38

Federal Retirement Program CSRS: Civil Service Retirement System FERS: Federal Employees’ Retirement System FEGLI: Federal Employees’ Group Life Insurance TSP: Thrift Savings Plan

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | chase-trusler |

| View: | 255 times |

| Download: | 2 times |

Federal Retirement Program

CSRS: Civil Service Retirement SystemFERS: Federal Employees’ Retirement

SystemFEGLI: Federal Employees’ Group Life

InsuranceTSP: Thrift Savings Plan

Civil Service Retirement System (CSRS)

• Contribution rates: Employee: 7% Employer: 7%

• Participants generally pay no Social Security retirement, survivor and disability (OASDI) tax, but must pay the Medicare tax.

• Employees may contribute up to 5% of their pay to the Thrift Savings Plan (TSP) but no agency contribution, either automatic (1%) or match (up to 4%).

CSRS Retirement Eligibility

AGE and CREDITABLE SERVICE

62 5 years 60 20 years 55 30 years

CSRS Annuity

CSRS benefits are based on the employee's "high-3" average pay and their years of service. The annuity will be increased

periodically by cost-of-living increases that occur after retirement. The initial cost-of-living increase will be prorated based on how long the annuitant has been retired

when the cost-of-living increase is granted.

CSRS Monthly Benefit Options

• Full annuity – nothing to survivors• Full survivor annuity

– Reduction to retiree’s annuity– 55% of full survivor benefit to survivor

• Partial survivor annuity– Reduction to retiree’s annuity based upon survivor

annuity– Can be any amount between zero and full survivor

annuity

Federal Employees’ Retirement System (FERS)

• Contribution rates:

– Employee: .8% Employer: 11.7%

• FERS is a three-tiered retirement plan:

– Social Security Benefits, Basic Benefit Plan, and Thrift Savings Plan

• Employees may contribute up to $16,500 for 2011 (the elective deferral limit) to the Thrift Savings Plan and up to $5,5000 in catch-up contributions. These dollars are tax-deferred. The agency contributes an automatic 1% and matches up to 4%.

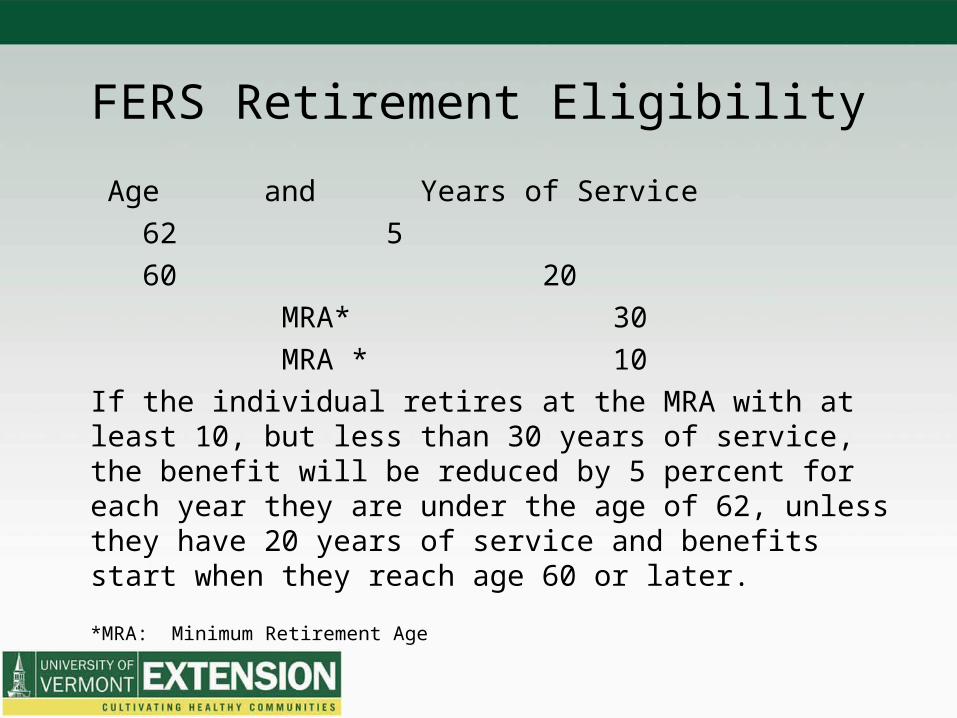

FERS Retirement Eligibility

Age and Years of Service 62 5

60 20 MRA* 30 MRA * 10

If the individual retires at the MRA with at least 10, but less than 30 years of service, the benefit will be reduced by 5 percent for each year they are under the age of 62, unless they have 20 years of service and benefits start when they reach age 60 or later.

*MRA: Minimum Retirement Age

FERS Retirement EligibilityMinimum Retirement Age (MRA)

If you were born Your MRA is Before 1948 55 In 1948 55 and 2 months In 1949 55 and 4 months In 1950 55 and 6 months In 1951 55 and 8 months In 1952 55 and 10 months In 1953 through 1964 56 In 1965 56 and 2 months In 1966 56 and 4 months In 1967 56 and 6 months In 1968 56 and 8 months In 1969 56 and 10 months In 1970 and after 57

FERS AnnuityThe basic FERS annuity is based on the employee's length

of service and the "high-3" average pay. For most employees, the formula for computing the annual annuity

is 1 percent of average pay for each year of creditable service.

The FERS annuity supplement is paid in addition to the monthly FERS annuity. It represents what the annuitant

would receive for their FERS civilian service from the Social Security Administration (SSA) and is calculated as

if the individual is eligible to receive social security benefits on the day they retire. The supplement

continues until the annuitant is eligible for social security or the last day of the month in which they reach age 62.

FERS Monthly Benefit Options

• Full annuity – nothing to survivor• Full survivor annuity

– 10% reduction to retiree’s annuity– Survivor receives 50% of retiree’s annuity

• Partial Survivor annuity– 5% reduction to retiree’s annuity– Survivor receives 25% of retiree’s annuity

Life insurance options after retirement• BASIC

– Amount is determined by the annual pay in effect when the annuitant separated for retirement, rounded to the next higher thousand (if not an even thousand), plus $2,000.

– Three election choices: 75% reduction, 50% reduction, or No reduction.

No Reduction after age 65• If the annuitant elects this reduction, the full amount of the

Basic life insurance remains in force after they reach age 65. • Premiums for this additional coverage are withheld from the

annuity beginning at retirement and continuing for life. • The most expensive.

Basic cont’d50% Reduction after age 65

• Begins to reduce by 1% of the face value each month beginning with the second month after the date the age 65 or the second month after the individual retires, whichever is later. This reduction continues until the Basic life insurance reaches 50% of the face value

• At age 65, 2% per month reduction of life insurance to 50% reduction (i.e., $40,000 to $20,000)

75% Reduction after age 65• Reduce by 2% of the face value each month beginning

with the second month after the date the individual is 65 or the second month after retirement, whichever is later.

• At age 65, 2% per month reduction to 75% reduction or, 25% of the face value ($40,000 to $10,000)

Federal Employees’ Group Life Insurance (FEGLI)

Cost for Annuitants for each $1,000 of the Basic Insurance Amount in Effect at the Time of Retirement

75% Reduction 50% Reduction No Reduction Until the Month afterthe 65th Birthday $0.3250 monthly $0.9250 monthly $2.1550 monthly

Starting the Monthafter the 65th Birthday Free $0.60 monthly $1.83 monthly

* This amount will be withheld from the annuity for life (unless the annuitant

cancels or subsequently elects 75% Reduction).

FEGLI – Option A

• Option A – Standard Insurance ($10,000)– Reduces by 2% per month beginning the

second month after the annuitant is 65 or the second month after retirement, whichever is later, until it reaches 25% of the face value ($2,500).

– Premiums will be withheld from the annuity through the end of the month in which the annuitant is 65, unless they elect to cancel this coverage.

FEGLI – Option B

• Option B – Additional Insurance• Amount is determined by multiplying the final annual

basic pay rate rounded to the next higher thousand by the number of Option B multiples (1 to 5) that were in effect for the five years of service immediately before retirement.

• Annuitants who are eligible will be given a second opportunity to make this election around their 65th birthday. – Can elect Full Reduction or No Reduction.– See page 11 of Information for Retirees and Their Families

(RI 76-12) for additional information.

FEGLI – Option C

• Option C – Family Insurance• $5,000 coverage for a spouse per multiple• $2,500 coverage for each eligible dependent child• Amount of insurance is determined by the number of

multiples (1 - 5) that were in effect for the five years of service immediately before retirement.

• The annuitant is the beneficiary. After the annuitant’s death, Option C stops. However, covered surviving family members will have an opportunity to convert to a non-group policy.

FEGLI

• Unless the annuitant has assigned the insurance, it may be canceled at any time. If the Basic life insurance is cancelled, ALL Optional insurance is cancelled as well.

• The annuitant should keep the designation of beneficiary up-to-date. OFEGLI cannot make payments if they cannot locate the beneficiary.

What are the requirements to keep life insurance in retirement?

• The participant has coverage when they retire; • The annuity begins within 30 days and, • The participant was insured for life insurance for

the five years immediately preceding retirement or the full periods of service when coverage was available.

Thrift Savings Plan (TSP)

How much can the participant contribute to TSP?

• The Internal Revenue Code places an annual limit on elective deferrals (e.g., tax-deferred employee contributions to the TSP). The elective deferral limit is $16,500 for 2011.

• Consequently, once the $16,500 limit has been met, the participant may not make any additional (regular) tax-deferred contributions for the rest of the year. For FERS employees, this also means that they will not receive any additional Agency Matching Contributions for the rest of the year.

TSP Catch-Up Contributions

• If the participant has made — or will make — the maximum amount of regular employee contributions for the year ($16,500 in 2011), they may also make catch-up contributions. The catch-up contribution limit for calendar year 2011 is $5,500.

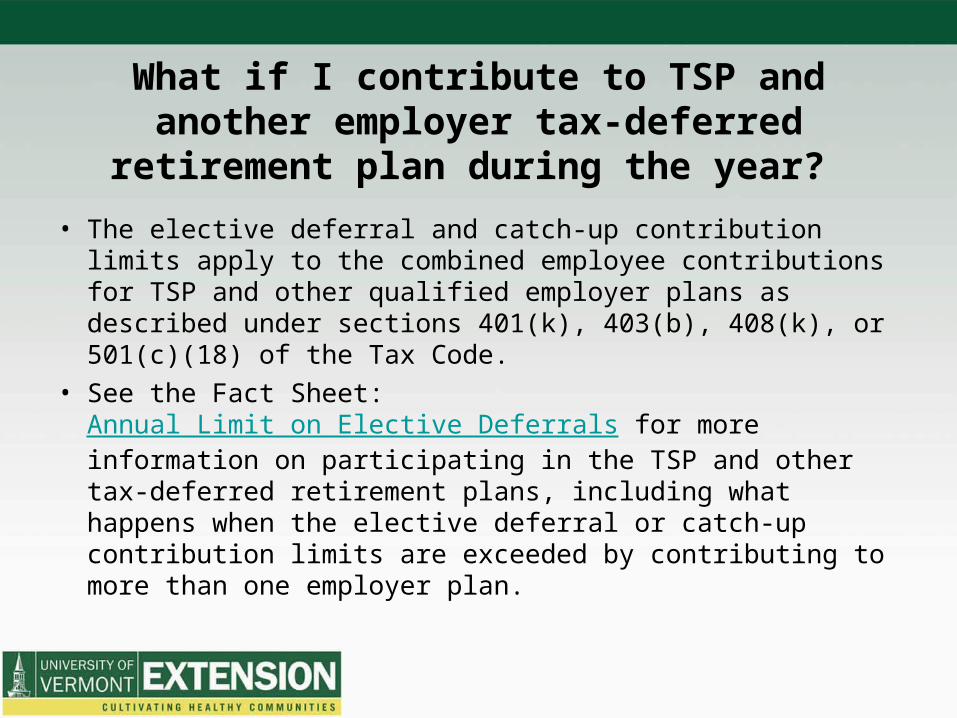

What if I contribute to TSP and another employer tax-deferred retirement plan

during the year?

• The elective deferral and catch-up contribution limits apply to the combined employee contributions for TSP and other qualified employer plans as described under sections 401(k), 403(b), 408(k), or 501(c)(18) of the Tax Code.

• See the Fact Sheet: Annual Limit on Elective Deferrals for more information on participating in the TSP and other tax-deferred retirement plans, including what happens when the elective deferral or catch-up contribution limits are exceeded by contributing to more than one employer plan.

Social Security

• Each individual should ask for a form SSA-7004-PC, Request for Earnings and Benefit Estimate Statement, from the local Social Security Office or visit the website at http://www.ssa.gov. If this form is submitted, the individual will get a statement that provides information on their future eligibility for Social Security benefits and estimates of these benefits at specified dates. These estimates do not reflect any reduction for the Government Pension Offset or the Windfall Elimination Provision (WEP).

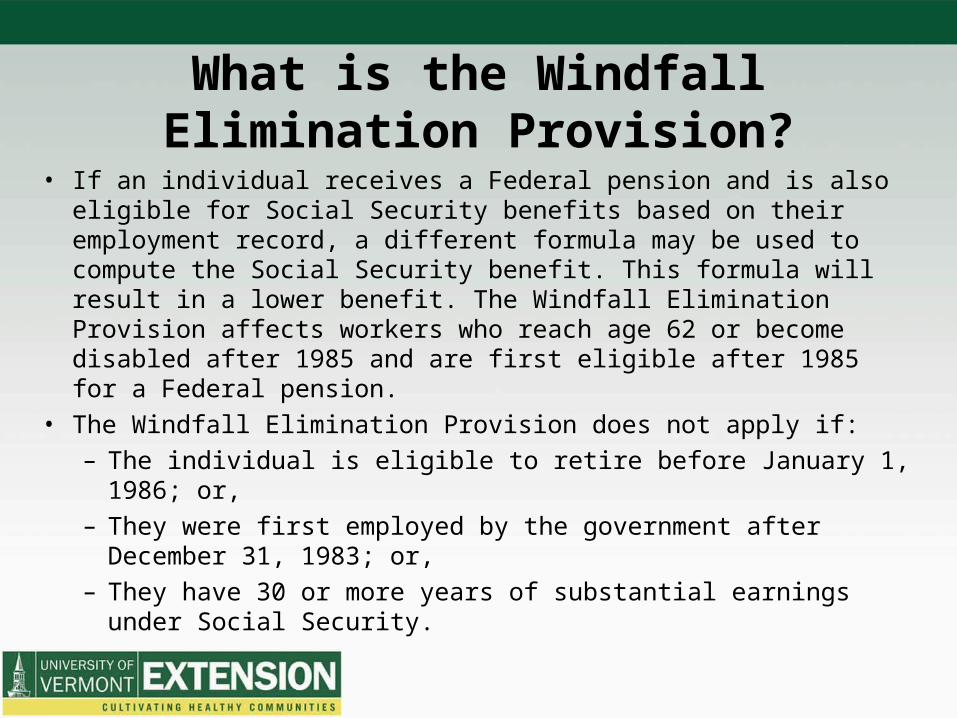

What is the Windfall Elimination Provision?

• If an individual receives a Federal pension and is also eligible for Social Security benefits based on their employment record, a different formula may be used to compute the Social Security benefit. This formula will result in a lower benefit. The Windfall Elimination Provision affects workers who reach age 62 or become disabled after 1985 and are first eligible after 1985 for a Federal pension.

• The Windfall Elimination Provision does not apply if: – The individual is eligible to retire before January 1, 1986;

or, – They were first employed by the government after

December 31, 1983; or, – They have 30 or more years of substantial earnings under

Social Security.

Consult a tax advisor once you have your annuity estimates!

What happens when an individual plans to retire?

• About six weeks prior to the retirement date, the individual will receive a package of forms from me. The enclosed letter will ask the individual to return the completed forms two weeks prior to the retirement date.– This is in case I have any questions, I can reach you.

• After I have reviewed the forms and completed the forms and/or sections of the forms I need to complete, I forward the information to OPM (Office of Personnel Management).

• The first two to four annuity payments will represent a portion of the final benefit and is usually made on the first business day of each month.

• OPM will send an annuity statement once they have finalized the application for retirement.

Session 23 Federal Benefits—Retirement Counseling

Panel

•Becky Priebe, Washington State University

•Celia Rainville, University of Vermont

•Mary Fran San Soucie, Montana State University

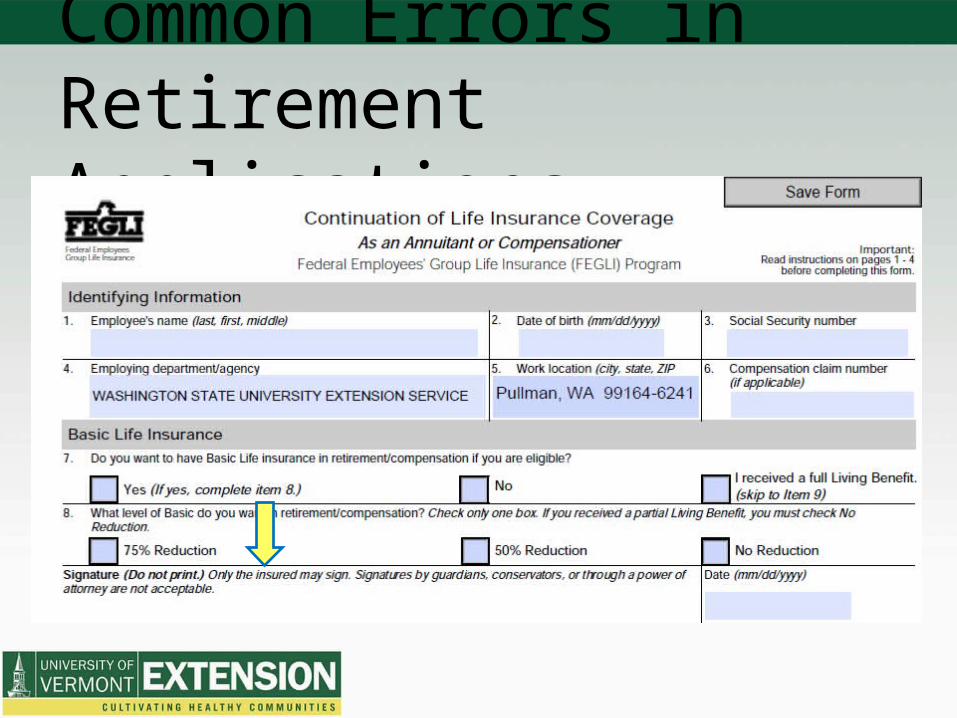

Common Errors on Retirement Applications

Common Errors on Retirement Applications

Common Errors on Retirement Applications

Common Errors on Retirement Applications

Common Errors in Retirement Applications

Common Errors in Retirement Applications

Common Error in Retirement Applications

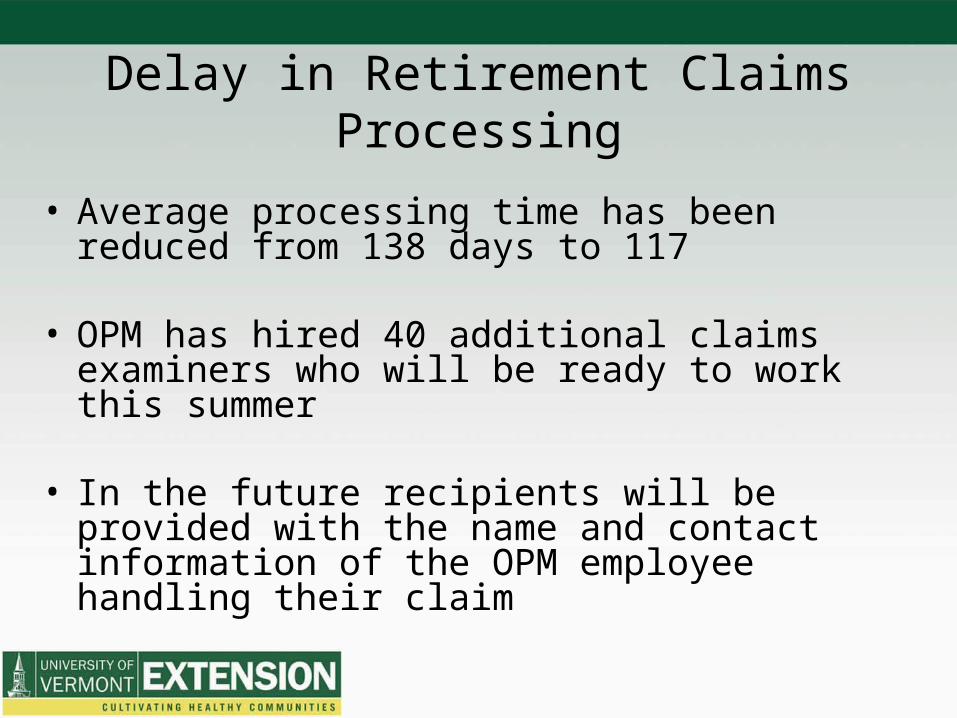

Delay in Retirement Claims Processing

• Average processing time has been reduced from 138 days to 117

• OPM has hired 40 additional claims examiners who will be ready to work this summer

• In the future recipients will be provided with

the name and contact information of the OPM employee handling their claim

Delay in Retirement Claims Processing

OPM is committed to providing retirees with as much of their annuity as possible. Conditions that may cause the annuitant to receive less are:

•FERS annuity supplement

•Unpaid service credit deposits

•Redeposits or military deposits

Questions