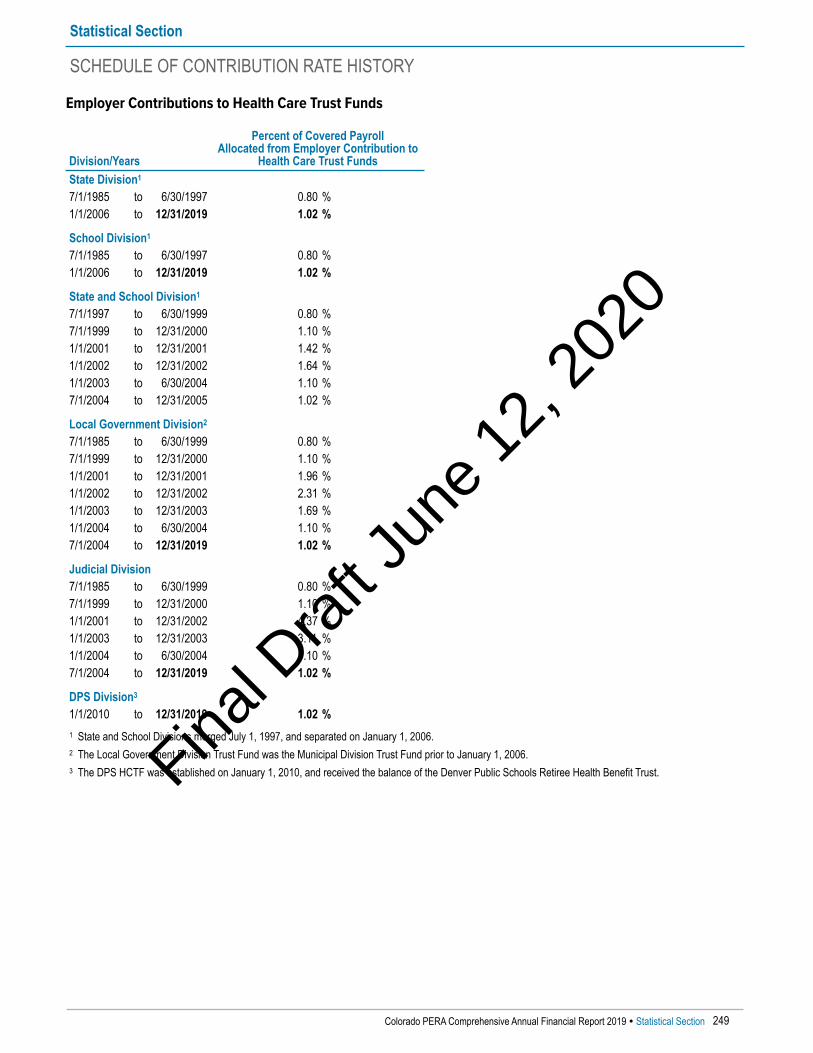

274

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

Introductory Section Financial Section (continued)

3 Letter of Transmittal Required Supplementary Information (Unaudited)—12 Professional Awards Health Care Trust Funds14 Board Chairman's Report 104 Schedule of Changes in Net OPEB Liability16 Report of the Colorado PERA Audit Committee 106 Schedule of Net OPEB Liability18 Board of Trustees 107 Schedule of Contributions from Employers and Other20 Administrative Organizational Chart and Executive Management Contributing Entities21 Consultants 108 Schedule of Investment Returns

109 Notes to the Required Supplementary Information (Unaudited) -Financial Section Health Care Trust Funds

109 Note 1—Significant Changes in Plan Provisions Affecting25 Report of the Independent Auditor Trends in Actuarial Information29 Management's Discussion and Analysis (Unaudited) 109 Note 2—Significant Changes in Assumptions or Other Inputs

Affecting Trends in Actuarial InformationBasic Financial Statements 112 Note 3—Methods and Assumptions Used in Calculations of ADCFund Financial Statements

44 Statements of Fiduciary Net Position Supplementary Schedules46 Statements of Changes in Fiduciary Net Position 114 Schedule of Administrative Expenses48 Notes to the Financial Statements 116 Schedule of Other Additions48 Note 1—Plan Description 116 Schedule of Other Deductions58 Note 2—Summary of Significant Accounting Policies 117 Schedule of Investment Expenses59 Note 3—Interfund Transfers and Balances 117 Schedule of Payments to Consultants60 Note 4—Contributions64 Note 5—Investments Investment Section74 Note 6—Derivative Instruments Defined Benefit Plans74 Note 7—Commitments and Contingencies 121 Introduction75 Note 8—Voluntary Investment Program, Defined Contribution 121 Report on Investment Activity

Retirement Plan, and Deferred Compensation Plan 123 Investment Brokers/Advisers (Internally Managed Assets)77 Note 9—Health Care Trust Funds-Defined Benefit Health 123 Schedule of Commissions

Care Plans 124 Schedule of Investment Expenses80 Note 10—Net Pension Liability of the Division Trust Funds 124 Schedule of Internal and External Asset Management83 Note 11—Net OPEB Liability of the Health Care Trust Funds 125 Schedule of Investment Income and Expense by Asset Class86 Note 12—Subsequent Events 125 Schedule of Private Market Investment Contributions,

Distributions, and Paid Carried InterestRequired Supplementary Information (Unaudited)— 126 Investment SummaryDivision Trust Funds 127 Schedule of Investment Results

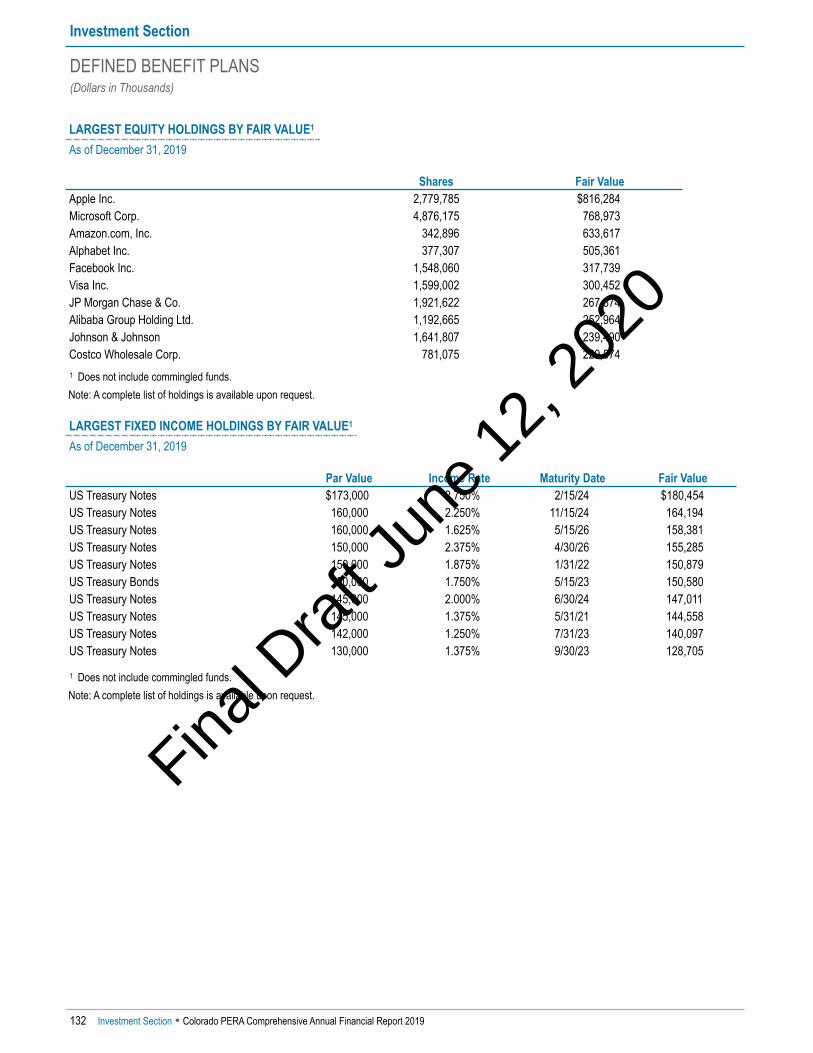

88 Schedule of Changes in Net Pension Liability 129 Fund Performance Evaluation93 Schedule of Net Pension Liability 131 Profile of Investments in Colorado96 Schedule of Employer and Nonemployer Contributions 132 Largest Equity Holdings by Fair Value98 Schedule of Investment Returns 132 Largest Fixed Income Holdings by Fair Value99 Notes to the Required Supplementary Information (Unaudited) -

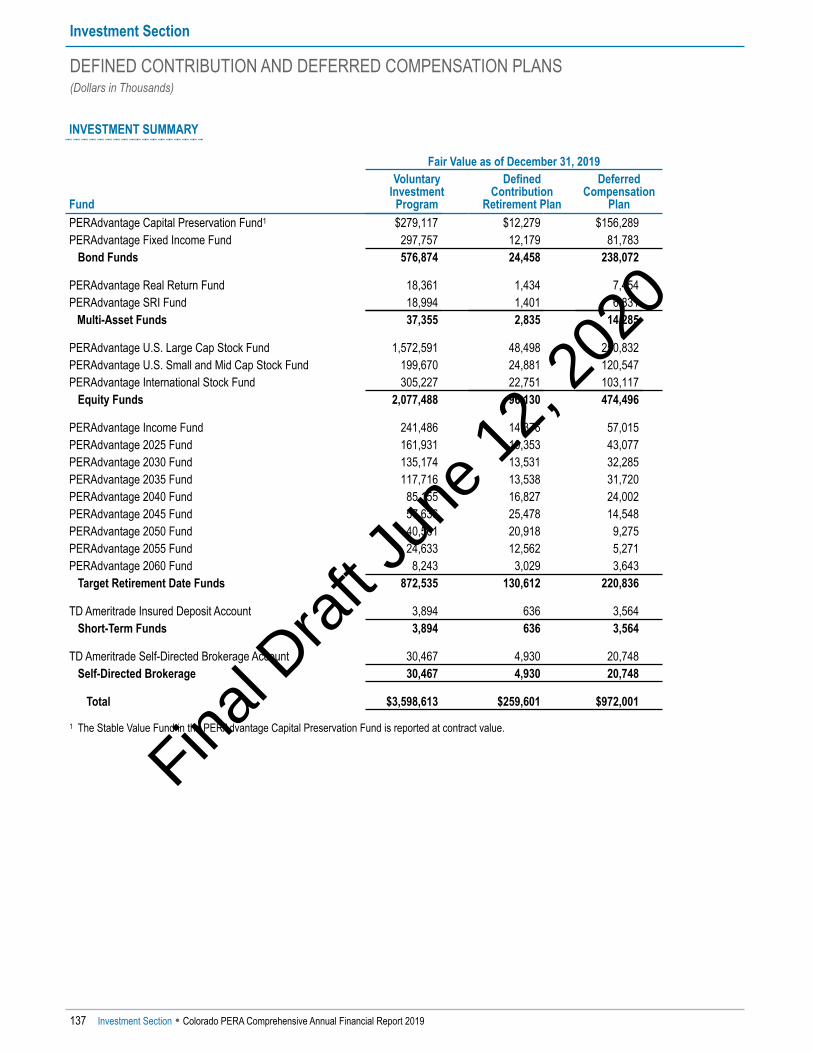

Division Trust Funds Defined Contribution and Deferred Compensation Plans99 Note 1—Significant Changes in Plan Provisions Affecting 133 Report on Investment Activity

Trends in Actuarial Information 136 Schedule of Investment Results100 Note 2—Significant Changes in Assumptions or Other Inputs 137 Investment Summary

Affecting Trends in Actuarial Information103 Note 3—Methods and Assumptions Used in Calculations of ADC

Table of Contents

Final D

raft

June

12,

202

0

Actuarial Section Statistical Section

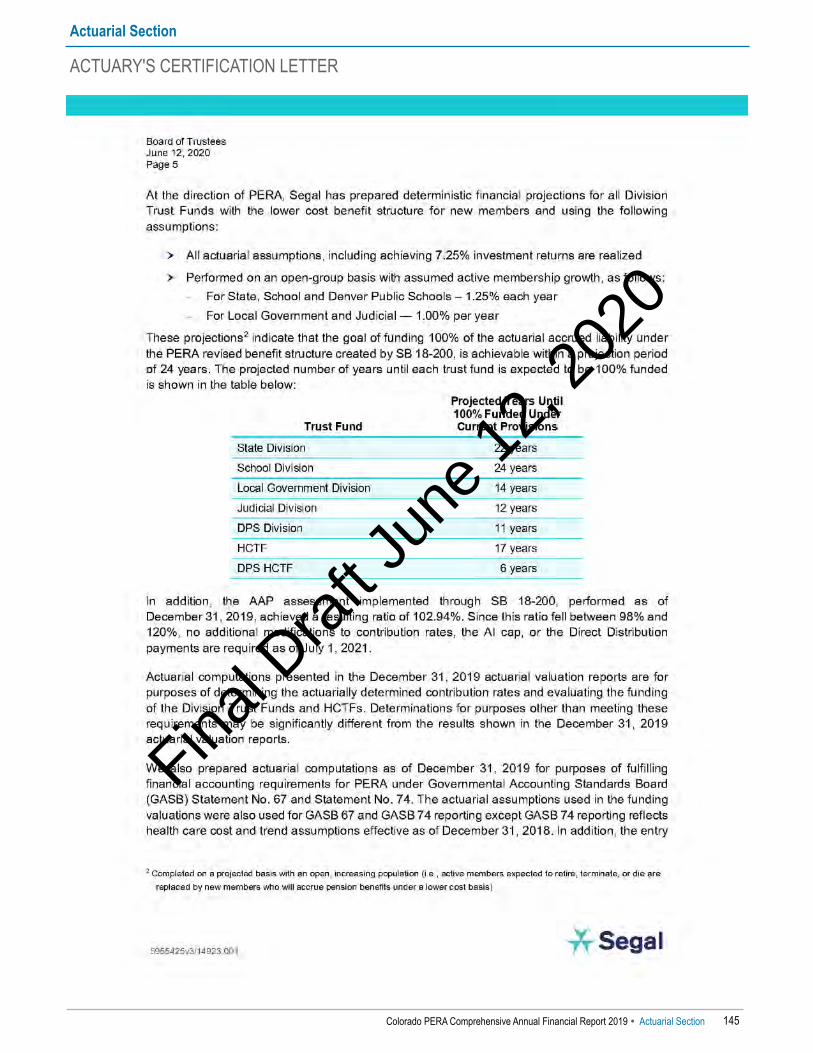

141 Actuary's Certification Letter 207 Overview208 Changes in Fiduciary Net Position

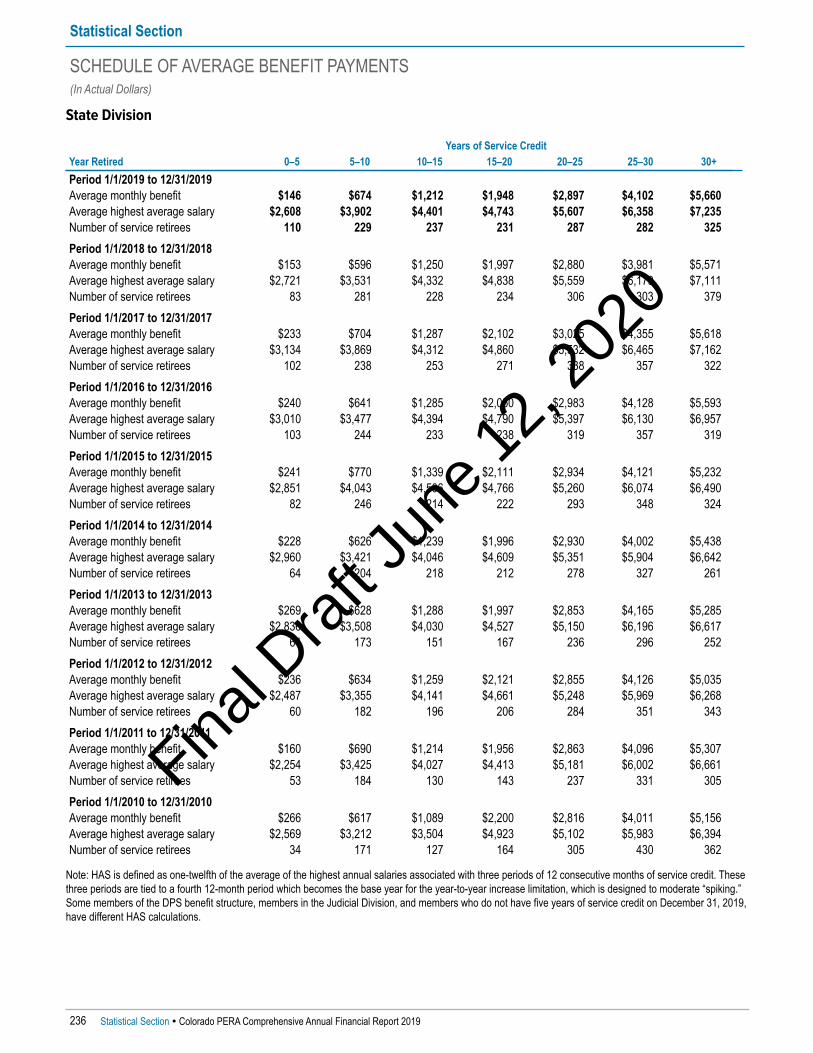

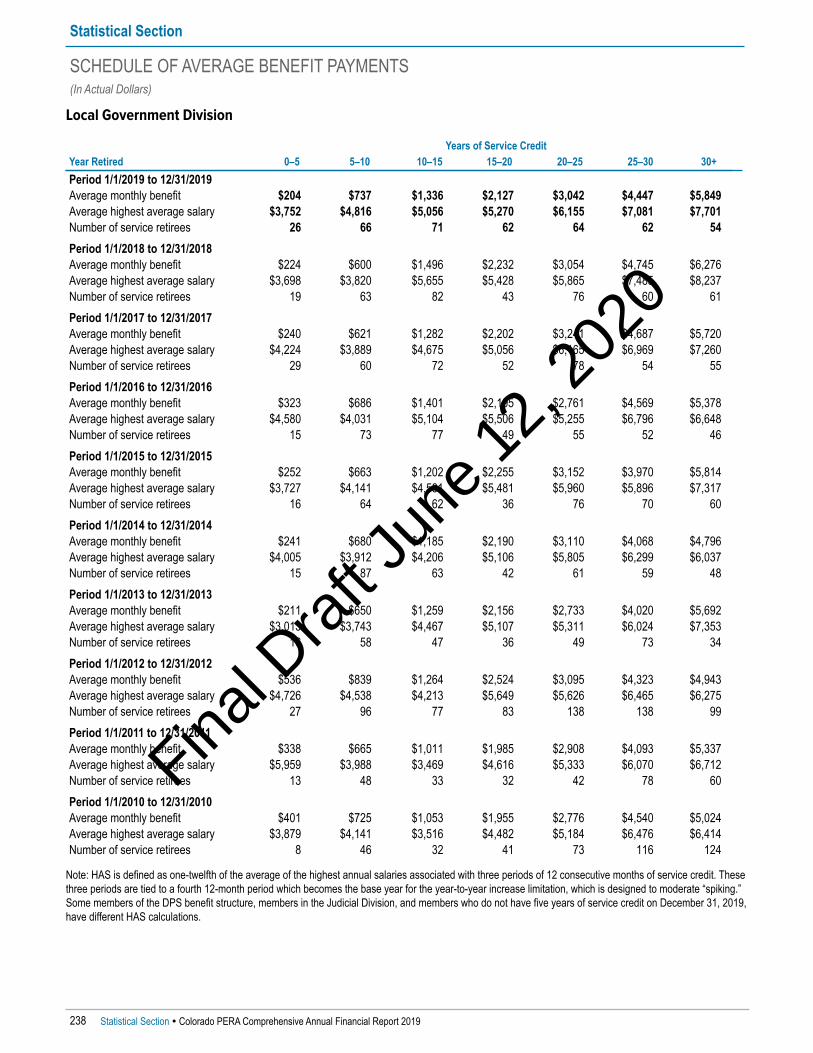

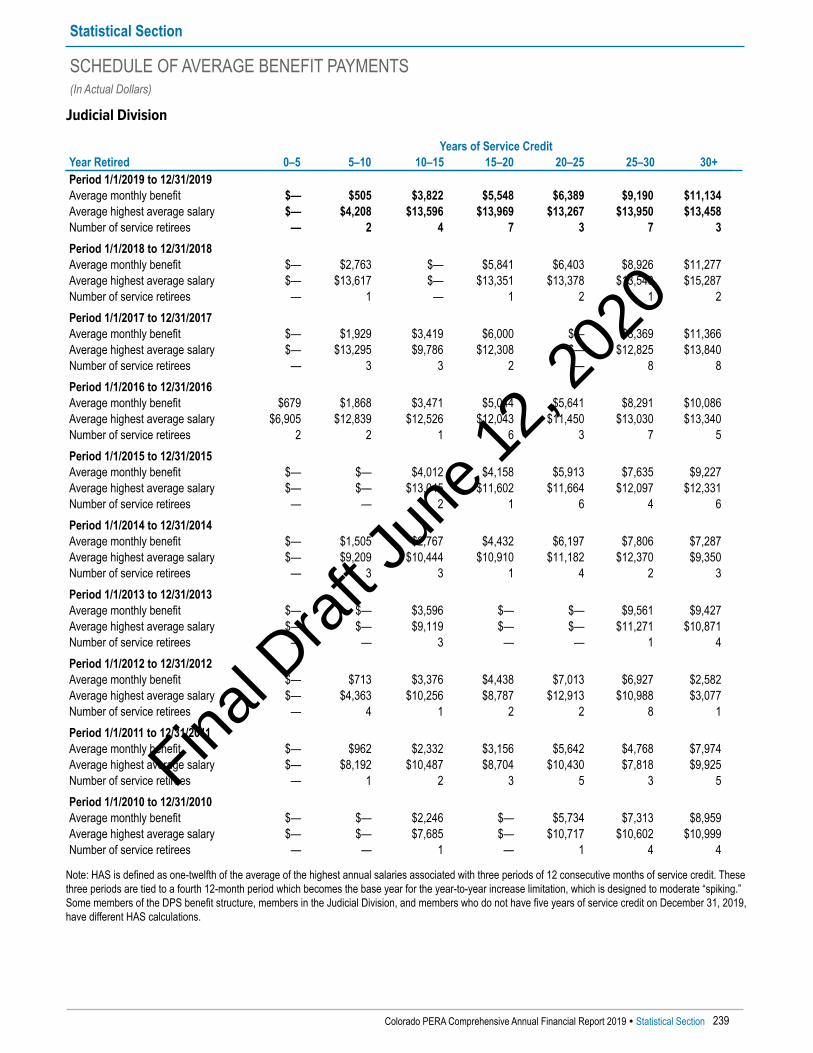

Division Trust Funds—Pension 219 Benefits and Refund Deductions From Fiduciary Net147 Actuarial Topics Position by Type155 Actuarial Assumptions: Exhibits A-I 224 Member and Benefit Recipient Statistics161 Summary of Funding Progress 225 Breakdown of Membership by Percentage161 Solvency Test 226 Schedule of Average Retirement Benefits Payable–All164 Unfunded Actuarial Accrued Liability Division Trust Funds167 Actuarial Gains and Loses 226 Schedule of Average Retirement Benefits Payable169 Actuarial Valuation Results 229 Colorado PERA Benefit Payments–All Division Trust Funds176 Plan Data 231 Schedule of Retirees and Survivors by Types of Benefits

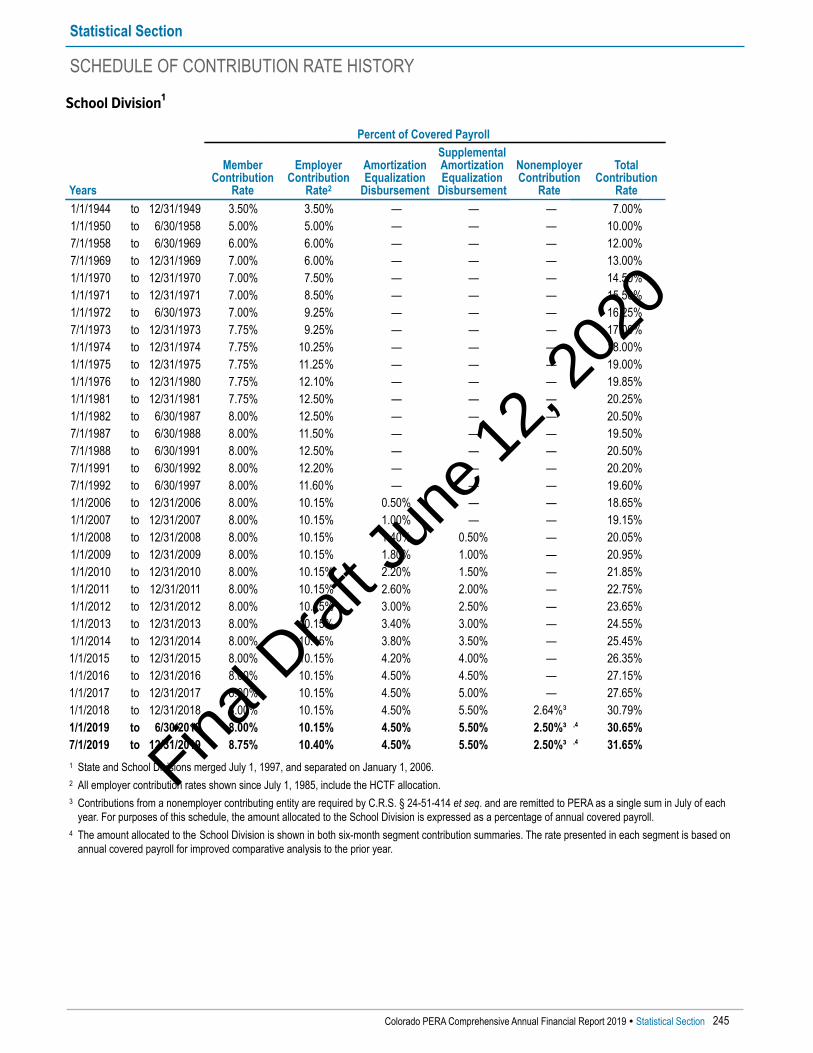

236 Schedule of Average Benefit PaymentsHealth Care Trust Funds—OPEB 243 Schedule of Contribution Rate History186 Actuarial Topics 251 Principal Participating Employers191 Actuarial Assumptions: Exhibits J-N 254 Schedule of Affiliated Employers194 Summary of Funding Progress194 Solvency Test Commonly Used Acronyms195 Unfunded Actuarial Accrued Liability197 Actuarial Gains and Losses 265 Commonly Used Acronyms197 Actuarial Valuation Results201 Plan Data

Table of Contents

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

June 19, 2020

Dear Colorado PERA Members, Benefit Recipients, Employers, andMembers of the Board of Trustees:

Ron BakerExecutive Director

This Comprehensive Annual Financial Report (CAFR) prepared by the PublicEmployees’ Retirement Association of Colorado (PERA) details the plan’sperformance from January 1, 2019, through December 31, 2019.

As I write this letter, the world is still reeling from the global pandemic thathas had a profound impact to our economy, our citizens, and our everydaylives. Throughout this difficult and uncertain time, many PERA memberswere on the front lines of this crisis. Your work serving all Coloradans is vitaland essential in countless ways. We are very proud of the work our membersdo for Colorado, and it is our privilege to serve you.

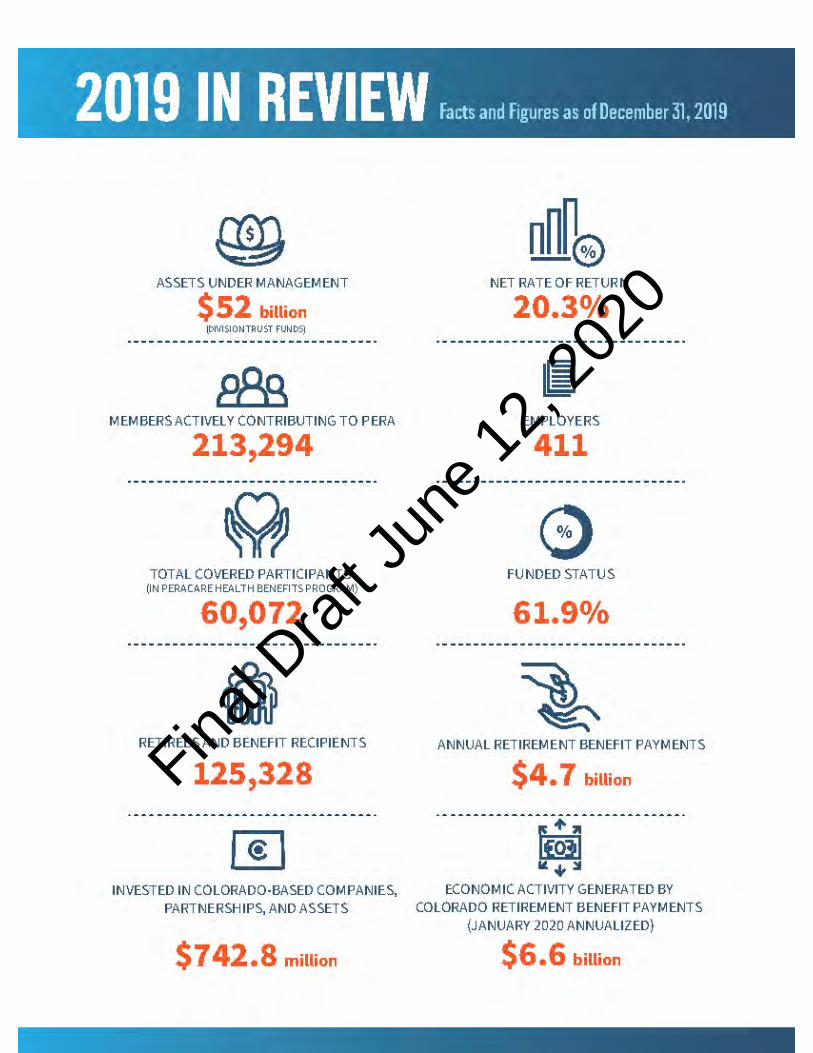

Entering this crisis, PERA was showing signs of strength and makingprogress toward our path to full funding. Aided by a robust global equitymarket, our 2019 investment returns were strong, and for the year endedDecember 31, 2019, the defined benefit funds had a time-weighted rate ofreturn of 20.3 percent net-of-fees. PERA’s total fund policy benchmarkreturned 19.8 percent for 2019.

Positive investment returns are only one component of a plan’s funded status. The degree to which demographic andemployment assumptions align with actual experience are also crucial, and PERA will continue monitoring thesefactors closely.

While we recognize the strong 2019 performance and the effect of the first full year of Senate Bill (SB) 18-200 reforms,the fiscal impact of the current pandemic permeates throughout the public sector of Colorado and includes PERA. Asthe Joint Budget Committee (JBC) grappled with balancing the State’s budget, the Committee moved forward withintroduction of two bills in 2020 as part of the budget-related package concerning PERA:

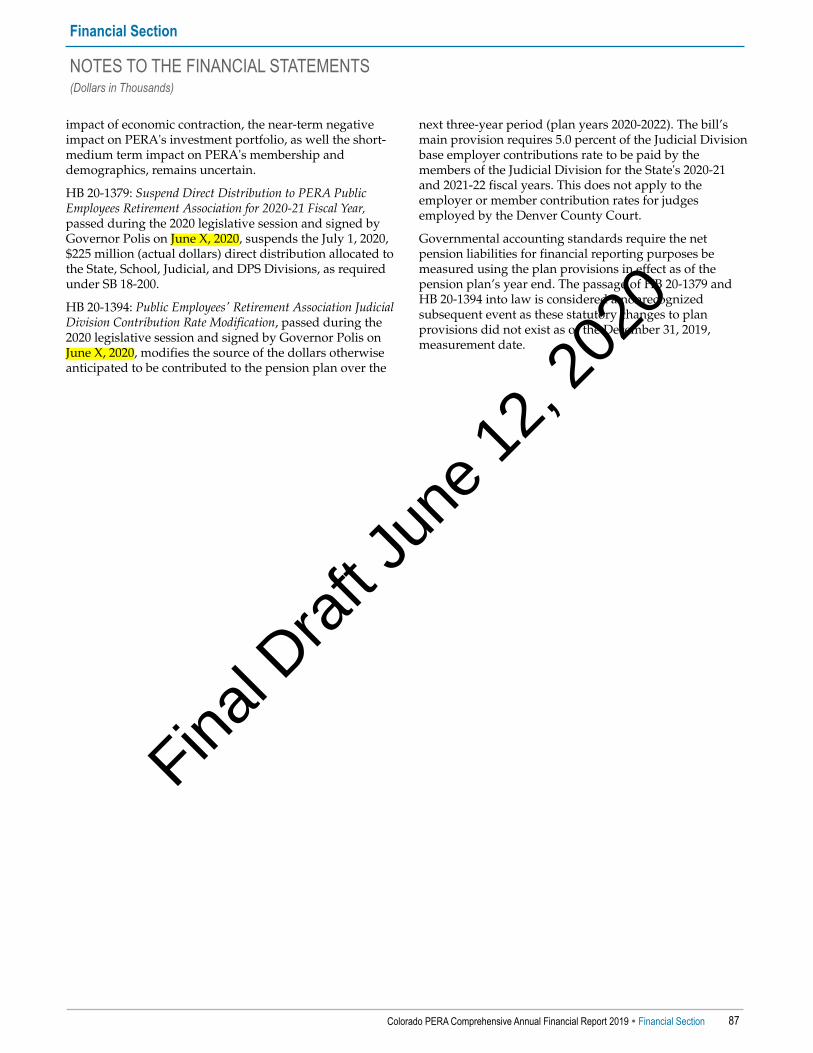

House Bill (HB) 20-1379: Concerning Suspending the Direct Distribution to the Public Employees’ Retirement Association forthe 2020-21 State Fiscal Year

SB 18-200 requires that a direct distribution of $225 million from State funds be paid annually to PERA, allocated tothe State, School, Judicial, and DPS Divisions. This direct distribution payment is to continue annually until theunfunded liabilities for each division receiving the payments are paid down. HB 20-1379 will suspend the July 1, 2020,$225 million direct distribution payment from the State to PERA for the 2020-21 State fiscal year. This one-yearsuspension means PERA will not receive a direct distribution until the payment scheduled July 1, 2021.

House Bill (HB) 20-1394: Concerning a Modification to the Contribution Rates to the Public Employees’ Retirement Associationfor the Judicial Division of the Association for Certain Fiscal Years

For the State’s fiscal years 2020-21 and 2021-22 only, this bill will decrease the employer contribution rate foremployers in the Judicial Division by 5.0 percent and increase the member contribution rate for employees in theJudicial Division by 5.0 percent. For the State’s 2020-21 fiscal year, the employer contribution rate is decreased from13.91 percent to 8.91 percent of salary and the member contribution rate is increased from 9.5 percent to 14.5 percent ofsalary. For the State’s 2021-22 fiscal year, the employer contribution rate is decreased from 13.91 percent to 8.91 percentof salary and the member contribution rate is increased from 10.0 percent to 15.0 percent of salary. This does not applyto the employer or member contribution rates for judges employed by the Denver County Court.

The contribution rates for the Judicial Division will continue to be subject to the automatic adjustment provision(AAP) in PERA law. More information about these changes can be found in Note 12 of the Notes to the FinancialStatements in the Financial Section.

Mail: PO Box 5800, Denver, CO 80217-5800 | 1.800.759.PERA (7372) | www.copera.org

Introductory Section

LETTER OF TRANSMITTAL

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 3

Final D

raft

June

12,

202

0

A strong and sustainable PERA plan is important notonly to our membership, but also to the state ofColorado, where our members live and work in ourcommunities and support our economy. PERAretirement distributions are a steady source of reliable,predictable income for PERA retirees in communitiesacross Colorado. These distributions provide $6.6 billionin economic output for the state, adding critical valueand stimulus to the economy. The 2019 Colorado PERAEconomic and Fiscal Impacts Report, prepared by theeconomic and business analysis firm Pacey Economics,shows that the billions of dollars PERA pays indistributions to more than 104,000 Colorado residentshave a significant benefit to local economies in everycorner of the state.

The modifications from SB 18-200 and 2019’s stronginvestment returns have improved PERA’s fundedstatus and are crucial in building resilience for the plan.However, the COVID-19 crisis will present somechallenges for PERA. Like most defined benefit pensionplans, we expect an impact on our investment gains/demographic experience and future performance.The extent of the impact is uncertain at this time.However, a highly likely outcome is that, when 2020concludes, the automatic adjustment will be triggered. Ifthis occurs, the results will be announced in June 2021,with the contribution increases and a decrease in theAnnual Increase, taking effect in July 2022.

PERA has weathered many unprecedented challengesespecially over the past two decades, and we willcontinue to make our way through these uncertain timesthe same way we have made it through other volatilemarkets. We will continue to be prudent with ourmembers’ and employers’ contributions and beresponsible stewards in making investments on behalfof our membership.

Challenging times present opportunities, and we plan tomeet these challenges on behalf of our membership, inpartnership with stakeholders and constituents, andwith steady leadership as we remain diligent andfocused on fortifying PERA’s sustainability for the longterm knowing that many across Colorado depend onPERA for their retirement security.

2019 LegislationDuring the 2019 legislative session, two bills affectingPERA were introduced, one of which was signedinto law.

House Bill 19-1217: PERA Local Government DivisionMember Contribution RateGovernor Polis signed this bill into law on May 20, 2019,and it eliminated the scheduled 2.0 percent increase inthe member contribution rate for the Local GovernmentDivision that was included in legislation passed in 2018.That legislation increased contributions paid by allPERA members. While this new bill eliminates those

increased contributions for members in the LocalGovernment Division, all members are still subject toany adjustments in contributions required to keep PERAon the path to full funding in 30 years. Contributions forall members can increase (or decrease) by up to0.5 percent per year.

The PERA Board of Trustees' (Board) originalrecommendation to the General Assembly presented inlate 2017 included increases in member contributionsacross all divisions.

House Bill 19-1270: PERA Board Assess Climate-Related Financial RisksThe bill would have required that the PERA Board retaina third-party organization by October 31, 2019, toperform a study to include:

• A comprehensive analysis of any climate-relatedfinancial risk to PERA’s portfolio, and exposure of thefund to long-term risks.

• A summary of climate-related financial risk-relatedengagement activities undertaken by PERA.

• A description of additional action that should betaken, or planned to be taken, by PERA to addressclimate-related financial risk, including a list ofproxy votes and shareholder proposals initiated bythe Board.

The PERA Board had concerns about the redundancy ofthis study with other required reporting and directedstaff to continue to work with the bill sponsors andmembers of the General Assembly to educate them onthese concerns.

This bill was postponed indefinitely by the HouseFinance Committee on April 8, 2019.

Economic Environment2019 started out in what would become the longestgovernment shutdown in U.S. history. Protracted tradenegotiations with China and four Federal Reserve (Fed)rate increases in 2018, combined with the governmentshutdown, added to concerns about a recession hittingthe U.S. economy. These concerns grew quieterthroughout 2019 as the U.S. reached a phase one tradedeal with China and the Fed provided monetarystimulus with three rate cuts to end the year in a rangeof 1.25 to 1.50 percent. By mid-year, the U.S. hadexperienced the longest economic expansion in U.S.history and by year end the U.S. economy had notched126 consecutive months of gross domestic product(GDP) growth. In December 2019, more than a decadeafter the fallout of the global financial crisis of 2008, theU.S. set another milestone by achieving the longest bullmarket in history, with the S&P 500 up 378 percent(price return) from its low in March 2009.

Consumer spending and confidence, boosted bydeclining interest rates, generally remained strong, but

Introductory Section

LETTER OF TRANSMITTAL

4 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

ongoing trade uncertainty held down economic growthin the U.S. with the real rate of growth slowing to2.3 percent in 2019. Wage growth continued into 2019,with the lowest paid workers experiencing the largestincreases as state and local governments across thenation increased their minimum wages. While wagegrowth increased, it remained lower than expectedgiven record low unemployment. The unemploymentrate continued to decline throughout 2019, ending theyear at 3.5 percent, which marked its lowest level sincethe 1960s after having recorded 22 consecutive monthsat or below 4.0 percent at year end. Both headlineinflation and core inflation, which does not includemore volatile components such as food and energy,ended the year at 2.3 percent. The risk of rising inflationis muted against the backdrop of a tight labor marketand modest wage growth, with the larger concern forthe Fed being inflation persistently coming in under its2.0 percent target. Moreover, the Personal ConsumptionExpenditures index, the Fed’s preferred measurement ofinflation, ended 2019 at 1.6 percent.

Growth in the world economy notably slowed to anestimated rate of 2.4 percent in 2019, the lowest levelsince the global financial crisis. Among advancedeconomies, growth in the United States held uprelatively well at 2.3 percent, while the Euro area andJapan measured at just 1.1 percent. Emerging marketsand developing economies fared better than advancedeconomies with overall growth of 3.5 percent, but this isa marked drop from prior years. The ongoing U.S.-China trade war, and the ensuing tariffs, have givenrise to more widespread protectionism amongeconomies, resulting in reduced trade and subduedeconomic growth. Moreover, increasing levels of debt ineconomies around the world have further slowedeconomic growth, although the rising debt burdens aresomewhat offset by increasingly accommodativemonetary policies with some economies, notably theEuro area, taking rates deeper into negative territory. Inthe U.S., the dollar continued to strengthen given thecomparatively strong economy, while the tail windsprovided by tax cuts have shown signs of shifting toheadwinds as the increasing deficit may begin to weighon economic growth.

Colorado, although it began to moderate in its rankingamong states, has again shown to be one of the strongerperforming U.S. state economies in 2019. This is due, inpart, to its employment sector diversification and highlyeducated workforce, ranking second nationally forpercent of workforce with a bachelor’s degree or higher.Colorado ranked seventh in the country for real GDPgrowth in 2019 and well above U.S. GDP of 2.3 percent,at 3.5 percent.

After a slight increase in the unemployment rate in 2018it began trending down again in 2019 to a historic low of2.5 percent, among the lowest in the nation, and a fullpercent lower than the U.S. unemployment rate.

Colorado continues to have one of the highest laborforce participation rates (LFPR) in the nation, rankingfourth nationally, at 69.4 percent and exceeding thenational average of 63.0 percent. Furthermore,Colorado’s population continues to grow at a pacenearly double the U.S. average with positive netmigration of working age adults contributing to the highLFPR and employment growth. A tight labor market in2019 aided in boosting personal income growth and percapita personal income growth, with Colorado rankingfourth and tenth nationally, respectively.

On the housing front, Colorado has consistently beenamong the markets experiencing the highestappreciation in home values, but this moderated furtherin 2019 to a rate of 5.5 percent, which still placesColorado in the top third for appreciation. The growthin housing units has now exceeded householdformations for the last two years, helping to easerelentless price pressure, but it will take time for themarket to find a balance after years of undersupply.

InvestmentsInvestment portfolio income is a significant source ofrevenue to PERA. The Board’s Investment Committee isresponsible for assisting the Board in overseeing PERA’sinvestment program.

In 2019, there was a net investment income of$9.9 billion compared with total member contributionsof $1.0 billion, employer contributions of $1.9 billion andnonemployer contributions of $225 million.

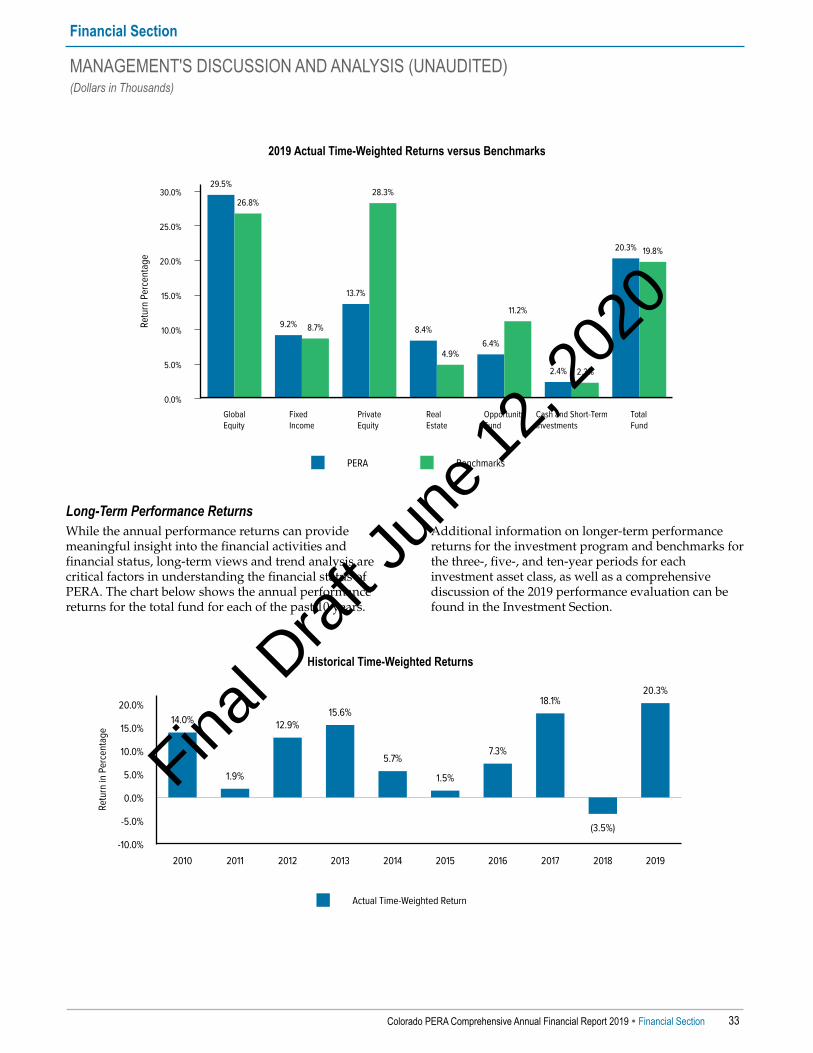

For the year ended December 31, 2019, the definedbenefit funds had a time-weighted rate of return of20.3 percent net-of-fees. The annualized, net-of-fees,time-weighted, rates of return over the last three andfive years were 11.1 percent and 8.4 percent,respectively, and over the last 10 years it was 9.1 percent.The 30-year annualized, gross-of-fees rate of return was8.6 percent.

Prudent funding and healthy investment returns areimportant to the financial soundness of PERA. Moreinformation on the composition of the portfolio isreflected in the Investment Summary on page 126.

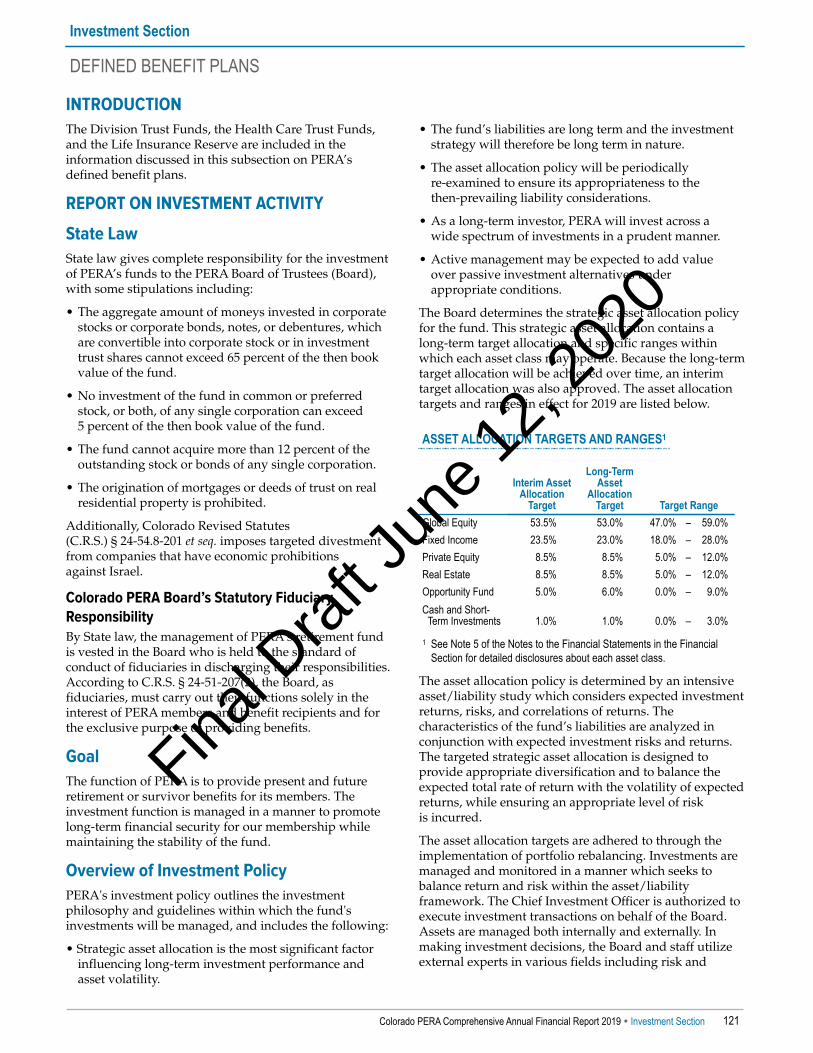

An integral part of the overall investment policy is thestrategic asset allocation policy. The strategic assetallocation is designed to provide appropriatediversification and balance expected total rates of returnwith the volatility of expected returns. The fund is to bebroadly diversified across and within asset classes tolimit the volatility of the total fund investment returnsand to limit the impact of large losses on individualinvestments. Both traditional and nontraditional assetsare incorporated into the asset allocation mix.

In addition to asset class targets, the Board sets rangeswithin which asset classes are maintained. The interimand long-term asset allocation mix and the specifiedranges for each asset class are presented on page 121. All

Introductory Section

LETTER OF TRANSMITTAL

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 5

Final D

raft

June

12,

202

0

of the asset classes were within their specified ranges atyear end.

PERA’s investment policy is summarized in the Reporton Investment Activity on page 121.

Investment StewardshipIt is PERA’s fiduciary duty to serve as stewards ofcapital for over 620,000 members, participants, andbeneficiaries. In 2019, PERA established the InvestmentStewardship Division to fortify our longstandingcommitment to the financial sustainability of the Fund.Foundational to PERA’s investment stewardship arecost-consciousness, materiality to PERA’s portfolio,regulatory and market advocacy, and the ongoingevaluation of our investments. Collectively, these effortsare intended to demonstrate PERA’s investmentstewardship across all asset classes in the portfolio as wecontinue to prioritize financial sustainability.

Corporate governance advocacy has been one of ourmost in-depth investment stewardship efforts. In 2019,PERA management reassigned corporate governancefunctions, including proxy voting, from the LegalDepartment to the Investment Department in adherenceto industry best practices and PERA’s strategic vision.The aim of this reorganization is to streamline andadvance our stewardship efforts to encourage profitablebusiness practices at the companies in which we invest.In addition, PERA continues to be active in the securitieslitigation arena, fulfilling the Board’s commitment tosupport corporate governance reforms such astransparency, accountability, and enforcement ofshareholders’ rights.

Actuarial ResultsActuarial valuations involve assumptions about theprobability of events far into the future in order toestimate the financial and actuarial status of the definedbenefit trust funds. Two types of actuarial valuations arerequired to be performed for PERA’s five defined benefitpension and two Other Postemployment Benefit (OPEB)trust funds: one for financial accounting and reportingpurposes and the other for funding purposes. Theresults of both actuarial valuations are included in thisCAFR. The actuarial valuations performed for financialaccounting and reporting purposes are prepared inaccordance with governmental accounting standards.Pension liabilities, OPEB liabilities, and other relatedamounts calculated in accordance with these standardsemphasize the costs incurred by PERA-affiliatedemployers for providing benefits to their employees aspart of the employment-exchange process. Assets arerequired to be stated at fair value and the liabilities aredetermined using a consistent, standardizedmethodology, which allows for transparency and thecomparability of amounts calculated for financialaccounting and reporting purposes across U.S.governmental defined benefit pension andOPEB systems.

The actuarial valuations for funding purposes areprepared in accordance with Actuarial Standards ofPractice and the Board’s pension and OPEB fundingpolicies. Liabilities and other actuarial metrics arecalculated for the purpose of determining a systematicapproach to pre-funding costs of the five defined benefitpension and two OPEB trust funds, as well as to assessthe adequacy of moneys that are available to pay post-employment benefits earned by the membership. Pre-funding future liabilities defrays the ultimate cost ofproviding benefits as dollars held in the trust fundsgenerate investment returns. The amount of actuarialaccrued liability (AAL) in excess of the actuarial value ofassets is referred to as the unfunded actuarial accruedliability (UAAL). The ratio of assets to AAL representsthe funded status of each plan.

For the year ended December 31, 2019, the UAALcalculated for purposes of systematically funding thefive defined benefit pension trust funds was $29.8 billioncompared to the unfunded liabilities, referred to as thenet pension liabilities calculated for accounting andfinancial reporting purposes of $26.1 billion. Althoughsome of the objectives and calculation methodologies ofthese valuations are similar, the liabilities calculated forfinancial reporting purposes and funding purposes canbe notably different under certain circumstances. For theyear ended, December 31, 2018, the UAAL calculated forpurposes of systematically funding the five definedbenefit pension trust funds was $31.0 billion comparedto the net pension liabilities calculated for accountingand financial reporting purposes of $31.5 billion.

The decrease in the unfunded liabilities calculated foraccounting and financial reporting purposes is primarilydue to favorable investment performance during 2019and the reduced annual increase (AI) maximum, knownas the AI cap, from 1.50 percent to 1.25 percent, perannum. In accordance with GASB 67, the discount ratedetermination for 2019 required the use of the long-termexpected rate of return of 7.25 percent for the fivedefined benefit pension trust funds. When calculatingthe AAL for purposes of funding, the discount rate usedis always equal to the long-term expected rate of returnset by the Board.

Information on certain actuarial metrics that assess themoneys required to systematically fund the five definedbenefit pension and two OPEB trust funds can be foundin the Management's Discussion and Analysis (MD&A)on pages 35-38 of the Financial Section. Acomprehensive discussion of the results of the actuarialvaluation performed for financial accounting andreporting purposes can be found in the MD&A onpages 40-42, as well as in Notes 10 and 11 of the Notes tothe Financial Statements in the Financial Section. Acomprehensive discussion of the results of the actuarialvaluations performed for funding purposes, as well asother analysis utilized by PERA can be found below andalso in the Actuarial Section.

Introductory Section

LETTER OF TRANSMITTAL

6 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

FundingOn December 31, 2019, the funded ratio for PERA’s fivedefined benefit pension trust funds was 61.9 percentcompared to 59.8 percent on December 31, 2018. Theunfunded liability as of December 31, 2019, was$29.8 billion, a decrease of approximately $1.2 billionfrom the previous year. The increase in the funded ratioin 2019 is attributable mainly to favorable investmentperformance for 2019 compared to the long-termexpected rate of return of 7.25 percent and the reducedAI cap, from 1.50 percent to 1.25 percent, per annum.

The development and ongoing review of a pensionfunding policy are responsibilities of the Board. PERA’scurrent pension funding policy was initially adopted bythe Board in March 2015, and last revised in November2018, for the five defined benefit pension trust funds.The Board adopted a similarly structured OPEB fundingpolicy in January 2018. Both policies focus on thedetermination of an actuarially determined contributionreflecting closed and layered 30-year amortizationperiods. The purpose of each policy is three-fold: (1) todefine the overall funding benchmarks of the trust fund,(2) to assess the adequacy of the contribution rates set bythe Colorado Legislature by comparing each trust fund’sstatutorily set contribution rate to an actuariallydetermined contribution benchmark, and (3) to definethe annual actuarial metrics which will assist inassessing the sustainability of the plan. The results ofthese three items help guide the Board whenconsidering whether to pursue or support proposedcontribution and benefit legislation.

A goal of the Board’s pension and OPEB fundingpolicies is the achievement of a combined Division TrustFund and a combined Health Care Trust Fund actuarialfunded ratio equal to or greater than 110 percent.

Investment income is the most significant driver of thefunded status in a defined benefit plan. To understandthe significance of this assumption, a sensitivity analysisis included in the Actuarial Section on page 175 for theDivision Trust Funds and page 200 for the Health CareTrust Funds. Additional information on PERA’s fundedratio, unfunded liabilities, and actuarial assumptionsmay be found in the Actuarial Section starting on page147 for the Division Trust Funds and on page 186 for theHealth Care Trust Funds.

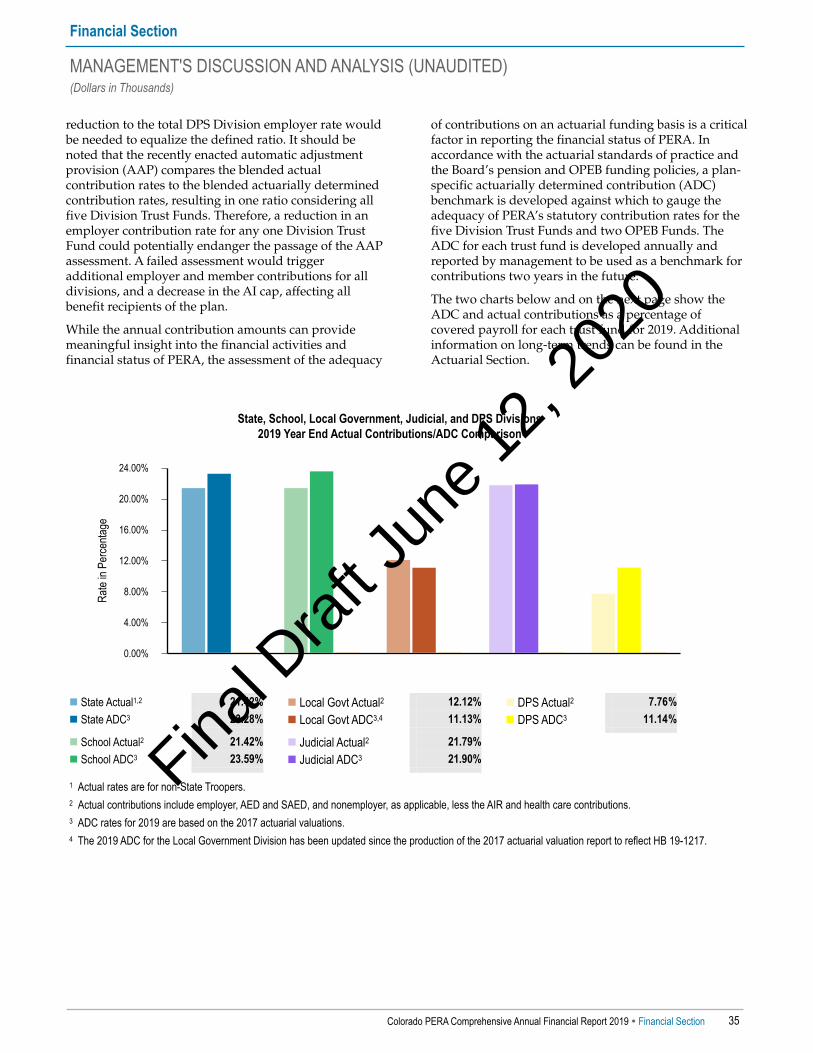

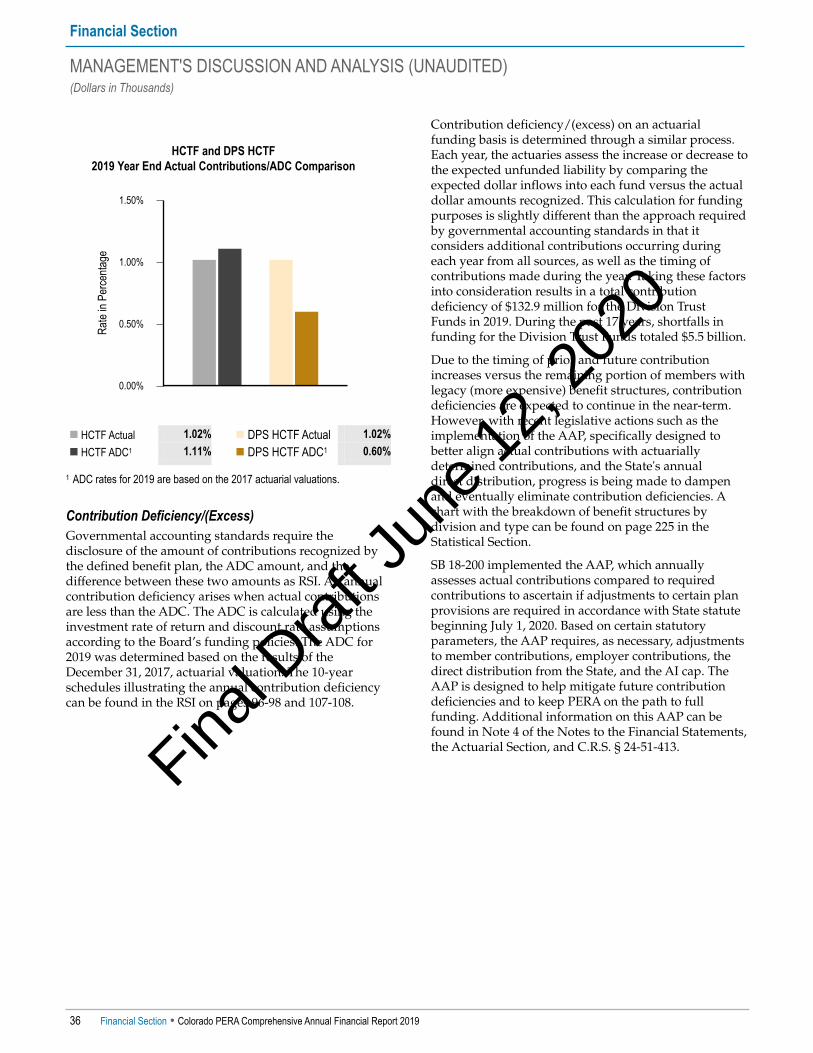

Employer contributions are also a driver of the fundedstatus. In 2019, actual employer contributions receivedpursuant to statute for the five defined benefit pensiontrust funds were $132.9 million less than the actuariallydetermined contributions required. During the past17 years, this contribution deficiency totaled $5.5 billion.See page 37 of Management’s Discussion and Analysis(MD&A) in the Financial Section for additional details.

Investment Rate of Return Sensitivity Effect onProjected Amortization PeriodsIn addition to the annual actuarial funding valuation,the Board’s actuary performs actuarial projections foreach Division Trust Fund. These projections are forward-looking and take into consideration the many tiers ofPERA benefit provisions and the statutory contributionrate structures, including the effective date of each tieror contribution rate. The projections also reflectapplicable salary, demographic, and economic actuarialassumptions, as well as anticipated member growth.Considering the various benefit tiers currently in effectwithin PERA, the Board believes the results of theactuarial projections to be the most comprehensive viewand best indication of the adequacy of the statutorilyprescribed pension contribution schedule.

The main focus of these projections is to provide theamortization period, or rather, the expected fundingperiod, by division, of the estimated number of yearsuntil full funding status is achieved. The projectedamortization periods reflect all actuarial assumptionsand the benefit and contribution provisions currentlyenacted, even if not yet effective.

The table below shows the projected amortizationperiods under three scenarios: (1) as of theDecember 31, 2018, actuarial valuation, (2) as of theDecember 31, 2019, actuarial valuation, reflecting thegreater than expected 2019 investment return and otherplan experience, and the anticipated adjustments,resulting from the AAP enacted through SB 18-200, and(3) as of the December 31, 2019, actuarial valuation,reflecting plan experience and the revised contributionprovisions enacted under HB 20-1379 and HB 20-1394(see Note 12 of the Notes to the Financial Statements inthe Financial Section for additional details).

Projected Amortization Periods (in years)

Division Trust Fund

2019 Valuation Results

Considering HB 20-1379 and

HB 20-1394

2019ValuationResults

2018ValuationResults

State 22 22 28School 24 24 34Local Government 14 14 29Judicial 12 12 21DPS 11 11 17

Since the projections are based on a wide variety ofassumptions, it is important to understand the risksrelated to defined benefit plans, specifically the risksassociated with the selection and application of the long-term expected rate of return on investments. Given thelong-term funding horizon and anticipated ongoingaspect of such defined benefit plans, particularly thoseproviding benefits in the public sector, it is generallyunderstood that the existence of the plan, itself, is not

Introductory Section

LETTER OF TRANSMITTAL

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 7

Final D

raft

June

12,

202

0

tied to the financial performance of private enterprise,but rather to the ongoing nature of governmentalservices. Therefore, it is common practice for plansponsors/administrators of governmental or publicsector pension plans also to apply the expected long-term rate of return as the discount rate used todetermine the liabilities of the plan.

In order to derive the long-term rate of returnassumption, the PERA Board looks to the expertise of itsinvestment and actuarial consultants to perform acomprehensive asset/liability study on a periodic basis(generally every three to five years). In conjunction withthis study, the Board reviews capital market data fromnumerous sources. PERA concluded the most recentasset/liability study in November 2019. As a result ofthat study, the Board updated and approved long-termasset allocations and target ranges effectiveJanuary 1, 2020, and reaffirmed the current 7.25 percentlong-term expected rate of return applicable to all fiveDivision Trust Funds as well as the two Health CareTrust Funds.

The table below illustrates the projected amortizationperiods, in years, of the School Division Trust Fundunder the various return scenarios (used for bothassumed investment return and to discount liabilities ofthe plan) which correspond to the confidence levels(probabilities of investment return) as indicated.

This table reflects the results and experience of theDecember 31, 2019, actuarial funding valuation, theeffect of the adjustments due to the results of the 2018AAP assessment, and the revised contributionprovisions enacted under HB 20-1379 and HB 20-1394.The projected funding periods below reflect 50-yearprobability outlooks (Monte Carlo simulations),provided by the Board’s actuaries, and based on 30-yearcapital market assumptions, employed in the mostrecent asset/liability study as described above, providedby the Board’s investment consultants.

Projected Amortization Periods—School Division Trust FundProbability of Achievingat Least the Rate ofReturn Displayed (or Better), Per Annum

Long-Term Expected Investment Return& Discount Rate

4.35% 6.18% 7.25% 8.63% 10.47%95th Percentile Infinite75th Percentile 4553rd Percentile 2425th Percentile 11 5th Percentile 3

Signal Light MethodologyAnother way of understanding PERA’s financialcondition was adopted by the Colorado GeneralAssembly’s Legislative Audit Committee in 2015, andfurther enhanced by the Board in 2019 to incorporatestochastic rather than deterministic modeling. By

definition, uncertain or variable factors are built into astochastic model, whereas variable factors are externalto a deterministic model. The stochastic model betterreflects actual market activity including the effect of thetiming and order of investment returns. Thismethodology also considers PERA’s portfolio, moreprecisely reflecting capital market assumptions, byinvestment category within PERA’s asset allocation.

Generally, the “signal light” methodology determinesthe funded position of each division on a projectedbasis. The results are categorized based on an expandedspectrum of signal light colors ranging from dark green,indicating a well-funded position, to dark red,indicating potential insolvency in the near future.

PERA updates the signal light indicators each yearfollowing the release of its CAFR. Recognizing the planexperience as of the December 31, 2019, actuarialvaluation, including the effect of HB 20-1379 andHB 20-1394, and better reflecting the effect of pathdependency, the signal light designation is green for theState and School Divisions and dark green for the LocalGovernment, Judicial and DPS Divisions.

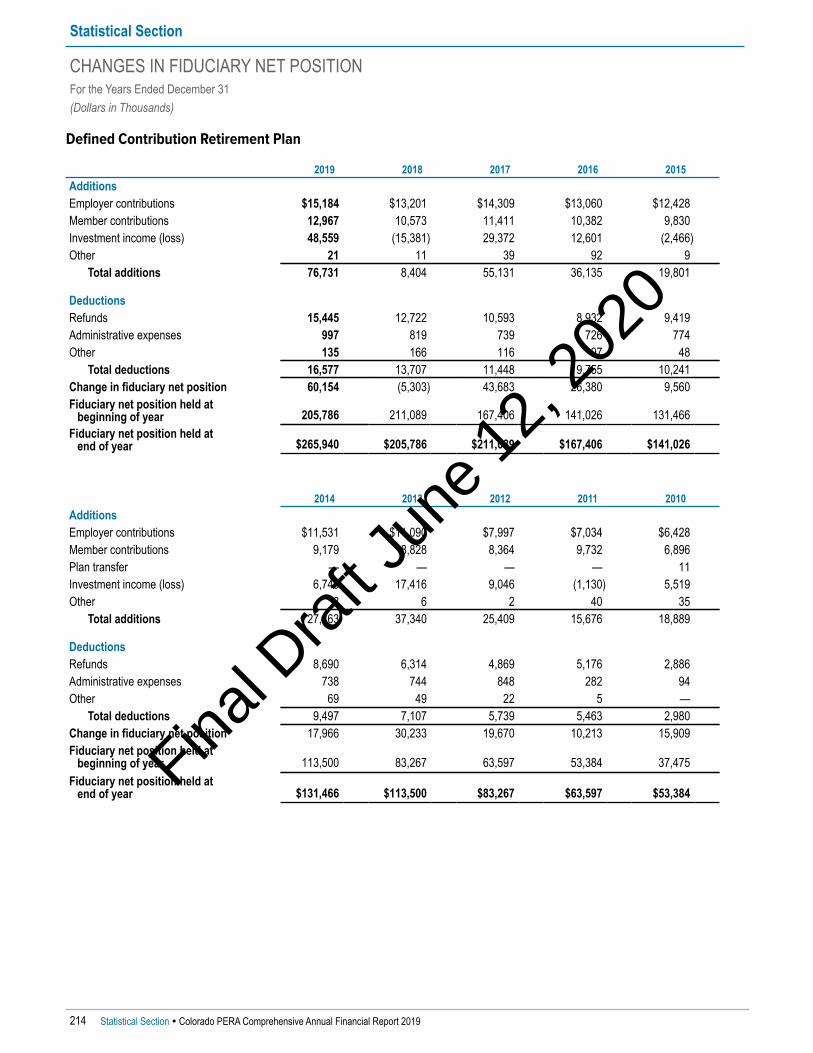

PERAPlus 401(k)/457 and Defined ContributionRetirement PlansPERA offers members opportunities to save forretirement through the PERAPlus 401(k), PERAPlus 457,and Defined Contribution (DC) Retirement Plans. As ofDecember 31, 2019, there were a total of 184 employerswho recognized the value of offering more choices insavings by affiliating into the PERAPlus 457 Plan. TheRoth option was added to the PERAPlus 401(k) and457 Plans at the end of 2014. As of December 31, 2019,there were a total of 79 employers who have adoptedthe Roth option. The Roth option in these plansoffers advantages over a Roth IRA, includinghigher contribution limits and no income-basedcontribution limitations.

The fiduciary net position of the PERAPlus 401(k) Plan,PERAPlus 457, and DC Retirement Plans increased forthe year ended December 31, 2019. The PERAPlus 401(k), PERAPlus 457, and DC Retirement Plans earned$700.3 million, $163.9 million, and $48.6 million ofinvestment income with a fiduciary net position of$3.7 billion, $989.6 million, and $265.9 million,respectively.

Overview of Colorado PERAEstablished in 1931, PERA operates by authority of theColorado General Assembly and is administered underTitle 24, Article 51 of the Colorado Revised Statutes.Initially covering all State employees, PERA hasexpanded to include all Colorado school districts, theState’s judicial system, and many municipalities andother local government entities.

Introductory Section

LETTER OF TRANSMITTAL

8 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

Board CompositionPERA is governed by a 16-member Board of Trustees;11 Trustees are elected by the membership for staggeredfour-year terms and serve without compensation exceptfor necessary expenses. In addition, there are threeGovernor-appointed Trustees confirmed by the Senatewho receive limited compensation. The State Treasurerserves as a voting ex officio Trustee, and the DPSDivision seat serves as a non-voting ex officio Trustee.

In January 2019, The Honorable Walker Stapleton leftthe Board when his term as State Treasurer ended. TheHonorable Dave Young was elected State Treasurer inNovember 2018, and he began serving as an ex officioTrustee effective January 2019.

In March 2019, the Board appointed The HonorableRebecca R. Freyre to the Judicial Division seat andreappointed Timothy M. O’Brien to the retiree seat. Eachwas the sole candidate duly nominated and eligible tobe elected to these seats. Terms for both Trustees beganJuly 1, 2019, and end June 30, 2023.

The Honorable Will Bain did not seek re-election for theJudicial Division seat, which was up for election in 2019.Also in March 2019, Trustee Robert Lamb announced hisretirement with Boulder County effective May 1, 2019.

By law, the Board was responsible for appointing areplacement for the vacant Local Government position,and an ad hoc search committee of the Board wasformed in March 2019. Cheryl Pattelli was appointedto the vacant Local Government Division seat onJune 21, 2019, serving until the next Board election in2020. Pattelli is the Chief Financial Officer at the Cityof Boulder.

At the March 2020 Board meeting, the Board re-appointed Trustee Pattelli since her seat wasuncontested in the Local Government Division election.She will begin serving a two-year term on July 1, 2020,which completes the term originally held by TrusteeLamb. At this meeting, the Board also re-appointed AmyGrant to the DPS Division seat, and she will beginserving a four-year term beginning on July 1, 2020.Additionally, the Board appointed Nathan Geroche, ascience teacher in the Jefferson County School District,to the School Division seat as he was the sole candidatefor this seat, which was held by Trustee William Parkerwho did not seek re-election. Trustee Geroche alsobegins serving a four-year term on July 1, 2020.

On behalf of the PERA executive team, we thankTrustees Bain, Lamb, Parker, and Stapleton for theircontributions and service to the PERA membership.

Management ChangesIn August 2019, Rebecca Shelton was promoted toInvestment Operating Officer in the Investment

Administration Division. Rebecca joined PERA inMarch 2011 as an Investment Business Analyst in theInvestment Operations Division and, in 2013, waspromoted to Investment Operations Manager. In hernew position, Rebecca is responsible for the overallbusiness management functions in the InvestmentDepartment working in conjunction with the ChiefInvestment Officer.

Also in August 2019, Tara Stacy was promoted toDirector of Investment Stewardship in the newly createdInvestment Stewardship Division. Tara joined PERA inAugust 2017 as an Investment Compliance andPerformance Analyst in the Investment AdministrationDivision. In this new role, Tara is responsible for thedevelopment and implementation of PERA’s investmentstewardship initiatives.

In October 2019, Ryan Ericson was promoted to Directorof Application Development replacing Rich Krough whoretired after 17 years of service. Ryan joined PERA inMarch 2011 as a Team Manager in the ApplicationDevelopment Division. In his new role, Ryan isresponsible for directing the development, management,and modification of all internal application softwaredeveloped at PERA.

In January 2020, Keith Tayman was promoted toDirector of Fixed Income in the Investment Departmentreplacing Mark Walter who left PERA in October 2019after nine years of service. Keith joined PERA in April2008 as a Senior Fixed Income Portfolio Manager. In hisnew role, Keith is responsible for the leadership of theFixed Income Division’s operations and staff, as well asthe overall management of PERA’s fixed income assetclass in accordance with established investment policiesand portfolio risk and return objectives.

In April 2020, Patrick Lane was hired as Chief BenefitsOfficer, a position previously held by Donna Baros whoretired in January 2019. Patrick joined PERA from theOklahoma Public Employees Retirement System, wherehe was Director of Member Services. In his new role,Patrick is responsible for providing strategic oversightand management of PERA’s retirement, disability, andsurvivor benefit payments; member account services;benefit counseling; and customer service programs.

In May 2020, Patrick von Keyserling was hired as SeniorDirector of Communications. This new position wascreated following the departure of former ChiefCommunications Officer, Tara May, who left PERA inJanuary 2020 after four years of service. Previously,Patrick was the Communication Director at the City ofBoulder. In this position, Patrick will advance PERA’sstrategic communications, government and publicaffairs, marketing, and public relations efforts with avariety of stakeholders locally and nationally.

Introductory Section

LETTER OF TRANSMITTAL

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 9

Final D

raft

June

12,

202

0

Financial Information and ManagementResponsibilityOur CAFR must comply with the reportingrequirements under Title 24, Article 51, Section 204(8) ofthe Colorado Revised Statutes (C.R.S.).

PERA’s financial statements are prepared bymanagement, who is responsible for the integrity andfairness of the data presented, including the manyamounts which must, out of necessity, be based onestimates and judgments. This CAFR was prepared toconform to the accounting principles generally acceptedin the United States of America. Financial informationpresented through the annual report is consistent withthat which is displayed in the basic financial statements.

Ultimate responsibility for the basic financial statementsand annual report rests with PERA management; theBoard provides an oversight role over financialreporting. The Board is assisted in its responsibilities bythe Audit Committee, which consists of seven Boardmembers and two independent outside members. TheAudit Committee is responsible for overseeing theadequacy and effectiveness of PERA’s system of internalcontrol and the accounting and financial reportingsystems. A more detailed description of the AuditCommittee’s role can be found in their report onpages 16-17.

Management is responsible for establishing andmaintaining adequate internal control over financialreporting. PERA’s internal control over financialreporting is designed to provide reasonable, but notabsolute assurance, regarding the reliability of financialreporting and the preparation of financial statements forexternal purposes in accordance with generally acceptedaccounting principles. The internal control over financialreporting includes those policies and procedures that:

• Pertain to the maintenance of records that, inreasonable detail, accurately and fairly reflect thetransactions and dispositions of assets;

• Provide reasonable assurance that transactions arerecorded as necessary to permit preparation offinancial statements in accordance with generallyaccepted accounting principles, and that receipts andexpenditures are being made only in accordance withauthorizations of management; and

• Provide reasonable assurance regarding prevention ortimely detection of unauthorized acquisition, use ordisposition of assets that could have a material effecton the financial statements.

Management has concluded that, as ofDecember 31, 2019, the system of internal controlsover financial reporting is effective.

There are inherent limitations in the effectiveness of anysystem of internal control, including the possibility ofhuman error, the circumvention or overriding of

controls, and that the cost of a control should not exceedthe benefits to be derived. Accordingly, even an effectiveinternal control system may not prevent or detectmisstatements and can provide only reasonableassurance with respect to financial statementpreparation. Also, projections of any evaluation ofeffectiveness to future periods are subject to the risk thatcontrols may become inadequate because of changes inconditions or that the degree of compliance with thepolicies or procedures may deteriorate.

State law requires that the State Auditor conducts orcauses to be conducted an annual audit of PERA.Pursuant to this requirement, the State Auditor selectedCliftonLarsonAllen LLP in 2015 to perform theindependent audit of PERA's annual financialstatements, beginning with the year endedDecember 31, 2015. Under the direction of the StateAuditor, CliftonLarsonAllen LLP audited PERA’s 2019basic financial statements in accordance with auditingstandards generally accepted in the United States ofAmerica and Government Auditing Standards.CliftonLarsonAllen LLP issued an unmodified opinionon PERA's financial statements, which can be found inthe Independent Auditors' Report within the FinancialSection on pages 25-27. Management has provided theauditors with full and unrestricted access to PERA’srecords and staff to discuss their audit and relatedfindings to facilitate independent validation of theintegrity of the plan’s financial reporting and to considerthe effectiveness of internal controls.

The Financial Section of the CAFR also contains theMD&A that serves as a narrative introduction, overview,and analysis of the basic financial statements. This Letterof Transmittal is designed to complement the MD&Aand should be read in conjunction with it.

Recognition of Achievements The Government Finance Officers Association of theUnited States and Canada (GFOA) awarded aCertificate of Achievement for Excellence in FinancialReporting to PERA for its CAFR for the year endedDecember 31, 2018. This was the 34th consecutive yearthat PERA has achieved this prestigious award. In orderto be awarded a Certificate of Achievement, agovernment must publish an easily readable andefficiently organized CAFR. This report must satisfyboth generally accepted accounting principles andapplicable legal requirements.

A Certificate of Achievement is valid for a period of oneyear only. We believe that our current CAFR continues tomeet the Certificate of Achievement Program’srequirements, and we are submitting it to the GFOA todetermine its eligibility for another certificate.

The GFOA also awarded PERA an Award forOutstanding Achievement in Popular Annual FinancialReporting for its Popular Annual Financial Report for theyear ended December 31, 2018. The Award for

Introductory Section

LETTER OF TRANSMITTAL

10 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

Outstanding Achievement in Popular Annual FinancialReporting is a prestigious national award recognizingconformance with the highest standards for preparationof state and local government popular reports.

In order to receive an Award for OutstandingAchievement in Popular Annual Financial Reporting, agovernment unit must publish a Popular AnnualFinancial Report, whose contents conform to programstandards of creativity, presentation, understandability,and reader appeal.

An award for Outstanding Achievement in PopularAnnual Financial Reporting is valid for a period of oneyear only. PERA has received a Popular Award for thelast 17 consecutive years. We believe our current reportcontinues to conform to the Popular Annual FinancialReporting requirements, and we are submitting it tothe GFOA.

PPCC Standards Award ProgramThe Public Pension Coordinating Council (PPCC)presented PERA with its Recognition Award forAdministration for meeting professional standards in2019 for plan administration as set forth in the PublicPension Standards. This is the 17th consecutive year thatPERA has received this annual award. In 2019, the PPCCpresented PERA with its Recognition Award forFunding by demonstrating the funding adequacy of thepension system. The PPCC is a coalition of threenational associations that represent public retirementsystems and administrators—the National Associationof State Retirement Administrators, National Council onTeacher Retirement, and National Conference on PublicEmployee Retirement Systems. These three associationsrepresent more than 500 of the largest pension plans inthe U.S.

In MemoriamRecently, PERA lost a visionary and true leader whotouched the lives of many. Robert (Bob) J. Scott, formerPERA Executive Director, passed away on April 20, 2020.Bob served as PERA’s Executive Director fromNovember 1984 until his retirement in July 2000. Prior tobeing appointed Executive Director, he was Colorado’sState Auditor from 1977 to 1984 and served as a Trusteeon the PERA Board for seven years.

During Bob’s tenure as PERA’s fourth ExecutiveDirector, the PERA trust fund grew to more than$28 billion. Under his leadership, PERA implementedthe 401(k) Voluntary Investment Plan program, theretiree health care program, and earned Certificates ofExcellence in Financial Reporting for its CAFR for15 successive years.

Bob was a leader in the public pension industry holdingseveral positions with the National Association of StateRetirement Administrators including serving as itsPresident. He served as Chairman of the National PublicPension Coordinating Council, on the ExecutiveCommittee of National Conference of State Legislatures,and on the Government Finance Officers AssociationCommittee on Public Employee RetirementAssociations. Bob’s exemplary credentials prepared himfor a life-long career in public service that also includedserving as the Executive Director of the Denver PublicSchools Retirement System from 2004-2005.

Bob earned the respect of members, retirees, employers,legislators, and peers across the country and will beremembered for his commitment to improve upon pastprograms and philosophies while drawing blueprintsfor the future. PERA and Colorado’s public employeesare still benefitting today from his vision and dedicationfor a better retirement plan for all PERA members.

It is with profound gratitude that I recognize andmemorialize Bob for his many contributions andaccomplishments during his 16-year career as PERA’sExecutive Director.

AcknowledgementsThe cooperation of our affiliated employers issignificant to the success of PERA, and we thank thestaff and management of these employers for theircontinuing support.

Copies of this CAFR are provided to all PERA-affiliatedemployers and other interested parties; a summary(Popular Annual Financial Report) will be sent to membersand benefit recipients. Electronic versions of bothpublications are available on the PERA website atwww.copera.org. For questions concerning any of theinformation provided in this CAFR, please [email protected].

I also thank the PERA staff and Board of Trustees fortheir commitment and efforts to ensure that PERA meetsthe needs of all public employees in Colorado. We arecognizant of the current challenges and uncertaintiesand will remain diligent and focused on keeping PERAstrong and sustainable.

Respectfully submitted,

Ron BakerColorado PERA Executive Director

Introductory Section

LETTER OF TRANSMITTAL

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 11

Final D

raft

June

12,

202

0

Introductory Section

PROFESSIONAL AWARDS

12 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

Introductory Section

PROFESSIONAL AWARDS

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 13

Final D

raft

June

12,

202

0

Timothy M. O'Brien Board Chairman

June 19, 2020

Dear Colorado PERA Members, Benefit Recipients, and Employers:

As Chairman of the Board of Trustees (Board) of the Public Employees’ RetirementAssociation of Colorado, I am pleased to present Colorado PERA’s ComprehensiveAnnual Financial Report for the year ended December 31, 2019.

PERA’s investments generated a return of 20.3 percent for 2019. Strong investmentperformance fortifies overall funding; however, during all market cycles, it isimportant to remember that PERA is a long-term investor whose goal is to provideretirement benefits in perpetuity.

While PERA experienced solid progress toward its funding goal during 2019, theuncertainty and significant market declines related to the 2020 global pandemic willno doubt impact PERA as it will nearly all other investors. The Board recognizes the

severity of this crisis and its expected impact on any gains made toward the funding goal and will remain vigilant inmonitoring PERA’s financial condition. Despite these unprecedented challenges, the Board’s top priority is ensuringthe long-term viability and sustainability of the PERA fund as we recognize the importance of PERA to ourmembership and the citizens of Colorado.

Although much of the current focus is related to the COVID-19 crisis, in 2019, several initiatives were completed or inprogress as part of the Board’s five-year strategic plan, which officially started in 2019. I would like to highlight a fewof these initiatives below.

As part of the Board’s ongoing commitment to sound stewardship, the Board commissioned an asset/liability studyduring 2019, which was prepared by Aon Hewitt Investment Consulting, Inc. (Aon). The objective of the study was todetermine the optimal strategic asset allocation policy that will ultimately allow PERA to meet its financial obligations,while also ensuring that PERA incurs appropriate levels of risk and liquidity. There will be a range of investmentreturns in any given short period but, over the long term, Aon’s modeling indicated 7.25 percent was near the medianexpectation. As a result of this study, the Board slightly modified the asset allocation ranges and targets, whilereaffirming the investment return assumption of 7.25 percent.

Additionally, in August 2019, the Board directed PERA staff to issue a Request for Proposal from qualified firms toprovide investment consulting services for the Voluntary Investment Program (401(k) Plan), Deferred CompensationPlan (457 Plan), and Defined Contribution Retirement Plan (DC Plan), collectively referred to as the CapitalAccumulation Plans (CAP). In November 2019, the Board identified three finalists and ultimately selected Callan LLCas the CAP Investment Consultant in December 2019.

Throughout 2019, the Board spent considerable time completing a comprehensive review of the Governance Manualas outlined in the Strategic Plan. This document codifies the policies and practices of the Board and provides a soundgovernance framework for the Board’s mandate to set policy and oversee the programs and operations of PERA. Tohelp streamline the operation of the Board, some roles and responsibilities were realigned within the committeestructure and a few committees were eliminated and absorbed into other committees. As a result, the responsibilitiesof the Shareholder Relations Committee transferred to the Investment Committee and the Stakeholder RelationsCommittee was eliminated with the responsibility to oversee and report on communications to the Board transferredto the Executive Director. Additionally, the CAP investment responsibilities transferred from the Benefits Committeeto the Investment Committee.

Finally, as outlined in the Strategic Plan as a goal to clarify the role and value of PERA to members and retirees, thePERA Communications Department completed a significant research project in 2019 to better understand satisfactionamong the PERA membership. Using existing data as well as new data from survey results, areas of servicestrengths and weaknesses within the organization were identified with recommendations for ways to increasemember satisfaction.

Mail: PO Box 5800, Denver, CO 80217-5800 | 1.800.759.PERA (7372) | www.copera.org

Introductory Section

BOARD CHAIRMAN'S REPORT

14 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

In addition to the work related to the Strategic Plan, the Board also amended its Statement on Divestment inJanuary 2019. As referenced in the revised Statement: “The issues facing our world today are not easily separated intogradations of severity or importance. Consensus as to the priority of these types of issues and the proper recourse isdifficult to achieve. As a result, once a divestment mandate is imposed to address one issue, the resulting 'slipperyslope' makes differentiation among the remaining issues contentious and divisive. Increased divestment is costly andlimits PERA’s ability to effectively seek the best risk-adjusted returns to secure the retirement benefits of publicservants. For these reasons, PERA will oppose divestment efforts unless such opposition is inconsistent with itsfiduciary duty, but will implement divestment mandates passed by the Colorado General Assembly.”

These initiatives and many others highlight the Board’s continued commitment to sound stewardship on behalf of allPERA members. I would like to recognize the following Trustees, who left the Board in 2019, for their diligence andthoughtful contributions while serving on the Board: The Honorable Will Bain (Judicial Division), Bob Lamb (LocalGovernment Division), and The Honorable Walker Stapleton (outgoing State Treasurer). With these departures wealso welcomed the following new Trustees to the Board: The Honorable Rebecca R. Freyre (Judicial Division), TheHonorable Dave Young (new State Treasurer), and Cheryl Pattelli (Local Government Division), who was appointedto fill the Local Government seat due to Bob Lamb’s retirement. Trustees devote many hours in fulfilling theirfiduciary duties while serving the membership, and all Trustees are recognized for their significant contributions oftime and service.

As we continue to work through challenging times, requiring PERA to be adaptive and responsible, I would liketo extend my gratitude to the Trustees for their dedication and continued perseverance as we work on behalf ofour members, beneficiaries, and employers. The Board’s guidance and support are essential to the success ofPERA. As Trustees, we are committed to ensuring the integrity and sustainability of the plan for all of Colorado’spublic employees.

Sincerely,

Timothy M. O’BrienChairman, Colorado PERA Board of Trustees

Introductory Section

BOARD CHAIRMAN'S REPORT

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 15

Final D

raft

June

12,

202

0

As described more fully in its Charter, the purpose of the Colorado PERA Audit Committee (Audit Committee) is toassist the Board of Trustees (Board) in fulfilling its fiduciary responsibilities as they relate to accounting policies andfinancial reporting, the system of internal control, PERA’s Standards of Professional and Ethical Conduct, the internalaudit process, and the practices of the Director of Internal Audit. Management is responsible for the preparation,presentation, and integrity of PERA’s financial statements; accounting and financial reporting principles; internalcontrol; and procedures designed to reasonably ensure compliance with accounting standards, applicable laws, andregulations. PERA has a full-time Internal Audit Division that reports functionally to the Audit Committee. TheInternal Audit Division is responsible for independently and objectively reviewing and evaluating the effectivenessand efficiency of PERA’s system of internal control.

In 2015, the State Auditor selected CliftonLarsonAllen LLP to perform the independent audit of PERA’s annualfinancial statements, commencing with the year ended December 31, 2015. CliftonLarsonAllen LLP is responsible forperforming an independent audit of PERA’s financial statements in accordance with generally accepted auditingstandards and the standards applicable to financial audits contained in Government Auditing Standards issued bythe Comptroller General of the United States. In accordance with law, the State Auditor has ultimate authority andresponsibility for selecting, evaluating, and, when appropriate, replacing PERA’s Independent Auditor.

The Audit Committee serves a Board-level oversight role in which it provides advice, counsel, and direction tomanagement and to the Internal Audit function on the basis of the information it receives, discussions withmanagement and Internal Audit, and the experience of the Audit Committee’s members in business, financial, andaccounting matters. In this role, the Audit Committee also reviews the audit plan of the Independent Auditor, theresults of the audit, and the status of management’s actions to implement recommendations from the audit.

The Audit Committee believes that a candid, substantive, and focused dialogue with the internal auditors and theIndependent Auditor is fundamental to the Audit Committee’s oversight responsibilities. To support this belief, theAudit Committee periodically meets separately with both the Director of Internal Audit and the IndependentAuditor, without management present. In the course of its discussions in these meetings, the Audit Committee askeda number of questions intended to bring to light any areas of potential concern related to PERA’s financial reportingand internal control. These questions include, but are not limited to:

• Are there any significant accounting judgments, estimates, or adjustments made by management in preparing thefinancial statements that would have been made differently had the Independent Auditor prepared and beenresponsible for the financial statements?

• Based on the Independent Auditors' expertise, and their knowledge of PERA and PERA’s financial statements, havesubsequent events been appropriately disclosed in the financial statements?

• Based on the Independent Auditors’ experience, and their knowledge of PERA, do PERA’s financial statementsfairly present to users, with clarity and completeness, PERA’s financial position and performance for the reportingperiod in accordance with generally accepted accounting principles?

• Based on the Independent Auditors’ experience, and their knowledge of PERA, has PERA implemented internalcontrol and internal audit procedures that are appropriate for PERA?

• Are the Independent Auditor and internal auditors getting the support they need from management to executetheir duties?

Questions raised by the Audit Committee regarding these matters were answered to the Audit Committee’ssatisfaction.

The Audit Committee had an agenda for 2019 that included the following items:

• Recommending the Comprehensive Annual Financial Report (CAFR) to the Board for its approval;

• Recruiting and hiring a new Director of Internal Audit;

Mail: PO Box 5800, Denver, CO 80217-5800 | 1.800.759.PERA (7372) | www.copera.org

Introductory Section

REPORT OF THE COLORADO PERA AUDIT COMMITTEE

16 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

• Reviewing and approving the plan and budget of the Internal Audit Division;

• Reviewing the adequacy of resources made available to the Internal Audit Division;

• Reviewing the scope, objectives, and timing of the annual independent audit of PERA’s financial statements;

• Providing input into the Executive Director’s annual performance evaluation of the Director of Internal Audit;

• Reviewing PERA’s compliance with its Standards of Professional and Ethical Conduct;

• Meeting with the Independent Auditor separately, without management present;

• Meeting separately with the Executive Director, Director of Internal Audit, Controller, and General Counsel; and

• Meeting with the Director of Internal Audit and with management to discuss the effectiveness of PERA’sinternal control.

The Audit Committee has reviewed and discussed the audited financial statements for the year ended December 31, 2019, with management and the Independent Auditor. Management represented to the AuditCommittee that PERA’s audited financial statements were prepared in accordance with accounting principlesgenerally accepted in the United States of America that apply to governmental accounting for fiduciary funds. TheIndependent Auditor represented that their presentations to the Audit Committee included the matters required byauditing standards on auditor communication to be discussed with the Independent Auditor. This review included adiscussion with management of the quality (not merely the acceptability) of PERA’s accounting principles, thereasonableness of significant estimates and judgments, and the clarity of disclosure in PERA’s financial statements,including the disclosures related to critical accounting estimates.

In reliance on these reviews and discussions, and the reports of the Independent Auditor, the Audit Committee hasrecommended to the Board, and the Board has approved PERA’s CAFR for the year ended December 31, 2019.

Audit Committee as of June 19, 2020

David Hall, Chairman

Ramon Alvarado

Honorable Rebecca R. Freyre

Julie Friedemann

A. Tom Hall

Tammie Lowrie

Susan G. Murphy

Timothy M. O’Brien

Cheryl Pattelli

Introductory Section

REPORT OF THE COLORADO PERA AUDIT COMMITTEE

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 17

Final D

raft

June

12,

202

0

By State law, authority over the public employees’ retirement association is vested in the Board of Trustees (Board).The Board is composed of the following 16 Trustees:

• Nine members elected by members from their respective Divisions to serve on the Board for four-year terms; fourfrom the School Division, three from the State Division, one from the Local Government Division, and one from theJudicial Division.

• Two retirees elected by retirees to serve on the Board for four-year terms.

• Three Trustees appointed by the Governor and confirmed by the State Senate to serve on the Board for four-year terms.

• The State Treasurer.

• One ex officio (non-voting) member or retiree elected by members and retirees of the Denver Public Schools (DPS)Division to serve on the Board for a four-year term.

If a Board member resigns, a new Trustee is appointed from the respective Division until the next election of Trustees.

Timothy M. O’BrienChairmanElected by RetireesRetired Colorado State AuditorOffice of the State AuditorCurrent term expires June 30, 2023

Thomas J. BarrettAppointed by the GovernorCurrent term expires July 10, 2022

Marcus PennellVice Chairman

Elected by School Members Physics Teacher Jefferson County School District Current term expires June 30, 2021

Guillermo BarrigaElected by School MembersProject Manager Aurora Public Schools Current term expires June 30, 2022

Ramon AlvaradoElected by State MembersAdjunct FacultyMetropolitan State University of DenverCurrent term expires June 30, 2022

Honorable Rebecca R. FreyreAppointed to Judicial Division seatJudge Colorado Court of AppealsCurrent term expires June 30, 2023

Honorable Will BainElected by Judicial Members Judge 4th Judicial District Term expired June 30, 2019

Julie FriedemannAppointed to Retiree seat Retired Mathematics Teacher Jefferson County School District Current term expires June 30, 2021

Introductory Section

BOARD OF TRUSTEES

18 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

Amy GrantNon-voting, Ex officio member Elected by DPS Division active members

and retirees Former Chair of the Denver Public Schools

Retirement System Board Retired Secretary Current term expires June 30, 2024

Susan G. MurphyAppointed by the Governor Current term expires July 10, 2021

David HallElected by State Members Sergeant and Legislative Liaison Colorado State Patrol Current term expires June 30, 2020

William N. ParkerElected by School Members International Baccalaureate

Coordinator and Literacy TeacherBrighton School District 27J Term to expire June 30, 2020

Roger P. JohnsonAppointed by the Governor Current term expires July 10, 2020

Cheryl PattelliAppointed to Local Government

Division seatChief Financial Officer City of Boulder Current term expires June 30, 2022

Suzanne E. KubecAppointed to State Division seat Liability Claims Manager State Office of Risk Management Current term expires June 30, 2021

Eric RothausDeputy State Treasurer Delegated Substitute for the State

Treasurer Continuous term effective January 2019

Robert LambElected by Local Government MembersFinance Division Director Boulder County Retired May 2019

Honorable Walker StapletonEx officio member State Treasurer Term ended January 2019

Tina MuehElected by School Members Middle School Science Teacher Boulder Valley School District Current term expires June 30, 2021

Honorable Dave YoungEx officio member State Treasurer Continuous term effective January 2019

Introductory Section

BOARD OF TRUSTEES

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 19

Final D

raft

June

12,

202

0

Introductory Section

ADMINISTRATIVE ORGANIZATIONAL CHART AND EXECUTIVE MANAGEMENTAs of June 1, 2020

20 Introductory Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

Fiduciary CounselBrownstein Hyatt Farber Schreck410 17th Street Suite 2200 Denver, CO 80202

Governance ConsultantCortex Applied Research, Inc. 2489 Bloor Street West Suite 304 Toronto, ON M6S 1R6 Canada

Health Care Program ConsultantIMA Financial Group, Inc. 1705 17th Street Suite 100 Denver, CO 80202

Independent AuditorsCliftonLarsonAllen LLP 370 Interlocken Boulevard Suite 500 Broomfield, CO 80021

Investment Performance ConsultantsAon Hewitt Investment Consulting, Inc. 200 East Randolph Street Suite 1500 Chicago, IL 60601

The Northern Trust Company50 South LaSalle Street Chicago, IL 60603

Investments—Portfolio ConsultantAon Hewitt Investment Consulting, Inc. 200 East Randolph Street Suite 1500 Chicago, IL 60601

Investments—Real Estate PerformanceAon Hewitt Investment Consulting, Inc. 200 East Randolph Street Suite 1500 Chicago, IL 60601

Master CustodianThe Northern Trust Company 50 South LaSalle Street Chicago, IL 60603

Pension and Health Care Program ActuarySegal 7951 East Maplewood AvenueSuite 327Greenwood Village, CO 80111

Pharmacy Benefits ConsultantsARMSRx Pharmacy Benefit Consulting 105 Down Court Windermere, FL 34786

Risk ManagementIMA of Colorado 1705 17th Street Suite 100 Denver, CO 80202

Voluntary Investment Program, DefinedContribution Retirement, and DeferredCompensation Plan Investment andPerformance ConsultantRVK, Inc. 1211 SW 5th Avenue Suite 900 Portland, OR 97204

Voluntary Investment Program, DefinedContribution Retirement, and DeferredCompensation Plan Service ProviderVoya Institutional Plan Services, LLC 30 Braintree Hill Office Park Braintree, MA 02184

A list of PERA’s Investment Brokers/Advisers, the Schedule of Commissions, and other information related to investment expenses can be found inthe Investment Section on pages 123-125.

Introductory Section

CONSULTANTSAs of December 31, 2019

Colorado PERA Comprehensive Annual Financial Report 2019 � Introductory Section 21

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

Financial Section

REPORT OF THE INDEPENDENT AUDITOR

Colorado PERA Comprehensive Annual Financial Report 2019 � Financial Section 25

Final D

raft

June

12,

202

0

Financial Section

REPORT OF THE INDEPENDENT AUDITOR

26 Financial Section � Colorado PERA Comprehensive Annual Financial Report 2019

Final D

raft

June

12,

202

0

Financial Section

REPORT OF THE INDEPENDENT AUDITOR

Colorado PERA Comprehensive Annual Financial Report 2019 � Financial Section 27

Final D

raft

June

12,

202

0

Final D

raft

June

12,

202

0

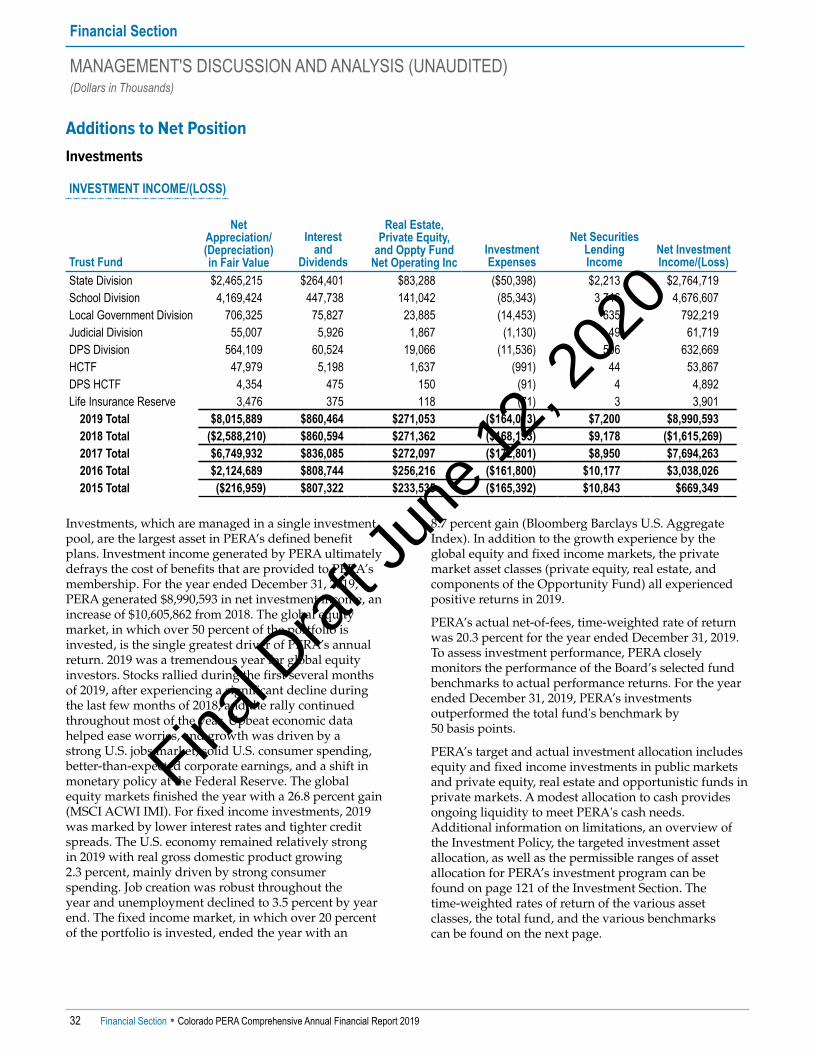

This Management’s Discussion and Analysis (MD&A)section provides a narrative overview and analysis ofthe financial activities of the Public Employees'Retirement Association of Colorado (PERA) for the yearended December 31, 2019. Please consider theinformation presented here in conjunction withadditional information in the Letter of Transmittalstarting on page 3 of this Comprehensive Annual FinancialReport (CAFR) and with the basic financial statements ofPERA on pages 44-47.

In addition to historical information, this MD&Aincludes forward-looking statements, which involvecertain risks and uncertainties. PERA’s actual results,performance, and achievements may differ materiallyfrom the results, performance, and achievementsexpressed or implied in such forward-lookingstatements, due to a wide range of factors, includingchanges in interest rates, changes in the capital markets,general economic conditions, legislative changes, as wellas other factors.

Overview of the AssociationPERA administers the following 11 fiduciary funds:

Plan NameDefined Benefit Pension Plans(Division Trust Funds)State Division Trust FundSchool Division Trust FundLocal Government Division Trust FundJudicial Division Trust FundDenver Public Schools (DPS) Division Trust Fund

Defined Benefit Other Postemployment Benefit Plans (Health Care Trust Funds)Health Care Trust Fund (HCTF)Denver Public Schools Health Care Trust Fund (DPS HCTF)

Defined Contribution PlansVoluntary Investment ProgramDefined Contribution Retirement Plan

Deferred Compensation PlanDeferred Compensation Plan

Private Purpose Trust FundLife Insurance Reserve

Additional information regarding the contribution andbenefit provisions of the plans can be found in Notes 1,8, and 9 of the Notes to the Financial Statements.

Legislative InitiativesGovernor Polis signed House Bill (HB) 19-1217:Concerning the Elimination of the Two Percent Increase in theMember Contribution Rate to the Public Employees'

Retirement Association in the Local Government of theAssociation into law on May 20, 2019, which eliminatedthe scheduled 2.0 percent increase in the membercontribution rate for the Local Government Division thatwas included in legislation passed in 2018. Thatlegislation increased contributions paid by all PERAmembers. While this new bill eliminates those increasedcontributions for members in the Local GovernmentDivision, all members are still subject to anyadjustments in contributions required to keep PERA onthe path to full funding by 2048 as defined within SenateBill (SB) 18-200. Contributions for all members, withincertain constraints, can increase (or decrease) by up to0.5 percent per year.

Financial Statement OverviewPERA’s financial statements are prepared inaccordance with governmental accounting standardsand the actuarial valuations that are reported in theActuarial Section are prepared in accordance with theActuarial Standards of Practice and the PERA Board’sFunding Policy.

Basic Financial StatementsPERA’s financial statements include the followingcomponents:

1. Basic Financial Statements

-Statements of Fiduciary Net Position

-Statements of Changes in Fiduciary Net Position

2. Notes to the Basic Financial Statements

3. Required Supplementary Information - Unaudited

4. Supplementary Schedules

The Statements of Fiduciary Net Position presentsinformation on PERA’s assets and liabilities, with thedifference between the two reported as fiduciary netposition. Over time, the increase or decrease in fiduciarynet position serves as an indicator of PERA’s financialcondition and our ability to fund future benefits.

The Statements of Changes in Fiduciary Net Positionreflects how PERA’s fiduciary net position (FNP)changed during the fiscal year, and includes additionssuch as contributions and investment income anddeductions such as benefit payments andadministrative expenses.

Notes to the Financial StatementsThe Notes to the Financial Statements provideinformation essential to understanding the basicfinancial statements.

Note 1—Plan Description: provides a generaldescription of PERA, the funds administered by PERA,

Financial Section

MANAGEMENT'S DISCUSSION AND ANALYSIS (UNAUDITED)(Dollars in Thousands)

Colorado PERA Comprehensive Annual Financial Report 2019 � Financial Section 29

Final D

raft

June

12,

202

0

and a general overview of plan provisions for thedefined benefit pension trust funds.

Note 2—Summary of Significant Accounting Policies:provides a summary of significant accounting policies,including the basis of accounting for PERA, andmanagement’s use of estimates.

Note 3—Interfund Transfers and Balances: providesinformation related to interfund activity and balances.