Page 1

University of Massachusetts BostonScholarWorks at UMass BostonCollege of Management Working Papers andReports College of Management

2-11-2010

Film and Television Production in Massachusetts:Industry Overview and AnalysisPacey C. FosterUniversity of Massachusetts Boston, [email protected]

David G. TerklaUniversity of Massachusetts Boston, [email protected]

Robert LaubacherMassachusetts Institute of Technology

Follow this and additional works at: http://scholarworks.umb.edu/management_wpPart of the Business Commons

This Research Report is brought to you for free and open access by the College of Management at ScholarWorks at UMass Boston. It has been acceptedfor inclusion in College of Management Working Papers and Reports by an authorized administrator of ScholarWorks at UMass Boston. For moreinformation, please contact [email protected] .

Recommended CitationFoster, Pacey C.; Terkla, David G.; and Laubacher, Robert, "Film and Television Production in Massachusetts: Industry Overview andAnalysis" (2010). College of Management Working Papers and Reports. Paper 7.http://scholarworks.umb.edu/management_wp/7

Page 2

Film and Television Production in Massachusetts: Industry Overview and Analysis

February 11, 2010

Page 3

FILMANDTELEVISIONPRODUCTIONINMASSACHUSETTS:

ANINDUSTRYOVERVIEWANDANALYSIS

February11,2010

ProfessorPaceyC.Foster,ManagementandMarketing,UniversityofMassachusettsBoston

ProfessorDavidTerkla,Economics,UniversityofMassachusettsBoston

WiththeassistanceofRobertLaubacher,MITSloanSchoolofManagement

Acknowledgements

ThisresearchwasmadepossiblewithagrantfromthePresident’sCreativeEconomyInitiativesFundattheUniversityofMassachusettsBoston.RobertLaubacherofMITcontributedsignificantlytothesectionsonunions,historyofdocumentaryproduction,postproduction,highereducation,services,studioprojects,residuals,healthcareandbenchmarking.HisworkwassupportedbytheAdamsArtsProgramoftheMassachusettsCulturalCouncil.WearealsogratefulfortheinputprovidedbyTheMassachusettsProductionCoalition(MPC)andTheMassachusettsFilmOffice(MFO)aswellaslocalunions(IATSE,SAG,IBT)andcompanieslikeBrickyardVFX,NationalBostonStudiosandPowderhouseProductions.WealsothankTheCenterforIndependentDocumentary,theLEFFoundationandofficialsattheMassachusettsDepartmentofRevenueandotherstateagenciesfortheirhelp.WearegratefultothemanyotherindustrymemberswhoagreedtotalkwithusforthestudyandespeciallytoBenOlendzkiforhisresearchassistancethroughouttheprojectandtoErinSiskforherworkonthelocaldocumentaryandindependentfilmmakingsector.Inaddition,wewanttothankRaijaVaisanenwiththeUniversityofMassachusettsDonahueInstituteforherassistanceinconductingtheIMPLANanalysisandtoDanKochwhohelpedusmapfilmindustrynon‐wagespendingpatterns.

Page 4

2

ExecutiveSummary

Thisreportdescribesthestructureandrecentgrowthofthefilmandtelevisionindustryin

Massachusetts.Webeginwithadiscussionofnationaltrendsinthisindustryandfindthat

Massachusettsisoneofthefastestgrowinglocationsforfilmandtelevisionproductioninthe

UnitedStates.Wethendiscussrecentemploymenttrendsinthissectorandfindthattherehas

beensignificantrecentgrowthinthetotalnumberoflocalfilmandtelevisionproductionjobs‐‐

particularlyamongtheunionizedcrewandactorsthatstafflocalproductions.Examinationof

federaldatarevealsthatbetween2005and2008therehasbeena117%anda126%growthin

employmentinthemotionpictureandvideoproductionandpostproductionindustries

respectively.Usingnetworkandgeographicmodelingtools,wealsoidentifynovelpatternsinthe

non‐wagespendingoflocalfilmandtelevisionproductions.Wecontinuewithadiscussionof

growthtrendsacrossseveralsubsectorsofthelocalfilmandtelevisionsectorandfindthat

severalaregrowingrapidly.

Whileourreportrecognizesanddiscussestherevenueandfiscalimplicationsofthefilmindustry

taxcredit,itisnotthefocusofouranalysis.Indeed,theevaluationoftherevenueimplicationsof

theMassachusettsFilmTaxCredit(FTC)1hasbeendonecarefullybytherecentMassachusetts

DepartmentofRevenuestudy(2009).Ourreportisfocusedmorebroadlyonunderstandingthe

breadth,performance,anddynamicsofthefilmandtelevisionindustryinMassachusetts.

Updatingthe“LensontheBayState”study(Laubacher,2006),weprovideanoverviewof

aggregateemploymenttrendsinthisindustryanditssub‐sectors.Weusefederalemployment

datatoexaminetheeconomicimpactofthisindustryontheCommonwealth.Wealsorelyon

interviewswithindustryparticipants,employmentandspendingdataprovidedbylocalunions,

archivaldatacollection,andbothnetworkanalysisandgeographicvisualizationstodescribe

productionandemploymenttrendsinspecificsub‐sectorsofthisindustry.

1 While we use the term Film Tax Credit (and its abbreviation FTC) in the report below, the program

actually applies to motion pictures as well as certain kinds of television programs. A description of the program is provided in Appendix 2.

Page 5

3

Weidentifyseveralimportanttrendsintherecentgrowthofthefilmandtelevisionindustryin

Massachusetts:

1. Massachusettsisamongthefastestgrowinglocationsforfilmandtelevisionproductionin

theUnitedStates;andnotablysomestateswithmoregeneroustaxcreditprogramshave

notexperiencedasmuchrecentgrowthasMassachusetts.

2. EmploymentinfilmandtelevisionproductionhasincreasedinMassachusettsduringa

periodwhentotalstateemploymenthasbeenonthedecline.Thereisalsoevidencethat

someofthisjobgrowthhashelpedtooffsetjoblossesinparticularlyhardhittradeslike

constructionandtransportation,asworkersfromthesesectorshavefoundworkinfilm

andtelevisionproduction.

3. Localnon‐fictiontelevisionandpost‐productioncompanieshaveexperiencedparticularly

dramaticgrowthinrecentyearsandseemtobegeneratingnewcareerpathsforlocal

collegegraduates.Inaddition,becauseorganizationsinthissectortendtospendalarge

proportionoftheirproductionexpenseslocally,theyrepresentaparticularlyinteresting

sectorforlocaleconomicdevelopment.Moreover,asthehometoWGBH,Massachusetts

hasalonghistoryofleadershipinnon‐fictiontelevisionanddocumentaryproduction.This

historycombinedwithitsnumerouscollegeprogramsgeneratingfilmandtelevision

students,researchuniversities,andhightechnologycompaniesprovidesMassachusetts

withauniquestrategicadvantageintheproductionofnon‐fictioncableandpublic

televisionshowsaswellasgrowingopportunitiesinpost‐production.

4. Thegrowthinlocalfilmandtelevisionproductionhasstimulatedgrowthamongacluster

oflocalfilmservicecompaniesthatsupporttheseproductions.Ithasalsoluredsome

largernationalfilmservicecompaniestotheCommonwealth.Thereremainsroomfor

growthinthisareaassomespecializedfilmandtelevisionproductionequipmentisstillnot

availableinMassachusettsandthereforeneedstobesourcedoutofstate.Totheextent

thatthelocalfilmservicesectorcontinuestogrowinresponsetoincreasingproduction

activity,anincreasingproportionofnon‐wagespendingmayremaininthe

Commonwealth.

Page 6

4

TableofContents

ExecutiveSummary..................................................................................................................... 2IntroductionandGoals ............................................................................................................... 5

DescribingMassachusettsFilmandTelevisionProduction .......................................................... 7 MassachusettsInTheNationalandRegionalLandscape 7

LaborMarketStructure 10 AggregateStateEmploymentTrends 11

TheContributionofFilmandTelevisionSpendingtotheMassachusettsEconomy ........................................................................................................... 16

EmploymentTrendsinLocalFilmProduction 17 Non‐wageSpendingPatterns .................................................................................................... 22

DevelopmentsinSpecificSubsectors ........................................................................................ 25

Conclusion ................................................................................................................................ 41Appendix1:Methodsandapproachesinstudiesofregionalfilmand

televisionindustriesandincentiveprograms ............................................................................ 42

Regionalfilmandtelevisionproductionincentiveprograms 44

Variationsinmodels:adiscussionandevaluation 47 Secondarymarketfortaxcredits 50 Marketingandtourismbenefits 51

Incometaxfromresidualsandthegrowthofalocalcreativetalentbase 53 Benefitsfromchangestothemassachusettscorporatetaxlaws 55 Increasedhealthcoverageandotherbenefits 56

Benchmarkinglongtermgrowthtrends 58Appendix2:AbriefsummaryoftheMassachusettsfilmindustrytaxcredit.............................. 59 References 61

Page 7

5

IntroductionandGoals

Asdocumentedinthe2006“LensontheBayState”report(Laubacher,2006),theMassachusetts

filmandtelevisionindustrywasonthedeclineinthe1990swithtotalemploymentfallingathird

between1990and2006.ThelocalindustryreachedanadirwiththeclosingoftheMassachusetts

FilmOfficein2002.Torevitalizethisoncethrivinglocalcreativeindustry,in2005theState

Legislaturepassedataxincentiveplanthatprovidedabankabletaxcreditforqualifyingmotion

pictureandtelevisionproductionsproducedinMassachusetts.Asupdatedin2007,the

MassachusettsFilmTaxCredit(FTC)providesarefundable/transferrabletaxcreditfor25%of

qualifyingwageandnon‐wageproductionexpensesandasalestaxexemptionforqualifyingin‐

statespending.2

TheFTChasclearlyincreasedtheamountoftimeandpercentageoftheirbudgetsthatfilmand

televisionproductionsarespendingintheBayState.Industryrepresentativesreportthatthis

increasedactivityhashadapositiveimpactonlocaljobs,non‐wagespendingandthegrowthof

localfilmservicecompanies.Whilemembersoftheindustryhaveclearlyexperiencedthepositive

impactofthisprogramandsomestudieshavefoundthattheyhavepositiveshorttermrevenue

implications(ErnstandYoung,2009a,2009b),othersstudiesraisequestionsbothaboutthevalue

oftheseprogramsandmethodsusedtomeasuretheirimpacts(Luther,2010;Gregg,2008;Saas,

2006;Tisei,2007).Thislackofagreementisdriveninpartbythechallengesofaccurately

measuringeconomicactivityinaproject‐basedindustrylikefilmandtelevisionproductionandin

partbyvariationsinthemodels,data,andassumptionsusedinstudiesofincentiveprograms(see

Appendix1forathoroughdiscussionoftheseissues).

TheprimarypurposeoftheFTCistostimulatefilmandtelevisionproductioninMassachusetts.

However,tobuildapermanentandstablefilmandtelevisionindustryrequiresthatpolicymakers

considerbothannualreturnsoninvestmentaswellasaggregateindustrytrends,localworkforce

developmentandcareerpaths,infrastructuredevelopmentandthegrowthoflocalfilmservice

2 For a detailed description of the provisions of the tax credit program see Appendix 2

Page 8

6

industries,aswellasvariationsinproductionpracticesandlinkagesamongsub‐sectorswithinthis

industryandemploymenttrendsineach.

BecauseMassachusettsisoneofmanystatesthatofferFTCprograms,itwouldalsobehelpfulto

evaluatehowMassachusettsisdoingrelativetootherstatesthatarecompetingforashareofthe

totalnationalfilmandtelevisionproductionbudgeteachyear.Finally,itisimportanttoidentify

whethertheCommonwealthhasasetofuniqueresourcesthatcanputsubstancebehindthe

aspirationofbecomingapermanentcenteroffilmandtelevisionproductionintheUnitedStates.

Industryrepresentativesarguethatbecauseofitsuniquecombinationofdesirablelocations,large

numbersofuniversitiesandstudents,atalentedcastandcrew,taxincentives,andstatusasa

worldclasscitythatisdesirabletotalent,Massachusettshasthepotentialtobecomethethird

largestcenteroffilmandtelevisionproductionintheUnitedStates(behindCaliforniaandNew

York).Indeed,ifthissectorgrowstothepointthatMassachusettsbecomesanewhuboffilm

production(likeVancouver,BritishColumbiadidinthe1990s),therewillbefuturebenefitsfrom

workforceretentionandattraction,infrastructuredevelopment,linkagesbetweenuniversities

andindustry,newcareerladders,etc.Conversely,iffilmproductionleavesMAassoonasanother

stateoffersamoreattractiveincentive,evenarevenuepositiveincentiveprogramcouldfailin

establishinganewindustryinMA.

Therearethreeprimarygoalsofthisstudy:

1. Todescribethestructureandrecentgrowthpatternsofthefilmandtelevisionindustryin

Massachusetts,identifyitskeysub‐sectors,andbegintounderstandthekeyeconomic

leversthatpromotesuccessinthissectorofthecreativeeconomy;

2. Toestimatetheaggregateimpactofthefilmandtelevisionproductionsectoronthestate

economythroughdirectandinducedspending.

3. Tosupplementanalysesusingstandardinput/outputmodelsbycollectinginterviewand

networkdataonemploymenttrendsandnon‐wagespendingpatternstobetter

understandthelinkagesamongthesesubsectorsandtheirconnectionstoothersectorsof

thestateeconomy.

Page 9

7

Toaddressthesegoals,wecombineeconomicmodelingwithinterviews,archivaldatacollection,

networkanalysisandgeographicmodelingtoprovideanuancedpictureofthemotionpictureand

televisionindustryinMassachusetts.Byfocusingonproductionpracticesandvariationsacross

sub‐sectorsofthislocalcreativeindustry,weidentifyfactorsthatmayimpactthelong‐term

healthofthefilmindustryinMassachusetts.

ThisreportbeginswithanoverviewofthecurrentstateoftheMassachusettsfilmindustryusing

datafromtheBureauofLaborStatisticsandtheMotionPictureAssociationofAmerica(2009)to

discussaggregatelocalandnationalfilmandtelevisionemploymenttrends.Followingthis

overviewoflocalandnationaltrends,weanalyzethelocalfilmandtelevisionproductionsectorby

classifyingorganizationsandemployeesprimarilybythekindsofproductstheyproduce(e.g.,

featurelengthfilms,advertisements,scriptedandnon‐fictiontelevisionprograms,independent

filmsanddocumentaries,etc.)andidentifyingconnectionsamongthesesectorsviashared

workforce,materialrequirementsandproductionpractices.

Wealsoidentifytheorganizationsthatprovidesupportservices,equipmentandmaterialtofilm,

television,andvideoproductionsanddiscussrecentactivityinthesesubsectors.Weconclude

withasummaryofourfindingsandadiscussionofourfuturework.Anextensivediscussionof

issuesinvolvedinevaluatingtheimpactofFTCprogramsisprovidedinAppendix1.

DescribingMassachusettsFilmandTelevisionProduction

ThissectionbeginsbycomparingthegrowthofthefilmandtelevisionindustryinMassachusetts

togrowthratesinotherstates.Afterdescribingtheaggregateemploymenttrendsinthe

Commonwealth,wediscusstrendsinnon‐wagespendingandidentifyacoreoffilmservicefirms

andlocation‐specificspendingpatternsassociatedwithlocalmotionpictureproductions.We

concludewithadiscussionofseveralimportantsub‐sectorsinthisindustryandinterconnections

amongthem.

MassachusettsintheNationalandRegionalLandscape:Overthelastdecade,severalimportant

nationaltrendshaveemergedthataffectthegrowthofthefilmandtelevisionindustryin

Page 10

8

Massachusetts.WhilethebulkoffilmandtelevisionproductionstilltakesplaceinLosAngelesand

NewYork,otherstatesareincreasinglycompetingwiththesetraditionalcentersthroughtax

creditandotherincentiveprograms.Infact,on‐locationshootingdaysinLosAngelesdropped

19%in2009;thesteepestdeclinesincetrackingbeganin1993(Verrier,2010).Toanalyzerecent

nationaltrends,weuseddatafromtheMotionPictureProductionAssociationofAmerica(2009)

andtheQuarterlyCensusofEmploymentandWages(QCEW)datafromtheBureauofLabor

Statistics.

AccordingtodatafromboththeMotionPictureAssociationofAmerica(2009)andtheQCEW,

Massachusettscapturedalittleover1%ofthetotalnationalspendingonmotionpicturesand

televisionproductionsin2007.WhileMassachusettsdoesnotcurrentlycapturealarge

percentageofthenationalfilmandtelevisionproductionspending,itseemstobegrowingmore

rapidlythanotherstates(someofwhichhavemoregeneroustaxprograms)andcapturingwork

thatmightotherwisebetakingplaceelsewhere.

Figure1usesdatafromtheMotionPictureProductionAssociation(2009)tochartthepercentage

changeinthenumberoffilmandtelevisionproductionsthattookplaceinthetop25mostactive

statesintheUnitedStatesbetween2007and2008.Duringthistime,workdeclinedintraditional

centerslikeCaliforniaandNewYorkandgrewrapidlyinstateslikeGeorgia,Indiana,

Massachusetts,Michigan,MinnesotaandWisconsin.Accordingtothesedata,Massachusettshad

thefifthlargestgrowthrateamongthetop25mostactivestatesinthecountry.Itisalsoclear

thatseveralstateswithactivetaxincentiveandinfrastructuredevelopmentprograms(andmore

generousincentivesthanMA)arenotamongthetop25mostactivestatesaccordingtotheMPAA

(2009).Careiswarrantedininterpretingthesedatagiventhatthemagnitudeofchangesinstates

likeWisconsinweredriveninlargepartbytheverysmallnumberofproductionsthatithadin

2007.

Page 11

9

Figure1.Percentagechangeinfilmandtelevisionproductions2007‐2008

Source:MotionPictureAssociationofAmerica

DataonnationalemploymentprovidesadditionalsupportforthenotionthatMassachusettsis

amongthemostactiveandrapidlygrowingstatesinthenationforfilmandtelevisionproduction.

UsingdatafromtheQuarterlyCensusofEmploymentandWagespublishedbytheBureauof

LaborStatistics,weexaminedrecentemploymenttrendsinthe15stateswiththemostfilmand

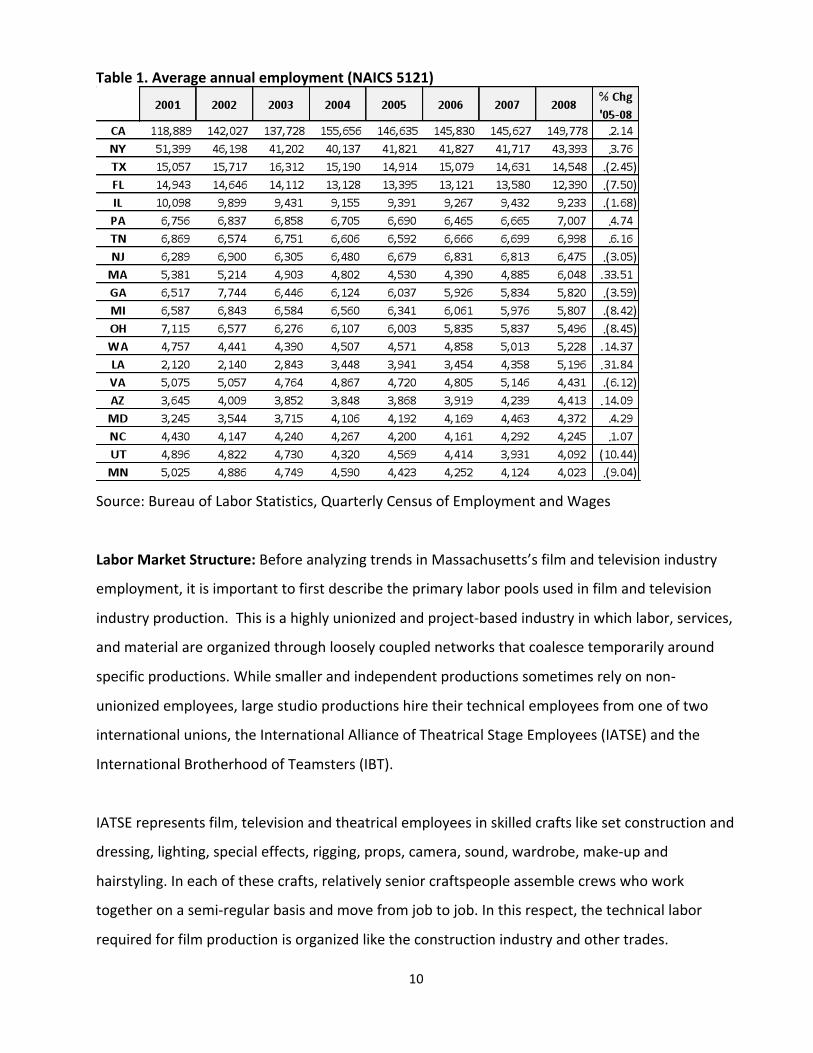

televisionworkersin2008.Table1presentstheaverageemploymentinthesestatesbetween

2001and2008.Notably,duringtheperiodencompassingtheenactmentoftheFTCin

Massachusetts(2005‐2008),totalemploymentintheNAICScode5121(MotionPictureandVideo

Industries)inMassachusettsincreased33%.Thisrepresentsthelargesttotalpercentagegrowth

between2005and2008ofanystateamongthe15withthemostmotionpictureandvideo

employeesin2008.Thisisnotablegiventhatstateswithmuchmoregenerouscreditslike

Michigan(whichoffersbetween30‐42%onqualifiedexpenses)actuallyexperiencedadeclinein

filmandtelevisionemploymentduringthisperiod.

Theseaggregatenationalemploymentandproductiondataconfirmthewidespreadreportsfrom

industryparticipants(aswellasthefrequentcoverageofHollywoodstarsightingsinlocalpapers)

thatMassachusettsisfastbecomingafavoredlocationforHollywoodproductions.Inthe

following,welookbeneaththesenationaltrendstodiscusslocalemploymentinthe

Massachusettsfilmandtelevisionindustry.

Page 12

10

Table1.Averageannualemployment(NAICS5121)

Source:BureauofLaborStatistics,QuarterlyCensusofEmploymentandWages

LaborMarketStructure:BeforeanalyzingtrendsinMassachusetts’sfilmandtelevisionindustry

employment,itisimportanttofirstdescribetheprimarylaborpoolsusedinfilmandtelevision

industryproduction.Thisisahighlyunionizedandproject‐basedindustryinwhichlabor,services,

andmaterialareorganizedthroughlooselycouplednetworksthatcoalescetemporarilyaround

specificproductions.Whilesmallerandindependentproductionssometimesrelyonnon‐

unionizedemployees,largestudioproductionshiretheirtechnicalemployeesfromoneoftwo

internationalunions,theInternationalAllianceofTheatricalStageEmployees(IATSE)andthe

InternationalBrotherhoodofTeamsters(IBT).

IATSErepresentsfilm,televisionandtheatricalemployeesinskilledcraftslikesetconstructionand

dressing,lighting,specialeffects,rigging,props,camera,sound,wardrobe,make‐upand

hairstyling.Ineachofthesecrafts,relativelyseniorcraftspeopleassemblecrewswhowork

togetheronasemi‐regularbasisandmovefromjobtojob.Inthisrespect,thetechnicallabor

requiredforfilmproductionisorganizedliketheconstructionindustryandothertrades.

Page 13

11

Moreover,becausethetechnicalskillsrequiredinsomeaspectsoffilmproduction(e.g.,set

constructionandlighting)aresimilartothoseintradeslikecarpentryandelectricalwork(and

becausebothsectorsarehighlyunionized),wefinditinstructivetocomparestateemployment

trendsacrossthesesectors.TheTeamstersrepresentthetransportationemployeesthatdrivethe

trucksandotherequipmentusedinfilmproductions.Becauseitalsorepresentstransportation

employeesinlargerlocalindustries,filmtransportationworkersrepresentarelativelysmall

segmentoftotalTeamstermembershipintheCommonwealth.

Inadditiontotheskilledemployeesdescribedabove,filmandtelevisionproductionsalsoemploy

creativepersonnellikeactors,writers,andproducerswhoareorganizedthroughtheirownunions

andtradegroups(e.g.,TheScreenActorsGuild,AmericanFederationofTelevisionandRadio

Artists,theWritersGuildofAmericaandtheDirectorsGuildofAmerica).Thesetwolaborpools

aretypicallyreferredtoas“belowtheline”(e.g.,IATSE,IBT)and“abovetheline”talent(e.g.,

AFTRA,SAG,etc.),respectively,andtogetherrepresentmorethanhalfthetotalcostsofatypical

majormotionpicture.

AggregateStateEmploymentTrends:Therearefour,five‐digitNAICScodesthatmakeupthe

5121MotionPictureandVideoIndustriescategoryanalyzedabove.Ofthese,twocapture

productionactivities(MotionPictureandVideoProduction51211andPostProductionServices

andOtherMotionPictureandVideoindustries51219).Thesearethetwoprimarycodeswefocus

oninthefollowing.Theremainingtwocodes(MotionPictureandVideoExhibition51213and

MotionPictureandVideoDistribution51212)donotrelyonthesamekindsofemployeesand

organizationsthatareengagedinproductionactivities(andparticularlyinthecaseofexhibition

aretreatedasseparateindustries).Asaresult,wedonotaddressthesesectorsinthisstudy,

althoughwerecognizethatoverthelongterm,thepresenceofanactiveproductionsectorinthe

Commonwealthcouldencouragegrowthofalocaldistributionsector.

InadditiontothetwoprimaryfilmindustryNAICScodes(51211and51219),wealsoexplore

employmenttrendsintwosectorsthatlikelycontainsignificantnumbersoffilmandtelevision

industryworkers.Becauseofthelargenumberoffreelanceemployeesinthissector,filmand

televisionproductionstypicallyusepayrollservicestomanagewithholdingsanddistributewages

Page 14

12

forcastandcrew.Before2008,theseworkerswerenotclassifiedbytheBureauofLaborStatistics

asbeingpartofMotionPictureandVideoProduction(NAICS51211).Beforethistime,some

proportionofemploymentinlocalfilmandtelevisionproductionlikelyappearedinthecategory

for541214(PayrollServices)andtheprocessofrecodingemploymentfromthiscategoryto51211

isstillongoing.Similarly,itisunclearwhatproportionofemploymentinrelatedNAICScategories

(e.g.,71151IndependentArtists,Writers&Performers)actuallyoccursinfilmandtelevision

production.Therefore,whilewereportandanalyzeBureauofLaborStatisticsdatainthe

following,werecognizethattheylikelyunderstateaggregateemploymentinthesector.

Between2008and2009,Massachusettsexperiencedsignificantjoblossescausedbycontraction

inthelocalandnationaleconomies.Overallemploymentdropped3.2%inMassachusetts

betweenMarch2008and2009continuingadownwardtrendthatbeganin2007.Although

Massachusettsexperiencedsignificantjoblossesin2008(withthestateunemploymentrate

increasingfrom4.9%inMay2008toover8%inMay2009),jobsinthefilmandtelevision

productionsectorhavebeengrowingrapidlyduringthesameperiod.

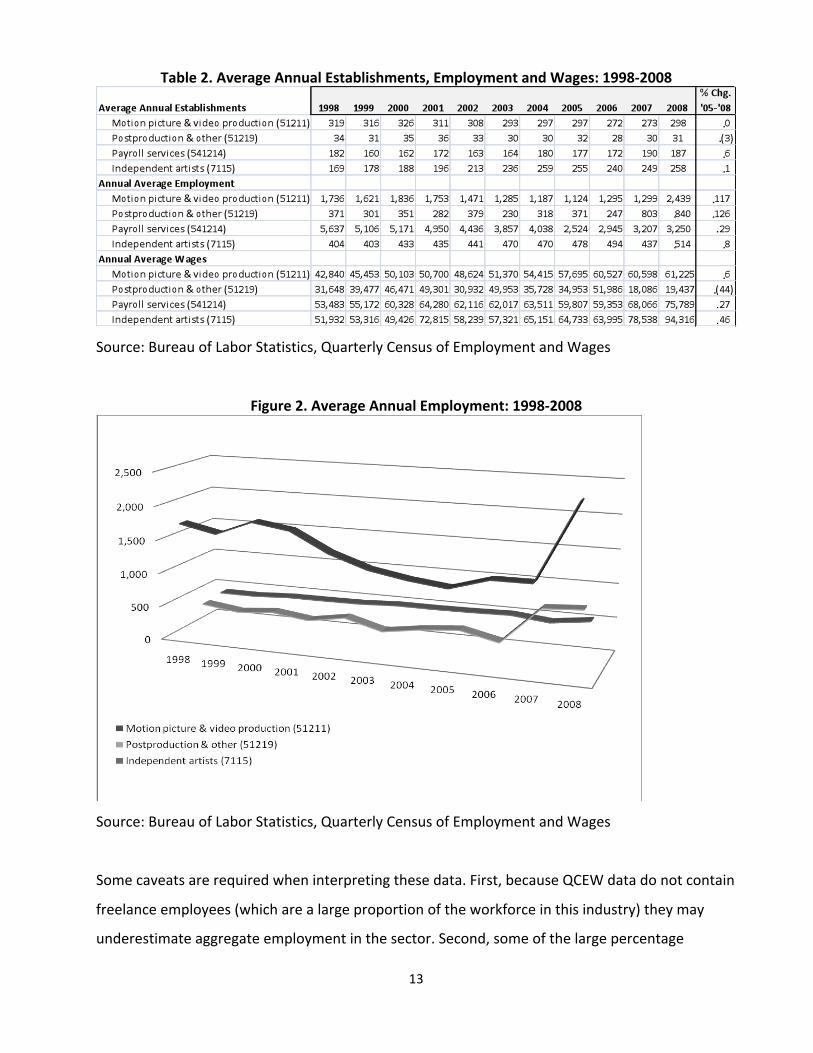

Between2005andthethirdquarterof2008,thenumberofmotionpictureproductionemployees

(NAICS51212),postproductionandotheremployees(NAICS51219)andindependentartists

(NAICS7115)intheCommonwealthgrew117%,126%and8%respectively(Table2andFigure2

below).ThesubstantialgrowthinNAICS51219(postproductionandother)isnotableparticularly

becauseestablishedlocalcompaniesaredoingsomeofthiswork.Inaddition,thePayrollServices

sectorgrewsubstantiallyinto2007,whichwasbeforerelevantfirmswerereclassifiedintoNAICS

51212,sosomeofthisgrowthmayreflectgrowthinthefilmindustry.Moreover,asnotedabove,

reclassificationisstillongoing,whichmeansthatsomeofthe2008figuresforNAICS541214still

representfilmindustryactivity.

Althoughthenumberofestablishmentshasnotgrownasrapidlyasemployment,thismaybe

causedbythewidespreaduseoffreelancelaborinthissectorandthefactthatexistinglocalfilm

servicecompanieshavegrowntomeetnewdemand.Itisalsoworthnotingthatmotionpicture

productionandindependentartistsareveryhighwagesectorsandthatpost‐productionhas

vacillatedbetweenhighandrelativelylowaveragewages.

Page 15

13

Table2.AverageAnnualEstablishments,EmploymentandWages:1998‐2008

Source:BureauofLaborStatistics,QuarterlyCensusofEmploymentandWages

Figure2.AverageAnnualEmployment:1998‐2008

Source:BureauofLaborStatistics,QuarterlyCensusofEmploymentandWages

Somecaveatsarerequiredwheninterpretingthesedata.First,becauseQCEWdatadonotcontain

freelanceemployees(whicharealargeproportionoftheworkforceinthisindustry)theymay

underestimateaggregateemploymentinthesector.Second,someofthelargepercentage

Page 16

14

increasesarepartiallyareflectionofthesmallbaseofemployeesinthesesectorsandthusdonot

representlargeabsoluteincreases.

Third,bothmotionpicture&videoproductionandpostproduction&otherservicesexperience

largefluctuationsinemploymentduringtheyear,reflectingthedifferingintensitiesof

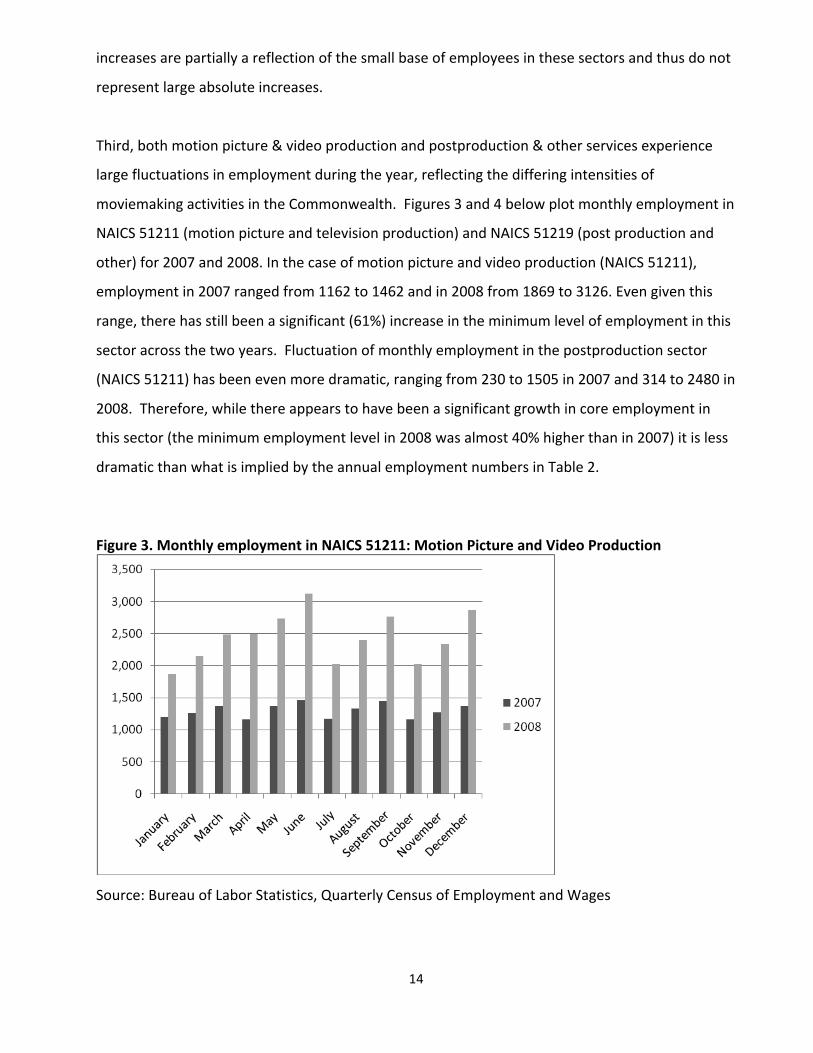

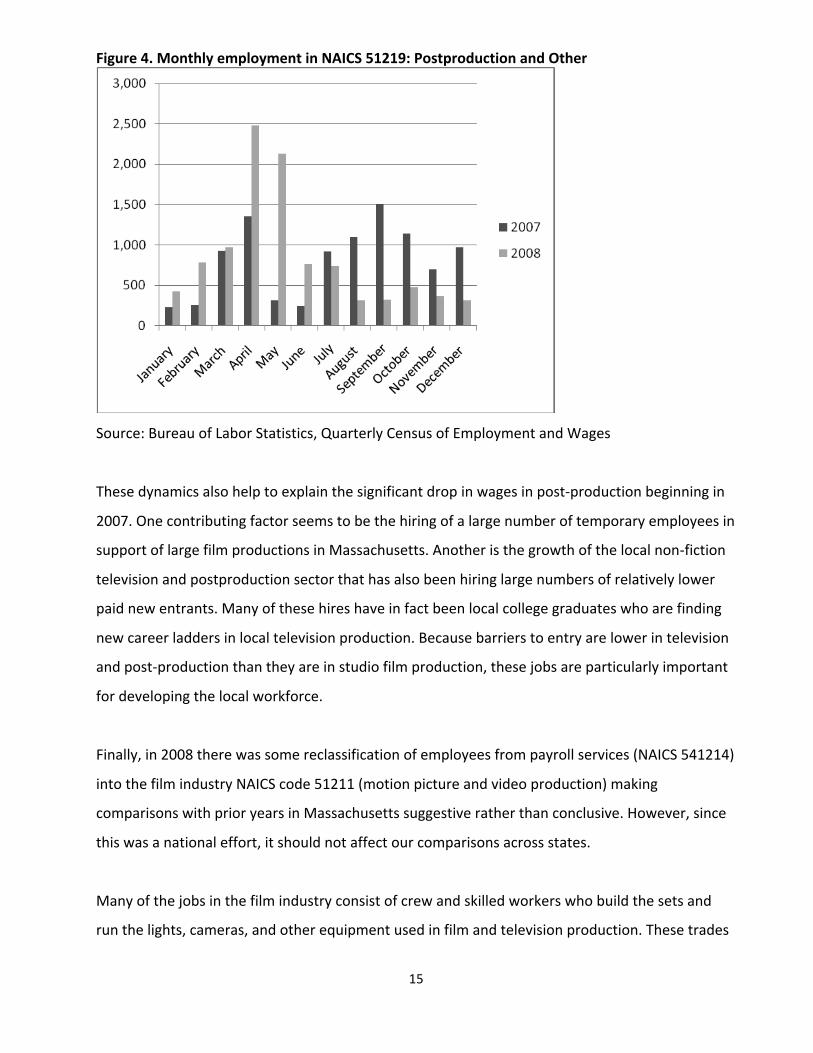

moviemakingactivitiesintheCommonwealth.Figures3and4belowplotmonthlyemploymentin

NAICS51211(motionpictureandtelevisionproduction)andNAICS51219(postproductionand

other)for2007and2008.Inthecaseofmotionpictureandvideoproduction(NAICS51211),

employmentin2007rangedfrom1162to1462andin2008from1869to3126.Evengiventhis

range,therehasstillbeenasignificant(61%)increaseintheminimumlevelofemploymentinthis

sectoracrossthetwoyears.Fluctuationofmonthlyemploymentinthepostproductionsector

(NAICS51211)hasbeenevenmoredramatic,rangingfrom230to1505in2007and314to2480in

2008.Therefore,whilethereappearstohavebeenasignificantgrowthincoreemploymentin

thissector(theminimumemploymentlevelin2008wasalmost40%higherthanin2007)itisless

dramaticthanwhatisimpliedbytheannualemploymentnumbersinTable2.

Figure3.MonthlyemploymentinNAICS51211:MotionPictureandVideoProduction

Source:BureauofLaborStatistics,QuarterlyCensusofEmploymentandWages

Page 17

15

Figure4.MonthlyemploymentinNAICS51219:PostproductionandOther

Source:BureauofLaborStatistics,QuarterlyCensusofEmploymentandWages

Thesedynamicsalsohelptoexplainthesignificantdropinwagesinpost‐productionbeginningin

2007.Onecontributingfactorseemstobethehiringofalargenumberoftemporaryemployeesin

supportoflargefilmproductionsinMassachusetts.Anotheristhegrowthofthelocalnon‐fiction

televisionandpostproductionsectorthathasalsobeenhiringlargenumbersofrelativelylower

paidnewentrants.Manyofthesehireshaveinfactbeenlocalcollegegraduateswhoarefinding

newcareerladdersinlocaltelevisionproduction.Becausebarrierstoentryarelowerintelevision

andpost‐productionthantheyareinstudiofilmproduction,thesejobsareparticularlyimportant

fordevelopingthelocalworkforce.

Finally,in2008therewassomereclassificationofemployeesfrompayrollservices(NAICS541214)

intothefilmindustryNAICScode51211(motionpictureandvideoproduction)making

comparisonswithprioryearsinMassachusettssuggestiveratherthanconclusive.However,since

thiswasanationaleffort,itshouldnotaffectourcomparisonsacrossstates.

Manyofthejobsinthefilmindustryconsistofcrewandskilledworkerswhobuildthesetsand

runthelights,cameras,andotherequipmentusedinfilmandtelevisionproduction.Thesetrades

Page 18

16

usemanyofthesameskillsthatarerequiredinconstructionandothersimilartradesthat

experiencedthefastestrateofjoblossesinMassachusettsin2008.InMassachusetts,

employmentintheconstructionindustrydropped12.8%betweenMarch2008andMarch2009

sheddingatotalof17,400jobs(BureauofLaborStatistics,2009).Asdiscussedbelow,thereis

evidencethattherapidincreaseinfilmindustryemploymentduringthisperiodhashelpedabsorb

someemployeesfromconstructionandothertrades.

TheContributionofFilmandTelevisionSpendingtothe

MassachusettsEconomy Asnotedinthediscussionabove,formalmodelingofthefilmindustry’scontributiontothe

Massachusettseconomyisdifficultbecauseoftheindustry’sstructure,fluidity,andthedifficulty

inobtaininganaccuratesnapshotofthecurrentstateoftheindustry.However,itisstillworth

knowingwhatstandardeconomicmodelscalculateastheeconomicimpactoftheindustryonthe

Commonwealth,giventhebestsourcesofemploymentdatathatareavailable.Itisimportantto

distinguishthisanalysisfromtheanalysisconductedbytheMassachusettsDepartmentof

Revenue(2009)inrelationtotheFTC,whichisdiscussedinAppendix1.Inthisanalysis,weare

concernedwiththecontributionoftheentirefilmindustryaswehavedescribeditonthe

Massachusettseconomy,notjusttheimpactoftheportionoftheindustrythatcanbeidentified

ashavingbeenattractedtoMassachusettsbytheFTC,whichisthefocusoftheMassachusetts

DepartmentofRevenue(2009)study.

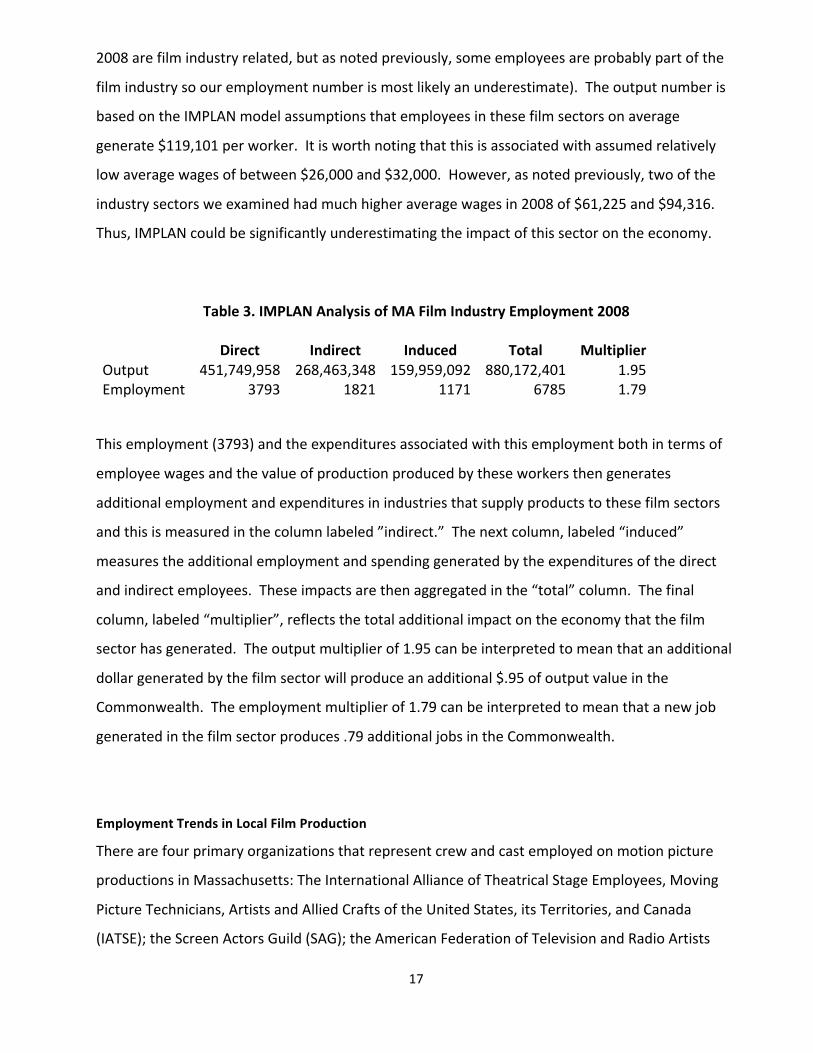

Table3showstheresultsoftheIMPLANanalysisforthefilmindustrysectorsthatwehave

focusedupon3.Thefirstcolumnrepresentsthenumbersthatwereusedasinputsintothemodel,

withtheemploymentnumberderivedfromthetotalofthethreeprimarysectorsdescribed

previously(wedidnotincludepayrollservicesbecauseitisnotclearallemployeesofthissectorin

3IMPLANisaninput‐outputmodelthatquantifiesinmonetarytermstheflowofgoodsand

servicesamongindustriesandhouseholdsintheeconomy.Thisenablesonetofollowaparticularexpenditureasitimpactsdifferentsectorsoftheeconomyandtracethemoneyasitisspentandre‐spent.Inthiscase,thepathofadollarthatoriginatesinthefilmsectorendswhenthatdollarleavestheCommonwealththroughdomesticorforeigntrade,oriscollectedasatax.Likewise,thisexpenditureanalysisalsoenablesustotraceemploymentimpactsinthesedifferentsectors.

Page 19

17

2008arefilmindustryrelated,butasnotedpreviously,someemployeesareprobablypartofthe

filmindustrysoouremploymentnumberismostlikelyanunderestimate).Theoutputnumberis

basedontheIMPLANmodelassumptionsthatemployeesinthesefilmsectorsonaverage

generate$119,101perworker.Itisworthnotingthatthisisassociatedwithassumedrelatively

lowaveragewagesofbetween$26,000and$32,000.However,asnotedpreviously,twoofthe

industrysectorsweexaminedhadmuchhigheraveragewagesin2008of$61,225and$94,316.

Thus,IMPLANcouldbesignificantlyunderestimatingtheimpactofthissectorontheeconomy.

Table3.IMPLANAnalysisofMAFilmIndustryEmployment2008

Direct Indirect Induced Total MultiplierOutput 451,749,958 268,463,348 159,959,092 880,172,401 1.95Employment 3793 1821 1171 6785 1.79

Thisemployment(3793)andtheexpendituresassociatedwiththisemploymentbothintermsof

employeewagesandthevalueofproductionproducedbytheseworkersthengenerates

additionalemploymentandexpendituresinindustriesthatsupplyproductstothesefilmsectors

andthisismeasuredinthecolumnlabeled”indirect.”Thenextcolumn,labeled“induced”

measurestheadditionalemploymentandspendinggeneratedbytheexpendituresofthedirect

andindirectemployees.Theseimpactsarethenaggregatedinthe“total”column.Thefinal

column,labeled“multiplier”,reflectsthetotaladditionalimpactontheeconomythatthefilm

sectorhasgenerated.Theoutputmultiplierof1.95canbeinterpretedtomeanthatanadditional

dollargeneratedbythefilmsectorwillproduceanadditional$.95ofoutputvalueinthe

Commonwealth.Theemploymentmultiplierof1.79canbeinterpretedtomeanthatanewjob

generatedinthefilmsectorproduces.79additionaljobsintheCommonwealth.

EmploymentTrendsinLocalFilmProduction

Therearefourprimaryorganizationsthatrepresentcrewandcastemployedonmotionpicture

productionsinMassachusetts:TheInternationalAllianceofTheatricalStageEmployees,Moving

PictureTechnicians,ArtistsandAlliedCraftsoftheUnitedStates,itsTerritories,andCanada

(IATSE);theScreenActorsGuild(SAG);theAmericanFederationofTelevisionandRadioArtists

Page 20

18

(AFTRA);andtheInternationalBrotherhoodofTeamsters(IBT).Therehasbeensignificant

employmentandwagegrowthineachoftheseunionsinMassachusettsinrecentyears.

IATSELocal481:MostlargemotionpictureandtelevisionproductionsinMassachusettsaredone

bycompaniesthathavesignednationalagreementswithIATSEoragreementswithLocal481

specifically.Asaresult,crewsonlargeandmediumbudgetstudiofeaturefilms,televisionpilots,

televisioncommercials,andsomelowbudgetindependentfeaturefilmstypicallyworkunderthe

termsofaunionagreement.IATSErepresentedemployeesmakeupalargeproportion(upto

75%)ofthecrewonfilmandtelevisionproductions.Alargeproportionofthesearemembersof

IATSELocal481(http://www.iatse481.com),whichrepresentsthestudiomechaniccraftsinthe

NewEnglandstates(Massachusetts,RhodeIsland,NewHampshire,Vermont,Maine).4

IATSEmembershiphasgrowndramaticallyinrecentyearsasaresultoftherecentgrowthinfilm

andtelevisionproductioninMassachusetts.Local481’sMassachusetts’smembershiphasmore

thandoubledsincethepassageoftheFTC,increasingfrom237in2005to585in2008.There

havebeensimilarratesofmembershipgrowthinotherMassachusettsIATSElocals.

TotalannualwagesearnedinMassachusettsbyLocal481membersincreasedten‐foldoverthe

sameperiod,growingfromapproximately$3millionin2005to$30millionin2008.Because

IATSE’swageratesareeffectivelyfixedbyitsagreementswithproducers,andinlightofthe

growthinLocal481’smembership,itissafetoassumethatthisgrowthinwagesrepresentsan

increaseinearningsfromincreasedworkopportunitiesacrossabroadspectrumofthelocal’s

members.

WhileLocal481’smembershiphasgrowninsize,ithasalsoincreasedinquality.Overthepastfew

years,manyLocal481membershaveadvancedfromjuniorrolestobecomeheadsof

departments,aprogressionthatnowprovidesthemwithincreasedresponsibilitiesandhigher

wages.ThisdevelopmenthasenhancedtheabilityofMassachusettstosupportlargeproductions

withlessneedtoimportkeyworkersfromoutofstate.Forexample,onarecentlyfilmedAdam

4 The 15 crafts represented by Local 481 are Art Department Coordinators, Construction, Costume/Wardrobe, Craft Services, Electric/Set, Lighting, Greens, Grip, Locations, Medical/First Aid, Properties, Set Dressing, Sound, Special Effects, Teleprompter Operators, and Video Assist.

Page 21

19

Sandlermovie(“LakeHouse”)almostallofthedepartmentsrepresentedbyIATSEmemberswere

staffedlocallyfromdepartmentheadsdown.Oneveteranofthelocalindustrynotedthatthe

Commonwealth’screwbasecouldnowsupport4‐5featurefilmsatonce,whichwasnotthecase

twoyearsago.

IATSErepresentativesreportthatsomeofthesenewmembershavemigratedfromrelatedtrades

thathavebeenexperiencingsignificantemploymentcontraction.Therearenumerousinstancesof

carpenterswhohadbeenlaidofforwereunderemployedintheconstructionindustry

transitioningtothemotionpictureindustry,workingsteadily,andthenjoiningLocal481.Each

newjobinfilmandtelevisionproductionthatreplacedalostjobinconstructionandrelatedfields

generatedbothdirectbenefits(inincreasedwages)andindirectbenefitsbyreducingdemandsfor

stateservicesandbenefitsthatwouldhavebeencollectedbyunemployedtradespeople.

ExperiencedmembersofotherIATSElocals,formerlybasedinLosAngelesorNewYork,whohad

familytieshereorwhohadattendeduniversitiesinMassachusetts,havealsomovedbacktothe

Commonwealthtoworkonproductions.Ifthesetrendscontinue,itcouldincreasetheproportion

ofwagesfromlargeproductionsthatgotoCommonwealthresidents(atrendtheDepartmentof

Revenueiscurrentlytracking).

SAGandAFTRA:SAG(http://www.sag.org/)andAFTRA(http://www.aftra.com/)bothrepresent

performerswhoappearintelevisionshowsandcommercialswhileSAGalonerepresents

performerswhoappearinmotionpictures.Sincemotionpictureproductionaccountedformost

oftherecentincreaseinproductioninMassachusetts,recentworkforcedevelopmentsinthelocal

branchofSAGareespeciallyrelevanttounderstandingtheimpactoftheseprojectsonthelocal

workforce.

TheBostonbranchofSAGgrewbyalmost30percentbetween2005and2008,withmembership

topping2100bytheendof2008.Therewasa58%increaseinwagesearnedonfeaturefilmsand

Page 22

20

televisionprogrammingin2008,ascomparedto2005.5Wagesearnedontelevisioncommercials

bymembersofSAG’sBostonbranchremainedroughlyconstantbetween2005and2008.This

mightbeduetotheoveralldownturninthecommercialindustryaswellaslessawarenessofthe

availabilityoftaxincentivesinthispartoftheindustryasopposedtofilmproduction.

Anotablefeatureoftelevisioncommercialsisthattheygenerateresidualpaymentsforactors.

Totalresidualsearnedbyactorsonacommercialtypicallyequaltwicethewagespaidduringthe

shootandmayrepresentfuturetaxableMassachusetts’sincome.Featurefilmresidualsare

currentlyaminorcomponentoftheearningsofBostonbranchSAGmembers,approximately10

percentofoverallfilmwagesin2008.However,thereisoftenaseveralyearlagbetween

productionandtheeventsthattriggerpaymentoffeatureresiduals,suchasreleaseofDVDand

appearanceoncable/broadcasttelevision.Featureresidualsarelikelytoincrease,potentially

markedly,forlocalSAGmembersasproductionsthathavebeenshotinMassachusettsoverthe

pasttwoyearsreachthosephasesofthedistributionprocess.Inaddition,itispossiblethatfuture

wagesfromresidualspaidtoprincipalperformersandparticipationagreementsforabovetheline

talentcouldbetreatedasMassachusettssourcedincome.Ifso,thiscouldrepresentasignificant

sourceoffutureCommonwealthtaxrevenue.(SeeAppendix1foradiscussionoftheseissues).

InternationalBrotherhoodofTeamstersLocal25:TheInternationalBrotherhoodofTeamsters

Local25(http://www.teamsterslocal25.com/)representsthetransportationworkerswhodrive

thetrucksandequipmentusedinfilmandtelevisionproduction.Althoughfilmandtelevision

employeesrepresentasmallproportionofLocal25’stotalmembershipof11,500employees,this

grouphasbeengrowingrapidly.Historically,therehaveonlybeen30Teamstersemployedinthis

industry.Currently,thereareover200.Inadditiontothegrowthintotalemployment,therehas

beenagrowthinthetotalhoursworkedbytheseemployees.In2008,therewereover330,000

hourspaidintotheTeamster’spensionandhealthandwelfarefundsbylocalfilmandtelevision

workers.AsinthecaseofIATSEmembers,someofthesenewworkershavecomefromotherlocal

transportationindustriesthathaveexperiencedrecentcontraction.

5 Permission is required from SAG’s national office to report on gross wages earned by local

branches, and since the national has not granted such permission to the Boston branch, we are only able to report on trends in this report.

Page 23

21

Becausetransportationcoordinatorstypicallygetcompetitivebidsfrommultiplevehicleand

equipmentleasingcompaniesandbecausemanykindsofequipmentandtrucksarenotavailable

intheCommonwealth,localproductionsoftenrentequipmentfromoutofstate.Somelocalpress

reportshaveusedthisfacttosuggestthattruckswithoutofstateregistrationsarebeingdriven

byoutofstateemployees.Infact,anytruckorpieceofequipmentthatisusedinaunionfilmor

televisionproductionisdrivenbyamemberofLocal25.Therehaveevenbeeninstancesof

TeamsterstravellingoutofstatetopickupequipmentbeingusedinMassachusetts’sproductions.

WhilethesedriversarepaidasMassachusetts’semployees,increasingthenumberoffilm

equipmentrentalcompaniesinMassachusettswouldincreasetheproportionofnon‐wage

spendingbeingkeptintheCommonwealth.

Workforcedevelopment:Asdescribedabove,therehasbeensignificantgrowthinboththe

numberandskilloflocalfilmproductionemployees.However,therearestillsomecraftswithtoo

fewemployeeswhoareexperiencedenoughtostaffkeypositions.Inthemiddleof2008,alocal

assistantdirectorandlocationmanagerreportedthatsomecrewlackedexperienceworkingon

largeproductionsandexpressedtheneedformorelocalseniorcrewinpositionslikecostumeand

productiondesign,specialeffects,directorsofphotography,digitalimagetechnicians,hair,and

makeup.Otherthingsbeingequal,filmsandtelevisionproductionsprefertouselocalcrew

becauseitsavesthetransportationandhousingcostsassociatedwithimportingtalent.However,

becausecrewsareassembledbykeypositionsanddepartmentheadswhodrawonnetworksof

employeesthatworktogetheronasemi‐regularbasis,thegrowthoflocalkeypositions

representsanimportantlynchpininlocalworkforcedevelopment.Becausethesekeypositions

tendtohirepeopletheyhaveworkedwithbefore,astheMassachusettscrewbasegainsmore

experienceandconnectionswithoutofstateproducers,wemayfindthattheproportionofwork

onlargefilmsgoingtolocalcrewwillincrease.

AIMMandMPC,alongwiththeMassachusettsFilmOffice,havecollaboratedwiththe

Commonwealth’sDepartmentofWorkforceDevelopmenttobuildawarenessaboutopportunities

infilmproduction.Anindustryinformationday,“Jobs,Camera,Action,”wasalsoheldinBostonin

January2009andattractedmorethan600people.Thisday‐longworkshopwasdesignedto

Page 24

22

educateattendeesonhowtobuildacareerintheMassachusettsfilmindustry.Itincludeda

careerexhibitionaswellasfoursessionswithindustryexecutivesexplainingwhattypesof

positionstheywillneedtofill.MPCandAIMMhavealsoheldseveraleventsforlocaluniversity

students.Thesefocusedonskillstrainingforentry‐levelpositionsandnetworkingtolink

employerswithstudents.

InJanuary2009,theDepartmentofWorkforceDevelopmentincollaborationwithIATSElocal481,

heldtwotrainingsessionsfor80servicescounselorsfrom37CareerCentersstatewideonhowto

helpdisplacedworkerstransitionintofilmindustryjobs/careerpaths.Thesesessionsparticularly

emphasizedworkerswhoseskillscouldbereadilytransferredtomotionpictureproduction,

includingcarpenters,painters,medics,andlandscapers.Subsequently,theDepartmentof

WorkforceDevelopmentscheduledeventstoidentifyworkerswiththoseskillswhomightbegood

prospectsforthefilmandtelevisionindustryandrecommendthemforacareerworkshopthat

willbeconductedbymembersofLocal481.Ifthismodelprovessuccessful,itmaysubsequently

beusedforothereventstochannelprospectiveworkerstounion‐basedjobopportunitiesthat

maybecreatedbytheAmericanRecoveryandReinvestmentAct(ARRA)

UsingacombinationofBLSdataandinterviews,wehavebeenabletodocumentsubstantial

growthinseveralsectorsofthefilmindustryintheCommonwealth,muchofwhichisassociated

withtheimplementationoftheFTC.Howeveritisclearthattherearemanyotherrelatedsectors,

includingindustriesthatservicethefilmindustryandtelevisioncommercials,independent,and

documentaryfilms,thatarebenefittingfromtheexpansionofthefilmindustryworkforce

associatedwiththeincreasedproductionoffilmsintheCommonwealth.Inordertoexplorethe

industriessupplyingthefilmindustryinmoredepth,thenextsectionfocusesonthenon‐wage

spendingpatternsassociatedwithfilmproductionintheCommonwealth.

Non‐wagespendingpatterns

AccordingtotheMassachusettsDepartmentofRevenue(2009:8),36%(e.g.,$247M)ofthetotal

filmindustryspendingintheCommonwealthbetween2006and2008wasonnon‐wageitems.The

Page 25

23

largestcategoriesoftheseitemswerelocationfees($56.8M),transportation($35.8M),fringe

benefits($33.5M),hotelsandhousing($29.3M),setconstruction($27.2M)andfood($17.7M).

Interviewssuggestthatalargeproportionofthisspendingiscenterednearproductionlocations

andcanrepresentsignificantsourcesofrevenueforlocalmerchants.Theyalsoraisequestions

aboutwhetherandhowwellthesepatternsarerepresentedinexistingeconometricmodels.For

example,locationfeesareoftenpaiddirectlytosmallorganizationsandevenindividual

households.Forexample,themovieZookeeperwasfilmedintheFranklinParkzoointhesummer

of2009.Atatimewhenthezoohadexperiencedasignificantbudgetcutandwasinriskof

shuttingitsdoors,themovieproductionpaidalarge(butundisclosedfee)bothtothezoodirectly

aswellasa$20,000feedirectlytothecity’sParksandRecreationDepartment(Irons,2009).In

additiontoprovidinganimportantcashinfusiontoastrugglingpublicinstitution,thisproduction

alsoprovideddirectinvestmentsintopublicfunds.Thesespendingpatternsmaybemissed,orat

bestincorrectlyspecified,bystandardeconometricmodelstypicallyusedineconomicimpact

studiesoflocalfilmandtelevisionproductions.

Togetabetterunderstandingofthesenon‐wagespendingpatterns,weinterviewedlocal

productionemployeesandvendorsaswellascollecteddataonthevendorsusedby10motion

picturesfilmedinMassachusettsin2008.Unfortunately,wewerenotabletoobtaindataonthe

amountsspentateachvendor.However,combininginterviewsandnetworkandgeographic

visualizationmethods,wewereabletoidentifyseveralinterestingpatternsinthedistributionof

thisspending.

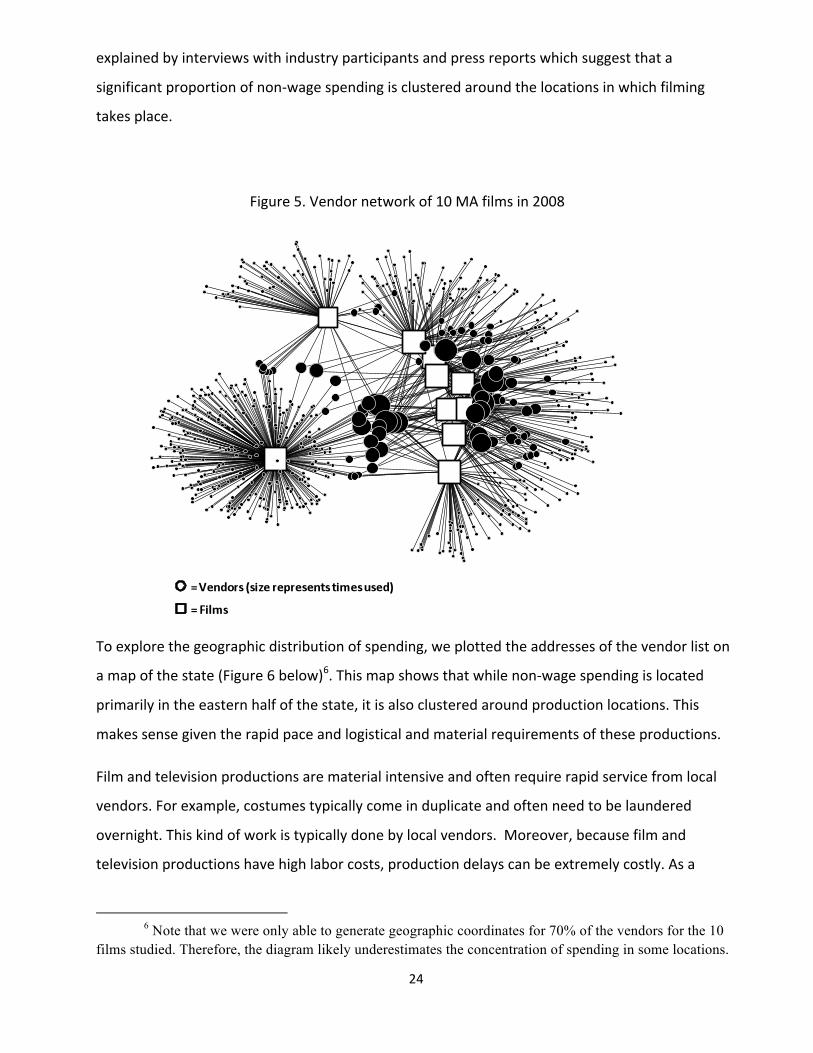

Figure5belowrepresentsanetworkanalysisofthevendorsusedby10motionpicturesfilmedin

Massachusettsin2008.Usingdataprovidedbyoneofthelocalunions,wecreatedthisdiagramby

importinglistsoffilmsandtheirvendorsintoanetworkanalysisprogramcalledUCINET(Borgatti,

Everett,&Freeman,1996).Inthediagram,filmsarerepresentedaswhitesquaresandvendorsas

blackcircles.Thisanalysisclearlyshowstwodynamicsinthenon‐wagespendingpatternsinthe

localfilmindustry.Thetwoclustersoflargeblackcirclessurroundingthefilmsrepresentthe

rapidlygrowingcoreofvendorsthatprovidespecializedservicesandequipmenttofilmand

televisionproductions.Eachfilmisalsosurroundedbyaclusterofuniquevendorsthatarenot

sharedwithotherfirms.Inotherwords,whilemostfilmsrelyonasmallcoreoffirmsthatprovide

specializedservicesandmaterial,eachfilmalsohasitsownuniquesetofvendors.Thispatternis

Page 26

24

explainedbyinterviewswithindustryparticipantsandpressreportswhichsuggestthata

significantproportionofnon‐wagespendingisclusteredaroundthelocationsinwhichfilming

takesplace.

Figure5.Vendornetworkof10MAfilmsin2008

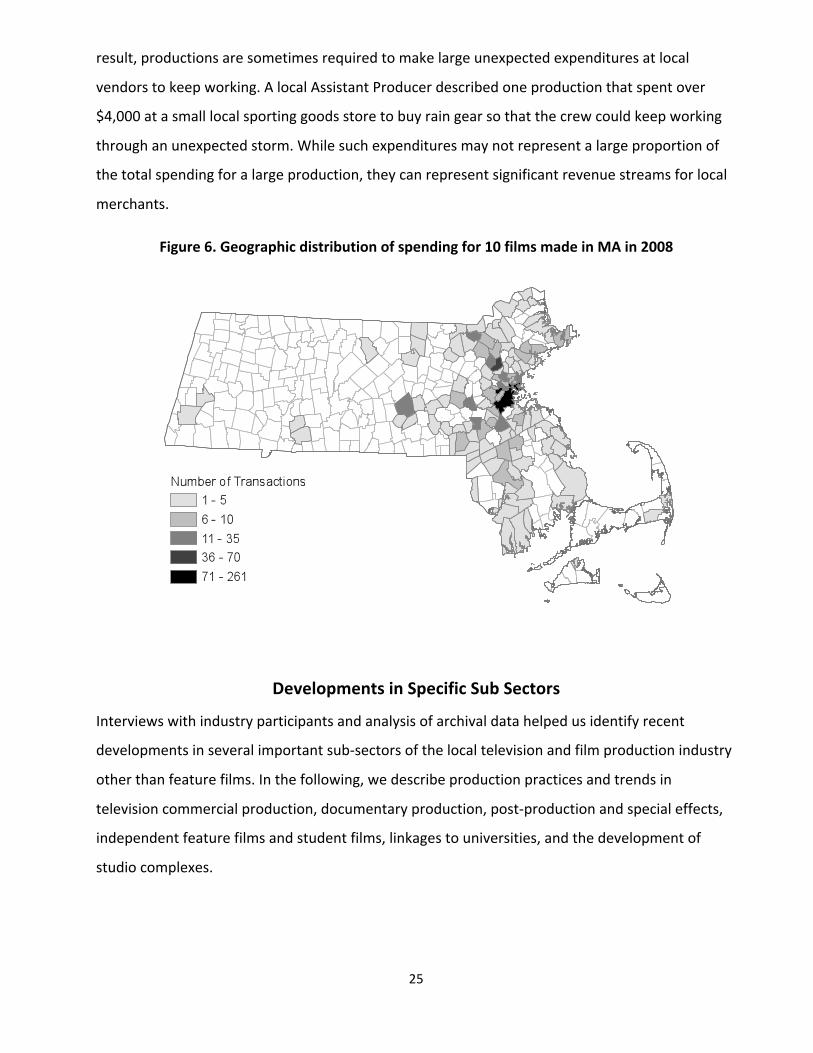

Toexplorethegeographicdistributionofspending,weplottedtheaddressesofthevendorliston

amapofthestate(Figure6below)6.Thismapshowsthatwhilenon‐wagespendingislocated

primarilyintheeasternhalfofthestate,itisalsoclusteredaroundproductionlocations.This

makessensegiventherapidpaceandlogisticalandmaterialrequirementsoftheseproductions.

Filmandtelevisionproductionsarematerialintensiveandoftenrequirerapidservicefromlocal

vendors.Forexample,costumestypicallycomeinduplicateandoftenneedtobelaundered

overnight.Thiskindofworkistypicallydonebylocalvendors.Moreover,becausefilmand

televisionproductionshavehighlaborcosts,productiondelayscanbeextremelycostly.Asa

6 Note that we were only able to generate geographic coordinates for 70% of the vendors for the 10

films studied. Therefore, the diagram likely underestimates the concentration of spending in some locations.

Page 27

25

result,productionsaresometimesrequiredtomakelargeunexpectedexpendituresatlocal

vendorstokeepworking.AlocalAssistantProducerdescribedoneproductionthatspentover

$4,000atasmalllocalsportinggoodsstoretobuyraingearsothatthecrewcouldkeepworking

throughanunexpectedstorm.Whilesuchexpendituresmaynotrepresentalargeproportionof

thetotalspendingforalargeproduction,theycanrepresentsignificantrevenuestreamsforlocal

merchants.

Figure6.Geographicdistributionofspendingfor10filmsmadeinMAin2008

DevelopmentsinSpecificSubSectors

Interviewswithindustryparticipantsandanalysisofarchivaldatahelpedusidentifyrecent

developmentsinseveralimportantsub‐sectorsofthelocaltelevisionandfilmproductionindustry

otherthanfeaturefilms.Inthefollowing,wedescribeproductionpracticesandtrendsin

televisioncommercialproduction,documentaryproduction,post‐productionandspecialeffects,

independentfeaturefilmsandstudentfilms,linkagestouniversities,andthedevelopmentof

studiocomplexes.

Page 28

26

Televisionproduction:AccordingtotheMassachusettsDepartmentofRevenue(2009:6),

televisionproductiongenerated70%(186)ofthetotalnumberofcrediteligibleprojectsfrom

2006‐2008.However,becauseoftherelativelysmallersizeoftheseproductions,thesectoronly

used7%ofthetotalvalueofthecreditsissuedduringthatperiod.Comparedtofeaturefilms,

televisionproductions(especiallycommercialsandnon‐fictionprograms)typicallyuseamuch

smallerproportionofabovethelinetalent.Asaresult,theseproductionsmaymakelarger

proportional(thoughamuchsmallertotal)contributiontolocalwageandnon‐wagespending.

Infact,thetelevisionproductionsectorinMassachusettsisitselfcomprisedofatleastthree

differentsub‐sectors.Inthefollowing,webrieflydescriberecenttrendsinscriptedanddramatic

television,non‐fictionandpublictelevision,andadvertisingproduction.

DramaticandScriptedTelevision:Ascriptedtelevisionshowbeginswiththeproductionofapilot

episode.Notallpilotsbecomelongrunningtelevisionshows.However,evenshowsthatare

pickedupandairforasingleseasongenerateconsistentemploymentforasmanyasonehundred

castandcrewmembers.Likeblockbusterfilms,therelativelysmallnumberofshowsthatbecome

popularcangeneratelong‐termeconomicbenefitsintheformoflocalwageandnon‐wage

spending,futureearningsfromresiduals,andpotentiallylocalbrandrecognition.Forexample,the

Cheerstelevisionshowgeneratedlong‐termeconomicbenefitsintheformofincreasedtourism

eventhoughitwasnotfilmedinMassachusetts.The1980stelevisionshow,“SpencerforHire,”

generatedlong‐termjobsformanylocaltelevisionproductionemployeesandcontributedtensof

millionsofdollarstothelocaleconomy.

TelevisionpilotsandserieshaverecentlybeenfilmedinMassachusettsandcaptured16%ofthe

totalcreditsissuedbetween2006and2008.Onerespondentdescribedthelong‐termimpactif

oneofthesepilotsgeneratesatelevisionshowthatismadeinMassachusetts.“Iftheshow

comes,everyepisodewillcostabout$2M.Theywillshoot10episodes.Thatis$20Mrightthere.

Therewillbe80corepeopleandupto140atlunchwhenyouincludetheextras,dayplayers,etc.”

However,becausescriptedtelevisionistypicallyproducedinastudio,Massachusettscurrently

lacksacriticalresourceforthegrowthofthissector.Respondentsarguedthatwithoutastudio,

scriptedtelevisionshowsmaycontinuetouseMassachusettsasabackdropforexteriorshots(as

Page 29

27

thelongrunningshow“BostonLegal”did)butwouldfinditdifficulttoproduceafullshowinthe

Commonwealth.

Non‐fictioncable:Non‐fictioncabletelevisionproductioniscurrentlythefastestgrowingand

mostprofitablepartofthetelevisionindustry.Thisisdrivenbythefactthatcablenetworks(as

opposedtobroadcastnetworks)cangeneraterevenuefrombothadvertisingandcarrier

subscriptionfees.Moreover,ascomparedtoscriptedtelevision,non‐fictiontelevisionhaslower

productioncosts.Respondentsreportthatthereissignificantroomforinternationalgrowthinthis

sector.

IndustryrepresentativessuggestthatMassachusettshasthepotentialtobethenation'sthird

largestcenterfornon‐fictiontelevisionproduction.Thereareseveralfactorsthatmaygive

Massachusettsastrategicadvantageinthisarea.First,thelaborpoolcontainsexperienced

documentaryproducers,videographers,andsoundrecordistsaswellasalargepoolofstudents.

OnlyLosAngelesandNewYorkgraduatemorefilm/TV/videostudentsannuallythan

Massachusettsandmanyofthesestudentsarecurrentlyfindingjobsintherapidlygrowinglocal

non‐fictiontelevisionsub‐sector.

Barrierstoentryintonon‐fictionTVarelowerthanforfeaturemovieproduction.Inparticular,

non‐fictionTVhasmanyopeningsforproductionassistants,assistanteditors,andresearchers.

Movementupcareerladders(tobeingassociateproducerandproducer)isalsomorerapidthanit

isinfeaturefilmproduction.Thejobsalsolastlongerthanfeaturefilmjobsbecausethecomplete

productioncycleofonehourofprimetimenon‐fictioncableTVisbetweensixandsevenmonths

long.

Massachusettsalsohasseveralotheradvantagesthatmaycontributetothegrowthofthissector.

Thestateishometooneofthenationalleadersinvideoeditingequipment,Tewksbury‐based

AVID,aswellasarapidlygrowingdigitalgamingindustry.PowderhouseProductionshasused

someofitssavingsfromtheFilmTaxCredittoinvestinAVID'snewUNITYISISeditingsystemand

recentlybecameoneoffewindependentproductioncompaniesinthecountrytohavethis

sophisticatedvideostorageandretrievalsystem.Notonlydiditgenerateadditionalsalesrevenue

foranotherMassachusettscompany(Avid),itwillalsoenablePowderhousetoeditlargenumbers

Page 30

28

ofprogramsatafractionofthecostofitscompetitors,givingthemasignificantcompetitive

advantage.PowderhousewillalsobefeaturedinanationalmarketingcampaignbyAVIDabout

theUNITYISISsystem.Thisstoryillustratessomeofthepositivespillovereffectsofincreasesin

localfilmandtelevisionproductiononotherlocalcompaniesthatarenotdirectlymonetizing

credits.

Finally,becausetheBostonareahasalargeconcentrationofresearchuniversities,high

technologyandbiotechnologyfirms,manyofthestoriesthatmakeupthecontentfornon‐fiction

televisionprogramscanbefoundlocally.Thisaccesstocontentprovidesanadditionaladvantage

forlocalnon‐fictiontelevisionfilmproducers.

AllofthesestrategicadvantagescombinedwiththepassageoftheFTChavehelpedthissector

growrapidlyinrecentyears.Onecompany(PowderhouseProductions)grewfrom35employees

in2006toahighof124employeesin2009.In2009,Powderhouseproduced36hoursofprime‐

timenon‐fictionTVforDiscovery,History,Science,AnimalPlanetandPBS.Duringthattime,they

hired45productionassistants,12assistanteditors,6researchersand105studentinterns.In

2010,Powderhouseexpectstoproduce45hoursofTVandexpectstocontinuehiringnew

employees.Notsurprisingly,thisgrowthisalsoreflectedindramaticrevenuegrowththatnearly

doubledbetween2007and2009.Itisalsoleadingtonationalrecognitionreflectedinthefactthat

oneoftheleadingagencies,CreativeArtistsAgency(CAA,)recentlytookonPowderhouseasa

clientandnowrepresentstheminbothLosAngelesandNewYork.

PublicTelevision:AshometothepublictelevisionstationWGBH,Bostonhaslongbeen

recognizedasanationalcenterfornon‐fictiontelevisionproduction.Asoneoftheflagship

stationsinthePublicBroadcastingSystem,WGBHhasa60yearhistoryproducinginternationally

recognizednon‐fictionprogramslikeFrontline,NOVAandThisOldHouseaswellasawardwinning

children’sprogramming(e.g.,Zoom,Arthur).WGBHtypicallyhasbetween100‐200projectsin

productionanddevelopmentatanygiventime.Itisalsothesourceoflocalproductionspending

andemployment.Infiscalyear2007,WGBHspentover$126milliononprogramdevelopmentand

productionalone(WGBH,2008).Asinfeaturefilmandotherkindsoftelevisionproduction,

locationdecisionsinpublictelevisionaredrivenbycomplexcombinationsoffinancial,aesthetic,

Page 31

29

andpracticalconsiderations.Forexample,aproducerforaspecificshowmightbeselectedforher

expertiseinthetopicwhileothercontractorsmaybeselectedforspecifictechnicalandartistic

skillslikeanimation.Therefore,someproportionofthetotalWGBHproductionbudgetgoestoout

ofstatevendorsandemployeeswithskillsandexpertisethatarenotavailablelocally.

Thesefactorsnotwithstanding,WGBHremainsalargelocalemployerintelevisionproductionwith

approximately900peopleatitsBostonheadquarters.Moreover,anexaminationofWGBHtax

filings(availableatwww.guidestar.org)revealsthatthreeofthefivemosthighlypaidindependent

contractorsforprofessionalservicesin2007wereMassachusettscompaniesthatreceivedmore

than$500Kthatyear.Althoughmanyoftheirlargestindependentcontractorsforproduction

servicesareoutofstatecompanies,somelocalcompanieshavereceivedworkfromWGBHandit

ispossiblethatthestationmaybeabletoincreasetheproportionofitsproductionworksourced

tolocalcompaniesastheygainnewexpertise,equipment,andskilledemployees.

Asignificantnewdevelopmentoccurredin2007whenWGBHopenedanewflagshipoffice

buildingandstudiocomplexinBrighton,MA.Thisbuildingrepresentsanimportantnewresource

inthelocalnon‐fictiontelevisionproductioncommunityandgeneratedover$20millionin

revenuesforlocalconstructioncompaniesbetween2006and2007.Becauseofthisnewspace,

WGBHhasbeenabletobringmembersofthepublicintoitsfacilitiesasneverbefore.For

example,anOctober2009premierforthecriticallyacclaimedseries,LatinMusicUSA,drewover

1,000gueststotheWGBHstudios.Thiskindofincreasedpublicengagementhasbeendirectly

enabledbytherecentWGBHexpansion.

Whilethefilmtaxcredithasnotbeenasignificantdriverofthisexpansion,ithashadapositive

impactonsomeWGBHproductiondecisions.Becauseitreliesheavilyonexternalfundraisingto

produceitsprogramsandtheseprogramsoftenhaveproductioncyclesof18monthsormore

(duringwhichtimefundraisingoftencontinues),programsoftenneedtobeapprovedbefore

fundingisfullysecured.TheavailabilityoftaxincentiveshashelpedWGBHmanagetheserisksby

providingafinancialcushionthatallowsthemtoapprovemoreprogramsbeforecomplete

fundingissecured.

Inadditiontomanagingtheserisks,WGBHhasusedcreditstoincreaseresearchanddevelopment

innewprograms.Forexample,the2006seasonofDesignSquadcost$2milliontoproduce.Of

Page 32

30

this,allbut$500,000wasspentinMassachusetts.Thisproductioninturngenerated$235,000in

cashforWGBH,whichwasthenusedtofundfutureproductionsandeasefundraisingpressureat

thestation(Mohl,2008).Therefore,onehiddenbenefitoftheFTCmaybeincreasingthescope

andbreadthofWGBH’spublicprogrammingandhelpingtoreducerisksandfundraisingpressure

atthisnationallyrecognizedpublictelevisionstation.Thecombinedimpactofthe900workers

WGBHemploysdirectlyandcontractswithlocalproductioncompaniesandfreelanceemployees,

aswellasitsrecentlybuiltstudiocomplex,representsignificantlong‐terminvestmentsinthelocal

non‐fictiontelevisionproductionsector.

Commercialsandadvertising:Amajorityofthetelevisioncommercialsproducedin

Massachusettsaremadebyasmallhandfuloffirms.Theresearchteamtalkedwiththreeofthe

largest.Thesefirmsreportedthattheiroverallbusinesshasremainedstablebetween2005and

2008,duringaperiodwhenproductionofcommercialsintheU.S.asawholehasbeenonthe

decline.Moreover,agrowingpercentageofthesefirms’workisnowbeingproducedin

Massachusetts.Onecompanyreportedthat70percentofitscommercialswereproducedinthe

Commonwealthin2008comparedtoonly40percentin2005.

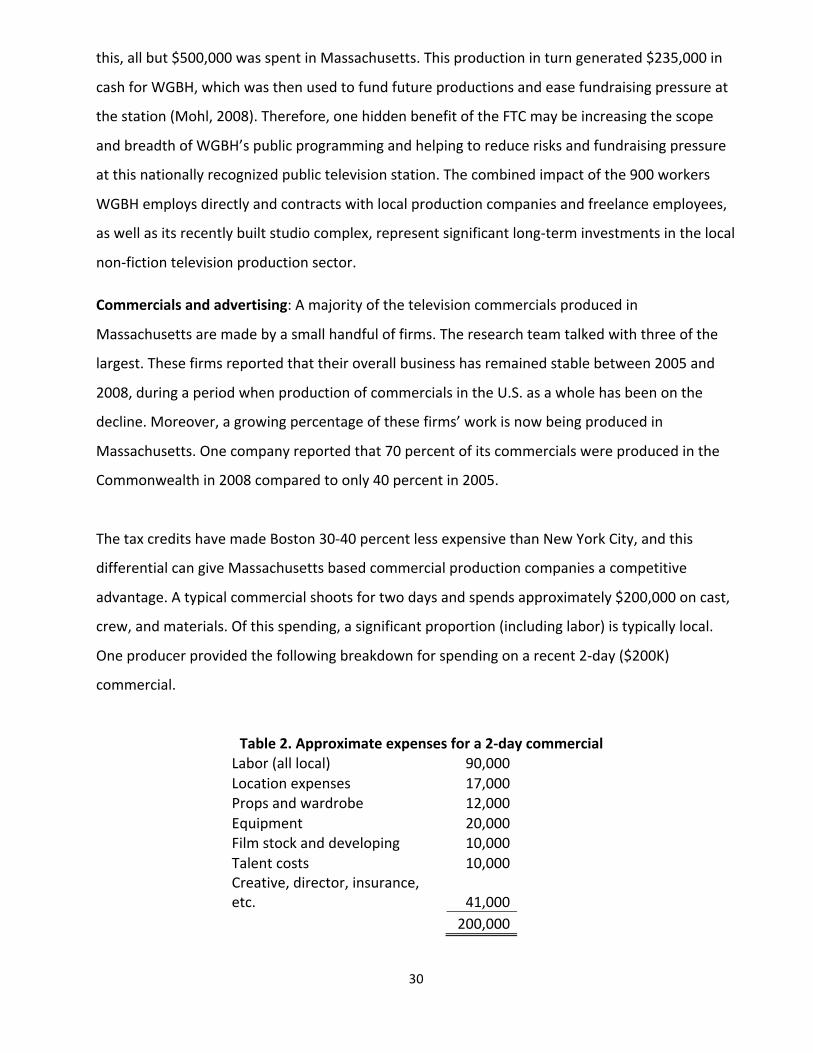

ThetaxcreditshavemadeBoston30‐40percentlessexpensivethanNewYorkCity,andthis

differentialcangiveMassachusettsbasedcommercialproductioncompaniesacompetitive

advantage.Atypicalcommercialshootsfortwodaysandspendsapproximately$200,000oncast,

crew,andmaterials.Ofthisspending,asignificantproportion(includinglabor)istypicallylocal.

Oneproducerprovidedthefollowingbreakdownforspendingonarecent2‐day($200K)

commercial.

Table2.Approximateexpensesfora2‐daycommercialLabor(alllocal) 90,000Locationexpenses 17,000Propsandwardrobe 12,000Equipment 20,000Filmstockanddeveloping 10,000Talentcosts 10,000Creative,director,insurance,etc. 41,000 200,000

Page 33

31

Commercialproductioncompanieshaverecentlyluredoutofstateadvertiserstoshoot

commercialsintheCommonwealth.Forexample,onelocalcompanyrecentlycompletedspots

hereforalargepharmaceuticalcompanybasedinNewYorkandanautocompany.

BostonadvertisingagenciesandlargeMassachusettsbasedadvertisers(forexample,Fidelity,New

Balance,GilletteandRebok),however,havestilltendedtouseoutoftownproductioncompanies

formostoftheircommercials(although2008wasthefirstyearpeoplehaveheardofoutofstate

commercialproductioncompaniesshootinginMassachusettstocapturethetaxcredit).TheMPC

hasrecentlyundertakenanaggressivecampaigntoencourageMassachusetts‐basedadvertisers,

suchasTJX,toshoottheircommercialsintheCommonwealth.

DocumentaryFilm:Documentaryfilmmakinghaslongbeenadistinctivestrengthof

Massachusetts.Manyofthepioneersof16‐millimeterdocumentaryfilmmakingwerebasedhere,

andWGBH’sroleastheflagshipPBSstationhasallowedtheCommonwealthtoestablishand

maintainaleadershippositioninbothseriesandlong‐formtelevisiondocumentaries.Interviews

indicatethatthetaxcreditshavebeenhelpfultosomeindependentdocumentarymakers,making

projectsfeasibleandenablingthemakerstoproducehigherqualityprojectsduringaperiodwhen

financialsupportforindependentworkhasbeengrowingscarce.

Whileitisimpossibletodeterminepreciselyhowmanyindependentdocumentaryproducersare

workinginthestate,theylikelyoutnumberindependentnarrativeproducers,asmallerbutnot

insignificantgroupoflocalfilmmakers.Itisworthnotingthatmostindependentfilmmakershave

incomesourcesotherthantheirindependentfilms.Thesefilmmakersoftenworkinrelated

sectorsincludingindustrial,educational,andcabletelevisionproductionandearnalowerwage

workingontheirownfilmsthantheyearnfromtheirotherjobs.

Becausethesefilmsareoftenmadeusinggrantsandotherdonations,independentfilmmakers

relyonfiscalsponsorswhoprovidethe501c3statusneededtoqualifyformajorgrants.While

therearemanyfiscalsponsorsintheCommonwealth,threeofthemworkwithalargenumberof

localproductionsandassistfilmmakersinresearching,applyingfor,andadministeringgrants.

Interviewswiththeexecutivedirectorsofthreesuchorganizationshelpedusunderstandrecent

trendsinthissector.

Together,theseorganizationssupportedapproximately150projectsin2009.Notalldocumentary

Page 34

32

filmsthatreceivemajorgrantsuseoneofthesethreeorganizationsandthereareseveralother

smallerfiscalsponsorshiporganizationsinthestate.Indeed,sinceany501c3organizationcan

serveasafiscalsponsorforafilm,somefilmmakerschoosetoworkwithnon‐profitsthatarenot

primarilymediaartsorganizations,butwhosemissionsareconcernedwiththecontentareathe

filmexplores.However,thesethreefiscalsponsorsrepresentalargeproportionofthetotalgrant

fundedindependentdocumentaryproductionintheCommonwealth.

Astheirprimarysourceofincome,twoofthesponsorsdependonthefeestheychargeonthe

grantsanddonationstheyacceptonbehalfoftheirfilmmakers.Theotherisadistributorand

makesasignificantportionofitsincomethroughthedistributionarmofitsoperations.Thereare

severalfactorsthatmakeithardtogaugewhetherthefinancialstatementsoftheseorganizations

canbeusedasindicatorsofthelevelofindependentfilmproductioninthestate.First,these

organizationsdonotexclusivelyworkwithlocalfilmmakers.Localfilmmakersoftenshootthe

majorityoftheirmaterialoutsideofthestate,andwhileitishardtoestimatewhattheratioof

shootingin‐statevs.out‐of‐stateis,allthreefiscalsponsorsreportthatamajorityoftheirprojects

areshotout‐of‐state.Therefore,asignificantportionofmoneyraisedforthesefilmsisspentin

otherstates.

Anotherimportantfactortonoteisthatmajorgrantsareoftenawardedinstages.Forexample,a

majorfundermightgrantafilm$300,000inthreeyearlyinstallmentsof$100,000.Sometimes

grantsareawardedwiththestipulationthatmatchingfundsareraised,soagrantmaybe

awardedbutnotactuallypaidoutuntilyearslaterwhenthefilmmakerisabletoraiseenough

moneytomatchthosefunds.Therefore,thefinancialstatementsinanygivenyeardonot

necessarilyreflectsignificantchangesinfunders'behavior;thereissomelagtimebeforeany

changesinfundingbehaviorwouldbereflectedintheincomefiguresofthesefiscalsponsors.

Althoughthenumbersdonotgiveusaclearsenseofmorerecentfundingchanges,twoofthe

fiscalsponsorsreportedthatmajorfundersarecurrentlygivingless.Oneofthesenotes:

“ThebiggesttrendI’venoticedbetween’04and’08isthedecreaseingovernment

funding,that,especiallytheNEHwhichiswhatwe’vealwaysearnedourbreadand

butterfrombecausetheytendtogiveverylargegrantsofhalfamillionormore….

I’venoticedespeciallyinthelastthreeyears,maybetwoyearseven,thatthose

Page 35

33

budgetshavebeenslashedandtheNEHishardlyfundinganyfilmsanymore…and

iftheydo,likethisyearwegotthreebuttheywereeach$70,000,theywerevery

small,asopposedtothreethatrangebetween$400,000and$700,000inthepast,

sothat’sahugedeclineinincomeforus.”

Severalfilmmakersinterviewedechoedthesentimentthatithasbecomeincreasinglydifficultto

raisemoneyfrommajorfoundations.Inreferencetoherattemptstoraisemoneyduringthe

periodof2005–2007onefilmmakersaid:

“Therearecompetingneeds.Alotoffoundationsyouknowjustdon’twanttofund

films.Or,ifthey’regoingtofundfilms,theymightfundoneortwofilms.And,that

–thattakesuptheirwholecommitmentforanythingthattheyweregoingtospend

onfilm.”

Thiscommentsuggeststhatperhapstherearemorefilmmakerscompetingformajorgrants,and

thathascreatedaperceptionthatthereislessmoneyavailable,evenifperhapstheamountof

majorgrantshasnotdecreased.Theprevailingviewintheindependentdocumentarycommunity

isthatlargefundersaregrantinglessmoneytofilms.Whilesomethinkitisdirectlyrelatedtothe

recenteconomicdownturn,otherslocatethechangebeginningasearlyasfiveyearsago.

IntermsofspendingforindependentdocumentaryfilmsinMA,noonereportedanysignificant

changesinspendingpatternssince2005.Allfourdocumentaryfilmmakersreportedtheytypically

shootoutsideofstate,whilepost‐productionismoreoftendonein‐state.Inmostcases,wages

forproductionandpost‐productioncrewwerethemajorexpenses.Insomecases,asignificant

portionofafilm’sbudgetwasdesignatedforobtainingrightstohistoricalfootageand/ormusic.

Noneofthedocumentaryfilmmakersinterviewedreportedthatthetaxcreditimpactedtheir

spendingdecisions.Onlyonefilmqualifiedforthetaxcredit,andinthatcase,duringthe

productionandpost‐productionofthefilm,thefilmmakerassumedthattheywouldnotqualify.

Eventhoughthetaxcreditprogramdoesnotappeartohaveinfluencedspendingdecisions,all

filmmakerssaidtheywerethankfulthatthetaxcreditprogramexistsandthatitmightimpact

theirspendingdecisionsinthefuture.Onefilmmakerreported:

“Forindependentbillings,peoplewhomakedocumentaries,whoworkonashoestring

basically…thetaxcreditisalifeline.It’saGodsend…Wedoalotofourworkin

Page 36

34

Massachusetts,partlyoutofpreferenceandpartlyyouknowoutofbecausewe’rehere

andwecan’taffordtotravelanyway…Havingsomeportionofthatcomebacktous

is…goldenand…foralotofusthat’swhatwillenableustocontinuetowork.”

Anothersaid:

“Ihavenotmadeanyfilmsthathavequalifiedanditdidn’tinfluencemydecisionto

makewhatfilmsIhavemadesofar…But…itmakesmewanttoshootandeditin

Massorfilmsometimesoon.Iamkeepingmyeyeswideopenforfilmideasthat

couldbedonehere.Whynotshoothere?Weshouldbedoingthatkindofthing.”

Independentnarrativeandstudentfilms:ThenumberoflowbudgetfeaturefilmsshotunderSAG

agreementinMassachusettsdoubledinrecentyears,risingfrom18in2005to37in2008.The

numberofstudentfilmsshotunderSAGagreementmorethandoubled,goingfrom16in2005to

41in2008.Althoughthesekindsofprojectsdonotmakealargeeconomicimpactintheshort

term,theyareimportantfordevelopingyoungtalent.Inparticular,youngdirectorswhoachieve

earlysuccessinMassachusettsmaychoosetoshootsomeoralloftheirfutureprojectsinthe

Commonwealth.Indeed,successfullocalactorslikeBenAffleckhaverecentlyreturnedtothe

Commonwealthtoproducefilmshere.

Independentnarrativefilmsarefinancedthroughinvestorsasopposedtothegrantsand

donationstypicallyusedindocumentaryproduction.Investorsaretypicallyattractedtoa

narrativeprojectiftheybelievetheprojectwillbefinanciallysuccessfulandtheywillreceivea

returnontheirinvestment.Becauseindependentnarrativefilmmakersdonottypicallyhavefiscal

sponsors,itwasnotpossibletogetthesamebroadviewofnarrativeproductionoverthepastfive

yearsaswaspossiblewithdocumentaryproduction.

Onenarrativeproducerwhomadeuseofthetaxcreditwasinterviewedforthisreport.Although

theproducerisnotfromMassachusetts,thedirectorandprimaryinvestorsare.Theystarted

raisingmoneyin2007,shottheirfilminFallRiverin2008,andcompletedpost‐productionin

2009.Thistimeframeistypicalfornarrativefilmsbecauseunlikedocumentaryfilms,the

Page 37

35

filmmakersknowthestoryaheadoftimeandcancondensetheshootingintooneconcentrated

periodoftime.Itisworthnotingthatthismakesiteasierfornarrativefilmmakerstotake

advantageofthetaxcredit,becausetheytypicallyknowwhich12‐monthperiodwillbethe

biggestspendingperiod.Incontrast,documentaryfilmmakersoftendonotknowwhatthe

biggestspendingperiodwasuntilafterthefilmiscomplete.Onthisparticularnarrativefilm,they

receivedthecreditbeforethepost‐productionwascompleteandappliedthemoneytowards

finishingpost‐production.Thefilmmakersarecurrentlylookingfordistribution,andhopeto

recouptheircostsandmakeaprofit.

Theproducerreportedthatthelargestspendingcategorywaswagesforcastandcrew.About

halfofthecastandcrewwerefromMAandtheotherhalfwerefromout‐of‐state,primarilyNew

YorkandLA.Anothermajorcategoryofspendingwasfilmandcameragear.Unlikeindependent

documentaries,whichareoftenshotonvideo,thisfilmwasshoton35mmfilm,asignificantly

moreexpensiveformat.Thesecostsaccountedforaboutafifthoftheoverallbudget.Thismoney

wasspentoutofstatebecausetheycouldnotfindtheequipmentorfilmstockinMA.Other

significantcostsincludedlocationfeesandcatering,whichwereallspentinstate,andpost‐

production,whichwasdoneprimarilyinLA.Theproducerestimatedthatabout40%ofthe

overallbudgetwasspentinMA.

Itseemsthetaxcredithasnotyetimpactedtheindependentdocumentaryandnarrativefilm

sectortothesamedegreeithasimpactedstudiofeatures.Forexample,seventeenfeaturefilms

wereproducedin2008,ascomparedtoanaverageof2‐4inyearspriortothetaxcreditprogram.

Incontrast,theoverallnumberofactiveprojectsreportedbythefiscalsponsorshipsorganizations

hasnotincreasedsignificantlysince2005.Itisdifficulttomeasuretheimpactoftheprogram

againstthefundingissuesfacedintheindependentsector.Thescarcityoffundslimitsthe

amountofprojectsmadeinthestate.Asthereappearstobefiercecompetitionforcurrentfunds,

ifthereweremorefundingthesectorwouldmostlikelygrow.

Itisworthnotingthatthetaxcreditmayimpacttheindependentsectorinsomeindirectways.

First,theincreaseinmajorstudioproductionshasenabledsomeofthelocalcrewbaseto

continuetoliveandworkinMA.Ifthesefilmshadnotbeenmadesomelocalcrewmighthave

Page 38

36

movedelsewhereinsearchofemployment.Oneproducerwhohasworkedonbothfeatureand

independentprojectsnoted:

“Inaverysimplisticsense,arisingtidedoesraiseallboats,asdoesthe

developmentofamoreexperiencedcrewbase.Anygeographicalregionthatis

experiencinganincreaseofactivitywillalsogeneratemoreinterestinindependent

projects.Thecrewgoestoalmostanyprojectaslongasthereappearstobesome

actualfinancialbasisandifitfitsintotheirownpersonalschedules.”

Additionally,thestudioinfrastructurethatisbeingproposedtoaccommodatemorefeaturefilms

mightalsobenefittheindependentsector.Severallargesoundstudiosarecurrentlyproposedin

MA.Onefiscalsponsorcommentedonapotentialbenefitofthesestudiostotheindependent

community:

“Forinstance,theymightgivereallygooddealstoindependentssothat

independentscouldactuallyaffordtousesomeofthestudiosfortheirown

projectsanditmightincentivizethemtoactuallyshootsomethinghereversus

goingtoNewYorkortheymightrealizethatsomeprojectisdoablebecause

whateverservicestheyneedareinMA.”

Ifmoreeffortwereplacedoninformingfilmmakersaboutthetaxcreditandmakingthefiling

processeasier,moreindependentanddocumentaryfilmmakersmighttakeadvantageofit.One

filmmakernoted:

“Mysenseisthat…alotofindependentfilmmakersandmyselfincludeddosomuch

onourfilmsthatit’slikepeoplejustdon’tknowalotaboutthat[thetaxcredits].

Theydon’tknowhowitworks.Theydon’tknowtheinsandouts,somebodyhas

beenthroughitbutit’sbeenreallyconfusingandthentheywererejectedandyou

don’tunderstandwhy.Youknowitjustseemsreallyforeignstill.”

ItisdifficulttospeculateonthefutureofindependentfilmmakinginMA.Thebiggest

determinateofitssuccessisfunding.ItappearsthatMAhasthecrewbaseand

infrastructuretosupportasignificantincreaseinindependentfilmproduction,butit

remainsunclearwherethefundingfortheseprojectswillcomefrom.

Page 39

37

Postproductionandspecialeffects:Theincreaseinmotionpictureproductionhashadapositive

spillovereffectinlocalpost‐productionandspecialeffects.Onenotableexamplehasbeenthe

expansionofBrickyardVFX.FoundedbyMassachusettsnativeandEmersonCollegegraduate,

DaveWaller,the16‐personorganizationisnowoneofthepremiervisualeffectsstudiosinNew

England.Brickyardbeganasaone‐manshopin1999andspecializedinvisualeffectsfortelevision

commercials.In2007,duetoanupsurgeofwork,thepartnerscreatedanewcompanycalled

BrickyardFilmworkscateringtothevisualeffectsneedsoffeaturefilms.ThenewFilmworks

companyenjoyedrapidgrowthandby2009hadtwentypeopleonstaffandcompletedhundreds

ofeffectsforfeaturefilmslike“TheProposal”and“Surrogates.”

Confirmingreportsfromothertelevisionandpost‐productioncompanies,employmentat

BrickyardalsodrewheavilyfromgraduatesoflocalcollegeslikeEmersonCollege,Boston

University,FitchburgState,andtheMassachusettsCollegeofArt.Inadditiontothesenew

entrants,Brickyardfoundthatitalsoneededindustryveteranstohelpkeepupwithincreasing

demandandrecruitedformerMassachusettsresidentswhohadmovedtoCaliforniaandagreed

tomovebacktoMassachusettstoworkatBrickyard.WhileBrickyard’sfeaturefilmworkhasbeen

growing,2008and2009werethefirstyearsthattelevisioncommercialrevenuesshoweddeclines

sincethecompany'sfoundinganditfacedtheprospectoflayoffs.However,bysharingthetax

creditsonseveralprojectswiththeirclients,theywereabletoobtainadditionalworkleadingto

thehiringofthreeemployeesalongwithassociatedworkstationsandequipment.Inthis,and

manyothercases,industryrepresentativesdescribehowthetaxcredithashelpedthemprevent

layoffs,obtainnewwork,andengageinnewhiringandequipmentpurchasingduringaperiod

witharapidlycontractingregionalandnationaleconomy.

Othercompaniesinthissectorhavereportedsimilarstories.NationalBostonStudiosbegana

relationshipwithSonyPicturesbypreparingthefirstHDVideoDailiesforthefilm"21"whichwas

shotmostlyinMassachusetts.SinceHDDailieswerealeadingedgestepinthedigitalworkflowat

thattime,NationalBostondevelopedanefficientprocessreplicatingthesameoperational

systemsusedforcreatingtraditionalfilmdailies.ThecompanyworkedwithEvertzofOntario

CanadatobuildspecialtyequipmentthatwasinstalledatNationalBoston’sStudiostohandlethe

processingofthesedigitaldailies.TheseHDvideodailieswereproducedovernightandthensent

Page 40

38

viafiberopticcableusingproprietaryinternetsoftwaretoCulverCitywhereDVD'swerethen

producedforviewingbystudioexecutives.ThetaxcreditencouragedSonytoworkwithNational

Bostontodevelopatechnologicalsystemandworkflowthathadneverbeenusedbefore.In

2008,NationalBostonproducedseveralcommercials,televisionpilotsandmediaprojectsthat

allowedthemtotakeadvantageofthetaxcredits.AstheydidforBrickyard,thecreditshelped

NationalBostonavoidstaffandproductioncutsduringadifficulteconomicperiod.

Post‐productiontechnologyisalsodriveninlargepartbychangesininformationtechnology,and

theCommonwealthhasalongstandingstrengthininformationtechnologyrelatedtothefilmand

televisionindustry.MassachusettsisthehomeofAvidTechnologyInc.,whichisoneoftheglobal

leadersineditinghardwareandsoftwarefortelevisionandfilmproduction.Avidaloneemploys

2,350peopleandgenerated$845Minsalesin2008.However,becauseAvidislistedintheNAICS

codeforPhotographicandPhotocopyingEquipmentManufacturing(333315),itdoesnotappear

indataonfilmandtelevisionemploymentintheCommonwealth.Moreover,becauseitisnot

monetizingtaxcredits,itwouldnotbeincludedinanyanalysisoftherevenueimpactsoftheFTC.

GenArts,aCambridgebaseddeveloperofFXsoftware,recentlyattractedventurecapital

investmentandacquiredaleadingUKbasedFXtechnologydeveloper.Thecombinedpresenceof

AvidTechnologies,smallspecialeffectssoftwaredevelopers,digitalgamingcompaniesand

leadingresearchlabsinartificialintelligenceandemergingmedia(especiallyatMIT)could

representapowerfulsetoffuturesynergies.

Education:Withitsconcentrationofuniversities,Bostonisanimportantcenterforstudents

studyingtheproductionoffilm,televisionandothermedia.TheMassachusettsCollegeofArtand

Design,EmersonCollege,BostonUniversity,FitchburgState,CurryCollegeandBentleyUniversity

allhavefilmandtelevisionprograms,someofwhichareimportantfeederschoolsforLosAngeles

andNewYorktelevisionandfilmcompanies.BostonUniversityalonehasover1,000students

enrolledinCommunicationsandFilmandTelevisionprogramsandin2009graduatedalmost300

studentsfromtheseprograms.Manyotherlocalschoolsalsohavedrama,film,andtelevision

coursesandgeneratemanyyounglocalemployeesseekingjobs.

Page 41

39

Untilrecently,graduatesoftheseprogramstypicallyfacedthechoiceofleavingMassachusettsor

givinguponacareerinthefilmindustry.Officialsassociatedwiththeseprogramsandother

industryrepresentativesreportthatalumniwhohadleftforLosAngelesandNewYorkhave

recentlyreturnedtoBoston,sinceitisnowpossibleforthemtoworkinthefilmindustryhere.

Moreover,asnotedabove,localproductioncompaniesareemployinganincreasingnumberof

thesestudentsasinternsandprovidingcareeradvancementopportunitiesforMassachusetts’s

collegegraduates.Inadditiontoprovidingalocalworkforcefortheindustry,theseprogramsalso

provideemploymentforthemanyseniormembersofthelocalfilmandtelevisionindustrywho

teachinthem.Industryrepresentativesdescribedtheseeducationalresourcesasuniquestrategic

advantagesforMassachusetts.

Careeropportunitiesforlocalgraduatesseemparticularlypromisinginnon‐fictiontelevision

productionthattendstohavemanyopeningsfornewentrants(e.g.,productionassistants,

assistanteditorsandresearchers).Moreover,thejobstendtolastlongerthanwithfeaturefilms,

becausetheproductioncycleislonger.Therearenumerousexamplesoflocaluniversityprograms

providingbothinternsandnewentrantstolocaltelevisionandpost‐productioncompanies.Ifthis

trendcontinues,itseemspossiblethatthiscouldinturngeneratepositivefeedbackloopsbothby

reducingwageleakagefromlocalfilmandtelevisionspendingwhilebuildingnewcareerpathsfor

Massachusettscreativeworkers.

Equipmentrentalandspecializedservicefirms:Thegeneraltrendinthispartoftheindustryhas

beeninvestmentbylocalfirmstoexpandtheirinventoryofequipmentandexpansionintothe

Commonwealthbyrecognizednationalfirms.Localgripandelectriccompanieshaveexpanded

theirofferings,andseveralnationalfirmshaveopenedMassachusetts’soffices.Therecentmerger

oftwolocalequipmentrentalfirms,RuleandBostonCamera,hascreatedaMassachusettsbased

firmthatpossessesthescaletoservelargestudioproductions.Anationalcateringfirm,HatTrick,

hasopenedanofficeinMassachusetts,fillingasignificantgapinthelocalindustry’scapabilities.In