36

Unlocking the Potential of India’s Gems & Jewellery Sector A Knowledge Report

| Date post: | 03-Jun-2018 |

| Category: |

Documents |

| Upload: | kavenindia |

| View: | 233 times |

| Download: | 0 times |

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 1/36

Unlocking the Potentialof India’sGems & Jewellery SectorA Knowledge Report

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 2/36

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 3/363Unlocking the Potential of India’s Gems & Jewellery Sector |

Executive Summary 06

Introduction 09

Market Structure and Potential 11

Growth Drivers, Opportunities &Challenges 13

Growth Drivers and Opportunities 13

Challenges 18

The Export Market 25

Recommendations 27

Recommendations for the Industry 27

Recommendations to the Government 30

About FICCI 33

About Technopak 34

Contents

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 4/364 | Unlocking the Potential of India’s Gems & Jewellery Sector

Foreword

Welcome to the first edition of the Indian Gem and Jewellery industry Knowledge report prepared jointlyby FICC and Technopak. It is being brought out on the occasion of FICCI’s International Conference forthe Indian Gem and Jewellery industry focusing on “Opportunities Led Growth”. We take this opportunityto thank Technopak Advisors our Knowledge Partners, who have devoted their valuable time, resources

and expertise to prepare this document on our behest

The Indian gem and jewellery industry is at a very significant point in its development. During the last fewdecades, the export side has developed, modernized and grown immensely and has been catering tothe global markets, particularly the USA. Meanwhile the much larger domestic industry continued with itstraditional structures and practices.

Since 2000, the export players began to get involved in the domestic industry, even as some of the largerdomestic jewellers began to adopt more contemporary business practices. In the context of the slowdownin the US market over the last few years, and the global financial crisis that we experienced last year, thisprocess has further accelerated to a great extent.

The Indian domestic market has shown very promising signs, and there has been a stupendous growthand increase in penetration of the brands and organized retail across the categories namely FMCG,Durables, Apparels, and Home Improvement etc. There is a great potential for the gem and jewellery sectorto achieve similar growth.

While exports will continue to play an important role in earning foreign exchange and providing employmentto large numbers, we have to ensure that the domestic industry marches in step with the transformationsweeping through other lifestyle segments, and modernizes itself in terms of products, outlook and businesspractices. The socio-economic conditions are ripe for this change with the large youthful population that isintegrating with a global culture having significant disposable incomes.

Mehul Choksi, Chairman, Gems & Jewellery Committee, FICCI

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 5/365Unlocking the Potential of India’s Gems & Jewellery Sector |

The large organized players within the industry have an important role to play in this process as they cancatalyse the growth of the industry, set higher standards and create more value across the value chain.This FICCI-Technopak report looks at all these factors in detail and provides many relevant pointers for thedirection of change.

But a forward looking industry is not enough, a business environment conducive to growth is equallyessential. The industry has been interacting with the government, voicing our concerns and indicating thedirection of the changes we desire. Many of these areas have been summarized in the report. Bodies likeFICCI and other industry associations have to work together and with the government to hasten the paceof policy change.

We thank Technopak for their effort at integrating their expertise with information and inputs gathered fromthe stake holders in the industry to prepare this report that is both comprehensive and concise. It will surelybe appreciated widely throughout the industry and among policy makers.

FICCI would also like to acknowledge the efforts made by the members and stakeholders of the Gem &Jewellery industry in various initiatives including this report and the Conference and hope that they willprovide a vigorous push to the growth of the industry in the years ahead.

Mehul ChoksiChairman, Gems & Jewellery CommitteeFICCI

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 6/366 | Unlocking the Potential of India’s Gems & Jewellery Sector

Executive Summary

Traditionally the focus of the gems and jewellery manufacturers has been on the large global markets.Indeed for years, barring the last year or so, these international markets have given large and growingbusiness to the Indian exporters and have contributed in creation of significant jobs in the country. The

Indian players, duly supported by the Government of India are placed highly competitively in the market.Hopefully with the revival of the international markets, the Indian players would again stand to gain.

We believe that the domestic market holds similar or even brighter potential for gems & jewellery sector.The industry can be put on accelerated growth path provided the industry, the government and otherstakeholders plan and act on the initiatives required by the transforming market. In the process the industryshall continue to generate large amounts of foreign exchange and employment to the Indian socio-economic fabric.

The key drivers and growth opportunities for this sector are:-

Growing spending power:•

There is a great opportunity to capitalise on the growing spending power ofthe Indians with increased discretionary spending such as that on Gems & Jewellery.

Organised players acting as catalysts:• The organised players (includes current players who arebecoming more organised) would act as a catalyst in this transformation. Although the current proportionof the organised sector is small at present, the available potential and growing momentum is veryencouraging.

Rationalised cost structures:• One good aspect of the slowdown is that it has also controlled therampant rise in key input costs such as manpower and real estate and this should accelerate the recoveryand growth.

While the opportunities and drivers are strong we need to also surmount some of the key challenges: -

Changing share of wallet:• While the share of wallet is changing for the Indian consumer towardsdiscretionary spending, other categories such as travel, entertainment, electronics etc are growing theirshare at a faster rate. Thus, we need to position Gems & Jewellery as a sought after lifestyle productespecially amongst todays’ youth.

Mindset & Manpower:• With the changing consumer and business environment there is also a need totransform the mindset & manpower in the industry. The human resources and leaders in the industry willneed to adopt a more modern and professional approach towards work and management while they alsoretain the best practices that our rich tradition in Gems & Jewellery has enabled us to cultivate. Bringingin outside professionals in this sector will help accelerate the change.

Upgradation & Modernisation• : Besides modernising manpower and mindset; the technology, systemsand processes also need to be upgraded and modernised. This would help not only to achieve the nextleap in growth but also to compete with rising international competition.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 7/367Unlocking the Potential of India’s Gems & Jewellery Sector |

Financing:• To enable all this growth and transformation the flow of finances to this sector would alsoneed to be ramped up, especially to the unorganised retail.

To make the most of the opportunities and overcome the challenges we have identified a set ofrecommendations for the industry and government. These should serve as a good starting point to kick-start this proposed journey of higher growth and excellence.

Recommendations for the Industry

(a) Potential Assessment and Strengthening Consumer UnderstandingThere is dire need for the industry to first understand the various segments of the consumers and theirpurchasing and shopping needs. The proposition, design and brands can be created around theseneeds.

(b) Invest in Retailing and BrandsThe organised retail and brands can provide impetus to the sector. Appropriate investments can potentiallyput the category on a higher priority in the consumer basket and can generate the higher margins. Anoverall investment of US $ 2 billion is required by for branded jewellery to achieve 15% share of the market.

A possible solution here is to create highly active Industry Co-ordination to bring together the outside

investors and industry stars.

(c) Improve skill sets & quality of peopleThe Gems & Jewellery industry needs to systematically and collectively invest in up gradation of the skillsets of its workforce through increased training and manpower development programs. A joint effort by theIndustry to invest in the development of vocational training institutes could be a way forward with Industrycaptains leading the efforts to underwrite recruitment of graduates and participate in syllabus design &development.

(d) Enhance Product Design & Manufacturing Quality Standards A National Institute of Jewellery Design & Development would go a long way in providing the platform fordevelopment of a pipeline of innovative high quality designers that can serve the industry as a whole. IfIndustry captains come together to invest in setting up the institute or expanding existing ones, efforts canbe made to lobby to obtain Government support and create national “centres of excellence” like NIFT withmultiple campuses and courses.

(e) Promote adoption of Industry wide standards for gaining consumer trustEnhancement of product quality standards and incentives for increasing adoption of the standards will goa long way in improving consumer trust and enable the industry to gain share of wallet of the consumer inthe long run. Eventually it will also help in the spread of e-selling in India which has seen a lot of successin western markets.

(f) Co-operative use of resourcesTo bring down cost of operation and investments in the sector, industry players should adopt co-operativeuse of technology and marketing. Even retail space can be hired by co-operatives when foraying intointernational markets.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 8/368 | Unlocking the Potential of India’s Gems & Jewellery Sector

Recommendations to the Government

Government and Apex bodies could act as facilitators in broadening the outlook of the exporters /playersand help them in familiarizing with the changing scenario both in the domestic and international fronts,where moving up the value chain and adoption of modern practices has become compelling imperatives.

(a) Provide Industry status to Gems & Jewellery SectorSpecial cell to look into specific needs of Industry- At ~US $15 bn, the domestic Gems & Jewellery industrydeserves the same attention and interest as a number of other industries such as Textiles & Steel. Thedomestic Gems & Jewellery Retail sector could especially benefit a lot from Industry status. Creating

Technology Upgradation Fund (TUF) for facilitating the modernization of the manufacturing and designfacilities is another important initiative.

(b) Creation of Design Centers /Studios, Holding FairsThe importance of design has been highlighted by us in this report. This can help significantly in movingthe industry from commoditized selling to design based selling.

(c) Asset (Gold) based leverage This could help individual investors mortgage their gold and jewellery for credit. Perhaps RBI can think andact on this suggestion which can potentially unlock significant value.

(d) Regulatory Laws & TaxationThere are some regulations which are restricting the growth of the industry such as search & seizure laws.Perhaps there is case of rationalizing /removing these restrictive laws. At the same time there is dire needto standardization in the industry, which can restore the credibility of the industry. In terms of taxation thereshould be a continuation and further enhancements of tax benefits, notably deduction under section 10A /10B / 10AA of the Income tax Act. Removal of Octroi from Mumbai will also go be a big help as the city isa major hub of Gems & Jewellery.

(e) Modernize Labor LawsThis will enable Indian manufacturers to improve efficiencies, serve Indian consumers better and also grow

exports from India by allowing manufacturers to adopt more flexible labor practices.

(f) Increase the setting up of export focused SEZsThis would help to meet and the growing needs of exporters and create the infrastructure for even fasterexport growth. The policy could also help to promote the spread of industry across India besides thecurrent pockets in western & southern India.

(g) Gold exchange A physical or internet based exchange to trade precious metals could help the Indian population torediscover their age old investment preference for precious metals and jewellery which have time andagain proved to be safe instrument with good returns.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 9/36

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 10/3610 | Unlocking the Potential of India’s Gems & Jewellery Sector

At this juncture when we prepare ourselves to take the higher growth trajectory for this sector we areconfronted with some pertinent questions: -

How can we take the industry to an accelerated path?•

How can we ensure that the exports retain their competitiveness and leadership in dynamic world•

economy?

How can we improve the quantity and quality of supply of manpower to this sector to support rapid•

growth?

How can we move up the value chain to improve returns in this sector besides the revenues?•

How can we improve financing for smoother operations (working capital) and rapid growth (long-term•

debt, investment)? What role can the government play in this endeavor?

We have attempted to to answer some of these questions in this report. This document is based on theextensive research, interaction with the various stakeholders and Technopak body of knowledge, attemptsto assess the enormous untapped opportunities and presents some known (still the need of the hour)initiatives and some new initiatives which can perhaps be the starting point in the future journey.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 11/36Unlocking the Potential of India’s Gems & Jewellery Sector |11

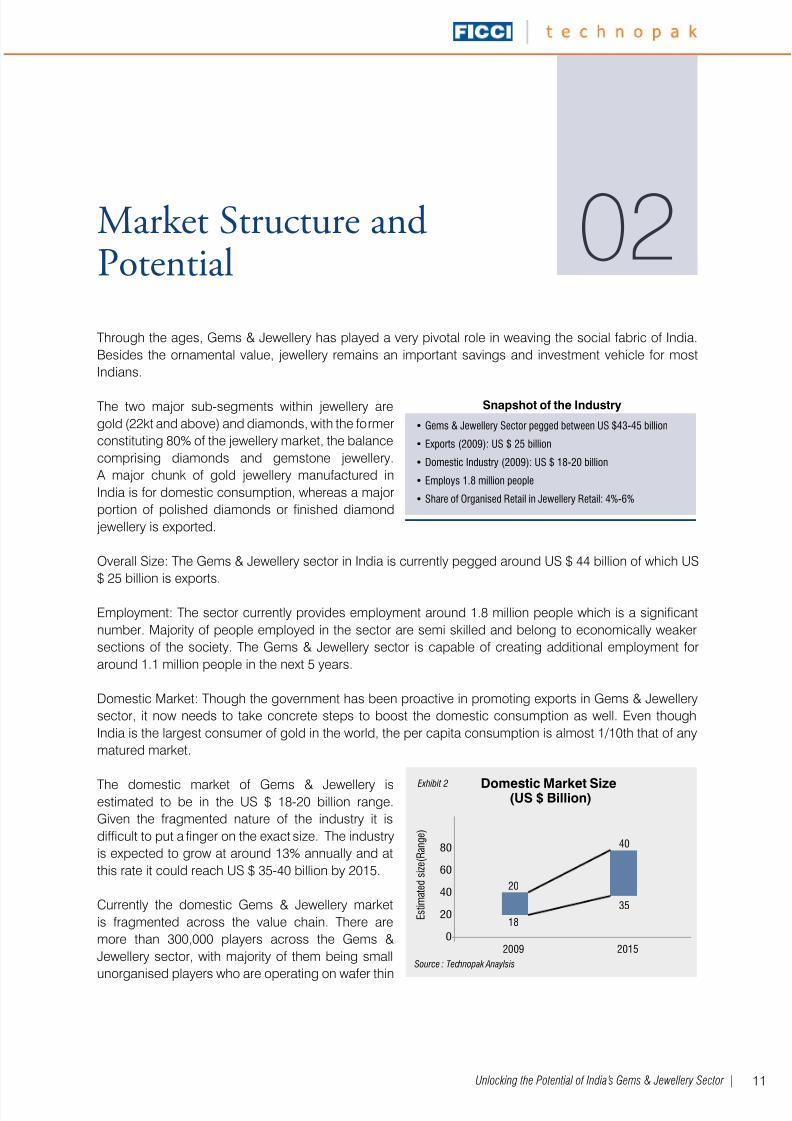

02Through the ages, Gems & Jewellery has played a very pivotal role in weaving the social fabric of India.Besides the ornamental value, jewellery remains an important savings and investment vehicle for mostIndians.

The two major sub-segments within jewellery aregold (22kt and above) and diamonds, with the formerconstituting 80% of the jewellery market, the balancecomprising diamonds and gemstone jewellery.

A major chunk of gold jewellery manufactured inIndia is for domestic consumption, whereas a majorportion of polished diamonds or finished diamondjewellery is exported.

Overall Size: The Gems & Jewellery sector in India is currently pegged around US $ 44 billion of which US$ 25 billion is exports.

Employment: The sector currently provides employment around 1.8 million people which is a significantnumber. Majority of people employed in the sector are semi skilled and belong to economically weakersections of the society. The Gems & Jewellery sector is capable of creating additional employment foraround 1.1 million people in the next 5 years.

Domestic Market: Though the government has been proactive in promoting exports in Gems & Jewellerysector, it now needs to take concrete steps to boost the domestic consumption as well. Even thoughIndia is the largest consumer of gold in the world, the per capita consumption is almost 1/10th that of anymatured market.

The domestic market of Gems & Jewellery isestimated to be in the US $ 18-20 billion range.Given the fragmented nature of the industry it isdifficult to put a finger on the exact size. The industryis expected to grow at around 13% annually and atthis rate it could reach US $ 35-40 billion by 2015.

Currently the domestic Gems & Jewellery marketis fragmented across the value chain. There aremore than 300,000 players across the Gems &Jewellery sector, with majority of them being smallunorganised players who are operating on wafer thin

Market Structure andPotential

Gems & Jewellery Sector pegged between US $43-45 billion•

Exports (2009): US $ 25 billion•

Domestic Industry (2009): US $ 18-20 billion•

Employs 1.8 million people•

Share of Organised Retail in Jewellery Retail: 4%-6%•

Snapshot of the Industry

Domestic Market Size(US $ Billion) Exhibit 2

2009 2015

35

40

20

18 E s t i m a t e d s

i z e ( R a n g e )

Source : Technopak Anaylsis

80

60

40

20

0

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 12/3612 | Unlocking the Potential of India’s Gems & Jewellery Sector

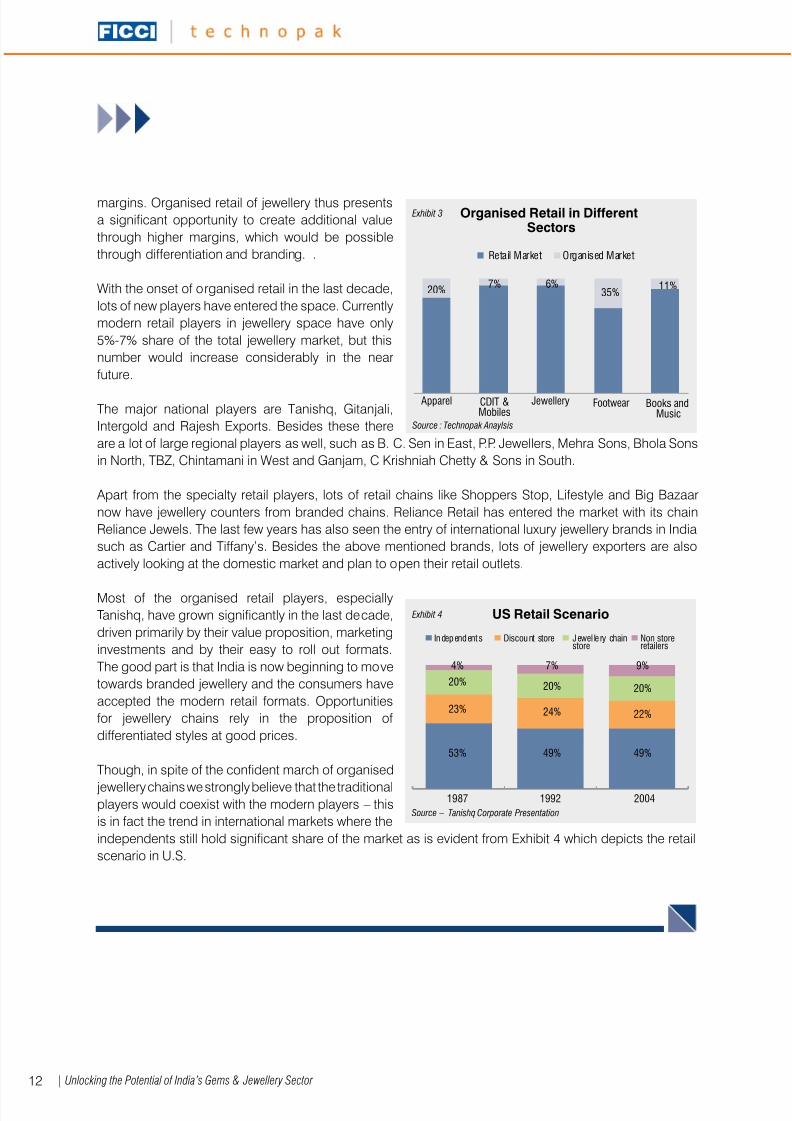

margins. Organised retail of jewellery thus presentsa significant opportunity to create additional valuethrough higher margins, which would be possiblethrough differentiation and branding. .

With the onset of organised retail in the last decade,lots of new players have entered the space. Currentlymodern retail players in jewellery space have only5%-7% share of the total jewellery market, but thisnumber would increase considerably in the nearfuture.

The major national players are Tanishq, Gitanjali,Intergold and Rajesh Exports. Besides these thereare a lot of large regional players as well, such as B. C. Sen in East, P.P. Jewellers, Mehra Sons, Bhola Sonsin North, TBZ, Chintamani in West and Ganjam, C Krishniah Chetty & Sons in South.

Apart from the specialty retail players, lots of retail chains like Shoppers Stop, Lifestyle and Big Bazaarnow have jewellery counters from branded chains. Reliance Retail has entered the market with its chainReliance Jewels. The last few years has also seen the entry of international luxury jewellery brands in Indiasuch as Cartier and Tiffany’s. Besides the above mentioned brands, lots of jewellery exporters are alsoactively looking at the domestic market and plan to open their retail outlets.

Most of the organised retail players, especiallyTanishq, have grown significantly in the last decade,driven primarily by their value proposition, marketinginvestments and by their easy to roll out formats.The good part is that India is now beginning to movetowards branded jewellery and the consumers haveaccepted the modern retail formats. Opportunitiesfor jewellery chains rely in the proposition ofdifferentiated styles at good prices.

Though, in spite of the confident march of organised

jewellery chains we strongly believe that the traditionalplayers would coexist with the modern players – thisis in fact the trend in international markets where theindependents still hold significant share of the market as is evident from Exhibit 4 which depicts the retailscenario in U.S.

Organised Retail in DifferentSectors

Exhibit 3

Apparel

20% 7% 6%35%

11%

CDIT &Mobiles

Jewellery Footwear Books andMusic

Retail Market Organised Market

Source : Technopak Anaylsis

US Retail Scenario Exhibit 4

1987 1992 2004

Independent s Discount store Jewel le ry chainstore

Non storeretailers

53%

23%

20%

4%

49%

24%

20%

7%

49%

22%

20%

9%

Source – Tanishq Corporate Presentation

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 13/36Unlocking the Potential of India’s Gems & Jewellery Sector |13

03Growth Drivers and Opportunities

Growing Spending Power

Despite recent slowdown, the move from a“Pyramid” to a “Diamond” shaped structure ofthe Indian consumer segments is well and trulyunderway. Robust income growth particularly in theservice sector accompanied with improvements ininfrastructure are enlarging consumer markets andaccelerating the convergence of consumer tastes.

With a real GDP of ~US$ 1.0 trillion, Globals,Strivers & Seekers are projected to grow at 11%,9% and 18% respectively, over the next 10 years.With this, India’s affluent & rich will number morethan the adult populations of many large countries.By 2025 Indian Middle class will reach 41% of thepopulation from 5% in 2005, creating a sizeableurban middle class. This will create fast paced andexciting opportunities for firms in the consumer &retail space.

Indias’ current per capita annual disposable incomeis expected to grow by 8-13% from the current level

of Rs. 32,299 in the next 5 years. Rising incomelevels with population increase will lead to anoverall increase in consumer spending and shift inconsumption basket of consumers from the basicproducts to more aspirational ones. As wealthgrows spend is added to discretionary categories,aspiration products and ultimately luxury products.Need based consumption categories to becomelow-involvement items for the “core” consuming classes. New, rapidly growing consumption categorieswould take a larger share of larger share of consumers’ household spending. Consumers will optimize theirpurchases largely on simple attributes of price & convenience (time efficiency) in order to release more

resources (money, time, mental involvement) for the aspiration/lifestyle based consumption categories.Gems and Jewellery falls in the aspirational based category and can therefore hold good potential.

Growth Drivers,Opportunities & Challenges

Over the next 10 years India’s affluent & rich will number more•

than the adult populations of many large countries

By 2025 Indian Middle class will reach 41% of the population•

Indias’ current per capital annual disposable income is expected•

to grow by 8-13%

There will be a shift in consumption basket of consumers from•

the basic products to more aspirational ones such as Gems &Jewellery

Growing Spending Power

1.2 40

3260

228

108

434

418612

27452

126

76304

293

76

2.4

10.9

91.3

101.1

3.3

5.155.1

106

74.1

9.533.1

94.9

93.1

49.9

Number ofhousholds

Houshold incomebrackets

Aggregatedisposable income

MillionUS $ US $ bn

Globals(> 20,000)

Strives(10,000-20,000)

Seekers (4,000-10,000)

Aspirers( 1,800 – 4,000)

Deprived(<1,800)

Globals(> 20,000)

Strives(10,000-20,000)Seekers (4,000-10,000)

Aspirers( 1,800 – 4,000)

Deprived(<1,800)

Globals(> 20,000)

Strives(10,000-20,000)

Seekers (4,000-10,000)

Aspirers( 1,800 – 4,000)

Deprived(<1,800)

2 0 0

5

2 0 1 6 P

2 0 2

5 P

The Indian Consumer Spectrum Exhibit 5

Source – Industry Reports

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 14/3614 | Unlocking the Potential of India’s Gems & Jewellery Sector

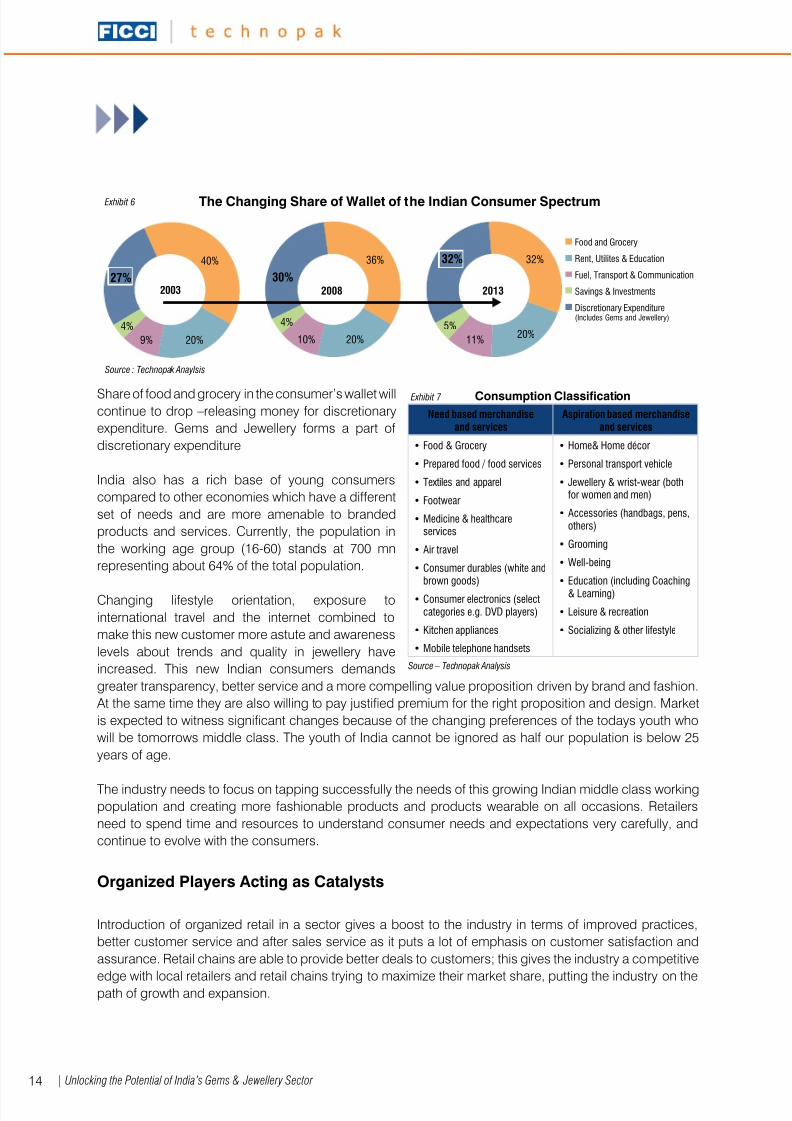

Share of food and grocery in the consumer’s wallet willcontinue to drop –releasing money for discretionaryexpenditure. Gems and Jewellery forms a part ofdiscretionary expenditure

India also has a rich base of young consumerscompared to other economies which have a differentset of needs and are more amenable to brandedproducts and services. Currently, the population inthe working age group (16-60) stands at 700 mnrepresenting about 64% of the total population.

Changing lifestyle orientation, exposure tointernational travel and the internet combined tomake this new customer more astute and awarenesslevels about trends and quality in jewellery haveincreased. This new Indian consumers demandsgreater transparency, better service and a more compelling value proposition driven by brand and fashion.

At the same time they are also willing to pay justified premium for the right proposition and design. Marketis expected to witness significant changes because of the changing preferences of the todays youth whowill be tomorrows middle class. The youth of India cannot be ignored as half our population is below 25years of age.

The industry needs to focus on tapping successfully the needs of this growing Indian middle class workingpopulation and creating more fashionable products and products wearable on all occasions. Retailersneed to spend time and resources to understand consumer needs and expectations very carefully, andcontinue to evolve with the consumers.

Organized Players Acting as Catalysts

Introduction of organized retail in a sector gives a boost to the industry in terms of improved practices,better customer service and after sales service as it puts a lot of emphasis on customer satisfaction andassurance. Retail chains are able to provide better deals to customers; this gives the industry a competitive

edge with local retailers and retail chains trying to maximize their market share, putting the industry on thepath of growth and expansion.

The Changing Share of Wallet of the Indian Consumer Spectrum Exhibit 6

Food and Grocery

Rent, Utilites & Education

Fuel, Transport & Communication

Savings & Investments

Discretionary Expenditure(Includes Gems and Jewellery)

40%

20%9%

4%

27%2003

20%10%

4%

30%

36%

2008

20%11%

5%

32%32%

2013

Source : Technopak Anaylsis

Exhibit 7

Source – Technopak Analysis

Consumption ClassificationNeed based merchandise

and servicesAspiration based merchandise

and services

Food & Grocery•

Prepared food / food services•

Textiles and apparel•

Footwear •

Medicine & healthcare•

services

Air travel•

Consumer durables (white and•

brown goods)

Consumer electronics (select•

categories e.g. DVD players)

Kitchen appliances•

Mobile telephone handsets•

Home& Home décor •

Personal transport vehicle•

Jewellery & wrist-wear (both•

for women and men)

Accessories (handbags, pens,•

others)

Grooming•

Well-being•

Education (including Coaching•

& Learning)Leisure & recreation•

Socializing & other lifestyle•

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 15/3615Unlocking the Potential of India’s Gems & Jewellery Sector |

Organized retail in the jewellery segment is a fairly newconcept. Currently organized retail has a penetrationbetween 5-7% but this is expected to grow in thenext few years. The expansion of organized retailand brands can provide impetus to this sector.

Already major retail chains like Big Bazaar, ShoppersStop, Pantaloons, Lifestyle etc have started havingjewellery section or “Shop-in-Shops” in their stores.Branded jewellery in India can now be seen as adeveloping phenomenon. The impact of thesemodern formats will be felt most in Urban India. We

anticipate that large investments of about US $ 1billion in the coming years would be made by largeretailers/brands which would catalyze the growth ofthe industry, set higher standards and create valueaddition across the industry. As is evident fromexhibit 8 below, retailing of gems and jewellery couldbe very lucrative once the startup phase is over.

The entry of leading brands like Gili (Gitanjali Group,1994), Tanishq (Tata Group, 1995), Sangini (JV ofSanghavi Exports and Gitanjali Group, 2004), Ishi’s (Suhashish Diamonds, 2003) Scintillating (DhanrajDhadda Group, 2003), Orra (Rosy Blue Group, 2004), Shubh, Laabh (Rajesh Exports, 2006) amongstmany others into the organized jewellery segment characterised the expansion phase. Tanishq (Tata group)has been a pioneer and contributes now to the maximum share of the organized retail jewellery market.These brands promised great quality and the best designs both traditional and contemporary.

The major brands pulling the organized market have now reached a critical point and are looking for moreopportunities to grow. They are already well established in all the top tier cities and state capitals in Indiaand are now looking to concentrate on their existing base and extend to other categories. Also there aremajor plans of expansion in tier 2 and tier 3 cities with the opening of new stores. For instance, Tanishqis planning to triple its turnover in the next five years timeframe by opening new stores and improvingrevenues in the existing ones.

Food &Grocery

CDITFootwear

Books & Music

Pharma & Wellness

Home

Apparel

Jewellery35%30%25%20%15%10%

5%0%

-5%-2% 2% 4% 6% 8% 10% 12% 14%

R O C E

ROCE vs EBITDA

EBITDA

Exhibit 8

Source : Technopak Anaylsis

Company Turnover 2009(Rs. Crores) Number of Outlets Announced Plans

Tanishq 2370 117 Tanishq plans to triple its turnover by opening new stores and focusing onimproving the revenues per store of the existing ones

Gitanjali Group 1275 1246 outlets includingshop in shops

Announced plans for 100 stores in May 2009 of which 30-40 were to belifestyle stores

Goldplus 390 30The retail brand plans to reach Tier-IV and Tier-V cities representing thesmaller towns and rural India with over 25 Goldplus stores across in sixstates

Reliance Jewels NA 15 Plan to open 85 more in next three years

Big Bazaar (Navras) NA 60 Shop-in-shops Plan to go to 150 by 2011

Rajesh Exports 100 30 Expansion after consolidating current turnover

Exhibit 9

Source – Company Announcements & Official Websites

Snapshot of a Few Organised Retail Players

Expansion of organized retail improves competitiveness and•

ultimately customer satisfaction

Currently organized retail has a penetration between 5-7% but•

this is expected to grow in the next few years

Branded jewellery in India can now be seen as a developing•

phenomenon

Compared to other categories jewellery is quite lucrative in terms•

of financial returns

Organized Players Acting as Catalysts

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 16/3616 | Unlocking the Potential of India’s Gems & Jewellery Sector

The last few years have seen the entry of a number of luxury brands in India such as Jimmy Choo, Gucci,Christian Dior, Louis Vuitton, Cartier, Piaget, Tiffany, Moschino and others. Many of them such as Cartierand Tiffany’s are well known for their jewellery ranges.

Better designs, new ranges and innovative marketing are the factors in the success of these brands inthe past few years. Retail chains focusing on these aspects are well positioned to rise since the customerwants to see variety in his purchases and the brand providing the same takes the cake. Latest ways ofsegmentation, targeting various consumer segments with specific designs and exclusive range and newusage styles has attracted a new set of consumers and created new occasions.

Thus it is very important to gain the momentum in this direction and focus on consumer research &

innovation in design. Players are also required to focus more on marketing and branding efforts and createinnovative campaigns to attract the new set of customers and increase the frequency of their purchaseoccasions. Globally there are examples of very successful campaigns that have been launched and havetranslated into a steep increase in the sales and revenue.

Real Estate and Other Costs are Now Under Manageable Limits

Last years’ slowdown has pushed the real estate prices southwards with substantial drop in the valueaccompanied far better lease terms. The malls & the main markets across the country saw a drop of 25%to 30% in footfalls and 10% to 15% dip in sales. There have been corrections of rentals in the range of 25%to 40% across major cities and markets over the last 2 to 3 quarters in 2009. The market is taking a ‘U’ turnfrom being landlord/developer driven market to being retailer driven. Developers are also experiencing lowoccupancy rates, (10-15% on an average) and have low negotiation power for charging high rental ratesdue to sluggish demand from retailers for new space booking. This is a good sign for the jewellery retailerslooking for expansion opportunities.

Case Studies - Marketing Success

WGC – Akshay Trithiya DTC – Nakshatra De Beers

Till some years ago, not many knew what the Akshaya Trithiya day stood for. It was aday largely celebrated in parts of Tamil Nadu& Maharashtra. People considered it to be anauspicious day to make purchases, as theybelieved it would be protected by Lord Vishnu.But it was after a massive campaign run byWorld Gold Council (WGC), an internationalorganisation funded by leading gold miningcompanies, that the day assumed importanceas an occasion to buy gold. Adding to thefrenzy, jewellery stores and goldsmiths luredcustomers with discounts, 24-hour sales and“latest designs”. In 2006 Akshaya Trithiya salesjumped 14% in terms of value and in 2007 theyjumped 55% in volume terms over the previousyear.

De Beers’ success with marketing of Diamondsin the west is well known, especially their “ADiamond is Forever” campaign. DTC whichis also closely associated with De Beerspulled another masterstroke in India through the Nakshatra campaign. Based on soundresearch, excellent marketing communicationand perfectly cast celebrity endorsement anage old Indian Jewellery design was used tocapture the imagination of the Indian buyer.The initiative was so successful that Nakshatrahas subsequently become a top brand whileit was originally meant to be only a vehicle toarouse cravings for diamonds amongst Indianconsumers. In the past few years diamondjewellery has recorded growth rates of above25%.

De Beers: “The Right Hand Ring Campaign”brings out the success story of De Beersby tracing its growth over a period of time.Realizing that the non-bridal market for diamond

rings had an immense potential, De Beers thenlaunched a campaign in 2003 targeted atindependent and accomplished women, whowanted to buy or receive diamond rings fornon-traditional reasons. The novel concept theypromoted was the “Women of the world, raiseyour right hand”. Which created a huge impact,according to industry sources, had become a$5 billion category by 2004. Right hand ringssuch as modern vintage, contemporary, floraland romantic brought about a psychologicalchange in the attitude of women consumers.

The key learning is that occasion based buyingof jewellery in India is strong. An effective

marketing connect of occasions with jewellerycan work wonders

The key learning is that a professional approach towards marketing can be very effective and

yield high returns through creation of high-margin brands

The key learning is creating new non traditionalways of motivating consumers to make thepurchase by realizing the need gaps in themarket and establishing an effective marketingconnect

Noteworthy Marketing Campaigns

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 17/3617Unlocking the Potential of India’s Gems & Jewellery Sector |

The Jewellery market is big and growing and the pricing situation has become more comfortable now than itever was. Retailers can get hold of new space at more favorable terms than before. New operating modelssuch as daily rental model, revenue sharing arrangements and minimum guarantee amount have nowbeen worked upon by mall owners to lure retailers towards their malls. Market is also expected to witnessmore quality space as developers are placing increasing importance to mall planning and managementthan just creating mall based on euphoria and hype, which the market saw in 2006-07. The markets arealso witnessing revival in customer demand and confidence. The slowdown has helped in maintaining agood supply demand equation, especially for markets which were staring at an oversupply situation.

Similarly the other costs such as manpower have shown stability, which would favorably impact the industry.Employment scenario becoming gloomy on the wake of slowdown coupled with decline in terms of salaryincrements and incentives in 2009 has helped the companies in controlling their payroll cost structures.Job instability in the market also reduced the attrition rates of employees in the industry. The share ofmanpower costs in the total operational expenses have reduced in 2009, they had increased substantiallyin 2007-08.

Exhibit 10 State of the Retail Real Estate MarketCity Micro Market Rental Values (INR/Month/sqft) % Change from 1 year ago

MumbaiGoregaonVashiGhatkopar

290185215

-24%-38%-36%

NCRNoidaSouth DelhiGurgaon

310490250

-35%-26%-35%

BangaloreKoramangalaCunninghum RoadMagrath Road

400210350

-18%-7%-5%

Chennai Chennai Central 220 -14%

Hyderabad NTR GardenHimayatnagar Banjara Hill No 1

10090130

-9%-28%-42%

PuneBund garden Road/ Koregaon Park Ganesh Khind RoadNagar Road

240140170

-31%-36%-6%

KolkataRajarhatSalt LakeElgin Road

120425315

-1%-15%-22%

AhmedabadKankaria LakeSG HighwayDrive in Road

459070

-55%-41%-33%

Source – Cushman and wakefield Research * Rentals mentioned are for ground floor premises on carpet area, for vanilla retailers

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 18/3618 | Unlocking the Potential of India’s Gems & Jewellery Sector

Challenges

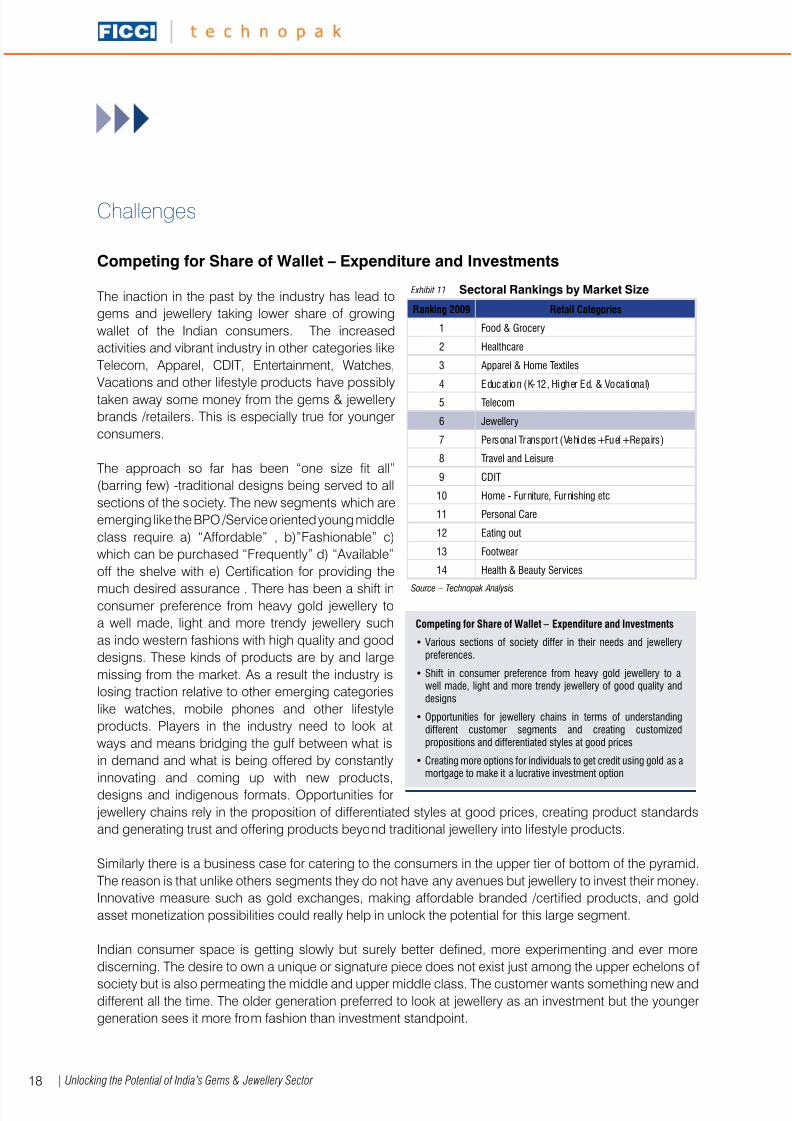

Competing for Share of Wallet – Expenditure and Investments

The inaction in the past by the industry has lead togems and jewellery taking lower share of growingwallet of the Indian consumers. The increasedactivities and vibrant industry in other categories likeTelecom, Apparel, CDIT, Entertainment, Watches,

Vacations and other lifestyle products have possiblytaken away some money from the gems & jewellerybrands /retailers. This is especially true for youngerconsumers.

The approach so far has been “one size fit all”(barring few) -traditional designs being served to allsections of the society. The new segments which areemerging like the BPO /Service oriented young middleclass require a) “Affordable” , b)”Fashionable” c)which can be purchased “Frequently” d) “Available”off the shelve with e) Certification for providing the

much desired assurance . There has been a shift inconsumer preference from heavy gold jewellery toa well made, light and more trendy jewellery suchas indo western fashions with high quality and gooddesigns. These kinds of products are by and largemissing from the market. As a result the industry islosing traction relative to other emerging categorieslike watches, mobile phones and other lifestyleproducts. Players in the industry need to look atways and means bridging the gulf between what isin demand and what is being offered by constantlyinnovating and coming up with new products,designs and indigenous formats. Opportunities forjewellery chains rely in the proposition of differentiated styles at good prices, creating product standardsand generating trust and offering products beyond traditional jewellery into lifestyle products.

Similarly there is a business case for catering to the consumers in the upper tier of bottom of the pyramid.The reason is that unlike others segments they do not have any avenues but jewellery to invest their money.Innovative measure such as gold exchanges, making affordable branded /certified products, and goldasset monetization possibilities could really help in unlock the potential for this large segment.

Indian consumer space is getting slowly but surely better defined, more experimenting and ever morediscerning. The desire to own a unique or signature piece does not exist just among the upper echelons of

society but is also permeating the middle and upper middle class. The customer wants something new anddifferent all the time. The older generation preferred to look at jewellery as an investment but the youngergeneration sees it more from fashion than investment standpoint.

Exhibit 11

Source – Technopak Analysis

Sectoral Rankings by Market Size

Ranking 2009 Retail Categories

1 Food & Grocery

2 Healthcare

3 Apparel & Home Textiles

4 Education (K-12, Higher Ed. & Vocational)

5 Telecom

6 Jewellery

7 Personal Transport (Vehicles+Fuel+Repairs)

8 Travel and Leisure

9 CDIT

10 Home - Furniture, Furnishing etc

11 Personal Care

12 Eating out

13 Footwear

14 Health & Beauty Services

Competing for Share of Wallet – Expenditure and Investments

Various sections of society differ in their needs and jewellery•

preferences.

Shift in consumer preference from heavy gold jewellery to a•

well made, light and more trendy jewellery of good quality anddesigns

Opportunities for jewellery chains in terms of understanding•

different customer segments and creating customizedpropositions and differentiated styles at good prices

Creating more options for individuals to get credit using gold as a•

mortgage to make it a lucrative investment option

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 19/3619Unlocking the Potential of India’s Gems & Jewellery Sector |

Brands and Retailers also need to keep in mindthe regional differences while creating their productproposition. India has great geographical diversityand cultural differences for jewellery. While northernand southern Indian jewellery is made from the purestof gold, Rajasthan delights in silver, precious stones,shells and mirror work. Likewise, Kashmiris are fondof silver ornaments set with semi- precious Ferozas.

The imperative for brands and retailers is tounderstand the various consumer segments and

make customized propositions and suitable designswhich have been missing, resulting in its lowerpreference in comparison with other emergingcategories. In this regards, the industry can drawsignificant learnings from other similar industries likewatches, which has very successfully positioned itselfas s lifestyle accessory and a fashion statement ( asopposed to functional positioning), thereby creatingsignificant value. As exhibit 13 depicts, the maximumvalue addition typically happens at the retail end.In the last two decades several alterative investmentoptions such a stocks and real estate have emerged.Gold as an investment option is facing competitionhere as well. As per “The World Wealth Report”the investment in gold is less than 10% of the totalinvestments for HNIs. Options have to be created forindividuals to get credit using gold as a mortgage tomake it a lucrative investment option.

Watch Industry – A Case Study

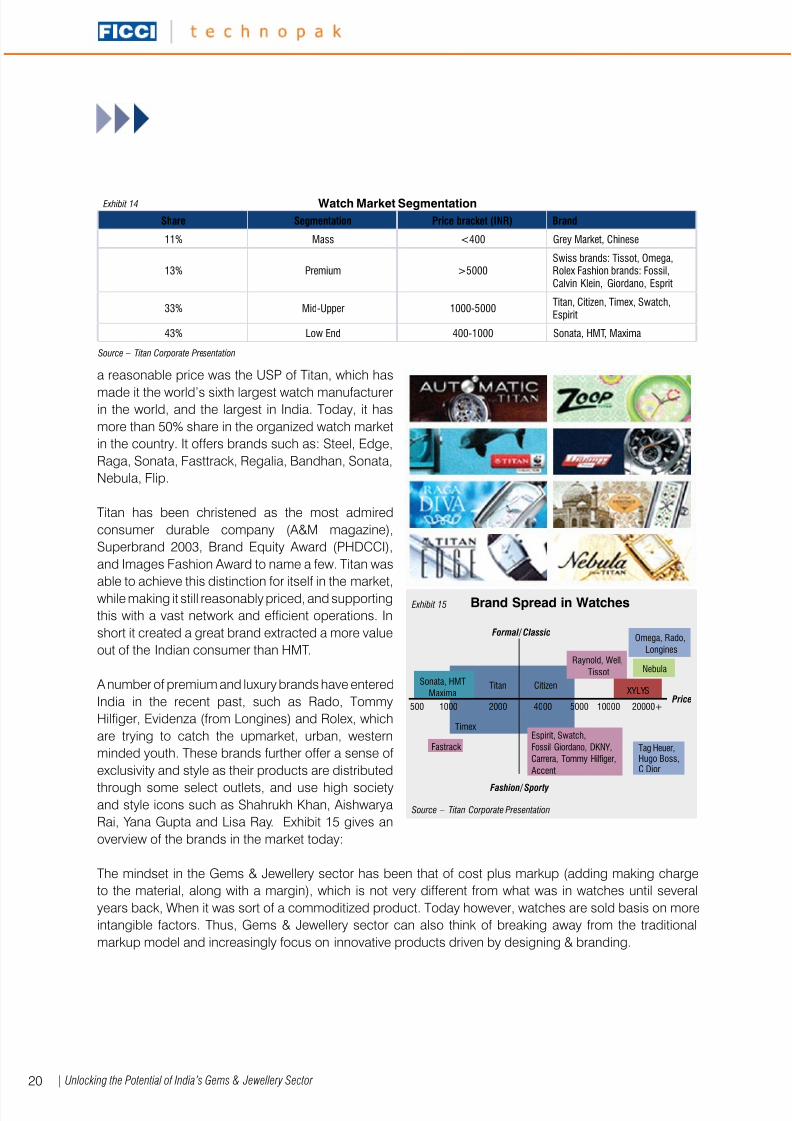

India is an under-penetrated market for watches,with only 27% of Indians owning a watch, and morethan 80% of the market by volume is below INR500 per watch. Exhibit 14 gives an idea about thesegmentation of the market:

Given the price sensitive Indian, watches as a segment has taken its time to penetrate the market. HMT wasthe first major watch manufacturer in the country, and undisputedly the market leader in this category for alot of years. The watch-maker offered sturdiness and reliability at a low price. The focus was not so muchon the design and brand as much as affordability for the average Indian.

However, with the entry of Titan in 1984 as a Joint Venture between the Tata group and Tamil Nadu IndustrialDevelopment Corporation, rules of the industry changed drastically. Designing, Branding and Precision at

120%

100%

80%

60%

40%

20%

0%

% Value Addition

72.3% Retail-Diamond JewelleryValue of diamond content inretailValue of polished from localproduction

Net rough used in localproduction

Rough sales to cuttingcentre

Rough production valueRough production

Mine sales

Exhibit 13

Source – International Diamond Exchange, 2007

International Diamond Jewellery Value Chain

Shift in Consumer Behavior Exhibit 12

Source – Geetanjali Group Presentation

Urbranded from familyjeweller Branded

Plain metaljewellery

Gems studdedjewellery

Jewellery forinvestment

Jewellery forfashion

Traditional ethnic andchunky designs Fashionable lightweight &

innovative designs

Marriage and festivalseason as peak seasons

Wearability & giftsspreading the demand

throught the year

jewellery sold oncommodity basis with

labor charges

jewellery being soldon a per piece bais

Yesterday Topday

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 20/3620 | Unlocking the Potential of India’s Gems & Jewellery Sector

a reasonable price was the USP of Titan, which has

made it the world’s sixth largest watch manufacturerin the world, and the largest in India. Today, it hasmore than 50% share in the organized watch marketin the country. It offers brands such as: Steel, Edge,Raga, Sonata, Fasttrack, Regalia, Bandhan, Sonata,Nebula, Flip.

Titan has been christened as the most admiredconsumer durable company (A&M magazine),Superbrand 2003, Brand Equity Award (PHDCCI),and Images Fashion Award to name a few. Titan wasable to achieve this distinction for itself in the market,while making it still reasonably priced, and supportingthis with a vast network and efficient operations. Inshort it created a great brand extracted a more valueout of the Indian consumer than HMT.

A number of premium and luxury brands have enteredIndia in the recent past, such as Rado, TommyHilfiger, Evidenza (from Longines) and Rolex, whichare trying to catch the upmarket, urban, westernminded youth. These brands further offer a sense ofexclusivity and style as their products are distributed

through some select outlets, and use high societyand style icons such as Shahrukh Khan, AishwaryaRai, Yana Gupta and Lisa Ray. Exhibit 15 gives anoverview of the brands in the market today:

The mindset in the Gems & Jewellery sector has been that of cost plus markup (adding making chargeto the material, along with a margin), which is not very different from what was in watches until severalyears back, When it was sort of a commoditized product. Today however, watches are sold basis on moreintangible factors. Thus, Gems & Jewellery sector can also think of breaking away from the traditionalmarkup model and increasingly focus on innovative products driven by designing & branding.

Share Segmentation Price bracket (INR) Brand

11% Mass <400 Grey Market, Chinese

13% Premium >5000Swiss brands: Tissot, Omega,Rolex Fashion brands: Fossil,Calvin Klein, Giordano, Esprit

33% Mid-Upper 1000-5000 Titan, Citizen, Timex, Swatch,Espirit

43% Low End 400-1000 Sonata, HMT, Maxima

Exhibit 14

Source – Titan Corporate Presentation

Watch Market Segmentation

Exhibit 15

Source – Titan Corporate Presentation

Brand Spread in Watches

Sonata, HMTMaxima

Raynold, Well,Tissot Nebula

XYLYS

Omega, Rado,Longines

Espirit, Swatch,Fossil Giordano, DKNY,Carrera, Tommy Hilfiger,Accent

Tag Heuer,Hugo Boss,C Dior

Formal/ Classic

Fashion/ Sporty

Price500 1000 2000

Titan Citizen

Timex

4000 5000 10000 20000+

Fastrack

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 21/3621Unlocking the Potential of India’s Gems & Jewellery Sector |

Mindset and Manpower

The Jewellery industry has traditionally been avery closely guarded industry, where skills of thetrade have been passed on within a family fromone generation to the other and restricted entry ofoutsiders. Although this has its own advantages, thisstructure of the industry has not allowed it to gain thescale benefits, and in professionalizing it to removeinefficiencies.

In order to tap the growing opportunity, the sector needs to attract and groom professionals at all levels –Managerial and Skilled workers. The sector so far has not caught the attention of the managerial resourcesbe at senior level or at entry level unlike other consumer product segments like FMCG, Durables or Retailfor that matter. The issue perhaps also stems from the fact that the majority of players operating in thesector have still not adopted the best practices from the corporate culture.

The sector currently employs close to 1.8 million people and in the next 6 years a further 1.1 million peoplewill be needed. As a large section of the workforce is employed in skill-based jobs such as diamondcutting, jewellery making, retail selling etc we need a large number of vocational training institutes spreadall across the country.

We can look at the apparel industry for solutions. It grew tremendously due to combined effort of favorablegovernment policies, investment in capacities, entry of multinationals, and the introduction of Fashiondesigners through a vast network of educational infrastructure. Thus, institutes like NIFT which have doneexceedingly well for their respective sectors, are more than just a need of the hour for the Gems & Jewelleryindustry today.

“National Institute of Fashion Technology wasset up in 1986 under the aegis of the Ministry ofTextiles, Government of India. It has emergedas the premier Institute of Design, Managementand Technology, developing professionalsfor taking up leadership positions in fashionbusiness in the emerging global scenario. NIFThas been granted statutory status under the actof Parliament of India in 2006, empowering the Institute to award degreesand other academic distinctions”

“The number of stores a Jewellerhas in India is equal to the numberof sons” - An industry leaderrequesting anonymity

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 22/3622 | Unlocking the Potential of India’s Gems & Jewellery Sector

There needs to be wholesome change, with the development of every skill set at every level of the industry,such as designing, marketing and management, apart from technical skills of workers. Government and

Apex bodies could act as facilitators in broadening the outlook of the exporters /players and help them infamiliarizing with the changing scenario both in the domestic and international fronts, where moving up thevalue chain and adoption of modern practices has become compelling imperatives.

Financing

In the Gems & Jewellery sector the government does not provide many innovative financing options forthe retailers and the wholesalers (refer Exhibit 17). Even though there are vanilla financing products for thejewellery retail sector, most of the retailers can’t avail the facility since they are unorganised.

The need of the hour is to develop some innovative solutions such as those available to the non-retailplayers and ensure access of the same to small unorganised retailers.

Apparel Gems & Jewellery

Both are sizeable sectors with a large export component

Both largely dominated by unorganized sectors

Both employ large chunks of the Indian population

Excellent educational infrastructure:India textile and apparel education sector is largest in the world with36 degree level engineering colleges, 56 diploma level institutesimparting education in textile technology dealing with yarn and fabricmanufacture, and more than 100 institutes offering education related to garment and fashion design and technology. The shining star in thisgallery is National Institute of Fashion Technology (NIFT); in May 2006 itwas recognized by an act of Parliament as an ‘Institute of Excellence’ ofDesign, Management and Technology in India.

Good educational infrastructure is limited

There is a need for a National Instituteof Gems & Jewellery and numerousvocational training institutes

Exhibit 16

Source – NIFT Website, Various Internet Sources

Learnings for Gems & Jewellery from the Textile & Apparel Sector

Exhibit 17

Source – FICCI

Financing Options in Gems & Jewellery

Financing Options Raw MaterialSourcing

Raw MaterialProcessing

Raw MaterialTrading

JewelleryManufacturing Wholesaling Retailing

Packing Credit (for diamond exportsonly)

Available for 180 days pre-shipment•

and 180 days post-shipment

Gold Loan

Available against bank guarantee•

Upto 90 days pre-shipment and 180•

days post-shipment

LC on gold is also available for 90•

days though nominated agencies

Cash Credit for Domestic Consumption

Working Capital demand Loan

LC – 180 to 364 days

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 23/3623Unlocking the Potential of India’s Gems & Jewellery Sector |

Also, since the sector lacks an “industry status” itdoes not qualify for obtaining friendly-terms financialassistance or any external financial aid in thedomestic market from banks or International fundingbodies.

An important requirement would be to makethe unorganised players more professional andtransparent in their dealings.

Upgradation /Modernization

As mentioned earlier, the industry needs to modernize itself. This is in light of the fact the industry is alsohighly fragmented with minimal benefits of economies of scale, latest production techniques or designcenters. All of them are critical for the industry to grow rapily and move towards the higher ends of thevalue chain.

In such a scenario the government could help with the creation of a Technology Upgradation Fund (TUF)for this sector. Such schemes have worked well in other sectors such as Textile & Apparel. Highlights of theTextile & Apparel TUF are given below: -

At the end of the last decade the apparel sector was in dire need of up gradation of technology to remain•

competitive internationally.However, the player specifically the small scale industries lacked both the funds as well as intent.•

TUFS was introducted with the intention of upgradation of technology.•

Under this scheme a capital subsidy of 10% and interest subsidy of 5% was provided for technology•

upgradation initiatives.

It was a grand success since during the period the ministry has disbursed INR 66,275 crore under the•

scheme, while it propelled investment of more than Rs. 1,16,981 crore.

The Indian industry can perhaps learn significantly from Turkey where the industralization of the jewlerysegment has transformed it into one representing the modern flexible production techniques, supreme

craftsmenship, excellent quality and immense variety.

An example of the benefits of focused structural support is thedomestic Film industry, which after the grant of Industry status in2000 has grown at a CAGR of 18% in the last 9 years, driven bygreater organization of the industry and better access to organizedsources of financing. IDBI Bank alone raised its film financing fromzero in 2000 to INR 500 crore in 2009. The government decision to grant Bollywood the industry status has also helped in stemming the flow of legitimate and appropriate funding to the sector.

Case Study – Indian Film Industry

Turkey Gold Jewellery – A Case Study

Turkey’s Gold exports have been on a strong vertical growth trajectoryfor the past 10 years reaching almost US $ 1.6 billion in 2008. Turkeyis expected to dethrone Italy as the largest exporter of Gold Jewellery,as it continues to grow strongly while Italy falls behind.

The Turkish jewellery sector traditionally was beset with problems,such as low usage of technology, high fragmentation, poor emphasison design etc. These problems were similar to the ones plaguing thecurrent Indian industry. During the 90s, the sector finally opened upfinancially due to several reasons, most notably technology, design,investment in production capacities, and government initiatives toliberalize the gold market. Since then the jewellery sector has charted

a blazing path which has borne great fruit in the last decade.

Exhibit 18 Turkey Gems & JewelleryExports (US $ Million)

0

500

1000

1500

2000

207

285

284431

568708

9321127

1095 1490

1585

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source – Undersecretariat of Foreign trade (Turkey)

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 24/3624 | Unlocking the Potential of India’s Gems & Jewellery Sector

Key Driver’s of Turkey’s Growth

Technology Centric Large Scale Manufacturing – In the 90’s•

Turkey’s organised sector only had a couple of workshops with100-200 workers. Today there are at least 15 factories with1000 plus workers. Total production capacity in Turkey for GoldJewellery is 400 tons per annum. The machine park of the industryhas upgraded to adopt the highest level of technology. Allowingit to meet the international customers’ requirements for intricatedesigns, quality and reliability of supply.

Focus on Designs – In the mid 90’s jewellery companies also star ted•

employing designers in a big way and now most of the world’s largestdesign teams work in Turkey. To promote jewellery designing WoldGold Council has been organising design competitions since 1994and there is a plethora of courses from universities to vocationalinstitutes for churning out well-trained designers. Use of ComputerAided Design (CAD) is now omnipresent.

Leveraging Tradition – Like India Turkey too has a rich heritage of indigenous designs and craftsmanship. Well-known techniques include filigree,•

niello & wickerwork. So while Turkey made a name for itself by excelling in international designs it then used the respect and attention it gained to propagate its unique heritage and strengths as well. Sales to tourists and “luggage traders” account for a whopping 70% of the total produce.Besides, international style jewellery many tourists refer to buy the intricate local designs for their uniqueness and as souvenirs.

Infrastructure – in 1995 a gold exchange was started by the Turkish Government. Today it has 62 members comprising of banks, precious metal•

companies, currency offices etc. A state of the art Istanbul Gold Refinery commenced operations in 2002 augmenting supply of quality gold.It has the technology to produce 9999 purity gold and convert scrap or Dore bullion into 9999 purity in four hours. Istanbul’s famous GrandBazaar which has been a historical centre for gold trade has been developed and positioned to attract buyers and tourists from the world overin a distinct yet friendly retail and wholesale environment. Istanbul boasts of the world’s largest integrated jewellery centre – Kuyumcukent. Theconstruction was started in 1996 and it has 328,000 square metres of built-up area with 2800 production units and shops. Besides designers, traders, retailers and manufacturers there is also a gold refinery branch and a branch of the gold exchange is expected soon.

Fairs & Journals – Four large scale jewellery fairs are organised in Turkey every year. The well-known Istanbul Jewellery Show takes place twice•

a year. Gold News is a widely circulated periodical which is published 6 times a year by Istanbul Chamber of Jewellery. Besides this the industryplayers, industry associations and Turkish Government regularly organise events and road-shows across the world to promote Turkish goldjewellery.

Exhibit 19 Kuyumcukent

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 25/36Unlocking the Potential of India’s Gems & Jewellery Sector |25

04Gems & Jewellery exports are the back-bone of thesector and also of our overall exports. The sector isexpected to grow at a CAGR of 15% to reach a size

of US $ 58 billion by 2015 from the current US $ 25billion.

In the export market, India has gained a competitiveadvantage because of its ability to deliver goodquality at low cost. For example, cost of cutting adiamond in India is 7% of that in Belgium and 60% ofthat in China. Highly skilled and low cost manpower,along with strong government support in the formof incentives and establishment of SEZs have beenthe major drivers for the rapid growth of Indian gemsand jewellery exports. The industry thus plays a vitalrole in the Indian economy as it is the top 5 foreignexchange earner in the country surpassing eventhe US $ 22 billion earned by the textile and apparelsector.

The current global economic crisis came as rudeinterruption to the exports growth story. Exporterswere doubly hit by falling demand and fluctuatingexchange rates. The Fiscal Year 2008-09 saw Gems& Jewellery exports decline by 1.5% in dollar termsand 13.5% in Rupee terms. However, the exports

have already bounced back in recent months andare expected to resume a near vertical march to double its foreign exchange earnings in the next 5 years.

If we study the recent export data we find that our core strength continues to be cut and polished diamondsbut gold jewellery is also now a sizeable share and indicates that we are diversifying expanding our offeringsto the world.

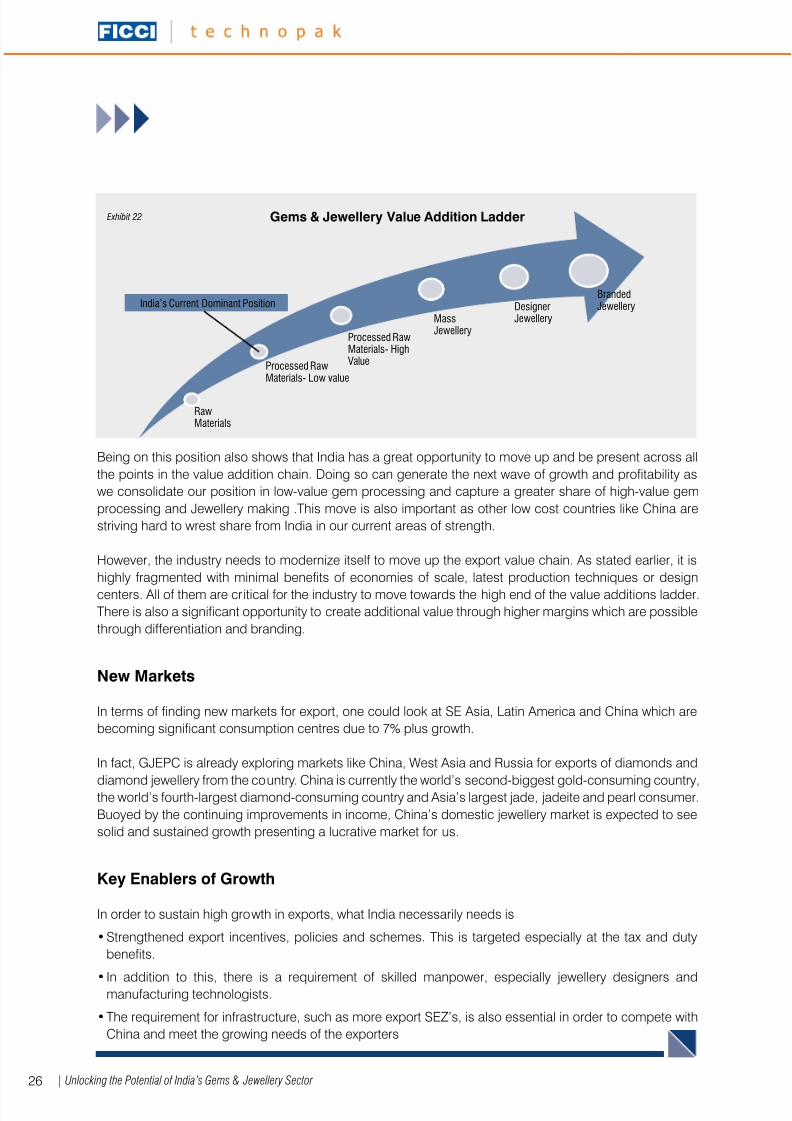

Moving Up the Value Chain

With regards to Exhibit 22 India currently lies on the 2nd level in the value addition ladder of the gems and

jewellery sector. This position has cushioned India a bit during the economic crisis as compared to otherexporters like Italy. This is because the higher value Gems & Jewellery products were hit much harder thanthe mass low value products

Te Export Market

Gems & Jewellery Exports(US $ Billion)

Exhibit 20

Source – GJEPC, Technopak Analysis

2009

25

58

20150

10

20

30

40

5060

Apr-Nov 2009 Exports (%) Exhibit 21

Source – GJEPC Statistics

Cut & Pol Diamond

Gold Jewellery

Rough Diamond60%34%

3% 2%

Others

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 26/3626 | Unlocking the Potential of India’s Gems & Jewellery Sector

Being on this position also shows that India has a great opportunity to move up and be present across allthe points in the value addition chain. Doing so can generate the next wave of growth and profitability aswe consolidate our position in low-value gem processing and capture a greater share of high-value gemprocessing and Jewellery making .This move is also important as other low cost countries like China arestriving hard to wrest share from India in our current areas of strength.

However, the industry needs to modernize itself to move up the export value chain. As stated earlier, it ishighly fragmented with minimal benefits of economies of scale, latest production techniques or designcenters. All of them are critical for the industry to move towards the high end of the value additions ladder.There is also a significant opportunity to create additional value through higher margins which are possiblethrough differentiation and branding.

New Markets

In terms of finding new markets for export, one could look at SE Asia, Latin America and China which arebecoming significant consumption centres due to 7% plus growth.

In fact, GJEPC is already exploring markets like China, West Asia and Russia for exports of diamonds and

diamond jewellery from the country. China is currently the world’s second-biggest gold-consuming country,the world’s fourth-largest diamond-consuming country and Asia’s largest jade, jadeite and pearl consumer.Buoyed by the continuing improvements in income, China’s domestic jewellery market is expected to seesolid and sustained growth presenting a lucrative market for us.

Key Enablers of Growth

In order to sustain high growth in exports, what India necessarily needs is

Strengthened export incentives, policies and schemes. This is targeted especially at the tax and duty•

benefits.

In addition to this, there is a requirement of skilled manpower, especially jewellery designers and•

manufacturing technologists.

The requirement for infrastructure, such as more export SEZ’s, is also essential in order to compete with•

China and meet the growing needs of the exporters

Gems & Jewellery Value Addition Ladder Exhibit 22

RawMaterials

Processed RawMaterials- Low value

Processed RawMaterials- HighValue

MassJewellery

DesignerJewellery

BrandedJewelleryIndia’s Current Dominant Position

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 27/36Unlocking the Potential of India’s Gems & Jewellery Sector |27

05Recommendations

Recommendations for the Industry

Potential Assessment and Strengthening Consumer Understanding

Unlike other consumer goods sectors such as FMCG, Apparel & Consumer Electronics there have been nocomprehensive studies done so far with regards to gaining insights into the gems & jewellery consumer.

The domestic market holds a significant opportunity and its potential needs to be fully explored.The consumers have evolved rapidly and the traditional ways of segmentation & usage have failed to provideany meaningful results to the brands and retailers. There is dire need for the industry to first understand thevarious segments of the consumers so that the transformations shown in Exhibit 5a can take place

Thus we recommend a comprehensive consumer-insight study to be commissioned by the various industrybodies with the objective of facilitating above transformations. The collaboration of all industry bodies isimportant so that no sections of the industry are left out.

Invest in Retailing and Brands

The organised retail and brands can provide impetus to the sector. Appropriate investments can potentiallyput the category on a higher priority in the consumer basket and can generate the higher margins. Anoverall investment of US $ 2 billion is required by the branded jewellery players to achieve 15% share ofthe market.

This is not a huge amount if you consider the investing power of Indian corporate houses and international

players. However the investors often perceive this sector to be secretive, closed and tough. We need toovercome these doubts and fears to promote a more rapid flow of investment.

While investment from outside the industry is welcome and needed there is great opportunity for the high-performing industry players as well. There are scores of leading family-run jewelers with highly profitableenterprises. Currently the surplus is invested back into inventory or in other investment avenues such as realestate and equities. We need to give these rising stars confidence and direction to invest in expansion.

Thus a possible solution here is to create highly active Industry Co-ordination Cells by the industry promotionbodies such as FICCI, GJEPC, GJF, WGC etc. This would help bring together the outside investors andindustry stars to create high-potential, low-risk joint-ventures and partnerships.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 28/3628 | Unlocking the Potential of India’s Gems & Jewellery Sector

Improve Skill Sets & Quality of People

While we have a large pool of skilled manpowerin the industry, the high growth rate that we aimboth in domestic and export markets means thatskilled manpower will be in great demand. In sucha scenario the traditional father-to-son tutelage andon-the-job training provided by organizations maynot be sufficient, especially as we try to modernize

and professionalise the industry.

The Gems & Jewellery industry needs tosystematically and collectively invest in up gradationof the skill sets of its workforce through increased training and manpower development programs. A jointeffort by the Industry to invest in the development of vocational training institutes could be the solution withIndustry captains showing the way forward by leading efforts to underwrite recruitment of graduates andparticipate in syllabus design & development. Some key proposed areas for vocational training are shownin Exhibit 23: -

Enhance Product Design & Manufacturing Quality Standards

A National Institute of Jewellery Design & Development would go a long way in providing the platformfor development of a pipeline of innovative high quality designers that can serve the industry as a whole.The Institute can play a role similar to NIFT – whichultimately proved to be a fertile ground that gavebirth to a number of marquee design apparel brandsin the country and improved product design andmanufacturing quality. Indian Institute of Gems &Jewellery (IIGJ) is a step in the right direction but thescale and reach needs to be even greater to meetthe huge demand. If Industry captains come together

to invest in setting up the institute or expandingexisting ones, efforts can be made to lobby to obtainGovernment support and create national “centres ofexcellence” like NIFT with multiple campuses andcourses.

Besides designing there are other high-end education areas which the institute can offer. The proposedareas are shown in Exhibit 24

Area Rationale

Processing ofGems

Export of Gems will continue to grow in doubledigits

JewelleryManufacturing

This is the next area of growth both for exportsas well as the domestic market

Retail Selling This is a key requirement for OrganisedRetailing to prosper

Quality Testing &Assurance

Quality is a must to improve margins and tomove up the value chain

Exhibit 23 Vocational Training Areas

Area Rationale

JewelleryDesigning

Important for our exports and domestic market to move up the value chain and improvemargins

ManufacturingTechnology

We will need more hi-tech manufacturingexpertise to excel in the jewellery spaceespecially with regards to exports

Merchandising &Retail Management This is a key requirement for the growth andprofitability of retail

Marketing & BrandBuilding

This would be key to transform the domesticmarket especially in the minds of the consumer

Exhibit 24 Specialised Education Areas

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 29/3629Unlocking the Potential of India’s Gems & Jewellery Sector |

Promote Adoption of Industry Wide Standards for Gaining Consumer Trust

Enhancement of product quality standards and incentives for increasing adoption of the standards willgo a long way in enhancement of consumer trust and enable the industry to gain share of wallet of theconsumer, in the long run.Currently various material purity and value certifications are already present in the Indian market such asGold Hallmarking, Diamond Certification, Pt950 Certification for Platinum etc. We now need the industry towidely adopt the certifications as a best practice. We thus need the industry bodies to organize workshopsfor educating and motivating the industry. Next there should also be consumer campaigns to improvethe awareness of consumers so that their trust in jewellery purchase gets strengthened. Once a betterunderstanding and acceptance of the certifications and standards is in place then we can also approachthe government to enact laws and regulations to make certifications and standards mandatory.

Eventually the trust and standardization brought in by the certifications and brands will also help in thespread of e-selling in India which in recent years has been the most exciting development as far as thewestern markets are concerned.

Co-operative Use of Resources

To bring down cost of operation and investments in the sector, industry players should adopt co-operativeuse of technology, marketing and retailing. This is an effective way to modernize and strengthen the highlyfragmented industry.

SEZs and jewellery hubs are a good place where common technology-intensive facilities can be setup andeven small players in industry can get access to them.

The success of marketing initiatives by industry bodies and associations has been highlighted in this reportearlier and proves the efficacy of collective marketing initiatives. This needs to be further escalated in India& abroad for the benefit of Indian Gems & Jewellery.

Even retail space can be hired by co-operatives when foraying into international markets. Thus a single“India-Oriented” space with numerous shop-in-shops could be opened in global jewellery destinationssuch as the Dubai mall.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 30/3630 | Unlocking the Potential of India’s Gems & Jewellery Sector

Recommendations to the Government

Government and Apex bodies could act as facilitators in broadening the outlook of the exporters /playersand help them in familiarizing with the changing scenario both in the domestic and international fronts,where moving up the value chain and adoption of modern practices has become compelling imperatives.

Provide Industry Status to Gems & Jewellery

At ~US $15 bn, the domestic Gems & Jewellery industry deserves the same attention and interest as anumber of other industries such as Textiles & Steel. Like the Indian film industry, the domestic Gems &

Jewellery Retail sector could especially benefit tremendously from Industry status as this would help easethe financing problems substantially. The roadmap for this could be as follows: -

Step 1: Constitute a special cell to look into specific needs of Industry, interacting with all the industry•

stakeholders

Step 2: Assess the exact benefits (quantitative and qualitative) that can accrue out of industry status and•

also identify the requirements from the industry as they prepare themselves to become an industry (e.g.transparency). Compile this in a report

Step 3: Get the industry buy-in on the report and jointly work out the details of policy, incentives, financing•

and role of Gems & Jewellery Ministry

Step 4: Extend industry status and constitute a Gems & Jewellery ministry•

Create a Technology Upgradation Fund (TUF)

This would help in facilitating the modernization of the manufacturing and design facilities. These fundshave been successfully created and implemented in other labor intensive industries like Textiles. The broadstructure of the TUF could be as follows: -

Interest subsidy: A reimbursement on the interest charged by the leading agency on a project of•

technology upgradation. This should be not less than 5 percentage points

Capital Subsidy: A re-imbursement of the purchase value for specified processing and manufacturing•

machinery. The specified machinery would represent more advanced technology. A minimum subsidy of10% should be offered

Additional interest and capital subsidies could be granted based on beneficiary size and sub-sector•

within the industry to give differentiated focus wherever required.

Creation of Design Centres /Studios, Holding Fairs

The importance of design has been highlighted by us in this report. This can help significantly in movingthe industry from commoditized selling to design based value added selling. These centres/studios canbe setup by the Government in SEZs as well as outside and should have the latest CAD technologies andother design and visualization equipment.

8/12/2019 FICCI Gems & Jewellery

http://slidepdf.com/reader/full/ficci-gems-jewellery 31/3631Unlocking the Potential of India’s Gems & Jewellery Sector |

India International Jewellery Show (IIJS) is awell known event to showcase Indian Jewellery.Government should actively promote the designingpart in such shows and perhaps also organizemore shows where designing can be given greaterimportance. Designing promotion could happenprimarily through organizing designing competitionswith substantive prizes & awards and subsidizingdesign oriented participation.

Asset (Gold) Based Leverage

Traditionally Gems & Jewellery have served a dual purpose of a fashion accessory as well as an investmentvehicle. However the investment appeal of Gems & Jewellery has been steadily dwindling in the wake ofother assets such as equities, bonds, real estate etc, where there is no loss in selling price. When Jewelleryis sold, the individual only realizes the material value and completely looses the making charge or designvalue addition.

Banks as a practice do not mortgage jewellery fromindividuals as collateral for lending although somecompanies in the private sector such as MuthootGroup do so. If banks also start lending by usingjewellery as a collateral after keeping a safe margin onthe price of the material, then precious metal jewelleryand precious stone jewellery will become moreattractive for their investment value. Two importantthings could help action this recommendations: -

Perhaps RBI can think and act on this suggestion and create policy and directives to facilitate this type of•

retail lending. The valuation norms should be especially spelled out for metals and gems.

There needs to be widespread adoption of certification because lending institutions will only accept•

standard and certified quality material and gems.

Regulatory Laws & Taxation

There are some tax provisions in the new Direct Taxes Code which are detrimental to the industry. The taxesrelate to the following areas: -