Exploration Targeting in a Business Context T. Campbell McCuaig – CET Pietro Guj – CET Jon Hronsky – Western Mining Services Richard Schodde – MinEx Consulting Fennoscandian Exploration and Mining 2009

Transcript

Exploration Targeting in a Business Context

T. Campbell McCuaig – CETPietro Guj – CET

Jon Hronsky – Western Mining ServicesRichard Schodde – MinEx Consulting

• The Mineral industry will be forced to undergo a paradigm shift over the next ten years to a focus on seeking quality greenfields discoveries, requiring:– Greater dependence on accurate conceptual targeting– Exploration systems that closely estimate probability of

success and monitor performance– Concomitant development of exploration technologies

that will allow us to explore new search spaces cost effectively

• The petroleum industry was forced to commence this shift over 30 years ago

We in the mineral industry are behind the times.

Topics to consider

• Drivers for change• Current industry practice misalignment with

future needs• Scale dependent targeting approaches• Corporate considerations and monitoring of

industry success

Drivers of change• Growing demand for mineral end energy

resources by society• Declining exploration success• Resource depletion outstrips replenishment

– Current resource base cannot meet this demand

• Depletion of residual search space• Need for targeting new provinces in areas of

challenging cover (new search space)• The expense of detection in this new search

space – need to target exploration moreeffectively

• Social change requiring a reduction of physical, social and environmental footprint (Europe!)

Minerals and energy demand:the case for the supercycle

Pyle, 2008GFC – major impact on industry funding, limited impact on demand!

Exploration effectiveness declining

7

McKeith (2009)

Challenge to maintain production levels

The graph for base metals tells the same story!

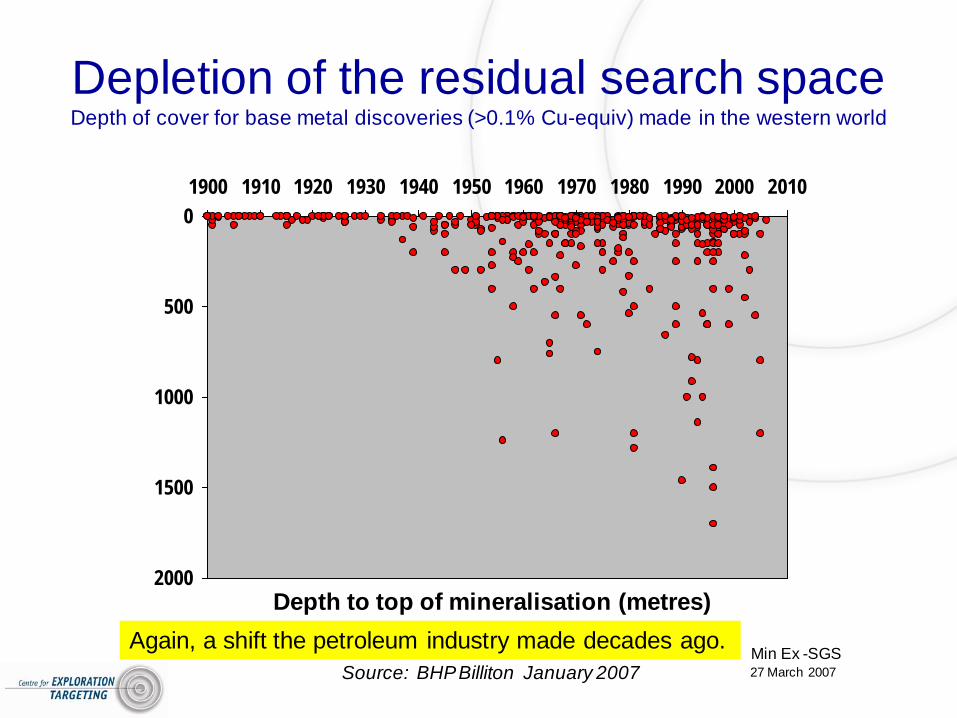

Depletion of the residual search spaceDepth of cover for base metal discoveries (>0.1% Cu-equiv) made in the western world

Min Ex -SGS27 March 2007Source: BHP Billiton January 2007

Depth to top of mineralisation (metres)Again, a shift the petroleum industry made decades ago.

Understanding the search space concept

• In any search space, the bulk of the metal is in a few large deposits

• The largest deposits in any search space are usually found early because they generally have the most obvious signatures

• Any given search space will progressively become exhausted over time, resulting in smaller and higher cost discoveries

• The most important discontinuities in the exploration business are those which significantly expand the search space through innovation– New technology (extraction and exploration)– New concepts (often linked to technology)

SEARCH SPACE OBSERVATION 1 :Most of the mineral industry's wealth is captured by a handful of giant deposits

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%Cumulative Number of Deposits

Cumulative NPV @ 8% discount rate

Source : Derived from Mackenzie 1995

129 Deposits with total value of US$32Billion in 1994 dollars

Base Metal Mines discovered in Canada & Australia to 1988

BASE METALS2/3rds of wealth

comes from 10% of all projects

Hronsky (2004)

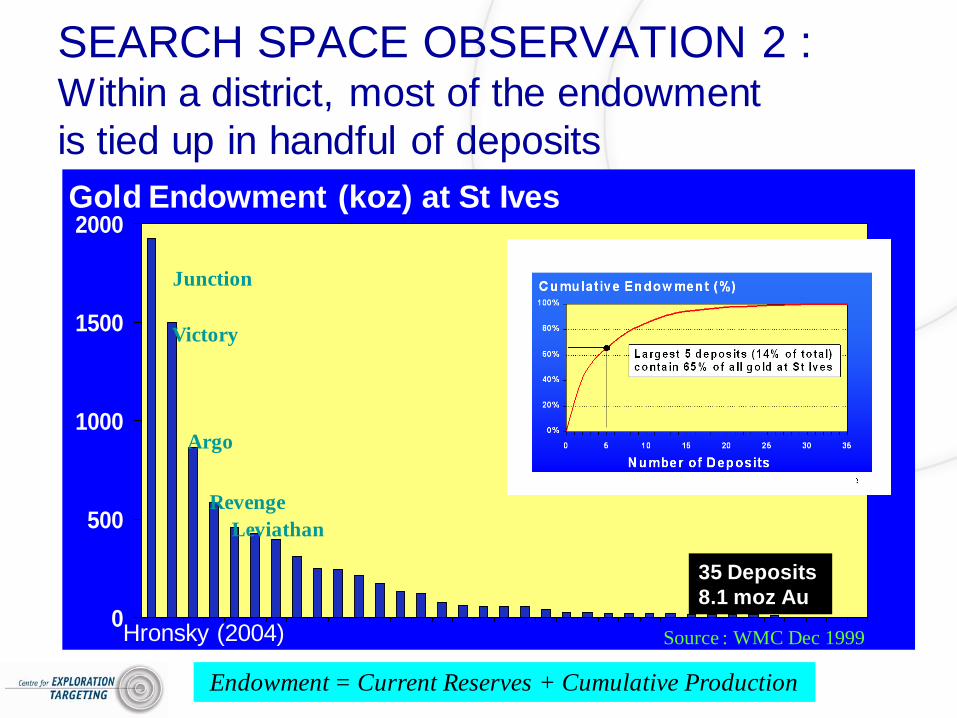

SEARCH SPACE OBSERVATION 2 :Within a district, most of the endowment is tied up in handful of deposits

0

500

1000

1500

2000

Junction

LeviathanRevenge

Argo

Victory

35 Deposits8.1 moz Au

Gold Endowment (koz) at St Ives

Endowment = Current Reserves + Cumulative Production

Source : WMC Dec 1999Hronsky (2004)

0.00.51.01.52.02.53.03.54.0

1960 1970 1980 1990 2000 2010

Minor (<10kt Ni)Moderate (10-100kt Ni)Major (100-1000kt Ni)Giant (>1000kt Ni)

Discovery Year

Total = 12.71mtexcluding 0.14mt in deposits with no

published discovery date

Source: R.Schodde (2004)

Mt Ni

Hronsky (2004)

SEARCH SPACE OBSERVATION 3 Largest deposits are generally found first - Yilgarn NiS

Greenfields

Brownfields

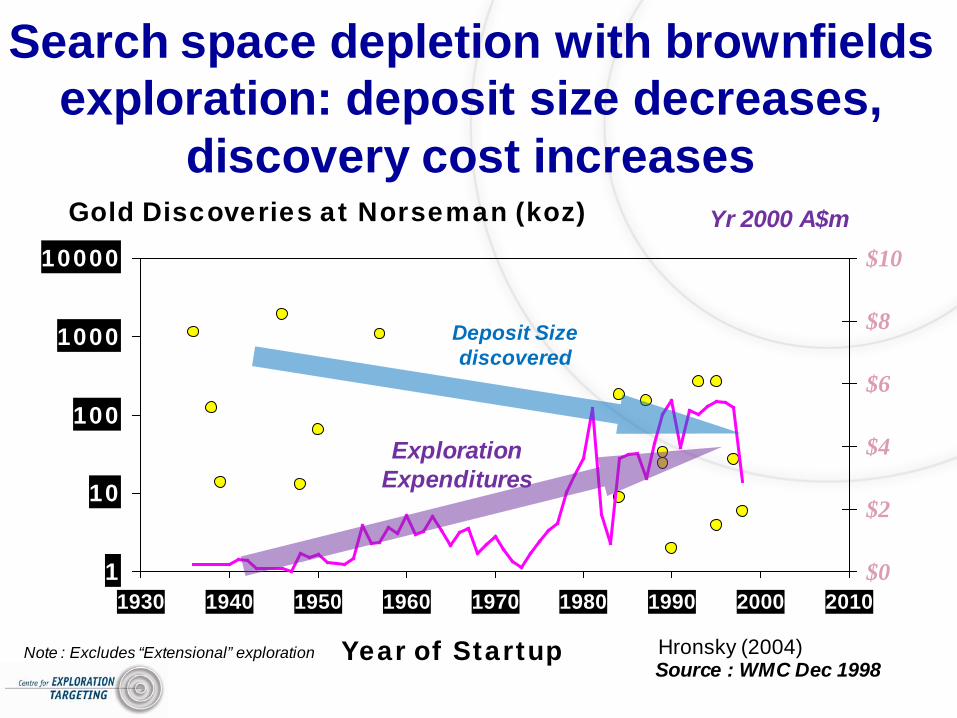

Search space depletion with brownfieldsexploration: deposit size decreases,

discovery cost increases

1

10

100

1000

10000

1930 1940 1950 1960 1970 1980 1990 2000 2010$0

$2

$4

$6

$8

$10

Year of Startup

Exploration Expenditures

Yr 2000 A$m

Note : Excludes “Extensional” exploration

Gold Discoveries at Norseman (koz)

Deposit Size discovered

Source : WMC Dec 1998Hronsky (2004)

New mineral provinces required

0

10

20

30

1900 1920 1940 1960 1980 2000 2020

Mine Production (mtpa Cu metal)

Sources: US Geological Survey (1900-83), Brook Hunt (1984 onwards)

Brook-Hunt Q3 2006 forecast

Copper consumption over the last 25 years accounted for half of all copper metal ever mined

in the world

World consumption over the next 25 years will exceed all of copper metal ever mined

to date

2005

1981

2030

Average 3.4% pa growth rate 1900-81 Average

2.0% pa 1982-2005

Average 3.2% pa

1986-2030

Schodde, 2007

Social pressures and deposit qualityPhysical and socio-economic footprintCarbon footprint

Success may look different in the future!- A focus on high quality deposits required

Current industry practice not inline with new paradigm

– External (equity market) and internal (remuneration packages and KPI) measures foster short-term thinking and short term results

– Results in focus on brownfields AT EXPENSE of greenfields

– Trend of majors away from exploration to acquisition, focus on extraction technologies

– Expectation that Juniors will fill the greenfields gap– A common belief that metal prices will sort out supply

All of these ideologies are fundamentally challenged looking to the future

Commitment to discovery: global non-ferrous exploration expenditures and metal prices

1989-2009

Sources: MEG and IAEA (for uranium 1989-2006)

US$ Billion of the day Relative Metal Price (1989 =1.0)

Richard Schodde

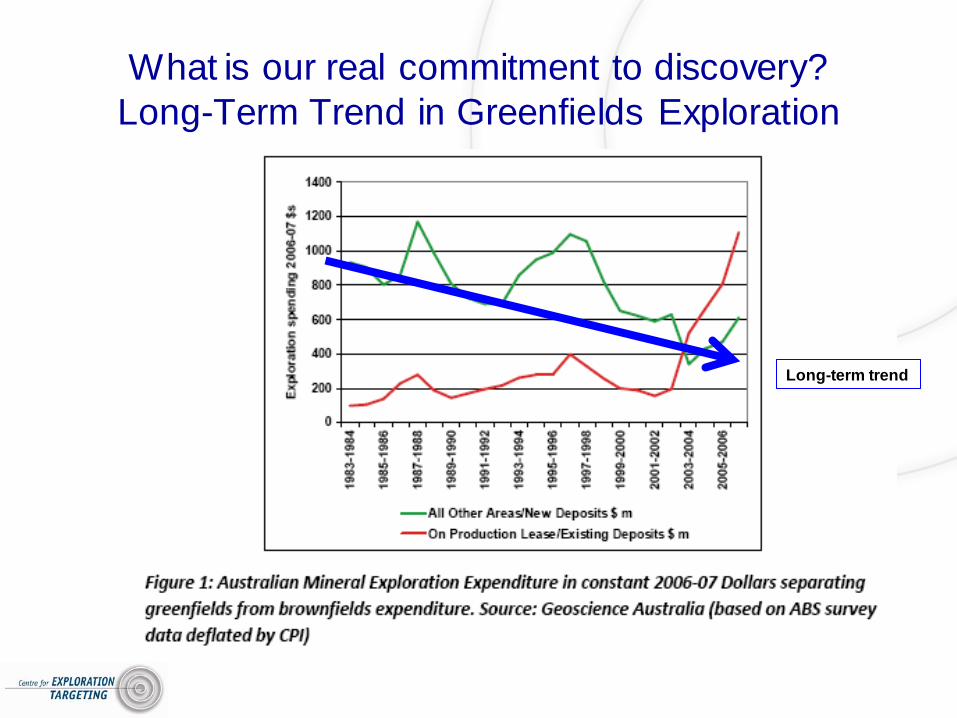

What is our real commitment to discovery?Long-Term Trend in Greenfields Exploration

Long-term trend

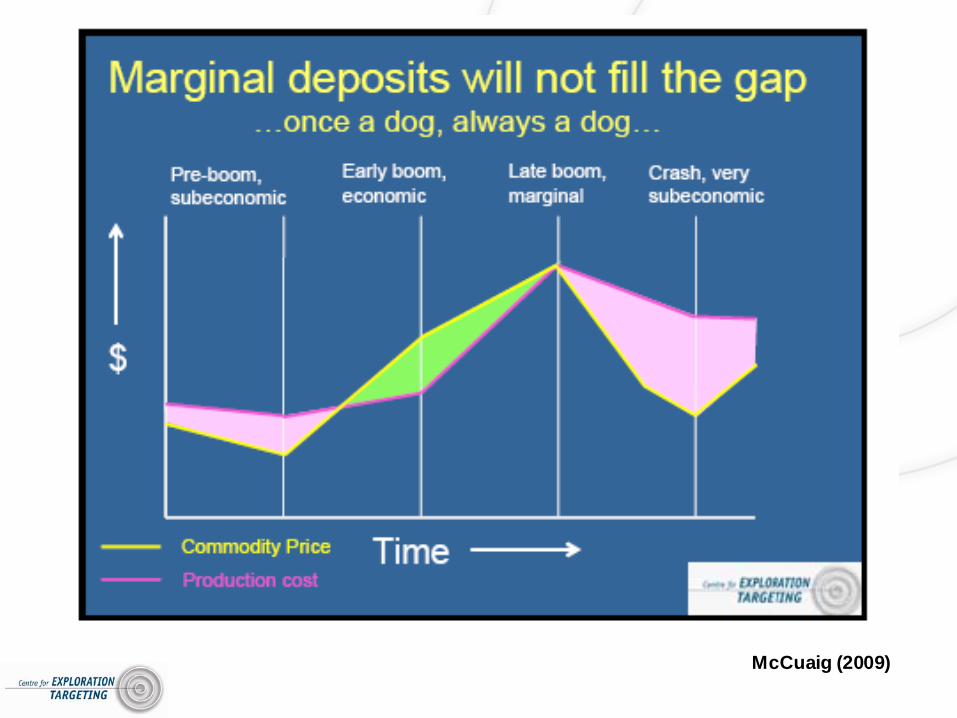

Juniors will not do the greenfields!

• Fundamental assumption is that greenfields exploration (and its inherent risks) will be outsourced to Juniors

• But structure of Juniors’ funding mitigates against greenfields exploration strategies

• Will metal prices simply sort it out? • There is a long list of marginal projects that could

potentially be economic with a sustained metal price rise

McCuaig (2009)

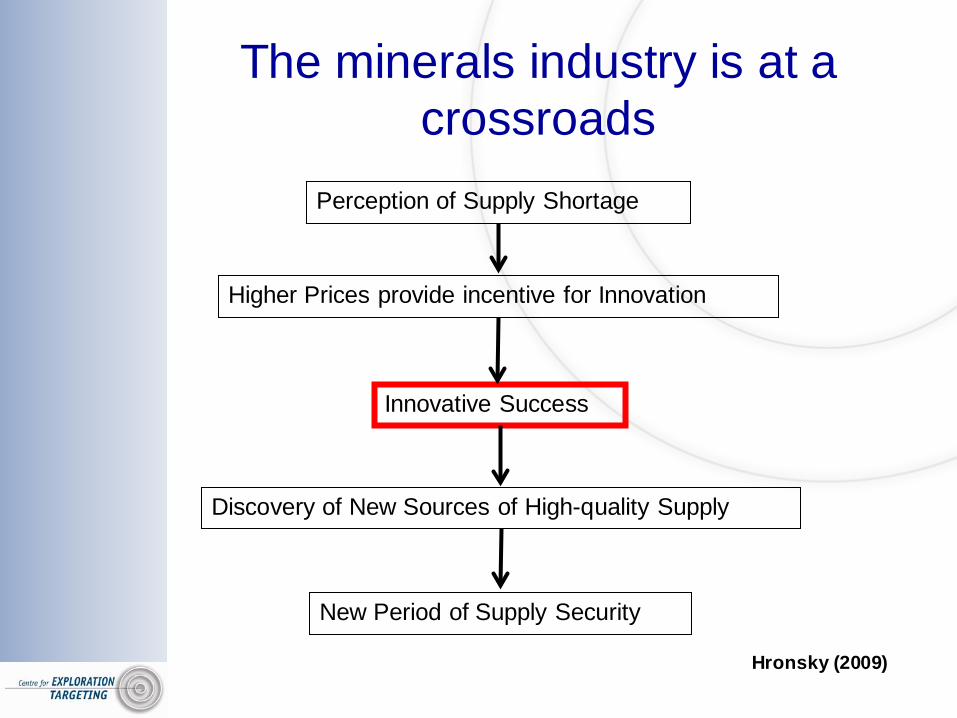

The minerals industry is at a crossroads

Perception of Supply Shortage

Higher Prices provide incentive for Innovation

Innovative Success

Discovery of New Sources of High-quality Supply

New Period of Supply Security

Hronsky (2009)

Innovation expanding search space:A Petroleum example

After 40 years of technology development…Think of this as mineral exploration under cover

The Minerals Example: Exploration Cost is the Key Barrier to Mining Deep High-Quality Orebodies

Hronsky (2005)

0

10

20

30

40

50

60

200 400 600 800 1000

DEPTH TO TOP OF OREBODY

IRR

(%)

0200400600800100012001400

NPV

(A$

M)

IRR NPV

Modelling for a Voisey’s Bay style orebody in remote WA(30 Mt @ 2.5% Ni, 2.0% Cu; 20m thick 60 degree dip)

Targeting new greenfields discoveries

• Our ability to mine at depth far outstrips our ability to explore at depth

• Requires an innovation in deep exploration technology• The key innovation is more accurate targeting of

mineralised volumes of rock under cover• Requires a shift from deposit model style concepts to

mineral system style concepts• Requires translation of understanding of mineral system

model into effective targeting model

Targeting approaches• Empirical

– correlations of geoscience datasets with known mineral deposits in well-explored, data-rich terranes

– Harder to apply in the new search space under cover

• Conceptual– Combination of geological elements from

mineral deposit models– mineral systems approaches

in reality, targeting approaches are a mixture between empirical and conceptual

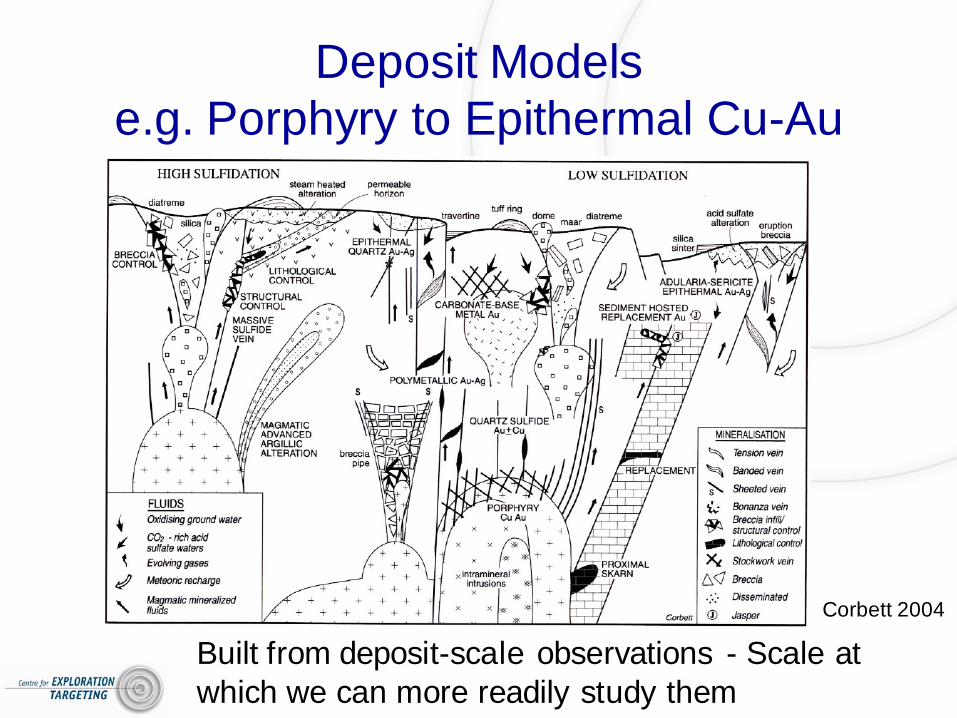

Deposit Modelse.g. Porphyry to Epithermal Cu-Au

Corbett 2004

Built from deposit-scale observations - Scale at which we can more readily study them

Deposit models - limitations• Often focus on one aspect of system, not holistic• Often too many ‘variations on a theme’ for

• Struggle to be predictive– Where predictive = local scale– Finds analogues of what you have already found

• Show that giant deposits and small showings often have similar fluids and deposit scale features (Groves, 2009)– E.g. fertile magmas hard to differentiate from infertile

on deposit scale (Cooke et al, 2009)

Deposit models struggle to be predictive

• We have a much better (albeit very incomplete) understanding of the processes controlling mineralisationthan 40 years ago

• So our targeting must be more effective, yes?– No– Find new deposits in brownfields, but struggle to find new ore

systems in greenfields terranes

• DEPOSIT MODELS ARE AT WRONG SCALE for large scale greenfields exploration decisions!

after McCuaig and Hronsky 2000

Prediction-detection tradeoff

LOWBROAD REGIONAL

PREDICTION

HIGH

PROSPECT SCALESCALE

RELA

TIVE

EFFE

CTI

VENE

SS DETECTION

Camp scale decision

A mineral systems approach

Focus must be on understanding the geological PROCESSES as opposed to CHARACTERISTICS

SEA LEVEL

INC

R. T

EM

PE

RA

TU

RE

WIT

H D

EP

TH

?

?

Sourcefor metals& brinesTiming

ofmovement

Migrationpathway -

rockinteractions

"Trap"controlled

by fluid-rockinteractions/P-T

"Seal"controlspathway

"Trap"controlled by

fluid-rockinteractions/P-T

fluid-fluidfluid-gas

Source - Release - Migration - Trap - Seal

Source(s) - Migration - Throttle - Scrubber

Critical Success Factors

Mass trapping

Mass scrubbing

Target Generation from Mineral Systems –Orogenic Au

Critical Processes (ranking level)

Constituent Processes (thinking level)

Targeting Elements (Geological features indicating the processes)Translation into mappable targeting criteria (proxies and predictor maps)

Source - fluid, magma, metals

Active Pathway

Physical throttle

Preservation

Reaction with wallrock reduces metal solubility

Pressure change induces chemical change and reduces solubility

Remote sensing response

Key alteration minerals

Rocks of favourable chemistry

lithogeochemistry

Recognise a chemical gradient

Weight by confidence, quality, support

Manually or through automated process query datasets for combination of evidence

Fluid Mixing

Chemical scrubber

Geophysical response

Solid geology interpretation

Pilbara Craton

Yilgarn Craton

Musgraves

Warakurna LIP

Craton margins

Tier 1 NiS deposits

Granitoid NdTM after Cassidy and Champion 2007

Controls on location of large mineral systems

Paleocraton margins

Yilgarn Au after Robert et al. 2005

Scale dependence of Targeting Elements - Au

McCuaig et al., in review OGR

Scale dependence of Targeting Elements – Komatiite Ni-Cu-S

McCuaig et al., in review OGR

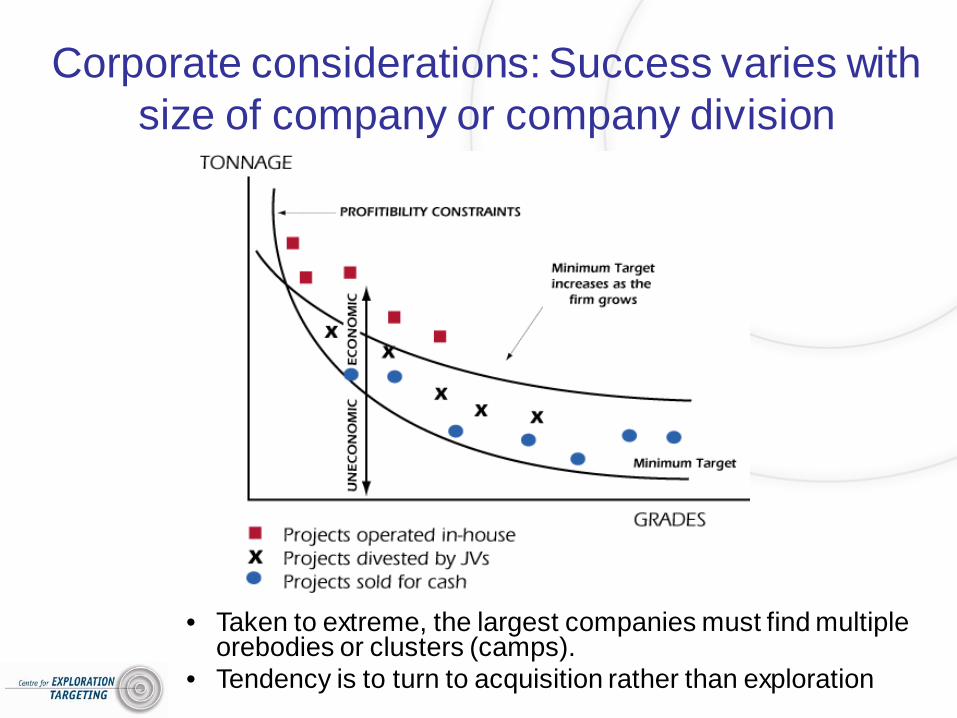

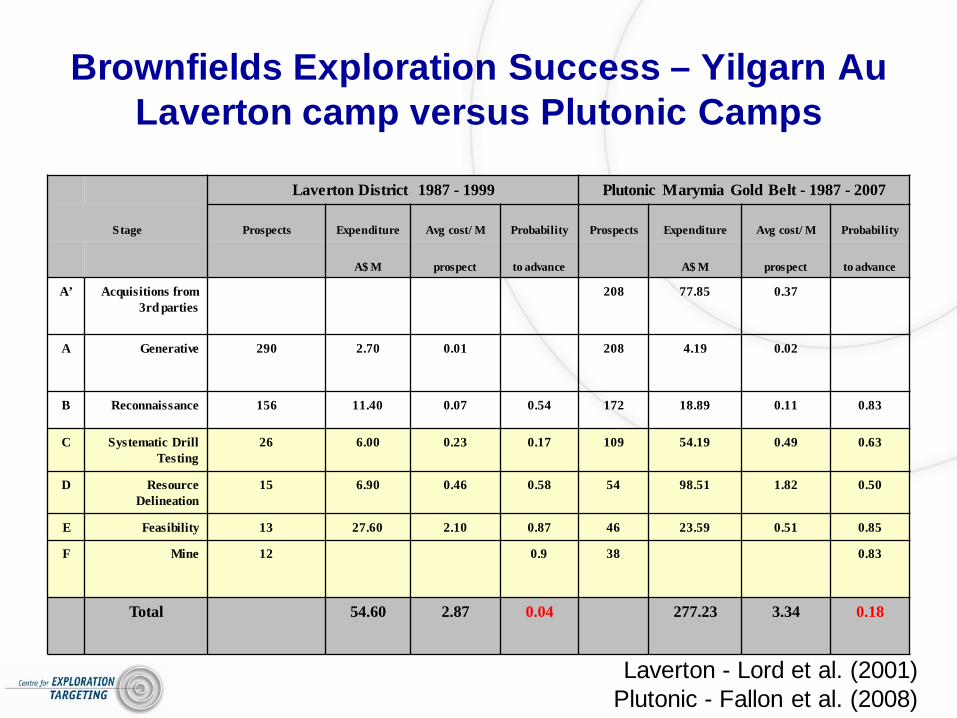

Corporate considerations: Success varies with size of company or company division

• Taken to extreme, the largest companies must find multiple orebodies or clusters (camps).

• Tendency is to turn to acquisition rather than exploration

Links to Targeting Strategy

• Any targeting strategy must be based on an understanding of the degree of depletion of the relevant search space (i.e. “exploration maturity”) for the target province (or district, or camp)

• Need to know when to walk away from an area (in a technical sense) – two requirements– Requires you know what success is TO YOU– Requires you can estimate residual endowment

• How can we estimate residual endowment?

300

200

100

01965 1970 1975 1980 1985 1990 1995 2000

Year of discovery

Komatiite-associated Ni-Cu deposits, Kambalda Region,Eastern Goldfields Province, Western Australia

Kt nickelmetal

production

andreserves

(2000)

Current endowmentInitial reserves

LARGEST DEPOSITS NORMALLY DISCOVERED

IN EARLY YEARS OF EXPLORATION IN

DISTRICT

Hronsky and Groves (2008)

Largest deposits found earlybut may not be recognised as largest! – how to tell?

Can we use this size-frequency relationship?

0

500

1000

1500

2000

Junction

LeviathanRevenge

Argo

Victory

35 Deposits8.1 moz Au

Gold Endowment (koz) at St Ives

Endowment = Current Reserves + Cumulative Production

US$ 0.25 M US$ 0.5 M US$ 0.75 MAverage cost of a greenfield exploration program

Preferred combination

Guj and Bartrop (2009) Based on MEG data of greenfieldsexploration spend and greenfields discoveries 1998-2004

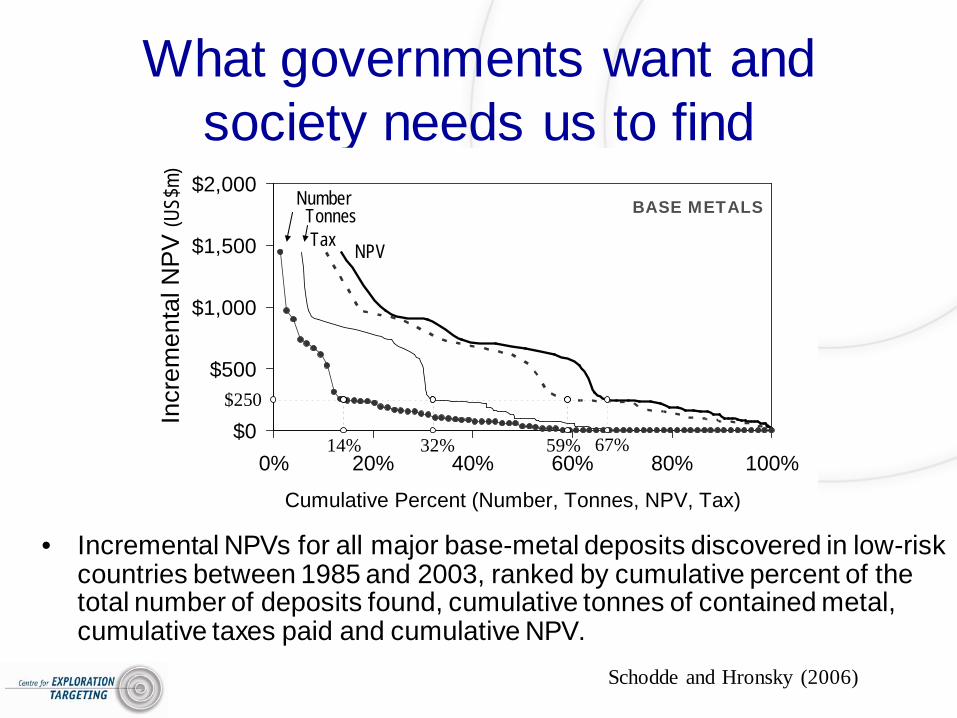

What governments want and society needs us to find

• Incremental NPVs for all major base-metal deposits discovered in low-risk countries between 1985 and 2003, ranked by cumulative percent of the total number of deposits found, cumulative tonnes of contained metal, cumulative taxes paid and cumulative NPV.

$0

$500

$1,000

$1,500

$2,000

0% 20% 40% 60% 80% 100%

Cumulative Percent (Number, Tonnes, NPV, Tax)

NPV

TonnesNumber

Tax

$250

67%32%14% 59%

BASE METALS

Incr

emen

tal N

PV (U

S$m)

Schodde and Hronsky (2006)

Conclusion

• The Mineral industry will be forced to undergo a paradigm shift over the next ten years to a focus on seeking quality greenfields discoveries– More dependence on accurate conceptual targeting– Exploration systems that closely estimate probability of

success and monitor performance– Development of exploration technologies that will allow

us to explore new search spaces cost effectively

• The petroleum industry was forced to commence this shift over 30 years ago