47

DEVELOPMENT OPTIONS APPRAISAL FOR HERNE BAY PIER ON BEHALF OF CANTERBURY CITY COUNCIL FINAL REPORT JANUARY 2010 HLL Development Options Appraisal – Herne Bay Pier 1

DEVELOPMENT OPTIONS APPRAISAL FOR

HERNE BAY PIER

ON BEHALF OF CANTERBURY CITY COUNCIL

FINAL REPORT JANUARY 2010

HLL Development Options Appraisal – Herne Bay Pier 1

CONTENTS 1 INTRODUCTION ........................................................................................................................................ 3

1.1 BACKGROUND ......................................................................................................................................... 31.2 HUMBERTS LEISURE LTD ......................................................................................................................... 31.3 METHODOLOGY ....................................................................................................................................... 31.4 RECOGNITION OF RISK............................................................................................................................. 4

2 SITE & SURROUNDINGS ......................................................................................................................... 5

2.1 INTRODUCTION ........................................................................................................................................ 52.2 THE SITE ................................................................................................................................................ 52.3 SURROUNDINGS ...................................................................................................................................... 72.4 REVIEW OF PREVIOUS STUDIES................................................................................................................ 72.5 SITE SUMMARY ....................................................................................................................................... 8

3 DEMOGRAPHIC & VISITOR APPRAISAL ............................................................................................... 9

3.1 INTRODUCTION ........................................................................................................................................ 93.2 LOCATION & ACCESSIBILITY ..................................................................................................................... 93.3 LOCAL POPULATION PROFILE ................................................................................................................. 103.4 ECONOMIC ENVIRONMENT ..................................................................................................................... 123.5 TOURISM............................................................................................................................................... 133.6 REGENERATION & KEY LOCAL DEVELOPMENTS....................................................................................... 143.7 STAKEHOLDER CONSULTATIONS............................................................................................................. 153.8 SUMMARY OF LOCAL DEMAND POTENTIAL............................................................................................... 16

4 MARKET ANALYSIS ............................................................................................................................... 17

4.1 INTRODUCTION ...................................................................................................................................... 174.2 FOOD & BEVERAGE ............................................................................................................................... 174.3 CONFERENCING, MEETINGS & EVENTS ................................................................................................... 194.4 VISITOR ATTRACTIONS........................................................................................................................... 204.5 INDOOR CHILDREN’S PLAY ..................................................................................................................... 244.6 OTHER URBAN LEISURE......................................................................................................................... 254.7 RETAIL OPPORTUNITIES......................................................................................................................... 274.8 ARTIST’S QUARTER ............................................................................................................................... 284.9 MARINA................................................................................................................................................. 284.10 WATERSPORTS ................................................................................................................................ 29 4.11 CABLE CAR...................................................................................................................................... 304.12 ENABLING DEVELOPMENT................................................................................................................. 324.13 COMMERCIAL INVESTMENT POTENTIAL - CONCLUSION........................................................................ 334.14 SUMMARY........................................................................................................................................ 34

5 DEVELOPMENT OPTIONS APPRAISAL ............................................................................................... 36

5.1 INTRODUCTION ...................................................................................................................................... 365.2 PIER PAVILION OPTIONS ........................................................................................................................ 365.3 DEVELOPMENT PHASE ONE (EVENTS SPACE) ......................................................................................... 375.4 DEVELOPMENT PHASE TWO (TRADITIONAL PIER) .................................................................................... 385.5 LONGER-TERM DEVELOPMENT OPTIONS................................................................................................. 395.6 ENABLING DEVELOPMENT & FUNDING POTENTIAL ................................................................................... 435.7 SUMMARY OF POTENTIAL DEVELOPMENT OPPORTUNITIES ....................................................................... 445.8 UNACCEPTABLE ALTERNATIVE OPTIONS ................................................................................................. 45

6 KEY RECOMMENDATIONS.................................................................................................................... 47

6.1 SHORT-TERM RECOMMENDATIONS......................................................................................................... 476.2 MEDIUM TO LONG-TERM RECOMMENDATIONS......................................................................................... 47

HLL Development Options Appraisal – Herne Bay Pier 2

1 INTRODUCTION

1.1 Background A wooden pier was first opened in Herne Bay in the 1830s, although this was subsequently demolished in 1870. A replacement iron pier was subsequently constructed in 1896 and was, in the late 1970s, the second longest Pier in the UK. Since this time, however, Herne Bay Pier has suffered due to a number of factors including storm damage to the extent that the Pier Head is now isolated from the rest of the structure. A sports centre was constructed and opened at the shore end of the Pier in 1976, but the activities catered for are due to be relocated to a new location by 2011. There is therefore a question mark over the future of the Pier. Canterbury City Council has identified the Pier as a regeneration priority – and views the Pier as integral to any future regeneration plans for the town. In addition, the Council has helped to establish the Herne Bay Pier Trust to preserve, restore and enhance the existing structure. Due to the impending closure of the Pier Sports Centre in 2011, HLL Humberts Leisure has been commissioned to undertake an initial options appraisal for the site, with a view to ensuring a sustainable and viable long-term leisure-led development on Herne Bay Pier.

1.2 Humberts Leisure Ltd HLL Humberts Leisure is a firm of specialist advisors in tourism and leisure business and property. The company operates out of five offices nationwide, with over fifty staff dealing with all aspects of leisure and community property. Our Consulting team provides strategic property advice to clients in the leisure industry ranging from local authorities, major institutions, private land owners and property investors to business occupiers of commercial and leisure property. Over the years we have built up considerable contacts and clients within the public and private sector and we have a clear understanding of trends and development via our comprehensive research databases which monitor property transactions, activity and trends in the leisure sector. Our current work experience ranges from SE Asia, through Europe and the UK to the West Indies.

1.3 Methodology In order to complete this study we have undertaken the following: • Site visit to Herne Bay and Herne Bay Pier, as well as meetings with key

Council officers and the Pier Trust; • An evaluation of demand through consideration of the number of visitors to

the area an analysis of the local population and a review of other business and regeneration activity;

• A review of current market trends in the relevant business sectors; • A quantitative and qualitative assessment of competing and complementary

facilities in the local area; and • Initial canvassing of interest in specific opportunities from potential developers

and operators of relevance.

HLL Development Options Appraisal – Herne Bay Pier 3

1.4 Recognition of Risk Our estimates and conclusions have been prepared on the basis of information from you upon which we have relied, our own knowledge of demand generators and trends, our in-house database of information, and the status of the competitive market at the time of our research in August, September and October 2009. We have made no provision for any unforeseen events which could impact the leisure or tourism markets in the UK. This report is provided for the stated purpose agreed in our correspondence and is for use only of the parties to whom it is addressed, or their appointees. It is not suitable for any other use or any other persons and should not be treated as valuation for loan security or any other valuation purposes. As per our standard practice, neither the whole nor any part of this report, or any reference thereto may be included in any document, circular or statement without our prior approval of the form and context in which it will appear. As is customary with market studies, our findings should be regarded as valid for a limited period of time of six months and should be subject to examination at regular intervals.

HLL Development Options Appraisal – Herne Bay Pier 4

2 SITE & SURROUNDINGS

2.1 Introduction In this section, we consider the background to the site in greater detail. This is with a view to identifying potential development opportunities that may exist to further unlock the regeneration potential of Herne Bay and its Pier.

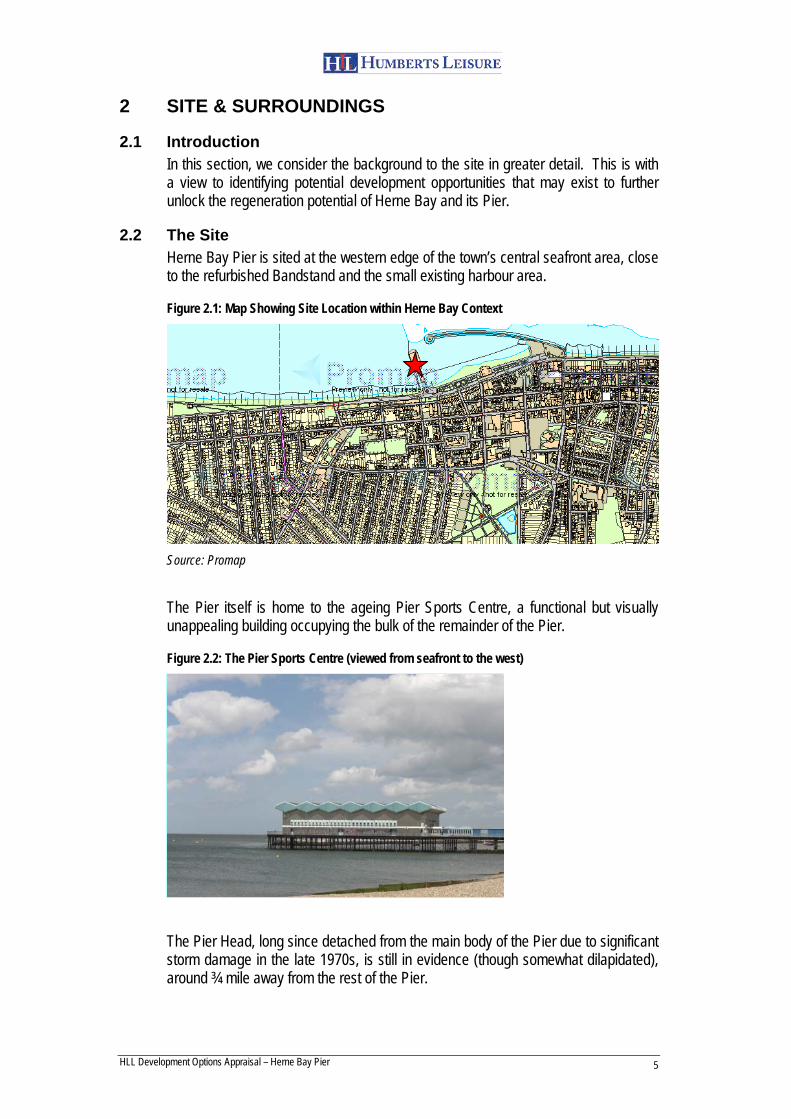

2.2 The Site Herne Bay Pier is sited at the western edge of the town’s central seafront area, close to the refurbished Bandstand and the small existing harbour area.

Figure 2.1: Map Showing Site Location within Herne Bay Context

Source: Promap

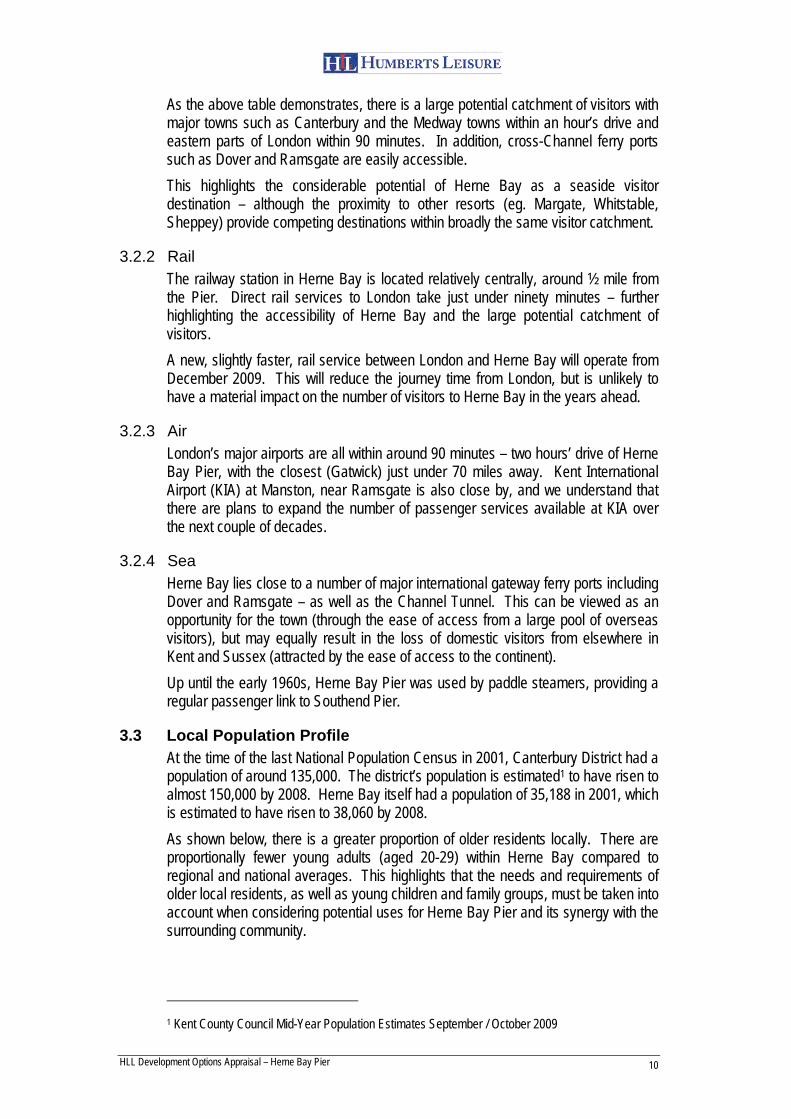

The Pier itself is home to the ageing Pier Sports Centre, a functional but visually unappealing building occupying the bulk of the remainder of the Pier.

Figure 2.2: The Pier Sports Centre (viewed from seafront to the west)

The Pier Head, long since detached from the main body of the Pier due to significant storm damage in the late 1970s, is still in evidence (though somewhat dilapidated), around ¾ mile away from the rest of the Pier.

HLL Development Options Appraisal – Herne Bay Pier 5

Figure 2.3: Close-up View of Pier Head

The current situation is somewhat different to how the Pier looked in the early twentieth century, as shown below.

Figure 2.4: Herne Bay Pier in its Former Glory

Source: Herne Bay Pier Trust

At the shore end of the Pier, there is some seating together with a former public convenience / ticket kiosk which has recently been refurbished by Canterbury City Council.

Figures 2.5 & 2.6: Seating on Pier & Former Ticket Kiosk

HLL Development Options Appraisal – Herne Bay Pier 6

2.3 Surroundings The Pier overlooks a small harbour area to the east, along with the town’s Bandstand – which includes a pub and café / ice cream parlour. There is a well-regarded seafront restaurant at the foot of the Pier. This is currently undergoing some refurbishment and expansion work. The wider seafront regeneration policy is reviewed in chapter 3.6.

Figures 2.7: View East from Pier, with Bandstand & Clock Tower (Harbour area to Left)

The Area Action Plan for Herne Bay (see chapter 3.6) comments that “it has been consistently expressed by local residents and stakeholders for the provision of a restored, and if possible extended, pier of such uses as eating facilities, entertainment, leisure, shops and fishing and boat trip facilities.” Given the visibility of the site in the seafront context, it is therefore vital that any commercial leisure or tourism uses fit well within the existing landscape and makes a positive contribution to the appearance of the resort.

2.4 Review of Previous Studies Although there have been a number of studies into the future regeneration and revitalisation of Herne Bay as a town, there have been fewer examining the Pier specifically. We are aware of the Capita Symonds report (2006) into the relocation of the Pier Sports Centre, but we summarise the PMP report from 2004 below to provide a greater context to this study.

2.4.1 A New Pier for Herne Bay - PMP Appointed jointly by Canterbury City Council, Kent County Council and Tourism South East, PMP undertook an initial feasibility study into rebuilding / restoring Herne Bay Pier. This included a degree of consideration of potential new leisure, tourism and enabling development. Some of the report’s key findings are summarised below:

HLL Development Options Appraisal – Herne Bay Pier 7

• That there was, in 2004, a strong level of commercial interest in developing on a new pier, although concerns were raised over the viability of particular uses;

• A casino could provide an attraction on a commercially redeveloped pier, complemented by other uses to “ensure a family friendly environment and all day / year round interest”;

• Rebuilding the pier to its original distance would make commercial viability impossible; and

• Of the range of options considered, none were found to be self-funding and would require a considerable amount of grant funding / public sector monies to ensure the Pier’s future.

Clearly the economic climate at the time of the PMP report was more favourable than it is at present – and this may restrict the levels of operator / developer interest in any commercial leisure opportunity. Such interest will be examined in this report.

2.5 Site Summary Herne Bay Pier is one of the key regeneration priorities for Canterbury City Council, and is therefore of considerable strategic importance. The displacement of existing sports and recreational activities from the Pier Pavilion offers an opportunity to enhance the town’s visitor offer, as well as appealing to the resident local populace. Previous studies have considered the potential for a range of commercial leisure opportunities, although the market climate today is very different to that in 2004. None of the range of options identified by PMP – in a considerably stronger economic climate – were found to be self-funding, and this may raise issues for development today. In this report we consider the market and commercial potential for a range of primarily leisure-based uses on the Pier, to enable the wider regeneration of Herne Bay and, potentially, the future restoration of the full length of Herne Bay Pier.

HLL Development Options Appraisal – Herne Bay Pier 8

3 DEMOGRAPHIC & VISITOR APPRAISAL

3.1 Introduction In this chapter, we begin our assessment of the likely demand for new leisure and tourism facilities that could be accommodated within a revamped Herne Bay Pier. This will look at the general picture for Herne Bay and the wider East Kent area, focusing on accessibility, demographic structure, the local economic environment, the relative importance of the local visitor economy and the proposed regeneration of the town centre.

3.2 Location & Accessibility Herne Bay is a seaside town with a population of nearly 40,000, situated between Whitstable and Margate on the northern coast of East Kent, overlooking the Thames Estuary.

Figure 3.1: Map showing Location of Herne Bay Pier in Wider Context

Source: Collins Road Atlas

3.2.1 Road The main access road to Herne Bay is the A299, leading from Junction 7 of the M2 motorway. Figure 3.2: Distance to Key Locations from Herne Bay Pier

Destination Approx. Distance (miles)

Approx. Journey Time by Private Car

Canterbury 9.1 0h20 Margate 13.5 0h20 Ashford 23.0 0h40 Dover 24.6 0h45 Rochester 38.1 0h50 Dartford 48.2 1h00 Central London 64.8 1h40 Source: The AA

HLL Development Options Appraisal – Herne Bay Pier 9

As the above table demonstrates, there is a large potential catchment of visitors with major towns such as Canterbury and the Medway towns within an hour’s drive and eastern parts of London within 90 minutes. In addition, cross-Channel ferry ports such as Dover and Ramsgate are easily accessible. This highlights the considerable potential of Herne Bay as a seaside visitor destination – although the proximity to other resorts (eg. Margate, Whitstable, Sheppey) provide competing destinations within broadly the same visitor catchment.

3.2.2 Rail The railway station in Herne Bay is located relatively centrally, around ½ mile from the Pier. Direct rail services to London take just under ninety minutes – further highlighting the accessibility of Herne Bay and the large potential catchment of visitors. A new, slightly faster, rail service between London and Herne Bay will operate from December 2009. This will reduce the journey time from London, but is unlikely to have a material impact on the number of visitors to Herne Bay in the years ahead.

3.2.3 Air London’s major airports are all within around 90 minutes – two hours’ drive of Herne Bay Pier, with the closest (Gatwick) just under 70 miles away. Kent International Airport (KIA) at Manston, near Ramsgate is also close by, and we understand that there are plans to expand the number of passenger services available at KIA over the next couple of decades.

3.2.4 Sea Herne Bay lies close to a number of major international gateway ferry ports including Dover and Ramsgate – as well as the Channel Tunnel. This can be viewed as an opportunity for the town (through the ease of access from a large pool of overseas visitors), but may equally result in the loss of domestic visitors from elsewhere in Kent and Sussex (attracted by the ease of access to the continent). Up until the early 1960s, Herne Bay Pier was used by paddle steamers, providing a regular passenger link to Southend Pier.

3.3 Local Population Profile At the time of the last National Population Census in 2001, Canterbury District had a population of around 135,000. The district’s population is estimated1 to have risen to almost 150,000 by 2008. Herne Bay itself had a population of 35,188 in 2001, which is estimated to have risen to 38,060 by 2008. As shown below, there is a greater proportion of older residents locally. There are proportionally fewer young adults (aged 20-29) within Herne Bay compared to regional and national averages. This highlights that the needs and requirements of older local residents, as well as young children and family groups, must be taken into account when considering potential uses for Herne Bay Pier and its synergy with the surrounding community.

1 Kent County Council Mid-Year Population Estimates September / October 2009

HLL Development Options Appraisal – Herne Bay Pier 10

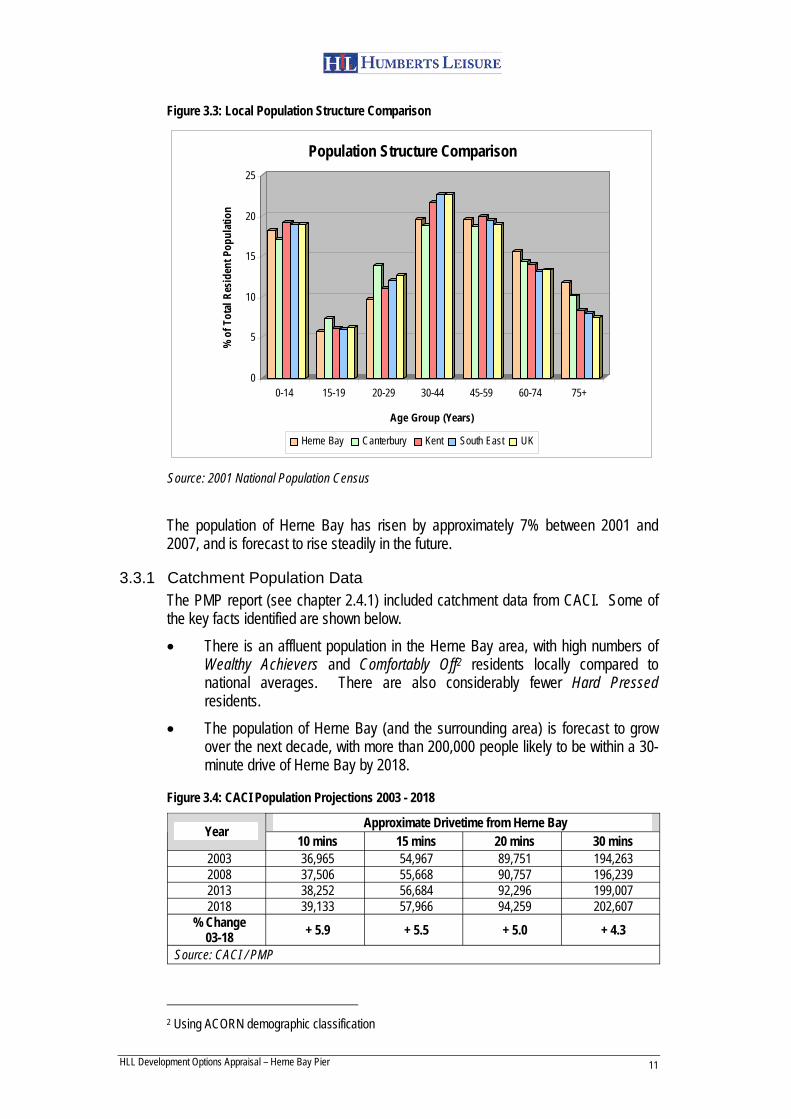

Figure 3.3: Local Population Structure Comparison

0

5

10

15

20

25

li

( )

i i

t Kent t UK

% o

f Tot

a R

esde

nt P

opul

atio

n

0-14 15-19 20-29 30-44 45-59 60-74 75+

Age Group Years

Populat on Structure Compar son

Herne Bay Can erbury South Eas

Source: 2001 National Population Census

The population of Herne Bay has risen by approximately 7% between 2001 and 2007, and is forecast to rise steadily in the future.

3.3.1 Catchment Population Data The PMP report (see chapter 2.4.1) included catchment data from CACI. Some of the key facts identified are shown below. • There is an affluent population in the Herne Bay area, with high numbers of

Wealthy Achievers and Comfortably Off2 residents locally compared to national averages. There are also considerably fewer Hard Pressed residents.

• The population of Herne Bay (and the surrounding area) is forecast to grow over the next decade, with more than 200,000 people likely to be within a 30minute drive of Herne Bay by 2018.

Figure 3.4: CACI Population Projections 2003 - 2018

Year

2003 2008 2013 2018

% Change 03-18

Source: CACI / PMP

10 mins 36,965 37,506 38,252 39,133

+ 5.9

Approximate Drivetime from Herne Bay 15 mins 20 mins 54,967 89,751 55,668 90,757 56,684 92,296 57,966 94,259

+ 5.5 + 5.0

30 mins 194,263 196,239 199,007 202,607

+ 4.3

2 Using ACORN demographic classification

HLL Development Options Appraisal – Herne Bay Pier 11

3.3.2 Surrounding Areas Although there is a limited resident population within Herne Bay and the surrounding district, Kent itself does have a considerable population base that generates additional visitors to the Pier and town. Mid-year population estimates for 2008 indicate that, including Medway, Kent has a population of 1.66 million, representing growth of almost 7% since 1998. It is important to note, however, that whilst this may represent an opportunity, there are a number of destinations within Kent as well as along the Sussex coast, and even in South Essex that will be competing for the same visitors.

3.4 Economic Environment

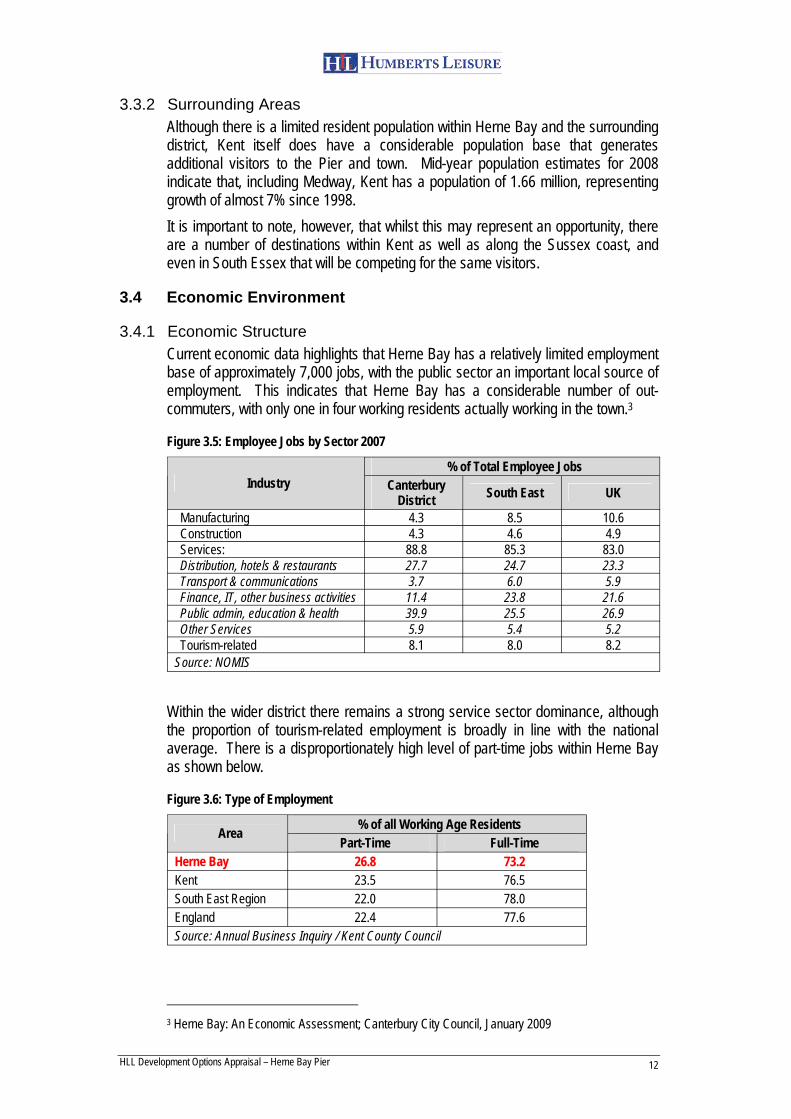

3.4.1 Economic Structure Current economic data highlights that Herne Bay has a relatively limited employment base of approximately 7,000 jobs, with the public sector an important local source of employment. This indicates that Herne Bay has a considerable number of out-commuters, with only one in four working residents actually working in the town.3

Figure 3.5: Employee Jobs by Sector 2007

Industry % of Total Employee Jobs

Canterbury District South East UK

Manufacturing 4.3 8.5 10.6 Construction 4.3 4.6 4.9 Services: 88.8 85.3 83.0 Distribution, hotels & restaurants 27.7 24.7 23.3 Transport & communications 3.7 6.0 5.9 Finance, IT, other business activities 11.4 23.8 21.6 Public admin, education & health 39.9 25.5 26.9 Other Services 5.9 5.4 5.2 Tourism-related 8.1 8.0 8.2

Source: NOMIS

Within the wider district there remains a strong service sector dominance, although the proportion of tourism-related employment is broadly in line with the national average. There is a disproportionately high level of part-time jobs within Herne Bay as shown below.

Figure 3.6: Type of Employment

Area % of all Working Age Residents Part-Time Full-Time

Herne Bay 26.8 73.2 Kent 23.5 76.5 South East Region 22.0 78.0 England 22.4 77.6 Source: Annual Business Inquiry / Kent County Council

3 Herne Bay: An Economic Assessment; Canterbury City Council, January 2009

HLL Development Options Appraisal – Herne Bay Pier 12

Herne Bay has a relatively high proportion of low-skilled residents, with almost one-third of residents having no qualifications – considerably higher than county, regional and national averages.

3.4.2 Unemployment From a peak of 11% in 1993, unemployment in Herne Bay has fallen markedly. This is highlighted by little long-term unemployment in the town – in contrast to many other seaside resorts around the UK. The unemployment rate in Canterbury district is marginally above the regional average for the South East, but below the national average. In 2008, 4.6% of economically active residents in the district were classed as unemployed4. This compares to 5.7% in Great Britain and 4.4% regionally.

3.5 Tourism

3.5.1 The Impact of the Current Global Economic Downturn The falling value of Sterling has resulted in a sharp rise in the cost of overseas holidays. National self-catering operators such as Hoseasons are recording increased demand for holiday rentals, with the price of overseas holidays forecast to increase by around 10% in 2009 compared to 3% in the UK, due to the weak pound.5

Furthermore, a 2009 survey6 commissioned by Travelodge found that just 27% of Britons planned to holiday abroad – down from 33% in 2008 – with 32% planning a domestic holiday. Of those staying at home, 40% will take a seaside holiday. This offers opportunities to Britain’s coastal areas, such as Herne Bay, to increase (and subsequently retain) visitor numbers in the future.

3.5.2 Regional Tourism Trends The South East is one of the most popular domestic visitor regions in England with 16.3 million visitors in 2008. These staying visitors accounted for almost 48 million bednights (an average of 2.92 nights per trip) and total expenditure of more than £2.3 billion (£144.22 per trip).

4 Office for National Statistics 5 The Independent 8 October 2008 6 The Caterer 5 June 2009

HLL Development Options Appraisal – Herne Bay Pier 13

Figure 3.7: Domestic Staying Tourism by Region Visited 2008

Govt Office Region Trips (millions) Nights (millions) Spend (£millions) South West 18.93 71.73 3,639 South East 16.29 47.52 2,350 North West 12.97 36.56 2,338 London 11.32 27.43 2,356 Yorkshire & Humberside 9.54 26.53 1,397 East of England 9.22 29.12 1,362 West Midlands 7.76 20.74 1,149 East Midlands 7.28 22.29 1,060 North East 4.02 12.22 697 Total England 95.53 295.38 16,433 N.B. May not total due to people visiting more than one region per trip Source: UKTS

Between 2007 and 2008, the number of domestic staying trips to the South East region fell by almost 9%, although total visitor expenditure fell fractionally. This highlights that the region is increasingly attracting more affluent leisure and business travellers.

3.5.3 Local Tourism Trends In 2006 (the latest available data), there were an estimated 6.4 million visitors to Canterbury District. More than 9% of these were staying visitors, and tourism generated £315.4 million in direct and indirect visitor expenditure, supporting more than 7,300 FTE jobs. We understand that there has been a gradual decline in visitor numbers to Herne Bay in recent years, although have not been provided with any specific figures by the Council. However, discussions with the Council’s Tourism Manager suggest that 2009 has been a particularly good year for tourism in Herne Bay, with an increase in visitor numbers – supporting national evidence highlighted in chapter 3.5.1. The Council’s own Economic Assessment7 notes that “it is accepted that tourism helped Herne Bay to remain prosperous throughout the 20th century until the 1970s in terms of employment and wealth. But changing patterns of tourism has meant that much of the town’s local retail sector is likely to be more dependent upon local resident spend over an average year.”

3.6 Regeneration & Key Local Developments There are a number of regeneration schemes and developments that are taking / have taken place in East Kent in the recent past (eg. the Turner Contemporary in Margate). However, of most relevance to the Pier is the wider regeneration of Herne Bay town centre. The recently published Area Action Plan (AAP) for Herne Bay8

highlights three prominent and centrally located development sites as shown below. These are the: • Central Development Area;

7 Herne Bay: An Economic Assessment; Canterbury City Council, January 2009 8 March 2009

HLL Development Options Appraisal – Herne Bay Pier 14

• Bus Depot site; and • Beach Street site.

Figure 3.8: Regeneration Proposals Map

Source: Herne Bay Area Action Plan – Proposed Submission – March 2009

The town centre offers a number of different sites for development and enhancing the visitor / community offer – with the town’s retail leakage a particular issue. It has been estimated that Herne Bay only retains 31p in every pound generated9. The Council’s recent Economic Assessment highlights the failure, so far, to bring forward seafront development opportunities. To this end, Policy HB11 of the AAP deals specifically with Herne Bay Pier: “During the period between the decision to relocate the sports facilities from the pier and the opening of replacement facilities the options for the future of the pier will be fully explored jointly by the City Council and Pier Trust. A detailed implementation plan will be developed to progress the preferred proposals, including the preparation of a Supplementary Planning Document to be adopted by the Council to set out detailed planning and design guidance for the delivery of a revived and thriving pier at Herne Bay.” There is therefore a need for a realisable and deliverable scheme at Herne Bay Pier. This will assist in the wider regeneration of – and more effectively linking - the seafront and town centre, increasing visitor / community interest in the pier, as well as generating new investment from the private sector.

3.7 Stakeholder Consultations Members of our team attended a meeting of the Herne Bay Pier Trust at the outset of this study, in order to better understand local aspirations for the Pier site and the unique opportunity that it represents for the town. All views expressed have been taken into consideration, particularly the wish to ensure that any initial development at the Pier does not prejudice the future expansion of the structure back to its

9 Property Week 12 June 2009

HLL Development Options Appraisal – Herne Bay Pier 15

original length. The views of the Pier Trust have assisted our team with its consideration of the range of potential uses, which we discuss in chapter 4. In addition, we have spoken to a number of local businesses to better understand the aspirations of local commerce for Herne Bay and its Pier. There was universal agreement that a key aspect of driving interest in Herne Bay is to restore the Pier to its original length. This would enable the Pier to once more welcome paddle steamers to Herne Bay. A raft of other ideas – that are perhaps more realisable in the shorter term – were also suggested. Some of these ideas, or variations on a similar theme, are again discussed in greater detail in chapter 4. We also understand that the City Council will be carrying out further consultation on this report, as this aspect did not form a major component of the brief given to HLL Humberts Leisure.

3.8 Summary of Local Demand Potential Herne Bay is a medium sized seaside town. It is, however, close to population centres in Canterbury and the Medway towns, and is also less than two hours from central London. The town’s population is now estimated at around 38,000, with almost 200,000 resident within an approximate thirty minute drive time. This local population is relatively more affluent than the UK, and has a greater proportion of both younger children and older (65+) residents than nationally, with a particular prevalence of older residents within Herne Bay itself. This may help to explain the disproportionately high level of part-time employment in the town, and also highlights the need to identify uses that may generate interest from older age groups, as well as those with young children. There are no specific visitor figures for the resort of Herne Bay itself. It is understood that there has been a fall in visitor numbers to the resort, in keeping with many traditional coastal destinations, due to the rise of the cheap foreign package holiday – particularly during the 1980s and 1990s. The economic downturn has apparently benefited domestic tourism destinations, with increases in bookings and visitor numbers being reported. This may help to reverse the gradual decline witnessed in Herne Bay over recent years. Together with the wider regeneration of the town centre, this may create new markets and opportunities for a redeveloped Herne Bay Pier. It must be borne in mind, however, that the Pier re-development and wider regeneration is inter-linked, with the regeneration of the town centre hinging, to a certain extent, on the redevelopment of the Pier and vice versa. In the following chapters, we consider a range of leisure and tourism uses that could be considered for Herne Bay Pier, together with the likely levels of demand for such facilities (and commercial operator / developer interest) in this location.

HLL Development Options Appraisal – Herne Bay Pier 16

4 MARKET ANALYSIS

4.1 Introduction In this chapter, we consider a range of leisure and tourism-based uses that may offer some potential for commercial investment and help secure the future of Herne Bay Pier. This analysis will briefly examine recent national trends in the market sectors of relevance, as well as the likely level of commercial interest in any such development opportunity at this particular site.

4.2 Food & Beverage

4.2.1 Restaurants The largest share of the eating out market in the UK is from pubs and hotels. In recent years, the market share of pubs has risen substantially due to both the rise in branded family pub-restaurants (e.g. Harvester & Brewers Fayre) and the trend for traditional pubs to be remade as ‘gastropubs’ focusing primarily on the food element of the pub product – particularly in light of the smoking ban.

Figure 4.1: Market Share by Restaurant Type 2003 - 2007

Restaurant Type

Share of Restaurant Meals Market in £ millions % Change 2003 – 072007 2006 2005 2004 2003

Pubs & Hotels 4,350 4,175 3,875 3,625 3,325 + 30.8 Fast Food 2,900 2,950 3,000 3,000 3,000 - 3.3 Traditional Asian 1,725 1,750 1,775 1,750 1,700 + 1.5

Italian / Pizza 1,725 1,700 1,550 1,475 1,400 + 23.2 Other Restaurants 2,400 2,300 2,400 2,175 1,930 + 24.4

Total 13,100 12,875 12,600 12,025 11,355 + 15.4 Source: Key Note

Over the same period, there has also been a slight decline in the market share of fast food restaurants. This has been due, in part, to national healthy eating drives, and may also indicate an increase in the quality of food on offer in the UK’s eating out market. It remains to be seen whether this trend will continue through the recession.

4.2.2 Cafés & Coffee Shops Recent years have also seen phenomenal growth in branded coffee shops and cafés. It is now estimated10 that the top 12 operators in the UK in late 2008 offer almost 2,800 units. The number of branded outlets operated by these major operators grew by around 15% a year in the mid-2000s, but increased by almost one-third during 2008. This perhaps suggests that the recession has created new high street opportunities for such operators to expand more rapidly, backed by (generally) strong business models. The recent travails of Coffee Republic, however, suggests that there may be more challenging times ahead for some operators.

10 Key Note Coffee & Sandwich Shops – July 2009

HLL Development Options Appraisal – Herne Bay Pier 17

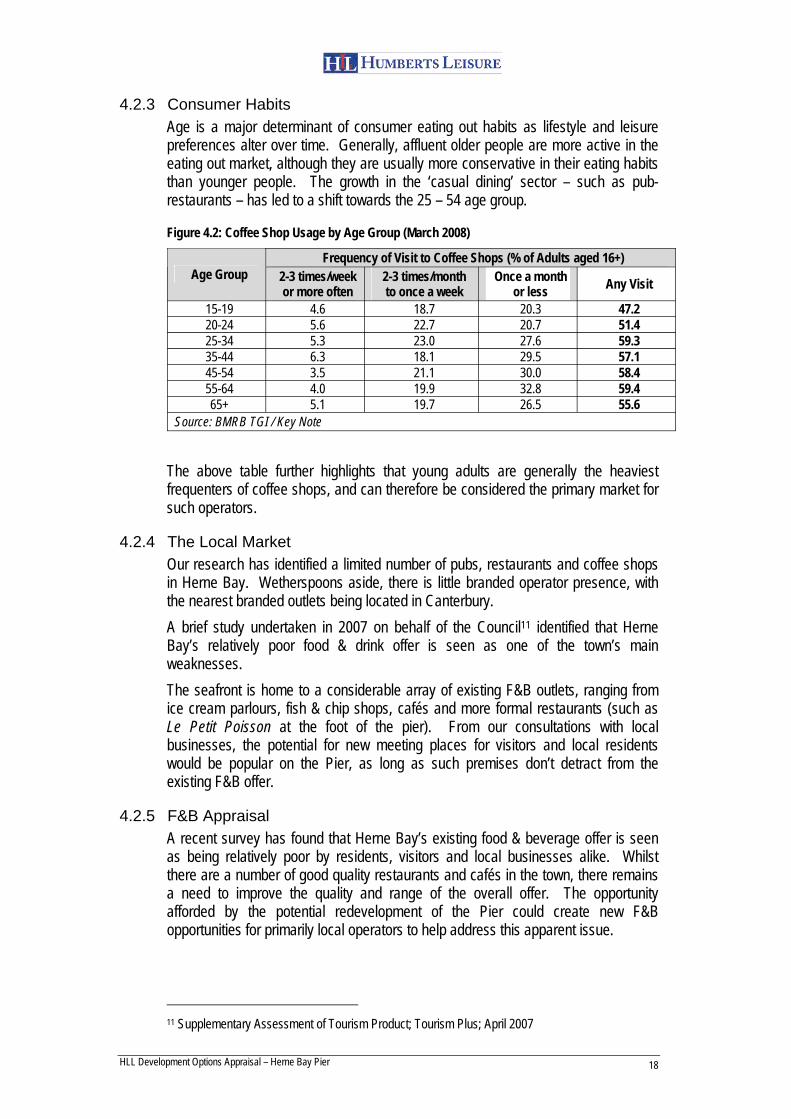

4.2.3 Consumer Habits Age is a major determinant of consumer eating out habits as lifestyle and leisure preferences alter over time. Generally, affluent older people are more active in the eating out market, although they are usually more conservative in their eating habits than younger people. The growth in the ‘casual dining’ sector – such as pub-restaurants – has led to a shift towards the 25 – 54 age group.

Figure 4.2: Coffee Shop Usage by Age Group (March 2008)

Age Group Frequency of Visit to Coffee Shops (% of Adults aged 16+)

2-3 times/week or more often

2-3 times/month to once a week

Once a month or less Any Visit

15-19 4.6 18.7 20.3 47.2 20-24 5.6 22.7 20.7 51.4 25-34 5.3 23.0 27.6 59.3 35-44 6.3 18.1 29.5 57.1 45-54 3.5 21.1 30.0 58.4 55-64 4.0 19.9 32.8 59.4 65+ 5.1 19.7 26.5 55.6

Source: BMRB TGI / Key Note

The above table further highlights that young adults are generally the heaviest frequenters of coffee shops, and can therefore be considered the primary market for such operators.

4.2.4 The Local Market Our research has identified a limited number of pubs, restaurants and coffee shops in Herne Bay. Wetherspoons aside, there is little branded operator presence, with the nearest branded outlets being located in Canterbury. A brief study undertaken in 2007 on behalf of the Council11 identified that Herne Bay’s relatively poor food & drink offer is seen as one of the town’s main weaknesses. The seafront is home to a considerable array of existing F&B outlets, ranging from ice cream parlours, fish & chip shops, cafés and more formal restaurants (such as Le Petit Poisson at the foot of the pier). From our consultations with local businesses, the potential for new meeting places for visitors and local residents would be popular on the Pier, as long as such premises don’t detract from the existing F&B offer.

4.2.5 F&B Appraisal A recent survey has found that Herne Bay’s existing food & beverage offer is seen as being relatively poor by residents, visitors and local businesses alike. Whilst there are a number of good quality restaurants and cafés in the town, there remains a need to improve the quality and range of the overall offer. The opportunity afforded by the potential redevelopment of the Pier could create new F&B opportunities for primarily local operators to help address this apparent issue.

11 Supplementary Assessment of Tourism Product; Tourism Plus; April 2007

HLL Development Options Appraisal – Herne Bay Pier 18

4.3 Conferencing, Meetings & Events It is estimated that around 1.6 million conferences are held in the UK each year, with residential conferences accounting for around one-third of these. The number of conferences held nationally has increased marginally over recent years.

Figure 4.3: UK Conference Venues by Distribution & Market Share

Type of Venue Distribution (%) Market Share (%)

Hotels 53 63.9 Unusual Venues 19 11.4 Conference / Training Centres 10 11.2 Multi-purpose Venues 11 5.8 University / Educational Venues 5 5.7 Purpose-built Centre 2 2.0 Total 100.0 100.0 Source: Key Note / BACD

4.3.1 The Local Market In larger coastal resorts, we would expect the bulk of conference and meeting room supply to be dominated by the hotel sector. However, there is little in the way of such visitor accommodation locally. The Conference Blue & Green12 identifies just two venues in Herne Bay itself: Kings Hall and Herne Bay Court. We understand, however, that the latter has now closed down. This highlights that the Kings Hall is the only such venue for local meetings, conferences and events.

Figure 4.4: Kings Hall

Kings Hall is a single, multi-purpose function room, with a bar attached that is available for hire. Broadly speaking, the events held at Kings Hall tend to attract local audiences (mainly from Whitstable and Herne Bay) comprised of generally older / retired residents. We understand that the existing building requires a considerable amount of expenditure and maintenance, and the future of the facility is currently the subject of a management review.

12 Nationally-recognised venue finder guides for events, conferences and meetings.

HLL Development Options Appraisal – Herne Bay Pier 19

Should the closure of Kings Hall be considered, then this would offer an opportunity to relocate events and functions to a new facility forming part of the wider redevelopment of Herne Bay Pier.

4.3.2 Conference Appraisal Herne Bay is a medium sized coastal town, with few major private sector employers. As such, there is limited demand for conference and meetings space. This is evidenced by the recent opening of the Premier Inn hotel at Blacksole Farm, which has no meeting room facilities. We therefore consider that, unless forming one element of a flexible multi-purpose conference, theatre, events and recreational space, there would be little demand for new conference and meetings facilities in Herne Bay. It has been suggested to us that the Pier Pavilion may be an appropriate alternative entertainment venue to the Kings Hall. This suggestion was made on the basis that the relocation would free up the Kings Hall site for other uses. A pier is certainly an appropriate location for such an entertainment venue, indeed in the past many piers have included such facilities. However, the cost of refurbishing and converting the existing Pier Pavilion building is likely to be substantial. We would expect that the cost would not be less than the £3.3 million estimate provided by the Council for the continued use of the Pier Pavilion as a sports centre. In the absence of very clear evidence to the effect that the disposal of Kings Hall would generate a sum close to this figure, there would seem little serious merit in transferring the use, even if this were thought to be desirable.

4.4 Visitor Attractions The visitor enterprise business is a very diverse sector which includes theme parks, zoos and wildlife parks, aquariums, museums, piers, historic houses and gardens, caves, farms and amusement centres. It is a multi-billion pound industry in the UK. It is forecast, however, that the current recession will have a negative impact on visitor numbers and expenditure across all types of visitor attraction, due primarily to consumers having less disposable income. Nevertheless, with higher numbers of people likely to be taking a holiday at home (as highlighted in chapter 3.5), it is possible that the attractions market may not be as badly affected as some forecasts have predicted. Clearly some types of visitor attraction would be inappropriate at Herne Bay Pier (for example, a steam railway or a wildlife park). We have therefore briefly considered the potential for a museum / heritage visitor centre and Victorian-style rides to reflect the Pier’s history. We have also considered the potential of attracting a major visitor attraction, such as an aquarium.

4.4.1 Museums Visits to UK historical and cultural attractions grew by an estimated 10% between 2003 and 2007 – with the museums and galleries segment growing 14% over the same period. It is further estimated that 52% of the adult population have visited an historical or cultural attraction at least once over the past twelve months.13

13 Mintel Historic & Cultural Visitor Attractions – UK – November 2008

HLL Development Options Appraisal – Herne Bay Pier 20

Visitors to such attractions are also most likely to be middle-aged and more elderly adults, with the 35-44 age group having the greatest propensity to visit museums and other, similar, heritage and cultural visitor attractions. This 35-44 age group is under-represented locally (as identified in chapter 3.3), and this may therefore limit likely levels of demand – although the generally ageing local population may drive some demand for a new museum facility on Herne Bay Pier.

4.4.2 Other Visitor Centres Visitor and heritage centres form an important part of the UK’s cultural landscape. It is estimated14 that there are over 500 visitor centres in the UK, attracting more than 30 million visitors each year. Such facilities act as information and educational facilities, typically at areas of tourist activity or natural beauty spots. The majority of centres are operated by local authorities, agencies and trusts. A visitor centre may include a reception area, provide tourist information, visitor management, refreshment and conveniences, but its primary function is interpretation.

4.4.3 Victorian-Style Rides The provision of a select number of traditional Victorian-style children’s rides may offer a visually appealing and less intrusive alternative to modern Piers (such as Brighton, for example). Such rides normally centre on a carousel, with other small fairground-style entertainments that will particularly appeal to the family market, and would fit well with the historic nature of the Pier as a part of a wider mix of attractions and facilities.

Figure 4.5: A Typical Victorian Carousel

Source: Wikimedia

Any such opportunity could be put out to tender to attract operators likely to pay a small seasonal rent for the space provided. Such a concept does have some merit. This is highlighted by the current proposals to restore the Dreamland theme park in nearby Margate. Opened in 1920, the park is a well-recognised local landmark – much like Herne Bay Pier – and finally closed in 2006.

14 Visit Britain Tourism Insights July 2002

HLL Development Options Appraisal – Herne Bay Pier 21

Figure 4.6: Aerial View of Dreamland Theme Park Today

Source: www.flickr.com

The Dreamland Trust have developed proposals to establish a ‘Heritage Amusement Park’ on around half of the current site, and have recently15 been awarded a grant of £384,500 by the Heritage Lottery Fund, as well as awaiting the results of a £4 million grant funding bid from Sea Change. It is anticipated16 that the park will reopen to visitors in 2012.

4.4.4 AquariumsWildlife-based attractions (such as zoos, safari parks and aquariums) are particularly popular amongst family groups. They can be educational and informative as well as exciting for adults and children alike. The market for aquariums in the UK appears to be relatively mature, with Merlin (owner of the Sealife Centres) and Aspro (Blue Reef Aquariums) the largest and most active developer / operators. Although most such schemes in the UK entail a significant amount of built development (probably in excess of the space available on the Pier), there are examples further afield of indoor / outdoor coastal aquariums. These include the Monterey Bay Aquarium in California, which attracts around 1.8 million visitors per year. Whilst this particular facility would be too large to be considered, there maybe scope for the concept of a pier-based aquarium with a mix of indoor and outdoor features.

15 August 2009 16 The Independent 15 August 2009

HLL Development Options Appraisal – Herne Bay Pier 22

Figure 4.7: Monterey Bay Aquarium

Source: Wikimedia

However, the cost of such schemes can be extremely high. For example, the Sea Life Centre at Loch Lomond in Scotland opened in 2006 at a cost of £3.5 million17. As a result, they require a large pool of local resident visitors and / or annual tourist numbers. Realistically speaking, we consider it unlikely that any developer would consider Herne Bay to be a suitable location in this respect – particularly when one takes into account the greater cost and risk associated with developing on a pier as opposed to a site on dry land.

4.4.5 The Local Market Herne Bay has just the one museum – located in a relatively central location on William Street – and is open all year round. A new museum / heritage visitor centre, as part of a revamped Pier offer, could potentially offer an expanded range of exhibits appealing to a wider range of visitors, and linking well with the historic and cultural heritage attractions on offer in nearby Canterbury. There are no major aquariums in East Kent, the nearest is the Blue Reef at Hastings in East Sussex, as well as Sealife Centres in both Brighton and London. Construction work on the new Turner Contemporary Gallery began in November 2008, with a view to opening in 2011. We consider that any spin-offs (in terms of smaller galleries) are likely to be heavily concentrated in Margate, particularly in the years immediately following opening in 2011.

4.4.6 Visitor Attractions Appraisal There would undoubtedly be scope in locating a small museum / heritage visitor attraction / visitor centre within part of a refurbished Herne Bay Pier. Such a facility could be used for interpretation and general tourist advice, augmented by refreshment (ie. café / restaurant) and retail facilities to generate additional revenue streams. If the exhibits in the existing museum on William Street were relocated into a new facility, the building could be sold for an alternative use. This would generate a capital receipt for the Council, which could be ring-fenced towards the development of a replacement venue at the pier.

17 Leisure Opportunities 17 July 2006

HLL Development Options Appraisal – Herne Bay Pier 23

Most new museums and visitor centres are constructed using public funds (eg. Heritage Lottery Funds) with few private developers / operators in the market for this type of visitor attraction, due to the limited revenue potential of such operations. Such a facility could be run and managed by volunteers – such as the Pier Trust – to minimise ongoing costs and the level of annual subsidy required to sustain the business. There is likely to be some concessionary interest in operating small-scale Victorian rides on a revamped pier. Whilst not representing a major level of development, such an offer would be popular with key visitor groups (such as those with young children), as well as local residents. The demolition of the existing Pier Pavilion would provide a suitable space for such facilities and generate annual rental income. Whilst a small number of aquariums continue to be developed by the private sector, we feel that the wider catchment for Herne Bay is probably too small to attract such developers to the town. There is, however, nothing to prevent entrepreneurs putting forward aquarium proposals should they so wish.

4.5 Indoor Children’s Play The indoor children’s play market consists of many types of play area ranging from simple ball pits to elaborate soft play and tube structures. There are three main categories of indoor play area that can be identified: • Freestanding Play Centre: where the play area is the primary business and

main reason for visiting; • Pub Play Areas: these are the play areas provided in family pub chains that

operate across the UK; and • Other Play Areas: those not covered above (excluding play areas in retail

destinations).18

By the end of 2008, the UK market was estimated to be worth in the region of £135 million (on admissions alone), a rise of more than 16% since 2003. Despite this, the number of admissions has remained largely static, and may indicate that admission prices have risen in line with a more sophisticated play offering by operators.

4.5.1 The Local Market Our research has identified just one indoor children’s play centre facility in Herne Bay. The Hippodrome is located on Kings Road (just to the north of the town centre). Snappy’s is a dinosaur-themed children’s indoor adventure play centre at Whitstable (adjacent to the Lazer Rush game). There is a large indoor and outdoor children’s play centre at Birchington (just to the west of Margate). Jungle Jim’s includes an indoor play barn as well as a range of outdoor activities including go-karting. Slightly further afield, Imagine opened in Kingsnorth, Ashford at the end of 2003 and offers 25,000ft² of indoor children’s play area.

18 Mintel Children’s Play Areas – UK – January 2006

HLL Development Options Appraisal – Herne Bay Pier 24

Figure 4.8: Some of the Facilities at Snappy’s, Whitstable

Source: Snappy’s Adventure Play

There is, therefore, a relatively limited supply of indoor children’s play facilities in Herne Bay and the surrounding area. The greater proportion of young children and adults aged 30 – 44 resident in Herne Bay, compared to the district (see chapter 3.3), suggests that there may be some demand for additional such facilities from the local community.

4.5.2 Indoor Children’s Play Appraisal Herne Bay is a popular destination for visitors with younger children and the limited local supply of similar facilities, especially for tourist visitors and local residents with children aged under 14, may suggest that there could be an opportunity for the development of an indoor children’s play centre at Herne Bay Pier. However, modern facilities tend to be quite large (i.e. Imagine at Kingsnorth), and we consider that there is likely to be insufficient space to attract any major national operator to Herne Bay Pier. This is more likely, therefore, to offer an opportunity for a local entrepreneur, possibly in tandem with other revenue-generating facilities such as themed rides or a family café / restaurant.

4.6 Other Urban Leisure Urban leisure covers a wider variety of facilities. For the purpose of this study, we have focused on the potential for a new cinema or a tenpin bowling alley to be accommodated as part of a revamped Pier.

4.6.1 Cinemas The advent of the multiplex in the mid-1980s has led to a huge growth in cinema admissions over the past couple of decades. There has been a slight fall in admissions since 2002, although the last two years (2007 and 2008) have shown signs of recovery – due in part to a significant increase in available screens.

HLL Development Options Appraisal – Herne Bay Pier 25

Figure 4.9: UK Cinema Market 2004 - 2008

Year Cinema Admissions (millions)

Number of Cinema Screens

Av. Admissions per Screen

2008 164.2 3,661 44,851 2007 162.4 3,514 46,215 2006 156.6 3,440 45,523 2005 164.7 3,357 49,062 2004 171.3 3,342 51,257

% Change 04 - 08 - 4.1 + 9.5 - 12.5 Source: UK Film Council

However, the rise of the multiplex has led to the closure of a number of smaller, independent cinemas (eg. Dreamland Cinema in Margate, which closed in late 2007). Many new cinema developments form part of wider urban leisure parks, including a range of F&B outlets, bingo, bowling and other leisure facilities intended to create urban ‘destinations’ for nearby communities to spend their leisure time and disposable income.

4.6.2 Bowling The market for tenpin bowling showed steady growth during the late 1990s and early 2000s, although growth has slowed slightly recently. As for cinemas, many newer centres form part of wider leisure park developments, benefiting from the high levels of footfall that such parks offer. As an activity, bowling is most popular amongst teenagers and younger adults. Given the lower proportion of this age range resident locally, this may suggest that Herne Bay will not fit the demographic requirements of such operators, and may therefore not be a suitable location for such a development.

4.6.3 The Local Market At present, there is just one cinema in Herne Bay. The two-screen Kavanagh Cinema on William Street is operated by Reeltime Cinemas (who also operate the cinema in Westgate-on-Sea). We understand, anecdotally, that the Kavanagh may be struggling somewhat at the current time due to broader issues with its parent company. Reeltime also operated the Dreamland Cinema in Margate, prior to its closure in 2007. The nearest multiplexes are located at Bluewater (Showcase), Westwood Cross (Vue) and Ashford (Cineworld). There are no multiplexes in Canterbury (although there is a city centre Odeon). All of these multiplex facilities have at least ten cinema screens and extensive car parking facilities on-site. This would not be achievable at Herne Bay Pier. There are no established tenpin bowling facilities in Herne Bay. AMF (one of the UK’s leading operators) operate bowling centres in Ashford, Maidstone and Margate, as well as a 10-lane facility in neighbouring Whitstable. The other leading bowling operators, Hollywood Bowl and Tenpin, have no facilities in Kent, although we are aware that the 8-lane Bugsy’s Ice & Bowl opened in the centre of Canterbury in September 2009.

HLL Development Options Appraisal – Herne Bay Pier 26

4.6.4 Urban Leisure Appraisal Herne Bay is already home to a cinema. Given the size of the resident population, we do not feel that there would be sufficient demand for additional cinema screens in the town. The limited space available on the Pier (and surrounding area for car parking, etc) would further deter the likelihood of any developer / operator interest in Herne Bay Pier as a viable new business opportunity. The demographic profile for tenpin bowling does not appear to fit well with the local catchment. Bowling centres generally form part of a wider leisure park development. There would be insufficient space on the Pier for such a scheme unless as a standalone entity.

4.7 Retail Opportunities In recent years, the rise of the out-of-town retail destination has mirrored the decline of the traditional high street experience. Major leisure and retail parks (eg. Bluewater) have garnered a large share of total retail sales, and leisure-led mixed use developments (eg. Xscape) have used specialist retail tenants to anchor their schemes and ensure financial viability.

4.7.1 The Local Market Over recent years, Herne Bay’s town centre has suffered a considerable degree of retail ‘leakage’ to new out-of-town retail destinations, as well as to Canterbury. It has been identified that the town’s independent retail sector is vulnerable to future changes in patterns of day tourism and local resident spend.19

The redevelopment of Herne Bay Pier may offer opportunities for some form of retail offer to help redress such ‘leakage’ and anchor a wider leisure offer on the Pier. We do not consider, however, that major branded retailers would be interested (or be appropriate) for such an opportunity. It may be possible to attract more locally-based (perhaps themed) retail relevant to the Pier / seaside location and complementary to other activities attracted to the Pier. This may include, for example, independent souvenir / beach-related retail outlets in keeping with the character and scale of Herne Bay as a seaside resort.

4.7.2 Retail Appraisal Herne Bay does have a real problem with retail leakage with few national retailers / a preponderance of charity and discount shops.20 An enhanced town centre and revamped Pier attracting more local residents and visitors to spend money in the town may lead to good demand for seasonal retail premises (eg. souvenir or beach-related shops) to capitalise on the summer season. By their very nature, however, such premises will only generate limited revenue, with the majority operating under the VAT threshold. Nevertheless, a rejuvenated Herne Bay, with higher footfall, may offer some small-scale retail opportunities on the Pier – or, indeed, elsewhere on the seafront. It is likely that any such premises would need to be developed by the Council with local concessions the most likely avenue for such an offer in this location.

19 Herne Bay: An Economic Assessment; Canterbury City Council, January 2009 20 Property Week 12 June 2009

HLL Development Options Appraisal – Herne Bay Pier 27

4.8 Artist’s Quarter The market for arts & crafts studios and workshops is very fragmented by nature, with primarily small-scale independent operators. This is one of the sector’s appeals in cultural areas, but does make it extremely difficult to accurately identify market trends pertaining to the future development of the industry. Nevertheless, recent examples in the UK have highlighted the economic and cultural benefits that such developments can have. For example, the Tate Gallery at St Ives in Cornwall has been a phenomenal success in regenerating the whole of St Ives as a year-round cultural destination, with many shops, galleries, pubs and restaurants opening to benefit from increased and higher-spending visitors. There is a strong expectation that the development of the Turner Contemporary Gallery will have the same impact on Margate. In time, it is possible that there could be some smaller spin-off effect upon Herne Bay if the right facilities are made available and publicised appropriately.

4.8.1 The Local Market There are no such facilities at present in Herne Bay. The concept has been successfully implemented in the regeneration of Brighton seafront, quickly becoming an integral part of the visitor experience. We understand that rental levels for such ‘Arches’ are, however, considerably below those for comparable commercial premises (such as retail, bars, etc). Indeed, the Artist Quarter is effectively used as a loss-leader to provide colour, interest and to attract people down to the seafront promenade to create passing trade for other income generating uses. With this in mind, together with the planned developments in Thanet, we consider it unlikely – at this stage – that such a concept would be suitable for Herne Bay. The development of the Turner Contemporary and the establishment of a creative community in the Old Town in Margate is likely to attract the vast majority of any arts-related private investment for the foreseeable future, with only marginal spin-off investment benefits likely to impact upon Herne Bay.

4.8.2 Arts & Crafts Appraisal Developing small-scale studios / workshops on the Pier could become a popular visitor attraction (as witnessed in Brighton), providing a small spin-off to benefit from the planned opening of the Turner Contemporary in Margate and to other arts & cultural developments across other areas of East Kent, including the more developed arts scenes in Whitstable or Margate. However, we consider that such a scheme in Herne Bay at this stage would be unlikely, as the impact and spin-off benefits for nearby destinations (such as Herne Bay) are, as yet, intangible. We do acknowledge that there is some anecdotal evidence that there is an element of the existing North Kent artist community that would welcome relatively cheap workshop / gallery space in Herne Bay.

4.9 Marina Many coastal harbours have traditionally catered for industrial craft such as freight carriers and fishing vessels. In recent years, there have been a number of new marina / harbour developments in coastal locations as developers and harbourmasters have acknowledged the growth and revenue potential of the leisure sailing market.

HLL Development Options Appraisal – Herne Bay Pier 28

There are at least 236 coastal marinas in the UK and Channel Islands, providing around 49,000 berths. These are concentrated in South East and South West England.21 The vast majority of these moorings are now occupied by leisure craft and there is a shortage of large berths to meet the growing trend for larger pleasure craft as boats become another badge of middle / upper class affluence – despite the recession.

4.9.1 The Local Market Herne Bay Sailing Club (HBSC) is located towards the eastern end of the seafront, adjacent to Kings Hall, and is an RYA-accredited training centre. We have spoken to the club and understand that they currently have 212 members and a strong cadet force. In addition, we understand that some members have graduated from dinghies to yachts, but have to moor their craft at Ramsgate, Faversham and Dover due to a dearth of local moorings in the Herne Bay & Whitstable area. There are established marinas at Swale (Conyer) and Ramsgate, although we understand that the latter may be full. Ramsgate also has a greater range of facilities than Swale, which is reflected in considerably higher prices. We also understand that there may be plans for a marina development at Whitstable Harbour, although have been unable to confirm specific plans / the current state of the project at the time of writing.

4.9.2 Marina Appraisal At present, there are a limited number of mooring buoys within Herne Bay’s harbour arm adjacent to the Pier. We have spoken to some local sailing enthusiasts who have highlighted that it would be possible to fit a number of floating pontoons within the existing harbour arm, and that there would be significant interest in such a facility – with limited maintenance requirements.

4.10 Watersports Watersports appeal to a broad spectrum of users. Recent years have witnessed a growth in participation in sailing and other watersports activities, with an estimated 4 million people in the UK participating in 2007. There was, however, a significant overall drop in participation levels last year, as shown below.

Figure 4.10: Participation in Selected Watersports & Sailing Activities

Activity Participation Rate (% of Adults) % Change 2006-082008 2007 2006

Any activity 23.03 29.63 28.03 - 17.8 Any boating activity 6.20 7.84 7.25 - 14.5 Water skiing 0.60 0.78 0.67 - 10.4 Small sail boat activities 0.87 1.16 1.09 - 20.2 Windsurfing 0.35 0.48 0.54 - 35.2 Kitesurfing 0.13 0.18 0.09 + 44.4 Angling (from the shore) 1.90 2.47 2.27 - 16.3 Coastal walking 10.42 13.32 12.21 - 14.7 Spending general leisure time at the beach 9.01 13.10 12.49 - 27.9

Source: Watersports and Leisure Participation Surveys 2006 – 2008

21 Economic Impact of Coastal Marinas; British Marine Federation, September 2007

HLL Development Options Appraisal – Herne Bay Pier 29

The market for most watersports activities is concentrated amongst affluent middle-aged groups (particularly those aged 35 – 54), although more ‘adventurous’ activities are most popular amongst those aged 16 – 34.

4.10.1 The Local Market We are aware that Herne Bay is currently a popular destination for leisure jetskiiers, both day and longer stay visitors. A number of these currently stay overnight at weekends in the Premier Inn at Blacksole Farm. This highlights the potential of the watersports market to attract new overnight visitors to Herne Bay and the surrounding area, although the impact of such visitors has, at present, not been quantified. The creation of the Herne Bay and Whitstable Jetski and Watercraft Society (JAWS) in 2003 demonstrates the growth of interest in such activities. Aside from the local sailing and yachting clubs (Herne Bay Sailing Club and Hampton Pier Yacht Club), our research has not identified any RYA-accredited watersports centres within the town. There is a watersports equipment rental facility located on Central Parade and Herne Bay Amateur Rowing Club is also located at Hampton Pier – adjacent to the yacht club.

4.10.2 Watersports Appraisal There would appear to be the potential for the Pier to house a base for watersports activities. Such a facility would be likely to fit well with the catchment population profile identified in chapter 3.3. There may, however, be some concerns over viability, with an extensive tidal range locally that may restrict watersports activities at low tide, for example. In addition, many of the existing watersports activities are informal and not based around either of the existing sailing / yachting clubs in Herne Bay. The development of a formal watersports base at or adjacent to the Pier (perhaps coupled with restrictions on areas for watersports activity), may in fact deter the existing jetskiiers / overnight visitors from continuing to visit Herne Bay. Such a scheme could, therefore, potentially have a negative economic impact on the town.

4.11 Cable Car The concept of a cable car / chair lift / aerial tramway has been highlighted by some of the stakeholders that we have consulted. Accordingly, we have considered the potential for such a scheme at Herne Bay Pier. Such attractions generally consist of one or two fixed cables , one loop of cable and a number of passenger cabins or seats. The cable is usually driven by an electric motor, with a number of supporting towers en-route.

HLL Development Options Appraisal – Herne Bay Pier 30

Figures 4.11 & 4.12: Examples of Gondola Lift-Style Cable Car Rides

Source: Poma

There are very few such developments in the UK. The key UK-based schemes are at the Needles on the Isle of Wight, Heights of Abraham in Derbyshire, Nevis Range in Scotland, and Llandudno in North Wales (although there are other rides at major theme parks – such as Alton Towers). This is due to the generally high cost and logistical difficulties of such rides. We are aware, for example, that the cost of replacing the 250-metre long cable car ride at the Needles (for insurance purposes) is £1.75 million.22 This is without the ongoing annual maintenance requirements. The cost of construction in Herne Bay (for a far longer ride) is likely to be considerably higher, and this is without the cost of restoring the Pier Head to accommodate visitors being taken into consideration.

4.11.1 The Local Market As highlighted, there are no comparable examples in the South East – aside from the Needles. This is likely due to the high costs associated with such schemes. We understand, however, that there are proposals for a cable car in Dover – running from the castle to the town and seafront as part of a £7.75 million bid for Sea Change funding23. We have spoken to the Council who have advised that a technical and commercial feasibility study is currently being undertaken, and the intention is to subsequently market this opportunity to the private sector in 2010. Due to the current financial climate, there must be a considerable degree of uncertainty as to whether this scheme will come to fruition. This project has received around £400,000 of Sea Change funding to develop in more detail, but is linked to other key attractions (eg. Dover Castle attracts more than 330,000 visitors pa).

4.11.2 Cable Car Appraisal There are few such attractions in the UK. Clearly, such an attraction would create a significant level of interest – the Needles ride, for example, attracts in excess of 300,000 visitors per year. The high cost of developing such rides does, however, preclude many from investing in the concept, and may stymie plans for such an attraction at Dover in the short to medium term at the very least. In addition, it should be noted that the potential ride at Dover is linked to well-established major

22 Heritage Great Britain Ltd 23 This is Kent 6 November 2008

HLL Development Options Appraisal – Herne Bay Pier 31

visitor attractions to generate potential visitor numbers. This would not be the case – to the same extent – at Herne Bay. We anticipate that the cost of construction of such a ride at the Pier would be extremely high, and is unlikely to be a realistic development opportunity. However, should the Council wish to investigate this option in more detail, then we would recommend commissioning a detailed feasibility study from an engineering firm that specialises in such schemes, to ascertain the costs involved.

4.12 Enabling Development There may be a need for some form of enabling development to meet any funding / development shortfall to ensure the future of the Pier. We have considered residential and beach hut development in this context.

4.12.1 Residential Development A number of comparable projects – see Southwold Pier in Appendix 1 – have used residential development at the root end of the pier to finance pier restoration. We do not consider the Pier itself a suitable location for residential development. There is some limited space at the root end of the Pier and, although we doubt that this would be considered acceptable in planning terms, it is perhaps something the Council may wish to consider before rejecting outright. Alternatively, there may be other local sites that could be sold off to provide an injection of capital funding for the redevelopment of Herne Bay Pier.

4.12.2 Chalets, Beach Huts & Summerhouses Beach huts are a very British phenomenon and have long been a traditional form of seaside leisure provision by local authorities in coastal areas. The concept originally began as changing rooms for bathers in Edwardian times. There are an estimated 20,000 beach huts around the British coastline24, with the majority to be found on the southern and eastern coasts of England, clusters in Wales and a few further huts dotted around Scotland and Ireland.25

Across the UK, the smallest beach huts are generally on the market for around £5,000 to £6,000, although huts have sold for considerably more. Indeed, pre-recession, a large wooden beach ‘chalet’ (17ft x 15ft) was put on the market for £280,000 at West Bexington in Dorset.26

There are a number of existing locations in East Kent. Canterbury City Council operate 257 beach huts to the west of the Pier, which are all privately owned. There is a proposal for 40 additional huts at East Cliff (near Kings Hall). Whitstable offers a number of beach huts and chalets on the Tankerton Slopes, with Dover District Council offering a number of beach huts at both St Margarets Bay and Kingsdown, near Deal. There are also ten locations in Thanet offering beach huts (managed by Leisure Force on behalf of the Council).

24 The Guardian 14 July 2007 25 www.beach-huts.com 26 BBC News 27 November 2007

HLL Development Options Appraisal – Herne Bay Pier 32

Figure 4.13: Beach Hut Sale Prices in East Kent (as at 13 August 2009)

Hut Location Approximate Size of Hut Low Price (£) High Price (£)

Whitstable 10ft x 10ft 19,000 26,000 Herne Bay 8ft x 6 ft 7,950 9,500

Source: HLL research

The above table does show that huts in Herne Bay are considerably cheaper than in Whitstable. Having spoken to Leisure Force and Dover District Council, we also understand that waiting lists in Thanet are “at least several years”, whilst the waiting list at St Margarets Bay (between Dover and Deal) has been closed due to an 11 – 12 year wait, whilst Kingsdown (near Deal) has an approximate 10 year waiting list.

4.12.3 Beach Huts Appraisal The asking price of huts currently being marketed in Whitstable – together with the extremely long waiting lists reported elsewhere in Kent – highlight that levels of demand for beach huts and chalets has remained extremely high despite the current recessionary climate. This suggests that there may be demand for additional units at Herne Bay, which would provide the Council with a degree of rental and / or capital income from new units. The location of any new beach huts will need careful consideration, but could possibly include huts sited at, or around, the foot of the Pier.

4.13 Commercial Investment Potential - Conclusion

4.13.1 Market Climate The current market is extremely challenging for most leisure operators. Whilst some sectors, such as cinemas, are performing well, the operating companies are displaying considerable caution in expanding, and are finding it difficult to fund further development. It is reasonable, however, to assume that this position will not continue indefinitely. Therefore, our advice is based upon a return to a more normal market, where funding is available – at sensible rates – to competent leisure businesses.

4.13.2 Initial Assessment of Commercial Potential Accordingly, this chapter has reviewed a number of possible uses which may be appropriate for Herne Bay Pier. To further identify the likely level of commercial interest we have spoken, on a confidential basis, to a wide range of leisure companies to establish whether they may have an appetite for involvement in any future development on the Pier. • The sample of major national restaurant companies approached do not have

any serious interest at present. Whilst this view is undoubtedly coloured by the current economic situation, we think it is unlikely that the position will change materially when the market improves. Major restaurant (and related) companies have a well-defined target profile for new investment sites. Herne Bay’s relatively limited population size, together with its catchment for such purposes, mean that it is unlikely that a major branded operator will be attracted, at least in the short term. That is not to say, however, that there will not be any interest from existing local operators in such an opportunity on Herne Bay Pier. It appears that a number of local operators are performing

HLL Development Options Appraisal – Herne Bay Pier 33

well and we consider that there is likely to be some interest from local operators in new opportunities on a revamped Pier. However, such interest may be tempered by the number of existing venues nearby, and the Council would probably need to develop the units itself, leasing the opportunities to local entrepreneurs in exchange for annual rental income.

We think it unlikely that restaurant operators would be interested in taking space within the existing building, however reconfigured it may be. • There is no current interest from urban leisure operators (such as cinema or

tenpin bowling). Most acquisition programmes have been closed down in the current market, but even in an improved climate it is unlikely that Herne Bay will figure highly on a target list for such uses given the alternative investment opportunities available.

• There has been a mixed response from children’s play operators. In general, concern was expressed regarding the nature of the catchment. One company has indicated a willingness to consider the proposition further. However, they are currently considering a site in Chatham which has a larger catchment and thus investment in Herne Bay may be unlikely.

• One of the principal operators of aquariums in the UK has turned down the location as unsuitable from their business perspective.

• Discussions with local property professionals indicate a relatively weak demand in general at the present time, although this should improve over the timescale of the project.