22

UNITED HOSPITAL FUND Coordinating Medicaid and the Exchange in New York Danielle Holahan

U N I T E D H O S P I T A L F U N D

Coordinating Medicaidand the Exchange in New York

Danielle Holahan

Support for this work was provided by the New York State Health Foundation (NYSHealth).The mission of NYSHealth is to expand health insurance coverage, increase access to high-qualityhealth care services, and improve public and community health. The views presented here arethose of the authors and not necessarily those of the New York State Health Foundation or itsdirectors, officers, or staff.

Copyright 2011 by United Hospital FundISBN 1-933881-16-X

Free electronic copies of this report are available atthe United Hospital Fund’s website, www.uhfnyc.org.

OFFICERS

J. Barclay Collins IIChairman

James R. Tallon, Jr.President

William M. Evarts, Jr.Patricia S. LevinsonFrederick W. Telling, PhDVice Chairmen

Sheila M. AbramsTreasurer

Sheila M. AbramsDavid A. GouldSally J. RogersSenior Vice Presidents

Michael BirnbaumDeborah E. HalperVice Presidents

Stephanie L. DavisCorporate Secretary

DIRECTORS

Richard A. BermanJo Ivey Boufford, MDRev. John E. CarringtonPhilip ChapmanJ. Barclay Collins IIRichard CottonRichard K. DeSchererWilliam M. Evarts, Jr.Michael R. Golding, MDJosh N. KuriloffPatricia S. LevinsonHoward P. MilsteinSusana R. Morales, MDRobert C. OsbornePeter J. PowersKatherine Osborn RobertsMary H. SchachneJohn C. SimonsHoward SmithMichael A. Stocker, MD, MPHMost Rev. Joseph M. SullivanJames R. Tallon, Jr.Frederick W. Telling, PhDMary Beth C. Tully

Howard SmithChairman Emeritus

HONORARY DIRECTORS

Donald M. EllimanDouglas T. YatesHonorary Chairmen

Herbert C. BernardJohn K. CastleTimothy C. ForbesBarbara P. GimbelRosalie B. GreenbergAllan Weissglass

United Hospital Fund

The United Hospital Fund is a health services researchand philanthropic organization whose mission is to shapepositive change in health care for the people of New York.We advance policies and support programs that promotehigh-quality, patient-centered health care services that areaccessible to all. We undertake research and policy analysisto improve the financing and delivery of care in hospitals,health centers, nursing homes, and other care settings. Weraise funds and give grants to examine emerging issues andstimulate innovative programs. And we work collaborativelywith civic, professional, and volunteer leaders to identifyand realize opportunities for change.

The Health Insurance Exchange is a central con-cept of the Affordable Care Act (ACA), and, asthe rubber hits the road with health care reform,decisionmakers are moving from concept topractice. Getting the Exchange to mesh with themany other moving parts in New York’s healthcare system — particularly the Medicaid pro-gram — will require great attention to detail,without losing sight of the broader goals of re-form.

With support from the New York StateHealth Foundation, the Fund is preparing a se-ries of reports about health care reform and theExchange. An earlier report by Peter Newell andRobert Carey examined the first set of gover-nance and organizational choices states mustmake in designing their exchanges. This reportexamines in detail the organizational improve-ments necessary for improving and integratingcurrent Medicaid processes for eligibility and en-rollment, information technology, and communi-cations with the new Exchange. It was prepared

by Danielle Holahan, former co-director of theFund’s Health Insurance Project, who recentlymoved into a leadership role with New YorkState’s health care reform team, focusing on pre-cisely these issues. Forthcoming reports in theseries will consider the possible merging of theindividual and small group markets, and whatrole the Exchange will play in defining productsand plan participation in the commercial market.

The Fund’s goal in preparing these reports isto help the State and stakeholders involved withthe planning and implementation of the Ex-change. As we grapple with the complex chal-lenges of reform, we are reminded of theimportance of the myriad decisions that promiseto improve the way millions of New Yorkers ob-tain coverage.

JAMES R. TALLON, JR.PresidentUnited Hospital Fund

Coordinating Medicaid and the Exchange 1

Foreword

Introduction

One of states’ greatest challenges with the im-plementation of federal health reform will be tointegrate Medicaid with their new Health Insur-ance Exchanges. Because Exchanges are ex-pected to be the primary place individuals andsmall firms will go to seek health insurance cov-erage in 2014 and beyond, it is critically impor-tant that the enrollment experience works wellfor them. Several improvements will be neces-sary in meeting these challenges: streamliningMedicaid’s historically complex eligibility andenrollment processes; managing transitions be-tween sources of coverage as circumstanceschange; and significantly upgrading state infor-mation technology systems and communicationswith consumers, in order to provide superior cus-tomer service for all, no matter where they fallon the coverage continuum. New York has astrong foundation on which to build, as a long-time leader in eligibility and enrollment policiesand, more recently, as a recognized leader in in-formation technology for state Exchanges. Stateswill receive significant federal aid in this workthrough formal guidance and technical and fi-nancial assistance to support this effort. The taskis enormous, so states will need to tackle it pieceby piece. But if the effort is great, so are the pos-sible measures of success: a major step towarduniversal coverage, including an estimated 1.2million or more newly insured New Yorkers; andimprovement of the way millions more NewYorkers buy coverage — both those who will benewly subsidized and those who purchase cover-age through the Exchange at full premium.

The Affordable Care Act (ACA) envisions ac-cess to affordable care for all Americans, astreamlined eligibility and enrollment process toobtain coverage, and seamless integration be-tween Medicaid and the Exchange to ensuresmooth transitions between sources of coverageas a person’s circumstances change over time. Toachieve the goal of seamlessness between Medi-caid and the Exchange, there are five key areas

for coordination, each with multiple considera-tions: eligibility and enrollment; renewals andtransitions; information systems; consumer com-munications; and challenges associated withaligning the plans, networks, and benefits of-fered. This paper explores the issues associatedwith these coordination challenges and identifiesoptions for New York as it considers how to bestapproach the integration of coverage optionsalong the continuum from fully subsidized pub-lic coverage to partially subsidized and unsubsi-dized private coverage offered in the Exchange.There will still be an insurance market outside ofthe Exchange, but discussion of coordinationwith the non-Exchange market is beyond thescope of this paper.

Eligibility and Enrollment

The ACA calls for a streamlined, user-friendlyapproach to health insurance enrollment andmakes a significant effort to ensure the sameconsumer experience regardless of the type ofcoverage for which a person is eligible.1 This sys-tem envisions that consumers will apply for cov-erage using a streamlined application form thatwill be the same for Medicaid and the Exchange.Consumers will be offered multiple accesspoints — on the web, by phone, by mail, and inperson — to apply for coverage and the option tostart via one avenue and complete the processthrough another. Both Medicaid and the Ex-change will screen for eligibility for all subsidizedcoverage options: Medicaid, Children’s HealthInsurance Program (CHIP), federally subsidizedprivate coverage available in the Exchange, and aBasic Health Plan (BHP), if the state pursuesthis option. States will be required to coordinateeligibility determination and enrollment betweenMedicaid and the Exchange. In this vein, in-come eligibility for Medicaid and subsidized cov-erage in the Exchange will be determined using amodified adjusted gross income (MAGI) stan-dard. (See accompanying box for a description of

2 United Hospital Fund

1 Patient Protection and Affordable Care Act, Sections 1413 and 2201; CMS/OCIIO 2010.

this MAGI standard.) Lastly, states will be en-couraged to verify eligibility factors through elec-tronic matches with state and federal databases,instead of relying on paper documentation. Thefederal vision is that consumers with incomefrom 0 to 400 percent of the federal poverty level(FPL) will have the same enrollment experi-ence.2

Within the ACA’s federal requirements for el-igibility and enrollment, there are a number ofareas of state discretion. First, New York may de-cide to use an application modeled on its currentpublic program application, Access New York. Ifthe state does so, it would need to eliminate un-needed questions and simplify it further to makeit so straightforward that consumers can accu-rately complete it without assistance. Second,New York has the option of offering a BHP, asubsidized coverage option for people with in-come above the Medicaid level (138 percent ofFPL) and below 200 percent of FPL, in lieu offederally subsidized coverage through the Ex-change. Offering a BHP would have several ef-fects. It would help smooth out differences inbenefits and cost sharing between Medicaid andExchange plans for individuals at this incomelevel because of federal requirements for theBHP. However, there would still be benefit andcost sharing differences between BHP and Ex-

change products, so there would still be a transi-tion — albeit less sharp — at 200 percent ofFPL instead of 138 percent of FPL. Also, a BHPwould add a third income eligibility cutoff, in ad-dition to Medicaid at 138 percent of FPL andsubsidies at 400 percent of FPL, and thereforecreate a third program requiring coordination.

A third significant decision facing the statepertains to the level of coordination versus inte-gration between Medicaid and the Exchange.The ACA requires states to “coordinate” enroll-ment between these entities. This could meanmerely collecting and sharing informationneeded for eligibility determinations, or it couldmean full integration of eligibility and enroll-ment processes for Medicaid and subsidized cov-erage options in the Exchange. Either methodwould require real-time connections and coordi-nation between entities to meet federal expecta-tions.

The ACA permits the Exchange to contractwith the state’s Medicaid agency to conduct eli-gibility determinations for all subsidized coverageoptions, which would align with the full integra-tion approach. Having integrated processeswould not, however, preclude making certain ex-ceptions. For example, some individuals applyingfor coverage through the Exchange will not be el-igible for or interested in subsidies and therefore

Coordinating Medicaid and the Exchange 3

2 For a more detailed discussion of these issues, see Bachrach et al. 2011.

Modified Adjusted Gross Income (MAGI). The ACA establishes a new, simplified income standard

for Medicaid and Exchange eligibility determination. Beginning January 1, 2014, states will be required

to use a modified adjusted gross income standard, or MAGI, to determine Medicaid eligibility for most

nonelderly, non-disabled people. This income standard consists of adjusted gross income, as defined in

the tax code, plus foreign income and tax-exempt interest. The new MAGI formula eliminates income

disregard adjustments and therefore the need for applicants to report and provide paper verification

of expenses as part of the Medicaid eligibility determination process.

Individuals who are elderly, disabled, medically needy, or eligible for Medicaid through other pro-

grams, such as cash assistance, will have their income calculated according to the traditional Medicaid

formula, instead of the more streamlined MAGI test, and will continue to be subject to an asset test.

In this paper we refer to “MAGI” and “non-MAGI” populations to distinguish between those whose

income eligibility will be determined using the more streamlined income standard and those whose

eligibility will continue to be determined using traditional methods.

HHS will define the methods for calculating family size and household income for the MAGI stan-

dard in guidance that is expected in the summer of 2011. (Patient Protection and Affordable Care Act,

Section 2002, and Internal Revenue Code of 1986 36B(d)(2)).

4 United Hospital Fund

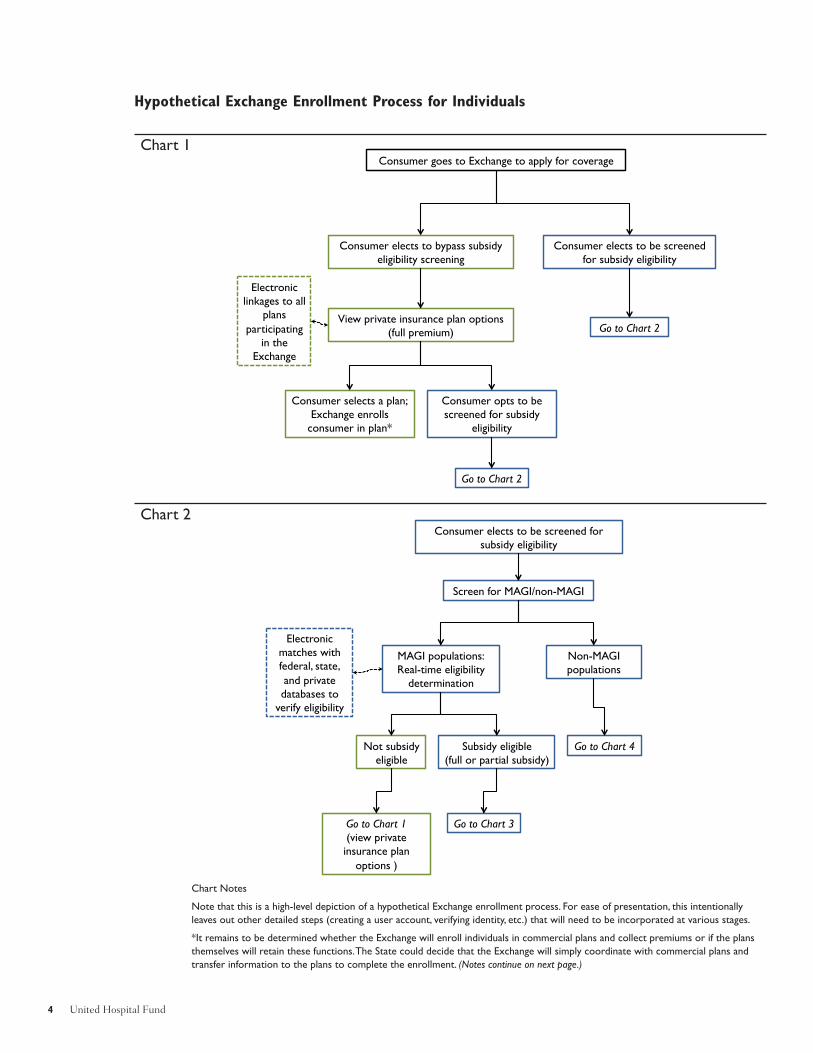

Consumer selects a plan; Exchange enrolls

consumer in plan*

View private insurance plan options (full premium)

Electronic linkages to all

plans participating

in the Exchange

Consumer opts to be screened for subsidy

eligibility

Consumer goes to Exchange to apply for coverage

Consumer elects to bypass subsidy eligibility screening

Consumer elects to be screened for subsidy eligibility

Go to Chart 2

Go to Chart 2

Hypothetical Exchange Enrollment Process for Individuals

Consumer elects to be screened for subsidy eligibility

Screen for MAGI/non-MAGI

MAGI populations: Real-time eligibility

determination

Non-MAGI populations

Electronic matches with federal, state, and private databases to

verify eligibility

Not subsidy eligible

Subsidy eligible (full or partial subsidy)

Go to Chart 3

Go to Chart 4

Go to Chart 1 (view private insurance plan

options )

Chart 1

Chart 2

Chart Notes

Note that this is a high-level depiction of a hypothetical Exchange enrollment process. For ease of presentation, this intentionally

leaves out other detailed steps (creating a user account, verifying identity, etc.) that will need to be incorporated at various stages.

*It remains to be determined whether the Exchange will enroll individuals in commercial plans and collect premiums or if the plans

themselves will retain these functions. The State could decide that the Exchange will simply coordinate with commercial plans and

transfer information to the plans to complete the enrollment. (Notes continue on next page.)

Coordinating Medicaid and the Exchange 5

MAGI populations, subsidy eligible: shown subsidized plan options and premium requirements (Medicaid,

CHIP, subsidized private)

Consumer selects a plan; Exchange enrolls consumer in plan*

Electronic linkages to all

plans participating in the Exchange

Exchange screens for other benefit program eligibility

Non-MAGI populations: eligibility determination

Eligible. Consumer enrolled in

fee-for-service Medicaid

Eligible. Consumer shown plan

options; makes selection. Exchange

enrolls consumer in plan

Electronic matches with federal, state,

and private databases to verify

eligibility

Exchange screens for other benefit program eligibility

Other eligibility determination steps,

as needed

Electronic linkages to

plans serving elderly and

disabled populations

Not Medicaid eligible

Go to Chart 1 (view private insurance plan

options )

Evaluate for subsidy eligibility

Chart 3

Chart 4

Hypothetical Exchange Enrollment Process for Individuals (continued)

Chart Notes (continued)

The federal and state databases used to verify eligibility will include the Internal Revenue Service (IRS), Social Security Administration

(SSA), Department of Homeland Security (DHS), Department of Vital Statistics, and State Wage File; private databases could include

the Work Number, eFIND, or similar databases containing employer information.

With regard to enrollment of beneficiaries into FFS Medicaid, it is worth noting that the Medicaid Redesign Team provisions adopted

in the 2011-12 budget envision enrolling additional populations in managed care over time (MRT Recommendation number 1458).

For those ineligible for all Exchange coverage options due to immigration status (i.e., undocumented noncitizens), the Exchange could

provide information about hospital financial assistance programs and Emergency Medicaid, or test eligibility for these programs.

will not need or want to answer detailed eligibil-ity screening questions. New York could consideran approach in which all individuals who applyfor coverage through the Exchange are given theoption of bypassing the income eligibility screen-ing and going directly to plan choices and pre-mium information. Others would be screened foreligibility for subsidies, and, depending uponwhat they are eligible for, given their choice ofMedicaid or subsidized plans and associated pre-mium requirements. Other considerations forthese enrollment systems include the need toscreen for eligibility for non-MAGI populations(e.g., elderly and disabled people) as well as theability to screen for eligibility for other publicbenefit programs (e.g., Food Stamps, cash assis-tance). However, these provisions would likelybe included in later stages of system design. (Seeaccompanying charts.)

In its Exchange planning materials, New Yorkhas stated that it would prefer to maximize theuniformity in Medicaid and Exchange programrules.3 However, the state’s ability to reformMedicaid’s rules and integrate them with the pri-vate coverage options offered in the Exchangewill require resolution of issues with four federalrules:

1. MAGI definition. States require guidancefrom the Centers for Medicare and MedicaidServices (CMS) on how Medicaid will apply theMAGI definition — specifically, what sources ofincome will “count” and how family size shouldbe calculated in 2014 — because currently thereare differences between Medicaid and federalincome tax definitions of these factors.

2. Age of data. States require guidance or awaiver from CMS that will allow them to use

older tax data to meet Medicaid’s point-in-timeincome requirement. This would enable states tosimplify income verification strictly through taxdata matching for Medicaid, as is expected forsubsidy eligibility determination.

However, CMS has suggested that tax datawill likely not suffice as the sole proof of incomefor Medicaid or subsidy purposes. This is be-cause the IRS is expected to use current incomedata to set repayment penalties, so individualswho receive subsidized coverage based on old in-come data could potentially face significantpenalties. States would need to consider alterna-tive verification sources for more current incomeinformation. Alternatives include private verifica-tion sources, such as the Work Number oreFIND, which contain current wage and salaryinformation compiled from national datasets ofemployers and are already used by certainstates,4 and paper documentation (e.g., paystubs) as a last resort.

3. Medical support provisions. States requireguidance from the federal Department of Healthand Human Services (HHS) or sponsorship of anamendment to the federal statute allowing statesto apply the ACA’s individual mandate in lieu ofmedical support enforcement provisions. TheACA mandates that all individuals obtain insur-ance for themselves and their dependents; med-ical support provisions require states to askMedicaid applicants about absent parents/spouses who may be legally responsible to pro-vide this support.

4. Federal Medical Assistance Percentage(FMAP) claims. States will need resolution ofissues related to enhanced federal matchingfunds for newly eligible beneficiaries. Specifi-

6 United Hospital Fund

3 New York State Comments to the Office of Consumer Information and Insurance Oversight, Department of Health and Human

Services Regarding Exchange-Related Provisions in Title I of the Patient Protection and Affordable Care Act (HHS-OS-2010-0021-

0001), submitted in October 2010, and New York State Department of Insurance Planning Grant Application.

4 Nationwide, over 2,000 employers participate in the Work Number, including 85 percent of the federal civilian workforce. The Work

Number has over 190 million employment and income records on file, including 50 million current employment records. In New

York, the Office of Temporary and Disability Assistance (OTDA) uses the Work Number in eligibility determinations and program in-

tegrity initiatives (http://www.theworknumber.com/SocialServices/eSeminars/NewYork.asp). For more detail on state experiences

with verification sources, see Edwards et al. 2009.

cally, states will need alternatives to requiring de-termination of eligibility under both old and neweligibility rules for claiming enhanced federalmatching funds.5 CMS has indicated its desireto ease this process for states to align with sim-plification goals.

Conversations between states and CMS onthese topics are ongoing, and formal guidance onthem is expected in the spring and summer of2011.

Other Issues to Consider

There are three other enrollment-related issuesto address when integrating new Exchange cov-erage options with existing programs andprocesses. First, New York will have to decidewhether to continue certain programs for peoplewith income above 138 percent of FPL or dis-continue them in lieu of federally subsidizedcoverage in the Exchange. If the state decides toretain all programs, people with income of 139–400 percent of FPL could be found eligible formultiple programs. These include federal subsi-dies, Family Health Plus (FHP), CHIP, Medi-caid spend-down, Medicaid buy-in for theworking disabled, FHP premium assistance,COBRA, the AIDS Drug Assistance Program,and potentially a BHP. The state’s eligibility sys-tem would need to screen for all programs andnotify individuals of their options. Screening forother program eligibility could occur separatelyfrom the Medicaid and Exchange subsidy eligi-bility determination process, so long as con-sumers are notified of other potential programeligibility.

Second, it is also possible that differentmembers of the same family will be eligible fordifferent sources of coverage based on their ageor immigration status, or that some family mem-bers could be ineligible for all Exchange options

due to their immigration status (e.g., undocu-mented noncitizens). Depending upon plan par-ticipation in various programs, different familymembers may be enrolled in different plans.New York will need to consider ways to best co-ordinate enrollment and renewal for families, in-cluding aligning coverage dates for all familymembers across plans to ease the renewalprocess. And, for those who are not eligible forany coverage through the Exchange, the Ex-change could provide information about hospitalfinancial assistance programs and EmergencyMedicaid or test eligibility for them.

Third, the Exchange will also have to collectinformation on available employer-sponsored in-surance (ESI) to determine eligibility for federalsubsidies, and exemptions from the individualmandate. Individuals with access to ESI thatmeets the ACA’s requirements for affordabilityand minimum essential benefits will not be eligi-ble for federal subsidies toward coverage in theExchange.6 New York will need to revise theprocesses it now uses to evaluate ESI in order toassess cost effectiveness for premium assistanceand third-party liability.

Coverage Renewals and Transitions

Another critical aspect to ensuring seamless cov-erage is to have processes in place to collect up-dated eligibility information as individuals’circumstances change during the year or at an-nual renewal. A recent analysis of survey dataprojects that 50 percent of low-income adults arelikely to experience a shift in eligibility fromMedicaid to an Exchange plan or vice versawithin a year (Sommers and Rosenbaum 2011).This level of fluctuation necessitates careful con-sideration of options for easing transitions orguaranteeing periods of eligibility regardless ofchanges in circumstances.

Coordinating Medicaid and the Exchange 7

5 See Bachrach et al. 2011 for more detailed discussion of issues related to these federal rules.

6 Note that individuals with access to grandfathered ESI plans will also be ineligible for subsidized coverage in the Exchange even if

this coverage is less comprehensive than the ACA’s required minimum essential coverage, so long as the employer makes a sufficient

contribution toward the coverage.

As outlined in the ACA, individuals who en-roll in a qualified health plan through the Ex-change will have a 12-month enrollment period,with a requirement to notify the Exchange ifthey have changes in circumstances (such as in-come or family size) during this period. This no-tification of changes is important because underthe law, individuals with higher than expectedincomes at year-end will have to repay excess ad-vanced subsidies, up to a maximum between$600 and the full excess amount, depending ontheir incomes.7 In addition, a change in eligibilitycould require a change in health plan, if differ-ent plans participate in Medicaid and subsidizedprivate coverage.

New York’s enrollment system will need to beset up to redetermine eligibility or adjust a sub-sidy level when an individual reports a change incircumstances. Furthermore, if a person’s eligi-bility change requires a change in program (e.g.,from subsidized private coverage to Medicaid orvice versa), the system will need to notify the in-dividual of new plan options and facilitate enroll-ment into the plan of choice. The processeswould be similar at annual renewal: redetermina-tion of eligibility, assessment of plan options, andfacilitated enrollment.

Due to differences in the timing of enroll-ment in Medicaid, CHIP, FHP, and subsidizedprivate coverage, when individuals shift amongthese coverage options they would likely experi-ence gaps in coverage. Traditionally, enrollmentin Medicaid is effective at the point an eligibilitydetermination is made, with three months of

retroactive coverage. In CHIP and FHP, enroll-ment is effective when an individual is enrolledin a plan, usually the first day of the month fol-lowing application. For commercial coverage, en-rollment is effective upon the plan’s receipt ofpremium payment. Shifts between plans, there-fore, would likely mean a gap in coverage. NewYork will want to consider options to eliminatesuch coverage gaps and ease transitions betweenprograms, such as extending Medicaid until Ex-change coverage is effective or vice versa.

New York could also consider pursuing guar-anteed 12-month eligibility for individuals en-rolled in subsidized private coverage through theExchange. (In fact, the state indicated its inter-est in this policy in its comments to HHS in Oc-tober 2010.8) This would align eligibility periodsacross Medicaid and subsidized private coveragebecause New York already guarantees 12-monthcontinuous eligibility to children in Medicaidand plans to implement this provision for adultslater in 2011.9,10 However, such a policy wouldrequire a waiver of the reporting requirementsand associated penalties discussed above. Absentsuch a waiver, New York should consider aligningthe reporting requirements between Medicaidand subsidized private coverage so that all MAGIpopulations follow the same reporting rules.

Information Systems

Modern information systems are a critical aspectof an accessible and consumer-friendly eligibility

8 United Hospital Fund

7 These repayment amounts were increased in December 2010 legislation from a flat cap of $250/individual to $600–$3,500, varying

by income, for those with incomes below 500 percent of FPL (Section 208 of PL 111-309). More recent legislation, PL 112-9, signed

into law by President Obama in April 2011, increased the maximum subsidy repayment amounts again, as follows: $600 for individuals

with incomes less than 200 percent of FPL, $1,500 for individuals with incomes between 200 and 300 percent of FPL, and $2,500 for

individuals with incomes between 300 and 400 percent of FPL. PL 112-9 eliminated the cap on the maximum subsidy repayment

amount for individuals with incomes of 400 percent of FPL and above.

8 See page 19 of “New York State Comments to the Office of Consumer Information and Insurance Oversight, Department of Health

and Human Services Regarding Exchange-Related Provisions in Title I of the Patient Protection and Affordable Care Act (HHS-OS-

2010-0021-0001),” submitted in October 2010.

9 New York’s proposal to implement 12-month continuous eligibility for adults in Medicaid was approved by CMS in February 2010

and is expected to be implemented in 2011.

10 A related issue pertains to Medicaid recoveries, which would be expected to change with the implementation of continuous eligibil-

ity. Once the 12-month continuous eligibility policy is in place for adults, the state would presumably no longer pursue recoveries due

to a change in eligibility during the 12-month period. Furthermore, the state assumption of Medicaid administration by 2016 will also

allow for more uniformity in Medicaid recoveries, which have traditionally varied by county.

and enrollment process and necessary for ensur-ing seamless coordination between Medicaidand the Exchange. These systems must accom-modate a high volume of applicants with variedtechnical skills and language abilities; interfacewith numerous federal, state, private, and em-ployer databases to verify eligibility information;enable real-time eligibility determination; inter-face with participating health plan systems to en-roll participants; store consumer information for re-use at renewal; process changes in enrolleecircumstances to re-determine eligibility andchange in health plan, if necessary; and notifyapplicants of eligibility, renewal, or other infor-mation. Because Medicaid and Exchange eligi-bility and enrollment systems must mesh soclosely, and because many enrollees are expectedto shift between sources of coverage as their cir-cumstances change, the Medicaid and Exchangeinformation systems must, at a minimum, behighly integrated. At most, they could share asingle system and achieve the necessary coordi-nation through a shared platform (CMS/OCIIO2010).

HHS has outlined its high expectations forstate Exchange and Medicaid information sys-tems in a series of federal guidance and fundingopportunity announcements:

• HHS Enrollment HIT Standards to facilitateenrollment and systems development (Sept2010)

• HHS-OCIIO Cooperative Agreement to Sup-port Innovative Exchange Information Tech-nology Systems grant (Oct 2010)

• CMS-OCIIO Guidance for Exchange andMedicaid Information Technology Systems,“Version 1.0” (Nov 2010)

• CMS Notice of Proposed Rule Making, Fed-eral Funding for Medicaid Eligibility Deter-mination and Enrollment Activities (Nov2010)

• HHS State Health Insurance Exchange Plan-ning and Establishment Grant Announce-ments11

This federal guidance requires systems that allowconsumers to apply for and renew benefits on-line; provide superior consumer service, includ-ing real-time transactions; obtain electronicverification of eligibility from federal and statedatabases; allow third parties to assist consumersin enrolling and maintaining coverage; notifyconsumers of eligibility and enrollment; and pro-vide seamless integration among health insur-ance options.12 Each component in this series ofguidance builds upon another with consistentstatements of goals and expectations for thiswork. HHS has also indicated that the federalgovernment will take the lead in developing sev-eral key systems components that will be avail-able to all states. The first is a “verification hub”that would allow states to connect to federaldatabases, such as those of the IRS, DHS, andSSA, to verify eligibility information. The secondis a “rules repository” that would contain MAGIeligibility rules written in a format enablingstates to easily leverage them for their own sys-tems. The intent of these federal initiatives is tocentralize elements that will be uniform acrossall states so that states do not need to duplicateeffort.

Furthermore, HHS has indicated that signifi-cant federal financial and technical support willbe available to states for systems work, includingthrough enhanced Medicaid federal matching

Coordinating Medicaid and the Exchange 9

11 HHS Enrollment HIT Standards Section 1561 to facilitate enrollment and systems development, September 2010:

http://healthit.hhs.gov/portal/server.pt?open=512&mode=2&objID=3161. HHS and OCIIO Cooperative Agreement to Support Inno-

vative Exchange Information Technology Systems grant, October 29, 2010:

http://www.grants.gov/search/search.do?mode=VIEW&oppId=58605. CMS and OCIIO Guidance for Exchange and Medicaid Informa-

tion Technology Systems, Version 1.0 November 3, 2010: https://www1.cms.gov/apps/docs/Joint-IT-Guidance-11-3-10-FINAL.pdf. CMS,

Notice of Proposed Rule Making, Federal Funding for Medicaid Eligibility Determination and Enrollment Activities, Federal Register

75(215): 68583-95, November 8, 2010: http://www.gpo.gov/fdsys/pkg/FR-2010-11-08/pdf/2010-27971.pdf. HHS State Health Insurance

Exchange Planning and Establishment Grant announcements: http://www.healthcare.gov/news/factsheets/esthealthinsurexch.html.

12 Section 1561 standards, Appendix A, and the November 3, 2010, Guidance for Exchange and Medicaid Information Technology Sys-

tems (Version 1.0).

funds and the Exchange “Early Innovator” fund-ing. New York was one of seven states (or groupsof states) awarded an “Early Innovator” grant inmid-February 2011, receiving an award of $27.4million over two years. (New York’s approach tothis systems work is described in the next sec-tion.) HHS also intends to be closely involvedwith states in systems design work to ensure thatthe highest quality results are attained.13 Thisfederal assistance offers New York an unprece-dented opportunity to update its information sys-tems to meet the requirements of the ACA.

Beyond these significant opportunities forstate systems work, there are two longer-termsystems challenges facing states. First, states willneed to consider how non-MAGI populations(e.g., elderly and disabled) will be included inthe upgraded system despite having different eli-gibility rules. In guidance to states, HHS has in-dicated its expectation that state Medicaidsystems will handle more than MAGIs.14 Fur-ther, while enhanced FMAP is available through2015 to design and build new Medicaid sys-tems,15 New York may need to seek an extensionof the enhanced FMAP beyond 2015 to allowtime to incorporate non-MAGI populations intoupgraded systems, which many anticipate willoccur in later stages of design.

Second, Exchange eligibility systems are alsoexpected to include a “consumer-mediated” ap-proach that will allow for connection with othersocial services programs, such as cash assistanceor Food Stamps. New York will need to considerthe complexity and timing of integrating Medi-caid with social services programs in addition tosubsidized private coverage. Again, this is morelikely to be incorporated in later stages of systemdesign.

Consumer Communications

The ACA’s vision for a consumer-friendly enroll-ment process also requires New York to signifi-cantly upgrade its communications with diversegroups of consumers through multiple media.The Exchange will need to provide consumerswith information in the following areas: availablecoverage options, eligibility requirements and en-rollment procedures, notification of eligibility de-termination results, and consumer rights andresponsibilities. This information will need to beprovided in clear, simple language. Further, be-cause states will be expected to communicatewith consumers in a variety of modes, includingpaper, e-mail, and text message, considerationwill be needed for these respective modes ofcommunication. It will be important that all con-sumer communications from the Exchange —whether they pertain to Medicaid, subsidized orunsubsidized private coverage — be consistentin tone, format, terminology, and literacy level.Forthcoming federal guidance is expected to out-line federal standards on these topics.

The ACA requires that, as of 2012, all insur-ance plans use a new health insurance disclosureform called the Summary of Benefits and Cover-age to let consumers compare health insuranceplans and understand the terms of their cover-age. This form will be important for state Ex-changes, which will provide information toconsumers to help them understand their cover-age options, and ultimately to facilitate the selec-tion of and enrollment in coverage. HHSregulations on this form are expected in the com-ing months. Additionally, the National Associa-tion of Insurance Commissioners has drafted aprototype of the form that was consumer-tested

10 United Hospital Fund

13 See, for example, HHS-OCIIO, “Cooperative Agreements to Support Innovative Exchange Information Technology Systems,” Fund-

ing Opportunity Announcement (CFDA 93.525), October 29, 2010.

14 See CMS/OCIIO 2010 and the HHS Exchange Establishment Grant application.

15 CMS, Notice of Proposed Rule Making, Federal Funding for Medicaid Eligibility Determination and Enrollment Activities, Federal

Register 75(215): 68583-95, November 8, 2010, http://www.gpo.gov/fdsys/pkg/FR-2010-11-08/pdf/2010-27971.pdf (accessed April 12,

2011).

by Consumers Union. These findings will likelyinform the federal guidance and will be relevantto states, which will likely tailor the federalmodel form to meet their own specific needs(Quincy 2011).

In addition, Exchanges will also be requiredto use a rating system for plans to enable con-sumers to evaluate plan choices in a uniformway. Currently, the New York State Departmentof Insurance issues an annual Consumer Guidefor Health Insurance that ranks insuranceproviders by specific criteria. Similarly, the De-partment of Health compiles consumer com-plaints and tracks HMO service and qualitythrough its QARR and CAHPS reporting sys-tems. The quality and consumer satisfaction in-formation is made available to Medicaid-eligibleindividuals when they are choosing a plan. Asmuch as possible, the plan rating system forNew York’s Exchange should use the same for-mat and language and include the same informa-tion for Medicaid and private plans. HHS isexpected to issue guidance on plan rating sys-tems in the coming months.

A recent United Hospital Fund-led initiativeexamining New York’s Medicaid client noticesmade a number of recommendations that are rel-evant for consumer communications from theExchange: notices should use plain language andbe written at an appropriate literacy level; usecreative font and formatting, including graphics;be individualized as much as possible (e.g., referto specific programs relevant to the consumer, bespecific about missing information); and greatlysimplify and streamline the fair hearing lan-guage. Background research for this project iden-tified Pennsylvania’s Medicaid notices as apotential model for New York. These notices usea creative layout with graphics and limit techni-cal and legal language and citations, focusing in-stead on the information consumers need tounderstand to take appropriate action.

The findings from another recent initiative to

evaluate New York City’s online Medicaid re-newal tool, ACCESS NYC, are also relevant tothe Exchange.16 Consumer testing of this toolfound that consumers had particular difficultywith questions about income. Specifically, con-sumers were confused about how to classify vari-ous sources of income, how to report grossincome, and how to report income if self-em-ployed or with variable income. The evaluationalso revealed the importance of literacy testing ofall language on the form, including explanatoryinformation that supplements the form (i.e.,“help text”). For example, it was recommendedthat the security questions be reviewed for cul-tural competency to assess their relevance toMedicaid populations. Additionally, the re-searchers identified problems with the transla-tion of the materials into other languages.Finally, many consumers noted the importanceof the facilitated enrollers, whose help they re-ceived with the online renewal process. Thus, itwas recommended that a help line be estab-lished for those who need real-time assistance tocomplete the process. While much emphasis isplaced on electronic and paper communicationwith consumers, it is critically important to re-member that many customers prefer live assis-tance, whether by phone or in person.

Finally, the Exchange will need processes inplace to handle grievances and appeals and willneed to coordinate them with Medicaid. Both in-dividuals and employers will have appeal rightswith the Exchange. Individuals can contest thedeterminations made by the Exchange regardingtheir eligibility to participate in the Exchange,their eligibility for subsidies, and denials of a re-quest for an exemption from the individual man-date. Employers can appeal Exchange decisionsif an employee is determined to be eligible for asubsidy because an employer does not offer min-imum essential or affordable coverage. In NewYork, the Departments of Health and Insurancecurrently have separate grievance and appeals

Coordinating Medicaid and the Exchange 11

16 This work was done by the Coalition of New York State Public Health Plans and Children’s Defense Fund of New York, with fund-

ing from the United Hospital Fund and New York Community Trust.

processes for public and commercial coverage(e.g., regarding access to care and coverage ofemergency care) and Medicaid’s Fair Hearingrights (available at DOH but not at SID) are thebiggest difference between them. As much aspossible, New York should seek to align and co-ordinate the grievance and appeals processes forMedicaid and private coverage.17

Other Challenges to Integration

Even if the aforementioned areas are well-coor-dinated between Medicaid and the Exchange,differences in participating plans, associatedprovider networks, and benefits offered betweenMedicaid and subsidized commercial coverageparticipating would present challenges as peoplemove between these sources of coverage. InNew York, only six of eighteen HMOs offer com-mercial coverage and participate in all publicprograms, and three-quarters of public programenrollees are served by eleven prepaid healthservices plans that do not offer commercial cov-erage (Newell, Baumgarten, and Heffernan2010).18 Left unchanged, this would necessitateplan changes as individuals’ eligibility fluctuates.Furthermore, there are currently differences be-tween networks and benefits in public and com-mercial plans, which would necessitate changingproviders and adjusting to a new benefit packageand cost-sharing obligations.19 The ACA require-ment that qualified health plans in the Exchangeinclude “essential community providers” in theirnetworks could help with the alignment between

Medicaid and commercial networks. Federalguidance defining essential community providersis expected in the coming months.

There are two key challenges to continuity ofcoverage and provider access across Medicaid,CHIP, and subsidized coverage options. The firstrelates to the churning discussed above associ-ated with fluctuations in income and eligibilityfor coverage and thus the potential to cycle be-tween different plans. The second relates to“mixed families,” or families in which differentmembers are eligible for different coverage,which could occur because of the different eligi-bility cutoffs for Medicaid (138 percent of FPL),FHP (150 percent of FPL), CHIP, and federalsubsidies (both 400 percent of FPL).

To achieve continuity of plans along the con-tinuum of coverage options, states may be per-mitted to require that all plans participating inthe Exchange offer all products: Medicaid,CHIP, subsidized and unsubsidized private cov-erage.20 This would mitigate disruptions in carewhen a person’s circumstances change. How-ever, states should carefully consider such a re-quirement because it would be a significant andcomplicated change. Absent a requirement, NewYork should consider ways to incentivize plans toparticipate in all products, including setting upthe Exchange so that it is attractive for plans toparticipate in all programs. States will need toconsider these incentives carefully so plans arenot dissuaded from participating in the Ex-change; robust plan participation is critical toachieving a high volume of enrollment in the Ex-change, which in turn can help the Exchangeachieve efficiencies and minimize adverse selec-

12 United Hospital Fund

17 One approach would be an integrated state appeals process for all subsidy eligibility determinations, modeled on the Medicaid Fair

Hearing process but administered by a state agency independent from Medicaid. (Personal communication with Trilby deJung, Empire

Justice Center, and “Designing an appeal process in conformity with Section 1411(f)(c),” the Tennessee Justice Center, National Health

Law Program, and Center for Medicare Advocacy, 2011.)

18 Note that under current New York State law, PHSPs cannot have more than 10 percent enrollment in commercial products.

HealthFirst is the only PHSP with a commercial HMO license.

19 See Newell and Baumgarten 2011 for detail about plan participation in Medicaid and commercial insurance products.

20 PPACA Section 1555 pertains to potential limits of federal/state authority to require such plan participation in federal health insur-

ance programs.

tion. Plans will also be incentivized to participatein multiple programs because they will under-stand the degree to which their enrollees’ in-comes fluctuate and will not want to loseenrollees to this eligibility churning.

New York’s Starting Point andEarly Vision for 2014

In preparing for reform, New York will need toassess its existing capabilities and determinewhat can be leveraged, which functions can beconsolidated, and what the State will need tobuild or buy in order to comply with the ACA’srequirements. Chief among the State’s relevantassets are its Enrollment Center, scheduled forlaunch in 2011; the Medicaid Enterprise infra-structure;21 a strong foundation of eligibility andenrollment policies; and the authority to central-ize Medicaid administration. Furthermore, NewYork has two important projects underway per-taining to its information systems: the Early In-novator grant for Exchange systems develop-ment, and an analysis of its information technol-ogy systems and needs being conducted by out-side consultants.

Enrollment Center/HEARTThe Healthcare Eligibility Assessment and Re-newal Tool (HEART) is an automated eligibilitydecision tool that will be used by EnrollmentCenter staff to assist eligible New Yorkers withphone and mail renewal beginning in June 2011.This tool will initially interface with the Depart-ment of Health’s upstate eligibility system and isreferred to as a “rules engine,” currently pro-grammed with approximately 10,000 Medicaidbusiness rules. The tool is designed for use byEnrollment Center staff to facilitate the renewalprocess, allowing the worker to confirm and ver-

ify certain information available in real time(e.g., while on the phone with a consumer), andhelping standardize the eligibility determinationprocess. Although HEART is currently pro-grammed to apply existing Medicaid eligibilityrules, it was designed to accommodate new rulesand program changes as they occur.

Eligibility and Enrollment PoliciesNew York has a strong history of implementingpolicies to streamline public program eligibilityand enrollment. These include elimination of theMedicaid asset test, 12-month continuous eligi-bility for children and adults (in 2011), and datamatching with the Social Security Administra-tion to verify citizenship status and identity. For2014, the state will need to build upon this foun-dation to further simplify enrollment, but has astrong starting point. For all groups except asmall percentage of childless adults, New York’spublic program eligibility levels already meet orexceed the ACA’s requirements for 2014.

Centralized Medicaid Administration New York’s 2010-11 budget mandated the cre-ation and implementation of a five-year plan forthe state to assume all Medicaid administration.Centralized administration of Medicaid will helpthe State consolidate functions, eliminate incon-sistencies in program administration, and signifi-cantly ease coordination with the Exchange. TheState’s November 2010 report on Medicaid ad-ministration contained a recommended phase-inplan that included the launch of the statewideEnrollment Center, with consolidation of con-sumer help lines and telephone renewal in 2011,and state assumption of responsibility for eligi-bility determinations for non-elderly and nondis-abled people under federal MAGI rules,concurrent with the implementation of federalhealth reform.22

Coordinating Medicaid and the Exchange 13

21 “Medicaid Enterprise” refers to Medicaid’s information technology infrastructure, which includes state Medicaid operations and in-

terfaces between state Medicaid agencies and stakeholders.

22 New York State Department of Health, “New York State Medicaid Administration, November 2010 Report”:

http://www.health.state.ny.us/health_care/docs/2010-11_medicaid_admin_report.pdf.

Early Innovator Exchange IT InitiativeIn its Early Innovator proposal, New York dis-cussed leveraging existing Medicaid Enterpriseassets (including the data center and the techni-cal architecture of its medication managementpilot) to support a modern, consumer-friendlyHealth Benefit Exchange.23 New York also plansto integrate HEART logic as part of the larger so-lution. In February 2011, New York was awardeda two-year $27.4 million Early Innovator grant tocarry out this work. HHS is expected to providesignificant technical support to help innovatorstates meet their goals, and to ensure that thisfederal money is well spent; as the programname suggests, these states are expected to leadthe way, serving as models for other states updat-ing their own information systems.

Information Technology Gap AnalysisAs part of New York’s work to prepare for healthreform, it is working with Social Interest Solu-tions (SIS) and The Lewin Group, with fundingfrom the New York State Health Foundation, toassess its eligibility and enrollment systems ca-pacity and needs. Through this gap analysis, SISwill inventory existing systems — in both thepublic and private sectors throughout the state— to assess the state’s existing information tech-nology (IT) assets, determine what can be lever-aged, and identify what else is needed to meetthe ACA requirements. SIS will assess the sys-tems capabilities for potential use in New York’sExchange and The Lewin Group will gatherstakeholder input from government, business,consumer, health plan, provider, and policy ex-perts on the challenges and opportunities pro-vided by the ACA’s systems requirements. Thefindings and recommendations from this analysisare expected in May 2011.

New York’s Vision

As outlined in several of the State’s planningdocuments, New York anticipates a vastly simpli-fied enrollment system built on modern informa-tion system standards and protocols.24 This willinclude a consumer-friendly front end and arules engine that will enable a more automateddetermination of eligibility for Exchange, Medi-caid, and CHIP, as part of a new eligibility andenrollment system. At the front end, it is envi-sioned that a consumer will supply minimal eligi-bility information, and will be able to have his orher eligibility determined easily and with signifi-cantly less reliance on paper. It is also contem-plated that a consumer, with identity and privacyprotections, will be able to view eligibility infor-mation the state has acquired through datamatches with state, federal, and private data-bases, and have the ability to update or correctpersonal information. The rules engine will takethe information and make a determination of eli-gibility. And the consumer will be able to selectand enroll in an appropriate health insurance op-tion, as well as switch from one option to an-other.

New York plans to leverage its investmentsand work on health information technology, andits work on HEART will be an important asset interms of the work required to establish a newHealth Insurance Exchange in New York that isanticipated to have more robust linkages to fed-eral and potentially other verification sources,and to be using a new federal data hub. Depend-ing upon emerging rules and construction of thefederal hub, the state might also want to exploreother verification sources, including the WorkNumber and eFIND, which contain currentwage and salary information compiled from na-

14 United Hospital Fund

23 The New York State Medicaid program claims processing system, eMedNY, was developed in 2005. The system allows New York

Medicaid providers to submit claims and receive payments for Medicaid-covered services provided to eligible clients. eMedNY offers

several technical and architectural features, facilitating the adjudication and payment of claims and providing support for its users.

Computer Sciences Corporation (CSC) is the eMedNY contractor and is responsible for its operation:

http://www.emedny.org/index.aspx.The MMIS contract is currently out for re-bid.

24 New York’s application for the Exchange planning grant (http://www.healthcarereform.ny.gov/exchange_planning_grant/docs/narra-

tive.pdf), comments to the Notice of Proposed Rulemaking submitted in October 2010

(http://healthcarereform.ny.gov/docs/nys_comments_title_i_ppaca.pdf), and conversations with senior staff in the Office of Health In-

surance Programs, New York State Department of Health.

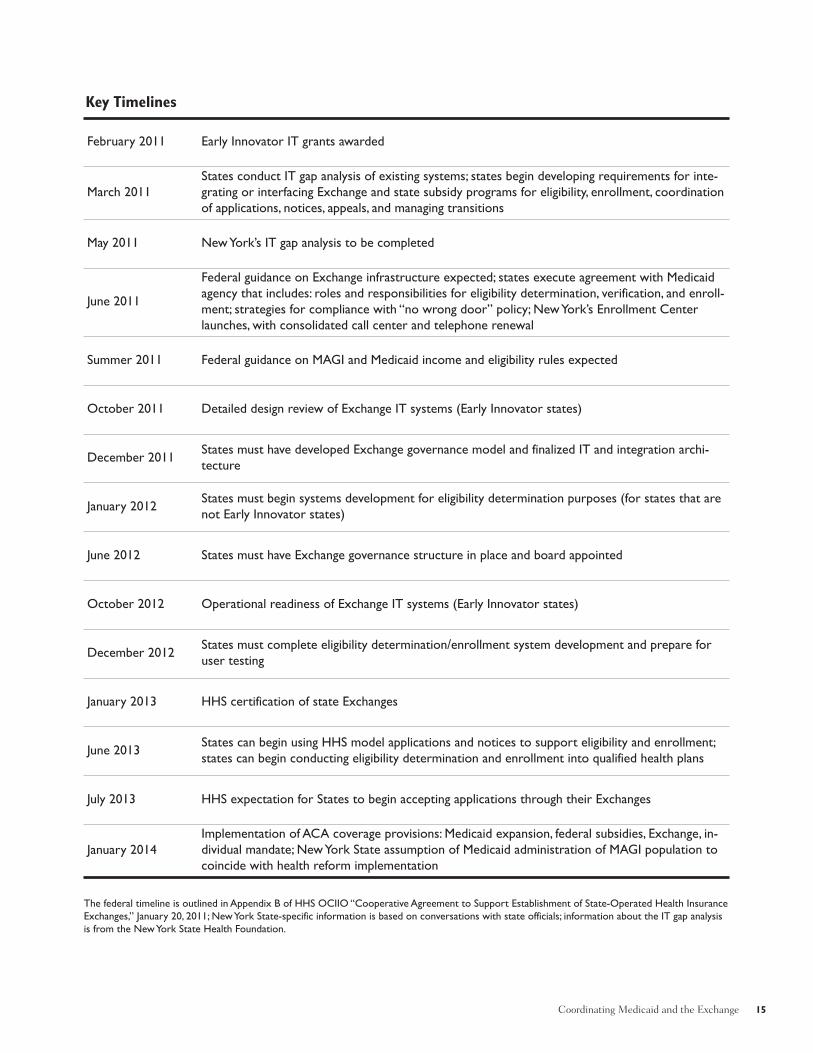

Coordinating Medicaid and the Exchange 15

February 2011 Early Innovator IT grants awarded

March 2011

States conduct IT gap analysis of existing systems; states begin developing requirements for inte-

grating or interfacing Exchange and state subsidy programs for eligibility, enrollment, coordination

of applications, notices, appeals, and managing transitions

May 2011 New York’s IT gap analysis to be completed

June 2011

Federal guidance on Exchange infrastructure expected; states execute agreement with Medicaid

agency that includes: roles and responsibilities for eligibility determination, verification, and enroll-

ment; strategies for compliance with “no wrong door” policy; New York’s Enrollment Center

launches, with consolidated call center and telephone renewal

Summer 2011 Federal guidance on MAGI and Medicaid income and eligibility rules expected

October 2011 Detailed design review of Exchange IT systems (Early Innovator states)

December 2011States must have developed Exchange governance model and finalized IT and integration archi-

tecture

January 2012States must begin systems development for eligibility determination purposes (for states that are

not Early Innovator states)

June 2012 States must have Exchange governance structure in place and board appointed

October 2012 Operational readiness of Exchange IT systems (Early Innovator states)

December 2012States must complete eligibility determination/enrollment system development and prepare for

user testing

January 2013 HHS certification of state Exchanges

June 2013States can begin using HHS model applications and notices to support eligibility and enrollment;

states can begin conducting eligibility determination and enrollment into qualified health plans

July 2013 HHS expectation for States to begin accepting applications through their Exchanges

January 2014

Implementation of ACA coverage provisions: Medicaid expansion, federal subsidies, Exchange, in-

dividual mandate; New York State assumption of Medicaid administration of MAGI population to

coincide with health reform implementation

The federal timeline is outlined in Appendix B of HHS OCIIO “Cooperative Agreement to Support Establishment of State-Operated Health Insurance

Exchanges,” January 20, 2011; New York State-specific information is based on conversations with state officials; information about the IT gap analysis

is from the New York State Health Foundation.

Key Timelines

16 United Hospital Fund

Other State Examples

WisconsinWisconsin has been a leader in developing eligibility and enrollment systems and is a potential

model for New York. Wisconsin offers a one-stop self-service tool, called “ACCESS,” with which

consumers can apply for several social programs, including BadgerCare Plus and FoodShare.

ACCESS includes an eligibility assessment, an online application, and the ability to renew benefits

and report changes in eligibility status; soon it will also perform a needs assessment to assist

with plan selection. Simplified eligibility rules, including a gross income test, are virtually identical

for anyone under 200 percent of FPL and have greatly eased the eligibility process. However, cer-

tain applications may require follow-up via telephone. Documentation requirements (submission

by fax, by mail, or in person) and the federal requirement that public employees actively verify el-

igibility are hurdles to further simplification and efficiency. Despite these modest limitations,

ACCESS has become the dominant application method among family coverage applicants in Wis-

consin. More than half of these BadgerCare Plus applicants used ACCESS between January 2008

and November 2009, whether they were at or above 150 percent of FPL (85 percent using

ACCESS) or below 150 percent of FPL (56 percent), and whether their primary language was

English (63 percent) or another language (51 percent) (Leininger et al. 2011). Wisconsin intends

to use ACCESS as the portal to its Exchange, and it currently has a prototype of its Exchange

system available online at http://exchange.wisconsin.gov.

ACCESS, the front-end program, is integrated with Wisconsin’s eligibility system, “CARES,”

and its Medicaid management information system. CARES exchanges data with state and federal

databases, including: IRS income and asset information; state wage, unemployment compensation,

and new hire data; SSA information on disability payments, SSI, and Medicare information; and

child support enforcement data (paid and received). While exchanges of SSA and certain state

data currently automatically update Wisconsin’s eligibility system or alert workers to changes,

most of its data exchange sources are verification tools that require action on the part of state

workers. However, the state’s new “integrated State of Wisconsin Acquisition of Proof” (iSWAP)

technology, scheduled for rollout in November 2011, will automatically update information in the

eligibility system using SSA, unemployment, child support, earned income (via the Work Num-

ber), vital statistics, and other third-party data. It will use these data to determine eligibility at

the point of enrollment, renewal, or when changes occur. The technology will also use state wage

data to confirm wage information provided by the applicant or beneficiary. The iSWAP program

will allow largely automated, real-time eligibility determinations with very little need for interac-

tion between state workers and consumers, putting verification of third-party information in the

hands of the consumers rather than the workers. (Kaiser 2010; Jones 2011.)

PennsylvaniaPennsylvania also has innovative enrollment tools that could serve as models for New York.

Pennsylvania’s online application system, COMPASS, bridges its Medicaid, CHIP, and state-funded

program for low-income adults, and also allows individuals to apply for cash assistance, the Sup-

plemental Nutrition Assistance Program, and other assistance programs. Pennsylvania’s “Health-

care Handshake” automatically transfers data between the Department of Public Welfare

(Pennsylvania’s Medicaid agency) and the Insurance Department. This transfer occurs at the

point of application, allowing a fully populated application to be submitted to other programs if

an individual is found ineligible for one. In addition, the data transfer occurs if an individual loses

eligibility for one public program but may be eligible for another, minimizing preventable gaps in

coverage.

One current limitation of the COMPASS system is that applications require paper documen-

tation to satisfy several eligibility elements, even where verifiable data are available electronically.

(Artiga et al. 2010; correspondence to CMS re: File Code OCIIO-9989-NC. http://www.chil-

drenspartnership.org/AM/Template.cfm?Section=Law_and_Guidance&Template=/CM/Content-

Display.cfm&ContentID=15118.)

tional employer databases. Some states have ex-perience using these databases, either in lieu ofdocuments at renewal (Louisiana) or as a supple-mentary verification source (Utah, Wisconsin).States will need to consider the costs associatedwith using private verification sources and couldconsider coordinating with other states for agroup purchase discount or asking HHS to do soon behalf of all states.

Eligibility and enrollment system needs willalso be addressed in the IT gap analysis de-scribed above. This analysis will assess NewYork’s IT capabilities and needs, and the EarlyInnovator grant will give New York significantsupport to develop and build its IT platform.Less is known about the State’s vision for con-sumer communications and potential integrationof plans, networks, and benefits across programsin the Exchange; however, the key issues andchoices are outlined above.

Conclusion

Meeting the ACA’s vision that all Americanshave access to affordable care will require suc-cessful implementation of a Health InsuranceExchange and seamless coordination betweenMedicaid and the Exchange so eligible peoplecan easily enroll in and retain coverage. Suchseamless integration will require careful atten-tion to five key areas: eligibility and enrollment,renewals and transitions, information systems,consumer communications, and challenges asso-ciated with aligning the plans, networks, andbenefits offered. Under this vision, consumerswith income from 0 to 400 percent of FPL areexpected to have the same “first-class” enroll-ment experience. A significant level of incomefluctuation is expected, so states will need to de-

velop ways to ease transitions between programsand eliminate any gaps in coverage when peopleshift between sources of coverage. Informationtechnology will be a key component to ensuringseamless coordination between Medicaid andthe Exchange and to implementing an accessi-ble, consumer-friendly eligibility and enrollmentprocess. New York will need to significantly up-grade its communications with diverse groups ofconsumers through multiple media, paying par-ticular attention to literacy levels. Finally, thestate will need to consider ways to incentivizeplans to participate in all programs offered in theExchange to minimize the need for individuals tochange plans or providers as they transition be-tween programs when their circumstanceschange.

The complexity of these tasks could easilyoverwhelm those charged with implementingthem, so it will be important for states to addressthem piece by piece. New York has a strongstarting point in this work and will receive sub-stantial financial and technical support from thefederal government. The importance of successshould not be understated: meeting the ACA’scoverage goals would mean an additional 1.2 mil-lion or more insured New Yorkers, and taking fulladvantage of this opportunity to implement theExchange will improve the way millions of otherNew Yorkers get their coverage.

Acknowledgments

The New York State Health Foundation provided support for this work. At the UnitedHospital Fund, Jim Tallon, Peter Newell, andDavid Gould provided helpful comments on ear-lier drafts, and Andrew Detty provided researchassistance.

Coordinating Medicaid and the Exchange 17

ReferencesArtiga S, R Rudowitz, and B Lyons. October 2010. Coordinating Coverage and Care in Medicaid andHealth Insurance Exchanges. Washington, DC: Kaiser Commission on Medicaid and the Uninsured.

Bachrach D, PM Boozang, MJ Dutton, and D Holahan. January 2011. “Revisioning” Medicaid as Partof New York’s Coverage Continuum. New York: United Hospital Fund.

Centers for Medicare & Medicaid Services, Office of Consumer Information and Insurance Over-sight (OCIIO). November 3, 2010. Guidance for Exchange and Medicaid Information Technology (IT)Systems, Version 1.0. Available at http://www.hhs.gov/ociio/regulations/joint_cms_ociio_guidance.pdf(accessed April 4, 2011).

Edwards J, J Bitterman, C Davis, R Kellenberg, and S Dorn. 2009. Reducing Paperwork to ImproveEnrollment and Retention in Medicaid and CHIP. New York: United Hospital Fund.

Kaiser Commission on Medicaid and the Uninsured. October 2010. Optimizing Medicaid Enroll-ment: Spotlight on Technology, Wisconsin’s ACCESS Internet Portal. Washington, DC: Kaiser Com-mission on Medicaid and the Uninsured.

Leininger LF, D Friedsam, K Voskuil, and T DeLeire. February 2011. The Target Efficiency of OnlineMedicaid/CHIP Enrollment: An Evaluation of Wisconsin’s ACCESS Internet Portal. Minneapolis:State Health Access Data Assistance Center.

Newell P, A Baumgarten, and J Heffernan. March 2010. The Big Picture Updated: Current Status ofNew York’s Health Insurance Markets. New York: United Hospital Fund.

Newell P and A Baumgarten. April 2011. The Big Picture III: Private and Public Health InsuranceMarkets in New York, 2009. New York: United Hospital Fund.

Quincy L. February 2011. Making Health Insurance Cost-Sharing Clear to Consumers: Challenges inImplementing Health Reform’s Insurance Disclosure Requirements. New York: Commonwealth Fund.

Sommers BD and S Rosenbaum. February 2011. Issues in Health Reform: How Changes in Eligibil-ity May Move Millions Back and Forth Between Medicaid and Insurance Exchanges. Health Affairs30(2): 228-236.

18 United Hospital Fund