81

Project PACE Implementation (Salt, Sugar, Agro Sacks, HQ Operations) Finance and Controlling Asset Accounting

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | satyaavanigadda69 |

| View: | 26 times |

| Download: | 0 times |

Project PACE Implementation (Salt, Sugar, Agro Sacks, HQ Operations)

Finance and Controlling Asset Accounting

Agenda

2

Introduction

Course Overview

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

3

Agenda

Introduction Introduction House Rules Training Objectives

Course Overview

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

4

• Name

• SBU

• Role within Dangote

• Role in Project PACE

• Expectations

Introduction

5

Cell Phones on silent

Designated Smoking Areas

Restrooms

Questions

Emergency Exits

Parking Lot

House Rules

Training Objectives

The objective of this training session is to provide Dangote staff with the required SAP knowledge to be able to perform their roles within the business. This course will enable you to:

• Understand the Asset Accounting process;

• Identify your role within the process;

• Identify any changes (system and process) that will affect how you do your job once Project PACE goes live;

• Understand key concepts, terminology and sub-processes related to the Asset Accounting process;

• Perform SAP transactions relevant to your role.

6

Agenda

7

Introduction

Course Overview Project PACE Training Structure Course Structure Key Information

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

8

Course Structure

In this course we will be reviewing the following sub-processes and related SAP transactions:

• Fixed Asset Master

• Asset Acquisition

• Capitalization

• Asset Transfer/Disposal

• Fixed Asset Period-End Closing

• Fixed Asset Year-End Closing

• Fixed Asset Reporting

Key Information

Integration with Other Modules As a result of integration in SAP, the Asset Management module transfers data directly to and from other SAP components

o It is possible to post from the Materials Management (MM) component directly to the Asset component. E.g. Asset can be capitalized during logistics invoice verification.

o At the same time, you can pass on depreciation directly to the Financial Accounting (FI) and Controlling (CO) components

Integration with FI & CO Integration with MM Component

Key Information

10

Create Asset Master Data

Acquisition of Asset

Perform Asset transfer/Disposal

Generate/Analyzes Fixed Asset Reports

Perform Fixed Asset Year-End Closing

Perform Fixed Asset Period-End Closing

Capitalization

Asset Accounting Process Overview

Key Information

Create Asset Master Data

Asset Accounting Process Overview

Create Asset Master Data

Fixed Asset Period End Closing

Fixed Asset Reporting

Agenda

12

Introduction

Course Overview

Finance Overview Training • Fixed Asset Master • Asset Acquisition • Capitalization • Asset Transfer/Disposal

Key Learning Points

Summary

Competency Assessment

Questions & Answers

• Fixed Asset Period-End Closing • Fixed Asset Year-End Closing • Fixed Asset Reporting

13

Asset Accounting Transactions

We will now review each of the sub-processes within the Asset Accounting process and the relevant SAP transactions.

For each transaction, the instructor will first perform a demonstration and then you will have the opportunity for hands-on practice in SAP.

14

Asset Accounting Transaction Training Agenda

Fixed Asset Master New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

15

Asset Accounting Transaction Training Agenda

Fixed Asset Master New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

New Terminology

SAP Terminology Description

Depreciation Key Key that determines the depreciation calculation method of the asset

Asset Value Date In some transactions, e.g. direct acquisition of asset via Asset Accounting module and asset transfer, asset value date field should be populated. In transactions where asset value date cannot be entered, asset value date is generally defaulted from posting date. Generally, asset value date determines depreciation start date. For example, if asset value date in direct acquisition is a date in the next period, asset depreciation will only start in the next period.

The following terminology will be introduced as part of the Project PACE

16

17

Asset Accounting Transaction Training Agenda

Fixed Asset Master New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

18

Chart of Depreciation

Depreciation Area

• Used for managing legal requirements for depreciattion .

• Identifies number of Depreciation Areas.

• Used to calculate different values in parallel for different purposes.

Country Chart of Depreciation

Depreciation Area

Country A Chart of Depreciation A

01 – Legal 15 – Taxation 30 – Local

Country B Chart of Depreciation B

01 – Legal 30 – Local

Fixed Asset Master Key Concepts

A chart of depreciation is used in order to manage various legal requirements for the depreciation and valuation of assets. It determines the number of deprecation areas that may be used. A company code is assigned to only one Chart of Depreciation. It is possible to assign multiple company codes to the same chart of depreciation

• Depreciation area 01 is for legal depreciation (IFRS). This depreciation area will post values to the General Ledger (GL) in real time.

• Depreciation Area 15 is for Capital Tax depreciation. This depreciation area will have no posting to financial books

• Depreciation Area 30 is for local GAAP reporting. It will post depreciation value to a local ledger (separate from IFRS ledger)

19

Fixed Asset Master Key Concepts

A chart of depreciation is used in order to manage various legal requirements for the depreciation and valuation of assets. It determines the number of deprecation areas that may be used. A company code is assigned to only one Chart of Depreciation. It is possible to assign multiple company codes to the same chart of depreciation

Nigeria Chart of Depreciation = 1000 • Depreciation area 01 is for legal

depreciation (IFRS). This depreciation area will post values to the General Ledger (GL) in real time.

• Depreciation Area 15 is for Capital Tax depreciation. This depreciation area will have no posting to financial books

• Depreciation Area 30 is for local GAAP reporting. It will post depreciation value to a local ledger (separate from IFRS ledger)

20

Creation of Asset Master

When asset is received from AUC

- Asset master for the receiving asset in non-AUC asset class needs to be created.

When asset is purchased

- If asset is purchased via purchase order (PO) , the asset master number must be entered in the PO

When there is need to transfer an asset initially created in a wrong asset class

-New asset master in the correct class is created.

When cross company asset transfer needs to take place

- The receiving asset master needs to be created.

This refers to the process of creating, changing, blocking and deleting asset master data. There is provision for both asset main numbers and asset sub numbers.

Fixed Asset Master Key Concepts

21

Changing Asset Master

During the life of the fixed asset, certain information, especially time-dependent information such as cost centre, plant, location, room, shutdown indicator in the asset master will be changed from time to time. Lock indicator can also be set in the asset master if no further acquisition should be posted to the asset. Master data maintenance roles will only be assigned to the master data team who will maintain master data (not just Fixed Asset master) in accordance with MDM governance

Fixed Asset Maintenance This refers to the process of creating, changing, blocking and deleting asset master data. Project PACE uses both asset main numbers and asset sub numbers.

Fixed Asset Master Key Concepts

22

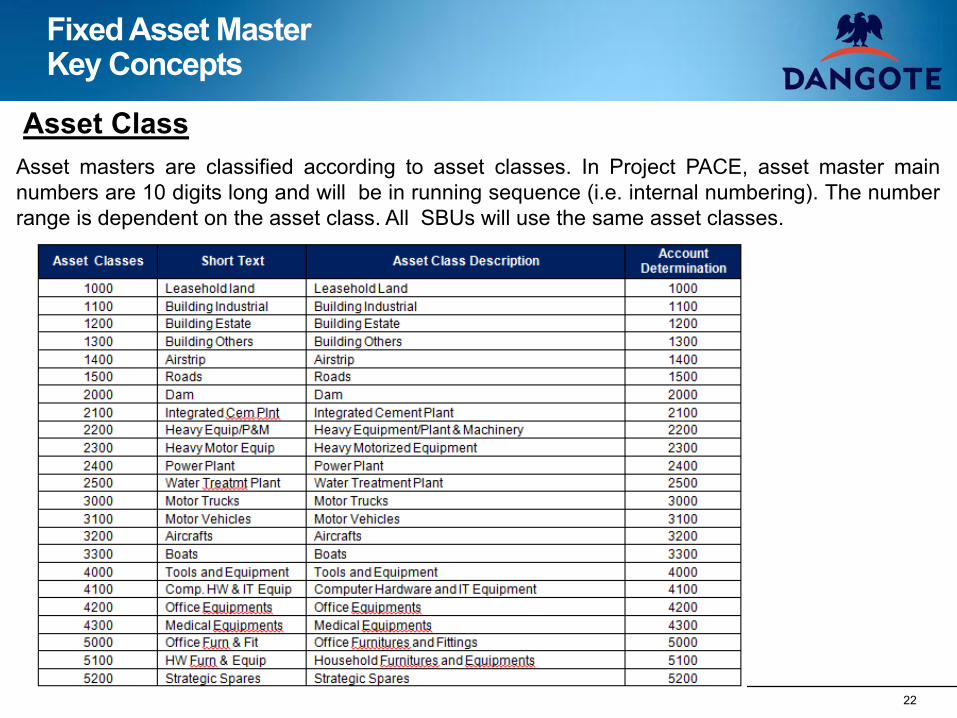

Asset Class Asset masters are classified according to asset classes. In Project PACE, asset master main numbers are 10 digits long and will be in running sequence (i.e. internal numbering). The number range is dependent on the asset class. All SBUs will use the same asset classes.

Fixed Asset Master Key Concepts

23

Asset Classes [cont’d]

Fixed Asset Master Key Concepts

24

Asset Master

The following are important fields for asset masters in all asset classes in Project PACE. Field Name Description

Main Asset Number This is system defined according to the asset class selected.

Sub-Asset Number Asset under main asset that is acquired at a later time and would like to be tracked together. It may have different depreciation key and useful life from main asset. This field may be utilized to capitalizing repair costs

Description Line 1 This contains the description of the fixed asset.

License Plate Number For vehicles, the plate numbers may be captured in this field. It’s an optional field

Evaluation Group 1-3 Values in this fields may be used to group assets for reporting purpose. Example: Asset Class Motor Vehicles may have Eval Grp 2 for Truck, Sedan, SUV. This is an optional field.

Scrap Value A scrap value (also called memo value or residual value) of N10 (Ten naira) will be maintained. This will ensure that depreciation stops when this value is reached

Fixed Asset Master Key Concepts

25

Field Name Description

Cost Center This contains the cost center which depreciation expense of the fixed asset will be charged to.

Plant This contains the plant where the asset is being used. The asset location setting is tied to plants

Depreciation Key Depreciation key determines the depreciation pattern of the fixed asset.

Acquisition Date* Asset value date of the first acquisition posting.

Capitalization Date* Asset value date of the first posting that results in the capitalization of the asset. Since both capitalization date field and the acquisition date field are set as display only in Project PACE, both dates will always be the same.

Asset Master

Fixed Asset Master Key Concepts

* These fields are set as display only in the asset master. This means that these fields cannot be changed in the asset master and are only updated via transactions.

26

Asset Accounting Transaction Training Agenda

Fixed Asset Master New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

27

Asset masters are created under the following scenarios: When asset is purchased:

o If asset is purchased via purchase order, the asset master number must be entered in the purchase order. If a purchase requisition is raised prior to purchase order, the asset master number must be entered in the purchase requisition. The asset master number will be copied over to the purchase order when the purchase requisition gets converted to a purchase order. Asset number will mandatory for POs with account assignment of “A” for assets.

When asset under construction (AUC) needs to be settled:

o Asset master for the receiving asset in non-AUC asset class needs to be created.

When cross company asset transfer needs to take place:

o The receiving asset master needs to be created.

Fixed Asset Master Process Overview

28

Asset Accounting Transaction Training Agenda

Fixed Asset Master New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

29

Standard rules and guidelines related to Fixed Asset Master are

recommended for proper control and management of data and processes Rules

• Fixed Asset maintenance form should be properly filled up. • Check the asset first if it already exists in the system.. • Asset should have a correct asset class.

Guidelines• Guidelines to be followed will be provided by the Master data governance

team

Rules & Guidelines

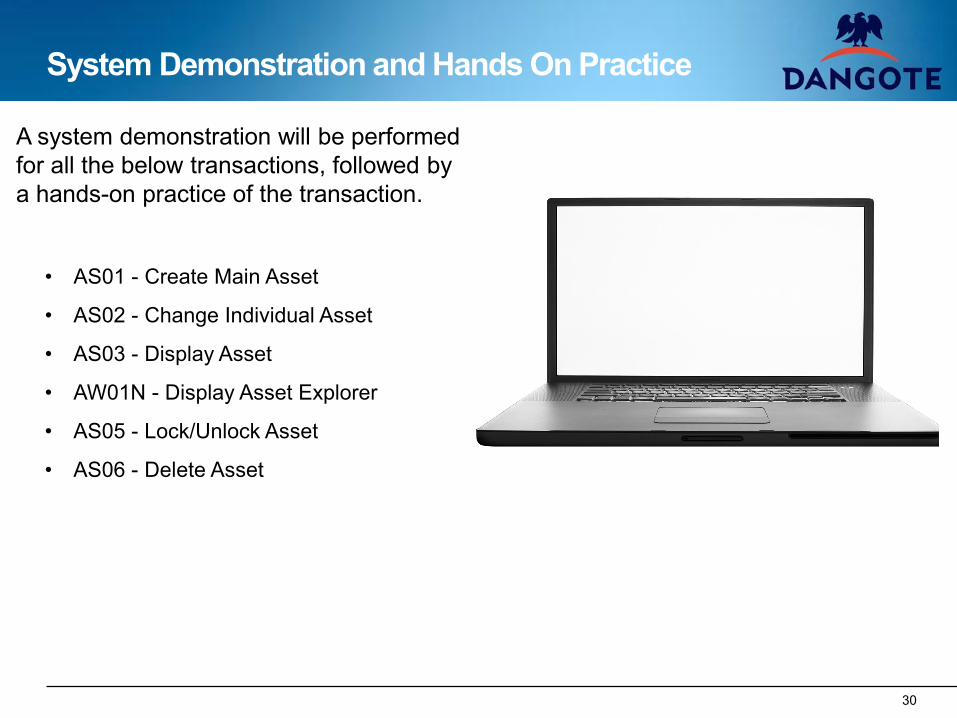

System Demonstration and Hands On Practice

A system demonstration will be performed for all the below transactions, followed by a hands-on practice of the transaction.

• AS01 - Create Main Asset

• AS02 - Change Individual Asset

• AS03 - Display Asset

• AW01N - Display Asset Explorer

• AS05 - Lock/Unlock Asset

• AS06 - Delete Asset

30

31

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition/Capitalization New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

32

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition & Capitalization New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

New Terminology

SAP Terminology Description

Transaction Type This is the object that classifies the business transaction (for example: acquisition, retirement, or transfer), and determines how the transaction is processed in the SAP system. The transaction type is the basis for the assignment of the business transaction to a column in the asset history sheet. Every transaction type belongs to aspecific transaction type group. e.g. transaction type for acquisition is 100 External Asset Acquisition.

Asset Under Construction An asset that is work in progress and it not ready to be utilized. Since economic benefits are not yet being derived from the AUC, depreciation should not be posted.

The following terminology will be introduced as part of the Project PACE

33

34

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

35

This refers to the purchase of fixed asset. Assets may be purchased externally or through internal construction.

For external purchase a Purchase Requisition / Purchase Order will be raised in MM. For assets purchased via purchase order, capitalization date will be the goods receipt date and capitalized amount will be the invoice receipt amount. Alternatively the business may capitalize when the asset is put to commercial use

o When goods receipt for the fixed asset is posted

– Dr AUC

– Cr GR/IR

o When the invoice verification is posted, the GR/IR Account is debited and vendor is credited.

– Dr GR/IR

– Cr Vendor

o The Final asset master will be created in the appropriate asset class. The final asset here refers to the asset that the AUC will be settled to

o The AUC will be ‘settled’ to the final asset. ‘Settlement’ is the process of transferring the asset values from the AUC to the final asset

Asset Acquisition Key Concepts

36

This refers to the process of settling an AUC to its final asset

Before capitalization

• Asset master in non-AUC asset classes should be created.

• Distribution rule should be maintained.

During capitalization

• Perform settlement (Dr Fixed Asset, Cr AUC).

• Non-AUC class will be capitalized with asset value date of settlement.

• Upon final settlement of the AUC, the AUC must be manually deactivated.

Capitalization Key Concepts

37

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition & Capitalization New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

System Demonstration and Hands On Practice

A system demonstration will be performed for all the below transactions, followed by a hands-on practice of the transaction. Acquisition t-codes in Asset Accounting.

• ME53N/ME21N PR/PO (MM)

• MIGO GR (MM)

• MIRO Invoice Receipt

• F-90 Acquisition with Vendor

Capitalization t-codes in Asset Accounting.

• AIAB Settlement of AUC Line Item

• AIBU Execute Settlement Test Run

• AIBU Execute Settlement Run

• AIST Reverse Settlement

38

39

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

40

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

41

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

42

This refers to the process of transferring fixed assets between cost centers or between SBUs

Asset Transfer - the system allows: • Complete and partial transfer,

– Full asset transfer is typically necessitated when an asset was initially capitalized in the wrong asset class. Asset master in the correct asset class should first be created and thereafter the values will be transferred

– A common reason for partial transfer is where multiple quantities of assets were capitalized in one asset master and some of the assets are transferred to another cost centre or plant. For example, 10 units of laptop were initially capitalized in one asset master with IT cost centre. If 5 units of the laptop need to be transferred to Finance cost centre, a new asset master in the same asset class will be created and partial transfer will be carried out for 5 units to the new asset master

• The asset transfer function will:

Dr Accum Depreciation account of sending asset Cr Gross book value account of sending asset Dr Gross book value account of receiving asset Cr Accumulated depreciation account of receiving asset

Asset Transfer Key Concepts

43

Asset Transfer

Asset Transfer Process

44

This refers to the process of fixed asset disposal

Once an asset has reached the end of its useful life, it needs to be taken off the financial books. An asset may have reached the end of its useful life if its fully depreciated, lost, stolen,or if the organisation has decided to sell it. Assets can be scrapped from SAP, in which case there is no revenue realised from disposing the asset and net book value is treated as an expense

Alternatively, the asset can be sold for a value either to a known or unknown buyer. When this is done, revenues from the disposal are posted into the GL and the profit or loss from the disposal is determined

Asset Retirement - the system allows: • Complete and partial retirement,

• Retirement with revenue and without revenue (Scrapping)

Asset Retirement Key Concepts

45

Asset Retirement without Revenue (Scrapping) In Project PACE, sometimes asset may be disposed without revenue (i.e. scrapped). If an asset is scrapped, the net book value at the time of scrapping will be the amount of loss on disposal.

• The scrapping (ABAVN) function will:

Dr Loss on disposal account Dr Accumulated depreciation account Cr Gross book value account

Asset Retirement with Revenue Asset retirement with sale to customer function will post the following entries. Different GL accounts are used for profit on disposal and loss on disposal [F-92]

Dr Accumulated depreciation account Dr Customer account Cr Gross book value account Dr/Cr Loss/Profit on disposal account (depends on whether the sale

amount is less/ greater than the net book value of the asset)

Asset Transfer/Disposal Process

46

Asset Disposal Process

Retire and Dispose of Asset

ASSET TRANSACTIONS PROCESSORAPPROVERADMIN

Scrap

Post against P&LAccount on sale of

asset

End

ShouldAsset

be SoldOR

Scrapped

Asset is to beDisposed

Sell

Obtain Approvalto Dispose of

Asset

Scrap Asset

47

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

System Demonstration and Hands On Practice

A system demonstration will be performed for all the below transactions, followed by a hands-on practice of the transaction.

• ABUMN - Transfer within Company Code

• ABT1N – Intercompany Transfer of asset

• ABAVN - Asset Retirement By Scrapping

• F-92 - Asset Retirement from Sale With Customer

• ABAON - Asset Sales w/o Customer

• AB02 - Change Asset Document

• AB03 - Display Asset Document

• AB08 - Reverse Asset Document

48

49

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

50

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

51

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

52

This is a series of activities to be completed prior to closing of period for fixed assets in order to ensure accurate and timely financial reporting.

Planned Depreciation – refers to the periodic depreciation amount calculated by the system based on the depreciation key and useful life maintained in the asset master

Depreciation will be run on each depreciable asset on a monthly basis. The depreciation key will be in asset master data and will determine automatic calculation of depreciation for that asset. Depreciation will not be posted to AUCs, since economic benefits are not yet derived

Depreciation for an asset will commence in the month of asset capitalization. Also, all assets will be depreciated to residual value of N10. The sap transaction AFAB will be used to post monthly depreciation. The system will make the following postings

Dr Depreciation Expense Account

Cr Accumulated Depreciation Account

SAP provides standard functionality for Unplanned Depreciation (Transaction ABAA). This functionality will be used for impairment of assets when necessary - when there is an unexpected permanent reduction in value of an asset (e.g. as a result of damage). The unplanned depreciation is treated as expense in P&L

Fixed Asset Period-End Closing Key Concepts - Depreciation

53

Fixed asset period-end closing consists of a serious of activities. All fixed asset invoices for the month should be booked and all AUCs which are ready for use should be settled before carrying out period-end closing activities.

Step Task 1 Generate custom report Locked Cost Centers and Internal Orders. If there are blocked cost

centers, these cost centers should be unblocked before depreciation run to ensure that depreciation run will not encounter errors. Alternatively, the cost center in the asset master should be changed to one which is not blocked.

2 Execute Depreciation run.

3 Execute Unplanned depreciation if necessary

4* Execute periodic APC posting program in order to post fixed asset values other than depreciation (e.g. Acquisitions) from other depreciation areas to GL. (usually only depr Are 01 posts in real time to the GL)

5 Check periodic APC posting

Fixed Asset Period-End Closing Process

*Scenario: You have done an asset retirement, the system already posted entries to dep area 01- you now need to post entries to the other depreciation areas

54

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

55

Standard rules and guidelines related to Fixed Asset Period End Closing are

recommended for proper control and management of data and processes Rules

• All Fixed Asset invoices for the period should be booked.

• All AuCs which are ready to be utilized should be settled.

Guidelines

• N/A.

Rules & Guidelines

56

Asset Accounting Transaction Training Agenda

Fixed Asset Master

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

System Demonstration and Hands On Practice

A system demonstration will be performed for all the below transactions, followed by a hands-on practice of the transaction.

• ZLOCKED - Run locked cost center and

internal order reports

• AFAB - Execute Depreciation Run

• SM37 - Job Overview

• ABAA - Unplanned Depreciation

57

58

Asset Accounting Transaction Training Agenda

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

59

Asset Accounting Transaction Training Agenda

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

60

Asset Accounting Transaction Training Agenda

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

61

A series of activities to be completed prior to fiscal year closing of period for fixed assets in order to ensure accurate and timely financial reporting.

Fixed Asset Fiscal Year Change • Standard SAP requires new fiscal year to be opened in the Fixed Assets module

before postings can be made to fixed assets in the new fiscal year.

• Opening of the new fiscal year also serves to carry forward the fixed asset balances to the new fiscal year.

• The system allows two fiscal years to be opened at any point in time.

Fixed Asset Year End Closing • Closing of fiscal year is necessary to ensure that depreciation values of the closing

fiscal year are not altered.

Fixed Asset Year-End Closing Key Concepts

62

Fixed asset year-end closing activities should only be carried out after fixed assets period-end activities have been completed.

The new fiscal year in Fixed Assets module should be open on or before the first day of the new fiscal year.

In Project PACE, before the fiscal year in Fixed Asset module can be closed, the reconciliation report in Fixed Assets module should be generated.

If there are any asset GL accounts where the values in Fixed Asset module are different from the GL, it will be shown in the reconciliation report.

The discrepancies have to be resolved before fiscal year closing is carried out in Fixed Asset module.

Fixed Asset Year-End Closing Process

63

Asset Accounting Transaction Training Agenda

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

64

Standard rules and guidelines related to Fixed Asset Year End Closing are

recommended for proper control and management of data and processes Rules

• Depreciation run for the last period in the fiscal year must be completed before fixed asset fiscal year can be closed in the system.

Guidelines • N/A.

Rules & Guidelines

65

Asset Accounting Transaction Training Agenda

Asset Acquisition

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

System Demonstration and Hands On Practice

A system demonstration will be performed for all the below transactions, followed by a hands-on practice of the transaction.

• ABST2 Reconciliation FI-AA

• AJAB Asset Year-End Closing • AJRW Fiscal Year Change • OAAQ View closed FYs

66

67

Asset Accounting Transaction Training Agenda

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing

Fixed Asset Reporting New Terminology Key Concepts, Process & Roles Process Overview Rules & Guidelines System Demonstration & Hands-on Practice

68

Asset Accounting Transaction Training Agenda

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing

Fixed Asset Reporting New Terminology Key Concepts, Process & Roles Rules & Guidelines System Demonstration & Hands-on Practice

69

Asset Accounting Transaction Training Agenda

Capitalization

Asset Transfer/Disposal

Fixed Asset Period-End Closing

Fixed Asset Year-End Closing

Fixed Asset Reporting New Terminology Key Concepts, Process & Roles Rules & Guidelines System Demonstration & Hands-on Practice

System Demonstration and Hands On Practice

A system demonstration will be performed for some of the below transactions, followed by a hands-on practice of the transactions.

• S_ALR_87012056 Directory of Unposted Assets • S_ALR_87012037 Changes to Asset Master Records Report • S_ALR_87011979 Physical Inventory List by Cost Center • S_ALR_87011980 Physical Inventory List by Location • S_ALR_87011981 Physical Inventory List by Asset Class

• S_ALR_87011981 Physical Inventory List by Plant

• S_ALR_87012075 Asset History Report

• S_ALR_87011990 Asset History Sheet

• S_ALR_87012039 Asset Transactions

• S_ALR_87012048 Asset Transactions

• S_ALR_87012050 Asset Acquisitions

• S_ALR_87012052 Asset Retirements

• S_ALR_87012054 Intracompany Asset Transfers

• AW01N Display Asset Explorer

• S_ALR_87011963 Asset Balances by Asset Number

• S_ALR_87011964 Asset Balances by Asset Class

• S_ALR_87011965 Asset Balances by Business Area

• S_ALR_87011966 Asset Balances by Cost Center

• S_ALR_87011967 Asset Balances by Plant

• S_ALR_87011968 Asset Balances by Location

70

Check

System Demonstration and Hands On Practice

A system demonstration will be performed for all the below transactions, followed by a hands-on practice of the transaction.

• S_ALR_87012004 Total Depreciation

• S_ALR_87012043 GL Account Balances

• S_ALR_87012936 Depreciation on Capitalized Asset

• S_ALR_87012026 Depreciation Current Year

• S_ALR_87012006 Ordinary Depreciation

• S_ALR_87012007 Special Depreciation

• S_ALR_87012008 Unplanned Depreciation

• S_ALR_87012013 Depreciation Comparison

• S_ALR_87010175 Posted Depreciation Related to Cost Centers

• S_ALR_87012035 Depreciation Current Year

71

Agenda

72

Introduction

Course Overview

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

Key Learning Points

This is a summary of the key learning points of this training session. • Fixed Asset master data is maintained in SAP, PACE used both the asset main

number and asset sub number.

• Retirement of asset is done, SAP standard functionalities had been used (via scrapping, with customer or without customer).

• Fixed Asset Period-End closing is performed before the year-end closing and all asset transactions, adjustments and depreciation should be booked.

• At the end of each year, new fiscal year for fixed assets module should be opened and all balances for the year should be carried forward for the next year.

• Various reports for the Fixed Assets will be generated and analyzed

73

Agenda

74

Introduction

Course Overview

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

75

Summary

S/No Discussion Subjects Done

1 Fixed Asset Master Y

2 Asset Acquisition Y

3 Capitalization Y

4 Asset Transfer/Disposal Y

5 Fixed Asset Period-End Closing Y

6 Fixed Asset Year-End Closing Y

7 Fixed Asset Reporting Y

Agenda

76

Introduction

Course Overview

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

77 Copyright © 2013 Accenture All rights reserved.

• All users are now required to complete a Competency Assessment.

• <insert instructions on how to complete the competency assessment and which transactions, by role, the user needs to be assessed on>

Competency Assessment

Agenda

78

Introduction

Course Overview

Finance Overview Training

Key Learning Points

Summary

Competency Assessment

Questions & Answers

79

Questions?

80

Please remember to fill in the training feedback form!

Thank You

Version Control

81

Sign-off date Business Owner Version No.

Description / Reason for Change