GROUP MEMBERS : Reg# HOSH MOHAMMAD (MBA) 4581 PSO SHELL MUHAMMAD FAROOQ (BBA) 3610 BYCO HAFEEZ-U-RAHMAN (MBA) 4469 ATTOCKSubmitted to:SIR IMTIAZ ASKARIHOSH MOHAMMAD (MBA) 0342-3802305Comparative Analysis of Petroleum Industry in Pakistan Analysis of Financial statements CID:9301

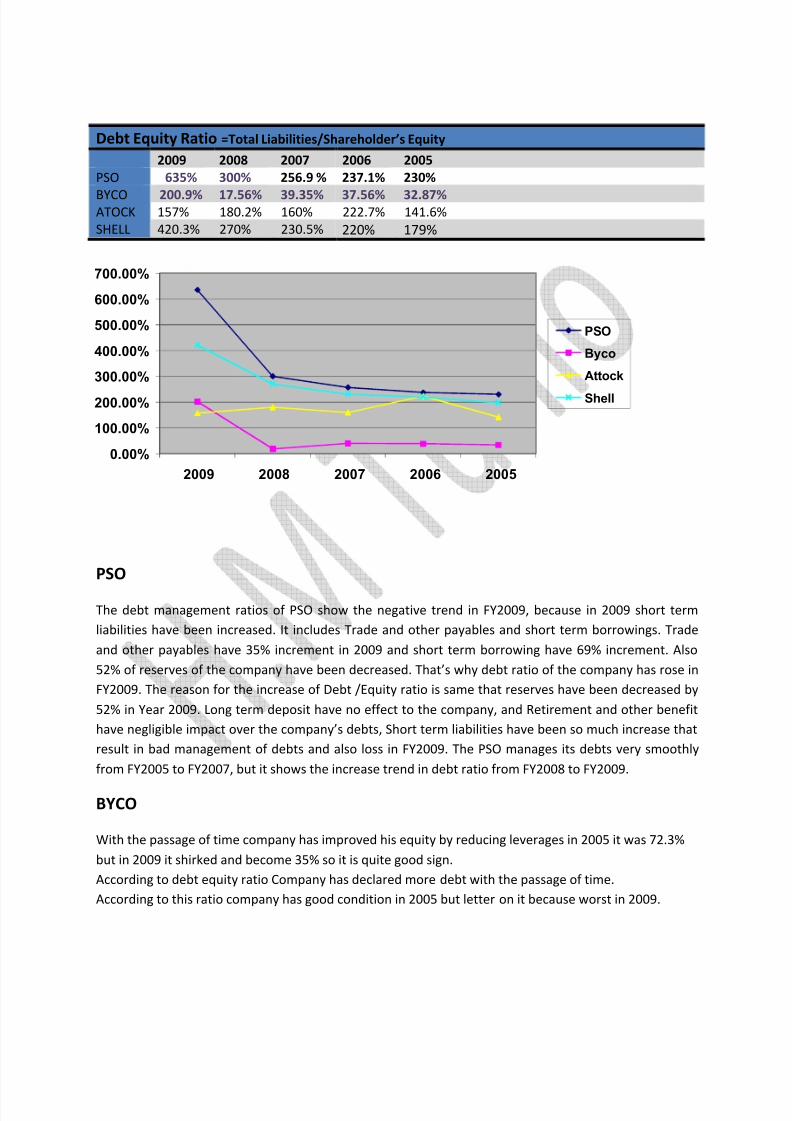

The debt management ratios of ATTOCK show the decreasing trend in FY2009, because in 2009 short

term liabilities have been increased and in 2009 and in 2005 the debt ratio is higher because currentassets are low. It includes Trade and other payables and short term borrowings The debt equity holderdecreases in 2009 because equity has been increased more as compared to the liabilities. The havemaximum amount of equity and the debt cost is negligible.

SHELL

In debt ratio company has been inefficient. Specially in 2009 the debt ratio was on its peek. Bydoing analysis we came to know that In 2005 debt ratio was 55.4% as a time goes on debt ratiohas increased at stable rate.

In debt equity ratio company again has been failed to achieve good performance, indebt/equity ratio company has negative trend and with the passage of time this negativeperformance has increased.

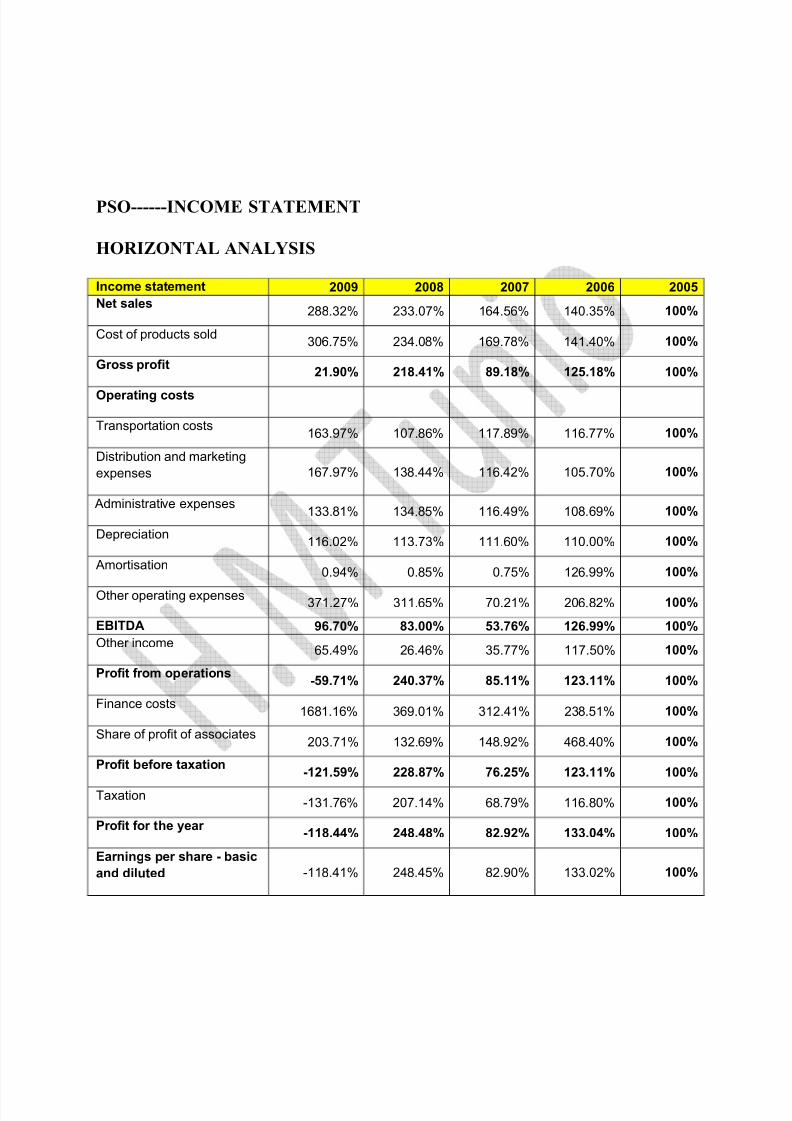

PSO facing declining in profit an FY2009, it is due to increase in cost of good sold, the cost of goods sold

increase by 31.04% as compare to FY2008, it is the main reason that company incurs loss in FY2009,however net sales also increased by 23.7%, but it is not enough to grow profit margin, company shouldtry to decrease the CGS as well as increase in sales. In 2008 CGS increased by 37.9%, but sales increasedby 42%, that results in increment of 45% in Gross profit. FY2008 seems to be in good position in whichGross profit margin is 5.1%. However FY2007 is less profitable due to increase in CGS.

BYCO

In 2009 company has shown loss in gross profit margin, so one can say that financial health of thecompany is not so good and in the future company will be unable to pay its operating and other

expenses.

ATTOCK

T he gross profit margin increase every year. Because the company increase their sale and thisincrement is due to high prices of petroleum products.

SHELL

As for as Gross profit is concerned company has increased its performance, although in 2006Gross profit ratio has decreased but latter on company recover the loss and increased its ratio

so we can say that this is the quite good sign for the company.

Net Profit M argin = Net Income before minority share of Earnings and Non Recurring Items /Net Sales

The profitability of the PSO fell by 48% in FY2009. Although the sales of the company increased, but dueto increased in CGS, company face loss, that result in negative ROA in FY2009, overall ROA of the PSO isvery stable, except FY2007 which is due to less profit in 2007.

BYCO

In 2009 company has shown loss, and in 2007 company also incurred loss, than in remaining yearscompany has earned profit, but not as much as other companies.In 2009 company has incurred heavy loss and 2008 was quite good. We can say that company hasearned on their assets, but in 2007 again company got the loss, so we can say that company is ininefficient to get the return on assets.

ATTOCK

The net profit rate of FY2009 is 4.98% and FY2008 4.96%. The net profit margin ratio approximatelysame in FY2009,2008,2005 but in 2007 and 2006 net profit margin go down because their expenseshave been increased in 2007 and 2006.

ROA in FY 2006 is higher and continuously decreasing till 2009. It mean the company don t have abilityto used the assets efficiently and don t earn a handsome return on from the sources available to thecompany

SHELLAs for as Net Profit margin is concerned company has not been good in performance, it hasdecreased the net profit margin continuously, and 2009 net profit margin has been shrieked to1.5% so we can say its not a favorable for company.

In 2005 Return on Asset were 11.03% it means company has earned quit well on their Assets, but in thesecond year 2006 company incurred loss. Then again in the next year company recovered itself andshowed a good sign till 2009.

Price/Earning ratio =M arket price per share/earning per share

2009 2008 2007 2006 2005PSO (5.47) times 5.1 times 14.3 times 7.0 times 11.6 timesBYCO (0.31) times 250 times (4.46) 11.25 times 14.58 timesATOCK 5.94 times 9.43 times 13.92 times 9.28 times 13.73 times SHELL 9.1 times 8.5 times 31.8 times 8.4 times 9.9 times

PSO

Return on Equity is most valuable profitability ratio, Return on equity reveals how much profit acompany earned in comparison to the total amount of shareholder equity found on the balance sheet,PSO has loss in 2009 so ROE is in negative trend, the best year for PSO in regard of ROE is FY2008, in thisyear Net is higher than previous years, and in FY2007 due to less income it is less ROE, in 2006-5 is in astable position.

A leverage ratio summarizing the affect a particular amount of financial leverage has on a company'searnings per share (EPS). The higher the degree of financial leverage, the more volatile EPS will be.

This ratio can be used to help determine the most appropriate level of financial leverage to use toachieve that goal. The company s P/E ratio is in increasing trend from 2005 to 2008, but due to loss in2009 it becomes in negative. Although EPS in FY2008 is about 81.9 and Market share price at year end isRs 417.2 which is highest rate as compare to previous years, it reduces the P/E Ratio of the company,P/E ratio of the company is fluctuating during 2005 to 2009. In 2007 due to less profit and highEarning/Share.

BYCO

In 2005 the company has 1.66 leverage o earning ratio, but with the passage of time it showed negativetrend because leverage on earning ratio has increased. In 2009 it got the highest position of worth10.5%.

If we will take a sigh of P/E ratio that we can analyze that company has earned more profit, but it is alsofact that company has shown loss in FY2009 and FY2007 as well and rest of the years company hasshown stable profit.

ROE in FY 2006 is higher and continuously decreasing till 2009. It mean the company don t have abilityto used the assets efficiently and don t earn a handsome return on from the sources available to thecompany

The financial leverage in FY 2006 is higher it mean in 2006 the company is more risky. In FY2009 and FY2005 the degree of financial leverage is low and the risk factor is also low in these years.

Theoretically, a stock's P/E tells us how much investor are willing to pay per dollar of earning. P/E ratiosare generally lower during times of high inflation

Price earing ratio is higher in FY 2005 and FY 2007 but in FY 2009 it is decrease due to low market priceof shares of the company. And high value of EPS.

Price earning ratio fluctuate every year because there is a high change in market price therefore P ratiofluctuate in FY 2007 and 2005 the company is more stable because P ratio is higher in these years

SHELL

In 2005 company had 1.8% leverage on Earning/Share it directly affected the earning but latteron leverage on per share has decreased so we can say company showed a good performance.In 2005 P/E ratio was so good but latter on company has shown decreasing trend till 2008, then againcompany has earned good profit.

In FY2009 loss incurred to the company , the investors had got nothing from company. In FY2008 theROE is highest which shows the better sign for company and it also shows maximization of profitcompare to other years, this is because of Highest sale in 2005 to 2008 which result in good Assetturnover, it means company utilized its assets in a efficient way.

BYCO

In 2009 BYCO didn t utilized its assets in efficient way, because sales decreased in that year. But in 2008it seems to be profitable but still company has many problems to become profitable. Because companyfailed to earn profit in two year, company s ability to run in long term seems to be not possible.

ATTOCK

If a company's ROE goes up due to an increase in the net profit margin or asset turnover, this is a verypositive sign for the company. InFY2006 the value is high and in FY 2009 it decreased it means that thecompany don t use its assets effectively.

SHELL

ROE of shell shows the decreasing trend, however these rates are fluctuating year by year. Company snet income margin (which is due to increase in operating expenses) is very low in each year that s why itmakes the company in downward trend.

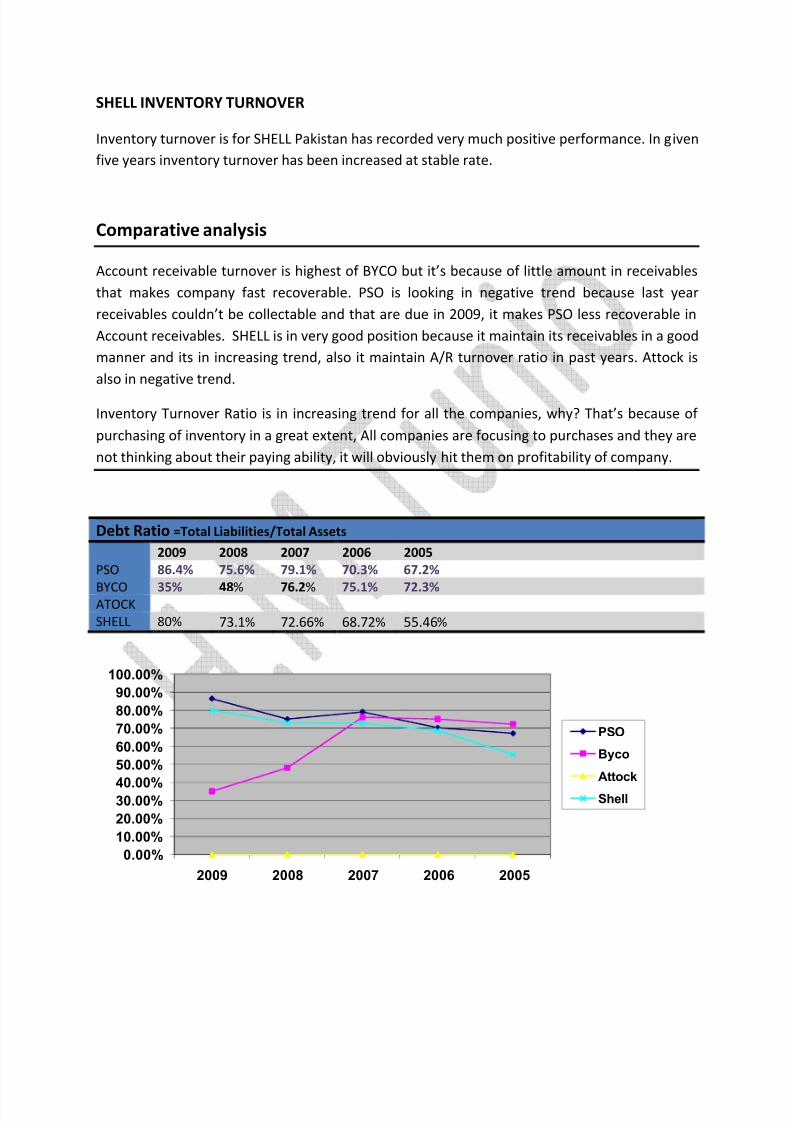

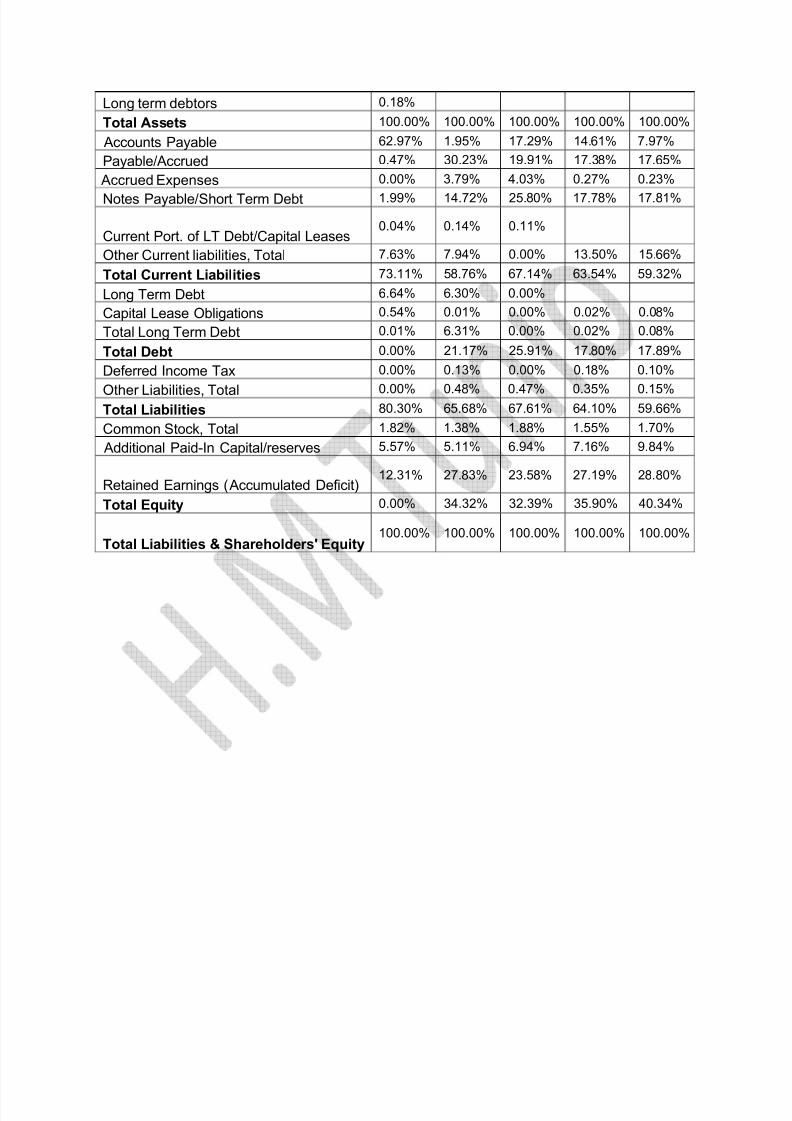

Comparative analysis of Profitability and Debt ratio

Debt Ratio of all the firms are in increasing trend, its main reason is that they borrow shortterm loans without interest and they want to take benefit of it that s why companies haveincreasing debt ratio.

When we see the gross profit of the firms; PSO has very low gross profit margin and BYCO hasloss, that is result of High amount of CGS, but ATTOCK and SHELL has a good position in GrossProfit, ATTOCK is seems to be a very good in Gross profit ratio and ROA as compare to othercompanies, that is because the ATTOCK is a small company as compare to PSO and SHELL sothat it seems to be very effective in Gross profit and ROA; for example if ATTOCK gross profit is1000 on sale of Rs. 10000 it will show the margin of 10% that is a good margin for ATTOCK but itwill be no more good for other companies, so we can not compare ATTOCK s GP ratio on othercompanies.

Net Profit margin shows that PSO and BYCO companies are in Loss and reason is described atmany positions, But ATTOCK and SHELL are in Profit. However Shell has low Net income marginwhich is because of increase in Operating expenses, Shell need to control its operatingexpenses, but still its in a good position because overall industry is going in loss and Shell runs inprofit.

Return on Equity of Petroleum Firms seems to be 2:2 ratio, it means that 2 companies earnedprofit in FY2009 and 2 got Losses. But it can not be decided on the basis of ROE that thecompanies who had losses can not run in Long term. PSO is a very stable and profitable in

previous years but due to high Raw material cost it run in Loss, that doesn t mean that PSO willbe liquidify, PSO is in a very strong position, its debt paying ability is very good, and it can run inLong Term relationship with its investors, The BYCO is really in trouble, because it had incurlosses two times within 5 years. And its debt paying ability is also not in a good position, itsamount of Profit is also very low.

ATTOCK has maintained its ROE in a good manner, however it is also in downtrend in FY2009but it is quit possible for Firm to keep it high in next year.

Shell has increasing trend in ROE, that is sign of good move in market, Shell Pakistan is runningin profit and it maintained its sales and Assets very efficiently, although FY2009 is not good formost of the Oil companies but Shell Pakistan proved itself as a stable company, Return onAssets of Shell is in increasing trend which means the company is utilizing its assets veryeffectively.

We can not say that a Single firm has a best performance in this industry, because PSO is alargest petroleum company in the Pakistan and it has 72% market share. However it incurred

loss in 2009 but it does not mean that It will not cover it in next year, the Firm has a best debtpaying ability, and a it has good control over Receivables and inventory as compare to others.

Although this time Shell is seems to be good profitable in Financial statements.

Changes in Cost, Sale and Gross Profit PSO =====Change in Sale, CGS, and Gross Profit

Sales Volume: Per Year (given)

2009: 92.4 million barrel 2008: 91 million barrel 2007: 82.6 million barrel 2006: 68.6 million barrel 2005: 67.9 million barrel

Change inCost/barrel

CGS (Rs.000)(A)

Barrels sold(B)

Per Barrel costA/B

Change withinyear

2009 609685478 92. 4 m 6598 14682008 465254907 91 m 5112 10272007 337446896 82.6 m 4085 (-12)2006 281042813 68.6 m 4097 11702005 212503650 67.9 m 3129 -

Change inSale/barrel

Sales (Rs.000)(A)

Barrels sold(B)

Per Barrel SalepriceA/B (Rs.)

Change withinyear

2009 612695589 92. 4 m 6631 11892008 495278533 91 m 5442 12082007 349706326 82.6 m 4233 (114)2006 298250039 68.6 m 4348 12192005 198757319 67.9 m 2927 -

In FY2009 company faced loss of Rs. (9966) millions. Why Company faced this Loss?

However the sale volume increased in a great extent but CGS also increased, company could not controlits cost, In 2009 Cost/barrel of Oil was Rs. 6598 with increase of Rs. 1468, it s a very big amount and insale price there is of only deference of Rs.33, its not sufficient to earn profit, the increase in CGS was theresult of increase the Cost in Purchases in FY2009, the deference between 2009-2008 purchases is about644, that result in loss to the company. In 2008 Cost/barrel also increased but the Sale price/barrel wasalso increased by Rs.330. it is a good amount to increase profitability, the purchases amount alsoincreased at a great extent in FY2008 but Prices were so high that makes company profitable. In FY2007company reduces Rs.12 in cost of goods sold, that was actually because of low prices of Oil inInternational Market.

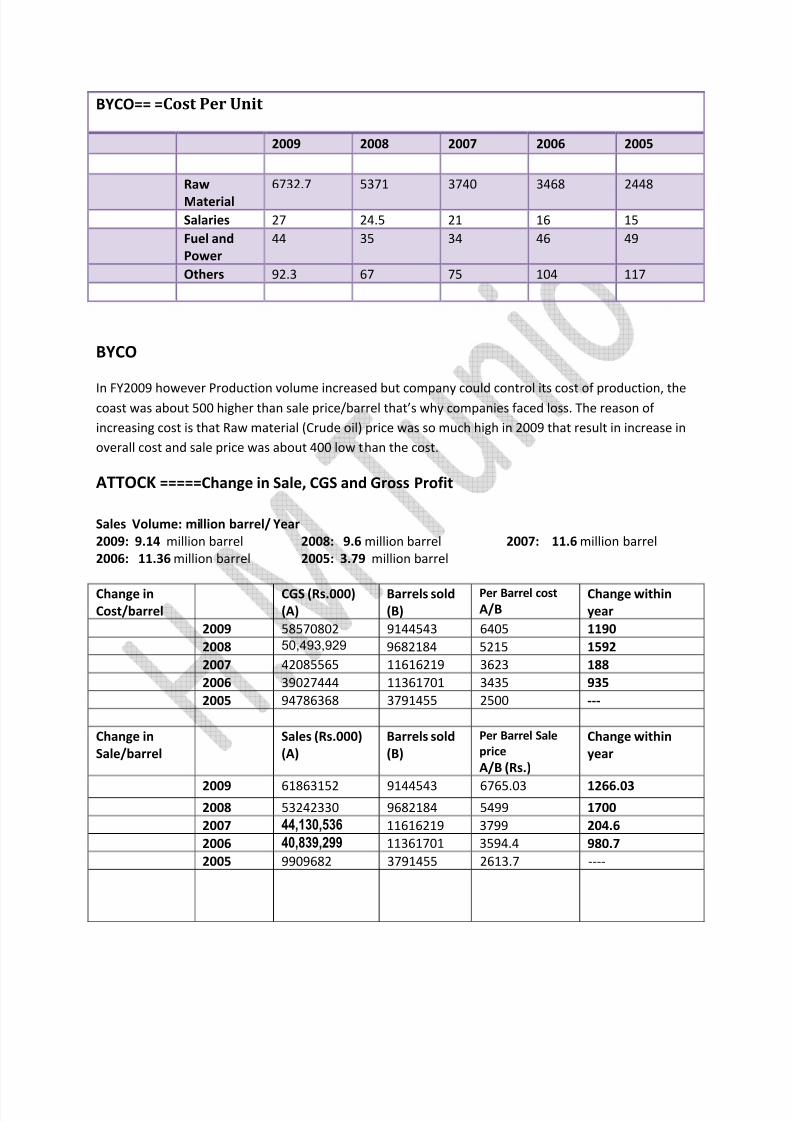

BYCO====Change in Sale, CGS and Gross Profit

Production Volume: million barrel/ Year2009: 7.03 million barrel 2008: 6.188 million barrel 2007: 5.06 million barrel 2006: 4.808 million barrel 2005: 3.789 million barrel

In FY2009 however Production volume increased but company could control its cost of production, thecoast was about 500 higher than sale price/barrel that s why companies faced loss. The reason of increasing cost is that Raw material (Crude oil) price was so much high in 2009 that result in increase inoverall cost and sale price was about 400 low than the cost.

ATTOCK=====Change in Sale, CGS and Gross Profit

Sales Volume: million barrel/ Year2009: 9.14 million barrel 2008: 9.6 million barrel 2007: 11.6 million barrel 2006: 11.36 million barrel 2005: 3.79 million barrel

Purchase 5898.4 5168.7 3296 2919 2225Petroleumdevelopment levy

497.4 20.9 289.8 234 175

Others 9.2 25 72 171.5 100

ATTOCK

The company sale increases in rupees in 2009 due to increase the price of the petroleum products. Butthe company sale in barrel is decrease in FY 2009 at 9.14 million barrel to 9.6 million barrel in 2008. But

in FY 2007 and 2006 the sale in barrel is higher. But the gross profit increase due to increase in prices.And gross profit ratio also increases.

Shell ====Change in CGS, Sale and Gross Profit

Sales Volume: million barrel/ Year2009: 18.09 million barrel 2008: 20.35 million barrel 2007: 19.04 million barrel 2006: 14.3 million barrel 2005: 15.4 million barrel

2009 2008 2007 2006 2005 Total Revenue 115221.51% 142.09% 11 6 .8 9% 119.14% 100%Cost of Revenue, Total 11 6 504. 8 5% 139.04% 121.1 6 % 119. 6 4% 100%Gross Profit 105688.02% 175.52% 70.32% 113.16% 100% S elling/General/Admin. Expenses, Total 5547.17% 139.40% 120.27% 11 8 .31% 100%Depreciation/Amortization 100.19% 9 8 .8 1% 8 5.42% 9 6 .88 % 100%Op e rati ng In com e 86841.21% 213.43% 29.35% 125.69% 100% Interest Expense, Net Non-Operating -345233. 6 1% 2 6 5.10% 274.9 8 % 120.2 8 % 100%Interest/Invest Income - Non-OperatingInterest Income (Exp), Net Non-

OperatingNe t In com e Be for e Tax e s 70970.22% 212.00% 10.40% 127.37% 100% Provision for Income Taxes 73972.9 8 % 21 6 .9 8 % -27.51% 125.27% 100%Ne t In com e Afte r Tax e s 695100.61% 209.58% 28.83% 128.40% 100% Diluted Normalized EP S 6 9.52% 20 8 .9 8 % 2 8 .8 3% 12 8 .40% 100%

V e rtica l An a lysis

Total Revenue 100% 100% 100% 100% 100%Cost of Revenue, Total 92.14% 8 9.17% 94.45% 91.50% 91.12%Gross Profit 7. 86 % 10.59% 5.1 6 % 8 .14% 8 .57%S elling/General/Admin. Expenses, Total 4. 8 2% 9 8 .23% 103.02% 99.42% 100.12%Depreciation/Amortization 0.00% 0.47% 0.50% 0.5 6 % 0. 68 %Op e rati ng In com e 3.04% 6 .0 6 % 1.01% 4.2 6 % 4.04%Interest Expense, Net Non-Operating 1.01% -0. 6 3% -0.79% -0.34% -0.34%Interest/Invest Income - Non-Operating 0.00% 0.15% 0.11% 0.04%Interest Income (Exp), Net Non-Operating 0.00% -0.07%

Ne t In com e Be for e Tax e s 2.2 8 % 5.52% 0.33% 3.9 6 % 3.70%Provision for Income Taxes 0.7 8 % 1. 8 5% -0.29% 1.27% 1.21%Ne t In com e Afte r Tax e s 15.02% 3. 6 7% 0. 6 1% 2. 68 % 2.49%

Cash Flow Activities 2009 2008 2007 2006 2005Cash inflow from operating activities (4828554) 4050125 3691454 1633774 5307821Net cash (outflow) from investing activities (2889) (172926) (707953) (173687) (1219568)Net cash (outflow) from financing activities 511790 (9649840) (1565507) (4104443) (3087422)Cash & Cash equivalents at end of the year (1510325) (7190672) (1418031) (2836025) (191669)

In F Y 2009 cash inflow from operation is in bad condition, its because of low recievabels turnover in 2009, thecompany was unable to recover its recievables in F Y 2009. However remaining years have positive value and seems

to be good.

Net cash flow from investing activities is in negative in F Y 2009, but its amount is so minimal that does not affect onequity, however in F Y 2009 inventory has been purchased in a big extent.

PSO has no longterm debts, it has only short term borrowings and deposits in its account, so PSO has positve valuein F Y 2009 that¶s not in good condition. Remaining years have very good outflow activities from financing.