How Progression of FERA to FEMA has helped Indian markets for healthy growth & decent Forex reserves Prepared by: Ashish Anchaliya (03) Jay Barchha (05) Rahul Govil (07) Swati Jain (09) Vipin Kumar (11) NMIMS

Transcript

How Progression of FERA to FEMA has helped Indian markets for healthy growth & decent Forex

reserves

Prepared by:

Ashish Anchaliya (03)

Jay Barchha (05)

Rahul Govil (07)

Swati Jain (09)

Vipin Kumar (11)

NMIMS

FERA TO FEMA:

Independence ushered in a complex web of controls for all external transactions through a legislation i.e., Foreign Exchange Regulation Act (FERA), 1947. There were further amendments made to the FERA in 1973 where the regulation was intensified. The policy was designed around the need to conserve Foreign Exchange Reserves for essential imports such as Petroleum goods and food grains. The year 1991 was an important milestone for the Economy. There was a paradigm shift in the Foreign Exchange Policy. It moved from an Import Substitution strategy to Export Promotion with sufficient Foreign Exchange Reserves. The adequacy of the Reserves was determined by the Guidotti Rule, though the actual implementation of the rule was modified to meet our requirements. As a result of measures initiated to liberalize capital inflows, India’s Foreign Exchange Reserves (mainly foreign currency assets) have increased from US$6 billion at end-March 1991 to US$270 billion2 as on 9th November 2007. It would be useful to note that the Reserves accretion can be attributed to large Foreign Capital Inflow that could not be absorbed in the economy. This has been as a result of shift of funds from developed economies to emerging markets like India, China and Russia.

From Foreign Exchange Control to Management (FERA to FEMA)

In the 1990s, consistent with the general philosophy of economic reforms a sea change relating to the broad approach to reform in the external sector took place. The Report of the High Level Committee on Balance of Payments (Chairman: Dr. C. Rangarajan, 1993) set the broad agenda in this regard. The Committee recommended the following:

The introduction of a market-determined exchange rate regime within limits Liberalization of current account transactions leading to current account

convertibility;

Compositional shift in capital flows away from debt to non debt creating flows;

Strict regulation of external commercial borrowings, especially short-term debt;

Discouraging volatile elements of flows from non-resident Indians; full freedom for outflows associated with inflows (i.e., principal, interest, dividend, profit and sale proceeds) and gradual liberalization of other outflows;

Dissociation of Government in the intermediation of flow of external assistance, as in the 1980s, receipts on capital account and external financing were confined to external assistance through multilateral and bilateral sources.

The sequence of events in the subsequent years generally followed these recommendations. In 1993, exchange rate of rupee was made market determined; close on the heels of this important step, India accepted Article VIII of the Articles of Agreement of the International Monetary Fund in August 1994 and adopted the current account convertibility. In June 2000 a legal framework, with implementation of FEMA, was put into effect to ensure convertibility on the current account.

Capital Account liberalization approach

Globalization of the world economy is a reality that makes opening up of the capital account and integration with global economy an unavoidable process. Today capital account liberalization is not a choice. The capital account liberalization primarily aims at liberalizing controls that hinder the international integration and diversification of domestic savings in a portfolio of home assets and foreign assets and allows agents to reap the advantages of diversification of assets in the financial and real sector. However, the benefits of capital mobility come with certain risks which should be categorized and managed through a combination of administrative measures, gradual opening up of prudential restrictions and safeguards to contain these risks.

Current scenario

The main objectives in managing a stock of reserves for any developing country, including India, are preserving their long-term value in terms of purchasing power over goods and services, and minimizing risk and volatility in returns. After the East Asian crises of 1997, India has followed a policy to build higher levels of Foreign Exchange Reserves that take into account not only anticipated current account deficits but also liquidity at risk arising from unanticipated capital movements. Accordingly, the primary objectives of maintaining Foreign Exchange Reserves in India are safety and liquidity; maximizing returns is considered secondary. In India, reserves are held for precautionary and transaction motives to provide confidence to the markets, those foreign obligations can always be met. The Reserve Bank of India (RBI), in consultation with the Government of India, currently manages Foreign Exchange Reserves. As the objectives of reserve management are liquidity and safety, attention is paid to the currency composition and duration of investment, so that a significant proportion can be converted into cash at short notice.

The Foreign Exchange Regulation Act of 1973 (FERA) in India was repealed on 1st June, 2000. It was replaced by the Foreign Exchange Management Act (FEMA), which was passed in the winter session of Parliament in 1999. Enacted in 1973, in the backdrop of acute shortage of Foreign Exchange in the country, FERA had a controversial 27 year stint during which many bosses of the Indian Corporate world found themselves at the mercy of the Enforcement Directorate (E.D.). Any offense under FERA was a criminal offense liable to imprisonment, whereas FEMA seeks to make offenses relating to foreign exchange civil offenses. FEMA, which has replaced FERA, had become the need of the hour since FERA had become incompatible with the pro-liberalization policies of the Government of India. FEMA has brought a new management regime of Foreign Exchange consistent with the emerging frame work of the World Trade Organization (WTO). It is another matter that enactment of FEMA also brought with it Prevention of Money Laundering Act, 2002 which came into effect recently from 1st July, 2005 and the heat of which is yet to be felt as “Enforcement Directorate” would be investigating the cases under PMLA too.

Unlike other laws where everything is permitted unless specifically prohibited, under FERA nothing was permitted unless specifically permitted. Hence the tenor and tone of the Act was very drastic. It provided for imprisonment of even a very minor offence. Under FERA, a

person was presumed guilty unless he proved himself innocent whereas under other laws, a person is presumed innocent unless he is proven guilty.

Objectives and Extent of FEMA

The objective of the Act is to consolidate and amend the law relating to foreign exchange with the objective of facilitating external trade and payments and for promoting the orderly development and maintenance of foreign exchange market in India. FEMA extends to the whole of India. It applies to all branches, offices and agencies outside India owned or controlled by a person who is a resident of India and also to any contravention there under committed outside India by any person to whom this Act applies.

Except with the general or special permission of the Reserve Bank of India, no person can :-

deal in or transfer any foreign exchange or foreign security to any person not being an authorized person;

make any payment to or for the credit of any person resident outside India in any manner;

receive otherwise through an authorized person, any payment by order or on behalf of any person resident outside India in any manner;

Reasonable restrictions for current account transactions as may be prescribed.

Any person may sell or draw foreign exchange to or from an authorized person for a capital account transaction. The Reserve Bank may, in consultation with the Central Government, specify:-

any class or classes of capital account transactions which are permissible; the limit up to which foreign exchange shall be admissible for such transactions

However, the Reserve Bank cannot impose any restriction on the drawing of foreign exchange for payments due on account of amortization of loans or for depreciation of direct investments in the ordinary course of business.

The Reserve Bank can, by regulations, prohibit, restrict or regulate the following:-

Transfer or issue of any foreign security by a person resident in India; Transfer or issue of any security by a person resident outside India;

Transfer or issue of any security or foreign security by any branch, office or agency in India of a person resident outside India;

Any borrowing or lending in foreign exchange in whatever form or by whatever name called;

Any borrowing or tending in rupees in whatever form or by whatever name called between a person resident in India and a person resident outside India;

Deposits between persons resident in India and persons resident outside India;

Export, import or holding of currency or currency notes;

Transfer of immovable property outside India, other than a lease not exceeding five years, by a person resident in India;

Acquisition or transfer of immovable property in India, other than a lease not exceeding five years, by a person resident outside India;

Giving of a guarantee or surety in respect of any debt, obligation or other liability incurred

(i) By a person resident in India and owed to a person resident outside India or

(ii) By a person resident outside India.

A person, resident in India may hold, own, transfer or invest in foreign currency, foreign security or any immovable property situated outside India if such currency, security or property was acquired, held or owned by such person when he was resident outside India or inherited from a person who was resident outside India.

A person resident outside India may hold, own, transfer or invest in Indian currency, security or any immovable property situated in India if such currency, security or property was acquired, held or owned by such person when he was resident in India or inherited from a person who was resident in India.

The Reserve Bank may, by regulation, prohibit, restrict, or regulate establishment in India of a branch, office or other place of business by a person resident outside India, for carrying on any activity relating to such branch, office or other place of business. Every exporter of goods and services must:-

Furnish to the Reserve Bank or to such other authority a declaration in such form and in such manner as may be specified, containing true and correct material particulars, including the amount representing the full export value or, if the full export value of the goods is not ascertainable at the time of export, the value which the exporter, having regard to the prevailing market conditions, expects to receive on the sale of the goods in a market outside India;

Furnish to the Reserve Bank such other information as may be required by the Reserve Bank for the purpose of ensuring the realization of the export proceeds by such exporter.

The Reserve Bank may, for the purpose of ensuring that the full export value of the goods or such reduced value of the goods as the Reserve Bank determines, having regard to the prevailing market-conditions, is received without any delay, direct any exporter to comply with such requirements as it deems fit. Where any amount of foreign exchange is due or has accrued to any person resident in India, such person shall take all reasonable steps to realize and repatriate to India such foreign exchange within such period and in such manner as may be specified by the Reserve Bank.

FEMA Rules & Policies

The Foreign Exchange Management Act, 1999 (FEMA) came into force with effect from June 1, 2000. With the introduction of the new Act in place of FERA, certain structural changes were brought in. The Act consolidates and amends the law relating to foreign exchange to facilitate external trade and payments, and to promote the orderly development and maintenance of foreign exchange in India.

From the NRI perspective, FEMA broadly covers all matters related to foreign exchange, investment avenues for NRIs such as immovable property, bank deposits, government bonds, investment in shares, units and other securities, and foreign direct investment in India.

FEMA vests with the Reserve Bank of India, the sole authority to grant general or special permission for all foreign exchange related activities mentioned above.

Section 2 - The Act here provides clarity on several definitions and terms used in the context of foreign exchange. Starting with the identification of the Non-resident Indian and Persons of Indian origin, it defines “foreign exchange” and “foreign security” in sections 2(n) and 2(o) respectively of the Act. It describes at length the foreign exchange facilities and where one can buy foreign exchange in India. FEMA defines an authorised dealer, and addresses the permissible exchange allowed for a business trip, for studies and medical treatment abroad, forex for foreign travel, the use of an international credit card, and remittance facility

Section 3 prohibits dealings in foreign exchange except through an authorised person. Similarly, without the prior approval of the RBI, no person can make any payment to any person resident outside India in any manner other than that prescribed by it. The Act restricts non-authorised persons from entering into any financial transaction in India as consideration for or in association with acquisition or creation or transfer of a right to acquire any asset outside India.

Section 4 restrains any person resident in India from acquiring, holding, owning, possessing or transferring any foreign exchange, foreign security or any immovable property situated outside India except as specifically provided in the Act.

Section 6 deals with capital account transactions. This section allows a person to draw or sell foreign exchange from or to an authorised person for a capital account transaction. RBI in consultation with the Central Government has issued various regulations on capital account transactions in terms of sub-sect ion (2) and (3) of section 6.

Section 7 covers the export of goods and services. All exporters are required to furnish to the RBI or any other authority, a declaration regarding full export value.

Section 8 puts the responsibility of repatriation on the persons resident in India who have any amount of foreign exchange due or accrued in their favour to get the same realised and repatriated to India within the specific period and in the manner specified by the RBI.

The duties and liabilities of the Authorised Dealers have been dealt with in Sections 10, 11 and 12, while Sections 13 to 15 cover penalties and enforcement of the orders of the Adjudicating Authority as well as the power to compound contraventions under the Act.

NOSTRO AND VOSTRO ACCOUNTS

International accounting procedures between Local banks and overseas banks often involve the use of nostro and vostro accounts.

A nostro (means "ours" in Latin) account is an account maintained by a Local bank with a foreign bank that allows the Local bank to buy foreign currency. A vostro (means "yours" in Latin) account is an account maintained by an overseas bank with a Local bank that allows the overseas bank to purchase Local currency. The system of nostro and vostro accounts facilitates foreign exchange dealings and settlements and allows the settlement of currency transactions between the Country's (Local)Bank and foreign banks.

Example : When X (Buyer) a trader in Base Country wants to purchase $5000 worth of goods by paying cash. Mr.X deposits the cash in his local bank in the country's currency for the corresponding amount ($5000) then a swift message is sent to the corresponding bank in the foreign country where the local bank holds a NOSTRO account requesting the bank to make the payment to Y (Seller) in his local currency i.e. US Dollars. Thus facilitating the trade between X & Y. IF Y wanted to buy something from X then the foreign bank would complete the deal using their VOSTRO account in X's country

Latest Developments with regards to Nostro accounts

RBI has asked banks to reconcile & closely monitor nostro accounts

The Reserve Bank of India (RBI) has advised banks to minimize the number of nostro accounts to have a better control over reconciliation and put in place a system of fast reconciliation and close monitoring of pending items in nostro accounts by top management at short intervals. Banks are also advised to leverage technology to avoid building up of such unreconciled balances.

RBI has been receiving representations from banks expressing practical difficulties and involvement of substantial expenditure in the elimination of outstanding entries in nostro accounts after the lapse of certain time. RBI in it’s circular dated May 11, 2009, has reviewed the position about reconciliation of nostro account and treatment of outstanding entries and decided as under:

a) In respect of outstanding debit/credit entries of individual value USD 2500 and above or equivalent in nostro accounts, banks will continue to make efforts for reconciliation.

b) In respect of outstanding credit entries of individual value less than USD 2500 or equivalent in nostro account originated upto March 31, 2002:

(i) Banks may transfer to profit and loss account the credit balance arising out of the netting of entries pertaining to the period prior to April 1, 1996 parked in blocked account.

(ii)The amount credited to the profit and loss account should be appropriated to the general reserve and will not be available for declaration of dividend.

(iii) Appropriate disclosure should be made in the Notes to Accounts including the impact on the profit and loss account.

(iv) Any future claim in respect of these entries should be honoured.

c) Banks may at their discretion, write off the unreconciled debit entries of individual value less than USD 2500 or equivalent in nostro and mirror accounts originated upto March 31, 2002 against the provision already held in terms of the circular dated July 1, 1999.

d) All unreconciled credit entries in the nostro accounts originated on or after April 1, 2002 which are outstanding for more than 3 years may be transferred to Blocked Account and shown as outstanding liabilities which will be reckoned for the purpose of CRR/SLR.

e) Make 100 per cent provision in respect of all unreconciled debit entries in the nostro accounts originated on or after April 1, 2002 which are outstanding for more than two years (instead of three years as at present).

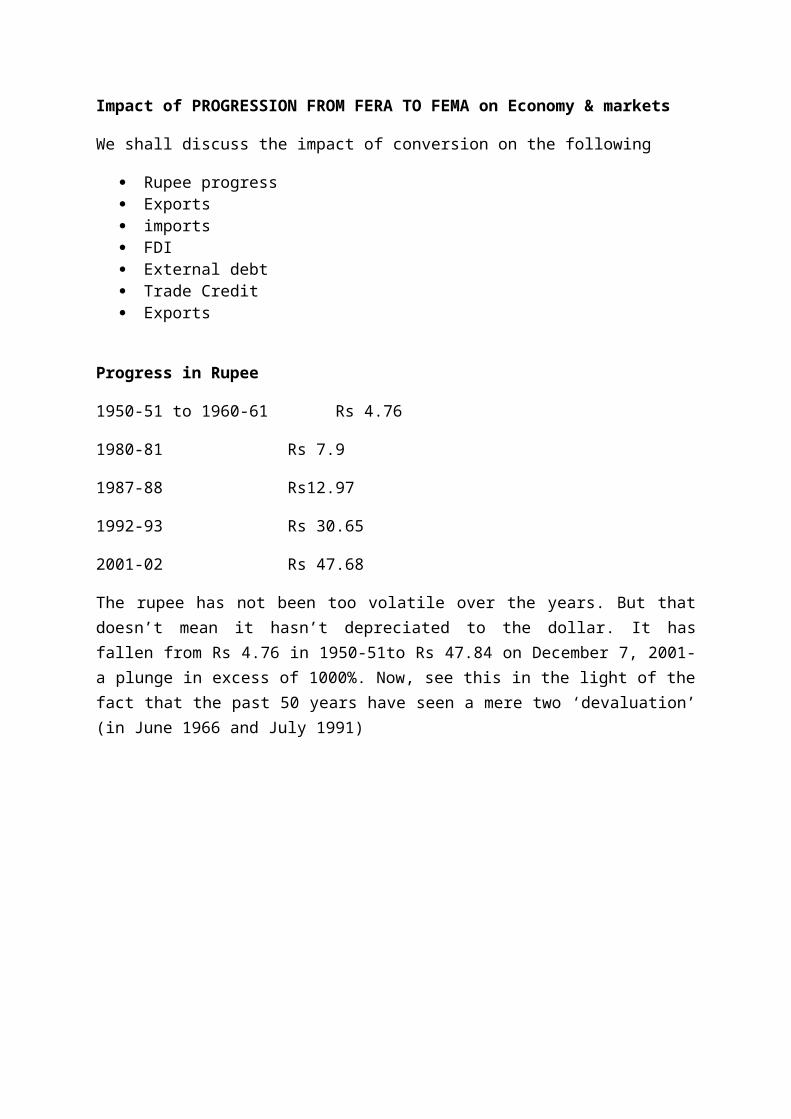

Impact of PROGRESSION FROM FERA TO FEMA on Economy & markets

We shall discuss the impact of conversion on the following

The rupee has not been too volatile over the years. But that doesn’t mean it hasn’t depreciated to the dollar. It has fallen from Rs 4.76 in 1950-51to Rs 47.84 on December 7, 2001-a plunge in excess of 1000%. Now, see this in the light of the fact that the past 50 years have seen a mere two ‘devaluation’ (in June 1966 and July 1991)

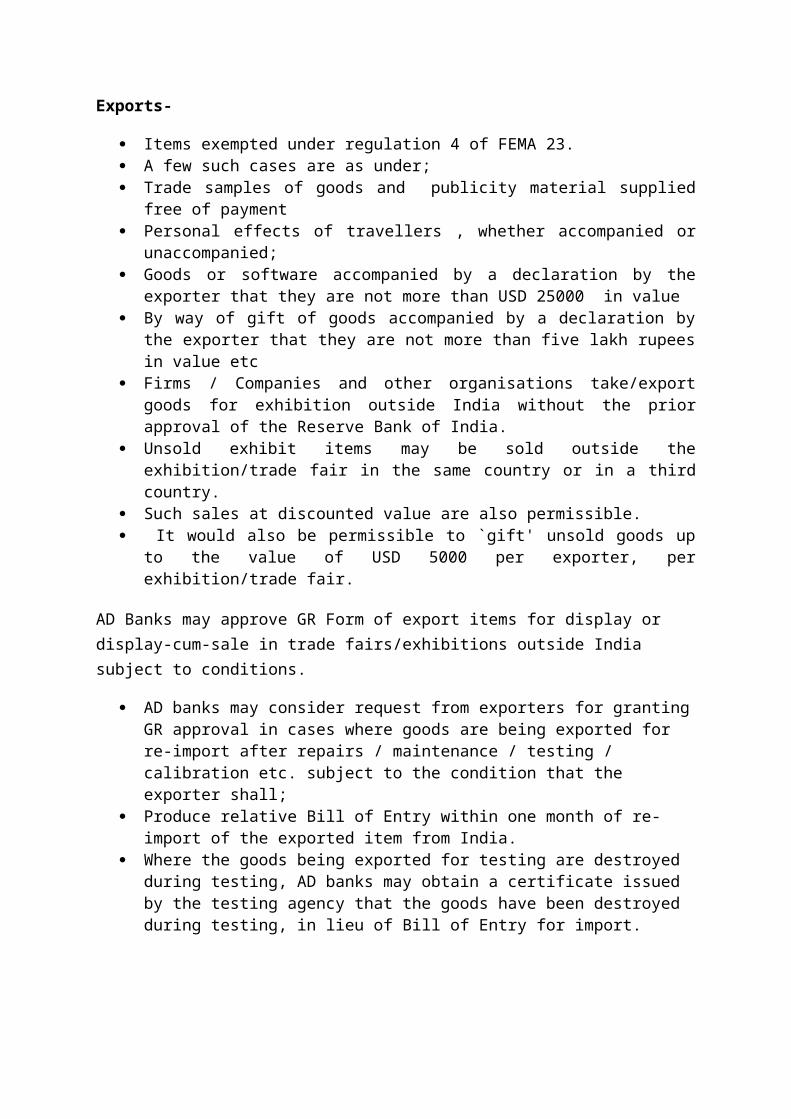

Exports-

Items exempted under regulation 4 of FEMA 23. A few such cases are as under; Trade samples of goods and publicity material supplied free of payment Personal effects of travellers , whether accompanied or unaccompanied; Goods or software accompanied by a declaration by the exporter that they are not

more than USD 25000 in value By way of gift of goods accompanied by a declaration by the exporter that they are

not more than five lakh rupees in value etc Firms / Companies and other organisations take/export goods for exhibition outside

India without the prior approval of the Reserve Bank of India. Unsold exhibit items may be sold outside the exhibition/trade fair in the same country

or in a third country. Such sales at discounted value are also permissible. It would also be permissible to `gift' unsold goods up to the value of USD 5000 per

exporter, per exhibition/trade fair.

AD Banks may approve GR Form of export items for display or display-cum-sale in trade fairs/exhibitions outside India subject to conditions.

AD banks may consider request from exporters for granting GR approval in cases where goods are being exported for re-import after repairs / maintenance / testing / calibration etc. subject to the condition that the exporter shall;

Produce relative Bill of Entry within one month of re-import of the exported item from India.

Where the goods being exported for testing are destroyed during testing, AD banks may obtain a certificate issued by the testing agency that the goods have been destroyed during testing, in lieu of Bill of Entry for import.

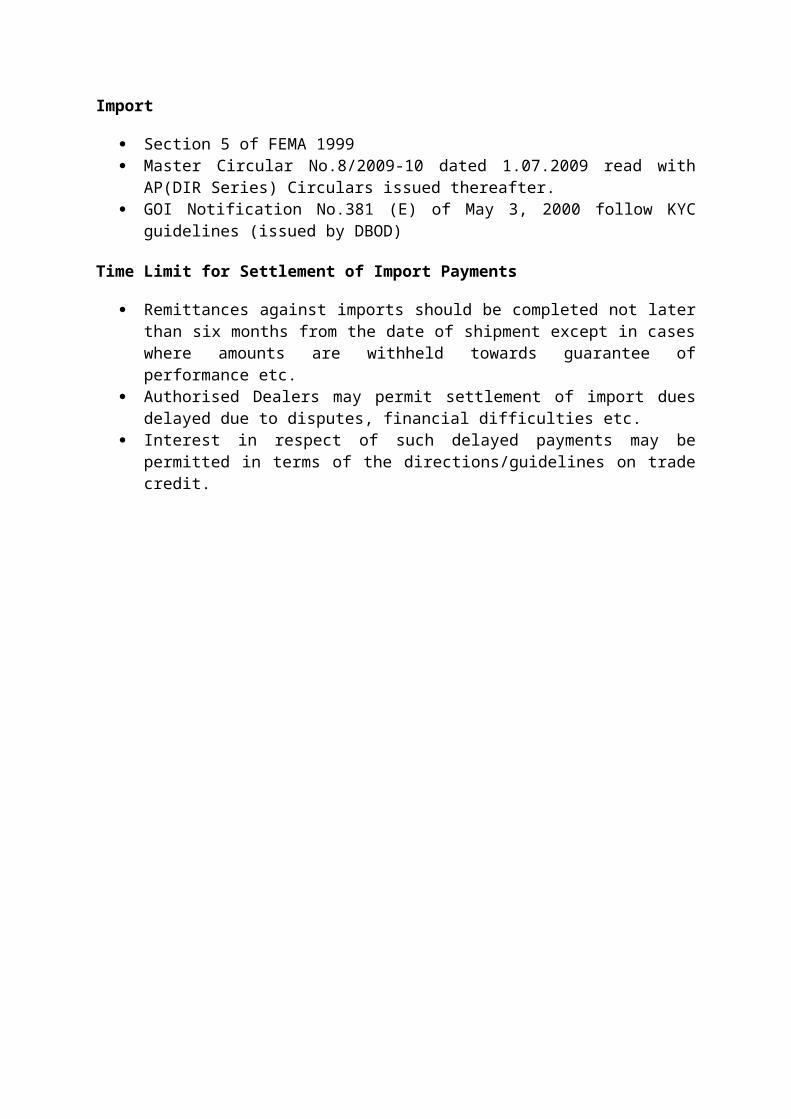

Import

Section 5 of FEMA 1999 Master Circular No.8/2009-10 dated 1.07.2009 read with AP(DIR Series) Circulars

issued thereafter. GOI Notification No.381 (E) of May 3, 2000 follow KYC guidelines (issued by

DBOD)

Time Limit for Settlement of Import Payments

Remittances against imports should be completed not later than six months from the date of shipment except in cases where amounts are withheld towards guarantee of performance etc.

Authorised Dealers may permit settlement of import dues delayed due to disputes, financial difficulties etc.

Interest in respect of such delayed payments may be permitted in terms of the directions/guidelines on trade credit.

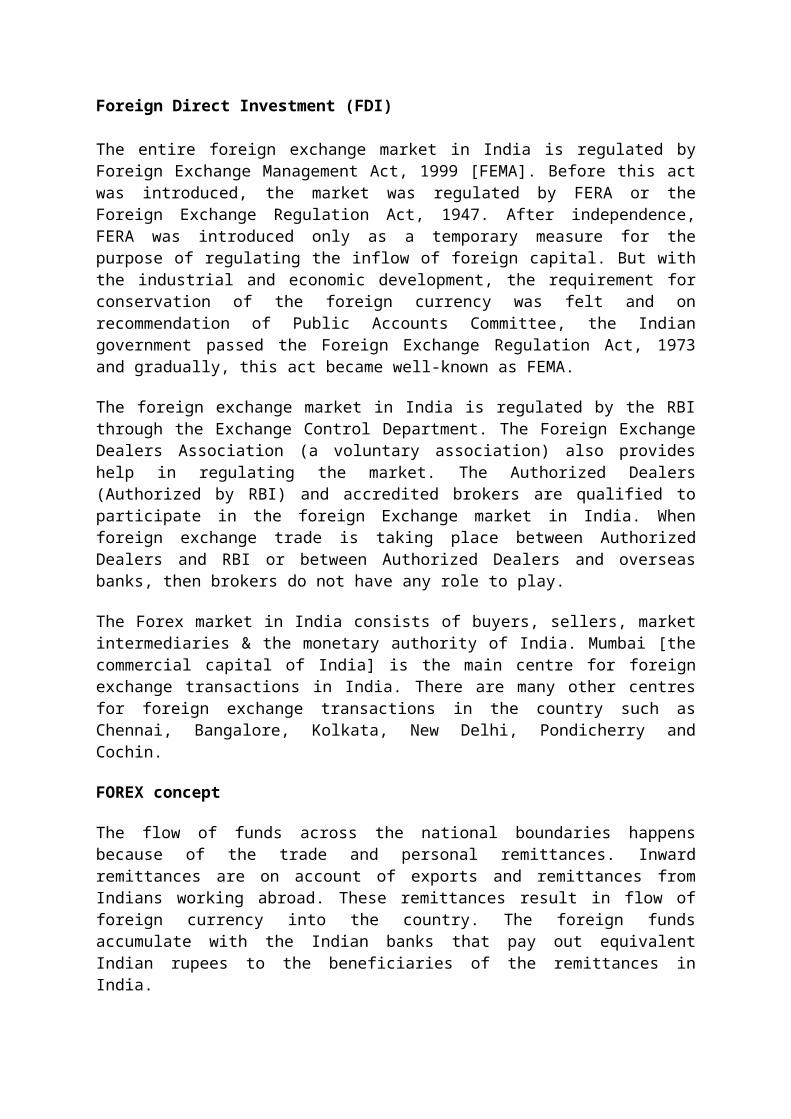

Foreign Direct Investment (FDI)

The entire foreign exchange market in India is regulated by Foreign Exchange Management Act, 1999 [FEMA]. Before this act was introduced, the market was regulated by FERA or the Foreign Exchange Regulation Act, 1947. After independence, FERA was introduced only as a temporary measure for the purpose of regulating the inflow of foreign capital. But with the industrial and economic development, the requirement for conservation of the foreign currency was felt and on recommendation of Public Accounts Committee, the Indian government passed the Foreign Exchange Regulation Act, 1973 and gradually, this act became well-known as FEMA.

The foreign exchange market in India is regulated by the RBI through the Exchange Control Department. The Foreign Exchange Dealers Association (a voluntary association) also provides help in regulating the market. The Authorized Dealers (Authorized by RBI) and accredited brokers are qualified to participate in the foreign Exchange market in India. When foreign exchange trade is taking place between Authorized Dealers and RBI or between Authorized Dealers and overseas banks, then brokers do not have any role to play.

The Forex market in India consists of buyers, sellers, market intermediaries & the monetary authority of India. Mumbai [the commercial capital of India] is the main centre for foreign exchange transactions in India. There are many other centres for foreign exchange transactions in the country such as Chennai, Bangalore, Kolkata, New Delhi, Pondicherry and Cochin.

FOREX concept

The flow of funds across the national boundaries happens because of the trade and personal remittances. Inward remittances are on account of exports and remittances from Indians working abroad. These remittances result in flow of foreign currency into the country. The foreign funds accumulate with the Indian banks that pay out equivalent Indian rupees to the beneficiaries of the remittances in India.

Indian banks accumulate the foreign currency funds in current accounts maintained with banks at foreign centers such as London and New York. Thus, foreign inward remittances result in increase in money in circulation. On the other hand, foreign outward remittances lead to contraction of money in circulation and outflow of foreign currency from the stock with Indian banks.

Banks having surplus foreign currency funds sells the funds to other Indian banks in exchange of Indian Rupees. If all banks have surplus foreign currency funds they sell these to the RBI. Balances in the foreign currency accounts of RBI become the foreign exchange reserve of the country.

Impact on money supply

In context of the Indian financial system, the relevant factor is that the increase in foreign currency reserves as a result of the larger foreign inward remittances, lead to increase in money supply; finding its way into the money market and capital market through the banking system.

Banks create credit and any inflow into the banking system gets multiplied by a factor. This factor depends on the reserves maintained by banks. If banks maintain n average reserve of 25%, any inflow into the banking system will increase money supply four times.

Similarly, any contraction of funds available with the banks will result in a four-fold reduction in money supply. Increase and decrease in the foreign exchange reserves of the country impact the financial system through increase or decrease in money supply.

Foreign Direct Investment [FDI] & Foreign Institutional Investors [FII]

Another aspect of Foreign Exchange market is that apart from flows resulting from personal and trade remittances, banks and corporate borrow funds from abroad and foreign entities invest in Indian business entities, such as Foreign Direct Investment [FDI], foreign funds and Foreign Institutional Investors [FII] that invest in the Indian capital markets. These flows are large in magnitude and have a great impact on capital market and the exchange rate.

However, there is also the danger that if FIIs pull out, the stock markets could crash which in turn can adversely impact the economy. This danger is not only on account of the impact of share prices but also because of the impact on exchange rate, which can adversely affect foreign trade and consequently the price level in the country.

External Debt

Major Highlights of External Debt

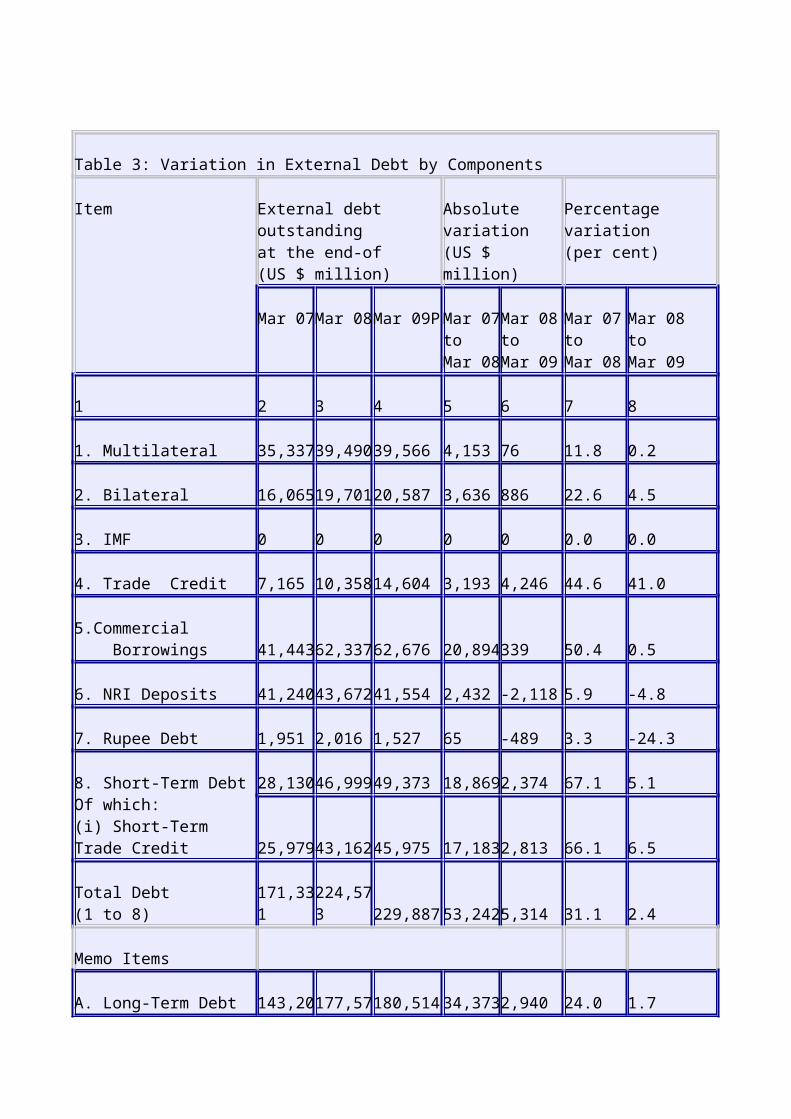

(i) India’s external debt, as at end-March 2009, was placed at US $ 229.9 billion (22.0 per cent of GDP) recording an increase of US $ 5.3 billion or 2.4 per cent over the level of the previous year mainly due to the increase in trade credits.

(ii) As per an international comparison of external debt of the twenty most indebted countries, India was the fifth most indebted country in 2007.

(iii) By way of composition of external debt, the share of commercial borrowings was the highest at 27.3 per cent as at end-March 2009 followed by short-term debt (21.5 per cent), NRI deposits (18.1 per cent) and multilateral debt (17.2 per cent).

(iv)The debt service ratio has declined steadily over the years, and stood at 4.6 per cent as at end-March 2009.

(v) Excluding the valuation effects due to appreciation of US dollar against other major currencies and Indian rupee, the stock of external debt would have increased by US$ 18.7 billion as compared with the stock as at end-March 2008.

(vi) The share of short-term debt in total debt increased to 21.5 per cent at end-March 2009 from 20.9 per cent at end-March 2008, primarily on account of rise in short-term trade credits.

(vii) Based on residual maturity, the short-term debt accounted for 40.6 per cent of the total external debt at end-March 2009

(viii) The ratio of short-term debt to foreign exchange reserves at 19.6 per cent in March 2009 was higher compared to 15.2 per cent in March 2008.

(ix) The US dollar continues to remain the dominant currency accounting for 57.1 per cent of the total external debt stock as at end-march 2009.

(x) India’s foreign exchange reserves provided a cover of 109.6 per cent to the external debt stock at the end of March 2009 as compared with 137.9 per cent as at end-March 2008.

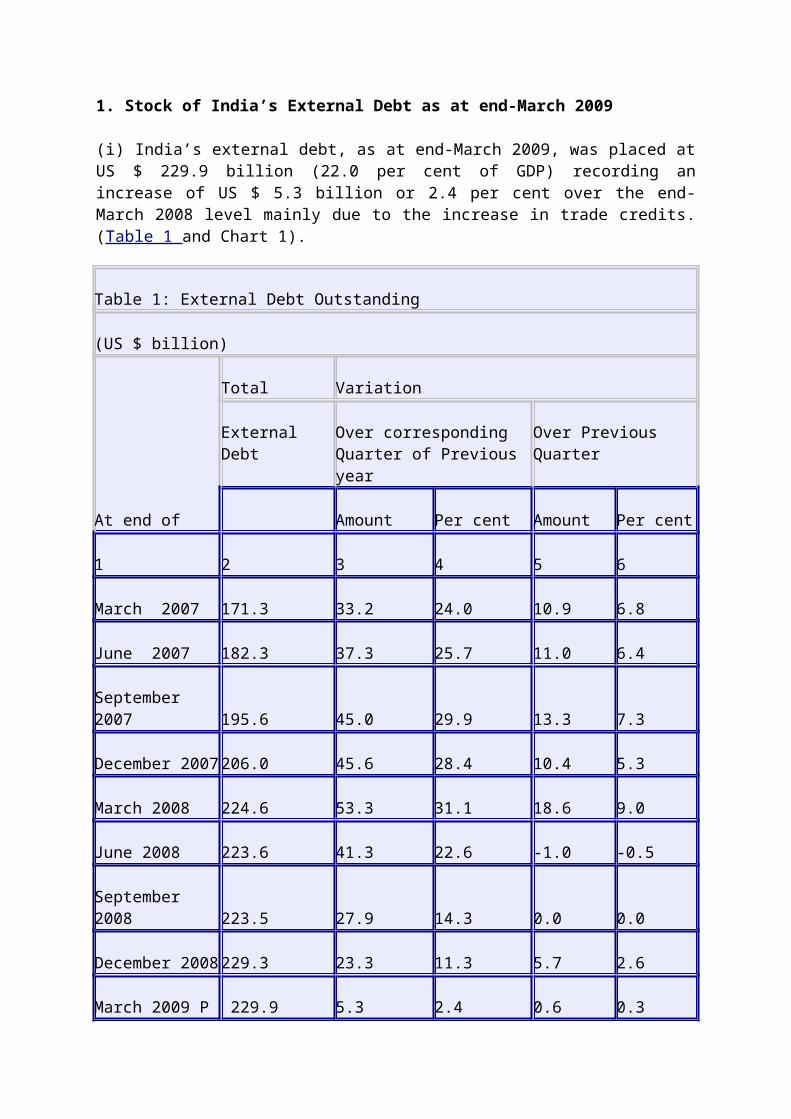

1. Stock of India’s External Debt as at end-March 2009

(i) India’s external debt, as at end-March 2009, was placed at US $ 229.9 billion (22.0 per cent of GDP) recording an increase of US $ 5.3 billion or 2.4 per cent over the end-March 2008 level mainly due to the increase in trade credits. (Table 1 and Chart 1).

Table 1: External Debt Outstanding

(US $ billion)

At end of

Total Variation

External Debt Over corresponding Quarter of Previous year

Over Previous Quarter

Amount Per cent Amount Per cent

1 2 3 4 5 6

March 2007 171.3 33.2 24.0 10.9 6.8

June 2007 182.3 37.3 25.7 11.0 6.4

September 2007 195.6 45.0 29.9 13.3 7.3

December 2007 206.0 45.6 28.4 10.4 5.3

March 2008 224.6 53.3 31.1 18.6 9.0

June 2008 223.6 41.3 22.6 -1.0 -0.5

September 2008 223.5 27.9 14.3 0.0 0.0

December 2008 229.3 23.3 11.3 5.7 2.6

March 2009 P 229.9 5.3 2.4 0.6 0.3

P: Provisional

Source: Ministry of Finance, Government of India and Reserve Bank of India.

2. Valuation Changes

(i) the valuation effect reflecting the appreciation of the US dollar against other major international currencies and Indian rupee resulted in a decline in India’s external debt by US $ 13.4 billion. This implies that excluding the valuation effects, the stock of external debt as

at end-March 2009 would have increased by US $ 18.7 billion over the level at end-March 2008.

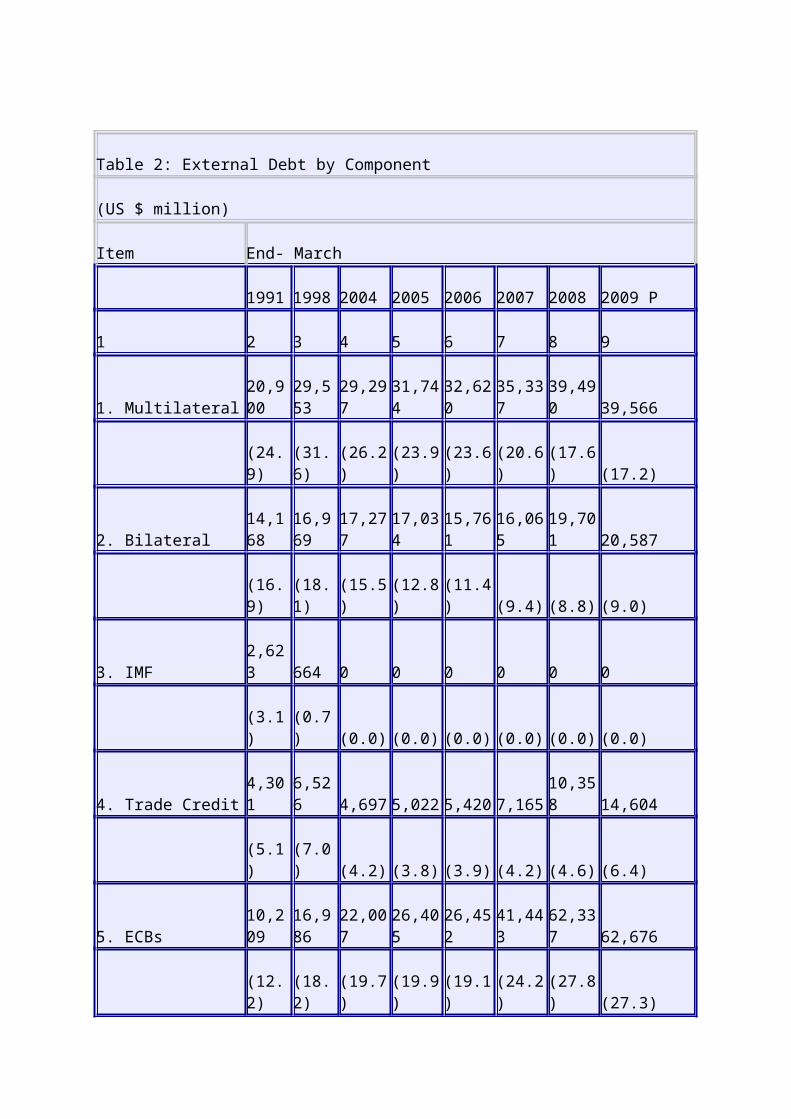

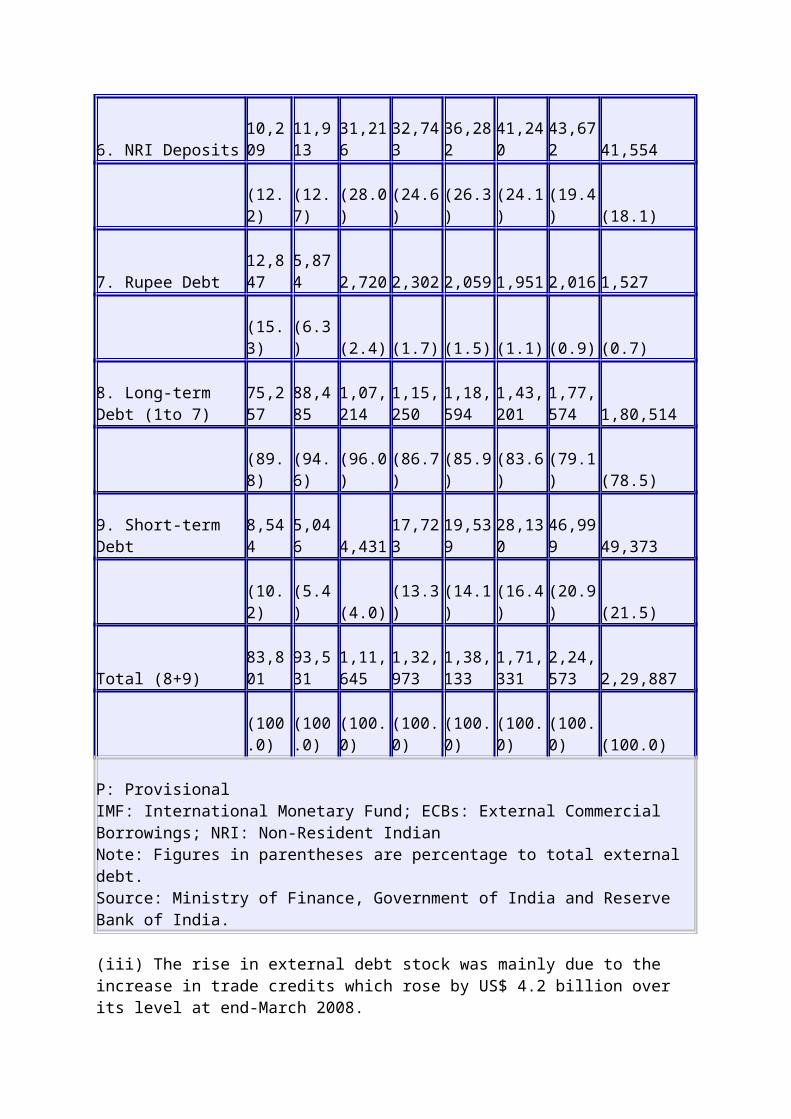

3. Components of External Debt

(i) By way of composition of external debt, the share of commercial borrowings was the highest at 27.3 per cent as at end-March 2009 followed by short-term debt (21.5 per cent), NRI deposits (18.1 per cent) and multilateral debt (17.2 per cent) (Table 2).

(ii) The long-term debt at US$ 180.5 billion and short-term debt at US$ 49.4 billion accounted for 78.5 per cent and 21.5 per cent, respectively, of the total external debt as at end-March 2009.

P: ProvisionalIMF: International Monetary Fund; ECBs: External Commercial Borrowings; NRI: Non-Resident IndianNote: Figures in parentheses are percentage to total external debt.Source: Ministry of Finance, Government of India and Reserve Bank of India.

(iii) The rise in external debt stock was mainly due to the increase in trade credits which rose by US$ 4.2 billion over its level at end-March 2008.

(iv) The short-term debt increased by US$ 2.4 billion as at end-March 2009 mainly on account of rise in short-term trade credits (Table 3 and Chart 2).

(v) Outstanding NRI deposits at US $ 41.6 billion as at end-March 2009 declined by US $ 2.1 billion over the level at end-March 2008 mainly due to valuation effects as there was positive inflows under NRI deposits during 2008-09.

Total Debt(1 to 8) 171,331 224,573 229,887 53,242 5,314 31.1 2.4

Memo Items

A. Long-Term Debt (1 to 7) 143,201 177,574 180,514 34,373 2,940 24.0 1.7

B. Short-Term Debt 28,130 46,999 49,373 18,869 2,374 67.1 5.1

P: ProvisionalSource: Ministry of Finance, Government of India and Reserve Bank of India.

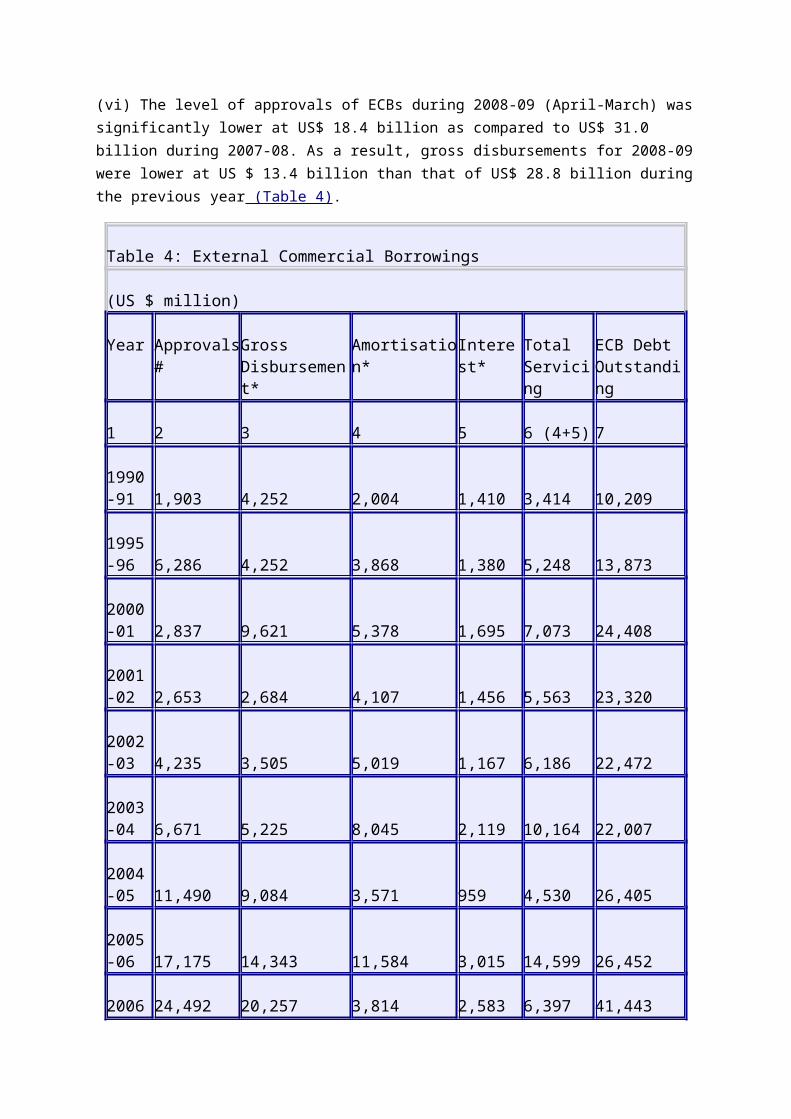

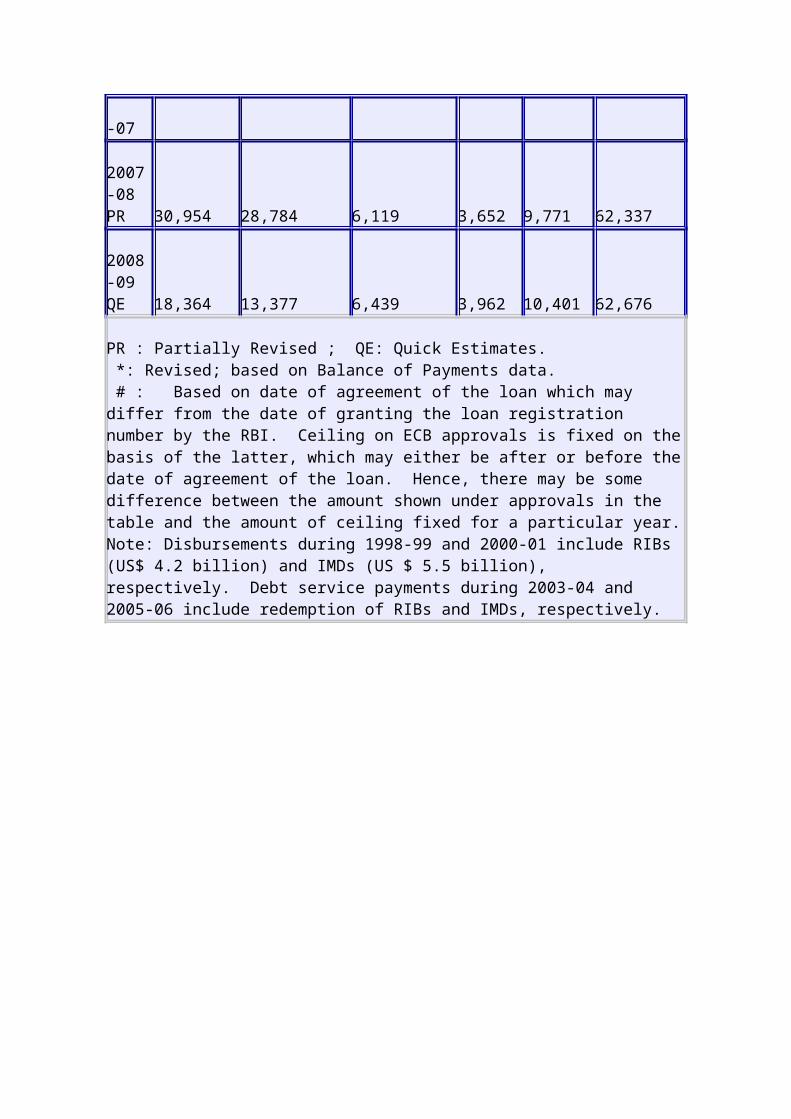

(vi) The level of approvals of ECBs during 2008-09 (April-March) was significantly lower at US$ 18.4 billion as compared to US$ 31.0 billion during 2007-08. As a result, gross disbursements for 2008-09 were lower at US $ 13.4 billion than that of US$ 28.8 billion during the previous year (Table 4).

Table 4: External Commercial Borrowings

(US $ million)

Year Approvals# Gross Disbursement*

Amortisation* Interest* Total Servicing

ECB Debt Outstanding

1 2 3 4 5 6 (4+5) 7

1990-91 1,903 4,252 2,004 1,410 3,414 10,209

1995-96 6,286 4,252 3,868 1,380 5,248 13,873

2000-01 2,837 9,621 5,378 1,695 7,073 24,408

2001-02 2,653 2,684 4,107 1,456 5,563 23,320

2002-03 4,235 3,505 5,019 1,167 6,186 22,472

2003-04 6,671 5,225 8,045 2,119 10,164 22,007

2004-05 11,490 9,084 3,571 959 4,530 26,405

2005-06 17,175 14,343 11,584 3,015 14,599 26,452

2006-07 24,492 20,257 3,814 2,583 6,397 41,443

2007-08 PR 30,954 28,784 6,119 3,652 9,771 62,337

2008-09 QE 18,364 13,377 6,439 3,962 10,401 62,676

PR : Partially Revised ; QE: Quick Estimates. *: Revised; based on Balance of Payments data. # : Based on date of agreement of the loan which may differ from the date of granting the loan registration number by the RBI. Ceiling on ECB approvals is fixed on the basis of the latter, which may either be after or before the date of agreement of the loan. Hence, there may be some difference between the amount shown under approvals in the table and the amount of ceiling fixed for a particular year.Note: Disbursements during 1998-99 and 2000-01 include RIBs (US$ 4.2 billion) and IMDs (US $ 5.5 billion), respectively. Debt service payments during 2003-04 and 2005-06 include redemption of RIBs and IMDs, respectively.

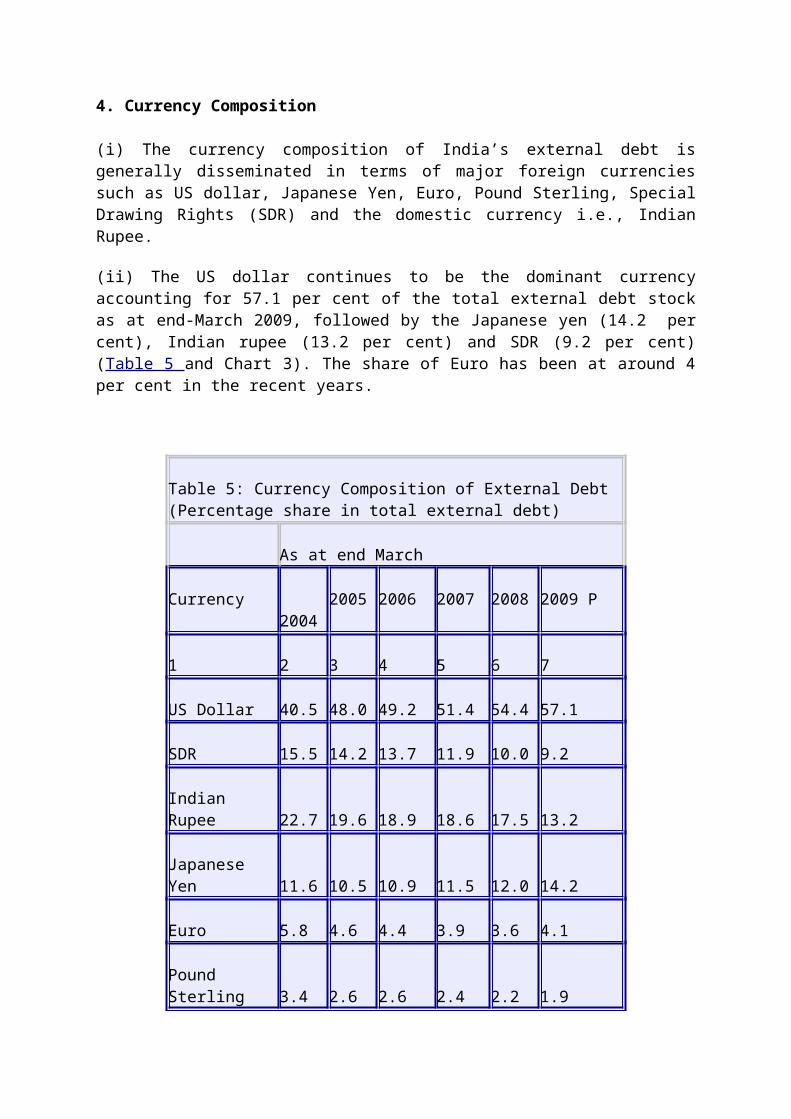

4. Currency Composition

(i) The currency composition of India’s external debt is generally disseminated in terms of major foreign currencies such as US dollar, Japanese Yen, Euro, Pound Sterling, Special Drawing Rights (SDR) and the domestic currency i.e., Indian Rupee.

(ii) The US dollar continues to be the dominant currency accounting for 57.1 per cent of the total external debt stock as at end-March 2009, followed by the Japanese yen (14.2 per cent), Indian rupee (13.2 per cent) and SDR (9.2 per cent) (Table 5 and Chart 3). The share of Euro has been at around 4 per cent in the recent years.

Table 5: Currency Composition of External Debt(Percentage share in total external debt)

As at end March

Currency 20042005 2006 2007 2008 2009 P

1 2 3 4 5 6 7

US Dollar 40.5 48.0 49.2 51.4 54.4 57.1

SDR 15.5 14.2 13.7 11.9 10.0 9.2

Indian Rupee 22.7 19.6 18.9 18.6 17.5 13.2

Japanese Yen 11.6 10.5 10.9 11.5 12.0 14.2

Euro 5.8 4.6 4.4 3.9 3.6 4.1

Pound Sterling 3.4 2.6 2.6 2.4 2.2 1.9

Others 0.5 0.5 0.3 0.3 0.3 0.3

Total 100.0 100.0 100.0 100.0 100.0 100.0

P: ProvisionalSource: Ministry of Finance, Government of India and Reserve Bank of India.

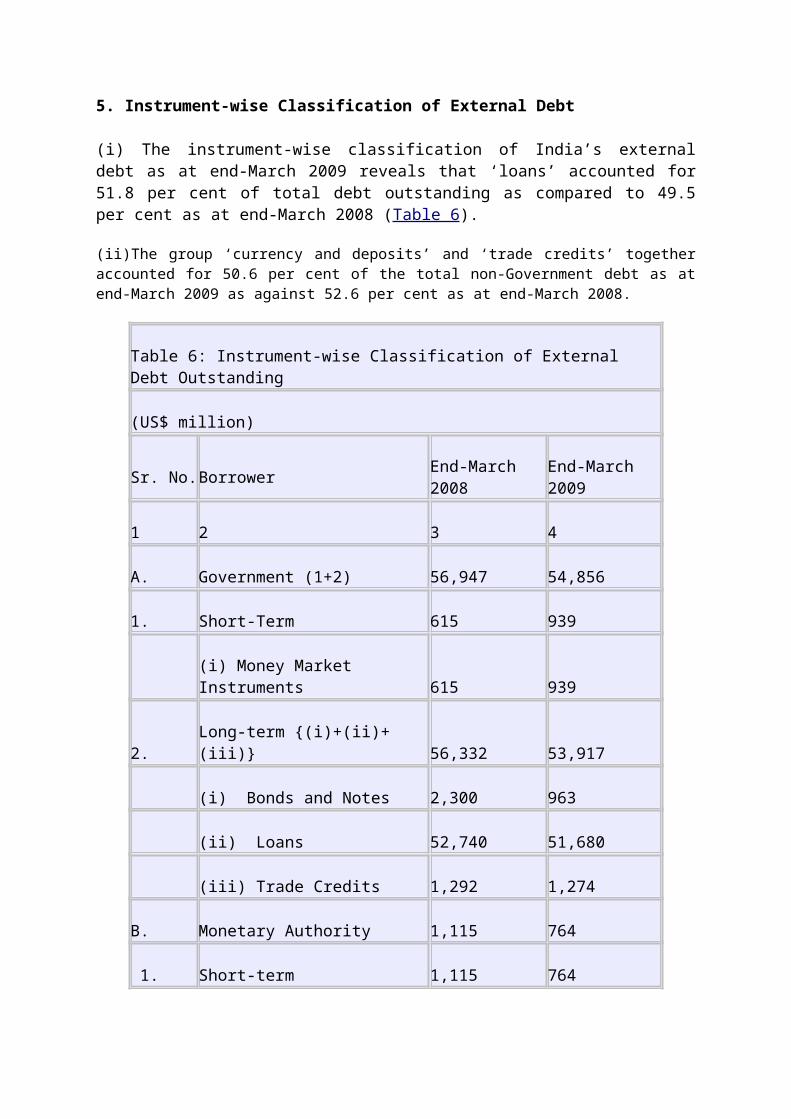

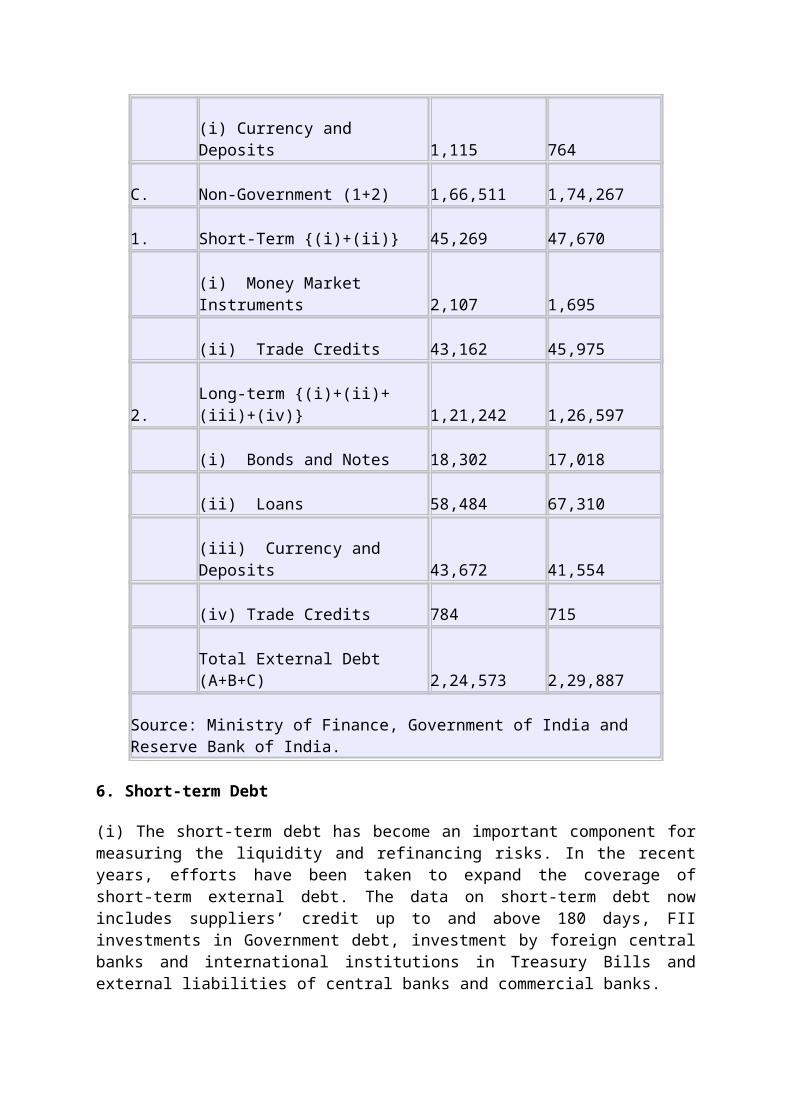

5. Instrument-wise Classification of External Debt

(i) The instrument-wise classification of India’s external debt as at end-March 2009 reveals that ‘loans’ accounted for 51.8 per cent of total debt outstanding as compared to 49.5 per cent as at end-March 2008 (Table 6).

(ii)The group ‘currency and deposits’ and ‘trade credits’ together accounted for 50.6 per cent of the total non-Government debt as at end-March 2009 as against 52.6 per cent as at end-March 2008.

Table 6: Instrument-wise Classification of External Debt Outstanding

Source: Ministry of Finance, Government of India and Reserve Bank of India.

6. Short-term Debt

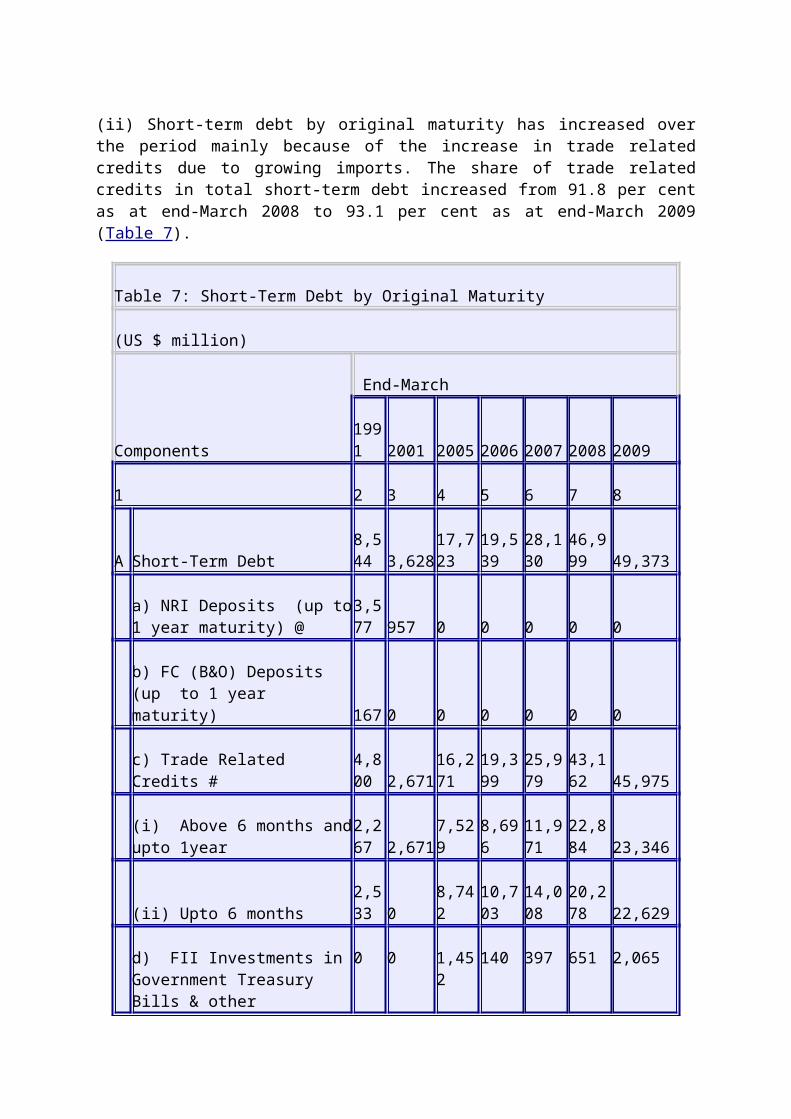

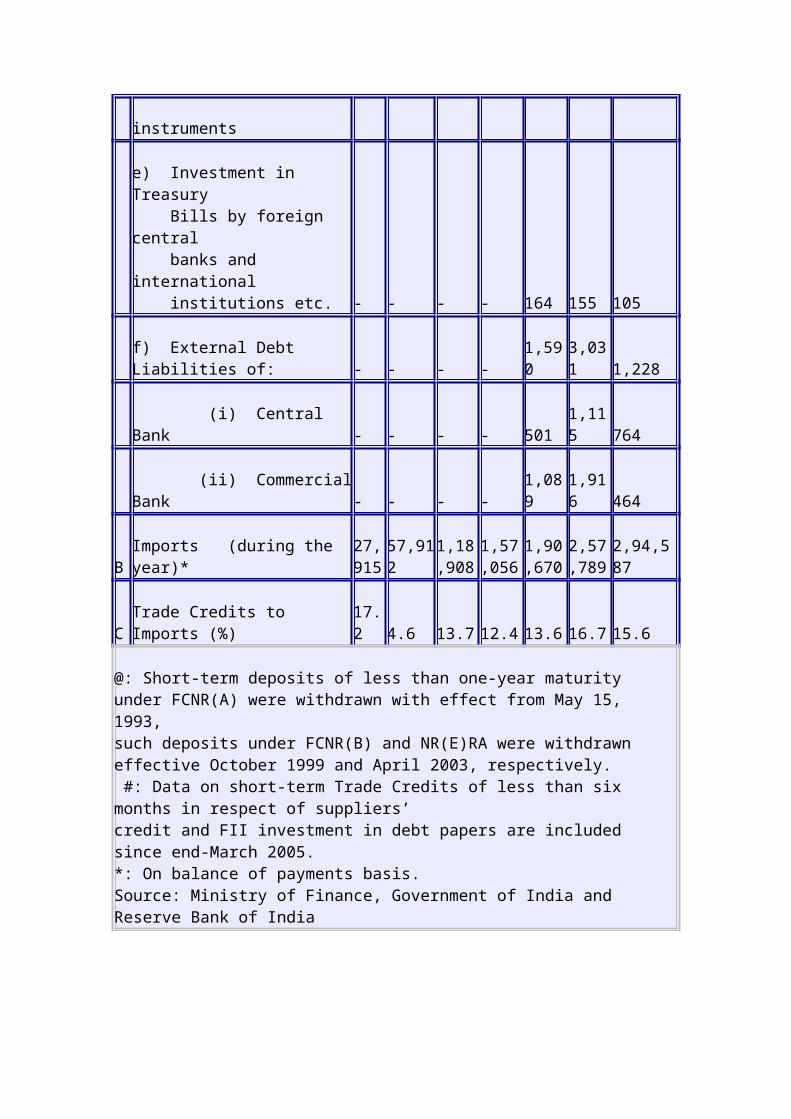

(i) The short-term debt has become an important component for measuring the liquidity and refinancing risks. In the recent years, efforts have been taken to expand the coverage of short-term external debt. The data on short-term debt now includes suppliers’ credit up to and above 180 days, FII investments in Government debt, investment by foreign central banks and international institutions in Treasury Bills and external liabilities of central banks and commercial banks.

(ii) Short-term debt by original maturity has increased over the period mainly because of the increase in trade related credits due to growing imports. The share of trade related credits in total short-term debt increased from 91.8 per cent as at end-March 2008 to 93.1 per cent as at end-March 2009 (Table 7).

Table 7: Short-Term Debt by Original Maturity

(US $ million)

Components

End-March

19912001 2005 2006 2007 2008 2009

1 2 3 4 5 6 7 8

A Short-Term Debt8,544 3,628 17,72319,53928,13046,99949,373

a) NRI Deposits (up to 1 year maturity) @

3,577 957 0 0 0 0 0

b) FC (B&O) Deposits (up to 1 year maturity) 167 0 0 0 0 0 0

c) Trade Related Credits #4,800 2,671 16,27119,39925,97943,16245,975

(i) Above 6 months and upto 1year

2,267 2,671 7,529 8,696 11,97122,88423,346

(ii) Upto 6 months2,533 0 8,742 10,70314,00820,27822,629

C Trade Credits to Imports (%) 17.2 4.6 13.7 12.4 13.6 16.7 15.6

@: Short-term deposits of less than one-year maturity under FCNR(A) were withdrawn with effect from May 15, 1993,such deposits under FCNR(B) and NR(E)RA were withdrawn effective October 1999 and April 2003, respectively. #: Data on short-term Trade Credits of less than six months in respect of suppliers’credit and FII investment in debt papers are included since end-March 2005.*: On balance of payments basis.Source: Ministry of Finance, Government of India and Reserve Bank of India

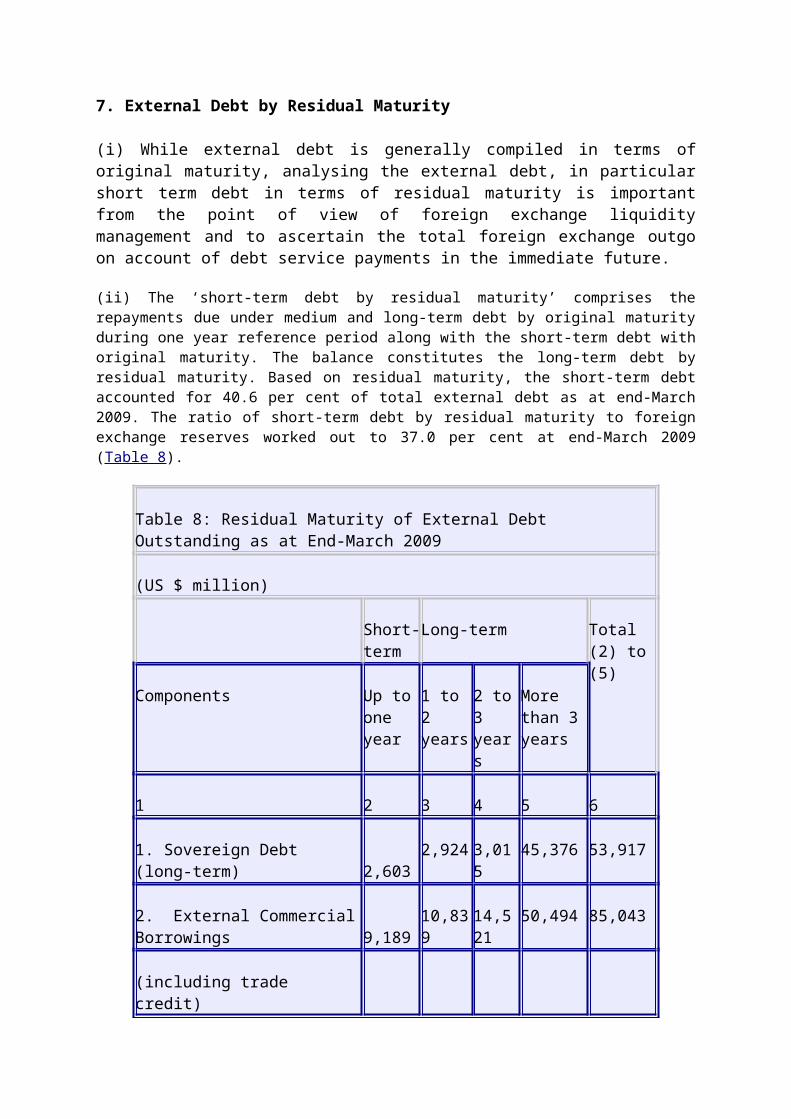

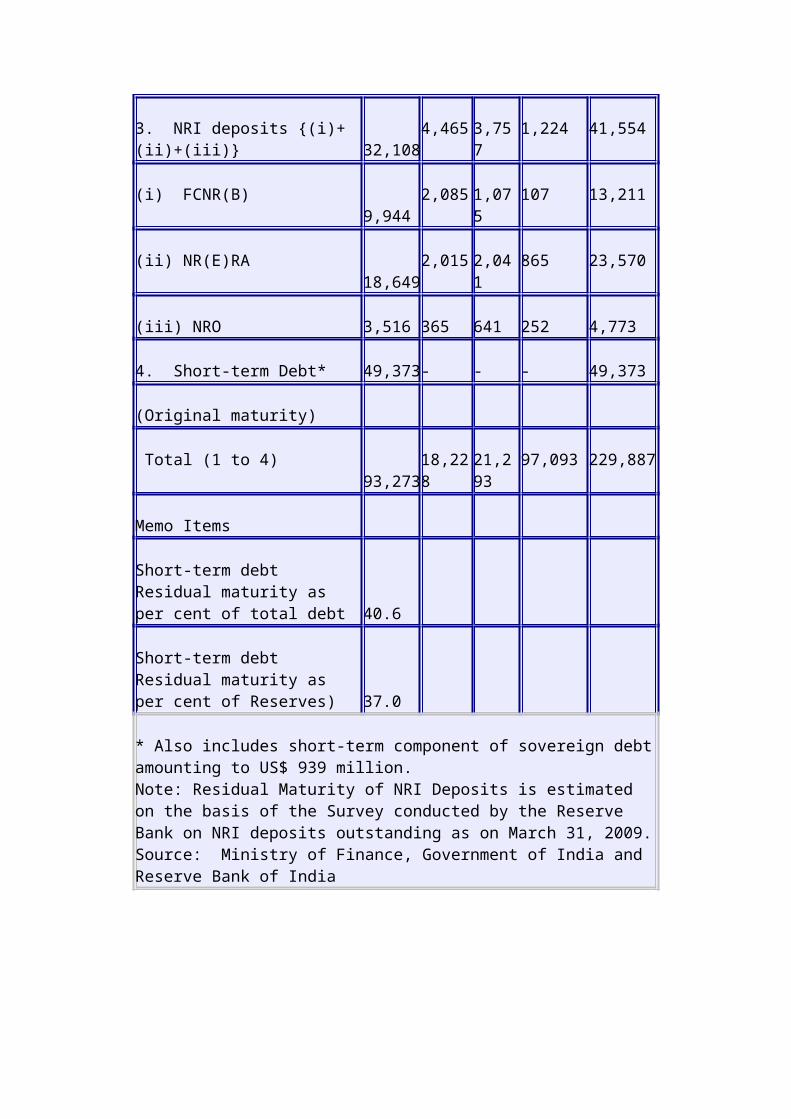

7. External Debt by Residual Maturity

(i) While external debt is generally compiled in terms of original maturity, analysing the external debt, in particular short term debt in terms of residual maturity is important from the point of view of foreign exchange liquidity management and to ascertain the total foreign exchange outgo on account of debt service payments in the immediate future.

(ii) The ‘short-term debt by residual maturity’ comprises the repayments due under medium and long-term debt by original maturity during one year reference period along with the short-term debt with original maturity. The balance constitutes the long-term debt by residual maturity. Based on residual maturity, the short-term debt accounted for 40.6 per cent of total external debt as at end-March 2009. The ratio of short-term debt by residual maturity to foreign exchange reserves worked out to 37.0 per cent at end-March 2009 (Table 8).

Table 8: Residual Maturity of External Debt Outstanding as at End-March 2009

(US $ million)

Short-term

Long-term Total(2) to (5)

Components Up to one year

1 to 2 years

2 to 3 years

More than 3 years

1 2 3 4 5 6

1. Sovereign Debt (long-term) 2,603 2,924 3,015 45,376 53,917

Short-term debtResidual maturity as per cent of total debt 40.6

Short-term debtResidual maturity as per cent of Reserves) 37.0

* Also includes short-term component of sovereign debt amounting to US$ 939 million.Note: Residual Maturity of NRI Deposits is estimated on the basis of the Survey conducted by the ReserveBank on NRI deposits outstanding as on March 31, 2009.Source: Ministry of Finance, Government of India and Reserve Bank of India

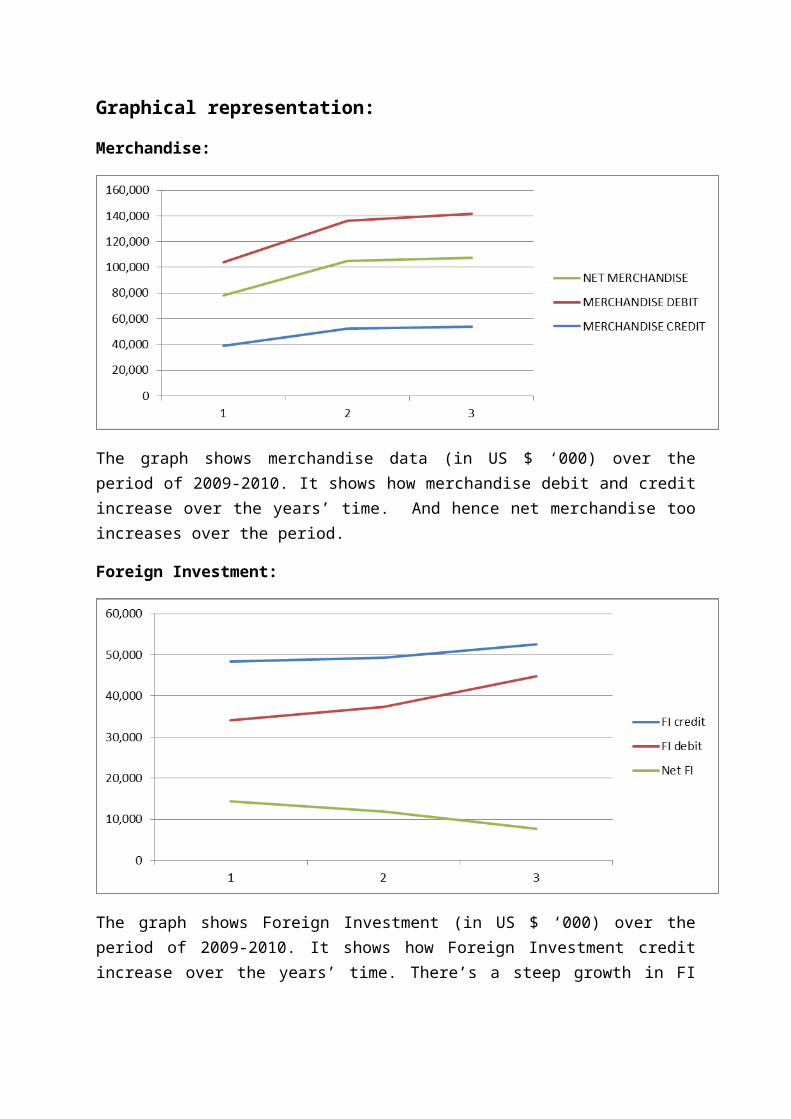

Graphical representation:

Merchandise:

The graph shows merchandise data (in US $ ‘000) over the period of 2009-2010. It shows how merchandise debit and credit increase over the years’ time. And hence net merchandise too increases over the period.

Foreign Investment:

The graph shows Foreign Investment (in US $ ‘000) over the period of 2009-2010. It shows how Foreign Investment credit increase over the years’ time. There’s a steep growth in FI debit. The net Foreign Investment shows decline over the given period.

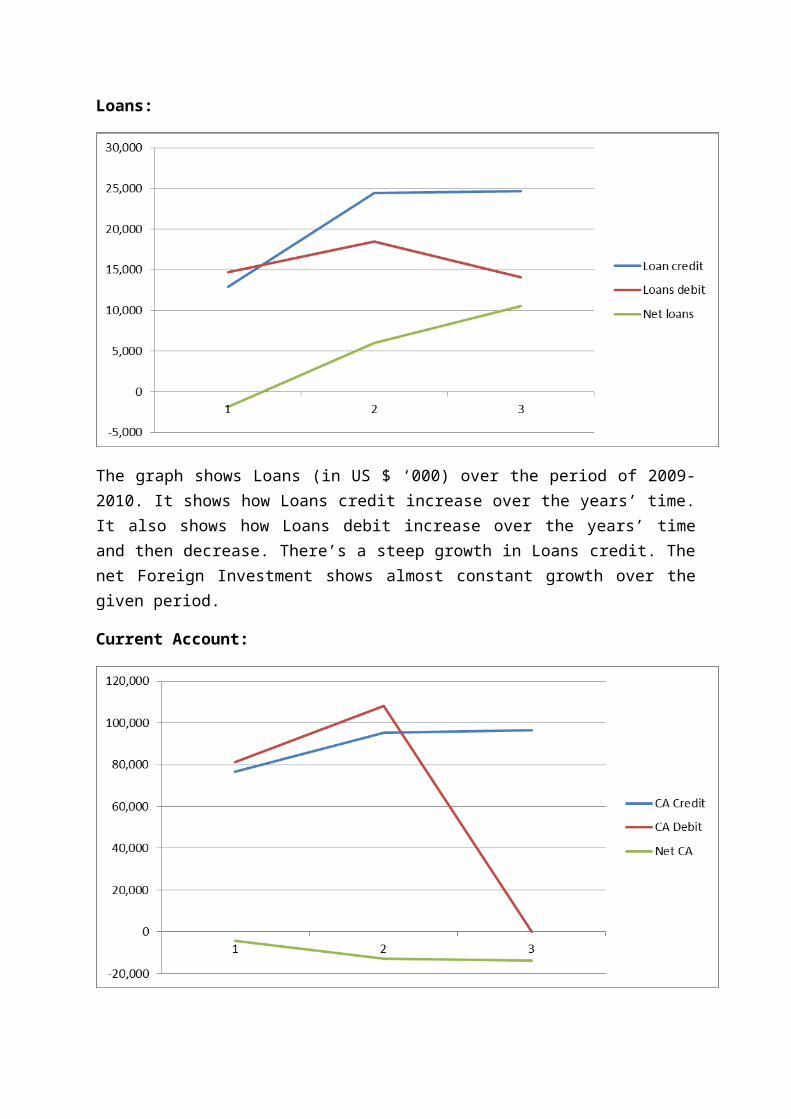

Loans:

The graph shows Loans (in US $ ‘000) over the period of 2009-2010. It shows how Loans credit increase over the years’ time. It also shows how Loans debit increase over the years’ time and then decrease. There’s a steep growth in Loans credit. The net Foreign Investment shows almost constant growth over the given period.

Current Account:

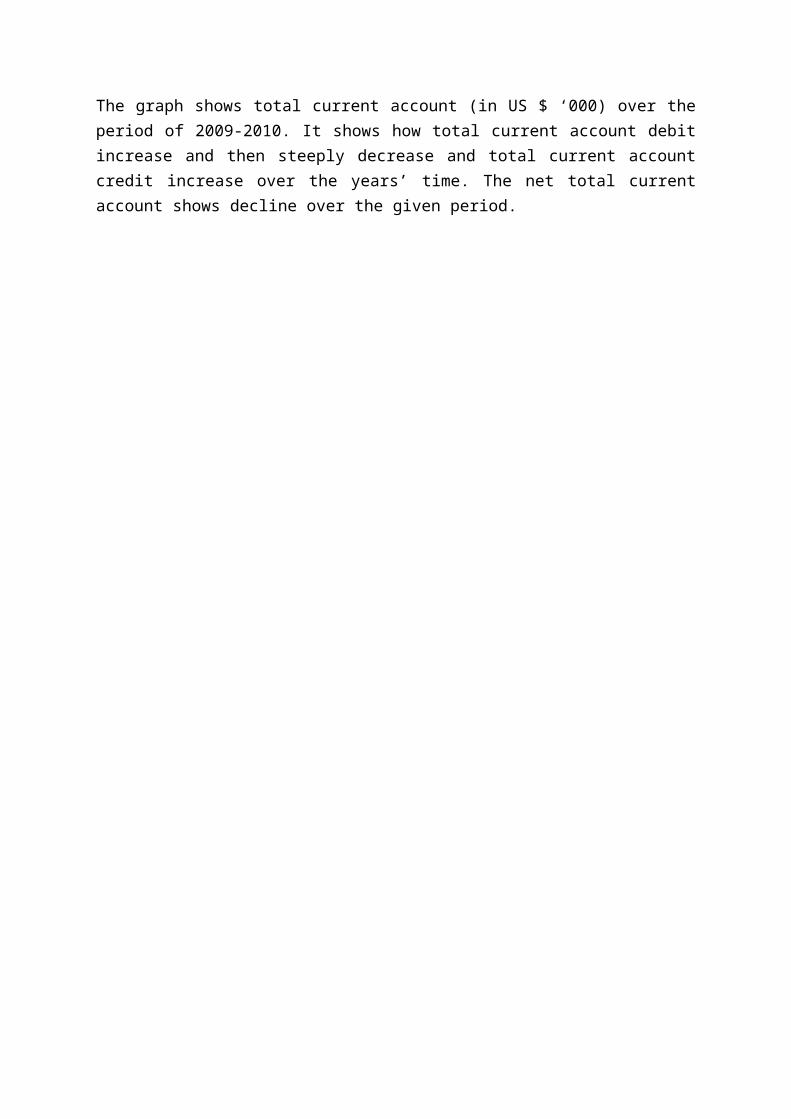

The graph shows total current account (in US $ ‘000) over the period of 2009-2010. It shows how total current account debit increase and then steeply decrease and total current account credit increase over the years’ time. The net total current account shows decline over the given period.

Banking Capital:

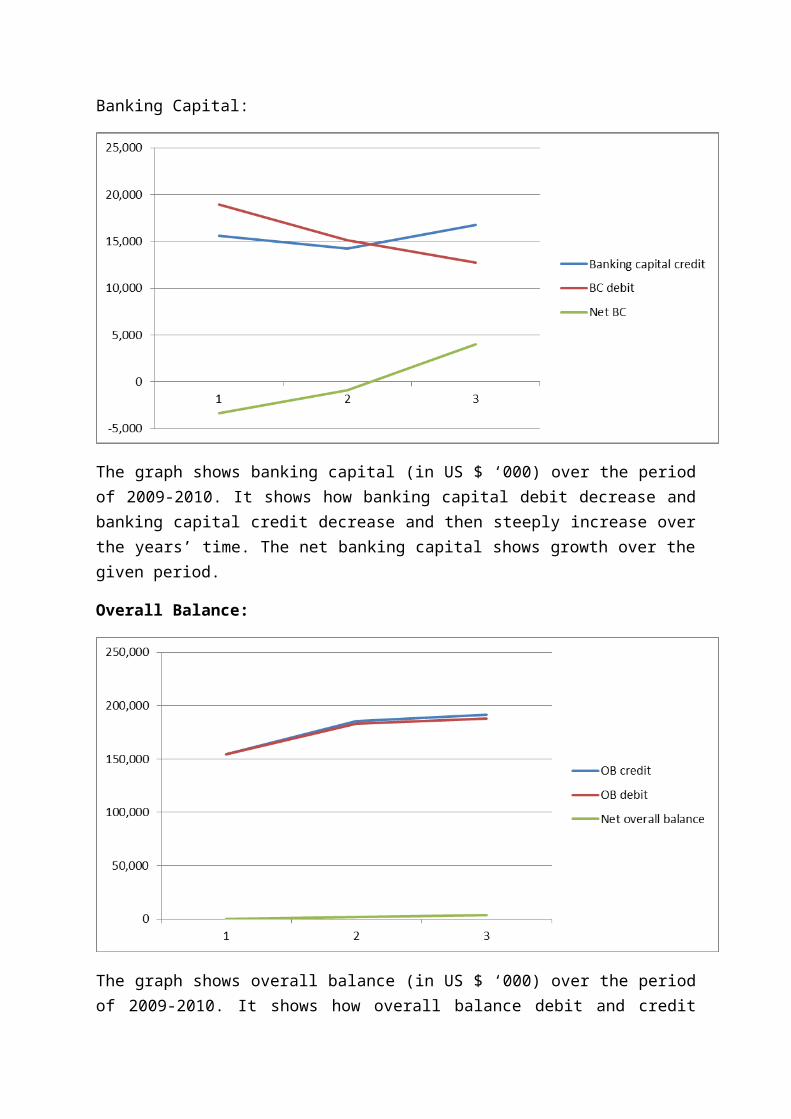

The graph shows banking capital (in US $ ‘000) over the period of 2009-2010. It shows how banking capital debit decrease and banking capital credit decrease and then steeply increase over the years’ time. The net banking capital shows growth over the given period.

Overall Balance:

The graph shows overall balance (in US $ ‘000) over the period of 2009-2010. It shows how overall balance debit and credit increase over the years’ time. Debit and credit data are almost same. The net overall balance shows growth over the given period.

Total Capital Account:

The graph shows total capital account (in US $ ‘000) over the period of 2009-2010. It shows how total capital account debit and credit increase over the years’ time. The net total current account shows constant growth initially and then steady growth over the given period.

TRADE CREDIT

Some Highlights of FEMA

It prohibits foreign exchange dealing undertaken other than an authorized person;

It also makes it clear that if any person residing in India, received any Forex payment (without there being a corresponding inward remittance from abroad) the concerned person shall be deemed to have received they payment from an unauthorized person.

There are 7 types of current account transactions, which are totally prohibited, and therefore no transaction can be undertaken relating to them. These include transaction relating to lotteries, football pools, banned magazines and a few others.

FEMA and the related rules give full freedom to Resident of India (ROI) to hold or own or transfer any foreign security or immovable property situated outside India.

Similar freedom is also given to a resident who inherits such security or immovable property from an ROI.

An ROI is permitted to hold shares, securities and properties acquired by him while he was a Resident or inherited such properties from a Resident.

The exchange drawn can also be used for purpose other than for which it is drawn provided drawl of exchange is otherwise permitted for such purpose.

Certain prescribed limits have been substantially enhanced. For instance, residence now going abroad for business purpose or for participating in conferences seminars will not need the RBI's permission to avail foreign exchange up to US$. 25,000 per trip irrespective of the period of stay, basic travel quota has been increased from the existing US$ 3,000 to US$ 5,000 per calendar year.

Buyers’ /Supplier's Credit

Trade Credit has been subjected to dynamic regulation over a period of last two years. Now, Reserve Bank of India (RBI) vide circular number A.P. (DIR Series) Circular No. 24, Dated November 1, 2004, has given general permission to ADs for issuance of Guarantee/ Letter of Undertaking (LoU) / Letter of Comfort (LoC) subject to certain terms and conditions . In view of the above, we are issuing consolidated guidelines and process flow for availing trade credit

Definition of Trade Credit: Credit extended for imports of goods directly by the overseas supplier, bank and financial institution for original maturity of less than three years from the date of shipment is referred to as trade credit for imports.

Depending on the source of finance, such trade credit will include supplier's credit or buyers credit, Supplier's credit relates to credit for imports into India extended by the overseas supplier, while Buyers credit refers to loans for payment of imports in to India arranged by

the importer from a bank or financial institution outside India for maturity of less than three years.

It may be noted that buyers’ credit and suppliers’ credit for three years and above come under the category of External Commercial Borrowing (ECB), which are governed by ECB guidelines. Trade credit can be availed for import of goods only therefore interest and other charges will not be a part of trade credit at any point of time.

Amount and tenor : For import of all items permissible under the Foreign Trade Policy (except gold), Authorized Dealers (ADs) have been permitted to approved trade credits up to 20 million per import transaction with a maturity period ( from the date of shipment) up to one year.

Additionally, for import of capital goods, ADs have been permitted to approve trade credits up to USD 20 million transactions with a maturity period of more than one year and less than three years. No roll over/ extension will be permitted by the AD beyond the permissible period.

All in cost ceiling: The all in cost ceiling are as under: Maturity period up to one year 6 months LIBOR +50 basis points. Maturity period more than one year but less than three years 6 months LIBOR* + 125 basis point for the respective currency of credit or applicable benchmark like EURIBOR. SIBOR, TIBOR, etc.

Issue of guarantee, letter of undertaking or letter of comfort in favor of overseas lender: RBI has given general permission to ADs for issuance of guarantee / Letter of Undertaking (LOU) / Letter of Comfort (LOC) in favor of overseas supplier, bank and financial instruction, up to USD 20 million per transaction for a period up to one year for import of all non capital goods permissible under Foreign Trade Policy (except gold) and up to three years for import of capital goods. In case the request for trade credit does not comply with any of the RBI stipulations, the importer needs to have approval from the central office of RBI.

FEMA regulations have an immense impact in international trade transactions and different modes of payments. RBI release regular notifications and circulars, outlining its clarifications and modifications related to various sections of FEMA

Emerging markets face hot money influx:

In the post-crisis era, the flow of international capital has taken on new features. FDI has decreased from 80 percent to 50 percent of net international capital flows. The gap is being filled by short term capital flows to emerging economies.

International hot money

Since the U.S., EU and Japan slashed interest rates, higher rates in emerging economies have become a magnet for arbitrageurs. Net capital inflows to Asia reached $35 billion in 2009, and the 2010 figure will be higher. Emerging markets have become the target of international hot money, causing asset bubbles in real estate and stock markets. In 2009, India's Sensex Index increased by 81 percent, the Brazilian BOVESPA index surged by 82.7 percent, and the Russian RTS Index rose by an astonishing 128.8 percent. In Indonesia, Philippines, Thailand, Vietnam and Argentina stock market indexes rose more than 60 percent, while the Dow Jones only managed 18.8 percent.

Stimulus packages, economic recovery and the inflow of foreign capital have caused a real estate boom in emerging economies. Brazil began to surge in 2009; real estate in Brasilia is now $6600 per square meter on average; in Moscow the average is $5320; in New Delhi it is $1400.

Vietnam and India are facing inflationary pressures. The forecast growth rate for the Vietnamese economy this year is 8.2 percent, while the CPI is expected to reach 10.8 percent. The wholesale price index in India has reached an 11-year high.

Why is hot money flowing into emerging countries?

Loose monetary policy is the financial platform for international hot money. Interest rates in major Western countries are almost zero, and capital is flowing into stock markets and real estate. The capital markets of emerging countries have become the destination of choice for excess liquidity.

Industrialization and urbanization in the emerging economies have contributed to the surge in asset values, providing a further spur to international arbitrageurs.

Exchange rate mechanisms in emerging economies lack the flexibility to react to the excessive hot money inflows. Most emerging countries still have exchange controls and lack the auto-adjustment function of free-floating exchange rates.

Negative impact

Hot money has several negative impacts. The inflow of foreign capital increases pressure on the domestic currency to appreciate. In countries with floating exchange rates, this can have a huge impact on the national economy. Countries with fixed exchange rates, on the other hand, have to make costly interventions in the currency markets. Inflows and outflows of hot money disrupt macroeconomic policies and make an independent monetary policy virtually impossible.

By early 2009, the international hot money was already active and predatory in the commodity markets, even before the economic recovery began. Hot money in commodities drives up prices, causing bubbles and cost-push inflation in emerging economies. Hot money flowing into capital and real estate markets causes property bubbles and distorts investment and consumption patterns. Finally after realizing its profits, hot money rapidly withdraws and the flow of capital reverses direction, inflicting even more serious damage on emerging countries.

Reasons for Inflow into India on a high:

India has been becoming a hot destination for foreign capital to be parked in its economic environment. The major reasons which have been identified for this shift towards India has been due to the following reasons

Inward Consumption Based Growth:

India’s economy is consumption oriented when compared to other emerging markets. India’s export contributes less than 15% to its $1.2T GDP. The IT outsourcing services and back office has garnered most of the business media coverage; however, these industries have less than 8% contribution to the GDP and employ less than 5 million people. This is an indicator of growth by internal production and consumption. It is less reliant on exports. Quite contrarily, these technology services perform better in recession, because it is all about optimizing operational cost.

Conservative Central Bank:

Its Reserve Bank (ie central bank) has very conservative monetary policy, which is why we did not see failure of the banks (or banking system) during recent financial meltdown. There were no widespread bank bailouts.

Transparency:

It has democratic governance which on many occasions slows down the decision making progress, but provides better transparency (relative to Russia and China). As of today, its currency is freely convertible for trading goods and services, but there are certain restrictions for international asset acquisition. However, it has a pragmatic roadmap to allow its currency to fully float with market dynamics. In 2007 and 2008, when Dollar dropped against Indian Rupee, Indian export started becoming uncompetitive.

Government Stimulus Driven Growth is Less: The Indian market has rebounded in line with other emerging markets like China or Brazil. An earlier fear of bubble seems to be a just – a fear. It’s economy indicator suggest it is back of growth. The key in this rebound is; not much is being supported by government driven expenditure or public infrastructure projects. In fact, it continues to stumble on its infrastructure.

Finally, India can boast that its government is run by a bunch of prominent economists (with political and public support). The architect of Indian economic reforms, who laid down the path for reforms 18 years ago, is now at its helm as a prime minister. It is always good to have a non-political leader who is not only an economist, but someone who knows how to execute it in the complex state like India. Therefore, I continue to believe that on long 10+ year time horizons my dollars are (a) relatively safer; and (b) provide above average returns in Indian markets. I do not expect to be a smooth ride. There will be time period when markets will crash, but it will eventually come out stronger.

Due to the above mentioned reasons, India finds itself in a favourable position, where a lot of foreign capital is getting attracted. The inflows have been in the forms of FII and FDI mainly, and have been the reason for the appreciation of Rupee against dollar.

The pumping in of money has heated the debate regarding management of “Hot Money” by the Reserve Bank of India. The RBI has not initiated any capital control measures to curb the inflow. Which many economists think might prove to be a mistake. On the other hand, other emerging economies like Brazil, Vietnam have enacted capital control measures, forcing foreign investors to park their funds in India, thereby further increasing the capital flow to India.

Impact of the appreciating Rupee on exporter’s mindset:

Indian exporters are overwhelmingly in favor of a fixed currency exchange rate as a recent currency gyration due to the Greek Contagion has made their lives very difficult. In a survey done by India’s Business association FICCI, 88% of the respondents wanted the Indian Currency Rupee to be fixed as they were suffering from big losses due to appreciation. Euro’s 20% depreciation against the US Dollar has resulted in massive problems for exporters all over the world. India with 25% of its exports going to the European Union faces similar problems. The exporters want India’s Central Bank the RBI to changes its Currency Policy from free floating to fixed for exporters. Note China has a fixed dollar Yuan currency peg at a much depreciated value. This has led to increasing international pressure on China to revalue the yuan as its swelling Forex Reserves and huge Trade Surplus leads to global imbalances

The Reserve Bank of India is not likely to oblige as its currency handling has been quite successful so far. RBI has intervened only to slow down rapid changes without interfering in the Rupee finding its market determined rate. RBI has a policy of not intervening to prevent either appreciation or depreciation resulting in the Rupee trading in a wide band of Rs 38-52 over the last Three years. Note Exports form a relatively smaller percentage of India’s GDP and so exporters have little influence over India’s currency exchange rate. Unlike countries like China and Japan which are heavily dependent on exports, India is not inconvenienced too much by Rupee appreciation. Caught off guard by recent appreciation of the rupee, particularly against the euro, the majority of the exporting firms surveyed by FICCI want the Reserve Bank to peg a fixed currency exchange rate. They took a cue from China, which has pegged a fixed rate of yuan against the US dollar. “At least for exporters, the central bank should give a facility like that in China of a fixed exchange rate. This would enable them to focus on managing their business and save them from the trouble of managing currency movements,” it said. An overwhelming 88 per cent of the 278 exporting firms participating in the survey, said the sudden appreciation in rupee has affected their margins. They lost on account of forward contracts that were booked to hedge currency rise

China state of Yuan:

China recently announced a series of measures to protect its economy against a possible devaluation of the US dollar by decoupling the Asian currencies from the American currency and using the Chinese yuan to gain access to raw materials from South America, the Caribbean and, most importantly, Russia.

The Chinese government has serious reasons to be alarmed. As the financial crisis deepens and the US debt multiplies to unprecedented levels, the possibilities of the US dollar failing to maintain its privileged position as the world reserve currency are very real.

Under such a scenario, China has much to lose. Its economy has been built around exports to the US, and the Chinese government holds $744 billion in US Treasury bonds, whose value would fall should the dollar be devaluated.

So far, the 21 percent gain of the yuan against the dollar since the Yuan’s fixed exchange rate was scrapped in 2005 has eroded China’s reserves as well as exporters’ profits. This was a factor in February’s 25.7 percent fall in exports in February.

The leaders of the Chinese Communist Party are aware that China lacks a domestic market capable of supporting the growth levels it needs to avoid mass unemployment. The jobless rate among China’s 225 million rural migrant workers has already reached 10 percent.

With a million college graduates from 2008 yet to find a job, another 6 million will join the labor market this year. The Chinese leaders fear that unemployment could lead to social unrest, threatening the wealth and privileges they have carved out for themselves since China opened itself to the world market.

Towards full convertibility of the yuan

Concerns over the stability of the US dollar led China in March 2008 to lobby the Group of 20 for the adoption of a “super-sovereign reserve currency.” This move, China feels, is necessary, all the more so since the yuan cannot be a reserve currency today because it is not fully convertible.

To redress this problem, China has embarked on a program to ensure that the yuan gains full convertibility in the not-too-distant future and is thereby in a position to compete with the dollar at some point for the role of world reserve currency.

The measures announced so far represent “baby steps toward liberalization of China’s capital account and internationalization of the renminbi,” said Tim Condon, head of Asia research at ING Group NV in Singapore. (Renminbi is another name for the yuan.)

Condon added, “Access to renminbi is not going to be an issue. China is using its financial might to hedge any risk it might face in terms of supplies of central raw materials for its growth and demand in other markets for its products.”

In a series of statements, the Chinese government has expressed its commitment to make the yuan a fully convertible currency. “China’s State Council said last week it allowed yuan settlement for international trade in Shanghai and four cities in Guangdong province—Guangzhou, Shenzhen, Zhuhai and Dongguan—to promote global use of the currency and protect companies from swings in the dollar,” reported Bloomberg News on April 9.

Other steps include the decision by the People’s Bank of China, approved in November 2008, to provide currency swaps for 650 billion yuan ($95 billion) to Belarus, Hong Kong, Indonesia, Malaysia, South Korea and Argentina. Last month, a similar arrangement with Jamaica was announced.

Bank Indonesia Deputy Governor Hartadi Sarwono told Bloomberg News last month that a 100 billion currency swap will enable Indonesia to buy Chinese goods using yuans for the first time.

China is also moving closer to eliminating the remnants of Hong Kong’s previous status as a British protectorate. Hong Kong will become the first city outside mainland China to start settling trades in yuan. In addition, China plans to allow Hong Kong companies to issue debt in yuan. Hong Kong had been accepting payments in yuan since 2004 to attract tourists from the mainland.

“It will reduce foreign exchange risks for companies, create more business for Hong Kong banks and diversify use of yuan funds,” Donald Tsang, chief executive of Hong Kong said at a press briefing last month, according to Bloomberg News. “The policy has already been approved. It’s almost here.”

With these actions, China plans to protect its exports to Hong Kong, Macao and the ASEAN nations, which reached $402.7 billion in 2008, a substantial 20 percent of China’s total

trading volume. This is a sufficiently large volume to make a statement to the world on the benefits of trading with China in yuans, rather than US dollars.

Latin America is another case in point. China is stepping in to fill a vacuum left in the region by a US in financial turmoil. A $10 billion currency swap will allow Argentina to purchase Chinese goods without using its depleted US dollar reserves.

The Argentina deal came as a direct challenge to US dictates in the region. The Argentina-China currency swap was announced a few weeks after the US approved $30 billion in swaps each to Mexico and Brazil, but was unwilling to extend a line to Argentina, which has yet to clear its defaulted Paris Club debt.

As the Argentine daily, La Nación, put it, the yuan swap was a “historical agreement with China to eliminate the US dollar on commercial exchanges.” For China, it represents the prospect of increasing its exports to a region where it already occupies the position of second trading partner after the US. Surely, other Latin American countries will follow closely the progress of this deal.

As China consolidates its influence among the ASEAN nations, moves to eliminate any vestiges of the British occupation of Hong Kong, and opens long-term relations with Latin America countries, it is significant that the steady steps taken by China to decouple its currency—and exports—from the US dollar have not received the attention they deserve in the American media. So far, economic analysts, speaking through American newspapers and cable news programs, have focused their commentary on what is happening to the US public debt, the ups and downs of the New York Stock Exchange and President Obama’s attempts to rescue Wall Street.

These are important aspects of the world crisis. But it is an illusion to think that these developments can be understood while leaving China out of the analysis. In reality, the measures to establish full convertibility of the Chinese yuan are highly correlated with developments in the US.

The far-reaching consequences, including the challenge to the US dollar, implicit in making the yuan fully convertible were dealt with on the Asia News web site (January 1, 2009). It noted: “If, after a trial period, China makes its currency convertible, the consequence is that importing countries must have reserves of yuan. To get them, central banks around the world will have to divest themselves of US assets and Treasury bonds. The euro has a rather limited role in Asian exchange.”

Maurizio d’Orlando, the chief economic analyst for Asia News, explained the relationship between yuan convertibility and the US dollar in a series of articles published on the Internet over the past six months. He wrote: “The massive levels reached by the foreign debt of the United States and the excessive and unjustified devaluation of China’s yuan are two high-risk factors for the world economy and stability.”

The huge US debt is threatening the US dollar’s position in the world. The unthinkable has become a possibility: that the US government may become insolvent, unable to borrow to cover its debt.

The American media has thus far not dared to analyze the future of the dollar. Because it strictly adheres to looking at the world from the point of view of the profit interests of the American ruling class, it finds it all but impossible to consider such a possibility. Having grown accustomed to seeing the US make others behave the way the US wants, the media lives in a state of denial. Nevertheless, there is mounting statistical data pointing in the direction of the possibility of insolvency.

US Debt:

In an article written in December 2008, Maurizio d’Orlando examined the explosion of US debt. He wrote that it “grew from $6.9 trillion as of 31 December 2003 to $13.4 trillion as of 31 December 2007. This is internationally circulated currency.”

The rate of growth of the debt has increased since the financial crisis began in the summer of 2007. The US public debt stood at $10.6 trillion, or 76.6 percent of gross domestic product (GDP), at the end of 2008. “Adding the Paulson plan and the rescue package for Fannie Mae and Freddie Mac (but not counting that for AIG), the ratio jumped to 118 percent,” wrote d’Orlando.

He continued: “If the figures published by Bloomberg are correct—$7.74 trillion in rescue packages—we arrive at about $23.3 trillion of public debt, for a ratio of 169 percent of GDP. In just a short period of time, the public debt of the United States has almost doubled or tripled. Whatever the case may be, it is far too high.”

“We can nonetheless roughly assume,” d’Orlando noted, “that a breaking point is quickly coming up, because if we add up US public debt and spending commitments in health care (Medicaid and Medicare) and pensions (Social Security), we get to 429.27 percent of GDP.”

An International Monetary Fund (IMF) study found that when the foreign-owned public debt of a country reaches 60 percent of GDP, that country faces the risks of a major monetary crisis. By the end of 2007, the ratio of US foreign-owned debt stood at 61.8 percent, up from 54.4 percent the previous year.

Even if one sets aside US commitments to Medicare, Medicaid and Social Security, its current public debt, at least 118 percent of GDP, implies that its foreign-owned debt stands at 73 percent of GDP, far above the 60 percent limit calculated by the IMF.

The only reason the IMF’s 60 percent limit does not apply to the US is that the US dollar remains the world reserve currency. Were the US dollar to lose its uniquely privileged position in world trade, the result would be nothing less than catastrophic.

It must also be borne in mind that Asian investors, especially the Japanese and Chinese, are the main foreign investors in US financial assets.

What are the alternatives for the US? Monetary policy reached a dead-end the day Federal Reserve Chairman Ben Bernanke set the federal funds interest rate at zero. The fiscal plans launched by the Obama administration—including the many rescue schemes offered to banks, insurers and auto makers—still do not satisfy Wall Street, and more may be allotted to bail out the banks. Most market practitioners consider the bottom of the financial crisis hasn’t been reached yet.

There is a real risk that fiscal policies alone won’t work either. As Washington runs out of options, the next measure available to the government is a massive devaluation of the US

dollar. That would have the effect of exporting the crisis to other countries, and would unquestionably raise calls by major US competitors to replace the dollar with another currency or basket of currencies as the world reserve currency.

Undervaluation of the yuan

For trade between China and the US, a devaluation of the US dollar is equivalent to an appreciation of the yuan. Asia News estimates that the yuan is undervalued by 55.5 percent.

“Currently,” writes Asia News, “because the exchange rate is controlled by the People’s Bank of China, the US dollar is worth about 6.8798 yuan.... If we applied the same relationship between China’s GDP in current dollars (6.04 percent of world GDP) and China’s GDP at purchasing power parity (which is 10.78 percent of World GDP), a US dollar should be exchanged at 3.821 yuan (hence the latter is undervalued by 55.54 per cent).”

A yuan appreciation of such magnitude—or a similar massive devaluation of the US dollar—would bring about a collapse of Chinese exports. Factories would have to shut down and lay off workers. This would cause social upheavals and threaten the power of the Chinese Communist Party and the cast of corrupt individuals who have enriched themselves by seeding capitalism in China. Equally affected would be foreigners who have at stake billions in direct investments in China.

Asia News writes, “Seen as the world’s workshop, China is a great success, but if we consider the amount of human resources, capital and raw materials used with regards to GDP growth per unit, then its system of production appears very inefficient. What is more, China’s yuan devaluation in 1994 led right to the 1998 Asian crisis. For Asia, that crisis was the price to pay for China’s transition from Communism to a market economy, the equivalent in some ways to the 1989 collapse of the Berlin Wall.”

Asia News summarized the relationship between China and the US in the following way: “Globalization is based on an unbalanced economic model. So far, public and private consumption in the United States have driven world demand. US consumers made export-driven growth in many countries possible.

“The absurdity of this method lies in the fact that producers get underpaid and are forced into saving in order to provide credit for those who do not produce and could hardly afford to buy. Workers in China, Brazil and India get starvation wages to produce goods tailor-made for the US (and Western) market, whilst US consumers are unable to generate corresponding resources and value.

“In fact, the trend for the US GDP is negative since the third quarter of 2000 when calculated on the basis of inflation as calculated prior to the Clinton era. Yet US consumers have been pushed, flattered and funded to live above their means, almost forced to buy every kind of goods. This is why there is a solvency problem.”

In fact, consumers in the US have been forced to assume an ever bigger and more unsustainable burden of debt while their wages steadily eroded as a result of corporate and government policy.

The steps taken by China to decouple its exports from the US dollar and increase its influence in emerging markets are strong indications that the financial crisis is evolving toward a new

stage in which the major countries will use their currencies, economic and political muscle, and military might to carve out a larger share in a new division of the world economy.

Rupee Yuan Trade Platform:

There have been recent discussions on the Rupee Yuan trade platform being strengthened sand the dollar peg. A new currency arrangement between India and China is desired by the local banks in light of the recent currency row. A simpler and less expensive mechanism is sought that would bypass dollar and allow trade payments in local currency between the international giants.

Since the Indian rupee and Chinese yuan are largely non-convertible currencies, export and import transactions between the two countries have dollar pegs. The rupees that an Indian buyer pays his bank for Chinese import, are converted into dollars which in turn is converted into yuan with the help of other banks for paying the Chinese seller.

The spiralling trade relations between India and China could prove to be a reason to move forward in this direction as otherwise, it takes 2-3 days to complete a transaction due to difference in time zones and involves additional operational costs.

“A direct yuan-rupee trade would cut transaction time, in fact the transactions could become real time. Also, the transaction cost would be lower,” said Aditya Puri, managing director and CEO of HDFC Bank, which is one of the domestic institutions that mooted the idea.

He said that the HDFC Bank team which recently visited China felt that Chinese authorities may be open to the suggestion. A bilateral trade using local currencies would require Indian banks opening yuan nostro accounts, which can be used for yuan trades, in Hong Kong or the mainland. This would need regulatory approvals from both countries

The proposal could benefit the India-China trade. It’s one of the most important trade corridors. Any means to facilitate that from a trade or a trade finance perspective would help both India and China. In an effort to internationalise the currency, China has permitted limited trading of yuan in the Hong Kong offshore market for trade and certain capital account transactions.

Also, in recent times it has entered into special currency arrangements with various countries. Last year China struck a ‘currency swap’ agreement with Brazil that allows payment for imports from China in yuan and imports from Brazil in the lira. It has also signed pacts with Malaysia, Argentina, South Korea, Belarus and Singapore. Across markets the deals were interpreted as China’s efforts to internationalise the yuan and slowly pave the way to help yuan eventually replace dollar as the world’s reserve currency.

Discussion on the possibilities of Rupee, Yuan being the next World Reserve Currency

Indian rupee and Chinese yuan are potential alternatives to US dollar for global transactions which has received a severe beating after the global financial crisis, says an RBI study.

The study, authored by RBI director Rajiv Ranjan and assistant advisor Anand Prakash, said the yuan and the rupee are "natural contenders" among emerging market currencies for international currency status. However, China is "far from ready" to achieve the global reserve currency status at the moment, while India needs to meet "all the necessary preconditions...before (it) could proceed further," it said.

Internationalisation of rupee would also require India to make the rupee fully convertible. This means that rupee could be exchanged against other currencies freely. There are currently curbs on such convertibility so far as capital accounts like stocks are concerned.

"The Indian rupee is rarely being used for invoicing of international trade," the study pointed out. It further said that "India has so far followed a calibrated approach towards capital account liberalisation.

India, at present, does not permit the rupee to be officially used for international transactions, except those with Nepal and Bhutan, though there are indications of the Indian rupee gaining acceptability in other countries." The study noted that the strength exhibited by the rupee in recent months and continued good performance of the Indian economy have raised the issue of greater internationalization of its currency and India needs to proactively take steps to increase the role of the domestic currency in the region.

The study also cautioned the Government over the risks associated with "internationalising" the rupee as it would increase sharp volatility in the forex markets. "There are, however, problems associated with internationalisation of the rupee as it could increase volatility of its exchange rate," the study said.

Withdrawal of short-term funds and portfolio investments by non-residents could also be a major potential risk of internationalisation of the rupee, it added.

Outlining the difficulty in positioning the Indian currency as a global reserve, the study said that unlike China, which has a large current account surplus, India has a significant trade and current account deficit. Current account balance broadly relates to exports and imports of goods and services and investment income from global trade.

The idea of "internationalising" the rupee and the yuan was mooted, after the global financial crisis and the weakening dollar threw open the debate on alternative global currency. However, the study also said that it is quite unlikely that the dollar will lose its predominance as the global reserve currency in the foreseeable future.

"The current crisis has, however, thrown open the debate on the need for a new global reserve currency in case the US economy fails to make a significant turnaround and the weakness of the US dollar persists," it added.

Case Study:

FERA Violations by ITC

ITC was started by UK-based tobacco major BAT (British American Tobacco). It was called the Peninsular Tobacco Company, for cigarette manufacturing, tobacco procurement and processing activities. In 1910, it set up a full-fledged sales organization named the Imperial Tobacco Company of India Limited. To cope with the growing demand, BAT set up another cigarette manufacturing unit in Bangalore in 1912. To handle the raw material (tobacco leaf) requirements, a new company called Indian Leaf Tobacco Company (ILTC) was incorporated in July 1912. By 1919, BAT had transferred its holdings in Peninsular and ILTC to Imperial. Following this, Imperial replaced Peninsular as BAT’s main subsidiary in India.

By the late 1960s, the Indian government began putting pressure on multinational companies to reduce their holdings. Imperial divested its equity in 1969 through a public offer, which raised the shareholdings of Indian individual and institutional investors from 6.6% to 26%. After this, the holdings of Indian financial institutions were 38% and the foreign collaborator held 36%. Though Imperial clearly dominated the cigarette business, it soon realized that making only a single product, especially one that was considered injurious to health, could become a problem. In addition, regular increases in excise duty on cigarettes started having a negative impact on the company’s profitability. To reduce its dependence on the cigarette and tobacco business, Imperial decided to diversify into new businesses. It set up a marine products export division in 1971. The company’s name was changed to ITC Ltd. in 1974. In the same year, ITC reorganized itself and emerged as a new organization divided along product lines. In 1975, ITC set up its first hotel in Chennai. The same year, ITC set up Bhadrachalam Paperboards. In 1981, ITC diversified into the cement business and bought a 33% stake in India Cements from IDBI. This investment however did not generate the synergies that ITC had hoped for and two years later the company divested its stake. In 1986, ITC established ITC Hotels, to which its three hotels were sold. It also entered the financial services business by setting up its subsidiary, ITC Classic

In 1994, ITC commissioned consultants McKinsey & Co. to study the businesses of the company and make suitable recommendations. McKinsey advised ITC to concentrate on its core strengths and withdraw from agri-business where it was incurring losses. During the late 1990s, ITC decided to retain its interests in tobacco, hospitality and paper and either sold off or gave up the controlling stake in several non-core businesses. ITC divested its 51% stake in ITC Agrotech to ConAgra of the US. Tribeni Tissues (which manufactured newsprint, bond paper, carbon and thermal paper) was merged with ITC.

By 2001, ITC had emerged as the undisputed leader, with over 70% share in the Indian cigarette market. ITC’ popular cigarette brands included Gold Flake, Scissors, Wills, India Kings and Classic.

Allegations:

A majority of ITC’s legal troubles could be traced back to its association with the US based Suresh Chitalia and Devang Chitalia (Chitalias). The Chitalias were ITC’s trading partners in its international trading business and were also directors of ITC International, the international trading subsidiary of ITC. In 1989, ITC started the ‘Bukhara’ chain of restaurants in the US, jointly with its subsidiary ITC International and some Non-Resident Indian (NRI) doctors. Though the venture ran into huge losses, ITC decided to make good the losses and honour its commitment of providing a 25% return on the investments to the NRI doctors. ITC sought Chitalias’ help for this.