

3 qualifications and above (%) or equivalent qualifications (%)

1994 2006 1994 2006

Production; support services, trades; Logistics and distribution 42.0 48.0 4.8 8.7

R&D, development; support services, professional; Sales and marketing 55.1 64.1 19.8 31.7

All employed in manufacturing 45.5 53.4 8.9 16.4

Source: ONS, Labour force survey, 4 quarter averages.

The picture of manufacturing increasingly focusing on more specialised, highervalue added areas, serving a more fragmented, global supply chain, is illustratedby case studies of the UK electronics and automotive industries (Box 1). The casestudies consider how the industries have adapted to remain competitive in thenew global supply chain through, for example, focusing on areas such asproduct development, design and systems integration, drawing on the UK’sworld-class academic research base.

BOX 1: CASE STUDIES – THE UK’S ELECTRONICS AND AUTOMOTIVE

INDUSTRIES

The restructuring of the UK’s electronics and automotive industries in recentyears helps illustrate how UK industry is continuing to respond to thechallenges and opportunities of globalisation.

The UK electronics manufacturing industry20, despite experiencing a declinein output since the peak of the global ICT boom in 2000, remains the fifth-largest in the world, accounting for 7 per cent of manufacturing GVA in 2006,and 6 per cent of manufacturing employment. Similarly, the UK’s automotivesector continues to employ around 180,000 people and accounted for 6 percent of manufacturing GVA in 2006. Both sectors have transformedthemselves in recent years in order to command a place in a global valuechain which has been increasingly influenced by both the entry of low-wagecompetition and technological change which has changed the nature of theproduction process and facilitated the fragmentation of the supply chain.

The global electronics sector, in particular, has been transformed by theincreased separation of activities into modules which, in turn, has been madepossible by rapid progress in standardisation, and in the development ofinterfaces for both production stages and components, based upon commonprotocols. The outsourcing to low-wage economies of electronic hardware,particularly components, is especially attractive given the high value-to-bulkratios for these goods.

Globalisation and the changing UK economy

24

20 As defined by Standard Industry Classification (SIC) codes 30 (office equipment & computers), 32 (components), 33(instrumentation).

7480-BERR-Global UK economy 31/1/08 17:34 Page 24

The ability to standardise has given rise to the growth of specialist electronicmanufacturing services (EMS)21 firms who increasingly manufacture on behalfof so-called original equipment manufacturers (OEMs) such as IBM, HewlettPackard and Ericsson. Such contracting out allows OEMs to focus on highvalue added activities such as design and marketing, while the EMS firms,who often supply to numerous competing OEMs, can exploit huge globaleconomies of scale which have facilitated continuing productivityimprovements and falling global prices for semiconductors and circuit boards.

In response to these forces, the UK electronics industry has increasinglyfocused on the product development, design, systems integration andprocess control stages of the supply chain, supported by a world-classacademic research base. The UK accounts for over 40 per cent of Europe’sindependent electronic design by turnover, with many small, innovation-intense companies, some of which have global reputations in their niches.Alongside this, the UK has continued to prosper in low volume, high skill,bespoke areas, for example the scientific and precision engineering sector,where specialised technologies and highly bespoke products, oftencustomised to small local markets, mean that pressures towards verticalintegration and restructuring have not been so prevalent. Finally, supplychain disintegration has led to an increased role for global logisticsoperations, including localisation (which ensures the product is customisedand packaged to meet local requirements), inventory control and distribution,with the UK playing a particularly active role.

The auto industry is the historical leader in terms of the development of ahighly detailed division of labour, process efficiency, outsourcing, and supplychain restructuring.

As in the electronics sector, modularisation has played a key role in reducingcomplexity and facilitating supply chain restructuring in auto manufacturing.Global supply chains have evolved whereby vehicle manufacturers (OEMs)tend to focus on product development and design, assembly and marketingwhile buying in raw materials, a high proportion of components, sub-assemblies and systems, specialist electronic technologies, and design andengineering services. Vehicle manufacturers tend to be supplied by a threetier supply chain:

Tier 1 firms supply whole systems directly to OEMs. They design andmanufacture complex systems and modules such as powertrain, interiorsand bodywork and can integrate a wide range of products and servicesincluding R&D and product development.

Tier 2 firms, on the other hand, supply minor sub-assembly components orsupport services to tier 1 suppliers or OEMs.

Globalisation and the changing UK economy

25

21 Also known as Contract Manufacturing Services (CMS) companies.

7480-BERR-Global UK economy 31/1/08 17:34 Page 25

The growth in the production and export of knowledge-intensive services isrelated to the ongoing transformation in manufacturing, discussed above. TheWork Foundation argue that manufacturing is itself responsible for our successin exporting knowledge services, with the manufacturing sector generatingadditional technical business services, royalties and licenses and trade-relatedjobs.22

Tier 3 firms supply raw materials, generic components and services usuallyto higher tier firms. Some tier 3 firms, such as materials suppliers, can belarge multi-nationals, while others, including component suppliers, tend to besmaller local operations.

Within this framework, first tier suppliers no longer just supply componentsand sub-systems, but have increasingly become partners in the innovationand production processes of vehicle manufacturers, carrying out about halfof all auto R&D activity in leading auto manufacturing countries. OEMsrecognise that they do not necessarily have all the knowledge and expertiseneeded to construct modern cars on their own.

But developments in the auto supply chain have not had as radicalimplications in terms of vertical integration as for the electronics industry.This is in part because labour costs are not a predominant component of costin this highly capital-intensive industry. Even where low cost economies doenjoy absolute cost advantages, relatively high transport costs as aproportion of production costs may mean these advantages do not translateinto increased trade between regions. Moreover, the functionality ofelectronic products is largely delivered via electronic technology, whereas acar has to integrate diverse components and fundamentally differenttechnologies. Innovation in vehicle design is increasingly dependent onelectronics and software control systems, which have to be integrated withmechanical components.

Within the UK, more than 40 companies manufacture vehicles, ranging fromvolume car and van makers, to specialist niche players manufacturing highvalue and luxury vehicles. In addition, there are over 2,600 companiesinvolved to some extent in the supply chain. While overall employment in theUK automotive industry has fallen in recent years, in line with many OECDeconomies, there are many positive stories regarding the UK auto sector’sresponse to globalisation. For example, Ford now sources 25 per cent of itsglobal engine requirement from the UK, with its Dagenham site now itsglobal diesel engine centre of excellence. Elsewhere, Nissan Sunderland’splant has become Europe’s most productive car plant, while Toyota(Burnaston) and Honda (Swindon) are also in Europe’s top 10 mostproductive car factories. The UK’s volume truck builder, Leyland Trucks,operates one of Europe’s largest and most advanced plants at Leyland.

Globalisation and the changing UK economy

26

22 Brinkley, I. (2007).

7480-BERR-Global UK economy 31/1/08 17:34 Page 26

Thus the expansion of the UK’s service sector has risen not solely throughdomestic demand, but through a focus on tradable, knowledge-intensiveservices in which low-wage economies with less skilled labour are unable tocompete. Figure 2.4 shows that the UK has a greater proportion of value addedarising from knowledge-intensive services (or high-growth services as the OECDdescribes them) than any other major OECD economy except the US.

Figure 2.4: The sectoral composition of output (% of total valueadded, 2003)

Source: OECD Economic Survey of the UK.

Knowledge-intensive services go hand-in-hand with increased innovation inservices. The latest data from the Community Innovation Survey suggests thatbusiness service firms have a high proportion of innovation active firms – over60 per cent (Figure 2.5), only slightly lower than in engineering-basedmanufacturing. Business services are particularly strong service and processinnovators and also score highly as ‘wider innovators’, which includes firms whohave made major changes in management practices, business structure,organisation or marketing strategy.

0

5%

10%

15%

20%

25%

USUKFranceOECDDEUItalyCanadaJapanFinlandIreland

Post and Telecommunications Finance and Insurance

Knowledge intensive services

Business Activities

Globalisation and the changing UK economy

27

7480-BERR-Global UK economy 31/1/08 17:34 Page 27

Figure 2.5: Types of innovation activity by business service firms,2005

Source: Community Innovation Survey (2005).

Both manufacturing and services have benefited from an increase in ‘intangibleinvestment’ in recent years. The phrase refers to a wide range of entities underthree broad headings: computerised information (software and databases),innovation-related assets (including research and development in natural andsocial science, mineral exploration and design) and ‘economic competences’such as brand-building, firm-provided training and management consulting.

Research23 suggests that intangible investment has increased rapidly in the UKover the last few decades, both as a proportion of overall output and in relationto tangible investment. Figure 2.6 shows the growing importance of intangibleinvestment in the economy, rising from around 6 per cent of output in the 1970sto 13 per cent in 2004, in which time some £130.8bn was invested in intangibles.This was more than 1.2 times the spend on tangible investment, up from 0.4times the spend on tangible investment back in 1970.

0

10%

20%

30%

40%

50%

60%

70%

80%

Widerinnovator

ProcessInnovator

ServicesInnovator

GoodsInnovator

Innovationactive

Retail and Distribution Engineering-based Manufacturing Business Services

Globalisation and the changing UK economy

28

23 Marrano, M., Haskel, J. and Wallis, G. (2007).

7480-BERR-Global UK economy 31/1/08 17:34 Page 28

Figure 2.6: Intangible investment as a percentage of output

Source: HMT estimates.

According to the OECD, thanks to the change in the orientation of the UKeconomy in the late 1970s and early 1980s towards more skilled and innovativeareas, by the mid-1990s the UK had already developed a specialisation in sectorsthat were less exposed to competition from emerging low-wage economies.They calculate that the UK’s specialisation24 is negatively correlated with that ofthe dynamic Asian economies, implying little head-to-head competition, withglobalisation ‘more an opportunity than a threat’. In short, the UK’s pattern ofeconomic specialisation seems to have already been poised to benefit fromglobalisation, according to the OECD.

THE ROLE OF FDI AND MIGRATION IN DRIVING UK PRODUCTIVITY GROWTH

AND COMPETITIVENESS

Alongside increased openness to goods and services trade, increased capitalflows (particularly FDI) and changes in the nature of migration into the UK haveboth played important roles in shaping the UK economy and helping to raiseproductivity and competitiveness.

The UK continues to be an attractive destination for inward investment. Figure 2.7shows that while flows into the UK fell following the end of the dot-com boom atthe start of the century, they have since recovered. The US remains by far thesingle most important source of inward investment, although its share of inwardinvestment has fallen over the past 10 years. The EU25’s share over this periodhas risen, to over 50 per cent in 2006, highlighting its importance as a source ofFDI. In 2006, the UK was the second only to the US in terms of FDI inflows.

0

2%

4%

6%

8%

10%

12%

14%

16%

200420022000199819961994199219901988198619841982198019781976197419721970

Brand equity Firm-specific resources

Computerised information

Scientific R&D Non scientific R&D

Globalisation and the changing UK economy

29

24 Calculated as revealed symmetric comparative advantage.

7480-BERR-Global UK economy 31/1/08 17:34 Page 29

Figure 2.7: Flow of net inward FDI in UK25

Source: ONS.