Final FATCA Regulations: Implications for U.S. Taxpayers Leveraging Benefits for Taxpayers Holding Assets in Offshore Financial Institutions or Other Vehicles Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. THURSDAY, MARCH 28, 2013 Presenting a live 110-minute teleconference with interactive Q&A Randall Andreozzi, Partner, Andreozzi Bluestein Fickess Muhlbauer Weber Brown, Clarence, N.Y. Susan Segar, Partner, Burt Staples & Maner, Washington, D.C. Kelli Wooten, Of Counsel, Burt Staples & Maner, Boston Matthew D. Lee, Partner, Blank Rome, Philadelphia For this program, attendees must listen to the audio over the telephone.

Transcript

Final FATCA Regulations:

Implications for U.S. Taxpayers Leveraging Benefits for Taxpayers Holding Assets in Offshore Financial Institutions or Other Vehicles

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

THE FOREIGN ACCOUNT TAX COMPLIANCE ACT: BACKGROUND AND GOALS

Matthew D. Lee, Blank Rome LLP

Matthew D. Lee is a former U.S. Department of Justice trial attorney who concentrates his practice on all aspects of white collar criminal defense and federal tax controversies. He has extensive experience in advising clients on issues regarding foreign bank account reporting (FBAR) obligations, the Foreign Account Tax Compliance Act (FATCA), and the Internal Revenue Service’s 2009 Offshore Voluntary Disclosure Program, 2011 Offshore Voluntary Disclosure Initiative, and 2012 Offshore Voluntary Disclosure Program. He has represented hundreds of U.S. taxpayers with undisclosed foreign bank accounts. Mr. Lee has published numerous articles regarding the IRS voluntary disclosure programs and FBAR and FATCA reporting obligations and speaks frequently on these topics.

He has also represented clients in all stages of proceedings before the Internal Revenue Service, including audits, appeals, and collections, and Tax Court litigation. Mr. Lee also has experience in conducting corporate internal investigations and advising clients as to corporate compliance issues involving the Bank Secrecy Act, the USA Patriot Act, and anti-money laundering laws and regulations.

Mr. Lee has represented both corporations and individuals in criminal investigations involving tax, money laundering, health care, securities, public corruption, and fraud offenses, and has significant experience in handling all stages of federal litigation including trials and appeals.

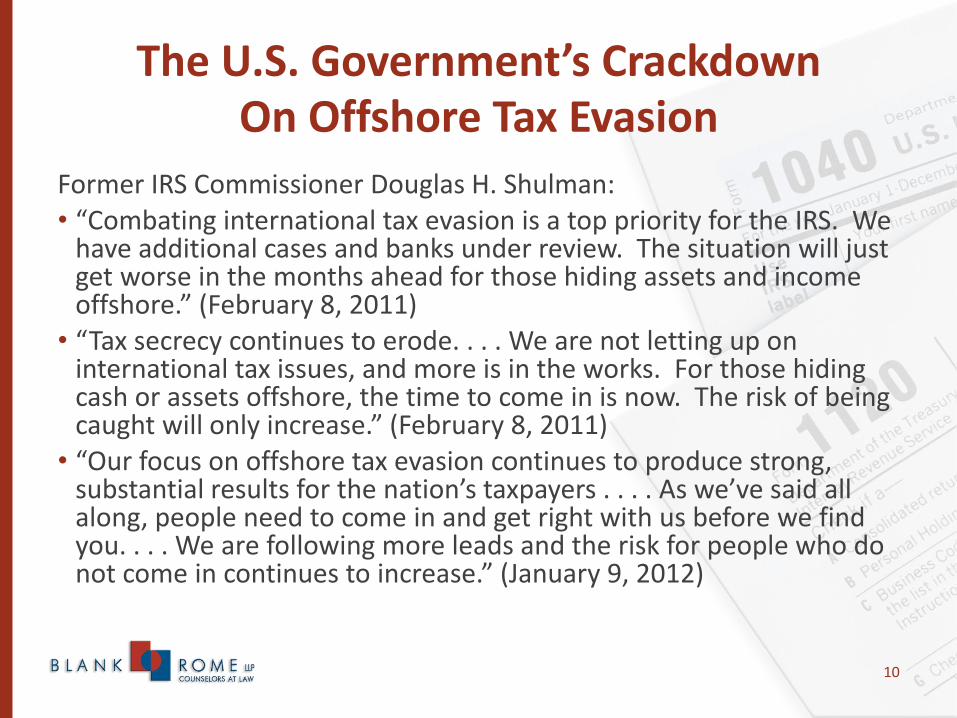

The U.S. Government’s Crackdown On Offshore Tax Evasion

Former IRS Commissioner Douglas H. Shulman: • “Combating international tax evasion is a top priority for the IRS. We

have additional cases and banks under review. The situation will just get worse in the months ahead for those hiding assets and income offshore.” (February 8, 2011)

• “Tax secrecy continues to erode. . . . We are not letting up on international tax issues, and more is in the works. For those hiding cash or assets offshore, the time to come in is now. The risk of being caught will only increase.” (February 8, 2011)

• “Our focus on offshore tax evasion continues to produce strong, substantial results for the nation’s taxpayers . . . . As we’ve said all along, people need to come in and get right with us before we find you. . . . We are following more leads and the risk for people who do not come in continues to increase.” (January 9, 2012)

10

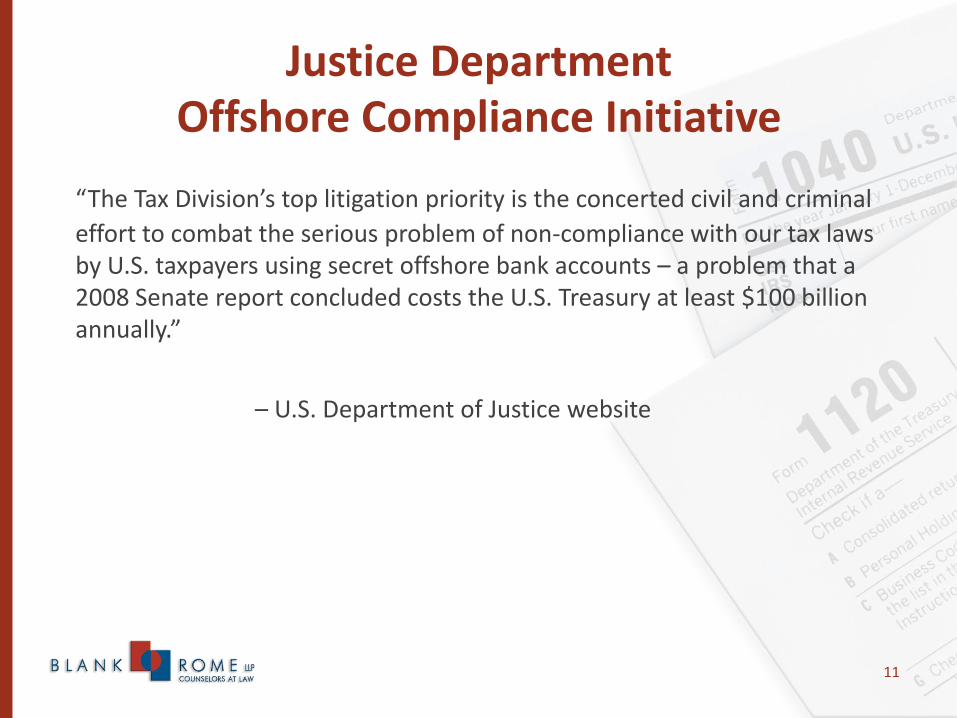

Justice Department Offshore Compliance Initiative

“The Tax Division’s top litigation priority is the concerted civil and criminal

effort to combat the serious problem of non-compliance with our tax laws by U.S. taxpayers using secret offshore bank accounts – a problem that a 2008 Senate report concluded costs the U.S. Treasury at least $100 billion annually.”

– U.S. Department of Justice website

11

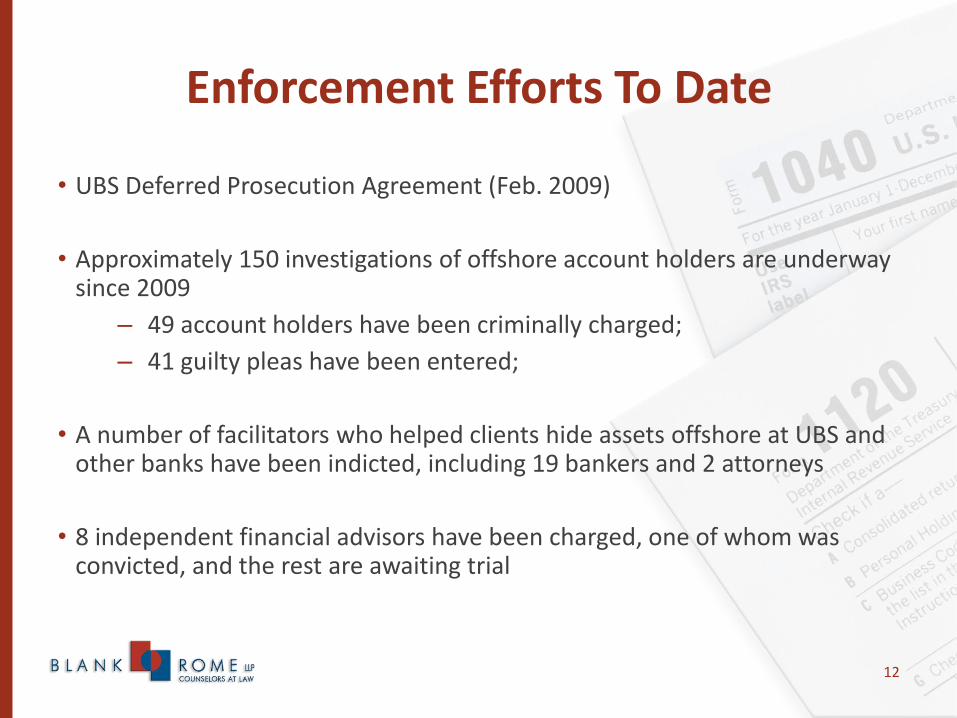

Enforcement Efforts To Date

• UBS Deferred Prosecution Agreement (Feb. 2009)

• Approximately 150 investigations of offshore account holders are underway since 2009

– 49 account holders have been criminally charged;

– 41 guilty pleas have been entered;

• A number of facilitators who helped clients hide assets offshore at UBS and other banks have been indicted, including 19 bankers and 2 attorneys

• 8 independent financial advisors have been charged, one of whom was convicted, and the rest are awaiting trial

12

Enforcement Efforts To Date (Cont.)

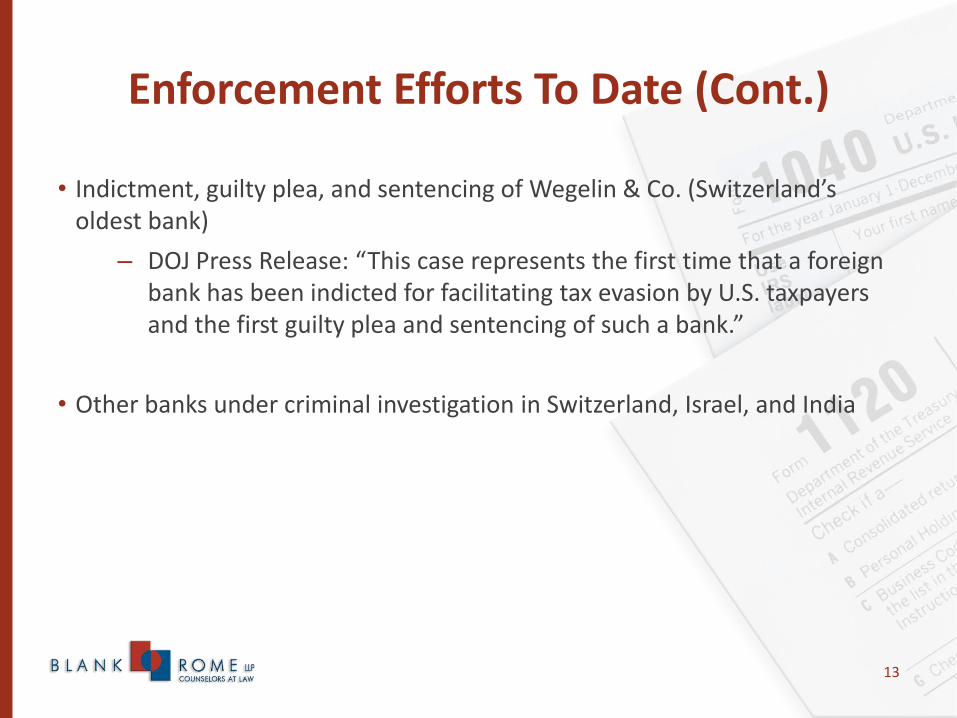

• Indictment, guilty plea, and sentencing of Wegelin & Co. (Switzerland’s oldest bank)

– DOJ Press Release: “This case represents the first time that a foreign bank has been indicted for facilitating tax evasion by U.S. taxpayers and the first guilty plea and sentencing of such a bank.”

• Other banks under criminal investigation in Switzerland, Israel, and India

13

What Is FATCA?

• “The Foreign Account Tax Compliance Act (FATCA) is an important development in U.S. efforts to improve tax compliance involving foreign financial assets and offshore accounts.” (www.IRS.gov)

• “FATCA was enacted in 2010 by Congress to target non-compliance by U.S. taxpayers using foreign accounts. FATCA requires foreign financial institutions (FFIs) to report to the IRS information about financial accounts held by U.S. taxpayers, or by foreign entities in which U.S. taxpayers hold a substantial ownership interest.” (www.treasury.gov)

• Enacted by Congress in 2010 as part of the Hiring Incentives to Restore Employment (HIRE) Act; added Chapter 4 of Subtitle A of Internal Revenue Code, and new IRC sections 1471 through 1474

• Numerous comments received; public hearing held on May 15, 2012

• Announcement 2012-42 issued October 24, 2012

• Final regulations issued January 17, 2013

15

FATCA Policy In Context Of U.S. Tax Laws

• U.S. taxpayers’ investments have become increasingly global in scope

• Recognition that foreign financial institutions (FFIs) are in best position to identify and report with respect to their U.S. account holders

• Absent reporting by FFIs, some U.S. taxpayers may attempt to evade U.S. tax by hiding money in offshore accounts

• “To prevent this abuse of the U.S. voluntary tax compliance system and address the use of offshore accounts to facilitate tax evasion, it is essential in today’s global investment climate that reporting be available with respect to both the onshore and offshore accounts of U.S. taxpayers.” (Preamble to Final Regulations)

16

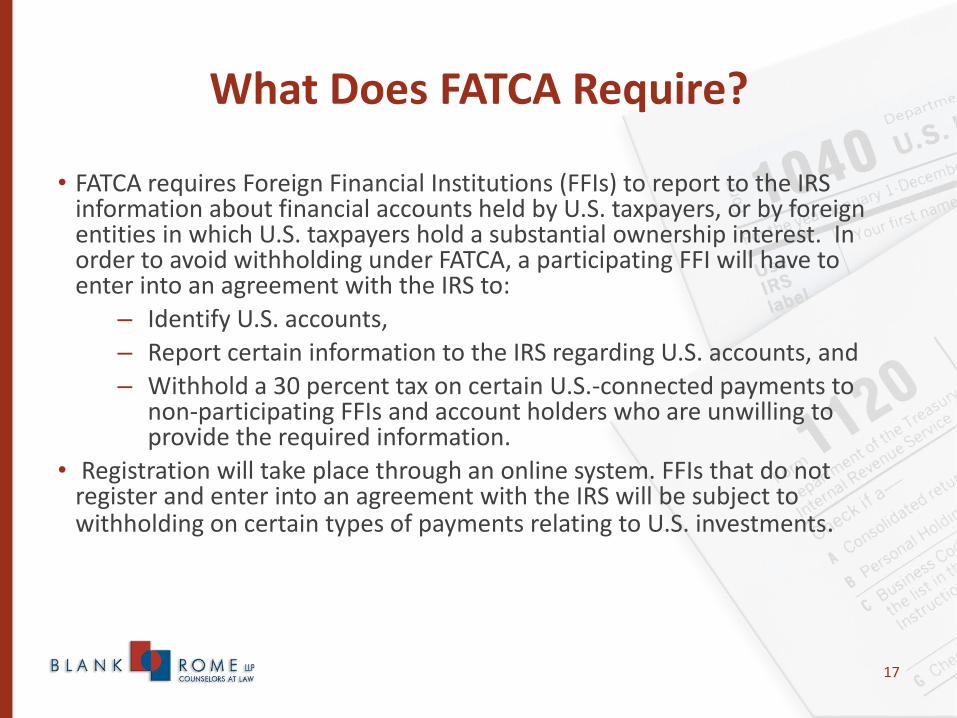

What Does FATCA Require?

• FATCA requires Foreign Financial Institutions (FFIs) to report to the IRS information about financial accounts held by U.S. taxpayers, or by foreign entities in which U.S. taxpayers hold a substantial ownership interest. In order to avoid withholding under FATCA, a participating FFI will have to enter into an agreement with the IRS to:

– Identify U.S. accounts,

– Report certain information to the IRS regarding U.S. accounts, and

– Withhold a 30 percent tax on certain U.S.-connected payments to non-participating FFIs and account holders who are unwilling to provide the required information.

• Registration will take place through an online system. FFIs that do not register and enter into an agreement with the IRS will be subject to withholding on certain types of payments relating to U.S. investments.

17

Slide Intentionally Left Blank

International Coordination And Model Intergovernmental Agreements

• Treasury is collaborating with foreign governments to develop two alternative model intergovernmental agreements that facilitate the effective and efficient implementation of FATCA.

• Model 1 IGA: FFIs in jurisdictions that have signed Model 1 IGAs report the information about U.S. accounts required by FATCA to their respective governments who then exchange this information with the IRS.

• Model 2 IGA: A partner jurisdiction signing an agreement based on the Model 2 IGA agrees to direct its FFIs to register with the IRS and report the information about U.S. accounts required by FATCA directly to the IRS.

19

International Coordination (Cont.)

• To date, United Kingdom, Mexico, Denmark, Ireland, Switzerland, Spain, and Norway have signed or initialed model agreements.

• Treasury is engaged with more than 50 countries and jurisdictions to curtail offshore tax evasion, and more signed agreements are expected to follow in the near future.

20

Final Regulations Issued Jan. 17, 2013

• “These regulations give the Administration a powerful set of tools to combat offshore tax evasion effectively and efficiently. The final rules mark a critical milestone in international cooperation on these issues, and they provide important clarity for foreign and U.S. financial institutions.”

– Treasury Department press release

21

FATCA Also Requires Reporting Of Foreign Assets By U.S. Taxpayers

• U.S. taxpayers with “specified foreign financial assets” that exceed certain thresholds must now report those assets to the IRS.

• A specified foreign financial asset includes (1) financial accounts maintained by foreign financial institutions and (2) other foreign financial assets held for investment such as foreign stocks or securities, interests in a foreign entity, any financial instrument or contract that has as an issuer or counterparty that is other than a U.S. person, foreign pensions and deferred compensation plans, and certain foreign trusts and estates

• Form 8938, “Statement of Foreign Financial Assets,” must be filed with the tax return.

22

OVERVIEW OF FATCA PROVISIONS

Susan Segar, Burt, Staples & Maner LLP

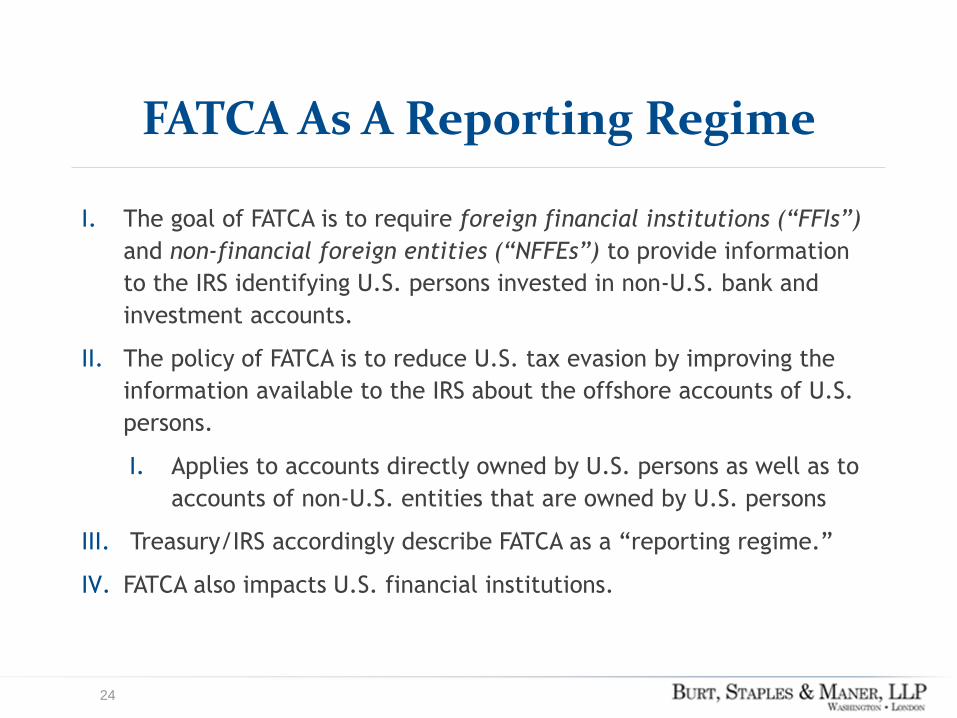

FATCA As A Reporting Regime

I. The goal of FATCA is to require foreign financial institutions (“FFIs”)

and non-financial foreign entities (“NFFEs”) to provide information

to the IRS identifying U.S. persons invested in non-U.S. bank and

investment accounts.

II. The policy of FATCA is to reduce U.S. tax evasion by improving the

information available to the IRS about the offshore accounts of U.S.

persons.

I. Applies to accounts directly owned by U.S. persons as well as to

accounts of non-U.S. entities that are owned by U.S. persons

III. Treasury/IRS accordingly describe FATCA as a “reporting regime.”

IV. FATCA also impacts U.S. financial institutions.

24

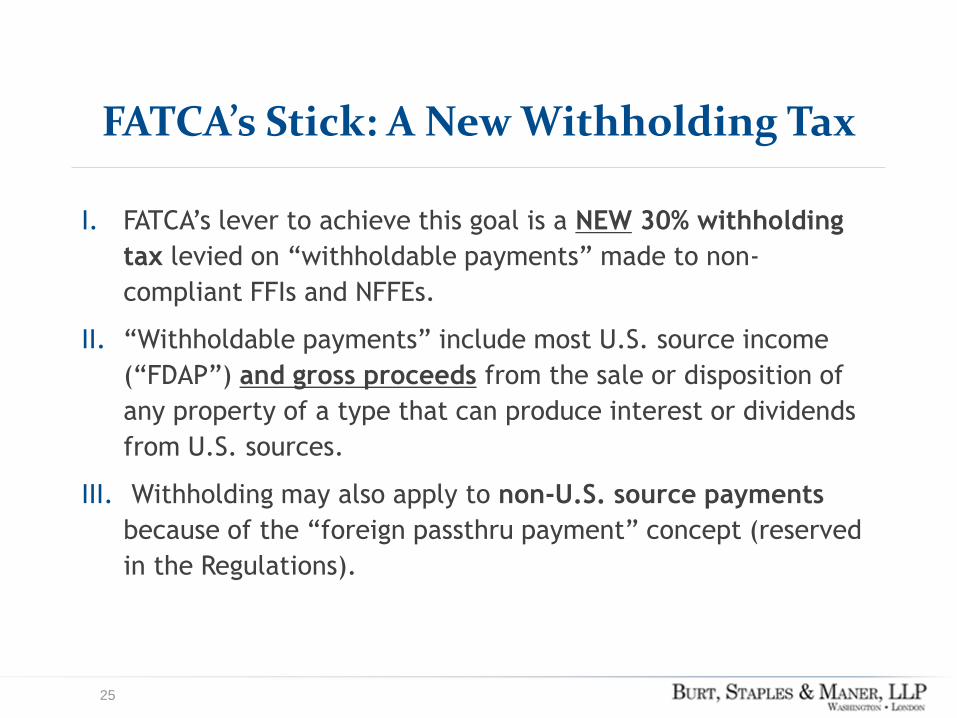

FATCA’s Stick: A New Withholding Tax

I. FATCA’s lever to achieve this goal is a NEW 30% withholding

tax levied on “withholdable payments” made to non-

compliant FFIs and NFFEs.

II. “Withholdable payments” include most U.S. source income

(“FDAP”) and gross proceeds from the sale or disposition of

any property of a type that can produce interest or dividends

from U.S. sources.

III. Withholding may also apply to non-U.S. source payments

because of the “foreign passthru payment” concept (reserved

in the Regulations).

25

Financial Institutions

I. Broad definition that includes any entity that:

A. Accepts deposits

B. Holds financial assets for the account of others

C. Acts as an “investment entity”, or

D. Engages in certain insurance businesses.

II. Foreign financial institution (“FFI”) - Any financial institution that is

a foreign entity (i.e., in general, an entity organized or created

outside the U.S.)

III. U.S. Financial Institutions (“USFI”) – Generally, any financial

institution that is a U.S. entity

I. Does not include branches of U.S. financial institutions in IGA

countries

26

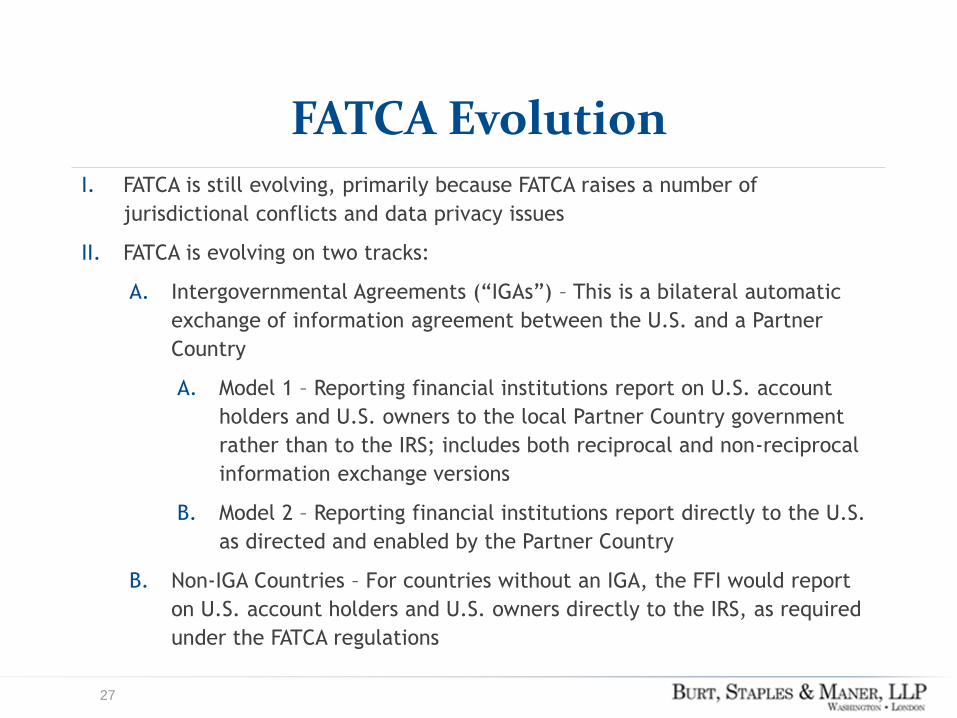

FATCA Evolution I. FATCA is still evolving, primarily because FATCA raises a number of

jurisdictional conflicts and data privacy issues

II. FATCA is evolving on two tracks:

A. Intergovernmental Agreements (“IGAs”) – This is a bilateral automatic

exchange of information agreement between the U.S. and a Partner

Country

A. Model 1 – Reporting financial institutions report on U.S. account

holders and U.S. owners to the local Partner Country government

rather than to the IRS; includes both reciprocal and non-reciprocal

information exchange versions

B. Model 2 – Reporting financial institutions report directly to the U.S.

as directed and enabled by the Partner Country

B. Non-IGA Countries – For countries without an IGA, the FFI would report

on U.S. account holders and U.S. owners directly to the IRS, as required

under the FATCA regulations

27

Compliant FFIs

I. To avoid FATCA withholding on withholdable payments, an FFI must

be compliant with FATCA.

II. To achieve compliance, an FFI must do one of the following:

A. In general, be located in an “intergovernmental agreement”

(“IGA”) jurisdiction and comply as a “reporting financial

institution.”

B. Enter into an “FFI Agreement” with the IRS with the attendant

obligations (“participating FFI”).

C. Belong to a class of institutions that Treasury/IRS – or an IGA

(including in IGA Annex II) – have designated as exempt or

“deemed-compliant.”

III. FFIs that are not deemed-compliant or that are not otherwise

compliant with FATCA are considered non-participating FFIs, and are

subject to FATCA withholding on withholdable payments.

28

Reporting IGA FIs

I. Reporting IGA FIs are generally subject to the rules set forth in

the IGA that was signed by their home country government, and

not those in the FATCA regulations

II. As with FFIs that are not in IGA countries, Reporting IGA FIs have

an due diligence, reporting and withholding obligations

I. Those obligations, however, are generally less stringent than

those applicable FFIs in non-IGA countries

III. Reporting IGA FIs are deemed to be compliant with FATCA, and

thus are not subject to 30% FATCA withholding on withholdable

payments received

IV. To date, the U.S. Treasury has signed or initialed Model 1 IGA

Agreements with 8 countries, and one Model 2 IGA Agreement.

29

Participating FFIs

I. A participating FFI (“PFFI”) must enter into an FFI agreement with the IRS to

do all of the following:

A. Identify its “U.S. accounts” including by all its worldwide affiliates;

B. Comply with due diligence criteria to ensure that it has really identified

its U.S. accounts;

C. Provide the IRS with an annual report with details about the U.S.

accounts that it has found;

D. Deduct and withhold 30% on withholdable payments made to

“recalcitrant account holders” or non-participating FFIs;

E. Provide any follow-up information requested by the IRS with respect to

the U.S. accounts; and

F. Request a waiver from any U.S. account holder if disclosure would

otherwise be prohibited on the basis of non-U.S. law (e.g., privacy or

bank secrecy laws), and close the account if the account holder refuses

to cooperate.

30

Slide Intentionally Left Blank

Deemed-Compliant FFIs

I. Treasury and the IRS have determined that certain financial institutions pose

a low risk of harboring U.S. tax evaders, and therefore should be deemed to

comply with FATCA.

II. There are two types of deemed-compliant FFIs – registered deemed-compliant

FFIs and certified deemed-compliant FFIs.

III. Registered deemed-compliant FFIs must still register with the IRS but are not

required to enter into an FFI Agreement.

A. Examples include Reporting IGA FFIs, and certain qualified collective

investment vehicles and qualified credit card issuers.

IV. Certified deemed-compliant FFIs are not required to register with the IRS but

must certify their status on Form W-8.

A. Examples include certain non-registering local banks and FFIs with only

low value accounts.

V. The IGAs also set forth in Annex II certain home country FIs that are treated

as deemed-compliant with FATCA.

32

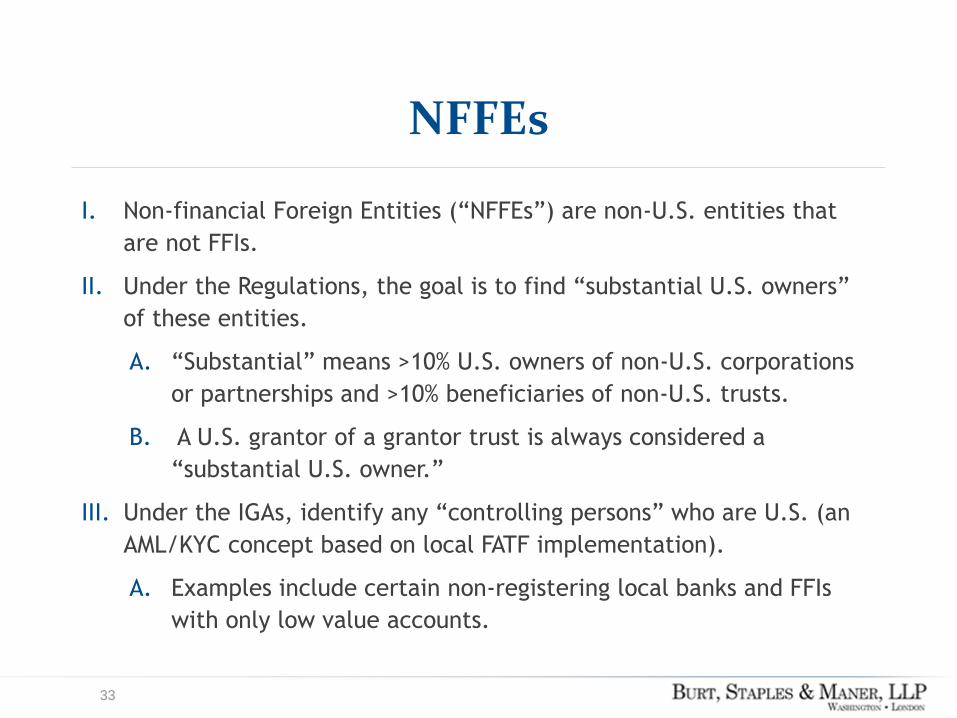

NFFEs

I. Non-financial Foreign Entities (“NFFEs”) are non-U.S. entities that

are not FFIs.

II. Under the Regulations, the goal is to find “substantial U.S. owners”

of these entities.

A. “Substantial” means >10% U.S. owners of non-U.S. corporations

or partnerships and >10% beneficiaries of non-U.S. trusts.

B. A U.S. grantor of a grantor trust is always considered a

“substantial U.S. owner.”

III. Under the IGAs, identify any “controlling persons” who are U.S. (an

AML/KYC concept based on local FATF implementation).

A. Examples include certain non-registering local banks and FFIs

with only low value accounts.

33

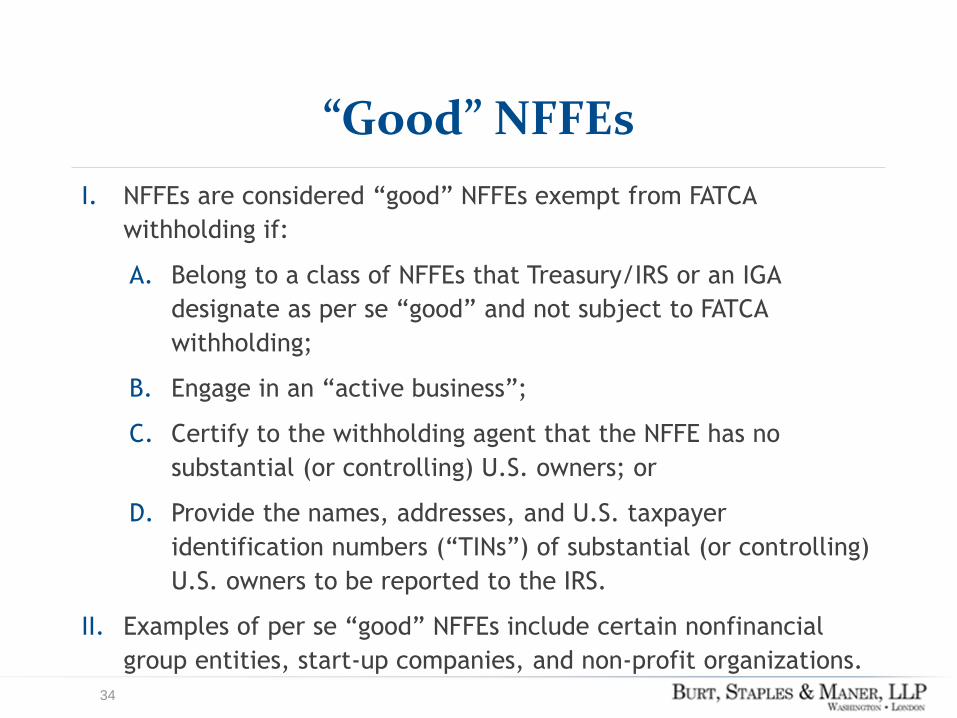

“Good” NFFEs

I. NFFEs are considered “good” NFFEs exempt from FATCA

withholding if:

A. Belong to a class of NFFEs that Treasury/IRS or an IGA

designate as per se “good” and not subject to FATCA

withholding;

B. Engage in an “active business”;

C. Certify to the withholding agent that the NFFE has no

substantial (or controlling) U.S. owners; or

D. Provide the names, addresses, and U.S. taxpayer

identification numbers (“TINs”) of substantial (or controlling)

U.S. owners to be reported to the IRS.

II. Examples of per se “good” NFFEs include certain nonfinancial

group entities, start-up companies, and non-profit organizations.

34

FATCA’S IMPACT ON FINANCIAL INSTITUTIONS

Kelli Wooten, Burt, Staples & Maner LLP

FATCA Requirements

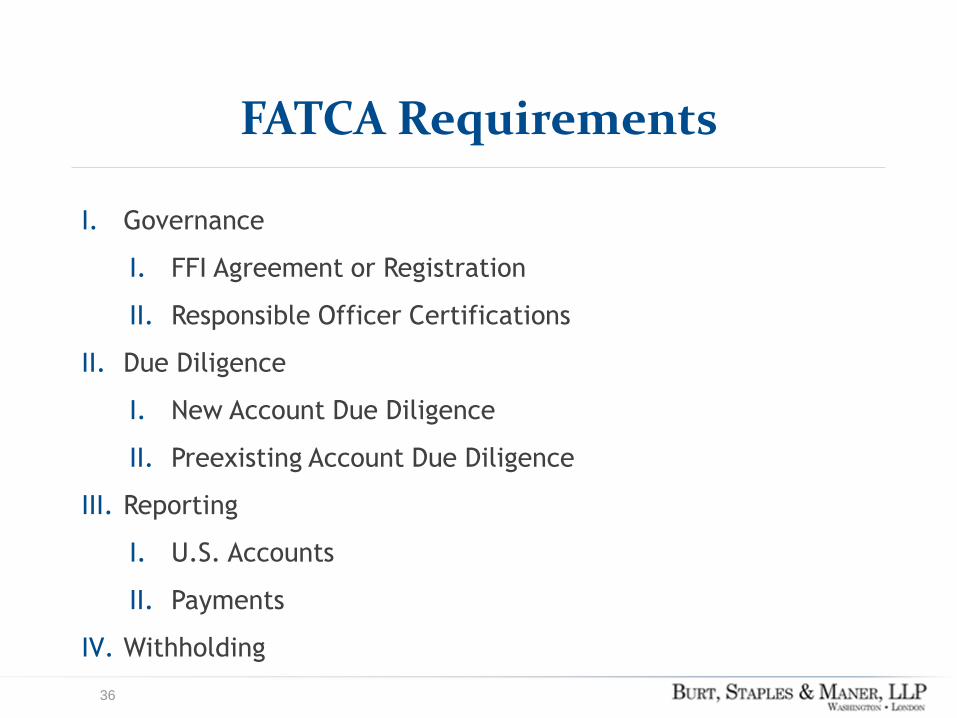

I. Governance

I. FFI Agreement or Registration

II. Responsible Officer Certifications

II. Due Diligence

I. New Account Due Diligence

II. Preexisting Account Due Diligence

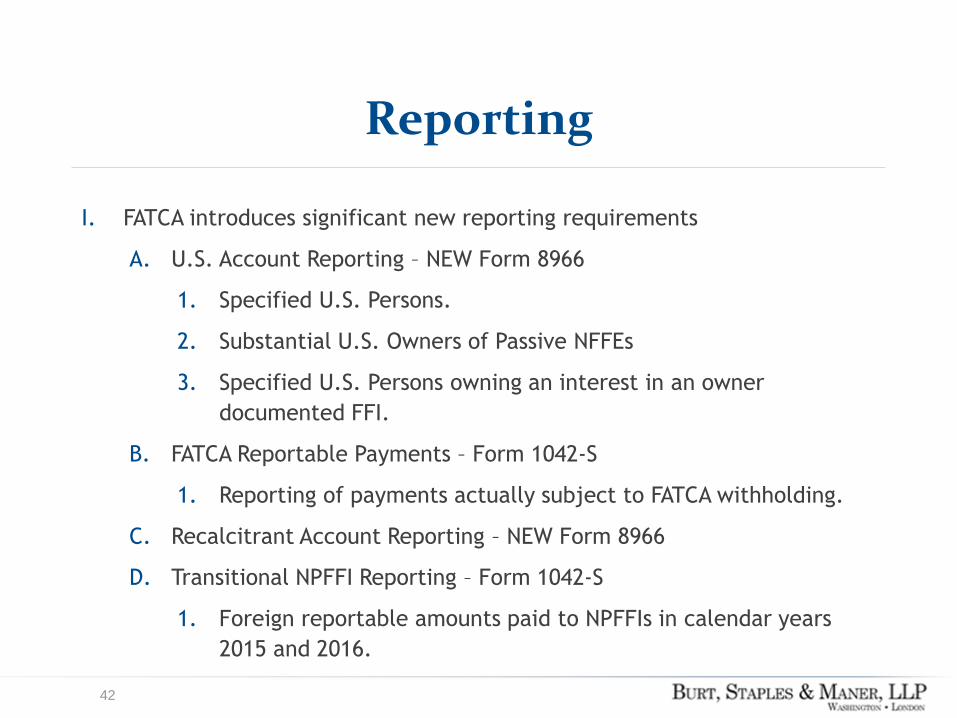

III. Reporting

I. U.S. Accounts

II. Payments

IV. Withholding

36

Governance

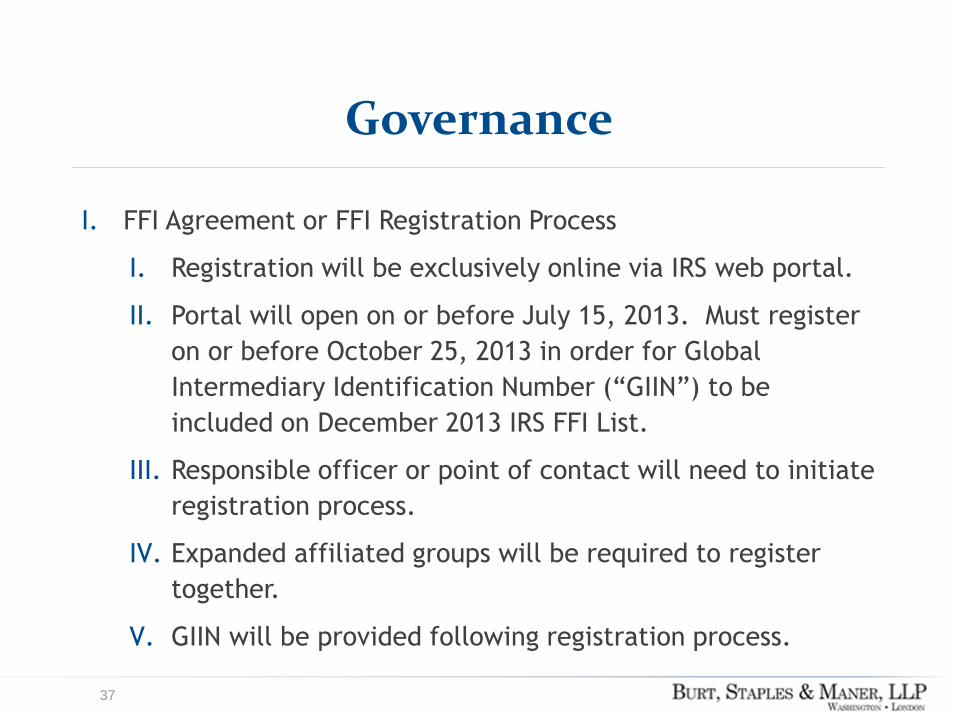

I. FFI Agreement or FFI Registration Process

I. Registration will be exclusively online via IRS web portal.

II. Portal will open on or before July 15, 2013. Must register

on or before October 25, 2013 in order for Global

Intermediary Identification Number (“GIIN”) to be

included on December 2013 IRS FFI List.

III. Responsible officer or point of contact will need to initiate

registration process.

IV. Expanded affiliated groups will be required to register

together.

V. GIIN will be provided following registration process.

37

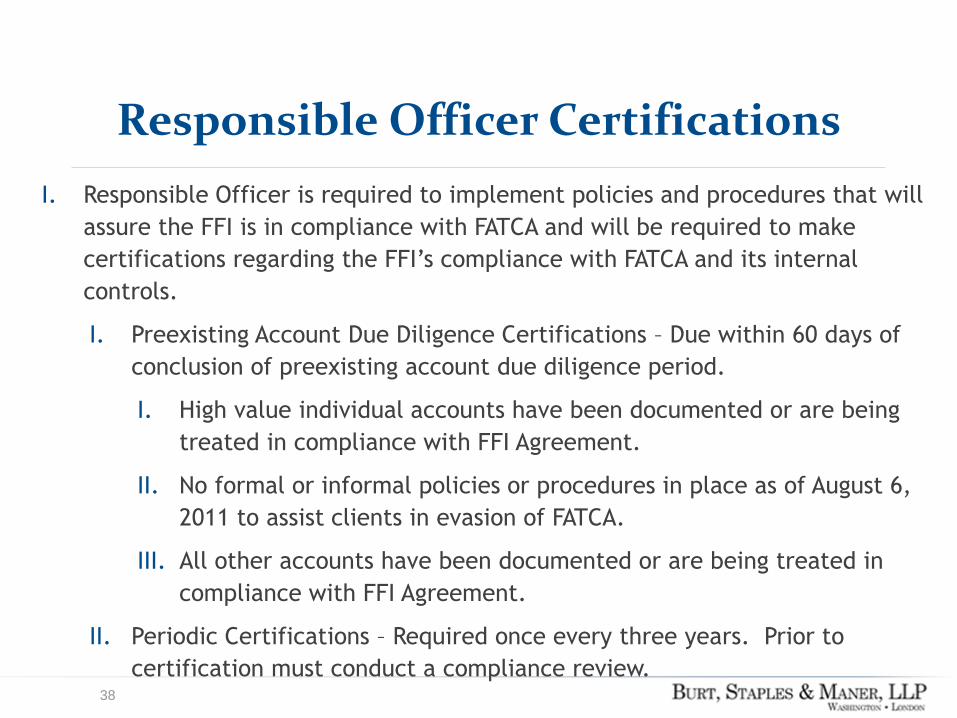

Responsible Officer Certifications

I. Responsible Officer is required to implement policies and procedures that will

assure the FFI is in compliance with FATCA and will be required to make

certifications regarding the FFI’s compliance with FATCA and its internal

controls.

I. Preexisting Account Due Diligence Certifications – Due within 60 days of

conclusion of preexisting account due diligence period.

I. High value individual accounts have been documented or are being

treated in compliance with FFI Agreement.

II. No formal or informal policies or procedures in place as of August 6,

2011 to assist clients in evasion of FATCA.

III. All other accounts have been documented or are being treated in

compliance with FFI Agreement.

II. Periodic Certifications – Required once every three years. Prior to

certification must conduct a compliance review.

38

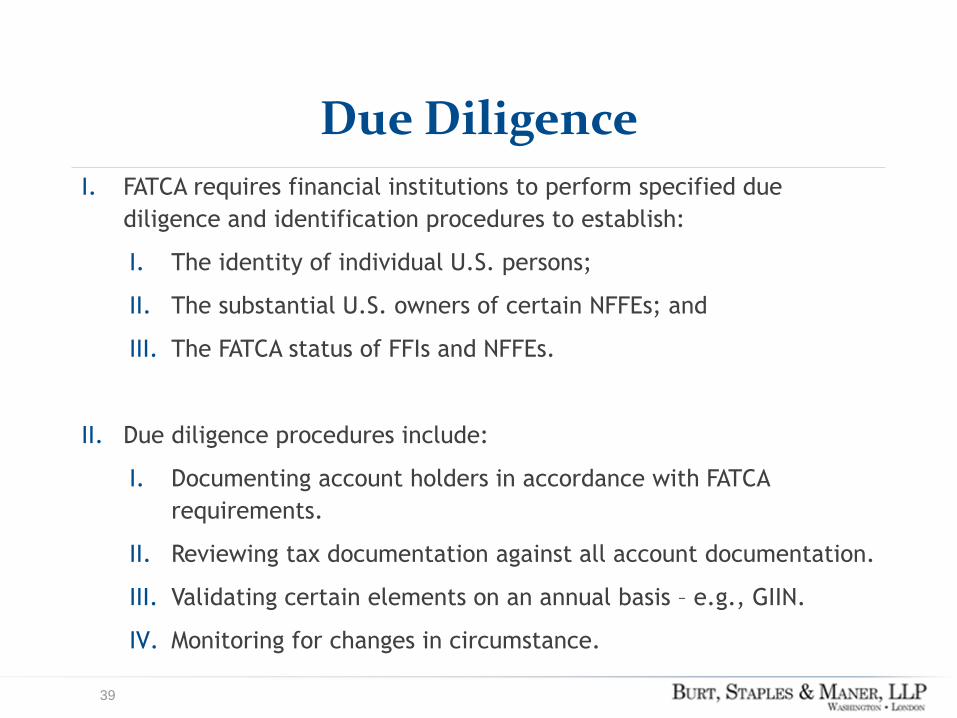

Due Diligence

I. FATCA requires financial institutions to perform specified due

diligence and identification procedures to establish:

I. The identity of individual U.S. persons;

II. The substantial U.S. owners of certain NFFEs; and

III. The FATCA status of FFIs and NFFEs.

II. Due diligence procedures include:

I. Documenting account holders in accordance with FATCA

requirements.

II. Reviewing tax documentation against all account documentation.

III. Validating certain elements on an annual basis – e.g., GIIN.

IV. Monitoring for changes in circumstance.

39

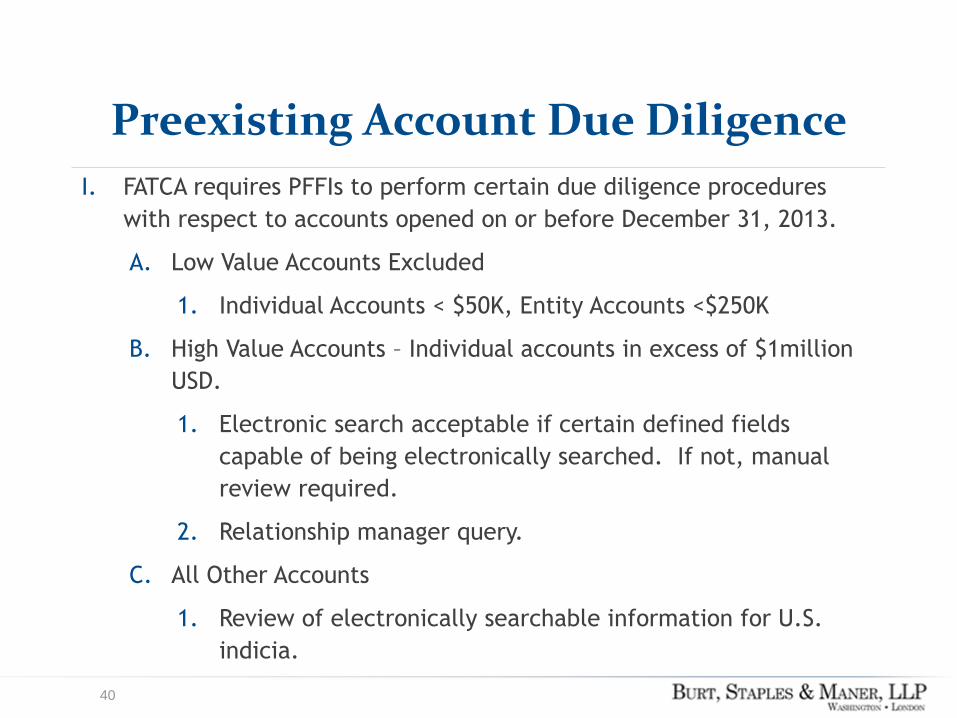

Preexisting Account Due Diligence

I. FATCA requires PFFIs to perform certain due diligence procedures

with respect to accounts opened on or before December 31, 2013.